WECAN Magic Indicator ₹ InvestmentScript Name: WECAN Magic Indicator 1

Company: WECAN GROW ACADEMY

Contact: +91 85678 98484

Description:

The WECAN Magic Indicator 1 is a powerful trading tool developed by WECAN GROW ACADEMY. It combines multiple technical analysis components such as EMA trends, MACD signals, and custom logic to generate precise Buy and Sell signals. The script features a clean on-chart display and a chronological table view of past trades, helping traders quickly review performance and market timing. Ideal for intraday and positional trading strategies, this indicator aims to simplify decision-making for both beginners and professionals.

For support or training, contact us at +91 85678 98484.

Portföy Yönetimi

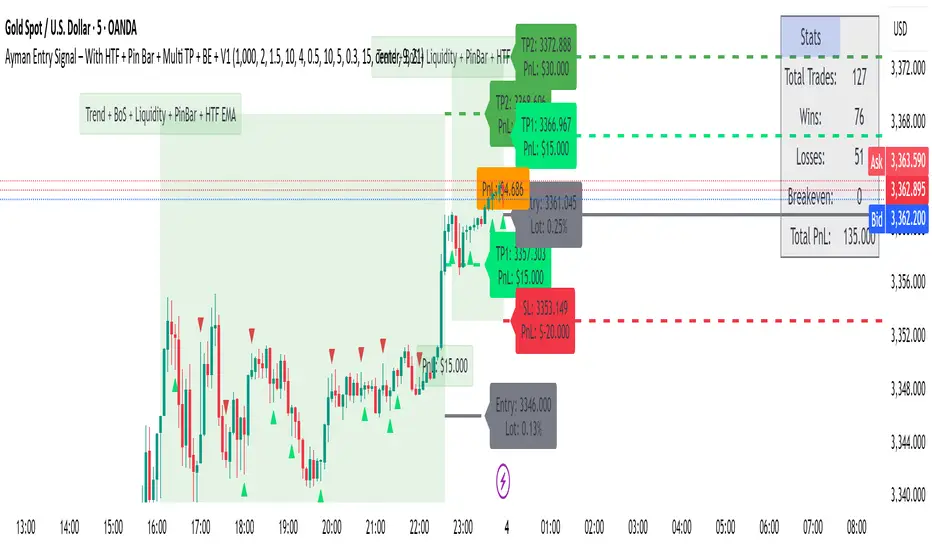

Ayman Entry Signal – With HTF + Pin Bar

A professional and versatile trading indicator combining classic technical analysis with Smart Money Concepts to detect high-probability entry points.

Designed especially for scalping gold and forex pairs on lower timeframes. Fully customizable to suit any trading style.

✅ Key Features:

EMA Trend Confirmation

Break of Structure (BoS) Detection

Order Block Zone Recognition

Fair Value Gap (FVG) Confirmation

Liquidity Sweep Detection

Pin Bar Candlestick Confirmation

Higher Timeframe Confirmation (HTF EMA + HTF BoS)

🎯 Smart Risk Management:

Automatically calculates Stop Loss (SL) and Take Profit (TP) based on the selected timeframe.

Dynamically adjusts lot size based on account capital and risk percentage.

📈 How It Works:

The indicator triggers a Buy or Sell signal only when a selected set of conditions are met, including:

Trend direction (EMA crossover)

Break of structure

Presence within strong supply/demand zones

Confirmation from higher timeframe

Reversal Pin Bar pattern

🛎 Alerts:

Built-in alert system notifies you instantly when a valid Buy or Sell signal is triggered.

⚙️ Customizable Settings:

Risk Percentage

Capital Size

HTF timeframe

Enable/Disable individual filters (EMA, BoS, OB, FVG, Liquidity, Pin Bar, HTF)

📌 Best Timeframes:

1-min, 5-min, and 15-min – especially during high-volume sessions like London or New York.

🔸 Note:

This is not financial advice. Always backtest and use manual confirmations before live trading.

Wallet Follower - [Silver-Wong]Track your active positions directly on your chart with a simple, clear display.

Key Features:

- Displays a summary table of up to 5 custom positions.

- Real-time calculation of P/L (%) and net gain/loss based on your entry price and quantity.

- Automatically updates with live prices.

- Works with any symbol: crypto, stocks, forex...

- Customizable display: text size and screen position.

Why use it?

Save time and keep a precise overview of your portfolio without leaving your chart. Ideal for both active traders and long-term holders.

🌊 Reinhart-Rogoff Financial Instability Index (RR-FII)Overview

The Reinhart-Rogoff Financial Instability Index (RR-FII) is a multi-factor indicator that consolidates historical crisis patterns into a single risk score ranging from 0 to 100. Drawing from the extensive research in "This Time is Different: Eight Centuries of Financial Crises" by Carmen M. Reinhart and Kenneth S. Rogoff, the RR-FII translates nearly a millennium of crisis data into practical insights for financial markets.

What It Does

The RR-FII acts like a real-time financial weather forecast by tracking four key stress indicators that historically signal the build-up to major financial crises. Unlike traditional indicators based only on price, it takes a broader view, examining the global market's interconnected conditions to provide a holistic assessment of systemic risk.

The Four Crisis Components

- Capital Flow Stress (Default weight: 25%)

- Data analyzed: Volatility (ATR) and price movements of the selected asset.

- Detects abrupt volatility surges or sharp price falls, which often precede debt defaults due to sudden stops in capital inflow.

- Commodity Cycle (Default weight: 20%)

- Data analyzed: US crude oil prices (customizable).

- Watches for significant declines from recent highs, since commodity price troughs often signal looming crises in emerging markets.

- Currency Crisis (Default weight: 30%)

- Data analyzed: US Dollar Index (DXY, customizable).

- Flags if the currency depreciates by more than 15% in a year, aligning with historical criteria for currency crashes linked to defaults.

- Banking Sector Health (Default weight: 25%)

- Data analyzed: Performance of financial sector ETFs (e.g., XLF) relative to broad market benchmarks (SPY).

- Monitors for underperformance in the financial sector, a strong indicator of broader financial instability.

Risk Scale Interpretation

- 0-20: Safe – Low systemic risk, normal conditions.

- 20-40: Moderate – Some signs of stress, increased caution advised.

- 40-60: Elevated – Multiple risk factors, consider adjusting positions.

- 60-80: High – Significant probability of crisis, implement strong risk controls.

- 80-100: Critical – Several crisis indicators active, exercise maximum caution.

Visual Features

- The main risk line changes color with increasing risk.

- Background colors show different risk zones for quick reference.

- Option to view individual component scores.

- A real-time status table summarizes all component readings.

- Crisis event markers appear when thresholds are breached.

- Customizable alerts notify users of changing risk levels.

How to Use

- Apply as an overlay for broad risk management at the portfolio level.

- Adjust position sizes inversely to the crisis index score.

