Overnight Gap Detector - 4H Body to BodyThis TradingView indicator automatically detects and tracks overnight price gaps based on 4-hour candle bodies, displaying them as colored rectangles on your chart.

Key Features:

Gap Detection:

Identifies true wick-to-wick gaps that occur at the start of each new trading day

Gap Up: Detected when previous candle's high is below current candle's low

Gap Down: Detected when previous candle's low is above current candle's high

Rectangles are drawn from candle body to body (not wicks), providing clean gap zones

Gap Tracking:

Gaps are marked as "GAP HOLE" when first detected

Automatically tracks when gaps get filled

Changes to "FILLED" label and color when price closes through the gap zone

Gaps extend horizontally until filled or chart end

Customizable Display:

Label Position: Choose between "Inside" (centered in box) or "Outside" the gap rectangle

Label Offset: Adjust how far from the right edge labels appear (0-50 bars)

Minimum Gap Size: Filter out small gaps by setting minimum percentage threshold (default 0.05%)

Max Stored Gaps: Control how many gaps are kept on chart (default 200)

Visual Options:

Optional midline showing the 50% fill level of each gap

Fully customizable colors for Gap Up, Gap Down, and Filled gaps

Separate transparency controls for box backgrounds and label backgrounds

Adjustable border and midline widths

Toggle labels and midlines on/off

Color Coding:

Green: Gap Up (default)

Red: Gap Down (default)

Yellow: Filled gaps (default)

Perfect for traders who use gap-fill strategies or want to track key price levels where gaps occurred

"track" için komut dosyalarını ara

JOPA Channel (Dual-Volumed) v1 [JopAlgo]JOPA Channel (Dual-Volumed) v1

Short title: JOPAV1 • License: MPL-2.0 • Provider: JopAlgo

We have developed our own, first channel-based trading indicator and we’re making it available to all traders. The goal was a channel that breathes with the tape—built on a volume-weighted backbone—so the outcome stays lively instead of static. That led to the JOPA Channel.

All important features (at a glance)

In one line: A Rolling-VWAP channel whose width adapts with two volumes (RVOL + dollar-flow), adds order-flow asymmetry (OBV tilt) and regime awareness (Efficiency Ratio), and frames risk with outer containment bands from residual extremes—so you see fair value, momentum, and exhaustion in one view.

Feature list

Rolling VWAP centerline: Tracks where volume traded (fair value).

Dual-volume width: Bands expand/contract with relative volume and value traded (price×volume).

OBV tilt: Upper/lower widths skew toward the side actually pushing.

Regime adapter (ER): Tighter in trend, wider in chop—automatically.

Outer containment rails: Residual-extreme ceilings/floors, smoothed + margin.

20% / 80% guides: 20% light blue (discount), 80% light red (premium).

Squeeze dots (optional): Orange circles below candles during compression.

Non-repainting: Uses rolling sums and past-only math; no lookahead.

Default visual in this release

Containment rails + fill: ON (stepline, medium).

Inner Value rails + fill: Rails OFF (stepline, thin), fill ON (drawn only if rails are shown).

20% & 80% guides: ON (dashed, thin; 20% light blue, 80% light red).

Squeeze dots: OFF by default (orange circles when enabled).

What you see on the chart

RVWAP (centerline): Your compass for fair value.

Inner Value Bands (optional): Tight rails for breakouts and pullback timing.

Outer Containment Bands (default ON): High-confidence ceilings/floors for targets and fades.

20% / 80% guides: Quick read of “where in the channel” price is sitting.

Squeeze dots (optional): Volatility compression heads-up (no text labels).

Non-repainting note: The indicator does not revise closed bars. Forecast-Lock uses linear regression to extrapolate 1–3 bars ahead without using future data.

How to use it

Core reads (works on any timeframe)

Bias: Above a rising RVWAP → long bias; below a falling RVWAP → short bias.

Breakouts (momentum): Close beyond an Inner Value rail with RVOL ≥ threshold (alert provided).

Reversions (fades): Tag Outer Containment, stall, then close back inside → expect mean reversion toward RVWAP.

20/80 timing:

At/above 80% (light red) → premium/exhaustion risk; trim longs or consider fades if RVOL cools.

At/below 20% (light blue) → discount/exhaustion risk; trim shorts or consider longs if RVOL cools.

Squeeze clusters: When dots bunch up, expect a range break; use the Breakout alert as confirmation.

Playbooks by trading style

Day Trading (1–5m)

Setup: Keep the chart clean (Containment ON, Value rails OFF). Toggle Inner Value ON when hunting a breakout or timing a pullback.

Pullback Long: Dip to RVWAP / Lower Value with sub-threshold RVOL, then a close back above RVWAP → long.

Stop: Just beyond Lower Containment or the pullback swing.

Targets (1:1:1): ⅓ at RVWAP, ⅓ at Upper Value, ⅓ trail toward Upper Containment.

Breakout Long: After a squeeze cluster, take the Breakout Long alert (close > Upper Value, RVOL ≥ min). If no retest, demand the next bar holds outside.

Range Fade: Only when RVWAP is flat and dots cluster; short Upper Containment → RVWAP (mirror for longs at the lower rail).

Intraday (15m–1H)

HTF compass: Take bias from 4H.

Pullback Long: “Touch & reclaim” of RVWAP while RVOL cools; enter on the reclaim close or break of that candle’s high.

Breakout: Run Inner Value ON; act on Breakout alerts (RVOL gate ≈ 1.10–1.15 typical).

Avoid low-probability fades against the 4H slope unless RVWAP is flat.

Swing (4H–1D)

Continuation: In uptrends, buy pullbacks to RVWAP / Lower Value with sub-threshold RVOL; scale at Upper Containment.

Adds: Post-squeeze Breakout Long adds; trail on RVWAP or Lower Value.

Fades: Prefer when RVWAP flattens and price oscillates between containments.

Position (1D+)

Framework: Daily RVWAP slope + position within containment.

Add rule: Each reclaim of RVWAP after a dip is an add; trim into Upper Containment or near 80% light red.

Sizing: Containment distance is larger—size down and trail on RVWAP.

Inputs & Settings (complete)

Core

Source: Price input for RVWAP.

Rolling VWAP Length: Window of the centerline (higher = smoother).

Volume Baseline (RVOL): SMA window for relative volume.

Inner Value Bands (volatility-based width)

k·StdDev(residuals), k·ATR, k·MAD(residuals): Blend three measures into base width.

StdDev / ATR / MAD Lengths: Lookbacks for each.

Two-Volume Fusion

RVOL Exponent: How aggressively width responds to relative volume.

Dollar-Flow Gain: Adds push from price×volume (value traded).

Dollar-Flow Z-Window: Standardization window for dollar-flow.

Asymmetry (Order-Flow Tilt)

Enable Tilt (OBV): Lets flow skew upper/lower widths.

Tilt Strength (0..1): Gain applied to OBV slope z-score.

OBV Slope Z-Window: Window to standardize OBV slope.

Regime Adapter

Efficiency Ratio Lookback: Measures trend vs chop.

ER Width Min/Max: Maps ER into a width factor (tighter in trend, wider in chop).

Band Tracking (inner value rails)

Tracking Mode:

Base: Pure base rails.

Parallel-Lock: Smooth RVWAP & width; track in parallel.

Slope-Lock: Adds a fraction of recent slope (momentum-friendly).

Forecast-Lock: 1–3 bar extrapolation via linreg (non-repainting on closed bars).

Attach Strength (0..1): Blend tracked rails vs base rails.

Tracking Smooth Length: EMA smoothing of RVWAP and width.

Slope Influence / Forecast Lead Bars: Gains for the chosen mode.

Outer Containment Bands

Show Containment Bands: Master toggle (default ON).

Residual Extremes Lookback: Highest/lowest residual window.

Extreme Smoothing (EMA): Stability on extreme lines.

Margin vs inner width: Extra padding relative to smoothed inner width.

Squeeze & Alerts

Squeeze Window / Threshold: Width vs average; at/under threshold = dot (when enabled).

Min RVOL for Breakout: Required RVOL for breakout alerts.

Style (defaults in this release)

Inner Value rails: OFF (stepline, thin).

Inner & Containment fills: ON.

Containment rails: ON (stepline, medium).

20% / 80% guides: ON — 20% light blue, 80% light red, dashed, thin.

Squeeze dots: OFF by default (orange circles below candles when enabled).

Practical templates (copy/paste into a plan)

Momentum Breakout

Context: Squeeze cluster near RVWAP; Inner Value ON.

Trigger: Breakout Long (close > Upper Value & RVOL ≥ min).

Stop: Below Lower Value (tight) or below RVWAP (safer).

Targets (1:1:1): ⅓ Value → ⅓ Containment → ⅓ trail on RVWAP.

Pullback Continuation

Context: Uptrend; dip to RVWAP / Lower Value with cooling RVOL.

Trigger: Close back above RVWAP or break of reclaim candle’s high.

Stop: Just outside Lower Containment or pullback swing.

Targets: RVWAP → Upper Value → Upper Containment.

Containment Reversion (range)

Context: RVWAP flat; repeated containment tags.

