Fed Balance Sheet vs GDP RatioThis indicator tracks the size of the Federal Reserve’s Balance Sheet relative to the total US Economy (Nominal GDP). It serves as a primary gauge for systemic liquidity and the extent of monetary intervention in the markets.

How it Works: The script calculates the ratio between:

Fed Total Assets (FRED:WALCL) - The total amount of bonds and assets held by the Fed.

US Nominal GDP (FRED:GDP) - The annualized economic output of the US.

How to Read the Levels: I have plotted historical reference lines to help contextualize the current cycle:

🔴 35% (Pandemic Peak): The absolute high of monetary stimulus (2020–2022). This represents maximum liquidity, where the Fed "printed" massive amounts of money to support the economy.

🟠 ~20% (The "Danger Zone"): This was the range established after the 2008 Financial Crisis (2014–2019). Watch this level closely. In late 2019, when the Fed tried to push the ratio below ~18%, the banking plumbing broke (the Repo Crisis), forcing them to restart QE. We are currently approaching this level again.

⚪ 6% (Pre-2008 Normal): The historical baseline before the era of Quantitative Easing (QE) began.

Why This Matters:

Rising Ratio: Suggests the Fed is expanding liquidity (QE) faster than the economy is growing. Historically, this is a tailwind for risk assets (Stocks, Crypto).

Falling Ratio: Suggests the Fed is tightening (QT) or the economy is outgrowing the money supply. This represents a headwind for liquidity and risk assets.

Methodology Note:

Data Source: Federal Reserve Economic Data (FRED).

Calculation: No manual annualization is applied to GDP, as FRED:GDP is already reported as a Seasonally Adjusted Annual Rate (SAAR).

Ratio

PEG RSI [Auto EPS Growth]The PEG RSI is a hybrid indicator that combines fundamental valuation with technical momentum. It applies the Relative Strength Index (RSI) directly to the Price/Earnings-to-Growth (PEG) Ratio.

Unlike traditional PEG indicators that require manual input for growth rates, this script automatically calculates the Compound Annual Growth Rate (CAGR) of Earnings Per Share (EPS) based on historical data.

Key Features

- Auto-Calculated Growth: Uses historical TTM Earnings Per Share (EPS) to calculate the CAGR over a user-defined period (Default: 4 years).

- Dynamic Valuation: Converts the static PEG ratio into an oscillator (RSI) to identify relative valuation extremes.

- Trend & Momentum: Visualizes the momentum of the PEG ratio relative to its own history.

Educational Case Study

This indicator is designed for educational purposes and research. Instead of relying on fixed overbought or oversold levels, users are encouraged to study the correlation between the PEG RSI and price action independently.

- Observe how the price reacts when the PEG RSI reaches upper or lower extremes.

- Different stocks may respect different RSI zones based on their growth stability.

- Use this tool to analyze how market valuation momentum shifts over time.

Settings:

- Years for CAGR Growth: Timeframe to calculate EPS growth (Default: 4 years).

- RSI Length: Lookback period for the RSI calculation (Default: 14).

Note: This indicator works best on stocks with a consistent history of earnings. It requires financial data to function (will not work on assets without EPS like Crypto or Forex).

Fibonacci Vision ProFibonacci Precision Signals Pro | Smart Buy & Sell Alerts

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

OVERVIEW

This indicator combines Fibonacci mathematics with advanced signal filtering to deliver precise buy and sell signals. It automatically detects swing structure, calculates the key 0.618 retracement level, and generates signals only when multiple confirmation factors align.

Clean. Accurate. Professional.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

HOW IT WORKS

The script identifies swing highs and lows, then calculates Fibonacci retracement levels automatically. When price interacts with the 0.618 zone and all filters confirm, a signal appears:

▲ buy — Long entry opportunity

▼ sell — Short entry opportunity

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

6-LAYER CONFIRMATION SYSTEM

Every signal must pass through:

Trend Direction Analysis

Fibonacci Level Interaction

EMA Trend Filter (50-period default)

RSI Momentum Validation (14-period default)

Volume Spike Detection

Candlestick Pattern Recognition (Pin bars, Engulfing, Momentum candles)

This multi-layer approach significantly reduces false signals.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

BUILT-IN RISK MANAGEMENT

Every trade includes automatic stop loss and take profit levels:

Stop Loss: 100 pips

Take Profit: 200 pips

Risk-Reward Ratio: 1:2

Adjust these values in settings to match your trading style.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

KEY FEATURES

✅ Automatic Fibonacci calculation — no manual drawing

✅ Multi-timeframe compatibility — M15 to Daily

✅ Universal market support — Forex, Crypto, Stocks, Indices

✅ Clean minimalist signals — white triangles with text

✅ Customizable filters — adjust sensitivity to your preference

✅ Built-in alerts — never miss a signal

✅ No repainting — signals remain fixed once confirmed

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Swing Detection:

Swing Length — Controls sensitivity to market structure (default: 10)

Confirmation Bars — Bars required to confirm signal (default: 1)

Signal Filters:

EMA Trend Filter — Toggle trend confirmation on/off

EMA Length — Adjust trend filter period (default: 50)

RSI Filter — Toggle momentum confirmation on/off

RSI Length — Adjust momentum period (default: 14)

