TitanGrid L/S SuperEngineTitanGrid L/S SuperEngine

Experimental Trend-Aligned Grid Signal Engine for Long & Short Execution

🔹 Overview

TitanGrid is an advanced, real-time signal engine built around a tactical grid structure.

It manages Long and Short trades using trend-aligned entries, layered scaling, and partial exits.

Unlike traditional strategy() -based scripts, TitanGrid runs as an indicator() , but includes its own full internal simulation engine.

This allows it to track capital, equity, PnL, risk exposure, and trade performance bar-by-bar — effectively simulating a custom backtest, while remaining compatible with real-time alert-based execution systems.

The concept was born from the fusion of two prior systems:

Assassin’s Grid (grid-based execution and structure) + Super 8 (trend-filtering, smart capital logic), both developed under the AssassinsGrid framework.

🔹 Disclaimer

This is an experimental tool intended for research, testing, and educational use.

It does not provide guaranteed outcomes and should not be interpreted as financial advice.

Use with demo or simulated accounts before considering live deployment.

🔹 Execution Logic

Trend direction is filtered through a custom SuperTrend engine. Once confirmed:

• Long entries trigger on pullbacks, exiting progressively as price moves up

• Short entries trigger on rallies, exiting as price declines

Grid levels are spaced by configurable percentage width, and entries scale dynamically.

🔹 Stop Loss Mechanism

TitanGrid uses a dual-layer stop system:

• A static stop per entry, placed at a fixed percentage distance matching the grid width

• A trend reversal exit that closes the entire position if price crosses the SuperTrend in the opposite direction

Stops are triggered once per cycle, ensuring predictable and capital-aware behavior.

🔹 Key Features

• Dual-side grid logic (Long-only, Short-only, or Both)

• SuperTrend filtering to enforce directional bias

• Adjustable grid spacing, scaling, and sizing

• Static and dynamic stop-loss logic

• Partial exits and reset conditions

• Webhook-ready alerts (browser-based automation compatible)

• Internal simulation of equity, PnL, fees, and liquidation levels

• Real-time dashboard for full transparency

🔹 Best Use Cases

TitanGrid performs best in structured or mean-reverting environments.

It is especially well-suited to assets with the behavioral profile of ETH — reactive, trend-intraday, and prone to clean pullback formations.

While adaptable to multiple timeframes, it shows strongest performance on the 15-minute chart , offering a balance of signal frequency and directional clarity.

🔹 License

Published under the Mozilla Public License 2.0 .

You are free to study, adapt, and extend this script.

🔹 Panel Reference

The real-time dashboard displays performance metrics, capital state, and position behavior:

• Asset Type – Automatically detects the instrument class (e.g., Crypto, Stock, Forex) from symbol metadata

• Equity – Total simulated capital: realized PnL + floating PnL + remaining cash

• Available Cash – Capital not currently allocated to any position

• Used Margin – Capital locked in open trades, based on position size and leverage

• Net Profit – Realized gain/loss after commissions and fees

• Raw Net Profit – Gross result before trading costs

• Floating PnL – Unrealized profit or loss from active positions

• ROI – Return on initial capital, including realized and floating PnL. Leverage directly impacts this metric, amplifying both gains and losses relative to account size.

• Long/Short Size & Avg Price – Open position sizes and volume-weighted average entry prices

• Leverage & Liquidation – Simulated effective leverage and projected liquidation level

• Hold – Best-performing hold side (Long or Short) over the session

• Hold Efficiency – Performance efficiency during holding phases, relative to capital used

• Profit Factor – Ratio of gross profits to gross losses (realized)

• Payoff Ratio – Average profit per win / average loss per loss

• Win Rate – Percent of profitable closes (including partial exits)

• Expectancy – Net average result per closed trade

• Max Drawdown – Largest recorded drop in equity during the session

• Commission Paid – Simulated trading costs: maker, taker, funding

• Long / Short Trades – Count of entry signals per side

• Time Trading – Number of bars spent in active positions

• Volume / Month – Extrapolated 30-day trading volume estimate

• Min Capital – Lowest equity level recorded during the session

🔹 Reference Ranges by Strategy Type

Use the following metrics as reference depending on the trading style:

Grid / Mean Reversion

• Profit Factor: 1.2 – 2.0

• Payoff Ratio: 0.5 – 1.2

• Win Rate: 50% – 70% (based on partial exits)

