Black-Scholes Model and Greeks for European OptionsThe Black-Scholes model is a mathematical model used for pricing options. From this model you can derive the theoretical fair value of a European option (an option where you have to wait until expiry to exercise). Additionally, you can derive various risk parameters called Greeks. This indicator includes three types of data: Theoretical Option Price (blue), the Greeks (green), and implied volatility (red); their values are presented in that order.

1) Theoretical Option Price:

This first value gives only the theoretical fair value of an option with a given strike based on the Black-Scholes framework. Remember this is a model and does not reflect actual option prices, just the theoretical price based on the Black-Scholes model and its parameters and assumptions.

2)Greeks (all of the Greeks included in this indicator are listed below):

a)Delta is the rate of change of the theoretical option price with respect to the change in the underlying's price. This can also be used to approximate the probability of your option expiring in the money. For example, if you have an option with a delta of 0.62, then it has about a 62% chance of expiring in-the-money. This number runs from 0 to 1 for Calls, and 0 to -1 for Puts.

b)Gamma is the rate of change of delta with respect to the change in the underlying's price.

c)Theta, aka "time decay", is the rate of change in the theoretical option price with respect to the change in time. Theta tells you how much an option will lose its value day by day.

d)Vega is the rate of change in the theoretical option price with respect to change in implied volatility.

e)Rho is the rate of change in the theoretical option price with respect to change in the risk-free rate. Rho is rarely used because it is the parameter that options are least effected by, it is more useful for longer term options, like LEAPs.

f)Vanna is the sensitivity of delta to changes in implied volatility. Vanna is useful for checking the effectiveness of delta-hedged and vega-hedged portfolios.

g)Charm, aka "delta decay", is the instantaneous rate of change of delta over time. Charm is useful for monitoring delta-hedged positions.

h)Vomma measures the sensitivity of vega to changes in implied volatility.

i)Veta measures the rate of change in vega with respect to time.

j)Vera measures the rate of change of rho with respect to implied volatility.

k)Speed measures the rate of change in gamma with respect to changes in the underlying's price. Speed can be used when evaluating delta-hedged and gamma hedged portfolios.

l)Zomma measures the rate of change in gamma with respect to changes in implied volatility. Zomma can be used to evaluate the effectiveness of a gamma-hedged portfolio.

m)Color, aka "gamma decay", measures the rate of change of gamma over time. This can also be used to evaluate the effectiveness of a gamma-hedged portfolio.

n)Ultima measures the rate of change in vomma with respect to implied volatility.

o)Probability of Touch, is not a Greek, but a metric that I included, which tells you the probability of price touching your strike price before expiry.

3) Implied Volatility:

This is the market's forecast of future volatility. Implied volatility is directionless, it cannot be used to forecast future direction. All it tells you is the forecast for future volatility.

How to use this indicator:

1st. Input the strike price of your option. If you input a strike that is more than 3 standard deviations away from the current price, the model will return a value of n/a.

2nd. Input the current risk-free rate.(Including this is optional, because the risk-free rate is so small, you can just leave this number at zero.)

3rd. Input the time until expiry. You can enter this in terms of days, hours, and minutes.

4th.Input the chart time frame you are using in terms of minutes. For example if you're using the 1min time frame input 1, 4 hr time frame input 480, daily time frame input 1440, etc.

5th. Pick what type of option you want data for, Long Call or Long Put.

6th. Finally, pick which Greek you want displayed from the drop-down list.

*Remember the Option price presented, and the Greeks presented, are theoretical in nature, and not based upon actual option prices. Also, remember the Black-Scholes model is just a model based upon various parameters, it is not an actual representation of reality, only a theoretical one.

"binary" için komut dosyalarını ara

Trend Pulse Pro V2Trend Pulse Pro V2 (Non Repaint)

TradingView Account Needed: Free

You don't need to be an expert to use Trend Pulse Pro.

Just follow the signals and that's all and use simple Fibonacci levels to find stop loss and take profit!

You can increase the win rate even more by following some simple technical analysis, for example, when trend breaks (price break signal level) you can use that as support become resistance level (sell) or resistance becomes support (buy):

No complex things. No waste of time.

And although you won't win 100% of the trades (no signals can guarantee that), your trading will surely improve a lot!

Even someone with almost no trading experience can read the simple trading rules given in the included user guide, watch the how-to videos and follow Trend Pulse Pro’s signals to consistently make smarter trades.

With Trend Pulse Pro you will get accurate buy and sell signals every time there is a new trading opportunity so that you never miss any big price movements and makes your trading both easier and more profitable.

How to use the signals and alerts:

Trend Pulse Pro automatically analyze trend and price action to give you a signal when there's a good trade.

These trend signals and alerts are derived from live data but the stability of our code allows it to not repaint.

Trend Pulse Pro allow you to easily determine the trend and will give you buy and sell entry levels.

Works on all markets on all time frames so it's suitable for scalpers, day and swing traders.

If you want more details, the link is in the signature.

Disclaimer:

Past performance is not indicative of future performance. No representation is being made that any results discussed within the service and its related media content will be achieved. All opinions, news, research, analyses, prices or other information is provided as general market commentary and not as investment advice. TradingWalk, their members, shareholders, employees, agents, representatives and resellers do not warrant the completeness, accuracy or timeliness of the information supplied, and they shall not be liable for any loss or damages, consequential or otherwise, which may arise from the use or reliance of the TradingWalk service and its content. © 2019 TradingWalk.

TradingWalk indicators are built for TradingView. TradingWalk is on no way a part of TradingView.

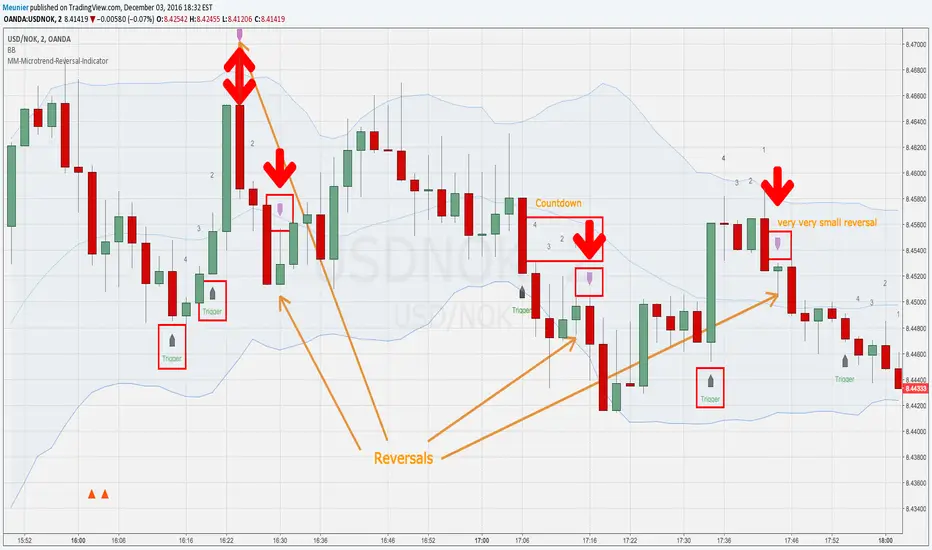

MM-Microtrend-Reversal-IndicatorThis indicator detects microtrend reversals based on crossing of the DMI+ and DMI- + signals

It indicates the trigger event on the chart as well as the reversal candle

In addition to that it shows a countdown above the bars

This is helping when multiple reversals occur

Important: when the Bollinger Bands are crossed in the previous bars it's possible that the prognosted reversal will NOT show up

Recommended timeframes are M1 and M2

Avoid trading sideway trends, the reverals are low and reversal triggers and assumed reversal candles could get chaotic

MM-Microtrend-Reversal-IndicatorThis indicator detects microtrend reversals based on crossings of the DMI+ and DMI- signals

It indicates the trigger event on the chart as well as the reversal candle

In addition to that it shows a countdown above the bars

This is helping when multiple reversals occur.

Important: when the Bollinger Bands are crossed in the previous bars it's possible that the prognosted reversal will NOT show up

Recommended timeframes are M1 and M2

Avoid trading sideway trends, the reversals are low and reversal triggers and assumed reversal candles could get chaotic sometimes

Chatterjee CorrelationThis is my first attempt on implementing a statistical method. This problem was given to me by @lejmer (who also helped me later on building more efficient code to achieve this) when we were debating on the need for higher resource allocation to run scripts so it can run longer and faster. The major problem faced by those who want to implement statistics based methods is that they run out of processing time or need to limit the data samples. My point was that such things need be implemented with an algorithm which suits pine instead of trying to port a python code directly. And yes, I am able to demonstrate that by using this implementation of Chatterjee Correlation.