Volume Filter — Toggle volume confirmation on/off

Volume Multiplier — Set volume threshold (default: 1.2x average)

Risk Management:

Stop Loss Pips — Set your stop loss distance (default: 100)

Take Profit Pips — Set your profit target (default: 200)

Pip Value — Adjust for your instrument (0.0001 for most Forex, 0.01 for JPY pairs)

Visuals:

Show Signals — Toggle signal visibility

Show Cloud — Toggle Fibonacci zone visibility

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

BEST PRACTICES

Use on H1 or H4 timeframes for optimal results

Trade in direction of the higher timeframe trend

Avoid trading during major news events

Combine with proper position sizing

Always use the built-in stop loss

Be patient — quality signals over quantity

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

MARKETS SUPPORTED

Forex — All major, minor, and exotic pairs

Crypto — BTC, ETH, and altcoins

Stocks — Any equity on TradingView

Indices — S&P500, NASDAQ, DAX, FTSE, etc.

Commodities — Gold, Silver, Oil, etc.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

WHY FIBONACCI?

The 0.618 ratio (Golden Ratio) is observed by traders worldwide. When price retraces to this level, it often:

Reverses direction

Finds support or resistance

Creates high-probability entry opportunities

This script automates the detection of these key moments.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ALERTS INCLUDED

Set up notifications to receive signals on:

Mobile push notifications

Desktop popups

Email alerts

Webhook integrations

Never miss a trading opportunity again.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

WHAT MAKES THIS DIFFERENT

Most indicators give too many signals. This one focuses on quality.

Most indicators clutter your chart. This one keeps it clean.

Most indicators ignore risk management. This one includes it.

Most indicators work on one market. This one works on all.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DISCLAIMER

This indicator is a trading tool, not financial advice. Trading involves substantial risk of loss. Past performance does not guarantee future results. Always use proper risk management and never trade with money you cannot afford to lose. Test on a demo account before trading live.

D.Y Volume Swing Strategy📌 Summary of the Daniel.Yer Volume Strategy

This strategy is based on identifying the "opening volume peak" at the start of each trading day, using a user-defined sampling window.

After the sampling period ends, the strategy looks for breakouts above the daily high or below the daily low, provided they occur with a strong high-volume candle that meets the user-set threshold.

When a breakout appears in one direction, the strategy waits for an opposite-direction confirmation candle (Reversal Confirmation) and then enters a smart counter-breakout trade.

Each trade includes dynamic Stop-Loss and Take-Profit levels calculated from recent price structure, with the option to multiply stop distance according to user preference.

The strategy also gives full control over entering long only, short only, or both, as well as choosing whether trades occur exclusively from the high/low or without restrictions.

The strategy can be tested on any timeframe and evaluated across four trading directions:

✔ Buy from High

✔ Sell from High

✔ Buy from Low

✔ Sell from Low

PE Fair ValueIn short, it’s an automated fair value estimator based on the price-to-earnings model, with full manual control if TradingView’s fundamental data is missing.

Summary:

1. Lets the user choose the EPS source – either automatically from TradingView fundamentals (EPS TTM) or a manual value.

2. Attempts to fetch the stock’s P/E ratio (TTM) automatically; if unavailable, it uses a manual fallback P/E.

3. Calculates:

Actual P/E = current price ÷ EPS

Fair Value = EPS × chosen (auto/manual) P/E

Percentage difference between market price and fair value

4. Plots the fair-value line on the chart for visual comparison.

5. Displays a table in the top-right corner showing:

EPS used

Target P/E

Actual P/E

Fair value

Current price

Difference vs fair value (colored green or red)

6. Creates alerts when the stock is trading above or below the calculated fair value.

7. Also plots the current closing price for reference.

Quarterly EarningsThis Pine script shows quarterly EPS, Sales, and P/E (TTM-based) in a styled table.

PE Rating by The Noiseless TraderPE Rating by The Noiseless Trader

This script analyzes a symbol’s Price-to-Earnings (P/E) ratio, using Diluted EPS (TTM) fundamentals directly from TradingView.

The script calculates the Price-to-Earnings ratio (P/E) using Diluted EPS (TTM) fundamentals. It then identifies:

PE High → the highest valuation point over a 3-year historical range.

PE Low → the lowest valuation point over a 3-year historical range.

PE Median → the midpoint between the two extremes, offering a fair-value benchmark.

PE (Int) → an additional intermediate low to track more recent undervaluation points. This is calculated based on lowest valuation point over a 1-year historical range

These levels are plotted directly on the chart as horizontal references, with markers showing the exact bars/dates when the extremes occurred. Candles corresponding to those days are also highlighted for context.

Bars corresponding to these extremes are highlighted (red = PE High, green = PE Low).

How it helps

Provides a historical valuation framework that complements technical analysis. We look for long opportunity or base formation near the PE Low and be cautious when stocks tends to trade near High PE.

We do not short the stock at High PE infact be cautious with long trades.

Helps identify whether current price action is happening near overvalued or undervalued zones.

Adds a long-term perspective to support swing trading and investing decisions. If a stock is coming from Low PE to Median PE and along with that if we get entry based on Classical strategies like Darvas Box, or HH-HL based on Dow Theory.