• Expectancy: 0.05% – 0.25%

• Drawdown: Moderate to high

• Commission Impact: High

Trend-Following

• Profit Factor: 1.5 – 3.0

• Payoff Ratio: 1.5 – 3.5

• Win Rate: 30% – 50%

• Expectancy: 0.3% – 1.0%

• Drawdown: Low to moderate

Scalping / High-Frequency

• Profit Factor: 1.1 – 1.6

• Payoff Ratio: 0.3 – 0.8

• Win Rate: 80% – 95%

• Expectancy: 0.01% – 0.05%

• Volume / Month: Very high

Breakout Strategies

• Profit Factor: 1.4 – 2.2

• Payoff Ratio: 1.2 – 2.0

• Win Rate: 35% – 60%

• Expectancy: 0.2% – 0.6%

• Drawdown: Can be sharp after failed breakouts

🔹 Note on Performance Simulation

TitanGrid includes internal accounting of fees, slippage, and funding costs.

While its logic is designed for precision and capital efficiency, performance is naturally affected by exchange commissions.

In frictionless environments (e.g., zero-fee simulation), its high-frequency logic could — in theory — extract substantial micro-edges from the market.

However, real-world conditions introduce limits, and all results should be interpreted accordingly.

Leverage

Mxwll Hedge Suite [Mxwll]Hello Traders!

The Mxwll Hedge Suite determines the best asset to hedge against the asset on your chart!

By determining correlation between the asset on your chart and a group of internally listed assets, the Mxwll Hedge Suite determines which asset from the list exhibits the highest negative correlation, and then determines exactly how many coins/shares/contracts of the asset must be bought to achieve a perfect 1:1 hedge!

The image above exemplifies the process!

The purple box on the chart shows the eligible price action used to determine correlation between the asset on my chart (BTCUSDT.P) and the list of cryptocurrencies that can be used as a hedge!

From this price action, the coin determined to have to greatest negative correlation to BTCUSDT.P is FTMUSD.

The image above further outlines the hedge table located in the bottom-right corner of your chart!

The hedge table shows exactly how many coins you’d need to purchase for the hedge asset at various leverages to achieve a perfect 1:1 hedge!

Hedge Suite works on any asset on any timeframe!

And that’s all! A short and sweet script that is hopefully helpful to traders looking to hedge their positions with a negatively correlated asset!

Thank you, Traders!

LRS-Strategy: 200-EMA Buffer & Long/Short Signals LRS-Strategy: 200-EMA Buffer & Long/Short Signals

This indicator is designed to help traders implement the Leveraged Return Strategy (LRS) using the 200-day Exponential Moving Average (EMA) as a key trend-following signal. The indicator offers clear long and short signals by analyzing the price movements relative to the 200-day EMA, enhanced by customizable buffer zones for increased precision.

Key Features:

200-Day EMA: The main trend indicator. When the price is above the 200-day EMA, the market is considered in an uptrend, and when it is below, it indicates a downtrend.

Customizable Buffer Zones: Users can define a percentage buffer around the 200-day EMA (default is 3%). The upper and lower buffer zones help filter out noise and prevent premature signals.

Precise Long/Short Signals:

Long Signal: Triggered when the price moves from below the lower buffer zone, crosses the 200-day EMA, and then breaks above the upper buffer zone.

Short Signal: Triggered when the price moves from above the upper buffer zone, crosses the 200-day EMA, and then breaks below the lower buffer zone.

Alternating Signals: Ensures that a new signal (long or short) is only generated after the opposite signal has been triggered, preventing multiple signals of the same type without a reversal.

Clear Visual Aids: The indicator displays the 200-day EMA and buffer zones on the chart, along with buy (long) and sell (short) signals. This makes it easy to track trends and time entries/exits.

How to Use:

Long Entry: Look for the price to move below the lower buffer, cross the 200-day EMA from below, and then break out of the upper buffer to confirm a long signal.

Short Entry: Look for the price to move above the upper buffer, cross below the 200-day EMA, and then break below the lower buffer to confirm a short signal.

This indicator is perfect for traders who prefer a structured, trend-following approach, using clear rules to minimize noise and identify meaningful long or short opportunities.

Liquidations [ChartPrime]Liquidations Indicator:

The Liquidations indicator is a powerful tool designed to help traders identify significant liquidation levels in financial markets. By analyzing volume data over a specified lookback period, the indicator highlights potential areas where market participants with high leverage positions may face liquidation, providing valuable insights into market dynamics.

