TopTenAlgo 2. HFT AlgoEN: High Frequency Trade Algo TVQ is an advanced algorithmic system developed using Volume Weighted / Exponential Moving Averages, vWap and Ichimoku . Said indicators are re-blended with the Volume Weighted Average ( vWap ) algorithm used by Merryl Lynch or Yapıkredi algorithms. It does not act like the classic Ichimoku or Moving Averages. TVQ was used instead of RSI . High Frequency Trade Algo's incorporate a 3-sided trading strategy that detects Risk Areas and allows you to stay Flat if necessary (red and white circles above the bars) or generates appropriate signals in the buy and sell regions, that measures the risk. In the triangle or flat / horizontal corrections you need to stay flat, it warns you beforehand that you are in the risky area, while the trend will occur, it warns you with a buy or sell signal.

This algorithm is prepared with @Top10Algo ... Optimization Risky and Wait Zone

TR: High Frequency Trade Algo TVQ, Hacim Ağırlıklı/Exponential Hareketli Ortalamalar, vWap ve Ichimoku kullanarak geliştirilen gelişmiş bir algoritmik sistemdir. Bahsi geçen göstergeler Merryl Lynch yada Yapıkredi algoritmalarının kullandığı Volume Weighted Average ( vWap ) algoritması ile yeniden harmanlanmıştır. Klasik Ichimoku yada Hareketli Ortalamalar gibi hareket etmez. RSI yerine TVQ kullanılmıştır. High Frequency Trade Algo’ lar Riskli Bölgeleri tespit edip gerekirse Flat kalmanızı sağlayan(barların üstündeki kırmızı ve beyaz daireler) yada alım ve satım bölgelerinde uygun sinyaller üreten yani riski ölçen 3 taraflı bir trading stratejisini içinde barındırır. Flat kalmanız gereken üçgen yada yassı/yatay düzeltmelerde sizi riskli bölgede olduğunuz konusunda önceden uyarırken, trend oluşacağı zamanda al yada sat sinyali ile önceden uyarır.

Bu algoritma @Top10Algo ile beraber hazırlanmıştır...Riskli ve Bekleme yapılan Flat bölgelerle ile ilgili iyileştirmeler yapıldı...

"algo" için komut dosyalarını ara

Price Action - Delivery Algorithm (Zeiierman)█ Overview

Price delivery algorithms in trading refer to complex computational algorithms used to determine the optimal price for executing trades. These algorithms are particularly relevant in electronic and algorithmic trading environments where large volumes of trades are executed automatically.

These algorithms are designed to analyze market data, including prices, volumes, and historical trends, to determine the most favorable price at which to execute a trade. They can take into account various factors such as market liquidity, price impact, and timing to optimize trade execution.

█ How It Works

Optimal price zones can be calculated in many different ways; we have decided to use a cycle method that determines the current dominant trend. The indicator functions by isolating a trend within a specific frequency range from various data.

Filter Logic and Loop:

The indicator computes a weighted average of historical prices over a range of past data points. It employs a loop to iterate over these past data points, applying a unique weight to each, depending on its position relative to the trend period.

Weight Calculation:

Weights are determined using triangle wave functions. The triangle wave function ensures that the weighting oscillates in synchronization with the desired trend period.

Summation:

The indicator aggregates the weighted prices from past periods to generate a single value for each point in time. This value signifies the strength and direction of the trend at the specified frequency. The results are used to determine the specific price zones.

█ How to Use

The price zones help traders identify the best times to enter and exit the market, similar to how support and resistance zones are used. The strategy is based on using price delivery algorithm zones to enter the market in areas commonly used by institutions for placing larger orders. The main advantage of this strategy is having the support of these heavier players.

█ Settings

Delivery Algorithm: This setting allows you to select the calculation method for the Delivery Algorithm. There are several options including "Price", "Swing High", "Swing Low", "Swing Mean", "Momentum", "Expansion", and "Volume". Each option represents a different way of analyzing market data, focusing on different aspects of price action or market dynamics. The choice here will influence how the algorithm interprets and responds to market data.

The corresponding length value is about the responsiveness of the Delivery Algorithm. Adjusting this value affects the algorithm's sensitivity to changes in market conditions. A higher value makes the algorithm more responsive, meaning it will react more strongly to recent market changes. This could be useful in volatile markets. On the other hand, a lower value makes the algorithm less responsive, resulting in more gradual adjustments. This might be preferable in more stable market conditions to avoid reacting to what might be considered 'market noise.'

Delivery Sensitivity: This setting adjusts the sensitivity of the algorithm's calculations to price movements. A higher value tends to smooth out the algorithm's output by considering a wider range of price data, which can be useful for identifying longer-term trends. A lower value makes the algorithm more sensitive to recent price movements, which can be helpful for short-term trading or scalping strategies. The option to enable Scalping Mode is particularly relevant for traders focusing on short-term, quick trades.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

TopTenAlgo 10. SQZMOM Algorithmic Strategy with Alerts & SignalsEN: This Algorithm is a derivative of John Carter's "TTM Squeeze" volatility indicator. Many strategists have taken the indicator on Tradingview with simple moving averages and have looked at the biggest mistake only by dealing with squeeze and exit processes to squeeze. But I used the algorithm to determine where the markets would actually explode. For example, instead of using SMAs , I tested them on the Linear Regression Curve using Volume Weighted Moving Averages and Hull MAs. This gave me the opportunity to develop a more responsive algorithm and identify where the actual explosion would occur. The Gray Circles in the midline show that the market is entering a new jam (in the Bollinger Bands and Keltner Channel). This means low volatility , the market prepares itself for an explosive move (up or down). White Circles mean that it is about to get out of the jam. The Blue Circles, which no one can calculate, now inform that the exit is no longer jammed and that the explosion has taken place.

Mr. Carter recommends that you wait until the first gray after a gray cross and take a position in the momentum direction (for example, if the momentum value is above zero, relax). Exit position when the momentum changes (increase or decrease, this is indicated by a color change). In this algorithm, I tried to achieve good entry points using an additional indicator such as ADX and WaveTrend. To draw the histogram, I used a different method based on Linear Regression . Mr.Carter uses a simple momentum indicator. Strategy, alarms and signals have been added to the indicator so that you can optimize in algorithmic trading.

In summary, this algorithm is a strict algorithm in which additional 4-5 indicators are blended. Conveniences for Everyone ...

