3-6-9 Time Pattern Highlighter v63-6-9 Time Pattern Highlighter

Description

The 3-6-9 Time Pattern Highlighter is a powerful tool designed to identify and highlight 1-minute candles based on specific time-based patterns, inspired by the 3-6-9 sequence. This indicator is ideal for traders who incorporate time-based analysis into their strategies, helping to pinpoint key moments in the market with customizable visual cues. It supports two distinct patterns, each with unique minute sequences, and offers flexible controls to tailor highlighting to your trading needs.

Features

• Pattern 1 (Minutes-Only): Highlights candles every 3 minutes (03, 06, …, 57) within each hour, perfect for consistent intraday timing analysis.

• Pattern 2 (Hour + Minutes): Highlights candles based on the hour’s position in a 12-hour cycle:

• Hours 3, 6, 9, 12: Minutes 00, 03, …, 57.

• Hours 1, 4, 7, 10: Minutes 02, 05, …, 59.

• Hours 2, 5, 8, 11: Minutes 01, 04, …, 58.

• Customizable Colors: Assign unique highlight colors for Pattern 1 and Pattern 2 to distinguish between patterns visually.

• Hourly Toggles: Enable or disable highlighting for each hour (0-23) individually, giving precise control over which time periods are analyzed.

• Pattern Toggles: Independently enable or disable Pattern 1 and Pattern 2 to focus on specific timing strategies.

How to Use

1. Add the indicator to your chart (best on 1-minute timeframes for maximum precision).

2. In the settings, customize:

• Enable/disable Pattern 1 and Pattern 2.

• Select specific hours to highlight using the 0-23 hour toggles.

• Choose distinct colors for each pattern to match your chart style.

3. Observe highlighted candles to identify key time-based opportunities aligned with the 3-6-9 patterns.

Use Cases

• Intraday Trading: Spot critical moments for trade entries or exits based on recurring time patterns.

• Time-Based Analysis: Combine with other indicators to validate signals at specific times.

• Custom Strategies: Tailor the indicator to focus on specific hours or patterns relevant to your market analysis.

Notes

• Optimized for 1-minute charts but works on any timeframe where candle open times match the pattern.

• Ensure your chart’s timezone aligns with your analysis for accurate highlighting.

• When both patterns trigger on the same candle, Pattern 1’s color takes precedence (customizable upon request).

Disclaimer

This indicator is for informational purposes and should be used as part of a broader trading strategy. Always conduct your own analysis and practice proper risk management.

"Cycle" için komut dosyalarını ara

Global M2 Money Supply -WinCAlgoWhat is this Indicator?

The Global M2 Money Supply Indicator aggregates the M2 money supply data from 20 major economies worldwide, converted to USD. This powerful macro-economic tool tracks the total liquidity injected into the global financial system, providing crucial insights for long-term investment decisions across all asset classes including crypto, stocks, bonds, and commodities.

Key Features:

20 Major Economies: US, EU, China, Japan, UK, Canada, Switzerland, and 13 other significant markets

USD Normalized: All currencies converted to USD for unified comparison

Real-time Data: Updates with latest central bank releases

Time Offset: Adjustable time offset for correlation analysis (-1000 to +1000 days)

Macro Analysis: Essential tool for understanding global liquidity cycles

How to Use:

Long-term Analysis: Use on weekly/monthly timeframes for macro trend identification

Liquidity Cycles: Rising M2 typically correlates with asset price increases

Market Timing: Major inflection points often coincide with policy changes

Cross-Asset Analysis: Compare with Bitcoin, Gold, Stock indices for correlation

Time Offset: Adjust offset to analyze leading/lagging relationships

Trading Applications:

Crypto Analysis: Bitcoin and altcoins often correlate with global liquidity

Stock Markets: Equity valuations tend to follow liquidity expansion/contraction

Commodities: Gold, Silver, and other commodities react to money supply changes

Bond Markets: Interest rate expectations influenced by monetary policy

Currency Analysis: Understand relative strength between major currencies

Investment Strategy:

Rising Trend: Indicates increasing global liquidity - favorable for risk assets

Declining Trend: Suggests tightening conditions - defensive positioning recommended

Acceleration/Deceleration: Changes in slope indicate shifting monetary policy

Correlation Analysis: Use time offset to find optimal lead/lag relationships

MVRV V4 - QuantSyMarket Value to Realized Value (MVRV) indicator that identifies accumulation and distribution zones through normalized z-score analysis.

Compares current price to the average cost basis of holders, highlighting when an asset is statistically overvalued or undervalued relative to historical norms.

Features automatic trend signals, multi-phase market detection, and visual zone mapping for timing entries and exits across market cycles.

Best for: Long-term cycle analysis, identifying market extremes

**⚠️ Disclaimer**

Educational tool only - does not constitute investment advice. The developer assumes no liability for any trading profits or losses incurred through the use/misuse of this indicator.

This indicator does not include any features related to interest, leverage, or gambling. Users are fully responsible for making sure their assets and trading practices align with Islamic guidelines.

Nexus cRSI + Energy DynamicsA configurable momentum and cycle-based indicator designed to highlight potential trend shifts, reversals, and divergences. Combines multiple complementary signal types to give traders filtered, actionable insights without relying on raw price alone.

Key Features:

-Holy Nexus Setup: Highlights where the lower band is above 50 and the CRSI breaks the band and the 50 level, and for longs when the upper band is bellow 50 and CRSI breaks above the band and above the 50 level.

-Divergences: Identifies decoupling between price and momentum.

-Momentum Flips: Flags shifts in short-term momentum relative to recent cycles.

-Band Breaks: Marks significant moves outside dynamic reference levels.

- Multi-timeframe Table for Holy Nexus readiness

- Adjustable tolerance for the Holy Nexus and Table

All features are optional and fully customizable, including visual display and alerts. Ideal for traders who want multi-layered guidance while retaining flexibility.

