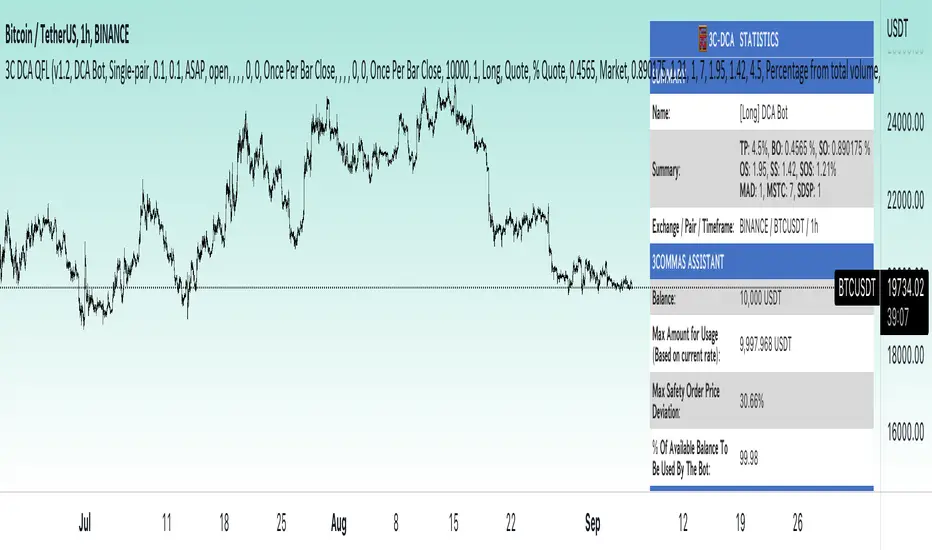

3Commas dollar cost averaging (DCA) QFL IndicatorAs investors, we often face the dilemma of willing high stock prices when we sell, but not when we buy. There are times when this dilemma causes investors to wait for a dip in prices, thereby potentially missing out on a continual rise. This is how investors get lured away from the markets and become tangled in the slippery slope of market timing, which is not advisable to a long-term investment strategy.

Skyrex developed a complex indicator based on dollar-cost averaging in Quick Fingers Luc's interpretation. It is a combinations of strategies which allows to systematically accumulate assets by investing scaled amounts of money at defined market cycle global support levels. Dollar-cost averaging can reduce the overall impact of price volatility and lower the average cost per asset thus even during market slumps only a small bounce is required to reach take profit.

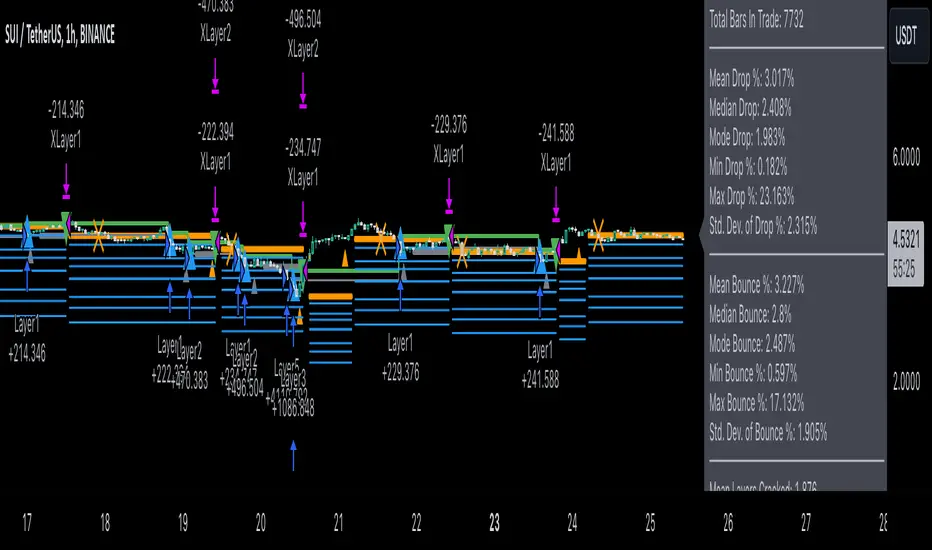

The indicator script monitors a chart price action and identifies bases as they form. When bases are reached the script provides entry alerts. During price action development an asset value can go lower and in this way the script will perform safety entries alerts at each subsequent accumulation levels. When weighted average entry price reaches target profit the script will perform a take profit action alert.

Bases are identified as pivot lows in a fractal pattern and validated by an adjustable decrease/rise percentage to ensure significancy of identified bases. To qualify a pivot low, the indicator will perform the following validation:

Validate the price rate of change on drops and bounces is above a given threshold amount.

Validate the volume at the low pivot point is above the volume moving average (using a given length).

Validate the volume amount is a given factor of magnitude above is above the volume moving average.

Validate the potential new base is not too close to the previous range by using a given price percent difference threshold amount.

A fractal pattern is a recurring pattern on a price chart that can predict reversals among larger, more chaotic price movements. These basic fractals are composed of five or more bars. The rules for identifying fractals are as follows:

A bearish turning point occurs when there is a pattern with the highest high in the middle and two lower highs on each side.

A bullish turning point occurs when there is a pattern with the lowest low in the middle and two higher lows on each side.

Basic dollar-cost averaging approach is enhances by implementation of adjustable accumulation levels in order to provide opportunity of setting them at defined global support levels and Martingale volume coefficient to increase averaging effect. According to Quick Fingers Luc's principles trading principles we added volume validation of a base because it allows to confirm that the market is resistant to further price decrease.

The indicator supports traditional and cryptocurrency spot, futures , options and marginal trading exchanges. It works accurately with BTC , USD, USDT, ETH and BNB quote currencies. Best to use with 1H timeframe charts and limit orders. The indicator can be and should be configured for each particular asset according to its global support and resistance levels and price action cycles. You can modify levels and risk management settings to receive better performance

The difference between core script and this interpretation is that this strategy is specially designed for 3Commas bots

How to use?

1. Apply indicator to a trading pair your are interested in using 1H timeframe chart

2. Configure the indicator: change layer values, order size multiple and take profit/stop loss values according to current market cycle stage

3. Set up a TradingView custom alert using the indicator settings to trigger on a condition you are interested in

4. The indicator will send alerts when to enter and when to exit positions which can be applied to your portfolio using external trading platforms

5. Update settings once market conditions are changed using backtests on a monthly period

"Cycle" için komut dosyalarını ara

3Commas Dollar cost averaging trading system (DCA)As investors, we often face the dilemma of willing high stock prices when we sell, but not when we buy. There are times when this dilemma causes investors to wait for a dip in prices, thereby potentially missing out on a continual rise. This is how investors get lured away from the markets and become tangled in the slippery slope of market timing, which is not advisable to a long-term investment strategy.

Skyrex developed a complex trading system based on dollar-cost averaging in Quick Fingers Luc's interpretation. It is a combinations of strategies which allows to systematically accumulate assets by investing scaled amounts of money at defined market cycle global support levels. Dollar-cost averaging can reduce the overall impact of price volatility and lower the average cost per asset thus even during market slumps only a small bounce is required to reach take profit.

The strategy script monitors a chart price action and identifies bases as they form. When bases are reached the script provides entry actions. During price action development an asset value can go lower and in this way the script will perform safety entries at each subsequent accumulation levels. When weighted average entry price reaches target profit the script will perform a take profit action.

Bases are identified as pivot lows in a fractal pattern and validated by an adjustable decrease/rise percentage to ensure significancy of identified bases. To qualify a pivot low, the indicator will perform the following validation:

Validate the price rate of change on drops and bounces is above a given threshold amount.

Validate the volume at the low pivot point is above the volume moving average (using a given length).

Validate the volume amount is a given factor of magnitude above is above the volume moving average.

Validate the potential new base is not too close to the previous range by using a given price percent difference threshold amount.

A fractal pattern is a recurring pattern on a price chart that can predict reversals among larger, more chaotic price movements.

These basic fractals are composed of five or more bars. The rules for identifying fractals are as follows:

A bearish turning point occurs when there is a pattern with the highest high in the middle and two lower highs on each side.

A bullish turning point occurs when there is a pattern with the lowest low in the middle and two higher lows on each side.

Basic dollar-cost averaging approach is enhances by implementation of adjustable accumulation levels in order to provide opportunity of setting them at defined global support levels and Martingale volume coefficient to increase averaging effect. According to Quick Fingers Luc's principles trading principles we added volume validation of a base because it allows to confirm that the market is resistant to further price decrease.

