Beyond Insights IndicatorThe Beyond Insights Indicator is a multi-timeframe overlay tool designed for TradingView that displays key Exponential Moving Averages (EMAs) and volatility insights to support various trading strategies. It intelligently adapts its display based on the current chart timeframe to reduce clutter and enhance relevance. Specifically, it shows EMA 6, 18, and 50 when viewing intraday timeframes.

In addition to EMAs, the indicator includes an ATR (Average True Range) calculation with a default length of 14, offering insight into market volatility.

Ortalama Gerçek Aralık (ATR)

Momentum (80) + ATR (14)his indicator combines two essential technical analysis tools in a single panel for enhanced market insight:

🔹 Momentum (80 periods): Measures the difference between the current price and the price 80 bars ago. Displayed as a semi-transparent filled area, it helps to visually identify shifts in price momentum over a longer timeframe.

🔸 ATR (Average True Range, 14 periods): Shown as a fine orange line, the ATR represents average market volatility over 14 periods, highlighting phases of calm or increased price fluctuations.

By viewing both momentum and volatility simultaneously, traders can better assess trend strength and market conditions, improving decision-making across assets such as stocks, forex, and cryptocurrencies.

✅ Suitable for all asset types

✅ Complements other indicators like RSI, MACD, and Bollinger Bands

✅ Categorized under Momentum & Volatility indicators

Candle Range DetectorCandle Range Detector

// Pine Script v6

// Detects candle-based ranges, mitigations, and sweeps with advanced logic

Overview

This indicator automatically detects price ranges based on candle containment, then tracks when those ranges are mitigated (broken) and when a sweep occurs. It is designed for traders who want to identify liquidity events and range breaks with precision.

How It Works

- Range Detection: A range is formed when a candle is fully contained within the previous candle (its high is lower and its low is higher). This marks a potential area of price balance or liquidity.

- Mitigation: A range is considered mitigated when price closes beyond its extension levels (configurable by normal or Fibonacci logic). This signals that the range has been invalidated or "taken out" by price action.

- Sweep Detection: After mitigation, the script watches for a sweep event: a candle that both trades through the range extreme and closes decisively beyond the log-mid of the candle itself. This is a strong sign of a liquidity grab or stop run.

- Alerts & Visuals: You can enable alerts and on-chart labels for sweeps. Only the most recent mitigated range can be swept, and each range can only be swept once.

- Timeframe Sensitivity: On weekly or monthly charts, a candle can both mitigate and sweep a range on the same bar. On lower timeframes, only one event can occur per bar.

Why It Works

- Candle containment is a robust way to identify natural price ranges and liquidity pools, as it reflects where price is consolidating or being absorbed.

- Mitigation marks the moment when a range is no longer defended, often leading to new directional moves.

- Sweeps are powerful signals of stop hunts or liquidity grabs, especially when confirmed by a close beyond the log-mid of the candle, indicating strong intent.

Visual Explanation

Tip: Use this tool to spot high-probability reversal or continuation zones, and to get alerted to key liquidity events in real time.

Filtered DTR Table📊 Filtered Daily True Range (DTR) Indicator

This indicator calculates and displays a filtered version of the Daily True Range (DTR) over the last 14 trading days, using high and low prices of each day.

It filters out extreme values by excluding any daily range that is:

Less than 0.5× the average range

Greater than 2× the average range

The indicator shows a table in the bottom-right corner of the main chart, containing:

Filtered ATR – The average of valid (filtered) daily ranges over the past 14 days, based on the high-low difference.

Current Day's Range – The high-low range of the current trading day.

% of ATR – How much of the filtered ATR has been covered by today's range, expressed as a whole number percentage.

Filt ADR🟠 Script Name: Filtered Average Daily Range (Filt ADR)

This script calculates a filtered version of the Average Daily Range (ADR) based on the last 14 daily candles. It's designed to reduce the influence of unusually high or low daily ranges (outliers) by applying a filter before calculating the average.

🔧 How It Works — Step by Step

1. Calculate Daily Ranges (High - Low)

It retrieves the daily price ranges (difference between daily high and low) for the last 14 days using request.security() with the "D" (daily) timeframe.

pinescript

Копировать

Редактировать

high - low // today's daily range

high - low // yesterday's daily range

...

These values are stored into individual variables dr0 to dr13.

2. Build an Array of Daily Ranges

An array named ranges is used to store the 14 daily ranges, but only if they are not na (missing data). This avoids errors during processing.

3. Calculate the Initial (Unfiltered) Average Range

The script sums all values in the ranges array and calculates their average:

pinescript

Копировать

Редактировать

avg_all = total sum of ranges / number of valid entries

4. Filter Out Outliers

Now it filters the values in ranges:

Only keeps the ranges that are between 0.5×avg_all and 2×avg_all.

This is to remove abnormally small or large daily ranges that could distort the average.

The filtered values are added to a second array called filtered.

5. Calculate the Filtered ADR

Finally, it calculates the average of the filtered daily ranges:

pinescript

Копировать

Редактировать

avg_filt = sum of filtered ranges / number of filtered values

This is the Filtered ADR.

6. Plot the Result

The result (avg_filt) is plotted as an orange line on the chart. It updates on each bar (depending on the current timeframe you're viewing) but the underlying data is based on the last 14 daily candles.

pinescript

Копировать

Редактировать

plot(avg_filt, title="Filtered ADR", color=color.orange, linewidth=2)

✅ Use Case

This script is useful for traders who use the Average Daily Range (ADR) to:

Estimate expected price movement during a day

Set volatility-based stop-loss or take-profit levels

Identify days with unusually high or low volatility

By filtering out extreme values, it provides a more stable and reliable estimate of daily volatility.

UT Bot + Hull MA Confirmed Signal DelayOverview

This indicator is designed to detect high-probability reversal entry signals by combining "UT Bot Alerts" (UT Bot Alerts script adapted from QuantNomad - Originally developed by Yo_adriiiiaan and idea of original code for "UT Bot Alerts" from HPotter ) with confirmation from a Hull Moving Average (HMA) Developed by Alan Hull . It focuses on capturing momentum shifts that often precede trend reversals, helping traders identify potential entry points while filtering out false signals.

🔍 How It Works

This strategy operates in two stages:

1. UT Bot Momentum Trigger

The foundation of this script is the "UT Bot Alerts" , which uses an ATR-based trailing stop to detect momentum changes. Specifically:

The script calculates a dynamic stop level based on the Average True Range (ATR) multiplied by a user-defined sensitivity factor (Key Value).

When price closes above this trailing stop and the short-term EMA crosses above the stop, a potential buy setup is triggered.