Trigger: Stall at containment, then close back inside.

Stop: A step beyond that containment.

Target: RVWAP; runner only if RVOL stays muted.

Alerts included

DVWAP Breakout Long / Short (Value Bands)

Top Zone / Bottom Zone (20% / 80% guides)

Tip: On lower TFs, act on Breakout alerts with higher-TF bias (e.g., trade 5–15m in the direction of 1H/4H RVWAP slope/position).

Best practices

Let RVWAP be the compass; if unsure, wait until price picks a side.

Respect RVOL; low-RVOL breaks are prone to fail.

Use guides for timing, not certainty. Pair 20/80 zones with flow context.

Start with defaults; change one knob at a time.

Common pitfalls

Fading every containment touch → only fade when RVWAP is flat or RVOL cools.

Over-tuning inputs → the defaults are robust; small tweaks go a long way.

Fighting the higher timeframe on low TFs → expensive habit.

Footer — License & Publishing

License: Mozilla Public License 2.0 (MPL-2.0). You may modify and redistribute; keep this file under MPL and provide source for this file.

Originality: © 2025 JopAlgo. No third-party code reused; Pine built-ins and common formulas only.

Publishing: Keep this header/description intact when releasing on TradingView. Avoid promotional links in the public script text.

Liquidity PocketLiquidity Pocket Indicator

This indicator identifies and tracks institutional liquidity zones through pivot-based support and resistance analysis, providing visual confirmation when price returns to test these critical levels.

Core Functionality:

Dynamic Pivot Detection: Automatically identifies swing highs and lows using customizable lookback parameters

Multi-Timeframe Analysis: Option to analyze pivots from higher timeframes while displaying on current chart

Liquidity Line Tracking: Draws horizontal lines from pivot points that extend until price interference occurs

Sweep Confirmation: Generates signals when price returns to test previously established pivot levels

Key Features:

Adaptive Timeframe Selection: Choose specific timeframes or use automatic multiplier system (Lvl1-Lvl4) for systematic higher timeframe analysis

Dynamic Line Management: Automatically manages active lines with performance optimization through maximum line limits

Visual Confirmation System: Customizable display options including line styles, candle coloring, and liquidity sweep signals

ATR-Based Signal Positioning: Intelligent signal placement using Average True Range calculations for optimal visibility

Signal Logic:

The indicator monitors when price returns to previously established pivot levels, interpreting these interactions as liquidity sweeps or institutional order execution zones. Signals trigger upon contact with tracked levels, providing confirmation of institutional interest areas.

Customization Options:

Adjustable pivot sensitivity through left/right bar lookback settings

Comprehensive visual customization including colors, line styles, and signal symbols

Performance controls with maximum active line limits

Alert system for real-time liquidity event notifications

This tool excels at identifying where institutional players may have placed orders, making it valuable for understanding market structure and potential reversal zones.

52SIGNAL RECIPE Whale Smart Money Detector52SIGNAL RECIPE Whale Smart Money Detector

◆ Overview

52SIGNAL RECIPE Whale Smart Money Detector is an innovative indicator that detects the movements of whales (large investors) in the cryptocurrency market in real-time. This powerful tool tracks large-scale trading activities that significantly impact the market, providing valuable signals before important market direction changes occur. It can be applied to any cryptocurrency chart, allowing traders to follow the movements of big money anytime, anywhere.

The unique strength of this indicator lies in its comprehensive analysis of volume surges, price volatility, and trend strength to accurately capture whale market entries and exits. By providing clear visual representation of large fund flow data that is difficult for ordinary traders to detect, you gain the opportunity to move alongside the big players in the market.

─────────────────────────────────────

◆ Key Features

• Whale Activity Detection System: Analyzes volume surges and price impacts to capture large investor movements in real-time

• Precise Volume Analysis: Distinguishes between regular volume and whale volume to track only meaningful market movements

• Market Impact Measurement: Quantifies and analyzes the real impact of whale buying/selling on the market

• Continuity Tracking: Follows market direction continuity after whale activity to confirm signal validity

• Intuitive Visualization: Easily identifies whale activity points through color bar charts and clear labels

• Trend Strength Display: Calculates and displays current market buy/sell strength in real-time in a table

• Whale Signal Filtering: Applies multiple filtering systems to detect only genuine whale activity

• Customizable Sensitivity Settings: Offers flexible parameters to adjust whale detection sensitivity according to market conditions

─────────────────────────────────────

◆ Understanding Signal Types

■ Whale Buy Signal

• Definition: Occurs when volume increases significantly above average, immediate volume impact is large, and price rises beyond normal volatility

• Visual Representation: Translucent blue bar coloring with "🐋Whale Buying Detected!" label on the candle where the buy signal occurs

• Market Interpretation: Indicates that large funds are actively buying the coin, which is likely to lead to price increases

■ Whale Sell Signal

• Definition: Occurs when volume increases significantly above average, immediate volume impact is large, and price falls beyond normal volatility

• Visual Representation: Translucent pink bar coloring with "🐋Whale Selling Detected!" label on the candle where the sell signal occurs

• Market Interpretation: Indicates that large funds are actively selling the coin, which is likely to lead to price decreases

─────────────────────────────────────

◆ Understanding Trend Analysis

■ Trend Analysis Method

• Definition: Measures current trend and strength by analyzing the ratio of up/down candles over a set period

• Visual Representation: Displayed in the table as "BUY" and "SELL" percentages, with the current trend clearly marked as "BULLISH", "BEARISH", or "NEUTRAL"

• Calculation Method:

▶ Buy ratio = (Number of up candles) / (Total analysis period)

▶ Sell ratio = (Number of down candles) / (Total analysis period)

▶ Current trend determined by the dominant ratio as "BULLISH" or "BEARISH"

■ Trend Utilization Methods

• Whale Signal Confirmation: Signal reliability increases when whale signals align with the current trend

• Reversal Point Identification: Opposing whale signals during strong trends may indicate important reversal points

• Market Strength Assessment: Understand the balance of power in the current market through buy/sell ratios

• Signal Context Understanding: Consider trend information alongside whale signals for interpretation in a broader market context

─────────────────────────────────────

◆ Indicator Settings Guide

■ Key Setting Parameters

• Volume Impact Factor:

▶ Purpose: Sets the minimum multiplier for immediate volume impact to be considered whale activity

▶ Lower values: Generate more signals, detect smaller whales

▶ Higher values: Fewer signals, detect only very large whales

▶ Recommended range: 2.0-4.0 (adjust according to market conditions)

• Sensitivity Factor:

▶ Purpose: Adjusts sensitivity of price movement relative to normal volatility

▶ Lower values: Increased sensitivity, more signals generated

▶ Higher values: Decreased sensitivity, only stronger price impacts detected

▶ Recommended range: 0.2-0.5 (set higher in highly volatile markets)

• Trend Analysis Period:

▶ Purpose: Sets the number of candles to calculate buy/sell ratios

▶ Lower values: More responsive to recent trends

▶ Higher values: More stable analysis considering longer-term trends

▶ Recommended range: 30-70 (adjust according to trading style)

─────────────────────────────────────

◆ Synergy with Other Indicators

• Key Support/Resistance Levels:

▶ Whale signals occurring near important technical levels have higher reliability

▶ Coincidence of weekly/monthly pivot points and whale signals confirms important price points

• Moving Averages:

▶ Pay attention to whale signals near key moving averages (50MA, 200MA)

▶ Simultaneous occurrence of moving average breakouts and whale signals indicates important technical events

• Volume Profile:

▶ Whale activity near high volume nodes confirms important price levels

▶ Whale signals at low volume nodes may indicate possibility of rapid price movements

• Volatility Indicators:

▶ Whale signals after periods of low volatility may mark the beginning of new market movements

▶ Whale signals after Bollinger Band contraction may be precursors to large movements

• Market Structure:

▶ Whale signals near key market structures (higher highs/lows, lower highs/lows) suggest structural changes

▶ Coincidence of market structure changes and whale activity may signal important trend changes

─────────────────────────────────────

◆ Conclusion

52SIGNAL RECIPE Whale Smart Money Detector tracks the trading activities of large investors in the cryptocurrency market in real-time, providing traders with valuable insights. Because it can be applied to any cryptocurrency chart, you can utilize it immediately on your preferred trading platform.

The core value of this indicator is providing intuitive visualization of large fund flows that are easily missed by ordinary traders. By comprehensively analyzing volume surges, immediate price impacts, and trend continuity to accurately capture whale activity, you gain the opportunity to move alongside the big players in the market.

Clear buy/sell signals and real-time trend strength measurements help traders quickly grasp market conditions and understand market direction. By integrating this powerful tool into your trading system, gain insights into where the market's smart money is flowing for better market understanding.

─────────────────────────────────────

※ Disclaimer: Like all trading tools, the 52SIGNAL RECIPE Whale Smart Money Detector should be used as a supplementary indicator and not relied upon exclusively for trading decisions. Past patterns of whale behavior may not guarantee future market movements. Always employ appropriate risk management strategies in your trading.