The strategy supports traditional and cryptocurrency spot, futures , options and marginal trading exchanges. It works accurately with BTC, USD, USDT, ETH and BNB quote currencies. Best to use with 1H timeframe charts and limit orders. The strategy can be and should be configured for each particular asset according to its global support and resistance levels and price action cycles. You can modify levels and risk management settings to receive better performance

The difference between core script and this interpretation is that this strategy is specially designed for 3Commas bots

How to use?

1. Apply strategy to a trading pair your are interested in using 1H timeframe chart

2. Configure the strategy: change layer values, order size multiple and take profit/stop loss values according to current market cycle stage

3. Set up a TradingView alert to trigger when strategy conditions are met

4. Strategy will send alerts when to enter and when to exit positions which can be applied to your portfolio using external trading platforms

5. Update settings once market conditions are changed using backtests on a monthly period

Dollar cost averaging (DCA) QFL IndicatorAs investors, we often face the dilemma of willing high stock prices when we sell, but not when we buy. There are times when this dilemma causes investors to wait for a dip in prices, thereby potentially missing out on a continual rise. This is how investors get lured away from the markets and become tangled in the slippery slope of market timing, which is not advisable to a long-term investment strategy.

Skyrex developed a complex indicator based on dollar-cost averaging in Quick Fingers Luc's interpretation. It is a combinations of strategies which allows to systematically accumulate assets by investing scaled amounts of money at defined market cycle global support levels. Dollar-cost averaging can reduce the overall impact of price volatility and lower the average cost per asset thus even during market slumps only a small bounce is required to reach take profit.

The indicator script monitors a chart price action and identifies bases as they form. When bases are reached the script provides entry alerts. During price action development an asset value can go lower and in this way the script will perform safety entries alerts at each subsequent accumulation levels. When weighted average entry price reaches target profit the script will perform a take profit action alert.

Bases are identified as pivot lows in a fractal pattern and validated by an adjustable decrease/rise percentage to ensure significancy of identified bases. To qualify a pivot low, the indicator will perform the following validation:

Validate the price rate of change on drops and bounces is above a given threshold amount.

Validate the volume at the low pivot point is above the volume moving average (using a given length).

Validate the volume amount is a given factor of magnitude above is above the volume moving average.

Validate the potential new base is not too close to the previous range by using a given price percent difference threshold amount.

A fractal pattern is a recurring pattern on a price chart that can predict reversals among larger, more chaotic price movements. These basic fractals are composed of five or more bars. The rules for identifying fractals are as follows:

A bearish turning point occurs when there is a pattern with the highest high in the middle and two lower highs on each side.

A bullish turning point occurs when there is a pattern with the lowest low in the middle and two higher lows on each side.

Basic dollar-cost averaging approach is enhances by implementation of adjustable accumulation levels in order to provide opportunity of setting them at defined global support levels and Martingale volume coefficient to increase averaging effect. According to Quick Fingers Luc's principles trading principles we added volume validation of a base because it allows to confirm that the market is resistant to further price decrease.

The indicator supports traditional and cryptocurrency spot, futures, options and marginal trading exchanges. It works accurately with BTC, USD, USDT, ETH and BNB quote currencies. Best to use with 1H timeframe charts and limit orders. The indicator can be and should be configured for each particular asset according to its global support and resistance levels and price action cycles. You can modify levels and risk management settings to receive better performance

Advantages of this indicator:

The indicator has custom alert settings for each strategy action

The indicator can be used with 3Commas, Cryptohopper, Alertatron or Zignaly bots

The indicator is sustainable to market slumps and can be used for long-term trading

The indicator provides a large number of entries which is good for diversification

Can be applied to any market and quote currency

Easy to configure user interface settings

How to use?

1. Apply indicator to a trading pair your are interested in using 1H timeframe chart

2. Configure the indicator: change layer values, order size multiple and take profit/stop loss values according to current market cycle stage

3. Set up a TradingView custom alert using the indicator settings to trigger on a condition you are interested in

4. The indicator will send alerts when to enter and when to exit positions which can be applied to your portfolio using external trading platforms

5. Update settings once market conditions are changed using backtests on a monthly period

Dollar cost averaging trading system (DCA)As investors, we often face the dilemma of willing high stock prices when we sell, but not when we buy. There are times when this dilemma causes investors to wait for a dip in prices, thereby potentially missing out on a continual rise. This is how investors get lured away from the markets and become tangled in the slippery slope of market timing, which is not advisable to a long-term investment strategy.

Skyrex developed a complex trading system based on dollar-cost averaging in Quick Fingers Luc's interpretation. It is a combinations of strategies which allows to systematically accumulate assets by investing scaled amounts of money at defined market cycle global support levels. Dollar-cost averaging can reduce the overall impact of price volatility and lower the average cost per asset thus even during market slumps only a small bounce is required to reach take profit.

The strategy script monitors a chart price action and identifies bases as they form. When bases are reached the script provides entry actions. During price action development an asset value can go lower and in this way the script will perform safety entries at each subsequent accumulation levels. When weighted average entry price reaches target profit the script will perform a take profit action.

Bases are identified as pivot lows in a fractal pattern and validated by an adjustable decrease/rise percentage to ensure significancy of identified bases. To qualify a pivot low, the indicator will perform the following validation:

Validate the price rate of change on drops and bounces is above a given threshold amount.

Validate the volume at the low pivot point is above the volume moving average (using a given length).

Validate the volume amount is a given factor of magnitude above is above the volume moving average.

Validate the potential new base is not too close to the previous range by using a given price percent difference threshold amount.

A fractal pattern is a recurring pattern on a price chart that can predict reversals among larger, more chaotic price movements.

These basic fractals are composed of five or more bars. The rules for identifying fractals are as follows:

A bearish turning point occurs when there is a pattern with the highest high in the middle and two lower highs on each side.

A bullish turning point occurs when there is a pattern with the lowest low in the middle and two higher lows on each side.

Basic dollar-cost averaging approach is enhances by implementation of adjustable accumulation levels in order to provide opportunity of setting them at defined global support levels and Martingale volume coefficient to increase averaging effect. According to Quick Fingers Luc's principles trading principles we added volume validation of a base because it allows to confirm that the market is resistant to further price decrease.

The strategy supports traditional and cryptocurrency spot, futures, options and marginal trading exchanges. It works accurately with BTC, USD, USDT, ETH and BNB quote currencies. Best to use with 1H timeframe charts and limit orders. The strategy can be and should be configured for each particular asset according to its global support and resistance levels and price action cycles. You can modify levels and risk management settings to receive better performance

Advantages of this script:

Strategy has high net profit of 255% at backtests

Backtests show high accuracy around 75%

Low Drawdowns of around 14% at backtests

Strategy is sustainable to market slumps and can be used for long-term trading

The strategy provides a large number of entries which is good for diversification

Can be applied to any market and quote currency

Easy to configure user interface settings

How to use?

1. Apply strategy to a trading pair your are interested in using 1H timeframe chart

2. Configure the strategy: change layer values, order size multiple and take profit/stop loss values according to current market cycle stage

3. Set up a TradingView alert to trigger when strategy conditions are met

4. Strategy will send alerts when to enter and when to exit positions which can be applied to your portfolio using external trading platforms

5. Update settings once market conditions are changed using backtests on a monthly period

BTC -50% Crash to Recovery ZoneGeneral Overview This is a macro-analysis tool designed to visualize the true duration of Bitcoin’s "Suffering & Recovery Cycles." Unlike standard oscillators that only signal oversold conditions, this script highlights the entire timeline required for the market to flush out leverage and return to All-Time Highs (ATH).

Operational Logic The algorithm tracks Bitcoin’s historical All-Time High (ATH).

The Trigger: It activates automatically when the price drops 50% below the last recorded ATH.

The "Recovery Zone": Once triggered, the chart background turns red (indicating a "Drawdown" state). This zone remains active persistently, even during intermediate relief rallies.

The Reset: The zone deactivates only when the price breaks above the previous ATH, marking the official start of a new Price Discovery phase.

How to Read It

Red Background: We are officially in a Bear Market or Recovery Phase. The asset is technically "underwater." For the long-term investor with a low time preference, this visually defines the accumulation window.

Red Horizontal Line: Indicates the "Target." This is the exact price level of the old ATH that Bitcoin must reclaim to close the bearish cycle.

