Seasonal Strategies V1Seasonal Strategies V1 is a rule-based futures seasonality framework built around predefined calendar windows per asset.

The strategy automatically detects the current symbol and activates long or short trading phases strictly based on historically observed seasonal tendencies. All entries and exits are fully time-based — no indicators, no predictions, no discretionary input.

Key Features

Asset-specific seasonal windows (MMDD-based)

Automatic long and short activation

Fully time-based entries and exits

One position at a time (no pyramiding)

Clean chart visualization using subtle background shading

No indicators, no filters, no curve fitting

Philosophy:

This strategy is designed as a structural trading tool, not a forecasting model.

It focuses on when a market historically shows seasonal tendencies — not why or how far price might move.

Seasonal Strategies V1 intentionally keeps the chart clean and minimal, making it suitable as a baseline framework for research, portfolio-style seasonal approaches, or further extensions in later versions.

Intended Use:

Futures and commodity markets

Seasonality research and testing

Systematic, calendar-driven strategies

Educational and analytical purposes

Disclaimer

This script is provided for educational and research purposes only.

Past seasonal tendencies do not guarantee future performance.

Risk management, position sizing, and portfolio decisions are the responsibility of the user.

Statistics

ETH Trading bot H1 Money maker i dont know what i did but it is looking good ; make sure you arent in a trade before you start the bot

Xbirch_Turtle_ Crypto_CalcМодернизированная стратегия Черепах.

Вход/выход по каналу Дончиана, стопы по величине ATR, возможность выбора лонг/шорт/всё. Имеется пирамидинг - добавление по +0,5ATR от первого бая, не более 4х входов. Модернизированный стоп - по ATR от первого бая.

Не финансовый совет.

A modernized Turtle strategy.

Entry/exit based on the Donchian Channel, stops based on the ATR value, and the ability to choose long/short/all options. Pyramiding is available – adding +0.5 ATR from the first buy, with a maximum of four entries. The modernized stop is based on the ATR value from the first buy.

This is not financial advice.

NQ Lunch High Low First Sweep StrategyThis script identifies the FIRST liquidity sweep of the Lunch session high or low

after the Lunch session has ended, based on ICT / Killzone concepts.

Logic summary:

• Tracks Lunch session High and Low (New York time)

• After Lunch session closes, monitors the market on 5-minute timeframe

• Triggers ONLY on the first sweep:

– Price wicks beyond Lunch High and closes back below → SHORT signal

– Price wicks beyond Lunch Low and closes back above → LONG signal

• Generates an alert at the exact bar where entry is expected

• Designed specifically for Nasdaq (NQ) futures

• One trade per day – no overtrading

Notes:

• Intended for 5-minute charts only

• Uses New York session timing

• This script does NOT manage exits (TP/SL) – entry logic only

• Best used as a confluence tool, not a standalone system

Educational & discretionary use only.

Improved Candle Strategy (without daily squared)# Candle Pattern Trading Strategy

## Core Logic

Analyzes the last 5 candlesticks to identify "close at high" and "close at low" patterns, generating long/short signals.

## Trading Conditions

- **Long**: ≥2 bars closed at high in past 5 bars + current bar closes at high → Open long

- **Short**: ≥2 bars closed at low in past 5 bars + current bar closes at low → Open short

- **Filter**: If ≥3 doji patterns detected, skip trading

## Risk Management

- Stop Loss: Based on entry bar's high/low

- Take Profit: Risk × 2x multiplier

- Cooldown: No trading for 2 bars after entry

- Session Filter: No trading for first 5 bars after market open

## Configurable Parameters

- Lookback period, doji threshold, close proximity ratio, TP/SL ratio, cooldown bars, etc.

**Use Cases**: 1-minute and higher timeframes on stocks/futures

Simple Candle Strategy# Candle Pattern Strategy - Pine Script V6

## Overview

A TradingView trading strategy script (Pine Script V6) that identifies candlestick patterns over a configurable lookback period and generates trading signals based on pattern recognition rules.

## Strategy Logic

The strategy analyzes the most recent N candlesticks (default: 5) and classifies their patterns into three categories, then generates buy/sell signals based on specific pattern combinations.

### Candlestick Pattern Classification

Each candlestick is classified as one of three types:

| Pattern | Definition | Formula |

|---------|-----------|---------|

| **Close at High** | Close price near the highest price of the candle | `(high - close) / (high - low) ≤ (1 - threshold)` |

| **Close at Low** | Close price near the lowest price of the candle | `(close - low) / (high - low) ≤ (1 - threshold)` |

| **Doji** | Opening and closing prices very close; long upper/lower wicks | `abs(close - open) / (high - low) ≤ threshold` |

### Trading Rules

| Condition | Action | Signal |

|-----------|--------|--------|

| Number of Doji candles ≥ 3 | **SKIP** - Market is too chaotic | No trade |

| "Close at High" count ≥ 2 + Last candle closes at high | **LONG** - Bullish confirmation | Buy Signal |

| "Close at Low" count ≥ 2 + Last candle closes at low | **SHORT** - Bearish confirmation | Sell Signal |

