NY Session Range Box with Labeled Time MarkersShows opening time ny session by timing with lines to inform traders to avoid 11:30am to 1:30pm for choppy sessions and mark early and power hour .

Statistics

Scalping m15 indicator RovTradingScalping Indicator Combining UT Bot and Linear Regression Candles.

UT Bot uses ATR Trailing Stop to identify entry points.

Linear Regression Candles smooth price action and provide trend signals.

The indicator is suitable for scalping trading on the M15 timeframe.

UTBotLibrary "UTBot"

is a powerful and flexible trading toolkit implemented in Pine Script. Based on the widely recognized UT Bot strategy originally developed by Yo_adriiiiaan with important enhancements by HPotter, this library provides users with customizable functions for dynamic trailing stop calculations using ATR (Average True Range), trend detection, and signal generation. It enables developers and traders to seamlessly integrate UT Bot logic into their own indicators and strategies without duplicating code.

Key features include:

Accurate ATR-based trailing stop and reversal detection

Multi-timeframe support for enhanced signal reliability

Clean and efficient API for easy integration and customization

Detailed documentation and examples for quick adoption

Open-source and community-friendly, encouraging collaboration and improvements

We sincerely thank Yo_adriiiiaan for the original UT Bot concept and HPotter for valuable improvements that have made this strategy even more robust. This library aims to honor their work by making the UT Bot methodology accessible to Pine Script developers worldwide.

This library is designed for Pine Script programmers looking to leverage the proven UT Bot methodology to build robust trading systems with minimal effort and maximum maintainability.

UTBot(h, l, c, multi, leng)

Parameters:

h (float) - high

l (float) - low

c (float)-close

multi (float)- multi for ATR

leng (int)-length for ATR

Returns:

xATRTS - ATR Based TrailingStop Value

pos - pos==1, long position, pos==-1, shot position

signal - 0 no signal, 1 buy, -1 sell

StoxAI Magic Trend Indicator V3V3 comes with enhanced capabilities:

- Trade Stats and Scoring Table set to hidden by default to make it more mobile friendly. Enable through style settings to make it visible.

- No Colour Range to indicate Side Ways Trend (in between 4 and 7 score)

- Live Score on the last candle to give idea of current trend.

Nq/ES daily CME risk intervalReverse engineering the risk interval for CME (Chicago Mercantile Exchange) products based on margin requirements involves understanding the relationship between margin requirements, volatility, and the risk interval (price movement assumed for margin calculation)

The CME uses a methodology called SPAN (Standard Portfolio Analysis of Risk) to calculate margins. At a high level, the initial margin is derived from:

Initial Margin = Risk Interval × Contract Size × Volatility Adjustment Factor

Where:

Risk Interval: The price movement range used in the margin calculation.

Contract Size: The unit size of the futures contract.

Volatility Adjustment Factor: A measure of how much price fluctuation is expected, often tied to historical volatility.

To calculate an approximate of the daily CME risk interval, we need:

Initial Margin Requirement: Available on the CME Group website or broker platforms.

Contract Size: The size of one futures contract (e.g., for the S&P 500 E-mini, it is $50 × index points).

Volatility Adjustment Factor: This is derived from historical volatility or CME's implied volatility estimates.

As we do not have access to CME calculations , the volatility adjustment factor can be estimated using historical volatility: We calculate the standard deviation of daily returns over a specific period (e.g., 20 or 30 or 60 days).

Key Considerations

The exact formulas and parameters used by CME for CME's implied volatility estimates are proprietary, so this calculation based on standard deviation of daily returns is an approximation.

How to use:

Input the maintenance margin obtained from the CME website.

Adjust volatility period calculation.

The indicator displays the range high and low for the trading day.

1.Lines can be used as targets intraday

2.Market tends to snap back in between the lines and close the day in the range

Live Volume TickerGives current real-time volume of tick movements denoted in the timeframe of the current candle.

PPI Inflation Monitor (Change YoY & MoM)📊 PPI Inflation Monitor - Leading Inflation Indicator

The Producer Price Index (PPI) measures wholesale/producer-level prices and serves as a critical leading indicator for consumer inflation trends. This tool helps you anticipate CPI movements and identify corporate margin pressures before they show up in earnings.

🎯 KEY FEATURES:

- Dual Perspective Analysis:

- Year-over-Year (YoY): Histogram bars showing annual producer price inflation

- Month-over-Month (MoM): Line overlay showing monthly wholesale price changes

- Visual Reference System:

- Dashed line at 2% (typical target for producer price inflation)

- Dotted line at 0.17% (equivalent monthly target)

- Color-coded bars: Red above target, Green below target

- Real-Time Data Table:

- Current PPI Index value

- YoY inflation rate with color coding

- MoM inflation rate with color coding

- Deviation from target level

- Automated Alerts:

- YoY crosses above/below target

- MoM crosses above/below target

- Early warning system for inflation trends

📈 WHY PPI IS YOUR EARLY WARNING SYSTEM:

PPI typically leads CPI by 1-3 months because:

- Producers face cost increases first

- These costs are eventually passed to consumers

- Shows whether companies can maintain pricing power

Rising PPI with stable CPI = Margin compression → Bearish for stocks

Rising PPI followed by rising CPI = Broad inflation → Fed hawkishness incoming

Falling PPI = Disinflationary trend starting → Positive for risk assets

🔍 TRADING APPLICATIONS:

1. Lead Time Advantage: Position before CPI confirms PPI trends

2. Sector Rotation: High PPI = favor companies with pricing power

3. Margin Analysis: PPI-CPI divergence = margin pressure/expansion signals

4. Fed Anticipation: PPI acceleration = Fed likely to turn hawkish soon

💡 STRATEGIC USE CASES:

- Value vs. Growth: Rising PPI favors value stocks with pricing power

- Commodities: PPI often correlates with commodity price trends

- Small Caps: More vulnerable to input cost increases (high PPI = cautious)

- Corporate Earnings: Anticipate margin pressure before quarterly reports

🔄 COMBINE WITH:

- CPI: Confirm if producer costs reach consumers

- PCE: Validate Fed's preferred inflation metric response

- Fed Funds Rate: Assess if Fed is behind/ahead of curve

📊 DATA SOURCE:

Official PPI data from FRED (Federal Reserve Economic Data), updated monthly when new data releases occur.

🎨 CUSTOMIZATION:

Fully customizable:

- Toggle YoY/MoM displays

- Adjust reference target levels

- Customize colors

- Show/hide absolute PPI values

Perfect for: Macro traders, fundamental analysts, earnings traders, and investors seeking early inflation signals before they appear in consumer prices.

⚡ Remember: PPI leads CPI. Use this advantage to position ahead of the crowd.

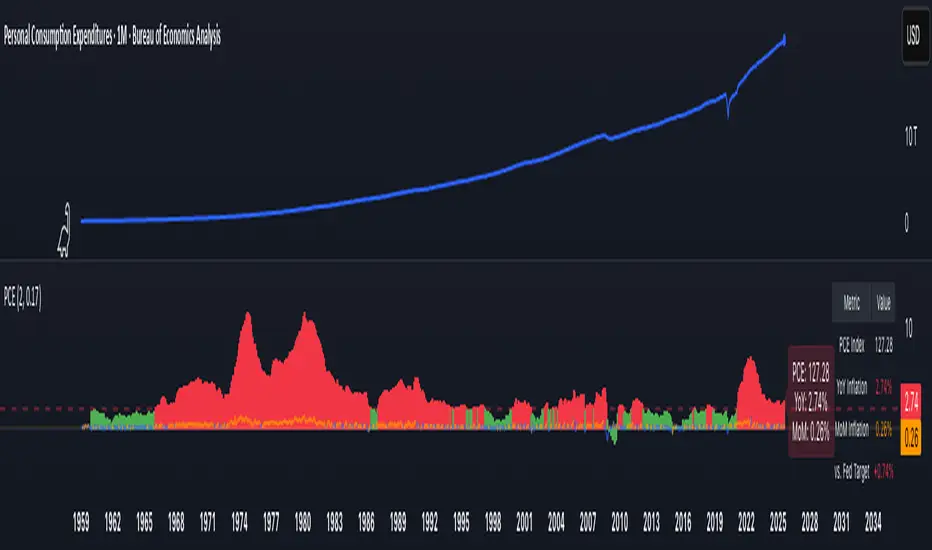

PCE Inflation Monitor (Change YoY & MoM)📊 PCE Inflation Monitor - The Fed's Most Important Metric

Personal Consumption Expenditures (PCE) is the Federal Reserve's preferred inflation measure and THE metric they target for their 2% inflation goal. If you want to predict Fed policy, you need to watch PCE.

🎯 KEY FEATURES:

- Dual Perspective Analysis:

- Year-over-Year (YoY): Histogram bars showing annual PCE inflation

- Month-over-Month (MoM): Line overlay showing monthly consumption price changes

- Visual Reference System:

- Dashed line at 2% (Fed's official PCE inflation target)

- Dotted line at 0.17% (equivalent monthly target)

- Color-coded bars: Red above Fed target, Green below target

- Real-Time Data Table:

- Current PCE Index value

- YoY inflation rate vs. Fed's 2% target

- MoM inflation rate with color coding

- Exact deviation from Fed target (critical for policy predictions)

- Automated Alerts:

- PCE crosses Fed's 2% target (major policy signal!)

- MoM crosses monthly target

- Stay informed of Fed-relevant inflation changes

📈 WHY PCE IS DIFFERENT (AND MORE IMPORTANT):

PCE vs. CPI differences:

- Flexible basket: PCE adjusts for substitution (beef → chicken if prices rise)

- Broader coverage: Includes healthcare paid by insurance/government

- Lower readings: Typically 0.2-0.4% below CPI

- Fed's choice: Explicitly stated as their target metric

Most importantly: When Powell speaks about "our 2% target," he means PCE, not CPI!

