Bitcoin Golden Ratio Fibonacci IndicatorI didn't see this one already it isn't my original idea either. I pulled the formula's from an article on medium, I also added few bear market bottom fib indicators.

Credit to the article I pulled the formula from.

The Golden Ratio Multiplier

Unlocking the mathematically organic nature of Bitcoin adoption

Go to the profile of Philip Swift (@PositiveCrypto)

Philip Swift (@PositiveCrypto)

Jun 17, 2019

By Philip Swift

Release Notes: Fixed spelling error on title, added a couple long and short labels for the top and bottom indicator.

"GOLD" için komut dosyalarını ara

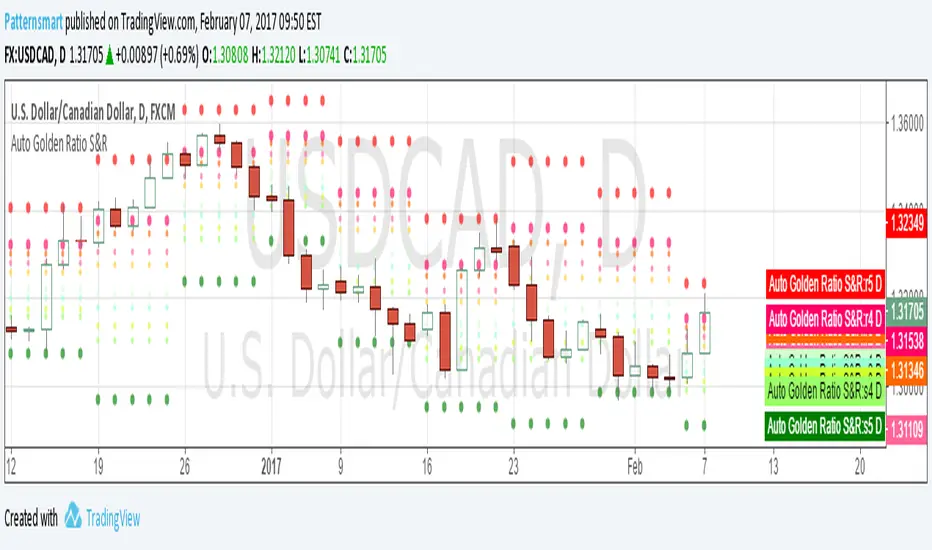

Automatic Golden Ratio Support & ResistanceThe golden ratio is also called the golden mean or golden section.

It has been used to analyze the proportions of natural objects as well as man-made systems such as financial markets.

The mathematics of the golden ratio and of the Fibonacci sequence is intimately interconnected. The Fibonacci sequence is: 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, ....

This Golden Ratio indicator automatically plots 5 support levels and 5 resistance levels based on the golden ratio for current timeframe. It shows a possible price range for current session, you can easily identify the major and minor support/resistance levels from the chart.

The levels of support and resistance are formed at the beginning of a new session

This indicator works on all default time frames.

It will never repaint.

There is no parameter. All you need to do is to load it to your chart.

Click the image links to view it in original size.

3.bp.blogspot.com

2.bp.blogspot.com

2.bp.blogspot.com

3.bp.blogspot.com

2.bp.blogspot.com

2.bp.blogspot.com

1.bp.blogspot.com

////////////////////////////////////////////////////////////

// Technical Analysis & Research Patternsmart

//

// Custom indicators, Strategies, SCAN, Screener, Backtesting, Converting service for:

// Tradingview, NinjaTrader, Thinkorswim, MetaTrader, MetaStock, Multicharts, Prorealtime, etc.

////////////////////////////////////////////////////////////

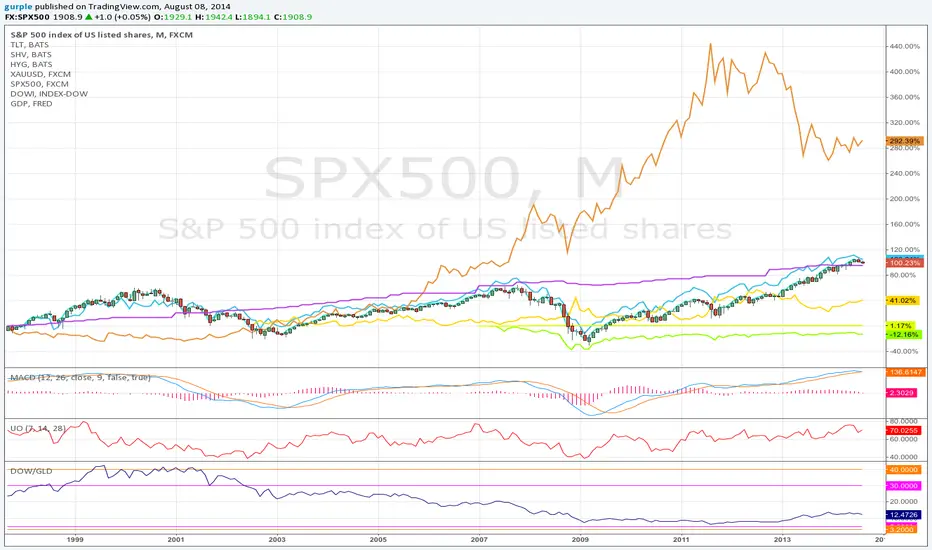

DOW / GOLD RatioThis indicator shows the ratio between the DJIA and the price of gold. When the ratio is below 5 it is generally accepted that a rotation from commodities to equities should be investigated. When the ratio is above 30 it is, likewise, advised to consider rotating from equities to commodities.