TR: Bu Algoritma John Carter'ın "TTM Squeeze" volatilite göstergesinin bir türevidir. Bir çok stratejist Tradingview' de gösterge' yi basit hareketli ortalamalarla ele almış ve en büyük hatayı sadece sıkışma ve sıkışmadan çıkış süreçlerini ele alarak bakmışlardır. Fakat ben algoritmayı piyasaların asıl patlama yapacağı yeri tespit etmek için kullandım. Örneğin SMA' ları kullanmak yerine Hacim Ağırlıklı Hareketli Ortalamaları ve Hull MA' ları kullanarak onları Linerar Regresyon Eğrisinde stress testine tabi tuttum. Buda bana daha duyarlı bir algoritma geliştirmem ve asıl patlamanın olacağı yerleri tespit etmem için fırsat verdi. Orta hattaki Gri Daireler, piyasanın yeni bir sıkışmaya girdiğini gösteriyor ( Bollinger Bantları ve Keltner Kanalı'nda). Bu, düşük volatilite anlamına gelir, piyasa kendisini patlayıcı bir harekete hazırlar (yukarı veya aşağı). Beyaz Daireler ise sıkışmadan çıkmak üzere olduğu anlamına gelir. Hiç kimsenin hesap edemediği Mavi Daireler ise artık sıkışmadan çıkıldığını ve patlamanın gerçekleştiğini haber verir.

Mr.Carter, gri bir çarpı işaretinden sonra ilk griye kadar beklemenizi ve momentum yönünde bir pozisyon almanızı önerir (örneğin, momentum değeri sıfırın üstünde ise, rahat olun). Momentum değiştiğinde pozisyondan çıkın (artırma veya azaltma, bunu o bir renk değişikliği ile belirtilir). Bu algoritmada ben, ADX ve WaveTrend gibi ek bir gösterge kullanarak iyi giriş noktalarıelde etmeye çalıştım. Histogramı çizmek için ise Linear Regresyon tabanlı farklı bir yöntem kullandım. Mr.Carter basit bir momentum göstergesi kullanır. Göstergeye algoritmik işlemlerde optimizasyon yapabilmeniz için strateji, alrmlar ve sinyaller eklenmiştir.

Özetle bu algoritma ek 4-5 göstergenin harmanlandığı sıkı bir algoritmadır. Herkese Kolaylıklar dilerim...

Gorb DNAIntroduction:

Gorb DNA is a versatile indicator using classic technical analysis components such as moving averages, stochastic oscillator, and histogram blending call/put flow analysis with our proprietary DNA algorithm. This indicator is designed to provide traders with useful market direction, volume, and momentum change visual cues.

Overview:

The Gorb DNA Indicator isn't just another momentum tool; it's a complex integration of innovative market analysis techniques.

By combining moving averages, stochastic oscillator, with proprietary algorithms, this indicator offers a multi-layered view of market trends, by merging call/put flow analysis with traditional market flow assessment.

This is designed for all kinds of traders, using a simple method to deliver visual changes in flow, volume, and momentum.

Core Features: Call/Put Flow & DNA

Call/Put Flow Analysis: This component examines the strength of market buying and selling pressures. It analyzes call (buying) and put (selling) flows using price range movements, providing insights smoothed over a defined period for analysis of market sentiment.

DNA Algorithm: A central feature of this indicator, the DNA algorithm utilizes a specialized moving average and oscillator technique to discern market trends. It presents an innovative approach, calculating the difference between bullish and bearish indicators to offer a detailed analysis of market momentum.

Visualization and Color Coding: The indicator employs a color-coded system for ease of interpretation, with distinct colors indicating different market conditions: white for upward/bullish movement and purple for downward/bearish movement. This feature translating complex data into a visual format that is simple to understand.

How Call/Put Flow Works:

Moving averages are used with volume and candlestick highs/lows over a specific range to help determine the overall flow. It then plots a colored line area that looks like a colored wave using just two colors to provide traders with a visual of the current market flow. This can help traders identify changes in sentiment with simple color cues.

How DNA Works:

A stochastic oscillator is used to measure the current price level relative to its price over a specific range period to analyze the momentum for the two DNA strands. Additionally moving averages are used to confirm trend and identify any divergences relative to the momentum. This is then plotted as two lines(DNA Strands) following the same color scheme as Call/Put Flow. When momentum is picking up in a specific direction, the lines will change colors and cross each other, this gives a visual of momentum now being fully on one side until it starts to change colors and flip that direction.

Custom Algorithm Elements:

Gorb DNA isn't just common tools combined into one indicator. It includes proprietary algorithmic elements tailored to enhance technical analysis and timing. These are the reasons what set this indicator apart from common momentum, sentiment, and volume methods.

We recommend experimenting with these features to choose what best suits your trading style.

Settings:

All skill-level friendly presets, easy to enable features with one-click

Call Flow: allows the user to plot a colored area that looks like waves showing increases/decreases in bullish volume (not to be followed blindly)

Put Flow: allows the user to plot a colored area that looks like waves showing increases/decreases in bearish volume (not to be followed blindly)

DNA Strand 1: allows the user to plot one of the algorithm lines to visualize momentum direction (not to be followed blindly)

DNA Strand 2: allows the user to plot one of the algorithm lines to visualize momentum direction (not to be followed blindly)

DNA Strength: allows the user to a histogram displaying momentum volume bars in the background

Flow Threshold: allows users to plot a dotted line to identify when call/put flow is now above average flow range

All colors are changeable for the user to customize to their liking

Call/Put Flow & DNA Demonstration

In the image below, we can see a basic illustration of how these core features function.

As stated above, call/put flow carefully monitors changes in moving averages, volume, and price action. If the market sentiment is shifting one direction, the call/put flow will plot those changes. If market is bullish, call flow should rise and put flow should decrease. The same goes for the opposite if the market is bearish.

As is the same for the DNA strands, if markets momentum is becoming bullish, the lines will change color and then cross to signify a change in momentum and the call flow in the background should match this change. This creates two layers of confluence in an easy understandable visual method.

Using Call/Put Flow

In the image below, we disabled everything but call flow to demonstrate usage.

On the left side of the image, you can see call flow matched price increase, then started to decline. This created a flow divergence, identifying a possible change in price action coming. This happened once flow crossed back below the threshold line and price then beginning to move lower. On the right side of the image, you can see call flow rising and price increasing. This is a good confluence showing there is bullish sentiment building in the market.

In this next image, we disabled everything but put flow to demonstrate usage.

The left side shows a put flow divergence. Put flow is slowly rising just like price is, this can help a trader identify a possible shift in sentiment coming. And on the right side, we have put flow rising above the threshold line and price beginning to decrease. Now we have confluence of bearish sentiment building in the market.

The image below shows only call & put flow enabled, to display what the above two images combined look like.

As you can see in the image above, these flow visuals help identify the underlying market sentiment. And when they cross, it leads to a change in price action in the direction of the sentiment over the threshold line.

Using DNA Strands

The image below has just DNA strands enabled to demonstrate usage.

On the left is a box highlighting bearish momentum cross. In the circles is the change in momentum shifting from bullish to bearish. The move gets stronger as the DNA strands get closer to cross over signifying strength in the move. On the right side is a box highlighting a bullish momentum cross. The circles again, show the change from bearish to bullish momentum. Like previously said, the move gets stronger as the DNA strands get closer to crossing over, signifying strength in that direction.

The next image shows call/put flow and DNA strands enabled for a full complete picture.

