KillstatsBacktest and identify at what times/days the high/low were formed. The periods are shown on the graph along with detailed statistics.

Exemple with "days : 600" and "13h : top 12%" : we understand that over 600 days, in 12% of the cases we have formed the top of the day at 13h.

up to 1000+ days studied to find favorable reversal time slots: killstats! The data presented can sometimes be... surprising.

Increasing/decreasing the timeframe on chart = increase/decrease the studied period.

A period of 1000 days ( UT : h1) allows to have solid but not exact statistics.

A period of 30 days allows to have current statistics but too little sample to know if the data is relevant.

I recommend looking for intersections of killstats over several periods: If over 1000 days AND 30 days, 3pm was a time with a high probability of forming a top, it is interesting to look for short positions between 3pm and 4pm.

The data is displayed in the form of a diagram whose visual allows to identify effective time slots.

Caution. Timeframe: h1 maximum for the study of the day's high/low to be correct - and daily maximum for the study of the week's high/low.

Caution2. Match the timezone with the input (by default set to GMT+1). So if you are at GMT+2, you must put "2" in timezone.

I recommend using this as part of an aggressive high frequency scalping strategy to make the most of your trading session - with the aim of quickly moving to TP1/BE and leaving your winning position open.

Statistic

Strategy weekly results as numbers v1This script is based on an idea of monthly statistics that have been found across tradingview community scripts. This is an improved version with weekly results with the ability to define the size of every group (number of weeks within one group).

Initial setup of the strategy

1. Set the period to calculate the results between.

2. Set the statistic precision and group size.

3. Enable "Recalculate" → "On every tick" under the strategy "Properties" section.

The logic under the hood

1. Get the period between which to calculate the strategy.

2. Calculate the first day of the first week within the period.

3. Calculate the latest day of the latest week within the period.

4. Calculate the results of the selected period.

5. Group the values by the defined number of cells.

6. Calculate the summary of every group.

7. Render the table.

Please, be careful . To use this tool you will need to enable the "Recalculate" → "On every tick" option but it means that your strategy will be executed on every tick instead of bar close. It can cause unexpected results in your strategy behaviour.

[co.n.g.] ADR 5/10/14/20Average Daily Range (ADR) over 5/10/14/20 Days

What it is

One of the oldest measurements of price volatility that is being used in technical and statistical trading is the range of a specific period of past days to estimate probability of chances, risk and price movements, as seen f.e. in

Molodovsky, N. (1967). Building a Stock Market Measure—A Case Study. Financial Analysts Journal, 23:3, 43-46 , DOI: 10.2469/faj.v23.n3.43.

Problem

After having tried all available community scripts I've encountered various indifferences, especially since Pine v5.

First, the anchor period changed, when I've switched between regular and extended trading hours.

- This meant, that the anchor switched between the official open of the day and the first bar of a new day beginnig at 00:00 UTC (or the corresponding timezone).

Second, thus in some scripts also changed the calculated average range, including or excluding pre market and after hours.

And therefor third, in many cases the distance between open and ADR high/low was indiffferent, putting one closer and the other further away.

Why is that?

After having tried seven different modes of calulation - from ta. to array, it appeared that especially since Pine v5 the calulation is lagging when calling

the request.security function and is thus rendering the calculations indifferent.

Especially the open is lagging and plotting delayed, about 15 minutes on a M1-chart or about 45 minutes on a M15 chart, which made id difficult to spot open (test) drives

- as f.e. described in Dalton, J. F., Jones, E. T., & Dalton, R. B. (1990). Mind over markets: power trading with market generated information. 1st edition . Probus. -

and estimating extremely strong or weak open moves.

While switching between regular and extended intraday charts, the open was either calculated on the open as request of "D" (open of the regular session)

and "1440" (which means full intraday since 00:00 UTC or the corresponding timezone), leading to undesired anchoring.

After having tried about five different anchoring periods and comparing the adr to @TradingView 's stock screener, there was no proper calulation or plotting possible,

if not partially hardcoded (being the least desired, elegant or flexible method).

Visualizing the problem

As described in the picture:

@sherwind 's ADR is plotting entirely wrong! I couldn't even figure out (even the source is available) whre the problem is rooted.

@treypeng 's ADR is anchored properly, but unfortunately the calculation is wrong.

Originality

As evident in the attached picture - and you are able to compare this to @TradingView 's stock screener - in this script as well the ADR is calculated PROPERLY

as well as the anchoring is set PROPERLY within the first tick of the session.

As matter of fact, you don't have to examine different timeframes, charts or sessions simoultaneously to see the correct levels and

you're able to ease observations and focus on your trading.

Innovation

There is no innovative approach, as described above, simply because this statistical approach is around since the 1960's.

Considering coding, neither is, but it is properly calculated and anchored.

What this script does

Anchoring at the first tick of the new New York session

Plotting the actual - not the past nor future - average day range (gray lines in picture)

Plotting the actual - not the past nor future - 75% average day range ( silver lines in picture)

Vizualising ADR breakouts by colouring the backround green (long breakout) or read (short breakout)

Selection methods

Keeping it simple stupid, as of now:

Abiliy to chose between 5/10/14/20 days

Additional

Theory says, that we are staying within the ADR of 75% every day.

_

Alas, there are some exceptions.

If price is breaking out of the ADR, we are likely to move in this direction for the rest of the day.

If price has broken out of the ADR on the previous day, ist highly unlikely to expect another ADR breakout day,

which doesn't mean that there might not appear a strong or weak second day.

Notes

Designed for intraday stock trading of the U.S. market.