52SIGNAL RECIPE Whale Smart Money Detector

◆ 개요

52SIGNAL RECIPE Whale Smart Money Detector는 암호화폐 시장에서 고래(대형 투자자)의 움직임을 실시간으로 감지하는 혁신적인 지표입니다. 이 강력한 도구는 시장에 큰 영향을 미치는 대규모 트레이딩 활동을 추적하여 중요한 시장 방향 전환이 일어나기 전에 귀중한 신호를 제공합니다. 모든 암호화폐 차트에 적용 가능하여 트레이더들이 언제 어디서든 대형 자금의 움직임을 따라갈 수 있게 해줍니다.

이 지표의 독보적인 강점은 거래량 급증, 가격 변동성, 그리고 추세 강도를 종합적으로 분석하여 고래의 시장 진입과 퇴출을 정확히 포착한다는 점입니다. 일반 트레이더들이 놓치기 쉬운 대형 자금의 흐름 데이터를 시각적으로 명확하게 제공함으로써, 여러분은 시장의 큰 손들과 함께 움직일 수 있는 기회를 얻게 됩니다.

─────────────────────────────────────

◆ 주요 특징

• 고래 활동 감지 시스템: 거래량 급증과 가격 임팩트를 분석하여 대형 투자자의 움직임을 실시간으로 포착

• 정밀한 거래량 분석: 일반 거래량과 고래 거래량을 구분하여 의미 있는 시장 움직임만 추적

• 시장 영향력 측정: 고래의 매수/매도가 시장에 미치는 실질적 영향력을 수치화하여 분석

• 연속성 추적: 고래 활동 이후 시장 방향의 지속성을 추적하여 신호의 유효성 확인

• 직관적 시각화: 컬러 바 차트와 명확한 라벨을 통해 고래 활동 지점을 쉽게 식별

• 추세 강도 표시: 현재 시장의 매수/매도 강도를 실시간으로 계산하여 테이블에 표시

• 고래 신호 필터링: 진정한 고래 활동만 감지하도록 다중 필터링 시스템 적용

• 맞춤형 감도 설정: 시장 상황에 따라 고래 감지 감도를 조절할 수 있는 유연한 파라미터 제공

─────────────────────────────────────

◆ 신호 유형 이해하기

■ 고래 매수 신호

• 정의: 거래량이 평균보다 크게 증가하고, 즉각적인 거래량 충격이 크며, 가격이 정상 변동성을 초과하여 상승할 때 발생

• 시각적 표현: 매수 신호가 발생한 캔들에 반투명 파란색 바 컬러링과 함께 "🐋Whale Buying Detected!" 라벨 표시

• 시장 해석: 대형 자금이 적극적으로 코인을 매수하고 있으며, 이는 곧 가격 상승으로 이어질 가능성이 높음을 의미

■ 고래 매도 신호

• 정의: 거래량이 평균보다 크게 증가하고, 즉각적인 거래량 충격이 크며, 가격이 정상 변동성을 초과하여 하락할 때 발생

• 시각적 표현: 매도 신호가 발생한 캔들에 반투명 분홍색 바 컬러링과 함께 "🐋Whale Selling Detected!" 라벨 표시

• 시장 해석: 대형 자금이 적극적으로 코인을 매도하고 있으며, 이는 곧 가격 하락으로 이어질 가능성이 높음을 의미

─────────────────────────────────────

◆ 추세 분석 이해하기

■ 추세 분석 방식

• 정의: 설정된 기간 동안의 상승/하락 캔들 비율을 분석하여 시장의 현재 추세와 강도를 측정

• 시각적 표현: 테이블에 "BUY"와 "SELL" 비율이 백분율로 표시되며, 현재 추세가 "BULLISH", "BEARISH" 또는 "NEUTRAL"로 명확하게 표시됨

• 계산 방식:

▶ 매수 비율 = (상승 캔들 수) / (전체 분석 기간)

▶ 매도 비율 = (하락 캔들 수) / (전체 분석 기간)

▶ 우세한 비율에 따라 "BULLISH" 또는 "BEARISH" 추세 결정

■ 추세 활용 방법

• 고래 신호 확인: 고래 신호가 현재 추세와 일치할 때 신호의 신뢰도가 높아짐

• 반전 포인트 식별: 강한 추세 속에서 발생하는 반대 방향의 고래 신호는 중요한 반전 포인트일 수 있음

• 시장 강도 평가: 매수/매도 비율을 통해 현재 시장의 세력 균형 파악

• 신호 발생 맥락 이해: 추세 정보와 고래 신호를 함께 고려하여 더 넓은 시장 컨텍스트에서 해석

─────────────────────────────────────

◆ 지표 설정 가이드

■ 주요 설정 매개변수

• Volume Impact Factor (거래량 임팩트 요소):

▶ 목적: 고래 활동으로 간주할 즉각적인 거래량 충격의 최소 배수 설정

▶ 낮은 값: 더 많은 신호 생성, 작은 고래도 감지

▶ 높은 값: 더 적은 신호, 매우 큰 고래만 감지

▶ 권장 범위: 2.0-4.0 (시장 상황에 따라 조정)

• Sensitivity Factor (민감도 요소):

▶ 목적: 정상 변동성 대비 가격 변동의 민감도 조절

▶ 낮은 값: 민감도 증가, 더 많은 신호 생성

▶ 높은 값: 민감도 감소, 더 강한 가격 충격만 감지

▶ 권장 범위: 0.2-0.5 (변동성이 높은 시장에서는 높게 설정)

• Trend Analysis Period (추세 분석 기간):

▶ 목적: 매수/매도 비율을 계산할 캔들 수 설정

▶ 낮은 값: 최근 추세에 더 민감하게 반응

▶ 높은 값: 더 긴 기간의 추세를 고려하여 안정적인 분석

▶ 권장 범위: 30-70 (트레이딩 스타일에 따라 조정)

─────────────────────────────────────

◆ 다른 지표와의 시너지

• 주요 지지/저항 레벨:

▶ 중요한 기술적 레벨 근처에서 발생하는 고래 신호는 더 높은 신뢰도를 가짐

▶ 주간/월간 피봇 포인트와 고래 신호의 일치는 중요한 가격 지점을 확인해줌

• 이동평균선:

▶ 주요 이동평균선(50MA, 200MA) 근처에서 발생하는 고래 신호에 주목

▶ 이동평균선 돌파와 고래 신호가 동시 발생 시 중요한 기술적 이벤트 확인

• 볼륨 프로필:

▶ 높은 볼륨 노드 근처에서의 고래 활동은 중요한 가격 레벨 확인

▶ 낮은 볼륨 노드에서 발생하는 고래 신호는 급격한 가격 이동 가능성 암시

• 변동성 지표:

▶ 낮은 변동성 구간 이후 발생하는 고래 신호는 새로운 시장 움직임의 시작일 수 있음

▶ 볼린저 밴드 수축 후 발생하는 고래 신호는 큰 움직임의 전조일 수 있음

• 시장 구조:

▶ 주요 시장 구조(높은 고점/저점, 낮은 고점/저점) 근처에서 발생하는 고래 신호는 구조 변화 암시

▶ 시장 구조 변화와 고래 활동의 일치는 중요한 트렌드 변화 신호일 수 있음

─────────────────────────────────────

◆ 결론

52SIGNAL RECIPE Whale Smart Money Detector는 암호화폐 시장에서 대형 투자자들의 거래 활동을 실시간으로 추적하여 트레이더들에게 귀중한 통찰력을 제공합니다. 모든 암호화폐 차트에 적용 가능하기 때문에, 여러분이 선호하는 트레이딩 플랫폼에서 바로 활용할 수 있습니다.

이 지표의 핵심 가치는 일반 트레이더들이 놓치기 쉬운 대형 자금의 흐름을 직관적으로 시각화하여 제공한다는 점입니다. 거래량 급증, 즉각적인 가격 충격, 그리고 추세 지속성을 종합적으로 분석하여 고래의 활동을 정확히 포착함으로써, 여러분은 시장을 움직이는 큰 손들과 함께할 수 있는 기회를 얻게 됩니다.

명확한 매수/매도 신호와 실시간 추세 강도 측정은 트레이더들이 시장 상황을 한눈에 파악하고 시장의 방향성을 이해하는 데 도움을 줍니다. 이 강력한 도구를 여러분의 트레이딩 시스템에 통합함으로써, 시장의 스마트 머니가 어디로 흘러가는지 파악하고 더 나은 통찰력을 얻으세요.

─────────────────────────────────────

※ 면책 조항: 모든 트레이딩 도구와 마찬가지로, 52SIGNAL RECIPE Whale Smart Money Detector는 보조 지표로 사용해야 하며 트레이딩 결정을 전적으로 의존해서는 안 됩니다. 과거의 고래 행동 패턴이 미래 시장 움직임을 보장하지는 않습니다. 항상 적절한 리스크 관리 전략을 트레이딩에 활용하세요.

Daily Performance Analysis [Mr_Rakun]The Daily Performance Analysis indicator is a comprehensive trading performance tracker that analyzes your strategy's success rate and profitability across different days of the week and month. This powerful tool provides detailed statistics to help traders identify patterns in their trading performance and optimize their strategies accordingly.

