Globex time (New York Time)This indicator is designed to highlight and analyze price movements within the Globex session. Primarily geared toward the Globex Trap trading strategy, this tool visually identifies the session's high and low prices, allowing traders to better assess price action during extended hours. Here’s a comprehensive breakdown of its features and functionality:

Purpose

The "Globex Time (New York Time)" indicator tracks price levels during the Globex trading session, providing a clear view of overnight market activity. This session, typically running from 6 p.m. ET (18:00) until the following morning at 8:30 a.m. ET, is a critical period where significant market positioning can occur before the regular session opens. In the Globex Trap strategy, the session high and low are essential levels, as price movements around these areas often indicate potential support, resistance, or reversal zones, which traders use to set up entries or exits when the regular trading session begins.

Key Features

Customizable Session Start and End Times

The indicator allows users to specify the exact start and end times of the Globex session in New York time. The default settings are:

Start: 6 p.m. ET (18:00)

End: 8:30 a.m. ET

These settings can be adjusted to align with specific market hours or personal preferences.

Session High and Low Identification

Throughout the defined session, the indicator dynamically calculates and tracks:

Session High: The highest price reached within the session.

Session Low: The lowest price reached within the session.

These levels are essential for the Globex Trap strategy, as price action around them can indicate likely breakout or reversal points when regular trading resumes.

Vertical Lines for Session Start and End

The indicator draws vertical lines at both the session start and end times:

Session Start Line: A solid line marking the exact beginning of the Globex session.

Session End Line: A similar vertical line marking the session’s conclusion.

Both lines are customizable in terms of color and thickness, making it easy to distinguish the session boundaries visually on the chart.

Horizontal Lines for Session High and Low

At the end of the session, the indicator plots horizontal lines representing the Globex session's high and low levels. Users can customize these lines:

Color: Define specific colors for the session high (default: red) and session low (default: green) to easily differentiate them.

Line Style: Options to set the line style (solid, dashed, or dotted) provide flexibility for visual preferences and chart organization.

Automatic Reset for Daily Tracking

To adapt to the next trading day, the indicator resets the session high and low data once the current session ends. This reset prepares it to start tracking new levels at the beginning of the next session without manual intervention.

Practical Application in the Globex Trap Strategy

In the Globex Trap strategy, traders are primarily interested in price behavior around the high and low levels established during the overnight session. Common applications of this indicator for this strategy include:

Breakout Trades: Watching for price to break above the Globex high or below the Globex low, indicating potential momentum in the breakout direction.

Reversal Trades: Monitoring for failed breakouts or traps where price tests and rejects the Globex high or low, suggesting a reversal as liquidity is trapped in these zones.

Support and Resistance Zones: Using the session high and low as key support and resistance levels during the regular trading session, with potential entry or exit points when price approaches these areas.

Additional Configuration Options

Vertical Line Color and Width: Define the color and thickness of the vertical session start and end lines to match your chart’s theme.

Upper and Lower Line Colors and Styles: Customize the appearance of the session high and low horizontal lines by setting color and line style (solid, dashed, or dotted), making it easy to distinguish these critical levels from other chart markings.

Summary

This indicator is a valuable tool for traders implementing the Globex Trap strategy. It visually segments the Globex session and marks essential price levels, helping traders analyze market behavior overnight. Through its customizable options and clear visual representation, it simplifies tracking overnight price activity and identifying strategic levels for potential trade setups during the regular session.

"session" için komut dosyalarını ara

FluxPulse Beacon## FluxPulse Beacon

FluxPulse Beacon applies a microstructure lens to every bar, combining directional thrust, realized volatility, and multi-timeframe liquidity checks to decide whether the tape is being pushed by real sponsorship or just noise. The oscillator's color-coded columns and adaptive burst thresholds transform complex flow dynamics into a single actionable flux score for futures and equities traders.

HOW IT WORKS

Momentum Extraction – Price differentials over a configurable pulse distance are smoothed using exponential moving averages to isolate directional thrust without reacting to single prints.

Volatility + Liquidity Normalization – The momentum stream is divided by realized volatility and multiplied by both local and higher-timeframe EMA volume ratios, ensuring pulses only appear when volatility and liquidity align.

Adaptive Thresholding – A volatility-derived standard deviation of flux is blended with the base threshold so bursts scale automatically between low-volatility and high-volatility market conditions.

Divergence Engine – Linear regression slopes compare price vs. flux to tag bullish/bearish divergences, highlighting stealth accumulation or distribution zones.

HOW TO USE IT

Continuation Entries : Go with the trend when histogram bars stay above the adaptive threshold, the signal line confirms, and trend bias agrees—this is where liquidity-backed follow-through lives.

Fade Plays : Watch for divergence alerts and shrinking compression values; when flux prints below zero yet price grinds higher, hidden selling pressure often precedes rollovers.

Session Filter : Compression percentage in the diagnostics table instantly tells you whether to trade thin overnight sessions—low compression means stand down.

VISUAL FEATURES

Dynamic background heat maps flux magnitude, while threshold lines provide a quick read on whether a pulse is statistically significant.

Diagnostics table displays live flux, signal, adaptive threshold, and compression for quick reference.

Alert-first workflow: The surface is intentionally clean—bursts and divergences are delivered via alerts instead of on-chart clutter.

PARAMETERS

Trend EMA Length (default: 34): Defines the macro bias anchor; increase for higher-timeframe confirmation.

Pulse Distance (default: 8): Controls how sensitive momentum extraction becomes.

Volatility Window (default: 21): Sample window for realized volatility normalization.

Liquidity Window (default: 55): Volume smoothing window that proxies liquidity expansion.

Liquidity Reference TF (default: 60): Select a higher timeframe to cross-check whether current volume matches institutional flows.

Adaptive Threshold (default: enabled): Disable for fixed thresholds on slower markets; enable for high-volatility assets.

Base Burst Threshold (default: 1.25): Minimum flux magnitude that qualifies as an actionable pulse.

ALERTS

The indicator includes four alert conditions:

Bull Burst: Detects upside liquidity pulses

Bear Burst: Detects downside liquidity pulses

Bull Divergence: Flags bullish delta divergence

Bear Divergence: Flags bearish delta divergence

LIMITATIONS

This indicator is designed for liquid futures and equity markets. Performance may degrade in low-volume or highly illiquid instruments. The adaptive threshold system works best on timeframes where sufficient volatility history exists (typically 15-minute charts and above). Divergence signals are probabilistic and should be confirmed with price action.

INSERT_CHART_SNAPSHOT_URL_HERE

---

## RangeLattice Mapper

RangeLattice Mapper constructs a higher-timeframe scaffolding on any intraday chart, locking in structural highs/lows, mid/quarter grids, VWAP confluence, and live acceptance/break analytics. It provides a non-repainting overlay that turns range management into a disciplined process.