## Configuration Parameters

All parameters are adjustable in TradingView's "Settings/Inputs" tab:

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| **K-line Lookback Period** | 5 | 3-20 | Number of candlesticks to analyze |

| **Doji Threshold** | 0.1 | 0.0-1.0 | Body size / Total range ratio for doji identification |

| **Doji Count Limit** | 3 | 1-10 | Number of dojis that triggers skip signal |

| **Close at High Proximity** | 0.9 | 0.5-1.0 | Required proximity to highest price (0.9 = 90%) |

| **Close at Low Proximity** | 0.9 | 0.5-1.0 | Required proximity to lowest price (0.9 = 90%) |

### Parameter Tuning Guide

#### Proximity Thresholds (Close at High/Low)

- **0.95 or higher**: Stricter - only very strong candles qualify

- **0.90 (default)**: Balanced - good for most market conditions

- **0.80 or lower**: Looser - catches more patterns, higher false signals

#### Doji Threshold

- **0.05-0.10**: Strict doji identification

- **0.10-0.15**: Standard doji detection

- **0.15+**: Includes near-doji patterns

#### Lookback Period

- **3-5 bars**: Fast, sensitive to recent patterns

- **5-10 bars**: Balanced approach

- **10-20 bars**: Slower, filters out noise

## Visual Indicators

### Chart Markers

- **Green Up Arrow** ▲: Long entry signal triggered

- **Red Down Arrow** ▼: Short entry signal triggered

- **Gray X**: Skip signal (too many dojis detected)

### Statistics Table

Located at top-right corner, displays real-time pattern counts:

- **Close at High**: Count of candles closing near the high

- **Close at Low**: Count of candles closing near the low

- **Doji**: Count of doji/near-doji patterns

### Signal Labels

- Green label: "✓ Long condition met" - below entry bar

- Red label: "✓ Short condition met" - above entry bar

- Gray label: "⊠ Too many dojis, skip" - trade skipped

## Risk Management

### Exit Strategy

The strategy includes built-in exit rules based on ATR (Average True Range):

- **Stop Loss**: ATR × 2

- **Take Profit**: ATR × 3

Example: If ATR is $10, stop loss is at -$20 and take profit is at +$30

### Position Sizing

Default: 100% of equity per trade (adjustable in strategy properties)

**Recommendation**: Reduce to 10-25% of equity for safer capital allocation

## How to Use

### 1. Copy the Script

1. Open TradingView

2. Go to Pine Script Editor

3. Create a new indicator

4. Copy the entire `candle_pattern_strategy.pine` content

5. Click "Add to Chart"

### 2. Apply to Chart

- Select your preferred timeframe (1m, 5m, 15m, 1h, 4h, 1d)

- Choose a trading symbol (stocks, forex, crypto, etc.)

- The strategy will generate signals on all historical bars and in real-time

### 3. Configure Parameters

1. Right-click the strategy on chart → "Settings"

2. Adjust parameters in the "Inputs" tab

3. Strategy will recalculate automatically

4. Backtest results appear in the Strategy Tester panel

### 4. Backtesting

1. Click "Strategy Tester" (bottom panel)

2. Set date range for historical testing

3. Review performance metrics:

- Win rate

- Profit factor

- Drawdown

- Total returns

## Key Features

✅ **Execution Model Compliant** - Follows official Pine Script V6 standards

✅ **Global Scope** - All historical references in global scope for consistency

✅ **Adjustable Sensitivity** - Fine-tune all pattern detection thresholds

✅ **Real-time Updates** - Works on both historical and real-time bars

✅ **Visual Feedback** - Clear signals with labels and statistics table

✅ **Risk Management** - Built-in ATR-based stop loss and take profit

✅ **No Repainting** - Signals remain consistent after bar closes

## Important Notes

### Before Trading Live

1. **Backtest thoroughly**: Test on at least 6-12 months of historical data

2. **Paper trading first**: Practice with simulated trades

3. **Optimize parameters**: Find the best settings for your trading instrument

4. **Manage risk**: Never risk more than 1-2% per trade

5. **Monitor performance**: Review trades regularly and adjust as needed

### Market Conditions

The strategy works best in:

- Trending markets with clear directional bias

- Range-bound markets with defined support/resistance

- Markets with moderate volatility

The strategy may underperform in:

- Highly choppy/noisy markets (many false signals)

- Markets with gaps or overnight gaps

- Low liquidity periods

### Limitations

- Works on chart timeframes only (not intrabar analysis)

- Requires at least 5 bars of history (configurable)

- Fixed exit rules may not suit all trading styles

- No trend filtering (will trade both directions)

## Technical Details

### Historical Buffer Management

The strategy declares maximum bars back to ensure enough historical data:

```pine

max_bars_back(close, 20)

max_bars_back(open, 20)

max_bars_back(high, 20)

max_bars_back(low, 20)

```

This prevents runtime errors when accessing historical candlestick data.