The circles labeled (1) are showing the change in momentum from bullish to bearish. Circle (2) shows call flow decreasing and put flow rising above calls. Finally the arrow points to the DNA strands crossing over and put flow rising above the threshold line. This is 3 levels of easy visual confluence showing a change in sentiment, volume, and momentum to the downside.

The next image will be showing the bullish side with call/put flow and DNA strands enabled.

The circles that are labeled (1), show the visual change in momentum on the DNA strands from bearish to bullish. Circle (2) is the crossing of call flow over put flow and the arrow points to the DNA strands crossing over and call flow above the threshold line. Three simple to use visual confluences to identify change in sentiment, volume, and momentum to the upside.

Conclusion:

Our goal is to provide a unique, yet simple approach to market sentiment & momentum analysis. It's a tool developed for traders seeking user-friendly and easy to use tools that provide easy visual insights of market dynamics. We believe in simplicity, effectiveness, and creating tools to support decision making for all traders.

How to get access:

You can see the Author's instructions to get access to this indicator

RISK DISCLAIMER

All content, tools, scripts & education provided by Gorb Algo are for informational & educational purposes only. Trading is risky and most lose their money, past performance does not guarantee future results.

MKAST V2 (lifetime)PLEASE READ THE ENTIRE POST BEFORE PURCHASING & USING THE MKAST Algorithm. Saves you and me some time in emails and messages. :)

This is the NEW LIFETIME ACCESS Version of the MKAST

The MKAST Buy Sell Algorithm is a very specific strategy, cut down to its roots and made perfect for the volatile crypto market.

Many Algorithms focus only on one aspect, one side, one specific rule.

As you know, this is not how life, the market or anything else works.

MKAST combines many different aspects at the same time, scans multiple other Algorithms and comes to a conclusion based on over 1350 lines of code.

It is based on Divergences, Elliott Waves, Ichimoku, MACD, MACD Histogram, RSI, Stoch, CCI, Momentum, OBV, DIOSC, VWMACD, CMF and multiple EMAs.

Every single aspect is weighted into the decision before giving out an indication.

Most buy/sell Algorithms FAIL because they try to apply the same strategy to every single chart, which

are as individual as humans.

To conquer this problem, MKAST has a wide range of settings and variables which can be easily

modified.

To make it a true strategy, MKAST has as well settings for Take Profit Points, Multiple Entries and Stop

Losses. Everything with an Alert Feature of course.

I know from experience that many people take one Algorithm and are simply too LAZY to add multiple Algorithms to make a rational choice.

The result of that is that they lose money, by following blatantly only one Algorithm.

MKAST has additional 9 Indicators, perfect for the crypto market, which can be turned on and off.

Manual

MKAST Signals Settings

“Show Signals?” - On/Off to show the Buy/Sell Signals.

“Aggressiveness” - Increase to make the signals less aggressive and decrease to make them more aggressive.

“Show Custom Signals?” - On/Off to show custom MKAST Signals as chosen in the settings below.

“Custom Buy/Sell Aggressiveness” - Choose a custom Aggressiveness for each buy and sell signal individually.

“TJ-Index Requirement For Buy/Sell” - If the TJ-Index is below the given number, it will show the signal in grey, this also applies for normal signals. Buy 0 and Sell 15 shows all signals in their original colour again.

“Don’t show signals that don’t meet index requirement?” - Checked, it will completely not show signals which would be “grey” as in the explanation above.

“Change Backgroundcolour if index is at 15 or 0?” - Checked, changes the colour of the chart if the index is at 15 or 0 points

MKAST Panel Settings

“Show Info Panel?” - Shows Info Panel on the chart.

“Move Info Panel UP by %” - Moves Info Panel up/down.

“Move Info Panel Left/Right ” - Moves Info Panel Left/Right.

“Show BitMEX Panel?” - Shows BitMEX Panel on the chart.

“Move BitMEX Panel by % ” - Moves BitMEX Panel up/down.

“Move BitMEX Panel Left/Right” - Moves BitMEX Panel Left/Right. “Signal Source” - Choose source of candle open/close for Equity calculation.

“Leverage Used?” - Select the used Leverage for your strategy and Equity calculation.

“Fees Per Trade in % ” - Deducts these fees after each trade from Equity calculation.

“Round Current Profit Price?” - Rounds the number on the Panel. “Trading Periods ” - Choose a trading Period which will be used to calculate Period Equity.

“Show separations of each Trading Period?” - Show separations on the chart of each Trading Period.

The very new feature on Tradingview and obviously now as well on MKAST are Information Panels.

I have chosen to add an Info Panel and a BitMEX Price Panel into MKAST, to make live and even

backtesting easier.

With only one blink of an eye the user is able to see ALL relevant information, without having to go

through various ways of checking and using other tools.

The Info Panel:

The first row shows the current profit. This is calculated since the signal initiation and the current candle close. Followed by a single number, which represents the current TJ-Index, removing the need of having to add the actual TJ-Index Oscillator on the chart.

The second row shows the current position and its status. This was added on request of many users wanting to know if their position is “about to change” or not. The status shows the users if the position is “endangered” or “okay”.

Followed by the “backtesting tool” already included inside the Panel. No need for complex oscillators with a hard reading for backtesting. With this one and simple panel, you see the Period Equity for the period chosen previously in the settings. This calculates all profits made inside that period and re-sets when the period ends. Right next to it, the Total Equity calculating ALL profits since the beginning of the chart.

Right below, you see the information about the last long and short position which have been open. This helps with the evaluation and documentation of the last trade.

The BitMEX Panel:

A convenient panel which shows all BitMEX contracts and their LIVE prices. The need for opening each chart goes away, the quality and experience of trading increases.

MKAST custom Signals are one of the notorious possibilities for ADVANCED strategies with MKAST.

Users who requested these features and use them frequently are the ones, having already a very unique trading strategy and they use these very custom signals as confluence or for multiple entry trades.

These custom signals and their settings can be mostly ignored by the majority of traders who are using this Algorithm.

The idea behind the grey signals has its roots in the idea of the TJ-Index. The TJ-Index being 15 Algorithms and conditions possible showing a bullish or bearish interpretation. The index counts the Algorithms which are showing a bullish interpretation.

Like that we can make sure that signals are shown in the original colour, are only those who have an additional confluence with the TJ-Index, not letting the user buy, if at least the majority is not bullish, and not letting the user sell, if at least the majority is bearish.

The custom buy and sell aggressiveness lets the user customise the MKAST algorithm even more.

Either the users wants to see how signals are changing on a different (slightly lower or higher) aggressiveness, being able to expect a change on their own settings. OR seeing that some signals of the same sort are a little out of place and is able to move these to a different aggressiveness, increasing the profitability even more.

Needless to say, custom signals are NOT a part of the Info Panel.

MKAST Label & Trendline Settings

“Show Labels?” - On/Off to show Labels above each signal, with the percentage gain or loss, calculated from the last signal to the new signal.

“Show Trendlines?” - On/Off to show automatic Trendlines following Gainzy Lines.

“Lookback Length” - Choose a length that the automatic trendiness use for calculation. Comparable to Aggressiveness.