HOW IT WORKS

Structure Harvesting – Using request.security() , the script samples highs/lows from a user-selected timeframe (default 240 minutes) over a configurable lookback to establish the dominant range.

Grid Construction – Midpoint and quarter levels are derived mathematically, mirroring how institutional traders map distribution/accumulation zones.

Acceptance Detection – Consecutive closes inside the range flip an acceptance flag and darken the cloud, signaling balanced auction conditions.

Break Confirmation – Multi-bar closes outside the structure raise break labels and alerts, filtering the countless fake-outs that plague breakout traders.

VWAP Fan Overlay – Session VWAP plus ATR-based bands provide a live measure of flow centering relative to the lattice.

HOW TO USE IT

Range Plays : Fade taps of the outer rails only when acceptance is active and VWAP sits inside the grid—this is where mean-reversion works best.

Breakout Plays : Wait for confirmed break labels before entering expansion trades; the dashboard's Width/ATR metric tells you if the expansion has enough fuel.

Market Prep : Carry the same lattice from pre-market into regular trading hours by keeping the structure timeframe fixed; alerts keep you notified even when managing multiple tickers.

VISUAL FEATURES

Range Tap and Mid Pivot markers provide a tape-reading breadcrumb trail for journaling.

Cloud fill opacity tightens when acceptance persists, visually signaling balance compressions ready to break.

Dashboard displays absolute width, ATR-normalized width, and current state (Balanced vs Transitional) so you can glance across charts quickly.

Acceptance Flag toggle: Keep the repeated acceptance squares hidden until you need to audit balance.

PARAMETERS

Structure Timeframe (default: 240): Choose the timeframe whose ranges matter most (4H for indices, Daily for stocks).

Structure Lookback (default: 60): Bars sampled on the structure timeframe.

Acceptance Bars (default: 8): How many consecutive bars inside the range confirm balance.

Break Confirmation Bars (default: 3): Bars required outside the range to validate a breakout.

ATR Reference (default: 14): ATR period for width normalization.

Show Midpoint Grid (default: enabled): Display the midpoint and quarter levels.

Show Adaptive VWAP Fan (default: enabled): Toggle the VWAP channel for assets where volume distribution matters most.

Show Acceptance Flags (default: disabled): Turn the acceptance markers on/off for maximum visual control.

Show Range Dashboard (default: enabled): Disable if screen space is limited, re-enable during prep sessions.

ALERTS

The indicator includes five alert conditions:

Range High Tap: Price interacted with the RangeLattice high

Range Low Tap: Price interacted with the RangeLattice low

Range Mid Tap: Price interacted with the RangeLattice mid

Range Break Up: Confirmed upside breakout

Range Break Down: Confirmed downside breakout

LIMITATIONS

This indicator works best on liquid instruments with clear structural levels. On very low timeframes (1-minute and below), the structure may update too frequently to be useful. The acceptance/break confirmation system requires patience—faster traders may find the multi-bar confirmation too slow for scalping. The VWAP fan is session-based and resets daily, which may not suit all trading styles.

---

Channels by TradingConTotoThis indicator plots clear and minimalistic High (H) and Low (L) pivot points only within the selected trading session (e.g., 10:00–12:00).

During the active session, the background is shaded for easy visual reference, and pivot labels alternate automatically — meaning no consecutive H or L points appear in a row. This makes it simple to identify real swing changes within a specific session.

⚙️ Features

Detects and labels pivots only during the chosen time range.

Alternating logic prevents consecutive highs or lows (H → L → H → L).

Clean session background highlight for visual clarity.

Fully customizable parameters (session time, sensitivity, colors, etc.).

Ideal for intraday traders, scalpers, and structure-based strategies.

💡 Suggested Use

Perfect for traders who focus on specific market sessions (e.g., New York, London, or custom hours).

The alternating pivot logic helps visualize market swings and structural shifts without visual clutter, making it an excellent companion for price action analysis.

Futures Key LevelsKey Levels — Sessions, Previous Ranges & Opens (Chicago-aligned sessions)

What it does

This indicator plots commonly used reference levels across multiple timeframes to help you frame the day and find confluence:

Sessions (Chicago TZ): London, New York, and Asia session high/low ranges.

Previous Period Ranges: Previous Day / Week / Month / Quarter / Year High/Low and optional Mid.

Opens: Current Daily / Weekly / Monthly / Quarterly / Yearly opens.

Intraday (4H): Previous 4-Hour High/Low + optional Mid.

Monday Range: Captures Monday’s High/Low (and optional Mid) to use as a weekly reference.

Price-scale markers: Optional markers that track key levels on the price scale without adding extra lines.

How it works (concepts & calculations)

Higher-timeframe values are retrieved using request.security() and update when a new period begins (e.g., previous day’s H/L become fixed at the start of the new day).

Session ranges are built from bar data within session windows using time(session, "America/Chicago"):

London: 02:00–05:00 CT

New York: 08:30–15:00 CT

Asia: 20:00–00:00 CT

“Mid” levels are simple midpoints between each period’s High and Low.

Merge Levels: when different levels land at the same price, their labels are merged to reduce clutter (e.g., “PDH / PWH”).

Why this version is useful / original bits

All-white baseline for clean charts; session colors stand out by design: London = Yellow, New York = Aquatic Blue, Asia = Red.

Right-anchored mode lets you park levels to the right side of the chart with a configurable anchor distance.

Label merging keeps the display minimal when multiple levels coincide.

Price-scale-only markers available when you prefer fewer lines on the chart.

Inputs & customization

Display Style: Standard or Right Anchored (+ distance controls).

Levels toggles: enable/disable each period (Daily/Weekly/Monthly/Quarterly/Yearly), Monday range, 4H range, and session ranges.

Text: optional shorthand labels (e.g., PDH/PDL, PWH/PWL).

Colors: global white theme, with session highlights; you can override in the Inputs.

Price-scale markers: on/off toggle.

How to use it

Use previous High/Low as liquidity pools and areas to watch for sweeps, breaks, or retests.

The Monday range often frames the rest of the week; breaks or rejections around Monday H/L can be informative.

The 4H previous range gives intraday context—great for mean-reversion vs. continuation reads.

Session ranges help you see where the active session expanded price and where liquidity may remain.

Notes & limitations

Sessions are computed in America/Chicago; higher-TF levels use the symbol’s exchange timezone.

This is an indicator, not a strategy; it does not place trades or claim performance.

Always combine levels with your own execution rules (structure, momentum, risk).

Credit: inspired by spacemanBTC; this version adds the all-white styling, Chicago-aligned sessions, right-anchoring, label merging, and price-scale markers.

Also my mentor to tell me about the levels

Disclaimer

This tool is for educational purposes only and is not financial advice. Markets involve risk; do your own research and manage risk appropriately.