Offers a simple visual map of how far the market has moved from “cheap” to “expensive.”

This tool is best suited for long-term investors and swing traders who want to merge fundamentals with technical setups.

This indicator is designed as an educational tool to illustrate how valuation metrics (like earnings multiples) can be viewed alongside price action, helping traders connect fundamental context with technical execution in real market conditions.

NYSE Advancing Issues & Volume RatiosOverview

This comprehensive market breadth indicator tracks two essential NYSE ratios that provide deep insights into market sentiment and internal strength:

NYSE Advancing Issues Ratio

NYSE Advancing Volume Ratio

Dual Ratio Analysis

Issues Ratio: Measures the percentage of NYSE stocks advancing vs. total issues

Volume Ratio: Measures the percentage of NYSE volume flowing into advancing stocks

Both ratios displayed as easy-to-read percentages (0-100%)

Customizable Display Options

Toggle each ratio on/off independently

Choose from multiple moving average types (SMA, EMA, WMA)

Adjustable moving average periods

Custom color schemes for better visualization

Reference Levels

50% Line: Market neutral point (gray dashed)

10% Line: Extremely bearish breadth (red dotted)

90% Line: Extremely bullish breadth (green dotted)

Optional background highlighting for extreme readings

Smart Alerts

Cross above/below 50% (neutral) for both ratios

Extreme readings: Above 90% (strong bullish) and below 10% (strong bearish)

Real-time notifications for key market breadth shifts

📈 How to Interpret

Bullish Signals

Above 50%: More stocks/volume advancing than declining

Above 90%: Extremely strong market breadth (rare occurrence)

Divergence: Price making new highs while breadth weakens (potential warning)

Market Timing

Extreme readings (10%/90%) often coincide with market turning points

Breadth thrusts from extreme levels can signal powerful moves

Use with other technical indicators for enhanced timing

Tick Ratio Simulator - Advanced Market Sentiment IndicatorOverview

The Tick Ratio Simulator is a sophisticated market sentiment indicator that provides real-time insights into buying and selling pressure dynamics. This proprietary indicator transforms complex market microstructure data into actionable trading signals.

Key Features

Real-Time Sentiment Analysis: Captures instantaneous shifts in market momentum

Multi-Timeframe Adaptability: Customizable calculation periods for any trading style

Visual Clarity: Color-coded histogram with dynamic zone highlighting

Integrated Alert System: Pre-configured alerts for key market transitions

Performance Dashboard: Live metrics display for informed decision-making

Trading Applications

✓ Trend Confirmation: Validate existing trends with momentum analysis

✓ Reversal Detection: Identify potential turning points at extreme readings

✓ Entry/Exit Timing: Optimize trade execution with overbought/oversold zones

✓ Risk Management: Clear visual boundaries for position sizing decisions

Signal Interpretation

Extreme Zones (±75): High probability reversal areas

Standard Thresholds (±50): Traditional overbought/oversold levels

Zero Line Crossings: Momentum shift confirmations

Histogram Expansion/Contraction: Strength of directional bias

Customization Options

Adjustable calculation and smoothing periods

Fully customizable color schemes

Toggle histogram and reference lines

Real-time information table positioning

Alert Conditions

Four pre-built alert templates for automated notifications:

Momentum threshold breaches

Directional changes

Extreme zone entries

Custom level crossovers

Best Practices

Works exceptionally well when combined with:

Volume analysis

Support/resistance levels

Price action patterns

Other momentum oscillators

Note: This indicator uses proprietary calculations to simulate institutional-grade tick analysis without requiring actual tick data feeds. Results are optimized for liquid markets with consistent volume profiles.

For optimal results, adjust parameters based on your specific instrument and timeframe. Past performance does not guarantee future results.

Forward P/E CalculatorI could not find a forward P/E indicator that gave me proper results. So here is mine.

Earnings X-Ray and Fundamentals Data:VSMarketTrendThis indicator calculates essential financial metrics for stocks using TradingView's built-in functions and custom algorithms. The values are derived from fundamental data sources available on TradingView.

Key Output Metrics(YOY Basic Quaterly DATA)

MC (Market Cap): Company’s total market value (Price × Total Shares).

TS (Total Shares Outstanding): All shares (float + restricted) in circulation.

Sales: Annual revenue (TTM or latest fiscal year).

NETIn: Net income

P/E (Price-to-Earnings): Valuation ratio (Market Cap / Net Income or Price / EPS).

EPS (Earnings Per Share): Net income per share (Net Income / TS).

OPM (Operating Margin %): Core profitability (Operating Income / Revenue × 100).

Quick Ratio: Short-term liquidity ((Current Assets – Inventory) / Current Liabilities).

BVPS (Book Value Per Share): Equity per share (Shareholders’ Equity / TS).

PS (Price-to-Sales): Revenue-based valuation (Market Cap / Annual Revenue).

FCF (Free Cash Flow Per Share): Post-CapEx cash ((Operating Cash Flow – CapEx) / TS).

Data Sources & Methods

Uses TradingView’s request.financial() for income/balance sheet data (Revenue, EBITDA, etc.).

Fetches real-time metrics via request.security() (e.g., Shares Outstanding).

Normalizes data across timeframes (quarterly/annual).

Disclaimer

Not financial advice. Verify with official filings before trading.