“Wicks//Bodies” - Change between trendiness connecting from wick to wick or from body to body.

“Black lines// Coloured lines” - Change between simply black lines or changing colour lines.

“Filter Trendlines?” - On/Off to show all trendiness or just resistance decreasing and support increasing ones.

“Limit Extensions Of The Lines?” - This value increases by how much the trendiness are being extended. 0 = endless extension, otherwise 100 = maximum custom extension.MKAST Strategy “Take Profit 1” - On/Off to show TP1 points.

“Take Profit After %” - Set the percentage after which TP1 is active.

“Take Profit 2 ” - On/Off to show TP2 points.

“Take Profit 2 After %” - Set the percentage after which TP1 is

active.

“Take Profit 3” - On/Off to show TP3 points.

“Take Profit 3 After %” - Set the percentage after which TP1 is active.

“Second Entry” - On/Off to show Second Entry points.

“Second Entry After %” - Set the percentage after which Second Entry is active.

“Third Entry” - On/Off to show Third Entry points.

“Third Entry After %” - Set the percentage after which Third Entry is active.

“Stop Loss” - On/Off to show Stop Loss points.

“Stop Loss After %” - Set the percentage after which Stop Loss is active.

MKAST Strategy

To make the life of the MKAST user even easier, I have added all adjustable Take Profit Points, Multiple entry points and Stop Loss points.

I have never seen a sustainable and reliable trading strategy without TPs, Multiple entry and especially without a stop loss. Everything in the usual and fully customisable MKAST style.

Simply choose how many Take Profit points you would like to have and choose the percentage after which you would like to see the Take Profit point appear on the chart and notify you to take profits.

Are you a Trader who likes Multiple Entries? Also no problem with MKAST. Select how many additional entries you would like to have and after how many percent you would like them to appear on the chart and remind you of adding to the position.

What would a Strategy be without a Stop Loss? Same settings apply here as on the TPs and MEs.

All of the settings are able to take fractions of a number as well. This enables users to even use all of the strategy settings for scalping or FX pairs, where high leverage and the smallest of moves are used for trading.

Needless to say, all of these settings work on RENKO and Heikin Ashi as well. These might need adjustment, since the calculation is different, yet there is nothing standing in the way of it anymore.

Crypto Modified Indicators

“Show Divergences?” - On/Off to show Divergences on the Chart based on the data of 10 different Algorithms.

“Show Oversold/bought?” - On/Off to change the colour of the chart in Oversold/bought conditions.

“Oversold/bought value?” - Choose a value for which the chart is Oversold/bought.

“Show Fibonacci Levels?” - On/Off to show automatic Fibonacci Levels.

“Fibonacci Lookback Lenght” - This value states how many candles from right now are taken into account to paint the Fibonacci Levels.

“Fibonacci Custom Period” - Choose a custom Timeframe that should be used to paint the Fibonacci Levels.

“2nd-7th Fibonacci Level” - Enter a value for the Fibonacci Levels you would like to use and see on the chart.

“Plot 1.618 Level?” - On/Off for the Fibonacci extension level.

Crypto Modified Indicators

“Show Bands?” - On/Off to show the TJ-Bands on the chart.

“Bands Length” - Choose a value for the TJ-Bands Lenght

“Show Show EMA 1-3?” - On/Off to show the EMAs 1-3 on the chart.

“EMA Lenght 1-3” - Choose a value for the first to third EMA Lenght

“Show Ichimoku? ” - On/Off to show Ichimoku on the chart.

“Show Tenkin?” - On/Off to show Tenkin on the chart. “Tenkin” - Set the lenght of the Tenkin.

“Show Kijun?” - On/Off to show Kijun on the chart.

“Kijun” - Set the lenght of the Kijun.

“Show Senkou?” - On/Off to show the Senkou on the chart. “Senkou” - Set the lenght of the Senkou.

“Displacement” - Set the value of the Displacement.

“Show Chikou Span?” - On/Off to show the Chikou Span on the chart.

Crypto Custom Indicators

In the picture above, you see the first pair of Crypto Custom Indicators. The oversold and overbought conditions are highlighted.

Bullish and Bearish divergences are also plotted on the chart.

This is personally my favourite combination of Indicators and MKAST settings. It shows nicely

everything one needs to know and makes it easier to decide wether to follow a signal or not.

We here as well a perfect example of the Automatic Fibonacci Lines (Lookback 50, Timeframe 1D).

It shows all significant levels, which we can see being respected.

Orange = 23.6%, Green = 38.2%, Red = 50%, Yellow = 61.8%, Blue = 78.6%, White = 0%;100%

In this picture above, we observe the perfect ensemble of MKAST and an EMA strategy, especially modified for crypto markets.

Here, as by default, we have the EMAs at 21, 90 and 200. These have shown to be very significant moving support and resistance points in the crypto market.

In this picture above, I lowered the timeframe to show the highly significant levels of the Ichimoku. It has not the “usual values”. These here have been modified for the volatile crypto market and set as default.

An incredibly powerful tool for anyone who is ready to step up their trading game. It is a huge part of the MKAST back end and the strategy behind it.

MKAST Custom Alerts

1

MKAST without any doubt has Custom Alerts for all Signals that it is painting on the chart.

One can even choose to receive custom notifications for Take Profit points, Multiple Entry points and

the Stop Loss points.

The signals appear on the chart DURING the candle, not at the end of the candle. Therefore, the

alerts do this as well. These appear during the candle.

Here we can see all of the possible Alerts that can be chosen to be displayed. In total it is 14 different custom alerts, based on what the trader is looking for and how he is trading.

Personally, I have 10-15 coins that I trade the most and for these I have custom notifications, mostly though only the MKAST Buy/Sell and Stop Loss Signals.

To activate Alerts for MKAST,

1) Go to the “ALERT” icon on the top tool bar of your Tradingview.

2) Select “CONDITION” as “—MKAST—“

3) Then choose ONE condition from the list of conditions.

4) On “OPTIONS” you can set how many times it appears, I have “Once per Bar”.

4.1) If you want to make sure that the signal is truly there and not just a condition for a second during the candle, choose “ONCE PER BAR CLOSE”.

5) “Expiration Time” sets the time until the alert expires. PRO users have no expiration for alerts.

6) “Alert Actions” give you a row of choices what happens and how you want to be notified.

7) “Message” is the message that you receive inside the notification.

Thank you, Kong

Gorb WallIntroduction:

Gorb Wall is a trading tool that offers a unique approach to market trend analysis. It extends the capabilities of the Gorb Algo indicator by presenting a multi-ticker, multi-timeframe dashboard, enabling traders to capture crucial market movements across various financial instruments without flipping through charts.

Overview:

Multi-Ticker Analysis: Monitor and analyze multiple financial instruments simultaneously.

Customizable Timeframes: Tailor the script to various timeframes to suit your trading strategy.

Gorb Algo Market Trend: An algorithm that adapts to market conditions, providing insights into trend changes.