🎲 What is Chatterjee Correlation?

The Chatterjee rank Correlation Coefficient (CCC) is a method developed by Sourav Chatterjee which can be used to study non linear correlation between two series.

Full documentation on the method can be found here:

arxiv.org

In short, the formula which we are implementing here is:

Algorithm can be simplified as follows:

1. Get the ranks of X

2. Get the ranks of Y

3. Sort ranks of Y in the order of X (Lets call this SortedYIndices)

4. Calculate the sum of adjacent Y ranks in SortedYIndices (Lets call it as SumOfAdjacentSortedIndices)

5. And finally the correlation coefficient can be calculated by using simple formula

CCC = 1 - (3*SumOfAdjacentSortedIndices)/(n^2 - 1)

🎲 Looks simple? What is the catch?

Mistake many people do here is that they think in Python/Java/C etc while coding in Pine. This makes code less efficient if it involves arrays and loops. And the simple code may look something like this.

var xArray = array.new()

var yArray = array.new()

array.push(xArray, x)

array.push(yArray, y)

sortX = array.sort_indices(xArray)

sortY = array.sort_indices(yArray)

SumOfAdjacentSortedIndices = 0.0

index = array.get(xSortIndices, 0)

for i=1 to n > 1? n -1 : na

indexNext = array.get(sortX, i)

SumOfAdjacentSortedIndices += math.abs(array.get(sortY, indexNext)-array.get(sortY, index))

index := indexNext

correlation := 1 - 3*SumOfAdjacentSortedIndices/(math.pow(n,2)-1)

But, problem here is the number of loops run. Remember pine executes the code on every bar. There are loops run in array.sort_indices and another loop we are running to calculate SumOfAdjacentSortedIndices. Due to this, chances of program throwing runtime errors due to script running for too long are pretty high. This limits greatly the number of samples against which we can run the study. The options to overcome are

Limit the sample size and calculate only between certain bars - this is not ideal as smaller sets are more likely to yield false or inconsistent results.

Start thinking in pine instead of python and code in such a way that it is optimised for pine. - This is exactly what we have done in the published code.

🎲 How to think in Pine?

In order to think in pine, you should try to eliminate the loops as much as possible. Specially on the data which is continuously growing.

My first thought was that sorting takes lots of time and need to find a better way to sort series - specially when it is a growing data set. Hence, I came up with this library which implements Binary Insertion Sort.

Replacing array.sort_indices with binary insertion sort will greatly reduce the number of loops run on each bar. In binary insertion sort, the array will remain sorted and any item we add, it will keep adding it in the existing sort order so that there is no need to run separate sort. This allows us to work with bigger data sets and can utilise full 20,000 bars for calculation instead of few 100s.

However, last loop where we calculate SumOfAdjacentSortedIndices is not replaceable easily. Hence, we only limit these iterations to certain bars (Even though we use complete sample size). Plots are made for only those bars where the results need to be printed.

🎲 Implementation

Current implementation is limited to few combinations of x and fixed y. But, will be converting this into library soon - which means, programmers can plug any x and y and get the correlation.

Our X here can be

Average volume

ATR

And our Y is distance of price from moving average - which identifies trend.

Thus, the indicator here helps to understand the correlation coefficient between volume and trend OR volatility and trend for given ticker and timeframe. Value closer to 1 means highly correlated and value closer to 0 means least correlated. Please note that this method will not tell how these values are correlated. That is, we will not be able to know if higher volume leads to higher trend or lower trend. But, we can say whether volume impacts trend or not.

Please note that values can differ by great extent for different timeframes. For example, if you look at 1D timeframe, you may get higher value of correlation coefficient whereas lower value for 1m timeframe. This means, volume to trend correlation is higher in 1D timeframe and lower in lower timeframes.

InsertionSortLibrary "InsertionSort"

Library of sorting algorithm for binary insertion sort and related methods

method binary_insertion_sort(sortedArray, item, order)

binary insertion sort - inserts item into sorted array while maintaining sort order

Namespace types: array

Parameters:

sortedArray (array) : array which is assumed to be sorted in the requested order

item (float) : float|int item which needs to be inserted into sorted array

order (series ORDER) : Sort order - positive number means ascending order whereas negative number represents descending order

Returns: int index at which the item is inserted into sorted array

method binary_insertion_sort(sortedArray, item, order)

Namespace types: array

Parameters:

sortedArray (array)

item (int)

order (series ORDER)

MM-Burj Khalifa IndicatorThis indicator uses several signals to visualize a "perfect candle" to enter a trade.

It colors the background to identify the zones of interest (multiple configurable high or low RSI zones). Underlying is a trendbar with the current MACD direction.

The indicator is using signals of:

--MACD

--RSI

--PVT

--ATR

--AD and DMI+/DMI-

When all 7 criterias are met it highlights the candle.

It also creates different colums with different height and width, so that you can see which signal is OK and which is maybe missing. When all signals are on GO you'll see a Burj-Khalifa-like figure. If not all signals are on GO you'see crippled versions.

To be clear:

it's not intended to detect trends or supertrends or reversals. It's purpose it's just to decide if this current candle is really going in the right direction.

The Burj-Khalifa indicator could help to confirm the entry point of an trade which was already planned.

Trading IQ - ICT LibraryLibrary "ICTlibrary"

Used to calculate various ICT related price levels and strategies. An ongoing project.

Hello Coders!

This library is meant for sourcing ICT related concepts. While some functions might generate more output than you require, you can specify "Lite Mode" as "true" in applicable functions to slim down necessary inputs.

isLastBar(userTF)

Identifies the last bar on the chart before a timeframe change

Parameters:

userTF (simple int) : the timeframe you wish to calculate the last bar for, must be converted to integer using 'timeframe.in_seconds()'

Returns: bool true if bar on chart is last bar of higher TF, dalse if bar on chart is not last bar of higher TF

necessaryData(atrTF)

returns necessaryData UDT for historical data access

Parameters:

atrTF (float) : user-selected timeframe ATR value.

Returns: logZ. log return Z score, used for calculating order blocks.

method gradBoxes(gradientBoxes, idColor, timeStart, bottom, top, rightCoordinate)

creates neon like effect for box drawings

Namespace types: array

Parameters:

gradientBoxes (array) : an array.new() to store the gradient boxes

idColor (color)

timeStart (int) : left point of box

bottom (float) : bottom of box price point

top (float) : top of box price point

rightCoordinate (int) : right point of box

Returns: void

checkIfTraded(tradeName)

checks if recent trade is of specific name

Parameters:

tradeName (string)

Returns: bool true if recent trade id matches target name, false otherwise

checkIfClosed(tradeName)

checks if recent closed trade is of specific name

Parameters:

tradeName (string)

Returns: bool true if recent closed trade id matches target name, false otherwise

IQZZ(atrMult, finalTF)

custom ZZ to quickly determine market direction.

Parameters:

atrMult (float) : an atr multiplier used to determine the required price move for a ZZ direction change

finalTF (string) : the timeframe used for the atr calcuation

Returns: dir market direction. Up => 1, down => -1

method drawBos(id, startPoint, getKeyPointTime, getKeyPointPrice, col, showBOS, isUp)

calculates and draws Break Of Structure

Namespace types: array

Parameters:

id (array)

startPoint (chart.point)

getKeyPointTime (int) : the actual time of startPoint, simplystartPoint.time

getKeyPointPrice (float) : the actual time of startPoint, simplystartPoint.price

col (color) : color of the BoS line / label

showBOS (bool) : whether to show label/line. This function still calculates internally for other ICT related concepts even if not drawn.

isUp (bool) : whether BoS happened during price increase or price decrease.

Returns: void

method drawMSS(id, startPoint, getKeyPointTime, getKeyPointPrice, col, showMSS, isUp, upRejections, dnRejections, highArr, lowArr, timeArr, closeArr, openArr, atrTFarr, upRejectionsPrices, dnRejectionsPrices)

calculates and draws Market Structure Shift. This data is also used to calculate Rejection Blocks.