- Use high index readings as a warning to increase vigilance or reduce exposure.

- Set up alerts for changes in risk levels.

- Analyze using various timeframes; daily and weekly charts yield the best macro insights.

Customizable Settings

- Change the weighting of each crisis factor.

- Switch commodity, currency, banking sector, and benchmark symbols for customized views or regional focus.

- Adjust thresholds and visual settings to match individual risk preferences.

Academic Foundation

Rooted in rigorous analysis of 66 countries and 800 years of data, the RR-FII uses empirically validated relationships and thresholds to assess systemic risk. The indicator embodies key findings: financial crises often follow established patterns, different types of crises frequently coincide, and clear quantitative signals often precede major events.

Best Practices

- Use RR-FII as part of a comprehensive risk management strategy, not as a standalone trading signal.

- Combine with fundamental analysis for complete market insight.

- Monitor for differences between component readings and the overall index.

- Favor higher timeframes for a broader macro view.

- Adjust component importance to suit specific market interests.

Important Disclaimers

- RR-FII assesses risk using patterns from past crises but does not predict future events.

- Historical performance is not a guarantee of future results.

- Always employ proper risk management.

- Consider this tool as one element in a broader analytical toolkit.

- Even with high risk readings, markets may not react immediately.

Technical Requirements

- Compatible with Pine Script v6, suitable for all timeframes and symbols.

- Pulls data automatically for USOIL, DXY, XLF, and SPY.

- Operates without repainting, using only confirmed data.

The RR-FII condenses centuries of financial crisis knowledge into a modern risk management tool, equipping investors and traders with a deeper understanding of when systemic risks are most pronounced.

🧪 Yuri Garcia Smart Money Strategy FULL (Slope Divergence))📣 Yuri Garcia – Smart Money Strategy FULL

This is my private Smart Money Concept strategy, designed for my family and community to learn, trade, and grow sustainably.

🔑 How it works:

✅ Volume Cluster Zones: Automatically detects areas where strong buyers or sellers concentrate, acting as dynamic S/R levels.

✅ HTF Institutional Zones (4H): Higher timeframe trend filter ensures you’re always trading in the direction of major flows.

✅ Wick Pullback Filter: Confirms price rejects the zone, catching smart money traps and reversals.

✅ Cumulative Delta (CVD): Confirms whether buyers or sellers are truly in control.

✅ Slope-Based Divergence: Optional hidden divergence between price & CVD to spot reversals others miss.

✅ ATR Dynamic SL/TP: Adapts stop loss and take profit to live volatility with adjustable risk/reward.

🧩 Visual Markers Explained:

🟦 Blue X: Price inside HTF zone

🟨 Yellow X: Price inside Volume Cluster zone

🟧 Orange Circle: Wick pullback detected

🟥 Red Square: CVD confirms order flow strength

🔼 Aqua Triangle Up: Bullish slope divergence

🔽 Purple Triangle Down: Bearish slope divergence

🟢 Green Triangle Up: Final Long Entry confirmed

🔴 Red Triangle Down: Final Short Entry confirmed

⚡ Who is this for?

This strategy is best suited for traders who understand smart money concepts, order flow, and want an adaptive framework to trade major assets like BTC, Gold, SP500, NASDAQ, or FX pairs.

🔒 Important

Use responsibly, backtest extensively, and combine with solid risk management. This is for educational purposes only.

✨ Credits

Built with ❤️ by Yuri Garcia – dedicated to my family & community.

✅ How to use it

1️⃣ Add to chart

2️⃣ Adjust inputs for your asset & timeframe

3️⃣ Enable/disable slope divergence filter to match your style

4️⃣ Set your alerts with built-in conditions

Quantum Dip Spectrum | QuantumResearch🔹 Quantum DipSpectrum | QuantumResearch

Purpose:

The Quantum DipSpectrum is a market breadth indicator designed to identify broad-based oversold conditions across a basket of 40 altcoins. It helps traders detect potential accumulation phases by measuring how many assets simultaneously enter deep dip territory.

How It Works:

The script computes a “dip condition” for each of 40 altcoins. For every asset, it checks two key criteria:

Whether price is below its 10th percentile (bottom decile) over a user-defined lookback period.

Whether price is also below the median minus 3× standard deviation — a volatility-adjusted drop threshold.

If both conditions are met, the asset is counted as being in a deep dip. The total number of dipped assets is calculated and plotted as a histogram. This count — or dip breadth — provides a powerful contrarian signal when it spikes.

Threshold Alert:

A customizable threshold line lets you define when the dip count is considered significant. If the dip breadth exceeds this line, the background turns green, signaling potential market-wide undervaluation.

Key Features:

Analyzes 40 altcoins using volatility-adjusted dip detection.

Histogram of total dipped assets with real-time updates.

Adaptive color gradients to reflect the severity of dips.

Fully customizable lookback and threshold.

Works on any timeframe; designed for daily chart use by default.

Trading Application:

Spot broad capitulation events across altcoins.

Help time altcoin rotations and bottom-fishing opportunities.

Combine with BTC/ETH trend indicators for multi-layered confluence.

⚠️ This is not a buy/sell signal but a strategic market breadth tool for sentiment analysis.

Disclaimer: Past performance does not guarantee future results. This indicator is for educational and informational purposes only. Trading cryptocurrencies involves substantial risk of loss and is not suitable for every investor.

Custom Portfolio [BackQuant]Custom Portfolio {BackQuant]

Overview

This script turns TradingView into a lightweight portfolio optimizer with institutional-grade analytics and real-time position management capabilities.

Rank up to 15 tickers every bar using a pair-wise relative-strength "league table" that compares each asset against all others through your choice of 12 technical indicators.

Auto-allocate 100% of capital to the single strongest asset and optionally apply dynamic leverage when the aggregate market is trending, with full position tracking and rebalancing logic.

Track performance against a custom buy-and-hold benchmark while watching a fully fledged stats dashboard update in real time, including 15 professional risk metrics.

How it works

Relative-strength engine – Each asset is compared against every other asset with a user-selectable indicator (default: 9/21 EMA cross). The system generates a complete comparison matrix where Asset A vs Asset B, Asset A vs Asset C, and so on, creating strength scores. The summed scores crown a weekly/daily/hourly "winner" that receives the full allocation.

Regime filter – A second indicator applied to TOTAL crypto-market cap (or any symbol you choose) classifies the environment as trending or mean-reverting . Leverage activates only in trending regimes, protecting capital during choppy or declining markets. Choose from indicators like Universal Trend Model, Relative Strength Overlay, Momentum Velocity, or Custom RSI for regime detection.

Capital & position logic – Equity grows linearly when flat and multiplicatively while invested. The system tracks entry prices, calculates returns including leverage adjustments, and handles position transitions seamlessly. Optional intra-trade leverage rebalancing keeps exposure in sync with market conditions, recalculating position sizes as regime conditions change.