User-Friendly Dashboard: Easily configure and customize the dashboard placement on your chart.

Color-Coded Trend Indicators: Visual cues to quickly assess bullish or bearish trends.

Optimized for Performance: Efficiently coded to ensure smooth running on TradingView without overloading resources.

How Gorb Wall Works:

The script utilizes Gorb Algo's market trend algorithm to process price and volume data across selected tickers and timeframes.

It applies a complex calculation to identify trends, using a combination of volatility analysis, momentum measurements, and trend strength indicators.

The output is a simplified visual representation on the dashboard, where colored circles indicate the trend direction, providing an at-a-glance market overview.

Unique Features:

Proprietary Algorithm: The heart of Gorb Wall lies in its unique Gorb Algo Market Trend algorithm. Unlike standard trend-following indicators, this proprietary algorithm integrates multiple technical analysis concepts (e.g., moving averages, volume data, price action, and oscillators) to provide a more comprehensive market trend analysis.

Multi-Dimensional Analysis: The script analyzes market trends by simultaneously processing data across multiple tickers and timeframes, offering a broader view of market movements than traditional single-ticker indicators.

We recommend exploring & choosing which tickers/timeframes best suits your needs and style of trading, and use that to combine with our suite of indicators.

Settings:

All skill-level friendly presets, easy to enable features with one-click

Dashboard Placement: Choose from top/bottom left/right for dashboard positioning.

Trend Speed Mode: Select the algorithm speed - Fast, Medium, Slow, Slowest.

Bullish/Bearish Trend Colors: Customize colors for trend indicators.

Additional Tickers: Input options for monitoring multiple financial instruments.

Timeframe Selection: Choose from a range of timeframes for each ticker.

How to Use

In the image below, we can see a basic example of how this indicator functions.

The dashboard displays up to three different tickers per the user's choice, with 4 different timeframes the user can choose. It that runs the algorithm line on the specified ticker & timeframe and plots a colored circle that identifies that tickers trend on the specified timeframes.

There are two colors, white for bullish trend and purple for bearish trend. These are the two consistent colors across our suit of indicators to help simplify trading by using simple color matching for confluence. Below is a continued breakdown on using this indicator:

Dynamic Trend Visualization in Real-Time Updates

The dashboard dynamically updates trend colors (white for bullish, purple for bearish) based on real-time market data, offering immediate insights into market sentiment. The next three images below these the live change in data as price action begins developing over multiple timeframes.

In the image above, we are on the 5min AAPL chart, we have SPY, QQQ, and VIX as our tickers on the dashboard with 1min, 2min, 3min, and 10min timeframes chosen. We begin to see VIX flip bullish, which can usually mean down side for indices.

We then see as AAPL's price begins to slow and reverse, we see SPY's trend following on the smaller timeframes first with VIX still leading the way indicating possible bearish change.

In the image above, we can see that price dips down and SPY & QQQ market trends have flipped bearish on all timeframes, while VIX continues to be bullish(validating the downwards price action)

Customizable Settings

Users can adjust settings such as dashboard placement, trend speed mode, and color themes to suit individual trading styles.

In the image below, we can see the dashboard placement setting offers four different locations the user can move the dashboard. Just like in Gorb Algo , the user can choose which trendline speed they want to use to best fit their trading strategy.

In the image below, we can see the "bullish trend" & "bearish trend" colors setting. These colors by default match the rest of our suite of indicators, white is bullish and purple is bearish. Users can change these color settings to meet their preferences.

In the image below, we can see there are three market ticker options that the user can change. This allows users to monitor their favorite tickers across or easily flip through multiple tickers in order to gauge their current market trends without having to change their chart

In the image below, we can see the 4 timeframes that are on the dashboard. The user has the ability to change each of those four, to whatever timeframe best suits their trading needs. There are 12 different timeframe options to choose from.

Quick Dashboard Review

Using color-coded trend detection, this quickly gauges market trends and provides a visual to easily identify these changes in real-time across multiple timeframes. When a circle changes color, this means that price has flipped that direction, causing a change in the Gorb Algo market trendline. As stated above, white is for bullish trend and purple is for bearish trend, but these colors can be changed to fit the users trading strategy and style. Each timeframe the user chooses will be updated in real-time, including the higher time frames like the daily & weekly. They have been modified to pull data a same speed the lower timeframes are.

This helps provide quick visual identification of real market trend changes as price action develops. It is best used in conjunction with other forms of technical analysis for a holistic trading approach.

Conclusion:

This indicator is designed to streamline market trend analysis, offering traders an innovative, efficient, and easy-to-use tool for making informed trading decisions. This tool complements our suite of indicators, providing unique market insights that are not typically available in traditional open-source scripts.

How to get access:

You can see the Author's instructions to get access to this indicator

RISK DISCLAIMER

All content, tools, scripts & education provided by Gorb Algo are for informational & educational purposes only. Trading is risky and most lose their money, past performance does not guarantee future results.

MKAST V2 (monthly)PLEASE READ THE ENTIRE POST BEFORE PURCHASING & USING THE MKAST Algorithm. Saves you and me some time in emails and messages. :)

This is the NEW MONTHLY ACCESS Version of the MKAST

The MKAST Buy Sell Algorithm is a very specific strategy, cut down to its roots and made perfect for the volatile crypto market.

Many Algorithms focus only on one aspect, one side, one specific rule.

As you know, this is not how life, the market or anything else works.

MKAST combines many different aspects at the same time, scans multiple other Algorithms and comes to a conclusion based on over 1350 lines of code.

It is based on Divergences, Elliott Waves , Ichimoku , MACD , MACD Histogram, RSI , Stoch , CCI , Momentum, OBV, DIOSC, VWMACD, CMF and multiple EMAs.

Every single aspect is weighted into the decision before giving out an indication.

Most buy/sell Algorithms FAIL because they try to apply the same strategy to every single chart, which

are as individual as humans.

To conquer this problem, MKAST has a wide range of settings and variables which can be easily

modified.

To make it a true strategy, MKAST has as well settings for Take Profit Points, Multiple Entries and Stop

Losses. Everything with an Alert Feature of course.

I know from experience that many people take one Algorithm and are simply too LAZY to add multiple Algorithms to make a rational choice.

The result of that is that they lose money, by following blatantly only one Algorithm.

MKAST has additional 9 Indicators, perfect for the crypto market, which can be turned on and off.

Manual

MKAST Signals Settings

“Show Signals?” - On/Off to show the Buy/Sell Signals.

“Aggressiveness” - Increase to make the signals less aggressive and decrease to make them more aggressive.

“Show Custom Signals?” - On/Off to show custom MKAST Signals as chosen in the settings below.

“Custom Buy/Sell Aggressiveness” - Choose a custom Aggressiveness for each buy and sell signal individually.

“TJ-Index Requirement For Buy/Sell” - If the TJ-Index is below the given number, it will show the signal in grey, this also applies for normal signals. Buy 0 and Sell 15 shows all signals in their original colour again.

