4 Bar Momentum Reversal strategy█ STRATEGY DESCRIPTION

The "4 Bar Momentum Reversal Strategy" is a mean-reversion strategy designed to identify price reversals following a sustained downward move. It enters a long position when a reversal condition is met and exits when the price shows strength by exceeding the previous bar's high. This strategy is optimized for indices and stocks on the daily timeframe.

█ WHAT IS THE REFERENCE CLOSE?

The Reference Close is the closing price from X bars ago, where X is determined by the Lookback period. Think of it as a moving benchmark that helps the strategy assess whether prices are trending upwards or downwards relative to past performance. For example, if the Lookback is set to 4, the Reference Close is the closing price 4 bars ago (`close `).

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price has been lower than the Reference Close for at least `Buy Threshold` consecutive bars. This indicates a sustained downward move, suggesting a potential reversal.

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Buy Threshold: The number of consecutive bearish bars needed to trigger a Buy Signal. Default is 4.

Lookback: The number of bars ago used to calculate the Reference Close. Default is 4.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for trending markets with frequent reversals.

It performs best in volatile conditions where price movements are significant.

Backtesting results should be analysed to optimize the Buy Threshold and Lookback parameters for specific instruments.

Swingtrading

Fibonacci Swing Trading BotStrategy Overview for "Fibonacci Swing Trading Bot"

Strategy Name: Fibonacci Swing Trading Bot

Version: Pine Script v5

Purpose: This strategy is designed for swing traders who want to leverage Fibonacci retracement levels and candlestick patterns to enter and exit trades on higher time frames.

Key Components:

1. Multiple Timeframe Analysis:

The strategy uses a customizable timeframe for analysis. You can choose between 4hour, daily, weekly, or monthly time frames to fit your preferred trading horizon. The high and low-price data is retrieved from the selected timeframe to identify swing points.

2. Fibonacci Retracement Levels:

The script calculates two key Fibonacci retracement levels:

0.618: A common level where price often retraces before resuming its trend.

0.786: A deeper retracement level, often used to identify stronger support/resistance areas.

These levels are dynamically plotted on the chart based on the highest high and lowest low over the last 50 bars of the selected timeframe.

3. Candlestick Based Entry Signals:

The strategy uses candlestick patterns as the only indicator for trade entries:

Bullish Candle: A green candle (close > open) that forms between the 0.618 retracement level and the swing high.

Bearish Candle: A red candle (close < open) that forms between the 0.786 retracement level and the swing low.

When these candlestick patterns align with the Fibonacci levels, the script triggers buy or sell signals.

4. Risk Management:

Stop Loss: The stop loss is set at 1% below the entry price for long trades and 1% above the entry price for short trades. This tight risk management ensures controlled losses.

Take Profit: The strategy uses a 2:1 risk-to-reward ratio. The take profit is automatically calculated based on this ratio relative to the stop loss.

5. Buy/Sell Logic:

Buy Signal: Triggered when a bullish candle forms above the 0.618 retracement level and below the swing high. The bot then places a long position.

Sell Signal: Triggered when a bearish candle forms below the 0.786 retracement level and above the swing low. The bot then places a short position.

The stop loss and take profit levels are automatically managed once the trade is placed.

Strengths of This Strategy:

Swing Trading Focus: The strategy is ideal for swing traders, targeting longer-term price moves that can take days or weeks to play out.

Simple Yet Effective Indicators: By only relying on Fibonacci retracement levels and basic candlestick patterns, the strategy avoids complexity while capitalizing on well-known support and resistance zones.

Automated Risk Management: The built-in stop loss and take profit mechanism ensures trades are protected, adhering to a strict 2:1 risk/reward ratio.

Multiple Timeframe Analysis: The script adapts to various market conditions by allowing users to switch between different timeframes (4hour, daily, weekly, monthly), giving traders flexibility.

Strategy Use Cases:

Retracement Traders: Traders who focus on entering the market at key retracement levels (0.618 and 0.786) will find this strategy especially useful.

Trend Reversal Traders: The strategy’s reliance on candlestick formations at Fibonacci levels helps traders spot potential reversals in price trends.

Risk Conscious Traders: With its 1% risk per trade and 2:1 risk/reward ratio, the strategy is ideal for traders who prioritize risk management in their trades.

Bitcoin CME-Spot Z-Spread - Strategy [presentTrading]This time is a swing trading strategy! It measures the sentiment of the Bitcoin market through the spread of CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. By applying Bollinger Bands to the spread, the strategy seeks to capture mean-reversion opportunities when prices deviate significantly from their historical norms

█ Introduction and How it is Different

The Bitcoin CME-Spot Bollinger Bands Strategy is designed to capture mean-reversion opportunities by exploiting the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. The strategy uses Bollinger Bands to detect when the spread between these two correlated assets has deviated significantly from its historical norm, signaling potential overbought or oversold conditions.