Namespace types: array

Parameters:

id (array)

startPoint (chart.point)

getKeyPointTime (int) : the actual time of startPoint, simplystartPoint.time

getKeyPointPrice (float) : the actual time of startPoint, simplystartPoint.price

col (color) : color of the MSS line / label

showMSS (bool) : whether to show label/line. This function still calculates internally for other ICT related concepts even if not drawn.

isUp (bool) : whether MSS happened during price increase or price decrease.

upRejections (array)

dnRejections (array)

highArr (array) : array containing historical highs, should be taken from the UDT "necessaryData" defined above

lowArr (array) : array containing historical lows, should be taken from the UDT "necessaryData" defined above

timeArr (array) : array containing historical times, should be taken from the UDT "necessaryData" defined above

closeArr (array) : array containing historical closes, should be taken from the UDT "necessaryData" defined above

openArr (array) : array containing historical opens, should be taken from the UDT "necessaryData" defined above

atrTFarr (array) : array containing historical atr values (of user-selected TF), should be taken from the UDT "necessaryData" defined above

upRejectionsPrices (array) : array containing up rejections prices. Is sorted and used to determine selective looping for invalidations.

dnRejectionsPrices (array) : array containing down rejections prices. Is sorted and used to determine selective looping for invalidations.

Returns: void

method getTime(id, compare, timeArr)

gets time of inputted price (compare) in an array of data

this is useful when the user-selected timeframe for ICT concepts is greater than the chart's timeframe

Namespace types: array

Parameters:

id (array) : the array of data to search through, to find which index has the same value as "compare"

compare (float) : the target data point to find in the array

timeArr (array) : array of historical times

Returns: the time that the data point in the array was recorded

method OB(id, highArr, signArr, lowArr, timeArr, sign)

store bullish orderblock data

Namespace types: array

Parameters:

id (array)

highArr (array) : array of historical highs

signArr (array) : array of historical price direction "math.sign(close - open)"

lowArr (array) : array of historical lows

timeArr (array) : array of historical times

sign (int) : orderblock direction, -1 => bullish, 1 => bearish

Returns: void

OTEstrat(OTEstart, future, closeArr, highArr, lowArr, timeArr, longOTEPT, longOTESL, longOTElevel, shortOTEPT, shortOTESL, shortOTElevel, structureDirection, oteLongs, atrTF, oteShorts)

executes the OTE strategy

Parameters:

OTEstart (chart.point)

future (int) : future time point for drawings

closeArr (array) : array of historical closes

highArr (array) : array of historical highs

lowArr (array) : array of historical lows

timeArr (array) : array of historical times

longOTEPT (string) : user-selected long OTE profit target, please create an input.string() for this using the example below

longOTESL (int) : user-selected long OTE stop loss, please create an input.string() for this using the example below

longOTElevel (float) : long entry price of selected retracement ratio for OTE

shortOTEPT (string) : user-selected short OTE profit target, please create an input.string() for this using the example below

shortOTESL (int) : user-selected short OTE stop loss, please create an input.string() for this using the example below

shortOTElevel (float) : short entry price of selected retracement ratio for OTE

structureDirection (string) : current market structure direction, this should be "Up" or "Down". This is used to cancel pending orders if market structure changes

oteLongs (bool) : input.bool() for whether OTE longs can be executed

atrTF (float) : atr of the user-seleceted TF

oteShorts (bool) : input.bool() for whether OTE shorts can be executed

@exampleInputs

oteLongs = input.bool(defval = false, title = "OTE Longs", group = "Optimal Trade Entry")

longOTElevel = input.float(defval = 0.79, title = "Long Entry Retracement Level", options = , group = "Optimal Trade Entry")

longOTEPT = input.string(defval = "-0.5", title = "Long TP", options = , group = "Optimal Trade Entry")

longOTESL = input.int(defval = 0, title = "How Many Ticks Below Swing Low For Stop Loss", group = "Optimal Trade Entry")

oteShorts = input.bool(defval = false, title = "OTE Shorts", group = "Optimal Trade Entry")

shortOTElevel = input.float(defval = 0.79, title = "Short Entry Retracement Level", options = , group = "Optimal Trade Entry")

shortOTEPT = input.string(defval = "-0.5", title = "Short TP", options = , group = "Optimal Trade Entry")

shortOTESL = input.int(defval = 0, title = "How Many Ticks Above Swing Low For Stop Loss", group = "Optimal Trade Entry")

Returns: void (0)

displacement(logZ, atrTFreg, highArr, timeArr, lowArr, upDispShow, dnDispShow, masterCoords, labelLevels, dispUpcol, rightCoordinate, dispDncol, noBorders)

calculates and draws dispacements

Parameters:

logZ (float) : log return of current price, used to determine a "significant price move" for a displacement

atrTFreg (float) : atr of user-seleceted timeframe

highArr (array) : array of historical highs

timeArr (array) : array of historical times

lowArr (array) : array of historical lows

upDispShow (int) : amount of historical upside displacements to show

dnDispShow (int) : amount of historical downside displacements to show

masterCoords (map) : a map to push the most recent displacement prices into, useful for having key levels in one data structure

labelLevels (string) : used to determine label placement for the displacement, can be inside box, outside box, or none, example below

dispUpcol (color) : upside displacement color

rightCoordinate (int) : future time for displacement drawing, best is "last_bar_time"

dispDncol (color) : downside displacement color

noBorders (bool) : input.bool() to remove box borders, example below

@exampleInputs

labelLevels = input.string(defval = "Inside" , title = "Box Label Placement", options = )

noBorders = input.bool(defval = false, title = "No Borders On Levels")

Returns: void

method getStrongLow(id, startIndex, timeArr, lowArr, strongLowPoints)

unshift strong low data to array id

Namespace types: array

Parameters:

id (array)

startIndex (int) : the starting index for the timeArr array of the UDT "necessaryData".

this point should start from at least 1 pivot prior to find the low before an upside BoS

timeArr (array) : array of historical times

lowArr (array) : array of historical lows

strongLowPoints (array) : array of strong low prices. Used to retrieve highest strong low price and see if need for

removal of invalidated strong lows

Returns: void

method getStrongHigh(id, startIndex, timeArr, highArr, strongHighPoints)

unshift strong high data to array id

Namespace types: array

Parameters:

id (array)

startIndex (int) : the starting index for the timeArr array of the UDT "necessaryData".

this point should start from at least 1 pivot prior to find the high before a downside BoS

timeArr (array) : array of historical times

highArr (array) : array of historical highs

strongHighPoints (array)

Returns: void

equalLevels(highArr, lowArr, timeArr, rightCoordinate, equalHighsCol, equalLowsCol, liteMode)

used to calculate recent equal highs or equal lows

Parameters:

highArr (array) : array of historical highs

lowArr (array) : array of historical lows

timeArr (array) : array of historical times

rightCoordinate (int) : a future time (right for boxes, x2 for lines)

equalHighsCol (color) : user-selected color for equal highs drawings

equalLowsCol (color) : user-selected color for equal lows drawings

liteMode (bool) : optional for a lite mode version of an ICT strategy. For more control over drawings leave as "True", "False" will apply neon effects

Returns: void

quickTime(timeString)

used to quickly determine if a user-inputted time range is currently active in NYT time

Parameters:

timeString (string) : a time range

Returns: true if session is active, false if session is inactive

macros(showMacros, noBorders)

used to calculate and draw session macros

Parameters:

showMacros (bool) : an input.bool() or simple bool to determine whether to activate the function

noBorders (bool) : an input.bool() to determine whether the box anchored to the session should have borders

Returns: void

po3(tf, left, right, show)

use to calculate HTF po3 candle

@tip only call this function on "barstate.islast"

Parameters:

tf (simple string)

left (int) : the left point of the candle, calculated as bar_index + left,

right (int) : :the right point of the candle, calculated as bar_index + right,

show (bool) : input.bool() whether to show the po3 candle or not

Returns: void

silverBullet(silverBulletStratLong, silverBulletStratShort, future, userTF, H, L, H2, L2, noBorders, silverBulletLongTP, historicalPoints, historicalData, silverBulletLongSL, silverBulletShortTP, silverBulletShortSL)

used to execute the Silver Bullet Strategy

Parameters:

silverBulletStratLong (simple bool)

silverBulletStratShort (simple bool)

future (int) : a future time, used for drawings, example "last_bar_time"

userTF (simple int)

H (float) : the high price of the user-selected TF

L (float) : the low price of the user-selected TF

H2 (float) : the high price of the user-selected TF

L2 (float) : the low price of the user-selected TF

noBorders (bool) : an input.bool() used to remove the borders from box drawings

silverBulletLongTP (series silverBulletLevels)

historicalPoints (array)

historicalData (necessaryData)

silverBulletLongSL (series silverBulletLevels)

silverBulletShortTP (series silverBulletLevels)

silverBulletShortSL (series silverBulletLevels)

Returns: void

method invalidFVGcheck(FVGarr, upFVGpricesSorted, dnFVGpricesSorted)

check if existing FVGs are still valid

Namespace types: array

Parameters:

FVGarr (array)

upFVGpricesSorted (array) : an array of bullish FVG prices, used to selective search through FVG array to remove invalidated levels

dnFVGpricesSorted (array) : an array of bearish FVG prices, used to selective search through FVG array to remove invalidated levels

Returns: void (0)

method drawFVG(counter, FVGshow, FVGname, FVGcol, data, masterCoords, labelLevels, borderTransp, liteMode, rightCoordinate)

draws FVGs on last bar

Namespace types: map

Parameters:

counter (map) : a counter, as map, keeping count of the number of FVGs drawn, makes sure that there aren't more FVGs drawn

than int FVGshow

FVGshow (int) : the number of FVGs to show. There should be a bullish FVG show and bearish FVG show. This function "drawFVG" is used separately

for bearish FVG and bullish FVG.