BPS Multi-MA 5 — 22/30, SMA/WMA/EMA# Multi-MA 5 — 22/30 base, SMA/WMA/EMA

**What it is**

A lightweight 5-line moving-average ribbon for fast visual bias and trend/mean-reversion reads. You can switch the MA type (SMA/WMA/EMA) and choose between two ways of setting lengths: by monthly “session-based” base (22 or 30) with multipliers, or by entering exact lengths manually. An optional info table shows the effective settings in real time.

---

## How it works

* Calculates five moving averages from the selected price source.

* Lengths are either:

* **Multipliers mode:** `Base × Multiplier` (e.g., base 22 → 22/44/66/88/110), or

* **Manual mode:** any five exact lengths (e.g., 10/22/50/100/200).

* Plots five lines with fixed legend titles (MA1…MA5); the **info table** displays the actual type and lengths.

---

## Inputs

**Length Mode**

* **Multipliers** — choose a **Base** of **22** (≈ trading sessions per month) or **30** (calendar-style, smoother) and set **×1…×5** multipliers.

* **Manual** — enter **Len1…Len5** directly.

**MA Settings**

* **MA Type:** SMA / WMA / EMA

* **Source:** any series (e.g., `close`, `hlc3`, etc.)

* **Use true close (ignore Heikin Ashi):** when enabled, the MA is computed from the underlying instrument’s real `close`, not HA candles.

* **Show info table:** toggles the on-chart table with the current mode, type, base, and lengths.

---

## Quick start

1. Add the indicator to your chart.

2. Pick **MA Type** (e.g., **WMA** for faster response, **SMA** for smoother).

3. Choose **Length Mode**:

* **Multipliers:** set **Base = 22** for session-based monthly lengths (stocks/FX), or **30** for heavier smoothing.

* **Manual:** enter your exact lengths (e.g., 10/22/50/100/200).

4. (Optional) On **Heikin Ashi** charts, enable **Use true close** if you want the lines based on the instrument’s real close.

---

## Tips & notes

* **1 month ≈ 21–22 sessions.** Using 30 as “monthly” yields a smoother, more delayed curve.

* **WMA** reacts faster than **SMA** at the same length; expect earlier signals but more whipsaws in chop.

* **Len = 1** makes the MA track the chosen source (e.g., `close`) almost exactly.

* If changing lengths doesn’t move the lines, ensure you’re editing fields for the **active Length Mode** (Multipliers vs Manual).

* For clean comparisons, use the **same timeframe**. If you later wrap this in MTF logic, keep `lookahead_off` and handle gaps appropriately.

---

## Use cases

* Trend ribbon and dynamic bias zones

* Pullback entries to the mid/slow lines

* Crossovers (fast vs slow) for confirmation

* Volatility filtering by spreading lengths (e.g., 22/44/88/132/176)

---

**Credits:** Built for clarity and speed; designed around session-based “monthly” lengths (22) or smoother calendar-style (30).

VWAP Suite {Phanchai}VWAP Suite {Phanchai}

Compact, readable, TradingView-friendly.

What is VWAP?

The Volume Weighted Average Price (VWAP) is the average price of a period weighted by traded volume. It’s used as a fair-value reference (mean) and resets at the start of each new period.

Included VWAP Modes

Session — resets each trading day (current session).

Week / Month / Quarter / Year — current calendar periods.

Anchored Week / Month / Quarter / Year — starts at the beginning of the previous completed period.

Rolling 7D / 30D / 90D — rolling windows: today + last 6/29/89 daily sessions.

Important

This suite does not generate buy/sell signals. It provides structure and confluence; decisions remain yours.

Use Cases

Identify fair-value zones / mean-reversion areas.

Plan TP / SL around periodic VWAPs.

Define DCA levels (e.g., anchored to prior week/month).

Gauge trend bias via VWAP slope and reactions.

How to Use

Inputs → VWAP 1..5: Choose the period per slot (Session, Anchored, Rolling, etc.) and toggle Show .

Sources: Select the price source for all VWAPs (default: HLC3).

Global: Line offset (bars) shifts plots visually (does not affect calculations).

Style tab: Adjust per-line colors, thickness, and line style.

Alerts

Price crosses a VWAP (per slot).

VWAP slope turns UP or DOWN (per slot).

Tips & Notes

Volume required: Poor/absent volume (e.g., some FX tickers) can degrade accuracy.

Anchored modes: Start at the prior period’s open; values appear only after that timestamp.

Rolling modes: Use completed daily sessions (including today).

Clutter control: If labels crowd, increase Line offset or hide unneeded slots.

Confluence: Combine with market structure, liquidity zones, or momentum filters for stronger context.

Built for clear VWAP workflows. Trade safe!

MACROFLOW 200 — Bias & Triggersstephtradez model

MACROFLOW 200 — at a glance (the elevator pitch)

Trade direction = Macro Bias + 1H 200 EMA filter + DXY confirm.

Locations = 1H supply/demand zones.

Triggers (15m): (T1) Retest rejection, (T2) Liquidity sweep + BOS/CHOCH, (T3) Momentum break + shallow pullback.

Stops: structure‑based beyond zone with ATR buffer.

Targets: 2R base, scale at 1.5R, trail to next HTF zone.

Sessions: 7–10 pm ET and 9:30–10:30 am ET.

Risk: tight, prop‑friendly max 1% per session

ABS Companion Oscillator — Trend / Exhaustion / New Trend (v1.1)

# ABS Companion Oscillator — Trend / Exhaustion / New Trend (v1.1)

## What it is (quick take)

**ABS CO** is a unified **–100…+100 trend oscillator** that fuses:

* **Regime**: EMA stack (fast/slow/long) + **HTF slope** (e.g., 60-minute)

* **Momentum**: **TSI** vs its signal

* **Stretch**: session-anchored **VWAP Z-score** for exhaustion and “fresh-trend” sanity checks

It paints the oscillator with **lime** in upstate, **red** in downstate, **gray** in neutral, and tags:

* **NEW↑ / NEW↓** when a **new trend** likely starts (zero-line cross with acceptable stretch)

* **EXH↑ / EXH↓** when an **existing trend looks exhausted** (large |Z| + momentum rollback)

> Use it as a **direction filter and context layer**. Works great in front of an entry engine and behind an exit tool.

---

## How to use it (operational workflow)

1. **Read the state**

* **Uptrend** when the oscillator is **≥ upThresh** (default +55) → prefer **long-side** plays.

* **Downtrend** when the oscillator is **≤ dnThresh** (default −55) → prefer **short-side** plays.

* **Neutral** between thresholds → be selective or flat; expect chop.

2. **Act on events**

* **NEW↑ / NEW↓**: zero-line cross with acceptable |Z| (not already overstretched). Treat as **trend start** cues.

* **EXH↑ / EXH↓**: trend state with **high |Z|** and TSI rollback versus its signal. Treat as **trend fatigue**; avoid fresh go-with entries and tighten risk.

3. **Practical pairing**

* Use **up/down state** (or above/below **neutralBand**) as your go/no-go filter for entries.

