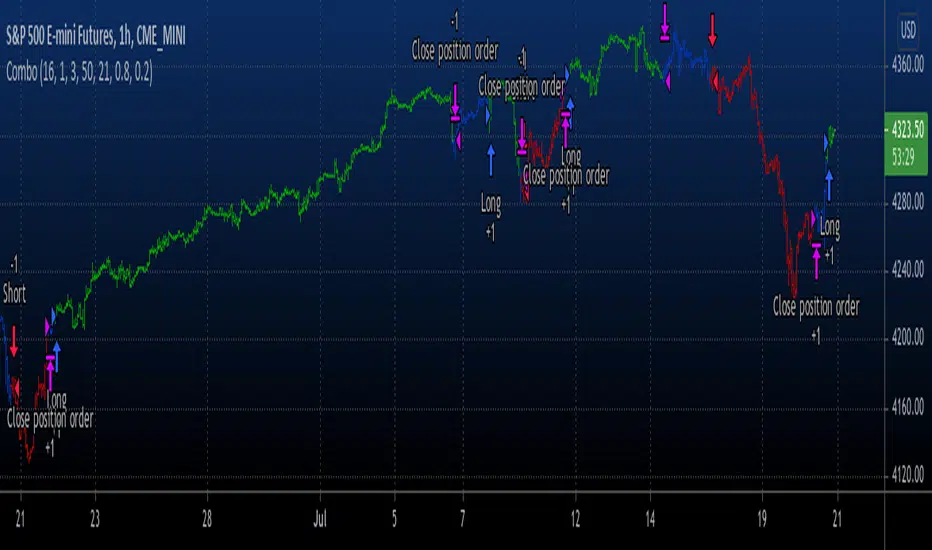

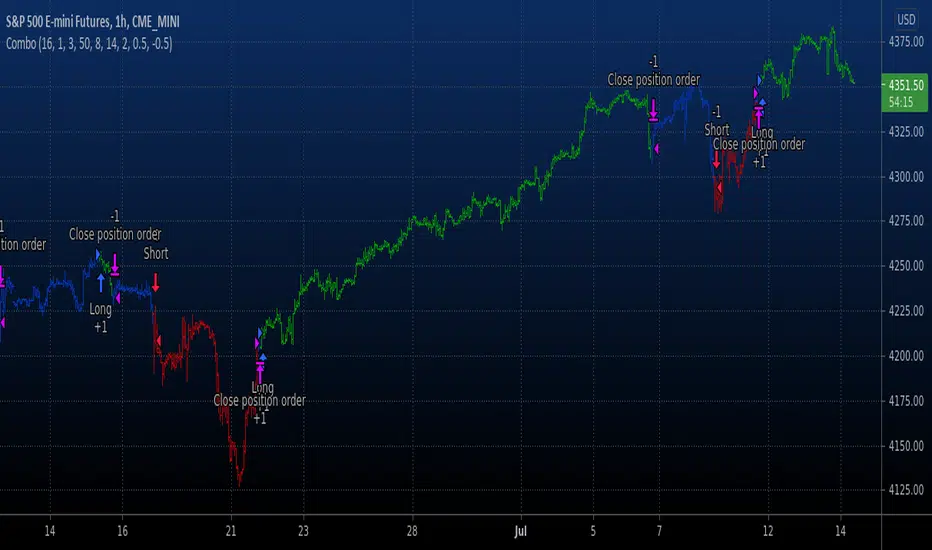

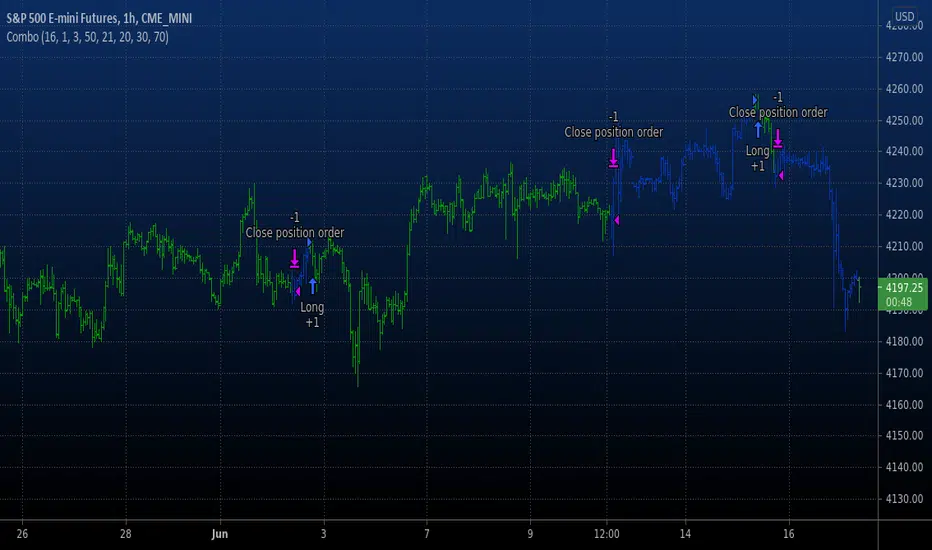

Multi-X by HamidBoxHello to All, introducing Multi Types Crossover strategy,

simply the best way of trading with Crossover and Crossunder Strategy, How it Works???

I added 5 types of Moving Averages,

1: Simple Moving Average ( SMA )

2: Exponential Moving Average ( EMA )

3: Weighted Moving Average ( WMA )

4: Volume Weighted Moving Average ( VWMA )

5: Relative Moving Average (RMA)

With this indicator, you can do scalping, You can trade not only with similar types of Moving Average indicators but also with different types of Moving Average indicators.

what is mean? like: Normal Condition is:

( Simple Moving Average ) Crossover to ( Simple Moving Average ), SMA x SMA

( Exponential Moving Average ) Crossover to ( Exponential Moving Average ), EMA x EMA

But we can Crossover with:

( Exponential Moving Average ) Crossover to ( Simple Moving Average ), EMA x SMA

( Simple Moving Average ) Crossover to ( Weighted Moving Average ), SMA x WMA

( Weighted Moving Average ) Crossover to ( Weighted Moving Average ), WMA x WMA

( Simple Moving Average ) Crossover to (Relative Moving Average), WMA x RMA

and also I added Moving Average ZONE in this tool, What does it work???

The zone will tell us what type of direction the market has, if the market is above the zone, it's mean we have a Bullish Trend, and if the market is below the zone, it means the market has a Bearish Trend,

so if you want to play on the safe side, never trade when the market is in Bearish Trend, and if you want to play on aggressive mood, you can skip Moving Average Zone section.

M-oscillator

Binary Options Strategy TemplateWith the hype around Binary Options trading (more like gambling instead of trading) it is good to be able to backtest a strategy before using it in the live markets.

In a Binary Options trade the trade get's closed after a specific amount of time and the only thing that matters is if the market has increased in price or decreased after that amount of time.

