Stochastic %K Colored by VolumeDescription:

"Stochastic %K Colored by Volume is a technical indicator that combines the traditional Stochastic %K oscillator with volume-based coloring. It highlights periods of high, low, and neutral trading volume by changing the color of the %K line. Additionally, it identifies bullish and bearish divergences between price and the %K oscillator, helping traders spot potential reversals and trend changes. The indicator also includes key levels for overbought, oversold, and extreme zones to guide trading decisions."

Volatilite

Wilder's ADX/DIワイルダー氏が作ったトレンドの強弱を計るインジケーターです。証券会社のものは微妙に計算式が違うため、ワイルダー氏のオリジナルの計算式で作りました。

It’s an indicator created by Mr. Wilder to measure the strength of a trend.

Since the calculation formulas used by brokerage firms vary slightly, this version is built using Mr. Wilder’s original formula.

Standard Deviation VolatilityThe Standard Deviation (StDev) measures the volatility or dispersion of price from its historical average. Higher values suggest greater price fluctuation and potentially a trending market. Lower values indicate lower volatility, often found during consolidation or ranging markets.

標準偏差(Standard Deviation)は、価格の過去の平均からの**ばらつき(ボラティリティ)**を測る指標です。値が高いほど価格変動が激しく、トレンド相場であることを示唆します。値が低いほど、レンジ相場または保ち合いであることを示します。

Smart Dip & Spike Finder v6Dip and Spike Finder

What This Adds

✅ Finds dips (for buying)

✅ Finds spikes (for selling)

✅ Works with your existing RSI & MA filters

✅ Shows BUY and SELL labels on the chart

✅ Triggers separate alerts for dip and spike conditions

Opening Range Fibonacci Extensions (ATR Adjusted)this script displays daily, weekly, or monthly range extensions as a function of ATR in a Fibonacci retracement

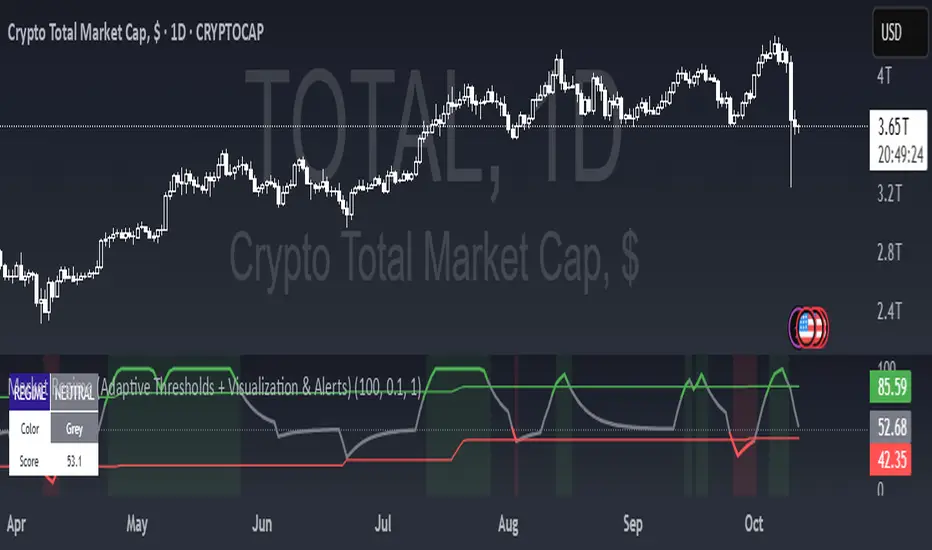

Market Regime (w/ Adaptive Thresholds)Logic Behind This Indicator

This indicator identifies market regimes (trending vs. mean-reverting) using adaptive thresholds that adjust to recent market conditions.

Core Components

1. Regime Score Calculation (0-100 scale)

Starts at 50 (neutral) and adjusts based on two factors:

A. Trend Strength

Compares fast EMA (5) vs. slow EMA (10)

If fast > slow by >1% → +60 points (strong uptrend)

If fast < slow by >1% → -60 points (strong downtrend)

B. RSI Momentum

Uses 7-period RSI smoothed with 3-period EMA

RSI > 70 → +20 points (overbought/trending)

RSI < 30 → -20 points (oversold/mean-reverting)

The score is then smoothed and clamped between 0-100.

2. Adaptive Thresholds

Instead of fixed levels, thresholds adjust to recent market behavior:

Looks back 100 bars to find the min/max regime score

High threshold = 80% of the range (trending regime)

Low threshold = 20% of the range (mean-reverting regime)

This prevents false signals in different volatility environments.

3. Regime Classification

Regime Score Classification Meaning

Above high threshold STRONG TREND Market is trending strongly (follow momentum)

Below low threshold STRONG MEAN REVERSION Market is choppy/oversold (fade moves)

Between thresholds NEUTRAL No clear regime (stay out or wait)

4. Regime Persistence Filter

Requires the regime to hold for a minimum number of bars (default: 1) before confirming

Prevents whipsaws from brief score fluctuations

What It Aims to Detect

When to use trend-following strategies (green = buy breakouts, ride momentum)

When to use mean-reversion strategies (red = buy dips, sell rallies)

When to stay out (gray = unclear conditions, high risk of false signals)

Visual Cues

Green background = Strong trend (momentum strategies work)

Red background = Strong mean reversion (contrarian strategies work)

Table = Shows current regime, color, and score

Alerts = Notifies when regime changes

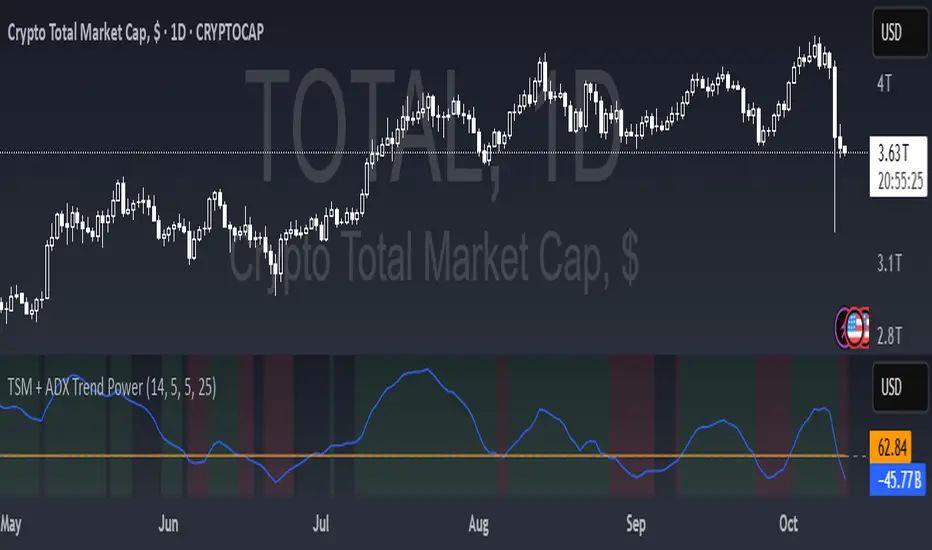

TSM + ADX Trend PowerLogic Behind This Indicator

This indicator combines two momentum/trend tools to identify strong, reliable trends in price movement:

1. TSM (Time Series Momentum)

What it does: Measures the difference between the current price and a smoothed average of past prices.

Formula: EMA(close - EMA(close, 14), 14)

Logic:

If TSM > 0 → Price is above its recent average = upward momentum

If TSM < 0 → Price is below its recent average = downward momentum

2. ADX (Average Directional Index)

What it does: Measures trend strength (not direction).

Logic:

ADX > 25 → Strong trend (either up or down)

ADX < 25 → Weak or no trend (choppy/sideways market)

Combined Logic (TSM + ADX)

The indicator only signals a trend when both conditions are met:

Condition Meaning

Uptrend TSM > 0 AND ADX > 25 → Strong upward momentum

Downtrend TSM < 0 AND ADX > 25 → Strong downward momentum

No signal ADX < 25 → Trend is too weak to trust

What It Aims to Detect

Strong, sustained trends (not just noise or small moves)

Filters out weak/choppy markets where momentum indicators often give false signals

Entry/exit points:

Green background = Strong uptrend (consider buying/holding)

Red background = Strong downtrend (consider selling/shorting)

No color = Weak trend (stay out or wait)

Multiple Symbol Trend Screener [Pineify]Multiple Symbol Trend Screener Pineify – Ultimate Multi-Indicator Scanner for TradingView

Empower your trading with deep market insights across multiple symbols using this feature-rich Pine Script screener. The Multiple Symbol Trend Screener Pineify enables traders to monitor and compare trends, reversals, and consolidations in real-time across the biggest equity symbols on TradingView, through a synergistic blend of popular technical indicators.