FVGname (string) : the name of the FVG, "FVG Up" or "FVG Down"

FVGcol (color) : desired FVG color

data (FVG)

masterCoords (map) : a map containing the names and price points of key levels. Used to define price ranges.

labelLevels (string) : an input.string with options "Inside", "Outside", "Remove". Determines whether FVG labels should be inside box, outside,

or na.

borderTransp (int)

liteMode (bool)

rightCoordinate (int) : the right coordinate of any drawings. Must be a time point.

Returns: void

invalidBlockCheck(bullishOBbox, bearishOBbox, userTF)

check if existing order blocks are still valid

Parameters:

bullishOBbox (array) : an array declared using the UDT orderBlock that contains bullish order block related data

bearishOBbox (array) : an array declared using the UDT orderBlock that contains bearish order block related data

userTF (simple int)

Returns: void (0)

method lastBarRejections(id, rejectionColor, idShow, rejectionString, labelLevels, borderTransp, liteMode, rightCoordinate, masterCoords)

draws rejectionBlocks on last bar

Namespace types: array

Parameters:

id (array) : the array, an array of rejection block data declared using the UDT rejection block

rejectionColor (color) : the desired color of the rejection box

idShow (int)

rejectionString (string) : the desired name of the rejection blocks

labelLevels (string) : an input.string() to determine if labels for the block should be inside the box, outside, or none.

borderTransp (int)

liteMode (bool) : an input.bool(). True = neon effect, false = no neon.

rightCoordinate (int) : atime for the right coordinate of the box

masterCoords (map) : a map that stores the price of key levels and assigns them a name, used to determine price ranges

Returns: void

method OBdraw(id, OBshow, BBshow, OBcol, BBcol, bullishString, bearishString, isBullish, labelLevels, borderTransp, liteMode, rightCoordinate, masterCoords)

draws orderblocks and breaker blocks for data stored in UDT array()

Namespace types: array

Parameters:

id (array) : the array, an array of order block data declared using the UDT orderblock

OBshow (int) : the number of order blocks to show

BBshow (int) : the number of breaker blocks to show

OBcol (color) : color of order blocks

BBcol (color) : color of breaker blocks

bullishString (string) : the title of bullish blocks, which is a regular bullish orderblock or a bearish orderblock that's converted to breakerblock

bearishString (string) : the title of bearish blocks, which is a regular bearish orderblock or a bullish orderblock that's converted to breakerblock

isBullish (bool) : whether the array contains bullish orderblocks or bearish orderblocks. If bullish orderblocks,

the array will naturally contain bearish BB, and if bearish OB, the array will naturally contain bullish BB

labelLevels (string) : an input.string() to determine if labels for the block should be inside the box, outside, or none.

borderTransp (int)

liteMode (bool) : an input.bool(). True = neon effect, false = no neon.

rightCoordinate (int) : atime for the right coordinate of the box

masterCoords (map) : a map that stores the price of key levels and assigns them a name, used to determine price ranges

Returns: void

FVG

UDT for FVG calcualtions

Fields:

H (series float) : high price of user-selected timeframe

L (series float) : low price of user-selected timeframe

direction (series string) : FVG direction => "Up" or "Down"

T (series int) : => time of bar on user-selected timeframe where FVG was created

fvgLabel (series label) : optional label for FVG

fvgLineTop (series line) : optional line for top of FVG

fvgLineBot (series line) : optional line for bottom of FVG

fvgBox (series box) : optional box for FVG

labelLine

quickly pair a line and label together as UDT

Fields:

lin (series line) : Line you wish to pair with label

lab (series label) : Label you wish to pair with line

orderBlock

UDT for order block calculations

Fields:

orderBlockData (array) : array containing order block x and y points

orderBlockBox (series box) : optional order block box

vioCount (series int) : = 0 violation count of the order block. 0 = Order Block, 1 = Breaker Block

traded (series bool)

status (series string) : = "OB" status == "OB" => Level is order block. status == "BB" => Level is breaker block.

orderBlockLab (series label) : options label for the order block / breaker block.

strongPoints

UDT for strong highs and strong lows

Fields:

price (series float) : price of the strong high or strong low

timeAtprice (series int) : time of the strong high or strong low

strongPointLabel (series label) : optional label for strong point

strongPointLine (series line) : optional line for strong point

overlayLine (series line) : optional lines for strong point to enhance visibility

overlayLine2 (series line) : optional lines for strong point to enhance visibility

displacement

UDT for dispacements

Fields:

highPrice (series float) : high price of displacement

lowPrice (series float) : low price of displacement

timeAtPrice (series int) : time of bar where displacement occurred

displacementBox (series box) : optional box to draw displacement

displacementLab (series label) : optional label for displacement

po3data

UDT for po3 calculations

Fields:

dHigh (series float) : higher timeframe high price

dLow (series float) : higher timeframe low price

dOpen (series float) : higher timeframe open price

dClose (series float) : higher timeframe close price

po3box (series box) : box to draw po3 candle body

po3line (array) : line array to draw po3 wicks

po3Labels (array) : label array to label price points of po3 candle

macros

UDT for session macros

Fields:

sessions (array) : Array of sessions, you can populate this array using the "quickTime" function located above "export macros".

prices (matrix) : Matrix of session data -> open, high, low, close, time

sessionTimes (array) : Array of session names. Pairs with array sessions.

sessionLines (matrix) : Optional array for sesion drawings.

OTEtimes

UDT for data storage and drawings associated with OTE strategy

Fields:

upTimes (array) : time of highest point before trade is taken

dnTimes (array) : time of lowest point before trade is taken

tpLineLong (series line) : line to mark tp level long

tpLabelLong (series label) : label to mark tp level long

slLineLong (series line) : line to mark sl level long

slLabelLong (series label) : label to mark sl level long

tpLineShort (series line) : line to mark tp level short

tpLabelShort (series label) : label to mark tp level short

slLineShort (series line) : line to mark sl level short

slLabelShort (series label) : label to mark sl level short

sweeps

UDT for data storage and drawings associated with liquidity sweeps

Fields:

upSweeps (matrix) : matrix containing liquidity sweep price points and time points for up sweeps

dnSweeps (matrix) : matrix containing liquidity sweep price points and time points for down sweeps

upSweepDrawings (array) : optional up sweep box array. Pair the size of this array with the rows or columns,

dnSweepDrawings (array) : optional up sweep box array. Pair the size of this array with the rows or columns,

raidExitDrawings

UDT for drawings associated with the Liquidity Raid Strategy

Fields:

tpLine (series line) : tp line for the liquidity raid entry

tpLabel (series label) : tp label for the liquidity raid entry

slLine (series line) : sl line for the liquidity raid entry

slLabel (series label) : sl label for the liquidity raid entry

m2022

UDT for data storage and drawings associated with the Model 2022 Strategy

Fields:

mTime (series int) : time of the FVG where entry limit order is placed

mIndex (series int) : array index of FVG where entry limit order is placed. This requires an array of FVG data, which is defined above.

mEntryDistance (series float) : the distance of the FVG to the 50% range. M2022 looks for the fvg closest to 50% mark of range.