Risk & performance analytics – Every confirmed bar records return, drawdown, VaR/CVaR, Sharpe, Sortino, alpha/beta vs your benchmark, gain-to-pain, Calmar, win-rate, Omega ratio, portfolio variance, skewness, and annualized statistics. All metrics render in a professional table for instant inspection with proper annualization based on your selected trading days (252 for traditional markets, 365 for crypto).

Key inputs

Backtest window – Hard-code a start date or let the script run from series' inception with full date range validation.

Asset list (15 slots) – Works with spot, futures, indices, even synthetic spreads (e.g., BYBIT:BTCUSDT.P). The script automatically cleans ticker symbols for display.

Indicator universe – Switch the comparative metric to DEMA, BBPCT, LSMAz adaptive scores, Volatility WMA, DEMA ATR, Median Supertrend, and more proprietary indicators.

With more always being added!

Leverage settings – Max leverage from 1x to any multiple, auto-rebalancing toggle, trend/reversion thresholds with precision controls.

Visual toggles – Show/hide equity curve, rolling drawdown heat-map, daily PnL spikes, position label, advanced metrics table, buy-and-hold comparison equity.

Risk-free rate input – Customize the risk-free rate for accurate Sharpe ratio calculations, supporting both percentage and decimal inputs.

On-chart visuals

Color-coded equity curve with "shadow" offset for depth perception that changes from green (profitable) to red (losing) based on recent performance momentum.

Rolling drawdown strip that fades from light to deep red as losses widen, with customizable maximum drawdown scaling for visual clarity.

Optional daily-return histogram line and zero reference for understanding day-to-day volatility patterns.

Bottom-center table prints the current winning ticker in real time with clean formatting.

Top-right metrics grid updates every bar with 15 key performance indicators formatted to three decimal places for precision.

Benchmark overlay showing buy-and-hold performance of your selected index (default: SPX) for relative performance comparison.

Typical workflow

Add the indicator on a blank chart (overlay off).

Populate ticker slots with the assets you actually trade from your broker's symbol list.

Pick your momentum or mean-reversion metric and a regime filter that matches your market hypothesis.

Set max leverage (1 = spot only) and decide if you want dynamic rebalancing.

Press the little " L " on the price axis to view the equity curve in log scale for better long-term visualization.

Enable the metrics table to monitor Sharpe, Sortino, and drawdown in real time.

Iterate through different asset combinations and indicator settings; compare performance vs buy-and-hold; refine until you find robust parameters.

Who is it for?

Systematic crypto traders looking for a one-click, cross-sectional rotation model with professional risk management.

Portfolio quants who need rapid prototyping without leaving TradingView or exporting to Python/R.

Swing traders wanting an at-a-glance health check of their multi-coin basket with instant position signals.

Fund managers requiring detailed performance attribution and risk metrics for client reporting.

Researchers backtesting momentum and mean-reversion strategies across multiple assets simultaneously.

Important notes & tips

Set Trading Days in a Year to 252 for traditional markets; 365 for 24/7 crypto to ensure accurate annualization.

CAGR and Sharpe assume the backtest start date you choose—short windows can inflate stats, so test across multiple market cycles.

Leverage is theoretical; always confirm your broker's margin rules and account for funding costs not modeled here.

The script is computationally heavy at 15 assets due to the N×N comparison matrix—reduce the list or lengthen the timeframe if you hit execution limits.

Best results often come from mixing assets with different volatility profiles rather than highly correlated instruments.

The regime filter symbol can be changed from CRYPTOCAP:TOTAL to any broad market index that represents your asset universe.

PnL_EMA_TRACK12_PRO_3.3_full_adjusted# Multi-Ticker Support

Manage up to 12 tickers simultaneously.

- For each symbol, input share quantities, entry prices, and two optional additional entry points (E2, E3) with their own shares and offset percentages.

- Dynamic handling of inputs using arrays for easier maintenance and scalability.

# Average Cost and PnL Calculation

- Computes weighted average entry costs across all position parts (E1 and optionally E2 and E3).

- Calculates real-time Profit & Loss (PnL) both in USD and percentage relative to the current price.

- Color-coded values: green for profit, red for loss — for quick visual feedback.

# Moving Averages as Benchmarks

- Uses daily EMAs (10, 21, 65) and 15-minute SMA 200 as reference levels.

- Calculates percentage deviations of these moving averages from the average entry price.

- Calculates dollar differences based on the total shares held.

# Chart Visualization

- Draws a dashed yellow line for the average cost of each position.

- Optionally draws two additional lines and labels for E2 (blue) and E3 (purple) if activated.

- Lines extend to the right to emphasize current relevance.

- Labels can be positioned left or right, with customizable horizontal offset.

# Interactive Table in Chart

- Positions the info table in any chosen corner or center of the chart (top/right/left/middle, etc.).

- Displays symbol, PnL (dollar and percentage), and deviations to key EMAs and SMA.

- Colors PnL values according to profit or loss for instant clarity.

# User-Friendly Settings

- Flexible font size options for both the table and labels.

- Customizable colors for positive and negative values (default green/red).

- Choice of label position and X-axis offset to fit your chart style.

Daily Gain/Loss Statistics by Day of WeekDaily Gain/Loss Statistics by Day of Week

Overview

This Pine Script indicator analyzes historical price data to provide comprehensive day-of-week performance statistics, helping traders identify patterns and optimize their trading strategies based on which days historically perform better or worse.

Key Features

📊 Day-of-Week Analysis

7-day breakdown showing Monday through Sunday statistics

Average Gain % - Average percentage gains on winning days for each day of the week

Average Loss % - Average percentage losses on losing days (displayed with minus sign)

Median High % - Typical percentage move from open to daily high

Median Low % - Typical percentage move from open to daily low

🎯 Visual Performance Indicators

🚀 Rocket symbol - Marks the best performing day (highest average gains)

🔻 Red triangle down - Marks the worst performing day (lowest average gains)

Current day highlighting - Today's row highlighted in yellow (#ffdd444b)

⚡ Real-Time Session Tracking

Current Session row - Shows today's performance percentage in real-time

Color-coded gains/losses - Green for positive, red for negative

🎨 Professional Themes

⚙️ Customization Options

Date range selection - Choose specific time periods for analysis

Table positioning - 9 different screen positions

Table sizing - 6 size options from tiny to huge

Timeframe protection - Works only on 1D timeframe with user-friendly warnings

How It Works

Data Collection - Analyzes daily OHLC data within your selected date range

Day Classification - Categorizes each trading day by day of the week

Statistical Calculation - Computes averages and medians for each day type

Performance Ranking - Identifies best and worst performing days

Real-Time Display - Shows current session performance vs historical patterns

Trading Applications

Entry/Exit Timing - Identify optimal days for opening/closing positions

Risk Management - Avoid trading on historically poor-performing days

Strategy Optimization - Align trading strategies with day-of-week patterns

Market Timing - Understand weekly market cycles and seasonality

This indicator transforms raw price data into actionable intelligence, helping traders make more informed decisions based on proven historical day-of-week performance patterns.