Weekly Performance Analysis:

Tracks wins/losses for each day of the week (Monday through Sunday)

Calculates net profit/loss for each trading day

Shows profit factor (gross profit ÷ gross loss) for each day

Displays win rate percentage for each day

Monthly Performance Analysis:

Monitors performance for each day of the month (1-31)

Provides the same detailed metrics as weekly analysis

Helps identify monthly patterns and trends

Add to Your Strategy:

Copy the performance analysis code and integrate it into your existing Pine Script strategy

Optimize Strategy: Use insights to refine entry/exit timing or avoid trading on poor-performing days

Pattern Recognition: Identify which days of the week/month work best for your strategy

Risk Management: Avoid trading on historically poor-performing days

Strategy Optimization: Fine-tune your approach based on empirical data

Performance Tracking: Monitor long-term trends in your trading success

Data-Driven Decisions: Make informed adjustments to your trading schedule

Uptrick: Asset Rotation SystemOverview

The Uptrick: Asset Rotation System is a high-level performance-based crypto rotation tool. It evaluates the normalized strength of selected assets and dynamically simulates capital rotation into the strongest asset while optionally sidestepping into cash when performance drops. Built to deliver an intelligent, low-noise view of where capital should move, this system is ideal for traders focused on strength-driven allocation without relying on standard technical indicators.

Purpose

The purpose of this tool is to identify outperforming assets based strictly on relative price behavior and automatically simulate how a portfolio would evolve if it consistently moved into the strongest performer. By doing so, it gives users a realistic and dynamic model for capital optimization, making it especially suitable during trending markets and major crypto cycles. Additionally, it includes an optional safety fallback mechanism into cash to preserve capital during risk-off conditions.

Originality

This system stands out due to its strict use of normalized performance as the only basis for decision-making. No RSI, no MACD, no trend oscillators. It does not rely on any traditional indicator logic. The rotation logic depends purely on how each asset is performing over a user-defined lookback period. There is a single optional moving average filter, but this is used internally for refinement, not for entry or exit logic. The system’s intelligence lies in its minimalism and precision — using normalized asset scores to continuously rotate capital with clarity and consistency.

Inputs

General

Normalization Length: Defines how many bars are used to calculate each asset’s normalized score. This score is used to compare asset performance.

Visuals: Selects between Equity Curve (show strategy growth over time) or Asset Performance (compare asset strength visually).

Detect after bar close: Ensures changes only happen after a candle closes (for safety), or allows bar-by-bar updates for quicker reactions.

Moving Average

Used internally for optional signal filtering.

MA Type: Lets you choose which moving average type to use (EMA, SMA, WMA, RMA, SMMA, TEMA, DEMA, LSMA, EWMA, SWMA).

MA Length: Sets how many bars the moving average should calculate over.

Use MA Filter: Turns the filter on or off. It doesn’t affect the signal directly — just adds a layer of control.

Backtest

Used to simulate equity tracking from a chosen starting point. All calculations begin from the selected start date. Prior data is ignored for equity tracking, allowing users to isolate specific market cycles or testing periods.

Starting Day / Month / Year: The exact day the strategy starts tracking equity.

Initial Capital $: The amount of simulated starting capital used for performance calculation.

Rotation Assets

Each asset has 3 controls:

Enable: Include or exclude this asset from the rotation engine.

Symbol: The ticker for the asset (e.g., BINANCE:BTCUSDT).

Color: The color for visualization (labels, plots, tables).

Assets supported by default:

BTC, ETH, SOL, XRP, BNB, NEAR, PEPE, ADA, BRETT, SUI

Cash Rotation

Normalization Threshold USDC: If all assets fall below this threshold, the system rotates into cash.

Symbol & Color: Sets the cash color for plots and tables.

Customization

Dynamic Label Colors: Makes labels change color to match the current asset.

Enable Asset Label: Plots asset name labels on the chart.

Asset Table Position: Choose where the key asset usage table appears.

Performance Table Position: Choose where the backtest performance table appears.

Enable Realism: Enables slippage and fee simulation for realistic equity tracking. Adjusted profit is shown in the performance table.

Equity Styling

Show Equity Curve (STYLING): Toggles an extra-thick visual equity curve.

Background Color: Adds a soft background color that matches the current asset.

Features

Dual Visualization Modes

The script offers two powerful modes for real-time visual insights:

Equity Curve Mode: Simulates the growth of a portfolio over time using dynamic asset rotation. It visually tracks capital as it moves between outperforming assets, showing compounded returns and the current allocation through both line plots and background color.

Asset Performance Mode: Displays the normalized performance of all selected assets over the chosen lookback period. This mode is ideal for comparing relative strength and seeing how different coins perform in real-time against one another, regardless of price level.

Multi-Asset Rotation Logic

You can choose up to 10 unique assets, each fully customizable by symbol and color. This allows full flexibility for different strategies — whether you're rotating across majors like BTC, ETH, and SOL, or including meme tokens and stablecoins. You decide the rotation universe. If none of the selected assets meet the strength threshold, the system automatically moves to cash as a protective fallback.

Key Asset Selection Table

This on-screen table displays how frequently each enabled asset was selected as the top performer. It updates in real time and can help traders understand which assets the system has historically favored.

Asset Name: Shortened for readability

Color Box: Visual color representing the asset

% Used: How often the asset was selected (as a percentage of strategy runtime)

This table gives clear insight into historical rotation behavior and asset dominance over time.

Performance Comparison Table

This second table shows a full backtest vs. chart comparison, broken down into key performance metrics:

Backtest Start Date

Chart Asset Return (%) – The performance of the asset you’re currently viewing

System Return (%) – The equity growth of the rotation strategy

Outperformed By – Shows how many times the system beat the chart (e.g., 2.1x)

Slippage – Estimated total slippage costs over the strategy

Fees – Estimated trading fees based on rotation activity

Total Switches – Number of times the system changed assets

Adjusted Profit (%) – Final net return after subtracting fees and slippage

Equity Curve Styling

To enhance visual clarity and aesthetics, the equity curve includes styling options:

Custom Thickness Curve: A second stylized line plots a shadow or highlight of the main equity curve for stronger visual feedback

Dynamic Background Coloring: The chart background changes color to match the currently held asset, giving instant visual context

Realism Mode

By enabling Realism, the system calculates estimated:

Trading Fees (default 0.1%)

Slippage (default 0.05%)

These costs are subtracted from the equity curve in real time, and shown in the table to produce an Adjusted Return metric — giving users a more honest and execution-aware picture of system performance.

Adaptive Labeling System

Each time the asset changes, an on-chart label updates to show:

Current Asset

Live Equity Value

These labels dynamically adjust in color and visibility depending on the asset being held and your styling preferences.

Full Customization

From visual position settings to table placements and custom asset color coding, the entire system is fully modular. You can move tables around the screen, toggle background visuals, and control whether labels are colored dynamically or uniformly.

Key Concepts

Normalized values represent how much an asset has changed relative to its past price over a fixed period, allowing performance comparisons across different assets. Outperforming refers to the asset with the highest normalized value at a given time. Cash fallback means the system moves into a stable asset like USDC when no strong performers are available. The equity curve is a running total of simulated capital over time. Slippage is the small price difference between expected and actual trade execution due to market movement.

Use Case Flexibility

You don’t need to use all 10 assets. The system works just as effectively with only 1 asset — such as rotating between CASH and SOL — for a simple, minimal strategy. This is ideal for more focused portfolios or thematic rotation systems.

How to Use the Indicator

To use the Uptrick: Asset Rotation System, start by selecting which assets to include and entering their symbols (e.g., BINANCE:BTCUSDT). Choose between Equity Curve mode to see simulated portfolio growth, or Asset Performance mode to compare asset strength. Set your lookback period, backtest start date, and optionally enable the moving average filter or realism settings for slippage and fees. The system will then automatically rotate into the strongest asset, or into cash if no asset meets the strength threshold. Use alerts to be notified when a rotation occurs.

Asset Switch Alerts

The script includes built-in alert conditions for when the system rotates into a new asset. You can enable these to be notified when the system reallocates to a different coin or to cash. Each alert message is labeled by target asset and can be used for automation or monitoring purposes.

Conclusion

The Uptrick: Asset Rotation System is a next-generation rotation engine designed to cut through noise and overcomplication. It gives users direct insight into capital strength, without relying on generic indicators. Whether used to track a broad basket or focus on just two assets, it is built for accuracy, adaptability, and transparency — all in real-time.

Disclaimer

This script is for research and educational purposes only. It is not intended as financial advice. Past performance is not a guarantee of future results. Always consult with a financial professional and evaluate risks before trading or investing.

EMA POD Indicator #gangesThis script is a technical analysis indicator that uses multiple Exponential Moving Averages (EMAs) to identify trends and track price changes in the market. Here's a breakdown:

EMA Calculation: It calculates six different EMAs (for periods 5, 10, 20, 50, 100, and 150) to track short- and long-term trends.

Trend Identification:

Uptrend: The script identifies an uptrend when the EMAs are in ascending order (EMA5 > EMA10 > EMA20 > EMA50 > EMA100 > EMA150).

Downtrend: A downtrend is identified when the EMAs are not in ascending order.

