Advanced Support and Resistance Levels[MAP]Advanced Support and Resistance Levels Indicator

Author

Developed by:

Overview

The "Advanced Support and Resistance Levels" indicator, created, is a sophisticated tool designed for TradingView's Pine Script v6 platform. It identifies and plots key support and resistance levels on a price chart, enhancing technical analysis by incorporating pivot strength, volume weighting, and level decay. The indicator overlays lines, zones, and labels on the chart, providing a visual representation of significant price levels where the market has historically reversed or consolidated.

Purpose

This indicator, authored by , aims to:

Detect significant pivot points (highs and lows) with customizable strength requirements.

Track and rank support/resistance levels based on their recency, volume, and number of touches.

Display these levels as lines and optional zones, with strength-based visual cues (e.g., line thickness and opacity).

Offer flexibility through user-configurable settings to adapt to different trading styles and market conditions.

Features

Pivot Detection:

Identifies high and low pivots using a strength parameter, requiring a specified number of bars on either side where no higher highs or lower lows occur.

Incorporates closing price checks and SMA-based trend confirmation to filter out noise and ensure pivots align with the broader market direction.

Level Management:

Maintains a dynamic array of levels with attributes: price, type (support/resistance), bars since last touch, strength, and volume.

Merges nearby levels within a tolerance percentage, updating prices with a strength-weighted average.

Prunes weaker or older levels when exceeding the maximum allowed, prioritizing those with higher calculated strength.

Strength Calculation:

Combines the number of touches (strength), volume (if enabled), and age decay (if enabled) into a single metric.

Volume weighting uses a logarithmic scale to emphasize high-volume pivots without over-amplifying extreme values.

Age decay reduces the importance of older levels over time, ensuring relevance to current price action.

Visualization:

Draws horizontal lines at each level, with thickness reflecting the number of touches (up to a user-defined maximum).

Optional price zones around levels, sized as a percentage of the price, to indicate areas of influence.

Labels display the level type (S for support, R for resistance), price, and strength score, with position (left or right) customizable.

Line opacity varies with strength, providing a visual hierarchy of level significance.

Plots small triangles at detected pivot points for reference.

Inputs

Lookback Period (lookback, default: 20): Number of bars to consider for trend confirmation via SMA. Range: 5–100.

Pivot Strength (strength, default: 2): Number of bars required on each side of a pivot to confirm it. Range: 1–10.

Price Tolerance % (tolerance, default: 0.5): Percentage range for merging similar levels. Range: 0.1–5.

Max Levels to Show (maxLevels, default: 10): Maximum number of levels displayed. Range: 2–50.

Zone Size % (zoneSizePercent, default: 0.1): Size of the S/R zone as a percentage of the price. Range: 0–1.

Line Width (lineWidth, default: 1): Maximum thickness of level lines. Range: 1–5.

Show Labels (showLabels, default: true): Toggle visibility of level labels.

Label Position (labelPos, default: "Right"): Position of labels ("Left" or "Right").

Level Strength Decay (levelDecay, default: true): Enable gradual reduction in strength for older levels.

Volume Weighting (volumeWeight, default: true): Incorporate volume into level strength calculations.

Support Color (supportColor, default: green): Color for support levels.

Resistance Color (resistColor, default: red): Color for resistance levels.

How It Works

Pivot Detection:

Checks for pivots only after enough bars (2 * strength) have passed.

A high pivot requires strength bars before and after with no higher highs or closes, and a short-term SMA above a long-term SMA.

A low pivot requires strength bars before and after with no lower lows or closes, and a short-term SMA below a long-term SMA.

Level Tracking:

New pivots create levels with initial strength and volume.

Existing levels within tolerance are updated: strength increases, volume takes the maximum value, and price adjusts via a weighted average.

Levels older than lookback * 4 bars with strength below 0.5 are removed.

If the number of levels exceeds maxLevels, the weakest (by calculated strength) are pruned using a selection sort algorithm.

Drawing:

Updates on the last confirmed bar or in real-time.

Lines extend lookback bars left and right from the current bar, with thickness based on touches.

Zones (if enabled) are drawn symmetrically around the level price.

Labels show detailed info, with opacity tied to strength.

Usage

Add to Chart: Apply the indicator to any TradingView chart via the Pine Script editor, as designed by .

Adjust Settings: Customize inputs to match your trading strategy (e.g., increase strength for stronger pivots, adjust tolerance for tighter level merging).

Interpret Levels: Focus on thicker, less transparent lines for stronger levels; use zones to identify potential reversal areas.

Combine with Other Tools: Pair with trend indicators or oscillators for confluence in trading decisions.

Notes

Performance: The indicator uses arrays and sorting, which may slow down on very long charts with many levels. Keep maxLevels reasonable for efficiency.

Accuracy: Enhanced by trend confirmation and volume weighting, making it more reliable than basic S/R indicators, thanks to 's design.

Limitations: Real-time updates may shift levels as new pivots form; historical levels are more stable.

Example Settings

For day trading: lookback=10, strength=1, tolerance=0.3, maxLevels=5.

For swing trading: lookback=50, strength=3, tolerance=0.7, maxLevels=10.

Credits

Author: – Creator of this advanced support and resistance tool, blending precision and customization for traders.

"track" için komut dosyalarını ara

Market Snap Shot with Pine ScreenerMarket Snap Shot

The Market Snap Shot is a comprehensive technical analysis tool designed to track and display key price metrics across multiple timeframes, including daily, weekly, monthly, quarterly, and yearly data. This script provides a range of essential calculations for traders and investors, enabling them to assess price action, volatility, and market trends at a glance.

Features:

Daily Metrics: Includes the daily percentage change, closing range relative to the daily high/low.

Weekly Metrics: Tracks weekly open, close, range, and calculates week-to-date performance for a broader market view.

Monthly Metrics: Provides similar calculations for monthly price action, offering insights into monthly performance.

Quarter-to-Date (QTD): Displays performance for the current quarter, offering insights into quarterly price movements.

Year-to-Date (YTD): Calculates year-to-date price change, helping users track performance relative to the start of the year.

52-Week High/Low: Displays the current price's distance from the 52-week high and low, giving context to long-term price levels.

Usage:

Traders can use this screener to quickly assess the current market position and make informed decisions based on short-term and long-term trends.

Investors can leverage the 52-week and YTD metrics to gauge the overall strength of an asset in the market.

The tool is versatile for both active traders looking for real-time performance data and for those focusing on longer-term market trends.

Instructions:

This script displays multiple metrics such as percentage changes and range data for daily, weekly, monthly, quarterly, and yearly timeframes. It is designed to be used as a screener tool to assess price action and monitor performance across these key time periods.

Warning:

The "Market Snap Shot" does not provide buy or sell signals but rather serves as a performance tracking tool. Users are encouraged to use this data in conjunction with other technical and fundamental analysis tools.

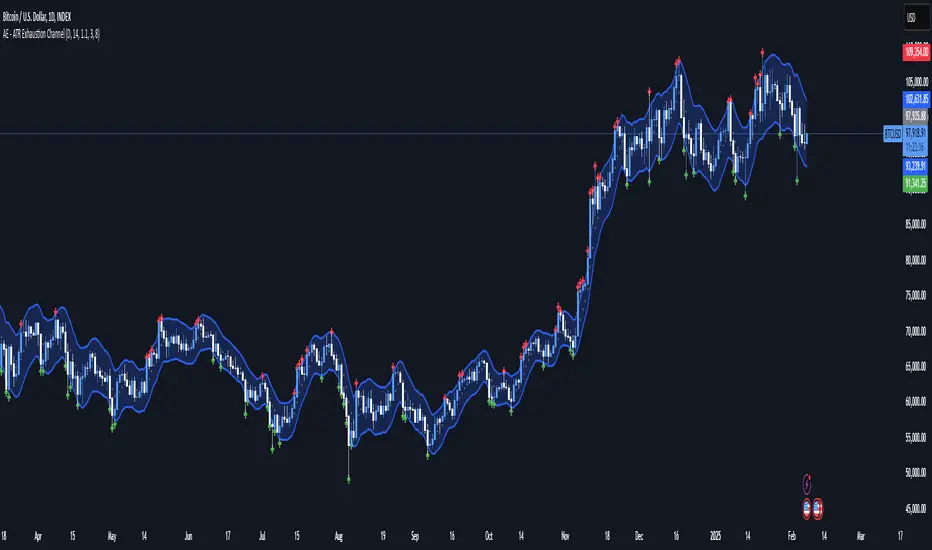

AE - ATR Exhaustion ChannelAE - ATR Exhaustion Channel

📈 Overview

Identify Exhaustion Zones & Trend Breakouts with ATR Precision!