Conversely, when price closes below the trailing stop and the short-term EMA crosses below, a potential sell setup is triggered.

These UT Bot alerts are designed to identify the initial shift in market direction, acting as the first filter in the signal process.

2. Hull MA Confirmation

To reduce noise and false triggers from the UT Bot alone, this script delays the entry signal until price confirms the move by crossing the Hull Moving Average (or its variants: HMA, THMA, EHMA) in the same direction as the UT Bot trigger:

A Buy Signal is generated only when:

A UT Bot Buy condition is active, and

The price closes above the Hull MA.

Or, if a UT Bot Buy condition was recently triggered but price hadn’t yet crossed above the Hull MA, a delayed buy is signaled when price finally breaks above it.

A Sell Signal is generated only when:

A UT Bot Sell condition is active, and

The price closes below the Hull MA.

Similarly, a delayed sell signal can occur if price breaks below the Hull MA shortly after a UT Bot Sell trigger.

This dual-confirmation process helps traders avoid premature entries and improves the reliability of reversal signals.

📈 Best Use Cases

Reversal Trading: This strategy is particularly well-suited for catching early trend reversals rather than trend continuations. It excels at identifying momentum pivots that occur after pullbacks or exhaustion moves.

Heikin Ashi Charts Recommended: The script offers a Heikin Ashi mode for smoothing out noise and enhancing visual clarity. Using Heikin Ashi candles can further reduce whipsaws and highlight cleaner shifts in trend direction.

MACD Alignment: For best results, trade in the direction of the MACD trend or use it as a filter to avoid counter-trend trades.

⚠️ Important Notes

Entry Signals Only: This indicator only plots entry points (Buy and Sell signals). It does not define exit strategies, so users should manage trades manually using trailing stops, profit targets, or other exit indicators.

No Signal = No Confirmation: You may see a UT Bot trigger without a corresponding Buy/Sell signal. This means the price did not confirm the move by crossing the Hull MA, and therefore the setup was considered too weak or incomplete.

⚙️ Customization

UT Bot Sensitivity: Adjust the “Key Value” and “ATR Period” to make the UT Bot more or less reactive to price action.

Use Heikin Ashi: Toggle between standard candles or Heikin Ashi in the indicator settings for a smoother trading experience.

The HMA length may also be modified in the indicator settings from its standard 55 length to increase or decrease the sensitivity of signal.

This strategy is best used by traders looking for a structured, logic-based way to enter early into reversals with added confirmation to reduce risk. By combining two independent systems—momentum detection (UT Bot) and trend confirmation (Hull MA)—it aims to provide high-confidence entries without overwhelming complexity.

Let the indicator guide your entries—you manage the exits.

Examples of use:

Futures:

Stock:

Crypto:

As shown in the snapshots this strategy, like most, works the best when price action has a sizeable ATR and works the least when price is choppy. Therefore it is always best to use this system when price is coming off known support or resistance levels and when it is seen to respect short term EMA's like the 9 or 15.

My personal preference to use this system is for day trading on a 3 or 5 minute chart. But it is valid for all timeframes and simply marks a high probability for a new trend to form.

Sources:

Quant Nomad - www.tradingview.com

Yo_adriiiiaan - www.tradingview.com

HPotter - www.tradingview.com

Hull Moving Average - alanhull.com

ADR & ATR Extension from EMAThis indicator helps identify how extended the current price is from a chosen Exponential Moving Average (EMA) in terms of both Average Daily Range (ADR) and Average True Range (ATR).

It calculates:

ADR Extension = (Price - EMA) / ADR

ATR Extension = (Price - EMA) / ATR

The results are shown in a floating table on the chart.

The ADR line turns red if the price is more than 4 ADRs above the selected EMA

Customization Options:

- Select EMA length

- Choose between close or high as price input

- Set ADR and ATR periods

- Customize the label’s position, color, and transparency

- Use the chart's timeframe or a fixed timeframe

(MVD) Meta-Volatility Divergence (DAFE) Meta-Volatility Divergence (MVD)

Reveal the Hidden Tension in Volatility.

The Meta-Volatility Divergence (MVD) indicator is a next-generation tool designed to expose the disagreement between multiple volatility measures—helping you spot when the market’s “volatility engines” are out of sync, and a regime shift or volatility event may be brewing.

What Makes MVD Unique?

Multi-Source Volatility Analysis:

Unlike traditional volatility indicators that rely on a single measure, MVD fuses four distinct volatility signals:

ATR (Average True Range): Captures the average range of price movement.

Stdev (Standard Deviation): Measures the dispersion of closing prices.

Range: The average difference between high and low.

VoVix: A proprietary “volatility of volatility” metric, quantifying the difference between fast and slow ATR, normalized by ATR’s own volatility.

Divergence Engine:

The core MVD line (yellow) represents the mean absolute deviation (MAD) of these volatility measures from their average. When the line is flat, all volatility measures are in agreement. When the line rises, it means the market’s volatility signals are diverging—often a precursor to regime shifts, volatility expansions, or hidden stress.

Dynamic Z-Score Normalization:

The MVD line is normalized as a Z-score, so you can easily spot when current divergence is rare or extreme compared to recent history.

Visual Clarity:

Yellow center line: Tracks the real-time divergence of volatility measures.

Green dashed thresholds: Mark the ±2.00 Z-score levels, highlighting when divergence is unusually high and action may be warranted.

Dashboard: Toggleable panel shows all key metrics (ATR, Stdev, VoVix, MVD Z) and your custom branding.

Compact Info Label : For mobile or minimalist users, a single-line summary keeps you informed without clutter.

What Makes The MVD line move?

- The MVD line rises when the included volatility measures (ATR, Stdev, Range, VoVix) are moving in different directions or at different magnitudes. For example, if ATR is rising but Stdev is falling, the line will move up, signaling disagreement.

- The line falls or flattens when all volatility measures are in sync, indicating a consensus in the market’s volatility regime.

- VoVix adds a unique dimension, making the indicator especially sensitive to sudden changes in volatility structure that most tools miss.

Inputs & Settings

ATR Length: Sets the lookback for ATR calculation. Shorter = more sensitive, longer = smoother.

Stdev Length: Sets the lookback for standard deviation. Adjust for your asset’s volatility.

Range Length: Sets the lookback for the average high-low range.

MVD Lookback: Controls the window for Z-score normalization. Higher values = more historical context, lower = more responsive.

Show Dashboard: Toggle the full dashboard panel on/off.

Show Compact Info Label: Toggle the mobile-friendly info line on/off.

Tip:

Adjust these settings to match your asset’s volatility and your trading timeframe. There is no “one size fits all”—tuning is key to extracting the most value from MVD.