Usage:

Traders can use the Liquidations indicator to:

◈ Identify liquidity grab opportunities: Liquidation levels often attract price action as market participants with leveraged positions face the risk of forced liquidation. Traders can anticipate price movements as the market aims to trigger these stops, potentially leading to rapid price movements or reversals.

◈ Confirm trend strength: A cluster of liquidation levels in the same direction as the prevailing trend may confirm the strength of the trend, while divergences between liquidation levels and price movements may signal potential trend reversals.

Settings:

◈ Previous Value Bars Back: Specifies the number of previous bars used in calculating the liquidation levels.

◈ Show Leverage: Allows users to selectively display liquidation levels for different leverage multiples, including 5x, 10x, 25x, 50x, and 100x.

◈ Liquidation Levels Width: Sets the width of the lines representing liquidation levels on the chart.

◈ Short Liquidations Color: Specifies the color of the lines representing short liquidation levels.

◈ Long Liquidations Color: Specifies the color of the lines representing long liquidation levels.

◈ Bar Color: Sets the color of the background bar when the indicator is active.

Visual Representation:

◈ Liquidation levels are plotted as horizontal lines on the chart, with different colors representing short and long liquidation levels.

◈ Each liquidation level is labeled with the corresponding leverage multiple (e.g., 5x, 10x, etc.).

A dashboard displays the active liquidation levels for each leverage multiple, allowing traders to quickly assess the current market conditions.

◈ Time Window allows users to cut off unnecessary part of the chart and concentrate on a current active part of the chart to make better trading decisions:

Interpretation:

Market participants tend to place stop-loss orders near liquidation levels , creating clusters of pending orders. As price approaches these levels, it may trigger a cascade of stop-loss orders, providing liquidity for market orders and potentially leading to rapid price movements in the opposite direction.

Traders can anticipate price reversals or accelerations as price interacts with liquidation levels, using them as reference points for identifying potential entry or exit opportunities.

Note:

While the Liquidations indicator provides valuable insights into market dynamics, traders should use it in conjunction with other technical analysis tools and risk management strategies to make informed trading decisions.

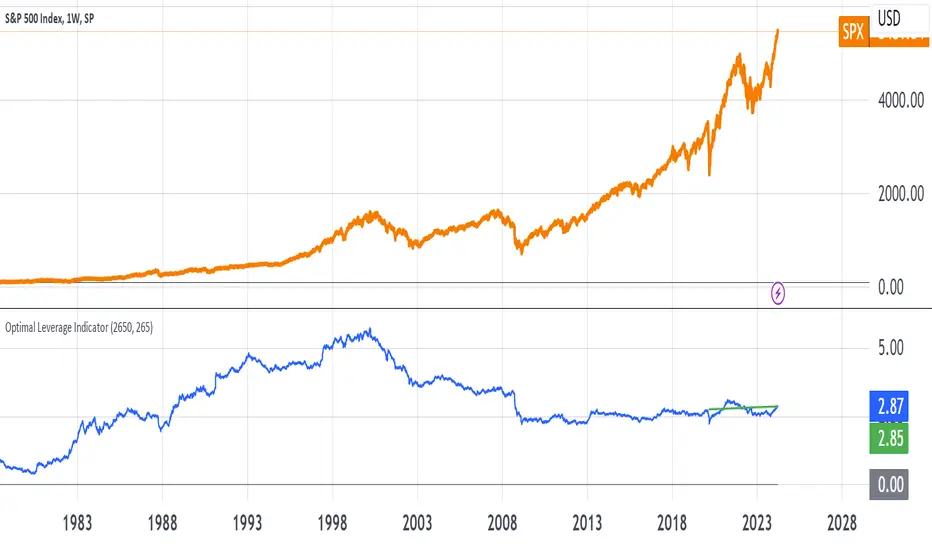

Optimal Leverage IndicatorThe goal of this indicator is to calculate and visualize the optimal leverage and average leverage for a given security based on its historical price data. The optimal leverage is determined by analyzing the relationship between the annualized return and annualized volatility of the security over a specified lookback period.

The methodology can be broken down into the following steps:

Data Input:

The script takes two user inputs: the lookback period and the number of annual trading days.

The lookback period determines the number of historical data points used in the calculations.

The number of annual trading days is used to annualize the return and volatility metrics.

Daily Returns Calculation:

The script retrieves the closing prices of the security on a daily timeframe.