* Prioritize entries **with** NEW↑/NEW↓ and **without** nearby EXH tags.

* Keep holding while the oscillator stays in state and no EXH appears; consider scaling out on EXH or on your exit tool.

---

## Visual semantics & alerts

* **ABS CO line** (–100…+100): lime in upstate, red in downstate, gray in neutral.

* **Horizontal guides**: `Up` threshold, `Down` threshold, `Zero`, and optional **neutral band** lines.

* **Background heat** (optional): shaded when EXH conditions trigger (lime/red tint with intensity scaled by |Z|).

* **Tags**: `NEW↑`, `NEW↓`, `EXH↑`, `EXH↓`.

**Alerts (stable):**

* **ABS CO — New Uptrend** (NEW↑)

* **ABS CO — New Downtrend** (NEW↓)

* **ABS CO — Exhausted Up** (EXH↑)

* **ABS CO — Exhausted Down** (EXH↓)

Set alerts to **“Once per bar close”** for clean signals.

---

## Non-repainting behavior

* HTF queries use **lookahead\_off**.

* With **Strict NR = true**, the HTF slope is taken from the **prior completed** HTF bar; events evaluate on confirmed bars → **safer, fewer, cleaner**.

* NEW/EXH tags finalize at bar close. Disabling strictness yields earlier but noisier responses.

---

## Every input explained (and how it changes behavior)

### A) Trend & HTF structure

* **EMA Fast / Slow / Long (`emaFastLen`, `emaSlowLen`, `emaLongLen`)**

Control the baseline regime. Larger = smoother, fewer flips; smaller = snappier, more flips.

* **HTF EMA Len (`htfLen`)** & **HTF timeframe (`htfTF`)**

HTF slope filter. Longer len or higher TF = steadier bias (fewer state changes); shorter/ lower = more sensitive.

* **Strict NR (`strictNR`)**

`true` uses the **previous** HTF bar for slope and evaluates on confirmed bars → cleaner, slower.

### B) Momentum (TSI)

* **TSI Long / Short / Signal (`tsiLong`, `tsiShort`, `tsiSig`)**

Standard TSI. Larger values = smoother momentum, fewer EXH triggers; smaller = snappier, more EXH sensitivity.

### C) Stretch (VWAP Z-score)

* **VWAP Z-score length (`zLen`)**

Window for Z over session-anchored VWAP distance. Larger = smoother |Z|; smaller = more reactive stretch detection.

* **Exhaustion |Z| (`zHot`)**

Minimum |Z| to flag **EXH**. Raise to demand **bigger** stretch (fewer EXH); lower to catch milder excess.

* **Max |Z| for NEW (`zNewMax`)**

NEW requires |Z| **≤ zNewMax** (avoid “new trend” when already stretched). Lower = stricter; higher = more NEW tags.

### D) States & thresholds

* **Uptrend threshold (`upThresh`)** / **Downtrend threshold (`dnThresh`)**

Where the oscillator flips into trend states. Widen (e.g., +60/−60) to reduce false states; narrow to get earlier signals.

* **Neutral band (`neutralBand`)**

Visual buffer around zero for “meh” momentum. Larger band = fewer go/no-go flips near zero.

### E) Visuals & tags

* **Show New / Show Exhausted (`showNew`, `showExh`)**

Toggle the tag labels.

* **Shade exhaustion heat (`plotHeat`)**

On = color background when EXH fires. Helpful for scanning.

### F) Smoothing

* **Osc smoothing (`smoothLen`)**

EMA over the raw composite. Higher = steadier line (fewer whip flips); lower = faster turns.

---

## Tuning recipes

* **Trend-day bias (follow moves longer)**

* Raise **`upThresh`** to \~60 and **`dnThresh`** to \~−60

* Keep **`zNewMax`** low (1.0–1.2) to avoid “fresh trend” when stretched

* **`smoothLen`** 3–5 to reduce noise

* **Range-day bias (fade edges)**

* Keep thresholds closer (e.g., +50/−50) for quicker state changes

* Lower **`zHot`** slightly (1.6–1.7) to catch earlier exhaustion

* Consider slightly shorter TSI (e.g., 21/9/5) for faster EXH response

* **Scalping LTF (1–3m)**

* TSI 21/9/5, **`smoothLen`** 1–2

* Thresholds +/-50; **`zNewMax`** 1.0–1.2; **`zHot`** 1.6–1.8

* StrictNR **off** if you want earlier calls (accept more noise)

* **Swing / HTF (1h–D)**

* TSI 35/21/9, **`smoothLen`** 4–7

* Thresholds +/-60\~65; **`zNewMax`** 1.2; **`zHot`** 1.8–2.0

* StrictNR **on** for cleaner bias

---

## Playbooks (how to actually trade it)

* **Go/No-Go Filter**

* Only take **long entries** when the oscillator is **above the neutral band** (preferably ≥ `upThresh`).

* Only take **short entries** when **below** the neutral band (preferably ≤ `dnThresh`).

* Avoid fresh go-with entries if an **EXH** tag appears; let the next setup re-arm.

* **Trend Genesis**

* Treat **NEW↑ / NEW↓** as “green light” for **first pullback** entries in the new direction (ideally within acceptable |Z|).

* **Trend Maturity**

* When in a position and **EXH** prints **against** you, tighten stops, take partials, or lean on your exit tool to protect gains.

---

## Suggested starting points

* **Day trading (5–15m):**

* TSI 25/13/7, `smoothLen=3`, thresholds **+55 / −55**, `zNewMax = 1.2`, `zHot = 1.8`, **StrictNR = true**

* **Scalping (1–3m):**

* TSI 21/9/5, `smoothLen=1–2`, thresholds **+50 / −50**, `zNewMax = 1.1–1.2`, `zHot = 1.6–1.8`, **StrictNR = false** (optional)

* **Swing (1h–D):**

* TSI 35/21/9, `smoothLen=4–6`, thresholds **+60 / −60**, `zNewMax = 1.2`, `zHot = 1.9–2.0`, **StrictNR = true**

---

## Notes & best practices

* **Session anchoring**: Z-score is session-anchored (resets by trading date). If you trade outside standard sessions, verify your data session.

* **Instrument specificity**: Tune **`zHot`**, **`zNewMax`**, and thresholds per symbol and timeframe.

* **Bar-close discipline**: Evaluate tags at **bar close** to avoid intrabar flip-flop.

* This is a **context/confirmation tool**, not a broker or strategy. Combine with your entry/exit rules and position sizing.

---

**Tip:** Start with the suggested day-trading profile. Use this oscillator as your **gate** (only trade with it), let your entry engine time executions, and rely on your exit tool for standardized profit-taking.