Trend Change Tracking: It tracks when an uptrend starts and ends, displaying the duration of the trend and the percentage price change during the trend.

Visuals:

It plots the EMAs on the chart with different colors.

It adds green and red lines to represent the ongoing uptrend and downtrend.

Labels are displayed showing when the uptrend starts and ends, along with the trend's duration and price change percentage.

In short, this indicator helps visualize trends, track their changes, and measure the impact of those trends on price.

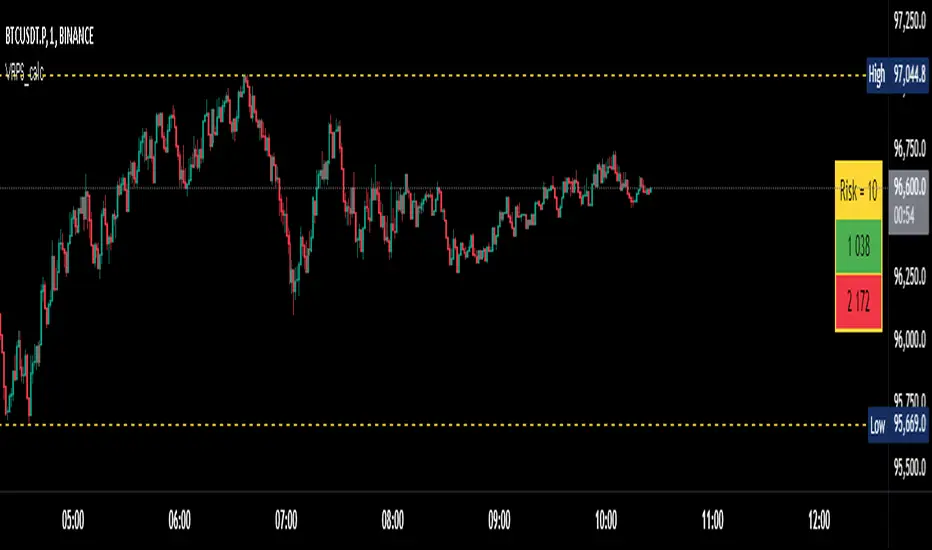

Visual Range Position Size CalculatorVisual Range Position Size Calculator

The "VR Position Size Calculator" helps traders determine the appropriate position size based on their risk tolerance and the current market conditions. Below is a detailed description of the script, its functionality, and how to use it effectively.

---

Key Features

1. Risk Calculation: The script allows users to input their desired risk in monetary terms (in the currency of the ticker). It then calculates the position sizes for both long and short trades based on this risk.

2. Dynamic High and Low Tracking: The script dynamically tracks the highest and lowest prices within the visible range of the chart, allowing for more accurate position sizing.

3. Formatted Output: The calculated values are displayed in a user-friendly table format with thousands separators for better readability.

4. Visual Indicators: Dashed lines are drawn on the chart at the high and low points of the visible range, providing a clear visual reference for traders.

5. If the risk in security price is 1% or less, the background of the cells displaying position sizes will be green for long positions and red for short positions. If the risk is between 1% and 5%, the background changes to gray, indicating that the risk may be too high for an effective trade. If the risk exceeds 5% of the price, the text also turns gray, rendering it invisible, which signifies that there is no justification for such a trade.

---

Code Explanation

The script identifies the start and end times of the visible range on the chart, ensuring calculations are based only on the data currently in view. It updates and stores the highest (hh) and lowest (ll) prices within this visible range. At the end of the range, dashed lines are drawn at the high and low prices, providing a visual cue for traders.

Users can input their risk amount, which is then used to calculate potential position sizes for both long and short trades based on the current price relative to the tracked high and low. The calculated risk values and position sizes are displayed in a table on the right side of the chart, with color coding to indicate whether the calculated position size meets specific criteria.

---

Usage Instructions

1. Add the Indicator: To use this script, copy and paste it into Pine Script editor, then add it to your chart.

2. Input Your Risk: Adjust the 'Risk in money' input to reflect your desired risk amount for trading.

3. Analyze Position Sizes: Observe the calculated position sizes for both long and short trades displayed in the table. Use this information to guide your trading decisions.

4. Visual Cues: Utilize the dashed lines on the chart to understand recent price extremes within your visible range.

Absorption AnalysisThe Absorption Analysis indicator identifies potential market turning points by analyzing volume, price patterns, and market structure across multiple dimensions. It combines traditional technical signals with volume analysis and success rate tracking to provide high-probability reversal opportunities.

Signal Types & Classification

1. Pattern-Based Signals (W-Bottom & M-Top)

**W-Bottom Pattern**

- Pattern Structure:

* Price makes a low below the lower Bollinger Band

* First bounce occurs with price moving higher

* Secondary test forms a higher low

* Final confirmation with bullish close above lower band

- Volume Requirements:

* Must exceed 1.5x the 20-period volume moving average

- Visual Indicators:

* Blue dotted line appears at pattern low

* Line remains until broken by price

* Label shows volume and percentage from baseline

- Success Tracking:

* Pattern stored in historical database

* Success measured by upward price movement

* Historical success rate displayed with signal

**M-Top Pattern**

- Pattern Structure:

* Price makes a high above the upper Bollinger Band

* First pullback occurs with price moving lower

* Secondary push forms a lower high

* Final confirmation with bearish close below upper band

- Volume Requirements:

* Must exceed 1.5x the 20-period volume moving average

- Visual Indicators:

* Orange dotted line appears at pattern high

* Line remains until broken by price

* Label shows volume and percentage from baseline

- Success Tracking:

* Pattern stored in historical database

* Success measured by downward price movement

* Historical success rate displayed with signal

2. Technical Reversals

**Bullish Reversal**

- Entry Conditions:

* Previous candle closes below lower Bollinger Band

* Previous candle must be bearish

* Current candle closes above lower band

* Current candle must be bullish

- Volume Validation:

* Volume must exceed 1.5x 20-period MA

- Visual Markers:

* Green label at reversal point

* Includes volume context

- Trading Implementation:

* Suggests strong buying pressure overcoming selling

* Often marks end of downward price exhaustion

**Bearish Reversal**

- Entry Conditions:

* Previous candle closes above upper Bollinger Band

* Previous candle must be bullish

* Current candle closes below upper band

* Current candle must be bearish

- Volume Validation:

* Volume must exceed 1.5x 20-period MA

- Visual Markers:

* Red label at reversal point

* Includes volume context

- Trading Implementation:

* Suggests strong selling pressure overcoming buying

* Often marks end of upward price exhaustion

3. Volume-Based Reversals

**High Volume Bear to Bull**

- Signal Formation:

* High volume bearish candle (2.5σ above mean)

* Immediately followed by high volume bullish candle

- Market Psychology:

* Shows strong selling being absorbed by buying

* Often indicates institutional accumulation

- Visual Identification:

* Purple "HV Bull" label

* Includes volume statistics

- Trading Context:

* Strong signal for trend reversal

* Most effective at support levels

**High Volume Bull to Bear**

- Signal Formation:

* High volume bullish candle (2.5σ above mean)

* Immediately followed by high volume bearish candle

- Market Psychology:

* Shows strong buying being absorbed by selling

* Often indicates institutional distribution

- Visual Identification:

* Purple "HV Bear" label

* Includes volume statistics

- Trading Context:

* Strong signal for trend reversal

* Most effective at resistance levels

4. Absorption Signals

**Buy Absorption**

- Technical Requirements:

* High volume conditions (2.5σ above mean)

* Spread momentum must be negative

* Fast spread MA below slow spread MA

* Bullish closing candle

- Market Interpretation:

* Indicates buying pressure absorbing selling

* Often precedes upward movement

- Visual Markers:

* Red label with volume context

* Placed at significant price levels

**Sell Absorption**

- Technical Requirements:

* High volume conditions (2.5σ above mean)

* Spread momentum must be negative

* Fast spread MA below slow spread MA

* Bearish closing candle

- Market Interpretation:

* Indicates selling pressure absorbing buying

* Often precedes downward movement

- Visual Markers:

* Green label with volume context

* Placed at significant price levels

Volume Analysis Components

Volume Calculation

- Rolling baseline volume calculated based on timeframe:

* Monthly: 6-period sum

* Weekly: 12-period sum

* Daily: 20-period sum

* Intraday: Proportional to timeframe

- Net volume = Bullish volume - Bearish volume

- Volume percentage calculated against baseline

- High volume threshold = 2.5 standard deviations

- Pattern volume threshold = 1.5x 20MA

Exchange Aggregation

- Primary symbol (chart) always included

- Optional secondary symbol data

- Combines volume data for stronger signals

- Useful for crypto markets with split liquidity

Success Rate Implementation

Rate Calculation

- Based on user-defined lookback period

- Separately tracked for each pattern type

- Bullish patterns: Percentage of times price moved higher

- Bearish patterns: Percentage of times price moved lower

- Used to filter alerts with minimum threshold

Pattern Storage

- Arrays maintain historical pattern data

- Limited to lookback period size

- Oldest patterns removed as new ones form

- Constantly updated success rates

## Trading Implementation

### Signal Priority

1. Pattern Signals (W/M)

- Highest reliability due to complex criteria

- Must meet all volume and price conditions

- Line break provides clear invalidation

2. High Volume Reversals

- Strong indication of institutional activity

- Clear volume confirmation

- Immediate reversal potential

3. Technical Reversals

- Traditional technical analysis backbone

- Enhanced with volume confirmation

- Good for trend trading

4. Absorption Signals

- Early warning system

- Best used with other confirmations

- Good for position building

Best Practices

- Look for multiple signal types aligning

- Consider higher timeframe context

- Use success rates to filter setups

- Monitor volume context closely

- Wait for candle closes

- Use line breaks for clear invalidation

- Consider market structure

- Pay attention to success rates

- Use appropriate position sizing

Risk Management

- Use pattern breaks for stop losses

- Consider historical success rates

- Larger positions for multiple signal confluence

- Respect timeframe hierarchy

- Monitor volume for confirmation

- Use proper position sizing

- Consider market volatility

This indicator provides a comprehensive framework for identifying potential market turning points while maintaining rigorous risk management through multiple confirmation factors and clear invalidation levels.