This is a modest improvement of the script to mark the key thresholds where equities/commodities holdings rotations could be prudent. I’m sure I’ll be submitting a number of instances of these scripts as I learn the syntax and features while developing them.

Gold DropGold Drop – Intraday Trading System (India Markets)

Gold Drop is a rule-based intraday trading strategy designed specifically for Indian index trading (BANKNIFTY / NIFTY), combining trend, momentum, strength, and fixed reference levels to deliver consistent and disciplined trade execution.

The system is built to avoid emotional trading, over-trading, and shifting levels during the session

Gold Scalping MACD ProGold Scalping MACD Pro is a custom-built technical indicator specifically optimized for gold (XAUUSD) scalping. It is based on an advanced adaptation of the classic MACD (Moving Average Convergence Divergence) concept, enhanced to provide faster, clearer, and more reliable signals in highly volatile gold markets.

🔹 Core Purpose

The indicator is designed to:

Capture short-term momentum shifts

Reduce market noise

Improve entry and exit timing during fast price movements

This makes it particularly effective for intraday and scalping strategies.

🔹 Key Features

Enhanced MACD-based momentum calculation for higher sensitivity

Early buy and sell signals during strong momentum phases

Noise filtering to reduce false signals in sideways markets

Optimized for gold’s volatility characteristics

Best performance on lower timeframes (M1, M5, M15)

🔹 How It Works

Gold Scalping MACD Pro analyzes the relationship between fast and slow moving averages, combined with momentum smoothing techniques.

By focusing on momentum strength rather than lagging confirmation, the indicator helps traders:

Identify high-probability scalping opportunities

Confirm short-term trend direction

Avoid weak or low-momentum setups

🔹 Best Use

Gold (XAUUSD) scalping

Momentum-based trading strategies

Trend confirmation on lower timeframes

Used alongside price action, support & resistance, or session timing

⚠️ Risk Disclaimer

Gold Scalping MACD Pro is a technical analysis tool and does not provide trading advice. Trading leveraged instruments such as gold involves significant risk. Proper risk management and confirmation from other analysis methods are strongly recommended.

KINETIC GOLD NQ Velocity Breakout [Ash_TheTrader]

🚀 Stop Guessing. Start Scalping with Physics.

Introducing the KINETIC GOLD NQ ⚡ VELOCITY BREAKOUT System

Author: Ash_TheTrader

Assets: Gold (XAUUSD), Nasdaq (US100), Bitcoin (BTC)

Style: High-Frequency Scalping (M1/M5)

---

🛑 The Problem: Why Most Indicators Fail

You’ve been there. The RSI says "Oversold," so you buy. But price keeps crashing. The Moving Average crosses over, so you enter. But the trend is already over.

Why? Because those indicators are lagging . They tell you what happened 10 candles ago.

⚡ The Solution: The "Physics" of Price

Markets move like objects in the real world. They have Velocity (Speed) and Momentum (Mass).

The Kinetic Velocity Breakout (KMB) system doesn't look at "Overbought" or "Oversold." It looks for FORCE .

It answers one simple question: Is the market moving fast enough to pay me?

---

🧠 The 4 "Smart Logic" Features

1. The Velocity Speedometer 🏎️

Most candles are "noise." This system ignores them. It uses a Normalized Volatility Engine to detect when price hits "WARP SPEED".

• Blue: Slow (Cruising). Don't touch.

• Yellow: Accelerating. Get ready.

• Red: WARP SPEED. Institutional money is entering.

2. The 1.5x Impulse Rule 💥

The algorithm strictly enforces the "1.5x Law." A signal ONLY fires if the breakout candle is 1.5 times larger than the average of the last 3 candles.

• Result? No more fakeouts. We only trade real expansions.

3. "Smart Mode" AI Dashboard 🖥️

A heads-up display (HUD) lives on your chart, auto-detecting your trading environment:

• Auto-Session: Tells you if you are in London, New York, or Asia.

• Risk Mode: Shows if you are using "Aggressive" or "Normal" logic.

• Status: Gives you a text readout like "READY ⚡" or "WAIT..."

4. Auto-Pilot Risk Management 🛡️

Scalping is fast. You don't have time to calculate Pips.

• The script draws the lines for you.

• As soon as a "ROCKET" signal appears, a Green TP Line (2x Reward) and Red SL Line appear instantly.

---

🎮 How to Trade: The 3-Step "Kinetic" Strategy

This strategy is designed for Gold (XAUUSD) and Nasdaq (US100) on the 5-Minute Timeframe .

Step 1: The "Yellow" Warning ⚠️

Watch the Smart Structure Lines (Dashed Lines).

• If the candles turn Yellow or the Dashboard says "FAST" , wake up.

• This means pressure is building against a key level.

Step 2: The "Warp" Trigger 🚀

Wait for a Confirmed Breakout . You are looking for:

1. A candle closes OUTSIDE the dashed structure line.

2. The candle color is NEON CYAN (Bullish) or NEON MAGENTA (Bearish).

3. The Signal Label appears: "ROCKET" (Buy) or "DROP" (Sell).

👉 Rule: No Label? No Trade. The 1.5x Logic saves you from bad trades.