Because of this a strategy backtest should close all positions after a specific amount of time. In this super small script the number of bars since the trade was opened is used as a way to close the position. So for example if you use this strategy on the 1 minute charts with number of bars set to 5 it will close the position 5 minutes after opening it. Purpose of this script is using it as a strategy on already existing scripts to check viability for options trading.

With the limited pine knowledge that I have I do not know if it is possible to create a more realistic binary options strategy which also calculated the profit. If someone knows a more advanced version of this please let me know.

Combo Backtest 123 Reversal & STARC BandsThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

A type of technical indicator that is created by plotting two bands around

a short-term simple moving average (SMA) of an underlying asset's price.

The upper band is created by adding a value of the average true range

(ATR) - a popular indicator used by technical traders - to the moving average.

The lower band is created by subtracting a value of the ATR from the SMA.

STARC is an acronym for Stoller Average Range Channels. The indicator is

named after its creator, Manning Stoller.

WARNING:

- For purpose educate only

- This script to change bars colors.

Kwan NRP Backtest To calculate the coordinates in which the kink of the line will cross,

the standard Forex instruments are used - Relative Strenght Index, Stochastic and Momentum.

It is very easy to optimize them for the existing trading strategy: they all have very

flexible and easily customizable parameters. Signals to enter the market can be 2 situations:

Change of color of the indicator line from red to blue. At the same time, it is worth entering into the purchase;

Change of color of the indicator line from blue to red. In this case, it is worth entering for sale.

