Price Region RegressionThis is an optimized price range regressor based on least squares regression.

(1) Supports setting regression from the Nth candle

(2) Supports the minimum and maximum regression candle interval length

(3) Supports finding the optimal regression region based on the length step among the minimum and maximum regression region lengths

(4) Supports displaying the optimal regression level

(5) The size of the regression region is two times the standard deviation by default

这是一个基于最小二乘回归的价格区间回归指标

(1) 支持设置从第N个蜡烛开始回归

(2) 支持最小和最大回归蜡烛的区间长度

(3) 在最小和最大回归区间长度中,根据长度步进寻找最优的回归区间

(4) 支持显示最优回归等级

(5) 回归区间的大小默认为2倍标准差

Doğrusal Regresyon

[_ParkF]Linreg & Trendlines* The script has been uploaded again.

Linear regression and trendline not only facilitate trend identification,

but also identify support and resistance within it,

and linear regression and trendline departure can detect trend changes, which are useful in trading.

Linear regression and trend lines are shown in the chart.

It offers a variety of options, length, color, thickness, on/off switch, etc.

I hope it will help you with your trading.

hope you become rich!

---------------------------------------------------------------------------------------------------------------------------

* 스크립트가 다시 업로드 되었습니다.

선형 회귀(채널) 및 추세선은 추세 식별을 용이하게 할 뿐만 아니라,

또한 그 안에서 지지와 저항을 식별하고,

선형 회귀(채널) 및 추세선 이탈은 거래에 유용한 추세 변화를 감지할 수 있습니다.

선형 회귀(채널) 및 추세선이 차트에 표시됩니다.

길이, 색상, 두께, 온/오프 스위치 등 다양한 옵션을 제공합니다.

거래에 도움이 되셨으면 합니다.

부자되세요!

---------------------------------------------------------------------------------------------------------------------------

* I would like to express my gratitude to zdmre for revealing the linear regression source.

Cashew NutsThis indicator used the average regression of stock prices.

In general, stock prices show how they form new prices when they are outside the average price or range.

Therefore, when stock prices show an average price flow, if you take both long and short positions, you will have an opportunity to convert the spread into profit in the meantime.

How to use -

When the direction is determined from the average price, and when the direction is up, it is generally interpreted as a drop as soon as it deviates from the resistance line.

When the direction is determined from the average price, and when the direction is lowered, it is generally expected to rise as soon as it breaks the support line.

Precautions -

These indicators do not guarantee profits.

[_ParkF]MFI+Added the Moneyflow Index indicator.

Divergence signals and diversion lines are drawn.

Support and resistance were also confirmed when linear regression and trend lines were used for the Moneyflow Index.

Two linear regression and two trend lines are drawn.

Because the two linear regression values are different, you can see the support and resistance of long-term and short-term linear regression.

Since the periodic values of the two trend lines are also different, support and resistance that could not be identified in linear regression can be identified.

Each linear regression line and trend line can be turned on or off.

In addition, each linear regression line and trend line can arbitrarily modify period values and deviation values.

I hope it will help you trade.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

머니플로우인덱스 지표를 추가하였습니다.

다이버전스 신호와 다이버전스 라인이 그려집니다.

머니플로우인덱스에도 선형회귀와 추세선을 이용했을 때 지지와 저항이 확인이 되었습니다.

2개의 선형회귀와 2개의 추세선이 그려지고

두 선형 회귀 값은 서로 다르기 때문에 장기 및 단기 선형 회귀의 지지 및 저항을 확인할 수 있습니다.

두 추세선의 주기 값도 다르므로 선형 회귀 분석에서 확인할 수 없었던 지지 및 저항을 확인할 수 있습니다.

각 선형 회귀선 및 추세선은 켜거나 끌 수 있습니다.

또한 각 선형 회귀선 및 추세선은 주기 값과 편차 값을 임의로 수정할 수 있습니다.

당신의 트레이딩에 도움이 되었으면 합니다.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

* I would like to express my gratitude to zdmre for revealing the linear regression source.

* I would like to express my gratitude to aaahopper for revealing the trendlines source.

[_ParkF]RSI+RSI ----- UPGRADE ----> RSI+

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

The RSI index has been upgraded.