Step 3: The Execution 💰

1. Enter at the close of the signal candle.

2. Stop Loss: Place it exactly on the Red Line provided by the indicator.

3. Take Profit: Place it on the Green Line .

4. Walk away. Let the physics work.

---

⚙️ Customizing Your Style

The script comes with two built-in "Personalities":

🛡️ Normal Scalper (Default)

• Best for: New traders, Funded Accounts.

• Logic: Waits for strong confirmation. High Win Rate.

• Risk: 1:2 Risk/Reward.

⚠️ QuickScalper (Aggressive)

• Best for: Gold M1, Volatility Hunters.

• Logic: Enters earlier on 1.2x Impulse. More signals, faster exits.

• Risk: 1:1.5 Risk/Reward (Grab the cash and go).

---

👇 Get the Code

Search for: KINETIC ⚡ in the TradingView library.

"Markets are physics. Trade the Velocity, not the noise." — @Ash_TheTrader

Gold Trend Tracker - TREND TRACKER DG25Gold Trend Tracker - Complete All-In-One Trading System

A professional, institutional-grade trading system specifically optimized for Gold (XAU/USD) that combines multiple technical indicators with session-based filtering and real-time performance tracking. No external indicators required - everything you need is built right in!

🎯 CORE FEATURES

Multi-Layered Confirmation System:

Dynamic EMA trend filter (default 10-period) with color-coded visualization

Optional secondary confirmation EMA (21-period) for stronger validation

3-minute MACD analysis with histogram tracking and direction monitoring

MACD bounce detection for high-probability continuation entries

Built-in Stochastic RSI (K=3, D=3, RSI Length=14, Stochastic Length=14)

Option to connect external Stochastic RSI if preferred

Intelligent Signal Generation:

Clear BUY/SELL triangles plotted directly on price chart

Minimum bars filter to eliminate signal spam and overtrading

Higher timeframe signal overlay (optional) - see 3min signals on 15min chart

Visual Stochastic RSI threshold cross markers (customizable shapes & sizes)

"Show Only First Cross" option to reduce visual clutter

Comprehensive alert system for all signal types

Advanced Session Management:

Pre-configured trading sessions: Asian (1-4am), London (6-9am), NY (12-3pm)

Timezone-aware filtering supporting major financial centers:

Europe/London

America/New_York

America/Chicago

Europe/Paris

Asia/Tokyo

Asia/Dubai

Color-coded session backgrounds (purple/blue/orange)

Individual session toggle switches

24/7 mode for continuous trading (crypto/forex)

Signals only generate during active sessions

Real-Time Performance Tracking:

Live P/L calculation since last signal entry

Customizable lot size for accurate dollar calculations

Pip movement tracking with automatic conversion

Last signal type and duration display

Performance color-coding (green profits, red losses)

Professional Dashboard:

Clean, scalable interface (Small/Medium/Large sizing)

Current time and active session display

Trading status indicator (TRADING/PAUSED/24/7)

Price position relative to Main EMA (ABOVE ↑ / BELOW ↓)

Confirmation EMA status (when enabled)

3-minute MACD color, direction arrow, and bar count

Stochastic RSI value with color-coded status

RSI status: BULLISH/BEARISH/NEUTRAL

Source type indicator (Built-in/External)

Large, clear SIGNAL display: BUY NOW / SELL NOW / WAIT

Performance summary: signal type + price change + dollar value

📊 HOW THE SYSTEM WORKS

BUY Signal Requirements:

✓ Price trading ABOVE main EMA (bullish trend confirmation)

✓ 3-minute MACD crosses above zero OR bounces higher after crossover

✓ Stochastic RSI K-line above bullish threshold (default 50)

✓ Within an active trading session (if session filter enabled)

✓ Confirmation EMA aligned (if secondary EMA enabled)

✓ Minimum bars since last signal met (prevents overtrading)

SELL Signal Requirements:

✓ Price trading BELOW main EMA (bearish trend confirmation)

✓ 3-minute MACD crosses below zero OR bounces lower after crossover

✓ Stochastic RSI K-line below bearish threshold (default 50)

✓ Within an active trading session (if session filter enabled)

✓ Confirmation EMA aligned (if secondary EMA enabled)

✓ Minimum bars since last signal met (prevents overtrading)

Multi-Confirmation Philosophy:

This system requires ALL conditions to align before generating a signal. This drastically reduces false signals and increases win rate by only trading the highest-probability setups where trend, momentum, and volume all confirm direction.

⚙️ BUILT-IN STOCHASTIC RSI

No External Dependencies:

The indicator includes a fully functional Stochastic RSI calculation based on the standard TradingView formula. No need to hunt for compatible indicators or worry about settings mismatches.

Default Settings (Optimized for Gold):

K Smoothing: 3

D Smoothing: 3

RSI Length: 14

Stochastic Length: 14

Bullish Threshold: 50

Bearish Threshold: 50

How It Works:

Calculates RSI on price data

Applies Stochastic formula to RSI values

Smooths result with K-period SMA

Uses K-line (not D-line) for cleaner, faster signals

Compares to your bullish/bearish thresholds

Generates visual cross markers when thresholds breached

Visual Markers:

Multiple shape options: Circle, Diamond, Square, Cross

Four size options: Tiny, Small, Normal, Large

Customizable colors for bullish/bearish crosses

"Show Only First Cross" prevents repetitive markers

Appears below bars (bullish) or above bars (bearish)

Flexibility:

Switch to "External" mode to connect your own Stochastic RSI indicator

Adjust all calculation parameters to match your trading style

Completely disable the filter if you prefer trend + MACD only

🎨 CUSTOMIZATION OPTIONS

Indicators:

Adjust Main EMA length (default 10)

Enable/disable Confirmation EMA (default OFF)

Set Confirmation EMA length (default 21)

Modify MACD parameters (Fast 5, Slow 14, Signal 9)

Enable/disable MACD bounces (default ON)

Set max bounces per trend (1-10, default 2)

Stochastic RSI:

Choose Built-in or External source

Adjust K/D smoothing periods

Modify RSI and Stochastic lengths

Set custom bullish/bearish thresholds

Configure cross marker appearance

Toggle dashboard display

Signals:

Show/hide signal triangles

Set minimum bars between signals (0-50, default 5)

Enable higher timeframe signal overlay

Choose HTF timeframe (e.g., 3min on 15min chart)

Sessions:

Enable/disable session filtering

Select your timezone

Toggle individual sessions (Asian/London/NY)

Customize session start/end hours

Show/hide session background colors

Display:

Choose dashboard size (Small/Medium/Large)

Adjust all visual elements

Customize colors and styling

💡 PRO TRADING TIPS

Session Optimization:

London Session (6-9am): Highest volatility, best for breakout trades

NY Session (12-3pm): Strong trends, ideal for momentum continuation

Avoid Asian Session (1-4am): Lower liquidity, choppier price action

Overlap Period (12-3pm London time): Peak volume, clearest signals

Signal Filtering:

Set 3-5 bars minimum between signals to avoid overtrading

Higher values (7-10 bars) for more conservative, swing-style entries

Lower values (1-3 bars) for aggressive scalping during high volatility

Confirmation EMA Usage:

Enable in choppy/ranging markets for extra validation

Disable during strong trending conditions (adds lag)

Set to 21 for short-term trends, 50 for medium-term

MACD Bounce Strategy:

Bounces occur when MACD histogram changes direction after crossover

Max 2 bounces = optimal (catches first continuation)

Max 1 bounce = conservative (only initial momentum shift)

Max 3-5 bounces = aggressive (catches multiple waves)

Stochastic RSI Thresholds:

50/50 = Balanced (default, works for most conditions)

30/70 = Conservative (fewer but stronger signals)

60/40 = Aggressive (more signals, requires tighter stops)

Adjust based on current market volatility

Risk Management:

Use the performance tracker to trail stops

Exit when dashboard shows opposite signal forming

Monitor MACD direction arrows for momentum shifts

Set profit targets based on average session ranges

🚀 QUICK START GUIDE

For Beginners:

Add indicator to 3-minute Gold (XAU/USD) chart

Leave all default settings (everything is pre-optimized)

Enable London session (6-9am) and NY session (12-3pm)

Set your timezone to your location

Wait for BUY/SELL triangle + "BUY NOW"/"SELL NOW" on dashboard

Enter trade when ALL conditions align

Exit on opposite signal or dashboard status change

For Advanced Traders:

Optimize EMA lengths for your preferred timeframe

Adjust Stochastic RSI thresholds based on backtesting

Fine-tune MACD bounce count for your risk tolerance

Enable Confirmation EMA for extra validation

Use HTF signal overlay for multi-timeframe confluence

Set signal filter to match your trading frequency

Customize session times for your specific market focus

📈 BEST TIMEFRAMES

Primary: 3-minute chart (system is MACD-optimized for 3min)

Alternative: 5-minute, 15-minute (adjust signal filter accordingly)

NOT Recommended: 1-minute (too noisy), 1-hour+ (signals too infrequent)

Chart Setup:

Main Chart: Your preferred timeframe (3min recommended)

MACD: Always references 3-minute data internally

Stochastic RSI: Calculates on current chart timeframe

Session Filter: Works on any timeframe

✅ WHAT MAKES THIS SYSTEM UNIQUE

All-In-One Solution:

✓ No hunting for compatible external indicators

✓ No configuration headaches or version conflicts

✓ One indicator = complete trading system

Session Intelligence:

✓ Only trades during optimal liquidity periods

✓ Automatically pauses during low-volume sessions

✓ Timezone-aware for global traders

Multi-Confirmation:

✓ Trend (EMA) + Momentum (MACD) + Volume (Stochastic RSI)

✓ Drastically reduces false signals

✓ Higher win rate through layered validation

Performance Transparency:

✓ Real-time P/L tracking on every trade

✓ Know your performance immediately

✓ Data-driven decision making

Professional Grade:

✓ Clean, institutional-style dashboard

✓ Customizable for any trading style

✓ Comprehensive alert system

⚠️ IMPORTANT NOTES

This is NOT a "Holy Grail":

No indicator is 100% accurate

Requires proper risk management

Works best during trending conditions

May produce whipsaws in choppy/ranging markets

Risk Disclosure:

Always use stop losses

Never risk more than 1-2% per trade

Past performance doesn't guarantee future results

Practice on demo account first

Optimization:

Default settings are optimized for Gold (XAU/USD)

May require adjustment for other instruments

Backtest on your specific market before live trading

Different session times may work better for your timezone

🔔 ALERTS INCLUDED

BUY Signal Alert

SELL Signal Alert

Stochastic RSI Cross Above Threshold

Stochastic RSI Cross Below Threshold

Alert Setup:

Click "Create Alert" button

Select desired alert condition

Choose notification method (popup/email/SMS/webhook)

Never miss a high-probability setup!