Supply/Demand Zones - Fixed v3 (Cross YES Only)This Pine Script indicator creates Supply/Demand Zones with specific filtering criteria for TradingView. Here's a comprehensive description:

Supply/Demand Zones -(Cross YES Only)

Core Functionality

Session-Based Analysis: Identifies and visualizes price ranges during user-defined time sessions

Cross Validation Filter: Only displays zones when the "Cross" condition is met (Open and Close prices cross the mid-range level)

Real-Time Monitoring: Tracks price action during active sessions and creates zones after session completion

Key Features

Time Range Configuration

Customizable session hours (start/end time with minute precision)

Timezone support (default: Europe/Bucharest)

Flexible scheduling for different trading sessions

Visual Elements

Range Border: Dotted outline showing the full session range (High to Low)

Key Levels: Horizontal lines for High, Low, and Mid-range levels

Sub-Range Zones: Shaded areas showing Open and Close price zones

Percentage Labels: Display the percentage of range occupied by Open/Close zones

Active Session Background: Blue background highlighting during active sessions

Smart Filtering System

Cross Condition: Only creates zones when:

Open < Mid AND Close > Mid (bullish cross), OR

Open > Mid AND Close < Mid (bearish cross)

This filter ensures only significant price movements that cross the session's midpoint are highlighted

Customization Options

Display Controls: Toggle visibility for borders, lines, zones, and labels

Color Schemes: Full color customization for all elements

Transparency Settings: Adjustable transparency for zone fills

Text Styling: Configurable label colors and information display

Technical Specifications

Maximum capacity: 500 boxes, 500 lines, 200 labels

Overlay indicator (draws directly on price chart)

Bar-time based positioning for accurate historical placement

Use Cases

Supply/Demand Trading: Identify key price levels where institutions may have interest

Session Analysis: Understand price behavior during specific trading hours

Breakout Detection: Focus on sessions where price crosses significant levels

Support/Resistance: Use range levels for future trade planning

What Makes It Unique

The "Cross YES Only" filter ensures that only meaningful price sessions are highlighted - those where the market shows directional bias by crossing from one side of the range to the other, indicating potential institutional interest or significant market sentiment shifts.

NY HIGH LOW BREAKNY HIGH LOW BREAK: A New York Session Breakout Strategy

The "NY HIGH LOW BREAK" indicator is a powerful TradingView script designed to identify and capitalize on breakout opportunities during the New York trading session. This strategy focuses on the initial price action of the New York market open, looking for clear breaches of the high or low established within the first 30 minutes. It's particularly suited for intraday traders who seek to capture momentum-driven moves.

Strategy Logic

The core of the "NY HIGH LOW BREAK" strategy revolves around these key components:

New York Session Opening Range Identification:

The script first identifies the opening range of the New York session. This is defined by the high and low prices established during the first 30 minutes of the New York trading session (from 7:01 AM GMT-4 to 7:31 AM GMT-4).

These crucial levels are then extended forward on the chart as horizontal lines, serving as potential support and resistance zones.

Breakout Signal Generation:

Long Signal: A buy signal is generated when the price breaks above the high of the New York opening range. Specifically, it looks for a candle whose open and close are both above the highLinePrice, and importantly, the previous candle's open was below and close was above the highLinePrice. This indicates a strong upward momentum confirming the breakout.

Short Signal: Conversely, a sell signal is generated when the price breaks below the low of the New York opening range. It looks for a candle whose open and close are both below the lowLinePrice, and the previous candle's open was above and close was below the lowLinePrice. This suggests strong downward momentum confirming the breakdown.

Supertrend Filter (Implicit/Future Enhancement):

While the supertrend and direction variables are present in the code, they are not actively used in the current signal generation logic. This suggests a potential future enhancement where the Supertrend indicator could be incorporated as a trend filter to confirm breakout directions, adding an extra layer of confluence to the signals. For example, only taking long breakouts when Supertrend indicates an uptrend, and short breakouts when Supertrend indicates a downtrend.

Second Candle Confirmation (Possible Future Enhancement):

The close_sec_candle function and openSEC, closeSEC variables indicate an attempt to capture the open and close of a "second candle" (30 minutes after the initial New York open). Currently, closeSEC is used in a specific condition for signal_way but not directly in the primary longSignal or shortSignal logic. This also suggests a potential future refinement where the price action of this second candle could be used for further confirmation or specific entry criteria.

Time-Based Filtering:

Signals are only considered valid within a specific trading window from 8:00 AM GMT-4 to 8:00 AM GMT-4 + 16 * 30 minutes (which is 480 minutes, or 8 hours) on 1-minute and 5-minute timeframes. This ensures that trades are taken during the most active and volatile periods of the New York session, avoiding late-session chop.

The script also highlights the New York session and lunch hours using background colors, providing visual context to the trading day.

Key Features

Automated New York Open Range Detection: The script automatically identifies and plots the high and low of the first 30 minutes of the New York trading session.

Clear Breakout Signals: Visually distinct "BUY" and "SELL" labels appear on the chart when a breakout occurs, making it easy to spot trading opportunities.

Timeframe Adaptability: While optimized for 1-minute and 5-minute timeframes for signal generation, the opening range lines can be displayed on various timeframes.

Customizable Risk-to-Reward (RR): The rr input allows users to define their preferred risk-to-reward ratio for potential trades, although it's not directly implemented in the current signal or trade management logic. This could be used by traders for manual trade management.

Visual Session and Lunch Highlights: The script colors the background to clearly delineate the New York trading session and the lunch break, helping traders understand the market context.

How to Use

Apply the Indicator: Add the "NY HIGH LOW BREAK" indicator to your chart on TradingView.

Select a Relevant Timeframe: For optimal signal generation, use 1-minute or 5-minute timeframes.

Observe the Opening Range: The green and red lines represent the high and low of the first 30 minutes of the New York session.

Look for Breakouts: Wait for price to decisively break above the green line (for a buy) or below the red line (for a sell).

Confirm Signals: The "BUY" or "SELL" labels will appear on the chart when the breakout conditions are met within the active trading window.

Implement Your Risk Management: Use your preferred risk management techniques, including stop-loss and take-profit levels, in conjunction with the signals generated. The rr input can guide your manual risk-to-reward calculations.

Potential Enhancements & Considerations

Supertrend Confirmation: Integrating the supertrend variable to filter signals would significantly enhance the strategy's robustness by aligning trades with the prevailing trend.

Stop-Loss and Take-Profit Automation: The rr input currently serves as a manual guide. Future versions could integrate automated stop-loss and take-profit placement based on this ratio, potentially using ATR for dynamic sizing.

Volume Confirmation: Adding a volume filter to confirm breakouts would ensure that only high-conviction moves are traded.

Backtesting and Optimization: Thorough backtesting across various assets and market conditions is crucial to determine the optimal settings and profitability of this strategy.

Session Times: The current session times are hardcoded. Making these user-definable inputs would allow for greater flexibility across different time zones and trading preferences.

The "NY HIGH LOW BREAK" is a straightforward yet effective strategy for capturing initial New York session momentum. By focusing on clear breakout levels, it aims to provide timely and actionable trading signals for intraday traders.