### Pattern Detection Algorithm

```

For each bar in lookback period:

1. Calculate (high - close) / (high - low) → close_to_high_ratio

2. If close_to_high_ratio ≤ (1 - threshold) → count as "Close at High"

3. Calculate (close - low) / (high - low) → close_to_low_ratio

4. If close_to_low_ratio ≤ (1 - threshold) → count as "Close at Low"

5. Calculate abs(close - open) / (high - low) → body_ratio

6. If body_ratio ≤ doji_threshold → count as "Doji"

Signal Generation:

7. If doji_count ≥ cross_count_limit → SKIP_SIGNAL

8. If close_at_high_count ≥ 2 AND last_close_at_high → LONG_SIGNAL

9. If close_at_low_count ≥ 2 AND last_close_at_low → SHORT_SIGNAL

```

## Example Scenarios

### Scenario 1: Bullish Signal

```

Last 5 bars pattern:

Bar 1: Closes at high (95%) ✓

Bar 2: Closes at high (92%) ✓

Bar 3: Closes at mid (50%)

Bar 4: Closes at low (10%)

Bar 5: Closes at high (96%) ✓ (last bar)

Result:

- Close at high count: 3 (≥ 2) ✓

- Last closes at high: ✓

- Doji count: 0 (< 3) ✓

→ LONG SIGNAL ✓

```

### Scenario 2: Skip Signal

```

Last 5 bars pattern:

Bar 1: Doji pattern ✓

Bar 2: Doji pattern ✓

Bar 3: Closes at mid

Bar 4: Doji pattern ✓

Bar 5: Closes at high

Result:

- Doji count: 3 (≥ 3)

→ SKIP SIGNAL - Market too chaotic

```

## Performance Optimization

### Tips for Better Results

1. **Use Higher Timeframes**: 15m or higher reduces false signals

2. **Combine with Indicators**: Add volume or trend filters

3. **Seasonal Adjustment**: Different parameters for different seasons

4. **Instrument Selection**: Test on liquid, high-volume instruments

5. **Regular Rebalancing**: Adjust parameters quarterly based on performance

## Troubleshooting

### No Signals Generated

- Check if lookback period is too large

- Verify proximity thresholds aren't too strict (try 0.85 instead of 0.95)

- Ensure doji limit allows for trading (try 4-5 instead of 3)

### Too Many False Signals

- Increase proximity thresholds to 0.95+

- Reduce lookback period to 3-4 bars

- Increase doji limit to 3-4

- Test on higher timeframes

### Strategy Tester Shows Losses

- Review individual trades to identify patterns

- Adjust stop loss and take profit ratios

- Change lookback period and thresholds

- Test on different market conditions

## References

- (www.tradingview.com)

- (www.tradingview.com)

- (www.investopedia.com)

- (www.investopedia.com)

## Disclaimer

**This strategy is provided for educational and research purposes only.**

- Not financial advice

- Past performance does not guarantee future results

- Always conduct thorough backtesting before live trading

- Trading involves significant risk of loss

- Use proper risk management and position sizing

## License

Created: December 15, 2025

Version: 1.0

---

**For updates and modifications, refer to the accompanying documentation files.**

Mutanabby_AI | ONEUSDT_MR1

ONEUSDT Mean-Reversion Strategy | 74.68% Win Rate | 417% Net Profit

This is a long-only mean-reversion strategy designed specifically for ONEUSDT on the 1-hour timeframe. The core logic identifies oversold conditions following sharp declines and enters positions when selling pressure exhausts, capturing the subsequent recovery bounce.

Backtested Period: June 2019 – December 2025 (~6 years)

Performance Summary

| Metric | Value |

|--------|-------|

| Net Profit | +417.68% |

| Win Rate | 74.68% |

| Profit Factor | 4.019 |

| Total Trades | 237 |

| Sharpe Ratio | 0.364 |

| Sortino Ratio | 1.917 |

| Max Drawdown | 51.08% |

| Avg Win | +3.14% |

| Avg Loss | -2.30% |

| Buy & Hold Return | -80.44% |

Strategy Logic :

Entry Conditions (Long Only):

The strategy seeks confluence of three conditions that identify exhausted selling:

1. Prior Move Filter:*The price change from 5 bars ago to 3 bars ago must be ≥ -7% (ensures we're not entering during freefall)

2. Current Move Filter: The price change over the last 2 bars must be ≤ 0% (confirms momentum is stalling or reversing)

3. Three-Bar Decline: The price change from 5 bars ago to 3 bars ago must be ≤ -5% (confirms a significant recent drop occurred)

When all three conditions align, the strategy identifies a potential reversal point where sellers are exhausted.

Exit Conditions:

- Primary Exit: Close above the previous bar's high while the open of the previous bar is at or below the close from 9 bars ago (profit-taking on strength)

- Trailing Stop: 11x ATR trailing stop that locks in profits as price rises

Risk Management

- Position Sizing:Fixed position based on account equity divided by entry price

- Trailing Stop:11× ATR (14-period) provides wide enough room for crypto volatility while protecting gains

- Pyramiding:Up to 4 orders allowed (can scale into winning positions)

- **Commission:** 0.1% per trade (realistic exchange fees included)

Important Disclaimers

⚠️ This is NOT financial advice.

