Enhanced Volume Trend Indicator with BB SqueezeEnhanced Volume Trend Indicator with BB Squeeze: Comprehensive Explanation

The visualization system allows traders to quickly scan multiple securities to identify high-probability setups without detailed analysis of each chart. The progression from squeeze to breakout, supported by volume trend confirmation, offers a systematic approach to identifying trading opportunities.

The script combines multiple technical analysis approaches into a comprehensive dashboard that helps traders make informed decisions by identifying high-probability setups while filtering out noise through its sophisticated confirmation requirements. It combines multiple technical analysis approaches into an integrated visual system that helps traders identify potential trading opportunities while filtering out false signals.

Core Features

1. Volume Analysis Dashboard

The indicator displays various volume-related metrics in customizable tables:

AVOL (After Hours + Pre-Market Volume): Shows extended hours volume as a percentage of the 21-day average volume with color coding for buying/selling pressure. Green indicates buying pressure and red indicates selling pressure.

Volume Metrics: Includes regular volume (VOL), dollar volume ($VOL), relative volume compared to 21-day average (RVOL), and relative volume compared to 90-day average (RVOL90D).

Pre-Market Data: Optional display of pre-market volume (PVOL), pre-market dollar volume (P$VOL), pre-market relative volume (PRVOL), and pre-market price change percentage (PCHG%).

2. Enhanced Volume Trend (VTR) Analysis

The Volume Trend indicator uses adaptive analysis to evaluate buying and selling pressure, combining multiple factors:

MACD (Moving Average Convergence Divergence) components

Volume-to-SMA (Simple Moving Average) ratio

Price direction and market conditions

Volume change rates and momentum

EMA (Exponential Moving Average) alignment and crossovers

Volatility filtering

VTR Visual Indicators

The VTR score ranges from 0-100, with values above 50 indicating bullish conditions and below 50 indicating bearish conditions. This is visually represented by colored circles:

"●" (Filled Circle):

Green: Strong bullish trend (VTR ≥ 80)

Red: Strong bearish trend (VTR ≤ 20)

"◯" (Hollow Circle):

Green: Moderate bullish trend (VTR 65-79)

Red: Moderate bearish trend (VTR 21-35)

"·" (Small Dot):

Green: Weak bullish trend (VTR 55-64)

Red: Weak bearish trend (VTR 36-45)

"○" (Medium Hollow Circle): Neutral conditions (VTR 46-54), shown in gray

In "Both" display mode, the VTR shows both the numerical score (0-100) alongside the appropriate circle symbol.

Enhanced VTR Settings

The Enhanced Volume Trend component offers several advanced customization options:

Adaptive Volume Analysis (volTrendAdaptive):

When enabled, dynamically adjusts volume thresholds based on recent market volatility

Higher volatility periods require proportionally higher volume to generate significant signals

Helps prevent false signals during highly volatile markets

Keep enabled for most trading conditions, especially in volatile markets

Speed of Change Weight (volTrendSpeedWeight, range 0-1):

Controls emphasis on volume acceleration/deceleration rather than absolute levels

Higher values (0.7-1.0): More responsive to new volume trends, better for momentum trading

Lower values (0.2-0.5): Less responsive, better for trend following

Helps identify early volume trends before they fully develop

Momentum Period (volTrendMomentumPeriod, range 2-10):

Defines lookback period for volume change rate calculations

Lower values (2-3): More responsive to recent changes, better for short timeframes

Higher values (7-10): Smoother, better for daily/weekly charts

Directly affects how quickly the indicator responds to new volume patterns

Volatility Filter (volTrendVolatilityFilter):

Adjusts significance of volume by factoring in current price volatility

High volume during high volatility receives less weight

High volume during low volatility receives more weight

Helps distinguish between genuine volume-driven moves and volatility-driven moves

EMA Alignment Weight (volTrendEmaWeight, range 0-1):

Controls importance of EMA alignments in final VTR calculation

Analyzes multiple EMA relationships (5, 10, 21 period)

Higher values (0.7-1.0): Greater emphasis on trend structure

Lower values (0.2-0.5): More focus on pure volume patterns

Display Mode (volTrendDisplayMode):

"Value": Shows only numerical score (0-100)

"Strength": Shows only symbolic representation

"Both": Shows numerical score and symbol together

3. Bollinger Band Squeeze Detection (SQZ)

The BB Squeeze indicator identifies periods of low volatility when Bollinger Bands contract inside Keltner Channels, often preceding significant price movements.

SQZ Visual Indicators

"●" (Filled Circle): Strong squeeze - high probability setup for an impending breakout

Green: Strong squeeze with bullish bias (likely upward breakout)

Red: Strong squeeze with bearish bias (likely downward breakout)

Orange: Strong squeeze with unclear direction

"◯" (Hollow Circle): Moderate squeeze - medium probability setup

Green: With bullish EMA alignment

Red: With bearish EMA alignment

Orange: Without clear directional bias

"-" (Dash): Gray dash indicates no squeeze condition (normal volatility)

The script identifies squeeze conditions through multiple methods:

Bollinger Bands contracting inside Keltner Channels

BB width falling to bottom 20% of recent range (BB width percentile)

Very narrow Keltner Channel (less than 5% of basis price)

Tracking squeeze duration in consecutive bars

Different squeeze strengths are detected:

Strong Squeeze: BB inside KC with tight BB width and narrow KC

Moderate Squeeze: BB inside KC with either tight BB width or narrow KC

No Squeeze: Normal market conditions

4. Breakout Detection System

The script includes two breakout indicators working in sequence:

4.1 Pre-Breakout (PBK) Indicator

Detects potential upcoming breakouts by analyzing multiple factors:

Squeeze conditions lasting 2-3 bars or more

Significant price ranges

Strong volume confirmation

EMA/MACD crossovers

Consistent price direction

PBK Visual Indicators

"●" (Filled Circle): Detected pre-breakout condition

Green: Likely upward breakout (bullish)

Red: Likely downward breakout (bearish)

Orange: Direction not yet clear, but breakout likely

"-" (Dash): Gray dash indicates no pre-breakout condition

The PBK uses sophisticated conditions to reduce false signals including minimum squeeze length, significant price movement, and technical confirmations.

4.2 Breakout (BK) Indicator

Confirms actual breakouts in progress by identifying:

End of squeeze or strong expansion of Bollinger Bands

Volume expansion

Price moving outside Bollinger Bands

EMA crossovers with volume confirmation

MACD crossovers with significant price range

BK Visual Indicators

"●" (Filled Circle): Confirmed breakout in progress

Green: Upward breakout (bullish)

Red: Downward breakout (bearish)

Orange: Unusual breakout pattern without clear direction

"◆" (Diamond): Special breakout conditions (meets some but not all criteria)

"-" (Dash): Gray dash indicates no breakout detected

The BK indicator uses advanced filters for confirmation:

Requires consecutive breakout signals to reduce false positives

Strong volume confirmation requirements (40% above average)

Significant price movement thresholds

Consistency checks between price action and indicators

5. Market Metrics and Analysis

Price Change Percentage (CHG%)

Displays the current percentage change relative to the previous day's close, color-coded green for positive changes and red for negative changes.

Average Daily Range (ADR%)

Calculates the average daily percentage range over a specified period (default 20 days), helping traders gauge volatility and set appropriate price targets.

Average True Range (ATR)

Shows the Average True Range value, a volatility indicator developed by J. Welles Wilder that measures market volatility by decomposing the entire range of an asset price for that period.

Relative Strength Index (RSI)

Displays the standard 14-period RSI, a momentum oscillator that measures the speed and change of price movements on a scale from 0 to 100.

6. External Market Indicators

QQQ Change

Shows the percentage change in the Invesco QQQ Trust (tracking the Nasdaq-100 Index), useful for understanding broader tech market trends.

UVIX Change

Displays the percentage change in UVIX, a volatility index, providing insight into market fear and potential hedging activity.

BTC-USD

Shows the current Bitcoin price from Coinbase, useful for traders monitoring crypto correlation with equities.

Market Breadth (BRD)

Calculates the percentage difference between ATHI.US and ATLO.US (high vs. low securities), indicating overall market direction and strength.

7. Session Analysis and Volume Direction

Session Detection

The script accurately identifies different market sessions:

Pre-market: 4:00 AM to 9:30 AM

Regular market: 9:30 AM to 4:00 PM

After-hours: 4:00 PM to 8:00 PM

Closed: Outside trading hours

This detection works on any timeframe through careful calculation of current time in seconds.

Buy/Sell Volume Direction

The script analyzes buying and selling pressure by:

Counting up volume when close > open

Counting down volume when close < open

Tracking accumulated volume within the day

Calculating intraday pressure (up volume minus down volume)

Enhanced AVOL Calculation

The improved AVOL calculation works in all timeframes by:

Estimating typical pre-market and after-hours volume percentages

Combining yesterday's after-hours with today's pre-market volume

Calculating this as a percentage of the 21-day average volume

Determining buying/selling pressure by analyzing after-hours and pre-market price changes

Color-coding results: green for buying pressure, red for selling pressure

This calculation is particularly valuable because it works consistently across any timeframe.