Mayer Mutiple | QRMayer Multiple | QR — Publication Description

What it does

Mayer Multiple | QR is a cycle/valuation style oscillator that measures how far price sits above or below its longer-term average and normalizes that distance by current volatility. It helps you spot overheated extensions and deep discounts relative to trend, with adaptive bands that expand/contract as conditions change.

How it works (principle)

The script compares price to a long lookback moving average (default uses a 200-period average of ohlc4) and turns that gap into an oscillator.

It then computes a rolling standard deviation of that oscillator to build dynamic upper/lower bands (±1σ, ±2σ, ±3σ).

When the oscillator rises above the upper bands, the move is statistically stretched (potential distribution/risk). When it falls below the lower bands, it’s statistically depressed (potential accumulation/opportunity).

A small baseline band around zero (scaled from volatility) provides a quick trend-bias read without crowding the view.

Why this matters: Classic “Mayer Multiple” tools use a fixed threshold over a single moving average. This version is volatility-aware: its bands adapt to the market’s current dispersion, reducing false signals in quiet regimes and avoiding constant “overheat” flags in high-vol regimes.

What you see on the chart

White oscillator line: volatility-normalized deviation from the long-term average.

Adaptive bands:

Upper 1/2/3σ (shaded blue tones) = progressively more extended.

Lower 1/2/3σ (shaded green tones) = progressively more discounted.

Baseline ribbon: subtle band around zero for quick bias.

Background highlights: optional flashes when the oscillator exceeds the ±3σ extremes.

All visuals are generated by this script alone; no other indicator is required to understand usage.

How to use it

Context: Use on higher timeframes to gauge where price sits versus its long-term “fair value corridor.”

Signal reading:

Above +1σ/+2σ/+3σ: extension → consider de-risking, trailing stops, or waiting for mean reversion.

Below −1σ/−2σ/−3σ: discount → consider scaling in, watching for trend resumption cues.

Confluence: Treat it as a condition, not a trigger. Pair with structure (higher highs/lows), breadth, or momentum for entries/exits.

Regime awareness: As volatility rises, bands widen; prioritize trend context over single print extremes.

Inputs you can tune

Color mode: preset palettes for lines/fills/backgrounds.

Dynamic Threshold Length: lookback for the volatility (σ) calculation driving the adaptive bands.

Source: price input used for the long-term reference.

Band toggles: show/hide ±1σ / ±2σ / ±3σ envelopes to reduce clutter.

Originality & value

Adaptive, volatility-aware implementation of a Mayer-style concept: rather than one fixed threshold, it scales to current regime, keeping readings comparable across cycles.

Clear, clean presentation (oscillator + bands + optional background) designed for publication with a clean chart so the script’s output is immediately identifiable.

Offers actionable context (stretch/discount zones) while leaving trade execution to the user’s process.

Limitations & good practices

Best used for context and risk framing, not stand-alone entries.

Adaptive bands depend on the lookback you choose; very short windows can overfit, very long windows can lag.

Extremes can persist in strong trends—don’t fade momentum blindly.

Disclaimer

This tool is for research and education only and not investment advice. Markets involve risk. Past performance does not predict or guarantee future results. Use prudent risk management and test settings on your instruments/timeframes.

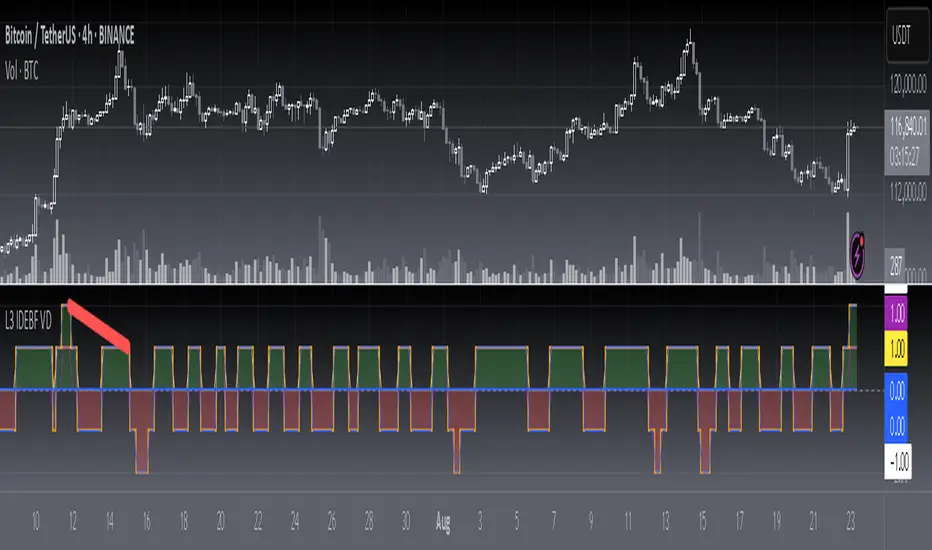

[blackcat] L3 Improved Dual Ehlers BPF for Volatility DetectionOVERVIEW

This script implements an advanced L3 Improved Dual Ehlers Bandpass Filter (BPF) for volatility detection, combining both L1 and L2 calculation methods to create a comprehensive trading signal. The script leverages John Ehlers' sophisticated digital signal processing techniques to identify market cycles and extract meaningful trading signals from price action. By combining multiple cycle detection methods and filtering approaches, it provides traders with a powerful tool for identifying trend changes, momentum shifts, and potential reversal points across various market conditions and timeframes. The L3 approach uniquely combines the outputs of both L1 (01 range) and L2 (-11 range) methods, creating a signal that ranges from -1~2 and provides enhanced sensitivity to market dynamics.