mEntry (series float) : the entry price for the most eligible fvg

fvgHigh (series float) : the high point of the eligible fvg

fvgLow (series float) : the low point of the eligible fvg

longFVGentryBox (series box) : long FVG box, used to draw the eligible FVG

shortFVGentryBox (series box) : short FVG box, used to draw the eligible FVG

line50P (series line) : line used to mark 50% of the range

line100P (series line) : line used to mark 100% (top) of the range

line0P (series line) : line used to mark 0% (bottom) of the range

label50P (series label) : label used to mark 50% of the range

label100P (series label) : label used to mark 100% (top) of the range

label0P (series label) : label used to mark 0% (bottom) of the range

sweepData (array)

silverBullet

UDT for data storage and drawings associated with the Silver Bullet Strategy

Fields:

session (series bool)

sessionStr (series string) : name of the session for silver bullet

sessionBias (series string)

sessionHigh (series float) : = high high of session // use math.max(silverBullet.sessionHigh, high)

sessionLow (series float) : = low low of session // use math.min(silverBullet.sessionLow, low)

sessionFVG (series float) : if applicable, the FVG created during the session

sessionFVGdraw (series box) : if applicable, draw the FVG created during the session

traded (series bool)

tp (series float) : tp of trade entered at the session FVG

sl (series float) : sl of trade entered at the session FVG

sessionDraw (series box) : optional draw session with box

sessionDrawLabel (series label) : optional label session with label

silverBulletDrawings

UDT for trade exit drawings associated with the Silver Bullet Strategy

Fields:

tpLine (series line) : tp line drawing for strategy

tpLabel (series label) : tp label drawing for strategy

slLine (series line) : sl line drawing for strategy

slLabel (series label) : sl label drawing for strategy

unicornModel

UDT for data storage and drawings associated with the Unicorn Model Strategy

Fields:

hPoint (chart.point)

hPoint2 (chart.point)

hPoint3 (chart.point)

breakerBlock (series box) : used to draw the breaker block required for the Unicorn Model

FVG (series box) : used to draw the FVG required for the Unicorn model

topBlock (series float) : price of top of breaker block, can be used to detail trade entry

botBlock (series float) : price of bottom of breaker block, can be used to detail trade entry

startBlock (series int) : start time of the breaker block, used to set the "left = " param for the box

includes (array) : used to store the time of the breaker block, or FVG, or the chart point sequence that setup the Unicorn Model.

entry (series float) : // eligible entry price, for longs"math.max(topBlock, FVG.get_top())",

tpLine (series line) : optional line to mark PT

tpLabel (series label) : optional label to mark PT

slLine (series line) : optional line to mark SL

slLabel (series label) : optional label to mark SL

rejectionBlocks

UDT for data storage and drawings associated with rejection blocks

Fields:

rejectionPoint (chart.point)

bodyPrice (series float) : candle body price closest to the rejection point, for "Up" rejections => math.max(open, close),

rejectionBox (series box) : optional box drawing of the rejection block

rejectionLabel (series label) : optional label for the rejection block

equalLevelsDraw

UDT for data storage and drawings associated with equal highs / equal lows

Fields:

connector (series line) : single line placed at the first high or low, y = avgerage of distinguished equal highs/lows

connectorLab (series label) : optional label to be placed at the highs or lows

levels (array) : array containing the equal highs or lows prices

times (array) : array containing the equal highs or lows individual times

startTime (series int) : the time of the first high or low that forms a sequence of equal highs or lows

radiate (array) : options label to "radiate" the label in connector lab. Can be used for anything

necessaryData

UDT for data storage of historical price points.

Fields:

highArr (array) : array containing historical high points

lowArr (array) : array containing historical low points

timeArr (array) : array containing historical time points

logArr (array) : array containing historical log returns

signArr (array) : array containing historical price directions

closeArr (array) : array containing historical close points

binaryTimeArr (array) : array containing historical time points, uses "push" instead of "unshift" to allow for binary search

binaryCloseArr (array) : array containing historical close points, uses "push" instead of "unshift" to allow the correct

binaryOpenArr (array) : array containing historical optn points, uses "push" instead of "unshift" to allow the correct

atrTFarr (array) : array containing historical user-selected TF atr points

openArr (array) : array containing historical open points

kNNLibrary "kNN"

Collection of experimental kNN functions. This is a work in progress, an improvement upon my original kNN script:

The script can be recreated with this library. Unlike the original script, that used multiple arrays, this has been reworked with the new Pine Script matrix features.

To make a kNN prediction, the following data should be supplied to the wrapper:

kNN : filter type. Right now either Binary or Percent . Binary works like in the original script: the system stores whether the price has increased (+1) or decreased (-1) since the previous knnStore event (called when either long or short condition is supplied). Percent works the same, but the values stored are the difference of prices in percents. That way larger differences in prices would give higher scores.

k : number k. This is how many nearest neighbors are to be selected (and summed up to get the result).

skew : kNN minimum difference. Normally, the prediction is done with a simple majority of the neighbor votes. If skew is given, then more than a simple majority is needed for a prediction. This also means that there are inputs for which no prediction would be given (if the majority votes are between -skew and +skew). Note that in Percent mode more profitable trades will have higher voting power.

depth : kNN matrix size limit. Originally, the whole available history of trades was used to make a prediction. This not only requires more computational power, but also neglects the fact that the market conditions are changing. This setting restricts the memory matrix to a finite number of past trades.

price : price series

long : long condition. True if the long conditions are met, but filters are not yet applied. For example, in my original script, trades are only made on crossings of fast and slow MAs. So, whenever it is possible to go long, this value is set true. False otherwise.

short : short condition. Same as long , but for short condition.

store : whether the inputs should be stored. Additional filters may be applied to prevent bad trades (for example, trend-based filters), so if you only need to consult kNN without storing the trade, this should be set to false.

feature1 : current value of feature 1. A feature in this case is some kind of data derived from the price. Different features may be used to analyse the price series. For example, oscillator values. Not all of them may be used for kNN prediction. As the current kNN implementation is 2-dimensional, only two features can be used.

feature2 : current value of feature 2.

The wrapper returns a tuple: [ longOK, shortOK ]. This is a pair of filters. When longOK is true, then kNN predicts a long trade may be taken. When shortOK is true, then kNN predicts a short trade may be taken. The kNN filters are returned whenever long or short conditions are met. The trade is supposed to happen when long or short conditions are met and when the kNN filter for the desired direction is true.

Exported functions :

knnStore(knn, p1, p2, src, maxrows)

Store the previous trade; buffer the current one until results are in. Results are binary: up/down

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

src : current price

maxrows : limit the matrix size to this number of rows (0 of no limit)

Returns: modified knn matrix

knnStorePercent(knn, p1, p2, src, maxrows)

Store the previous trade; buffer the current one until results are in. Results are in percents

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

src : current price

maxrows : limit the matrix size to this number of rows (0 of no limit)

Returns: modified knn matrix

knnGet(distance, result)

Get neighbours by getting k results with the smallest distances

Parameters:

distance : distance array

result : result array

Returns: array slice of k results

knnDistance(knn, p1, p2)

Create a distance array from the two given parameters

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

Returns: distance array

knnSum(knn, p1, p2, k)

Make a prediction, finding k nearest neighbours and summing them up

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

k : sum k nearest neighbors

Returns: sum of k nearest neighbors

doKNN(kNN, k, skew, depth, price, long, short, store, feature1, feature2)

execute kNN filter

Parameters:

kNN : filter type

k : number k

skew : kNN minimum difference

depth : kNN matrix size limit

price : series

long : long condition

short : short condition

store : store the supplied features (if false, only checks the results without storage)

feature1 : feature 1 value

feature2 : feature 2 value

Returns: filter output

Bifurcation Zone - CAEBifurcation Zone — Cognitive Adversarial Engine (BZ-CAE)

Bifurcation Zone — CAE (BZ-CAE) is a next-generation divergence detection system enhanced by a Cognitive Adversarial Engine that evaluates both sides of every potential trade before presenting signals. Unlike traditional divergence indicators that show every price-oscillator disagreement regardless of context, BZ-CAE applies comprehensive market-state intelligence to identify only the divergences that occur in favorable conditions with genuine probability edges.

The system identifies structural bifurcation points — critical junctures where price and momentum disagree, signaling potential reversals or continuations — then validates these opportunities through five interconnected intelligence layers: Trend Conviction Scoring , Directional Momentum Alignment , Multi-Factor Exhaustion Modeling , Adversarial Validation , and Confidence Scoring . The result is a selective, context-aware signal system that filters noise and highlights high-probability setups.

This is not a "buy the arrow" indicator. It's a decision support framework that teaches you how to read market state, evaluate divergence quality, and make informed trading decisions based on quantified intelligence rather than hope.

What Sets BZ-CAE Apart: Technical Architecture

The Problem With Traditional Divergence Indicators

Most divergence indicators operate on a simple rule: if price makes a higher high and RSI makes a lower high, show a bearish signal. If price makes a lower low and RSI makes a higher low, show a bullish signal. This creates several critical problems:

Context Blindness : They show counter-trend signals in powerful trends that rarely reverse, leading to repeated losses as you fade momentum.

Signal Spam : Every minor price-oscillator disagreement generates an alert, overwhelming you with low-quality setups and creating analysis paralysis.