Customization Options

Display Settings

The dashboard has two customizable tables: Volume Table and Metrics Table, with positions selectable as bottom_left or bottom_right.

All metrics can be individually toggled on/off:

Pre-market data (PVOL, P$VOL, PRVOL, PCHG%)

Volume data (AVOL, RVOL Day, RVOL 90D, Volume, SEED_YASHALGO_NSE_BREADTH:VOLUME )

Price metrics (ADR%, ATR, RSI, Price Change%)

Market indicators (QQQ, UVIX, Breadth, BTC-USD)

Analysis indicators (Volume Trend, BB Squeeze, Pre-Breakout, Breakout)

These toggle options allow traders to customize the dashboard to show only the metrics they find most valuable for their trading style.

Table and Text Customization

The dashboard's appearance can be customized:

Table background color via tableBgColor

Text color (White or Black) via textColorOption

The indicator uses smart formatting for volume and price values, automatically adding appropriate suffixes (K, M, B) for readability.

MACD Configuration for VTR

The Volume Trend calculation incorporates MACD with customizable parameters:

Fast Length: Controls the period for the fast EMA (default 3)

Slow Length: Controls the period for the slow EMA (default 9)

Signal Length: Controls the period for the signal line EMA (default 5)

MACD Weight: Controls how much influence MACD has on the volume trend score (default 0.3)

These settings allow traders to fine-tune how momentum is factored into the volume trend analysis.

Bollinger Bands and Keltner Channel Settings

The Bollinger Bands and Keltner Channels used for squeeze detection have preset (hidden) parameters:

BB Length: 20 periods

BB Multiplier: 2.0 standard deviations

Keltner Length: 20 periods

Keltner Multiplier: 1.5 ATR

These settings follow standard practice for squeeze detection while maintaining simplicity in the user interface.

Practical Trading Applications

Complete Trading Strategies

1. Squeeze Breakout Strategy

This strategy combines multiple components of the indicator:

Wait for a strong squeeze (SQZ showing ●)

Look for pre-breakout confirmation (PBK showing ● in green or red)

Enter when breakout is confirmed (BK showing ● in same direction)

Use VTR to confirm volume supports the move (VTR ≥ 65 for bullish or ≤ 35 for bearish)

Set profit targets based on ADR (Average Daily Range)

Exit when VTR begins to weaken or changes direction

2. Volume Divergence Strategy

This strategy focuses on the volume trend relative to price:

Identify when price makes a new high but VTR fails to confirm (divergence)

Look for VTR to show weakening trend (● changing to ◯ or ·)

Prepare for potential reversal when SQZ begins to form

Enter counter-trend position when PBK confirms reversal direction

Use external indicators (QQQ, BTC, Breadth) to confirm broader market support

3. Pre-Market Edge Strategy

This strategy leverages pre-market data:

Monitor AVOL for unusual pre-market activity (significantly above 100%)

Check pre-market price change direction (PCHG%)

Enter position at market open if VTR confirms direction

Use SQZ to determine if volatility is likely to expand

Exit based on RVOL declining or price reaching +/- ADR for the day

Market Context Integration

The indicator provides valuable context for trading decisions:

QQQ change shows tech market direction

BTC price shows crypto market correlation

UVIX change indicates volatility expectations

Breadth measurement shows market internals

This context helps traders avoid fighting the broader market and align trades with overall market direction.

Timeframe Optimization

The indicator is designed to work across different timeframes:

For day trading: Focus on AVOL, VTR, PBK/BK, and use shorter momentum periods

For swing trading: Focus on SQZ duration, VTR strength, and broader market indicators

For position trading: Focus on larger VTR trends and use EMA alignment weight

Advanced Analytical Components

Enhanced Volume Trend Score Calculation

The VTR score calculation is sophisticated, with the base score starting at 50 and adjusting for:

Price direction (up/down)

Volume relative to average (high/normal/low)

Volume acceleration/deceleration

Market conditions (bull/bear)

Additional factors are then applied, including:

MACD influence weighted by strength and direction

Volume change rate influence (speed)

Price/volume divergence effects

EMA alignment scores

Volatility adjustments

Breakout strength factors

Price action confirmations

The final score is clamped between 0-100, with values above 50 indicating bullish conditions and below 50 indicating bearish conditions.

Anti-False Signal Filters

The indicator employs multiple techniques to reduce false signals:

Requiring significant price range (minimum percentage movement)

Demanding strong volume confirmation (significantly above average)

Checking for consistent direction across multiple indicators

Requiring prior bar consistency (consecutive bars moving in same direction)

Counting consecutive signals to filter out noise

These filters help eliminate noise and focus on high-probability setups.

MACD Enhancement and Integration

The indicator enhances standard MACD analysis:

Calculating MACD relative strength compared to recent history

Normalizing MACD slope relative to volatility

Detecting MACD acceleration for stronger signals

Integrating MACD crossovers with other confirmation factors

EMA Analysis System

The indicator uses a comprehensive EMA analysis system:

Calculating multiple EMAs (5, 10, 21 periods)

Detecting golden cross (10 EMA crosses above 21 EMA)

Detecting death cross (10 EMA crosses below 21 EMA)

Assessing price position relative to EMAs

Measuring EMA separation percentage

Recent Enhancements and Evolution

Version 5.2 includes several improvements:

Enhanced AVOL to show buying/selling direction through color coding

Improved VTR with adaptive analysis based on market conditions

AVOL display now works in all timeframes through sophisticated estimation

Removed animal symbols and streamlined code with bright colors for better visibility

Improved anti-false signal filters throughout the system

Optimizing Indicator Settings

For Different Market Types

Range-Bound Markets:

Lower EMA Alignment Weight (0.2-0.4)

Higher Speed of Change Weight (0.8-1.0)

Focus on SQZ and PBK signals for breakout potential

Trending Markets:

Higher EMA Alignment Weight (0.7-1.0)

Moderate Speed of Change Weight (0.4-0.6)

Focus on VTR strength and BK confirmations

Volatile Markets:

Enable Volatility Filter

Enable Adaptive Volume Analysis

Lower Momentum Period (2-3)

Focus on strong volume confirmation (VTR ≥ 80 or ≤ 20)

For Different Asset Classes

Equities:

Standard settings work well

Pay attention to AVOL for gap potential

Monitor QQQ correlation

Futures:

Consider higher Volume/RVOL weight

Reduce MACD weight slightly

Pay close attention to SQZ duration

Crypto:

Higher volatility thresholds may be needed

Monitor BTC price for correlation

Focus on stronger confirmation signals

Integrated Visual System for Trading Decisions

The colored circle indicators create an intuitive visual system for quick market assessment:

Progression Sequence: SQZ (Squeeze) → PBK (Pre-Breakout) → BK (Breakout)

This sequence often occurs in order, with the squeeze leading to pre-breakout conditions, followed by an actual breakout.

VTR (Volume Trend): Provides context about the volume supporting these movements.

Color Coding: Green for bullish conditions, red for bearish conditions, and orange/gray for neutral or undefined conditions.

"Table" için komut dosyalarını ara

Financial Data Spreadsheet [By MUQWISHI]The Financial Data Spreadsheet indicator displays tables in the form of a spreadsheet containing a set of selected financial performances of a company within the most recent reported period. Analyzing Financial data is one of the classic methods to evaluate whether the company’s stock price is overvalued or undervalued based on its income statement, balance sheet, and cash flow statement. This indicator might be practical to investors to collect needed data of a company to analyze and compare it with other companies on a TradingView chart or print it in spreadsheet form.

█ OVERVIEW

█ BEST PRACTICES

Due to strict limitations on calling request.financial() function, I tried to develop the table with the best ways to be more dynamic to move and the ability to join multiple tables into a spreadsheet. Users can add up to 20 instruments and 2 financial metrics per table. However, it’s possible to add many tables with other financial metrics, then connect them to the main table.

Credits: The idea of joining multiple tables inspired by @QuantNomad Screener for 40+ instruments

█ INDICATOR SETTINGS

1- Moving Table toward right-left up-down from its origin.

2- Hiding Column Title checkmark. Useful for adding a joined table underneath with additional instruments.

3- Hiding Instruments Title checkmark. Useful for adding a joined table on the right with other financial metrics.

4- Shade Alternate Rows checkmark. I believe it’ll make the table easier to read.

5- Selecting Financial Period. (Year, Quarter).

6- Entering a currency.

7- Choosing a financial ID for each column. There’re over 200 financial IDs. Source: What financial data is available in Pine? — TradingView

8- Optional to highlight values in between.

9- Entering the ticker’s symbol with the ability to activate/deactivate.

█ TIP

For best technical performance, use the indicator in a 1D timeframe.

Please let me know if you have any questions.