How to make MVD work for you:

Threshold Crosses: When the MVD line crosses above or below the green dashed thresholds (±2.00), it signals that volatility measures are diverging more than usual. This is a heads-up that a volatility event, regime shift, or hidden market stress may be developing.

Not a Buy/Sell Signal: A threshold cross is not a direct buy or sell signal. It is an indication that the market’s volatility structure is changing. Use it as a filter, confirmation, or alert in combination with your own strategy and risk management.

Dashboard & Info Line: Use the dashboard for a full view of all metrics, or the info label for a quick glance—especially useful on mobile.

Chart: MNQ! on 5min frames

ATR: 14

StDev L: 11

Range L: 13

MDV LB: 13

Important Note

MVD is a market structure and volatility regime tool.

It is designed to alert you to potential changes in market conditions, not to provide direct trade entries or exits. Always combine with your own analysis and risk management.

Meta-Volatility Divergence:

See the market’s hidden tension. Anticipate the next wave.

For educational purposes only. Not financial advice. Always use proper risk management.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Horizontal ATR LinesDisclaimer:

This script was generated using OpenAI’s ChatGPT. I take no responsibility for the correctness, performance, or financial impact of this indicator. Use it at your own risk and discretion.

This indicator draws horizontal ATR-based levels from the last closed candle on a user-selected timeframe. It is designed for traders who want to visualize realistic volatility zones for setting dynamic support/resistance, take-profit, or stop-loss levels.

What it does:

Calculates the Average True Range (ATR) using a customizable period and timeframe.

Plots four horizontal lines:

+1 ATR and –1 ATR from the last closed candle’s close

+X ATR and –X ATR, where X is a second custom multiplier

Each level includes a compact label showing:

The price of the level

The percentage distance from the close price

Use cases:

Identify realistic intraday or swing price movement boundaries

Build volatility-aware take-profit and stop-loss zones

Visually track market compression or expansion in context

Customization:

ATR period and timeframe

Two independent ATR multipliers

Custom color settings for each group of levels

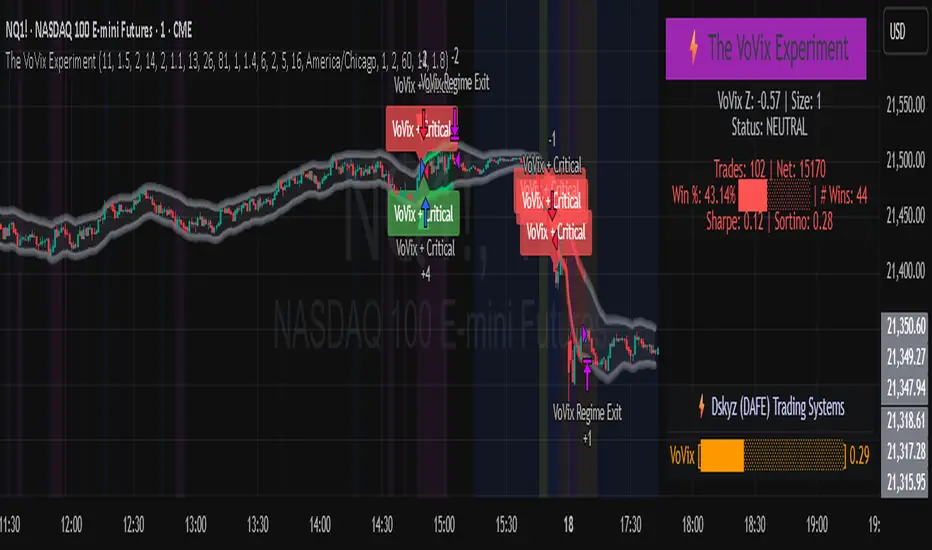

The VoVix Experiment The VoVix Experiment

The VoVix Experiment is a next-generation, regime-aware, volatility-adaptive trading strategy for futures, indices, and more. It combines a proprietary VoVix (volatility-of-volatility) anomaly detector with price structure clustering and critical point logic, only trading when multiple independent signals align. The system is designed for robustness, transparency, and real-world execution.

Logic:

VoVix Regime Engine: Detects pre-move volatility anomalies using a fast/slow ATR ratio, normalized by Z-score. Only trades when a true regime spike is detected, not just random volatility.

Cluster & Critical Point Filters: Price structure and volatility clustering must confirm the VoVix signal, reducing false positives and whipsaws.

Adaptive Sizing: Position size scales up for “super-spikes” and down for normal events, always within user-defined min/max.

Session Control: Trades only during user-defined hours and days, avoiding illiquid or high-risk periods.

Visuals: Aurora Flux Bands (From another Original of Mine (Options Flux Flow): glow and change color on signals, with a live dashboard, regime heatmap, and VoVix progression bar for instant insight.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 15 min (but works on all timeframes)

Order size: Adaptive, 1–2 contracts

Session: 5:00–15:00 America/Chicago (default, fully adjustable)

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for MNQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Forward Testing: (This is no guarantee. I've provided these results to show that executions perform as intended. Test were done on Tradovate)

ALL TRADES

Gross P/L: $12,907.50

# of Trades: 64

# of Contracts: 186

Avg. Trade Time: 1h 55min 52sec

Longest Trade Time: 55h 46min 53sec

% Profitable Trades: 59.38%

Expectancy: $201.68

Trade Fees & Comm.: $(330.95)

Total P/L: $12,576.55

Winning Trades: 59.38%

Breakeven Trades: 3.12%

Losing Trades: 37.50%

Link: www.dropbox.com

Inputs & Tooltips

VoVix Regime Execution: Enable/disable the core VoVix anomaly detector.

Volatility Clustering: Require price/volatility clusters to confirm VoVix signals.

Critical Point Detector: Require price to be at a statistically significant distance from the mean (regime break).

VoVix Fast ATR Length: Short ATR for fast volatility detection (lower = more sensitive).

VoVix Slow ATR Length: Long ATR for baseline regime (higher = more stable).

VoVix Z-Score Window: Lookback for Z-score normalization (higher = smoother, lower = more reactive).

VoVix Entry Z-Score: Minimum Z-score for a VoVix spike to trigger a trade.

VoVix Exit Z-Score: Z-score below which the regime is considered decayed (exit).

VoVix Local Max Window: Bars to check for local maximum in VoVix (higher = stricter).

VoVix Super-Spike Z-Score: Z-score for “super” regime events (scales up position size).

Min/Max Contracts: Adaptive position sizing range.

Session Start/End Hour: Only trade between these hours (exchange time).

Allow Weekend Trading: Enable/disable trading on weekends.

Session Timezone: Timezone for session filter (e.g., America/Chicago for CME).