Key Features

Monitor up to 15 symbols and their trends simultaneously

Integrates 7 professional-grade indicators: MA Distance, Aroon, Parabolic SAR (PSAR), ADX, Supertrend, Keltner Channel, and BBTrend

Color-coded table display for instant visual assessment

Customizable lookback periods, indicator types, and calculation methods

SEO optimized for multi-symbol trend detection, screener, and advanced TradingView indicator

How It Works

This indicator leverages TradingView’s Pine Script v6 and request.security() to process multiple symbols across selected timeframes. Data populates a dynamic table, updating each cell based on the calculated value of every underlying indicator. MA Distance highlights deviation from moving averages; Aroon flags emerging trend strength; PSAR marks potential trend reversals; ADX assesses trend momentum; Supertrend detects bullish/bearish phases; Keltner Channel and BBTrend offer volatility and power insights.

Set up your preferred symbols and timeframes

Each indicator runs its calculation per symbol using its parameter group

All results are displayed in a table for a comprehensive dashboard view

Trading Ideas and Insights

Traders can use this screener for cross-market comparison, directional bias, entry/exit filtering, and comprehensive trend evaluation. The screener is excellent for swing trading, day trading, and portfolio tracking. It enables confirmation across multiple frameworks — for example, spotting momentum with ADX before confirming direction with Supertrend and PSAR.

Identify correlated movements or divergences across selected assets

Spot synchronized trend changes for basket trading ideas

Filter symbols by volatility, strength, or trend status for precise trade selection

How Multiple Indicators Work Together

The screener’s edge lies in its intelligent correlation of popular indicators. MA Distance measures the proximity to chosen moving averages, ideal for spotting overbought/oversold conditions. Aroon reveals the strength of new price trends, PSAR indicates reversal signals, and ADX quantifies the momentum of these trends. Supertrend provides a directional phase, while Keltner Channel & BBTrend analyze volatility shifts and band compressions. This amalgamation allows for a robust, multi-dimensional market snapshot, capturing details missed by single-indicator tools.

By displaying all key metrics side-by-side, the screener enables holistic decision-making, revealing confluence zones and contradiction areas across multiple tickers and timeframes.

Unique Aspects

Original implementation combining seven independent trend and momentum indicators for each symbol

Rich customization for symbols, timeframes, and all indicator parameters

Intuitive color-coding for quick reading of bullish/bearish/neutral signals

Comprehensive dashboard for instant actionable insights

How to Use

Load the indicator onto your TradingView chart

Go to the script’s settings and input your preferred symbols and relevant timeframes

Set your desired parameters for each indicator group: Moving Average type, Aroon length, PSAR values, ADX smoothing, etc.

Observe the results in the top-right table, then use it to filter candidates and validate trade setups

The screener is suitable for all timeframes and asset classes available on TradingView. Make sure your chart’s timeframe matches the one used in the scanner for optimal accuracy.

Customization

Choose up to 15 symbols to monitor in a single dashboard

Customize lookback periods, indicator types, colors, and display settings

Configure alerting options and thresholds for advanced trade automation

Conclusion

The Multiple Symbol Trend Screener Pineify sets a new standard for multi-asset screening on TradingView. By elegantly merging seven proven technical indicators, the screener delivers powerful trend detection, reversal analysis, and volatility monitoring — all in one dashboard. Take your trading to new heights with in-depth, customizable market surveillance.

ADR - Average Daily Range [KasTrades]This is an Average Daily Range (ADR) indicator.

There are two settings for ADR:

Two Look back period ADR range (e.g. 7 and 14 days)

One Look back period ADR (e.g. 5 days only)

Two day ADR ranges are typically used in equities and index futures whereas one day ADR is typically used in forex.

The opening time by default is 17:00 New York (Eastern) time. The ranges are always calculated from the opening price of the first bar on the respected timeframe.

- Standardized Money Flow Index with Multi-MA and BB OverlayThis custom Money Flow Index (MFI) script enhances the standard MFI by introducing multiple layers of configurability, statistical normalization, and visual clarity. It begins with the traditional MFI calculation using the average price, hlc3, and a user-defined length, then offers the option to standardize the output. Standardization transforms the MFI into a z-score by subtracting a rolling mean and dividing by a rolling standard deviation, making the indicator statistically interpretable across different assets, timeframes, and volatility regimes. When standardization is active, the overbought and oversold thresholds shift from the conventional 80 and 20 to +2 and –2, aligning them with standard deviation boundaries and improving signal clarity in volatile environments.

Beyond standardization, the script introduces a robust smoothing engine. Users can choose from several moving average types, including SMA, EMA, SMMA (RMA), WMA, and VWMA, to reduce noise and highlight trend shifts. A particularly advanced option is the “SMA + Bollinger Bands” mode, which overlays volatility envelopes around the smoothed MFI using a user-defined standard deviation multiplier. This feature helps traders identify when the MFI is unusually high or low relative to its recent behaviour, adding a volatility-adjusted layer of insight, especially useful in momentum or mean-reversion setups.

Visually, the script is designed for clarity, modularity, and flexibility. It plots the raw or standardized MFI in purple, overlays the smoothed version in yellow if enabled, and adds green Bollinger Bands when selected. It also includes horizontal reference lines for overbought, oversold, and midpoint levels, which dynamically adjust based on whether standardization is active. A shaded background between the overbought and oversold lines further enhances readability, helping traders quickly assess momentum extremes and potential inflection zones.

Compared to the standard MFI, which offers a fixed calculation, limited visual feedback, and no statistical context, this enhanced version is modular, customizable, and statistically grounded. It allows traders to tailor the indicator to their strategy, whether they prefer raw signals, smoothed trends, or volatility-adjusted extremes. These enhancements make it a powerful building block for more sophisticated signal engines, especially when combined with filter gating, persistent state logic, or multi-indicator overlays.

Adaptive Trend CatcherAdaptive Trend Catcher is an original indicator that combines Hull Moving Average smoothing, ATR-based volatility bands, and a CCI filter within an adaptive logic framework. It’s built to react intelligently to changing market conditions rather than applying fixed parameters.

The system uses hysteresis to confirm trend flips only after several consistent signals, minimizing noise and false reversals. During strong momentum bursts, it automatically tightens its internal deadzone and step size to stay responsive while maintaining stability in quieter periods.

The result is a dynamic trend engine that plots a color-shifting adaptive line — green for bullish, red for bearish — that adjusts smoothly with volatility. Optional upper/lower ATR bands can be displayed for added context.

How to use: Watch for confirmed trend color flips with supporting momentum. Bullish flips occur when price regains the lower band and CCI turns positive; bearish flips when price falls below the upper band and CCI turns negative.

Includes alert conditions for both reversals.

For educational purposes only. Not financial advice.

ADR [KasTrades]This ADR indicator has 2 options: a Range of ADR, such as 7 and 14 which is typically used for indexes, index futures and equities, or a single ADR such as a 5 day which is typically used for forex.

The session start time is 17:00 ET (NY Time) by default, this is adjustable.

You can adjust the ADR days to different ranges such as 5 and 10, or a single ADR day such as 7.

Colors of the ADR high and low are also adjustable.

RSI Donchian Channel [DCAUT]█ RSI Donchian Channel

📊 ORIGINALITY & INNOVATION

The RSI Donchian Channel represents an important synthesis of two complementary analytical frameworks: momentum oscillators and breakout detection systems. This indicator addresses a common limitation in traditional RSI analysis by replacing fixed overbought/oversold thresholds with adaptive zones derived from historical RSI extremes.

Key Enhancement:

Traditional RSI analysis relies on static threshold levels (typically 30/70), which may not adequately reflect changing market volatility regimes. This indicator adapts the reference zones dynamically based on the actual RSI behavior over the lookback period, helping traders identify meaningful momentum extremes relative to recent price action rather than arbitrary fixed levels.

The implementation combines the proven momentum measurement capabilities of RSI with Donchian Channel's breakout detection methodology, creating a framework that identifies both momentum exhaustion points and potential continuation signals through the same analytical lens.

