Price Forecast - Future price Ichimoku ATR RSI Kumo It predicts

Future price (projected close)

future high-low (ATR projection)

Ichimoku Future Span overlay

alerts "future price above/below threshold".

Ichimoku Kumo Projection (Leading Span A & B). Senkou Span A (Future A) Senkou Span B (Future B).

ATR Projection Channel (ATR Bands/Volatility Forecast).

Linear regression forecast for +1 bar.

Multi timeframe

RSI+Kumo filter for clearer signals.

Forecasting

Precious Matrix Signal-S-L15-sum⭐ PRECIOUS MATRIX SIGNAL™

Today Range + R1–R6 Multi-Layer Market Structure Engine

Final Output → 🔵 BUY | 🔴 SELL | ⏹ NEUTRAL

A powerful, multi-range decision engine that reads today’s live structure and compares it with six major past ranges, Δ/E shifts, and daily strength summaries to generate a precise directional signal.

📘 What This Indicator Does

This indicator builds a complete price-behavior matrix combining:

🔹 Today’s High–Low structure

🔹 Six custom historical ranges (R1–R6)

🔹 Live Δ/E trend shifts

🔹 A/R (Above–Below Range) positioning

🔹 Remaining Potential %

🔹 Last-5, Last-10, Last-15 day trend summary

🔹 Auto Spot–Future selection

🔹 Lot size & Margin info

( Not for dark mode &only on NSE Futures & Spot )

All layers combine to produce a single actionable signal.

🔶 How It Works (Simple Flow)

1️⃣ Symbol Auto-Detection

If chart is futures, uses futures data

If futures range missing → switches to continuous 1!

If chart is spot, uses spot cleanly

Auto-reads lot size and margin

2️⃣ Today’s Live Range Engine

Live High / Low

Time of High & Low

Δ (Range size)

A/R (Where current price sits inside the range)

Remaining Potential % (powerful continuation measure)

3️⃣ R1–R6 Custom Range Engine

Each user-set range displays:

High & Low

Δ

A/R positioning

Remaining Potential %

Overshoot/Breakdown markers

Δ/E (Direction shift)

Color-coded range strength

4️⃣ Δ/E Shift Logic (Live Mode)

For each R1–R6:

Prev = previous close before the range

E = end-close of the range

Δ/E = Direction:

▲ Positive → Bullish

▼ Negative → Bearish

■ Neutral → Sideways

If the range ends today → uses intraday close (E*).

5️⃣ Trend Validation (Last-5 / 10 / 15 Days)

Automatic summary tables:

Daily Date

Close

H/L

Δ

A/R

Net Trend Color

Strongest zone marked

This prevents false signals and confirms bias.

6️⃣ Final Signal Engine

Uses a weighted scoring across:

Today’s bias

R1–R6 bias

Δ/E direction

Remaining potential

Last-5/10/15 confirmation

🔵 BUY

→ Majority Ranges UP

→ Today’s structure UP

→ Δ/E = ▲

→ Last-5 positive

🔴 SELL

→ Majority Ranges DOWN

→ Today’s structure DOWN

→ Δ/E = ▼

→ Last-5 negative

⏹ NEUTRAL

→ Mixed or no clear dominance

→ Low potential/compressed price

📊 Dashboard Panels

Panel 1 – Today + R1–R6 Master Matrix

Shows:

H / L / Δ

A/R

Remaining Potential %

Δ/E (live option)

Range badges & colors

Panel 2 – Last-5 / 10 / 15 Summary

Your secondary confirmation panel.

Panel 3 – Lot Size + Margin

Auto margin estimate at 24%.

⚙️ Input Controls

Show/Hide HLX Panel

Custom Range Start/End

Δ/E Live Override

Force Intraday Mode

Last-5/10/15 Selector ( last work properly display on mobile )

Nudge (Panel Offset)

Potential % thresholds

Designed to adjust smoothly for all timeframes.

🎯 Recommended Usage

Use on 3m / 5m / 15m / 30m / 1H / 2H / 4H

Works great on Index Futures, Stock Futures, and Spot

Keep Option-2 Δ/E enabled for live trading

Last-5 and R2–R6 give strongest confirmation for trend days

📈 Who Is This For?

Traders who want:

Multi-range professional context

Reliable bias confirmation

High-probability directional entries

Auto-range intelligence without manual marking

Futures–spot multi-engine precision

🟢 SUPER-SIMPLE FLOWCHART

START

|

Detect Spot/Future + Lot

|

Compute TODAY H/L

|

Compute R1–R6 Ranges

|

Apply Δ/E Live Logic

|

Build Range Strength Score

|

Build Last5/10/15 Trend

|

Combine All Scores (matrix)

|

BUY ? SELL ? NEUTRAL ?

|

Display Full Dashboard

🛑 Disclaimer

This is an educational tool.

No buy/sell recommendations.

Always use proper risk management.

Bollinger Bands SMThis script plots four custom Bollinger Band envelopes on price to map volatility, trend and extremes on a single chart.

What it shows

BB Set 1 – 50-length, 1.25σ (cyan/red)

Short–to–medium-term volatility channel. Good for spotting squeezes, early breakouts and pullbacks in the active trend.

BB Set 2 – 200-length, 1.25σ (lime/yellow)

Higher-timeframe “trend envelope”. When price rides the upper band the trend is strong; closes below the lower band often signal deeper corrections.

BB Set 3 – 14-length, 3.2σ (white/blue, green fill)

Fast, very wide band for short-term volatility spikes. Tags of these outer bands highlight overextended moves that often mean-revert.

BB Set 4 – 200-length, 5σ (white/red, purple fill)

Extreme long-term volatility boundary. Price reaching this zone is rare and can mark exhaustion, blow-off moves or panic washes.

How I use it

Look for squeezes where bands contract tightly before large moves.

Watch for confluence when multiple bands line up as support/resistance.

Treat outer band touches as risk zones, not automatic reversal signals – wait for confirmation from structure or your own system.

This is a visual tool to understand volatility and trend context, not a standalone buy/sell system and not financial advice.

Vassago & Tesla Ex-Machina 197 45 21 [Hakan Yorganci]Vassago & Tesla Ex-Machina 197 45 21

"Any sufficiently advanced technology is indistinguishable from magic." — Arthur C. Clarke

🌑 The Genesis: Algorithmic Esotericism

This script is not merely a technical indicator; it is a digital artifact born from the convergence of Software Engineering and Hermetic Tradition.