Show Trade Labels: Show/hide entry/exit labels on chart.

Flux Glow Opacity: Opacity of Aurora Flux Bands (0–100).

Flux Band EMA Length: EMA period for band center.

Flux Band ATR Multiplier: Width of bands (higher = wider).

Compliance & Transparency

* No hidden logic, no repainting, no pyramiding.

* All signals, sizing, and exits are fully explained and visible.

* Backtest settings are stricter than most real accounts.

* All visuals are directly tied to the strategy logic.

* This is not a mashup or cosmetic overlay; every component is original and justified.

Disclaimer

Trading is risky. This script is for educational and research purposes only. Do not trade with money you cannot afford to lose. Past performance is not indicative of future results. Always test in simulation before live trading.

Proprietary Logic & Originality Statement

This script, “The VoVix Experiment,” is the result of original research and development. All core logic, algorithms, and visualizations—including the VoVix regime detection engine, adaptive execution, volatility/divergence bands, and dashboard—are proprietary and unique to this project.

1. VoVix Regime Logic

The concept of “volatility of volatility” (VoVix) is an original quant idea, not a standard indicator. The implementation here (fast/slow ATR ratio, Z-score normalization, local max logic, super-spike scaling) is custom and not found in public TradingView scripts.

2. Cluster & Critical Point Logic

Volatility clustering and “critical point” detection (using price distance from a rolling mean and standard deviation) are general quant concepts, but the way they are combined and filtered here is unique to this script. The specific logic for “clustered chop” and “critical point” is not a copy of any public indicator.

3. Adaptive Sizing

The adaptive sizing logic (scaling contracts based on regime strength) is custom and not a standard TradingView feature or public script.

4. Time Block/Session Control

The session filter is a common feature in many strategies, but the implementation here (with timezone and weekend control) is written from scratch.

5. Aurora Flux Bands (From another Original of Mine (Options Flux Flow)

The “glowing” bands are inspired by the idea of volatility bands (like Bollinger Bands or Keltner Channels), but the visual effect, color logic, and integration with regime signals are original to this script.

6. Dashboard, Watermark, and Metrics

The dashboard, real-time Sharpe/Sortino, and VoVix progression bar are all custom code, not copied from any public script.

What is “standard” or “common quant practice”?

Using ATR, EMA, and Z-score are standard quant tools, but the way they are combined, filtered, and visualized here is unique. The structure and logic of this script are original and not a mashup of public code.

This script is 100% original work. All logic, visuals, and execution are custom-coded for this project. No code or logic is directly copied from any public or private script.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Dskyz (DAFE) GENESIS Dskyz (DAFE) GENESIS: Adaptive Quant, Real Regime Power

Let’s be honest: Most published strategies on TradingView look nearly identical—copy-paste “open-source quant,” generic “adaptive” buzzwords, the same shallow explanations. I’ve even fallen into this trap with my own previously posted strategies. Not this time.

What Makes This Unique

GENESIS is not a black-box mashup or a pre-built template. It’s the culmination of DAFE’s own adaptive, multi-factor, regime-aware quant engine—built to outperform, survive, and visualize live edge in anything from NQ/MNQ to stocks and crypto.

True multi-factor core: Volume/price imbalances, trend shifts, volatility compression/expansion, and RSI all interlock for signal creation.

Adaptive regime logic: Trades only in healthy, actionable conditions—no “one-size-fits-all” signals.

Momentum normalization: Uses rolling, percentile-based fast/slow EMA differentials, ALWAYS normalized, ALWAYS relevant—no “is it working?” ambiguity.

Position sizing that adapts: Not fixed-lot, not naive—not a loophole for revenge trading.

No hidden DCA or pyramiding—what you see is what you trade.

Dashboard and visual system: Directly connected to internal logic. If it’s shown, it’s used—and nothing cosmetic is presented on your chart that isn’t quantifiable.

📊 Inputs and What They Mean (Read Carefully)

Maximum Raw Score: How many distinct factors can contribute to regime/trade confidence (default 4). If you extend the quant logic, increase this.

RSI Length / Min RSI for Shorts / Max RSI for Longs: Fine-tunes how “overbought/oversold” matters; increase the length for smoother swings, tighten floors/ceilings for more extreme signals.

⚡ Regime & Momentum Gates

Min Normed Momentum/Score (Conf): Raise to demand only the strongest trends—your filter to avoid algorithmic chop.

🕒 Volatility & Session

ATR Lookback, ATR Low/High Percentile: These control your system’s awareness of when the market is dead or ultra-volatile. All sizing and filter logic adapts in real time.

Trading Session (hours): Easy filter for when entries are allowed; default is regular trading hours—no surprise overnight fills.

📊 Sizing & Risk

Max Dollar Risk / Base-Max Contracts: All sizing is adaptive, based on live regime and volatility state—never static or “just 1 contract.” Control your max exposures and real $ risk. ATR will effect losses in high volatility times.

🔄 Exits & Scaling

Stop/Trail/Scale multipliers: You choose how dynamic/flexible risk controls and profit-taking need to be. ATR-based, so everything auto-adjusts to the current market mode.

Visuals That Actually Matter

Dashboard (Top Right): Shows only live, relevant stats: scoring, status, position size, win %, win streak, total wins—all from actual trade engine state (not “simulated”).

Watermark (Bottom Right): Momentum bar visual is always-on, regime-aware, reflecting live regime confidence and momentum normalization. If the bar is empty, you’re truly in no-momentum. If it glows lime, you’re riding the strongest possible edge.

*No cosmetics, no hidden code distractions.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 1 min (but works on all timeframes)

Order size: Adaptive, 1–3 contracts

No pyramiding, no hidden DCA

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for NQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Why It Wins

While others put out “AI-powered” strategies with little logic or soul, GENESIS is ruthlessly practical. It is built around what keeps traders alive:

- Context-aware signals, not just patterns

- Tight, transparent risk

- Inputs that adapt, not confuse

- Visuals that clarify, not distract

- Code that runs clean, efficient, and with minimal overfitting risk (try it on QQQ, AMD, SOL, etc. out of the box)

Disclaimer (for TradingView compliance):

Trading is risky. Futures, stocks, and crypto can result in significant losses. Do not trade with funds you cannot afford to lose. This is for educational and informational purposes only. Use in simulation/backtest mode before live trading. No past performance is indicative of future results. Always understand your risk and ownership of your trades.

This will not be my last—my goal is to keep raising the bar until DAFE is a brand or I’m forced to take this private.

Use with discipline, use with clarity, and always trade smarter.

— Dskyz , powered by DAFE Trading Systems.