No Quality Ranking : All signals are treated identically. A marginal divergence in choppy conditions receives the same visual treatment as a high-conviction setup at a major exhaustion point.

Single-Sided Evaluation : They ask "Is this a good long?" without checking if the short case is overwhelmingly stronger, leading you into obvious bad trades.

Static Configuration : You manually choose RSI 14 or Stochastic 14 and hope it works, with no systematic way to validate if that's optimal for your instrument.

BZ-CAE's Solution: Cognitive Adversarial Intelligence

BZ-CAE solves these problems through an integrated five-layer intelligence architecture:

1. Trend Conviction Score (TCS) — 0 to 1 Scale

Most indicators check if ADX is above 25 to determine "trending" conditions. This binary approach misses nuance. TCS is a weighted composite metric:

Formula : 0.35 × normalize(ADX, 10, 35) + 0.35 × structural_strength + 0.30 × htf_alignment

Structural Strength : 10-bar SMA of consecutive directional bars. Captures persistence — are bulls or bears consistently winning?

HTF Alignment : Multi-timeframe EMA stacking (20/50/100/200). When all EMAs align in the same direction, you're in institutional trend territory.

Purpose : Quantifies how "locked in" the trend is. When TCS exceeds your threshold (default 0.80), the system knows to avoid counter-trend trades unless other factors override.

Interpretation :

TCS > 0.85: Very strong trend — counter-trading is extremely high risk

TCS 0.70-0.85: Strong trend — favor continuation, require exhaustion for reversals

TCS 0.50-0.70: Moderate trend — context matters, both directions viable

TCS < 0.50: Weak/choppy — reversals more viable, range-bound conditions

2. Directional Momentum Alignment (DMA) — ATR-Normalized

Formula : (EMA21 - EMA55) / ATR14

This isn't just "price above EMA" — it's a regime-aware momentum gauge. The same $100 price movement reads completely differently in high-volatility crypto versus low-volatility forex. By normalizing with ATR, DMA adapts its interpretation to current market conditions.

Purpose : Quantifies the directional "force" behind current price action. Positive = bullish push, negative = bearish push. Magnitude = strength.

Interpretation :

DMA > 0.7: Strong bullish momentum — bearish divergences risky

DMA 0.3 to 0.7: Moderate bullish bias

DMA -0.3 to 0.3: Balanced/choppy conditions

DMA -0.7 to -0.3: Moderate bearish bias

DMA < -0.7: Strong bearish momentum — bullish divergences risky

3. Multi-Factor Exhaustion Modeling — 0 to 1 Probability

Single-metric exhaustion detection (like "RSI > 80") misses complex market states. BZ-CAE aggregates five independent exhaustion signals:

Volume Spikes : Current volume versus 50-bar average

2.5x average: 0.25 weight

2.0x average: 0.15 weight

1.5x average: 0.10 weight

Divergence Present : The fact that a divergence exists contributes 0.30 weight — structural momentum disagreement is itself an exhaustion signal.

RSI Extremes : Captures oscillator climax zones

RSI > 80 or < 20: 0.25 weight

RSI > 75 or < 25: 0.15 weight

Pin Bar Detection : Identifies rejection candles (2:1 wick-to-body ratio, indicating failed breakout attempts): 0.15 weight

Extended Runs : Consecutive bars above/below EMA20 without pullback

30+ bars: 0.15 weight (market hasn't paused to consolidate)

Total exhaustion score is the sum of all applicable weights, capped at 1.0.

Purpose : Detects when strong trends become vulnerable to reversal. High exhaustion can override trend filters, allowing counter-trend trades at genuine turning points that basic indicators would miss.

Interpretation :

Exhaustion > 0.75: High probability of climax — yellow background shading alerts you visually

Exhaustion 0.50-0.75: Moderate overextension — watch for confirmation

Exhaustion < 0.50: Fresh move — trend can continue, counter-trend trades higher risk

4. Adversarial Validation — Game Theory Applied to Trading

This is BZ-CAE's signature innovation. Before approving any signal, the engine quantifies BOTH sides of the trade simultaneously:

For Bullish Divergences , it calculates:

Bull Case Score (0-1+) :

Distance below EMA20 (pullback quality): up to 0.25

Bullish EMA alignment (close > EMA20 > EMA50): 0.25

Oversold RSI (< 40): 0.25

Volume confirmation (> 1.2x average): 0.25

Bear Case Score (0-1+) :

Price below EMA50 (structural weakness): 0.30

Very oversold RSI (< 30, indicating knife-catching): 0.20

Differential = Bull Case - Bear Case

If differential < -0.10 (default threshold), the bear case is dominating — signal is BLOCKED or ANNOTATED.

For Bearish Divergences , the logic inverts (Bear Case vs Bull Case).

Purpose : Prevents trades where you're fighting obvious strength in the opposite direction. This is institutional-grade risk management — don't just evaluate your trade, evaluate the counter-trade simultaneously.

Why This Matters : You might see a bullish divergence at a local low, but if price is deeply below major support EMAs with strong bearish momentum, you're catching a falling knife. The adversarial check catches this and blocks the signal.

5. Confidence Scoring — 0 to 1 Quality Assessment

Every signal that passes initial filters receives a comprehensive quality score:

Formula :

0.30 × normalize(TCS) // Trend context

+ 0.25 × normalize(|DMA|) // Momentum magnitude

+ 0.20 × pullback_quality // Entry distance from EMA20

+ 0.15 × state_quality // ADX + alignment + structure

+ 0.10 × divergence_strength // Slope separation magnitude

+ adversarial_bonus (0-0.30) // Your side's advantage

Purpose : Ranks setup quality for filtering and position sizing decisions. You can set a minimum confidence threshold (default 0.35) to ensure only quality setups reach your chart.

Interpretation :

Confidence > 0.70: Premium setup — consider increased position size

Confidence 0.50-0.70: Good quality — standard size

Confidence 0.35-0.50: Acceptable — reduced size or skip if conservative

Confidence < 0.35: Marginal — blocked in Filtering mode, annotated in Advisory mode

CAE Operating Modes: Learning vs Enforcement

Off : Disables all CAE logic. Raw divergence pipeline only. Use for baseline comparison.

Advisory : Shows ALL signals regardless of CAE evaluation, but annotates signals that WOULD be blocked with specific warnings (e.g., "Bull: strong downtrend (TCS=0.87)" or "Adversarial bearish"). This is your learning mode — see CAE's decision logic in action without missing educational opportunities.

Filtering : Actively blocks low-quality signals. Only setups that pass all enabled gates (Trend Filter, Adversarial Validation, Confidence Gating) reach your chart. This is your live trading mode — trust the system to enforce discipline.

CAE Filter Gates: Three-Layer Protection

When CAE is enabled, signals must pass through three independent gates (each can be toggled on/off):

Gate 1: Strong Trend Filter

If TCS ≥ tcs_threshold (default 0.80)

And signal is counter-trend (bullish in downtrend or bearish in uptrend)

And exhaustion < exhaustion_required (default 0.50)

Then: BLOCK signal

Logic: Don't fade strong trends unless the move is clearly overextended

Gate 2: Adversarial Validation

Calculate both bull case and bear case scores

If opposing case dominates by more than adv_threshold (default 0.10)

Then: BLOCK signal

Logic: Avoid trades where you're fighting obvious strength in the opposite direction

Gate 3: Confidence Gating

Calculate composite confidence score (0-1)

If confidence < min_confidence (default 0.35)

Then: In Filtering mode, BLOCK signal; in Advisory mode, ANNOTATE with warning

Logic: Only take setups with minimum quality threshold

All three gates work together. A signal must pass ALL enabled gates to fire.

Visual Intelligence System

Bifurcation Zones (Supply/Demand Blocks)

When a divergence signal fires, BZ-CAE draws a semi-transparent box extending 15 bars forward from the signal pivot:

Demand Zones (Bullish) : Theme-colored box (cyan in Cyberpunk, blue in Professional, etc.) labeled "Demand" — marks where smart money likely placed buy orders as price diverged at the low.

Supply Zones (Bearish) : Theme-colored box (magenta in Cyberpunk, orange in Professional) labeled "Supply" — marks where smart money likely placed sell orders as price diverged at the high.

Theory : Divergences represent institutional disagreement with the crowd. The crowd pushed price to an extreme (new high or low), but momentum (oscillator) is waning, indicating smart money is taking the opposite side. These zones mark order placement areas that become future support/resistance.

Use Cases :

Exit targets: Take profit when price returns to opposite-side zone

Re-entry levels: If price returns to your entry zone, consider adding

Stop placement: Place stops just beyond your zone (below demand, above supply)

Auto-Cleanup : System keeps the last 20 zones to prevent chart clutter.