The AE - ATR Exhaustion Channel is a powerful volatility-based trading tool that combines an averaged SMA with ATR bands to dynamically highlight potential trend exhaustion zones. It provides real-time breakout detection by marking when price moves beyond key volatility bands, helping traders spot overextensions and reversals with ease.

🔑 Key Features

✔️ ATR-SMA Hybrid Channel: Uses an averaged SMA as the core trend filter while incorporating adaptive ATR-based bands for precise volatility tracking.

✔️ Dynamic Exhaustion Markers: Marks red crosses when price exceeds the upper band and green crosses when price drops below the lower band.

✔️ Customizable ATR Sensitivity: Adjust the ATR multiplier and length settings to fine-tune band sensitivity based on market conditions.

✔️ Clear Channel Visualization: A gray SMA midpoint and a blue-filled ATR band zone make it easy to track market structure.

📚 How It Works

1️⃣ Averaged SMA Calculation: The script calculates an averaged SMA over a user-defined range (min/max period). This smooths out short-term fluctuations while preserving trend direction.

2️⃣ ATR Band Construction: The ATR value (adjusted by a multiplier) is added to/subtracted from the SMA to form dynamic upper and lower volatility bands.

3️⃣ Exhaustion Detection:

If high > upper ATR band, a red cross is plotted (potential overextension).

If low < lower ATR band, a green cross is plotted (potential reversal zone).

4️⃣ Filled ATR Channel: The area between the upper and lower bands is shaded blue, providing a visual trading range.

🎨 Customization & Settings

⚙️ ATR Length – Adjusts the ATR calculation period (default: 14).

⚙️ ATR Multiplier – Scales the ATR bands for tighter or wider volatility tracking (default: 0.8, adjustable in 0.1 steps).

⚙️ SMA Range (Min/Max Length) – Defines the period range for calculating the averaged SMA (default: 5-20).

⚙️ Rolling Lookback Length – Controls how far back the high/low comparison is calculated (default: 50 bars).

🚀 Practical Usage

📌 Spotting Exhaustion Zones – Look for red/green markers appearing outside the ATR bands, signaling potential trend exhaustion and possible reversal opportunities.

📌 Breakout Confirmation – Price consistently breaching the upper band with momentum could indicate continuation, while repeated touches without strong closes may hint at reversal zones.

📌 Trend Reversal Signals – Watch for green markers below the lower band in uptrends (buy signals) and red markers above the upper band in downtrends (sell signals).

🔔 Alerts & Notifications

📢 Set Alerts for Exhaustion Signals!

Traders can configure alerts to trigger when price breaches the ATR bands, allowing for instant notifications when volatility-based exhaustion is detected.

📊 Example Scenarios

✔ Trend Exhaustion in Overextended Moves – A series of red crosses near resistance may indicate a short opportunity.

✔ Trend Exhaustion in Overextended Moves – A series of red crosses near resistance may indicate an opportunity to open a short trade.

✔ Volatility Compression Breakouts – If price consolidates within the ATR bands and suddenly breaks out, it could signify a momentum shift.

✔ Reversal Catching in Trending Markets – Spot potential trend reversals by looking for green markers below the ATR bands in bullish markets.

🌟 Why Choose AE - ATR Exhaustion Channel?

Trade with Confidence. Spot Volatility. Catch Breakouts.

The AE - ATR Exhaustion Channel is an essential tool for traders looking to identify trend exhaustion, detect breakouts, and manage volatility effectively. Whether you're trading stocks, crypto, or forex, this ATR-SMA hybrid system provides clear visual cues to help you stay ahead of market moves.

✅ Customizable to Fit Any Market

✅ Combines Volatility & Trend Analysis

✅ Easy-to-Use with Instant Breakout Detection

Auto-Length Moving Average + Trend Signals (Zeiierman)█ Overview

The Auto-Length Moving Average + Trend Signals (Zeiierman) is an easy-to-use indicator designed to help traders dynamically adjust their moving average length based on market conditions. This tool adapts in real-time, expanding and contracting the moving average based on trend strength and momentum shifts.

The indicator smooths out price fluctuations by modifying its length while ensuring responsiveness to new trends. In addition to its adaptive length algorithm, it incorporates trend confirmation signals, helping traders identify potential trend reversals and continuations with greater confidence.

This indicator suits scalpers, swing traders, and trend-following investors who want a self-adjusting moving average that adapts to volatility, momentum, and price action dynamics.

█ How It Works

⚪ Dynamic Moving Average Length

The core feature of this indicator is its ability to automatically adjust the length of the moving average based on trend persistence and market conditions:

Expands in strong trends to reduce noise.

Contracts in choppy or reversing markets for faster reaction.

This allows for a more accurate moving average that aligns with current price dynamics.

⚪ Trend Confirmation & Signals

The indicator includes built-in trend detection logic, classifying trends based on market structure. It evaluates trend strength based on consecutive bars and smooths out transitions between bullish, bearish, and neutral conditions.

Uptrend: Price is persistently above the adjusted moving average.

Downtrend: Price remains below the adjusted moving average.

Neutral: Price fluctuates around the moving average, indicating possible consolidation.

⚪ Adaptive Trend Smoothing

A smoothing factor is applied to enhance trend readability while minimizing excessive lag. This balances reactivity with stability, making it easier to follow longer-term trends while avoiding false signals.

█ How to Use

⚪ Trend Identification

Bullish Trend: The indicator confirms an uptrend when the price consistently stays above the dynamically adjusted moving average.

Bearish Trend: A downtrend is recognized when the price remains below the moving average.

⚪ Trade Entry & Exit

Enter long when the dynamic moving average is green and a trend signal occurs. Exit when the price crosses below the dynamic moving average.

Enter short when the dynamic moving average is red and a trend signal occurs. Exit when the price crosses above the dynamic moving average.

█ Slope-Based Reset

This mode resets the trend counter when the moving average slope changes direction.

⚪ Interpretation & Insights

Best for trend-following traders who want to filter out noise and only reset when a clear shift in momentum occurs.

Higher slope length (N): More stable trends, fewer resets.

Lower slope length (N): More reactive to small price swings, frequent resets.

Useful in swing trading to track significant trend reversals.

█ RSI-Based Reset

The counter resets when the Relative Strength Index (RSI) crosses predefined overbought or oversold levels.

⚪ Interpretation & Insights

Best for reversal traders who look for extreme overbought/oversold conditions.

High RSI threshold (e.g., 80/20): Fewer resets, only extreme conditions trigger adjustments.

Lower RSI threshold (e.g., 60/40): More frequent resets, detecting smaller corrections.

Great for detecting exhaustion in trends before potential reversals.

█ Volume-Based Reset

A reset occurs when current volume significantly exceeds its moving average, signaling a shift in market participation.

⚪ Interpretation & Insights

Best for traders who follow institutional activity (high volume often means large players are active).

Higher volume SMA length: More stable trends, only resets on massive volume spikes.

Lower volume SMA length: More reactive to short-term volume shifts.

Useful in identifying breakout conditions and trend acceleration points.

█ Bollinger Band-Based Reset

A reset occurs when price closes above the upper Bollinger Band or below the lower Bollinger Band, signaling potential overextension.

⚪ Interpretation & Insights

Best for traders looking for volatility-based trend shifts.

Higher Bollinger Band multiplier (k = 2.5+): Captures only major price extremes.

Lower Bollinger Band multiplier (k = 1.5): Resets on moderate volatility changes.

Useful for detecting overextensions in strong trends before potential retracements.

█ MACD-Based Reset

A reset occurs when the MACD line crosses the signal line, indicating a momentum shift.