TDO & Hit Rates by Weekday (5 min)Purpose

Tracks how often the next NY session “hits” the previous day’s True Day Open (TDO) level, separately for sessions that open above vs. below TDO, and breaks the statistics down by weekday (Mon–Fri) plus an overall summary.

Key Features

True Day Open (TDO) Plot

Captures the prior day’s 23:00 CT close price as the TDO.

Plots it as a continuous yellow line across your chart.

Session Labeling

At the end of each NY session (08:30–15:00 CT), places a small “TDO” label at the TDO price to confirm visually where it lay during that day.

Hit‑Count Logic

For each 5 min bar in the NY session, checks if the bar’s high ≥ TDO ≥ low (i.e. the TDO level was “hit”).

Classifies each session by whether its opening price (first 5 min bar) was above or below the TDO.

Weekday Statistics Table

Displays in the bottom‑left of your main chart window.

Rows: Header, Mon, Tue, Wed, Thu, Fri, All.

Columns:

% Hit Above: % of “above‑TDO” sessions that saw at least one hit

% Hit Below: % of “below‑TDO” sessions that saw at least one hit

Automatically updates in real time as new sessions complete.

Inputs & Settings

Data Resolution: Default = 5 min; use any intraday timeframe you like (1, 3, 15 min, etc.).

Extended Hours: Make sure your chart’s Extended Session (overnight) is enabled so the 23:00 CT bar exists.

Overlay: Draws directly on your price chart (no separate pane).

How to Use

Add to Chart: Paste the Pine v5 code into TradingView’s editor and apply to your ES (or other) futures chart.

Enable Overnight Bars: In Chart Settings → Symbol/Session → include Extended Hours.

Select Timeframe: Set the chart (or the indicator’s “Data Resolution” input) to 5 min (or your preferred intraday).

Read the Table:

Each weekday row shows how reliable TDO touches have been historically, separately for “above” and “below” opens.

The bottom “All” row summarizes combined performance.

What You Learn

Edge Analysis: Do sessions opening above TDO tend to test that level more often than those opening below (or vice versa)?

Day‑of‑Week Bias: Are certain weekdays more prone to TDO retests?

Overall Confidence: The “All” row lets you see your full-sample hit‑rate on both sides.

Quarterly Cycle Theory with DST time AdjustedThe Quarterly Theory removes ambiguity, as it gives specific time-based reference points to look for when entering trades. Before being able to apply this theory to trading, one must first understand that time is fractal:

Yearly Quarters = 4 quarters of three months each.

Monthly Quarters = 4 quarters of one week each.

Weekly Quarters = 4 quarters of one day each (Monday - Thursday). Friday has its own specific function.

Daily Quarters = 4 quarters of 6 hours each = 4 trading sessions of a trading day.

Sessions Quarters = 4 quarters of 90 minutes each.

90 Minute Quarters = 4 quarters of 22.5 minutes each.

Yearly Cycle: Analogously to financial quarters, the year is divided in four sections of three months each:

Q1 - January, February, March.

Q2 - April, May, June (True Open, April Open).

Q3 - July, August, September.

Q4 - October, November, December.

S&P 500 E-mini Futures (daily candles) — Monthly Cycle.

Monthly Cycle: Considering that we have four weeks in a month, we start the cycle on the first month’s Monday (regardless of the calendar Day):

Q1 - Week 1: first Monday of the month.

Q2 - Week 2: second Monday of the month (True Open, Daily Candle Open Price).

Q3 - Week 3: third Monday of the month.

Q4 - Week 4: fourth Monday of the month.

S&P 500 E-mini Futures (4 hour candles) — Weekly Cycle.

Weekly Cycle: Daye determined that although the trading week is composed by 5 trading days, we should ignore Friday, and the small portion of Sunday’s price action:

Q1 - Monday.

Q2 - Tuesday (True Open, Daily Candle Open Price).

Q3 - Wednesday.

Q4 - Thursday.

S&P 500 E-mini Futures (1 hour candles) — Daily Cycle.

Daily Cycle: The Day can be broken down into 6 hour quarters. These times roughly define the sessions of the trading day, reinforcing the theory’s validity:

Q1 - 18:00 - 00:00 Asia.

Q2 - 00:00 - 06:00 London (True Open).

Q3 - 06:00 - 12:00 NY AM.

Q4 - 12:00 - 18:00 NY PM.

S&P 500 E-mini Futures (15 minute candles) — 6 Hour Cycle.

6 Hour Quarters or 90 Minute Cycle / Sessions divided into four sections of 90 minutes each (EST/EDT):

Asian Session

Q1 - 18:00 - 19:30

Q2 - 19:30 - 21:00 (True Open)

Q3 - 21:00 - 22:30

Q4 - 22:30 - 00:00

London Session

Q1 - 00:00 - 01:30

Q2 - 01:30 - 03:00 (True Open)

Q3 - 03:00 - 04:30

Q4 - 04:30 - 06:00

NY AM Session

Q1 - 06:00 - 07:30

Q2 - 07:30 - 09:00 (True Open)

Q3 - 09:00 - 10:30

Q4 - 10:30 - 12:00

NY PM Session

Q1 - 12:00 - 13:30

Q2 - 13:30 - 15:00 (True Open)

Q3 - 15:00 - 16:30

Q4 - 16:30 - 18:00

S&P 500 E-mini Futures (5 minute candles) — 90 Minute Cycle.

Micro Cycles: Dividing the 90 Minute Cycle yields 22.5 Minute Quarters, also known as Micro Sessions or Micro Quarters:

Asian Session

Q1/1 18:00:00 - 18:22:30

Q2 18:22:30 - 18:45:00

Q3 18:45:00 - 19:07:30

Q4 19:07:30 - 19:30:00

Q2/1 19:30:00 - 19:52:30 (True Session Open)

Q2/2 19:52:30 - 20:15:00

Q2/3 20:15:00 - 20:37:30

Q2/4 20:37:30 - 21:00:00

Q3/1 21:00:00 - 21:23:30

etc. 21:23:30 - 21:45:00

London Session

00:00:00 - 00:22:30 (True Daily Open)

00:22:30 - 00:45:00

00:45:00 - 01:07:30

01:07:30 - 01:30:00

01:30:00 - 01:52:30 (True Session Open)

01:52:30 - 02:15:00

02:15:00 - 02:37:30

02:37:30 - 03:00:00

03:00:00 - 03:22:30

03:22:30 - 03:45:00

03:45:00 - 04:07:30

04:07:30 - 04:30:00

04:30:00 - 04:52:30

04:52:30 - 05:15:00

05:15:00 - 05:37:30

05:37:30 - 06:00:00

New York AM Session

06:00:00 - 06:22:30

06:22:30 - 06:45:00

06:45:00 - 07:07:30

07:07:30 - 07:30:00

07:30:00 - 07:52:30 (True Session Open)

07:52:30 - 08:15:00

08:15:00 - 08:37:30

08:37:30 - 09:00:00

09:00:00 - 09:22:30

09:22:30 - 09:45:00

09:45:00 - 10:07:30

10:07:30 - 10:30:00

10:30:00 - 10:52:30

10:52:30 - 11:15:00

11:15:00 - 11:37:30

11:37:30 - 12:00:00

New York PM Session

12:00:00 - 12:22:30

12:22:30 - 12:45:00

12:45:00 - 13:07:30

13:07:30 - 13:30:00

13:30:00 - 13:52:30 (True Session Open)

13:52:30 - 14:15:00

14:15:00 - 14:37:30

14:37:30 - 15:00:00

15:00:00 - 15:22:30

15:22:30 - 15:45:00

15:45:00 - 15:37:30

15:37:30 - 16:00:00

16:00:00 - 16:22:30

16:22:30 - 16:45:00

16:45:00 - 17:07:30

17:07:30 - 18:00:00

S&P 500 E-mini Futures (30 second candles) — 22.5 Minute Cycle.