FEATURES

🔄 Dual Calculation Methods: Choose between L1 (01 range), L2 (-11 range), or combine both for L3 signal (-1~2 range) to match your trading style

📊 Multiple Cycle Detection: Seven different dominant cycle calculation methods including HoDyDC (Hilbert Transform Dominant Cycle), PhAcDC (Phase Accumulation Dominant Cycle), DuDiDC (Duane Dominant Cycle), CycPer (Cycle Period), BPZC (Bandpass Zero Crossing), AutoPer (Autocorrelation Period), and DFTDC (Discrete Fourier Transform Dominant Cycle)

🎛️ Flexible Mixing Options: Six sophisticated mixing methods including weighted averaging, simple sum, difference extraction, dominant-only, subdominant-only, and adaptive mixing that adjusts based on signal strength

🌊 Bandpass Filtering: Precise bandwidth control for both dominant and subdominant filters, allowing fine-tuning of frequency response characteristics

📈 Advanced Divergence Detection: Robust algorithm for identifying bullish and bearish divergences with customizable lookback periods and range constraints

🎨 Comprehensive Visualization: Extensive customization options for all signals, colors, plot styles, and display elements

🔔 Comprehensive Alert System: Built-in alerts for divergence signals, zero line crosses, and various market conditions

📊 Real-time Cycle Information: Optional display of dominant and subdominant cycle periods for educational purposes

🔄 Adaptive Signal Processing: Dynamic adjustment of parameters based on market conditions and volatility

🎯 Multiple Signal Outputs: Simultaneous generation of L1, L2, and L3 signals for different trading strategies

HOW TO USE

Select Calculation Method: Choose between "l1" (01 range), "l2" (-11 range), or "both" (L3, -1~2 range) in the Calculation Method settings based on your preferred signal characteristics

Configure Cycle Detection: Select your preferred Dominant Cycle Method from the seven available options and adjust the Cycle Part parameter (0.1-0.9) to fine-tune cycle sensitivity

Set Subdominant Parameters: Configure the subdominant cycle either as a ratio of the dominant cycle or as a fixed period, depending on your analysis approach

Adjust Filter Bandwidth: Fine-tune the bandwidth settings for both dominant and subdominant filters (0.1-1.0) to control the frequency response and signal smoothing

Choose Mixing Method: Select how to combine the filters - weighted averaging for balance, sum for maximum sensitivity, difference for trend isolation, or adaptive mixing for dynamic response

Configure Smoothing: Select from SMA, EMA, or HMA smoothing methods with adjustable length (1-20 bars) to reduce noise in the final signal

Customize Visualization: Enable/disable individual plots, divergence detection, zero line, fill areas, and customize all colors to match your chart preferences

Set Divergence Parameters: Configure lookback ranges (5-60 bars) for divergence detection to match your trading timeframe and style

Monitor Signals: Watch for crosses above/below zero line and divergence patterns, paying attention to signal strength and consistency

Set Up Alerts: Configure alerts for divergence signals, zero line crosses, and other market conditions to stay informed of trading opportunities

LIMITATIONS

The script requires the dc_ta library from blackcat1402 for several advanced cycle calculation methods (HoDyDC, PhAcDC, DuDiDC, CycPer, BPZC, AutoPer, DFTDC)

L1 method operates in 01 range while L2 method uses -11 range, requiring different interpretation approaches

Combined L3 signal ranges from -1~2 when both methods are selected, creating unique signal characteristics that traders must adapt to

Divergence detection accuracy depends on proper lookback period settings and market volatility conditions

Performance may be impacted with very long lookback ranges (>60 bars) or when multiple plots are simultaneously enabled

The script is designed for non-overlay use and may not display correctly on certain chart types or with conflicting indicators

Adaptive mixing method requires careful threshold tuning to avoid excessive signal fluctuation

Cycle detection algorithms may produce unreliable results during low volatility or highly choppy market conditions

The script assumes regular price data and may not perform optimally with irregular or gapped price sequences

NOTES

The script implements advanced mathematical calculations including bandpass filters, Hilbert transforms, and various cycle detection algorithms developed by John Ehlers

For optimal results, experiment with different cycle detection methods and bandwidth settings across various market conditions and timeframes

The adaptive mixing method automatically adjusts weights based on signal strength, providing dynamic response to changing market conditions

Divergence detection works best when the "Plot Divergence" option is enabled and when combined with other technical analysis tools

Zero line crosses can indicate potential trend changes or momentum shifts, especially when confirmed by volume or other indicators

The script includes commented code for cycle information display that can be enabled if you want to monitor cycle periods in real-time

Different calculation methods may perform better in different market environments - L1 tends to be smoother while L2 is more sensitive

The subdominant cycle helps filter out noise and provides additional confirmation for signals generated by the dominant cycle

Bandwidth settings control the filter's frequency response - lower values provide more smoothing while higher values increase sensitivity

Mixing methods offer different approaches to combining signals - weighted averaging is generally most reliable for most trading applications

THANKS

Special thanks to John Ehlers for his pioneering work in cycle analysis and digital signal processing for financial markets. This script implements and significantly improves upon his bandpass filter methodology, incorporating multiple advanced techniques from his extensive body of work. Also heartfelt thanks to blackcat1402 for the dc_ta library that provides essential cycle calculation methods and for maintaining such a valuable resource for the Pine Script community. Additional appreciation to the TradingView platform for providing the tools and environment that make sophisticated technical analysis accessible to traders worldwide. This script represents a collaborative effort in advancing the field of algorithmic trading and technical analysis.

CCI with Subjective NormalizationCCI (Commodity Channel Index) with Subjective Normalization

This indicator computes the classic CCI over a user-defined length, then applies a subjective mean and scale to transform the raw CCI into a pseudo Z‑score range. By adjusting the “Subjective Mean” and “Subjective Scale” inputs, you can shift and rescale the oscillator to highlight significant tops and bottoms more clearly in historical data.

1. CCI Calculation:

- Uses the standard formula \(\text{CCI} = \frac{\text{price} - \text{SMA(price, length)}}{0.015 \times \text{mean deviation}}\) over a user-specified length (default 500 bars).