⚪ Interpretation & Insights

Best for momentum traders looking for trend continuation vs. exhaustion signals.

Longer MACD lengths (260, 120, 90): Captures major trend shifts.

Shorter MACD lengths (10, 5, 3): Reacts quickly to momentum changes.

Useful for detecting strong divergences and market shifts.

█ Stochastic-Based Reset

A reset occurs when Stochastic %K crosses overbought or oversold levels.

⚪ Interpretation & Insights

Best for short-term traders looking for fast momentum shifts.

Longer Stochastic length: Filters out false signals.

Shorter Stochastic length: Captures quick intraday shifts.

█ CCI-Based Reset

A reset occurs when the Commodity Channel Index (CCI) crosses predefined overbought or oversold levels. The CCI measures the price deviation from its statistical mean, making it a useful tool for detecting overextensions in price action.

⚪ Interpretation & Insights

Best for cycle traders who aim to identify overextended price deviations in trending or ranging markets.

Higher CCI threshold (e.g., ±200): Detects extreme overbought/oversold conditions before reversals.

Lower CCI threshold (e.g., ±10): More sensitive to trend shifts, useful for early signal detection.

Ideal for detecting momentum shifts before price reverts to its mean or continues trending strongly.

█ Momentum-Based Reset

A reset occurs when Momentum (Rate of Change) crosses zero, indicating a potential shift in price direction.

⚪ Interpretation & Insights

Best for trend-following traders who want to track acceleration vs. deceleration.

Higher momentum length: Captures longer-term shifts.

Lower momentum length: More responsive to short-term trend changes.

█ How to Interpret the Trend Strength Table

The Trend Strength Table provides valuable insights into the current market conditions by tracking how the dynamic moving average is adjusting based on trend persistence. Each metric in the table plays a role in understanding the strength, longevity, and stability of a trend.

⚪ Counter Value

Represents the current length of trend persistence before a reset occurs.

The higher the counter, the longer the current trend has been in place without resetting.

When this value reaches the Counter Break Threshold, the moving average resets and contracts to become more reactive.

Example:

A low counter value (e.g., 10) suggests a recent trend reset, meaning the market might be changing directions frequently.

A high counter value (e.g., 495) means the trend has been ongoing for a long time, indicating strong trend persistence.

⚪ Trend Strength

Measures how strong the current trend is based on the trend confirmation logic.

Higher values indicate stronger trends, while lower values suggest weaker trends or consolidations.

This value is dynamic and updates based on price action.

Example:

Trend Strength of 760 → Indicates a high-confidence trend.

Trend Strength of 50 → Suggests weak price action, possibly a choppy market.

⚪ Highest Trend Score

Tracks the strongest trend score recorded during the session.

Helps traders identify the most dominant trend observed in the timeframe.

This metric is useful for analyzing historical trend strength and comparing it with current conditions.

Example:

Highest Trend Score = 760 → Suggests that at some point, there was a strong trend in play.

If the current trend strength is much lower than this value, it could indicate trend exhaustion.

⚪ Average Trend Score

This is a rolling average of trend strength across the session.

Provides a bigger picture of how the trend strength fluctuates over time.

If the average trend score is high, the market has had persistent trends.

If it's low, the market may have been choppy or sideways.

Example:

Average Trend Score of 147 vs. Current Trend Strength of 760 → Indicates that the current trend is significantly stronger than the historical average, meaning a breakout might be occurring.

Average Trend Score of 700+ → Suggests a strong trending market overall.

█ Settings

⚪ Dynamic MA Controls

Base MA Length – Sets the starting length of the moving average before dynamic adjustments.

Max Dynamic Length – Defines the upper limit for how much the moving average can expand.

Trend Confirmation Length – The number of bars required to validate an uptrend or downtrend.

⚪ Reset & Adaptive Conditions

Reset Condition Type – Choose what triggers the moving average reset (Slope, RSI, Volume, MACD, etc.).

Trend Smoothing Factor – Adjusts how smoothly the moving average responds to price changes.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Uptrick Signal Density Cloud🟪 Introduction

The Uptrick Signal Density Cloud is designed to track market direction and highlight potential reversals or shifts in momentum. It plots two smoothed lines on the chart and fills the space between them (often called a “cloud”). The bars on the chart change color depending on bullish or bearish conditions, and small triangles appear when certain reversal criteria are met. A metrics table displays real-time values for easy reference.

🟩 Why These Features Have Been Linked Together

1) Dual-Line Structure

Two separate lines represent shorter- and longer-term market tendencies. Linking them in one tool allows traders to view both near-term changes and the broader directional bias in a single glance.

2) Smoothed Averages

The script offers multiple smoothing methods—exponential, simple, hull, and an optimized approach—to reduce noise. Using more than one type of moving average can help balance responsiveness with stability.

3) Density Cloud Concept

Shading the region between the two lines highlights the gap or “thickness.” A wider gap typically signals stronger momentum, while a narrower gap could indicate a weakening trend or potential market indecision. When the cloud is too wide and crosses a certain threshold defined by the user, it indicates a possible reversal. When the cloud is too narrow it may indicate a potential breakout.

🟪 Why Use This Indicator

• Trend Visibility: The color-coded lines and bars make it easier to distinguish bullish from bearish conditions.

• Momentum Tracking: Thicker cloud regions suggest stronger separation between the faster and slower lines, potentially indicating robust momentum.

• Possible Reversal Alerts: Small triangles appear within thick zones when the indicator detects a crossover, drawing attention to key moments of potential trend change.

• Quick Reference Table: A metrics table shows line values, bullish or bearish status, and cloud thickness without needing to hover over chart elements.

🟩 Inputs

1) First Smoothing Length (length1)

Default: 14

Defines the lookback period for the faster line. Lower values make the line respond more quickly to price changes.

2) Second Smoothing Length (length2)

Default: 28

Defines the lookback period for the slower line or one of the moving averages in optimized mode. It generally responds more slowly than the faster line.

3) Extra Smoothing Length (extraLength)

Default: 50

A medium-term period commonly seen in technical analysis. In optimized mode, it helps add broader perspective to the combined lines.

4) Source (source)

Default: close

Specifies the price data (for example, open, high, low, or a custom source) used in the calculations.

5) Cloud Type (cloudType)

Options: Optimized, EMA, SMA, HMA

Determines the smoothing method used for the lines. “Optimized” blends multiple exponential averages at different lengths.

6) Cloud Thickness Threshold (thicknessThreshold)

Default: 0.5

Sets the minimum separation between the two lines to qualify as a “thick” zone, indicating potentially stronger momentum.

🟪 Core Components

1) Faster and Slower Lines

Each line is smoothed according to user preferences or the optimized technique. The faster line typically reacts more quickly, while the slower line provides a broader overview.

2) Filled Density Cloud

The space between the two lines is filled to visualize in which direction the market is trending.

3) Color-Coded Bars

Price bars adopt bullish or bearish colors based on which line is on top, providing an immediate sense of trend direction.

4) Reversal Triangles

When the cloud is thick (exceeding the threshold) and the lines cross in the opposite direction, small triangles appear, signaling a possible market shift.

5) Metrics Table

A compact table shows the current values of both lines, their bullish/bearish statuses, the cloud thickness, and whether the cloud is in a “reversal zone.”

🟩 Calculation Process

1) Raw Averages

Depending on the mode, standard exponential, simple, hull, or “optimized” exponential blends are calculated.

2) Optimized Averages (if selected)

The faster line is the average of three exponential moving averages using length1, length2, and extraLength.

The slower line similarly uses those same lengths multiplied by 1.5, then averages them together for broader smoothing.

3) Difference and Threshold

The absolute gap between the two lines is measured. When it exceeds thicknessThreshold, the cloud is considered thick.

4) Bullish or Bearish Determination

If sma1 (the faster line) is above sma2 (the slower line), conditions are deemed bullish; otherwise, they are bearish. This distinction is reflected in both bar colors and cloud shading.

5) Reversal Markers

In thick zones, a crossover triggers a triangle at the point of potential reversal, alerting traders to a possible trend change.