It calculates the daily returns by comparing the current close price with the previous close price.

Mean Return and Volatility Calculation:

The script calculates the mean daily return by taking the simple moving average (SMA) of the daily returns over the specified lookback period.

It also calculates the volatility by taking the standard deviation of the daily returns over the same lookback period.

Annualized Return and Volatility Calculation:

The mean daily return is annualized by compounding it over the number of annual trading days.

The daily volatility is annualized by multiplying it by the square root of the number of annual trading days.

Optimal Leverage Calculation:

The optimal leverage is calculated using the formula: Optimal Leverage = Annualized Return / (Annualized Volatility)^2

This formula assumes that the optimal leverage is proportional to the ratio of the annualized return to the square of the annualized volatility. This is based in this paper: papers.ssrn.com

Average Leverage Calculation:

The script calculates the average leverage by taking the simple moving average (SMA) of the optimal leverage over the specified lookback period.

This provides a smoothed representation of the optimal leverage over time.

The script plots two lines on the chart:

The optimal leverage line (blue) represents the calculated optimal leverage values over time.

The average leverage line (green) represents the average of the optimal leverage values over the specified lookback period.

The main idea behind this methodology is to determine the optimal leverage based on the historical risk-return characteristics of the security. By analyzing the relationship between the annualized return and volatility, the script aims to identify the leverage level that maximizes the return relative to the risk.

The average leverage line provides a smoothed representation of the optimal leverage over time.

Bitcoin Leverage Sentiment - Strategy [presentTrading]█ Introduction and How it is Different

The "Bitcoin Leverage Sentiment - Strategy " represents a novel approach in the realm of cryptocurrency trading by focusing on sentiment analysis through leveraged positions in Bitcoin. Unlike traditional strategies that primarily rely on price action or technical indicators, this strategy leverages the power of Z-Score analysis to gauge market sentiment by examining the ratio of leveraged long to short positions. By assessing how far the current sentiment deviates from the historical norm, it provides a unique lens to spot potential reversals or continuation in market trends, making it an innovative tool for traders who wish to incorporate market psychology into their trading arsenal.

BTC 4h L/S Performance

local

█ Strategy, How It Works: Detailed Explanation

🔶 Data Collection and Ratio Calculation

Firstly, the strategy acquires data on leveraged long (**`priceLongs`**) and short positions (**`priceShorts`**) for Bitcoin. The primary metric of interest is the ratio of long positions relative to the total of both long and short positions:

BTC Ratio=priceLongs / (priceLongs+priceShorts)

This ratio reflects the prevailing market sentiment, where values closer to 1 indicate a bullish sentiment (dominance of long positions), and values closer to 0 suggest bearish sentiment (prevalence of short positions).

🔶 Z-Score Calculation

The Z-Score is then calculated to standardize the BTC Ratio, allowing for comparison across different time periods. The Z-Score formula is:

Z = (X - μ) / σ

Where:

- X is the current BTC Ratio.

- μ is the mean of the BTC Ratio over a specified period (**`zScoreCalculationPeriod`**).

- σ is the standard deviation of the BTC Ratio over the same period.

The Z-Score helps quantify how far the current sentiment deviates from the historical norm, with high positive values indicating extreme bullish sentiment and high negative values signaling extreme bearish sentiment.

🔶 Signal Generation: Trading signals are derived from the Z-Score as follows:

Long Entry Signal: Occurs when the BTC Ratio Z-Score crosses above the thresholdLongEntry, suggesting bullish sentiment.

- Condition for Long Entry = BTC Ratio Z-Score > thresholdLongEntry

Long Exit/Short Entry Signal: Triggered when the BTC Ratio Z-Score drops below thresholdLongExit for exiting longs or below thresholdShortEntry for entering shorts, indicating a shift to bearish sentiment.

- Condition for Long Exit/Short Entry = BTC Ratio Z-Score < thresholdLongExit or BTC Ratio Z-Score < thresholdShortEntry

Short Exit Signal: Happens when the BTC Ratio Z-Score exceeds the thresholdShortExit, hinting at reducing bearish sentiment and a potential switch to bullish conditions.

- Condition for Short Exit = BTC Ratio Z-Score > thresholdShortExit

🔶Implementation and Visualization: The strategy applies these conditions for trade management, aligning with the selected trade direction. It visualizes the BTC Ratio Z-Score with horizontal lines at entry and exit thresholds, illustrating the current sentiment against historical norms.