As a developer and researcher dedicated to "Technomancy"—the study of applying esoteric logic to computational systems—I designed this algorithm using a custom, experimental programming environment I am currently developing. My goal was to move beyond standard, arbitrary financial inputs (like the default 200 SMA or 14 RSI) and instead derive parameters based on Universal Harmonics and Historical Archetypes.

This indicator, Ex-Machina, is the result of that transmutation. It applies ancient numeric precision to modern market chaos.

🔢 Decoding the Protocol: 197 - 45 - 21

Why these specific numbers? They were not chosen randomly; they were calculated through specific harmonic reductions to filter out market noise.

1. The Harmonic Trend (Tesla Protocol)

* The Logic: Standard analysis uses the 200-period Moving Average simply out of habit. However, applying Nikola Tesla’s 3-6-9 vibrational principles, the engine reduced the period to 197.

* The Numerology: 1+9+7 = 17 \rightarrow 1+7 = \mathbf{8}. In esoteric numerology, 8 represents infinite power, authority, and financial flow. This creates a baseline that aligns more organically with market accumulation than the static 200.

2. The Hidden Dip (Solomonic Sight)

* The Archetype: Based on the attributes of Vassago, the archetype of discovering "hidden things," the algorithm identified 45 as the precise threshold for a "Sniper Entry."

* The Function: Unlike the standard 30 RSI, this level identifies the exact moment a correction matures within a bullish trend—catching the dip before the crowd returns.

3. The Prophetic Vision

* The Logic: Using the Fibonacci Sequence, the indicator projects the support line 21 bars into the future.

* The Utility: This allows you to visualize where the support will be, granting you foresight before price action arrives.

⚖️ The Dual Mode Engine: Sealed vs. Living

Respecting the user's will, I have engineered this script as a Hybrid System. You can choose how the "spirit" of the code interacts with the market via the settings menu.

1. The Sealed Ritual (Default - Unchecked)

* Philosophy: "Trust in the Constants."

* Behavior: Strictly adheres to the 197 SMA and 45 RSI.

* Visual: Displays a Blue Trend Line.

* Best For: Traders who value stability, long-term trends, and the unyielding nature of harmonic mathematics.

2. The Living Spirit (Adaptive Mode - Checked)

* Philosophy: "As the market breathes, so does the code."

* Behavior:

* Transmutation: The trend line shifts from a Simple Moving Average (SMA) to an Exponential Moving Average (EMA 197) for faster reaction.

* Adaptive Volatility: The RSI entry level (45) becomes dynamic. It expands and contracts based on ATR (Average True Range). In high volatility, it demands a deeper dip to trigger a signal, protecting you from fake-outs.

* Visual: Displays a Fuchsia (Pink) Trend Line.

* Best For: Volatile markets (Crypto/Forex) and traders who want the algorithm to "sense" the fear and greed in the air.

⚙️ How to Trade

* Timeframe: Optimized for 4H (The Builder) and 1D (The Architect).

* The Signal: Wait for the "EX-MACHINA ENTRY" label. This signal manifests ONLY when:

* Price is holding above the 197 Harmonic Trend.

* Momentum crosses the Optimized Threshold (45 or Adaptive).

* Trend Strength is confirmed via ADX.

Author's Note:

I built this tool for those who understand that code is the modern spellbook. Use it wisely, risk responsibly, and let the harmonics guide your entries.

— Hakan Yorganci

Technomancer & Full Stack Developer

Opening Range ICT 3-Bar FVG + Engulfing Signals (Overlay)Beta testing

open range break out and retest of FVG.

Still working on making it accurate so bear with me

Grok Gold Master 2025Grok Gold Master 2025 – Full Indicator Description Always & Forever Free, only for self use only

(TradingView Pine Script v6 – specially built for XAUUSD / Gold)

This is a clean, professional, all-in-one Gold trading indicator designed for swing/day traders who want clear institutional-style levels, bias confirmation, and visual structure on the chart.

Core Purpose

Help you trade Gold (XAUUSD) with a high-probability bullish bias when price is above key levels, using a simple but powerful “3-zone” framework:

- Support (demand zone)

- Buy Zone (the sweet spot where you actually want to go long)

- Resistance (supply zone)

Main Visual Elements on the Chart

1. **Daily Range Box**

- A semi-transparent green box that covers the entire trading day from Support to Resistance

- Automatically refreshes every new day without any “future leak” errors

- Gives instant context of the current daily range

2. **Three Horizontal Levels (always visible)**

**

- Support → dashed lime line (default 4114)

- Buy Zone → thick solid yellow line (default 4180) ← your main long trigger level

- Resistance → dashed red line (default 4314)

3. **Zone Fills**

- Yellow fill between Support ↔ Buy Zone (caution/neutral area)

Green fill between Buy Zone ↔ Resistance (bullish control area)

4. **4-hour EMA 50 (thick dodger blue line)**

- Pulled from the 4H timeframe (multi-timeframe)

- Acts as dynamic trend filter

5. **Entry Signals**

- Big green “LONG” label + arrow appears only the first bar when:

close > Buy Zone AND close > 4H EMA 50

- Optional green triangles below bars when there is also high volume confirmation (volume > 1.5× 20-period average)

6. **Info Panel (top-right mini table + big label)**

Shows current values for:

- Support / Buy Zone / Resistance

- Current 4H EMA 50

- Live BIAS: “BULLISH – LONG ✅” (green) or “NEUTRAL – WAIT ⏸️” (gray)

Key Logic & Rules Built Into the Indicator

Bullish / Long condition (all must be true):

- Price closes above the Buy Zone level

- Price closes above the 4-hour EMA 50

When both are satisfied → entire info label turns green and says “BULLISH – LONG ✅”

If not → stays neutral/gray and tells you to wait.