- Past performance does not guarantee future results

- Backtest results may contain look-ahead bias or curve-fitting

- Real trading involves slippage, liquidity issues, and execution delays

- This strategy is optimized for ONEUSDT specifically — results may differ on other pairs

- Always test before risking real capital

Recommended Usage

- Timeframe:*1H (as designed)

- Pair: ONEUSDT (Binance)

- Account Size: Ensure sufficient capital to survive max drawdown

Source Code

Feedback Welcome

I'm sharing this strategy freely for educational purposes. Please:

- Drop a comment with your backtesting results any you analysis

- Share any modifications that improve performance

- Let me know if you spot any issues in the logic

Happy trading

As a quant trader, do you think this strategy will survive in live trading?

Yes or No? And why?

I want to hear from you guys

EMA + Sessions + RSI Strategy v1.0A professional trading strategy that combines multiple technical indicators for high-probability entries. This system uses EMA crossovers, RSI zone filtering, and trend confirmation to identify optimal trading opportunities while managing risk with advanced position management tools.

Key Features:

✅ Dual Entry Signals (EMA21 + EMA100 crossover conditions)

✅ Trend Filter EMA750 (trade only with the major trend)

✅ Complete Risk Management (SL 1%, TP 3% default)

✅ Trailing Stop & Breakeven (maximize profits, protect capital)

✅ Compact Statistics Table (real-time performance metrics)

✅ RSI & Session Filters (avoid low-probability setups)

✅ Optional Pyramiding (scale into winning positions)

Perfect for swing trading and trend-following on any timeframe. Fully customizable to match your trading style.

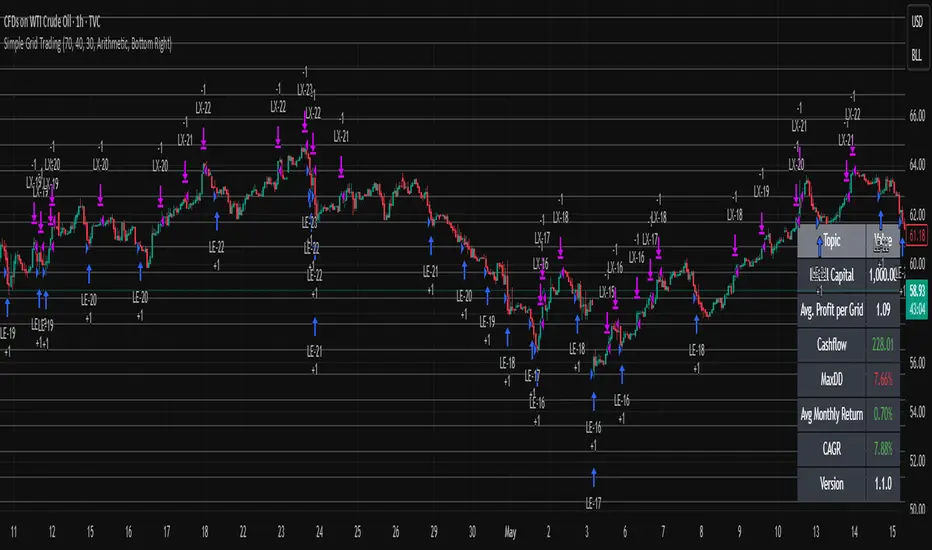

Simple Grid Trading v1.0 [PUCHON]Simple Grid Trading v1.0

Overview

This is a Long-Only Grid Trading Strategy developed in Pine Script v6 for TradingView. It is designed to profit from market volatility by placing a series of Buy Limit orders at predefined price levels. As the price drops, the strategy accumulates positions. As the price rises, it sells these positions at a profit.

Features

Grid Types : Supports both Arithmetic (equal price spacing) and Geometric (equal percentage spacing) grids.

Flexible Order Management : Uses strategy.order for precise control and prevents duplicate orders at the same level.

Performance Dashboard : A real-time table displaying key metrics like Capital, Cashflow, and Drawdown.

Advanced Metrics : Includes Max Drawdown (MaxDD) , Avg Monthly Return , and CAGR calculations.

Customizable : Fully adjustable price range, grid lines, and lot size.

Dashboard Metrics

The dashboard (default: Bottom Right) provides a quick snapshot of the strategy's performance:

Initial Capital : The starting capital defined in the strategy settings.

Lot Size : The fixed quantity of assets purchased per grid level.

Avg. Profit per Grid : The average realized profit for each closed trade.

Cashflow : The total realized net profit (closed trades only).

MaxDD : Maximum Drawdown . The largest percentage drop in equity (realized + unrealized) from a peak.

Avg Monthly Return : The average percentage return generated per month.