2. Subjective Normalization:

- After CCI is calculated, it is divided by “Subjective Scale” and offset by “Subjective Mean.”

- This step effectively re-centers and re-scales the oscillator, helping you align major lows or highs at values like –2 or +2 (or any desired range).

3. Usage Tips:

- CCI Length controls how far back the script measures average price and deviation. Larger values emphasize multi-year cycles.

- Subjective Mean and Scale let you align the oscillator’s historical lows and highs with numeric levels you prefer (e.g., near ±2).

- Adjust these parameters to fit your particular market analysis or to match known cycle tops/bottoms.

4. Plot & Zero Line:

- The indicator plots the normalized CCI in yellow, along with a zero line for quick reference.

- Positive values suggest price is above its long-term mean, while negative values suggest it’s below.

This approach offers a straightforward momentum oscillator (CCI) combined with a customizable normalization, making it easier to spot historically significant overbought/oversold conditions without writing complex code yourself.

[blackcat] L2 Ehlers Autocorrelation Periodogram V2OVERVIEW

The Ehlers Autocorrelation Periodogram is a sophisticated technical analysis tool that identifies market cycles and their dominant frequencies using autocorrelation and spectral analysis techniques.

BACKGROUND

Developed by John F. Ehlers and detailed in his book "Cycle Analytics for Traders" (2013), this indicator combines autocorrelation functions with discrete Fourier transforms to extract cyclic information from price data.

FUNCTION

The indicator works through these key steps:

Calculates autocorrelation using minimum three-bar averaging

Applies discrete Fourier transform to extract cyclic information

Uses center-of-gravity algorithm to determine dominant cycle

ADVANTAGES

• Rapid response within half-cycle periods

• Accurate relative cyclic power estimation over time

• Correlation constraints between -1 and +1 eliminate amplitude compensation needs

• High resolution independent of windowing functions

HOW TO USE

Add the indicator to your chart

Adjust AvgLength input parameter:

• Default: 3 bars

• Higher values increase smoothing

• Lower values increase sensitivity

Interpret the results:

• Colored bars represent spectral power

• Red to yellow spectrum indicates cycle strength

• White line shows dominant cycle period

INTERPRETATION

• Strong colors indicate significant cyclic activity

• Sharp color transitions suggest potential cycle changes

• Dominant cycle line helps identify primary market rhythm

LIMITATIONS

• Requires sufficient historical data

• Performance may vary in non-cyclical markets

• Results depend on proper parameter settings

NOTES

• Uses highpass and super smoother filtering techniques

• Spectral estimates are normalized between 0 and 1

• Color intensity varies based on spectral power

THANKS

This implementation is based on Ehlers' original work and has been adapted for TradingView's Pine Script platform.

SW Gann DaysGann pressure days, named after the famous trader W.D. Gann, refer to specific days in a trading month that are believed to have significant market influence. These days are identified based on Gann's theories of astrology, geometry, and market cycles. Here’s a general outline of how they might be understood:

1. **Market Cycles**: Gann believed that markets move in cycles and that certain days can have heightened volatility or trend changes. Traders look for specific dates based on historical price movements.

2. **Timing Indicators**: Pressure days often align with key economic reports, earnings announcements, or geopolitical events that can cause price swings.

3. **Mathematical Patterns**: Gann used angles and geometric patterns to predict price movements, with pressure days potentially aligning with these calculations.

4. **Historical Patterns**: Traders analyze past data to identify dates that historically show strong price reactions, using this to predict future behavior.

5. **Astrological Influences**: Some practitioners incorporate astrological elements, believing that celestial events (like full moons or planetary alignments) can impact market psychology.

Traders might use these concepts to make decisions about entering or exiting positions, but it’s important to note that Gann's methods can be complex and are not universally accepted in trading communities.

Interval & Session Market StatisticsThe "Interval & Session Market Statistics" indicator is designed to uncover recurring patterns and market inefficiencies by analyzing market cycles. By breaking down price movements into defined intervals and sessions, this tool helps traders pinpoint periods of strength and weakness—identifying both bullish and bearish trends with clear percentage breakdowns. Its comprehensive visual tables make it easier to detect accumulation, distribution, and potential turning points, providing valuable insights that can be leveraged to optimize trading strategies.

Important: If the indicator does not reveal a strong bias toward either short or long positions and the statistics hover around 50%, consider reducing the analysis start date and adjusting the end time of the first interval in the settings. Over longer periods, the market tends to revert to a 50/50 balance, so significant deviations are often more visible in weekly or monthly intervals. Since this indicator focuses on intraday cycles, fine-tuning these parameters is crucial for capturing actionable trends.

Индикатор "Interval & Session Market Statistics" разработан для выявления закономерностей и неэффективностей на основе рыночных циклов. Разбивая ценовые движения на заданные интервалы и сессии, инструмент помогает трейдерам определить периоды силы и слабости, выявляя как бычьи, так и медвежьи тренды с наглядным процентным отображением. Подробные таблицы позволяют обнаруживать зоны накопления и распределения, а также потенциальные разворотные моменты, что даёт ценные данные для оптимизации торговых стратегий.

Важно: Если индикатор не выявляет ярко выраженного перекоса в сторону шортового или лонгового приоритета, и статистика колеблется в районе 50%, рекомендуется уменьшить дату начала анализа и поработать с окончанием первого интервала в настройках индикатора. На более длительных периодах рынок обычно стремится к балансу в 50%, поэтому существенные отклонения эффективнее искать в рамках недельных или месячных интервалов. Поскольку данный индикатор ориентирован на внутридневные циклы, корректировка этих параметров имеет решающее значение для выявления значимых трендов.

Retrograde Periods (Multi-Planet)**Retrograde Periods (Multi-Planet) Indicator**

This TradingView script overlays your chart with a dynamic visualization of planetary retrograde periods. Built in Pine Script v6, it computes and displays the retrograde status of eight planets—Mercury, Venus, Mars, Jupiter, Saturn, Uranus, Neptune, and Pluto—using hard-coded retrograde intervals from 2009 to 2026.