Customization Options (Inputs)

- Show/hide the big info label

- Show/hide high-volume confirmation triangles

- Use Dynamic Levels → turn on to manually override the three levels with your own values (very useful when Gold breaks to new all-time highs or you spot new initiation levels)

Why This Indicator Feels “Institutional”

- Clean three-zone structure (exactly how smart money & banks draw their levels)

- Daily range box gives perfect context

- Multi-timeframe trend filter (4H EMA50)

- Volume spike confirmation option

- No repainting, no future leaks

- Instant visual bias at a glance

Best Used On

- XAUUSD (Gold) on 5m, 15m, 1H or 4H charts

- Works beautifully in both ranging and trending markets

In short: “Grok Gold Master 2025” is your 2025-2026 Gold trading dashboard — it tells you exactly where the important levels are, when the trend is truly bullish, and when to press the long button with confidence.

Just add it to your chart and you’ll immediately see why many Gold traders already using almost this exact setup. Now it’s packaged, automated, and looks gorgeous.

Next Candle Probability (EB, EWMA, Regime)Purpose

This indicator provides a quantitative assist to day traders by estimating the probability that the next candle will close green or red.

It analyzes recent red/green sequences across pattern depths N = 1…7 and produces a unified probability score.

By understanding which side has statistically higher likelihood, traders can align their decision-making with dominant directional bias rather than emotion.

Methodology

Strict no-lookahead logic (no repaint, doji filtered out)

Hierarchical smoothing across depths (1 → 7) using empirical-frequency regularization

Optional exponential decay (EWMA) for adaptive weighting toward recent market behavior

Higher-timeframe EMA regime filter (trend-aligned / countertrend-blocked / off)

ALL / SELECTED scope modes with a single, consolidated decision per bar

On-chart informational tags showing raw frequency (“R”) and smoothed estimate (“E”)

Full alert support for directional probability shifts

How it helps day traders

The indicator highlights whether the next bar’s probability distribution favors the bullish or bearish side.

This supports decision-making that is aligned with:

recent statistical behavior,

trend direction,

and adaptive weighting of market conditions.

It is designed for traders who want a structured, probability-based confirmation rather than relying on subjective interpretation.

Research & Theory

This script is based on:

empirical pattern-frequency modeling,

hierarchical Bayesian-style smoothing,

and regime filtering through higher-timeframe trend structure.

OXE MTF Support/Resistance+Demand/Supply Zone ArsenalOXE MTF Support/Resistance + Demand/Supply Zones Indicator

Your Complete Multi-Timeframe Zone Arsenal

This professional-grade indicator transforms your chart into a zone confluence powerhouse, simultaneously tracking high-probability price reaction areas across 5 timeframes (Daily, H4, H1, M15, M5) – giving you the institutional edge you need to dominate the markets.

🎯 What It Is

A sophisticated dual-system zone detector that identifies both:

Classic Support/Resistance levels using pivot point detection

Smart Money Demand/Supply zones triggered by Break-of-Structure (BOS) confirmations

Unlike basic S/R indicators, this tool employs institutional methodology – capturing order blocks and imbalance zones where smart money is positioned, not just where price bounced.

⚡ Core Capabilities

Multi-Timeframe Mastery

Track up to 5 timeframes simultaneously without switching charts

Identify confluence zones where multiple timeframe levels align

Customize which timeframes to display for clean, focused analysis

Intelligent Zone Management

Automatic zone validation – tracks when zones flip from resistance→support or supply→demand

Invalid zone filtering – hide broken/invalidated zones to focus only on active opportunities

Configurable zone limits – control the number of zones per timeframe (up to 8 each)

Smart Money Detection

BOS-confirmed zones – only marks demand/supply after break-of-structure confirmation

Precise zone timing – captures the exact candle that created the imbalance

Visual differentiation – dashed borders distinguish demand/supply from traditional S/R

Professional Dashboard

Real-time zone counter – shows active zones per timeframe at a glance

Filter status indicators – tracks which validation filters are enabled

Color-coded timeframe labels – instant visual organization

💰 How This Transforms Your Trading

1. Find High-Probability Entries

Enter trades at zones where multiple timeframes converge – when H4 demand aligns with Daily support, you've found institutional backing.

2. Stay on the Right Side of the Market

The zone flipping system shows you when market structure changes – a supply zone that flips to demand tells you the narrative has shifted bullish.

3. Eliminate Guesswork

No more wondering "is this level still valid?" The automatic invalidation tracking removes subjectivity – zones are either active (tradeable) or broken (ignored).

4. Scale Your Timeframe Analysis

Whether you're scalping M5 or swing trading Daily, access all relevant zones without the mental overhead of switching between charts and manually tracking levels.

5. Trade Like Institutions

By combining pivot-based S/R with BOS-confirmed order blocks, you're seeing where retail AND institutional money is positioned – giving you the complete picture.

🔥 Perfect For

Day traders seeking M15/H1 confluence for precise entries

Scalpers needing M5 zones with higher-timeframe confirmation

Swing traders looking for Daily/H4 zone alignment for position trades

ICT/SMC practitioners combining order blocks with traditional analysis

Any trader who values clean, validated, multi-timeframe zones over cluttered charts

6B1! Manipulation/Distribution Projections (OHLC Stats)Overview

The Manipulation/Distribution Projections (OHLC Stats) indicator is a powerful tool designed to forecast potential price levels for various timeframes on British Pound futures (6B1!). It operates on a simple yet profound principle: price action within a single candle can be broken down into “manipulation” and “distribution” phases.

By analyzing over 17 years of 6B (6B1!) historical OHLC data externally in Python, this script calculates the average (mean) and typical (median) extent of these movements. These statistical insights are then used to project key levels on your chart based on the current period’s opening price—providing a statistically-grounded framework for potential support, resistance, and price targets.

________________________________________

Key Concepts Explained

The indicator’s logic is based on how price wicks and bodies form relative to the opening price.

• Manipulation: This refers to the initial move that goes against the candle’s eventual direction.

o For a bullish candle, it’s the lower wick (the move from the open down to the low before reversing higher).

o For a bearish candle, it’s the upper wick (the move from the open up to the high before selling off).

It represents a “fake out” or a stop hunt.

• Distribution: This is the primary, directional move of the candle from the opening price.

o For a bullish candle, it’s the distance from the open to the high.

o For a bearish candle, it’s the distance from the open to the low.

It represents the “real” intended direction of price for that period.

________________________________________

How It Works

This indicator does not calculate these ratios in real-time. Instead, it leverages a comprehensive statistical analysis performed externally in Python on over 17 years of 6B (6B1!) OHLC data. This analysis determined the mean and median ratios for both Manipulation and Distribution movements across different timeframes and, for intraday periods, different times of day.