🟪 Smoothing Methods

1) Exponential (EMA)

Prioritizes recent data for quicker responsiveness.

2) Simple (SMA)

Takes a straightforward average of the chosen period, smoothing price action but often lagging more in volatile markets.

3) Hull (HMA)

Employs a specialized formula to reduce lag while maintaining smoothness.

4) Optimized (Blended Exponential)

Combines multiple EMA calculations to strike a balance between responsiveness and noise reduction.

🟩 Cloud Logic and Reversal Zones

Cloud thickness above the defined threshold typically signals exceeding momentum and can lead to a quick reversal. During these thick periods, if the width exceeds the defined threshold, small triangles mark potential reversal points. In order for the reversal shape to show, the color of the cloud has to be the opposite. So, for example, if the cloud is bearish, and exceeds momentum, defined by the user, a bullish signal appears. The opposite conditions for a bullish signal. This approach can help traders focus on notable changes rather than minor oscillations.

🟪 Bar Coloring and Layered Lines

Bars take on bullish or bearish tints, matching the faster line’s position relative to the slower line. The lines themselves are plotted multiple times with varying opacities, creating a layered, glowing look that enhances visibility without affecting calculations.

🟩 The Metrics Table

Located in the top-right corner of the chart, this table displays:

• SMA1 and SMA2 current values.

• Bullish or bearish alignment for each line.

• Cloud thickness.

• Reversal zone status (in or out of zone).

This numeric readout allows for a quick data check without hovering over the chart.

🟪 Why These Specific Moving Average Lengths Are Used

Default lengths of 14, 28, and 50 are common in technical analysis. Fourteen captures near-term price movement without overreacting. Twenty-eight, roughly double 14, provides a moderate smoothing level. Fifty is widely regarded as a medium-term benchmark. Multiplying each length by 1.5 for the slower line enhances separation when combined with the faster line.

🟩 Originality and Usefulness

• Multi-Layered Smoothing. The user can select from several moving average modes, including a unique “optimized” blend, possibly reducing random fluctuations in the market data.

• Combined Visual and Numeric Clarity. Bars, clouds, and a real-time table merge into a single interface, enabling efficient trend analysis.

• Focus on Significant Shifts. Thick cloud zones and triangles draw attention to potentially stronger momentum changes and plausible reversals.

• Flexible Across Markets. The adjustable lengths and threshold can be tuned to different asset classes (stocks, forex, commodities, crypto) and timeframes.

By integrating multiple technical concepts—cloud-based trend detection, color coding, reversal markers, and an immediate reference table—the Uptrick Signal Density Cloud aims to streamline chart reading and decision-making.

🟪 Additional Considerations

• Timeframes. Intraday, daily, and weekly charts each yield different signals. Adjust the smoothing lengths and threshold to suit specific trading horizons.

• Market Types. Though applicable across asset classes, parameters might need tweaking to address the volatility of commodities, forex pairs, or cryptocurrencies.

• Confirmation Tools. Pairing this indicator with volume studies or support/resistance analysis can improve the reliability of signals.

• Potential Limitations. No indicator is foolproof; sudden market shifts or choppy conditions may reduce accuracy. Cautious position sizing and risk management remain essential.

🟩 Disclaimers

The Uptrick Signal Density Cloud relies on historical price data and may lag sudden moves or provide false positives in ranging conditions. Always combine it with other analytical techniques and sound risk management. This script is offered for educational purposes only and should not be considered financial advice.

🟪 Conclusion

The Uptrick Signal Density Cloud blends trend identification, momentum assessment, and potential reversal alerts in a single, user-friendly tool. With customizable smoothing methods and a focus on cloud thickness, it visually highlights important market conditions. While it cannot guarantee predictive accuracy, it can serve as a comprehensive reference for traders seeking both a quick snapshot of the current trend and deeper insights into market dynamics.

MEMEQUANTMEMEQUANT

This script is a comprehensive and specialized tool designed for tracking trends and money flow within meme coins and DEX tokens. By combining various features such as trend lines, Fibonacci levels, and category-based indices, it helps traders make informed decisions in highly volatile markets.

Key Features:

1. Category-Based Indices:

• Tracks the performance of token categories like:

• AI Agent Tokens

• AI Tokens

• Animal Tokens

• Murad Picks

• Each category consists of leader tokens, which are selected based on their higher market cap and trading volume. These tokens act as benchmarks for their respective categories.

• Visualizes category indices in a line chart to identify trends and compare money flow between categories.

2. Fibonacci Correction Zones:

• Highlights key retracement levels (e.g., 60%, 70%, 80%).

• These levels are crucial for identifying potential reversal zones, commonly observed in meme coin trading patterns.

• Fully customizable to match individual trading strategies.

3. Trend Lines:

• Automatically detects major support and resistance levels.

• Separates long-term and short-term trend lines, allowing traders to focus on significant price movements.

4. Enhanced Info Table:

• Provides real-time insights, including:

• % Distance from All-Time High (ATH)

• Current Trading Volume

• 50-bar Average Volume

• Volume Change Percentage

• Displays information in an easy-to-read table on the chart.

5. Customizable Settings:

• Users can adjust transparency, colors, and ranges for Fibonacci zones, trend lines, and the table.

• Enables or disables individual features (e.g., Fibonacci, trend lines, table) based on preferences.

How It Works:

1. Tracking Money Flow Across Categories:

• The script calculates the market cap to volume ratio for each category of tokens to help identify the dominant trend.

• A higher ratio indicates greater liquidity and stability, while a lower ratio suggests higher volatility or price manipulation.

2. Identifying Retracement Patterns:

• Leverages common retracement behaviors (e.g., 70% correction levels) observed in meme coins to detect potential reversal zones.

• Combines this with trend line analysis for additional confirmation.

3. Leader Tokens as Indicators:

• Each category is represented by its leader tokens, which have historically higher liquidity and market cap. This allows the script to accurately reflect the overall trend in each category.

When to Use:

• Trend Analysis: To identify which category (e.g., AI Tokens or Animal Tokens) is leading the market.

• Reversal Zones: To spot potential support or resistance levels using Fibonacci zones.

• Money Flow: To understand how capital is moving across different token categories in real time.

Who Is This For?

This script is tailored for:

• Traders specializing in meme coins and DEX tokens.

• Those looking for an edge in trend-based trading by analyzing market cap, volume, and retracement levels.

• Anyone aiming to track money flow dynamics between different token categories.

Future Updates:

This is the initial version of the script. Future updates may include:

• Support for additional token categories and DEX data.

• More advanced pattern recognition and alerts for volume and price anomalies.

• Enhanced visualization for historical data trends.

With this tool, traders can combine money flow analysis with the 60-70% retracement strategy, turning it into a powerful assistant for navigating the fast-paced world of meme coins and DEX tokens.

This script is designed to provide meaningful insights and practical utility for traders, adhering to TradingView’s standards for originality, clarity, and user value.

Volume and Price, EMA Hierarchy Scoring Relations V 1.1Understanding the Volume and Price, EMA Hierarchy Scoring Indicator

Financial markets are often analyzed through a series of technical indicators, each providing valuable but isolated insights into price movements, volume dynamics, and trends. While these tools are widely used, they often lack context when applied individually. The Volume and Price, EMA Hierarchy Scoring Indicator was developed to bridge this gap by introducing structure, context, and relationships between these known indicators.

By utilizing Exponential Moving Averages (EMAs) and assigning periods derived from prime numbers, this indicator creates a scoring system that evaluates the relative positioning and interaction of 13 widely used technical tools. This approach adds meaning to individual indicator outputs by:

Revealing how their results align, diverge, or complement each other.

Quantifying their collective behavior through a hierarchy scoring system.

Enabling traders to not only analyze indicators individually but also combine them to uncover how they influence and interact with each other.

The result is a tool that provides clarity and insight into market behavior, enabling traders to move beyond surface-level analysis and uncover deeper patterns and relationships within the data.

Key Features and Methodology

The Volume and Price, EMA Hierarchy Scoring Indicator is built on a robust mathematical framework that evaluates and visualizes the relationships between 13 widely used technical indicators. By leveraging Exponential Moving Averages (EMAs) and prime numbers, the indicator provides meaningful insights into individual indicator performance as well as their combined behavior.