█ Trade Direction

The strategy offers flexibility in trade direction, allowing users to choose between long, short, or both, depending on their market outlook and risk tolerance. This adaptability ensures that traders can align the strategy with their individual trading style and market conditions.

█ Usage

To employ this strategy effectively:

1. Customization: Begin by setting the trade direction and adjusting the Z-Score calculation period and entry/exit thresholds to match your trading preferences.

2. Observation: Monitor the Z-Score and its moving average for potential trading signals. Look for crossover events relative to the predefined thresholds to identify entry and exit points.

3. Confirmation: Consider using additional analysis or indicators for signal confirmation, ensuring a comprehensive approach to decision-making.

█ Default Settings

- Trade Direction: Determines if the strategy engages in long, short, or both types of trades, impacting its adaptability to market conditions.

- Timeframe Input: Influences signal frequency and sensitivity, affecting the strategy's responsiveness to market dynamics.

- Z-Score Calculation Period: Affects the strategy’s sensitivity to market changes, with longer periods smoothing data and shorter periods increasing responsiveness.

- Entry and Exit Thresholds: Set the Z-Score levels for initiating or exiting trades, balancing between capturing opportunities and minimizing false signals.

- Impact of Default Settings: Provides a balanced approach to leverage sentiment trading, with adjustments needed to optimize performance across various market conditions.

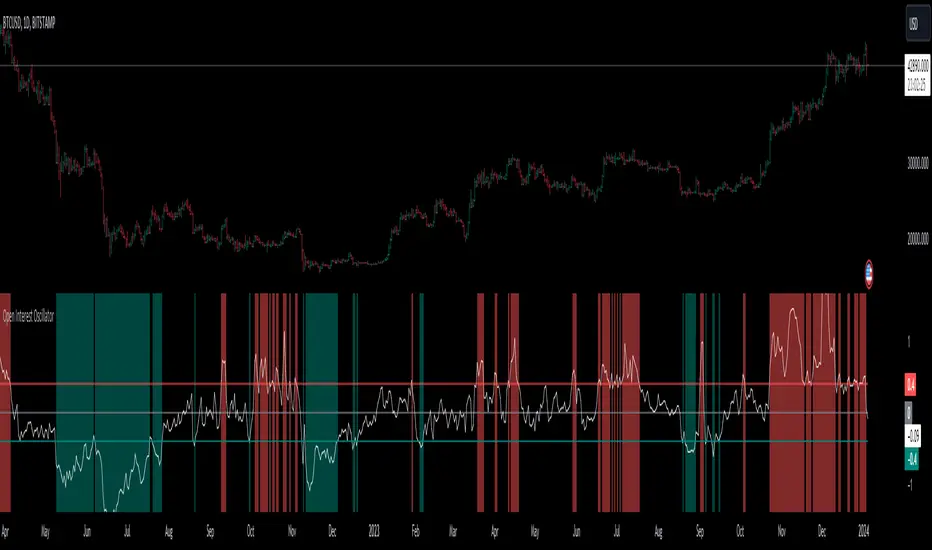

Open Interest OscillatorIn the middle of a bustling cryptocurrency market, with Bitcoin navigating a critical phase and the community hype over potential ETF approvals, current funding rates, and market leverage, the timing is optimal to harness the capabilities of sophisticated trading tools.

Meet the Open Interest Oscillator – special indicator tailored for the volatile arena of cryptocurrency trading. This powerful instrument is adept at consolidating open interest data from a multitude of exchanges, delivering an in-depth snapshot of market sentiment across all timeframes, be it a 1-minute sprint or a weekly timeframe.

This versatile indicator is compatible with nearly all cryptocurrency pairs, offering an expansive lens through which traders can gauge the market's pulse.

Key Features:

-- Multi-exchange Data Aggregation: This feature taps into the heart of the crypto market by aggregating open interest data from premier exchanges such as BINANCE, BITMEX, BITFINEX, and KRAKEN. It goes a step further by integrating data from various pairs and stablecoins, thus providing traders with a rich, multi-dimensional view of market activities.

-- Open Interest Bars: Witness the flow of market dynamics through bars that depict the volume of positions being opened or closed, offering a clear visual cue of trading behavior. In this mode, If bars are going into negative zone, then traders are closing their positions. If they go into positive territory - leveraged positions are being opened.

-- Bollinger Band Integration: Incorporate a layer of statistical analysis with standard deviation calculations, which frame the open interest changes, giving traders a quantified edge to evaluate the market's volatility and momentum.