These pre-computed, static ratios are embedded directly into the script. When a new period begins (e.g., a new day on the Daily timeframe), the indicator:

1. Takes the opening price for that period.

2. Retrieves the corresponding pre-calculated Manipulation and Distribution ratios.

3. Applies these ratios to the opening price to project eight potential price levels:

o

/ - Mean Distribution

o

/ - Median Distribution

o

/ - Mean Manipulation

o

/ - Median Manipulation

This approach provides a stable, forward-looking set of levels for the entire duration of the trading period.

________________________________________

Features

• Statistically-Derived Projections: Plots eight key price levels based on historical tendencies, providing clear potential zones for entries, exits, and stop placement.

• Selectable Timeframe: Choose to view projections for the 1H, 4H, 1D, or 1W periods directly from the settings.

• Dynamic Stats Table: A powerful, on-chart dashboard that provides real-time context. For all four timeframes (1H, 4H, 1D, 1W), it shows:

o Position: Where the current price is relative to the projected zones (e.g., “In +Manip Zone,” “Below -Dist”).

o Range Completed: The percentage of the historical average range that the current period has already covered.

o Current & Average Range: The current high-to-low range in points vs. the historical average.

• Historical Context: You can display levels for previous periods to see how price has interacted with them in the past.

• Full Customization: Control the color, style, and visibility of every line, label, and fill to match your chart’s theme.

________________________________________

How to Use

This indicator is versatile and can be integrated into various trading strategies.

• Identifying Targets & Reversal Zones: The Distribution levels (especially the zone between the median and mean) can serve as logical take-profit targets, as they represent a historical point of extension. Conversely, Manipulation levels can indicate areas where price might form a wick and reverse.

• Gauging Volatility: Use the Stats Table’s “Range Completed” column to assess market conditions. If the 1D range is only 30% complete by mid-day, there may be room for significant expansion. If it’s already at 150%, the market might be overextended and due for consolidation.

• Multi-Timeframe Confluence: Use the Stats Table to quickly check if the price on a lower timeframe (e.g., 1H) is approaching a significant level on a higher timeframe (e.g., 1D), adding more weight to that level.

• Defining Bias: If the price opens and holds above the Manipulation zones, it can signal a strong directional bias for the rest of the period.

________________________________________

Settings

• Projection Timeframe: The primary timeframe for which to calculate and display the levels.

• Historical Periods to Show: Set to 1 for only the current period, or increase to see how levels from past periods held up.

• Timezone: Set the timezone for accurate hourly calculations (defaults to America/New_York).

• Visuals: Customize the appearance of the projection lines, labels, and the shaded zones between mean and median levels.

• Stats Table: Enable/disable the table and configure its position, size, and colors.

________________________________________

Disclaimer

This indicator is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset. All trading involves risk, and past performance is not indicative of future results. Please do your own research and risk management.

Enjoy!

GC1! Manipulation/Distribution Projections (17 years OHLC Stats)Overview

The Manipulation/Distribution Projections (OHLC Stats) indicator is a powerful tool designed to forecast potential price levels for various timeframes on Gold futures (GC1!). It operates on a simple yet profound principle: price action within a single candle can be broken down into “manipulation” and “distribution” phases.

By analyzing over 17 years of GC (GC1!) historical OHLC data externally in Python, this script calculates the average (mean) and typical (median) extent of these movements. These statistical insights are then used to project key levels on your chart based on the current period’s opening price—providing a statistically-grounded framework for potential support, resistance, and price targets.

________________________________________

Key Concepts Explained

The indicator’s logic is based on how price wicks and bodies form relative to the opening price.

• Manipulation: This refers to the initial move that goes against the candle’s eventual direction.

o For a bullish candle, it’s the lower wick (the move from the open down to the low before reversing higher).

o For a bearish candle, it’s the upper wick (the move from the open up to the high before selling off).

It represents a “fake out” or a stop hunt.

• Distribution: This is the primary, directional move of the candle from the opening price.

o For a bullish candle, it’s the distance from the open to the high.

o For a bearish candle, it’s the distance from the open to the low.

It represents the “real” intended direction of price for that period.

________________________________________

How It Works

This indicator does not calculate these ratios in real-time. Instead, it leverages a comprehensive statistical analysis performed externally in Python on over 17 years of GC (GC1!) OHLC data. This analysis determined the mean and median ratios for both Manipulation and Distribution movements across different timeframes and, for intraday periods, different times of day.

These pre-computed, static ratios are embedded directly into the script. When a new period begins (e.g., a new day on the Daily timeframe), the indicator:

1. Takes the opening price for that period.

2. Retrieves the corresponding pre-calculated Manipulation and Distribution ratios.

3. Applies these ratios to the opening price to project eight potential price levels:

o

/ - Mean Distribution

o

/ - Median Distribution

o

/ - Mean Manipulation

o

/ - Median Manipulation

This approach provides a stable, forward-looking set of levels for the entire duration of the trading period.

________________________________________

Features

• Statistically-Derived Projections: Plots eight key price levels based on historical tendencies, providing clear potential zones for entries, exits, and stop placement.

• Selectable Timeframe: Choose to view projections for the 1H, 4H, 1D, or 1W periods directly from the settings.

• Dynamic Stats Table: A powerful, on-chart dashboard that provides real-time context. For all four timeframes (1H, 4H, 1D, 1W), it shows:

o Position: Where the current price is relative to the projected zones (e.g., “In +Manip Zone,” “Below -Dist”).

o Range Completed: The percentage of the historical average range that the current period has already covered.

o Current & Average Range: The current high-to-low range in points vs. the historical average.

• Historical Context: You can display levels for previous periods to see how price has interacted with them in the past.

• Full Customization: Control the color, style, and visibility of every line, label, and fill to match your chart’s theme.

________________________________________

How to Use

This indicator is versatile and can be integrated into various trading strategies.

• Identifying Targets & Reversal Zones: The Distribution levels (especially the zone between the median and mean) can serve as logical take-profit targets, as they represent a historical point of extension. Conversely, Manipulation levels can indicate areas where price might form a wick and reverse.

• Gauging Volatility: Use the Stats Table’s “Range Completed” column to assess market conditions. If the 1D range is only 30% complete by mid-day, there may be room for significant expansion. If it’s already at 150%, the market might be overextended and due for consolidation.