What sets this strategy apart is its focus on spread trading between futures and spot markets rather than price-based indicators. By applying Bollinger Bands to the spread rather than individual prices, the strategy identifies price inefficiencies across markets, allowing traders to take advantage of the natural reversion to the mean that often occurs in these correlated assets.

BTCUSD 8hr Performance

█ Strategy, How It Works: Detailed Explanation

The strategy relies on Bollinger Bands to assess the volatility and relative deviation of the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. Bollinger Bands consist of a moving average and two standard deviation bands, which help measure how much the spread deviates from its historical mean.

🔶 Spread Calculation:

The spread is calculated by subtracting the Bitfinex spot price from the CME Bitcoin futures price:

Spread = CME Price - Bitfinex Price

This spread represents the difference between the futures and spot markets, which may widen or narrow based on supply and demand dynamics in each market. By analyzing the spread, the strategy can detect when prices are too far apart (potentially overbought or oversold), indicating a trading opportunity.

🔶 Bollinger Bands Calculation:

The Bollinger Bands for the spread are calculated using a simple moving average (SMA) and the standard deviation of the spread over a defined period.

1. Moving Average (SMA):

The simple moving average of the spread (mu_S) over a specified period P is calculated as:

mu_S = (1/P) * sum(S_i from i=1 to P)

Where S_i represents the spread at time i, and P is the lookback period (default is 200 bars). The moving average provides a baseline for the normal spread behavior.

2. Standard Deviation:

The standard deviation (sigma_S) of the spread is calculated to measure the volatility of the spread:

sigma_S = sqrt((1/P) * sum((S_i - mu_S)^2 from i=1 to P))

3. Upper and Lower Bollinger Bands:

The upper and lower Bollinger Bands are derived by adding and subtracting a multiple of the standard deviation from the moving average. The number of standard deviations is determined by a user-defined parameter k (default is 2.618).

- Upper Band:

Upper Band = mu_S + (k * sigma_S)

- Lower Band:

Lower Band = mu_S - (k * sigma_S)

These bands provide a dynamic range within which the spread typically fluctuates. When the spread moves outside of these bands, it is considered overbought or oversold, potentially offering trading opportunities.

Local view

🔶 Entry Conditions:

- Long Entry: A long position is triggered when the spread crosses below the lower Bollinger Band, indicating that the spread has become oversold and is likely to revert upward.

Spread < Lower Band

- Short Entry: A short position is triggered when the spread crosses above the upper Bollinger Band, indicating that the spread has become overbought and is likely to revert downward.

Spread > Upper Band

🔶 Risk Management and Profit-Taking:

The strategy incorporates multi-step take profits to lock in gains as the trade moves in favor. The position is gradually reduced at predefined profit levels, reducing risk while allowing part of the trade to continue running if the price keeps moving favorably.

Additionally, the strategy uses a hold period exit mechanism. If the trade does not hit any of the take-profit levels within a certain number of bars, the position is closed automatically to avoid excessive exposure to market risks.

█ Trade Direction

The trade direction is based on deviations of the spread from its historical norm:

- Long Trade: The strategy enters a long position when the spread crosses below the lower Bollinger Band, signaling an oversold condition where the spread is expected to narrow.

- Short Trade: The strategy enters a short position when the spread crosses above the upper Bollinger Band, signaling an overbought condition where the spread is expected to widen.

These entries rely on the assumption of mean reversion, where extreme deviations from the average spread are likely to revert over time.

█ Usage

The Bitcoin CME-Spot Bollinger Bands Strategy is ideal for traders looking to capitalize on price inefficiencies between Bitcoin futures and spot markets. It’s especially useful in volatile markets where large deviations between futures and spot prices occur.

- Market Conditions: This strategy is most effective in correlated markets, like CME futures and spot Bitcoin. Traders can adjust the Bollinger Bands period and standard deviation multiplier to suit different volatility regimes.

- Backtesting: Before deployment, backtesting the strategy across different market conditions and timeframes is recommended to ensure robustness. Adjust the take-profit steps and hold periods to reflect the trader’s risk tolerance and market behavior.

█ Default Settings

The default settings provide a balanced approach to spread trading using Bollinger Bands but can be adjusted depending on market conditions or personal trading preferences.

🔶 Bollinger Bands Period (200 bars):

This defines the number of bars used to calculate the moving average and standard deviation for the Bollinger Bands. A longer period smooths out short-term fluctuations and focuses on larger, more significant trends. Adjusting the period affects the responsiveness of the strategy:

- Shorter periods (e.g., 100 bars): Makes the strategy more reactive to short-term market fluctuations, potentially generating more signals but increasing the risk of false positives.

- Longer periods (e.g., 300 bars): Focuses on longer-term trends, reducing the frequency of trades and focusing only on significant deviations.

🔶 Standard Deviation Multiplier (2.618):

The multiplier controls how wide the Bollinger Bands are around the moving average. By default, the bands are set at 2.618 standard deviations away from the average, ensuring that only significant deviations trigger trades.

- Higher multipliers (e.g., 3.0): Require a more extreme deviation to trigger trades, reducing trade frequency but potentially increasing the accuracy of signals.

