timer/tr/atr [keypoems]Session and Instant Volatility Ticker

What it actually does:

- Session ATR – Reports the historical (e.g. “0200-0600”) average true range of the past x sessions, reports the +1Stdev value.

- Real-time ATR feed – streams the current ATR value every tick.

- Ticker line – Sess. ATR +1Stdev | Current ATR | Previous TR | 🕒 Time-left-in-bar |

Think of it as a volatility check: a single glance tells you if the average candle size is compatible with your usual stop or not.

Open Source.

"session" için komut dosyalarını ara

ORB 15m + MAs (v4.1)Session ORB Live Pro — Pre-Market Boxes & MA Suite (v4.1)

What it is

A precision Opening Range Breakout (ORB) tool that anchors every session to one specific 15-minute candle—then projects that same high/low onto lower timeframes so your 1m/5m levels always match the source 15m bar. Perfect for scalpers who want session structure without drift.

What it draws

Asia, Pre-London, London, Pre-New York, New York session boxes.

On 15m: only the high/low of the first 15-minute bar of each window (optionally persists for extra bars).

On 5m: mirrors the same 15m range, visible up to 10 bars.

On 1m: mirrors the same 15m range, visible up to 15 bars.

Levels update live while the 15m candle is forming, then lock.

Fully editable windows (easy UX)

Change session times with TradingView’s native input.session fields using the familiar format HHMM-HHMM:1234567. You can tweak each window independently:

Asia

Pre-London

London

Pre-New York

New York

Multi-TF logic (no guesswork)

Designed to show only on 1m, 5m, 15m (by default).

15m = ground truth. Lower timeframes never “recalculate a different range”—they mirror the 15m bar for that session, exactly.

Alerts

Optional breakout alerts when price closes above/below the session range.

Clean visuals

Per-session color controls (box + lines). Boxes extend only for the configured number of bars per timeframe, keeping charts uncluttered.

Built-in MA suite

SMA 50 and RMA 200.

Three extra MAs (SMA/EMA/RMA/WMA/HMA) with selectable color, width, and style (line, stepline, circles).

Why traders like it

Consistency: Lower-TF ranges always match the 15m source bar.

Speed: You see structure immediately—no waiting for N bars.

Control: Edit session times directly; tune how long boxes stay on chart per TF.

Clarity: Minimal, purposeful plotting with alerts when it matters.

Quick start

Set your session times via the five input.session fields.

Choose how long boxes persist on 1m/5m/15m.

Enable alerts if you want instant breakout notifications.

(Optional) Configure the MA suite for trend/bias context.

Best for

Intraday traders and scalpers who rely on repeatable session behavior and demand exact cross-TF alignment of ORB levels.

Sessions High/LowIndicator lines to show the prior days NY high/low, overnight Asian high/low, and recent London high/low. Time frame variables are included as well as the option to change colors for both the high and low. Good luck.

Sessions Rainbow EST with overlapsThis script displays the trading zones with overlaps based on the color of the rainbow. It is used with a Point&Figure chart to show trends associated with trading periods and overlapping trading periods.

Sessions - London NY overlapOther scripts show London closing at 5pm GMT whereas i believe the forex market on London closes at 4pm GMT. So i have adjusted an already published script to reflect this

Session SFPThis script is a powerful, multi-timeframe tool designed to identify high-probability Swing Failure Patterns (SFPs) at key historical levels.

Instead of looking for traditional "pivots" (like a 3-bar swing), this indicator finds the actual high and low of a previous higher-timeframe (HTF) bar (e.g., the previous weekly high/low) and waits for a lower-timeframe (LTF) candle to sweep that level and fail.

This allows you to spot liquidity sweeps and potential reversals at significant, structural price points.

How It Works

The indicator's logic is based on a simple, two-timeframe process:

Level Detection: First, it finds the high and low of the previous bar on your chosen "Level Timeframe" (e.g., W for Weekly, D for Daily). It plots these as small 'x' markers on your chart.

SFP Identification: Second, it watches price action on a lower "SFP Timeframe" (e.g., 240 for 4H). A potential SFP is identified when a candle's wick sweeps above a key high or below a key low.

Confirmation: The SFP is only confirmed after the SFP candle closes back below the high (for a bearish SFP) or above the low (for a bullish SFP). It then waits for a set number of "Confirmation Bars" to pass. If price does not close back over the level during this window, the signal is locked in, and a label is printed.