-- Oscillator with Customizable Thresholds: Personalize your trading signals by setting thresholds that resonate with your unique trading tactics. This customization brings the power of tailored analytics to your strategic arsenal.

-- Max OI Ceiling Setting: In the fast-paced crypto environment where data can surge to overwhelming levels, the Max OI Ceiling ensures you maintain a clear view by capping the open interest data, thus preserving the readability and interpretability of information, even when market activity reaches feverish heights.

Liquidations Meter [LuxAlgo]The Liquidation Meter aims to gauge the momentum of the bar, identify the strength of the bulls and bears, and more importantly identify probable exhaustion/reversals by measuring probable liquidations.

🔶 USAGE

This tool includes many features related to the concept of liquidation. The two core ones are the liquidation meter and liquidation price calculator, highlighted below.

🔹 Liquidation Meter

The liquidation meter presents liquidations on the price chart by measuring the highest leverage value of longs and shorts that have been potentially liquidated on the last chart bar, hence allowing traders to:

gauge the momentum of the bar.

identify the strength of the bulls and bears.

identify probable reversal/exhaustion points.

Liquidation of low-leveraged positions can be indicative of exhaustion.

🔹 Liquidation Price Calculator

A liquidation price calculator might come in handy when you need to calculate at what price level your leveraged position in Crypto, Forex, Stocks, or any other asset class gets liquidated to add a protective stop to mitigate risk. Monitoring an open position gets easier if the trader can calculate the total risk in order for them to choose the right amount of margin and leverage.

Liquidation price is the distance from the trader's entry price to the price where trader's leveraged position gets liquidated due to a loss. As the leverage is increased, the distance from trader's entry price to the liquidation price shrinks.

While you have one or several trades open you can quickly check their liquidation levels and determine which one of the trades is closest to their liquidation price.

If you are a day trader that uses leverage and you want to know which trade has the best outlook you can calculate the liquidation price to see which one of the trades looks best.

🔹 Dashboard

The bar statistics option enables measuring and presenting trading activity, volatility, and probable liquidations for the last chart bar.

🔶 DETAILS

It's important to note that liquidation price calculator tool uses a formula to calculate the liquidation price based on the entry price + leverage ratio.

Other factors such as leveraged fees, position size, and other interest payments have been excluded since they are variables that don’t directly affect the level of liquidation of a leveraged position.

The calculator also assumes that traders are using an isolated margin for one single position and does not take into consideration the additional margin they might have in their account.

🔹Liquidation price formula

the liquidation distance in percentage = 100 / leverage ratio

the liquidation distance in price = current asset price x the liquidation distance in percentage

the liquidation price (longs) = current asset price – the liquidation distance in price

the liquidation price (shorts) = current asset price + the liquidation distance in price

or simply

the liquidation price (longs) = entry price * (1 – 1 / leverage ratio)

the liquidation price (shorts) = entry price * (1 + 1 / leverage ratio)

Example:

Let’s say that you are trading a leverage ratio of 1:20. The first step is to calculate the distance to your liquidation point in percentage.

the liquidation distance in percentage = 100 / 20 = 5%

Now you know that your liquidation price is 5% away from your entry price. Let's calculate 5% below and above the entry price of the asset you are currently trading. As an example, we assume that you are trading bitcoin which is currently priced at $35000.

the liquidation distance in price = $35000 x 0.05 = $1750

Finally, calculate liquidation prices.

the liquidation price (longs) = $35000 – $1750 = $33250

the liquidation price (short) = $35000 + $1750 = $36750

In this example, short liquidation price is $36750 and long liquidation price is $33250.

🔹How leverage ratio affects the liquidation price

The entry price is the starting point of the calculation and it is from here that the liquidation price is calculated, where the leverage ratio has a direct impact on the liquidation price since the more you borrow the less “wiggle-room” your trade has.

An increase in leverage will subsequently reduce the distance to full liquidation. On the contrary, choosing a lower leverage ratio will give the position more room to move on.

🔶 SETTINGS

🔹Liquidations Meter

Base Price: The option where to set the reference/base price.

🔹Liquidation Price Calculator

Liquidation Price Calculator: Toggles the visibility of the calculator. Details and assumptions made during the calculations are stated in the tooltip of the option.

Entry Price: The option where to set the entry price, a value of 0 will use the current closing price. Details are given in the tooltip of the option.