• Multi-Timeframe Confluence: Use the Stats Table to quickly check if the price on a lower timeframe (e.g., 1H) is approaching a significant level on a higher timeframe (e.g., 1D), adding more weight to that level.

• Defining Bias: If the price opens and holds above the Manipulation zones, it can signal a strong directional bias for the rest of the period.

________________________________________

Settings

• Projection Timeframe: The primary timeframe for which to calculate and display the levels.

• Historical Periods to Show: Set to 1 for only the current period, or increase to see how levels from past periods held up.

• Timezone: Set the timezone for accurate hourly calculations (defaults to America/New_York).

• Visuals: Customize the appearance of the projection lines, labels, and the shaded zones between mean and median levels.

• Stats Table: Enable/disable the table and configure its position, size, and colors.

________________________________________

Disclaimer

This indicator is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset. All trading involves risk, and past performance is not indicative of future results. Please do your own research and risk management.

Enjoy!

ES1! Manipulation/Distribution Projections (17 years OHLC Stats)Overview

The Manipulation/Distribution Projections (OHLC Stats) indicator is a powerful tool designed to forecast potential price levels for various timeframes on S&P 500 E-mini futures (ES1!). It operates on a simple yet profound principle: price action within a single candle can be broken down into “manipulation” and “distribution” phases.

By analyzing over 17 years of ES (ES1!) historical OHLC data externally in Python, this script calculates the average (mean) and typical (median) extent of these movements. These statistical insights are then used to project key levels on your chart based on the current period’s opening price—providing a statistically-grounded framework for potential support, resistance, and price targets.

________________________________________

Key Concepts Explained

The indicator’s logic is based on how price wicks and bodies form relative to the opening price.

• Manipulation: This refers to the initial move that goes against the candle’s eventual direction.

o For a bullish candle, it’s the lower wick (the move from the open down to the low before reversing higher).

o For a bearish candle, it’s the upper wick (the move from the open up to the high before selling off).

It represents a “fake out” or a stop hunt.

• Distribution: This is the primary, directional move of the candle from the opening price.

o For a bullish candle, it’s the distance from the open to the high.

o For a bearish candle, it’s the distance from the open to the low.

It represents the “real” intended direction of price for that period.

________________________________________

How It Works

This indicator does not calculate these ratios in real-time. Instead, it leverages a comprehensive statistical analysis performed externally in Python on over 17 years of ES (ES1!) OHLC data. This analysis determined the mean and median ratios for both Manipulation and Distribution movements across different timeframes and, for intraday periods, different times of day.

These pre-computed, static ratios are embedded directly into the script. When a new period begins (e.g., a new day on the Daily timeframe), the indicator:

1. Takes the opening price for that period.

2. Retrieves the corresponding pre-calculated Manipulation and Distribution ratios.

3. Applies these ratios to the opening price to project eight potential price levels:

o

/ - Mean Distribution

o

/ - Median Distribution

o

/ - Mean Manipulation

o

/ - Median Manipulation

This approach provides a stable, forward-looking set of levels for the entire duration of the trading period.

________________________________________

Features

• Statistically-Derived Projections: Plots eight key price levels based on historical tendencies, providing clear potential zones for entries, exits, and stop placement.

• Selectable Timeframe: Choose to view projections for the 1H, 4H, 1D, or 1W periods directly from the settings.

• Dynamic Stats Table: A powerful, on-chart dashboard that provides real-time context. For all four timeframes (1H, 4H, 1D, 1W), it shows:

o Position: Where the current price is relative to the projected zones (e.g., “In +Manip Zone,” “Below -Dist”).

o Range Completed: The percentage of the historical average range that the current period has already covered.

o Current & Average Range: The current high-to-low range in points vs. the historical average.

• Historical Context: You can display levels for previous periods to see how price has interacted with them in the past.

• Full Customization: Control the color, style, and visibility of every line, label, and fill to match your chart’s theme.

________________________________________

How to Use

This indicator is versatile and can be integrated into various trading strategies.

• Identifying Targets & Reversal Zones: The Distribution levels (especially the zone between the median and mean) can serve as logical take-profit targets, as they represent a historical point of extension. Conversely, Manipulation levels can indicate areas where price might form a wick and reverse.

• Gauging Volatility: Use the Stats Table’s “Range Completed” column to assess market conditions. If the 1D range is only 30% complete by mid-day, there may be room for significant expansion. If it’s already at 150%, the market might be overextended and due for consolidation.

• Multi-Timeframe Confluence: Use the Stats Table to quickly check if the price on a lower timeframe (e.g., 1H) is approaching a significant level on a higher timeframe (e.g., 1D), adding more weight to that level.

• Defining Bias: If the price opens and holds above the Manipulation zones, it can signal a strong directional bias for the rest of the period.

________________________________________

Settings

• Projection Timeframe: The primary timeframe for which to calculate and display the levels.

• Historical Periods to Show: Set to 1 for only the current period, or increase to see how levels from past periods held up.

• Timezone: Set the timezone for accurate hourly calculations (defaults to America/New_York).

• Visuals: Customize the appearance of the projection lines, labels, and the shaded zones between mean and median levels.

• Stats Table: Enable/disable the table and configure its position, size, and colors.

________________________________________

Disclaimer

This indicator is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset. All trading involves risk, and past performance is not indicative of future results. Please do your own research and risk management.

Enjoy!

SOFR - IORB Spread (pct pts & bps)Tracks short-term funding conditions by measuring the spread between the Secured Overnight Financing Rate (SOFR) and the Fed’s Interest on Reserve Balances (IORB). When SOFR persistently trades above IORB, it signals cash scarcity and stress in overnight funding markets. This indicator is best used as a risk-regime and plumbing health check, not as a directional trading signal. Calm readings allow trends to persist; sustained spikes often precede periods of volatility and forced deleveraging.