UniversalPositionCalculatorV5🚀 Universal Position Calculator v5 (with Margin-Check) 🚀

Stop using calculators and complicated Excel sheets! 🤯 With the Universal Position Calculator v5, you have the ultimate tool right on your TradingView chart to manage your position size perfectly. Whether it's Forex, Gold, or Indices – this indicator does all the work for you!

✨ What does this indicator do? ✨

This indicator is your personal risk manager. It calculates the exact lot size for your next trade based on your capital, your desired risk, and your leverage. The best part? It immediately checks if your trade is even possible with your margin and warns you if you're about to over-leverage your account! 🚦

🌟 Key Features at a Glance 🌟

Automatic Lot Calculation: Just enter your risk in percent, and the indicator calculates the perfect lot size.

Margin Check: Instantly detects if your desired position size is limited by your margin and adjusts it. No more margin calls due to oversized positions!

For All Asset Classes: Works perfectly for Forex pairs (e.g., EURUSD) and other assets like commodities (XAUUSD) or indices (GER30). 💹

Currency Conversion: Automatically converts between your account currency and the asset's currency. It doesn't matter if you trade in EUR, USD, CHF, or JPY. 💱

Interactive Lines: Simply drag and drop the Entry and Stop Loss lines directly on the chart to plan your trade. 🎯

Clear Info Panel: All important information (lot size, required margin, risk in €/$/...) is displayed cleanly and clearly on your chart.

🛠️ How to Use: It's This Easy! 🛠️

The setup is a piece of cake and done in two simple steps.

Step 1: Configure Your Setup

Go to the indicator settings and fill out the "1. Setup" section:

Asset Type: Choose Forex for currency pairs or Other for everything else (e.g., Gold, Oil, Indices).

Account Currency: Enter the currency of your trading account (e.g., USD).

Account Capital: Enter your current account capital.

Risk in % per Trade: How much of your capital do you want to risk per trade? (e.g., 1.0 for 1%).

Leverage: Enter your account's leverage (e.g., 30 for 30:1).

Contract Size for 'Other': IMPORTANT! Only for the Other type. For Gold (XAUUSD), this is often 100; for the DAX (GER30), it's often 1 or 25. Check your broker's specifications for this!

Step 2: Plan Your Trade

Now for the fun part in the "2. Trade Control" section:

Entry Line (Blue Line): Click on the blue line and drag it to your desired entry level. You can also enter the value manually in the settings.

Stop Loss Line (Red Line): Click on the red line and drag it to your stop-loss level.

Step 3: Read the Results

As soon as you've set your Entry and Stop Loss, the Info Panel in the top-right corner will instantly show you the results:

Correct Lot Size: This is the lot size you need to enter with your broker for this trade.

⚠️ Heads up: If it says "Lot Size (Margin Limited!)" in orange, it means your desired risk was too high for your leverage. The indicator has automatically reduced the lot size to the maximum possible to avoid a margin call.

Required Margin: This is how much capital will be blocked on your account as a security deposit (margin) for this trade.

Risk in : The exact amount of money you will lose if your stop loss is triggered.

With this tool, you can make disciplined and mathematically sound trading decisions. Good luck and Happy Trading! 📈💰

ATR Stop Loss Non-Decreasing & LineThe script calculates a custom stop-loss level based on the Average True Range (ATR) indicator, ensuring that this stop-loss level never decreases from one bar to the next unless a reset condition is met. It also visually displays the ATR value and the calculated stop-loss level as a line on the chart.

Risk Guardian Pro📊 Risk Guardian Pro - Complete Script Summary

🎯 Overview

Risk Guardian Pro is a comprehensive Pine Script indicator for advanced trading risk management. It provides real-time position sizing, risk calculation, fee tracking, and profit/loss analysis with intelligent profit stop detection.

⚙️ Settings Sections

1. Account Settings

2. Risk Management

3. Stop Loss Settings

4. Trading Fees Settings

5. Display Settings

6. Table Row Toggles

7. Position Settings

🧮 Core Calculations

Risk Analysis

Position Risk

Risk Percentage

Risk:Reward Ratio

Fee Calculations

Trading Fee: Position Size × Leverage × Trading Fee %

Funding Rate: Full Margin × Funding Rate % × 8-Hour Periods

Total Fees: Trading Fee + Accumulated Funding Fees

P&L Calculations

Gross P&L: Position Size × Leverage × Price Movement / Entry Price

Net P&L: Gross P&L - Total Fees

Adjusted Risk/Reward: All targets include fee impact

🎨 Visual Display System

Risk Management Table

Header: "RISK GUARDIAN PRO" with version info

Status Bar: Position direction + Risk heat level with color coding

Main Metrics (11 configurable rows):

Account Balance: Total trading capital

Position Size: Trade allocation with size warnings

Risk %: Percentage at risk with progress bars

Risk:Reward: Current ratio with quality indicators

Stop Loss: Exit price with profit stop intelligence

Take Profit: Target price for profits

Trading Fee: One-time entry cost

Funding Rate: 8-hour accumulation with auto-timer

Total Fees: Complete cost breakdown

Potential Loss: Maximum risk including fees

Potential Win: Profit target minus fees

Chart Elements

Entry Line: Blue horizontal line at entry price

Stop Loss Line: Red line (turns green for profit stops)

Take Profit Line: Green horizontal line

Live P&L Plot: Real-time profit/loss line

Price Labels

Entry Label: "ENTRY" - Blue box

Stop Label: "STOP or "PROFIT STOP"

"PROFITSTOP" - Red/Green

Target Label: "TARGET" - Green box

Live P&L Label: "NET P&L" - Dynamic colour

🧠 Intelligent Features

Profit Stop Detection

Automatically detects when stop loss moves into profit territory:

Long Position: Stop above entry price

Short Position: Stop below entry price

Smart Transformations:

Status → "PROFIT SECURED" 🔒

Stop Loss → "Profit Stop" (green)

Risk % → "Secured Profit %"

Risk:Reward → "Secured:Additional"

Chart elements turn green

Risk Heat Levels

LOW: <2% risk (Green indicators)

MODERATE: 2-3% risk (Yellow indicators)

HIGH: >3% risk (Red indicators)

PROFIT SECURED: Stop in profit (Dark green)