**Key Features:**

- Dynamic Background Coloring:

The indicator changes the chart’s background color based on the current retrograde status of the planets. The colors follow a priority order (Mercury > Venus > Mars > Jupiter > Saturn > Uranus > Neptune > Pluto) so that if multiple planets are retrograde simultaneously, the highest-priority planet’s color is displayed.

- Interactive Planet Selection:

User-friendly checkboxes allow you to choose which planets to list in the table’s “Selected” row. Note that while these checkboxes control the display of the planet names in the table, the retrograde calculations remain independent of these selections.

- Real-Time Retrograde Status Table:

A table in the top-right corner displays each planet’s retrograde status in real time. “Yes” is shown in red for a planet in retrograde and “No” in green when it isn’t. This offers an at-a-glance view of the cosmic conditions influencing your charts.

- Astrological & Astronomical Insights:

Whether you’re into sidereal astrology or simply fascinated by celestial mechanics, this script lets you visualize those retrograde cycles. In astrology, retrograde periods are often seen as times for reflection and re-evaluation, while in astronomy they reflect the natural orbital motions seen from our perspective on Earth.

Enhance your trading setup by integrating cosmic cycles into your technical analysis. Happy trading and cosmic exploring!

Time Syndicate: Sweep & ShiftTime Syndicate: Sweep & Shift

The Hierarchy of Time.

Most traders look at price and wonder "where." Time Syndicate asks "when."

This system is a paradigm shift away from lagging indicators. It is built on a proprietary temporal engine that mathematically divides market activity into predictive windows of opportunity. It does not guess; it waits for the market to reveal its hand at specific, algorithmically determined intervals.

Core Capabilities

100% Non-Repainting Logic: Built for professional reliability. Unlike tools that rewrite history to look perfect in hindsight, this strategy features Absolute Signal Permanence. Once a signal is confirmed and the bar closes, it never vanishes or shifts. What you see live is exactly what remains, ensuring that your backtesting reality matches your live execution.

Temporal Segmentation: The indicator ignores noise by isolating price action into a rigid, non-linear time hierarchy. It automatically detects when the market is in a "Reference Phase" versus an "Expansion Phase," keeping you out of the chop and aligning you with institutional volatility.

Algorithmic Bias Detection: Forget drawing manual support and resistance. The system utilizes a dynamic, time-weighted volatility model to determine the immediate directional bias. It identifies exactly when liquidity has been harvested and when the smart money is committing to a direction.

Fractal Confirmation Engine: A bias is nothing without timing. The "Shift" mechanism is a secondary confirmation layer that monitors sub-structural price delivery. It validates that the momentum matches the time cycle, ensuring you only execute when Time, Price, and Structure are in perfect confluence.

Adaptive Cycle Modes: Whether you are positioning for macro moves or scalp executions, the system adapts its internal clock to your objective:

Daily Mode: For capturing significant intraday expansions.

Session (Indian Market): A bespoke calibration tuned specifically to the volatility signature of the Indian trading session.

90-Min (Scalp): High-frequency cycle detection for rapid precision plays.

Discipline Protocols: Built-in execution filters prevent over-trading by locking signals once a cycle objective is met. This enforces a "sniper" mentality—one trigger, one cycle, zero noise.

Stop chasing candles. Start trading Time.

TOTAL3ES/ETH Mean ReversionTOTAL3ES/ETH Mean Reversion Indicator

Overview

The TOTAL3ES/ETH Mean Reversion indicator is a specialized tool designed exclusively for analyzing the ratio between TOTAL3 excluding stablecoins (TOTAL3ES) and Ethereum's market capitalization. This ratio provides crucial insights into the relative performance and valuation cycles between altcoins and ETH, making it an essential tool for cryptocurrency portfolio allocation and market timing decisions.

What This Indicator Measures

This indicator tracks the market cap ratio of all altcoins (excluding ETH and stablecoins) to Ethereum's market cap. When the ratio is:

Above 1.0 (Parity): Altcoins have a larger combined market cap than ETH

Below 1.0 (Parity): ETH's market cap exceeds the combined altcoin market cap

Key Features

Historical Context

Historical Range: 0.64 (July 2017 low) to 3.49 (all-time high)

Midpoint: 2.065 - the mathematical center of the historical range

Parity Line: 1.0 - the psychological level where altcoins = ETH market cap

Mean Reversion Zones

The indicator identifies extreme valuation zones based on historical data:

Upper Extreme Zone (~2.92 at 80% threshold): Suggests altcoins may be overvalued relative to ETH

Lower Extreme Zone (~1.21 at 80% threshold): Suggests altcoins may be undervalued relative to ETH

Visual Elements

Color-coded zones: Red shading for bearish reversion areas, green for bullish reversion areas

Multiple reference lines: Parity, midpoint, and historical extremes

Information table: Real-time metrics including current ratio, range position, and reversion pressure

Customizable display: Toggle zones, lines, and adjust transparency

How to Use This Indicator

Market Cycle Analysis

Extreme High Zone (Red): When ratio enters this zone, consider potential ETH outperformance

Extreme Low Zone (Green): When ratio enters this zone, consider potential altcoin season

Parity Crossovers: Monitor when ratio crosses above/below 1.0 for sentiment shifts

Portfolio Allocation Signals

High Ratio Values: May indicate overextended altcoin valuations relative to ETH

Low Ratio Values: May suggest undervalued altcoins relative to ETH

Midpoint Reversions: Historical tendency to revert toward the 2.065 midpoint

Alert Conditions

The indicator includes built-in alerts for:

Entering extreme high/low zones

Parity crossovers (above/below 1.0)