How to Use (Key Settings)

Level Timeframe (Most Important): This is the timeframe for the levels you want to trade. Set this to W to find SFPs of the previous weekly high/low. Set it to D to find SFPs of the previous daily high/low.

SFP Timeframe: This is the timeframe you want to use to find the SFP candle itself. This should be lower than your Level Timeframe (e.g., 240 or 60).

Level Lookback: This controls how many old levels the script will track. A value of 10 on a W Level Timeframe will track the highs and lows of the last 10 weeks.

Confirmation Bars: This is your "patience" filter. It's the number of SFP Timeframe bars that must close without reclaiming the level after the SFP. A value of 0 will confirm the SFP immediately on the candle's close.

Enable Wick % Filter: A quality filter. If checked, this ensures the SFP candle's rejection wick is a significant percentage of the candle's total range.

Chart Visuals

'x' Markers: These are the historical highs and lows from your "Level Timeframe". You can turn these on or off in the settings.

SFP Label: When an SFP is fully confirmed, a label (Bearish SFP or Bullish SFP) will appear, detailing the level that was swept and the timeframes used.

SFP Line: A solid horizontal line is drawn from the 'x' marker to the SFP candle to highlight the sweep.

Colored Boxes (Optional): If you are viewing a chart timeframe lower than your "SFP Timeframe", you can enable background boxes to highlight the exact SFP candle and its confirmation bars.

SeparatorsSession - H1 and below Time Frame

Day - H4 and below Time Frame

Month - D Time Frame

Quarter - W Time Frame

Session Key Levels Lines (with Labels)This is an extension of the previous indicator, it just plots all the information you need automatically for you so you dont have to lift a finger. hope it helps :)

Session Moving AveragesAdds EMAs and SMAs to chart using 8am-8pm EST values. Completely configurable in settings.

Some platforms allow users to configure what time frame they would like to view market data. One popular selection is 8am-8pm EST as 8am is when institutional orders go through. An argument can be made that price action before 8am EST is not valid yet moving averages will use that data.

This matters less for shorter moving averages such as a 9 or 20 ema, but it dramatically changes the 200 or the 50 sma for example.

This script allows you to ignore that pre-market data (or any data you choose to configure in the settings) and select up to 3 moving averages (either Exponential or Simple) for a set time.

By default the moving averages include the 9-ema (gray), 20-ema (green), and 200-sma (purple) and is set to 8am-8pm EST

This is configurable in the settings including the time frame you would like the moving averages to start using market data.

By default the script will use your charts timeframe. You are able to use multi-time frames with this script just scroll down to "timeframe", then click "chart" in settings... this will then allow you to select a timeframe.

A popular choice is 5-minute value of 8am-8pm EST moving averages. This means regardless of the time frame you are on (sub 1-minute, 1-minute, etc.) the script will display 5-minute data.

Final note: In settings you are able to turn on/off shapes (the gray lines at the bottom) which shows when the data is being used. This can be helpful on certain tickers that trade continuously such as /ES or /NQ.

Session Time RangesHave you ever wondered if you are trading at the right time of the day or feel like all the good trades happen when you are sleeping? Well now you can check your theory :)

This Script allows you to highlight a time range on your chart over a 24hour time period. For example 3AM to 6AM

The script has two time variables, set your start time and end time based on a 24 hour clock and set the time zone offset variable to match your charts time zone. For example New York -4 (for utc just enter 0 for no offset )

This is a quick script I put together so hopefully it is error free enjoy :)

Session P4L MTFCorrected indicator for better support of smaller time frames. version 3.0 with better interface. thank you

Session P EdgesThis is an attempt to chart the primary balance ranges, however,

I have been having difficulty getting the lows to work in the graph, any assistance would be welcome

VX-Time Quadrant Overlay (Quarterly Cycles) by Ikaru-s-The Time Quadrant Overlay is a purely time-based visualization tool designed to structure market time into repeating quarterly cycles across multiple timeframes.

It does not generate trade signals, entries, or bias.

Its sole purpose is to provide time context, so price action can be interpreted within a clear cyclical framework.

What this indicator does

The indicator divides time into four repeating quarters (Q1–Q4) and displays them simultaneously across different time horizons, such as:

Weekly

Daily (6-hour quarters)

90-minute cycles

Micro cycles (within 90-minute structure)

Each row represents a different time cycle, allowing traders to see time alignment, transitions, and overlaps at a glance.