Dynamic Color Coding

Table borders change based on risk level

Position size warnings for oversized trades

Progress bars show risk proximity to limits

All elements adapt to profit stop status

⏰ Time & Fee Management

Automatic Fee Accumulation

Set trade entry time using calendar picker

Funding fees automatically increase every 8 hours

Real-time progression as chart time advances

Visual feedback shows elapsed time and periods

Fee Impact Integration

All P&L calculations include fee deductions

Risk calculations add fee costs to potential loss

Take profit targets account for fee impact

Breakeven point automatically adjusts for fees

🚨 Alert System

Risk Alerts

High Risk: When risk exceeds 3% of capital

High Fees: When fees exceed 10% of position risk

Long Hold: Position held over 10 days

Extended Trade: Trade duration review reminder

Profit Alerts

Profit Secured: Stop loss moved to profit territory

🎛️ Customization Options

Visual Customization

2 Currency options with proper symbols

9 Table positions around chart

4 Size options for table and labels

200-bar range for label positioning

Progress bar toggles for risk visualization

Data Display Control

11 Individual row toggles for table content

Percentage displays in chart labels

Emoji options for visual enhancement

Tooltip information on hover

💡 Key Benefits

Professional Risk Management

✅ Comprehensive fee tracking with real-time accumulation

✅ Intelligent profit stop detection with visual adaptation

✅ Multi-method stop loss (ATR, percentage, manual)

✅ Advanced R:R calculations with fee impact

User Experience

✅ Date/time picker for precise entry timing

✅ Real-time updates as market moves

✅ Visual risk indicators with progress bars

✅ Extensive customization for personal preferences

Trading Integration

✅ Works with any timeframe and instrument

✅ Suitable for long-term use on charts

✅ Accurate fee modeling for realistic P&L

✅ Professional alert system for risk management

🎯 Perfect For

Active traders needing precise risk management

Position traders with long-term holds

Leveraged trading with fee-conscious strategies

Professional risk assessment and portfolio management

Risk Guardian Pro V2.5 represents a complete, professional-grade risk management solution that adapts intelligently to your trading style while providing comprehensive oversight of costs, risks, and profit potential.

Ticker Industry and Competitor LookupThe Ticker Industry and Competitor Lookup is a comprehensive indicator that provides instant access to industry classification data and competitive intelligence for any ticker symbol. Built using the advanced SIC_TICKER_DATA library, this tool delivers professional-grade sector analysis with enterprise-level performance. It's a simple yet great tool for competitor research, sector studies, portfolio diversification, and investment decision-making.

This indicator is a simple tool built on based on our SIC_TICKER_DATA library to demonstrate the use cases of the library. In this case, you enter a ticker and it displays the sector, SIC or Standard Industrial Classification which is a SEC identifier, and more importantly, the competitors that are listed to be in the exact same SIC by SEC.

There isn't much to say about the indicator itself but we strongly recommend checking out the SIC_TICKER_DATA library we just published to learn more about the types of indicators you can build using it.

Checklist Dashboard Table# Checklist Dashboard Table – ICT/SMC Trading Helper

Overview

The “Checklist Dashboard Table” is a TradingView indicator designed to help traders structure, organize, and validate their market analyses following the ICT/SMC (Inner Circle Trader / Smart Money Concepts) methodology. It provides a visual and interactive checklist directly on your chart, ensuring you never miss a crucial step in your decision-making process.

Key Features

- Visual Checklist : All your trading criteria are displayed as color-coded checkboxes (green for validated, red for not validated), making your analysis process both clear and efficient.

- Clear Separation Between Analysis and Confirmations :

- Analysis : Reminders for your routine, such as timeframe selection (M3 to H4), trend analysis via RSI, and identification of key zones (Midnight Open, SSL/BSL, Asian High/Low).

- Confirmations : Six customizable criteria to check off as you validate your setup (clear trend, OB + FVG, OTE zone, Premium/Discount, R/R > 1:2, CBDR/Midnight).

- Personal Notes Section : Keep your trade entries, observations, or comments in a dedicated field in the indicator’s settings. Your notes are displayed right in the checklist for quick reference and journaling.

- Elegant and Compact Display : The table is styled for readability and can be positioned anywhere on your chart.

- Quick Customization : Instantly update any criterion or your personal notes via the script settings.

How to Use

1. Add the indicator to your chart.

2. Review the “Analysis” section as your pre-trade routine reminder.

3. Check off the “Confirmations” criteria as you validate your entry strategy.

4. Write your trade notes or comments in the provided notes section.

5. Use the checklist to reinforce discipline and repeatability in your trading.

Why Use This Checklist?

- Prevents you from skipping important steps in your analysis.

- Reinforces trading discipline and consistency.

- Allows you to document and review your trade decisions for ongoing improvement.

Who Is It For?

Perfect for ICT/SMC traders, but also valuable for anyone looking to organize and systematize their trading process.

Happy trading!

Dynamic SL/TP Levels (ATR or Fixed %)This indicator, "Dynamic SL/TP Levels (ATR or Fixed %)", is designed to help traders visualize potential stop loss (SL) and take profit (TP) levels for both long and short positions, refreshing dynamically on each new bar. It assumes entry at the current bar's close price and uses a fixed 1:2 risk-reward ratio (TP is twice the distance of SL in the profit direction). Levels are displayed in a compact table in the chart pane for easy reference, without cluttering the main chart with lines.

Key Features:

Calculation Modes:

ATR-Based (Dynamic): SL distance is derived from the Average True Range (ATR) multiplied by a user-defined factor (default 1.5x). This adapts to the asset's volatility, providing breathing room based on recent price movements.

Fixed Percentage: SL is set as a direct percentage of the current close price (default 0.5%), offering consistent gaps regardless of volatility.

Long and Short Support: Calculates and shows SL/TP for longs (SL below close, TP above) and shorts (SL above close, TP below), with toggles to hide/show each.

Real-Time Updates: Levels recalculate every bar, making them readily available for entry decisions in your trading system.

Display: Outputs to a table in the top-right pane, showing precise values formatted to the asset's tick size (e.g., full decimal places for crypto).

How to Use:

Add the indicator to your chart via TradingView's Pine Editor or library.

Adjust settings:

Toggle "Use ATR?" on/off to switch modes.

Set "ATR Length" (default 14) and "ATR Multiplier for SL" for dynamic mode.

Set "Fixed SL %" for percentage mode.

Enable/disable "Show Long Levels" or "Show Short Levels" as needed.

Interpret the table: Use the displayed SL/TP values when your strategy signals an entry. For risk management, combine with position sizing (e.g., risk 1% of account per trade based on SL distance).

Example: On a volatile asset like BTC, ATR mode might set a wider SL for realism; on stable pairs, fixed % ensures predictability.

This tool promotes disciplined trading by tying levels to price action or fixed rules, but it's not financial advice—always backtest and use with your full strategy. Feedback welcome!