“Don’t show signals that don’t meet index requirement?” - Checked, it will completely not show signals which would be “grey” as in the explanation above.

“Change Backgroundcolour if index is at 15 or 0?” - Checked, changes the colour of the chart if the index is at 15 or 0 points

MKAST Panel Settings

“Show Info Panel?” - Shows Info Panel on the chart.

“Move Info Panel UP by %” - Moves Info Panel up/down.

“Move Info Panel Left/Right ” - Moves Info Panel Left/Right.

“Show BitMEX Panel?” - Shows BitMEX Panel on the chart.

“Move BitMEX Panel by % ” - Moves BitMEX Panel up/down.

“Move BitMEX Panel Left/Right” - Moves BitMEX Panel Left/Right. “Signal Source” - Choose source of candle open/close for Equity calculation.

“Leverage Used?” - Select the used Leverage for your strategy and Equity calculation.

“Fees Per Trade in % ” - Deducts these fees after each trade from Equity calculation.

“Round Current Profit Price?” - Rounds the number on the Panel. “Trading Periods ” - Choose a trading Period which will be used to calculate Period Equity.

“Show separations of each Trading Period?” - Show separations on the chart of each Trading Period.

The very new feature on Tradingview and obviously now as well on MKAST are Information Panels.

I have chosen to add an Info Panel and a BitMEX Price Panel into MKAST, to make live and even

backtesting easier.

With only one blink of an eye the user is able to see ALL relevant information, without having to go

through various ways of checking and using other tools.

The Info Panel:

The first row shows the current profit. This is calculated since the signal initiation and the current candle close. Followed by a single number, which represents the current TJ-Index, removing the need of having to add the actual TJ-Index Oscillator on the chart.

The second row shows the current position and its status. This was added on request of many users wanting to know if their position is “about to change” or not. The status shows the users if the position is “endangered” or “okay”.

Followed by the “backtesting tool” already included inside the Panel. No need for complex oscillators with a hard reading for backtesting. With this one and simple panel, you see the Period Equity for the period chosen previously in the settings. This calculates all profits made inside that period and re-sets when the period ends. Right next to it, the Total Equity calculating ALL profits since the beginning of the chart.

Right below, you see the information about the last long and short position which have been open. This helps with the evaluation and documentation of the last trade.

The BitMEX Panel:

A convenient panel which shows all BitMEX contracts and their LIVE prices. The need for opening each chart goes away, the quality and experience of trading increases.

MKAST custom Signals are one of the notorious possibilities for ADVANCED strategies with MKAST.

Users who requested these features and use them frequently are the ones, having already a very unique trading strategy and they use these very custom signals as confluence or for multiple entry trades.

These custom signals and their settings can be mostly ignored by the majority of traders who are using this Algorithm.

The idea behind the grey signals has its roots in the idea of the TJ-Index. The TJ-Index being 15 Algorithms and conditions possible showing a bullish or bearish interpretation. The index counts the Algorithms which are showing a bullish interpretation.

Like that we can make sure that signals are shown in the original colour, are only those who have an additional confluence with the TJ-Index, not letting the user buy, if at least the majority is not bullish , and not letting the user sell, if at least the majority is bearish .

The custom buy and sell aggressiveness lets the user customise the MKAST algorithm even more.

Either the users wants to see how signals are changing on a different (slightly lower or higher) aggressiveness, being able to expect a change on their own settings. OR seeing that some signals of the same sort are a little out of place and is able to move these to a different aggressiveness, increasing the profitability even more.

Needless to say, custom signals are NOT a part of the Info Panel.

MKAST Label & Trendline Settings

“Show Labels?” - On/Off to show Labels above each signal, with the percentage gain or loss, calculated from the last signal to the new signal.

“Show Trendlines?” - On/Off to show automatic Trendlines following Gainzy Lines.

“Lookback Length” - Choose a length that the automatic trendiness use for calculation. Comparable to Aggressiveness.

“Wicks//Bodies” - Change between trendiness connecting from wick to wick or from body to body.

“Black lines// Coloured lines” - Change between simply black lines or changing colour lines.

“Filter Trendlines?” - On/Off to show all trendiness or just resistance decreasing and support increasing ones.

“Limit Extensions Of The Lines?” - This value increases by how much the trendiness are being extended. 0 = endless extension, otherwise 100 = maximum custom extension.MKAST Strategy “Take Profit 1” - On/Off to show TP1 points.

“Take Profit After %” - Set the percentage after which TP1 is active.

“Take Profit 2 ” - On/Off to show TP2 points.

“Take Profit 2 After %” - Set the percentage after which TP1 is

active.

“Take Profit 3” - On/Off to show TP3 points.

“Take Profit 3 After %” - Set the percentage after which TP1 is active.

“Second Entry” - On/Off to show Second Entry points.

“Second Entry After %” - Set the percentage after which Second Entry is active.

“Third Entry” - On/Off to show Third Entry points.

“Third Entry After %” - Set the percentage after which Third Entry is active.

“Stop Loss” - On/Off to show Stop Loss points.

“Stop Loss After %” - Set the percentage after which Stop Loss is active.

MKAST Strategy

To make the life of the MKAST user even easier, I have added all adjustable Take Profit Points, Multiple entry points and Stop Loss points.

I have never seen a sustainable and reliable trading strategy without TPs, Multiple entry and especially without a stop loss. Everything in the usual and fully customisable MKAST style.

Simply choose how many Take Profit points you would like to have and choose the percentage after which you would like to see the Take Profit point appear on the chart and notify you to take profits.

Are you a Trader who likes Multiple Entries? Also no problem with MKAST. Select how many additional entries you would like to have and after how many percent you would like them to appear on the chart and remind you of adding to the position.

What would a Strategy be without a Stop Loss? Same settings apply here as on the TPs and MEs .

All of the settings are able to take fractions of a number as well. This enables users to even use all of the strategy settings for scalping or FX pairs, where high leverage and the smallest of moves are used for trading.

Needless to say, all of these settings work on RENKO and Heikin Ashi as well. These might need adjustment, since the calculation is different, yet there is nothing standing in the way of it anymore.

Crypto Modified Indicators

“Show Divergences?” - On/Off to show Divergences on the Chart based on the data of 10 different Algorithms.

“Show Oversold/bought?” - On/Off to change the colour of the chart in Oversold/bought conditions.

“Oversold/bought value?” - Choose a value for which the chart is Oversold/bought.

“Show Fibonacci Levels?” - On/Off to show automatic Fibonacci Levels.

“Fibonacci Lookback Lenght” - This value states how many candles from right now are taken into account to paint the Fibonacci Levels.

“Fibonacci Custom Period” - Choose a custom Timeframe that should be used to paint the Fibonacci Levels.

“2nd-7th Fibonacci Level” - Enter a value for the Fibonacci Levels you would like to use and see on the chart.

“Plot 1.618 Level?” - On/Off for the Fibonacci extension level.

Crypto Modified Indicators

“Show Bands?” - On/Off to show the TJ-Bands on the chart.