Quarter Structure

Each cycle follows the same repeating sequence:

Q1 – Early phase

Q2 – Expansion / “True Open” phase

Q3 – Continuation

Q4 – Late phase / Transition

The quarters are visualized using color-coded boxes, making it easy to see:

where the market currently is in time

when a new quarter begins

when multiple cycles align or diverge

Quarter Start Marker

An optional Quarter Start Marker (vertical dashed line) can be enabled to highlight the start of a selected quarter (default: Q2).

This is intended as a time reference, not a signal:

useful for planning

useful for contextualizing reactions to levels

useful for session and cycle awareness

How to use it (practical)

This tool is best used to:

provide time structure to existing analysis

plan around upcoming time transitions

contextualize reactions to levels or areas

understand where price is acting within a cycle

It works well alongside:

discretionary price action

session-based trading

futures and index markets

any methodology that respects time as a variable

Customization

The indicator is fully customizable:

Enable / disable individual cycles

Adjust box transparency and history depth

Toggle labels and pane labels

Enable / disable quarter start markers

Select which quarter to highlight

This allows the tool to remain clean on higher timeframes and detailed on lower ones.

Important Notes

This is a visual framework, not a strategy.

No claims of predictive power are made.

Time structure does not replace risk management or execution logic.

The indicator is designed to adapt across markets, but interpretation remains discretionary.

Final Thoughts

Time is often treated as secondary to price.

This tool exists to make time visible, structured, and easy to work with — nothing more, nothing less.

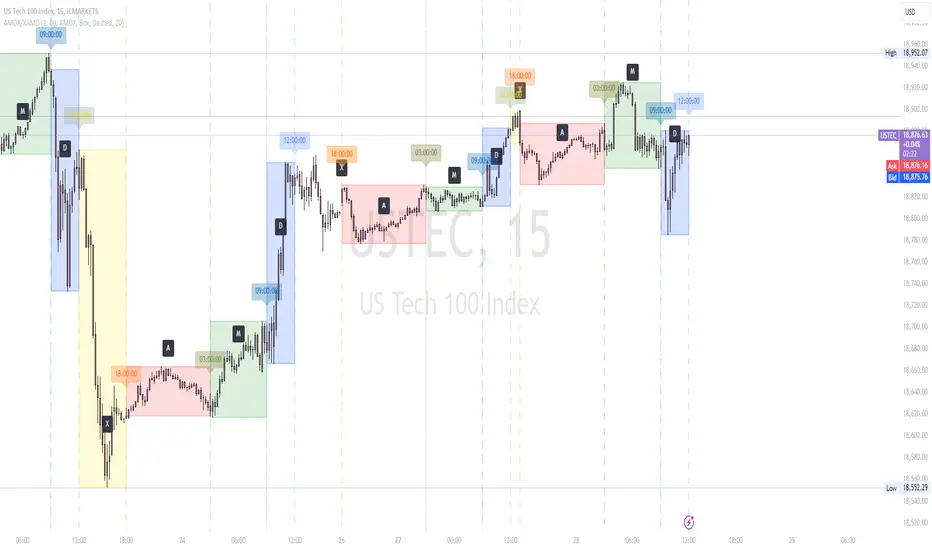

AMDX/XAMD indicatorThe AMDX/XAMD indicator is designed to highlight specific trading sessions on the chart using distinct colors and optional vertical lines. Users can choose between two session types, AMDX or XAMD, and customize the visual appearance of the sessions. This tool is particularly useful for traders who want to analyze market behavior during different trading periods.

Meaning of AMDX:

A: Accumulation

M: Manipulation

D: Distribution

X: Continuation Or Reversal

Features:

Session Highlighting:

AMDX Sessions: Split into four segments - A, M, D, X.

XAMD Sessions: Split into four segments - X, A, M, D.

Customizable Colors:

Choose individual colors for each session (A, M, D, X).

Adjust the transparency of the session boxes for better visual integration with the chart.

Drawing Styles:

Box Style: Draws colored boxes around the session ranges.

Line Style: Draws vertical lines at session start and end times.

Vertical Lines:

Option to enable or disable vertical lines at session boundaries.

Customizable line style: Solid, Dotted, or Dashed.

Session Labels:

Automatically labels each session for easy identification.