1. EMA Hierarchy Scoring

At the core of the indicator is its ability to assess the hierarchy of EMAs for each tool. This hierarchy scoring evaluates how the EMAs are aligned relative to one another, providing traders with a quantifiable measure of the indicator's internal consistency and its alignment with trends.

How It Works:

Each EMA is assigned a period derived from a unique prime number. This ensures that no two EMAs overlap, preserving their individuality.

The scoring system measures the gaps between these EMAs, assigning weighted values to these relationships based on their position in the hierarchy.

Why Prime Numbers?

Prime numbers ensure that the EMA periods are distinct and mathematically unrelated, creating a structured yet diverse dataset for analysis.

This approach allows the scoring system to capture both short-term and long-term trends, while avoiding redundancy.

2. Independent Indicator Evaluation

One of the key features of this indicator is the ability to analyze any of the 13 tools individually. Each indicator has its own module, complete with adjustable parameters and dedicated visualizations:

Histograms: Represent the raw EMA hierarchy score. Positive bars indicate alignment with upward trends, while negative bars highlight potential reversals or misalignments.

Smoothed Line: Averages the histogram values, reducing short-term noise and emphasizing longer-term trends.

Signal Line: Highlights trend shifts by smoothing the smoothed line further. Crossovers between the smoothed line and the signal line act as actionable signals for traders.

3. Combining Indicators for Context

Beyond individual analysis, the indicator allows users to combine multiple indicators to evaluate their interactions. For example:

Pairing ALMA (price smoothing) with Volume enables traders to see how price trends are supported or contradicted by market activity.

Combining Delta Volume and CMF (Chaikin Money Flow) reveals nuanced dynamics of buying and selling pressure.

Number of Combinations

With 13 tools available, the indicator supports "two to the power of thirteen minus one," which equals 8,191possible combinations. This flexibility empowers traders to experiment with various subsets of indicators, tailoring their analysis to specific market conditions or strategies.

Detailed Breakdown of Indicators

The Volume and Price, EMA Hierarchy Scoring Indicator integrates 13 widely used technical indicators, each bringing a unique perspective to market analysis. These indicators are scored individually using the EMA hierarchy system and can also be combined for more comprehensive insights.

Here’s a detailed look at what each indicator contributes:

Price Analysis

Arnaud Legoux Moving Average (ALMA):

Purpose:

ALMA smooths price data, reducing noise while maintaining responsiveness to trends.

Unique Features:

The EMA hierarchy scoring highlights how well ALMA’s EMAs align, revealing the strength of price trends.

Visualization includes a histogram of ALMA scores, a smoothed line, and a signal line.

Settings:

Adjustable parameters for the window size, offset, and sigma.

Tooltips guide users on how each setting affects the calculation.

Application:

Evaluate price momentum or combine with volume-based indicators to validate trends.

2. Price Hierarchy Score (PRC):

Purpose:

Focuses solely on price behavior to identify consistency and strength.

Visualization:

Includes a histogram representing raw scores and smoothed and signal lines for trend detection.

Settings:

Adjustable EMA periods derived from prime numbers.

Customizable smoothing and signal periods.

Volume Insights

3. Chaikin Money Flow (CMF):

Purpose:

Integrates price and volume data to measure capital flow direction and strength.

Visualization:

Raw CMF hierarchy scores are plotted, alongside smoothed and signal lines for easier trend identification.

Settings:

Lookback period adjustment for CMF calculation.

Toggle for enabling/disabling the module.

Application:

Use alongside Delta Volume to assess buying and selling pressure.

Above chart snapshot, in addition to the well-known CMF indicator, the Volume and Price indicator and the EMA Hierarchy Scoring can also be seen in the chart. By enabling the CMF evaluation, you can observe both how the CMF is analyzed and how it aligns with the price chart.

4. Delta Volume:

Purpose:

Captures the balance between buying and selling activity in the market.

Visualization:

A histogram represents the raw divergence in buying and selling strength.

Signal lines help identify momentum shifts.

Settings:

Options to set lower timeframes for more granular analysis.

Adjustable smoothing and signal periods.

Application:

Combine with CMF for a deeper understanding of capital flow dynamics.

In the above chart, alongside the Volume Delta indicator, you can observe our evaluation of this indicator's performance.

In the above chart, as explained, you can observe the impact of our evaluation metrics both individually and in combination with other indicators. This chart featuring VPR (Volume and Price Indicator along with EMA Hierarchy Scoring) illustrates the interplay between CMF and Volume Delta.

5. Volume Hierarchy Score (VOL):

Purpose:

Tracks raw volume data to identify areas of heightened market activity.

Visualization:

Histogram and smoothed lines highlight volume trends.

Settings:

Prime-numbered EMA periods to analyze volume hierarchy.

Adjustable smoothing and signal line parameters.

In the above chart, as previously explained, by analyzing the EMA of volume data over 25 iterations within specified periods (based on the first 25 prime numbers), you can observe the relationship between volume and price. We are witnessing a price increase, while the current volume position shows significant deviation and instability relative to the EMAs calculated over 25 different time periods.

In the above chart, by simultaneously enabling the evaluation of both volume and price, you can clearly observe the interplay and impact of volume and price in relation to each other.

Momentum and Trend Strength

6. Aroon Up:

Purpose:

Evaluates the strength of trends by measuring time since price highs.

Visualization :

Hierarchy scores plotted as histograms with trend-tracking smoothed and signal lines.

Settings:

Lookback period adjustments.

Module toggle for focus on Aroon trends.

If the analysis and interpretation of Aroon lines seem somewhat complex, the Volume and Price Indicator along with EMA Hierarchy Scoring provides a clear and intuitive representation of the Aroon indicator in relation to the price chart, as you can see in the current chart.

7. Average Directional Index (ADX):

Purpose:

Quantifies the strength of trends, regardless of direction.

Visualization:

ADX scores and smoothed lines for trend confirmation.

Settings:

Adjustable directional indicator (DI) and ADX smoothing periods.

Tooltip guidance for parameter optimization.

The simultaneous chart of the well-known ADX indicator alongside the evaluation system of the Volume and Price Indicator with EMA Hierarchy Scoring provides an integrated perspective on the ADX indicator.

8. Elder Force Index (EFI):

Purpose:

Combines price and volume to measure the strength of price movements.

Visualization:

EFI hierarchy scores with clear trend representation through signal and smoothed lines.

Settings:

Length adjustments for sensitivity control.

Smoothing and signal line customization.

In the above chart, we simultaneously have the well-known EFI indicator and the Volume and Price Indicator along with EMA Hierarchy Scoring. As we progress further, you will become increasingly familiar with the functionality and precision of the Volume and Price Indicator along with EMA Hierarchy Scoring.

Volatility and Oscillators

9. Ehler Fisher Transform:

Purpose:

Highlights extreme price movements by transforming price data into a Gaussian distribution.

Visualization:

Fisher Transform scores with smoothed trend indicators.

Settings:

Fisher length adjustment.

Module toggle and smoothing controls.

10. McGinley Dynamic (MGD):

Purpose:

Tracks price trends while adjusting for volatility, providing a smoother signal.

Visualization:

Raw MGD hierarchy scores with smoothed and signal lines.

Settings:

Lookback period customization.

Adjustable smoothing and signal periods

.

Ichimoku Components

11. Conversion Line (ICMC):

Purpose:

Captures short-term price equilibrium levels within the Ichimoku framework.

Visualization:

Short-term hierarchy scores visualized with smoothed lines.

Settings:

Adjustable conversion line length.

Tooltips explaining Ichimoku-related insights.

12. Base Line (ICMB):

Purpose:

Identifies medium-term equilibrium levels in the Ichimoku system.

Visualization:

Scores and smoothed trend lines for medium-term trends.

Settings:

Base line period adjustments.

Tooltip guidance for Ichimoku analysis.

In the chart below, to better illustrate the capabilities of the Volume and Price, EMA Hierarchy Scoring relation, we present a chart that evaluates the simultaneous interaction of Ichimoku Base and Conversion lines, Price, Volume, and Delta Volume.