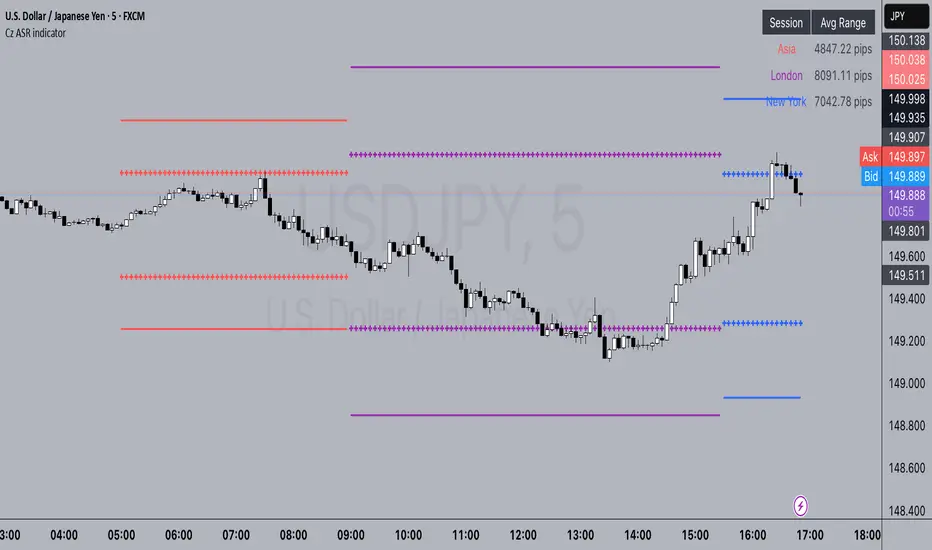

Cz ASR indicatorAverage session range indicator built by me. Great tool to gauge volatility and intraday reversal zones. Great for FX as there is an included table that shows range in pips; however, this can be applied across all assets as a volatility measure.

How it works:

The script measures the range of sessions, including Asia, London, and New York. The lookback period could be adjusted so you can find what length works best and is most accurate. This is then averaged out to provide the ASR. This provides us with an upper and lower bound of which the price could potentially fluctuate in based on the past session ranges. I have also added the 50% ASR, which is also a super useful metric for reversals or continuations.

There is also a configurable UTC so that you can adjust the indicator so it can accurately measure the range within certain sessions.

Note - different session start and stop times vary from market to market. I have set the code to the standard forex market opens however, if you wish to change the time ,you are able to do so by editing the variables in the script

Enjoy :)

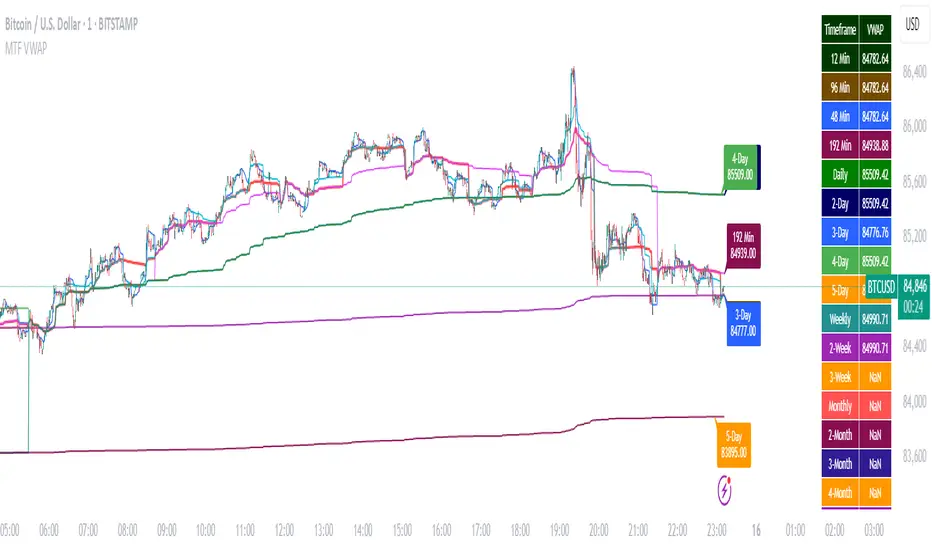

Multi-Timeframe VWAP DashboardMulti-Timeframe VWAP Dashboard with Advanced Customization**

Unlock the power of **Volume-Weighted Average Price (VWAP)** across multiple timeframes with this highly customizable and feature-rich Pine Script. Designed for traders who demand precision and flexibility, this script provides a **comprehensive VWAP dashboard** that adapts to your trading style and strategy. Whether you're a day trader, swing trader, or long-term investor, this tool offers unparalleled insights into market trends and price levels.

---

### **Key Features:**

1. **Multi-Timeframe VWAP Calculation:**

- Calculate VWAP across **12-minute, 48-minute, 96-minute, 192-minute, daily, weekly, monthly, and even yearly timeframes**.

- Supports **custom timeframes** for tailored analysis.

2. **Price Source Selection:**

- Choose from multiple price sources for VWAP calculation, including **Open, High, Low, Close, HL2, HLC3, HLCC4, and All**.

- Optimize VWAP for **uptrends and downtrends** by selecting the most relevant price source.

3. **Customizable Labels:**

- Add **dynamic labels** to each VWAP line for quick reference.

- Customize label **colors, sizes, and offsets** to suit your chart setup.

- Display **price values** and **session types** (e.g., "12 Min", "Daily", "Weekly") directly on the chart.

4. **Advanced Session Detection:**

- Automatically detect new sessions for **intraday, daily, weekly, monthly, and yearly timeframes**.

- Ensures accurate VWAP calculations for each session.

5. **Plot Visibility Control:**

- Toggle the visibility of individual VWAP plots to **reduce clutter** and focus on the most relevant timeframes.

- Includes options for **short-term, medium-term, and long-term VWAPs**.