Thank you.

new takesi_2Step_Screener_MOU_KAKU_FIXED4 (Visible)//@version=5

indicator("MNO_2Step_Screener_MOU_KAKU_FIXED4 (Visible)", overlay=true, max_labels_count=500)

// =========================

// Inputs

// =========================

emaSLen = input.int(5, "EMA Short (5)")

emaMLen = input.int(13, "EMA Mid (13)")

emaLLen = input.int(26, "EMA Long (26)")

macdFast = input.int(12, "MACD Fast")

macdSlow = input.int(26, "MACD Slow")

macdSignal = input.int(9, "MACD Signal")

macdZeroTh = input.float(0.2, "MOU: MACD near-zero threshold", step=0.05)

volLookback = input.int(5, "Volume MA days", minval=1)

volMinRatio = input.float(1.3, "MOU: Volume ratio min", step=0.1)

volStrong = input.float(1.5, "Strong volume ratio (Breakout/KAKU)", step=0.1)

volMaxRatio = input.float(3.0, "Volume ratio max (filter)", step=0.1)

wickBodyMult = input.float(2.0, "Pinbar: lowerWick >= body*x", step=0.1)

pivotLen = input.int(20, "Resistance lookback", minval=5)

pullMinPct = input.float(5.0, "Pullback min (%)", step=0.1)

pullMaxPct = input.float(15.0, "Pullback max (%)", step=0.1)

breakLookbackBars = input.int(5, "Pullback route: valid bars after break", minval=1)

// --- Breakout route (押し目なし初動ブレイク) ---

useBreakoutRoute = input.bool(true, "Enable MOU Breakout Route (no pullback)")

breakConfirmPct = input.float(0.3, "Break confirm: close > R*(1+%)", step=0.1)

bigBodyLookback = input.int(20, "Break candle body MA length", minval=5)

bigBodyMult = input.float(1.2, "Break candle: body >= MA*mult", step=0.1)

requireCloseNearHigh = input.bool(true, "Break candle: close near high")

closeNearHighPct = input.float(25.0, "Close near high threshold (% of range)", step=1.0)

allowMACDAboveZeroInstead = input.bool(true, "Breakout route: allow MACD GC above zero instead")

// 表示

showEMA = input.bool(true, "Plot EMAs")

showMou = input.bool(true, "Show MOU label")

showKaku = input.bool(true, "Show KAKU label")

// ★ここを改善:デバッグ表はデフォルトON

showDebugTbl = input.bool(true, "Show debug table (last bar)")

// ★稼働確認ラベル(最終足に必ず出す)

showStatusLbl = input.bool(true, "Show status label (last bar always)")

locChoice = input.string("Below Bar", "Label location", options= )

lblLoc = locChoice == "Below Bar" ? location.belowbar : location.abovebar

// =========================

// EMA

// =========================

emaS = ta.ema(close, emaSLen)

emaM = ta.ema(close, emaMLen)

emaL = ta.ema(close, emaLLen)

plot(showEMA ? emaS : na, color=color.new(color.yellow, 0), title="EMA 5")

plot(showEMA ? emaM : na, color=color.new(color.blue, 0), title="EMA 13")

plot(showEMA ? emaL : na, color=color.new(color.orange, 0), title="EMA 26")

emaUpS = emaS > emaS

emaUpM = emaM > emaM

emaUpL = emaL > emaL

goldenOrder = emaS > emaM and emaM > emaL

above26_2days = close > emaL and close > emaL

// 勝率維持の土台(緩めない)

baseTrendOK = (emaUpS and emaUpM and emaUpL) and goldenOrder and above26_2days

// =========================

// MACD

// =========================

= ta.macd(close, macdFast, macdSlow, macdSignal)

macdGC = ta.crossover(macdLine, macdSig)

macdUp = macdLine > macdLine

macdNearZero = math.abs(macdLine) <= macdZeroTh

macdGCAboveZero = macdGC and macdLine > 0 and macdSig > 0

macdMouOK = macdGC and macdNearZero and macdUp

macdBreakOK = allowMACDAboveZeroInstead ? (macdMouOK or macdGCAboveZero) : macdMouOK

// =========================

// Volume

// =========================

volMA = ta.sma(volume, volLookback)

volRatio = volMA > 0 ? (volume / volMA) : na

volumeMouOK = volRatio >= volMinRatio and volRatio <= volMaxRatio

volumeStrongOK = volRatio >= volStrong and volRatio <= volMaxRatio

// =========================

// Candle patterns

// =========================

body = math.abs(close - open)

upperWick = high - math.max(open, close)

lowerWick = math.min(open, close) - low

pinbar = (lowerWick >= wickBodyMult * body) and (lowerWick > upperWick) and (close >= open)

bullEngulf =

close > open and close < open and

close >= open and open <= close

bigBull =

close > open and

open < emaM and close > emaS and

(body > ta.sma(body, 20))

candleOK = pinbar or bullEngulf or bigBull

// =========================

// Resistance / Pullback route

// =========================

res = ta.highest(high, pivotLen)

pullbackPct = res > 0 ? (res - close) / res * 100.0 : na

pullbackOK = pullbackPct >= pullMinPct and pullbackPct <= pullMaxPct

brokeRes = ta.crossover(close, res )

barsSinceBreak = ta.barssince(brokeRes)

afterBreakZone = (barsSinceBreak >= 0) and (barsSinceBreak <= breakLookbackBars)

pullbackRouteOK = afterBreakZone and pullbackOK

// =========================

// Breakout route (押し目なし初動ブレイク)

// =========================

breakConfirm = close > res * (1.0 + breakConfirmPct / 100.0)

bullBreak = close > open

bodyMA = ta.sma(body, bigBodyLookback)

bigBodyOK = bodyMA > 0 ? (body >= bodyMA * bigBodyMult) : false

rng = math.max(high - low, syminfo.mintick)

closeNearHighOK = not requireCloseNearHigh ? true : ((high - close) / rng * 100.0 <= closeNearHighPct)

mou_breakout =

useBreakoutRoute and

baseTrendOK and

breakConfirm and

bullBreak and

bigBodyOK and

closeNearHighOK and

volumeStrongOK and

macdBreakOK

mou_pullback = baseTrendOK and volumeMouOK and candleOK and macdMouOK and pullbackRouteOK

mou = mou_pullback or mou_breakout

// =========================

// KAKU (Strict): 8条件 + 最終三点

// =========================

cond1 = emaUpS and emaUpM and emaUpL

cond2 = goldenOrder

cond3 = above26_2days

cond4 = macdGCAboveZero

cond5 = volumeMouOK

cond6 = candleOK

cond7 = pullbackOK

cond8 = pullbackRouteOK

all8_strict = cond1 and cond2 and cond3 and cond4 and cond5 and cond6 and cond7 and cond8

final3 = pinbar and macdGCAboveZero and volumeStrongOK

kaku = all8_strict and final3

// =========================

// Display (猛 / 猛B / 確)

// =========================

showKakuNow = showKaku and kaku

showMouPull = showMou and mou_pullback and not kaku

showMouBrk = showMou and mou_breakout and not kaku

plotshape(showMouPull, title="MOU_PULLBACK", style=shape.labelup, text="猛",

color=color.new(color.lime, 0), textcolor=color.black, location=lblLoc, size=size.tiny)

plotshape(showMouBrk, title="MOU_BREAKOUT", style=shape.labelup, text="猛B",

color=color.new(color.lime, 0), textcolor=color.black, location=lblLoc, size=size.tiny)

plotshape(showKakuNow, title="KAKU", style=shape.labelup, text="確",

color=color.new(color.yellow, 0), textcolor=color.black, location=lblLoc, size=size.small)

// =========================

// ★稼働確認:最終足に必ず出すステータスラベル

// =========================

var label status = na

if showStatusLbl and barstate.islast

label.delete(status)

statusTxt =

"MNO RUNNING\n" +

"MOU: " + (mou ? "YES" : "no") + " (pull=" + (mou_pullback ? "Y" : "n") + " / brk=" + (mou_breakout ? "Y" : "n") + ")\n" +

"KAKU: " + (kaku ? "YES" : "no") + "\n" +

"BaseTrend: " + (baseTrendOK ? "OK" : "NO") + "\n" +

"MACD(mou): " + (macdMouOK ? "OK" : "NO") + " / MACD(zeroGC): " + (macdGCAboveZero ? "OK" : "NO") + "\n" +

"Vol: " + (na(volRatio) ? "na" : str.tostring(volRatio, format.mintick)) + "\n" +

"Pull%: " + (na(pullbackPct) ? "na" : str.tostring(pullbackPct, format.mintick))

status := label.new(bar_index, high, statusTxt, style=label.style_label_left,

textcolor=color.white, color=color.new(color.black, 0))

// =========================

// Alerts

// =========================

alertcondition(mou, title="MNO_MOU", message="MNO: MOU triggered")

alertcondition(mou_breakout, title="MNO_MOU_BREAKOUT", message="MNO: MOU Breakout triggered")

alertcondition(mou_pullback, title="MNO_MOU_PULLBACK", message="MNO: MOU Pullback triggered")

alertcondition(kaku, title="MNO_KAKU", message="MNO: KAKU triggered")

// =========================

// Debug table (optional)