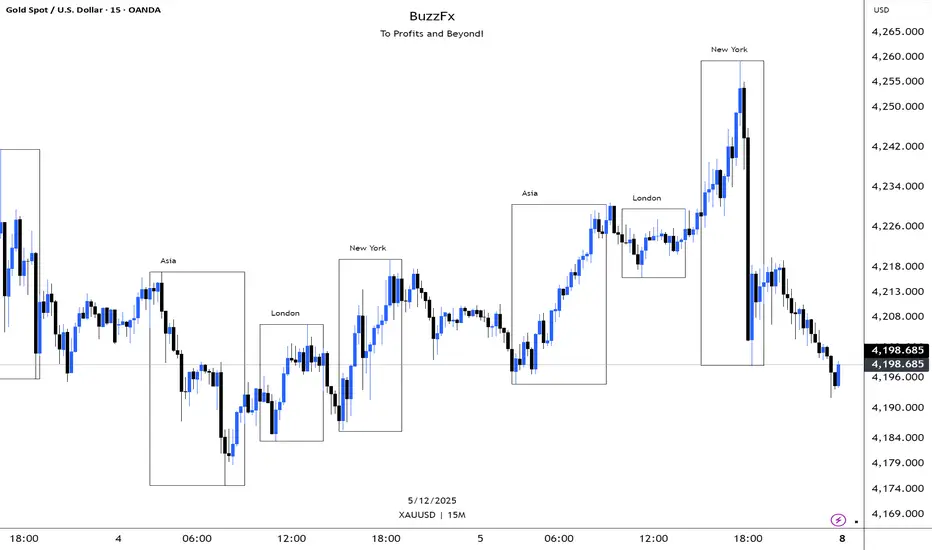

BuzzFx Market SessionsBuzzFx Market Sessions is a clean and powerful tool that highlights the most important trading sessions directly on your chart.

It automatically marks:

London Session

New York Session

Asian Session

Pre-New York

Session highs & lows (optional)

Session ranges & volatility zones

This indicator helps traders instantly understand:

When major liquidity enters the market

When volatility typically increases

How price reacts inside each session

Which session is driving the current trend

Designed for both beginners and advanced traders, BuzzFx Market Sessions gives you a clearer view of market structure and timing—so you can trade smarter, not harder.

Perfect for day traders, scalpers, and SMC traders who rely on timing, volatility, and session behavior.

Pivot Points Standard w/ Future PivotsPivot Points Standard with Future Projections

This indicator displays traditional pivot point levels with an added feature to project future pivot levels based on the current period's price action.

Key Features:

Multiple Pivot Types: Choose from Traditional, Fibonacci, Woodie, Classic, DM, and Camarilla pivot calculations

Flexible Timeframes: Auto-detect or manually select Daily, Weekly, Monthly, Quarterly, Yearly, and multi-year periods

Future Pivot Projections: Visualize potential pivot levels for the next period based on current price movement

Custom Price Scenarios: Test "what-if" scenarios by entering a custom close price to see resulting pivot levels

Customizable Display: Adjust line styles, colors, opacity, and label positioning for both historical and future pivots

Historical Pivots: View up to 200 previous pivot periods for context

Future Pivot Options:

The unique future pivot feature calculates what the next period's support and resistance levels would be using the current period's High, Low, Open, and either the current price or a custom price you specify for the closing value. Future pivots are displayed with customizable line styles (solid, dashed, dotted) and opacity to distinguish them from historical levels.

Use Cases:

Plan entries and exits based on projected support/resistance

Scenario analysis with custom price targets

Identify key levels before the period closes

Multi-timeframe pivot analysis

Works on all timeframes and instruments.

MTF S/R Array - Full CustomA clean, institutional-style multi-timeframe support and resistance indicator designed for precision trading decisions. Plots previous and current period levels with full customization for backtesting and live trading.

━━━━━━━━━━━━━━━━━━━━━━

WHAT IT PLOTS

━━━━━━━━━━━━━━━━━━━━━━

MONTHLY

- Previous Month High / Low / Close

- Previous Month Highest Closing Price

- Current Month High / Low / Highest Close

WEEKLY

- Previous Week High / Low / Close

- Current Week High / Low

DAILY

- Previous Day High / Low / Close

- Current Day High / Low

SESSIONS (Full Session - EST)

- Asian: 7pm - 4am

- London: 3am - 12pm

- New York: 8am - 5pm

OPENING RANGE

- Monday/Tuesday combined high and low

- Clean box visualization for weekly initial balance

━━━━━━━━━━━━━━━━━━━━━━

WHY THESE LEVELS MATTER

━━━━━━━━━━━━━━━━━━━━━━

Institutions and smart money reference these key levels for:

- Liquidity targets

- Stop hunts

- Reversal zones

- Trend continuation entries

Previous period levels act as magnets for price. Current levels show where the battle is happening now.

━━━━━━━━━━━━━━━━━━━━━━

FULL CUSTOMIZATION

━━━━━━━━━━━━━━━━━━━━━━

Every level type has independent controls:

- Show/Hide Previous and Current separately

- Extend Bars - control how far each level stretches

- Line Width - adjust thickness per level

- Transparency - fade previous levels for clarity

- Colors - separate colors for High/Low vs Close

Additional settings:

- Labels on/off with size and style options

- Info table with position and size controls

- Opening range box transparency and border width

━━━━━━━━━━━━━━━━━━━━━━

HOW TO USE

━━━━━━━━━━━━━━━━━━━━━━

1. Use on lower timeframes (1m, 5m, 15m) to see HTF levels

2. Watch for price reactions at previous period highs/lows

3. Look for session high/low sweeps followed by reversals

4. Use Monday/Tuesday opening range for weekly bias and targets

5. Previous levels extend further back for backtesting context

━━━━━━━━━━━━━━━━━━━━━━

TIPS

━━━━━━━━━━━━━━━━━━━━━━

- Increase "Prev Extend Bars" on monthly/weekly to see levels across more history

- Use higher transparency on previous levels to keep chart clean

- Turn off sessions you don't trade to reduce clutter

- The info table shows all values at a glance - position it where it doesn't block price action

━━━━━━━━━━━━━━━━━━━━━━

BEST FOR

━━━━━━━━━━━━━━━━━━━━━━

- ICT / Smart Money Concepts traders

- Session-based strategies

- Swing traders using HTF levels on LTF entries

- Anyone who wants clean, customizable S/R levels

Works on Forex, Crypto, Stocks, Futures, and Indices.