The signals are extremely clear and can be used in practice even by beginners. The indicator

itself shows when to make deals: the user only has to accompany them and set the values

of Take Profit and Stop Loss. As a rule, the signal to complete trading is the approach of

the indicator level to the levels of the maximum or minimum of the previous time period.

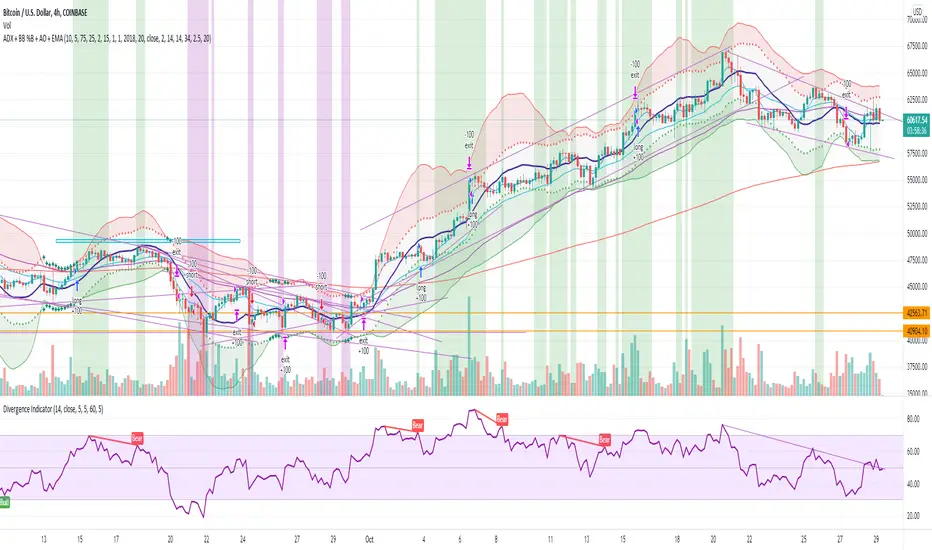

ADX + BB %B + AO + EMA [Luca Massuda]This trading strategy combines different indicators:

1) ADX, Average Directional Movement: to spot the trend

2) BB %B Bollinger Band %B: to spost relative price position to Bollinger Bands

3) AO Awesome Oscillator: to spot momentum

4) ema 5,ema21, ema50, ema200: to decide long or short position

You can configure:

Take profit % : at which % gains to take profit from the entry price

Stop loss % : at which % stop loss from the entry price

BB %B Overbought: At which level you consider Overbought respect to Bollinger Bands (values 0 to 100)

BB %B Oversold: At which level you consider Oversold respect to Bollinger Bands (values 0 to 100)

Awesome Oscillator: AO level to consider a long or short position +/- 2

ADX: ADX value to consider a long or short position

Start Date, Month, Year: Starting point for a backtesting strategy

Lenght , Source , Standard Deviation: Bollinger Bands values

ADX smoothing, DI Lenght: ADX values

Green and purple zones indicate when the strategy can go long or short.

Default Long conditions:

ema5>ema21 and ema50>ema200 and bb>75% and ao>2 and adx>15

Default Short conditions:

ema515

Combo Backtest 123 Reversal & Smoothed Williams ADThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Accumulation is a term used to describe a market controlled by buyers;

whereas distribution is defined by a market controlled by sellers.

Williams recommends trading this indicator based on divergences:

Distribution of the security is indicated when the security is making

a new high and the A/D indicator is failing to make a new high. Sell.

Accumulation of the security is indicated when the security is making

a new low and the A/D indicator is failing to make a new low. Buy.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Smoothed RSIThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is new version of RSI oscillator indicator, developed by John Ehlers.

The main advantage of his way of enhancing the RSI indicator is smoothing

with minimum of lag penalty.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & SMI Ergodic Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The SMI Ergodic Indicator is the same as the True Strength Index (TSI) developed by

William Blau, except the SMI includes a signal line. The SMI uses double moving averages

of price minus previous price over 2 time frames. The signal line, which is an EMA of the

SMI, is plotted to help trigger trading signals. Adjustable guides are also given to fine

tune these signals. The user may change the input (close), method (EMA), period lengths

and guide values.