No Background Color: We are in Price Discovery. The market is healthy and pushing for new highs.

The Financial Lesson This indicator visually demonstrates a fundamental market truth: "Price takes the elevator down, but takes the stairs up." It shows that after a halving of value (-50%), Bitcoin may take months or years to recover previous levels, helping investors filter out the noise of short-term pumps that fail to break the macro-bearish structure.

True Seasonal Pattern [tradeviZion]True Seasonal Pattern: Uncover Hidden Market Cycles

Markets have rhythms and patterns that repeat with surprising regularity. The True Seasonal Pattern indicator reveals these hidden cycles across different timeframes, helping you anticipate potential market movements based on historical seasonal tendencies.

What This Indicator Does

The True Seasonal Pattern analyzes years of historical price data to identify recurring seasonal trends. It then plots these patterns on your chart, showing you both the historical pattern and future projection based on past seasonal behavior.

Automatic Timeframe Detection: Works with Monthly, Weekly, and Daily charts

Historical Pattern Analysis: Analyzes up to 100 years of data (customizable)

Future Projection: Projects the seasonal pattern ahead on your chart

Smart Smoothing: Applies appropriate smoothing based on your timeframe

How to Use This Indicator

Add the indicator to a Daily, Weekly, or Monthly chart (not designed for intraday timeframes)

The indicator automatically detects your chart's timeframe

The blue line shows the historical seasonal pattern

Watch for potential turning points in the pattern that align with other technical signals

Seasonal patterns work best as a supporting factor in your analysis, not as standalone trading signals. They are particularly effective in markets with well-established seasonal influences.

Best Applications

Futures Markets: Commodities and futures often show strong seasonal tendencies due to production cycles, weather patterns, and economic factors

Stock Indices: Many stock markets demonstrate regular seasonal patterns (like the "Sell in May" phenomenon)

Individual Stocks: Companies with seasonal business cycles often show predictable price patterns

Practical Applications

Identify potential turning points based on historical seasonal patterns

Plan entries and exits around seasonal tendencies

Add seasonal context to your existing technical analysis

Understand why certain months or periods might show consistent behavior

Pro Tip: For best results, use this tool on instruments with at least 5+ years of historical data. Longer timeframes often reveal more reliable seasonal patterns.

Important Notes

This indicator works best on Daily, Weekly, and Monthly timeframes - not intraday charts

Seasonal patterns are tendencies, not guarantees

Always combine seasonal analysis with other technical tools

Past patterns may not repeat exactly in the future

// Sample of the seasonal calculation approach

float yearHigh = array.max(currentYearHighs)

float yearLow = array.min(currentYearLows)

// Calculate seasonality for each period

for i = 0 to array.size(currentYearCloses) - 1

float periodClose = array.get(currentYearCloses, i)

if not na(periodClose) and yearHigh != yearLow

float seasonality = (periodClose - yearLow) / (yearHigh - yearLow) * 100

I developed this indicator to help traders incorporate seasonal analysis into their trading approach without the complexity of traditional seasonal tools. Whether you're analyzing agricultural commodities, energy futures, or stock indices, understanding the seasonal context can provide valuable insights for your trading decisions.

Remember: Markets don't always follow seasonal patterns, but when they do, being aware of these tendencies can give you a meaningful edge in your analysis.

[GYTS] Filters ToolkitFilters Toolkit indicator

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- 1. INTRODUCTION --------- 🌸

💮 Overview

The GYTS Filters Toolkit indicator is an advanced, interactive interface built atop the high‐performance, curated functions provided by the FiltersToolkit library . It allows traders to experiment with different combinations of filtering methods -— from smoothing low-pass filters to aggressive detrenders. With this toolkit, you can build custom indicators tailored to your specific trading strategy, whether you're looking for trend following, mean reversion, or cycle identification approaches.

🌸 --------- 2. FILTER METHODS AND TYPES --------- 🌸

💮 Filter categories

The available filters fall into four main categories, each marked with a distinct symbol:

🌗 Low Pass Filters (Smoothers)

These filters attenuate high-frequency components (noise) while allowing low-frequency components (trends) to pass through. Examples include:

Ultimate Smoother

Super Smoother (2-pole and 3-pole variants)

MESA Adaptive Moving Average (MAMA) and Following Adaptive Moving Average (FAMA)

BiQuad Low Pass Filter

ADXvma (Adaptive Directional Volatility Moving Average)

A2RMA (Adaptive Autonomous Recursive Moving Average)

Low pass filters are displayed on the price chart by default, as they follow the overall price movement. If they are combined with a high-pass or bandpass filter, they will be displayed in the subgraph.

🌓 High Pass Filters (Detrenders)

These filters do the opposite of low pass filters - they remove low-frequency components (trends) while allowing high-frequency components to pass through. Examples include:

Butterworth High Pass Filter

BiQuad High Pass Filter

High pass filters are displayed as oscillators in the subgraph below the price chart, as they fluctuate around a zero line.

🌑 Band Pass Filters (Cycle Isolators)

These filters combine aspects of both low and high pass filters, isolating specific frequency ranges while attenuating both higher and lower frequencies. Examples include:

Ehlers Bandpass Filter

Cyber Cycle

Relative Vigor Index (RVI)

BiQuad Bandpass Filter

Band pass filters are also displayed as oscillators in a separate panel.

🔮 Predictive Filter

Voss Predictive Filter: A special filter that attempts to predict future values of band-limited signals (only to be used as post-filter). Keep its prediction horizon short (1–3 bars) for reasonable accuracy.

Note that the the library contains elaborate documentation and source material of each filter.

🌸 --------- 3. INDICATOR FEATURES --------- 🌸

💮 Multi-filter configuration

One of the most powerful aspects of this indicator is the ability to configure multiple filters. compare them and observe their combined effects. There are four primary filters, each with its own parameter settings.

💮 Post-filtering

Process a filter’s output through an additional filter by enabling the post-filter option. This creates a filter chain where the output of one filter becomes the input to another. Some powerful combinations include:

Ultimate Smoother → MAMA: Creates an adaptive smoothing effect that responds well to market changes, good for trend-following strategies

Butterworth → Super Smoother → Butterworth: Produces a well-behaved oscillator with minimal phase distortion, John Ehlers also calls a "roofing filter". Great for identifying overbought/oversold conditions with minimal lag.

A bandpass filter → Voss Prediction filter: Attempts to predict future movements of cyclical components, handy to find peaks and troughs of the market cycle.

💮 Aggregate filters

Arguably the coolest feature: aggregating filters allow you to combine multiple filters with different weights. Important notes about aggregation:

You can only aggregate filters that appear on the same chart (price chart or oscillator panel).

The weights are automatically normalised, so only their relative values matter

Setting a weight to 0 (zero) excludes that filter from the aggregation

Filters don't need to be visibly displayed to be included in aggregation

💮 Rich visualisation & alerts

The indicator intelligently determines whether a filter is displayed on the price chart or in the subgraph (as an oscillator) based on its characteristics.

Dynamic colour palettes, adjustable line widths, transparency, and custom fill between any of enabled filters or between oscillators and the zero-line.

A clear legend showing which filters are active and how they're configured

Alerts for direction changes and crossovers of all filters

🌸 --------- 4. ACKNOWLEDGEMENTS --------- 🌸

This toolkit builds on the work of numerous pioneers in technical analysis and digital signal processing:

John Ehlers, whose groundbreaking research forms the foundation of many filters.

Robert Bristow-Johnson for the BiQuad filter formulations.

The TradingView community, especially @The_Peaceful_Lizard, @alexgrover, and others mentioned in the code of the library.

Everyone who has provided feedback, testing and support!

Stage AnalysisStage Analysis was created by Stan Weinstein, and helps traders to identify where a stock/etf/index is in its Price Cycle.

The Price Cycle was introduced by Richard D. Wyckoff in the early 1900s, where he noted that stocks repeatedly go through a cycle of Accumulation, Markup, Distribution and Markdown. Stan Weinstein’s Stage Analysis method modified the Wyckoff Price Cycle, and converted it into four stages, which are:

Stage 1 = Accumulation

Stage 2 = Markup

Stage 3 = Distribution

Stage 4 = Markdown

Stage Analysis indicator:

Stan Weinstein had different definitions for the four stages – Stage 1: The Basing Area, Stage 2: The Advancing Phase, Stage 3: The Top Area, Stage 4: The Declining Phase. But for the purposes of the Stage Analysis indicator, you’ll note that we’ve combined Stage 1 and Stage 3, as they share numerous technical characteristics, and in our opinion, still require some discretionary judgement to determine whether they are showing accumulation or distribution characteristics.