REVELATIONS (VoVix - PoC) REVELATIONS (VoVix - POC): True Regime Detection Before the Move

Let’s not sugarcoat it: Most strategies on TradingView are recycled—RSI, MACD, OBV, CCI, Stochastics. They all lag. No matter how many overlays you stack, every one of these “standard” indicators fires after the move is underway. The retail crowd almost always gets in late. That’s never been enough for my team, for DAFE, or for anyone who’s traded enough to know the real edge vanishes by the time the masses react.

How is this different?

REVELATIONS (VoVix - POC) was engineered from raw principle, structured to detect pre-move regime change—before standard technicals even light up. We built, tested, and refined VoVix to answer one hard question:

What if you could see the spike before the trend?

Here’s what sets this system apart, line-by-line:

o True volatility-of-volatility mathematics: It’s not just "ATR of ATR" or noise smoothing. VoVix uses normalized, multi-timeframe v-vol spikes, instantly detecting orderbook stress and "outlier" market events—before the chart shows them as trends.

o Purist regime clustering: Every trade is enabled only during coordinated, multi-filter regime stress. No more signals in meaningless chop.

o Nonlinear entry logic: No trade is ever sent just for a “good enough” condition. Every entry fires only if every requirement is aligned—local extremes, super-spike threshold, regime index, higher timeframe, all must trigger in sync.

o Adaptive position size: Your contracts scale up with event strength. Tiny size during nominal moves, max leverage during true regime breaks—never guesswork, never static exposure.

o All exits governed by regime decay logic: Trades are closed not just on price targets but at the precise moment the market regime exhausts—the hardest part of systemic trading, now solved.

How this destroys the lag:

Standard indicators (RSI, MACD, OBV, CCI, and even most “momentum” overlays) simply tell you what already happened. VoVix triggers as price structure transitions—anyone running these generic scripts will trade behind the move while VoVix gets in as stress emerges. Real alpha comes from anticipation, not confirmation.

The visuals only show what matters:

Top right, you get a live, live quant dashboard—regime index, current position size, real-time performance (Sharpe, Sortino, win rate, and wins). Bottom right: a VoVix "engine bar" that adapts live with regime stress. Everything you see is a direct function of logic driving this edge—no cosmetics, no fake momentum.

Inputs/Signals—explained carefully for clarity:

o ATR Fast Length & ATR Slow Length:

These are the heart of VoVix’s regime sensing. Fast ATR reacts to sharp volatility; Slow ATR is stability baseline. Lower Fast = reacts to every twitch; higher Slow = requires more persistent, “real” regime shifts.

Tip: If you want more signals or faster markets, lower ATR Fast. To eliminate noise, raise ATR Slow.

o ATR StdDev Window: Smoothing for volatility-of-volatility normalization. Lower = more jumpy, higher = only the cleanest spikes trigger.

Tip: Shorten for “jumpy” assets, raise for indices/futures.

o Base Spike Threshold: Think of this as your “minimum event strength.” If the current move isn’t volatile enough (normalized), no signal.

Tip: Higher = only biggest moves matter. Lower for more signals but more potential noise.

o Super Spike Multiplier: The “are you sure?” test—entry only when the current spike is this multiple above local average.

Tip: Raise for ultra-selective/swing-trading; lower for more active style.

Regime & MultiTF:

o Regime Window (Bars):

How many bars to scan for regime cluster “events.” Short for turbo markets, long for big swings/trends only.

o Regime Event Count: Only trade when this many spikes occur within the Regime Window—filters for real stress, not isolated ticks.

Tip: Raise to only ever trade during true breakouts/crashes.

o Local Window for Extremes:

How many bars to check that a spike is a local max.

Tip: Raise to demand only true, “clearest” local regime events; lower for early triggers.

o HTF Confirm:

Higher timeframe regime confirmation (like 45m on an intraday chart). Ensures any event you act on is visible in the broader context.

Tip: Use higher timeframes for only major moves; lower for scalping or fast regimes.

Adaptive Sizing:

o Max Contracts (Adaptive): The largest size your system will ever scale to, even on extreme event.

Tip: Lower for small accounts/conservative risk; raise on big accounts or when you're willing to go big only on outlier events.

o Min Contracts (Adaptive): The “toe-in-the-water.” Smallest possible trade.

Tip: Set as low as your broker/exchange allows for safety, or higher if you want to always have meaningful skin in the game.

Trade Management:

o Stop %: Tightness of your stop-loss relative to entry. Lower for tighter/safer, higher for more breathing room at cost of greater drawdown.

o Take Profit %: How much you'll hold out for on a win. Lower = more scalps. Higher = only run with the best.

o Decay Exit Sensitivity Buffer: Regime index must dip this far below the trading threshold before you exit for “regime decay.”

Tip: 0 = exit as soon as stress fails, higher = exits only on stronger confirmation regime is over.

o Bars Decay Must Persist to Exit: How long must decay be present before system closes—set higher to avoid quick fades and whipsaws.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 1 min (but works on all timeframes)

Order size: Adaptive, 1–3 contracts

No pyramiding, no hidden DCA

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for NQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Tip: Set to 1 for instant regime exit; raise for extra confirmation (less whipsaw risk, exits held longer).

________________________________________

Bottom line: Tune the sensitivity, selectivity, and risk of REVELATIONS by these inputs. Raise thresholds and windows for only the best, most powerful signals (institutional style); lower for activity (scalpers, fast cryptos, signals in constant motion). Sizing is always adaptive—never static or martingale. Exits are always based on both price and regime health. Every input is there for your control, not to sell “complexity.” Use with discipline, and make it your own.

This strategy is not just a technical achievement: It’s a statement about trading smarter, not just more.

* I went back through the code to make sure no the strategy would not suffer from repainting, forward looking, or any frowned upon loopholes.

Disclaimer:

Trading is risky and carries the risk of substantial loss. Do not use funds you aren’t prepared to lose. This is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

Expect more: We’ll keep pushing the standard, keep evolving the bar until “quant” actually means something in the public code space.

Use with clarity, use with discipline, and always trade your edge.

— Dskyz , for DAFE Trading Systems

ATR ComboA Collection of three ATRs.

The whole idea of this indicator is to easily visualise the relationship of volatility to the current price action.

The default settings are:

5 Moving Average (Pink)

50 Moving Average (Blue)

1000 Moving Average (Yellow)

Using the default settings, the Yellow line represents the larger-scale volatility average.

the Blue line represents more recent volatility and the Pink lien represents the very recent average.

Using this indicator is possible in a number of ways:

If volatility is high and directional, you will see a sharp increase in the Pink line.

If volatility is high and choppy, the Pink line will be well above the Blue line and will oscillate up and down.