WARNING:

- For purpose educate only

- This script to change bars colors.

Hull MA of RSI StrategyThis simple strategy base on RSI value of Close Price, High Price, Low Price, Median Price and RSI value smoothed by Hull Moving Average.

1. Optimize parameter on BTC H1 Binance chart

RSI period: 13

Hull MA period: 3

Middle Channel: 55-45

Overbough / Oversold: 70-30

2. Setup

2.1 Long Condition

- RSI of Close Price crossunder Overbought

- Close Price lower than Median Price (HL2)

- RSI of Median Price above Overbought

2.2 Close Long Position

- RSI of Close Price crossover Overbought (Take profit)

or

- RSI of Low Price crossunder upper value of Middle Channel (Stop loss)

2.2 Short Condition

- RSI of Close Price crossover Oversold

- Close Price higher than Median Price (HL2)

- RSI of Median Price below Oversold

2.2 Close Long Position

- RSI of Close Price crossunder Oversold (Take profit)

or

- RSI of High Price crossover lower value of Middle Channel (Stop loss)

3. Idea

- Follow strong momentum of Price to catch Flash Buy/Sell Bar in Crypto Market

- RSI of High Price and Low Price help to regconize setup failure quickly.

- This case study desire to find a balance of Winrate, Profit factor, Sharpe Ratio

Combo Backtest 123 Reversal & Smart Money Index (SMI) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Smart money index (SMI) or smart money flow index is a technical analysis indicator demonstrating investors sentiment.

The index was invented and popularized by money manager Don Hays. The indicator is based on intra-day price patterns.

The main idea is that the majority of traders (emotional, news-driven) overreact at the beginning of the trading day

because of the overnight news and economic data. There is also a lot of buying on market orders and short covering at the opening.

Smart, experienced investors start trading closer to the end of the day having the opportunity to evaluate market performance.

Therefore, the basic strategy is to bet against the morning price trend and bet with the evening price trend. The SMI may be calculated

for many markets and market indices (S&P 500, DJIA, etc.)

The SMI sends no clear signal whether the market is bullish or bearish. There are also no fixed absolute or relative readings signaling

about the trend. Traders need to look at the SMI dynamics relative to that of the market. If, for example, SMI rises sharply when the

market falls, this fact would mean that smart money is buying, and the market is to revert to an uptrend soon. The opposite situation

is also true. A rapidly falling SMI during a bullish market means that smart money is selling and that market is to revert to a downtrend

soon. The SMI is, therefore, a trend-based indicator.

Some analysts use the smart money index to claim that precious metals such as gold will continually maintain value in the future.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Stochastic This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This back testing strategy generates a long trade at the Open of the following

bar when the %K line crosses up UpBand line.

It generates a short trade at the Open of the following bar when the %K line

crosses down DownBand line.

WARNING:

- For purpose educate only

- This script to change bars colors.

MACD ReLoaded STRATEGYSTRATEGY version of MACD ReLOADED Indicator:

A different approach to Gerald Appel's classical Moving Average Convergence Divergence.

Appel originaly set MACD with exponential moving averages.

In this version users can apply 11 different types of moving averages which they can benefit from their smoothness and vice versa sharpnesses...

Built in Moving Average type defaultly set as VAR but users can choose from 11 different Moving Average types like:

SMA : Simple Moving Average

EMA : Exponential Moving Average

WMA : Weighted Moving Average

DEMA : Double Exponential Moving Average

TMA : Triangular Moving Average

VAR : Variable Index Dynamic Moving Average a.k.a. VIDYA

WWMA : Welles Wilder's Moving Average

ZLEMA : Zero Lag Exponential Moving Average

TSF : True Strength Force

HULL : Hull Moving Average

TILL : Tillson T3 Moving Average

In shorter time frames backtest results shows us TILL, WWMA, VIDYA (VAR) could be used to overcome whipsaws because they have less numbers of signals.

In longer time frames like daily charts WMA, Volume Weighted MACD V2, and MACDAS and SMA are more accurate according to backtest results.