🔍 TRADING IMPLICATIONS:

PCE Above 2% (Red Zone):

→ Fed under pressure to maintain/raise rates

→ Hawkish policy stance likely

→ Negative for growth stocks, crypto

→ Positive for USD, bearish for gold

PCE Below 2% (Green Zone):

→ Fed has flexibility to cut rates

→ Dovish policy stance possible

→ Positive for risk assets, growth stocks

→ Negative for USD, bullish for commodities

PCE Approaching 2% from Above:

→ Fed "mission accomplished" narrative

→ Rate cut cycle becomes possible

→ Major bullish signal for equities/crypto

💡 ADVANCED STRATEGIES:

1. Fed Meeting Preparation: Check PCE before FOMC meetings for policy clues

2. Dot Plot Predictions: PCE trend determines Fed's rate forecast updates

3. Pivot Timing: When PCE MoM turns negative, Fed pivot becomes realistic

4. Press Conference Analysis: Compare Powell's comments to PCE deviation

🎯 KEY LEVELS TO WATCH:

- 2.0% YoY: Fed's official target - crossing this level is major news

- 2.5% YoY: "Uncomfortably high" - Fed forced to stay restrictive

- 3.0% YoY: "Crisis mode" - Fed turns very hawkish

- 1.5% YoY: "Below target" - Rate cuts become likely

🔄 COMBINE WITH:

- CPI: Public perception vs. Fed's metric (often diverge)

- Core PCE: Even more important (excludes food/energy volatility)

- Fed Funds Rate: Is Fed responding appropriately to PCE?

📊 DATA SOURCE:

Official PCE data from FRED (Federal Reserve Economic Data), updated monthly typically in the last week of each month (after CPI/PPI releases).

🎨 CUSTOMIZATION:

Fully customizable:

- Toggle YoY/MoM displays

- Adjust Fed target if needed

- Customize colors

- Show/hide absolute PCE values

Perfect for: Fed watchers, macro traders, policy analysts, and serious investors who want to predict monetary policy changes before they happen.

⚠️ CRITICAL INSIGHT: While media focuses on CPI, the Fed focuses on PCE. Trade what the Fed trades, not what the headlines say.

🎓 Pro Tip: Fed members often mention "Core PCE" (excluding food/energy). Consider adding that indicator alongside this one for complete Fed policy analysis.

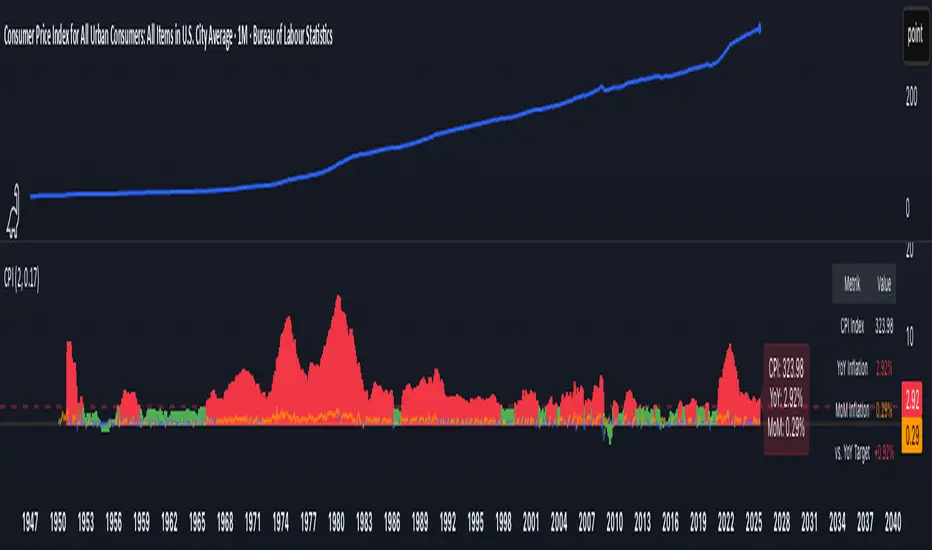

CPI Inflation Monitor (Change YoY & MoM)📊 CPI Inflation Monitor - Complete Macro Analysis Tool

This indicator provides a comprehensive view of Consumer Price Index (CPI) inflation trends, essential for understanding monetary policy, market conditions, and making informed trading decisions.

🎯 KEY FEATURES:

- Dual Perspective Analysis:

- Year-over-Year (YoY): Histogram bars showing annual inflation rate

- Month-over-Month (MoM): Line overlay showing monthly price changes

- Visual Reference System:

- Dashed line at 2% (Fed's official inflation target for YoY)

- Dotted line at 0.17% (equivalent monthly target for MoM)

- Color-coded bars: Red above target, Green below target

- Real-Time Data Table:

- Current CPI Index value

- YoY inflation rate with color coding

- MoM inflation rate with color coding

- Deviation from Fed target

- Automated Alerts:

- YoY crosses above/below 2% target

- MoM crosses above/below 0.17% target

- Perfect for staying informed without constant monitoring

📈 WHY THIS MATTERS FOR TRADERS:

CPI is the most widely reported inflation metric and directly influences:

- Federal Reserve interest rate decisions

- Bond yields and currency valuations

- Stock market sentiment (especially growth vs. value rotation)

- Cryptocurrency and risk asset performance

Rising inflation (red bars) typically leads to:

→ Higher interest rates → Negative for growth stocks, crypto

→ Stronger USD → Pressure on commodities

Falling inflation (green bars) typically leads to:

→ Rate cut expectations → Positive for growth stocks, crypto

→ Weaker USD → Support for commodities

🔍 HOW TO USE:

1. Strategic Positioning: Use YoY trend (thick bars) for long-term asset allocation

2. Tactical Timing: Use MoM trend (thin line) to identify turning points early

3. Divergence Trading: When MoM falls but YoY remains high, anticipate trend reversal

4. Fed Policy Prediction: Distance from 2% target indicates Fed's likely hawkishness

💡 PRO TIPS:

- Multiple months of MoM above 0.3% = Accelerating inflation → Fed turns hawkish

- MoM turning negative while YoY still elevated = Peak inflation → Position for pivot

- Compare with PPI and PCE indicators for complete inflation picture

- Use alerts to catch important threshold crossings automatically

📊 DATA SOURCE:

Official CPI data from FRED (Federal Reserve Economic Data), updated monthly mid-month when new data releases occur.