💬 SUPPORT & UPDATES

This indicator is actively maintained and updated based on user feedback. Future updates may include:

Additional timeframe options

More session presets

Enhanced performance analytics

Multi-asset optimization

Tags: Gold Trading, XAU/USD, Trend Following, MACD Strategy, Stochastic RSI, Session Trading, Day Trading, Scalping, London Session, New York Session, EMA System, Multi-Timeframe Analysis, Trading Dashboard, Performance Tracking

Forexsebi - GOLD Psychological Levels - TrendflowPsychological GOLD levels every $50 with clear zones, highlighted $100 & $500 levels, SMA 50 & 200, and a multi-timeframe trend table. Perfect for structure, trend, and rejection trading on XAUUSD.

Psychologische GOLD-Levels in 50-Dollar-Abständen mit klaren Zonen, 100- & 500-Dollar-Highlights, SMA 50 & 200 sowie einer Multi-Timeframe Trend-Tabelle. Ideal für Struktur-, Trend- und Rejection-Trading auf XAUUSD.

Key Features

Psychological Gold Levels

Automatic levels every $50

Adjustable number of levels above and below current price

Highlighted zones around each level for clearer reaction areas

Special Level Highlighting

$100 levels (xx00) highlighted for medium importance

$500 levels (x000 / x500) marked as major psychological levels

Different colors and stronger line thickness for key zones

Price Labels

Clean price labels displayed on the chart

Special symbols for 100 and 500 dollar levels

Trend Analysis with SMAs

SMA 50 & SMA 200 plotted directly on the chart

Individually toggleable

Clear color separation for fast trend recognition

Multi-Timeframe SMA Trend Table

Trend status (BULLISH / BEARISH / NEUTRAL) across:

5M, 15M, 1H, 4H, 1D

Logic: Price relative to SMA 50 & SMA 200

Color-coded, easy-to-read table

Displays the current trading session (Asia, Frankfurt, London, NY)

Info Box

Current Gold price

Nearest psychological level above and below price

Alert System

Alerts when price approaches a psychological level

User-defined alert distance

Distinction between normal, $100 and $500 levels

Gold Sniper V21: M15 Holding MasterGold Sniper Entry (Follow Trend to enter)

My Indicator :

- Clarify the M30 in Up/Down Trend

- Only entry the trade in M1/M5 Timeframe to make a Sniper Entry.

- Indicator will show when to TP before the Trend Change

Gold Fair Value [Alpha Extract]Gold-anchored Bitcoin fair value model is a macro-fundamental valuation indicator that anchors Bitcoin price assessment to gold market dynamics, establishing fair value zones through percentage change influence modelling and adaptive band multipliers. This overlay system provides institutional-grade context for identifying accumulation zones, distribution zones, and fair value equilibrium across all market cycles with minimal chart clutter through sophisticated gradient fill visualization.

🔶 Gold-Anchored Valuation Framework

Establishes Bitcoin's theoretical fair value by integrating daily gold price movements into a smoothed asset baseline, applying percentage change calculations over configurable periods to measure gold's momentum influence. The system translates gold's relative strength or weakness into Bitcoin price expectations through adjustable influence multipliers, creating a dynamic fair value line that adapts to shifting macro-fundamental relationships between digital and traditional store-of-value assets.

🔶 Multi-Layer Statistical Band System

Implements asymmetric upper and lower band multipliers applied to the fair value baseline, creating five distinct valuation zones: extreme overvaluation, moderate overvaluation, fair value equilibrium, moderate undervaluation, and extreme undervaluation. The asymmetric configuration (default 1.46x upper, 0.74x lower) reflects Bitcoin's historical tendency toward asymmetric volatility patterns with more violent upside moves and grinding downside action, optimizing zone accuracy for actionable trading decisions.

🔶 Gradient Fill Visualization

Employs sophisticated transparency-based gradient fills between bands to create visually intuitive valuation heat maps, with darker orange shading indicating proximity to fair value and lighter shading showing extreme deviation zones. The system maintains chart readability by hiding individual band lines while preserving the filled zones, eliminating visual clutter while delivering maximum information density for rapid market assessment without overwhelming the trader with excessive line plots.

🔶 Historical Context & Position Management

The lower band zones have historically preceded periods of constructive price behavior including consolidation phases and early-stage recovery rallies, while upper band interactions have preceded distribution and correction events. This historical pattern recognition enables traders to position proactively based on valuation extremes rather than reactively chasing momentum, supporting systematic accumulation during undervaluation periods and graduated profit-taking during overvaluation extremes.

All analysis provided by Alpha Extract is for educational and informational purposes only. The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations.

GOLD-DIGGERgold trading make education of trading much easier, just follow risk and reward to achieve it lmax

Anchor SafeSwing Gold StrategyOverview:

The Anchor SafeSwing Gold Strategy is designed for users who prefer structured, rule-based swing trading on XAUUSD. It focuses on identifying high-quality trade setups rather than frequent entries.

This strategy analyzes the market using multiple technical indicators and methods—including trend analysis, multi-chart confirmation, and support/resistance evaluation—to identify potential swing points. It also incorporates a dynamic approach to risk management through adaptive stop-loss and take-profit logic.

How the Strategy Works

1. Multi-Chart & Trend Analysis:

The strategy evaluates trend direction using several indicators and multiple charts. This helps determine whether the trend favors long or short setups.

2. Buy/Sell Conditions:

a. Buy Conditions: When the broader trend is identified as bullish, the strategy waits for the formation of a strong support zone before considering a long position.

b. Sell Conditions: When the trend is bearish, it waits for a confirmed resistance zone before initiating short positions.