The display function of RSI Candle, RSI Line, Divergence, and Divergence Line, which were previous functions, has been maintained.

As an upgrade, two linear regression and two trend lines are drawn.

Since the two linear regression values are different, support and resistance of long-term and short-term linear regression can be confirmed.

The two trend lines also have different period values, so it is possible to check support and resistance that could not be confirmed in linear regression.

Each linear regression and trend line can be turned on and off.

In addition, each linear regression and trend line can arbitrarily modify period values and deviation values.

Log charts and linear chart switches have been added to the trend line.

I hope it will help you with your trading.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

RSI 인덱스가 업그레이드되었습니다.

기존 기능이었던 캔들, 라인, 다이버전스, 다이버전스 라인의 디스플레이 기능은 그대로 유지됐다.

업그레이드로 두 개의 선형 회귀 분석과 두 개의 추세선이 그려집니다.

두 선형 회귀 값은 서로 다르기 때문에 장기 및 단기 선형 회귀의 지지 및 저항을 확인할 수 있습니다.

두 추세선의 주기 값도 다르므로 선형 회귀 분석에서 확인할 수 없었던 지지 및 저항을 확인할 수 있습니다.

각 선형 회귀선 및 추세선은 켜거나 끌 수 있습니다.

또한 각 선형 회귀선 및 추세선은 주기 값과 편차 값을 임의로 수정할 수 있습니다.

로그 차트 및 선형 차트 스위치가 추세선에 추가되었습니다.

당신의 트레이딩에 도움이 되었으면 합니다.

* I would like to express my gratitude to zdmre for revealing the linear regression source.

* I would like to express my gratitude to aaahopper for revealing the trendlines source.

[_ParkF]RSI (+ichimoku cloud)RSI

Typical RSI indicators were plotted with candles and expressed wick to resemble a candle chart,

and linear regression was added to predict changes in force intensity,

which allowed us to confirm support and resistance within linear regression .

In addition, divergence signal was marked as an additional basis for the price fluctuation point due to support and resistance .

In other words,

if the diversity signal appears together when the rsi candle is supported and resisted within linear regression ,

this is the basis for predicting that it is a point of change in the existing trend.

Finally, the period value and standard deviation of linear regression can be arbitrarily modified and used.

I hope it will help you with your trading.

--------------------------------------------------------------------------------------------------------------------------------------------------------------

(+ichimoku cloud)

Clouds made of the preceding span 1 and the preceding span 2 of the balance table can predict the trend by displaying the current price balance ahead of the future.

In addition to the role of clouds in the above-described balance sheet, this indicator also shows the cloud band support and resistance of the current RSI value.

일반적인 RSI 지표를 캔들화 하였고 꼬리까지 포함하여 캔들 차트와 유사하게 표현 하고,

캔들화한 RSI 지표에 선형회귀(채널)를 추가 하여 RSI 지표 특유의 힘의 강도의 변화를 지지와 저항으로 확인할 수 있게 해봤습니다.

또한 다이버전스 신호를 추가하여 선형회귀(채널)로 인한 지지와 저항에 따른 가격 변동의 근거로 삼을 수 있습니다.

즉, 선형회귀(채널) 안에서 RSI 캔들이 지지와 저항을 받을 때 다이버전스 신호가 함께 나타난다면 이는 기존 추세의 변화 지점임을

예측해 볼 수 있는 근거가 됩니다.

마지막으로 선형회귀(채널)의 기간값과 표준편차는 임의로 수정하여 사용할 수 있습니다.

당신의 트레이딩에 도움이 되었으면 합니다.

--------------------------------------------------------------------------------------------------------------------------------------------------------------

(+일목균형표의 구름)

일목균형표의 선행스팬1과 선행스팬2로 만들어진 구름은 현재 가격의 균형을 미래에 선행하여 표시하여 추세를 예측해볼 수 있습니다.

본 지표에서는 위에서 설명한 일목균형표의 구름의 역할과 더불어 현 RSI 값의 구름대 지지, 저항 또한 확인해볼 수 있습니다.

* I would like to express my gratitude to zdmre for revealing the linear regression source.