RATIO TPI SOLETH | JeffreyTimmermansSOLETH Ratio Trend Probability Indicator

Medium-Term Trend Assessment | Dominant Major Detector: The SOLETH Ratio TPI is a medium-term trend-following tool designed to measure the performance relationship between Solana and Ethereum — two of the leading smart contract platforms in the crypto market. By tracking the SOLETH ratio, this indicator determines which of the two is acting as the dominant major in the current market environment.

Rather than focusing on absolute price movements, the SOLETH Ratio TPI isolates relative strength. An upward-trending ratio means Solana is outperforming Ethereum, while a downward trend means Ethereum is taking the lead.

Key Features

Dominant Major Identification:

The indicator’s primary function is to determine leadership between Solana and Ethereum:

SOL Dominant: SOLETH ratio trending up

ETH Dominant: SOLETH ratio trending down

Neutral: No clear leader

8 Trend-Following Inputs:

Integrates 8 carefully selected medium-term trend-following signals into a composite score for clarity and accuracy in dominance detection.

Score-Based Regime Classification:

Score > 0.1 → SOL in relative uptrend → Dominant Major: SOL

Score < -0.1 → ETH in relative uptrend → Dominant Major: ETH

Between -0.1 and 0.1 → Neutral → No clear dominance

Dynamic Visual Interface:

Background colors change according to the dominant asset.

Bottom dashboard displays the status of all inputs, the composite score, and the determined dominance label.

Use Cases:

Smart Contract Sector Rotation: Identify leadership shifts between Solana and Ethereum to guide allocation within the L1 ecosystem.

Sector Sentiment Insight: Dominance changes often precede broader capital flows into or out of each ecosystem.

Multi-Timeframe Confirmation: Combine with broader market LTPI and MTPI tools to reinforce conviction in rotation-based strategies.

Conclusion

The SOLETH Ratio TPI condenses the competition between two of crypto’s top smart contract platforms into one clear, actionable view. By aggregating 8 powerful medium-term trend-following inputs, it delivers a precise assessment of which chain currently leads the market.

RATIO TPI SOLBTC | JeffreyTimmermansSOLBTC Ratio Trend Probability Indicator

Medium-Term Trend Assessment | Dominant Major Detector: The SOLBTC Ratio TPI is a medium-term trend-following indicator designed to measure the relative strength between Solana and Bitcoin — two of the most influential assets in the crypto market. By analyzing the SOLBTC ratio, this tool identifies which of the two is currently the dominant major in the market cycle.

Unlike standard price-based analysis, this indicator focuses on relative dominance. When Solana outperforms Bitcoin, the ratio trends upward, signaling SOL dominance. When Bitcoin outperforms Solana, the ratio trends downward, signaling BTC dominance.

Key Features

Dominant Major Identification:

The primary goal of this TPI is to determine whether Solana or Bitcoin is leading the market:

SOL Dominant: SOLBTC is trending up

BTC Dominant: SOLBTC is trending down

Neutral: No clear leader in the current cycle

8 Trend-Following Inputs:

Combines 8 carefully selected medium-term trend-following indicators into a single composite score for clear and actionable dominance detection.

Score-Based Regime Classification:

Score > 0.1 → SOL in relative uptrend → Dominant Major: SOL

Score < -0.1 → BTC in relative uptrend → Dominant Major: BTC

Between -0.1 and 0.1 → Neutral → No clear dominance

Dynamic Visuals:

Background colors shift to match the dominant asset

Bottom dashboard displays the state of each input, the composite score, and the resulting dominance label

Use Cases:

Rotation Strategies: Identify when capital is rotating between Solana and Bitcoin to optimize positioning.

Market Leadership Signals: Use dominance changes as a leading indicator for broader altcoin cycles and sentiment shifts.

Multi-Timeframe Confirmation: Pair with LTPI and STPI for higher conviction in directional bias.

Conclusion

The SOLBTC Ratio TPI distills the relationship between Solana and Bitcoin into one simple question: Who is leading right now? By combining 8 powerful trend-following inputs into a clear dominance score, it provides traders and investors with a precise, medium-term view of market leadership.

RATIO TPI ETHBTC | JeffreyTimmermansETHBTC Ratio Trend Probability Indicator

Medium-Term Trend Assessment | Dominant Major Detector: The ETHBTC Ratio TPI is a medium-term trend-following indicator designed to measure the relative strength between Ethereum and Bitcoin — the two most dominant assets in crypto. By analyzing the ETHBTC ratio, this tool provides insights into which of the two is currently leading the market trend.

Unlike absolute price indicators, this tool tracks relative dominance. When Ethereum outperforms Bitcoin, the ratio trends upward, signaling ETH dominance. When Bitcoin outperforms Ethereum, the ratio trends downward, signaling BTC dominance.

Key Features

Dominant Major Identification:

The core purpose of this TPI is to determine which asset — Ethereum or Bitcoin — is the dominant major in the current crypto cycle.

ETH Dominant: ETHBTC is trending up

BTC Dominant: ETHBTC is trending down

Neutral: No clear directional edge

8 Trend-Following Inputs:

The indicator aggregates 8 hand-picked, medium-term trend-following metrics into a single score that simplifies the ETHBTC trend assessment.