So, we believe that neutral better describes them from a purely technical aspect, as being in Stage 3 doesn’t necessarily mean the top area, as it can still make a Stage 2 continuation breakout to new highs, instead of breaking down into Stage 4. Just as a Stage 1 basing pattern, can still make a further Stage 4 continuation breakdown, and won’t necessarily breakout into a Stage 2 advance. Hence, we display both Stage 1 and Stage 3 as Neutral, to help remove the perceived bias associated with Stage 3 and Stage 1.

So, in the indicator the Stages are displayed as three different colored backgrounds:

Blue = Stage 1 / Stage 3: Neutral

Green = Stage 2: Uptrend

Red = Stage 4: Downtrend

Stage 1 / Stage 3: Neutral (Blue background)

Stage 1 shows signs of a potential accumulation base structure developing and begins with a close above the 30-week simple moving average, when the stock is still below its (usually declining) 40-week MA as well, following a Stage 4 downtrend, and then remains in Stage 1 until either it breaks out into a Stage 2 uptrend, or returns to a Stage 4 downtrend once more. Although, there are often multiple failed breakout and breakdown attempts, which change the Stage briefly to Stage 2 or Stage 4, before reverting back into Stage 1, as the base broadens out.

The initial move into Stage 1 can occur in numerous different ways. Sometimes following a powerful rebound rally from the 52-week lows to above the 30-week MA, and at other times, after a basing period first, while the stock is still in Stage 4, and then only briefly moving into Stage 1, before breaking out into a new Stage 2 uptrend. But with all ways, there is a notable Change of Character compared to the previous Stage 4 downtrend, as supply and demand moves towards equilibrium, and the stock starts to build a more significant sideways range/base structure.

Stage 3 is the exact opposite of Stage 1, and instead of accumulation. Signs of distribution begin to appear when a stock is getting later in a Stage 2 Uptrend, with the stock first closing below its 30-week MA, and then starting to build a more significant sideways range/base structure, than the minor structures that formed when it was still trending higher in Stage 2.

It begins with a change of behaviour (i.e. a bigger correction than seen during the rest of Stage 2, that takes it below its 30-week, but still above its (usually rising) 40-week MA, and then that often broadens out into a sideways structure, with multiple swings above and below the 30-week MA, with tests of the highs and lows of the developing structure. Which can see it briefly revert to Stage 2, with failed breakout attempts at the highs (Upthrusts), or Stage 4, with failed breakdown attempts at the lows of the structure (Shakeouts or Springs).

So, Stage 1 and Stage 3 are both more neutral periods between the Stage 2 (Uptrend) and Stage 4 (Downtrend).

Stage 2: Uptrend (Green Background)

Stage 2 is the most important Stage for traders looking to buy stocks with the Stage Analysis method, and begins with a breakout from the prior Stage 1 base, but can also occur more suddenly from a V-bottom pattern or earnings gaps. In which case, it will move directly from a Stage 4 downtrend into a Stage 2 uptrend.

The move to Stage 2 requires certain technical aspects to be present, including a close above its near-term range (we use a 13-week range based on weekly closes), as well as its 200-day MA (40-week MA), and for our proprietary Stage Analysis Technical Attributes (SATA)* score to be at a least a SATA 6 of 10. And so, the change from Stage 1 to Stage 2 will often occur while the stock is still within a “broader” base structure, as the quarterly range is continually shifting, and doesn’t consider technical levels prior to that period.

The breakout point as Stage 2 begins is the Stage Analysis methods favoured entry zone for investors, as it marks the change from the Stage 1 basing period into the more dynamic Stage 2 uptrend (chart changes to green)

A secondary investor entry point can often form soon after the Stage 2 breakout, as the momentum fades from the initial rally, and it pulls back towards the breakout level, before finding support and swinging back higher into the advancing phase. So, the Stage Analysis indicator can be used to determine this secondary entry point by dropping down to an intraday timeframe – such as the 30-minute chart, and waiting for a Stage 2 breakout attempt on that much shorter timescale.

The Trader method entry points also form during the Stage 2 advance, and occur at the Stage 2 continuation breakout points of the more minor re-accumulation bases that form as the Stage 2 advance progresses higher.

Stage 4: Downtrend (Red Background)

Stage 4 is the opposite of Stage 2, and marks the beginning of a potential downtrend, as the distributional forces from Stage 3 gain control, and the stock attempts to move lower.

Stage 4 is the most important Stage for traders looking to short stocks with the Stage Analysis method, and as with Stage 2, it can also begin more suddenly following a sudden sharp decline or an earnings gap lower etc, that knifes through the key MAs and quarterly range.

The move to Stage 4 also requires certain technical aspects to be present, including a close below its near-term range (we use a 13-week range based on weekly closes), as well as its 200-day MA (40-week MA), and for our proprietary Stage Analysis Technical Attributes (SATA) score to be a maximum of a SATA 3 of 10, as if the SATA score is higher than 3, then it will still be considered as Stage 3 (blue) until that drops to a SATA 3 or lower.

The initial short entry point in Stage 4 occurs at the breakdown from Stage 3 to Stage 4 (chart changes to red), and as with Stage 2, a secondary entry point can form, but in Stage 4 it is on a potential pullback towards the breakdown level that then reverses lower once more. So, the Stage Analysis indicator can be used to determine this secondary entry point by dropping down to an intraday timeframe – such as the 30-minute chart, and waiting for a Stage 4 breakdown attempt on that much shorter timescale.

The Trader method short entry points also form during the Stage 4 decline, and occur at the Stage 4 continuation breakdown points of the more minor re-distribution bases that form as the Stage 4 decline progresses lower.

Recommended Chart Setup:

Weekly

Logarithmic scale

Recommended Indicators:

10 – Simple Moving Average

30 – Simple Moving Average

40 – Simple Moving Average (optional)

Mansfield Relative Strength (Original Version) (optional)

Stage Analysis Technical Attributes (SATA) (optional)

The Stages are intended to be used on the Weekly timeframe with a Logarithmic scale primarily, with a 10-week MA, 30-week MA and 40-week MA. But Stage Analysis can be used across multiple timeframes. So, for shorter-term swing traders, the 195-min (2bars/day), 2-hour, 1-hour, 30-min charts etc are often used with the same relative chart settings. But note that the lower the timeframe, the more noise that you’ll get, so you should always refer back to the weekly Stage to trade with the major trend.

Customise the Stage Analysis indicator

Edit colours of the Stages

Show/Hide Stages

Reference:

*Stage Analysis Technical Attributes (SATA)

The Stage Analysis Technical Attributes (SATA) scoring system is our proprietary tool which measures 10 of the key components that we look for in the Stage Analysis method to help to determine the Stage, and is made up of the following components:

Breakouts and Breakdowns

Price / Moving Averages

Relative Strength versus the S&P 500

Momentum

Volume

Overhead Resistance

Combining the SATA score with the price elements described in the Stages descriptions above, provides a Stage Analysis indicator that is faithful to Stan Weinstein's Stage Analysis method, and truly unique from other more simplistic automated versions of the Stages that you might find elsewhere.

Disclaimer: This indicator is for informational and educational purposes only. We accept no liability for any loss which may arise from the use of this indicator. All trading decisions are your own, and should be researched thoroughly, with appropriate risk management in place.

We are not affiliated with Stan Weinstein, and this is our own unique interpretation of the Stage Analysis method, based on our long experience with it.

Financial Astrology Indexes ML Daily TrendDaily trend indicator based on financial astrology cycles detected with advanced machine learning techniques for some of the most important market indexes: DJI, UK100, SPX, IBC, IXIC, NI225, BANKNIFTY, NIFTY and GLD fund (not index) for Gold predictions. The daily price trend is forecasted through planets cycles (angular aspects, speed phases, declination zone), fast cycles are based on Moon, Mercury, Venus and Sun and Mid term cycles are based on Mars, Vesta and Ceres . The combination of all this cycles produce a daily price trend prediction that is encoded into a PineScript array using binary format "0 or 1" that represent sell and buy signals respectively. The indicator provides signals since 2021-01-01 to 2022-12-31, the past months signals purpose is to support backtesting of the indicator combined with other technical indicator entries like MAs, RSI or Stochastic . For future predictions besides 2022 a machine learning models re-train phase will be required.