[_ParkF]RSIRSI

Typical RSI indicators were plotted with candles and expressed wick to resemble a candle chart,

and linear regression was added to predict changes in force intensity,

which allowed us to confirm support and resistance within linear regression.

In addition, divergence signal was marked as an additional basis for the price fluctuation point due to support and resistance.

In other words,

if the diversity signal appears together when the rsi candle is supported and resisted within linear regression,

this is the basis for predicting that it is a point of change in the existing trend.

Finally, the period value and standard deviation of linear regression can be arbitrarily modified and used.

I hope it will help you with your trading.

일반적인 RSI 지표를 캔들화 하였고 꼬리까지 포함하여 캔들 차트와 유사하게 표현 하고,

캔들화한 RSI 지표에 선형회귀(채널)를 추가 하여 RSI 지표 특유의 힘의 강도의 변화를 지지와 저항으로 확인할 수 있게 해봤습니다.

또한 다이버전스 신호를 추가하여 선형회귀(채널)로 인한 지지와 저항에 따른 가격 변동의 근거로 삼을 수 있습니다.

즉, 선형회귀(채널) 안에서 RSI 캔들이 지지와 저항을 받을 때 다이버전스 신호가 함께 나타난다면 이는 기존 추세의 변화 지점임을

예측해 볼 수 있는 근거가 됩니다.

마지막으로 선형회귀(채널)의 기간값과 표준편차는 임의로 수정하여 사용할 수 있습니다.

당신의 트레이딩에 도움이 되었으면 합니다.

* I would like to express my gratitude to zdmre for revealing the linear regression source.

Standard Deviation ChannelThe standard deviation channel allows you to visually see the trend in the market using a linear regression calculation. This script has two lower and two upper bounds, with different deviations. Each of these boundaries has an alert when it has been breached.

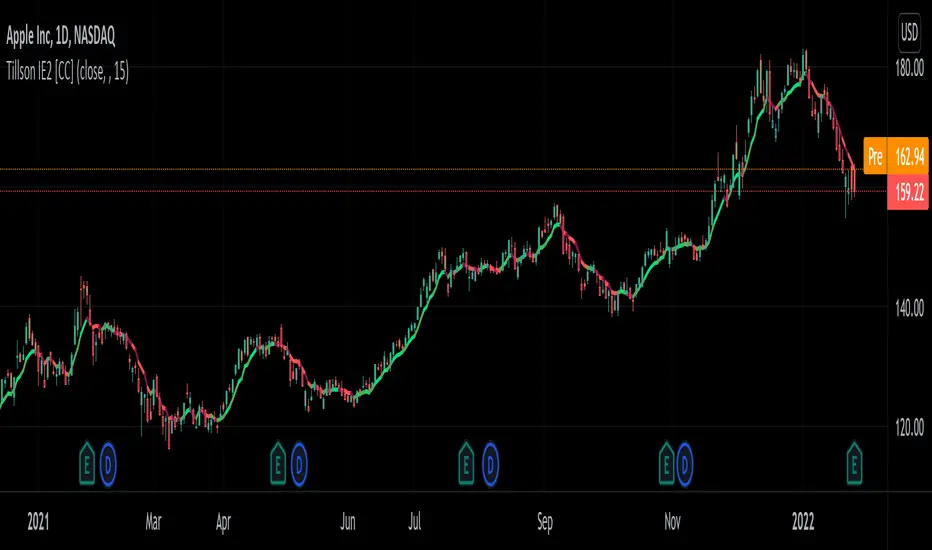

Tillson IE/2 [CC]The IE/2 was created by Tim Tillson (Stocks and Commodities Jan 1998) and this is a practically undiscovered gem because in that same article he goes on to to create the popular T3 moving average and the GDEma but practically no one seemed to notice the IE2 or maybe it is just my imagination. Anyway this indicator name is short for Integral of Linear Regression Slope + Endpoint Moving Average / 2 so you can why it was shortened to IE/2. Like the name implies this takes two variations of smoothing that complement each other and averages them together to in theory get the benefits of each. The EPMA is much noiser but follows the data more closely and the complete opposite for the ILRS so you can see the idea in action. Like all of my indicators I include strong buy and sell signals in addition to normal ones so strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators or scripts you would like to see me publish!