// =========================

var table t = table.new(position.top_right, 2, 14, border_width=1, border_color=color.new(color.white, 60))

fRow(_name, _cond, _r) =>

bg = _cond ? color.new(color.lime, 70) : color.new(color.red, 80)

tx = _cond ? "OK" : "NO"

table.cell(t, 0, _r, _name, text_color=color.white, bgcolor=color.new(color.black, 0))

table.cell(t, 1, _r, tx, text_color=color.white, bgcolor=bg)

if showDebugTbl and barstate.islast

table.cell(t, 0, 0, "MNO Debug", text_color=color.white, bgcolor=color.new(color.black, 0))

table.cell(t, 1, 0, "", text_color=color.white, bgcolor=color.new(color.black, 0))

fRow("BaseTrend", baseTrendOK, 1)

fRow("MOU Pullback", mou_pullback, 2)

fRow("MOU Breakout", mou_breakout, 3)

fRow("Break confirm", breakConfirm, 4)

fRow("Break big body", bigBodyOK, 5)

fRow("Break close high", closeNearHighOK, 6)

fRow("Break vol strong", volumeStrongOK, 7)

fRow("Break MACD", macdBreakOK, 8)

fRow("KAKU all8", all8_strict, 9)

fRow("KAKU final3", final3, 10)

fRow("MOU any", mou, 11)

fRow("KAKU", kaku, 12)

takeshi_2Step_Screener_MOU_KAKU_FIXED3//@version=5

indicator("MNO_2Step_Screener_MOU_KAKU_FIXED3", overlay=true, max_labels_count=500)

// =========================

// Inputs

// =========================

emaSLen = input.int(5, "EMA Short (5)")

emaMLen = input.int(13, "EMA Mid (13)")

emaLLen = input.int(26, "EMA Long (26)")

macdFast = input.int(12, "MACD Fast")

macdSlow = input.int(26, "MACD Slow")

macdSignal = input.int(9, "MACD Signal")

macdZeroTh = input.float(0.2, "MOU: MACD near-zero threshold", step=0.05)

volLookback = input.int(5, "Volume MA days", minval=1)

volMinRatio = input.float(1.3, "MOU: Volume ratio min", step=0.1)

volStrong = input.float(1.5, "Strong volume ratio (Breakout/KAKU)", step=0.1)

volMaxRatio = input.float(3.0, "Volume ratio max (filter)", step=0.1)

wickBodyMult = input.float(2.0, "Pinbar: lowerWick >= body*x", step=0.1)

pivotLen = input.int(20, "Resistance lookback", minval=5)

pullMinPct = input.float(5.0, "Pullback min (%)", step=0.1)

pullMaxPct = input.float(15.0, "Pullback max (%)", step=0.1)

breakLookbackBars = input.int(5, "Pullback route: valid bars after break", minval=1)

// --- Breakout route (押し目なし初動ブレイク) ---

useBreakoutRoute = input.bool(true, "Enable MOU Breakout Route (no pullback)")

breakConfirmPct = input.float(0.3, "Break confirm: close > R*(1+%)", step=0.1)

bigBodyLookback = input.int(20, "Break candle body MA length", minval=5)

bigBodyMult = input.float(1.2, "Break candle: body >= MA*mult", step=0.1)

requireCloseNearHigh = input.bool(true, "Break candle: close near high")

closeNearHighPct = input.float(25.0, "Close near high threshold (% of range)", step=1.0)

allowMACDAboveZeroInstead = input.bool(true, "Breakout route: allow MACD GC above zero instead")

// 表示

showEMA = input.bool(true, "Plot EMAs")

showMou = input.bool(true, "Show MOU label")

showKaku = input.bool(true, "Show KAKU label")

showDebugTbl = input.bool(false, "Show debug table (last bar)")

locChoice = input.string("Below Bar", "Label location", options= )

lblLoc = locChoice == "Below Bar" ? location.belowbar : location.abovebar

// =========================

// EMA

// =========================

emaS = ta.ema(close, emaSLen)

emaM = ta.ema(close, emaMLen)

emaL = ta.ema(close, emaLLen)

// plot は if の中に入れない(naで制御)

plot(showEMA ? emaS : na, color=color.new(color.yellow, 0), title="EMA 5")

plot(showEMA ? emaM : na, color=color.new(color.blue, 0), title="EMA 13")

plot(showEMA ? emaL : na, color=color.new(color.orange, 0), title="EMA 26")

emaUpS = emaS > emaS

emaUpM = emaM > emaM

emaUpL = emaL > emaL

goldenOrder = emaS > emaM and emaM > emaL

above26_2days = close > emaL and close > emaL

// 勝率維持の土台(緩めない)

baseTrendOK = (emaUpS and emaUpM and emaUpL) and goldenOrder and above26_2days

// =========================

// MACD

// =========================

= ta.macd(close, macdFast, macdSlow, macdSignal)

macdGC = ta.crossover(macdLine, macdSig)

macdUp = macdLine > macdLine

macdNearZero = math.abs(macdLine) <= macdZeroTh

macdGCAboveZero = macdGC and macdLine > 0 and macdSig > 0

macdMouOK = macdGC and macdNearZero and macdUp

macdBreakOK = allowMACDAboveZeroInstead ? (macdMouOK or macdGCAboveZero) : macdMouOK

// =========================

// Volume

// =========================

volMA = ta.sma(volume, volLookback)

volRatio = volMA > 0 ? (volume / volMA) : na

volumeMouOK = volRatio >= volMinRatio and volRatio <= volMaxRatio

volumeStrongOK = volRatio >= volStrong and volRatio <= volMaxRatio

// =========================

// Candle patterns

// =========================

body = math.abs(close - open)

upperWick = high - math.max(open, close)

lowerWick = math.min(open, close) - low

pinbar = (lowerWick >= wickBodyMult * body) and (lowerWick > upperWick) and (close >= open)

bullEngulf =

close > open and close < open and

close >= open and open <= close

bigBull =

close > open and

open < emaM and close > emaS and

(body > ta.sma(body, 20))

candleOK = pinbar or bullEngulf or bigBull

// =========================

// Resistance / Pullback route

// =========================

res = ta.highest(high, pivotLen)

pullbackPct = res > 0 ? (res - close) / res * 100.0 : na

pullbackOK = pullbackPct >= pullMinPct and pullbackPct <= pullMaxPct

brokeRes = ta.crossover(close, res )

barsSinceBreak = ta.barssince(brokeRes)

afterBreakZone = (barsSinceBreak >= 0) and (barsSinceBreak <= breakLookbackBars)

pullbackRouteOK = afterBreakZone and pullbackOK

// =========================

// Breakout route (押し目なし初動ブレイク)

// =========================

breakConfirm = close > res * (1.0 + breakConfirmPct / 100.0)

bullBreak = close > open

bodyMA = ta.sma(body, bigBodyLookback)

bigBodyOK = bodyMA > 0 ? (body >= bodyMA * bigBodyMult) : false

rng = math.max(high - low, syminfo.mintick)

closeNearHighOK = not requireCloseNearHigh ? true : ((high - close) / rng * 100.0 <= closeNearHighPct)

mou_breakout =

useBreakoutRoute and

baseTrendOK and

breakConfirm and

bullBreak and

bigBodyOK and

closeNearHighOK and

volumeStrongOK and

macdBreakOK

mou_pullback = baseTrendOK and volumeMouOK and candleOK and macdMouOK and pullbackRouteOK

mou = mou_pullback or mou_breakout

// =========================

// KAKU (Strict): 8条件 + 最終三点

// =========================

cond1 = emaUpS and emaUpM and emaUpL

cond2 = goldenOrder

cond3 = above26_2days

cond4 = macdGCAboveZero

cond5 = volumeMouOK

cond6 = candleOK

cond7 = pullbackOK

cond8 = pullbackRouteOK

all8_strict = cond1 and cond2 and cond3 and cond4 and cond5 and cond6 and cond7 and cond8

final3 = pinbar and macdGCAboveZero and volumeStrongOK

kaku = all8_strict and final3

// =========================

// Display (統一ラベル)

// =========================

showKakuNow = showKaku and kaku

showMouPull = showMou and mou_pullback and not kaku

showMouBrk = showMou and mou_breakout and not kaku

plotshape(showMouPull, title="MOU_PULLBACK", style=shape.labelup, text="猛",

color=color.new(color.lime, 0), textcolor=color.black, location=lblLoc, size=size.tiny)

plotshape(showMouBrk, title="MOU_BREAKOUT", style=shape.labelup, text="猛B",

color=color.new(color.lime, 0), textcolor=color.black, location=lblLoc, size=size.tiny)

plotshape(showKakuNow, title="KAKU", style=shape.labelup, text="確",

color=color.new(color.yellow, 0), textcolor=color.black, location=lblLoc, size=size.small)

// =========================

// Alerts

// =========================

alertcondition(mou, title="MNO_MOU", message="MNO: MOU triggered")

alertcondition(mou_breakout, title="MNO_MOU_BREAKOUT", message="MNO: MOU Breakout triggered")

alertcondition(mou_pullback, title="MNO_MOU_PULLBACK", message="MNO: MOU Pullback triggered")

alertcondition(kaku, title="MNO_KAKU", message="MNO: KAKU triggered")

// =========================

// Debug table (optional)

// =========================

var table t = table.new(position.top_right, 2, 14, border_width=1, border_color=color.new(color.white, 60))

fRow(_name, _cond, _r) =>

bg = _cond ? color.new(color.lime, 70) : color.new(color.red, 80)

tx = _cond ? "OK" : "NO"

table.cell(t, 0, _r, _name, text_color=color.white, bgcolor=color.new(color.black, 0))

table.cell(t, 1, _r, tx, text_color=color.white, bgcolor=bg)

if showDebugTbl and barstate.islast

// ❗ colspanは使えないので2セルでヘッダーを作る

table.cell(t, 0, 0, "MNO Debug", text_color=color.white, bgcolor=color.new(color.black, 0))

table.cell(t, 1, 0, "", text_color=color.white, bgcolor=color.new(color.black, 0))

fRow("BaseTrend", baseTrendOK, 1)

fRow("MOU Pullback", mou_pullback, 2)

fRow("MOU Breakout", mou_breakout, 3)

fRow("Break confirm", breakConfirm, 4)

fRow("Break big body", bigBodyOK, 5)

fRow("Break close high", closeNearHighOK, 6)

fRow("Break vol strong", volumeStrongOK, 7)

fRow("Break MACD", macdBreakOK, 8)

fRow("KAKU all8", all8_strict, 9)

fRow("KAKU final3", final3, 10)

fRow("MOU any", mou, 11)

fRow("KAKU", kaku, 12)

Luxy Momentum, Trend, Bias and Breakout Indicators V7

TABLE OF CONTENTS

This is Version 7 (V7) - the latest and most optimized release. If you are using any older versions (V6, V5, V4, V3, etc.), it is highly recommended to replace them with V7.