Score-Based Regime Classification:

Score > 0.1 → ETH is in relative uptrend → Dominant Major: ETH

Score < -0.1 → BTC is in relative uptrend → Dominant Major: BTC

Between -0.1 and 0.1 → Neutral trend → No clear dominance

Dynamic Visuals:

Background color adapts to the dominant asset

Score, trend state per input, and composite result are shown in a clean dashboard

Use Cases:

Rotation Strategy Insight: Understand whether capital is flowing into Ethereum or Bitcoin to adjust your portfolio positioning accordingly.

Dominance-Based Macro Timing: Use the dominance shift as a leading signal for broader altcoin cycles.

Multi-Timeframe Confirmation: Combine with LTPI (Long-Term) and STPI (Short-Term) to build directional conviction.

Conclusion

The ETHBTC Ratio TPI is a highly focused tool that simplifies the complex relationship between Ethereum and Bitcoin into one clear output: who is currently leading the crypto market. With 8 inputs driving a composite trend score and a dynamic dominance label, this indicator is essential for anyone looking to time ETH vs BTC rotations with precision.

Calc win-LoserHow to Use the Calc win-Loser Indicator

The indicator calculates the profit or loss of the operation, showing how much you gained or lost on the invested amount, without adding the initial capital, displaying only the profit or loss separately.

Use a period (.) to separate decimal numbers, without thousand separators (e.g., 1000 for one thousand, 1000.50 for one thousand and fifty cents).

Price Definition for Calculation

Long Position (buy):

Low Price: entry price (lower)

High Price: exit price (higher)

Example: enter at 1 and exit at 3

Short Position (sell):

High Price: entry price (higher)

Low Price: exit price (lower)

Example: enter at 3 and exit at 1

Main Parameters

Parameter Description Example

Low Price Base price for calculation (Long: entry; Short: exit) 1

High Price Base price for calculation (Long: exit; Short: entry) 3

Leverage Operation multiplier (leverage) 2.0

Universal Amount Total amount invested 1000

Broker Fee (%) Percentage fee charged by broker 0.1

Currency Currency symbol for value display USD

Practical Example

Long: entry at 1, exit at 3, 2x leverage, $1000 investment, 0.1% fee.

Short: entry at 3, exit at 1, 2x leverage, $1000 investment, 0.1% fee.

The indicator will show the expected profit or loss based on the percentage difference adjusted by leverage and subtracting the broker fee.

Notes

Adjust prices according to the type of operation (Long or Short).

Use a period for decimals and do not use thousand separators.

This indicator is a simulation tool and does not execute automatic trades.

Original indicator by Canhoto-Medium — protected to maintain order and respect, prevent copying and plagiarism.

Enhanced Zones with Volume StrengthEnhanced Zones with Volume Strength

Your reliable visual guide to market zones — now with Multi-Timeframe (MTF) power!

What you get:

Clear visual zones on your chart — color-coded boxes that highlight important price areas.

Blue Boxes for neutral zones — easy to spot areas of indecision or balance.

Gray Boxes to show normal volume conditions, giving you context without clutter.

Green Boxes highlighting bullish zones where strength is showing.

Red Boxes marking bearish zones where weakness might be in play.

Multi-Timeframe Support:

Seamlessly visualize these zones from higher timeframes directly on your current chart for a bigger-picture view, helping you make smarter trading decisions.

How to use it:

Adjust the box width (in bars) to fit your trading style and timeframe.

Customize colors and opacity to suit your chart theme.

Toggle neutral blue and gray volume boxes on/off to focus on what matters most to you.

Set the maximum number of boxes to keep your chart clean and performant.

Why you’ll love it:

This indicator cuts through the noise by visually marking zones where volume and price action matter the most — without overwhelming your chart. The MTF feature means you’re always aligned with higher timeframe trends without switching views.

Pro tip:

Use these boxes as dynamic support/resistance areas or to confirm trade setups alongside your favorite indicators.

No complicated formulas here, just crisp, actionable visuals designed for clarity and confidence.

Metatrader CalculatorThe “ Metatrader Calculator ” indicator calculates the position size, risk, and potential gain of a trade, taking into account the account balance, risk percentage, entry price, stop loss price, and risk/reward ratio. It supports the XAUUSD, XAGUSD, and BTCUSD pairs, automatically calculating the position size (in lots) based on these parameters. The calculation is displayed in a table on the chart, showing the lot size, loss in dollars, and potential gain based on the defined risk.