Soldi OscillatorThe Soldi Oscillator measures the mean of logarithmic returns, given this data you can assume market expectancy in returns of the mean. When seeing positive Means you can assume positive returns will follow positive returns if positive autocorrelation is present. Vice versa for the other event of negative returns.

How you can effectively use this indicator and oscillator is by looking at a higher time frame and if the oscillator is positive, you can go to a lower timeframe and try to trade in that direction of the market as the expected returns are positive in nature.

You can also spot trend divergences very well as the trend continues but the returns are dropping that means the returns are mean reverting and can have a potential to flip to the other side

Linear Regression Relative Strength[image/x/iZvwDWEY/

Relative Strength indicator comparing the current symbol to SPY (or any other benchmark). It may help to pick the right assets to complement the portfolio build around core ETFs such as SPY.

The general idea is to show if the current symbol outperforms or underperforms the benchmark (SPY by default) when bought some certain time ago. Relative performance is displayed as percent and is calculated for three different time ranges - short (1 mo by default), mid (1 quarter), and long (half a year). To smooth the volatility, the script uses linear regression to estimate the trend and takes the start and the end points of the linear regression line to compute the relative strength.

It is important to remember that the script shows the gain relative to SPY (or other selected benchmark), not the asset's gain. Therefore, it may indicate that the asset is profitable, but it still may lose value if SPY is in downtrend.

Therefore, it is crucial to check other indicators before making a decision. In the example above, standard linear regression for one quarter is used to indicate the direction of the trend.

Trends_2022Hello everyone,

we are developing a strategy which is suited for people that likes to trade in small time frames.

Our strategy uses many indications for entries. These indicators can be used individually or better solution we combined them together for best prediction.

These indications like True Range, Average True Range , moving averages also previous bars highs, lows and closes values and finally mathematical equations to decide close price wave movement. Most of the work is in scaling price data and comparing them with the indicators to decide trend

The strategy is planned to go only long direction..

now we will discuss how each indicator is used to decide trend

* According to ATR trend prediction ...

it is up when the scaled bar price greater than ATR value

it turns down when the scaled bar price is less than ATR value

* According to MAs trend prediction ...

we use SMA and previous bar data averages then apply linReg ( Linear regression curve) this result in curve up and down zero

it is up when the value is up zero

it turns down when the value is down zero

* According to close price wave movement ...

we applied cos function on previous bars close data to get the sloping wave of close movement

If the slope is increasing ... this means the current wave value is greater than the previous value

If the slope is decreasing ... this means the current wave value is less than the previous value

Now as we mentioned before... The strategy goes only long direction.

LONG ENTRY Conditions (ANDing condition not ORing):

we can use any one of these indicators individually, or mix any two of them or use them all simultaneously

So... LONG ENTRY Conditions are as below:

if ATR trend is used .. it should be UP.

if MAs trend used .. it should be > 0.

if close wave slope is used .. it should be increasing.

On the other side… the Exit conditions are also (ANDing condition not ORing):

So... LONG Exit Conditions are as below:

if ATR trend is used .. it should be down.

if MAs trend used .. it should be < 0.

if close wave slope is used .. it should be decreasing.

Please send me private message for script authorization.

Happy trading everyone!

Fusion: Trend and thresholdsThis is your basic single moving average but with a "slope" component. The idea here is that once a slope reaches a value great enough you should probably only trade with the trend so this indicator allows you to set that threshold separately for going long and short.

The indicator is designed to display on both the main chart and a separate chart area. If you want to display it on the main chart then the quick way is to just check the "On main chart" option and it will disable off main chart items and then just move it to the main chart.

There's half a dozen or so moving average types to select from so you will probably find one that suits you pretty well.

Once a threshold is reached you will get a signal showing the trend is strong enough where you probably should not trade in the opposite direction.

There is a "normalize" option which will fix the oscillator to a maximum of 100. The upside of this is that you can be more consistent in your settings of a threshold. The down side is that normalization happens over a predefined number of bars so it's a floating number, not an absolute number however I set the number of bars default to 3,000 so it should be pretty close to ideal. I haven't found a perfect way of getting a consistent maximum on the oscillator as a benchmark yet so if anyone has any ideas please contact me and I'll do an update. I may look into using percentage rank instead of normalization.