Leverage: The option where to set the leverage value.

Show Calculated Liquidation Prices on the Chart: Toggles the visibility of the liquidation prices on the price chart.

🔹Dashboard

Show Bar Statistics: Toggles the visibility of the last bar statistics.

🔹Others

Liquidations Meter Text Size: Liquidations Meter text size.

Liquidations Meter Offset: Liquidations Meter offset.

Dashboard/Calculator Placement: Dashboard/calculator position on the chart.

Dashboard/Calculator Text Size: Dashboard text size.

🔶 RELATED SCRIPTS

Here are some of the scripts that are related to the liquidation and liquidity concept, for more and other conceptual scripts you are kindly invited to visit LuxAlgo-Scripts .

Liquidation-Levels

Liquidations-Real-Time

Buyside-Sellside-Liquidity

Margin/Leverage CalculationMargin

This library calculates margin liquidation prices and quantities for long and short positions in your strategies.

Usage example

// ############################################################

// # INVESTMENT SETTINGS / INPUT

// ############################################################

// Get the investment capital from the properties tab of the strategy settings.

investment_capital = strategy.initial_capital

// Get the leverage from the properties tab of the strategy settings.

// The leverage is calculated from the order size for example: (300% = x3 leverage)

investment_leverage = margin.leverage()

// The maintainance rate and amount.

investment_leverage_maintenance_rate = input.float(title='Maintanance Rate (%)', defval=default_investment_leverage_maintenance_rate, minval=0, maxval=100, step=0.1, tooltip=tt_investment_leverage_maintenance_rate, group='MARGIN') / 100

investment_leverage_maintenance_amount = input.float(title='Maintanance Amount (%)', defval=default_investment_leverage_maintenance_amount, minval=0, maxval=100, step=0.1, tooltip=tt_investment_leverage_maintenance_amount, group='MARGIN')

// ############################################################

// # LIQUIDATION PRICES

// ############################################################

leverage_liquidation_price_long = 0.0

leverage_liquidation_price_long := na(leverage_liquidation_price_long ) ? na : leverage_liquidation_price_long

leverage_liquidation_price_short = 0.0

leverage_liquidation_price_short := na(leverage_liquidation_price_short ) ? na : leverage_liquidation_price_short

leverage_liquidation_price_long := margin.liquidation_price_long(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

leverage_liquidation_price_short := margin.liquidation_price_short(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

Get the qty for margin long or short position.

margin.qty_long(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

margin.qty_short(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

Get the price and qty for margin long or short position.

= margin.qty_long(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

= margin.qty_short(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

Risk Management GO8686: Stop Loss, Position Size & TargetFull Name: Risk Management GO8686: Stop Loss, Position Size & Target

What this indicator provides:

A dashboard to calculate Stop Loss, Position Size and Target, where users can customize Risk Management parameters in the setting.

Position Size: calculated from "initialCapital", "Leverage", "Max Loss", "feeMaker", "feeTaker".

Stop Loss Price: using pivots, default length is set to 3, with an extra ATR value controlled by "'Multiplier OF Extra ATR".

Target: calculated from entry price, risk reward, distance between entry and stop loss, fees

What the indicator does Not provides:

entries of positions: The Long/Short entries displayed are just MACD signal crossing zero, users can apply their own entry logic, by modifying ready2L / ready2S variables.

What the indicator does Not guarantee:

the integrity, timeliness, accuracy, and comprehensiveness of the data, calculation method, calculation results, etc.

Two types labels:

1. Automated labels: they are displayed when MACD signal crossing zero, use "Display History Labels" to toggle display or not.

2. Setup Manually label: located at the right side of the latest bar, to display results when users setup manually

The settings of the indicator:

"Toggle to Reload",

"InitialCapital", "Leverage", "Max Loss % per trade", "feeMaker", "feeTaker",

4 length inputs for Pivot, "Multiplier of Extra ATR for stop loss",

"Toggle To setup manually", "Toggle between Long / Short", "Entry Price, set manually", "Stop Loss Price, set manually", "Risk-Reward Ratio"

"Display History Labels"

---------- Disclaimer ----------

Before using or requesting access to the indicator, customers/users acknowledge that they have read and accepted that the indicator, any associated contents on all social medias and any communication with the indicator author, including but not limited to: product and service details, signals, alerts, data, calculation methods, calculation results, user manual, tutorials, ideas, videos, chats, messages, emails, blogs, tweets, etc. are provided solely for educational purpose and Not as financial advice. Customers/users understand and agree to use the aforementioned indicator and information at their own risk.