Trend Continuation RatioThis TradingView indicator calculates the likelihood of consecutive bullish or bearish days over a specified period, giving insights into day-to-day continuation patterns within the market.

How It Works

Period Length Input:

The user sets the period length (e.g., 20 days) to analyze.

After each period, the counts reset, allowing fresh data for each new interval.

Bullish and Bearish Day Definitions:

A day is considered bullish if the closing price is higher than the opening price.

A day is considered bearish if the closing price is lower than the opening price.

Count Tracking:

Within each specified period, the indicator tracks:

Total Bullish Days: The number of days where the close is greater than the open.

Total Bearish Days: The number of days where the close is less than the open.

Bullish to Bullish Continuations: Counts each instance where a bullish day is followed by another bullish day.

Bearish to Bearish Continuations: Counts each instance where a bearish day is followed by another bearish day.

Calculating Continuation Ratios:

The Bullish Continuation Ratio is calculated as the percentage of bullish days that were followed by another bullish day:

Bullish Continuation Ratio = (Bullish to Bullish Continuations /Total Bullish Days)×100

Bullish Continuation Ratio=( Total Bullish Days/Bullish to Bullish Continuations )×100

The Bearish Continuation Ratio is the percentage of bearish days followed by another bearish day:

Bearish Continuation Ratio = (Bearish to Bearish Continuations/Total Bearish Days)×100

Bearish Continuation Ratio=( Total Bearish Days/Bearish to Bearish Continuations )×100

Display on Chart:

The indicator displays a table in the top-right corner of the chart with:

Bullish Continuation Ratio (%): Percentage of bullish days that led to another bullish day within the period.

Bearish Continuation Ratio (%): Percentage of bearish days that led to another bearish day within the period.

Usage Insights

High Ratios: If the bullish or bearish continuation ratio is high, it suggests a trend where bullish/bearish days often lead to similar days, indicating possible momentum.

Low Ratios: Low continuation ratios indicate frequent reversals, which could suggest a range-bound or volatile market.

This indicator is helpful for assessing short-term trend continuation tendencies, allowing traders to gauge whether they are more likely to see follow-through on bullish or bearish days within a chosen timeframe.

LumleyTrading GapsName: LumleyTrading Gaps

Description:

The Gap Tracker Indicator is a powerful tool designed for traders to identify, monitor, and capitalize on price gaps in financial markets. It serves two primary functions:

Identifying Gaps: The indicator scans price action to detect instances where the current trading session's opening price significantly differs from the previous session's closing price. These disparities indicate the presence of price gaps.

Tracking Gap Fills: Once a gap is identified, the indicator continues to monitor the price movement. It dynamically adjusts its parameters to track whether and when the price retraces back to fill the gap. As soon as the gap is filled, the indicator generates a signal to notify traders of this occurrence.

Key Features:

Customizable Parameters: Traders can adjust the sensitivity and criteria for what constitutes a significant gap based on their trading preferences and the market conditions.

Visual Alerts: The indicator provides clear visual signals on price charts, highlighting the presence of gaps and indicating when they are filled. This helps traders to easily spot trading opportunities and make informed decisions.

Alert Notifications: In addition to visual cues, traders can opt to receive real-time alerts via email, SMS, or within their trading platform, ensuring they never miss an opportunity or a filled gap.

Historical Analysis: The indicator may also offer historical gap data, allowing traders to conduct backtesting and analyze the performance of trading strategies based on gap patterns.

Benefits:

Gap Trading Opportunities: Traders can use the indicator to identify potential areas of price continuation or reversal, leveraging the phenomenon of gap trading for profit.

Risk Management: By tracking gap fills, traders can manage their risk more effectively, knowing when a gap is likely to act as support or resistance and adjusting their positions accordingly.

Enhanced Decision Making: With real-time gap detection and fill tracking, traders gain valuable insights into market sentiment and price dynamics, empowering them to make timely and informed trading decisions.

Compatibility:

The Gap Tracker Indicator is compatible with popular trading platforms and can be seamlessly integrated into various technical analysis tools and strategies.

Conclusion:

In the fast-paced world of financial markets, identifying and understanding price gaps is crucial for successful trading. The Gap Tracker Indicator provides traders with a reliable tool to spot, track, and capitalize on gap opportunities, enhancing their trading efficiency and profitability.

Ultimate Multi-Asset Correlation System by able eiei Ultimate Multi-Asset Correlation System - User Guide

Overview

This advanced TradingView indicator combines WaveTrend oscillator analysis with comprehensive multi-asset correlation tracking. It helps traders understand market relationships, identify regime changes, and spot high-probability trading opportunities across different asset classes.

Key Features

1. WaveTrend Oscillator

Main Signal Lines: WT1 (blue) and WT2 (red) plot momentum and its moving average

Overbought/Oversold Zones: Default levels at +60/-60

Cross Signals:

🟢 Bullish: WT1 crosses above WT2 in oversold territory

🔴 Bearish: WT1 crosses below WT2 in overbought territory

Higher Timeframe (HTF) Analysis: Shows WT1 from 4H, Daily, and Weekly timeframes for trend confirmation

2. Multi-Asset Correlation Tracking

Monitors relationships between:

Major Assets: Gold (XAUUSD), Dollar Index (DXY), US 10-Year Yield, S&P 500

Crypto Assets: Bitcoin, Ethereum, Solana, BNB

Cross-Asset Analysis: Correlation between traditional markets and crypto

3. Market Regime Detection

Automatically identifies market conditions:

Risk-On: High correlation + positive sentiment (🟢 Green background)

Risk-Off: High correlation + negative sentiment (🔴 Red background)

Crypto-Risk-On: Strong crypto correlations (🟠 Orange background)

Low-Correlation: Divergent market behavior (⚪ Gray background)

Neutral: Mixed signals (🟡 Yellow background)

How to Use

Basic Setup

Add to Chart: Apply the indicator to any chart (works on all timeframes)

Choose Display Mode (Display Options):

All: Shows everything (recommended for comprehensive analysis)

WaveTrend Only: Focus on momentum signals

Correlation Only: View market relationships

Heatmap Only: Simplified correlation view

Enable Asset Groups:

✅ Major Assets: Traditional markets (stocks, bonds, commodities)

✅ Crypto Assets: Digital currencies

Mix and match based on your trading focus

Reading the Charts

WaveTrend Section (Bottom Panel)

Above 0 = Bullish momentum

Below 0 = Bearish momentum

Above +60 = Overbought (potential reversal)

Below -60 = Oversold (potential bounce)

Lighter lines = Higher timeframe trends

Correlation Histogram (Colored Bars)

Blue bars: Major asset correlations

Orange bars: Crypto correlations

Purple bars: Cross-asset correlations

Bar height: Correlation strength (-50 to +50 scale)

Background Color

Intensity reflects correlation strength

Color shows market regime

Dashboard Elements

🎯 Market Regime Analysis (Top Left)

Current Regime: Overall market condition

Average Correlation: Strength of relationships (0-1 scale)

Risk Sentiment: -100% (risk-off) to +100% (risk-on)

HTF Alignment: Multi-timeframe trend agreement

Signal Quality: Confidence level for current signals

📊 Correlation Matrix (Top Right)

Shows correlation values between asset pairs:

1.00: Perfect positive correlation

0.75+: Strong correlation (🟢 Green)

0.50+: Medium correlation (🟡 Yellow)

0.25+: Weak correlation (🟠 Orange)

Below 0.25: Negative/no correlation (🔴 Red)

🔥 Correlation Heatmap (Bottom Right)

Visual matrix showing:

Gold vs. DXY, BTC, ETH

DXY vs. BTC, ETH

BTC vs. ETH

Color-coded strength

📈 Performance Tracker (Bottom Left)

Tracks individual asset momentum:

WT1 Values: Current momentum reading

Status: OB (overbought) / OS (oversold) / Normal

Trading Strategies

1. High-Probability Trend Following

✅ Entry Conditions:

WaveTrend bullish/bearish cross

HTF Alignment matches signal direction

Signal Quality > 70%

Correlation supports direction

2. Regime Change Trading

🎯 Watch for regime shifts:

Risk-Off → Risk-On = Consider long positions

High correlation → Low correlation = Reduce position size

Crypto-Risk-On = Focus on crypto longs

3. Divergence Trading

🔍 Look for:

Strong correlation breakdown = Potential volatility

Cross-asset correlation surge = Follow the leader

Volume-price correlation extremes = Trend confirmation

4. Overbought/Oversold Reversals

⚡ Trade reversals when:

WT crosses in extreme zones (-60/+60)

HTF alignment shows opposite trend weakening

Correlation confirms mean reversion setup

Customization Tips

Fine-Tuning Parameters

WaveTrend Core:

Channel Length (10): Lower = more sensitive, Higher = smoother

Average Length (21): Adjust for your timeframe

Correlation Settings:

Length (50): Longer = more stable, Shorter = more responsive

Smoothing (5): Reduce noise in correlation readings

Market Regime:

Risk-On Threshold (0.6): Lower = earlier regime signals

High Correlation Threshold (0.75): Adjust sensitivity

Custom Asset Selection

Replace default symbols with your preferred markets:

Major Assets: Any forex, indices, bonds

Crypto: Any digital currencies

Must use correct exchange prefix (e.g., BINANCE:BTCUSDT)

Alert System

Enable "Advanced Alerts" to receive notifications for:

✅ Market regime changes

✅ Correlation breakdowns/surges

✅ Strong signals with high correlation

✅ Extreme volume-price correlation

✅ Complete HTF alignment

Correlation Interpretation Guide

ValueMeaningTrading Implication+0.75 to +1.0Strong positiveAssets move together+0.5 to +0.75Moderate positiveGenerally aligned+0.25 to +0.5Weak positiveLoose relationship-0.25 to +0.25No correlationIndependent movements-0.5 to -0.25Weak negativeSlight inverse relationship-0.75 to -0.5Moderate negativeTend to move opposite-1.0 to -0.75Strong negativeStrongly inversely correlated

Best Practices

Use Multiple Timeframes: Check HTF alignment before trading

Confirm with Correlation: Strong signals work best with supportive correlations

Watch Regime Changes: Adjust strategy based on market conditions

Volume Matters: Enable volume-price correlation for confirmation

Quality Over Quantity: Trade only high-quality setups (>70% signal quality)

Common Patterns to Watch

🔵 Risk-On Environment:

Gold-BTC positive correlation

DXY negative correlation with risk assets

High crypto correlations

🔴 Risk-Off Environment:

Flight to safety (Gold up, stocks down)

DXY strength

Correlation breakdowns

🟡 Transition Periods:

Low correlation across assets

Mixed HTF signals

Use caution, reduce position sizes

Technical Notes

Calculation Period: Uses HLC3 (average of high, low, close)

Correlation Window: Rolling correlation over specified length

HTF Data: Accurately calculated using security() function

Performance: Optimized for real-time calculation on all timeframes

Support

For optimal performance:

Use on 15-minute to daily timeframes

Enable only needed asset groups

Adjust correlation length based on trading style

Combine with your existing strategy for confirmation

Enjoy comprehensive multi-asset analysis! 🚀

Inversion Fair Value Gap Model [PJ Trades]GENERAL OVERVIEW:

The Inversion Fair Value Gap Model indicator is a complete rule-based system designed to identify trade setups using the Inversion Fair Value Gap strategy taught by PJ Trades. It automates the strategy’s workflow by detecting liquidity sweeps, confirming V-shape recoveries, identifying valid Inversion Fair Value Gaps, validating higher-timeframe Fair Value Gap taps, and checking for a clear opposite Draw On Liquidity. These factors are evaluated together to produce a signal rating of A, A+, or A++, based on how many of these criteria the setup satisfies. When a long or short setup is confirmed, the indicator automatically plots an entry, stop-loss, break-even, and two take-profit levels.

A dashboard that updates in real-time displays the current directional bias, liquidity sweep activity, Inversion Fair Value Gap confirmation state, V Shape Recovery state, higher-timeframe Fair Value Gap context, opposite Draw on Liquidity, SMT divergence, and other key information relevant to the trading model. The indicator also includes optional trade statistics on the dashboard that tracks the recent win rates for A, A+, and A++ setups, as well as separate long and short win rates.

This indicator was developed by Flux Charts, in collaboration with PJ Trades.

What is the theory behind the indicator?:

The Inversion Fair Value Gap model is built on the idea that when the market pushes above a high or below a low, it often does so to sweep liquidity. If that move quickly fails and price reverses, it shows the sweep was a grab for orders and not a continuation. That quick rejection is the V Shape Recovery behavior. An Inversion Fair Value Gap forms when a Fair Value Gap that once supported the original move gets invalidated afterward. That invalidation confirms the shift in direction and becomes the new reference point for trades. The Inversion Fair Value Gap model uses this sequence because it highlights when the market has taken liquidity, rejected continuation, and started delivering in the opposite direction.

INVERSION FAIR VALUE GAP MODEL FEATURES:

The Inversion Fair Value Gap Model indicator includes 15 main features:

Sessions

Key Levels & Swing Levels

Liquidity Levels

Liquidity Sweeps

V Shape Recoveries

Higher-Timeframe Fair Value Gaps

Inversion Fair Value Gaps

Macros

Bias

Signals

New Day Opening Gap

New Week Opening Gap

SMT Divergences

Dashboard

Alerts

SESSIONS:

The Inversion Fair Value Gap Model indicator includes five trading sessions (times in EST):

Asia: 20:00 - 00:00

London: 02:00 - 05:00

NY AM: 09:30 - 12:15

NY Lunch: 12:15 - 13:30

NY PM: 13:30 - 16:00

Session highs and lows are automatically tracked and used within the indicator’s signal logic.

🔹Session Zones:

Each session has a zone that outlines its active time window. These zones can be toggled on or off independently. When active, they visually separate each part of the trading day. Users can adjust the color and opacity of each session box. Users can also enable session labels, which place a label above each session zone showing its corresponding session name.

🔹Session Time:

Users can toggle on ‘Time’ which will display each session’s time window next to its session title.

🔹Session Highs/Lows:

Every session can display its own high and low as horizontal lines. Users can customize the line style for session highs/lows, choosing between solid, dashed, or dotted. The color of the lines will match the same color used for the session box. Users can adjust the color of the labels as well, which is applied to all session high/low labels.

When price has moved above a session high, or below a session low, the label will not be displayed anymore.

🔹Extend Levels:

When enabled, each session’s high and low levels can be extended forward by a set number of bars.

Please Note: Disabling a session under the main Sessions section only hides its visuals (boxes, lines, or labels). It does not impact signal detection or logic.

KEY LEVELS:

The Inversion Fair Value Gap Model indicator includes 11 key market levels that outline important structural price areas across daily, weekly, and monthly timeframes. These levels include the Daily Open, Previous Day High/Low, Weekly Open, Previous Week High/Low, Monthly Open, Previous Month High/Low, Midnight Open, and 08:30 Open. The levels can be enabled or disabled and customized in color and line style. All of the levels except the Midnight Open and 08:30 Open are used for the indicator’s signal logic.

🔹Daily Open

The Daily Open marks where the current trading day began.

🔹Previous Day High/Low

The Previous Day High (PDH) marks the highest price reached during the previous regular trading session. It shows where buyers pushed price to its highest point before the market closed.

The Previous Day Low (PDL) marks the lowest price reached during the previous regular trading session. It shows where selling pressure reached its lowest point before buyers stepped in.

When price pushes above the PDH or below the PDL, the level is removed from the chart.

🔹Weekly Open

The Weekly Open marks the first price of the current trading week.

🔹Previous Week High/Low

The Previous Week High (PWH) marks the highest price reached during the previous trading week. It shows where buying pressure reached its peak before the weekly close.

The Previous Week Low (PWL) marks the lowest price reached during the previous trading week. It shows where sellers pushed price to its lowest point before buyers regained control.

When price pushes above the PWH or below the PWL, the level is removed from the chart.

🔹Monthly Open

The Monthly Open marks the opening price of the current month.

🔹Previous Month High/Low

The Previous Month High (PMH) marks the highest price reached during the previous calendar month. It represents the point at which buyers achieved the strongest push before the monthly close.

The Previous Month Low (PML) marks the lowest price reached during the previous calendar month. It shows where selling pressure was strongest before buyers stepped back in.

When price pushes above the PMH or below the PML, the level is removed from the chart.

🔹Midnight Open

The Midnight Open marks the first price of the trading day at 00:00 EST.

🔹08:30 Open

The 08:30 Open marks the opening price at 08:30 EST.

🔹Customization Options:

Users can fully customize the appearance of all key levels, including the following:

Labels

Label Size

Line Style

Line Colors

Labels:

Users can toggle on ‘Show Labels’ to display labels for each toggled-on level that price hasn’t pushed above/below. Users can also adjust the size of labels, choosing between auto, tiny, small, normal, large, or huge.

Line Style:

Users can select a line style, choosing between solid, dashed, or dotted, which is applied to all toggled-on key levels.