I like to see it as both an oscillator and on the main chart so I generally have two copies.

The settings are certainly not optimized so set to whatever suits your needs as my defaults will probably be wrong for you.

The code is structured to easily drop into a bigger system so use it as a lone indicator or add the code to some bigger project you are creating. If you do, send me a note, it would be nice to know it's being well used.

Finally, if you find value please do make a comment, give a thumbs up etc.

Enjoy and good luck!

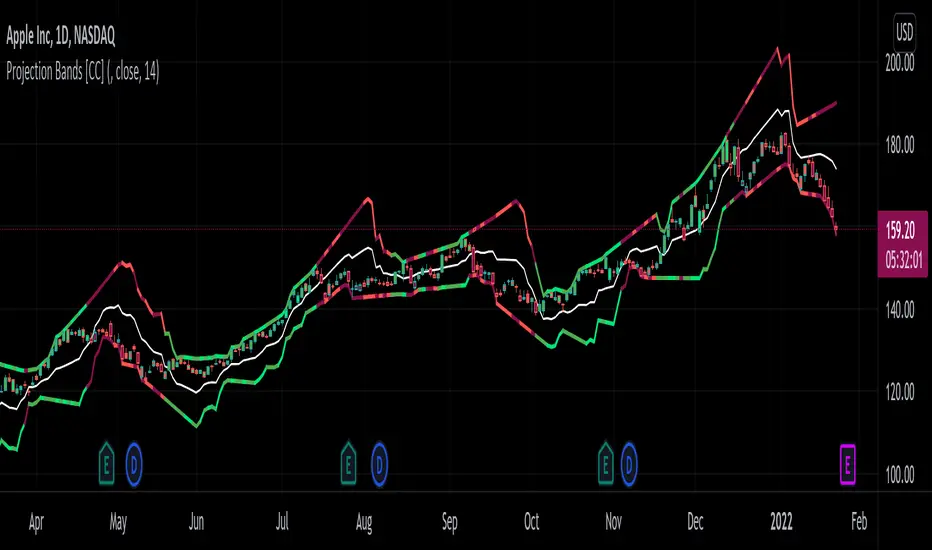

Projection Bands [CC]The Projection Bands were created by Mel Widner (Stocks and Commodities Jul 1995) and this indicator and the other two that rely on this one (I will publish them later) are very underappreciated in my humble opinion. The biggest strength of this indicator is the fact that it is a leading indicator for dramatic price movements. As you can see in my example chart it consistently gives great exit points before a downturn. I have included strong buy and sell signals in addition to normal ones so strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators or scripts you would like to see me publish!

Linear Regression 200/100/50/20Four time frames in one indicator in different colors, showing current price trend in different scopes.

If the slope of the smaller time frame is in a (0,75;1,25) interval of some of the bigger ones the smaller one is omitted (different signs near zero are not coalesced in that way though).

Every time frame has four deltas of range in trend lines of different grade of transparency (2-1-4-3), as well as a vertical line denoting regression date range start, also bearing the same color (blue-red-green-gray for 200/100/50/20).

On the right of the latest bar are Pearson coefficients and slopes of the regressions, 200/100/50/20 bottom-up, also appropriately colored.

Pairs Trading (basic OLS regression)Pairs trading using hedge ratio.

Firstly, it calculates hedge ration using OLS linear regression.

Then it calculates spread and z-score of spread.

if spread in specific range (which it's possible to change in settings) it makes Long/Short orders.

The very basic script.

Logarithmic Trend ChannelThis indicator automatically draws a regression channel plotted on logarithmic scale from the first quotation.

This model is useful for the long term series data (such as 10 or 20 years time span).

The Pearson correlation measures the strength of the linear relationship between two variables. It has a value between to 1, with a value of 0 meaning no correlation, and + 1 meaning a total positive correlation.

Logarithmic price scales are a type of scale used on a chart, plotted such that two equivalent price changes are represented by the same vertical changes on the scale.