Best (and easiest) chances are to be spotted in special conditions.

//Cheers,

//Constantine

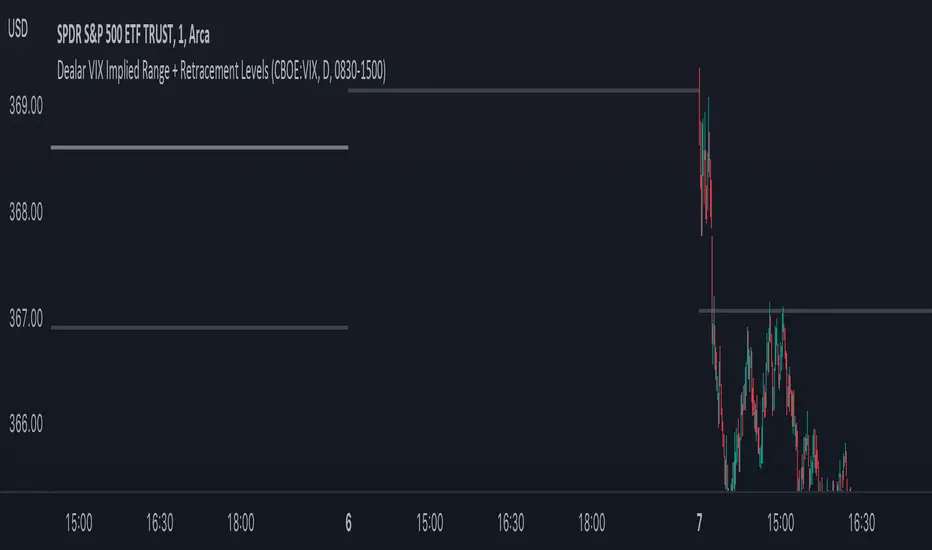

Dealar VIX Implied Range + Retracement LevelsThis Implied range Is derived by the VIX(1 sd annual +/- Implied move.)

This Indicator plots the daily Implied range, A lot of quantitative trading firms/ MM firms hedge their delta & gamma exposure around the Implied range(prop calc). I have added retracement levels as well, so you have more pivot levels.

Enjoy!

Full Volatility Statistics and Forecast

This is a tool designed to translate the data from the expected volatility of different assets, such as for example VIX, which measures the volatility of SP500 index.

Once get the data from the volatility asset we want to measure(for this test I have used VIX), we are going to translate it the required timeframe expected move by dividing the initial value into :

252 = if we want to use the daily timeframe, since there are ~252 aproximative daily trading days

52 = if we want to use the weekly timeframe, since there 52 trading weeks in a year

12 = if we want to use the monthly timeframe, since there are 12 months in a year

For this example I have used 252 with the daily timeframe.

In this scenario, we can see that we had 5711 total cnadles which we analysed, and in this case, we had 942 crosses, where the daily movement ended up either above or below the channel made from the opening daily candle value + expected movement from the volatility, giving as a total of 16.5% of occurances that volatility was higher than expected, and in 83.5% of the times, we can see that the price stayed within our channel.

At the same time, we can see that we had 6 max losses in a row ( OUT) AND 95 max wins in a row (IN), and at the same time in those moments when the volatility crosses happen we had a 0.51% avg movements when the top crossed happened, and 0.67% avg movements when the bot happened.

Lastly on the second part of the panel, we had E which means the expected movement of today, for example it has 61.056$ , so lets say price opened on 4083, our top is 4083 + 61 and our bot is 4083 - 61 ( giving us the daily channel). At continuation we can see that overall the avg bull candle os 0.714% and avg bear candle was 0.805% .

I hope this tool will help you with your future analysis and trades !

If you have any questions please let me know !

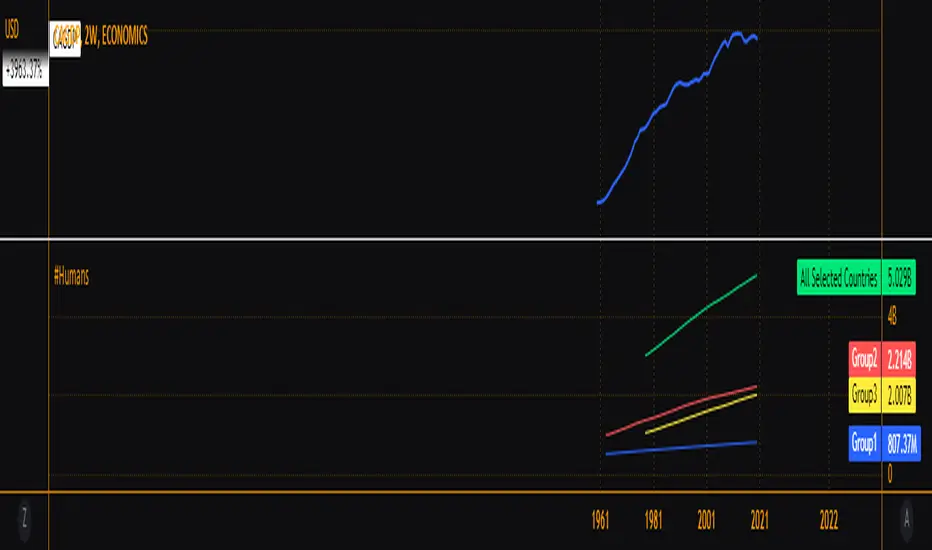

Relevant Populations GroupedUSPOP Same idea as my previous grouped GDP indicator but now population sizes. Goes to show how a small portion of the world is responsible for most of what we consider economic productivity.