CAGR : Compound Annual Growth Rate . The mean annual growth rate of the investment over the specified time period.

Strategy Settings (Inputs)

Grid Settings

Upper Price : The highest price level for the grid.

Lower Price : The lowest price level for the grid.

Number of Grid Lines : The total number of levels (lines) in the grid.

Grid Type :

Arithmetic: Distance between lines is fixed in price terms (e.g., $10, $20, $30).

Geometric: Distance between lines is fixed in percentage terms (e.g., 1%, 2%, 3%).

Lot Size : The fixed amount of the asset to buy at each level.

Dashboard Settings

Show Dashboard : Toggle to hide/show the performance table.

Position : Choose where the dashboard appears on the chart (e.g., Bottom Right, Top Left).

How It Works

Initialization : On the first bar, the script calculates the price levels based on your Upper/Lower price and Grid Type.

Entry Logic :

The strategy places Buy Limit orders at every grid level below the current price.

It checks if a position already exists at a specific level to avoid "stacking" multiple orders on the same line.

Exit Logic :

For every Buy order, a corresponding Sell Limit (Take Profit) order is placed at the next higher grid level.

MaxDD Calculation :

The script continuously tracks the highest equity peak.

It calculates the drawdown on every bar (including intra-bar movements) to ensure accuracy.

Displayed as a percentage (e.g., 5.25%).

Disclaimer

This script is for educational and backtesting purposes only. Grid trading involves significant risk, especially in strong trending markets where the price may move outside your grid range. Always use proper risk management.

MTF Scalper - alemicihanMulti-Timeframe Scalper Strategy: Aligning the Big Picture for Quick Gains

This article presents a robust futures trading strategy designed for high-frequency scalping in the crypto market. It’s built on the principle of minimizing risk by ensuring that short-term entries are always aligned with the dominant, higher-timeframe trend.

The Core Concept: Alignment is Key

A Balanced Trend Follower approach, now refined for rapid scalping, uses a Multi-Timeframe (MTF) confirmation system to filter out market noise and increase the probability of a successful trade.

The strategy operates on a Low Timeframe (LTF) chart (e.g., 3m, 5m, or 15m) but only executes trades if the direction is validated by three Higher Timeframes (HTF).

ComponentPurposeFunctionHTF (D, 4h, 1h) EMA => Trend Confirmation =>Checks if the current price is above/below all three Exponential Moving Averages (EMA 20). This provides a strong directional bias.

LTF (5m) Stochastic RSI => Momentum Entry => Generates the actual buy/sell signal by spotting a swift crossover, indicating fresh momentum in the direction of the confirmed HTF trend.

How The Signal Is Generated

Trend Alignment: The system first confirms the trend. If the price is trading above the Daily, 4-Hour, and 1-Hour EMAs, the market is deemed to be in a Strong LONG Trend. Only LONG signals are permitted.

Momentum Trigger: Once the trend is confirmed, a Long Signal is generated only when the Stochastic K-Line crosses above the D-Line, indicating a momentum shift (a pullback ending) towards the main trend direction.

Short Signal: The inverse logic applies to the Short Trend confirmation and entry signal.

Mandatory Risk Management: ATR-Based Exit

Given the high leverage nature of futures and scalping, static Stop-Loss (SL) and Take-Profit (TP) levels are inefficient. This strategy uses the Average True Range (ATR) indicator to dynamically set profit and loss targets based on current market volatility.

Stop Loss (SL): Set dynamically at 1.5 x ATR below (for long) or above (for short) the entry price. This gives the trade enough room to breathe without risking excessive capital.

Take Profit (TP): Set dynamically at 3.0 x ATR, establishing a robust Risk-to-Reward Ratio of 1:2.

Final Thoughts on Testing

This sophisticated approach combines the reliability of MTF analysis with the speed of momentum indicators. However, data analysis is key. Backtesting these parameters (EMA, ATR Multipliers, RSI/Stochastic lengths) on your chosen asset (like BTC/USDT or ETH/USDT) and timeframe is crucial to achieving optimal performance.

HPAS mean reversion strategy testerTakes Krown HPAS values hardcoded and simulates longs and short with configurable standard deviation multiplier TP/SL. Best used on lower timeframes

Pivot Fib 4H — EAStrategy uses the pivot standard to open position, it has well define entry and exit point with SL, it also has a proper money management plan, maximum 4 trades a day, each trade risk 0.5% of the account, I have it EA version of it also.

Any Strategy BacktestA simple script for backtesting your strategies with TP and SL settings. For this to work, your indicators must have sources for long and short conditions.

Vandan V2Vandan V2 is an automated trading strategy for NQ1! (E-mini Nasdaq-100) based on short-term mean reversion with dynamic risk control. It combines volatility filters and overbought/oversold signals to capture local market imbalances.

Backtested from 2015 to 2025, it achieved a +730% total return, Profit Factor of 1.40, max drawdown of only 1.61%, and over 106,000 trades. Designed for systematic scalping or intraday arbitrage with a limit of 3 simultaneous contracts.