Mean reversion signals

Input Parameters

Display Settings

Show Reversion Zones: Toggle colored extreme zones on/off

Show Midpoint: Display the historical midpoint line

Show Parity Line: Show the 1.0 parity reference line

Zone Transparency: Adjust shaded area opacity (70-95%)

Calculation Settings

Reversion Strength Period: Moving average period for reversion calculations (10-50)

Extreme Threshold: Percentage of historical range defining extreme zones (0.5-1.0)

Information Table Metrics

The bottom-right table displays:

Current Ratio: Live TOTAL3ES/ETH value

Range Position: Current position within historical range (%)

From Parity: Distance from 1.0 parity level (%)

Reversion Pressure: Intensity of mean reversion forces (%)

Zone: Current market zone classification

Historical Range: Reference boundaries (0.64 - 3.49)

Midpoint: Historical center value

Important Notes

Chart Compatibility

Exclusively designed for CRYPTOCAP:TOTAL3ES/CRYPTOCAP:ETH

Built-in validation ensures proper chart usage

Will display error message if applied to incorrect charts

Trading Considerations

This is an analytical tool, not trading advice

Mean reversion is a tendency, not a guarantee

Consider multiple timeframes and confirmations

Factor in overall market conditions and trends

Risk Disclaimer

Past performance does not guarantee future results. Cryptocurrency markets are highly volatile and unpredictable. Always conduct your own research and consider your risk tolerance before making investment decisions.

Ideal Use Cases

Portfolio rebalancing between ETH and altcoins

Market cycle timing for position adjustments

Sentiment analysis of crypto market phases

Long-term allocation strategies based on historical patterns

Risk management through extreme zone identification

This indicator serves as a quantitative framework for understanding the cyclical relationship between Ethereum and the broader altcoin market, helping traders and investors make more informed allocation decisions based on historical valuation patterns.ons

- Factor in overall market conditions and trends

### Risk Disclaimer

Past performance does not guarantee future results. Cryptocurrency markets are highly volatile and unpredictable. Always conduct your own research and consider your risk tolerance before making investment decisions.

cycle144 dr ramy After Given Date📌 Description for Script Publishing

Cycle144 dr ramy After Given Date is a visual tool that highlights time-based cycles on the chart by marking specific candles that occur after a user-defined starting point.

🔹 How It Works:

You choose a specific date and time.

The script automatically identifies and labels the 18th, 36th, 54th, 72nd, 90th, 108th, 126th, and 144th candles after your selected date.

At each of those candles, the script:

Places a label (e.g., "18th Candle", "36th Candle", etc.).

Draws horizontal lines from the candle's high and low, extended to the right.

🔹 Purpose:

This indicator helps traders observe and analyze market behavior at regular cycle intervals after a significant date. It's useful for cycle-based strategies, time symmetry analysis, or just to visualize how price reacts at recurring time steps.

🛠️ No signals or strategies are included — this is a charting utility only.

Gann & Fibonacci Analysis for MSTRYes! Below is a step-by-step guide to performing Gann Analysis on MSTR in TradingView for the last year.

Step 1: Set Up the Chart

Open TradingView and search for MSTR (MicroStrategy).

Select the 1-day (D) timeframe to analyze the past year.

Set your chart to logarithmic scale (⚙ Settings → Scale → Log).

Enable grid lines for alignment (⚙ Settings → Appearance → Grid Lines).

Step 2: Identify Key Highs and Lows (Last Year)

Find the 52-week high and 52-week low for MSTR.

As of now:

52-Week High: ~$999 (March 2024).

52-Week Low: ~$280 (October 2023).

Step 3: Plot Gann Angles

Using TradingView's Gann Fan Tool:

Select "Gann Fan" (Press / and type “Gann Fan” to find it).

Start at the 52-week low (~$280, October 2023) and drag upwards.

Adjust the angles to match key levels:

1x1 (45°) → Main trendline

2x1 (26.5°) → Strong uptrend

4x1 (15°) → Weak trendline

1x2 (63.75°) → Strong resistance

Repeat the process from the 52-week high (~$999, March 2024) downward to see bearish angles.

Step 4: Apply Fibonacci & Gann Retracement Levels

Using Fibonacci Retracement:

Select "Fibonacci Retracement" tool.

Draw from 52-week high ($999) to 52-week low ($280).

Enable key Fibonacci levels:

23.6% ($816)

38.2% ($678)

50% ($640)

61.8% ($550)

78.6% ($430)

Watch for price reactions near these levels.

Using Gann Retracement Levels:

Select "Gann Box" in TradingView.

Draw from 52-week high ($999) to low ($280).

Enable key Gann retracement levels:

12.5% ($912)

25% ($850)

37.5% ($768)

50% ($640)

62.5% ($550)

75% ($480)

87.5% ($350)

Identify confluences with Gann angles and Fibonacci levels.

Step 5: Identify Significant Dates & Time Cycles

Use "Date Range" Tool in TradingView.

Mark major turning points:

High → Low: ~180 days (Half-year cycle).

Low → High: ~90 days (Quarter cycle).

Use Square-Outs (Time = Price method):

Example: If MSTR hit $500, check 500 days from key events.

Mark key anniversaries of past highs/lows for possible reversals.

Step 6: Analyze and Trade Execution

✅ If MSTR is at a Gann angle + Fibonacci level + key date → Expect a reaction.

✅ Use RSI, MACD, and Volume for extra confirmation.

✅ Set Stop-Loss at nearest Gann support/resistance.

Dominant Direction (DD)The Dominant Direction indicator is a custom technical analysis tool that uses the Dominant Cycle Estimators library to identify the dominant trend direction in the market. The indicator utilizes the MAMA Cycle function, which is a part of the library, to calculate the period of the data. The resulting period is then used to plot lines on the chart that represent the dominant trend direction.

The indicator takes two inputs, the source of data, and the high and low values of the source. The MAMA Cycle function is used to calculate the period of the data, with the lower bound and upper bound of the dynamic length defined by the user. The indicator then plots lines on the chart to represent the dominant trend direction. The lines are plotted from the current bar to the bar that is a certain number of periods away, as defined by the MAMA Cycle function, in the direction of the trend.