Why This Indicator is Different

Who Should Use This

Core Components Overview

The UT Bot Trading System

Understanding the Market Bias Table

Candlestick Pattern Recognition

Visual Tools and Features

How to Use the Indicator

Performance and Optimization

FAQ

---

### CREDITS & ATTRIBUTION

This indicator implements proven trading concepts using entirely original code developed specifically for this project.

### CONCEPTUAL FOUNDATIONS

• UT Bot ATR Trailing System

- Original concept by @QuantNomad: (search "UT-Bot-Strategy"

- Our version is a complete reimplementation with significant enhancements:

- Volume-weighted momentum adjustment

- Composite stop loss from multiple S/R layers

- Multi-filter confirmation system (swing, %, 2-bar, ZLSMA)

- Full integration with multi-timeframe bias table

- Visual audit trail with freeze-on-touch

- NOTE: No code was copied - this is a complete reimplementation with enhancements.

• Standard Technical Indicators (Public Domain Formulas):

- Supertrend: ATR-based trend calculation with custom gradient fills

- MACD: Gerald Appel's formula with separation filters

- RSI: J. Welles Wilder's formula with pullback zone logic

- ADX/DMI: Custom trend strength formula inspired by Wilder's directional movement concept, reimplemented with volume weighting and efficiency metrics

- ZLSMA: Zero-lag formula enhanced with Hull MA and momentum prediction

### Custom Implementations

- Trend Strength: Inspired by Wilder's ADX concept but using volume-weighted pressure calculation and efficiency metrics (not traditional +DI/-DI smoothing)

- All code implementations are original

### ORIGINAL FEATURES (70%+ of codebase)

- Multi-Timeframe Bias Table with live updates

- Risk Management System (R-multiple TPs, freeze-on-touch)

- Opening Range Breakout tracker with session management

- Composite Stop Loss calculator using 6+ S/R layers

- Performance optimization system (caching, conditional calcs)

- VIX Fear Index integration

- Previous Day High/Low auto-detection

- Candlestick pattern recognition with interactive tooltips

- Smart label and visual management

- All UI/UX design and table architecture

### DEVELOPMENT PROCESS

**AI Assistance:** This indicator was developed over 2+ months with AI assistance (ChatGPT/Claude) used for:

- Writing Pine Script code based on design specifications

- Optimizing performance and fixing bugs

- Ensuring Pine Script v6 compliance

- Generating documentation

**Author's Role:** All trading concepts, system design, feature selection, integration logic, and strategic decisions are original work by the author. The AI was a coding tool, not the system designer.

**Transparency:** We believe in full disclosure - this project demonstrates how AI can be used as a powerful development tool while maintaining creative and strategic ownership.

---

1. WHY THIS INDICATOR IS DIFFERENT

Most traders use multiple separate indicators on their charts, leading to cluttered screens, conflicting signals, and analysis paralysis. The Suite solves this by integrating proven technical tools into a single, cohesive system.

Key Advantages:

All-in-One Design: Instead of loading 5-10 separate indicators, you get everything in one optimized script. This reduces chart clutter and improves TradingView performance.

Multi-Timeframe Bias Table: Unlike standard indicators that only show the current timeframe, the Bias Table aggregates trend signals across multiple timeframes simultaneously. See at a glance whether 1m, 5m, 15m, 1h are aligned bullish or bearish - no more switching between charts.

Smart Confirmations: The indicator doesn't just give signals - it shows you WHY. Every entry has multiple layers of confirmation (MA cross, MACD momentum, ADX strength, RSI pullback, volume, etc.) that you can toggle on/off.

Dynamic Stop Loss System: Instead of static ATR stops, the SL is calculated from multiple support/resistance layers: UT trailing line, Supertrend, VWAP, swing structure, and MA levels. This creates more intelligent, price-action-aware stops.

R-Multiple Take Profits: Built-in TP system calculates targets based on your initial risk (1R, 1.5R, 2R, 3R). Lines freeze when touched with visual checkmarks, giving you a clean audit trail of partial exits.

Educational Tooltips Everywhere: Every single input has detailed tooltips explaining what it does, typical values, and how it impacts trading. You're not guessing - you're learning as you configure.

Performance Optimized: Smart caching, conditional calculations, and modular design mean the indicator runs fast despite having 15+ features. Turn off what you don't use for even better performance.

No Repainting: All signals respect bar close. Alerts fire correctly. What you see in history is what you would have gotten in real-time.

What Makes It Unique:

Integrated UT Bot + Bias Table: No other indicator combines UT Bot's ATR trailing system with a live multi-timeframe dashboard. You get precision entries with macro trend context.

Candlestick Pattern Recognition with Interactive Tooltips: Patterns aren't just marked - hover over any emoji for a full explanation of what the pattern means and how to trade it.

Opening Range Breakout Tracker: Built-in ORB system for intraday traders with customizable session times and real-time status updates in the Bias Table.

Previous Day High/Low Auto-Detection: Automatically plots PDH/PDL on intraday charts with theme-aware colors. Updates daily without manual input.

Dynamic Row Labels in Bias Table: The table shows your actual settings (e.g., "EMA 10 > SMA 20") not generic labels. You know exactly what's being evaluated.

Modular Filter System: Instead of forcing a fixed methodology, the indicator lets you build your own strategy. Start with just UT Bot, add filters one at a time, test what works for your style.

---

2. WHO WHOULD USE THIS

Designed For:

Intermediate to Advanced Traders: You understand basic technical analysis (MAs, RSI, MACD) and want to combine multiple confirmations efficiently. This isn't a "one-click profit" system - it's a professional toolkit.

Multi-Timeframe Traders: If you trade one asset but check multiple timeframes for confirmation (e.g., enter on 5m after checking 15m and 1h alignment), the Bias Table will save you hours every week.

Trend Followers: The indicator excels at identifying and following trends using UT Bot, Supertrend, and MA systems. If you trade breakouts and pullbacks in trending markets, this is built for you.

Intraday and Swing Traders: Works equally well on 5m-1h charts (day trading) and 4h-D charts (swing trading). Scalpers can use it too with appropriate settings adjustments.

Discretionary Traders: This isn't a black-box system. You see all the components, understand the logic, and make final decisions. Perfect for traders who want tools, not automation.

Works Across All Markets:

Stocks (US, international)

Cryptocurrency (24/7 markets supported)

Forex pairs

Indices (SPY, QQQ, etc.)

Commodities

NOT Ideal For :

Complete Beginners: If you don't know what a moving average or RSI is, start with basics first. This indicator assumes foundational knowledge.

Algo Traders Seeking Black Box: This is discretionary. Signals require context and confirmation. Not suitable for blind automated execution.

Mean-Reversion Only Traders: The indicator is trend-following at its core. While VWAP bands support mean-reversion, the primary methodology is trend continuation.

---

3. CORE COMPONENTS OVERVIEW

The indicator combines these proven systems:

Trend Analysis:

Moving Averages: Four customizable MAs (Fast, Medium, Medium-Long, Long) with six types to choose from (EMA, SMA, WMA, VWMA, RMA, HMA). Mix and match for your style.

Supertrend: ATR-based trend indicator with unique gradient fill showing trend strength. One-sided ribbon visualization makes it easier to see momentum building or fading.

ZLSMA : Zero-lag linear-regression smoothed moving average. Reduces lag compared to traditional MAs while maintaining smooth curves.

Momentum & Filters:

MACD: Standard MACD with separation filter to avoid weak crossovers.

RSI: Pullback zone detection - only enter longs when RSI is in your defined "buy zone" and shorts in "sell zone".

ADX/DMI: Trend strength measurement with directional filter. Ensures you only trade when there's actual momentum.

Volume Filter: Relative volume confirmation - require above-average volume for entries.

Donchian Breakout: Optional channel breakout requirement.

Signal Systems:

UT Bot: The primary signal generator. ATR trailing stop that adapts to volatility and gives clear entry/exit points.