Vandan V2Vandan V2 is an automated trend-following strategy for NASDAQ E-mini Futures (NQ1!).

It uses multi-timeframe momentum and volatility filters to identify high-probability entries.

Includes dynamic risk management and trailing logic optimized for intraday trading.

Master Trend Strategy - by jake_thebossMaster Trend Strategy

This strategy combines multiple technical indicators to identify high-probability trend entries across all asset classes.

Core Signal Logic:

Entry triggered when EMA 4 crosses above/below EMA 5

Confirmation required from RSI (>50 for long, <50 for short)

Price must be above/below key moving averages: EMA 21, SMA 50, EMA 55, EMA 89, and EMA 750

Additional confirmation from Stochastic (>52 bullish, <48 bearish) or EMA 89 breakout or VWAP cross

Key Features:

VWAP filter: Only takes bullish signals above VWAP and bearish signals below VWAP

Optional pyramiding: Allows multiple entries in the same direction (up to 200 orders)

Individual stop loss and take profit management for each pyramid level

Time filter: Customizable trading hours with timezone offset

Risk management: Adjustable stop loss (default 0.3%) and take profit (default 0.6%)

Visualization:

Entry, stop loss, and take profit levels drawn as horizontal lines

Customizable signal markers (triangles) for bull/bear entries

Optional EMA overlay display

The strategy is designed for trend-following on lower timeframes, with strict multi-indicator confirmation to filter out false signals.

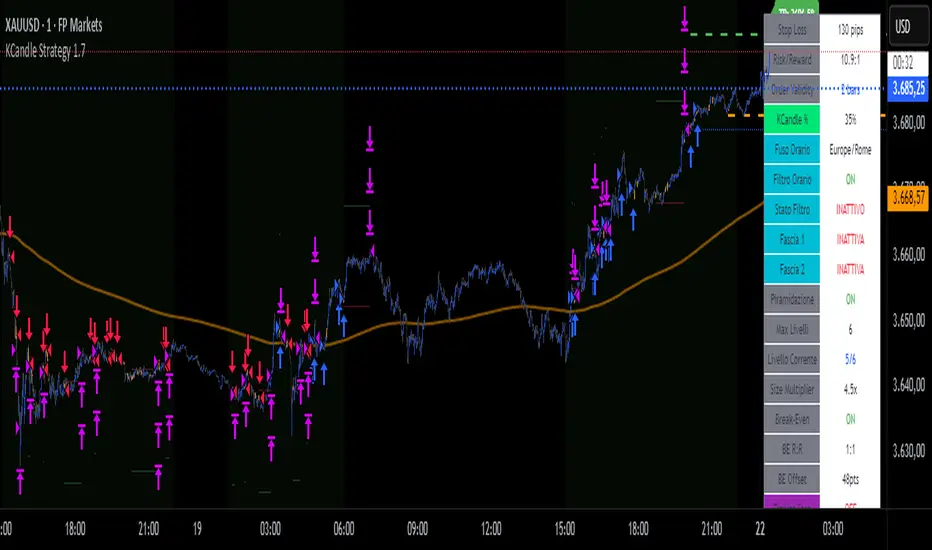

KCandle Strategy 1.0# KCandle Strategy 1.0 - Trading Strategy Description

## Overview

The **KCandle Strategy** is an advanced Pine Script trading system based on bullish and bearish engulfing candlestick patterns, enhanced with sophisticated risk management and position optimization features.

## Core Logic

### Entry Signal Generation

- **Pattern Recognition**: Detects bullish and bearish engulfing candlestick formations

- **EMA Filter**: Uses a customizable EMA (default 25) to filter trades in the direction of the trend

- **Entry Levels**:

- **Long entries** at 25% of the candlestick range from the low

- **Short entries** at 75% of the candlestick range from the low

- **Signal Validation**: Orange candlesticks indicate valid setup conditions

### Risk Management System

#### 1. **Stop Loss & Take Profit**

- Configurable stop loss in pips

- Risk-reward ratio setting (default 2:1)

- Visual representation with colored lines and labels

#### 2. **Break-Even Management**

- Automatically moves stop loss to break-even when specified R:R is reached

- Customizable break-even offset for added protection

- Prevents losing trades after reaching profitability

#### 3. **Trailing Stop System**

- **Activation Trigger**: Activates when position reaches specified R:R level

- **Distance Control**: Maintains trailing stop at defined distance from entry

- **Step Management**: Moves stop loss forward in incremental R steps

- **Dynamic Protection**: Locks in profits while allowing for continued upside

### Advanced Features

#### Position Management

- **Pyramiding Support**: Optional multiple position entries with size reduction

- **Order Expiration**: Pending orders automatically cancel after specified bars

- **Position Sizing**: Percentage-based allocation with pyramid level adjustments

#### Visual Interface

- **Real-time Monitoring**: Comprehensive information panel with all strategy metrics

- **Historical Tracking**: Visual representation of past trades and levels

- **Color-coded Indicators**: Different colors for break-even, trailing, and standard stops