Customization Options:

Session Type: Select between AMDX and XAMD session types.

Colors: Set custom colors for each session and vertical lines.

Border Width: Adjust the width of the session box borders.

Transparency: Control the transparency level of the session boxes.

Drawing Style: Choose between Box and Line styles for session representation.

Vertical Lines: Enable or disable vertical lines and select the line style.

How It Works:

The indicator calculates the start and end times for each session based on the selected session type (AMDX or XAMD). It then draws either boxes or lines to highlight these sessions on the chart. The indicator also includes options to draw vertical lines at the session boundaries and labels each session with a corresponding letter (A, M, D, X).

Use Cases:

Market Session Analysis: Easily identify and analyze market behavior during different trading sessions.

Intraday Trading: Helps intraday traders to focus on specific time segments of the trading day.

Visual Segmentation: Provides a clear visual segmentation of the trading day, aiding in better decision-making.

Times for AMDX/XAMD session:

A Session: 18:00 (previous day) to 03:00 (current day)

M Session: 03:00 to 09:00

D Session: 09:00 to 12:00

X Session: 12:00 to 18:00

Time for the XAMD session :

X Session: 18:00 (previous day) to 00:00 (current day)

A Session: 00:00 to 09:00

M Session: 09:00 to 12:00

D Session: 12:00 to 18:00

Time Zone PSenseiTitle: Time Zone PS Indicator

Author: Orlando Depablos

Description:

The Time Zone PS Indicator is a tool designed to help traders visualize different trading sessions on their charts. It allows users to specify three different trading sessions: the start of the day, the London session, and the New York (NYC) session. Each session is represented by a distinct color-coded background on the chart.

Features:

Customizable Sessions: Traders can define the start time and end time for each trading session according to their preference. This flexibility enables users to tailor the indicator to their specific trading strategies session time zones.

Session Display Control: Users have the option to choose whether they want to display each trading session on the chart. This feature allows for a clutter-free charting experience, where traders can focus on the sessions relevant to their analysis.

Visual Clarity: The indicator uses distinct colors for each trading session, making it easy for traders to differentiate between different time zones. This visual clarity aids in quickly identifying key trading periods throughout the day.

How to Use:

Setting Up Sessions: Use the input options to define the start and end times for the start of the day, the London session, and the NYC session. Adjust these values based on your trading preferences and time zone.

Display Preferences: Toggle the display options to choose which trading sessions you want to visualize on the chart. This allows for a customizable charting experience tailored to your specific needs.

Interpreting the Chart: Once configured, the indicator will display color-coded backgrounds on the chart corresponding to the defined trading sessions. Interpret these visual cues to identify key trading periods and plan your trading strategies accordingly.

Originality:

The Time Zone PS Indicator adds value to the TradingView community by providing traders with a customizable tool to visualize different trading sessions. While similar indicators exist, this script offers flexibility and ease of use, enhancing the charting experience for traders across various time zones.

Use Cases:

Session-Based Analysis: Traders can use the indicator to analyze price action within specific trading sessions, such as the London or NYC session, to identify potential trading opportunities.

Time Zone Adjustment: Traders operating in different time zones can adjust the indicator settings to align with their local trading hours, ensuring accurate visualization of relevant trading sessions.

Strategy Development: The indicator can aid in the development of trading strategies that capitalize on price movements during specific trading sessions, helping traders optimize their trading performance.

Chart Visualization:

The indicator provides a clear and concise visualization of different trading sessions on the chart. Each session is represented by a color-coded background, allowing traders to quickly identify key trading periods and make informed trading decisions.

Volume Profile [Makit0]VOLUME PROFILE INDICATOR v0.5 beta

Volume Profile is suitable for day and swing trading on stock and futures markets, is a volume based indicator that gives you 6 key values for each session: POC, VAH, VAL, profile HIGH, LOW and MID levels. This project was born on the idea of plotting the RTH sessions Value Areas for /ES in an automated way, but you can select between 3 different sessions: RTH, GLOBEX and FULL sessions.