“Bands Length” - Choose a value for the TJ-Bands Lenght

“Show Show EMA 1-3?” - On/Off to show the EMAs 1-3 on the chart.

“EMA Lenght 1-3” - Choose a value for the first to third EMA Lenght

“Show Ichimoku? ” - On/Off to show Ichimoku on the chart.

“Show Tenkin?” - On/Off to show Tenkin on the chart. “Tenkin” - Set the lenght of the Tenkin.

“Show Kijun?” - On/Off to show Kijun on the chart.

“Kijun” - Set the lenght of the Kijun.

“Show Senkou?” - On/Off to show the Senkou on the chart. “Senkou” - Set the lenght of the Senkou.

“Displacement” - Set the value of the Displacement.

“Show Chikou Span?” - On/Off to show the Chikou Span on the chart.

Crypto Custom Indicators

In the picture above, you see the first pair of Crypto Custom Indicators. The oversold and overbought conditions are highlighted.

Bullish and Bearish divergences are also plotted on the chart.

This is personally my favourite combination of Indicators and MKAST settings. It shows nicely

everything one needs to know and makes it easier to decide wether to follow a signal or not.

We here as well a perfect example of the Automatic Fibonacci Lines (Lookback 50, Timeframe 1D).

It shows all significant levels, which we can see being respected.

Orange = 23.6%, Green = 38.2%, Red = 50%, Yellow = 61.8%, Blue = 78.6%, White = 0%;100%

In this picture above, we observe the perfect ensemble of MKAST and an EMA strategy, especially modified for crypto markets.

Here, as by default, we have the EMAs at 21, 90 and 200. These have shown to be very significant moving support and resistance points in the crypto market.

In this picture above, I lowered the timeframe to show the highly significant levels of the Ichimoku . It has not the “usual values”. These here have been modified for the volatile crypto market and set as default.

An incredibly powerful tool for anyone who is ready to step up their trading game. It is a huge part of the MKAST back end and the strategy behind it.

MKAST Custom Alerts

1

MKAST without any doubt has Custom Alerts for all Signals that it is painting on the chart.

One can even choose to receive custom notifications for Take Profit points, Multiple Entry points and

the Stop Loss points.

The signals appear on the chart DURING the candle, not at the end of the candle. Therefore, the

alerts do this as well. These appear during the candle.

Here we can see all of the possible Alerts that can be chosen to be displayed. In total it is 14 different custom alerts, based on what the trader is looking for and how he is trading.

Personally, I have 10-15 coins that I trade the most and for these I have custom notifications, mostly though only the MKAST Buy/Sell and Stop Loss Signals.

To activate Alerts for MKAST,

1) Go to the “ALERT” icon on the top tool bar of your Tradingview.

2) Select “CONDITION” as “—MKAST—“

3) Then choose ONE condition from the list of conditions.

4) On “OPTIONS” you can set how many times it appears, I have “Once per Bar”.

4.1) If you want to make sure that the signal is truly there and not just a condition for a second during the candle, choose “ONCE PER BAR CLOSE”.

5) “Expiration Time” sets the time until the alert expires. PRO users have no expiration for alerts.

6) “Alert Actions” give you a row of choices what happens and how you want to be notified.

7) “Message” is the message that you receive inside the notification.

Thank you, Kong

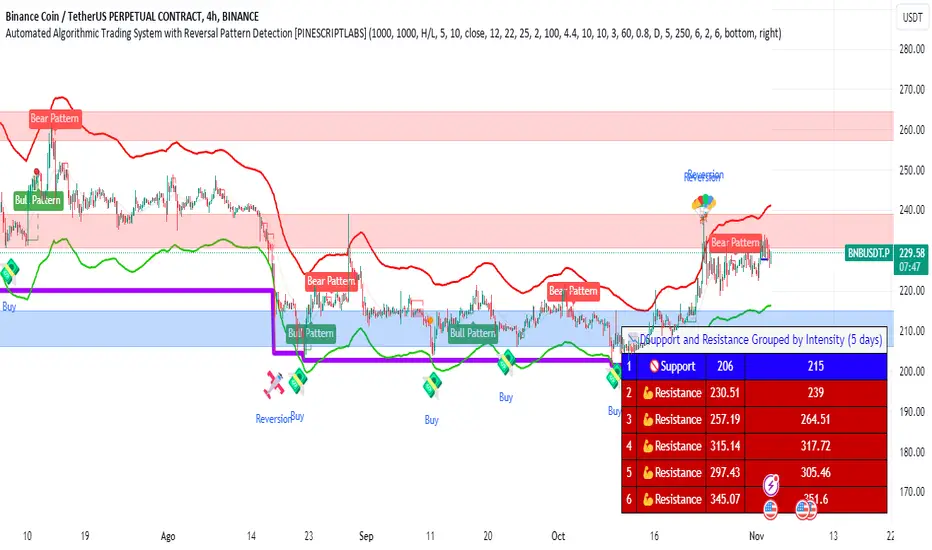

Automated Algorithmic Trading System with RP DetectionFirst, we use a calculation of "higher highs" and "lower lows" price channels, which we see represented on the chart in purple. These channels provide us with a broad view that helps us identify on the chart where the price has reached significantly higher levels than before during a specific period and lower points than previous levels. As we observe, a channel forms, and when the price approaches or touches this channel initially, it reacts violently. But this is where the magic begins, as we will use these as areas of significant reversal, although they won't be the only filter, as we will need confluence with other patterns once we are in areas of significant reversal to make a buying or selling decision.

Secondly, the algorithm uses a fundamental and precise calculation as it shows us the most important support and resistance levels of the asset, which we observe in two ways on the chart. First, supports are represented in a blue block, and resistances in a red block. These are also grouped in a table by default in the last 5 days, although we can modify these calculations according to our needs in the indicator's configuration.

In addition, our algorithm performs a special calculation of a rational quadratic kernel, estimating the price regression function. This provides us with a clear idea of where the price of the asset is heading and its trend. This channel is always calculated and working optimally within the "higher highs" and "lower lows" channel we reviewed a moment ago, and it provides us with a macro view of the price.

Now, the algorithm uses this last quadratic microchannel to give us some reversal signals within this same microchannel that can be utilized by us for precise scalping entries. Considering the following, as we visualize on the chart:

First, we will explain the Reversal signals. At the top of our quadratic microchannel, the first automated signal is generated, which we will observe as a Reversal and is represented by a parachutist. This occurs when the price breaks the upper microchannel, and we expect a price pullback. A piece of advice: if we are in a resistance area, the price will have more strength to return to the microchannel zone, allowing us to take a short position.

On the other hand, as observed on the chart, the same reversal signal represented by an airplane is generated when there is a downward price break of the microchannel, which makes us expect a pullback back to the channel. In case we are in a support zone, the price's return will gain more strength, enabling us to enter a long position.