- Lower multipliers (e.g., 2.0): Make the bands narrower, increasing the number of trade signals but potentially decreasing their reliability.

🔶 Take-Profit Levels:

The strategy has four take-profit levels to gradually lock in profits:

- Level 1 (3%): 25% of the position is closed at a 3% profit.

- Level 2 (8%): 20% of the position is closed at an 8% profit.

- Level 3 (14%): 15% of the position is closed at a 14% profit.

- Level 4 (21%): 10% of the position is closed at a 21% profit.

Adjusting these take-profit levels affects how quickly profits are realized:

- Lower take-profit levels: Capture gains more quickly, reducing risk but potentially cutting off larger profits.

- Higher take-profit levels: Let trades run longer, aiming for bigger gains but increasing the risk of price reversals before profits are locked in.

🔶 Hold Days (20 bars):

The strategy automatically closes the position after 20 bars if none of the take-profit levels are hit. This feature prevents trades from being held indefinitely, especially if market conditions are stagnant. Adjusting this:

- Shorter hold periods: Reduce the duration of exposure, minimizing risks from market changes but potentially closing trades too early.

- Longer hold periods: Allow trades to stay open longer, increasing the chance for mean reversion but also increasing exposure to unfavorable market conditions.

By understanding how these default settings affect the strategy’s performance, traders can optimize the Bitcoin CME-Spot Bollinger Bands Strategy to their preferences, adapting it to different market environments and risk tolerances.

Dual RSI Differential - Strategy [presentTrading]█ Introduction and How it is Different

The Dual RSI Differential Strategy introduces a nuanced approach to market analysis and trading decisions by utilizing two Relative Strength Index (RSI) indicators calculated over different time periods. Unlike traditional strategies that employ a single RSI and may signal premature or delayed entries, this method leverages the differential between a shorter and a longer RSI. This approach pinpoints more precise entry and exit points, providing a refined tool for traders to exploit market conditions effectively, particularly in overbought and oversold scenarios.

Most important: it is a good eductional code for swing trading.

For beginners, this Pine Script provides a complete function that includes crucial elements such as holding days and the option to configure take profit/stop loss settings:

- Hold Days: This feature ensures that trades are not exited too hastily, helping traders to ride out short-term market volatility. It's particularly valuable for swing trading where maintaining positions slightly longer can lead to capturing significant trends.

- TPSL Condition (None by default): This setting allows traders to focus solely on the strategy's robust entry and exit signals without being constrained by preset profit or loss limits. This flexibility is crucial for learning to adjust strategy settings based on personal risk tolerance and market observations.

BTCUSD 6h LS Performance

█ Strategy, How It Works: Detailed Explanation

🔶 RSI Calculation:

The RSI is a momentum oscillator that measures the speed and change of price movements. It is calculated using the formula:

RSI = 100 - (100 / (1 + RS))

Where RS (Relative Strength) = Average Gain of up periods / Average Loss of down periods.

🔶 Dual RSI Setup:

This strategy involves two RSI indicators:

RSI_Short (RSI_21): Calculated over a short period (21 days).

RSI_Long (RSI_42): Calculated over a longer period (42 days).

Differential Calculation:

The strategy focuses on the differential between these two RSIs:

RSI Differential = RSI_Long - RSI_Short

This differential helps to identify when the shorter-term sentiment diverges from longer-term trends, signaling potential trading opportunities.

BTCUSD Local picuture

🔶 Signal Triggers:

Entry Signal: A buy (long) signal is triggered when the RSI Differential exceeds -5, suggesting strengthening short-term momentum. Conversely, a sell (short) signal occurs when the RSI Differential falls below +5, indicating weakening short-term momentum.

Exit Signal: Trades are generally exited when the RSI Differential reverses past these thresholds, indicating a potential momentum shift.

█ Trade Direction

This strategy accommodates various trading preferences by allowing selections among long, short, or both directions, thus enabling traders to capitalize on diverse market movements and volatility.

█ Usage

The Dual RSI Differential Strategy is particularly suited for:

Traders who prefer a systematic approach to capture market trends.

Those who seek to minimize risks associated with rapid and unexpected market movements.

Traders who value strategies that can be finely tuned to different market conditions.

█ Default Settings

- Trading Direction: Both — allows capturing of upward and downward market movements.

- Short RSI Period: 21 days — balances sensitivity to market movements.

- Long RSI Period: 42 days — smoothens out longer-term fluctuations to provide a clearer market trend.

- RSI Difference Level: 5 — minimizes false signals by setting a moderate threshold for action.

Use Hold Days: True — introduces a temporal element to trading strategy, holding positions to potentially enhance outcomes.

- Hold Days: 5 — ensures that trades are not exited too hastily, helping to ride out short-term volatility.

- TPSL Condition: None — enables traders to focus solely on the strategy's entry and exit signals without preset profit or loss limits.

- Take Profit Percentage: 15% — aims for significant market moves to lock in profits.