- **Debug Options**: Optional labels for troubleshooting and optimization

## Key Parameters

### Basic Settings

- **EMA Length**: Trend filter period

- **Stop Loss**: Risk per trade in pips

- **Risk/Reward**: Target profit ratio

- **Order Validity**: Duration of pending orders

### Risk Management

- **Break-Even R:R**: Profit level to trigger break-even

- **Trailing Activation**: R:R level to start trailing

- **Trailing Distance**: Stop distance from entry when trailing

- **Trailing Step**: Increment for stop loss advancement

## Strategy Benefits

1. **Objective Entry Signals**: Based on proven candlestick patterns

2. **Trend Alignment**: EMA filter ensures trades align with market direction

3. **Robust Risk Control**: Multiple layers of protection (SL, BE, Trailing)

4. **Profit Optimization**: Trailing stops maximize winning trade potential

5. **Flexibility**: Extensive customization options for different market conditions

6. **Visual Clarity**: Complete visual feedback for trade management

## Ideal Use Cases

- **Swing Trading**: Medium-term positions with trend-following approach

- **Breakout Trading**: Capturing momentum from engulfing patterns

- **Risk-Conscious Trading**: Suitable for traders prioritizing capital preservation

- **Multi-Timeframe**: Adaptable to various timeframes and instruments

---

*The KCandle Strategy combines traditional technical analysis with modern risk management techniques, providing traders with a comprehensive tool for systematic market participation.*

Supertrend [TradingConToto]Supertrend — ADX/DI + EMA Gap + Breakout (with Mobile UI)

What makes it original

Supertrend combines trend strength (ADX/DI), multi-timeframe bias (EMA63 and EMA 200D equivalent), a structural filter based on the distance between EMA2400 and EMA4800 expressed in ATR units, and a momentum confirmation through a previous high breakout.

This is not a random mashup — it’s a sequence of filters designed to reduce trades in ranging markets and prioritize mature trends:

Direction: +DI > -DI (trend led by buyers).

Strength: ADX > mean(ADX) (avoids weak, choppy phases).

Short-term bias: Close > EMA63.

Long-term bias: Close > EMA4800 ≈ EMA200 daily on H1.

Momentum: Close > High (immediate breakout).

Structure: (EMA2400 − EMA4800) > k·ATR (ensures separation in ATR units, filters out flat phases).

Entries & exits

Entry: when all six conditions are met and no open position exists.

Exit: if +DI < -DI or Close < EMA63.

Visuals: EMA63 is painted green while in position and red otherwise, with a supertrend-style band; “BUY” labels appear below the green band and “SELL” labels above the red band.

UI: includes a compact table (mobile-friendly) showing the state of each condition.

Default parameters used in this publication

Initial capital: 10,000

Position size: 10% of equity (≤10% per trade is considered sustainable).

Commission: 0.01% per side (adjust to your broker/market).

Slippage: 1 tick

Pyramiding: 0 (only one position at a time)

Adjust commission/slippage to match your market. For US equities, commissions are often per share; for spot crypto, 0.10–0.20% total is common. I publish with 0.01% per side as a conservative example to avoid overestimating results.

Recommended backtest dataset

Timeframe: H1

Multi-cycle window (e.g. 2015–today)

Symbols with high liquidity (e.g. NASDAQ-100 large caps, or BTC/ETH spot) to generate 100+ trades. Avoid cherry-picked short windows.

Why each filter matters

+DI > -DI + ADX > mean: reduce counter-trend trades and weak signals.

Close > EMA63 + Close > EMA4800: enforce trend alignment in short and long horizons.

Breakout High : requires immediate momentum, avoids early entries.

EMA gap in ATR units: blocks flat or compressed structures where EMA200D aligns with price.

Limitations

The breakout filter may skip healthy pullbacks; the design prioritizes continuation over perfect entry price.

No fixed trailing stop/TP; exits depend on trend degradation via DI/EMA63.

Results vary with real costs (commissions, slippage, funding). Adjust defaults to your broker.

How to use

Apply it on a clean chart (no other indicators when publishing).

Keep in mind the default parameters above; if you change them, mention it in your notes and use the same values in the Strategy Tester.

Ensure your dataset produces 100+ trades for statistical validity.

Lunar calendar day Crypto Trading StrategyLunar calendar day Crypto Trading Strategy

This strategy explores the potential impact of the lunar calendar on cryptocurrency price cycles.

It implements a simple but unconventional rule:

Buy on the 5th day of each lunar month

Sell on the 26th day of the lunar month

No trades between January 1 (solar) and Lunar New Year’s Day (holiday buffer period)

Research background

Several academic studies have investigated the influence of lunar cycles on financial markets. Their findings suggest:

Returns tend to be higher around the full moon compared to the new moon.

Periods between the full moon and the waning phase often show stronger average returns than the waxing phase.

This strategy combines those observations into a practical implementation by testing fixed entry (lunar day 5) and exit (lunar day 26) points, while excluding the transition period from solar New Year to Lunar New Year, effectively capturing mid-month lunar effects.