3. Dynamic Take-Profit Logic

The strategy uses adaptive take-profit behavior based on evolving market conditions. It monitors new support/resistance structures and various overbought/oversold signals to dynamically exit trades.

4. Dynamic and Configurable Stop-Loss:

A flexible stop-loss system adjusts according to volatility and market structure.

Users can modify the stop-loss threshold in the settings based on their own risk tolerance and account size.

Trading Frequency :

This strategy focuses on select, high-quality setups. As a result, trade frequency is relatively low and may vary depending on market conditions. Backtesting may show roughly several trades per month, but actual live performance can differ.

Important Notes

All trading involves risk, and users should evaluate the strategy and adjust settings according to their own risk management preferences.

Willy ORB for Gold – Session Presets (NY 5m)What it does:

Plots the opening-range high/low for the main Gold sessions (Shanghai, Tokyo, Sydney, Frankfurt, London, New York 5-minute OR by default). It projects TP1/TP2 expansion targets, supports a timezone offset so opens line up with your broker, and includes breakout alerts on confirmed closes.

⸻

Why it’s Gold-friendly

• New York (COMEX pit): 5-minute opening range at ~20:20 local (via your offset) to capture the most active burst.

• London / Frankfurt: strong European volatility windows for XAU/USD.

• Shanghai / Tokyo / Sydney: structure-setting sessions before momentum builds.

⸻

Features

• Session presets: SH, TK, SY, FR, LDN, NY (5m) — toggle individually

• 15m OR for all sessions except NY (5m) by default (editable per session)

• TP1 / TP2 expansion targets (user-defined multiples)

• Labels for 15m/5m range and targets; customizable styles

• Timezone offset control (aligns lines to your local clock)

• Daily auto-reset for clean levels

• Alerts: “Closed Above Range High” / “Closed Below Range Low” per session

⸻

How to use

1. Add to chart (best on 1–15m).

2. In settings → Gold Sessions, toggle the sessions you want.

3. Set “My time offset from chart (hours)” so session lines match your broker time.

4. Trade the breakouts: when price closes beyond the session high/low, TP levels plot automatically.

⸻

Parameters (quick guide)

• Targets: TP1/TP2 multiples (e.g., 1.0 and 2.0).

• Labels: left/right label placement, line styles/colors.

• Sessions: enable/disable + choose each session’s OR length (NY defaults to 5m).

⸻

Tips for XAU/USD

• London often gives the cleanest first breakout.

• New York tends to drive continuation after data releases.

• Consider pairing with volume/volatility or HTF trend for confluence.

⸻

Notes

• Built in Pine Script v6.

• Indicator (not a strategy). For backtests, use a companion strategy that trades the closes beyond the OR with SL at the opposite side and TP by R.

⸻

Disclaimer

For educational purposes only. Not financial advice. Always backtest and manage risk.

ATHENS GOLD MASTER v1.1e — by ATHENSATHENS GOLD MASTER v1.1e — by ATHENS

Professional Smart-Money-Based Gold Trading System

Built with institutional precision and ICT logic for XAUUSD traders.

⚙️ Core Strategy Components

✅ ICT Premium/Discount Model

✅ Daily Pivot Points & Price Bias

✅ Order Block & Break of Structure Detection

✅ Fair Value Gap (FVG) Mitigation Logic

✅ Dynamic Support & Resistance Recognition

✅ Candlestick + Chart Pattern Confirmation

✅ Multi-Timeframe Structure Alignment

💡 How It Works

The indicator scans real-time GOLD price action and generates Buy / Sell signals only when 3 or more confirmations align across smart money and technical confluence.

Each signal is visually marked on the chart with labels showing:

Confirmation count (1–5)

Key structure notes (Pivot, OB, FVG, etc.)

Support/Resistance zone tags

🧠 Optional Filters for Accuracy (90%+)

EMA-200 Trend Filter

ATR Volatility Filter

Volume Strength Filter

Session-Time Restriction (London–New York Overlap)

🟩 Buy Signal Example

Price above Pivot & in Discount Zone

Bullish Order Block Retest

FVG Mitigation Confirmed

Bullish Engulfing / Pin-Bar Confirmation

🟥 Sell Signal Example

Price below Pivot & in Premium Zone

Bearish Order Block Retest

FVG Mitigation Confirmed

Bearish Engulfing / Pin-Bar Confirmation

📊 Extra Features

Live Bias Table (Panel)

Selective Smart S/R Zones

Auto Session Filter

Alerts for Buy, Sell, and Strong Confluences

Best for: Gold Traders, ICT Students, Smart-Money Concepts Enthusiasts, and Professional Price-Action Analysts.

⚜️ Developed by ATHENS | Sahan Akalanka

📈 “Trade Smart. Think Institutional.”

Golden Flow MapGolden Flow Map is a multi–timeframe moving–average system

designed to reveal the underlying direction of long–term market flow,

beyond daily volatility or short–term signals.

This script overlays four major trend lines — each representing a different layer of market rhythm:

Timeframe Length Meaning

🟣 1D – 365 MA Annual average — the true life line of the trend

🔴 1D – 200 MA Institutional benchmark — the long-term threshold

🟢 1W – 20 MA Mid-cycle momentum guide

🟠 3D – 100 MA Wave transition detector — captures trend shifts early

By combining these four perspectives on a single chart,

you can instantly distinguish between a short-term bounce and a major trend reversal.