They differ from linear price scales because they display percentage points and not dollar price increases for a stock.

Technical issues

*The user have to pan over the chart from the beginning to the end of the study range (such as 10 years of bars) so the pine script could generate those lines on the chart.

*If on the chart the number of bar is less than the lookback period, it won't generate any lines as well.

[YUTAS] Linear Regression Trend Channel

・Indicator for linear regression channel.

・Multiple deviations can be displayed.

・The color changes by reading the angle of the center line according to the direction of the market.

Rising market → blue

Down market → Red

----------------------------------------------

・線形回帰チャネルのインジケーター。

・偏差を複数表示可能。

・相場の向きに合わせてセンターラインの角度を読み取り色が変わります。

上げ相場 → 青

下げ相場 → 赤

Buy and Sell with Master_in_chart-ind. [V1]This script indicates the Buy and Sell positions on your chart. In addition, it shows entry price , stop loss and possible targets on the chart. The same information are shown in a table where you can find the position type (long/short) in green and red color, entry point, stop-loss (always in red) and targets.

The targets are defined by Risk to Reward ratios 1:1, 1:1.5 and 1:2.

the labels appears when the all conditions are satisfied.

Interesting part of the script is the alert function. Here one can set the script for different

securities and activate alert in TV.

In summary, one can change and tune the setting of the indicator easily by clicking on the gear icon. In the setting, there are four sections. First section sets the slop-loss. Second section activates and shows the super trend indicator. Third section is designed to tune the signals. Finally, you can apply the script on five different symbols at different time-frames. Here you can set alarm to alert you the signals.

I hope you enjoy it!

Profit Maxima: a crypto strategyThis strategy is designed for those who are looking for long-term positions with low risk and high profitability.

How does it work?

In short, the basis of this strategy is the frequent modeling of the price using regression equations and the estimation of the range of price movements.

The price modeling process starts from the first bars and will be repeated on each bar. This process is performed in each candle based on the data available up to that candle, and data for subsequent bars is not used.

There is also no fixed price model, but it will change from one candle to the next; Therefore, the more candles there are, the larger the statistical population and therefore the quality of the price model increases.

I have also used the concept of scarcity. Bitcoin is the first scarce digital object in the world. Once something becomes scarce enough, it can be used as money. This scarcity gradually increases and affects the price. The entire crypto market also follows Bitcoin.

However, always remember that past results in no way guarantee future performance.

Why this strategy generates a small number of trades?

Preston Pysh believed Bitcoin cycles happen in three phases: the Bull Run, the Correction, and the Reversion to the Mean. He estimates there are about 200,000 blocks per cycle and there are about 144 blocks per day.

Therefore, each cycle of Bitcoin lasts about four years. The entire crypto market follows bitcoin. On the other hand, cryptocurrency is a new phenomenon. They have a limited price history.

This strategy is designed to open a long position at the lowest possible price. In addition, due to the concept of scarcity and its continued impact on prices, trading in the “short” direction is avoided.

The combination of these factors leads to generate a small number of trades. However, you can test it on several different charts to make sure it works properly.

Default settings

{ default_qty_type } = strategy.percent_of_equity

{ default_qty_value } = 3.3

{ commission_value } = 0.1

{ pyramiding } = 3

{ close_entries_rule } = "ANY"

In a simple word, buy (Entry) and sell (take-profit) orders are each done at three different levels. At each level, 3.3% of equity is used (9.9% in total)

0.1% commission is considered for each transaction.

“close_entries_rule” determines the order in which orders are closed. The default is FIFO (first in, first out), but in this strategy, orders are executed in “first in, last out” order. In this way, the lowest buy (Entry) order corresponds to the lowest sell (take profit) order.

Choose the best chart

Charts have a significant impact on the performance of the strategy. As mentioned, the more historical bars there are, the larger the statistical population and therefore the quality of the price model increases.

You can use the Chart Quality panel to choose the appropriate chart:

The ‘Historical Bars’ field shows the number of candles in the chart. Choose the chart of an exchange that has the most historical bars.

The ‘Recommended Chart’ field shows the suggested chart for some symbols.