TrendZonesTrendZones

This is an indicator which I use, have tested, tweaked and added features to for use in my trend following investing system. I got the idea for it when for some reason I was looking for a dynamic reference to measure the height of a channel or something. In search of this I made MA’s of the high and low borders of a Donchian channel which turned out to be two near parallel and stunningly smooth curves. This visual was so appealing that I immediately tried to turn it into a replacement for the KeltCOG which I previously used in my system. First I created a curve in the middle of the upper and lower curves, which I called COG (Center Of Gravity). Then I decided to enter only one lookback and let the script create a Donchian channel with half the lookback and use this to create the curves with an MA of whole lookback. For this reason the minimum lookback is set to 14, enough room for the Donchian Channel of 7 periods. This Donchian ChanneI has a special way of calculating the borders, involving a 5 period Median value. Thanks to this these borders are really a resistance and support level, which won’t change at a whim, e.g. when a ‘dead cat bounce’ occurs. I prevented the Donchian channel to show itself between the curves and only pop out from behind these. These pop outs now function as “strong trend zones”. I gave it colors (blue:-strong up, green: moderate up, orange: moderate down, red: strong down, near COG: gray, curves horizontal: gray) and it looked very appealing. I tested it in different time frames. In some weekend, when I was bored, I observed for a few hours the minute chart of bitcoin. It turned out that you can reliably tell that an uptrend ends when the candles go under the COG beginning a downtrend. Uptrend starts again once the candles go above COG. As Trends on minute charts only last around half an hour, this entertainment made the potential of this indicator very clear to me in just one afternoon.

Risk Management, Safe Level and Logical Stops.

In the inputs are settings for “Risk Tolerance”, and to activate “Show Logical Stop Level” (activated in example chart) and “Show Safe Level”. As a rule of thump a trade should not expose the invested capital to a risk of losing more than 2 percent. I divided my investment capital in ten equal parts which are allocated to ten different stocks or other instruments or kept liquid. This means that when a position is closed by triggering a Stop with a loss of 20 percent, the invested capital suffers only 2 percent (20% x 10% = 2%). This is why the value for “Risk Tolerance” has a default of 20. Because I put my Stops on the lower curve, a “Safe Level” can be calculated such that when you buy for a price below or at this level, the stop will protect the position sufficiently. Because I only buy when the instrument is in uptrend, the buying price should be between COG and Safe Level. Although I never do that, putting the stop at other curves is feasible and when you want to widen the stop (I never lower my stops btw) in a downtrend situation, even 1 ATR below the “Low Border”. I call these “Logical Stop Levels”, marked with dark green circles on the lower curve when safe buying by placing the Stoploss on this curve is possible, gray circles on the other curves, on the Upper Curve navy when price enters very profitable level. In a downtrend situation maroon circles appear.

Target lines

When I open a position I always set a Stoploss and a Target, for this purpose two types of Target values can be set and corresponding Target lines activated. These lines are drawn above the “High Border” at the set distance. If one expects some price to be used, differences will occur.

Other Features

Support Zone, this is 1 ATR below the “Low Border”, the maroon circles of the “Logal Stops” are placed on this “Support level”.

Stop distance and Channel Width. (activated in example chart) These are reported in a two cell table in the right lower corner of the main panel. I created this because I want to be able to check the volatility, whether the channel shows a situation in which safe buying in most levels of the channel is possible or what risk you take when you buy now and set the Stop at the nearest logical level (which is not always the “Lower curve”). This feature comes in handy for creating a setup I propose in the “Day Trading Fantasy” below.

Some General and User Settings. I never activate this, perhaps you will.

Use Of TrendZones In My System.

Create a list of stocks in uptrend. I define ‘stock in uptrend’ as in uptrend zone in all three monthly, weekly and daily charts, all three should at the same time be in uptrend. The advantage of TrendZones is that you can immediately see in which zone the candle moves.

Opening a position in a stock from the above list. I do this only when in both the daily and weekly the green dot on the lower curve indicates a buying opportunity. This is usually not the case in most of the items of the list, this feature thus provides a good timing for opening a position. Sometimes you need to wait a few weeks for this to happen.

Setting a target over a position. For this I use the Target percent line of the weekly chart with the default value of 10.

Updating the Stoploss and Target values. Every week or two weeks I set these to the new values of the “Lower Curve” and the Target line of the weekly. Attention: never shift down Stops, only up or let them stay the same when the curve moves down. I never use Stop levels on other curves.

I Check the charts whenever I like to do this. Close the position when the uptrend obviously shifts down. Otherwise I let the profits run until the Target triggers which closes the position with some profit.

For selecting stocks an checking charts for volume events, I also use a subpanel indicator called “TZanalyser”, which borrows the visual of my “Fibonacci Zone Oscillator”, is based on TrendZones and includes code from my REVE indicators. I intend to publish that as well.

Day Trading Fantasy.

Day trading is an attempt to earn a dime by opening a position in the morning and close it during the day again with a profit (or a loss). Before the market closes, you close all day trading positions.

In my fantasy the “Logical Stop Level” is repurposed for use as entry point and the ATR-based Target line is used to provide a target setting in an intraday chart, like e.g. 15 minute. To do this the “Safe Level” should be limited to between Channel width and COG. This can be done by showing “Safe Level” and “Channel Width” and then set “Risk Tolerance” to around the shown Channel Width. In this setting you can then wait for the green circle to show up for entering your trade and protect it with the stop.

I don’t know if this works fine or if it’s better than other day trade systems, because I don’t do day trading.

Take care and have fun.

Risk Distribution HistogramStatistical risk visualization and analysis tool for any ticker 📊

The Risk Distribution Histogram visualizes the statistical distribution of different risk metrics for any financial instrument. It converts risk data into histograms with quartile-based color coding, so that traders can understand their risk, tail-risks, exposure patterns and make data-driven decisions based on empirical evidence rather than assumptions.

The indicator supports multiple risk calculation methods, each designed for different aspects of market analysis, from general volatility assessment to tail risk analysis.

Risk Measurement Methods

Standard Deviation

Captures raw daily price volatility by measuring the dispersion of price movements. Ideal for understanding overall market conditions and timing volatility-based strategies.

Use case: Options trading and volatility analysis.

Average True Range (ATR)

Measures true range as a percentage of price, accounting for gaps and limit moves. Valuable for position sizing across different price levels.

Use case: Position sizing and stop-loss placement.

The chart above illustrates how ATR statistical distribution can be used by looking at the ATR % of price distribution. For example, 90% of the movements are below 5%.

Downside Deviation

Only considers negative price movements, making it ideal for checking downside risk and capital protection rather than capturing upside volatility.

Use case: Downside protection strategies and stop losses.

Drawdown Analysis

Tracks peak-to-trough declines, providing insight into maximum loss potential during different market conditions.

Use case: Risk management and capital preservation.

The chart above illustrates tale risk for the asset (TQQQ), showing that it is possible to have drawdowns higher than 20%.

Entropy-Based Risk (EVaR)

Uses information theory to quantify market uncertainty. Higher entropy values indicate more unpredictable price action, valuable for detecting regime changes.

Use case: Advanced risk modeling and tail-risk.