🎨 CUSTOMIZATION:

Fully customizable through settings:

- Toggle YoY/MoM displays

- Adjust target levels

- Customize colors for visual preference

- Show/hide absolute CPI values

Perfect for: Macro traders, swing traders, long-term investors, and anyone wanting to understand the inflation environment affecting their portfolio.

Note: This indicator works on any chart timeframe as it loads external monthly economic data.

Whale HunterThis script searches for gaps (above selected price gap percent), and mark it with a box (that can be extend right)

also it takes the buy price of Gap-Up and sell price of a Gap-Down and tries to cluster them into price ranges in a table (the space between price clusters is configurable), so you can see what are the most likely price range that the whales are buying and selling that makes the price move in a way that causes a X% gap,

so this indicator will show you where the whales are buying and selling

CMF, RSI, CCI, MACD, OBV, Fisher, Stoch RSI, ADX (+DI/-DI)Eight normalized indicators are used in conjunction with the CMF, CCI, MACD, and Stoch RSI indicators. You can track buy and sell decisions by tracking swings. The zero line is for reversal tracking at -20, +20, +50, and +80. You can use any of the nine indicators individually or in combination.

Gamma Big Walls Regime Tel by Tradeorthe indicator shows put strikes and call strikes and the negative net gamma or positive after Inserting date manually, also it shows big walls

Simplified Percentile ClusteringSimplified Percentile Clustering (SPC) is a clustering system for trend regime analysis.

Instead of relying on heavy iterative algorithms such as k-means, SPC takes a deterministic approach: it uses percentiles and running averages to form cluster centers directly from the data, producing smooth, interpretable market state segmentation that updates live with every bar.

Most clustering algorithms are designed for offline datasets, they require recomputation, multiple iterations, and fixed sample sizes.

SPC borrows from both statistical normalization and distance-based clustering theory , but simplifies them. Percentiles ensure that cluster centers are resistant to outliers , while the running mean provides a stable mid-point reference.

Unlike iterative methods, SPC’s centers evolve smoothly with time, ideal for charts that must update in real time without sudden reclassification noise.

SPC provides a simple yet powerful clustering heuristic that:

Runs continuously in a charting environment,

Remains interpretable and reproducible,

And allows traders to see how close the current market state is to transitioning between regimes.

Clustering by Percentiles

Traditional clustering methods find centers through iteration. SPC defines them deterministically using three simple statistics within a moving window:

Lower percentile (p_low) → captures the lower basin of feature values.

Upper percentile (p_high) → captures the upper basin.

Mean (mid) → represents the central tendency.

From these, SPC computes stable “centers”:

// K = 2 → two regimes (e.g., bullish / bearish)

=

// K = 3 → adds a neutral zone

=

These centers move gradually with the market, forming live regime boundaries without ever needing convergence steps.

Two clusters capture directional bias; three clusters add a neutral ‘range’ state.

Multi-Feature Fusion

While SPC can cluster a single feature such as RSI, CCI, Fisher Transform, DMI, Z-Score, or the price-to-MA ratio (MAR), its real strength lies in feature fusion. Each feature adds a unique lens to the clustering system. By toggling features on or off, traders can test how each dimension contributes to the regime structure.

In “Clusters” mode, SPC measures how far the current bar is from each cluster center across all enabled features, averages these distances, and assigns the bar to the nearest combined center. This effectively creates a multi-dimensional regime map , where each feature contributes equally to defining the overall market state.

The fusion distance is computed as:

dist := (rsi_d * on_off(use_rsi) + cci_d * on_off(use_cci) + fis_d * on_off(use_fis) + dmi_d * on_off(use_dmi) + zsc_d * on_off(use_zsc) + mar_d * on_off(use_mar)) / (on_off(use_rsi) + on_off(use_cci) + on_off(use_fis) + on_off(use_dmi) + on_off(use_zsc) + on_off(use_mar))

Because each feature can be standardized (Z-Score), the distances remain comparable across different scales.

Fusion mode combines multiple standardized features into a single smooth regime signal.

Visualizing Proximity - The Transition Gradient

Most indicators show binary or discrete conditions (e.g., bullish/bearish). SPC goes further, it quantifies how close the current value is to flipping into the next cluster.

It measures the distances to the two nearest cluster centers and interpolates between them:

rel_pos = min_dist / (min_dist + second_min_dist)

real_clust = cluster_val + (second_val - cluster_val) * rel_pos

This real_clust output forms a continuous line that moves smoothly between clusters:

Near 0.0 → firmly within the current regime

Around 0.5 → balanced between clusters (transition zone)

Near 1.0 → about to flip into the next regime

Smooth interpolation reveals when the market is close to a regime change.