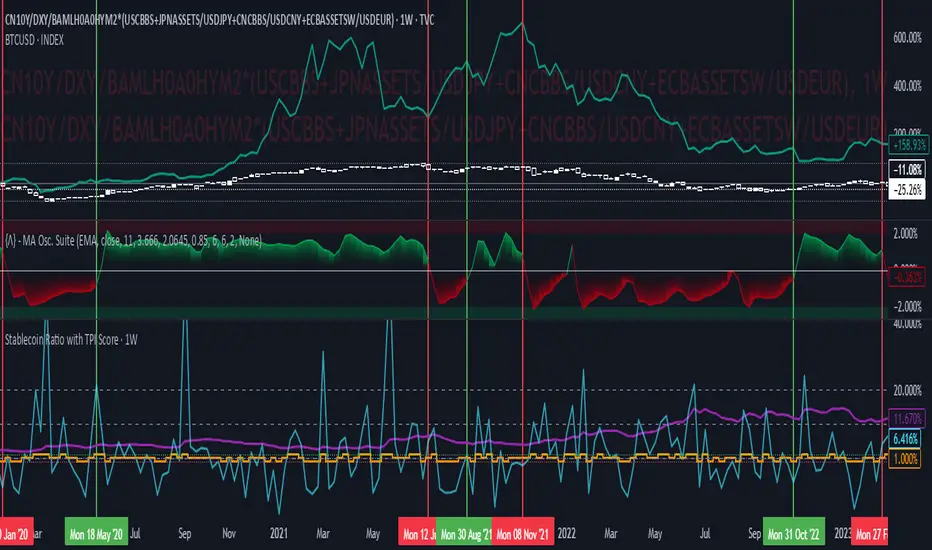

Stablecoin Ratio with TPI ScoreThe script measures the stablecoin ratio (total stablecoin market cap divided by total crypto market cap, times 100) and its weekly change. Stablecoins (e.g., USDT, USDC) are a key gateway for capital entering or exiting the crypto ecosystem.

A rising ratio suggests more capital is parked in stablecoins (potential buying power), while a falling ratio indicates capital leaving (selling or withdrawal).

In a macro analysis, this is critical—it reflects the availability of liquid funds that could fuel price movements.

In macroeconomics, liquidity is a driver of asset prices.

In crypto, stablecoins represent sidelined capital ready to deploy.

How does it work?

Stablecoin Ratio:

Formula: (total_stablecoin_mcap / total_crypto_mcap) * 100.

Example: If stablecoins = $235B and total market cap = $2.5T, ratio = 9.4%.

Plotted as a red line in the oscillator pane, showing the percentage of the market held in stablecoins.

Weekly Change:

Calculates the percentage change in the ratio from the previous week:

(current_ratio - previous_ratio) / previous_ratio * 100.

Example: Ratio goes from 9% to 10% = +11.11% change.

TPI Score Assignment:

+1 (Bullish): If the ratio increases by more than 5% week-over-week.

-1 (Bearish): If the ratio decreases by more than 5% week-over-week.

0 (Neutral): If the change is between -5% and +5%.

Plotted as orange step line bars in the oscillator pane, snapping to +1, 0, or -1.

Put/Call RatioPut/Call Ratio Indicator

This indicator visualizes the Put/Call Ratio for various market symbols, helping traders assess market sentiment and potential reversals. It offers a dropdown menu to select from a range of Put/Call Ratios, including broad equities (CBOE), major indices (SPX, QQQ, IWM, VIX), and individual stocks (TSLA, GOOG, META, AMZN, MSFT, INTC).

The indicator plots the Put/Call Ratio with adjustable moving averages and standard deviation bands to highlight overbought or oversold conditions. A short-term moving average (default: 10 periods) is displayed with trend-based coloring, while longer-term moving averages (defaults: 30 and 200 periods) are calculated but hidden by default. Bands at 1, 1.5, and 2 standard deviations provide context for extreme readings.

Key Overbought/Oversold Signals:

Short-Term Extremes: The 10-day moving average moves beyond 1 standard deviation from the 200-day moving average, signaling potential overbought (above) or oversold (below) conditions. This will be highlighted by red or green background color.

Ratio Extremes: The Put/Call Ratio line itself crosses outside 2 standard deviations from the 200-day moving average, indicating stronger overbought or oversold zones.

Conditional coloring of the ratio line reflects its position relative to the bands, and background shading highlights when the short-term moving average crosses key levels.

Key Features:

Selectable Put/Call Ratio symbols.

Trend-colored moving averages.

Standard deviation bands for volatility analysis.

Dynamic line and background coloring for quick insights.

Usage:

Use this indicator to gauge market sentiment—high ratios may suggest bearish sentiment or oversold conditions, while low ratios may indicate bullish sentiment or overbought conditions. Combine with price action or other tools for confirmation.