When the signal moving average is increasing from 0 to 1 indicates an increase of buy force, when is decreasing from 1 to 0 indicates an increase in sell force, finally, when is sideways around the 0.4-0.6 area predicts a period of buy/sell forces equilibrium, traders indecision which result in a price congestion within a narrow price range.

We also have published same indicator for Crypto-Currencies research portfolio:

DISCLAIMER: This indicator is experimental and don’t provide financial or investment advice, the main purpose is to demonstrate the predictive power of financial astrology. Any allocation of funds following the documented machine learning model prediction is a high-risk endeavour and it’s the users responsibility to practice healthy risk management according to your situation.

Fibonacci Degree System This Pine Script creates a sophisticated technical analysis tool that combines Fibonacci retracements with a degree-based cycle system. Here's a comprehensive breakdown:

Core Concept

The indicator maps price movements onto a 360-degree circular framework, treating market cycles like geometric angles. It creates a visual "mesh" where Fibonacci ratios intersect in both price (horizontal) and time (vertical) dimensions.

How It Works

1. Finding Reference Points

The script looks back over a specified period (default 100 bars) to identify:

Highest High: The peak price point

Lowest Low: The trough price point

Time Locations: Exactly which bars these extremes occurred on

These two points form the boundaries of your analysis window.

2. Creating the Fibonacci Grid

Horizontal Lines (Price Levels):

The script divides the price range between high and low into seven key Fibonacci ratios:

0% (Low) - Bottom boundary in red

23.6% - Minor retracement in orange

38.2% - Shallow retracement in yellow

50% - Midpoint in lime green

61.8% - Golden ratio in aqua (most significant)

78.6% - Deep retracement in blue

100% (High) - Top boundary in purple

Each line represents a potential support/resistance level where price might react.

Vertical Lines (Time Cycles):

The same Fibonacci ratios are applied to the time dimension between the high and low bars. If your high and low are 50 bars apart, vertical lines appear at:

Bar 0 (0%)

Bar 12 (23.6%)

Bar 19 (38.2%)

Bar 25 (50%)

Bar 31 (61.8%)

Bar 39 (78.6%)

Bar 50 (100%)

These suggest when price might make significant moves.

3. The Degree Mapping System

The innovative feature maps the time progression to degrees:

0° = Start point (0% time)

85° = 23.6% through the cycle

138° = 38.2% through the cycle

180° = Midpoint (50%)

222° = 61.8% through the cycle (golden angle)

283° = 78.6% through the cycle

360° = Complete cycle (100%)

This treats market movements as circular patterns, similar to how planets orbit or pendulums swing.

Visual Output

When you apply this indicator, you'll see:

A rectangular mesh extending beyond your high-low range (by 150% default)

Color-coded horizontal lines showing price Fibonacci levels

Matching vertical lines showing time Fibonacci intervals

Price labels on the right showing percentage levels

Degree labels at the bottom showing the angular position in the cycle

Intersection points creating a grid of potentially significant price-time coordinates

Trading Application

Traders use this to identify:

Support/Resistance Zones: Where horizontal and vertical lines intersect

Time Targets: When price might reverse (at vertical Fibonacci times)

Cycle Completion: When approaching 360°, a new cycle may begin

Harmonic Patterns: Geometric relationships between price and time

Customization Features

The script offers extensive control:

Lookback period: Adjust cycle length (10-500 bars)

Mesh extension: How far to project the grid forward

Visual toggles: Show/hide horizontal lines, vertical lines, labels

Styling: Line thickness, style (solid/dashed/dotted), colors

Label positioning: Fine-tune text placement for readability

The intersection at 61.8% time and 61.8% price at 222° becomes a key target zone.

This tool essentially converts the abstract concept of market cycles into a concrete, visual geometric framework that traders can analyze and act upon.

DISCLAIMER: This information is provided for educational purposes only and should not be considered financial, investment, or trading advice.

No guarantee of profits: Past performance and theoretical models do not guarantee future results. Trading and investing involve substantial risk of loss.

Not a recommendation: This script illustration does not constitute a recommendation to buy, sell, or hold any financial instrument.

Do your own research: Always conduct thorough independent research and consider consulting with a qualified financial advisor before making any trading decisions.

QuantMotions - Pivot Timeline ProjectionQuantMotions – Pivot Timeline Projections is an advanced time-based forecasting tool that uses a unique Twin Pivot model to project future price-time structures.

It combines classical Gann principles with modern quantitative logic to generate highly precise time projections, dynamic angles, and future support/resistance timelines across multiple timeframes.

Whenever two matching pivots (High ↔ Low) of the same length are detected, the indicator calculates a true calendar-time angle and extends it forward, forming dynamic Gann-style fans that adapt to the market in real time.

Perfect for traders who want to integrate price + time forecasting into their strategy.

Key Features:

✔ Twin Pivot Detection

Automatically identifies valid pivot pairs of equal cycle length and opposite direction.

Once confirmed, the pivot becomes a time anchor for future projections.

✔ True Time-Based Angle Projections

Unlike standard Gann tools that rely on bar-counting, this indicator uses real calendar time (milliseconds) to calculate:

This produces significantly more accurate forecasting lines.

✔ Multi-Timeframe Pivot Cycles

Activate time cycles such as:

30M, 1H, 4H, 12H

1D, 7D, 30D

60D, 90D, 120D, 180D, 270D, 360D

Each cycle uses a dedicated color and projection style for clarity.

✔ Dynamic Support/Resistance Timefans

- Every confirmed pivot generates two future projections:

- The main time-angle projection (Gann-style forward fan)

- A secondary projection based on a fixed ratio (1/8), acting as dynamic future support

Both extend until the structure breaks based on ATR tolerance.

✔ ATR-Based Validation

Projection lines remain valid until price breaks them with a configurable ATR multiplier.

This removes noise and keeps only meaningful structures.

✔ Volume Delta Tracking (Optional)

Tracks up-volume and down-volume along the time cycle to validate directional bias.

Info labels show:

- cycle length

- angle

- delta volume

- delta percentage

Seconds-based volume tracking supported for Premium users.

✔ Smart Info Labels

Displays detailed pivot information only for the highest-timeframe pivot at each bar

→ ensures high usability without chart clutter.

🔷 Why This Indicator Is Special

This tool merges Gann angles, time cycles, and quantitative price action into a single engine.

It does not rely on static angles or simple bar offsets.

Instead, it uses:

- real time

- real slope

- real cycle symmetry

- real price movement

The result is a uniquely accurate forecasting model that is extremely difficult to replicate manually.

🔷 Perfect For

- Intraday traders

- Swing traders

- Index, Crypto, Metals, and FX traders

- Gann and cycle-based analysts

- Structure and trend change detection

- Time/price projection strategies

🔷 Inputs & Customization

- ATR break tolerance

- Multiple cycle activation toggles

- Custom color sets for each timeframe

- Second-based or standard timeframe volume tracking

- Enable/Disable info labels

🔷 Note

Some features (like seconds-based volume tracking) depend on TradingView Premium and additional broker data sources.

Loading times may vary when many long-term cycles are enabled simultaneously.

🔷 Access

This is an Invite-Only Script by QuantMotions.

Access is granted after purchase.

For more information, please visit the official product page or contact us directly.

Dynamic Gann Square Pro - [Magic_xD]Premium Gann Analysis System for Professional Traders

Dynamic Gann Square Pro is an advanced technical analysis tool that combines classical Gann theory with modern geometric analysis to identify high-probability support/resistance zones, time cycles, and market turning points.