📐 MATHEMATICAL FOUNDATION

Core Calculation Process:

Step 1: RSI Calculation

The Relative Strength Index measures momentum by comparing the magnitude of recent gains to recent losses:

Calculate price changes between consecutive periods

Separate positive changes (gains) from negative changes (losses)

Apply selected smoothing method (RMA standard, also supports SMA, EMA, WMA) to both gain and loss series

Compute Relative Strength (RS) as the ratio of smoothed gains to smoothed losses

Transform RS into bounded 0-100 scale using the formula: RSI = 100 - (100 / (1 + RS))

Step 2: Donchian Channel Application

The Donchian Channel identifies the highest and lowest RSI values within the specified lookback period:

Upper Channel: Highest RSI value over the lookback period, represents the recent momentum peak

Lower Channel: Lowest RSI value over the lookback period, represents the recent momentum trough

Middle Channel (Basis): Average of upper and lower channels, serves as equilibrium reference

Channel Width Dynamics:

The distance between upper and lower channels reflects RSI volatility. Wide channels indicate high momentum variability, while narrow channels suggest momentum consolidation and potential breakout preparation. The indicator monitors channel width over a 100-period window to identify squeeze conditions that often precede significant momentum shifts.

📊 COMPREHENSIVE SIGNAL ANALYSIS

Primary Signal Categories:

Breakout Signals:

Upper Breakout: RSI crosses above the upper channel, indicates momentum reaching new relative highs and potential trend continuation, particularly significant when accompanied by price confirmation

Lower Breakout: RSI crosses below the lower channel, suggests momentum reaching new relative lows and potential trend exhaustion or reversal setup

Breakout strength is enhanced when the channel is narrow prior to the breakout, indicating a transition from consolidation to directional movement

Mean Reversion Signals:

Upper Touch Without Breakout: RSI reaches the upper channel but fails to break through, may indicate momentum exhaustion and potential reversal opportunity

Lower Touch Without Breakout: RSI reaches the lower channel without breakdown, suggests potential bounce as momentum reaches oversold extremes

Return to Basis: RSI moving back toward the middle channel after touching extremes signals momentum normalization

Trend Strength Assessment:

Sustained Upper Channel Riding: RSI consistently remains near or above the upper channel during strong uptrends, indicates persistent bullish momentum

Sustained Lower Channel Riding: RSI stays near or below the lower channel during strong downtrends, reflects persistent bearish pressure

Basis Line Position: RSI position relative to the middle channel helps identify the prevailing momentum bias

Channel Compression Patterns:

Squeeze Detection: Channel width narrowing to 100-period lows indicates momentum consolidation, often precedes significant directional moves

Expansion Phase: Channel widening after a squeeze confirms the initiation of a new momentum regime

Persistent Narrow Channels: Extended periods of tight channels suggest market indecision and accumulation/distribution phases

🎯 STRATEGIC APPLICATIONS

Trend Continuation Strategy:

This approach focuses on identifying and trading momentum breakouts that confirm established trends:

Identify the prevailing price trend using higher timeframe analysis or trend-following indicators

Wait for RSI to break above the upper channel in uptrends (or below the lower channel in downtrends)

Enter positions in the direction of the breakout when price action confirms the momentum shift

Place protective stops below the recent swing low (long positions) or above swing high (short positions)

Target profit levels based on prior swing extremes or use trailing stops to capture extended moves

Exit when RSI crosses back through the basis line in the opposite direction

Mean Reversion Strategy:

This method capitalizes on momentum extremes and subsequent corrections toward equilibrium:

Monitor for RSI reaching the upper or lower channel boundaries

Look for rejection signals (price reversal patterns, volume divergence) when RSI touches the channels

Enter counter-trend positions when RSI begins moving back toward the basis line

Use the basis line as the initial profit target for mean reversion trades

Implement tight stops beyond the channel extremes to limit risk on failed reversals

Scale out of positions as RSI approaches the basis line and closes the position when RSI crosses the basis

Breakout Preparation Strategy:

This approach positions traders ahead of potential volatility expansion from consolidation phases:

Identify squeeze conditions when channel width reaches 100-period lows

Monitor price action for consolidation patterns (triangles, rectangles, flags) during the squeeze

Prepare conditional orders for breakouts in both directions from the consolidation

Enter positions when RSI breaks out of the narrow channel with expanding width

Use the channel width expansion as a confirmation signal for the breakout's validity

Manage risk with stops just inside the opposite channel boundary

Multi-Timeframe Confluence Strategy:

Combining RSI Donchian Channel analysis across multiple timeframes can improve signal reliability:

Identify the primary trend direction using a higher timeframe RSI Donchian Channel (e.g., daily or weekly)

Use a lower timeframe (e.g., 4-hour or hourly) to time precise entry points

Enter long positions when both timeframes show RSI above their respective basis lines

Enter short positions when both timeframes show RSI below their respective basis lines

Avoid trades when timeframes provide conflicting signals (e.g., higher timeframe below basis, lower timeframe above)

Exit when the higher timeframe RSI crosses its basis line in the opposite direction

Risk Management Guidelines:

Effective risk management is essential for all RSI Donchian Channel strategies:

Position Sizing: Calculate position sizes based on the distance between entry point and stop loss, limiting risk to 1-2% of capital per trade

Stop Loss Placement: For breakout trades, place stops just inside the opposite channel boundary; for mean reversion trades, use stops beyond the channel extremes

Profit Targets: Use the basis line as a minimum target for mean reversion trades; for trend trades, target prior swing extremes or use trailing stops

Channel Width Context: Increase position sizes during narrow channels (lower volatility) and reduce sizes during wide channels (higher volatility)

Correlation Awareness: Monitor correlations between traded instruments to avoid over-concentration in similar setups

📋 DETAILED PARAMETER CONFIGURATION

RSI Source:

Defines the price data series used for RSI calculation:

Close (Default): Standard choice providing end-of-period momentum assessment, suitable for most trading styles and timeframes

High-Low Average (HL2): Reduces the impact of closing auction dynamics, useful for markets with significant end-of-day volatility

High-Low-Close Average (HLC3): Provides a more balanced view incorporating the entire period's range

Open-High-Low-Close Average (OHLC4): Offers the most comprehensive price representation, helpful for identifying overall period sentiment

Strategy Consideration: Use Close for end-of-period signals, HL2 or HLC3 for intraday volatility reduction, OHLC4 for capturing full period dynamics

RSI Length:

Controls the number of periods used for RSI calculation:

Short Periods (5-9): Highly responsive to recent price changes, produces more frequent signals with increased false signal risk, suitable for short-term trading and volatile markets

Standard Period (14): Widely accepted default balancing responsiveness with stability, appropriate for swing trading and intermediate-term analysis

Long Periods (21-28): Produces smoother RSI with fewer signals but more reliable trend identification, better for position trading and reducing noise in choppy markets

Optimization Approach: Test different lengths against historical data for your specific market and timeframe, consider using longer periods in ranging markets and shorter periods in trending markets

RSI MA Type:

Determines the smoothing method applied to price changes in RSI calculation:

RMA (Relative Moving Average - Default): Wilder's original smoothing method providing stable momentum measurement with gradual response to changes, maintains consistency with classical RSI interpretation

SMA (Simple Moving Average): Treats all periods equally, responds more quickly to changes than RMA but may produce more whipsaws in volatile conditions

EMA (Exponential Moving Average): Weights recent periods more heavily, increases responsiveness at the cost of potential noise, suitable for traders prioritizing early signal generation

WMA (Weighted Moving Average): Applies linear weighting favoring recent data, offers a middle ground between SMA and EMA responsiveness

Selection Guidance: Maintain RMA for consistency with traditional RSI analysis, use EMA or WMA for more responsive signals in fast-moving markets, apply SMA for maximum simplicity and transparency

DC Length:

Specifies the lookback period for Donchian Channel calculation on RSI values:

Short Periods (10-14): Creates tight channels that adapt quickly to changing momentum conditions, generates more frequent trading signals but increases sensitivity to short-term RSI fluctuations

Standard Period (20): Balances channel responsiveness with stability, aligns with traditional Bollinger Bands and moving average periods, suitable for most trading styles

Long Periods (30-50): Produces wider, more stable channels that better represent sustained momentum extremes, reduces signal frequency while improving reliability, appropriate for position traders and higher timeframes

Calibration Strategy: Match DC length to your trading timeframe (shorter for day trading, longer for swing trading), test channel width behavior during different market regimes, consider using adaptive periods that adjust to volatility conditions

Market Adaptation: Use shorter DC lengths in trending markets to capture momentum shifts earlier, apply longer periods in ranging markets to filter noise and focus on significant extremes

Parameter Combination Recommendations:

Scalping/Day Trading: RSI Length 5-9, DC Length 10-14, EMA or WMA smoothing for maximum responsiveness

Swing Trading: RSI Length 14, DC Length 20, RMA smoothing for balanced analysis (default configuration)

Position Trading: RSI Length 21-28, DC Length 30-50, RMA or SMA smoothing for stable signals

High Volatility Markets: Longer RSI periods (21+) with standard DC length (20) to reduce noise

Low Volatility Markets: Standard RSI length (14) with shorter DC length (10-14) to capture subtle momentum shifts