- Stop Loss Percentage: 10% — safeguards against large losses, essential for long-term capital preservation.

Strategy for UT Bot Alerts indicator Using the UT Bot alerts indicator by @QuantNomad, this strategy was designed for showing an example of how this indicator could be used, also, it has the goal to help some people from a group that use to use this indicator for their trading. Under any circumstance I recommend to use it without testing it before in real time.

Backtesting context: 2020-02-05 to 2023-02-25 of BTCUSD 4H by Tvc. Commissions: 0.03% for each entry, 0.03% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 3 indicators are used:

UT Bot Alerts indicator by Quantnomad

One Ema of 200 periods for indicate the trend

Atr stop loss from Gatherio

Trade conditions:

For longs:

Close price is higher than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our long signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as buy (open long position)

The other half will be closed when close price is lower than Atr and Ema from UT Bot cross under Atr. This will be showed as cl buy (close long position)

For shorts:

Close price is lower than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our short signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as sell (open short position)

The other half will be closed when close price is higher than Atr and Ema from UT Bot cross over Atr. This will be showed as cl sell (close short position)

Risk management

For calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a long signal at price of 20,000 usd. The stop loss price from atr stop loss is 19,000. You calculate the distance in percent between 20,000 and 19,000. In this case, that distance would be of 5,0%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(5,0%) = 500usd. It means, you have to use 500 usd for risking 2.5% of your account.

We will use this risk management for apply compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital

---> Do not forget to deactivate Trades on chart option in style settings for a cleaner look of the chart <---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Strategies for trending markets use to have more looses than wins and it takes a long time to get profits, so do not forget to be patient and consistent !

---> The strategy can still be improved, you can change some parameters depending of the asset and timeframe like risk/reward for taking profits, for break even, also the main parameters of the UT Bot Alerts <----

Investments/swing trading strategy for different assetsStop worrying about catching the lowest price, it's almost impossible!: with this trend-following strategy and protection from bearish phases, you will know how to enter the market properly to obtain benefits in the long term.

Backtesting context: 1899-11-01 to 2023-02-16 of SPX by Tvc. Commissions: 0.05% for each entry, 0.05% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 5 indicators are used:

One Ema of 200 periods

Atr Stop loss indicator from Gatherio

Squeeze momentum indicator from LazyBear

Moving average convergence/divergence or Macd

Relative strength index or Rsi

Trade conditions:

There are three type of entries, one of them depends if we want to trade against a bearish trend or not.

---If we keep Against trend option deactivated, the rules for two type of entries are:---

First type of entry:

With the next rules, we will be able to entry in a pull back situation:

Squeeze momentum is under 0 line (red)

Close is above 200 Ema and close is higher than the past close

Histogram from macd is under 0 line and is higher than the past one

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

For closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Second type of entry:

With the next rules, we will not lose a possible bullish movement:

Close is above 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entry, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

---If we keep Against trend option activated, the rules are the same as the ones above, but with one more type of entry. This is more useful in weekly timeframes, but could also be used in daily time frame:---

Third type of entry:

Close is under 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entries, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Risk management

For calculating the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a buy signal at price of 4,000 usd. The stop loss price from atr stop loss is 3,900. You calculate the distance in percent between 4,000 and 3,900. In this case, that distance would be of 2.50%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(2,5%) = 1000usd. It means, you have to use 1000 usd for risking 2.5% of your account.

We will use this risk management for applying compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

If you activate break even using rsi, when rsi crosses under overbought zone break even will be activated. This can work in some assets.

---Important: In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Some assets and timeframes where the strategy has also worked:

BTCUSD : 4H, 1D, W

SPX (US500) : 4H, 1D, W

GOLD : 1D, W

SILVER : 1D, W

ETHUSD : 4H, 1D

DXY : 1D

AAPL : 4H, 1D, W

AMZN : 4H, 1D, W

META : 4H, 1D, W

(and others stocks)

BANKNIFTY : 4H, 1D, W

DAX : 1D, W

RUT : 1D, W

HSI : 1D, W

NI225 : 1D, W

USDCOP : 1D, W

Simple SuperTrend Strategy for BTCUSD 4HHello guys!, If you are a swing trader and you are looking for a simple trend strategy, you should check this one. Based in the supertrend indicator, this strategy will help you to catch big movements in BTCUSD 4H and avoid losses as much as possible in consolidated situations of the market

This strategy was designed for BTCUSD in 4H timeframe

Backtesting context: 2020-01-02 to 2023-01-05 (The strategy has also worked in previous years)

Trade conditions:

Rules are actually simple, the most important thing is the risk and position management of this strategy

For long:

Once Supertrend changes from a downtrend to a uptrend, you enter into a long position. The stop loss will be defined by the atr stop loss

The first profit will be of 0.75 risk/reward ratio where half position will be closed. When this happens, you move the stop loss to break even.

Now, just will be there two situations:

Once Supertrend changes from a uptrend to a downtrend, you close the other half of the initial long position.

If price goes againts the position, the position will be closed due to breakeven.