If volatility is starting to cool down, the Pink line will approach the Blue and Yellow lines.

ATR Volatility giua64ATR Volatility giua64 – Smart Signal + VIX Filter

📘 Script Explanation (in English)

Title: ATR Volatility giua64 – Smart Signal + VIX Filter

This script analyzes market volatility using the Average True Range (ATR) and compares it to its moving average to determine whether volatility is HIGH, MEDIUM, or LOW.

It includes:

✅ Custom or preset configurations for different asset classes (Forex, Indices, Gold, etc.).

✅ An optional external volatility index input (like the VIX) to refine directional bias.

✅ A directional signal (LONG, SHORT, FLAT) based on ATR strength, direction, and external volatility conditions.

✅ A clean visual table showing key values such as ATR, ATR average, ATR %, VIX level, current range, extended range, and final signal.

This tool is ideal for traders looking to:

Monitor the intensity of price movements

Filter trading strategies based on volatility conditions

Identify momentum acceleration or exhaustion

⚙️ Settings Guide

Here’s a breakdown of the user inputs:

🔹 ATR Settings

Setting Description

ATR Length Number of periods for ATR calculation (default: 14)

ATR Smoothing Type of moving average used (RMA, SMA, EMA, WMA)

ATR Average Length Period for the ATR moving average baseline

🔹 Asset Class Preset

Choose between:

Manual – Define your own point multiplier and thresholds

Forex (Pips) – Auto-set for FX markets (high precision)

Indices (0.1 Points) – For index instruments like DAX or S&P

Gold (USD) – Preset suitable for XAU/USD

If Manual is selected, configure:

Setting Description

Points Multiplier Multiplies raw price ranges into useful units (e.g., 10 for Gold)

Low Volatility Threshold Threshold to define "LOW" volatility

High Volatility Threshold Threshold to define "HIGH" volatility

🔹 Extended Range and VIX

Setting Description

Timeframe for Extended High/Low Used to compare larger price ranges (e.g., Daily or Weekly)

External Volatility Index (VIX) Symbol for a volatility index like "VIX" or "EUVI"

Low VIX Threshold Below this level, VIX is considered "low" (default: 20)

High VIX Threshold Above this level, VIX is considered "high" (default: 30)

🔹 Table Display

Setting Description

Table Position Where the visual table appears on the chart (e.g., bottom_center, top_left)

Show ATR Line on Chart Whether to display the ATR line directly on the chart

✅ Signal Logic Summary

The script determines the final signal based on:

ATR being above or below its average

ATR rising or falling

ATR percentage being significant (>2%)

VIX being high or low

Conditions Signal

ATR rising + high volatility + low VIX LONG

ATR falling + high volatility + high VIX SHORT

ATR flat or low volatility or low %ATR FLAT

timer/tr/atr [keypoems]Session and Instant Volatility Ticker

What it actually does:

- Session ATR – Reports the historical (e.g. “0200-0600”) average true range of the past x sessions, reports the +1Stdev value.

- Real-time ATR feed – streams the current ATR value every tick.

- Ticker line – Sess. ATR +1Stdev | Current ATR | Previous TR | 🕒 Time-left-in-bar |

Think of it as a volatility check: a single glance tells you if the average candle size is compatible with your usual stop or not.

Open Source.

Volume MAs Supertrend | Lyro RS📊 Volume MAs Supertrend | Lyro RS is an advanced trading tool that combines volume-adjusted moving averages with a dynamic Supertrend system. This indicator provides a robust framework for identifying market trends and entry/exit points.

✨ Key Features :

📈 Volume-Weighted Moving Averages (VWMA): Integrates price and volume data to provide a more accurate moving average, allowing for better trend analysis.

🔧 Multiple MA Types: Choose from SMA, EMA, WMA, VWMA, DEMA, TEMA, RMA, HMA, ALMA to suit your preferred trading strategy.

📊 Dual-Multiplier Supertrend System: Uses ATR to dynamically calculate upper and lower bands for long and short trends, with distinct multipliers for each.

🎨 Customizable Color Schemes: Choose from Classic, Mystic, Accented, and Royal color palettes or customize your own colors for bullish and bearish trends.

🔍 Visual Enhancements: Color-coded Supertrend lines, candlesticks, and bars for quick trend identification.

⏰ Alert System: Alerts for long and short signals based on trend changes.

🔧 How It Works :

The Supertrend line is calculated using ATR over a user-defined period, with separate multipliers for long and short positions.

📈 A bullish trend is signaled when the price crosses above the upper band, and a bearish trend is signaled when the price crosses below the lower band.

🎨 The Supertrend line changes color to reflect trend direction, with candlesticks and bars matching the trend's color for visual clarity.

⚙️ Customization Options :

🛠️ Moving Average Settings: Select your preferred moving average type (SMA, EMA, VWMA, etc.) and adjust the length for smoother or more responsive trend signals.

📐 Supertrend Parameters: Define the ATR period and adjust multipliers to fine-tune sensitivity for long and short signals.

🎨 Color Configuration: Choose from predefined color palettes or create your own custom scheme for trend signals.

📈 Use Cases :

✅ Confirm market trends before entering trades.

🚪 Identify potential entry/exit points as trend directions shift.

👀 Visually analyze market conditions with color-coded candlesticks and bars.

⚠️ Disclaimer :

This indicator should not be used as a standalone tool for making trading decisions. Always combine with other forms of analysis and risk management practices.

Daily Price RangeThe indicator is designed to analyze an instrument’s volatility based on daily extremes (High-Low) and to compare the current day’s range with the typical (median) range over a selected period. This helps traders assess how much of the "usual" daily movement has already occurred and how much may still be possible during the trading day.

SuperTrade ST1 StrategyOverview

The SuperTrade ST1 Strategy is a long-only trend-following strategy that combines a Supertrend indicator with a 200-period EMA filter to isolate high-probability bullish trade setups. It is designed to operate in trending markets, using volatility-based exits with a strict 1:4 Risk-to-Reward (R:R) ratio, meaning that each trade targets a profit 4× the size of its predefined risk.

This strategy is ideal for traders looking to align with medium- to long-term trends, while maintaining disciplined risk control and minimal trade frequency.

How It Works

This strategy leverages three key components:

Supertrend Indicator

A trend-following indicator based on Average True Range (ATR).

Identifies bullish/bearish trend direction by plotting a trailing stop line that moves with price volatility.

200-period Exponential Moving Average (EMA) Filter

Trades are only taken when the price is above the EMA, ensuring participation only during confirmed uptrends.

Helps filter out counter-trend entries during market pullbacks or ranges.