Base Signals: MA cross system with all the above filters applied. More conservative than UT Bot alone.

Market Bias Table: Multi-timeframe dashboard showing trend alignment across 7 timeframes plus macro bias (3-day, weekly, monthly, quarterly, VIX).

Candlestick Patterns: Six major reversal patterns auto-detected with interactive tooltips.

ORB Tracker: Opening range high/low with breakout status (intraday only).

PDH/PDL: Previous day levels plotted automatically on intraday charts.

VWAP + Bands : Session-anchored VWAP with up to three standard deviation band pairs.

---

4. THE UT BOT TRADING SYSTEM

The UT Bot is the heart of the indicator's signal generation. It's an advanced ATR trailing stop that adapts to market volatility.

Why UT Bot is Superior to Fixed Stops:

Traditional ATR stops use a fixed multiplier (e.g., "stop = entry - 2×ATR"). UT Bot is smarter:

It TRAILS the stop as price moves in your favor

It WIDENS during high volatility to avoid premature stops

It TIGHTENS during consolidation to lock in profits

It FLIPS when price breaks the trailing line, signaling reversals

Visual Elements You'll See:

Orange Trailing Line: The actual UT stop level that adapts bar-by-bar

Buy/Sell Labels: Aqua triangle (long) or orange triangle (short) when the line flips

ENTRY Line: Horizontal line at your entry price (optional, can be turned off)

Suggested Stop Loss: A composite SL calculated from multiple support/resistance layers:

- UT trailing line

- Supertrend level

- VWAP

- Swing structure (recent lows/highs)

- Long-term MA (200)

- ATR-based floor

Take Profit Lines: TP1, TP1.5, TP2, TP3 based on R-multiples. When price touches a TP, it's marked with a checkmark and the line freezes for audit trail purposes.

Status Messages: "SL Touched ❌" or "SL Frozen" when the trade leg completes.

How UT Bot Differs from Other ATR Systems:

Multiple Filters Available: You can require 2-bar confirmation, minimum % price change, swing structure alignment, or ZLSMA directional filter. Most UT implementations have none of these.

Smart SL Calculation: Instead of just using the UT line as your stop, the indicator suggests a better SL based on actual support/resistance. This prevents getting stopped out by wicks while keeping risk controlled.

Visual Audit Trail: All SL/TP lines freeze when touched with clear markers. You can review your trades weeks later and see exactly where entries, stops, and targets were.

Performance Options: "Draw UT visuals only on bar close" lets you reduce rendering load without affecting logic or alerts - critical for slower machines or 1m charts.

Trading Logic:

UT Bot flips direction (Buy or Sell signal appears)

Check Bias Table for multi-timeframe confirmation

Optional: Wait for Base signal or candlestick pattern

Enter at signal bar close or next bar open

Place stop at "Suggested Stop Loss" line

Scale out at TP levels (TP1, TP2, TP3)

Exit remaining position on opposite UT signal or stop hit

---

5. UNDERSTANDING THE MARKET BIAS TABLE

This is the indicator's unique multi-timeframe intelligence layer. Instead of looking at one chart at a time, the table aggregates signals across seven timeframes plus macro trend bias.

Why Multi-Timeframe Analysis Matters:

Professional traders check higher and lower timeframes for context:

Is the 1h uptrend aligning with my 5m entry?

Are all short-term timeframes bullish or just one?

Is the daily trend supportive or fighting me?

Doing this manually means opening multiple charts, checking each indicator, and making mental notes. The Bias Table does it automatically in one glance.

Table Structure:

Header Row:

On intraday charts: 1m, 5m, 15m, 30m, 1h, 2h, 4h (toggle which ones you want)

On daily+ charts: D, W, M (automatic)

Green dot next to title = live updating

Headline Rows - Macro Bias:

These show broad market direction over longer periods:

3 Day Bias: Trend over last 3 trading sessions (uses 1h data)

Weekly Bias: Trend over last 5 trading sessions (uses 4h data)

Monthly Bias: Trend over last 30 daily bars

Quarterly Bias: Trend over last 13 weekly bars

VIX Fear Index: Market regime based on VIX level - bullish when low, bearish when high

Opening Range Breakout: Status of price vs. session open range (intraday only)

These rows show text: "BULLISH", "BEARISH", or "NEUTRAL"

Indicator Rows - Technical Signals:

These evaluate your configured indicators across all active timeframes:

Fast MA > Medium MA (shows your actual MA settings, e.g., "EMA 10 > SMA 20")

Price > Long MA (e.g., "Price > SMA 200")

Price > VWAP

MACD > Signal

Supertrend (up/down/neutral)

ZLSMA Rising

RSI In Zone

ADX ≥ Minimum

These rows show emojis: GREEB (bullish), RED (bearish), GRAY/YELLOW (neutral/NA)

AVG Column:

Shows percentage of active timeframes that are bullish for that row. This is the KEY metric:

AVG > 70% = strong multi-timeframe bullish alignment

AVG 40-60% = mixed/choppy, no clear trend

AVG < 30% = strong multi-timeframe bearish alignment

How to Use the Table:

For a long trade:

Check AVG column - want to see > 60% ideally

Check headline bias rows - want to see BULLISH, not BEARISH

Check VIX row - bullish market regime preferred

Check ORB row (intraday) - want ABOVE for longs

Scan indicator rows - more green = better confirmation

For a short trade:

Check AVG column - want to see < 40% ideally

Check headline bias rows - want to see BEARISH, not BULLISH

Check VIX row - bearish market regime preferred

Check ORB row (intraday) - want BELOW for shorts

Scan indicator rows - more red = better confirmation

When AVG is 40-60%:

Market is choppy, mixed signals. Either stay out or reduce position size significantly. These are low-probability environments.

Unique Features:

Dynamic Labels: Row names show your actual settings (e.g., "EMA 10 > SMA 20" not generic "Fast > Slow"). You know exactly what's being evaluated.

Customizable Rows: Turn off rows you don't care about. Only show what matters to your strategy.

Customizable Timeframes: On intraday charts, disable 1m or 4h if you don't trade them. Reduces calculation load by 20-40%.

Automatic HTF Handling: On Daily/Weekly/Monthly charts, the table automatically switches to D/W/M columns. No configuration needed.

Performance Smart: "Hide BIAS table on 1D or above" option completely skips all table calculations on higher timeframes if you only trade intraday.

---

6. CANDLESTICK PATTERN RECOGNITION

The indicator automatically detects six major reversal patterns and marks them with emojis at the relevant bars.

Why These Six Patterns:

These are the most statistically significant reversal patterns according to trading literature:

High win rate when appearing at support/resistance

Clear visual structure (not subjective)

Work across all timeframes and assets

Studied extensively by institutions

The Patterns:

Bullish Patterns (appear at bottoms):

Bullish Engulfing: Green candle completely engulfs prior red candle's body. Strong reversal signal.

Hammer: Small body with long lower wick (at least 2× body size). Shows rejection of lower prices by buyers.

Morning Star: Three-candle pattern (large red → small indecision → large green). Very strong bottom reversal.

Bearish Patterns (appear at tops):

Bearish Engulfing: Red candle completely engulfs prior green candle's body. Strong reversal signal.

Shooting Star: Small body with long upper wick (at least 2× body size). Shows rejection of higher prices by sellers.

Evening Star: Three-candle pattern (large green → small indecision → large red). Very strong top reversal.

Interactive Tooltips:

Unlike most pattern indicators that just draw shapes, this one is educational:

Hover your mouse over any pattern emoji

A tooltip appears explaining: what the pattern is, what it means, when it's most reliable, and how to trade it

No need to memorize - learn as you trade

Noise Filter:

"Min candle body % to filter noise" setting prevents false signals:

Patterns require minimum body size relative to price

Filters out tiny candles that don't represent real buying/selling pressure

Adjust based on asset volatility (higher % for crypto, lower for low-volatility stocks)

How to Trade Patterns:

Patterns are NOT standalone entry signals. Use them as:

Confirmation: UT Bot gives signal + pattern appears = stronger entry

Reversal Warning: In a trade, opposite pattern appears = consider tightening stop or taking profit

Support/Resistance Validation: Pattern at key level (PDH, VWAP, MA 200) = level is being respected

Best combined with:

UT Bot or Base signal in same direction

Bias Table alignment (AVG > 60% or < 40%)

Appearance at obvious support/resistance

---

7. VISUAL TOOLS AND FEATURES

VWAP (Volume Weighted Average Price):

Session-anchored VWAP with standard deviation bands. Shows institutional "fair value" for the trading session.

Anchor Options: Session, Day, Week, Month, Quarter, Year. Choose based on your trading timeframe.

Bands: Up to three pairs (X1, X2, X3) showing statistical deviation. Price at outer bands often reverses.

Auto-Hide on HTF: VWAP hides on Daily/Weekly/Monthly charts automatically unless you enable anchored mode.

Use VWAP as:

Directional bias (above = bullish, below = bearish)

Mean reversion levels (outer bands)

Support/resistance (the VWAP line itself)

Previous Day High/Low:

Automatically plots yesterday's high and low on intraday charts:

Updates at start of each new trading day

Theme-aware colors (dark text for light charts, light text for dark charts)

Hidden automatically on Daily/Weekly/Monthly charts

These levels are critical for intraday traders - institutions watch them closely as support/resistance.