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Adaptive Threshold Mechanism:

Unlike traditional RSI analysis with fixed 30/70 thresholds, this indicator's Donchian Channel approach provides several improvements:

Context-Aware Extremes: Overbought/oversold levels adjust automatically based on recent momentum behavior rather than arbitrary fixed values

Volatility Adaptation: In low volatility periods, channels narrow to reflect tighter momentum ranges; in high volatility, channels widen appropriately

Market Regime Recognition: The indicator implicitly adapts to different market conditions without manual threshold adjustments

False Signal Reduction: Adaptive channels help reduce premature reversal signals that often occur with fixed thresholds during strong trends

Signal Quality Characteristics:

The indicator's dual-purpose design provides distinct advantages for different trading objectives:

Breakout Trading: Channel boundaries offer clear, objective breakout levels that update dynamically, eliminating the ambiguity of when momentum becomes "too high" or "too low"

Mean Reversion: The basis line provides a natural profit target for reversion trades, representing the midpoint of recent momentum extremes

Trend Strength: Persistent channel boundary riding offers an objective measure of trend strength without additional indicators

Consolidation Detection: Channel width analysis provides early warning of potential volatility expansion from compression phases

Comparative Analysis:

When compared to traditional RSI implementations and other momentum frameworks:

vs. Fixed Threshold RSI: Provides market-adaptive reference levels rather than static values, helping to reduce false signals during trending markets where RSI can remain "overbought" or "oversold" for extended periods

vs. RSI Bollinger Bands: Offers clearer breakout signals and more intuitive extreme identification through actual high/low boundaries rather than statistical standard deviations

vs. Stochastic Oscillator: Maintains RSI's momentum measurement advantages (unbounded calculation avoiding scale compression) while adding the breakout detection capabilities of Donchian Channels

vs. Standard Donchian Channels: Applies breakout methodology to momentum space rather than price, providing earlier signals of potential trend changes before price breakouts occur

Performance Characteristics:

The indicator exhibits specific behavioral patterns across different market conditions:

Trending Markets: Excels at identifying momentum continuation through channel breakouts, RSI tends to ride one channel boundary during strong trends, providing trend confirmation

Ranging Markets: Channel width narrows during consolidation, offering early preparation signals for potential breakout trading opportunities

High Volatility: Channels widen to reflect increased momentum variability, automatically adjusting signal sensitivity to match market conditions

Low Volatility: Channels contract, making the indicator more sensitive to subtle momentum shifts that may be significant in calm market environments

Transition Periods: Channel squeezes often precede major trend changes, offering advance warning of potential regime shifts

Limitations and Considerations:

Users should be aware of certain operational characteristics:

Lookback Dependency: Channel boundaries depend entirely on the lookback period, meaning the indicator has no predictive element beyond identifying current momentum relative to recent history

Lag Characteristics: As with all moving average-based indicators, RSI calculation introduces lag, and channel boundaries update only as new extremes occur within the lookback window

Range-Bound Sensitivity: In extremely tight ranges, channels may become very narrow, potentially generating excessive signals from minor momentum fluctuations

Trending Persistence: During very strong trends, RSI may remain at channel extremes for extended periods, requiring patience for mean reversion setups or commitment to trend-following approaches

No Absolute Levels: Unlike traditional RSI, this indicator provides no fixed reference points (like 50), making it less suitable for strategies that depend on absolute momentum readings

USAGE NOTES

This indicator is designed for technical analysis and educational purposes to help traders understand momentum dynamics and identify potential trading opportunities. The RSI Donchian Channel has limitations and should not be used as the sole basis for trading decisions.

Important considerations:

Performance varies significantly across different market conditions, timeframes, and instruments

Historical signal patterns do not guarantee future results, as market behavior continuously evolves

Effective use requires understanding of both RSI momentum principles and Donchian Channel breakout concepts

Risk management practices (stop losses, position sizing, diversification) are essential for any trading application

Consider combining with additional analytical tools such as volume analysis, price action patterns, or trend indicators for confirmation

Backtest thoroughly on your specific instruments and timeframes before live trading implementation

Be aware that optimization on historical data may lead to curve-fitting and poor forward performance

The indicator performs best when used as part of a comprehensive trading methodology that incorporates multiple forms of market analysis, sound risk management, and realistic expectations about win rates and drawdowns.

Arisa RSI Rebound Alert (v6.2)Short description:

Simple RSI-based rebound detection with ATR confirmation — designed for traders who prefer a clean and intuitive signal.

Full description:

This indicator detects oversold and rebound phases using RSI and confirms the strength of each rebound with ATR slope analysis.

It is optimized for deep correction phases (e.g. RSI 25→35 cross), helping traders catch early reversal signals while avoiding unnecessary noise.

💡 Recommended use:

• Timeframes: 30min–4h

• Ideal for short- to mid-term rebound trades

• Combine with Heikin-Ashi or volume expansion for higher accuracy

✨ Key Features:

• Clear oversold/rebound thresholds (default RSI <25 / cross-up >35)

• Background highlight for deep oversold conditions

• Visual markers for strong vs. weak rebounds (ATR slope filter)

• Alert-ready (three conditions included)

🪶 Concept:

This script is designed for traders who value simplicity and intuition — focusing on meaningful signals rather than automation overload.

It’s for those who still want to see and feel the market before taking action.

⸻

Author:

Arisa Sanjo (Japan)

Created with the support of GPT-5, based on live trading insights from October 2025.

License:

Free to use and modify with proper attribution.

If you redistribute or enhance this script, please mention “Based on Arisa RSI Rebound Alert (v6.2)” in your description.

Inverse VIX / Custom Inverse Line🎯 Main Idea

This indicator creates a line that moves opposite to the VIX (Volatility Index) — or any symbol you choose.

When VIX rises (fear increases), → this line goes down.

When VIX falls (market calm), → this line goes up.

It helps you visually understand market sentiment — calm periods (bullish) vs fear periods (bearish).

⚙️ Input Settings

Setting Description

Symbol to invert The symbol to invert. Default is CBOE:VIX.

Inverse mode The method used to invert the values. There are 3 options:

① Negate Simply flips the sign (multiplies by -1). Very straightforward.

② Reciprocal Uses the mathematical inverse (1 ÷ value). High values become smaller, and vice versa.

③ Inverse Normalized The most useful mode 🔥 — normalizes values between 0–100 and flips them, similar to an RSI.

Normalization lookback How many bars to use for normalization (default 252 = roughly one trading year).

Smoothing (SMA) Number of bars for smoothing (makes the line smoother).

Use log for reciprocal Uses logarithmic scaling to stabilize big swings.

Plot color / width Customize the line’s color and thickness.

Show original source If enabled, shows the original VIX line for comparison.

📈 How It Works

The script fetches the close price of the VIX (or your chosen symbol).

It applies the selected inversion method.

The inverted line is plotted on the chart.

In “Inverse Normalized” mode:

The range is 0–100.

Values above 75 = high optimism (market often overheated).

Values below 25 = high fear (potential buying opportunity).

A middle line at 50 marks neutral sentiment.

⚠️ Alerts

The indicator includes two default alerts when using “Inverse Normalized” mode:

🔔 Above 75: Market showing strong optimism (potential top or correction zone).

🔔 Below 25: Market showing fear (potential bottom or buy signal).

🧠 How to Use It

Use it on daily or weekly charts for clearer signals.

Compare it with SPX or NASDAQ:

When the Inverse VIX line rises, markets often go up.

When it falls, markets usually drop or consolidate.

Combine it with other indicators (e.g., RSI, MACD) for confirmation.

Keltner Channel Enhanced [DCAUT]█ Keltner Channel Enhanced

📊 ORIGINALITY & INNOVATION

The Keltner Channel Enhanced represents an important advancement over standard Keltner Channel implementations by introducing dual flexibility in moving average selection for both the middle band and ATR calculation. While traditional Keltner Channels typically use EMA for the middle band and RMA (Wilder's smoothing) for ATR, this enhanced version provides access to 25+ moving average algorithms for both components, enabling traders to fine-tune the indicator's behavior to match specific market characteristics and trading approaches.

Key Advancements:

Dual MA Algorithm Flexibility: Independent selection of moving average types for middle band (25+ options) and ATR smoothing (25+ options), allowing optimization of both trend identification and volatility measurement separately

Enhanced Trend Sensitivity: Ability to use faster algorithms (HMA, T3) for middle band while maintaining stable volatility measurement with traditional ATR smoothing, or vice versa for different trading strategies

Adaptive Volatility Measurement: Choice of ATR smoothing algorithm affects channel responsiveness to volatility changes, from highly reactive (SMA, EMA) to smoothly adaptive (RMA, TEMA)

Comprehensive Alert System: Five distinct alert conditions covering breakouts, trend changes, and volatility expansion, enabling automated monitoring without constant chart observation

Multi-Timeframe Compatibility: Works effectively across all timeframes from intraday scalping to long-term position trading, with independent optimization of trend and volatility components

This implementation addresses key limitations of standard Keltner Channels: fixed EMA/RMA combination may not suit all market conditions or trading styles. By decoupling the trend component from volatility measurement and allowing independent algorithm selection, traders can create highly customized configurations for specific instruments and market phases.