Alpha Signal AI ProAlpha Signal AI Pro

Short description:

A smart, ensemble-style indicator that blends trend, momentum, volume, volatility, and candle patterns into a score & star system that produces Buy/Sell signals confirmed by MACD crosses. After a signal, it projects smart targets (TP1/TP2/TP3) and a stop-loss derived from ATR, with forward drawings and a control panel for trade management.

Inputs

Minimum Score (min_score): default 6.0 — higher = fewer but stronger signals.

Minimum Stars (min_stars): default 2 — extra filter for strength.

Future Bars (future_bars): default 15 — how far targets/SL are drawn ahead.

Use AI Targets (use_ai_targets): toggle the AI multiplier for TP/SL.

How it works

Computes buy_score/sell_score from: EMA8/21/50/200, RSI & its MA, MACD & Histogram, Stochastic, ADX/DMI, VWAP, Volume, 15m MTF tilt, ROC/Momentum, Heikin Ashi, and candle patterns (engulfing/hammer/shooting star).

Converts scores into Stars (⭐⭐ to ⭐⭐⭐⭐⭐) via tiered thresholds.

Signals fire only when: Score ≥ minimum + Stars ≥ minimum + MACD cross (up = Buy, down = Sell).

On a signal, one active trade is managed until TP3 or SL is reached.

Targets & Stop (AI-driven)

Targets and SL are ATR-based, then adjusted by an AI multiplier derived from: ATR%, momentum (ROC), relative volume, trend strength (ADX), and star rating.

Approximate formulas:

TP1 ≈ 1.5×ATR × AI

TP2 ≈ 2.5×ATR × AI

TP3 ≈ 4.0×ATR × AI

SL ≈ 1.0×ATR ÷ AI

What you’ll see on chart

“Buy/Sell” markers with small Star labels, an Entry line (blue), SL (red dotted), TP1/TP2 (green), TP3 (gold) with shaded target boxes and a guide line towards the final target.

A central AI badge showing the multiplier % and star rating.

A top-right Panel showing status, strength, AI%, price, scores, and during trades: entry, TP1/TP2/TP3, and live P/L.

Alerts

Two ready-made conditions: Buy and Sell when the respective signal triggers.

Add alert: Right click → Add alert → choose the indicator → select condition.

Best practices

Match timeframe to instrument:

Scalping 5–15m: min_score 8, min_stars 3–4.

Swing H1–H4: min_score 7, min_stars 3.

Daily/Equities: min_score 6–7, min_stars 2–3.

Prefer trades with EMA200 and 15m MTF trend alignment.

De-risk around major news.

Use fixed risk per trade (e.g., 1%).

Important notes

Prefer bar close confirmation to avoid mid-bar MACD flips.

Single trade at a time via the in_trade state.

15m MTF uses request.security with lookahead_off; evaluate at close for consistency.

FAQ

Use it standalone? You can, but it’s stronger when combined with S/R zones/trendlines and solid risk management.

Why do targets vary? The AI multiplier adapts TP/SL to current market conditions.

Disclaimer

This is an analytical/educational tool, not financial advice. Always backtest and use appropriate risk management.

Developer note

Built in Pine Script v6, uses var for trade state, clears drawings on the last bar to keep the chart tidy, and raises drawing limits to avoid runtime errors.

wedge hunter (Buy - Sell) signalsthis indicator can work on different options like forex and stock markets(shares).

this indicator watching charts for highs and lows and search for squeeze and pıvots for finding entrıes. i try to help to community for understand the formations and easly find an entry point. with rsi confirmation you find the best entry locations

NeuroSwarm ETH — Crowd vs Experts Forecast TrackerEnglish:

NeuroSwarm — Crowd vs Experts Forecast Tracker (ETH)

This indicator visualizes monthly forecast data collected from two independent groups:

Crowd – a large sample of retail participants

Experts – a curated group of analysts and experienced market participants

For each month, the indicator plots the following values as horizontal levels on the price chart:

Median forecast (Crowd)

Average forecast (Crowd)

Median forecast (Experts)

Average forecast (Experts)

Shaded zones highlighting the difference between median and mean

All values are fixed for each month and stay unchanged historically.

This allows traders to analyze sentiment dynamics and compare how expectations from both groups align or diverge from actual price action.

Purpose:

This tool is intended for sentiment visualization and analytical insight — it does not generate trading signals.

Its main goal is to compare collective expectations of retail traders vs experts across time.

Data source:

All forecasts come from monthly surveys conducted within the NeuroSwarm project between the 1st and 5th day of each month.

Interface notice:

The script's UI may contain non-English labels for convenience, but a full English documentation is provided here in compliance with TradingView rules.

Русская версия:

NeuroSwarm — Мудрость Толпы vs Эксперты (ETH)

Индикатор отображает ежемесячные прогнозы двух групп:

Толпа: медиана и средняя прогнозов

Эксперты: медиана и средняя прогнозов

Значения фиксируются для каждого месяца и показываются горизонтальными уровнями.

Заливка отображает диапазон между медианой и средней, что упрощает визуальное сравнение настроений.

Это аналитический инструмент для визуализации настроений — не торговая стратегия.

Все данные берутся из ежемесячных опросов проекта NeuroSwarm.

12M Return Strategy This strategy is based on the original Dual Momentum concept presented by Gary Antonacci in his book “Dual Momentum Investing.”

It implements the absolute momentum portion of the framework using a 12-month rate of change, combined with a moving-average filter for trend confirmation.

The script automatically adapts the lookback period depending on chart timeframe, ensuring the return calculation always represents approximately one year, whether you are on daily, weekly, or monthly charts.

How the Strategy Works

1. 12-Month Return Calculation

The core signal is the 12-month price return, computed as:

(Current Price ÷ Price from ~1 year ago) − 1

This return:

Plots as a histogram

Turns green when positive

Turns red when negative

The lookback adjusts automatically:

1D chart → 252 bars

1W chart → 52 bars

1M chart → 12 bars

Other timeframes → estimated to approximate 1 calendar year

2. Trend Filter (Moving Average of Return)

To smooth volatility and avoid noise, the strategy applies a moving average to the 12M return:

Default length: 12 periods

Plotted as a white line on the indicator panel

This becomes the benchmark used for crossovers.