VIX Histogram

Incorporates the market's fear index directly into analysis, showing how current volatility expectations compare to historical patterns. The CAPITALCOM:VIX histogram is independent from the ticker on the chart.

Use case: Volatility trading and market timing.

Visual Features

The histogram uses quartile-based color coding that immediately shows where current risk levels stand relative to historical patterns:

Green (Q1): Low Risk (0-25th percentile)

Yellow (Q2): Medium-Low Risk (25-50th percentile)

Orange (Q3): Medium-High Risk (50-75th percentile)

Red (Q4): High Risk (75-100th percentile)

The data table provides detailed statistics, including:

Count Distribution: Historical observations in each bin

PMF: Percentage probability for each risk level

CDF: Cumulative probability up to each level

Current Risk Marker: Shows your current position in the distribution

Trading Applications

When current risk falls into upper quartiles (Q3 or Q4), it signals conditions are riskier than 50-75% of historical observations. This guides position sizing and portfolio adjustments.

Key applications:

Position sizing based on empirical risk distributions

Monitoring risk regime changes over time

Comparing risk patterns across timeframes

Risk distribution analysis improves trade timing by identifying when market conditions favor specific strategies.

Enter positions during low-risk periods (Q1)

Reduce exposure in high-risk periods (Q4)

Use percentile rankings for dynamic stop-loss placement

Time volatility strategies using distribution patterns

Detect regime shifts through distribution changes

Compare current conditions to historical benchmarks

Identify outlier events in tail regions

Validate quantitative models with empirical data

Configuration Options

Data Collection

Lookback Period: Control amount of historical data analyzed

Date Range Filtering: Focus on specific market periods

Sample Size Validation: Automatic reliability warnings

Histogram Customization

Bin Count: 10-50 bins for different detail levels

Auto/Manual Bin Width: Optimize for your data range

Visual Preferences: Custom colors and font sizes

Implementation Guide

Start with Standard Deviation on daily charts for the most intuitive introduction to distribution-based risk analysis.

Method Selection: Begin with Standard Deviation

Setup: Use daily charts with 20-30 bins

Interpretation: Focus on quartile transitions as signals

Monitoring: Track distribution changes for regime detection

The tool provides comprehensive statistics including mean, standard deviation, quartiles, and current position metrics like Z-score and percentile ranking.

Enjoy, and please let me know your feedback! 😊🥂

Universal ATR Grid from Entry Price with AlertsUniversal ATR Grid from Entry Price with Alerts

This Pine Script v6 indicator creates a dynamic price grid based on a user-defined entry price and ATR for selected instruments (SOLUSDT, XRPUSDT, DOGEUSDT, PEPEUSDT, WIFUSDT).

Users can customize the entry price, ATR, number of levels (up to 5), and step multiplier per instrument.

The grid shows long (green) and short (red) levels around the entry price (gray), with labels offset right.

Lines extend from labels to the current bar, updating dynamically.

Alerts trigger on breakouts of long, short, and entry levels. Instrument names can be modified in the script.

Cobra Hedge Dashboard – V1.0 Final Master🧠 Cobra Hedge Dashboard – V1.0 Final Master

V1.0 | Smart Risk Filter for Open Hedge Positions

📝 (Description):

Cobra Hedge Dashboard is built specifically for traders managing open hedge positions. It provides a real-time view of directional pressure, smart zones, and price behavior to help make informed decisions such as:

When to partially close hedge orders

When to reverse positions based on flow & exhaustion

Which side (Buy or Sell) currently has momentum

Detecting price reaching critical zones (Supply/Demand)

Measuring volume strength to avoid fake exits

🔍 Ideal for traders already in the market — this dashboard is not an entry signal system, but a tool to manage hedge exits and exposure.

Built-in calculations include:

VWAP and EMA cross-pressure

Directional flow meter

Auto Supply & Demand Zones

Volume spikes and breakout strength

Best used on 1m–15m charts.

Open-source for transparency and improvement.

Hedging SimulatorHedging Simulator

The Hedging Simulator is a straightforward hedging tool designed to simulate potential profit and loss outcomes from combined Spot and Futures positions in the cryptocurrency market.

Users can define their equity allocation separately for both spot and futures, allowing for flexible and realistic scenario modelling.

The tool also incorporates MNV (Minimum Notional Value) and MTA (Minimum Trade Amount) parameters to estimate order sizes based on symbol-specific trading rules set by exchanges. While the results may differ slightly from actual exchange calculations, the simulator aims to provide a close approximation for general understanding.

📌Note: Crypto-Only - This tool is designed specifically for cryptocurrency trading and is not intended for use with traditional financial instruments.

Entry Price: Users can input custom entry prices for both spot and futures trades to simulate from specific market positions.

Live Price: The entry price fields for both spot and futures support Live Price based on the currently viewed symbol on your chart.

📌Note: In the real market, spot and futures prices are not always identical—there can be a price gap between them. While the difference is typically small, it's important to understand that the live price shown is only for rough estimation purposes and may not reflect the exact trading price on your chosen exchange.

Expecting Market Price: This represents the projected or target price to simulate potential profit and loss across the hedged position based on market movement.

📌Note: Profit and loss calculations exclude all trading fees. Actual results in live markets may vary due to fees, slippage, and exchange rules.

Feedback: If you notice any bugs, errors on calculation, or have suggestions for better calculations or new features, feel free to share your thoughts. Your feedback helps improve the tool and will be considered for future updates.

⚠️ Disclaimer: This simulator is intended for educational and illustrative purposes only. It does not constitute financial advice or guarantee trading results. Market conditions may vary, and all trading carries inherent risks. Users are solely responsible for any decisions made based on this tool and bear full responsibility for their own trading outcomes.

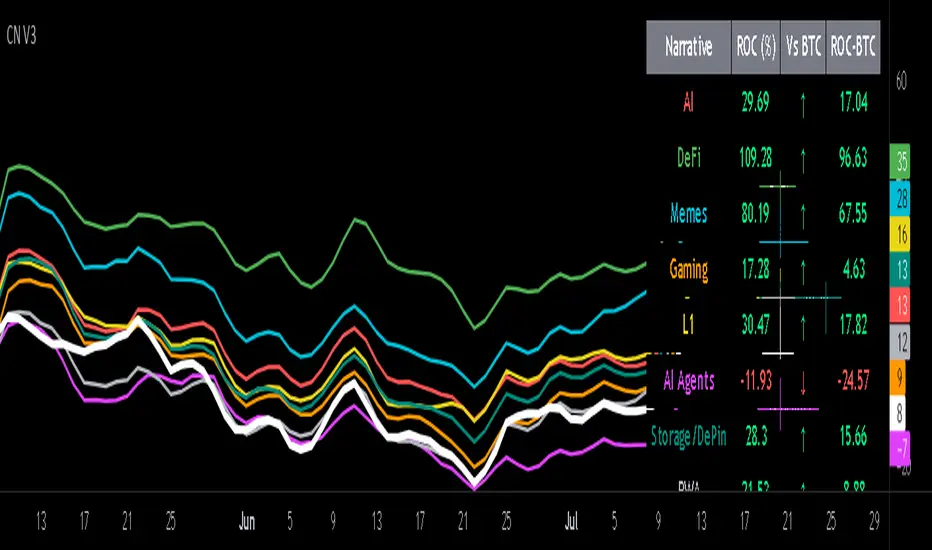

Crypto Narratives: Relative Strength V2Simple Indicator that displays the relative strength of 8 Key narratives against BTC as "Spaghetti" chart. The chart plots an aggregated RSI value for the 5 highest Market Cap cryopto's within each relevant narrative. The chart plots a 14 period SMA RSI for each narrative.