The indicator also has a feature of removing the lines when the trend is no longer confirmed. If the bar state is confirmed, the line is deleted and this helps the user to have a clearer view of the chart.

In summary, the Dominant Direction indicator is a powerful tool for identifying the dominant trend direction in the market. It uses the MAMA Cycle function to calculate the period of the data and plots lines on the chart to represent the dominant trend direction. This can help traders identify potential entry and exit points, and make more informed trading decisions.

週一普跌策略 Monday shit Strategy Strategy Description / 策略敘述

EN

This strategy takes a short position at the start of each Monday, based on the hypothesis that cryptocurrency markets tend to experience post-weekend risk-off behavior.

The system enters a full-equity short position at the Tokyo open (Taipei 08:00), aiming to capture Monday downside pressure resulting from accumulated weekend information and macro sentiment adjustments when traditional financial markets reopen.

Risk management uses fixed percentage take-profit and stop-loss levels, emphasizing asymmetric reward-to-risk (large occasional gains, small frequent losses).

The model reflects the increasing alignment between crypto price behavior and traditional financial market cycles.

ZH-TW

本策略於每週一開盤時做空,基於假設加密資產在週末後具有風險釋放與補跌傾向。

系統會在台北時間早上 08:00 以全倉做空,目標捕捉因週末累積消息與傳統金融市場重新開盤所造成的下跌壓力。

風控採固定止盈、止損百分比,強調高報酬/低風險的不對稱結構(小虧多次、偶爾大賺)。

此模型反映加密貨幣市場行為與華爾街週期愈趨一致的市場現象。

IPDA TIMES GWU369Between 2:30 AM and 16:00 PM NY occur 270 where the hours or the sum of the hours plus the minutes generate a sequence of 3,6 or 9. Examples: 03:00, 09:30. 04:20= 0+4+2+0=6, 07:05=0+7+5+0=12 12= 1+2=3 etc.

And between each opening and closing, a range is generated that dictates the OF of the next range and is how the timed price is delivered by time cycles.

This is how you can detect when an SMR or CSD will occur very accurately.

Earnings Season Highlighter (Jan/Apr/Jul/Oct)Purpose:

This indicator visually highlights the four “earnings season” months — January, April, July, and October — on any TradingView chart. It is designed for traders and investors who want a quick visual cue of when companies typically report quarterly earnings.

Features:

Highlights Jan, Apr, Jul, and Oct with a light blue background.

Works on any timeframe: intraday, daily, weekly, or monthly charts.

No dependency on price data — purely a time-based visual overlay.

Simple, lightweight, and easy to apply to any chart.

Usage:

Apply the indicator to your chart.

During the highlighted months, the background will turn light blue, signaling earnings season.

Ideal for planning trades, earnings plays, or simply monitoring market cycles.

Trading Sessions with Holidays & Timer🌍 Trading Sessions Matter

Markets breathe in cycles. When Tokyo, London, or New York steps in, liquidity shifts and price often reacts fast.

Example: New York closed BTC at $110K, and when traders woke up, the price was already $113K. That gap says everything about overnight pressure and the next move.

⚡ Indicator Features

✅ Session boxes (Tokyo, London, NY) with custom colors & time zones

✅ Open/close lines → spot gaps & momentum

✅ Average price per session → see where pressure builds

✅ Tick range → quick volatility check

✅ 🏖 Holiday markers → avoid false quiet markets

✅ Live status table → session OPEN / CLOSED + countdown timer

🚀 How to Use

Works on intraday timeframes (1m–4h)

Watch session opens/closes → liquidity shift points

Compare ranges & averages between Tokyo, London, NY

Use the timer to prep before the next wave

This tool helps you visualize the heartbeat of global markets session by session.

🔖 #BTCUSDT #Forex #TradingSessions #Crypto #DayTrading

True Open CalculationsIndicator Description: True Open Calculations

This custom Pine Script indicator calculates and plots key "True Open" levels based on specific time intervals and trading sessions. The True Open levels represent significant price points on the chart, helping traders identify key reference points tied to various market opening times. These levels are important for understanding price action in relation to market sessions and trading cycles. The indicator is designed to plot lines corresponding to different "True Opens" on the chart and display labels with the associated information.

Key Features:

True Year Open:

This represents the opening price on the first Monday of April each year. It serves as a reference point for the yearly price level.

Plot Color: Green.

True Month Open:

This represents the opening price on the second Monday of each month. It helps in identifying monthly trends and provides a key reference for monthly price movements.

Plot Color: Blue.

True Week Open:

This represents the opening price every Monday at 6:00 PM. It gives traders a level to track weekly opening movements and can be useful for weekly trend analysis.

Plot Color: Orange.

True Day Open:

This represents the opening price at 12:00 AM (midnight) each day. It serves as a daily benchmark for price action at the start of the trading day.

Plot Color: Red.

True New York Session Open:

This represents the opening price at 7:30 AM (New York session start time). This level is crucial for traders focused on the New York trading session.

Plot Color: Purple.

Additional Features:

Labels: The indicator displays labels to the right of each plotted line to describe which "True Open" it represents (e.g., "True Year Open," "True Month Open," etc.).

Dynamic Plotting: The lines are only plotted on the current candle, and the lines are dynamically updated for each time period based on the corresponding "True Open."

Visual Cues: The colors of the plotted lines (green, blue, orange, red, purple) help quickly distinguish between different "True Open" levels, making it easy for traders to track price action and make informed decisions.

Use Cases:

Yearly, Monthly, Weekly, Daily, and Session Benchmarking: This indicator provides traders with important price levels to use as benchmarks for the current year, month, week, and day, helping to identify trends and potential reversals.

Session Awareness: It is particularly useful for traders who want to track key market sessions, such as the New York session, and their impact on price movement.