Adversarial Bar Coloring — Real-Time Market Debate Heatmap

Each bar is colored based on the Bull Case vs Bear Case differential:

Strong Bull Advantage (diff > 0.3): Full theme bull color (e.g., cyan)

Moderate Bull Advantage (diff > 0.1): 50% transparency bull

Neutral (diff -0.1 to 0.1): Gray/neutral theme

Moderate Bear Advantage (diff < -0.1): 50% transparency bear

Strong Bear Advantage (diff < -0.3): Full theme bear color (e.g., magenta)

This creates a real-time visual heatmap showing which side is "winning" the market debate. When bars flip from cyan to magenta (or vice versa), you're witnessing a shift in adversarial advantage — a leading indicator of potential momentum changes.

Exhaustion Shading

When exhaustion score exceeds 0.75, the chart background displays a semi-transparent yellow highlight. This immediate visual warning alerts you that the current move is at high risk of reversal, even if trend indicators remain strong.

Visual Themes — Six Aesthetic Options

Cyberpunk : Cyan/Magenta/Yellow — High contrast, neon aesthetic, excellent for dark-themed trading environments

Professional : Blue/Orange/Green — Corporate color palette, suitable for presentations and professional documentation

Ocean : Teal/Red/Cyan — Aquatic palette, calming for extended monitoring sessions

Fire : Orange/Red/Coral — Warm aggressive colors, high energy

Matrix : Green/Red/Lime — Code aesthetic, homage to classic hacker visuals

Monochrome : White/Gray — Minimal distraction, maximum focus on price action

All visual elements (signal markers, zones, bar colors, dashboard) adapt to your selected theme.

Divergence Engine — Core Detection System

What Are Divergences?

Divergences occur when price action and momentum indicators disagree, creating structural tension that often resolves in a change of direction:

Regular Divergence (Reversal Signal) :

Bearish Regular : Price makes higher high, oscillator makes lower high → Potential trend reversal down

Bullish Regular : Price makes lower low, oscillator makes higher low → Potential trend reversal up

Hidden Divergence (Continuation Signal) :

Bearish Hidden : Price makes lower high, oscillator makes higher high → Downtrend continuation

Bullish Hidden : Price makes higher low, oscillator makes lower low → Uptrend continuation

Both types can be enabled/disabled independently in settings.

Pivot Detection Methods

BZ-CAE uses symmetric pivot detection with separate lookback and lookforward periods (default 5/5):

Pivot High : Bar where high > all highs within lookback range AND high > all highs within lookforward range

Pivot Low : Bar where low < all lows within lookback range AND low < all lows within lookforward range

This ensures structural validity — the pivot must be a clear local extreme, not just a minor wiggle.

Divergence Validation Requirements

For a divergence to be confirmed, it must satisfy:

Slope Disagreement : Price slope and oscillator slope must move in opposite directions (for regular divs) or same direction with inverted highs/lows (for hidden divs)

Minimum Slope Change : |osc_slope| > min_slope_change / 100 (default 1.0) — filters weak, marginal divergences

Maximum Lookback Range : Pivots must be within max_lookback bars (default 60) — prevents ancient, irrelevant divergences

ATR-Normalized Strength : Divergence strength = min(|price_slope| × |osc_slope| × 10, 1.0) — quantifies the magnitude of disagreement in volatility context

Regular divergences receive 1.0× weight; hidden divergences receive 0.8× weight (slightly less reliable historically).

Oscillator Options — Five Professional Indicators

RSI (Relative Strength Index) : Classic overbought/oversold momentum indicator. Best for: General purpose divergence detection across all instruments.

Stochastic : Range-bound %K momentum comparing close to high-low range. Best for: Mean reversion strategies and range-bound markets.

CCI (Commodity Channel Index) : Measures deviation from statistical mean, auto-normalized to 0-100 scale. Best for: Cyclical instruments and commodities.

MFI (Money Flow Index) : Volume-weighted RSI incorporating money flow. Best for: Volume-driven markets like stocks and crypto.

Williams %R : Inverse stochastic looking back over period, auto-adjusted to 0-100. Best for: Reversal detection at extremes.

Each oscillator has adjustable length (2-200, default 14) and smoothing (1-20, default 1). You also set overbought (50-100, default 70) and oversold (0-50, default 30) thresholds.

Signal Timing Modes — Understanding Repainting

BZ-CAE offers two timing policies with complete transparency about repainting behavior:

Realtime (1-bar, peak-anchored)

How It Works :

Detects peaks 1 bar ago using pattern: high > high AND high > high

Signal prints on the NEXT bar after peak detection (bar_index)

Visual marker anchors to the actual PEAK bar (bar_index - 1, offset -1)

Signal locks in when bar CONFIRMS (closes)

Repainting Behavior :

On the FORMING bar (before close), the peak condition may change as new prices arrive

Once bar CLOSES (barstate.isconfirmed), signal is locked permanently

This is preview/early warning behavior by design

Best For :

Active monitoring and immediate alerts

Learning the system (seeing signals develop in real-time)

Responsive entry if you're watching the chart live

Confirmed (lookforward)

How It Works :

Uses Pine Script's built-in ta.pivothigh() and ta.pivotlow() functions

Requires full pivot validation period (lookback + lookforward bars)

Signal prints pivot_lookforward bars after the actual peak (default 5-bar delay)

Visual marker anchors to the actual peak bar (offset -pivot_lookforward)

No Repainting Behavior

Best For :

Backtesting and historical analysis

Conservative entries requiring full confirmation

Automated trading systems

Swing trading with larger timeframes

Tradeoff :

Delayed entry by pivot_lookforward bars (typically 5 bars)

On a 5-minute chart, this is a 25-minute delay

On a 4-hour chart, this is a 20-hour delay

Recommendation : Use Confirmed for backtesting to verify system performance honestly. Use Realtime for live monitoring only if you're actively watching the chart and understand pre-confirmation repainting behavior.

Signal Spacing System — Anti-Spam Architecture

Even after CAE filtering, raw divergences can cluster. The spacing system enforces separation:

Three Independent Filters

1. Min Bars Between ANY Signals (default 12):

Prevents rapid-fire clustering across both directions

If last signal (bull or bear) was within N bars, block new signal

Ensures breathing room between all setups

2. Min Bars Between SAME-SIDE Signals (default 24, optional enforcement):

Prevents bull-bull or bear-bear spam

Separate tracking for bullish and bearish signal timelines

Toggle enforcement on/off

3. Min ATR Distance From Last Signal (default 0, optional):

Requires price to move N × ATR from last signal location

Ensures meaningful price movement between setups

0 = disabled, 0.5-2.0 = typical range for enabled

All three filters work independently. A signal must pass ALL enabled filters to proceed.

Practical Guidance :

Scalping (1-5m) : Any 6-10, Same-side 12-20, ATR 0-0.5

Day Trading (15m-1H) : Any 12, Same-side 24, ATR 0-1.0

Swing Trading (4H-D) : Any 20-30, Same-side 40-60, ATR 1.0-2.0

Dashboard — Real-Time Control Center

The dashboard (toggleable, four corner positions, three sizes) provides comprehensive system intelligence:

Oscillator Section

Current oscillator type and value

State: OVERBOUGHT / OVERSOLD / NEUTRAL (color-coded)

Length parameter

Cognitive Engine Section

TCS (Trend Conviction Score) :

Current value with emoji state indicator

🔥 = Strong trend (>0.75)

📊 = Moderate trend (0.50-0.75)

〰️ = Weak/choppy (<0.50)

Color: Red if above threshold (trend filter active), yellow if moderate, green if weak

DMA (Directional Momentum Alignment) :

Current value with emoji direction indicator

🐂 = Bullish momentum (>0.5)

⚖️ = Balanced (-0.5 to 0.5)

🐻 = Bearish momentum (<-0.5)

Color: Green if bullish, red if bearish

Exhaustion :

Current value with emoji warning indicator

⚠️ = High exhaustion (>0.75)

🟡 = Moderate (0.50-0.75)

✓ = Low (<0.50)

Color: Red if high, yellow if moderate, green if low

Pullback :

Quality of current distance from EMA20

Values >0.6 are ideal entry zones (not too close, not too far)

Bull Case / Bear Case (if Adversarial enabled):

Current scores for both sides of the market debate

Differential with emoji indicator:

📈 = Bull advantage (>0.2)

➡️ = Balanced (-0.2 to 0.2)

📉 = Bear advantage (<-0.2)

Last Signal Metrics Section (New Feature)

When a signal fires, this section captures and displays:

Signal type (BULL or BEAR)

Bars elapsed since signal

Confidence % at time of signal

TCS value at signal time

DMA value at signal time

Purpose : Provides a historical reference for learning. You can see what the market state looked like when the last signal fired, helping you correlate outcomes with conditions.