🎯 What This Indicator Does

This indicator provides a comprehensive suite of Gann-based analytical tools designed to help traders identify:

Dynamic Support & Resistance Levels: Automatically calculated key price zones based on market structure

Gann Square of 9 Calculations: Multiple calculation methods including Range, Daily, Weekly, and Monthly timeframes

Advanced Time Cycle Analysis: Gann cycles, Fibonacci time projections, and Square Root cycles for anticipating market turns

Geometric Pattern Recognition: Gann Stars with customizable shapes (Square, Triangle, Pentagon, Hexagon, Octagon, and more)

Price Action Zones: Color-coded zones highlighting critical decision points

Whale Detection System: Volume-weighted analysis to identify institutional activity

Multi-Timeframe Dashboard: Real-time technical rating system combining 10+ indicators (RSI, MACD, Stochastic, ADX, Bollinger Bands, and more)

📊 Key Features

Flexible Calculation Modes:

Select Candle Mode: Click directly on your chart to select your reference point

Lookback Mode: Define custom lookback periods (1-5000 bars)

Auto-Timeframe Detection: Automatically adjusts to Daily, Weekly, or Monthly ranges

Advanced Gann Tools:

Configurable Gann Square spacing with 17 precision levels (from 0.00000001 to 100000000)

Cycle multipliers (1-10 cycles) representing 360° to 3600° rotations

14 geometric shapes for market division analysis

Infinite Squares projection system for extended future projections

Time Cycle Systems:

Classical Gann Time Cycles with automatic repetition

Extended Fibonacci Time Ratios (0.382, 0.618, 1.618, 2.618, 3.618, up to 21.0)

W.D. Gann Square Root Method for geometric time expansion

Time grid subdivisions with customizable styles

Visual Clarity:

Multiple color themes (Dark Blue, Dark Gray, Black, Dark Green, Dark Purple)

Adjustable line styles (Solid, Dashed, Dotted) for all elements

Customizable labels with offset controls

Zone highlighting with transparency controls

Clean, professional chart presentation

🔮 Who Should Use This

This indicator is designed for:

Experienced traders familiar with Gann analysis methodology

Swing traders looking for high-probability reversal zones

Position traders using geometric and time-based analysis

Technical analysts who incorporate classical market theory

Gold & Forex traders (optimized for XAUUSD, BTCUSD, and major pairs)

⚙️ How to Use

Select Your Mode: Choose between "Select Candle" (click a pivot) or "Lookback" (automatic detection)

Configure Calculation Method: Pick your preferred Gann Square method (Range, Sqr9, Daily, Weekly, Monthly)

Adjust Cycles & Shape: Set the number of cycles and geometric division pattern

Enable Desired Features: Toggle Gann levels, Stars, Time Cycles, Trendlines, and Dashboard as needed

Customize Visual Style: Match your chart theme and preferences

The indicator automatically updates as new price data arrives, continuously calculating fresh support/resistance zones and time projections.

📈 What Makes This Different

Unlike simple support/resistance indicators, Dynamic Gann Square Pro implements authentic W.D. Gann methodology including:

True Square of 9 spiral calculations

Geometric price-time relationships

Natural angle divisions based on sacred geometry

Volume-weighted institutional detection

Multi-indicator consensus analysis

The system combines price analysis with time analysis, recognizing that Gann theory emphasizes both dimensions equally for accurate market forecasting.

⚠️ Important Notes

This is a technical analysis tool and should be used alongside proper risk management

Best results achieved when combined with your existing trading strategy

The indicator works on all timeframes but is optimized for H1, H4, and Daily charts

Customization is key: Spend time adjusting settings to match your trading instrument and style

The dashboard provides a technical rating but is not financial advice

🎓 Educational Foundation

This indicator is built on the teachings of W.D. Gann, one of the most legendary traders of the 20th century, incorporating:

Square of 9 theory

Natural geometric divisions (360° cycles)

Price-time equivalence principles

Support/resistance zone analysis.

Coded by Magic_xD - Ahmed Ramzey

Professional Algorithmic Trading System Developer

All copyrights reserved. This indicator represents years of research into Gann theory combined with modern programming techniques.

ATC v6 with ORB by SabnATC v6 with ORB: Advanced Automatic Session and Opening

Range Indicator

ATC v6 is an advanced indicator designed by Alfa Trade Club for

TradingView users. This tool not only automatically marks important session

opens, closes, or specific times of financial markets on your chart but also

visualizes powerful Opening Range (ORB) strategies directly on your chart.

This tool removes the need to manually monitor critical trading hours, allowing

you to easily analyze price action in relation to these important timeframes.

Key Features

This indicator comes with a set of powerful features to provide the flexibility,

visual clarity, and strategic advantage that traders need:

1. Multi-Time Zone Support The indicator is based on the world's most

important financial market centers:

New York (America/New_York)

London (Europe/London)

Tokyo (Asia/Tokyo)

Istanbul (Europe/Istanbul)

This allows you to always set the lines accurately according to the local time of

the market you are trading.

2. Advanced 3-Stage Timing (Pre / Main / Next) Each time line is more than

just a simple line; it can manage a three-stage event cycle:

"Pre-Session": Draws a dotted line a few minutes before the main time you

specify (e.g., market open). This allows you to see the price level just before a

significant event.

"Main Session": Marks the opening price at the exact event time (e.g., 08:00

London Open) with a solid line.

"Next / ORB" (Opening Range): Draws another dotted line a specified number

of minutes after the main event (e.g., 15 minutes later). This is used to define the

Opening Range.

3. Automatic Price Boxes (Volatility & ORB) The indicator can draw two

different types of boxes based on this timing:

Opening Volatility Box (Pre -> Main): If the "Pre-Session" feature is active, the

indicator draws a colored box between the price at the pre-session moment and

the price at the main event. This box visualizes the initial volatility at the session

open.

Opening Range Box (Main -> Next): If the "Next" feature is active, the indicator

draws a box between the price at the main event and the "next" event.

4. Customizable Time Lines You have full control over each line. Users can:

Enable/Disable each line.

Set any desired hour and minute.

Define the "Pre" and "Next" durations in minutes.

Assign a different color for visual distinction.

5. Smart and Efficient Drawing

Forward-Extending Lines: All drawn lines and boxes automatically extend from

the moment they are created until the next day. This makes it easy to track how

these levels act as support/resistance throughout the day.

High Performance: Instead of deleting old lines and drawing new ones when a

new day starts, the code intelligently extends the existing lines into the next day

Weekend and DST Protection: Automatically skips weekends (from Friday to

Monday) and is not affected by Daylight Saving Time (DST) changes.

Who Is It For?

Session-Focused Traders: Ideal for those who track volatility during the London,

New York, Asian, or Istanbul session opens.

Day Traders: Perfect for those who want to mark important economic data

release times or daily market open/close levels.

Technical Analysts: A powerful aid for those who want to visually analyze how

opening prices at specific times and time ranges play a role throughout the day.

ATC v6 with ORB is much more than just a simple session line; it is a dynamic

analysis and strategy tool that combines price and time.

HADES Timecycle SMTWhat this indicator tracks

1) Time‑cycles based on QT (Micro → 90‑minute → Daily → Weekly)

HADESSMT segments the trading day and week into recurring phases and paints them directly on your chart:

real time plotting of SSMTs for Micro cycles, when Q1 and Q2 highs or lows are different for correlated assets. same for the 90‑minute quarters , Daily cycles and Weekly cycles

2) SSMT : The script continuously compares your chart to a correlated instrument and highlights cycle‑scoped SMT divergences :

Scopes: Micro, 90m, Daily, Weekly.

The tool draws compact slanted segments between consecutive cycle highs/lows and places a small label with the scope tag (e.g., 90m, D, W, Mic.) and the comparison ticker.

Table summary: A docked panel logs Bullish/Bearish SMT currently active per scope.

In plain English: when two tightly related markets fail to confirm each other’s new extremes inside the same cycle window, HADESSMT calls that out visually and in the table.

3) PSP /scanner (👁️)

A compact scanner runs on 240m, 60m, and 15m composite views of your chosen inter‑market set and tags bars with an eye icon (👁️):

👁️ below price → a bullish turning‑point signature.

👁️ above price → a bearish turning‑point signature.

Events are logged in the table (e.g., “60m Bullish PSP 👁️”).

Treat PSP tags as context—they’re not trade signals by themselves. They often add confluence when they align with SSMT and cycle boundaries.

4) “True Open” levels

includes a daily open line that marks midnight open for the day.

Inter‑market sets (Triads & Dyads)

HADESSMT automatically picks a comparison instrument based on what you’re charting. Two mechanisms exist:

Triads (auto‑pairing):

FX: EUR + GBP ↔ inverse DXY

Metals: Gold + Silver

US Indices: NQ + YM + ES

You can show one or both comparison legs.

Tip: If you don’t see SMT labels, ensure your symbol belongs to one of the configured sets or customize the tickers in Triad inputs.

On‑chart visuals you’ll see

Thin slanted SMT markers between successive cycle extremes with a small scope/ticker tag.

👁️ PSP labels on higher‑timeframe bars.

True‑Open lines labeled 00:00 (daily) .

Summary table (right side by default) containing:

The comparison ticker currently in use,

Any active Bullish/Bearish SMT per scope,

Recent PSP 👁️ calls at 240/60/15 minutes.