As we see in the chart, we have two other types of signals with very complex calculations that the algorithm detects, alerting us about price reversals. The first reversal patterns are shown visually as purple and green flags and are executed when there is a change in the price structure and the price reversal within the microchannel is confirmed. This allows us to have buy and sell operations. The second signals are shown visually as Bear Pattern and Bull Pattern, confirming a pattern when the price does not fall (for bulls) or rise (for bears) below or above a specific level after detecting the "hook." This is explained subtly, as the calculation is very complex, but the effectiveness of these reversals is impressive for working with pullbacks within the microchannel.

Now, let's explain how the grand signal is generated through confluences from all the algorithmic calculations of the indicator:

First, the buy signal is generated when we observe that the Quadratic Channel crosses down our "higher highs" and "lower lows" channel, meaning there is now a cross between channels, and at the same time, we are in a Support Zone. At this moment, when these three confluences are met, it will send us the buy alert that we visually observe as a pile of bills.

Similarly, for the sell signal, it is generated when we observe that the Quadratic Channel crosses up our "higher highs" and "lower lows" channel, meaning there is now a cross between channels, and at the same time, we are in a Resistance Zone. At this moment, when these three confluences are met, it will send us the sell alert that we visually observe as an explosion.

These grand confluence signals are usually of the day trading type since they will be executed in a significant move.

All our indicators come with two types of alerts to automate our trading. The first type of alert will notify us on our devices when a signal of interest occurs on the chart, previously configured by us.

The second type is configured to make our indicators work for us without the need to be present on the chart. This is done with a special programming within the indicator's code, and it will execute automatic buys and sells on our preferred exchange through an alert configured for the 3Commas bot. It will only be necessary to enter our Bot number or Bot ID provided by the 3Commas provider and insert it into the alert. All premium indicators have an explanation in their configuration that will detail where to enter your Bot ID.

ESPAÑOL:

Primero, usamos un cálculo de Canales de Precios "altos mas altos" y "bajos mas bajos", que vemos representados en el gráfico en color morado. Estos canales nos otorgan una amplia visión que nos ayuda a identificar en el gráfico dónde el precio ha alcanzado niveles significativamente más altos que los anteriores durante un período específico y puntos más bajos que los anteriores. Como observamos, se forma un canal en el que, en primer instancia, cuando el precio se acerca o toca este canal, reacciona violentamente. Pero es aquí donde comienza la magia, ya que los usaremos como zonas de gran reversión, aunque no serán el único filtro, ya que necesitaremos que exista confluencia con otros patrones una vez estemos en zonas de gran reversión para tomar una decisión de compra o venta.

En segunda instancia, el algoritmo utiliza un cálculo fundamental y preciso ya que Nos muestra los soportes y resistencias más importantes del activo, que observamos de dos maneras en el gráfico. Primero, están representados en un bloque azul los soportes y en un bloque rojo las resistencias. Estos también se agrupan en una tabla por orden de importancia por defecto en los últimos 5 días, aunque estos cálculos los podremos modificar de acuerdo a nuestras necesidades en la configuración del indicador.

adicional nuestro algoritmo realiza un cálculo especial de un kernel cuadrático racional, que estima la función de regresión del precio. Esto nos proporciona una idea clara de hacia dónde va el precio del activo y su tendencia. Este canal siempre está calculado y trabajando de manera óptima dentro del otro canal de "altos mas altos " y "bajos mas bajos" que revisamos hace unos momentos, y que nos brinda una visión macro del precio.

Ahora bien, el algoritmo utiliza este último micro canal cuadrático para darnos algunas señales de reversión dentro de este mismo micro canal que pueden ser aprovechadas por nosotros para hacer entradas precisas y del tipo scalping. Considerando lo siguiente, como visualizamos en el gráfico:

Primero, explicaremos las señales de Reversión en la parte alta de nuestro micro canal cuadrático, se genera la primera señal automatizada que observaremos como Reversión y está representada con un paracaidista. Esto ocurre cuando el precio rompe el micro canal alto, y esperamos que se genere un pullback del precio. Un consejo: si estamos en un área de resistencia, el precio tendrá más fuerza para regresar a la zona del micro canal, lo que nos permitirá tomar una posición corta.

Por otro lado, como observamos en el gráfico, la misma señal de reversión representada por una avioneta se genera cuando hay una ruptura del precio hacia abajo del micro canal, lo que nos hace esperar un pullback de retorno al canal. En caso de que estemos en una zona dentro del soporte, el retorno del precio tomará más fuerza, permitiéndonos obtener una entrada larga.

Como vemos en el gráfico, tenemos otros dos tipos de señales con cálculos muy complejos que el algoritmo detecta, avisándonos sobre las reversiones del precio. Los primeros patrones de reversión se muestran visualmente como banderas moradas y verdes y se ejecutan cuando hay un cambio en la estructura del precio y se confirma la reversión del precio dentro del micro canal. Esto nos permite tener operaciones de compra y venta. Las segundas señales se muestran visualmente como Bear Pattern y Bull Pattern, confirmando un patrón cuando el precio no vuelve a caer (para alcistas) o subir (para bajistas) por debajo o por encima de un nivel específico después de detectar el "gancho". Esto está explicado de manera sutil, ya que el cálculo es muy complejo, pero la efectividad de estas reversiones es impresionante para trabajar con pullbacks dentro del micro canal.

ahora bien vamos a explicar como se genera la gran señal por confluencias por todos los calculos algoritmicos del indicador:

primero la señal de compra se generá Cuando observamos que el Canal Cuadrático cruza hacia abajo nuestro Canal de bajos mas bajos, es decir ahora hay un cruce entre canales y al mismo tiempo nos encontramos en una Zona de Soporte, en este momento al cumplirse estas tres confluencias nos enviará la alerta de compra que observamos visualmente como un cumulo de billetes.

asi mismo para la venta se generá Cuando observamos que el Canal Cuadrático cruza hacia arriba nuestro Canal de altos mas altos, es decir ahora hay un cruce entre canales y al mismo tiempo nos encontramos en una Zona de Resistencia, en este momento al cumplirse estas tres confluencias nos enviará la alerta de venta que observamos visualmente como una explosión.

estas grandes señales por confluencia suelen ser del tipo day trading ya que se ejecutarán en un gran movimiento.

Todos nuestros indicadores cuentan con dos tipos de alertas para automatizar nuestro trading. El primer tipo de alerta nos avisará en nuestros dispositivos cuando ocurra alguna señal en el grafico y que sea de nuestro interes previamente configurada por nosotros.

La segunda está configurada para que nuestros indicadores trabajen para nosotros sin necesidad de estar presentes en el gráfico, esto con una programacion especial dentro del codigo del indicador y que hará por nosotros compras y ventas automáticas en nuestro Exchange de preferencia mediante una alerta configurada para el bot 3Commas, solo bastará con que pongamos nuestro numero de Bot o Bot ID que da el provedoor de 3Commas y lo insertemos en la alerta, todos los indicadores premium tienen en su configuracion una explicacion que te indicará detalladamente donde poner tus Bot ID.

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100