6. **Comprehensive Timeframe Coverage:**

- From **12-minute intervals** to **12-month intervals**, this script covers all major timeframes.

- Perfect for traders who analyze markets across multiple horizons.

7. **User-Friendly Inputs:**

- Intuitive input options for **timeframes, colors, labels, and offsets**.

- Easily customize the script to match your trading preferences.

8. **Dynamic Label Positioning:**

- Labels adjust automatically based on price movements and session changes.

- Choose from **multiple offset options** to position labels precisely.

9. **Miscellaneous Customization:**

- Adjust **text color, label size, and price display settings**.

- Enable or disable **price values** and **session type labels** for a cleaner chart.

---

### **Why Use This Script?**

- **Versatility:** Suitable for all trading styles, including scalping, day trading, swing trading, and long-term investing.

- **Precision:** Accurate VWAP calculations across multiple timeframes ensure you never miss key price levels.

- **Customization:** Tailor the script to your specific needs with a wide range of input options.

- **Clarity:** Dynamic labels and customizable plots make it easy to interpret market trends at a glance.

---

### **How It Works:**

1. **Select Your Price Source:**

- Choose the price source (e.g., Open, Close, HL2) for VWAP calculation based on your trading strategy.

2. **Choose Timeframes:**

- Define the timeframes for VWAP calculation, from intraday to yearly intervals.

3. **Customize Labels and Plots:**

- Enable or disable labels and plots for each timeframe.

- Adjust colors, sizes, and offsets to match your chart setup.

4. **Analyze Market Trends:**

- Use the VWAP lines and labels to identify **support/resistance levels**, **trend direction**, and **potential reversal points**.

5. **Adapt to Market Conditions:**

- Switch between timeframes and price sources to adapt to changing market conditions.

---

### **Ideal For:**

- **Day Traders:** Use short-term VWAPs (e.g., 12-minute, 48-minute) to identify intraday trends and key levels.

- **Swing Traders:** Leverage medium-term VWAPs (e.g., 96-minute, daily) to spot swing opportunities.

- **Long-Term Investors:** Analyze long-term VWAPs (e.g., weekly, monthly) to gauge overall market direction.

---

### **How to Get Started:**

1. Add the script to your TradingView chart.

2. Customize the inputs to match your trading preferences.

3. Analyze the VWAP lines and labels to make informed trading decisions.

---

### **Pro Tip:**

Combine this script with other technical indicators (e.g., moving averages, RSI) for a **holistic view** of the market. Use the VWAP lines as dynamic support/resistance levels to enhance your entry and exit strategies.

This script is a must-have tool for traders who value precision, flexibility, and clarity. Share it with your audience to help them elevate their trading game. Whether they're beginners or seasoned professionals, this **Multi-Timeframe VWAP Dashboard** will become an essential part of their toolkit.

Opening Range, Initial Balance, Opening Price, Pre-market Levels### Description of the Indicator: **Opening Range, Initial Balance, Opening Price, Pre-market Levels**

This custom TradingView indicator provides a comprehensive view of key price levels for intraday trading, specifically designed to track important levels from the Opening Range (OR), Initial Balance (IB), Opening Price (OP), and Pre-market session (PM). These levels are essential for traders to gauge potential market movements and identify critical areas of support and resistance.

#### **Features:**

1. **Opening Range (OR):**

- This is the high and low of the first 30 minutes of the regular market session (09:30 - 10:00 EST).

- The OR high and low act as significant levels that may influence price movement for the rest of the day.

- The mid-level of the Opening Range (OR Mid) is also plotted to give a more detailed view of potential price action.

2. **Initial Balance (IB):**

- The Initial Balance is the range created during the first hour of market activity (09:30 - 10:30 EST).

- This range often sets the tone for the market's direction. The IB high and low, along with the IB midline, are plotted for quick reference.

3. **Opening Price (OP):**

- The opening price of the market is marked as a circle and labeled "OP."

- This level provides context for market sentiment when compared to the high and low levels.

4. **Pre-market Levels (PM):**

- The pre-market session (04:00 - 09:30 EST) has its own important levels that are calculated for the high, low, and mid range (PM High, PM Low, and PM Mid).

- These levels are plotted and are useful for traders to understand where the market stood before the regular session opened.

#### **Customization Options:**

- **Exchange Timezone:** You can choose whether to display the times in the exchange's local timezone or in your own preferred timezone.

- **Mid Levels Display:** You can toggle whether the mid levels for each range (OR, IB, PM) should be shown on the chart.

- **Level Color Change:** The colors of the plotted levels (high, low, mid) change based on whether the price is above or below the respective level, making it easy to visualize potential support and resistance.

- **Label Positions:** The position of the labels (OR, IB, OP, PM) on the chart can be customized to avoid overlap with other data points.

#### **Key Use Cases:**

- **Intraday Trend Analysis:** Use the OR and IB to identify key levels for the day, providing insights into the possible trend or range for the day.

- **Pre-market Insights:** The PM levels are crucial for understanding where the market stood during the pre-market hours and can be used as reference points during the regular session.

- **Potential Support and Resistance:** The high and low levels of the OR, IB, and PM sessions can act as potential support or resistance, which are useful for setting stop-loss and take-profit levels.

#### **How to Use:**

- Pay attention to the levels provided for OR, IB, and PM as potential entry and exit points.

- Watch for breakouts or reversals around these levels, especially when combined with other technical indicators or price action patterns.

- The mid levels offer an additional reference to assess price direction or identify possible areas of consolidation.

This indicator is perfect for day traders who rely on key intraday levels and pre-market activity to make informed trading decisions. It helps to streamline the process of identifying potential breakouts, reversals, and ranges in the market.

Fib Speed Resistance Fan"Fib Speed Resistance Fan," automatically draws Fibonacci Speed Resistance Fan lines based on the first and third candles of the trading session. Here’s a breakdown of its functionality:

Functionality

Session Start Time Identification

The script identifies the first candle at 9:15 AM using timestamp(), which ensures it captures the market's opening candle.

Candle Indexing

It determines the index of the first candle (firstCandleIndex) using ta.barssince(time >= sessionStart).

The third candle is found by adding two bars to the first candle's index (thirdCandleIndex = firstCandleIndex + 2).

Ensuring Single Execution

A boolean flag hasDrawn ensures that the lines are drawn only once and do not update on future candles.

Validating Data

It checks if the firstCandleIndex and thirdCandleIndex are valid (validSession).

If conditions are met, it extracts the highs and lows of the first and third candles.

Fibonacci Calculation

The script calculates a 0.75 level price between the first candle high/low and third candle low/high.

This level helps in drawing intermediate Fibonacci fan lines.

Drawing the Fibonacci Speed Resistance Fan

If conditions are valid and hasDrawn is false, the script draws:

Main fan lines from:

First candle high → Third candle low (Blue line)

First candle low → Third candle high (Blue line)