How to use it (practical flow)

Pick your market & ensure a comparison exists (Triad ).

Important: HADESSMT is a context engine, not a trade system. Use your own risk management and confirmation.

Triad– enable one/both SMT comparisons; edit the default tickers if your broker symbols differ.

Timezone – UTC offset (default -4) to align cycle splits with your session.

Micro features appear on charts ≤ 5m.

90‑minute features are designed for charts ≤ 30m.

Daily features prefer charts ≤ 3h.

Weekly features render reliably on daily charts and below.

(If a layer doesn’t appear, you may be on a timeframe above its designed threshold.)

FAQs

Why don’t I see SMT on my market?

Ensure the symbol is in one of the configured Triad sets, or add your own correlated ticker(s).

What exactly is PSP?

A compact pressure/turn signature across your inter‑market set. It’s presented as an 👁️ tag and a table entry (bullish/bearish). The internal detection specifics are intentionally abstracted.

BTC Dominance Zones (For Altseason)Overview

The "BTC Dominance Zones (For Altseason)" indicator is a visual tool designed to help traders navigate the different phases of the altcoin market cycle by tracking Bitcoin Dominance (BTC.D).

It provides clear, color-coded zones directly on the BTC.D chart, offering an intuitive roadmap for the progression of alt season.

Purpose & Problem Solved

Many traders often miss altcoin rotations or get caught at market tops due to emotional decision-making or a lack of a clear framework. This indicator aims to solve that problem by providing an objective, historically informed guide based on Bitcoin Dominance, helping users to prepare before the market makes its decisive moves. It distils complex market dynamics into easily digestible sections.

Key Features & Components

Color-Coded Horizontal Zones: The indicator draws fixed horizontal bands on the BTC.D chart, each representing a distinct phase of the altcoin market cycle.

Descriptive Labels: Each zone is clearly labeled with its strategic meaning (e.g., "Alts are dead," "Danger Zone") and the corresponding BTC.D percentage range, positioned to the right of the price action for clarity.

Consistent Aesthetics: All text within the labels is rendered in white for optimal visibility across the colored zones.

Symbol Restriction: The indicator includes an automatic check to ensure it only draws its visuals when applied specifically to the CRYPTOCAP:BTC.D chart. If applied to another chart, it displays a helpful message and remains invisible to prevent confusion.

Methodology & Interpretation

The indicator's methodology is based on the historical behavior of Bitcoin Dominance during various market cycles, particularly the 2021 bull run. Each zone provides a specific interpretation for altcoin strategy:

Grey Zone (BTC.D 60-70%+): "Alts Are Dead"

Interpretation: When Bitcoin Dominance is in this grey zone (typically above 60%), Bitcoin is king, and capital remains concentrated in BTC. This indicates that alt season is largely inactive or "dead". This phase is generally not conducive for aggressive altcoin trading.

Blue Zone (BTC.D 55-60%): "Alt Season Loading"

Interpretation: As BTC.D drops into this blue zone (below 60%), it signals that the market is "heating up" for altcoins. This is the time to start planning and executing your initial positions in high-conviction large-cap and strong narrative plays, as capital begins to look for more risk.

Green Zone (BTC.D 50-55%): "Alt Season Underway"

Interpretation: Entering this green zone (below 55%) signifies that "real momentum" is building, and alt season is genuinely "underway". Money is actively flowing from Ethereum into large and mid-cap altcoins. If you've positioned correctly, your portfolio should be showing strong gains in this phase.

Orange Zone (BTC.D 45-50%): "Alt Season Ending"

Interpretation: As BTC.D dips into this orange zone (below 50%), it suggests that altcoin dominance is reaching its peak, indicating the "ending" phase of alt season. While euphoria might be high, this is a critical warning zone to prepare for profit-taking, as it's a phase of "peak risk".

Red Zone (BTC.D Below 45%): "Danger Zone - Alts Overheated"

Interpretation: This red zone (below 45%) is the most critical "DANGER ZONE". It historically marks the point of maximum froth and risk, where altcoins are overheated. This is the decisive signal to aggressively take profits, de-risk, and exit positions to preserve your capital before a potential sharp correction. Historically, dominance has gone as low as 39-40% in this phase.

How to Use

Open TradingView and search for the BTC.D symbol to load the Bitcoin Dominance chart and view the indicator.

Double click the indicator to access settings.

Inputs/Settings

The indicator's zone boundaries are set to historically relevant levels for consistency with the Alt Season Blueprint strategy. However, the colors of each zone are fully customizable through the indicator's settings, allowing users to personalize the visual appearance to their preference. You can access these color options in the indicator's "Settings" menu once it's added to your chart.

Disclaimer

This indicator is provided for informational and educational purposes only. It is not financial advice. Trading cryptocurrencies involves substantial risk of loss and is not suitable for every investor. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial professional before making any investment decisions.

About the Author

This indicator was developed by Nick from Lab of Crypto.

Release Notes

v1.0 (June 2025): Initial release featuring color-coded horizontal BTC.D zones with descriptive labels, based on Alt Season Blueprint strategy. Includes symbol restriction for correct chart application and consistent white text.

FloWave Oscillator [StabTrading]The FloWave Oscillator is a powerful trading tool designed to identify market trends and reversals by analysing reversal zones based on momentum and fear algorithms.

Serving as the first stage in a comprehensive trading system, it is intentionally straightforward, allowing traders to clearly see potential entry points across all charts and timeframes.

By inputting their own market sentiment, traders can customize the algorithm to align with their trading style. This flexibility helps traders navigate complex market environments with greater precision, whether they are seeking to capitalize on short-term opportunities or ride longer-term trends.

💡 Features

Reversal Zones - The FloWave Oscillator identifies key reversal zones driven by momentum and fear dynamics. Lighter green zones signal the initial stages of a potential reversal, while darker green zones indicate that a trend flip is imminent.

Trading Style Customization - The indicator allows traders to adjust their trading style with sensitivity settings ranging from Very Aggressive to Very Conservative. This flexibility lets traders tailor the indicator to their preferred time horizon—whether they seek to scalp short-term opportunities or capture long-term reversals.

🔥 Sensitivity Settings

Very Aggressive/Aggressive - These settings increase the indicator's sensitivity, generating more frequent signals, ideal for traders focused on short-term gains or those navigating choppy markets.

Neutral - Offers a balanced approach, combining both aggressive and conservative elements. It's a starting point for traders to evaluate performance before adjusting to more specific styles.

Conservative/Very Conservative - These settings reduce signal frequency, focusing on stronger, more reliable reversals. Best suited for long-term traders aiming to minimize risk and avoid premature market entries or exits.

🛠️ Usage/Practice

In the above example we’ll analysis how the indicator accurately predicts both the tops and bottoms of a market cycle.

Top of the Bull Market - The trendline initially shows two light red reversal zones, signalling a potential weakening in the upward momentum. As the trend progresses, a dark red zone emerges, confirming that a more substantial trend reversal to the downside is likely. This sequence provides an early warning, allowing traders to prepare for a possible market shift.

First Bull Signal - In the following phase, the indicator mirrors the previous action but in the opposite direction, identifying a reversal towards the upside. This behaviour demonstrates the indicator's ability to adapt to changing market conditions.

Bottom of the Bear Market - As the market continues its downward trajectory, the indicator presents two dark green reversal zones, highlighting areas where the selling pressure may be easing. These dark green zones offer three distinct opportunities to dollar-cost average (DCA) into the asset, allowing traders to build or enhance their positions during the end of the bear cycle. The indicator’s sensitivity in this phase ensures that traders can navigate the bearish market with confidence.

Continuation of Bull Cycle - In this segment, the indicator does not display any dark green reversal zones, implying that the uptrend remains robust. The absence of these zones suggests that the upward momentum is likely to continue, providing traders with another opportunity to add to their long positions. This scenario underscores the indicator’s capacity to identify when a trend is strong enough to warrant additional investment.

Potential Correction in an Uptrend - A light red zone appears, signalling a possible correction within the ongoing uptrend. However, the absence of a dark red zone indicates that the correction may be minor and that the overall trend is still upward. Traders might view this as a conservative point to take some profits off the table, managing risk while staying aligned with the broader bull market.

Bearish Signal - Eventually, a dark red reversal zone emerges, indicating that the trend has lost its upward momentum. This signal serves as a strong indicator that the uptrend may be concluding, prompting traders to consider exiting their positions or taking a more defensive stance. As the market enters a sideways phase, the trader can switch to a more aggressive trading style, seeking opportunities to scalp within the range while navigating the flat market conditions.