For short:

Once Supertrend changes from a uptrend to a downtrend, you enter into a short position. The stop loss will be defined by the atr stop loss

The first profit will be of 0.75 risk/reward ratio where half position will be closed. When this happens, you move the stop loss to break even.

Like in the long position, just will be there two situations:

Once Supertrend changes from a downtrend to a uptrend, you close the other half of the initial short position.

If price goes againts the position, the position will be closed due to breakeven.

Risk management

For calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a long signal at price of 20,000 usd. The stop loss price from atr stop loss is 19,000. You calculate the distance in percent between 20,000 and 19,000. In this case, that distance would be of 5,0%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(5,0%) = 500usd. It means, you have to use 500 usd for risking 2.5% of your account.

We will use this risk management for apply compound interest.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, supertrend or positions.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

Signals meanings:

L for long position. CL for close long position.

S for short position. CS for close short position.

Tp for take profit (it also appears when the position is closed due to stop loss, this due to the script uses two kind of positions)

Exit due to break even or due to stop loss

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

The amount of trades closed in the backtest are not exactly the real ones. If you want to know the real ones, go to settings and change % of trade for first take profit to 100 for getting the real ones. In the backtest, the real amount of opened trades was of 194.

Indicators used:

Supertrend

Atr stop loss by garethyeo

This is the fist strategy that I publish in tradingview, I will be glad with you for any suggestion, support or advice for future scripts. Do not doubt in make any question you have and if you liked this content, leave a boost. I plan to bring more strategies and useful content for you!

[Sniper] SuperTrend + SSL Hybrid + QQE MODHi. I’m DuDu95.

**********************************************************************************

This is the script for the series called "Sniper".

*** What is "Sniper" Series? ***

"Sniper" series is the project that I’m going to start.

In "Sniper" Series, I’m going to "snipe and shoot" the youtuber’s strategy: to find out whether the youtuber’s video about strategy is "true or false".

Specifically, I’m going to do the things below.

1. Implement "Youtuber’s strategy" into pinescript code.

2. Then I will "backtest" and prove whether "the strategy really works" in the specific ticker (e.g. BTCUSDT) for the specific timeframe (e.g. 5m).

3. Based on the backtest result, I will rate and judge whether the youtube video is "true" or "false", and then rate the validity, reliability, robustness, of the strategy. (like a lie detector)

*** What is the purpose of this series? ***

1. To notify whether the strategy really works for the people who watched the youtube video.

2. To find and build my own scalping / day trading strategy that really works.

**********************************************************************************

*** Strategy Description ***

This strategy is from " QQE MOD + supertrend + ssl hybrid" by korean youtuber "코인투데이".

"코인투데이" claimed that this strategy will make you a lot of money in any crypto ticker in 15 minute timeframe.

### Entry Logic

1. Long Entry Logic

- Super Trend Short -> Long

- close > SSL Hybrid baseline upper k

- QQE MOD should be blue

2. Short Entry Logic

- Super Trend Long -> Short

- close < SSL Hybrid baseline lower k

- QQE MOD should be red

### Exit Logic

1. Long Exit Logic

- Super Trend Long -> Short

2. Short Entry Logic

- Super Trend Short -> Long

### StopLoss

1. Can Choose Stop Loss Type: Percent, ATR, Previous Low / High.

2. Can Chosse inputs of each Stop Loss Type.

### Take Profit

1. Can set Risk Reward Ratio for Take Profit.

- To simplify backtest, I erased all other options except RR Ratio.

- You can add Take Profit Logic by adding options in the code.

2. Can set Take Profit Quantity.

### Risk Manangement

1. Can choose whether to use Risk Manangement Logic.

- This controls the Quantity of the Entry.

- e.g. If you want to take 3% risk per trade and stop loss price is 6% below the long entry price,

then 50% of your equity will be used for trade.

2. Can choose How much risk you would take per trade.

### Plot

1. Added Labels to check the data of entry / exit positions.

2. Changed and Added color different from the original one. (green: #02732A, red: #D92332, yellow: #F2E313)

3. SuperTrend and SSL Hybrid Baseline is by default drawn on the chart.

4. If you check EMA filter, EMA would be drawn on the chart.

5. Should add QQE MOD indicator manually if you want to see QQE MOD.

**********************************************************************************

*** Rating: True or False?

### Rating:

→ 3.5 / 5 (0 = Trash, 1 = Bad, 2 = Not Good, 3 = Good, 4 = Great, 5 = Excellent)

### True or False?

→ True but not a 'perfect true'.

→ It did made a small profit on 15 minute timeframe. But it made a profit so it's true.

→ It worked well in longer timeframe. I think super trend works well so I will work on this further.

### Better Option?

→ Use this for Day trading or Swing Trading, not for Scalping. (Bigger Timeframe)

→ Although the result was not good at 15 minute timeframe, it was quite profitable in 1h, 2h, 4h, 8h, 1d timeframe.

→ Crypto like BTC, ETH was ok.