Some basic concepts:

- Volume Profile calculates the total volume for the session at each price level and give us market generated information about what price and range of prices are the most traded (where the value is)

- Value Area (VA): range of prices where 70% of the session volume is traded

- Value Area High (VAH): highest price within VA

- Value Area Low (VAL): lowest price within VA

- Point of Control (POC): the most traded price of the session (with the most volume)

- Session HIGH, LOW and MID levels are also important

There are a huge amount of things to know of Market Profile and Auction Theory like types of days, types of openings, relationships between value areas and openings... for those interested Jim Dalton's work is the way to come

I'm in my 2nd trading year and my goal for this year is learning to daytrade the futures markets thru the lens of Market Profile

For info on Volume Profile: TV Volume Profile wiki page at www.tradingview.com

For info on Market Profile and Market Auction Theory: Jim Dalton's book Mind over markets (this is a MUST)

BE AWARE: this indicator is based on the current chart's time interval and it only plots on 1, 2, 3, 5, 10, 15 and 30 minutes charts.

This is the correlation table TV uses in the Volume Profile Session Volume indicator (from the wiki above)

Chart Indicator

1 - 5 1

6 - 15 5

16 - 30 10

31 - 60 15

61 - 120 30

121 - 1D 60

This indicator doesn't follow that correlation, it doesn't get the volume data from a lower timeframe, it gets the data from the current chart resolution.

FEATURES

- 6 key values for each session: POC (solid yellow), VAH (solid red), VAL (solid green), profile HIGH (dashed silver), LOW (dashed silver) and MID (dotted silver) levels

- 3 sessions to choose for: RTH, GLOBEX and FULL

- select the numbers of sessions to plot by adding 12 hours periods back in time

- show/hide POC

- show/hide VAH & VAL

- show/hide session HIGH, LOW & MID levels

- highlight the periods of time out of the session (silver)

- extend the plotted lines all the way to the right, be careful this can turn the chart unreadable if there are a lot of sessions and lines plotted

SETTINGS

- Session: select between RTH (8:30 to 15:15 CT), GLOBEX (17:00 to 8:30 CT) and FULL (17:00 to 15:15 CT) sessions. RTH by default

- Last 12 hour periods to show: select the deph of the study by adding periods, for example, 60 periods are 30 natural days and around 22 trading days. 1 period by default

- Show POC (Point of Control): show/hide POC line. true by default

- Show VA (Value Area High & Low): show/hide VAH & VAL lines. true by default

- Show Range (Session High, Low & Mid): show/hide session HIGH, LOW & MID lines. true by default

- Highlight out of session: show/hide a silver shadow over the non session periods. true by default

- Extension: Extend all the plotted lines to the right. false by default

HOW TO SETUP

BE AWARE THIS INDICATOR PLOTS ONLY IN THE FOLLOWING CHART RESOLUTIONS: 1, 2, 3, 5, 10, 15 AND 30 MINUTES CHARTS. YOU MUST SELECT ONE OF THIS RESOLUTIONS TO THE INDICATOR BE ABLE TO PLOT

- By default this indicator plots all the levels for the last RTH session within the last 12 hours, if there is no plot try to adjust the 12 hours periods until the seesion and the periods match

- For Globex/Full sessions just select what you want from the dropdown menu and adjust the periods to plot the values

- Show or hide the levels you want with the 3 groups: POC line, VA lines and Session Range lines

- The highlight and extension options are for a better visibility of the levels as POC or VAH/VAL

THANKS TO

@watsonexchange for all the help, ideas and insights on this and the last two indicators (Market Delta & Market Internals) I'm working on my way to a 'clean chart' but for me it's not an easy path

@PineCoders for all the amazing stuff they do and all the help and tools they provide, in special the Script-Stopwatch at that was key in lowering this indicator's execution time

All the TV and Pine community, open source and shared knowledge are indeed the best way to help each other

IF YOU REALLY LIKE THIS WORK, please send me a comment or a private message and TELL ME WHAT you trade, HOW you trade it and your FAVOURITE SETUP for pulling out money from the market in a consistent basis, I'm learning to trade (this is my 2nd year) and I need all the help I can get

GOOD LUCK AND HAPPY TRADING

ICT Opening Range Projections (tristanlee85)ICT Opening Range Projections

This indicator visualizes key price levels based on ICT's (Inner Circle Trader) "Opening Range" concept. This 30-minute time interval establishes price levels that the algorithm will refer to throughout the session. The indicator displays these levels, including standard deviation projections, internal subdivisions (quadrants), and the opening price.

🟪 What It Does

The Opening Range is a crucial 30-minute window where market algorithms establish significant price levels. ICT theory suggests this range forms the basis for daily price movement.

This script helps you:

Mark the high, low, and opening price of each session.