ATR-Based Stop Loss and Take Profit

Each trade uses the ATR to calculate volatility-adjusted exit levels.

Stop Loss: 1× ATR below entry.

Take Profit: 4× ATR above entry (1:4 R:R).

This asymmetry ensures that even with a lower win rate, the strategy can remain profitable.

Entry Conditions

A long trade is triggered when:

Supertrend flips from bearish to bullish (trend reversal).

Price closes above the Supertrend line.

Price is above the 200 EMA (bullish market bias).

Exit Logic

Once a long position is entered:

Stop loss is set 1 ATR below entry.

Take profit is set 4 ATR above entry.

The strategy automatically exits the position on either target.

Backtest Settings

This strategy is configured for realistic backtesting, including:

$10,000 account size

2% equity risk per trade

0.1% commission

1 tick slippage

These settings aim to simulate real-world conditions and avoid overly optimistic results.

How to Use

Apply the script to any timeframe, though higher timeframes (1H, 4H, Daily) often yield more reliable signals.

Works best in clearly trending markets (especially in crypto, stocks, indices).

Can be paired with alerts for live trading or analysis.

Important Notes

This version is long-only by design. No short positions are executed.

Ideal for swing traders or position traders seeking asymmetric returns.

Users can modify the ATR period, Supertrend factor, or EMA filter length based on asset behavior.

ADR & ATR OverlayADR & ATR Overlay

This indicator will display the following as an overlay on your chart:

ADR

% of ADR

ADR % of Price

ATR

% of ATR

ATR % of Price

Description:

ADR : Average Day Range

% of ADR : Percentage that the current price move has covered its average.

ADR % of Price : The percentage move implied by the average range.

ATR : Average True Range

% of ATR : Percentage that the current price move has covered its average.

ATR % of Price : The percentage move implied by the average true range.

Options:

Time Frame

Length

Smoothing

Enable or Disable each value

Text Color

Background Color

How to use this indicator:

The ADR and ATR can be used to provide information about average price moves to help set targets, stop losses, entries and exits based on the potential average moves.

Example: If the "% of ADR" is reading 100%, then 100% of the asset's average price range has been covered, suggesting that an additional move beyond the range has a lower probability.

Example: "ADR % of Price" provides potential price movement in percentage which can be used to asses R/R for asset.

Example: ADR (D) reading is 100% at market close but ATR (D) is at 70% at close. This suggests that there is a potential move of 30% in Pre/Post market as suggested by averages.

Notes:

These indicators are available as oscillators to place under your chart through trading view but this indicator will place them on the chart in numerical only format.

Please feel free to modify this script if you like but please acknowledge me, I am only a hobby coder so this takes some time & effort.

ADX Supertrend | [DeV]The "ADX Supertrend" indicator is a user-friendly tool that blends two popular trading indicators—the Supertrend and the Average Directional Index (ADX)—to help traders spot trends and make smarter trading decisions. By combining these two, it offers a clearer picture of when a market is trending strongly and in which direction, while cutting down on misleading signals. Here’s a straightforward explanation of how each part works, how they team up, the benefits of using them together, and why the ADX makes the Supertrend even better.

Supertrend:

It's like a guide that follows the market’s price movements to tell you whether prices are trending up or down. It creates two lines, one above and one below the price, based on how much the market is bouncing around (its volatility). When the price moves above the upper line, it signals an uptrend (a good time to buy), and the indicator draws a line below the price to show support. When the price drops below the lower line, it signals a downtrend (a potential time to sell), and the line appears above the price as resistance. The Supertrend is great because it adjusts to market conditions, widening the gap between lines in wild markets and tightening it in calm ones.

Average Directional Index:

The ADX is all about measuring how strong a trend is, without caring whether it’s going up or down. Think of it as a meter that tells you if the market is charging forward with purpose or just drifting aimlessly. It uses a scale from 0 to 100, where higher numbers mean a stronger trend. For example, an ADX above 25 often suggests a solid trend worth paying attention to, while a low ADX signals a sleepy, sideways market. The ADX also looks at whether buyers or sellers are in control to confirm the trend’s direction.

Confluence:

The Supertrend is great at spotting trends, but it can be a bit trigger-happy, giving signals in markets that aren’t really trending. That’s where the ADX shines. It acts like a quality control check, making sure the Supertrend’s signals only count when the market is moving with conviction. By filtering out weak or messy trends, the ADX helps you avoid wasting time on trades that fizzle out. It also double-checks the trend’s direction, so you’re not just guessing whether buyers or sellers are in charge. This teamwork means you get signals that are more reliable and less likely to lead you astray, especially in tricky markets where prices bounce around without a clear path.

ZenLab ATR FNSThis indicator was created specifically for Zen Labs which includes a custom ATR (Average True Range) table that displays the ATR value for a selected period of candles.

ATR is a volatility indicator that measures the average range between high and low prices over a given number of periods. It helps traders assess how much an asset typically moves, providing valuable information for setting stop losses, take profits, or identifying market conditions. It adapts to changing market conditions, making it useful across different timeframes and asset classes.

How the ATR Indicator Works:

The ATR is based on the concept of True Range (TR), which is the greatest of the following three values:

- Current High minus Current Low

- Absolute value of Current High minus Previous Close

- Absolute value of Current Low minus Previous Close

Averaging the True Range:

Once the True Range is calculated for each period, the ATR is computed by averaging these True Ranges over a set number of periods and is displayed in the table.

Interpreting the ATR:

- A higher ATR value indicates higher volatility—prices are moving more significantly.

- A lower ATR value indicates lower volatility—prices are more stable and less active.

Enjoy!

- Rebel Empire

Adaptive ATR Limits█ OVERVIEW

This indicator plots adaptive ATR limits for intraday trading. A key feature of this indicator, which makes it different from other ATR limit indicators, is that the top and bottom ATR limit lines are always exactly one ATR apart from each other (in "auto" mode; there is also a "basic" mode, which plots the limits in the more traditional way—i.e., one ATR above the low and one ATR below the high at all times—and this can be used for comparison).

█ FEATURES

Provides an algorithm to plot the most reasonable intraday ATR top/bottom limits based on currently available information

Dynamically adapts limits as the price evolves during the day

Works correctly and consistently on both RTH and ETH charts

Has a user-selected ADR mode to base the limits on ADR instead of ATR

Option to include the current pre-market and previous day's post-market range in the calculation

Configurable ATR/ADR averaging length

Provides a visual smoothing option

Provides an information box showing the current numerical ATR/ADR values

Reasonable defaults that work well if the user changes nothing

Well-documented, high-quality, open-source code for those interested

█ HOW TO USE

At a minimum, there is nothing that needs to be set. The defaults work well. The ATR top line (red, configurable) gives you the most reasonable move given the currently available information. The line will move away from the price as the price approaches it; that is normal—it is reacting to new information. This happens until the ATR bottom limit hits the lower of the daily low and the previous day's close (in ATR mode). The ATR bottom line (green, configurable) works the same way, with reversed logic.