In this example, we demonstrate how to identify scalp trading opportunities by combining the Very Conservative and Very Aggressive settings. The key strategy is to use the Very Conservative trend to confirm the validity of reversal zones identified by the Very Aggressive setting.

The VC trend doesn’t indicate a buy reversal zone, but it shows an upward divergence. This suggests that the reversal buy zone on the VA chart is a potential entry point due to the supportive VC trend.

Multiple sell zones appear on the VA chart, but the VC trend shows a strong and steady uptrend. This suggests that we should wait for confirmation from the VC trend before considering a sell position, as the market is still moving upward strongly.

The VA chart shows several buy zones, but the VC trend indicates a strong downtrend, and no buy zone appears on the conservative setting. This suggests waiting for the next VA buy zone, confirmed by an upward divergence on the VC trend, before entering a trade.

Similar to Point 3 but in the opposite direction, the VA chart shows sell zones, but the VC trend indicates caution. The strategy would be to wait for confirmation from the VC trend before making a move.

🔶Conclusion

When used in conjunction with other indicators like the MeanRevert Matrix, the FloWave Oscillator becomes an integral part of a comprehensive trading system. It helps traders make informed decisions by providing clear signals that are aligned with the current market sentiment and broader economic trends. By following the implementation guidelines and adjusting the indicator settings as market conditions change, traders can effectively enhance their trading performance.

ZigCycleBarCount [MsF]Japanese below / 日本語説明は英文の後にあります。

Based on "ZigZag++" indicator by DevLucem. Thanks for the great indicator.

-------------------------

This indicator that displays the candle count (bar count) at the peaks of Zigzag .

It also displays the price of the peaks.

You can easily count candles (bars) from peak to peak. Helpful for candles (bars) in cycle theory.

This logic of the indicator is based from the mt4 zigzag indicator .

Parameter:

Depth = depth (price range)

Backstep = Period

Deviation = Percentage of how much the price has wrapped around the previous line.

Example:

Depth = 12

Backstep = 3

Deviation = 5

In this case, the price range is updated by 12 pips or more (Depth), and after 3 or more candlesticks line up (Backstep), if the price deviates from the previous line by 5% or more (Deviation), a peak is added.

-------------------------

Zigzagの頂点にローソクカウント(バーカウント)を表示するインジケータです。

頂点の価格も表示します。

頂点から頂点までのローソク(バー)を容易にカウントすることができます。

サイクル理論のローソク(バー)に役立ちます。

Zigzagロジック自体はMT4のzigzagインジケータを流用しています。

<パラメータ>

Depth=深さ(値幅)

Backstep=期間

Deviation=価格がどれだけ直前のラインの折り返したかの割合

例:

Depth=12

Backstep=3

Deviation=5

この場合、値幅を12pips以上更新し(Depth)、ローソク足が3本以上並んだ後(Backstep)、価格が直前のラインの5%以上折り返せば(Deviation)、頂点を付けます。

<表示オプション>

Label_Style = "TEXT"…テキスト表示、"BALLOON"…吹き出し表示

Altcoins Exit Planner [SwissAlgo]Altcoins Exit Planner

Navigating Altcoin Exits: A Strategic Approach: Planning your exits before emotions take over

------------------------------------------------------------------

✅ THE PSYCHOLOGY OF ALTCOIN TRADING

Many traders face recurring challenges when managing altcoin positions:

The Greed Trap : Holding through euphoric rallies, hoping for unrealistic targets, only to watch gains evaporate during market reversals.

The Paralysis Problem : Sitting on large unrealized profits but unsure which assets to exit, when, or how much — leading to inaction.

The FOMO Cycle : Rotating into trending coins too early or too late, often abandoning solid positions prematurely.

Analysis Overload : Consuming endless opinions and indicators without ever forming a clear, actionable exit strategy.

These patterns often stem from a lack of structure and planning . Emotional decision-making in volatile markets can be costly — especially with altcoins.

Developing a systematic framework can help define exit levels in advance , aiming to reduce emotional bias and improve decision clarity. The goal is to build disciplined exit strategies based on predefined logic rather than reactive impulses.

------------------------------------------------------------------

✅ FEATURES & FUNCTIONALITY

This indicator is designed to provide traders with a structured framework for exit planning. It aims to reduce decision-making under pressure by offering a visual roadmap on the chart.

The tool provides an analysis of key data points, including:

Structured Analysis : The indicator evaluates asset strength, identifies potential market phases, and derives potential exit levels from historical price behavior. This analysis may help traders assess whether an asset shows characteristics of strength (e.g., potential for extended targets) or weakness (e.g., early exit signals).

Actionable Information : It generates specific price levels and quantities for consideration as part of a predefined exit strategy.

Proactive Alerts : The system includes configurable alerts that can notify users as prices approach these key levels, allowing time for preparation. This feature is intended to support a shift from reactive trading toward systematic, criteria-based exit planning.

------------------------------------------------------------------

✅ HOW IT WORKS - AUTOMATED ANALYSIS & PLANNING

This indicator is designed to automate key aspects of exit planning that would otherwise require manual effort:

Fibonacci Level Calculation & Plotting : Automatically identifies key historical cycle points (e.g., bear market lows, bull market highs, recent pullbacks) and calculates relevant Fibonacci levels (both "Fib Retracments" from previous cycle ATH to bear market bottom, and "Fib. extensions" - considering major price impulses/waves in current bull market). This may help reduce manual drawing errors and streamline target identification.

Automated Calculation and Plotting of "Fib. Retracement "Levels

(from ATH of previous cycle to bottom in bear market)

Fibonacci retracement levels are a popular tool used in technical analysis to identify potential support and resistance levels in a market. After a significant price move, traders look for the price to "retrace" or pull back to one of several key Fibonacci ratios of the original move before continuing in its original direction. The most common retracement levels are 23.6%, 38.2%, 50%, 61.8%, and 78.6%. These levels are static horizontal lines on a chart, and their predictive power is based on the idea that they are "areas of interest" where a trend might pause or reverse.

Automated Calculation and Plotting of "Fib. Extension" Levels

(Price Impulses/Waves within current Bull Market)

Fibonacci extension levels are used to identify potential price targets or profit zones once a market has moved past its previous high or low. Unlike retracements, which measure a pullback, extensions project how far a trend might continue in the direction of its impulse move. They are typically used to anticipate where a wave or a rally might end and are based on ratios like 127.2%, 161.8%, 261.8%, and sometimes even higher. Extensions are a key tool for traders looking to set price targets for taking profits.

Coin Strength Assessment: Evaluates recovery performance relative to previous cycle peaks and classifies assets into four categories (Weak, Average, Strong, Outlier). Strength ratings may adjust dynamically based on momentum conditions — all derived from price data.

Market Phase Detection : Continuously monitors trend indicators, volume behavior, and altseason dynamics to estimate the current market phase. This may assist in contextualizing exit decisions without requiring manual phase analysis.

Exit Level Generation : Based on the asset’s strength classification and selected strategy (Conservative, Balanced, Aggressive), the system generates sequential exit levels with suggested percentages and quantities. Designed to support structured planning across three stages.

Signal Detection : Tracks multiple conditions — including price extensions, volume surges, momentum shifts, and cycle patterns — to generate alerts when predefined criteria are met.

Emergency Exit Detection : Scans for rare but high-risk scenarios (e.g., cycle top formations with multiple confluences) that may warrant immediate attention. Alerts are designed to highlight potential overextension during volatile phases.

Transfer Alerts : Calculates proximity to key exit zones and may issue early warnings to prepare for execution (e.g., moving assets from cold storage to exchanges), aiming to reduce last-minute decision pressure.

The script operates in two distinct modes:

Coin Analysis Mode Displays automatically-calculated Fibonacci levels, asset strength classification, market phase estimation, and contextual risk factors — designed to support structured analysis.

Exit Plan Mode Generates a customizable exit strategy with calculated price levels, suggested quantities, and potential outcome scenarios — aiming to assist with disciplined planning and reduce emotional bias.

------------------------------------------------------------------

✅ SETUP & INSTALLATION

Step 1: Chart Setup

Add the indicator to your altcoin USD chart (e.g., spot market pairs).

Recommended timeframe: 3 days for signal clarity.

Dark theme suggested for visual contrast.

Step 2: Configure Your Exit Strategy

Open Settings → “Setup Your Exit Plan”