Functionality:

The indicator calculates the average RSI values for the current leading tokens associated with ten different crypto narratives:

- AI (Artificial Intelligence)

- DeFi (Decentralized Finance)

- Memes

- Gaming

- Level 1 (Layer 1 Protocols)

- AI Agents

- Storage/DePin

- RWA (Real-World Assets)

- BTC

Usage Notes:

The 5 crypto coins should be regularly checked and updated (in the script) by overtyping the current values from Rows 24 - 92 to ensure that you are using the up to date list of highest marketcap coins (or coins of your choosing).

The 14 period SMA can be changed in the indicator settings.

The indicator resets every 24 hours and is set to UTC+10. This can be changed by editing the script line 19 and changing the value of "resetHour = 1" to whatever value works for your timezone.

There is also a Rate of Change table that details the % rate of change of each narrative against BTC

Horizontal lines have been included to provide an indication of overbought and oversold levels.

The upper and lower horizontal line (overbought and oversold) can be adjusted through the settings.

The line width, and label offset can be customised through the input options.

Alerts can be set to triggered when a narrative's RSI crosses above the overbought level or below the oversold level. The alerts include the narrative name, RSI value, and the RSI level.

Capital Risk OptimizerCapital Risk Optimizer 🛡️

The Capital Risk Optimizer is an educational tool designed to help traders study capital efficiency, risk management, and scaling strategies when using leverage.

This script calculates and visualizes essential metrics for managing leveraged positions, including:

Entry Price – The current market price.

Stop Loss Level – Automatically derived using the 30-bar lowest low minus 1 ATR (default: 14-period ATR), an approach designed to create a dynamic, volatility-adjusted stop loss.

Stop Loss Distance (%) – The percentage distance between entry and stop.

Maximum Safe Leverage – The highest leverage allowable without risking liquidation before your stop is reached.

Margin Required – The amount of collateral necessary to support the desired position size at the calculated leverage.

Position Size – The configurable notional value of your trade.

These outputs are presented in a clean, customizable table overlay so you can quickly understand how position sizing, volatility, and leverage interact.

By default, the script uses a 14-period ATR combined with the lowest low of the past 30 bars, providing an optimal balance between sensitivity and noise for defining stop placement. This methodology helps traders account for market volatility in a systematic way.

The Capital Risk Optimizer is particularly useful as a portfolio management tool, supporting traders who want to study how to scale into positions using risk-adjusted sizing and capital efficiency principles. It pairs best with backtested strategies, and does not directly produce signals of any kind.

How to Use:

Set your desired position size.

Adjust the ATR and lookback settings to fine-tune stop loss placement.

Study the resulting leverage and margin requirements in real time.

Use this information to simulate and visualize potential trade scenarios and capital allocation models.

Disclaimer:

This script is provided for educational and informational purposes only. It does not constitute financial advice and should not be relied upon for live trading decisions. Always do your own research and consult with a qualified professional before making any trading or investment decisions.

Crypto Risk-Weighted Allocation SuiteCrypto Risk-Weighted Allocation Suite

This indicator is designed to help users explore dynamic portfolio allocation frameworks for the crypto market. It calculates risk-adjusted allocation weights across major crypto sectors and cash based on multi-factor momentum and volatility signals. Best viewed on INDEX:BTCUSD 1D chart. Other charts and timeframes may give mixed signals and incoherent allocations.

🎯 How It Works

This model systematically evaluates the relative strength of:

BTC Dominance (CRYPTOCAP:BTC.D)

Represents Bitcoin’s share of the total crypto market. Rising dominance typically indicates defensive market phases or BTC-led trends.

ETH/BTC Ratio (BINANCE:ETHBTC)

Gauges Ethereum’s relative performance versus Bitcoin. This provides insight into whether ETH is leading risk appetite.

SOL/BTC Ratio (BINANCE:SOLBTC)

Measures Solana’s performance relative to Bitcoin, capturing mid-cap layer-1 strength.

Total Market Cap excluding BTC and ETH (CRYPTOCAP:TOTAL3ES)

Represents Altcoins as a broad category, reflecting appetite for higher-risk assets.

Each of these series is:

✅ Converted to a momentum slope over a configurable lookback period.

✅ Standardized into Z-scores to normalize changes relative to recent behavior.

✅ Smoothed optionally using a Hull Moving Average for cleaner signals.

✅ Divided by ATR-based volatility to create a risk-weighted score.

✅ Scaled to proportionally allocate exposure, applying user-configured minimum and maximum constraints.

🪙 Dynamic Allocation Logic

All signals are normalized to sum to 100% if fully confident.

An overall confidence factor (based on total signal strength) scales the allocation up or down.

Any residual is allocated to cash (unallocated capital) for conservative exposure.

The script automatically avoids “all-in” bias and prevents negative allocations.

📊 Outputs

The indicator displays:

Market Phase Detection (which asset class is currently leading)

Risk Mode (Risk On, Neutral, Risk Off)

Dynamic Allocations for BTC, ETH, SOL, Alts, and Cash

Optional momentum plots for transparency

🧠 Why This Is Unique

Unlike simple dominance indicators or crossovers, this model:

Integrates multiple cross-asset signals (BTC, ETH, SOL, Alts)

Adjusts exposure proportionally to signal strength

Normalizes by volatility, dynamically scaling risk

Includes configurable constraints to reflect your own risk tolerance

Provides a cash fallback allocation when conviction is low

Is entirely non-repainting and based on daily closing data

⚠️ Disclaimer

This script is provided for educational and informational purposes only.

It is not financial advice and should not be relied upon to make investment decisions.

Past performance does not guarantee future results.

Always consult a qualified financial advisor before acting on any information derived from this tool.

🛠 Recommended Use

As a framework to visualize relative momentum and risk-adjusted allocations

For research and backtesting ideas on portfolio allocation across crypto sectors

To help build your own risk management process

This script is not a turnkey strategy and should be customized to fit your goals.

✅ Enjoy exploring dynamic crypto allocations responsibly!