The “Predictability” field indicates to what extent price movements can be predicted using the model; the higher the “predictability”, the more credible the results of the strategy. "Predictability" indicates that the results of the strategy are reliable or not.

The image below shows the recommended chart for 20 different symbols:

How to use

You don't need automated trading platforms to use it. It can be used by placing simple buy and sell (take-profit) orders manually.

The green and red lines indicate the 'Entry' and 'Profit' levels respectively. If there is no order (buy / sell) active on one of these levels, it will be displayed in gray. The corresponding values are displayed in the Entry & Profit Limits table.

After choosing the appropriate chart, you can use this table to place your orders manually.

Note that trading in the "short" direction is not recommended at all.

Samples

NEXT Regressive VWAPOverview:

This version of the Volume-Weighted Average Price (VWAP) indicator features an extended algorithm, which, in addition to volume and price, also incorporates regression analysis. The result is a more responsive, often leading VWAP slope with a degree of statistical predictability built in. Just like with the original VWAP, NEXT Regressive VWAP offers two optional Standard Deviation bands that parallel it. These can be set to any deviation level, with the default being 1 and -1, indicating one standard deviation above and one below Regressive VWAP, respectively.

Below is a screenshot comparing NEXT Regressive VWAP (green) to the original VWAP (blue) on CME_MINI:ES1! M3 chart.

Application and Strategy Ideas:

Price above NEXT Regressive VWAP is interpreted to have a bullish bias, and below, bearish. You can use TradingView's native Set Alert functionality to be notified, in real-time, when price crosses Regressive VWAP, and/or any of its standard deviation bands. Another popular "probability play" strategy is to scalp price when it crosses under the upper band (short) and crosses over the lower band (long). The screenshot below visualizes such a strategy on NASDAQ:QQQ M1 chart:

Input Parameters:

There are 3 groups of input.

Regression Settings

Length - controls the length of time (in bars) for regression analysis with higher values yielding smoother, more responsive values.

Regression Weighting - controls the degree of regression analysis incorporated into VWAP, with 5 being average, 0-4 less, 6-10 more. The higher the value, the more responsive the Regressive VWAP curve.

VWAP Settings

Anchor Period - controls the origin of VWAP calculations, start of session being the default.

Source - data used for calculating the VWAP, typically HLC/3, but can be used with other price formats and data sources as well.

Offset - shifting of the VWAP line forward (+) or backward (-).

Standard Deviation Bands Settings

Calculate Bands - checking this will add 2 bands, each equidistant (by the amount of Multiplier) from the NEXT Regressive VWAP line.

Bands Multiplier - standard deviation multiplier, with 1 being the default

Signals and Alerts:

Here is how to set price (close) crossing NEXT Regressive VWAP alerts: open a chart, attach NEXT Regressive VWAP, and right-click on chart -> Add Alert. Condition: Symbol e.g. ES (close) >> Crossing >> Regressive VWAP >> VWAP >> Once Per Bar Close.

Linear Regression Histogram [LuxAlgo]This indicator is inspired by traditional statistical histograms. It will return the number of occurrences of price falling within each interval (bins) of the linear regression channel. This can be useful to highlight zones of interest within a trend.

Settings

Length: Number of recent closing prices used for the computation of the linear regression.

Bins Number: Number of intervals constructed from the linear regression channel.

Mult: Multiplicative factor for the RMSE. Controls the width of the linear regression channel.

Src: Input source of the indicator.

Usage

The indicator is constructed by dividing the linear regression channel range into a series of intervals (bins) of equal width. We then count the number of price values falling within each interval.

If a significant number of price values fall within a specific interval then that interval can highlight a potential zone of interest within a trend.

The zone of interest is highlighted in blue.

RSI Linear Regression with ZigZag by zdmreBoth the RSI (Relative Strength Index) and the Linear Regression ( LR ) rank among the most popular momentum indicators used in trading. When used in combination with other technical indicators (ZigZag), both RSI, LR and ZigZag can offer value in validating trade opportunities to optimize your risk management practices.

Here’s a look at how to use RSI, LR and ZigZag (Can be used for divergence patterns.) as part of your trade analysis.

If you have new ideas to improve this indicator then let me know please.

***Use it at your own risk