How it works

The script includes a custom lunar date calculation function, reconstructing lunar months and days for each year (2020–2026).

On lunar day 5, the strategy opens a long position with 100% of equity.

On lunar day 26, the strategy closes the position.

No trades are executed between Jan 1 and Lunar New Year’s Day.

All trades include:

Commission: 0.1%

Slippage: 3 ticks

Position sizing uses the entire equity (100%) for simplicity, but this is not recommended for live trading.

Why this is original

Unlike mashups of built-in indicators, this script:

Implements a full lunar calendar system inside Pine Script.

Translates academic findings on lunar effects into an applied backtest.

Adds a realistic trading filter (holiday gap) based on cultural/seasonal calendar rules.

Provides researchers and traders with a framework to explore non-traditional, time-based signals.

Notes

This is an experimental, research-oriented strategy, not financial advice.

Results are highly dependent on the chosen period (2020–2026).

Using 100% equity per trade is for simplification only and is not a viable money management practice.

The purpose is to investigate whether cyclical patterns linked to lunar time can provide any statistical edge in ETHUSDT.

Mutanabby_AI | ATR+ | Trend-Following StrategyThis document presents the Mutanabby_AI | ATR+ Pine Script strategy, a systematic approach designed for trend identification and risk-managed position entry in financial markets. The strategy is engineered for long-only positions and integrates volatility-adjusted components to enhance signal robustness and trade management.

Strategic Design and Methodological Basis

The Mutanabby_AI | ATR+ strategy is constructed upon a foundation of established technical analysis principles, with a focus on objective signal generation and realistic trade execution.

Heikin Ashi for Trend Filtering: The core price data is processed via Heikin Ashi (HA) methodology to mitigate transient market noise and accentuate underlying trend direction. The script offers three distinct HA calculation modes, allowing for comparative analysis and validation:

Manual Calculation: Provides a transparent and deterministic computation of HA values.

ticker.heikinashi(): Utilizes TradingView's built-in function, employing confirmed historical bars to prevent repainting artifacts.

Regular Candles: Allows for direct comparison with standard OHLC price action.

This multi-methodological approach to trend smoothing is critical for robust signal generation.

Adaptive ATR Trailing Stop: A key component is the Average True Range (ATR)-based trailing stop. ATR serves as a dynamic measure of market volatility. The strategy incorporates user-defined parameters (

Key Value and ATR Period) to calibrate the sensitivity of this trailing stop, enabling adaptation to varying market volatility regimes. This mechanism is designed to provide a dynamic exit point, preserving capital and locking in gains as a trend progresses.

EMA Crossover for Signal Generation: Entry and exit signals are derived from the interaction between the Heikin Ashi derived price source and an Exponential Moving Average (EMA). A crossover event between these two components is utilized to objectively identify shifts in momentum, signaling potential long entry or exit points.

Rigorous Stop Loss Implementation: A critical feature for risk mitigation, the strategy includes an optional stop loss. This stop loss can be configured as a percentage or fixed point deviation from the entry price. Importantly, stop loss execution is based on real market prices, not the synthetic Heikin Ashi values. This design choice ensures that risk management is grounded in actual market liquidity and price levels, providing a more accurate representation of potential drawdowns during backtesting and live operation.

Backtesting Protocol: The strategy is configured for realistic backtesting, employing fill_orders_on_standard_ohlc=true to simulate order execution at standard OHLC prices. A configurable Date Filter is included to define specific historical periods for performance evaluation.

Data Visualization and Metrics: The script provides on-chart visual overlays for buy/sell signals, the ATR trailing stop, and the stop loss level. An integrated information table displays real-time strategy parameters, current position status, trend direction, and key price levels, facilitating immediate quantitative assessment.

Applicability

The Mutanabby_AI | ATR+ strategy is particularly suited for:

Cryptocurrency Markets: The inherent volatility of assets such as #Bitcoin and #Ethereum makes the ATR-based trailing stop a relevant tool for dynamic risk management.

Systematic Trend Following: Individuals employing systematic methodologies for trend capture will find the objective signal generation and rule-based execution aligned with their approach.

Pine Script Developers and Quants: The transparent code structure and emphasis on realistic backtesting provide a valuable framework for further analysis, modification, and integration into broader quantitative models.

Automated Trading Systems: The clear, deterministic entry and exit conditions facilitate integration into automated trading environments.

Implementation and Evaluation

To evaluate the Mutanabby_AI | ATR+ strategy, apply the script to your chosen chart on TradingView. Adjust the input parameters (Key Value, ATR Period, Heikin Ashi Method, Stop Loss Settings) to observe performance across various asset classes and timeframes. Comprehensive backtesting is recommended to assess the strategy's historical performance characteristics, including profitability, drawdown, and risk-adjusted returns.

I'd love to hear your thoughts, feedback, and any optimizations you discover! Drop a comment below, give it a like if you find it useful, and share your results.