Opening Range Breakout (ORB):

Tracks the high/low of the first 5, 15, 30, or 60 minutes of the trading session:

Customizable session times (preset for NYSE, LSE, TSE, or custom)

Shows current breakout status in Bias Table row (ABOVE, BELOW, INSIDE, BUILDING)

Intraday only - auto-disabled on Daily+ charts

ORB is a classic day trading strategy - breakout above opening range often leads to continuation.

Extra Labels:

Change from Open %: Shows how far price has moved from session open (intraday) or daily open (HTF). Green if positive, red if negative.

ADX Badge: Small label at bottom of last bar showing current ADX value. Green when above your minimum threshold, red when below.

RSI Badge: Small label at top of last bar showing current RSI value with zone status (buy zone, sell zone, or neutral).

These labels provide quick at-a-glance confirmation without needing separate indicator windows.

---

8. HOW TO USE THE INDICATOR

Step 1: Add to Chart

Load the indicator on your chosen asset and timeframe

First time: Everything is enabled by default - the chart will look busy

Don't panic - you'll turn off what you don't need

Step 2: Start Simple

Turn OFF everything except:

UT Bot labels (keep these ON)

Bias Table (keep this ON)

Moving Averages (Fast and Medium only)

Suggested Stop Loss and Take Profits

Hide everything else initially. Get comfortable with the basic UT Bot + Bias Table workflow first.

Step 3: Learn the Core Workflow

UT Bot gives a Buy or Sell signal

Check Bias Table AVG column - do you have multi-timeframe alignment?

If yes, enter the trade

Place stop at Suggested Stop Loss line

Scale out at TP levels

Exit on opposite UT signal

Trade this simple system for a week. Get a feel for signal frequency and win rate with your settings.

Step 4: Add Filters Gradually

If you're getting too many losing signals (whipsaws in choppy markets), add filters one at a time:

Try: "Require 2-Bar Trend Confirmation" - wait for 2 bars to confirm direction

Try: ADX filter with minimum threshold - only trade when trend strength is sufficient

Try: RSI pullback filter - only enter on pullbacks, not chasing

Try: Volume filter - require above-average volume

Add one filter, test for a week, evaluate. Repeat.

Step 5: Enable Advanced Features (Optional)

Once you're profitable with the core system, add:

Supertrend for additional trend confirmation

Candlestick patterns for reversal warnings

VWAP for institutional anchor reference

ORB for intraday breakout context

ZLSMA for low-lag trend following

Step 6: Optimize Settings

Every setting has a detailed tooltip explaining what it does and typical values. Hover over any input to read:

What the parameter controls

How it impacts trading

Suggested ranges for scalping, day trading, and swing trading

Start with defaults, then adjust based on your results and style.

Step 7: Set Up Alerts

Right-click chart → Add Alert → Condition: "Luxy Momentum v6" → Choose:

"UT Bot — Buy" for long entries

"UT Bot — Sell" for short entries

"Base Long/Short" for filtered MA cross signals

Optionally enable "Send real-time alert() on UT flip" in settings for immediate notifications.

Common Workflow Variations:

Conservative Trader:

UT signal + Base signal + Candlestick pattern + Bias AVG > 70%

Enter only at major support/resistance

Wider UT sensitivity, multiple filters

Aggressive Trader:

UT signal + Bias AVG > 60%

Enter immediately, no waiting

Tighter UT sensitivity, minimal filters

Swing Trader:

Focus on Daily/Weekly Bias alignment

Ignore intraday noise

Use ORB and PDH/PDL less (or not at all)

Wider stops, patient approach

---

9. PERFORMANCE AND OPTIMIZATION

The indicator is optimized for speed, but with 15+ features running simultaneously, chart load time can add up. Here's how to keep it fast:

Biggest Performance Gains:

Disable Unused Timeframes: In "Time Frames" settings, turn OFF any timeframe you don't actively trade. Each disabled TF saves 10-15% calculation time. If you only day trade 5m, 15m, 1h, disable 1m, 2h, 4h.

Hide Bias Table on Daily+: If you only trade intraday, enable "Hide BIAS table on 1D or above". This skips ALL table calculations on higher timeframes.

Draw UT Visuals Only on Bar Close: Reduces intrabar rendering of SL/TP/Entry lines. Has ZERO impact on logic or alerts - purely visual optimization.

Additional Optimizations:

Turn off VWAP bands if you don't use them

Disable candlestick patterns if you don't trade them

Turn off Supertrend fill if you find it distracting (keep the line)

Reduce "Limit to 10 bars" for SL/TP lines to minimize line objects

Performance Features Built-In:

Smart Caching: Higher timeframe data (3-day bias, weekly bias, etc.) updates once per day, not every bar

Conditional Calculations: Volume filter only calculates when enabled. Swing filter only runs when enabled. Nothing computes if turned off.

Modular Design: Every component is independent. Turn off what you don't need without breaking other features.

Typical Load Times:

5m chart, all features ON, 7 timeframes: ~2-3 seconds

5m chart, core features only, 3 timeframes: ~1 second

1m chart, all features: ~4-5 seconds (many bars to calculate)

If loading takes longer, you likely have too many indicators on the chart total (not just this one).

---

10. FAQ

Q: How is this different from standard UT Bot indicators?

A: Standard UT Bot (originally by @QuantNomad) is just the ATR trailing line and flip signals. This implementation adds:

- Volume weighting and momentum adjustment to the trailing calculation

- Multiple confirmation filters (swing, %, 2-bar, ZLSMA)

- Smart composite stop loss system from multiple S/R layers

- R-multiple take profit system with freeze-on-touch

- Integration with multi-timeframe Bias Table

- Visual audit trail with checkmarks

Q: Can I use this for automated trading?

A: The indicator is designed for discretionary trading. While it has clear signals and alerts, it's not a mechanical system. Context and judgment are required.

Q: Does it repaint?

A: No. All signals respect bar close. UT Bot logic runs intrabar but signals only trigger on confirmed bars. Alerts fire correctly with no lookahead.

Q: Do I need to use all the features?

A: Absolutely not. The indicator is modular. Many profitable traders use just UT Bot + Bias Table + Moving Averages. Start simple, add complexity only if needed.

Q: How do I know which settings to use?

A: Every single input has a detailed tooltip. Hover over any setting to see:

What it does

How it affects trading

Typical values for scalping, day trading, swing trading

Start with defaults, adjust gradually based on results.

Q: Can I use this on crypto 24/7 markets?

A: Yes. ORB will not work (no defined session), but everything else functions normally. Use "Day" anchor for VWAP instead of "Session".

Q: The Bias Table is blank or not showing.

A: Check:

"Show Table" is ON

Table position isn't overlapping another indicator's table (change position)

At least one row is enabled

"Hide BIAS table on 1D or above" is OFF (if on Daily+ chart)

Q: Why are candlestick patterns not appearing?

A: Patterns are relatively rare by design - they only appear at genuine reversal points. Check:

Pattern toggles are ON

"Min candle body %" isn't too high (try 0.05-0.10)

You're looking at a chart with actual reversals (not strong trending market)

Q: UT Bot is too sensitive/not sensitive enough.

A: Adjust "Sensitivity (Key×ATR)". Lower number = tighter stop, more signals. Higher number = wider stop, fewer signals. Read the tooltip for guidance.

Q: Can I get alerts for the Bias Table?

A: The Bias Table is a dashboard for visual analysis, not a signal generator. Set alerts on UT Bot or Base signals, then manually check Bias Table for confirmation.

Q: Does this work on stocks with low volume?

A: Yes, but turn OFF the volume filter. Low volume stocks will never meet relative volume requirements.

Q: How often should I check the Bias Table?

A: Before every entry. It takes 2 seconds to glance at the AVG column and headline rows. This one check can save you from fighting the trend.

Q: What if UT signal and Base signal disagree?

A: UT Bot is more aggressive (ATR trailing). Base signals are more conservative (MA cross + filters). If they disagree, either:

Wait for both to align (safest)

Take the UT signal but with smaller size (aggressive)

Skip the trade (conservative)

There's no "right" answer - depends on your risk tolerance.

---

FINAL NOTES

The indicator gives you an edge. How you use that edge determines results.

For questions, feedback, or support, comment on the indicator page or message the author.

Happy Trading!

Volume Spike Alert & Overlay"Volume Spike Alert & Overlay" highlights unusually high trading volume on a chart. It calculates whether the current volume exceeds a user-defined percentage above the historical average and triggers an alert if it does. The information is also displayed in a customizable on-screen table.

What It Does

Monitors volume for each bar and compares it to an average over a user-defined lookback period.

Supports multiple smoothing methods (SMA, EMA, WMA, RMA) for calculating the average volume.

Triggers an alert when current volume exceeds the threshold percentage above the average.

Displays a table on the chart with:

Current Volume

Average Volume

Threshold Percentage

Optional empty row for spacing/formatting

How It Works

User Inputs:

lookbackPeriods: Number of bars used to calculate the average volume.

thresholdPercent: % above the average that triggers a volume spike alert.

smoothingType: Type of moving average used for volume calculation.

textColor, bgColor: Formatting for the display table.

tablePositionInput: Where the table appears on the chart (e.g., Bottom Right).