→ The result was better when I use EMA filter.

### Robust?

→ Yes. Although result was super bad in 5m timeframe, backtest result was "consistently" profitable on longer timeframe (when timeframe was bigger than 15m, it was profitable).

→ Also, MDD was good under risk management option on.

**********************************************************************************

*** Conclusion?

→ I recommend you not to use this on short timeframe as the youtuber first mentioned.

→ In my opinion, I can use on longer timeframe like 2h or bigger with EMA filter, stoploss and risk management.

Booz StrategyBooz Backtesting : Booz Backtesting is a method for analyzing the performance of your current trading strategy . Booz Backtesting aims to help you generate results and evaluate risk and return without risking real capital.

The Booz Backtesting is the Booz Super Swing Indicator equivalent but gives you the ability to backtest data on different charts.

This is an Indicator created for the purpose of identifying trends in Multiple Markets, it is based on Moving Average Crossover and extra features.

Swing Trading: This function allows you to navigate the entire trend until it is not strong enough, so you can compare it with fixed parameters such as Take Profit and Stop Loss.

Take Profit and Stop Loss function: With this function you will be able to choose the most optimal parameters and see in real time the results in order to choose the best combination of parameters.

Leverage : We have this function for the futures markets where you can check which is the most appropriate leverage for your operation.

Trend Filter: allows you to take multiple entries in the same direction of the market.

If the market crosses below the 200 moving average, it will take only short entries.

If the market crosses above the 200 moving average, it will take only long entries.

Timeframes

Charting from 1 Hour, 4 Hour, Daily, Weekly, Weekly

Markets :Booz Backtesting can be tested in Cryptocurrency, Stocks and Futures markets.

Background Color : at a glance, you can see what cycle the market is in.

Green background : Shows that the market is in a bullish cycle.

Red background: Shows that the market is in a bearish cycle.

Co-relation and St-deviation Strategy - BNB/USDT 15minThis indicator based on statistical analysis. it uses standard deviation and its co-relation to price action to generate signals. and following indicators has been used to calculate standard deviation and its co-relation values. finally it is capable to identify market changes in bottoms to pic most suitable points.

1. Parabolic SAR (parabolic stop and reverse)

2. Supertrend

3. Relative strength index (RSI)

4. Money flow index (MFI)

5. Balance of Power

6. Chande Momentum Oscillator

7. Center of Gravity (COG)

8. Directional Movement Index (DMI)

9. Stochastic

10. Symmetrically weighted moving average with fixed length

11. True strength index (TSI)

12. Williams %R

13. Accumulation/distribution index

14. Intraday Intensity Index

15. Negative Volume Index

16. Positive Volume Index

17. On Balance Volume

18. Price-Volume Trend

19. True range

20. Volume-weighted average price

21. Williams Accumulation/Distribution

22. Williams Variable Accumulation/Distribution

23. Simple Moving Average

24. Exponential Moving Average

25. CCI (commodity channel index)

26. Chop Zone

27. Ease of Movement

28. Detrended Price Oscillator

29. Advance Decline Line

30. Bull Bear Power

Up & Down Trend Trading Strategy - BNB/USDT 15minThis strategy will focus on up trend trading and down trend trading based on several indicators such as;

for up trend

1. SAR indicator

2. Super trend indicator

3. Simple moving average for the period of 100

down trend

1. RSI Indicator

2. Money flow index

3. Relative volatility index

4. Balance of powder

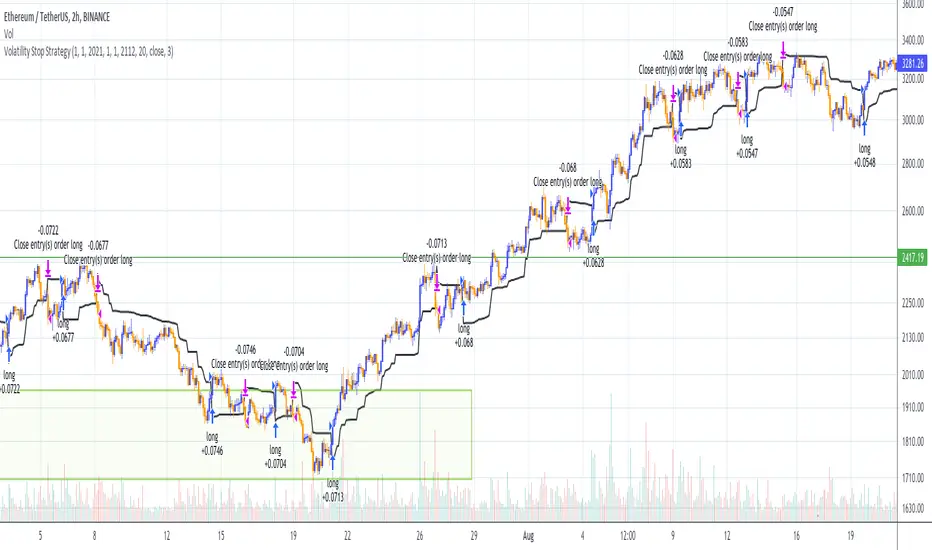

Volatility Stop Strategy (by Coinrule)Traders often use the volatility stop to protect trades dynamically, adjusting the stop price gradually based on the asset's volatility.