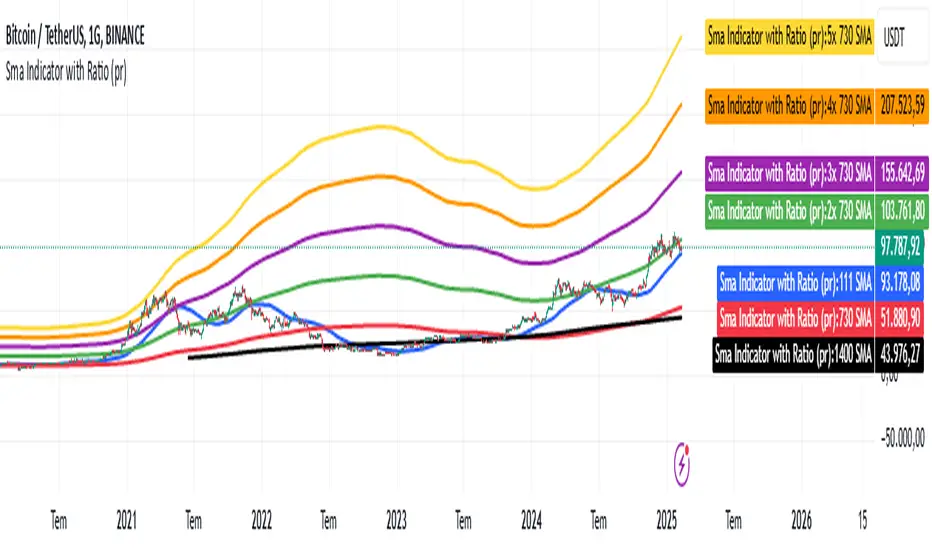

Sma Indicator with Ratio (pr)SMA Indicator with Ratio (PR) is a technical analysis tool designed to provide insights into the relationship between multiple Simple Moving Averages (SMAs) across different time frames. This indicator combines three key SMAs: the 111-period SMA, 730-period SMA, and 1400-period SMA. Additionally, it introduces a ratio-based approach, where the 730-period SMA is multiplied by factors of 2, 3, 4, and 5, allowing users to analyze potential market trends and price movements in relation to different SMA levels.

What Does This Indicator Do?

The primary function of this indicator is to track the movement of prices in relation to several SMAs with varying periods. By visualizing these SMAs, users can quickly identify:

Short-term trends (111-period SMA)

Medium-term trends (730-period SMA)

Long-term trends (1400-period SMA)

Additionally, the multiplied versions of the 730-period SMA provide deeper insights into potential price reactions at different levels of market volatility.

How Does It Work?

The 111-period SMA tracks the shorter-term price trend and can be used for identifying quick market movements.

The 730-period SMA represents a longer-term trend, helping users gauge overall market sentiment and direction.

The 1400-period SMA acts as a very long-term trend line, giving users a broad perspective on the market’s movement.

The ratio-based SMAs (2x, 3x, 4x, 5x of the 730-period SMA) allow for an enhanced understanding of how the price reacts to higher or lower volatility levels. These ratios are useful for identifying key support and resistance zones in a dynamic market environment.

Why Use This Indicator?

This indicator is useful for traders and analysts who want to track the interaction of price with different moving averages, enabling them to make more informed decisions about potential trend reversals or continuations. The added ratio-based values enhance the ability to predict how the market might react at different levels.

How to Use It?

Trend Confirmation: Traders can use the indicator to confirm the direction of the market. If the price is above the 111, 730, or 1400-period SMA, it may indicate an uptrend, and if below, a downtrend.

Support/Resistance Levels: The multiplied versions of the 730-period SMA (2x, 3x, 4x, 5x) can be used as dynamic support or resistance levels. When the price approaches or crosses these levels, it might indicate a change in the trend.

Volatility Insights: By observing how the price behaves relative to these SMAs, traders can gauge market volatility. Higher multiples of the 730-period SMA can signal more volatile periods where price movements are more pronounced.

Zanger Volume Ratio (ZVR)Zanger Volume Ratio (ZVR)

Credits:

Most of the underlying code and logic in this script have been adapted from the work originally published by The_Peaceful_Lizard

Overview

The Zanger Volume Ratio (ZVR) is a powerful indicator designed to reveal market dynamics by comparing current cumulative volume to an average determined over a historical look-back period. It uses the concept of relative volume to not only highlight unusual volume spikes, but also uses color to illustrate how today's trading compares to typical levels. This unique method of volume analysis was popularized by Dan Zanger - a trader known for turning $10,775 into $18,000,000 in less than two years - by identifying key shifts in market interest and volume behavior.

Key Features

Volume Pacing Analysis:

The script calculates a volume delta by comparing the cumulative volume at any given moment to an average derived over a user-defined lookback period (Default 20-day). The resulting percentage difference offers a clear visualization and insight into unusual volume activity.

Dynamic Visual Representation:

Choose between either “Columns” or “Area” plot styles to display the percent difference. Additionally, you have the option to switch between a standard plot or a background color display, with customizable transparency, ensuring the indicator fits seamlessly with your chart’s aesthetics.

Dashboard Integration:

A simple dashboard table is displayed on the chart, showcasing the current ZVR value in real-time. With user-configurable position, text size, alignment, and color options, this feature ensures that the key metric is always visible and easy to interpret.

Why Use the Zanger Volume Ratio?

The ZVR is more than just a volume indicator. It acts as a window into market sentiment by highlighting days when trading interest intensifies. Many traders believe that an unusually high volume ratio may confirm trend strength or signal a reversal, making the indicator a valuable tool when used in conjunction with other technical analysis methods.

Whether you’re monitoring stocks, commodities, or forex markets, the Zanger Volume Ratio offers an accessible yet sophisticated method to decode volume dynamics. Its practical design and real-time visual feedback provide traders of all experience levels with critical data to spot high-potential setups.

Chart Description

First Pane: normal Volume Indicator on the foreground, ZVR as Background colors

Second Pane: ZVR Indicator with Column Style (default)

First panel: normal volume indicator in foreground, ZVR as background colors

Second panel: ZVR indicator with column style (default)

Note: This indicator is intended for use on intraday charts only!