📐 MATHEMATICAL FOUNDATION

Keltner Channel Enhanced uses a three-component calculation system that combines a flexible moving average middle band with ATR-based (Average True Range) upper and lower channels, creating volatility-adjusted trend-following bands.

Core Calculation Process:

1. Middle Band (Basis) Calculation:

The basis line is calculated using the selected moving average algorithm applied to the price source over the specified period:

basis = ma(source, length, maType)

Supported algorithms include EMA (standard choice, trend-biased), SMA (balanced and symmetric), HMA (reduced lag), WMA, VWMA, TEMA, T3, KAMA, and 17+ others.

2. Average True Range (ATR) Calculation:

ATR measures market volatility by calculating the average of true ranges over the specified period:

trueRange = max(high - low, abs(high - close ), abs(low - close ))

atrValue = ma(trueRange, atrLength, atrMaType)

ATR smoothing algorithm significantly affects channel behavior, with options including RMA (standard, very smooth), SMA (moderate smoothness), EMA (fast adaptation), TEMA (smooth yet responsive), and others.

3. Channel Calculation:

Upper and lower channels are positioned at specified multiples of ATR from the basis:

upperChannel = basis + (multiplier × atrValue)

lowerChannel = basis - (multiplier × atrValue)

Standard multiplier is 2.0, providing channels that dynamically adjust width based on market volatility.

Keltner Channel vs. Bollinger Bands - Key Differences:

While both indicators create volatility-based channels, they use fundamentally different volatility measures:

Keltner Channel (ATR-based):

Uses Average True Range to measure actual price movement volatility

Incorporates gaps and limit moves through true range calculation

More stable in trending markets, less prone to extreme compression

Better reflects intraday volatility and trading range

Typically fewer band touches, making touches more significant

More suitable for trend-following strategies

Bollinger Bands (Standard Deviation-based):

Uses statistical standard deviation to measure price dispersion

Based on closing prices only, doesn't account for intraday range

Can compress significantly during consolidation (squeeze patterns)

More touches in ranging markets

Better suited for mean-reversion strategies

Provides statistical probability framework (95% within 2 standard deviations)

Algorithm Combination Effects:

The interaction between middle band MA type and ATR MA type creates different indicator characteristics:

Trend-Focused Configuration (Fast MA + Slow ATR): Middle band uses HMA/EMA/T3, ATR uses RMA/TEMA, quick trend changes with stable channel width, suitable for trend-following

Volatility-Focused Configuration (Slow MA + Fast ATR): Middle band uses SMA/WMA, ATR uses EMA/SMA, stable trend with dynamic channel width, suitable for volatility trading

Balanced Configuration (Standard EMA/RMA): Classic Keltner Channel behavior, time-tested combination, suitable for general-purpose trend following

Adaptive Configuration (KAMA + KAMA): Self-adjusting indicator responding to efficiency ratio, suitable for markets with varying trend strength and volatility regimes

📊 COMPREHENSIVE SIGNAL ANALYSIS

Keltner Channel Enhanced provides multiple signal categories optimized for trend-following and breakout strategies.

Channel Position Signals:

Upper Channel Interaction:

Price Touching Upper Channel: Strong bullish momentum, price moving more than typical volatility range suggests, potential continuation signal in established uptrends

Price Breaking Above Upper Channel: Exceptional strength, price exceeding normal volatility expectations, consider adding to long positions or tightening trailing stops

Price Riding Upper Channel: Sustained strong uptrend, characteristic of powerful bull moves, stay with trend and avoid premature profit-taking

Price Rejection at Upper Channel: Momentum exhaustion signal, consider profit-taking on longs or waiting for pullback to middle band for reentry

Lower Channel Interaction:

Price Touching Lower Channel: Strong bearish momentum, price moving more than typical volatility range suggests, potential continuation signal in established downtrends

Price Breaking Below Lower Channel: Exceptional weakness, price exceeding normal volatility expectations, consider adding to short positions or protecting against further downside

Price Riding Lower Channel: Sustained strong downtrend, characteristic of powerful bear moves, stay with trend and avoid premature covering

Price Rejection at Lower Channel: Momentum exhaustion signal, consider covering shorts or waiting for bounce to middle band for reentry

Middle Band (Basis) Signals:

Trend Direction Confirmation:

Price Above Basis: Bullish trend bias, middle band acts as dynamic support in uptrends, consider long positions or holding existing longs

Price Below Basis: Bearish trend bias, middle band acts as dynamic resistance in downtrends, consider short positions or avoiding longs

Price Crossing Above Basis: Potential trend change from bearish to bullish, early signal to establish long positions

Price Crossing Below Basis: Potential trend change from bullish to bearish, early signal to establish short positions or exit longs

Pullback Trading Strategy:

Uptrend Pullback: Price pulls back from upper channel to middle band, finds support, and resumes upward, ideal long entry point

Downtrend Bounce: Price bounces from lower channel to middle band, meets resistance, and resumes downward, ideal short entry point

Basis Test: Strong trends often show price respecting the middle band as support/resistance on pullbacks

Failed Test: Price breaking through middle band against trend direction signals potential reversal

Volatility-Based Signals:

Narrow Channels (Low Volatility):

Consolidation Phase: Channels contract during periods of reduced volatility and directionless price action

Breakout Preparation: Narrow channels often precede significant directional moves as volatility cycles

Trading Approach: Reduce position sizes, wait for breakout confirmation, avoid range-bound strategies within channels

Breakout Direction: Monitor for price breaking decisively outside channel range with expanding width

Wide Channels (High Volatility):

Trending Phase: Channels expand during strong directional moves and increased volatility

Momentum Confirmation: Wide channels confirm genuine trend with substantial volatility backing

Trading Approach: Trend-following strategies excel, wider stops necessary, mean-reversion strategies risky

Exhaustion Signs: Extreme channel width (historical highs) may signal approaching consolidation or reversal

Advanced Pattern Recognition:

Channel Walking Pattern:

Upper Channel Walk: Price consistently touches or exceeds upper channel while staying above basis, very strong uptrend signal, hold longs aggressively

Lower Channel Walk: Price consistently touches or exceeds lower channel while staying below basis, very strong downtrend signal, hold shorts aggressively

Basis Support/Resistance: During channel walks, price typically uses middle band as support/resistance on minor pullbacks

Pattern Break: Price crossing basis during channel walk signals potential trend exhaustion

Squeeze and Release Pattern:

Squeeze Phase: Channels narrow significantly, price consolidates near middle band, volatility contracts

Direction Clues: Watch for price positioning relative to basis during squeeze (above = bullish bias, below = bearish bias)

Release Trigger: Price breaking outside narrow channel range with expanding width confirms breakout

Follow-Through: Measure squeeze height and project from breakout point for initial profit targets

Channel Expansion Pattern:

Breakout Confirmation: Rapid channel widening confirms volatility increase and genuine trend establishment

Entry Timing: Enter positions early in expansion phase before trend becomes overextended

Risk Management: Use channel width to size stops appropriately, wider channels require wider stops

Basis Bounce Pattern:

Clean Bounce: Price touches middle band and immediately reverses, confirms trend strength and entry opportunity

Multiple Bounces: Repeated basis bounces indicate strong, sustainable trend

Bounce Failure: Price penetrating basis signals weakening trend and potential reversal

Divergence Analysis:

Price/Channel Divergence: Price makes new high/low while staying within channel (not reaching outer band), suggests momentum weakening

Width/Price Divergence: Price breaks to new extremes but channel width contracts, suggests move lacks conviction

Reversal Signal: Divergences often precede trend reversals or significant consolidation periods

Multi-Timeframe Analysis:

Keltner Channels work particularly well in multi-timeframe trend-following approaches:

Three-Timeframe Alignment:

Higher Timeframe (Weekly/Daily): Identify major trend direction, note price position relative to basis and channels

Intermediate Timeframe (Daily/4H): Identify pullback opportunities within higher timeframe trend

Lower Timeframe (4H/1H): Time precise entries when price touches middle band or lower channel (in uptrends) with rejection

Optimal Entry Conditions:

Best Long Entries: Higher timeframe in uptrend (price above basis), intermediate timeframe pulls back to basis, lower timeframe shows rejection at middle band or lower channel

Best Short Entries: Higher timeframe in downtrend (price below basis), intermediate timeframe bounces to basis, lower timeframe shows rejection at middle band or upper channel

Risk Management: Use higher timeframe channel width to set position sizing, stops below/above higher timeframe channels

🎯 STRATEGIC APPLICATIONS

Keltner Channel Enhanced excels in trend-following and breakout strategies across different market conditions.