How to Tune the Parameters

SPC includes intuitive parameters to adapt sensitivity and stability:

K Clusters (2–3): Defines the number of regimes. K = 2 for trend/range distinction, K = 3 for trend/neutral transitions.

Lookback: Determines the number of past bars used for percentile and mean calculations. Higher = smoother, more stable clusters. Lower = faster reaction to new trends.

Lower / Upper Percentiles: Define what counts as “low” and “high” states. Adjust to widen or tighten cluster ranges.

Shorter lookbacks react quickly to shifts; longer lookbacks smooth the clusters.

Visual Interpretation

In “Clusters” mode, SPC plots:

A colored histogram for each cluster (red, orange, green depending on K)

Horizontal guide lines separating cluster levels

Smooth proximity transitions between states

Each bar’s color also changes based on its assigned cluster, allowing quick recognition of when the market transitions between regimes.

Cluster bands visualize regime structure and transitions at a glance.

Practical Applications

Identify market regimes (bullish, neutral, bearish) in real time

Detect early transition phases before a trend flip occurs

Fuse multiple indicators into a single consistent signal

Engineer interpretable features for machine-learning research

Build adaptive filters or hybrid signals based on cluster proximity

Final Notes

Simplified Percentile Clustering (SPC) provides a balance between mathematical rigor and visual intuition. It replaces complex iterative algorithms with a clear, deterministic logic that any trader can understand, and yet retains the multidimensional insight of a fusion-based clustering system.

Use SPC to study how different indicators align, how regimes evolve, and how transitions emerge in real time. It’s not about predicting; it’s about seeing the structure of the market unfold.

Disclaimer

This indicator is intended for educational and analytical use.

It does not generate buy or sell signals.

Historical regime transitions are not indicative of future performance.

Always validate insights with independent analysis before making trading decisions.

ETH OHLC by tncylyvETH OHLC Projection Levels

📜 Indicator Description

This indicator projects key potential price levels for Ethereum (ETH) based on its historical price behavior. Using the opening price of a user-selected timeframe (4H, 1D, or 1W) as a baseline, it calculates and displays statistically-derived levels for potential "Manipulation" and "Distribution" phases of price action.

These projections are designed to provide traders with potential zones of interest for support, resistance, stop-loss placement, and take-profit targets for the current trading period.

________________________________________

🧠 Core Concepts Explained

The indicator is built on two key concepts derived from candlestick analysis:

• Manipulation: This represents the initial price movement that occurs against the candle's eventual primary direction.

o For a bullish candle, it's the extent of the lower wick (the move from Open down to Low).

o For a bearish candle, it's the extent of the upper wick (the move from Open up to High).

o The "M" levels on the chart project the average (mean and median) historical size of this manipulation wick, suggesting potential areas for liquidity grabs or stop hunts.

• Distribution: This represents the primary price movement in the direction of the candle's trend.

o For a bullish candle, it's the total move from Open to High.

o For a bearish candle, it's the total move from Open to Low.

o The "D" levels project the average (mean and median) historical range of this price expansion, suggesting potential targets for the period.

________________________________________

📊 Data & Methodology

It is important to note that the statistical ratios used for the projections are not calculated in real-time by the indicator itself.

These values have been pre-calculated through an extensive historical analysis performed in Python. The analysis used the complete historical ETH/USD price data from the Coinbase exchange to determine the mean and median ratios for both manipulation and distribution across the different timeframes. The resulting fixed values are then hard-coded into the script to ensure performance and consistency.

________________________________________

⚙️ How to Use It

At the beginning of each new period (e.g., at the start of a new day on the 1D timeframe), the indicator will draw a new set of horizontal lines and zones based on that period's opening price.

• The central dotted line represents the Opening Price for the selected timeframe.

• Manipulation Levels (+M / -M): These inner levels can be interpreted as potential reversal zones. Price may test these areas to trigger stops before moving in the primary direction for the session.

• Distribution Levels (+D / -D): These outer levels can be used as potential take-profit targets, representing the average historical price extension for a period.

• Mean vs. Median Zones: The script plots levels based on both the historical mean (average) and median (middle value). The shaded area between them creates a zone rather than a single price line, offering a more practical range for analysis.

________________________________________

🛠️ Settings and Features

• Projection Timeframe: Select the primary timeframe for the analysis (4H, 1D, or 1W). The historical data used for projections is specific to the chosen timeframe.

• Historical Periods to Show: Adjust how many past periods of data you want to see on your chart. A value of 1 will only show the projections for the current, active period.

• Timezone (UTC-4): The 4H calculations are based on a fixed UTC-4 timezone to align with specific, high-volume market sessions (e.g., New York open). This is not changeable to ensure data consistency.

• Visual Customization: You have full control over the appearance of the indicator.

o Toggle the visibility, colors, and line styles for the Open price line and each of the Manipulation/Distribution levels using their respective checkboxes and inputs.

o Enable or disable the shaded fills between the mean and median levels.

o Tip: To quickly hide all price labels at once, edit the "Label Color" setting and set its opacity to 100% (fully transparent).