Simple Time-Based Strategy(Price Action Hypothesis)Core Theory: Trend Continuation Pattern Recognition**

1. **Price Action Hypothesis**

The strategy is built on the assumption that consecutive price movements (3-bar patterns) indicate momentum continuation:

- *Long Pattern*: Three consecutive higher closes combined with ascending highs

- *Short Pattern*: Three consecutive lower closes combined with descending lows

This reflects a belief that sustained directional price movement creates self-reinforcing trends that can be captured through simple pattern recognition.

2. **Time-Based Risk Management**

Implements a dynamic exit mechanism:

- *Training Phase*: 5-bar holding period (quick turnover)

- *Testing Phase*: 10-bar holding period (extended exposure)

This dual timeframe approach suggests the hypothesis that market conditions may require different holding durations in different market eras.

3. **Adaptive Market Hypothesis**

The structure incorporates two distinct phases:

- *Training Period (11 years)*: Pattern recognition without stop losses

- *Testing Period*: Pattern recognition with stop losses

This assumes markets may change character over time, requiring different risk parameters in different epochs.

4. **Asymmetric Risk Control**

Implements stop-losses only in the testing phase:

- Fixed 500-pip (point) stop distance

- Activated post-training period

This reflects a belief that historical patterns might need different risk constraints than real-time trading.

5. **Dual-Path Validation**

The split between training/testing phases suggests:

- Pattern validity should first be confirmed without protective stops

- Real-world implementation requires added risk constraints

6. **Market Efficiency Paradox**

The simultaneous use of both long/short entries assumes:

- Markets exhibit persistent inefficiencies

- These inefficiencies manifest differently in bullish/bearish conditions

- A symmetric approach can capture opportunities in both directions

7. **Behavioral Finance Elements**

The 3-bar pattern recognition potentially exploits:

- Herd mentality in trend formation

- Delayed reaction to price momentum

- Cognitive bias in trend confirmation

8. **Quantitative Time Segmentation**

The annual-based period division (training vs testing) implies:

- Market cycles operate on multi-year timeframes

- Strategy robustness requires validation across different market regimes

- Parameter sensitivity needs temporal validation

This strategy combines elements of technical pattern recognition, temporal adaptability, and phased risk management to create a systematic approach to trend exploitation. The theoretical framework suggests markets exhibit persistent but evolving patterns that can be systematically captured through rule-based execution.

MATA GOLD RATIOMata Gold Instrument: User Guide

The Instrument to Gold Oscillator is a technical analysis tool that normalizes the ratio of an instrument's price (e.g., BTC/USD) to the price of gold (XAU/USD) into a 0-100 scale. This provides a clear and intuitive way to evaluate the relative performance of an instrument compared to gold over a specified period.

---

How It Works

1. Calculation of the Ratio:

The ratio is calculated as:

\text{Ratio} = \frac{\text{Instrument Price}}{\text{Gold Price}}

2. Normalization:

The ratio is normalized using the highest and lowest values over a user-defined period (length), typically 14 periods:

\text{Normalized Ratio} = \frac{\text{Ratio} - \text{Min(Ratio)}}{\text{Max(Ratio)} - \text{Min(Ratio)}} \times 100

3. Overbought/Oversold Levels:

Above 80: The instrument is relatively expensive compared to gold (overbought).

Below 20: The instrument is relatively cheap compared to gold (oversold).

---

How to Use the Oscillator

1. Identify Overbought and Oversold Levels:

If the oscillator rises above 80, the instrument may be overvalued relative to gold. This could signal a potential reversal or correction.

If the oscillator falls below 20, the instrument may be undervalued relative to gold. This could signal a buying opportunity.

2. Track Trends:

Rising oscillator values indicate the instrument is gaining value relative to gold.

Falling oscillator values indicate the instrument is losing value relative to gold.

3. Crossing the Midline (50):

When the oscillator crosses above 50, the instrument's value is gaining strength relative to gold.

When it crosses below 50, the instrument is weakening relative to gold.

4. Combine with Other Indicators:

Use this oscillator alongside other technical indicators (e.g., RSI, MACD, STOCH) for more robust decision-making.

Confirm signals from the oscillator with price action or volume analysis.

---

Example Scenarios

1. Trading Cryptocurrencies Against Gold:

If BTC/USD's oscillator value is above 80, Bitcoin may be overvalued relative to gold. Consider reducing exposure or looking for short opportunities.

If BTC/USD's oscillator value is below 20, Bitcoin may be undervalued relative to gold. This could be a good time to accumulate.

2. Commodities vs. Gold:

Analyze the relative strength of commodities (e.g., oil, silver) against gold using the oscillator to identify periods of overperformance or underperformance.

---

Advantages of the Oscillator

Relative Performance Insight: Tracks the performance of an instrument relative to gold, providing a macro perspective.

Clear Visual Representation: The 0-100 scale makes it easy to identify overbought/oversold conditions and trend shifts.

Customizable Periods: The user-defined length allows flexibility in analyzing short- or long-term trends.

---

Limitations

Dependence on Gold: As the oscillator is based on gold prices, any external shocks to gold (e.g., geopolitical events) can influence its signals.

No Absolute Buy/Sell Signals: The oscillator should not be used in isolation but as part of a broader analysis strategy.

---

By using the Instrument to Gold Oscillator effectively, traders and investors can gain valuable insights into the relative valuation and performance of assets compared to gold, enabling more informed trading and investment decisions.