Divide the range into quadrants (premium, discount, and midpoint/Consequent Encroachment).

Project potential price targets beyond the range using configurable standard deviation multiples .

🟪 How to Use It

This tool aids in time-based technical analysis rooted in ICT's Opening Range model, helping you observe price interaction with algorithmic levels.

Example uses include:

Identifying early structural boundaries.

Observing price behavior within premium/discount zones.

Visualizing initial displacement from the range to anticipate future moves.

Comparing price reactions at projected standard deviation levels.

Aligning price action with significant times like London or NY Open.

Note: This indicator provides a visual framework; it does not offer trade signals or interpretations.

🟪 Key Information

Time Zone: New York time (ET) is required on your chart.

Sessions: Supports multiple sessions, including NY midnight, NY AM, NY PM, and three custom timeframes.

Time Interval: Supports multi-timeframe up to 15 minutes. Best used on a 1-minute chart for accuracy.

🟪 Session Options

The Opening Range interval is configurable for up to 6 sessions:

Pre-defined ICT Sessions:

NY Midnight: 12:00 AM – 12:30 AM ET

NY AM: 9:30 AM – 10:00 AM ET

NY PM: 1:30 PM – 2:00 PM ET

Custom Sessions:

Three user-defined start/end time pairs.

This example shows a custom session from 03:30 - 04:00:

🟪 Understanding the Levels

The Opening Price is the open of the first 1-minute candle within the chosen session.

At session close, the Opening Range is calculated using its High and Low . An optional swing-based mode uses swing highs/lows for range boundaries.

The range is divided into quadrants by its midpoint ( Consequent Encroachment or CE):

Upper Quadrant: CE to high (premium).

Lower Quadrant: Low to CE (discount).

These subdivisions help visualize internal range dynamics, where price often reacts during algorithmic delivery.

🟪 Working with Ranges

By default, the range is determined by the highest high and lowest low of the 30-minute session:

A range can also be determined by the highest/lowest swing points:

Quadrants outline the premium and discount of a range that price will reference:

Small ranges still follow the same algorithmic logic, but may be deemed insignificant for one's trading. These can be filtered in the settings by specifying a minimum ticks limit. In this example, the range is 42 ticks (10.5 points) but the indicator is configured for 80 ticks (20 points). We can select which levels will plot if the range is below the limit. Here, only the 00:00 opening price is plotted:

You may opt to include the range high/low, quadrants, and projections as well. This will plot a red (configurable) range bracket to indicate it is below the limit while plotting the levels:

🟪 Price Projections

Projections extend beyond the Opening Range using standard deviations, framing the market beyond the initial session and identifying potential targets. You define the standard deviation multiples (e.g., 1.0, 1.5, 2.0).

Both positive and negative extensions are displayed, symmetrically projected from the range's high and low.

The Dynamic Levels option plots only the next projection level once price crosses the previous extreme. For example, only the 0.5 STDEV level plots until price reaches it, then the 1.0 level appears, and so on. This continues up to your defined maximum projections, or indefinitely if standard deviations are set to 0.

This example shows dynamic levels for a total of 6 sessions, only 1 of which meet a configured minimum limit of 50 ticks:

Small ranges followed by significant displacement are impacted the most with the number of levels plotted. You may hide projections when configuring the minimum ticks.

A fixed standard deviation will plot levels in both directions, regardless of the price range. Here, we plot up to 3.0 which hiding projections for small ranges:

🟪 Legal Disclaimer

This indicator is provided for informational and educational purposes only. It is not financial advice, and should not be construed as a recommendation to buy or sell any financial instrument. Trading involves substantial risk, and you could lose a significant amount of money. Past performance is not indicative of future results. Always consult with a qualified financial professional before making any trading or investment decisions. The creators and distributors of this indicator assume no responsibility for your trading outcomes.

Vertical Time LinesVertical Time Lines is an indicator that draws vertical lines at specific times of each day on the price chart.

⚙️ Main Features

Up to 5 independent time lines

Precise hour and minute editing (HH:MM)

Individual enable/disable option per line

Customizable line color and style

Works on any asset and any timeframe

📝 Note

Due to Pine Script limitations, the lines are drawn using UTC time, not the time zone configured on the chart.

Lines are generated only when a candle exists exactly at the configured minute. If candles for the specified hours and minutes are not visible on the chart, the lines will not be displayed.