BTC OHLC by tncylyvBTC OHLC Projection Levels

📜 Indicator Description

This indicator projects key potential price levels for Bitcoin (BTC) based on historical price behavior. Using the opening price of a user-selected timeframe (4H, 1D, or 1W) as a baseline, it calculates and displays statistically-derived levels for potential "Manipulation" and "Distribution" phases of price action.

These projections are designed to provide traders with potential zones of interest for support, resistance, stop-loss placement, and take-profit targets for the current trading period.

________________________________________

🧠 Core Concepts Explained

The indicator is built on two key concepts derived from candlestick analysis:

• Manipulation: This represents the initial price movement that occurs against the candle's eventual primary direction.

o For a bullish candle, it's the extent of the lower wick (the move from Open down to Low).

o For a bearish candle, it's the extent of the upper wick (the move from Open up to High).

o The "M" levels on the chart project the average (mean and median) historical size of this manipulation wick, suggesting potential areas for liquidity grabs or stop hunts.

• Distribution: This represents the primary price movement in the direction of the candle's trend.

o For a bullish candle, it's the total move from Open to High.

o For a bearish candle, it's the total move from Open to Low.

o The "D" levels project the average (mean and median) historical range of this price expansion, suggesting potential targets for the period.

________________________________________

📊 Data & Methodology

It is important to note that the statistical ratios used for the projections are not calculated in real-time by the indicator itself.

These values have been pre-calculated through an extensive historical analysis performed in Python. The analysis used the complete historical BTC/USD price data from the Coinbase exchange to determine the mean and median ratios for both manipulation and distribution across the different timeframes. The resulting fixed values are then hard-coded into the script to ensure performance and consistency.

________________________________________

⚙️ How to Use It

At the beginning of each new period (e.g., at the start of a new day on the 1D timeframe), the indicator will draw a new set of horizontal lines and zones based on that period's opening price.

• The central dotted line represents the Opening Price for the selected timeframe.

• Manipulation Levels (+M / -M): These inner levels can be interpreted as potential reversal zones. Price may test these areas to trigger stops before moving in the primary direction for the session.

• Distribution Levels (+D / -D): These outer levels can be used as potential take-profit targets, representing the average historical price extension for a period.

• Mean vs. Median Zones: The script plots levels based on both the historical mean (average) and median (middle value). The shaded area between them creates a zone rather than a single price line, offering a more practical range for analysis.

________________________________________

🛠️ Settings and Features

• Projection Timeframe: Select the primary timeframe for the analysis (4H, 1D, or 1W). The historical data used for projections is specific to the chosen timeframe.

• Historical Periods to Show: Adjust how many past periods of data you want to see on your chart. A value of 1 will only show the projections for the current, active period.

• Timezone (UTC-4): The 4H calculations are based on a fixed UTC-4 timezone to align with specific, high-volume market sessions (e.g., New York open). This is not changeable to ensure data consistency.

• Visual Customization: You have full control over the appearance of the indicator.

o Toggle the visibility, colors, and line styles for the Open price line and each of the Manipulation/Distribution levels using their respective checkboxes and inputs.

o Enable or disable the shaded fills between the mean and median levels.

o Tip: To quickly hide all price labels at once, edit the "Label Color" setting and set its opacity to 100% (fully transparent).

ATC v6ATC v6 Indicator: Automatic Session and Time Lines

Designed by Alfa Trade Club for TradingView users, ATC v6 is an advanced

indicator that automatically marks key session opens, closes, and specific times

of financial markets on your chart. This tool eliminates the need to manually track

critical trading hours, allowing you to easily analyze price action in relation to

these important timeframes.

Key Features

This indicator comes with a set of powerful features that provide the flexibility

and visual clarity traders need:

Multi-Time Zone Support: The indicator is based on the world’s three largest

financial market centers:

New York (America/New_York)

London (Europe/London)

Tokyo (Asia/Tokyo)

This allows you to accurately set the lines according to the local time of the

market you are trading.

Customizable Time Lines: Each time zone includes multiple predefined lines

(e.g., “NY Midnight,” “London Open,” “Tokyo Open”). Users can:

Enable or disable each line

Set any desired hour and minute

Assign distinct colors for clear visual separation

Pre-Session Function: This standout feature draws a dotted line a few

minutes before a main time you specify (e.g., the market open). This lets you see

the price level immediately before a key event.

Automatic Price Boxes: When the Pre-Session feature is active, the indicator

draws a colored box between the price at the pre-session moment and the price

at the main event. This box highlights the price range between the pre-

session and the main event, effectively visualizing the volatility at the

session open.

Forward-Extending Lines: All lines extend forward from the moment they are

drawn until the next day. This helps you track how these levels act as support or

resistance throughout the trading session.

Who Is It For?

Session-Focused Traders: Ideal for those tracking volatility during

London, New York, or Asian session opens.

Day Traders: Perfect for marking key economic data releases or daily

open/close levels.

Technical Analysts: A powerful tool for visually analyzing how opening

prices influence price behavior throughout the day.

EM Range (VIX1D PrevClose • Close & Hi/Lo, N-Day View)What this indicator does

This study projects a one-day expected move (EM) from the CBOE:VIX1D using a simple 1-σ model with 252 trading days. It visualizes the possible intraday range from three anchors and also gives a T+1 forecast using today’s real-time VIX1D:

• PrevClose ±σ (solid) – a symmetric bracket around yesterday’s close.