Toggles for showing/hiding parts of the table.

Volume Calculations:

Calculates current bar's volume.

Calculates average volume using the selected smoothing method.

Computes the threshold: avgVol * (1 + thresholdPercent / 100).

Compares current volume to threshold.

Table Display:

Dynamically creates a table with volume stats.

Adds rows based on user preferences.

Alerts:

alertcondition fires when currentVol crosses above the calculated threshold.

Message: "Volume Threshold Exceeded"

Usage Examples

Example 1: Spotting High Activity

Apply the script to a stock like AAPL on a 5-minute chart.

Set lookbackPeriods to 20 and thresholdPercent to 30.

Use EMA for more reactive volume tracking.

When volume spikes more than 30% above the 20-period EMA, an alert triggers.

Example 2: Day Trading Filter

For scalpers, apply it to a 1-minute crypto chart (e.g., BTC/USDT).

Set thresholdPercent to 50 to catch only strong surges.

Position the table at the top left and reduce visible info for a clean layout.

Example 3: Long-Term Context

On a daily chart, use SMA and set lookbackPeriods to 50.

Helps identify breakout moves supported by strong volume.

How this is different from Trading View's Volume indicator:

The standard volume plot from trading view allows users to set a alert when the average line is crossed, but it does not allow you to set a custom percentage at which to trigger an alert. This indicator will allow you to set any percentage you wish to monitor and above that percentage threshold will trigger your alert.

===== ORIGINAL DESCRIPTION =====

Volume Spike Alert & Overlay

This indicator will display the following as an overlay on your chart:

Current volume

Average Volume

Threshold for Alert

Description:

This indicator will display the current bar volume based on the chart time frame,

display the average volume based on selected conditions,

allow user selectable threshold over the average volume to trigger an alert.

Options:

Average lookback period

Smoothing type

Alert Threshold %

Enable / Disable Each Value

Change Text Color

Change Background Color

Change Table location

Add/Remove extra row for placement in top corner

Usage Example:

I use this indicator to alert when the current volume exceeds the average volume by a specified percentage to alert to volume spikes.

Set the threshold to 25% in the settings

Create an alert by clicking on the 3 dots on the right of the indicator title on the chart

When the threshold is exceeded the alert will trigger

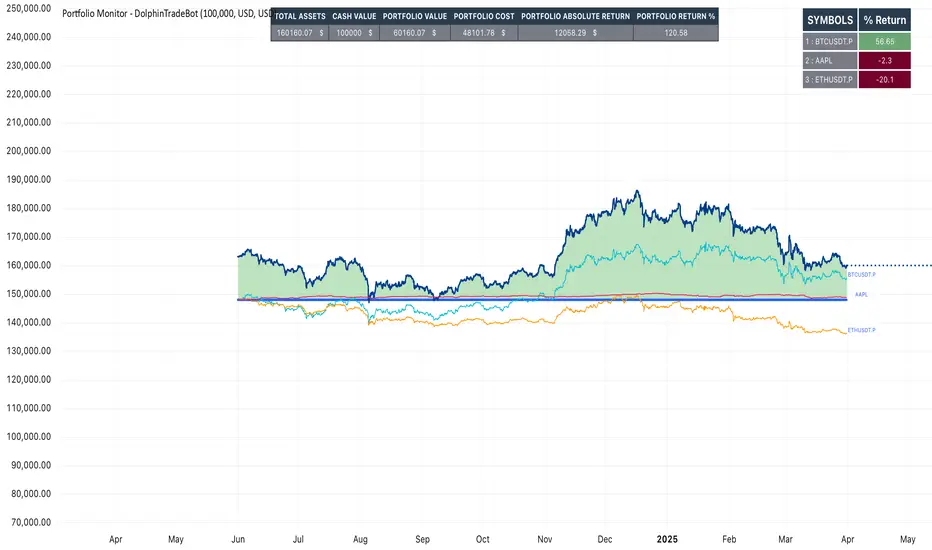

Portfolio Monitor - DolphinTradeBot1️⃣ Overview

▪️This indicator unifies the value of all your investments—whether stocks, currencies, or cryptocurrencies—in your chosen currency. This tool not only provides a clear snapshot of your overall portfolio performance but also highlights the individual growth of each asset with intuitive visualizations and an easy-to-understand performance report.

2️⃣ What sets this indicator apart

▪️is its ability to convert values from various currency pairs into any currency you choose. This means you can monitor your portfolio's performance against any currency pair you prefer, offering a flexible and comprehensive view of your investments.

3️⃣ How Is It Work ?

🔍The indicator can be analyzed under two main categories: visual representations and tables.

1- Visual representations ;

The indicator includes three different types of lines:

1. 1 - Reference Line → This represents the cost of all assets we hold, based on the selected date.

1. 2 - Total Assets Line → Displays the real-time value of all assets in our possession, including cash value, in the selected trading pair.

The area between the reference line is filled with green and red. The section above the reference line is represented in green, while the section below is shown in red.

1. 3 - Performance Lines → These visualize the performance of the assets, starting from the reference line and taking into account their weights in the portfolio. (Note: The lines are scaled for visualization purposes, so their absolute values should not be considered.)

"The names of the lines are shown in the image below."⤵️

2- Tables

The indicator includes three different types of tables:

2. 1 - Analysis Table : It provides a superficial overview of wallet statistics and values.

▪️TOTAL ASSETS → The current equivalent of all assets in the target currency

▪️CASH VALUE → The current value of the amount "Cash Value", in the target currency.

▪️PORTFOLIO VALUE → The total value of assets excluding Cash, in the target currency.

▪️POSTFOLIO COST → The cost of assets excluding Cash, in the target currency.

▪️PORTFOLIO ABSOLUTE RETURN → It shows the profit or loss relative to the cost of assets

▪️PORTFOLIO RETURN % →It shows the profit or loss relative to the cost of assets on a percentage basis

2. 2 - Performance Table : It displays the names of assets excluding Cash and their profit amounts, sorted from highest to lowest profit. If "Show as Percentage" is selected in the settings, it shows the percentage profit or loss relative to the cost. Profits are represented in green, while losses are represented in red.

"You can see the visual showing the tables below"⤵️

4️⃣How to Use ?

1- Choose the date on which the visualization will begin (📌The start date only affects the exchange rate used for calculating the reference line in the target currency.)

2- If you have cash holdings, enter the amount and specify the currency.

3- Select the currency in which your portfolio value will be displayed.(Default value is USD)

4- To set up your portfolio;

SYMBOLS - QUANTITY - PURCHASE PRICE

Enter the symbols of your assets - the number of units you hold - and their cost levels.

5- If you have cash, be sure to include your cash balance. If you also hold other currencies, enter them as separate assets with their corresponding quantities and purchase prices.

6- If you want to see the percentage returns of the assets in the performance table relative to their cost, select the "Show as Percent" option.

7- If you want to see the performance visuals of the assets, click on the "Show Asset Performance" option.

You can find an image of the settings section where the numbers above are used as references below.⤵️

📌 NOTE → By default, a few assets and their values have been pre-added in the initial settings. This is to ensure that you don’t see an empty screen when adding the indicator to the chart. Please remember to enter your own assets and values. The default settings are only provided as an example.

Historical High/Lows Statistical Analysis(More Timeframe interval options coming in the future)

Indicator Description

The Hourly and Weekly High/Low (H/L) Analysis indicator provides a powerful tool for tracking the most frequent high and low points during different periods, specifically on an hourly basis and a weekly basis, broken down by the days of the week (DOTW). This indicator is particularly useful for traders seeking to understand historical behavior and patterns of high/low occurrences across both hourly intervals and weekly days, helping them make more informed decisions based on historical data.

With its customizable options, this indicator is versatile and applicable to a variety of trading strategies, ranging from intraday to swing trading. It is designed to meet the needs of both novice and experienced traders.

Key Features

Hourly High/Low Analysis:

Tracks and displays the frequency of hourly high and low occurrences across a user-defined date range.

Enables traders to identify which hours of the day are historically more likely to set highs or lows, offering valuable insights into intraday price action.

Customizable options for:

Hourly session start and end times.

22-hour session support for futures traders.

Hourly label formatting (e.g., 12-hour or 24-hour format).

Table position, size, and design flexibility.

Weekly High/Low Analysis by Day of the Week (DOTW):

Captures weekly high and low occurrences for each day of the week.

Allows traders to evaluate which days are most likely to produce highs or lows during the week, providing insights into weekly price movement tendencies.

Displays the aggregated counts of highs and lows for each day in a clean, customizable table format.

Options for hiding specific days (e.g., weekends) and customizing table appearance.

User-Friendly Table Display:

Both hourly and weekly data are displayed in separate tables, ensuring clarity and non-interference.

Tables can be positioned on the chart according to user preferences and are designed to be visually appealing yet highly informative.

Customizable Date Range:

Users can specify a start and end date for the analysis, allowing them to focus on specific periods of interest.

Possible Uses

Intraday Traders (Hourly Analysis):