3. Trade Signals (Long / Short / Cash)

Trades are generated using a simple crossover mechanism:

Bullish Signal (Go Long)

When:

12M Return crosses ABOVE its MA

Action:

Close short (if any)

Enter long

Bearish Signal (Go Short or Go Flat)

When:

12M Return crosses BELOW its MA

Action:

If shorting is enabled → Enter short

If shorting is disabled → Exit position and go to cash

Shorting can be enabled or disabled with a single input switch.

4. Position Sizing

The strategy uses:

Percent of Equity position sizing

You can specify the percentage of your portfolio to allocate (default 100%).

No leverage is required, but the strategy supports it if your account settings allow.

5. Visual Signals

To improve clarity, the strategy marks signals directly on the indicator panel:

Green Up Arrows: return > MA

Red Down Arrows: return < MA

A status label shows the current mode:

LONG

SHORT

CASH

6. Backtest-Ready

This script is built as a full TradingView strategy, not just an indicator.

This means you can:

Run complete backtests

View performance metrics

Compare long-only vs long/short behavior

Adjust inputs to tune the system

It provides a clean, rule-driven interpretation of the classic absolute momentum approach.

Inspired By: Gary Antonacci – Dual Momentum Investing

This script reflects the absolute momentum side of Antonacci’s original research:

Uses 12-month momentum (the most statistically validated lookback)

Applies a trend-following overlay to control downside risk

Recreates the classic signal structure used in academic studies

It is a simplified, transparent version intended for practical use and educational clarity.

Disclaimer

This script is for educational and research purposes only.

Historical performance does not guarantee future results.

Always use proper risk management.

NeuroSwarm BTC — Crowd vs Experts Forecast TrackerEnglish:

NeuroSwarm — Crowd vs Experts Forecast Tracker (BTC)

This indicator visualizes monthly forecasts collected from two independent groups:

Crowd – a large sample of retail traders

Experts – a smaller, curated group of analysts and experienced market participants

For each month, the following values are displayed as horizontal levels on the chart:

Median forecast of the Crowd

Average forecast of the Crowd

Median forecast of Experts

Average forecast of Experts

Shaded zones showing the range between median and mean

The values remain fixed throughout each month. This allows traders to compare sentiment dynamics between groups and see how expectations evolve relative to actual market movement.

Purpose:

This indicator is designed for sentiment analysis — NOT for generating trading signals.

It helps identify divergences between retail expectations and expert forecasts, which can be informative during trend transitions.

Data source:

All values come from monthly surveys conducted within the NeuroSwarm project (1–5 of every month).

Crowd and Expert groups are collected separately to avoid bias and to preserve independent aggregation.

Interface language note:

The indicator’s interface may contain non-English labels for ease of use, but full English documentation is provided here in compliance with TradingView House Rules.

Русская версия (optional, allowed only AFTER English):

NeuroSwarm — Мудрость Толпы vs Эксперты (BTC)

Индикатор показывает ежемесячные прогнозы двух групп:

Толпа: медиана и средняя прогнозов

Эксперты: медиана и средняя прогнозов

Значения фиксируются на весь месяц и отображаются на графике горизонтальными уровнями.

Заливка показывает диапазон между медианой и средней.

Цель индикатора — визуализировать настроение толпы и экспертов и сравнить его с реальным движением цены.

Это аналитический инструмент, а не торговая стратегия.

Данные берутся из ежемесячных опросов (1–5 числа), проводимых в рамках проекта NeuroSwarm.

Vacs - Trade Support Panel 📈 Multi-Function Trade Support Panel (MACD + CVPE + MTF Bias)

This is a comprehensive Pine Script indicator designed to provide **multi-timeframe (MTF) bias** and **cumulative volume analysis** alongside standard **Moving Average Convergence Divergence (MACD)**, primarily intended as a **support panel** for confirming signals generated by other trading indicators and strategies.

🛠️ Included Modules and Functionality

This panel combines three powerful analysis tools into a single, unified view, all with customizable input controls for visibility and calculation:

1. **MACD (Moving Average Convergence Divergence) Module**

Function: Calculates and plots the standard MACD line, Signal line, and Histogram.

*Key Feature: Supports an **MTF mode**, allowing you to calculate the MACD based on a higher timeframe (e.g., 4H on a 1H chart) to identify broader momentum shifts.

Controls : Separate toggles for the MACD Line, Signal Line, and Histogram plots, along with standard length inputs (Fast EMA, Slow EMA, Signal Length).

2. **CVPE (Cumulative Volume & Position Engine) Module**

Function: Provides deeper insight into market pressure by analyzing the cumulative delta/volume flow.

CVD (Cumulative Volume Delta):** Tracks the running sum of buying or selling pressure, indicating the direction of order flow and potential accumulation/distribution.

Position Bias: Calculates the rate of change (slope) of the CVD, normalized by volatility, to show the immediate strength and conviction of buyers versus sellers.

Purpose: Helps identify divergences and confirm the conviction behind price moves.

Controls: A master toggle to enable/disable the entire CVPE engine and customizable smoothing methods/lengths.

3. **MTF Bias Panel (Dashboard)

Function: Provides a weighted, holistic score for the market bias across **four custom timeframes** (e.g., 1H, 4H, Daily, Weekly).

Calculation: The total bias score is derived by combining the directional signals from the MACD Histogram and the CVD Slope (Position Bias) for each selected timeframe, weighted according to user preference.

Purpose: Offers a quick, top-down view of the market structure and helps traders align their entries/exits with the larger trend direction.

Controls: Master toggle to show/hide the panel, independent weight adjustments for each of the four timeframes, and customizable component weights (MACD vs. CVD) for scoring.

💡 Recommended Use

This panel is designed to serve as a **critical confirmation tool** for any existing strategy:

1. **Trend Confirmation:** Use the **MTF Bias Panel** to confirm that the higher timeframes align with your trade direction before entering a signal generated by your primary indicator.

2. **Momentum Confirmation:** Use the **MACD** and **CVPE** modules to confirm that momentum is strong and order flow supports the anticipated move. Look for rising MACD Histograms and increasing Position Bias (CVD slope) in the direction of your trade.

3. **Divergence Spotting:** CVPE is excellent for identifying cumulative volume divergences against price, signaling potential reversals or exhaustion.

By providing multiple layers of analysis from different perspectives (momentum, order flow, and multi-timeframe), this indicator significantly reduces noise and helps traders take only the highest-conviction setups.

Would you like me to write a short, punchy title or tagline for this description?