Long-term Analysis: By including the yearly open, this indicator helps traders gain a broader perspective on market trends and provides context for analyzing shorter-term price movements.

Benefits:

Helps identify important reference points for longer-term trends (yearly, monthly) as well as shorter-term moves (daily, weekly, and session).

Visually intuitive with color-coded lines and labels, allowing quick and easy identification of key market open levels.

Dynamic and real-time: The indicator plots and updates the True Open levels dynamically as the market progresses.

Trading Sessions Highs/Lows | InvrsROBINHOODTrading Sessions Highs/Lows | InvrsROBINHOOD

🚀 A powerful indicator for tracking key trading sessions and the highs and lows of each session!

📌 Description

The Trading Sessions Highs/Lows indicator visually marks the most critical trading sessions—Asia, London, and New York—using small colored dots at the bottom of the candle. It also tracks and plots the highs and lows of each session, along with the Daily Open and Weekly Open levels.

This tool is designed to help traders identify session-based liquidity zones, price reactions, and potential trade setups with minimal chart clutter.

Key Features:

✅ Session markers (Asia, London, NY AM, NY Lunch, NY PM) plotted as small dots

✅ Plots session highs and lows for market structure insights

✅ Daily Open line for intraday reference

✅ Weekly Open line for higher timeframe bias

✅ Alerts for session high/low breaks to capture momentum shifts

✅ User-defined UTC offset for global traders

✅ Customizable session colors for personal preference

📖 How to Use the Indicator

1️⃣ Understanding the Sessions

Asia Session (Yellow Dot) → Marks liquidity buildup & pre-London moves

London Session (Blue Dot) → Strong volatility, breakout opportunities

New York AM Session (Green Dot) → Major trends & institutional participation

New York Lunch (Red Dot) → Low volume, ranging market

New York PM Session (Dark Green Dot) → End-of-day movements & reversals

2️⃣ Session Highs & Lows for Market Structure

Session Highs can act as resistance or breakout points.

Session Lows can act as support or stop-hunt zones.

Break of a session high/low with volume may indicate continuation or reversal.

3️⃣ Using the Daily & Weekly Open

The Daily Open (Black Line) helps gauge the intraday trend.

Above Daily Open → Bearish Bias

Below Daily Open → Bullish Bias

The Weekly Open (Red Line) sets the higher timeframe directional bias.

4️⃣ Alerts for Breakouts

The indicator will trigger alerts when price breaks session highs or lows.

Useful for setting stop-losses, breakout trades, and risk management.

💡 Why This Indicator is Important for Beginners

1️⃣ Avoids Overtrading:

Many beginners trade in low-volume periods (NY Lunch, Asia session) and get stuck in choppy price action.

This indicator highlights when volatility is high so traders focus on better opportunities.

2️⃣ Session-Based Liquidity Traps:

Market makers often run stops at session highs/lows before reversing.

Watching session breaks prevents traders from falling into liquidity grabs.

3️⃣ Reduces Emotional Trading:

If price is above the Daily Open, a beginner shouldn’t look for shorts.

If price is below a key session low, it may signal a fake breakout.

4️⃣ Aligns with Institutional Trading:

Smart money traders use session highs/lows to set stop hunts & reversals.

Beginners can use this indicator to spot these zones before entering trades.

🛡️ How to Mitigate Risk with This Indicator

✅ Wait for Confirmations – Don’t trade blindly at session highs/lows. Look for wicks, rejections, or break/retests.

✅ Use Stop-Loss Above/Below Session Levels – If you’re going long, set SL below a session low. If short, set SL above a session high.

✅ Watch Volume & News Events – Breakouts without strong volume or news may be fake moves.

✅ Combine with Other Strategies – Use price action, trendlines, or EMAs with this indicator for higher probability trades.

✅ Use the Weekly Open for Trend Bias – If price stays below the Weekly Open, avoid bullish setups unless key support holds.

🎯 Who is This Indicator For?

📌 Beginners who need clear session-based trading levels.

📌 Day traders & scalpers looking to refine their intraday setups.

📌 Smart money traders using liquidity concepts.

📌 Swing traders tracking higher timeframe momentum shifts.

🚀 Final Thoughts

This indicator is an essential tool for traders who want to understand market structure, liquidity, and volatility cycles. Whether you’re trading forex, stocks, or crypto, it helps you stay on the right side of the market and avoid unnecessary risks.

🔹 Set it up, customize your colors, define your UTC offset, and start trading smarter today! 🏆📈

Yearly Profit BackgroundDescription:

The Yearly Profit Background indicator is a powerful tool designed to help traders quickly visualize the profitability of each calendar year on their charts. By analyzing the annual performance of an asset, this indicator colors the background of each completed year green if the year was profitable (close > open) or red if it resulted in a loss (close < open). This visual representation allows traders to identify long-term trends and historical performance at a glance.

Key Features:

Annual Profit Calculation: Automatically calculates the yearly performance based on the opening price of January 1st and the closing price of December 31st.

Visual Background Coloring: Highlights each completed year with a green (profit) or red (loss) background, making it easy to spot trends.

Customizable Transparency: The background colors are set at 90% transparency, ensuring they don’t obstruct your chart analysis.

Optional Price Plots: Displays the annual opening (blue line) and closing (orange line) prices for additional context.

How to Use:

Add the indicator to your chart.

Observe the background colors for each completed year:

Green: The year was profitable.

Red: The year resulted in a loss.

Use the optional price plots to analyze annual opening and closing levels.

Ideal For:

Long-term investors analyzing historical performance.

Traders looking to identify multi-year trends.

Anyone interested in visualizing annual market cycles.

Why Use This Indicator?

Understanding the annual performance of an asset is crucial for making informed trading decisions. The Yearly Profit Background indicator simplifies this process by providing a clear, visual representation of yearly profitability, helping you spot patterns and trends that might otherwise go unnoticed.