Trend Following Strategy:

Setup Requirements:

Identify established trend with price consistently on one side of basis line

Wait for pullback to middle band (basis) or brief penetration through it

Confirm trend resumption with price rejection at basis and move back toward outer channel

Enter in trend direction with stop beyond basis line

Entry Rules:

Uptrend Entry:

Price pulls back from upper channel to middle band, shows support at basis (bullish candlestick, momentum divergence)

Enter long on rejection/bounce from basis with stop 1-2 ATR below basis

Aggressive: Enter on first touch; Conservative: Wait for confirmation candle

Downtrend Entry:

Price bounces from lower channel to middle band, shows resistance at basis (bearish candlestick, momentum divergence)

Enter short on rejection/reversal from basis with stop 1-2 ATR above basis

Aggressive: Enter on first touch; Conservative: Wait for confirmation candle

Trend Management:

Trailing Stop: Use basis line as dynamic trailing stop, exit if price closes beyond basis against position

Profit Taking: Take partial profits at opposite channel, move stops to basis

Position Additions: Add to winners on subsequent basis bounces if trend intact

Breakout Strategy:

Setup Requirements:

Identify consolidation period with contracting channel width

Monitor price action near middle band with reduced volatility

Wait for decisive breakout beyond channel range with expanding width

Enter in breakout direction after confirmation

Breakout Confirmation:

Price breaks clearly outside channel (upper for longs, lower for shorts), channel width begins expanding from contracted state

Volume increases significantly on breakout (if using volume analysis)

Price sustains outside channel for multiple bars without immediate reversal

Entry Approaches:

Aggressive: Enter on initial break with stop at opposite channel or basis, use smaller position size

Conservative: Wait for pullback to broken channel level, enter on rejection and resumption, tighter stop

Volatility-Based Position Sizing:

Adjust position sizing based on channel width (ATR-based volatility):

Wide Channels (High ATR): Reduce position size as stops must be wider, calculate position size using ATR-based risk calculation: Risk / (Stop Distance in ATR × ATR Value)

Narrow Channels (Low ATR): Increase position size as stops can be tighter, be cautious of impending volatility expansion

ATR-Based Risk Management: Use ATR-based risk calculations, position size = 0.01 × Capital / (2 × ATR), use multiples of ATR (1-2 ATR) for adaptive stops

Algorithm Selection Guidelines:

Different market conditions benefit from different algorithm combinations:

Strong Trending Markets: Middle band use EMA or HMA, ATR use RMA, capture trends quickly while maintaining stable channel width

Choppy/Ranging Markets: Middle band use SMA or WMA, ATR use SMA or WMA, avoid false trend signals while identifying genuine reversals

Volatile Markets: Middle band and ATR both use KAMA or FRAMA, self-adjusting to changing market conditions reduces manual optimization

Breakout Trading: Middle band use SMA, ATR use EMA or SMA, stable trend with dynamic channels highlights volatility expansion early

Scalping/Day Trading: Middle band use HMA or T3, ATR use EMA or TEMA, both components respond quickly

Position Trading: Middle band use EMA/TEMA/T3, ATR use RMA or TEMA, filter out noise for long-term trend-following

📋 DETAILED PARAMETER CONFIGURATION

Understanding and optimizing parameters is essential for adapting Keltner Channel Enhanced to specific trading approaches.

Source Parameter:

Close (Most Common): Uses closing price, reflects daily settlement, best for end-of-day analysis and position trading, standard choice

HL2 (Median Price): Smooths out closing bias, better represents full daily range in volatile markets, good for swing trading

HLC3 (Typical Price): Gives more weight to close while including full range, popular for intraday applications, slightly more responsive than HL2

OHLC4 (Average Price): Most comprehensive price representation, smoothest option, good for gap-prone markets or highly volatile instruments

Length Parameter:

Controls the lookback period for middle band (basis) calculation:

Short Periods (10-15): Very responsive to price changes, suitable for day trading and scalping, higher false signal rate

Standard Period (20 - Default): Represents approximately one month of trading, good balance between responsiveness and stability, suitable for swing and position trading

Medium Periods (30-50): Smoother trend identification, fewer false signals, better for position trading and longer holding periods

Long Periods (50+): Very smooth, identifies major trends only, minimal false signals but significant lag, suitable for long-term investment

Optimization by Timeframe: 1-15 minute charts use 10-20 period, 30-60 minute charts use 20-30 period, 4-hour to daily charts use 20-40 period, weekly charts use 20-30 weeks.

ATR Length Parameter:

Controls the lookback period for Average True Range calculation, affecting channel width:

Short ATR Periods (5-10): Very responsive to recent volatility changes, standard is 10 (Keltner's original specification), may be too reactive in whipsaw conditions

Standard ATR Period (10 - Default): Chester Keltner's original specification, good balance between responsiveness and stability, most widely used

Medium ATR Periods (14-20): Smoother channel width, ATR 14 aligns with Wilder's original ATR specification, good for position trading

Long ATR Periods (20+): Very smooth channel width, suitable for long-term trend-following

Length vs. ATR Length Relationship: Equal values (20/20) provide balanced responsiveness, longer ATR (20/14) gives more stable channel width, shorter ATR (20/10) is standard configuration, much shorter ATR (20/5) creates very dynamic channels.

Multiplier Parameter:

Controls channel width by setting ATR multiples:

Lower Values (1.0-1.5): Tighter channels with frequent price touches, more trading signals, higher false signal rate, better for range-bound and mean-reversion strategies

Standard Value (2.0 - Default): Chester Keltner's recommended setting, good balance between signal frequency and reliability, suitable for both trending and ranging strategies

Higher Values (2.5-3.0): Wider channels with less frequent touches, fewer but potentially higher-quality signals, better for strong trending markets

Market-Specific Optimization: High volatility markets (crypto, small-caps) use 2.5-3.0 multiplier, medium volatility markets (major forex, large-caps) use 2.0 multiplier, low volatility markets (bonds, utilities) use 1.5-2.0 multiplier.

MA Type Parameter (Middle Band):

Critical selection that determines trend identification characteristics:

EMA (Exponential Moving Average - Default): Standard Keltner Channel choice, Chester Keltner's original specification, emphasizes recent prices, faster response to trend changes, suitable for all timeframes

SMA (Simple Moving Average): Equal weighting of all data points, no directional bias, slower than EMA, better for ranging markets and mean-reversion

HMA (Hull Moving Average): Minimal lag with smooth output, excellent for fast trend identification, best for day trading and scalping

TEMA (Triple Exponential Moving Average): Advanced smoothing with reduced lag, responsive to trends while filtering noise, suitable for volatile markets

T3 (Tillson T3): Very smooth with minimal lag, excellent for established trend identification, suitable for position trading

KAMA (Kaufman Adaptive Moving Average): Automatically adjusts speed based on market efficiency, slow in ranging markets, fast in trends, suitable for markets with varying conditions

ATR MA Type Parameter:

Determines how Average True Range is smoothed, affecting channel width stability:

RMA (Wilder's Smoothing - Default): J. Welles Wilder's original ATR smoothing method, very smooth, slow to adapt to volatility changes, provides stable channel width

SMA (Simple Moving Average): Equal weighting, moderate smoothness, faster response to volatility changes than RMA, more dynamic channel width

EMA (Exponential Moving Average): Emphasizes recent volatility, quick adaptation to new volatility regimes, very responsive channel width changes

TEMA (Triple Exponential Moving Average): Smooth yet responsive, good balance for varying volatility, suitable for most trading styles

Parameter Combination Strategies:

Conservative Trend-Following: Length 30/ATR Length 20/Multiplier 2.5, MA Type EMA or TEMA/ATR MA Type RMA, smooth trend with stable wide channels, suitable for position trading

Standard Balanced Approach: Length 20/ATR Length 10/Multiplier 2.0, MA Type EMA/ATR MA Type RMA, classic Keltner Channel configuration, suitable for general purpose swing trading

Aggressive Day Trading: Length 10-15/ATR Length 5-7/Multiplier 1.5-2.0, MA Type HMA or EMA/ATR MA Type EMA or SMA, fast trend with dynamic channels, suitable for scalping and day trading

Breakout Specialist: Length 20-30/ATR Length 5-10/Multiplier 2.0, MA Type SMA or WMA/ATR MA Type EMA or SMA, stable trend with responsive channel width

Adaptive All-Conditions: Length 20/ATR Length 10/Multiplier 2.0, MA Type KAMA or FRAMA/ATR MA Type KAMA or TEMA, self-adjusting to market conditions

Offset Parameter:

Controls horizontal positioning of channels on chart. Positive values shift channels to the right (future) for visual projection, negative values shift left (past) for historical analysis, zero (default) aligns with current price bars for real-time signal analysis. Offset affects only visual display, not alert conditions or actual calculations.