Line Color:

Users can choose different colors for each of the following key levels:

Daily Open, Previous Day High, Previous Day Low

Weekly Open, Previous Week High, Previous Week Low,

Monthly Open, Previous Month High, Previous Month Low

Midnight Open

08:30 Open

🔹Extend Levels:

When enabled, each key level is extended forward by a set number of bars.

Please Note: Disabling a level in the “Key Levels” section only hides its visuals and does not affect the indicator’s signals.

🔹Swing Levels

The indicator automatically plots Swing Highs and Swing Lows which are used in the indicator’s signal generation logic.

A swing high forms when a candle’s high is greater than the highs of the bars immediately before and after it.

A swing low forms when a candle’s low is lower than the lows of the bars immediately before and after it.

🔹Swing Level Colors

Users can customize the color of Active Levels and Swept Levels.

Active Levels are levels that price has not pushed above or below

Swept Levels are levels that price pushed above or below.

🔹Swing Levels – Show Nearest

This setting determines how many swing highs/lows are displayed on the chart. The indicator will display the nearest X highs to price and the nearest X lows to price.

For example, if ‘Show Nearest’ is set to 2, the nearest 2 swing highs and nearest 2 swing lows to price will be plotted on the chart.

LIQUIDITY LEVELS:

The Inversion Fair Value Gap Model indicator automatically identifies and plots liquidity at key structural points in the market. These include swing highs and swing lows, session highs and lows, and major higher timeframe reference points as explained in the SESSIONS and KEY LEVELS sections above. All of these areas are treated as potential pools of resting orders and are used throughout the indicator’s signal logic.

🔹What is Buyside Liquidity?:

Buyside Liquidity (BSL) represents price levels where many buy stop orders are sitting, usually from traders holding short positions. When price moves into these areas, those stop-loss orders get triggered and short sellers are forced to buy back their positions. These zones often form above key highs such as the previous day, week, or month. Understanding BSL is important because when price reaches these levels, the sudden wave of buy orders can create sharp reactions or reversals as liquidity is taken from the market.

🔹What is Sellside Liquidity?:

Sellside Liquidity (SSL) represents price levels where many sell stop orders are waiting, usually from traders holding long positions. When price drops into these areas, those stop-loss orders are triggered and long traders are forced to sell their positions. These zones often form below key lows such as the previous day, week, or month. Understanding SSL is important because when price reaches these levels, the surge of sell orders can cause sharp reactions or reversals as liquidity is taken from the market.

🔹 Which Liquidity Levels Are Used

The indicator tracks liquidity at the following areas:

Asia Session High/Low

London High/Low

NY AM High/Low

NY Lunch High/Low

NY PM High/Low

Previous Day High and Low

Previous Week High and Low

Previous Month High and Low

Daily Open

Weekly Open

Monthly Open

Swing Highs/Lows

🔹 How Liquidity Levels Are Used

All tracked levels across sessions, swing points, and higher timeframes serve as potential liquidity targets. When price trades above one of these highs, the indicator looks for short setups if other confluences align. When price trades below lows, the indicator looks for long setups if other confluences align.

LIQUIDITY SWEEPS:

The indicator automatically detects Buyside Liquidity and Sellside Liquidity sweeps using the liquidity levels mentioned in the previous section.

🔹What is a Liquidity Sweep?

Liquidity sweeps occur when price trades beyond a key high or low and activates resting buy-stop or sell-stop orders in that area. It’s how the market gathers the liquidity needed for larger participants to enter positions.

Traders often place stop-loss orders around obvious highs and lows, such as the previous day’s, week’s, or month’s levels. When price pushes through one of these areas, it triggers the stops placed there and generates a burst of volume. This can lead to quick movements in price as those orders are executed.

🔹Sellside Liquidity Sweep

These occur when price dips below a Sellside Liquidity (SSL) level, taking out the stop-loss orders placed by long traders below that low. When this happens, the indicator records the sweep and begins monitoring for potential long setups as the next step in the IFVG trading strategy. Long trades are only eligible after a SSL sweep.

🔹Buyside Liquidity Sweep

These occur when price dips above a Buyside Liquidity (BSL) level, taking out the stop-loss orders placed by short seller traders above that high. When this happens, the indicator records the sweep and begins monitoring for potential short setups as the next step in the trading strategy. Short trades are only eligible after a BSL sweep.

🔹How to Use Liquidity Sweeps

Liquidity sweeps are not direct trade signals. They are best used as context when forming a directional bias. A sweep shows that the market has removed liquidity from one side, which can hint at where the next move may develop.

For example:

When BSL is swept, it often signals that buy stops have been triggered and the market may be preparing to move lower. Traders may then begin looking for short opportunities.

When SSL is swept, it often signals that sell stops have been triggered and the market may be preparing to move higher. Traders may then begin looking for long opportunities.

V SHAPE RECOVERIES:

🔹 What Is a V Shape Recovery?

A V shape recovery is a sharp, immediate reversal that happens right after price sweeps BSL or SSL. It indicates that price quickly moved back in the opposite direction after trading through the level. This behavior signals a shift in momentum and is a required confirmation in the indicator for signal generation. The indicator will not look for long trades after a SSL sweep unless a V shape recovery occurs. It will not look for short trades after a BSL sweep unless a V shape recovery occurs. Without this behavior, the indicator assumes that price may still be delivering in the direction of the sweep, so no valid setups can form.

🔹 Why V Shape Recoveries Matter

V shape recoveries help confirm that the liquidity the sweep did not immediately continue in the same direction. They separate false breaks from true continuation. A sweep without recovery often means price may keep trending, so the indicator does not generate signals in those cases. A sweep with a V shape recovery confirms rejection and sets the foundation for valid Inversion Fair Value Gap formation. This makes the V shape recovery one of the most important sequence steps in the Inversion Fair Value Gap Model.

🔹 How the Indicator Detects V Shape Recoveries

V shape recoveries can be visually intuitive when looking at a chart, but they are difficult to define consistently programmatically. To ensure reliable and repeatable detection, the indicator uses a rules-based method that evaluates candle size, candle direction, and the strength of the move immediately following the liquidity sweep. This approach removes subjectivity and allows the indicator to confirm V shape behavior the same way every time.

The indicator does not plot any visual elements specifically for V shape recoveries. Instead, the presence of a V shape recovery is implied through the signals themselves. Every valid long or short signal that appears after a liquidity sweep requires a confirmed V shape recovery. This means that if a signal is generated following a sweep, a V shape recovery has occurred.

🔹 V Shape Recovery After a Sellside Sweep (SSL Sweep)

After price trades below a sellside liquidity level, long positions are liquidated. If buyers quickly step in and force price upward with strong momentum, this forms a V shape recovery. This signals that the sweep below the low was rejected and that buyers have reclaimed control. When this occurs, the indicator begins monitoring for long setups.

🔹 V Shape Recovery After a Buyside Sweep (BSL Sweep)

After price pushes above a buyside liquidity level, many short positions are stopped out. If sellers immediately step in and drive price back down with strong movement, this forms a V shape recovery. This behavior reflects a quick change in candle direction immediately following the sweep. When this occurs, the indicator begins monitoring for short setups.

🔹Failed V Shape Recoveries

These examples show failed V shape recoveries, where price did not reverse decisively after the BSL or SSL sweep. The lack of strong response from buyers or sellers indicates that momentum did not shift. Thus, the indicator will not detect valid long/short setups using these liquidity sweeps.

HIGHER-TIMEFRAME FAIR VALUE GAPS:

Higher-timeframe Fair Value Gaps (HTF FVGs) provide important context in the Inversion Fair Value Gap Model because they show where significant imbalance occurred on larger market structures. The indicator automatically detects HTF FVGs and uses them as part of the signal rating system.

🔹 What Is a Fair Value Gap?

A Fair Value Gap (FVG) is an area where the market’s perception of fair value suddenly changes. On your chart, it appears as a three-candle pattern: a large candle in the middle, with smaller candles on each side that don’t fully overlap it.

A bullish FVG forms when a bullish candle is between two smaller bullish/bearish candles, where the first and third candles’ wicks don’t overlap each other at all.

A bearish FVG forms when a bearish candle is between two smaller bullish/bearish candles, where the first and third candles’ wicks don’t overlap each other at all.

This creates an imbalance because price moved so quickly that one side of the auction did not trade.

Examples:

🔹 What Makes an FVG “Higher-Timeframe”?

In this indicator, HTF FVGs are Fair Value Gaps detected on timeframes higher than the chart’s current timeframe. For example, on a 5-minute chart, a 1-hour FVG would be considered a HTF FVG. The indicator automatically plots and checks whether price interacts with these HTF FVGs during a liquidity sweep and incorporates this into the signal rating (A, A+, A++).

🔹 How the Indicator Uses Higher-Timeframe FVGs

The indicator automatically scans up to three user-selected higher timeframes for valid bullish and bearish FVGs and tracks price’s behavior around them in the background. When any of these higher timeframes are enabled, their FVGs are used directly within the signal logic.

During a liquidity sweep, the indicator checks whether price taps into any enabled HTF FVG. A tap occurs when price trades inside the boundaries of a higher-timeframe FVG during or immediately after the sweep.

A bullish HTF FVG tap during a sellside sweep supports a long setup.