There is an option to use ADR instead of ATR. The ATR includes the previous day's RTH close in the range, whereas ADR does not. Another option allows the user to add the current day's pre-market range or the previous day's post-market into the current day's range, which has an effect if either of those went outside of today's RTH range, plus yesterday's RTH close (in the default ATR mode). Pre-market and post-market range is not typically included in the daily true range, so only change it if you really know you want it.

█ CONCEPTS

Most traditional ATR limit indicators plot the top ATR limit one ATR above the current daily low, and the bottom ATR limit one ATR below the current daily high. This indicator can also do that (in "basic" mode), but its value lies in its default "auto" mode, which uses an algorithm to dynamically adapt the ATR limits throughout the day, keeping them one ATR apart at all times. It tries to plot the most sensible ATR limits based on the current daily ATR, in order to provide a reasonable visual intraday target, given the available information at that point in time.

"Auto" mode is actually a weighted average of two methods: midpoint and relative (both of which can also be explicitly selected). The midpoint method places the midpoint of the ATR limit equal to the midpoint of the currently established daily range. The relative method measures the currently established daily range and calculates the position of the current price within it (as a ratio between 0 and 1). It then uses that value as a weight in a weighted average of extreme locations for the ATR limits, which are: the ATR top anchored to one ATR above the daily low, and the ATR bottom anchored to one ATR below the daily high.

The relative method is more advanced and better for most of the day; however, it can cause wild swings in the early market or pre-market before a reasonable range (as a percentage of ATR) has been established. "Auto" mode therefore takes another weighted average between the two methods, with the weight determined by the percentage of the ATR currently established within the day, more strongly weighting the calmer midpoint method before a good range is established. Once the full ATR has been achieved, the algorithm in "auto" mode will have fully switched to the relative method and will remain with that method for the rest of the day.

To explain the effect further, as an example, imagine that the price is approaching the full ATR range on the high side. At this point, the indicator will have almost fully transitioned to the second (relative) method. The lower ATR limit will now be anchored to the daily low as the price hits the upper ATR limit. If the price goes beyond the upper ATR, the lower ATR limit will stay anchored to the daily low, and the upper limit will stay anchored to one ATR above the lower limit. This allows you to see how far the price is going beyond the upper ATR limit. If the price then returns and backs off the upper ATR limit, the lower ATR limit will un-anchor from the daily low (it will actually rise, since the daily ATR range has been exceeded, so the lower ATR limit needs to come up because the actual daily range can’t fit into the ATR range anymore). The overall effect is to give you the best visual indication of where the price is in relation to a possible upper ATR-based target. Reverse this example for when the price low approaches the ATR range on the low side.

Care was taken so that the code uses no hard-coded time zones, exchanges, or session times. For this reason, it can in principle work globally. However, it very much depends on the information provided by the exchange, which is reflected in built-in Pine Script variables (see Limitations below).

█ LIMITATIONS

The indicator was developed for US/European equities and is tested on them only. It is also known to work on US futures; in this case, the whole 23-hour session is used, and the "Sessions to include in range" setting has no effect. It may or may not work as intended on security types and equities/futures for other countries.

Smart Range DetectorSmart Range Detector

What It Does

This indicator automatically detects and validates significant trading ranges using pivot point analysis combined with logarithmic fibonacci relationships. It operates by identifying specific pivot patterns (High-Low-High and Low-High-Low) that meet fibonacci validation criteria to filter out noise and highlight only the most reliable trading ranges. Each range is continuously monitored for potential mitigation (breakout) events.

Key Features

Identifies both High-Low-High and Low-High-Low range patterns

Validates each range using logarithmic fibonacci relationships (more accurate than linear fibs)

Detects range mitigations (breakouts) and visually differentiates them

Shows fibonacci levels within ranges (25%, 50%, 75%) for potential reversal points

Visualizes extension levels beyond ranges for breakout targets

Analyzes volume profile with customizable price divisions (default: 60)

Displays Point of Control (POC) and Value Area for traded volume analysis

Implements performance optimization with configurable range limits

Includes user-adjustable safety checks to prevent Pine Script limitations

Offers fully customizable colors, line widths, and transparency settings

How To Use It

Identify Valid Ranges : The indicator automatically detects and highlights trading ranges that meet fibonacci validation criteria

Monitor Fibonacci Levels : Watch for price reactions at internal fib levels (25%, 50%, 75%) for potential reversal opportunities

Track Extension Targets : Use the extension lines as potential targets when price breaks out of a range

Analyze Volume Structure : Enable the volume profile mode to see where most volume was traded within mitigated ranges

Trade Range Boundaries : Look for reactions at range highs/lows combined with volume POC for higher probability entries

Manage Performance : Adjust the maximum displayed ranges and history bars settings for optimal chart performance

Settings Guide

Left/Right Bars Look Back : Controls how far back the indicator looks to identify pivot points (higher values find more ranges but may reduce sensitivity)

Max History Bars : Limits how far back in history the indicator will analyze (stays within Pine Script's 10,000 bar limitation)

Max Ranges to Display : Restricts the total number of ranges kept in memory for improved performance (1-50)

Volume Profile : When enabled, shows volume distribution analysis for mitigated ranges

Volume Profile Divisions : Controls the granularity of the volume analysis (higher values show more detail)

Display Options : Toggle visibility of range lines, fibonacci levels, extension lines, and volume analysis elements

Transparency & Color Settings : Fully customize the visual appearance of all indicator elements

Line Width Settings : Adjust the thickness of lines for better visibility on different timeframes

Technical Details

The indicator uses logarithmic fibonacci calculations for more accurate price relationships

Volume profile analysis creates 60 price divisions by default (adjustable) for detailed volume distribution

All timestamps are properly converted to work with Pine Script's bar limitations

Safety checks prevent "array index out of bounds" errors that plague many complex indicators

Time-based coordinates are used instead of bar indices to prevent "bar index too far" errors

This indicator works well on all timeframes and instruments, but performs best on 5-minute to daily charts. Perfect for swing traders, range traders, and breakout strategists.

What Makes It Different

Most range indicators simply draw boxes based on recent highs and lows. Smart Range Detector validates each potential range using proven fibonacci relationships to filter out noise. It then adds sophisticated volume analysis to help traders identify the most significant price levels within each range. The performance optimization features ensure smooth operation even on lower timeframes and extended history analysis.