Statistics Section

Total Signals : Lifetime count across session

Blocked Signals : Count and percentage (filter effectiveness metric)

Bull Signals : Total bullish divergences

Bear Signals : Total bearish divergences

Purpose : System health monitoring. If blocked % is very high (>60%), filters may be too strict. If very low (<10%), filters may be too loose.

Advisory Annotations

When CAE Mode = Advisory, this section displays warnings for signals that would be blocked in Filtering mode:

Examples:

"Bull spacing: wait 8 bars"

"Bear: strong uptrend (TCS=0.87)"

"Adversarial bearish"

"Low confidence 32%"

Multiple warnings can stack, separated by " | ". This teaches you CAE's decision logic transparently.

How to Use BZ-CAE — Complete Workflow

Phase 1: Initial Setup (First Session)

Apply BZ-CAE to your chart

Select your preferred Visual Theme (Cyberpunk recommended for visibility)

Set Signal Timing to "Confirmed (lookforward)" for learning

Choose your Oscillator Type (RSI recommended for general use, length 14)

Set Overbought/Oversold to 70/30 (standard)

Enable both Regular Divergence and Hidden Divergence

Set Pivot Lookback/Lookforward to 5/5 (balanced structure)

Enable CAE Intelligence

Set CAE Mode to "Advisory" (learning mode)

Enable all three CAE filters: Strong Trend Filter , Adversarial Validation , Confidence Gating

Enable Show Dashboard , position Top Right, size Normal

Enable Draw Bifurcation Zones and Adversarial Bar Coloring

Phase 2: Learning Period (Weeks 1-2)

Goal : Understand how CAE evaluates market state and filters signals.

Activities :

Watch the dashboard during signals :

Note TCS values when counter-trend signals fail — this teaches you the trend strength threshold for your instrument

Observe exhaustion patterns at actual turning points — learn when overextension truly matters

Study adversarial differential at signal times — see when opposing cases dominate

Review blocked signals (orange X-crosses):

In Advisory mode, you see everything — signals that would pass AND signals that would be blocked

Check the advisory annotations to understand why CAE would block

Track outcomes: Were the blocks correct? Did those signals fail?

Use Last Signal Metrics :

After each signal, check the dashboard capture of confidence, TCS, and DMA

Journal these values alongside trade outcomes

Identify patterns: Do confidence >0.70 signals work better? Does your instrument respect TCS >0.85?

Understand your instrument's "personality" :

Trending instruments (indices, major forex) may need TCS threshold 0.85-0.90

Choppy instruments (low-cap stocks, exotic pairs) may work best with TCS 0.70-0.75

High-volatility instruments (crypto) may need wider spacing

Low-volatility instruments may need tighter spacing

Phase 3: Calibration (Weeks 3-4)

Goal : Optimize settings for your specific instrument, timeframe, and style.

Calibration Checklist :

Min Confidence Threshold :

Review confidence distribution in your signal journal

Identify the confidence level below which signals consistently fail

Set min_confidence slightly above that level

Day trading : 0.35-0.45

Swing trading : 0.40-0.55

Scalping : 0.30-0.40

TCS Threshold :

Find the TCS level where counter-trend signals consistently get stopped out

Set tcs_threshold at or slightly below that level

Trending instruments : 0.85-0.90

Mixed instruments : 0.80-0.85

Choppy instruments : 0.75-0.80

Exhaustion Override Level :

Identify exhaustion readings that marked genuine reversals

Set exhaustion_required just below the average

Typical range : 0.45-0.55

Adversarial Threshold :

Default 0.10 works for most instruments

If you find CAE is too conservative (blocking good trades), raise to 0.15-0.20

If signals are still getting caught in opposing momentum, lower to 0.07-0.09

Spacing Parameters :

Count bars between quality signals in your journal

Set min bars ANY to ~60% of that average

Set min bars SAME-SIDE to ~120% of that average

Scalping : Any 6-10, Same 12-20

Day trading : Any 12, Same 24

Swing : Any 20-30, Same 40-60

Oscillator Selection :

Try different oscillators for 1-2 weeks each

Track win rate and average winner/loser by oscillator type

RSI : Best for general use, clear OB/OS

Stochastic : Best for range-bound, mean reversion

MFI : Best for volume-driven markets

CCI : Best for cyclical instruments

Williams %R : Best for reversal detection

Phase 4: Live Deployment

Goal : Disciplined execution with proven, calibrated system.

Settings Changes :

Switch CAE Mode from Advisory to Filtering

System now actively blocks low-quality signals

Only setups passing all gates reach your chart

Keep Signal Timing on Confirmed for conservative entries

OR switch to Realtime if you're actively monitoring and want faster entries (accept pre-confirmation repaint risk)

Use your calibrated thresholds from Phase 3

Enable high-confidence alerts: "⭐ High Confidence Bullish/Bearish" (>0.70)

Trading Discipline Rules :

Respect Blocked Signals :

If CAE blocks a trade you wanted to take, TRUST THE SYSTEM

Don't manually override — if you consistently disagree, return to Phase 2/3 calibration

The block exists because market state failed intelligence checks

Confidence-Based Position Sizing :

Confidence >0.70: Standard or increased size (e.g., 1.5-2.0% risk)

Confidence 0.50-0.70: Standard size (e.g., 1.0% risk)

Confidence 0.35-0.50: Reduced size (e.g., 0.5% risk) or skip if conservative

TCS-Based Management :

High TCS + counter-trend signal: Use tight stops, quick exits (you're fading momentum)

Low TCS + reversal signal: Use wider stops, trail aggressively (genuine reversal potential)

Exhaustion Awareness :

Exhaustion >0.75 (yellow shading): Market is overextended, reversal risk is elevated — consider early exit or tighter trailing stops even on winning trades

Exhaustion <0.30: Continuation bias — hold for larger move, wide trailing stops

Adversarial Context :

Strong differential against you (e.g., bullish signal with bear diff <-0.2): Use very tight stops, consider skipping

Strong differential with you (e.g., bullish signal with bull diff >0.2): Trail aggressively, this is your tailwind

Practical Settings by Timeframe & Style

Scalping (1-5 Minute Charts)

Objective : High frequency, tight stops, quick reversals in fast-moving markets.

Oscillator :

Type: RSI or Stochastic (fast response to quick moves)

Length: 9-11 (more responsive than standard 14)

Smoothing: 1 (no lag)

OB/OS: 65/35 (looser thresholds ensure frequent crossings in fast conditions)

Divergence :

Pivot Lookback/Lookforward: 3/3 (tight structure, catch small swings)

Max Lookback: 40-50 bars (recent structure only)

Min Slope Change: 0.8-1.0 (don't be overly strict)

CAE :

Mode: Advisory first (learn), then Filtering

Min Confidence: 0.30-0.35 (lower bar for speed, accept more signals)

TCS Threshold: 0.70-0.75 (allow more counter-trend opportunities)

Exhaustion Required: 0.45-0.50 (moderate override)

Strong Trend Filter: ON (still respect major intraday trends)

Adversarial: ON (critical for scalping protection — catches bad entries quickly)

Spacing :

Min Bars ANY: 6-10 (fast pace, many setups)

Min Bars SAME-SIDE: 12-20 (prevent clustering)

Min ATR Distance: 0 or 0.5 (loose)

Timing : Realtime (speed over precision, but understand repaint risk)

Visuals :

Signal Size: Tiny (chart clarity in busy conditions)

Show Zones: Optional (can clutter on low timeframes)

Bar Coloring: ON (helps read momentum shifts quickly)

Dashboard: Small size (corner reference, not main focus)

Key Consideration : Scalping generates noise. Even with CAE, expect lower win rate (45-55%) but aim for favorable R:R (2:1 or better). Size conservatively.

Day Trading (15-Minute to 1-Hour Charts)

Objective : Balance quality and frequency. Standard divergence trading approach.

Oscillator :

Type: RSI or MFI (proven reliability, volume confirmation with MFI)

Length: 14 (industry standard, well-studied)

Smoothing: 1-2

OB/OS: 70/30 (classic levels)

Divergence :

Pivot Lookback/Lookforward: 5/5 (balanced structure)

Max Lookback: 60 bars

Min Slope Change: 1.0 (standard strictness)

CAE :

Mode: Filtering (enforce discipline from the start after brief Advisory learning)

Min Confidence: 0.35-0.45 (quality filter without being too restrictive)