Market Health

13. Money Flow Index (MFI):

Purpose:

Detects overbought or oversold conditions using price and volume data.

Visualization:

MFI hierarchy scores with trend tracking through smoothed and signal lines.

Settings:

Lookback period customization for sensitivity adjustment.

Module toggle and visualization controls.

EMA of Indicators: A Unified Scoring Metric

The EMA of Indicators module introduces a unique way to aggregate and analyze the individual scores of all 13 indicators. By applying a unified EMA calculation to their hierarchy scores, this module provides a single, combined metric that reflects the overall market sentiment based on the collective behavior of all indicators.

How It Works

1. Indicator-Specific EMAs:

An EMA is calculated for each of the 13 indicator hierarchy scores. The EMA period is adjustable in the settings menu, allowing traders to control how responsive the metric is to recent changes.

2. Combined EMA Calculation:

The individual EMAs are summed and averaged to generate a single Combined EMA Value. This value represents the average performance and alignment of all the indicators.

3. Smoothed and Signal Lines:

To enhance the interpretability of the Combined EMA Value:

- A Smoothed EMA is calculated using an additional EMA to filter out short-term fluctuations.

- A Signal Line is applied to the Smoothed EMA, providing actionable signals when crossovers occur.

Visualization

The Combined EMA Value is visualized as:

Histogram Bars: Represent the raw Combined EMA Value, highlighting positive or negative market alignment.

Smoothed Line: Tracks longer-term trends by smoothing the combined value.

Signal Line: Marks potential shifts in market sentiment when it crosses the Smoothed Line.

Customization and Settings

The settings menu allows full control over the EMA calculation:

Enable/Disable Module: Toggle the entire EMA of Indicators functionality.

Adjust EMA Period: Define the responsiveness of the individual indicator EMAs.

Set Smoothing Period: Control the degree of smoothing applied to the combined score.

Signal Line Period: Fine-tune the signal line's sensitivity for detecting trend shifts.

Tooltips accompany each parameter, ensuring that users understand their impact on the final visualization.

Applications in Market Analysis

1. Market Health Overview:

Use the Combined EMA Value as a quick snapshot of overall market sentiment based on all 13 indicators.

2. Trend Confirmation:

Analyze crossovers between the Smoothed EMA and Signal Line to confirm market trends or reversals.

3. Flexible Strategy Development:

Adjust EMA and smoothing periods to align the module with short-term or long-term trading strategies.

From EMA Scoring to Divergence-Weighted Insights

While the EMA scoring system provides insights into individual indicators and their trends, the Divergence-Weighted Volatility Adjusted Score takes this analysis further by combining and comparing all 13 indicators into a unified metric.

The Divergence-Weighted Volatility Adjusted Score

This score evaluates how the EMA scores of the 13 indicators interact and diverge, adding a layer of context and collective behavior analysis to the raw hierarchy scores.

1. Normalization:

All EMA scores are scaled to a common range, ensuring comparability regardless of the magnitude of individual indicators.

2. Divergence Analysis:

The system calculates the average score of the 13 indicators and evaluates the deviation (or divergence) of each individual score from this average.

Indicators with significant divergence are highlighted, as they often signal critical market dynamics.

3. Dynamic Weighting:

Indicators with greater divergence are assigned higher weights in the combined score. This ensures that outliers with meaningful signals are emphasized.

4. Volatility Adjustment:

The combined score is adjusted based on market volatility (calculated as the standard deviation of the score over a defined lookback period). This stabilizes the output, making it reliable even during turbulent market conditions.

Visualization and Customization

The Divergence-Weighted Volatility Adjusted Score is plotted as a dynamic line chart, offering a clear visual summary of the collective behavior of all indicators. The chart includes:

Smoothed Score Line: Filters out noise and emphasizes longer-term trends.

Signal Line: Helps identify potential trend shifts by tracking smoothed score crossovers.

Settings:

Lookback Period: Defines the time frame for volatility calculation.

Smoothing Period: Controls the degree of noise reduction in the smoothed score line.

Signal Line Period: Adjusts the responsiveness of the signal line.

These settings are fully adjustable, with tooltips guiding users to understand their impact.

Applications

The Divergence-Weighted Volatility Adjusted Score has several practical applications:

1. Cross-Indicator Alignment:

Detect when multiple indicators align or diverge, signaling potential opportunities or risks.

2. Dynamic Market Insights:

Adapt to changing conditions with the volatility-adjusted scoring.

3. Trend Confirmation:

Use smoothed and signal lines to validate trends identified by individual indicators.

Conclusion

The Volume and Price, EMA Hierarchy Scoring Indicator redefines how traders analyze financial markets. By combining 13 widely used technical tools with a structured scoring system based on Exponential Moving Averages (EMAs) and prime-numbered periods, this indicator brings depth and context to market analysis.

Key features include:

Independent Analysis: Evaluate individual indicators with precise EMA hierarchy scoring to assess their alignment with market trends.

Dynamic Combinations: Explore the relationships between indicators through over 8,000 combinations to uncover nuanced interactions and patterns.

Divergence-Weighted Scoring: Compare the collective behavior of indicators using a divergence-weighted system, providing a holistic market perspective adjusted for volatility.

Customization: Enable or disable modules, adjust smoothing and signal periods, and fine-tune settings to align the indicator with specific trading strategies.

User-Friendly Visualizations: Intuitive histograms, smoothed lines, and signal lines help traders identify trends, reversals, and market alignment at a glance.

This indicator empowers traders to move beyond isolated analysis by creating meaning and context between known tools. Whether you’re a scalper seeking short-term trends or a swing trader analyzing broader market movements, the Volume and Price, EMA Hierarchy Scoring Indicator offers insights tailored to your strategy.

Disclaimer

The Volume and Price, EMA Hierarchy Scoring Indicator is a tool for technical analysis and market evaluation. While it provides structured insights into market behavior, no indicator can guarantee success or eliminate the inherent risks of trading. Market conditions are complex, and multiple factors influence price movements.

Users are advised to:

Combine this indicator with other analysis methods, such as fundamental analysis or risk management strategies.

Make informed decisions based on their own analysis, trading goals, and risk tolerance.

Trading involves significant risk, and past performance does not guarantee future results. Always consult with a financial advisor or professional before making trading decisions.

Crypto Sectors Performance [Daveatt]IMPORTANT

⚠️ This script must be used on the Daily timeframe only.

OVERVIEW

This indicator brings the powerful sector analysis capabilities from velo.xyz/market's

Sector Performance chart to TradingView.

It enables traders to track and compare performance across the crypto market's major sectors, providing essential insights for sector rotation strategies and market analysis.

CALCULATION METHOD

The indicator calculates performance across six key crypto sectors: DeFi, Gaming, Layer 1s, Layer 2s, AI, and Memecoins.

For each sector, it computes a rolling percentage performance by averaging the performance of multiple representative tokens.

All sector performances are rebased to 0% at the start of each period, making relative comparisons clear and intuitive.

VISUALIZATION MODES

The script features two distinct visualization methods:

Plots Mode:

Displays continuous performance lines for each sector over time, ideal for tracking relative strength trends and sector momentum. Each sector has its own color-coded line with performance values clearly marked.

Bars Mode:

Presents current sector performance as vertical bars, offering an immediate visual comparison of sector gains and losses.

The bars are color-coded and labeled with exact percentage values for precise analysis.

For the "Bars Mode", I used the box.new() function

SECTOR COMPOSITION

Each sector comprises carefully selected representative tokens:

- DeFi: AAVE, 1INCH, JUP, MKR, UNI

- Gaming: GALA, AXS, RONIN, SAND

- Layer 1: BTC, ETH, AVAX, APT, SOL, BNB, SUI

- Layer 2: ARB, OP, ZK, POL, STRK, MNT

- AI: FET, NEAR, RENDER, TAO

- Memecoins: PEPE, BONK, SHIB, DOGE, WIFU, POPCAT

PERFORMANCE TRACKING

The indicator implements a rolling window approach for performance calculations.

Starting from 0% at the beginning of each period, it tracks relative performance with positive values indicating outperformance and negative values showing underperformance.