🧭 How to Use

When all four lines align in one direction → that’s the main current of the market.

If price loses the 200D or 365D, ignore small rebounds — the structure has shifted.

The cross between Weekly 20 and 3D 100 often marks a wave transition.

Focus on alignment order rather than crossovers —

markets ultimately return to the direction of the higher timeframe.

⚙️ Features

SMA / EMA toggle

Individual MA on/off controls

Built-in alerts for 200D and 1W20 cross events

🧠 Concept

“Indicators are not signals — they are maps.”

This tool is not meant to predict, but to reveal the pulse of the market

and guide you through its long-term structure.

✍️ Creator’s Note

Developed from DDU’s personal long-term trend framework,

this indicator serves as a visual compass to expand a trader’s vision

from short-term reactions to macro-level flow.

Gold $25 line + CDCGold Trading CDC + option line

trading with ema to see trendline + Option strike price

Indian Gold Festival Dates HistoricalIndian Gold Festival Dates (1975-2025)

Marks 8 major Indian festivals associated with gold buying over 50 years of historical data. Essential for analyzing seasonal patterns and cultural demand cycles in gold markets.

Festivals Included:

Dhanteras (Gold) - Most auspicious gold buying day

Diwali (Orange) - Festival of Lights

Akshaya Tritiya (Green) - "Never-ending" prosperity

Dussehra (Red) - Victory and success

Makar Sankranti (Cyan) - Solar new year

Gudi Padwa (Magenta) - Hindu New Year (Maharashtra)

Ugadi (Purple) - Hindu New Year (South India)

Navratri (Yellow) - 9-day festival

Features:

✓ 408 exact historical dates (1975-2025)

✓ Color-coded vertical lines for easy identification

✓ Toggle individual festivals on/off

✓ Adjustable line width and labels

✓ Works on all timeframes (best on daily/weekly)

Perfect for traders analyzing gold seasonality, Indian market sentiment, and cultural demand patterns. Use on XAUUSD, GC1!, or Indian gold futures.

Gold Total Market Cap By Wave Trader Gold Total Market Cap (Updated 2025)

Overview

This indicator calculates and visualizes the total market capitalization of gold in real-time, based on the current XAUUSD spot price and the estimated above-ground gold supply. It transforms the raw gold price into a scaled "market cap" view (in trillions USD), helping traders contextualize gold's global value—often compared to stocks, crypto, or fiat reserves. As of October 2025, gold's cap hovers around $26–27T, underscoring its status as a premier safe-haven asset.

How It Works

Core Formula: Market Cap = Gold Price (USD/oz) × Total Supply (troy oz), scaled to trillions for chart readability.

Supply Data: Defaults to the World Gold Council (WGC) mid-2025 estimate of ~218,000 metric tonnes (~7.01B troy oz), but customizable for scenarios like historical or projected figures.

Plotted as a smooth yellow line below the price pane, mirroring gold's price movements but in cap terms.

Key Features

Dynamic Label: A real-time label on the yellow line displays the exact market cap (e.g., "26.8") for instant reference, styled like popular TradingView cap indicators.

Reference Line: Horizontal dashed line at 25T USD to highlight key thresholds (e.g., surpassing Bitcoin's cap).

Info Table: Top-right panel shows current gold price and full market cap (e.g., "26.8T USD") for quick stats.

Overlay-Free: Designed for a separate pane to avoid cluttering your main XAUUSD chart.

Data Sources & Customization

Relies on live XAUUSD close prices from TradingView.

Supply input: Switch between "WGC Mid-2025" (default) or custom values—ideal for sensitivity analysis (e.g., adding future mining output).

No external API calls; fully self-contained for fast performance.

Usage Tips

For Gold Traders: Spot divergences between price momentum and cap growth to gauge overbought/oversold conditions.

Portfolio Context: Compare to S&P 500 cap (~$50T) or BTC (~$2T) by adding multi-symbol alerts.

Timeframes: Best on daily/weekly for long-term trends; works on 1H+ for intraday macro views.

Alerts: Set notifications for cap milestones (e.g., "Gold Cap > 28T") via TradingView's alert system.

Track gold's "infinite market cap" evolution—because unlike stocks, gold's supply grows slowly, amplifying price impact. Updated for 2025 data; feedback welcome! 🚀

Golden/Death Cross with SMAGolden Cross: Triggered when the 50 SMA crosses above the 200 SMA.

Death Cross: Triggered when the 50 SMA crosses below the 200 SMA.

GOLD KEEPER – Multi‑Timeframe Trading AssistantGOLD KEEPER is a multi‑timeframe chart analysis tool designed to display visual markers when certain technical conditions are met.

It is intended to assist traders in their own chart study and decision‑making.

Usage Recommendations:

• Use a higher timeframe (e.g., 1H, 30M, or 15M) for overall market context.

• Drop to a lower timeframe (e.g., 5M or 3M) for potential entries that fit your own strategy.

• Combine with your personal analysis tools such as price action, support/resistance, and volatility levels.

Notes:

• Invite‑only script – access is granted to authorized users.

• For educational and chart‑analysis purposes only.

• This tool does not provide financial advice or guarantee results.

Gold 3min Trading Pro [XAU/USD]# Gold 3min Trading Pro - User Guide

## Overview

This is a professional scalping indicator specifically designed for Gold (XAU/USD) trading on 3-minute timeframes. It combines multiple technical analysis methods to provide high-probability entry signals for short-term trading.