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Keltner Channel Enhanced provides improvements over standard implementations while maintaining proven effectiveness.

Response Characteristics:

Standard EMA/RMA Configuration: Moderate trend lag (approximately 0.4 × length periods), smooth and stable channel width from RMA smoothing, good balance for most market conditions

Fast HMA/EMA Configuration: Approximately 60% reduction in trend lag compared to EMA, responsive channel width from EMA ATR smoothing, suitable for quick trend changes and breakouts

Adaptive KAMA/KAMA Configuration: Variable lag based on market efficiency, automatic adjustment to trending vs. ranging conditions, self-optimizing behavior reduces manual intervention

Comparison with Traditional Keltner Channels:

Enhanced Version Advantages:

Dual Algorithm Flexibility: Independent MA selection for trend and volatility vs. fixed EMA/RMA, separate tuning of trend responsiveness and channel stability

Market Adaptation: Choose configurations optimized for specific instruments and conditions, customize for scalping, swing, or position trading preferences

Comprehensive Alerts: Enhanced alert system including channel expansion detection

Traditional Version Advantages:

Simplicity: Fewer parameters, easier to understand and implement

Standardization: Fixed EMA/RMA combination ensures consistency across users

Research Base: Decades of backtesting and research on standard configuration

When to Use Enhanced Version: Trading multiple instruments with different characteristics, switching between trending and ranging markets, employing different strategies, algorithm-based trading systems requiring customization, seeking optimization for specific trading style and timeframe.

When to Use Standard Version: Beginning traders learning Keltner Channel concepts, following published research or trading systems, preferring simplicity and standardization, wanting to avoid optimization and curve-fitting risks.

Performance Across Market Conditions:

Strong Trending Markets: EMA or HMA basis with RMA or TEMA ATR smoothing provides quicker trend identification, pullbacks to basis offer excellent entry opportunities

Choppy/Ranging Markets: SMA or WMA basis with RMA ATR smoothing and lower multipliers, channel bounce strategies work well, avoid false breakouts

Volatile Markets: KAMA or FRAMA with EMA or TEMA, adaptive algorithms excel by automatic adjustment, wider multipliers (2.5-3.0) accommodate large price swings

Low Volatility/Consolidation: Channels narrow significantly indicating consolidation, algorithm choice less impactful, focus on detecting channel width contraction for breakout preparation

Keltner Channel vs. Bollinger Bands - Usage Comparison:

Favor Keltner Channels When: Trend-following is primary strategy, trading volatile instruments with gaps, want ATR-based volatility measurement, prefer fewer higher-quality channel touches, seeking stable channel width during trends.

Favor Bollinger Bands When: Mean-reversion is primary strategy, trading instruments with limited gaps, want statistical framework based on standard deviation, need squeeze patterns for breakout identification, prefer more frequent trading opportunities.

Use Both Together: Bollinger Band squeeze + Keltner Channel breakout is powerful combination, price outside Bollinger Bands but inside Keltner Channels indicates moderate signal, price outside both indicates very strong signal, Bollinger Bands for entries and Keltner Channels for trend confirmation.

Limitations and Considerations:

General Limitations:

Lagging Indicator: All moving averages lag price, even with reduced-lag algorithms

Trend-Dependent: Works best in trending markets, less effective in choppy conditions

No Direction Prediction: Indicates volatility and deviation, not future direction, requires confirmation

Enhanced Version Specific Considerations:

Optimization Risk: More parameters increase risk of curve-fitting historical data

Complexity: Additional choices may overwhelm beginning traders

Backtesting Challenges: Different algorithms produce different historical results

Mitigation Strategies:

Use Confirmation: Combine with momentum indicators (RSI, MACD), volume, or price action

Test Parameter Robustness: Ensure parameters work across range of values, not just optimized ones

Multi-Timeframe Analysis: Confirm signals across different timeframes

Proper Risk Management: Use appropriate position sizing and stops

Start Simple: Begin with standard EMA/RMA before exploring alternatives

Optimal Usage Recommendations:

For Maximum Effectiveness:

Start with standard EMA/RMA configuration to understand classic behavior

Experiment with alternatives on demo account or paper trading

Match algorithm combination to market condition and trading style

Use channel width analysis to identify market phases

Combine with complementary indicators for confirmation

Implement strict risk management using ATR-based position sizing

Focus on high-quality setups rather than trading every signal

Respect the trend: trade with basis direction for higher probability

Complementary Indicators:

RSI or Stochastic: Confirm momentum at channel extremes

MACD: Confirm trend direction and momentum shifts

Volume: Validate breakouts and trend strength

ADX: Measure trend strength, avoid Keltner signals in weak trends

Support/Resistance: Combine with traditional levels for high-probability setups

Bollinger Bands: Use together for enhanced breakout and volatility analysis

USAGE NOTES

This indicator is designed for technical analysis and educational purposes. Keltner Channel Enhanced has limitations and should not be used as the sole basis for trading decisions. While the flexible moving average selection for both trend and volatility components provides valuable adaptability across different market conditions, algorithm performance varies with market conditions, and past characteristics do not guarantee future results.

Key considerations:

Always use multiple forms of analysis and confirmation before entering trades

Backtest any parameter combination thoroughly before live trading

Be aware that optimization can lead to curve-fitting if not done carefully

Start with standard EMA/RMA settings and adjust only when specific conditions warrant

Understand that no moving average algorithm can eliminate lag entirely

Consider market regime (trending, ranging, volatile) when selecting parameters

Use ATR-based position sizing and risk management on every trade

Keltner Channels work best in trending markets, less effective in choppy conditions

Respect the trend direction indicated by price position relative to basis line

The enhanced flexibility of dual algorithm selection provides powerful tools for adaptation but requires responsible use, thorough understanding of how different algorithms behave under various market conditions, and disciplined risk management.

Total Info Indicator by MikePenzin

Install & Add to Chart

• Copy the script into Pine Editor → click Add to Chart .

• Open the ⚙️ Settings → Inputs to customize.

What It Does

• Displays key info in a floating table — trend, volume, ATR, RSI, stop loss, and more.

• Detects breakouts , smart SELL signals , and opening strength .

• Uses emojis and colours to make trends easy to read: 🟢 good, 🟡 neutral, 🔴 risky.

For Swing Traders

• Works best on Daily or 4H charts.

• Watch for 🟢 Uptrend + ⚡BUY / 🔥BUY breakout signals.

• Use ATR-based Stop Loss (shown in table).

• Avoid new entries a few days before earnings.

Suggested Setup

• 20/50/150 MA Lines: ON

• 200 MA Line: optional

• ATR Multiplier: 1.3

• Breakout Detection: ON (Volume + RSI + Trend filters)

• Smart SELLs: ON (RSI 70, EMA 20)

• Pivots: ON for quick swing levels

How to Read

• MA Row: 🟢 = price above MA (bullish).

• ATR/Stop Loss: Suggests where to place protective stop.

• Volume Info: Today’s vs 20-day average, plus pace.

• RSI & CCI: Shows momentum and overbought/oversold levels.

• Breakouts: ⚡BUY (early), 🔥BUY (confirmed).

• Smart SELLs: RSI🔴 / DIV🟣 / EMA🔵 mean potential exit zones.

Example Use

1️⃣ Find stocks with Uptrend 🟢 , rising volume, and ⚡BUY signal.

2️⃣ Enter near breakout; set Stop = shown level.

3️⃣ Take profits or trail when Smart SELLs appear or RSI peaks.

Tips

• Choose table corner under “Table Visualization.”

• Reduce clutter on small timeframes (turn off Pivots/200 MA).

• Use “Volume speed” to spot surging interest before breakouts.

• Compatible with most equities and ETFs.

Disclaimer

This script is for education & analysis only .

Not financial advice — always manage your own risk.

Crypto Mean Reversion System (Pullback & Bounce)Mean Reversion Theory

The indicator operates on the principle that extreme price movements in crypto markets tend to revert toward their mean over time.

Consider this a valuable aid for your dollar-cost averaging strategy, effectively identifying periods ripe for accumulating or divesting from the market.