• Low → Upper (dashed) – the upper bound implied from today’s low.

• High → Lower (dashed) – the lower bound implied from today’s high.

• NextDay (solid, optional) – tomorrow’s expected bracket built from the current price using today’s VIX1D (intraday it updates; after the daily close it freezes to the daily close).

All ranges are plotted in points, not percentages.

How it’s computed

Let σ = (VIX1D/100)/sqrt(252) * multiplier.

• PrevClose bands: prevClose * (1 ± σ) using yesterday’s VIX1D close.

• Low → Upper: todayLow * (1 + σ) using yesterday’s VIX1D close.

• High → Lower: todayHigh * (1 − σ) using yesterday’s VIX1D close.

• NextDay (T+1): currentPrice * (1 ± σ_today) where σ_today uses today’s VIX1D (real-time via 15m/30m/60m fallbacks; after session close it uses the daily close).

What you’ll see on the chart

• Two solid lines (PrevClose ±σ), two dashed lines (from Low/High).

• Optional blue solid lines for NextDay ±σ (toggle).

• Lines are per-day segments (not infinite). Yesterday’s dashed lines are carried into today for quick context; other lines do not carry across days.

• Colors are fully configurable; defaults use a deep, high-contrast palette tuned for dark backgrounds.

N-Day history (no over-extension)

Use “Show last N days” to display previous sessions. Historical lines are drawn only within their own day (clean separation of regimes).

Compact table (top-right by default)

The on-chart table shows concise, single-line rows:

• VIX1D−1: yesterday’s VIX1D close | ±EM (points) from PrevClose

• VIX1D (RT): today’s real-time VIX1D | ±EM (points) from current price

• Prev ±σ: numeric around PrevClose

• L → Upper: today’s low and its implied upper bound

• H → Lower: today’s high and its implied lower bound

• NextDay: tomorrow’s implied from current price

• >±σ: count of daily closes that finished outside PrevClose ±σ over the last N−1 completed days (with up/down breakdown)

Inputs & options

• VIX1D symbol: default CBOE:VIX1D.

• σ multiplier: default 1.0 (try 0.5 / 1.5 / 2.0 based on your risk model).

• Show last N days: how many sessions to render (incl. today).

• Show NextDay lines (blue): on/off toggle.

• Line width and color pickers for each band type.

• Table position: top/bottom, left/right.

Works on…

• Any instrument priced in points (stocks, ETFs, futures incl. ES).

• Any timeframe. For the T+1 forecast, the price anchor is real-time on intraday charts; on higher timeframes it uses an intraday proxy (60-minute) intraday and switches to the daily close after session end.

Notes & good practice

• VIX1D is an implied daily move proxy; it’s not a guarantee. Treat bands as probabilistic, not absolute barriers.

• The outside-±σ close count is a quick sanity check on how often price exceeds the one-day expectation—useful for regime awareness and sizing.

• If your market isn’t well-described by VIX1D (e.g., non-US hours or crypto), consider substituting a more relevant vol index.

Disclaimer: This tool is for research/education only and is not financial advice. Always manage risk.

Aggregated Open Interest Multi-Exchange (USD)This indicator aggregates Open Interest (OI) data from multiple major cryptocurrency exchanges into a single unified view in USD, using data available on TradingView. It automatically adapts to the asset you're viewing on the chart.

Features:

Aggregates OI from 7 major exchanges: Binance, Bybit, OKX, Bitget, Deribit, HTX, and Coinbase

All values converted to USD - unlike native OI which shows contracts/coins

Uses only data available on TradingView platform

Automatically detects the asset from your chart (BTC, ETH, SOL, etc.)

True apples-to-apples comparison across exchanges

Displays as candlesticks showing OI open, high, low, and close

Toggle exchanges on/off individually

Handles different contract types per exchange automatically

Why USD conversion matters:

Traditional OI indicators show values in contracts or crypto units, making it difficult to compare across exchanges. This indicator converts everything to USD, giving you the real dollar value of open positions across all exchanges.

How it works:

Simply add the indicator to any crypto perpetual futures chart. It will automatically fetch and aggregate OI data from all supported exchanges for that asset using TradingView's built-in data feeds, converting everything to USD.

Supported Exchanges:

Binance, Bybit, Bitget, HTX: USDT perpetuals

Deribit: BTC/ETH use USD contracts, others use USDC

OKX: Contract-based (automatically converted)

Coinbase: USDC perpetuals

Perfect for traders who want a comprehensive view of total market Open Interest in USD across exchanges using reliable TradingView data.

RPT Position Sizer🎯 Purpose

This indicator is a position sizing and stop-loss calculator designed to help traders instantly determine:

How many shares/contracts to buy,

How much risk (₹) they are taking per trade,

How much capital will be deployed, and

The precise stop-loss price level based on user-defined parameters.

It displays all key values in a compact on-chart table (bottom-left corner) for quick trade planning.

💡 Use Case

Perfect for discretionary swing traders, systematic position traders, and risk managers who want instant visual feedback of trade sizing metrics directly on the chart — eliminating manual calculations and improving discipline.

⚙️ Key Features

Dynamic Inputs

Trading Capital (₹) — total available capital for trading.