## Key Features

### 1. Multi-Timeframe Trend Analysis

- **Major Trend**: Analyzes 15min, 1H, and 4H timeframes using moving averages

- **Short-term Trend**: Focuses on 3-minute price action and moving average alignment

- **Trend Strength**: Rated from 1-3 based on timeframe agreement

### 2. Core Indicators

- **RSI (9-period)**: Momentum oscillator for overbought/oversold conditions

- **Stochastic (9-period)**: %K and %D lines for entry timing

- **MACD**: Additional trend confirmation

- **Volume Analysis**: Detects volume spikes for signal validation

- **ATR-based Volatility Filter**: Ensures adequate market movement

### 3. Signal Types

- **Primary Signals**: Green triangles (LONG) and Red triangles (SHORT)

- **Enhanced Signals**: Stronger signals with multiple confirmations

- **Confirmation Signals**: Small circles for stochastic crossovers

## How to Use

### 1. Setup

- **Timeframe**: Use on 3-minute charts for Gold (XAU/USD)

- **Settings**: Default settings are optimized for Gold scalping

- **Session Filter**: Enable for London/New York sessions (recommended)

### 2. Entry Conditions

#### LONG Entry:

- Major trend is bullish (green background)

- Short-term trend is up or neutral

- RSI shows bullish momentum

- Stochastic indicates oversold recovery

- Volume spike confirmation

- Strong price action (bullish candle)

#### SHORT Entry:

- Major trend is bearish (red background)

- Short-term trend is down or neutral

- RSI shows bearish momentum

- Stochastic indicates overbought reversal

- Volume spike confirmation

- Strong price action (bearish candle)

### 3. Trade Management

- **Quick Target**: 50% of ATR-based calculation

- **Main Target**: Full ATR-based target

- **Stop Loss**: 60% of ATR below/above entry

- **Time Limit**: Exit if no progress within 20 bars (60 minutes)

### 4. Risk Management

- **Position Size**: Risk 1-2% of account per trade

- **Maximum Trades**: 3-5 trades per session

- **Avoid**: Low volatility periods and major news events

## Visual Elements

### Background Colors

- **Light Green**: Bullish major trend

- **Light Red**: Bearish major trend

- **Yellow**: Volume spike detected

- **Intense Colors**: Very strong trend alignment

### Chart Indicators

- **RSI Line (Blue)**: Main momentum indicator

- **Stochastic %K (Orange)**: Fast stochastic line

- **Stochastic %D (Yellow)**: Slow stochastic line

- **Horizontal Lines**: 70 (overbought), 30 (oversold), 50 (midline)

### Information Table (Top Right)

- Total signal count and performance statistics

- Current market conditions and trend strength

- RSI levels and volatility status

- Trading session information

- Last signal timing

## Alert System

### Standard Alerts

- **Scalp Long Signal**: Basic long entry signal

- **Scalp Short Signal**: Basic short entry signal

- **Premium Signals**: High-quality signals with strong confirmation

- **Trend Reversal**: Major trend change notifications

### Alert Setup

1. Right-click on chart → "Add Alert"

2. Select desired alert condition

3. Configure notification method (popup, email, webhook)

4. Set alert frequency to "Once Per Bar Close"

## Best Practices

### 1. Trading Sessions

- **Optimal**: London-NY overlap (3:00-5:00 PM EST)

- **Good**: London session (2:00-11:00 AM EST)

- **Avoid**: Asian session and major news releases

### 2. Market Conditions

- **Best**: Trending markets with normal to high volatility

- **Moderate**: Ranging markets during active sessions

- **Avoid**: Extremely low volatility or choppy conditions

### 3. Confirmation Rules

- Wait for signal triangle to appear

- Check that major trend aligns with signal direction

- Verify volume spike (yellow background)

- Ensure volatility is adequate (check info table)

### 4. Entry Timing

- Enter immediately after signal confirmation

- Use market orders for scalping speed

- Set stop loss and take profit levels immediately

## Settings Customization

### Essential Settings

- **MA Type**: EMA (recommended) or SMA

- **RSI Length**: 9 (default, can adjust 5-14)

- **Volume Threshold**: 1.8 (higher = fewer but stronger signals)

- **Volatility Filter**: Keep enabled for better signal quality

### Display Options

- **Show Scalping Signals**: Main entry signals

- **Show Performance Stats**: Information table

- **Show Trend Filter**: Background trend colors

- **Use Time Filter**: Session-based filtering

## Performance Optimization

### 1. Backtesting Tips

- Test on different market conditions

- Analyze win rate and average profit/loss

- Adjust settings based on historical performance

### 2. Signal Quality

- Higher trend strength (2-3) = better signals

- Volume confirmation improves success rate

- Enhanced signals have higher probability

### 3. Risk Control

- Never risk more than 2% per trade

- Use proper position sizing

- Stop trading after 3 consecutive losses

## Troubleshooting

### Common Issues

1. **No Signals**: Check volatility filter and session timing

2. **Too Many Signals**: Increase volume threshold or enable filters

3. **Poor Performance**: Verify timeframe (must be 3-minute) and symbol (XAU/USD)

### Support

- Ensure TradingView Pro+ subscription for multi-timeframe data

- Verify Gold symbol matches your broker's format

- Update to latest TradingView version

This indicator is designed for experienced traders familiar with scalping techniques and risk management. Always practice on demo accounts before live trading.