Research shows that:

Short-term momentum often persists briefly after surges, but extreme moves trigger mean reversion

Sharp drops exhibit strong bounce patterns, especially after capitulation events

Longer timeframes (7-day) show stronger mean reversion tendencies than shorter ones (1-day)

Timeframe Analysis

1-Day Timeframe

Pullback probabilities: 45-85% depending on surge magnitude

Bounce probabilities: 55-95% depending on drop severity

Captures immediate overextension and panic selling

More volatile but faster signal generation

7-Day Timeframe

Pullback probabilities: 50-90% (higher confidence)

Bounce probabilities: 50-90% (slightly moderated)

Filters out noise and identifies sustained trends

Stronger mean reversion signals due to extended moves

Probability Tiers

Pullback Risk (After Surges)

Moderate (45-60%): 5-10% surge → Expected -3% to -12% pullback

High (55-70%): 10-15% surge → Expected -5% to -18% pullback

Very High (65-80%): 15-25% surge → Expected -10% to -25% pullback

Extreme (75-90%): 25%+ surge → Expected -15% to -40% pullback

Bounce Probability (After Drops)

Moderate (55-65%): -5% to -10% drop → Expected +3% to +10% bounce

High (65-75%): -10% to -15% drop → Expected +6% to +18% bounce

Very High (75-85%): -15% to -25% drop → Expected +10% to +30% bounce

Extreme (85-95%): -25%+ drop → Expected +18% to +45% bounce

The probability ranges are derived from:

Crypto volatility patterns: Higher volatility than traditional assets creates stronger mean reversion

Behavioral finance: Extreme moves trigger emotional trading (FOMO/panic) that reverses

Historical backtesting: Probability estimates based on typical reversion patterns in crypto markets

Timeframe correlation: Longer timeframes show increased reversion probability due to reduced noise

Key Features

Dual-direction signals: Identifies both overbought (pullback) and oversold (bounce) conditions

Multi-timeframe confirmation: 1D and 7D analysis for different trading styles

Customizable thresholds: Adjust sensitivity based on asset volatility

Visual alerts: Color-coded labels and table for quick assessment

Risk categorization: Clear severity levels for position sizing

Uptrick: Volatility Adjusted TrailIntroduction

The "Uptrick: Volatility Adjusted Trail" is a dynamic trailing band indicator. It adapts in real time to changing market conditions by adjusting both to volatility and trend consistency. Inspired by Supertrend-style logic, it enhances traditional approaches by introducing adaptive mechanisms for more context-sensitive behavior in both trending and consolidating environments.

Overview

This indicator combines an exponential moving average (EMA) as its basis with an Average True Range (ATR)-derived multiplier that adjusts dynamically. Unlike fixed-multiplier tools, this indicator modifies its band distances in real time according to volatility expansion and trend persistence. The result is a trailing system that adapts to the prevailing market regime, providing traders with clearer signals for trend bias, stop placement, and potential momentum shifts.

Originality

The script’s originality lies in its multi-layered approach to trail calculation. It introduces a real-time ATR multiplier adjustment driven by two factors: a volatility expansion ratio and a trend persistence model. The expansion ratio compares the current ATR to its moving average, making the indicator more sensitive during volatile conditions and less sensitive during quieter periods. The trend persistence model assesses directional consistency to widen the bands during sustained trends. This dual adjustment method creates a system that evolves with market behavior, making it more responsive and adaptive than static-band or fixed-multiplier alternatives.

Components & Inspiration

This indicator was designed with specific components that work together:

Exponential Moving Average (EMA): Chosen as the central baseline because it responds faster to recent price changes than a simple moving average, providing a more current reference for trailing bands.

Average True Range (ATR): Used as the volatility measure because it accounts for both intraday and gap movement, making it a robust and widely accepted standard for market volatility.

Dynamic Multiplier: The multiplier is adjusted by both volatility expansion and trend persistence to produce bands that tighten during low volatility and widen during consistent trends. This combination was chosen to give the indicator the ability to self-regulate across different market regimes.

Trend Persistence Model: Integrated to assess directional consistency, ensuring the bands expand during strong trends, which can prevent premature stop-outs.

Flip Confirmation Logic: Added to filter out noise by requiring multiple bar closes beyond a band before confirming a state change, reducing false reversals.

For inspiration, the indicator draws on the core idea behind Supertrend—using a baseline and volatility-derived bands to define trailing stop levels. However, while Supertrend uses a fixed ATR multiplier, this indicator introduces a dynamic multiplier system and persistence weighting, making it more adaptive and suited for varying conditions.

Inputs and Parameters

Basis EMA Length

Defines the period for the EMA that serves as the core price reference.

ATR Length

Sets the lookback period for the Average True Range calculation used in band spacing.

Base ATR Mult

The base multiplier applied to ATR before adjustments. Forms the starting scale of the band offset.

Volatility Expansion Sensitivity

Controls how strongly the band spacing reacts to short-term volatility bursts. Higher values create more pronounced band expansions or contractions.

Trend Persistence Window

Determines how many bars are used to calculate directional trend consistency using a smoothed step function.

Persistence Impact

Scales how much influence the trend persistence has on band widening. Values range from 0 (no effect) to 1 (maximum effect).

Min Effective Mult

Sets the minimum value that the adjusted multiplier can reach. Prevents the bands from becoming too narrow.

Max Effective Mult

Sets the maximum value the adjusted multiplier can reach. Prevents the bands from over-expanding during high volatility.

Bars Above/Below to Confirm Flip

Number of consecutive bars required to close above or below the opposing trail before confirming a bullish or bearish flip. Helps reduce noise and false signals.

Show Flip Labels

Enables or disables the display of flip markers on the chart.

Label Size

Allows users to adjust the size of flip labels from Tiny to Huge.

Label ATR Offset

Adjusts the vertical placement of flip labels in relation to the trail using an ATR-based offset.

Features and Logic

EMA Basis: All calculations stem from an EMA that tracks the centerline of price action.

Dynamic ATR Multiplier: The ATR multiplier adjusts in real time based on volatility expansion and trend persistence.

Clamped Multiplier: The adjusted multiplier is limited between user-defined minimum and maximum values to keep the band scale practical.

Upper and Lower Bands: Bands are plotted above and below the EMA using the dynamic multiplier and ATR values.

Trailing Logic: The script uses Supertrend-style trailing logic, updating the active band in the current trend direction and resetting the opposite band.

Trend State Detection: A state variable tracks the current market regime (bullish, bearish, or neutral). Transitions are confirmed only after a user-specified number of bars close beyond the respective bands.

Visual Elements: Trail lines and fill zones are color-coded (bullish cyan, bearish magenta). Candlestick and bar colors match the trend state. Optional flip labels mark confirmed transitions.

Alerts: Built-in alert conditions allow users to receive real-time notifications for bullish or bearish flips.

Usage Guidelines

This indicator can be used for:

Defining context-aware dynamic stop levels that adjust with market behavior.

Identifying trend direction and reversal points based on adaptive logic.

Filtering entry or exit signals during trending vs. consolidating conditions.

Supplementing trade management strategies with responsive visual markers.

Entering long or short positions based on the appearance of flip labels and managing stop losses by following the adaptive trail.

Traders may tune the parameters to suit different trading styles or timeframes. For example, lower ATR and EMA values may suit intraday setups, while longer settings may benefit swing or positional trading.

Summary

The "Uptrick: Volatility Adjusted Trail" provides a flexible, adaptive trailing band system that accounts for both volatility and directional consistency. By combining an EMA baseline with a dynamic ATR multiplier influenced by volatility expansion and trend persistence, it creates a context-sensitive trailing system that aligns with changing market conditions. Customizable confirmation, flip labels, alerts, and dynamic visual cues make it a versatile tool for trend-following, breakout filtering, and trailing stop logic.

Disclaimer

This indicator is provided for educational and research purposes only. It does not constitute financial advice. Trading involves risk, and past performance does not guarantee future results. Always conduct your own analysis and risk management before making trading decisions.

Continuation Suite v1 — 5m/15mContinuation Suite v1 — 5m/15m (Non-Repainting, S/R + Trend Continuation)

What it does

Continuation Suite v1 is a practical intraday toolkit that combines non-repainting trend-continuation signals with auto-built Support/Resistance (S/R) from confirmed pivots. It’s designed for fast, liquid names on 5m charts with an optional 15m higher-timeframe (HTF) overlay. You get: stacked-EMA bias, disciplined pullback+reclaim entries, optional volume/volatility gates, a “Strong” signal tier, solid S/R lines or zones, and a compact dashboard for fast reads.

⸻

Why traders use it

• Clear bias using fast/mid/slow EMA stacking.

• Actionable entries that require a pullback, a reclaim, and (optionally) a minor break of prior extremes.