My interpretation of Buff Dormeier's Volume Weighted MACD V2:

Thomas Aspray's MACD: (MACDAS)

Ichimoku Cloud Strategy Long Only [Bitduke]Slightly modificated and optimized for Pine Script 4.0, Ichimoku Cloud Strategy which, suddenly, good suitable for the several crypto assets.

Details:

Enter position when conversion line crosses base line up, and close it when the opposite happens.

Additional condition for open / close the trade is lagging span, it should be higher than cloud to open position and below - to close it.

Backtesting:

Backtested on SOLUSDT ( FTX, Binance )

+150% for 2021 year, 8% dd

+191% for all time, 32% dd

Disadvantages:

- Small number of trades

- Need to vary parameters for different coins (not very robust)

Should be tested carefully for other coins / stock market. Different parameters could be needed or even algo modifications.

Strategy doesn't repaint.

FXFUNDINGMATE TREND INDICATORA simple trend continuation strategy based on Ichimoku, moving average, Stochastic and MACD

Combo Backtest 123 Reversal & RSI HistoAlert This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This simple indicator modified RSI

WARNING:

- For purpose educate only

- This script to change bars colors.

PMax on Rsi w/T3 *Strategy*Profit Maximizer Indicator on RSI with Tillson T3 Moving Average:

PMax uses ATR calculation inside, for this reason users couldn't manage to use PMax on RSI because RSI indicator doesn't have High and Low values in bars, but ATR needs that values. So I personally calculate RSI in a different way to have High and Low values of RSI wrt price bars.

IMPORTANT:

Because of the sudden movements and divergences on RSI , this indicator must firstly optimized for the charts before using. Optimization can be held by users for the meaningful parameters for each chart.

3 parameters are critical when optimizing:

First: Multiplier

Second: Tillson T3 Length

Third: T3 Volume Factor

Says, Kıvanç Özbilgiç. Here's the strategy version for you to backtest & optimize properly.

Enjoy.

Relative Volume & RSI PopThis is a basic idea/script designed to take a breakout trade by taking advantage of volume spikes when price/strength is extended (either long or short).

The script only utilises two indicators, the Relative Volume (RV) and the Relative Strength Index (RSI). The script allows the user to select a RSI value between 69 up to 100 for a long trade and between 35 down to 0 for short trade and then pair this with RV from 0 - 10. The period for both the RSI and RV can also be amended by the user but I found in most cases there was no benefit gained by changing away from normal "14" period lookback. The script typically only has small draw downs as the script is designed to exit the trade when the RSI returns back to "normalised" level, therefore the trades are generally quite short. The exit condition for a long trade is when RSI crosses back below 69 (which is why you cannot enter a long below this value) and for a short the, trade will close when RSI crosses back above 35 (which is why you cannot enter a short above this value). These exit values are locked.

By allowing RSI value to go all the way up to "100" on the long side and "0" on the short side this in effect is a way of eliminating the script from taking either longs or shorts if lets say you wanted to back test the script for long only spikes or short only spike. E.G. By setting RSI upper value to "75" the RV to "1" and RSI lower value to "0" then no short trades will not be taken in your back test as the RSI never really gets down to zero.

I put this together with meme stocks in mind and back tested it on day charts for AMC and then a few trending style stocks too. It typically worked best as long only and with RSI settings between 71 - 75 and RV at 1 or 1.5. I also found it had okay results on some lower 1hr timeframe futures markets and weekly time frames too (albeit trades were few and far between on weekly timeframe).

The beauty of such a basic script you could easily set up a trading view screener to look for these opportunities everyday and perhaps even add in an ADX filter on the screener to see if the trend is increasing. Then use this script to run a back test on the stocks that you've selected from the screener.

Know Sure Thing and EMA Strategy by JLXThis is a simple strategy based in Know Sure Thing indicator and an Exponential moving average,

Rules are as follow:

- You can go long when the KST cross signal bellow 0 and price closes above the target EMA

- You can go short when the KST cross signal above 0 and price closes bellow the target EMA

I include a trailing stop loss, default its 0.5%

Hope you enjoy it

Combo Backtest 123 Reversal & RSI based on ROC This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is the new-age indicator which is version of RSI calculated upon

the Rate-of-change indicator.