RPT % — risk-per-trade as a percentage of total capital.

SL % — stop-loss distance in percent below CMP (Current Market Price).

CMP Source — can be linked to close, hl2, etc.

Rounding Style — round position size to Nearest, Floor, or Ceil.

Decimals Show — control number formatting precision in the table.

Core Calculations

SL Points: CMP × SL%

SL Price: CMP − SL Points

Risk Amount (₹): Capital × RPT%

Position Size: Risk ÷ SL Points

Capital Used: Position Size × CMP

Clean On-Chart Table Display

Displays:

Trading Capital

RPT %

Risk Amount (₹)

Position Size (shares/contracts)

Capital Required (₹)

Stop-Loss % & SL Price

The table uses a minimalistic white-on-black design with clear labeling and rupee formatting for quick reference.

Data Window Integration

Plots hidden values (Position Size, Risk Amount, SL Points, Capital Used) for use in TradingView’s Data Window—ideal for strategy testing and exporting values.

NQ Manipulation/Distribution Projections + Average RangeThis is not your typical OHLC indicator :)

Overview:

The Manipulation/Distribution Projections (OHLC Stats) indicator is a powerful tool designed to forecast potential price levels for various timeframes. It operates on a simple yet profound principle: price action within a single candle can be broken down into "manipulation" and "distribution" phases. By analyzing over 17 years of historical data for major assets in Python, this script calculates the average (mean) and typical (median) extent of these movements.

These statistical insights are then used to project key levels on your chart based on the current period's opening price, providing a statistically-grounded framework for potential support, resistance, and price targets.

Key Concepts Explained

The indicator's logic is based on how price wicks and bodies form relative to the opening price.

• Manipulation: This refers to the initial move that goes against the candle's eventual direction. For a bullish candle, it's the lower wick (the move from the open down to the low before reversing higher). For a bearish candle, it's the upper wick (the move from the open up to the high before selling off). It represents a "fake out" or a stop hunt.

• Distribution: This is the primary, directional move of the candle from the opening price. For a bullish candle, it's the distance from the open to the high. For a bearish candle, it's the distance from the open to the low. It represents the "real" intended direction of price for that period.

How It Works

This indicator does not calculate these ratios in real-time. Instead, it leverages a comprehensive statistical analysis performed externally in Python on over 17 years of OHLC data. This analysis determined the mean and median ratios for both Manipulation and Distribution movements across different timeframes and, for intraday periods, different times of day.

These pre-computed, static ratios are embedded directly into the script. When a new period begins (e.g., a new day on the Daily timeframe), the indicator:

1. Takes the opening price for that period.

2. Retrieves the corresponding pre-calculated Manipulation and Distribution ratios.

3. Applies these ratios to the opening price to project eight potential price levels:

o + / - Mean Distribution

o + / - Median Distribution

o + / - Mean Manipulation

o + / - Median Manipulation

This approach provides a stable, forward-looking set of levels for the entire duration of the trading period.

________________________________________

Features

• Statistically-Derived Projections: Plots eight key price levels based on historical tendencies, providing clear potential zones for entries, exits, and stop placement.

• Selectable Timeframe: Choose to view projections for the 1H, 4H, 1D, or 1W periods directly from the settings.

• Dynamic Stats Table: A powerful, on-chart dashboard that provides real-time context. For all four timeframes (1H, 4H, 1D, 1W), it shows:

o Position: Where the current price is relative to the projected zones (e.g., "In +Manip Zone," "Below -Dist").

o Range Completed: The percentage of the historical average range that the current period has already covered.

o Current & Average Range: The current high-to-low range in points vs. the historical average.

• Historical Context: You can display levels for previous periods to see how price has interacted with them in the past.

• Full Customization: Control the color, style, and visibility of every line, label, and fill to match your chart's theme.

________________________________________

How to Use

This indicator is versatile and can be integrated into various trading strategies.

• Identifying Targets & Reversal Zones: The Distribution levels (especially the zone between the median and mean) can serve as logical take-profit targets, as they represent a historical point of extension. Conversely, Manipulation levels can indicate areas where price might form a wick and reverse.

• Gauging Volatility: Use the Stats Table's "Range Completed" column to assess market conditions. If the 1D range is only 30% complete by mid-day, there may be room for significant expansion. If it's already at 150%, the market might be overextended and due for consolidation.

• Multi-Timeframe Confluence: Use the Stats Table to quickly check if the price on a lower timeframe (e.g., 1H) is approaching a significant level on a higher timeframe (e.g., 1D), adding more weight to that level.

• Defining Bias: If the price opens and holds above the Manipulation zones, it can signal a strong directional bias for the rest of the period.

________________________________________

Settings

• Projection Timeframe: The primary timeframe for which to calculate and display the levels.

• Historical Periods to Show: Set to 1 for only the current period, or increase to see how levels from past periods held up.

• Timezone: Set the timezone for accurate hourly calculations (defaults to America/New_York).

• Visuals: Customize the appearance of the projection lines, labels, and the shaded zones between mean and median levels.

• Stats Table: Enable/disable the table and configure its position, size, and colors.

________________________________________

Disclaimer: This indicator is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset. All trading involves risk, and past performance is not indicative of future results. Please do your own research and risk management.

Enjoy!