Just like the volatility stop is a great way to capture trend reversals on the downside, the opposite applies as well. Therefore, another useful application of the volatility stop is to add it to a trading system to signal potential trend reversals to catch a good buy opportunity.

ENTRY

- When the price crosses above the Volatility Stop

EXIT

- When the price crosses below the Volatility Stop

For this strategy, the Volatility stop's multiplier is set to 3 to allow more flexibility to the trade. The strategy is designed for medium-term trades.

Based on the backtest result from a sample of crypto trading pairs, the most profitable time frame is the 2-hr.

The strategy works well with both crypto-to-crypto and crypto-to-fiat pairs. To make results more realistic, a trading fee of 0.1% is added to the script. The fee is aligned to the base fee applied on Binance.

Swing/Scalper HULL + T3 avg Crypto StrategyThis is a both a swing and a scalper strategy(depends on the timeframe that you use), that works with all timeframes, however I noticed that with swing 3h works the best on most crypto pairs, such as ETH, BTC and so on.

Its main components are:

Hull moving average

T3 moving average

Risk management

With them I make an average and use it as the main moving average.

Rules for entry

For long: Average moving average is bigger than previous average moving average value.

For short:Average moving average is lower than previous average moving average value.

Rules for exit

We exit when either the TP/SL has been hit, or when we get a different condition than previous one(both for long and short).

If you have any questions, let me know !

Donchian Channel StrategyRide the trend with full potential. Filter out false signals using long period ema. Lower bands take care of the stop loss.

Use this strategy for banknifty futures for consistent quarterly returns.

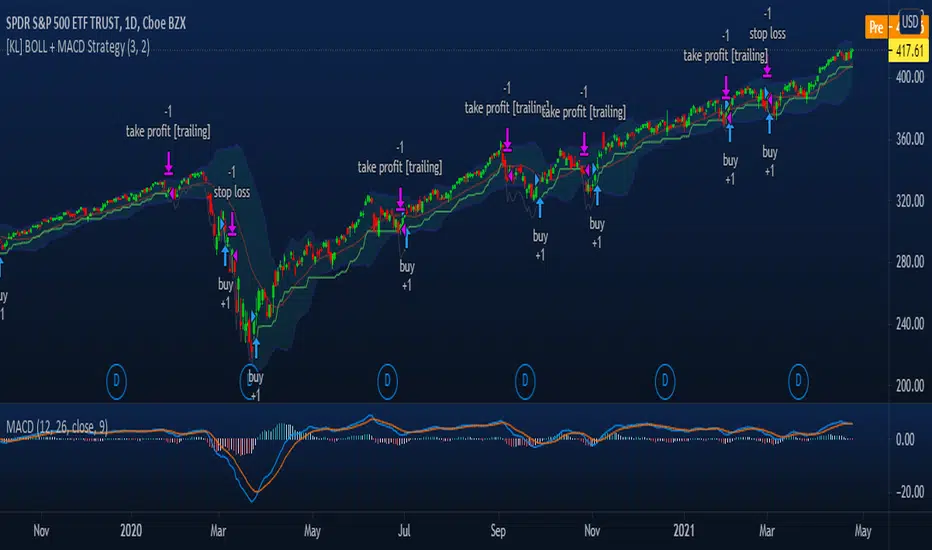

[KL] BOLL + MACD Strategy v2 (published)This strategy will look for opportunities when price touches the lower Bollinger band, then enters Long when it anticipates a MACD crossover signal.

Setup: on 1-day chart interval

Exits when either (a) hitting trailing stop loss, or (b) meeting risk-to-reward, if defined by user.

RSI Classic Strategy (by Coinrule)One of the questions hobbyist traders more often ask is: what is the perfect trading indicator?

Every indicator is just a tool, so its efficiency is proportional to your ability to read its signals and translate them into an actionable trading strategy. The RSI is likely the most flexible and easy to use among the technical indicators.

This trading strategy tries to catch short-term swings on the coins of your choice with a simple yet profitable setup.

Buy when the RSI is lower than 30 (you can adjust it to 35 in times of steep uptrend).

Sell when the RSI is greater than 65 (the target may range between 60 and 75 depending on the volatility of the coin).

Note that the buy signal comes when the indicator crosses below 30 and not when it crosses above 30 as it happens on the built-in RSI strategy on Tradingview.

The present script overperforms the built-in strategy, even adding trading fees and using a lower amount of capital for each trade (30%). That means that the system can deliver higher net-profits with lower risk levels.

A typical example of market conditions where this strategy works perfectly is as follows.

The first initial breakout indicates that a new leg up in the trend may start. Bitcoin starts to trade within a range which you can identify when it reaches the point 3. That is the perfect time to start the rule because

- trading within a channel anticipates possible swings up and down

- the trend is on the upside, providing low downside risk in buying the dips.