The name "Relative Strength Index" is slightly misleading as the RSI

does not compare the relative strength of two securities, but rather

the internal strength of a single security. A more appropriate name

might be "Internal Strength Index." Relative strength charts that compare

two market indices, which are often referred to as Comparative Relative Strength.

And in its turn, the Rate-of-Change ("ROC") indicator displays the difference

between the current price and the price x-time periods ago. The difference can

be displayed in either points or as a percentage. The Momentum indicator displays

the same information, but expresses it as a ratio.

WARNING:

- For purpose educate only

- This script to change bars colors.

Take America Back Version 1.0So basically, the when the price goes down a little, it buys, and when it goes up a little it buys. The only indicators are account balances, and the price, that’s it. Now I wish that Pine Script had a function or variable in which I could recall the balances of specific portions of the portfolio, but it doesn’t. So, I had to improvise. Now for this to work accurately, all of the money needs to be in the “base” side before the bot can begin. Now, the thing about this is that it does not re-invest the amount that is “saved” to all but guarantee the balance will go up. However, as this goes up it will not add up as quickly in order to allow more wiggle room so that the bot does not work itself into a corner. If you want to keep some of your base, enter how much you want to keep it in the initial “saved” setting, as long as you allow at least enough to be equal to the default quantity value. Also, I recommend you setting the pyramiding setting to the result of the base value divided by the default quantity value. The default quantity value is how much you invest, measured in the base currency.

This would have been sooooo much easier if pine script could allow me to recall specific balances, but maybe a future one will.

Finally, THIS is why I made this program, I wanted to create something that would prevent the little ones from being stepped on by the big players who don't always play fair.

Besides, cryptocurrencies were made in response to the 2008 financial meltdown that caused a global recession. This decentralized currency is not just the money of the banks, the corporations, or the governments, but the money of the people. Use this tool to level the massive wealth inequality in my country and take America Back.

I will post more links and updates later once my reputation score goes up. I will discuss more about what influenced me to make this program and as some advise and possible future improvements as well.

Combo Backtest 123 Reversal & Reverse Engineering RSI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Reverse Engineering RSI, by Giorgos Siligardos

The related article is copyrighted material from

Stocks & Commodities.

WARNING:

- For purpose educate only

- This script to change bars colors.

MACD Long StratFirst script I've written, but the concept is pretty simple. This uses the MACD with settings fast_SMA = 6 and slow SMA=16 and uses the distance between the 2 (histogram) to look for potential trend reversals to flag potential entries for Long trades. It waits for the confirmation looking backward 2 x timeframes (to reduce false calls slightly). You can adjust it to open / close quicker (1 timeframe instread of 2) but backtesting shows 2 timeframe delay is best to avoid false signals.

The script suggests Long entry points based on this criteria and uses the converse (reducing histogram / SMA difference delayed by 2 timeframes) to suggest exit or trade close points for downward reversal. It was originally written looking at 1m scalps but backtesting shows this is even more effective on higher timeframes (1D).

Maximized Scalping On Trend (by Coinrule)" The trend is your friend. " This is one of the most famous and valuable teachings that experienced traders can give to newbies. There is a reason for that.

No matter your views about where the price moves, what matters is where the price heads to . The market is always right, and ultimately it decides who gets the profit and who has to take a loss.

The purpose of this strategy is to spot when it's the most suitable time to buy an asset profiting from a potential short-term price increase. The strategy tends to open trades frequently, closing them on average in one and a half days.

ENTRY

The buy order is placed on assets that present strong momentum when it's more likely that it is about to increase further in the short term.

To capture momentum on the asset, the rule strategy requires:

the MA50 greater than the MA100

the RSI greater than 50

The rule, then, places the order when

The price crosses above the MA9.

EXIT

This strategy comes with a stop loss and a take profit which adapt dynamically to market conditions.

The trade is closed in profit when the RSI is greater than 70 , as the trend could experience a pull-back.

Alternatively, the trade is closed when the RSI is lower than 30 , being this a sign of weakening of the trend.

Pro tip : The 1-hour time frame has proven to return the best results on average. The strategy can also work well in the 15-min time frame if you want to increase the trades' frequency.

The strategy assumes each order to trade 30% of the available capital and opens a trade at a time. A trading fee of 0.1% is taken into account.