Multiple timeframe options (1W, 1M, 3M, 6M, and 1Y) allow for both short-term and long-term analysis.

APPLICATIONS

This tool proves invaluable for:

- Sector rotation analysis

- Identifying trending sectors

- Comparing relative strength

- Gauging market sentiment

- Understanding market structure through sector performance

Thanks for reading and for the support

Daveatt

[AlbaTherium] Volume Venturius Premium Volume Venturius Premium

Introduction

The Volume Venturius Premium is an advanced market analysis tool designed to deeply investigate the behavior of active market participants. By focusing exclusively on executed market orders, Volume Venturius offers traders a unique perspective on buy and sell volumes. Unlike traditional order books that track passive orders, this indicator isolates active orders, shedding light on real market dynamics.

Chapter 1: Understanding Market Participants

1.1 Categories of Market Participants

Market participants can be classified into several categories based on their:

Size : The volume of trades executed.

Influence : Their ability to initiate bull or bear campaigns.

Strategy : The trading methods employed, such as scalping, swing trading, or high-frequency trading.

Objectives : Whether their focus is on speculation, hedging, or arbitrage.

Time Horizon : Short-term versus long-term goals.

Behavioral Patterns : Their reaction to liquidity levels or price movements.

1.2 Objectives of Market Participants

Each category pursues specific objectives, such as profit-making or risk management. Regulatory reports like the Commitment of Traders (COT) provide weekly insights into the positions and intentions of major players.

Chapter 2: The Philosophy of Volume Analysis

2.1 Active Orders vs. Passive Orders

Unlike passive orders waiting to be filled at specific prices, active orders directly impact market prices. By focusing on these executed orders, Volume Venturius Premium provides traders with actionable insights into market trends and momentum.

2.2 Wyckoff’s Market Dynamics

According to Wyckoff, markets operate in two primary phases:

Manipulation: Where large participants accumulate or distribute positions to prepare for a move.

Expansion: The phase where price trends begin to unfold, either in a bullish or bearish direction.

Wyckoff’s theory emphasizes understanding how major players manipulate the market to identify accumulation or distribution zones. Volume Venturius Premium aids in pinpointing these manipulative actions by analyzing volume and order flow data.

Chapter 3: The Secrets of Order Flow and Volume

3.1 Unveiling Market Control

By studying the positioning and execution volumes of large players, traders can discern who holds control in the market. Volume Venturius Premium identifies the balance of power and tracks shifts that signal potential trend reversals.

3.2 Behavioral Patterns in Volume

Key metrics tracked by Volume Venturius Premium include:

Volume Clusters : Areas of concentrated buying or selling activity.

Directional Bias : Whether market participants are net buyers or sellers.

Momentum Shifts : Changes in execution speed and volume that may precede major moves.

3.2.1 Volume Clusters, Directional Bias and Directional Bias: Areas of Concentrated Buying or Selling Activity

Volume clusters play a crucial role in understanding market dynamics by highlighting areas where aggressive buying or selling activity is most concentrated. These clusters often serve as key decision zones, providing insights into potential reversals, breakouts, or continuations. To better visualize and interpret these zones, a distinct color-coding system has been implemented. Each color represents a specific market condition or level of activity, allowing for a more intuitive analysis of volume behavior and its influence on price movement.

Below is a detailed explanation of the color logic used to represent these clusters and their significance within the trading framework.

Color Interpretation and Meaning :

Extra Extreme Zones

These zones highlight areas where clusters of aggressive buyers or sellers are most heavily concentrated. They represent critical levels for identifying potential reversals or strong continuations.

Bright Red (#ff003c) : Represents extra-extreme sell zones, where aggressive sellers dominate.

Meaning: Indicates extreme selling pressure, often signaling potential exhaustion of sellers.

Bright Blue (#001eff) : Represents extra-extreme buy zones, where aggressive buyers are most active.

Meaning: Shows extreme buying pressure, possibly marking a saturation point for buyers.

Main Zones

These zones help identify key levels based on volume activity and well-defined clusters.

Dark Red (#d60033) : Represents strong selling pressure.

Orange (#ff8000) : Indicates significant selling pressure that begins to fade.

Yellow (#ffff00) : Represents moderate selling pressure, signaling a potential slowdown.

White (#ffffff) : Marks transition zones, which are interesting entry points for potential reversals or continuations.

Transition Zones (Frontier Zones)

These zones indicate intermediate movements and potential shifts in momentum.

Transparent Black (#000000, 50) : Represents transition areas, where the market tests boundaries between buyers and sellers.

Meaning: These are critical decision points.

Neutral Zone (Sea Zone)- Trend Zones

These zones represent more balanced market activity, where neither buyers nor sellers dominate clearly.

Transparent Green (#00e040, 25) : Indicates slight bullish activity in a neutral zone.

Transparent Red (#e01a00, 25) : Indicates slight bearish activity in a neutral zone.

This color logic allows you to pinpoint areas where volume clusters show a clear dominance, exhaustion, or optimal entry opportunities.

3.3 Divergences Between Price and Volume

Divergences between price and volume are critical for identifying key shifts in market sentiment. Volume Venturius Premium distinguishes two main types of divergences: Lack of Participation and Absorption, each offering valuable signals for potential reversals or continuations.

Lack of Participation

This divergence occurs when price movements are not supported by corresponding volume dynamics, signaling a reduction in activity from significant market participants.

1. Bullish Lack of Participation:

Characteristics : Price is making lower lows, but volume is making higher lows.

This indicates waning selling pressure as prices drop.

Inference : A potential bullish reversal may occur. Traders could consider looking for opportunities to go long.

2.Bearish Lack of Participation:

Characteristics : Price is making higher highs, but volume is making lower highs. This suggests diminishing buying pressure even as prices rise.

Inference : A potential bearish reversal might follow. Traders might position to go short.

Absorption

Absorption occurs when larger market participants neutralize the pressure from smaller participants, often leading to significant market moves.

1.Bullish Absorption:

Characteristics : Price is making higher bottoms, but volume is making lower bottoms.

This reflects sellers being trapped as their selling efforts are absorbed by larger buyers.

Inference : A potential upward breakout is likely. Traders may look for opportunities to go long.

2.Bearish Absorption:

Characteristics : Price is making lower tops, but volume is making higher tops. This indicates buyers being trapped as larger sellers absorb their buying activity.

Inference : A downward breakout is probable. Traders may consider positioning to go short.

Chapter 4: Practical Application and Trading Strategies

4.1 Leveraging Active Order Insights

Learn how to use Volume Venturius Premium to detect hidden accumulation or distribution phases. Strategies include identifying spikes in active volume that signal institutional participation.

4.2 Confirming Bull and Bear Campaigns

Gain confidence in detecting the early stages of bullish or bearish campaigns by analyzing the interplay between active orders and volume flow.

Chapter 5: Real-World Examples

5.1 Analyzing Market Manipulation

See how Volume Venturius Premium can reveal manipulation tactics employed by large players to trigger liquidity events.

5.2 Spotting Trends with Active Orders

Real-life scenarios demonstrate how the tool can be used to identify and ride the market’s dominant trend.

Conclusion

The Volume Venturius Premium is an indispensable tool for traders who seek to understand the underlying mechanics of market movement. By focusing on active order flows and drawing on Wyckoff’s principles, it provides unique insights into market manipulation and expansion phases. Whether you’re an intraday trader or a long-term strategist, this tool empowers you to anticipate market shifts and trade with confidence.

Stay tuned for updates as we continue to refine Volume Venturius Premium to further enhance your trading journey.

Richs Market StructureThis Pine Script indicator, "Last Bullish High & Lowest Low Tracker with Timeframe Background and Fill", is designed to visually track bullish and bearish trends based on price action on the current chart and a user-defined timeframe. It provides dynamic line plotting, area fills, and background coloring to represent trend alignment between the current chart and the selected timeframe.

Features and Functionalities

Tracks Bullish Highs and Bearish Lows:

The script identifies:

Bullish High: The highest price reached after a bullish (green) candle.

Bearish Low: The lowest price reached after a bearish (red) candle.

It dynamically updates these levels based on the price movements.