This strategy works well with selected coins of your choice, and it's a great fit on leverage exchanges like Binance Futures.

If you prefer to run it across all available coins on the market, instead, you may choose an optimized version.

Ichimoku Strategy [CDI]Strategy used in the CDI community that consists of having as a signal to enter long when it crosses the entire Ichimoku cloud .

It is recommended to use the strategy in one hour candles and the profit / loss ratio is 2 to 1 for swing trading, however it can be used at any time frame.

The purpose is to perform a bakctesting quickly by setting the limit and stop in the study settings (Proffit and Loss). It is also possible to deactivate the trades on chart changing the configuration in the settings pannel to visualize more clearly the yellow candles that are marked on the chart to identify the signal of the strategy.

Strategy settings:

- Profit %: approximate profit on each entry

- Loss %: approximate loss limit in each entry

- Crossing Candles: number of candles that establishes the crossing of the Ichimoku clouds

Alerts can be configured.

For more information about the strategy, you can search on YouTube for Hyenuk Chu's video "Cómo construir una buena tasa Riesgo Beneficio"

WARNING:

- For purpose educate only

- The entries are used under your responsibility

Crypto MultiTrend multi timeframesHello, today I bring you another crypto strategy which can work with multiple timeframes and most of crypto currencies

Its made entirelly of multiple EMA , of different lengths : like super fast, fast, normal, slow and very slow

We also combine a little bit of price action together with the trend direction both for entry and for exits, to have a more precise control.

The rules for long close is above all EMA's, they are in ascending order and the at same time close is bigger than the previous high, and previous high > second previous high, close > 3rd previous high , close > 4th previous high, close > 5th previous high, 5th high > 6th high.

For short we have the same, but instead of high, we use lows, and instead of > we use < .

As exit we have 2 conditions for long and 2 for short

To exit long we have : super fast ema < fast ema and fast ema < normal and normal < slow ema. For short, they would be the opposite, using > sign.

The second exit for long is when our current low crosses below 4 of ours EMA during the same candle. For short, is when the high crosses above 4 of ours EMA during the same candle.

CAUTIOUS : Currently it uses not risk management system, so in this current condition is extremely risky . Be careful

If you have any questions lets me know

Price action strategy FOREX with amazing results

Hello, today I bring another amazing strategy for forex .

Its made of T3 moving average , combined together with a pattern rule and a specific entry time.

We take all of that and we trade it in inverse.

So what normally for long would be : close higher than the previos high and close higher than the average, we use this as a short condition. We do the same stuff for long condition.

So in the end we end up with an amazing product.

It also has a risk management inside, with a TP/SL based on % move of the price .

Let me know how it goes .

Forex SWING TraderThis strategy is mainly designed for swing trading applied to FOREX.

In this case we make use of 2 moving averages but with different time frame, lets say 1h and 1 day.

When they cross above we would initially have a long trade, but in this strategy we trade it in reverse, so we would actually enter a short position.

The same for short trade.

At the same time we make use of hours for entry, so we can filter even better between the trades, and select the best possible hours for entries.

For exit we have 2 conditions : one is when we receive an opposite signal ( by default ).

The other is when a certain movement between moving averages, like lets say 1% of price movement, we will exit. This can act both as TP and SL.

Parabolic SAR Swing strategy GBP JPY Daily timeframeToday I bring you a new strategy thats made of parabolic sar. It has optmized values for GBPJPY Daily timeframe chart.

It also has a time period selection, in order to see how it behave between selected years.

The strategy behind it is simple :

We have an uptrend , (the psar is below our candles) we go long. We exit when our candle crosses the psar value.

The same applies for downtrend(the psar is above our candles), where we go short. We exit when our candle cross the psar value.

Among the basic indicators, it looks like PSAR is one of the best canditates for swing trading.

If you have any questions, please let me know.

Bollinger %B Candles StrategyStrategy built based on earlier published indicator:

Looks to be doing good for short term swing trades. But, I am not sure if there is repainting. I tried to avoid buy/sell trades on same day - but wasn't successful.

So far back-tested on following:

COINBASE:BTCUSD - works on both long and short

CURRENCYCOM:GOLD and equities - long only.

Some of the failures: ASX:WPL , ASX:WHC , ASX:NHC

As usual for back-testing - using 1000 as initial capital with 100% invested on each trade and no compounding so that it will be easy to compare with buy and hold. Trade with caution :)

2HLA very simple, almost naive strategy, in which you buy on the lowest of the two previous candles and sell at the highest of the two previous candles. You can configure these highest and lowest lenght, in some assets two is too small of a number to make profit. You can also configure to exit the position after X, and I found that 7 (which is a week of working days) is a good number for that.

This is strategy is intended to be used as a swing trade. Your capital needs to be high enough so that it can pay the operaitonal costs, and reach it's target with a reasonable profit.

Since this is a volatility based strategy, assets that are more liquid won't work properly.