Line Plotting:

Current Chart Lines:

The Plotted Bullish High line (green/red) indicates the last bullish high.

The Lowest Low line (green/red) indicates the last bearish low.

Selected Timeframe Lines:

A separate set of lines is plotted for the user-defined timeframe (e.g., daily, weekly):

A Bullish High Line for the selected timeframe (lighter green).

A Lowest Low Line for the selected timeframe (lighter red).

Dynamic Area Fills:

The area between the Plotted Bullish High and Lowest Low is filled:

Green Fill: When both lines are green (indicating a bullish alignment).

Red Fill: When both lines are red (indicating a bearish alignment).

For the selected timeframe:

The area between the timeframe-specific Bullish High and Lowest Low is similarly filled with lighter colors.

Background Color Based on Timeframe Alignment:

The background color represents the trend alignment on the selected timeframe:

Green Background: When the timeframe’s Bullish High is rising and Lowest Low is rising (bullish trend).

Red Background: When the timeframe’s Bullish High is falling and Lowest Low is falling (bearish trend).

What It’s For

This indicator is designed for traders who want to:

Visualize Trends Across Timeframes:

It helps identify when the current chart’s trend aligns with a higher timeframe trend (e.g., daily, weekly).

Useful for multi-timeframe analysis.

Spot Bullish and Bearish Trends:

The color-coded lines and fills clearly show the dominant trend on both the current chart and the selected timeframe.

Plan Trades Based on Trend Alignment:

When the current chart and selected timeframe show the same trend:

Both lines and fills turn green (bullish).

Both lines and fills turn red (bearish).

This alignment is a potential signal for entering long or short trades.

Identify Reversals and Divergences:

Divergence between the current chart and timeframe trends (e.g., green on one, red on the other) may indicate trend weakening or reversal.

Visual Elements

Lines:

Solid lines (current chart): Represent the Plotted Bullish High and Lowest Low.

Dashed/lighter lines (selected timeframe): Represent the timeframe-specific Bullish High and Lowest Low.

Fills:

Green/Red fills highlight trend zones:

On the current chart (darker).

On the selected timeframe (lighter).

Background:

The entire chart background turns green or red based on the selected timeframe’s trend alignment.

Summary

This indicator is ideal for traders who want a clear visual representation of price trends and multi-timeframe alignment. It simplifies trend-following strategies by providing:

Easy-to-interpret fills and background colors.

Clear bullish and bearish zones.

Multi-timeframe trend confirmation.

Adaptive bollinger bands cloud v1 trend & trade signalsadaptive bollinger bands cloud:

the script extends the concept of bollinger bands by creating a "cloud" between the upper and lower bands. this cloud visually represents market conditions, with its color dynamically adjusting based on trend strength and volatility.

the gradient fill between the bands changes according to the deviation of the price from its basis, offering a visual cue for trend momentum.

trend detection logic:

a trend variable determines whether the price is in a bullish, bearish, or neutral state. if the price is above the upper band and the basis, the trend is marked bullish. if it's below the lower band and the basis, the trend is bearish. otherwise, it's neutral.

this trend logic is further enhanced with visual markers like arrows to indicate potential trend reversals.

extended take-profit bands:

additional upper and lower bands are calculated using a higher multiplier. these extended bands help identify potential take-profit levels, signaling when the price may have reached an overextended state.

gradient calculation:

the script computes a gradient based on the deviation of the price from its basis and normalizes it over a lookback period. this normalized gradient is smoothed to reflect volatility intensity and used to color the cloud dynamically.

signal generation:

buy and sell signals are generated based on crossovers of the trend variable. for instance, when the trend shifts from negative to positive, it signals a bullish opportunity. conversely, a shift from positive to negative indicates bearish conditions.

take-profit markers ("x") are plotted when the price crosses the extended bands, suggesting potential exit points.

trade entry tracking:

the script includes a table to display real-time entry signals and prices for long (buy) or short (sell) trades. this feature helps traders keep track of signals without needing to reference the chart visually.

customizable inputs:

users can adjust the bb period, multiplier, and colors to suit their trading preferences. this flexibility allows for tuning the indicator based on different market conditions or asset classes.

overall, the indicator blends traditional bollinger bands with innovative visualization, trend identification, and trading signals to enhance decision-making.

how to use this indicator

trend detection:

watch for arrows indicating trend shifts:

an upward arrow (green) signals a bullish trend; consider buying or entering a long position.

a downward arrow (red) signals a bearish trend; consider selling or entering a short position.

use the gradient-colored cloud to assess trend strength:

bright and strong colors indicate significant momentum.

fading colors suggest weakening trends or consolidation.

entry signals:

refer to the table in the top-right corner of the chart for real-time buy or sell entry signals.

when a "buy" signal is displayed with the price, it suggests a potential entry point for a long trade.

when a "sell" signal is displayed, consider shorting or exiting long positions.

take-profit signals:

look for the "x" markers near the extended bands (upper1 and lower1):

an "x" above the price suggests taking profit on long positions.

an "x" below the price suggests taking profit on short positions.

background gradient analysis:

observe the dynamic background color:

a strong purple gradient indicates significant price movement or volatility.

a lighter gradient suggests reduced momentum, signaling caution or a potential reversal.

alerts for automation:

set alerts using the predefined conditions:

bullish trend start, bearish trend start, and take-profit levels can be used to automate notifications for trade actions.

why to use this indicator

enhanced decision-making:

the adaptive cloud and gradient provide visual insights into trend strength and volatility, allowing traders to assess market conditions at a glance.

precise signals:

the indicator uses crossover logic and extended bollinger bands to generate clear buy, sell, and take-profit signals, reducing guesswork.

trend confirmation:

combining the bollinger bands with the trend variable ensures that traders only act on confirmed market trends rather than noise.

dynamic volatility assessment:

the normalized gradient calculation highlights periods of high or low volatility, helping traders adjust their strategies accordingly.

customizable settings:

adjustable parameters (period, multiplier, colors) allow the indicator to fit various markets, timeframes, and trading styles.

all-in-one tool:

integrates trend detection, entry signals, and take-profit levels into a single indicator, minimizing the need for multiple tools.

this indicator is especially useful for traders seeking a balance between simplicity and precision, whether scalping, day trading, or swing trading. it not only identifies trends but also highlights actionable entry and exit points, making it a versatile addition to any trading strategy.

Dynamic Support & Resistance based on SMI CrossoverExplanation:

SMI Calculation: The script calculates the Stochastic Momentum Index (SMI) and its signal line using the specified input lengths.

Crossover Detection: It detects when the SMI crosses above (crossUp) or below (crossDown) its signal line.

Period Tracking: The script keeps track of up and down periods based on SMI crossovers. During an up period, it records the lowest low (support), and during a down period, it records the highest high (resistance).

Support and Resistance Levels: When a crossover occurs, it captures the highest or lowest value since the last crossover to define dynamic resistance and support levels.

Midline Calculation: The midline is calculated as the average of the current support and resistance levels.

Buy and Sell Signals: Buy signals are generated when the close price crosses above the midline, and sell signals are generated when it crosses below.

Plotting: The support, resistance, and midline are plotted on the upper chart. Buy and sell signals are indicated with arrows. Trendlines are added for visual clarity.

Note: This indicator should be used in conjunction with other analysis tools and is intended for educational purposes. Always perform thorough analysis before making trading decisions.

Like all technical indicators, this script is based on historical data and may not predict future market movements.

Always perform due diligence and consider multiple factors when making trading decisions.

Manual Trading Checklist by Afnan TajuddinHey traders! This Trading Checklist indicator like your personal to-do list right on your chart! Here’s what it does:

Easy Tracking: Seven checkboxes to make sure you’ve done all your trading steps.

Colorful Signs: Green "✔" for done stuff and red "✘" for things you need to fix.

Make It Yours: Change where the table is on the chart, pick your favorite colors, and set the text size just how you like it.

Simple Setup: Rename the checklist items and toggle them on or off in the settings.

Clean Look: It stays neat on your chart without messing things up.

Whether you’re just starting out or you’ve been trading for a while, this checklist helps you stay organized and stick to your plan. Perfect for anyone who loves keeping things tidy and on track!