---------- Updates ----------

The latest updates override the previous content.

To activate a update, if it does not load as expected: close the indicator, save the chart, clear browser caches, restart the browser, reload the chart and apply the indicator to the chart.

TTP OI + LS signal filterThis oscillator helps filtering specific conditions in the market based on open interest (OI) and the ratio of longs and shorts (LS) for crypto assets.

Currently it works with BINANCE:BTCUSDT.P but soon I'll be adding support for more assets.

It flags areas of interest like:

- Too many longs, too many shorts in the market

- Open interest too high or too low

It accepts an external signal as a source in which case filters can be applied to the original signal. For example the external signal might trigger and plot a 1 when RSI break below 70. By connecting such signal with this oscillator you'll be able to only pass-through the ones that occur when any of the areas of interest mentioned above are also valid.

If both filter are applied it acts as an OR. For example, if too many longs and too many shorts are active, it will pass through the signal in either condition.

The results of the original signal filtered is printed to be able to later use it in any external backtester strategy that accepts external sources too.

If external source signal is disabled it will trigger any time the combined filters are returning true.

Open interest and the ratio of longs/shorts is considered too high whenever the stochastic RSI calculation of the OI or ratio LS reaches a level above 80 and too low when below 20

The ratio of long/shorts is calculated by dividing the ratio of longs vs shorts from BITFINEX:BTCUSDLONGS and BITFINEX:BTCUSDSHORTS

Crypto Leverage Ratio [Market Cap / Open Interest in %]This indicator calculates what percentage of market cap data corresponds to open interest data.

Leverage Ratio = 1/(Market Cap / 100 * Open Interest)

Market Cap data comes from TradingView -> CRYPTOCAP:YOURCOINSYMBOL

Open Interest data comes from IntoTheBlock -> INTOTHEBLOCK:YOURCOINSYMBOL_PERPETUALOPENINTEREST

IntoTheBlock refresh perpetual data at the end of the day. It means there is no intraday data.

It can only be used in Daily or higher time intervals.

This indicator and any other indicator can not precisely calculate real leverage ratio except exchanges itself. This calculation is just based on assumption.

You can see the exact same result by just adding:

1/(CRYPTOCAP:BTC/100*INTOTHEBLOCK:BTC_PERPETUALOPENINTEREST)

to your symbol search, if your chart is a BTC chart.

"

The Futures Open Interest Leverage Ratio is calculated by dividing the market open contract value, by the market cap of the asset (presented as %). This returns an estimate of the degree of leverage that exists relative to market size as a gauge for whether derivatives markets are a source of deleveraging risk.

High Values indicate that futures market open interest is large relative to the market size. This increases the risk of a short/long squeeze, deleveraging event, or liquidation cascade.

Low Values indicate that futures market open interest is small relative to the market size. This is generally coincident with a lower risk of derivative led forced buying/selling and volatility.

Deleveraging Events such as short/long squeezes, or liquidation cascades can be identified by rapid declines in OI relative to market cap, and vertical drops in the metric.

-glassnode

"

says glassnode. I think it is more than that. Especially with MAs.

Leverage HelperCalculate position size & leverage the easy way!

- Drag & drop entry + stop loss level

- Input account size + risk size in the settings

- Calculation plotted on table

LibIndicadoresUteisLibrary "LibIndicadoresUteis"

Collection of useful indicators. This collection does not do any type of plotting on the graph, as the methods implemented can and should be used to get the return of mathematical formulas, in a way that speeds up the development of new scripts. The current version contains methods for stochastic return, slow stochastic, IFR, leverage calculation for B3 futures market, leverage calculation for B3 stock market, bollinger bands and the range of change.

estocastico(PeriodoEstocastico)

Returns the value of stochastic

Parameters:

PeriodoEstocastico : Period for calculation basis

Returns: Float with the stochastic value of the period

estocasticoLento(PeriodoEstocastico, PeriodoMedia)

Returns the value of slow stochastic

Parameters:

PeriodoEstocastico : Stochastic period for calculation basis

PeriodoMedia : Average period for calculation basis

Returns: Float with the value of the slow stochastic of the period

ifrInvenenado(PeriodoIFR, OrigemIFR)

Returns the value of the RSI/IFR Poisoned of Guima

Parameters:

PeriodoIFR : RSI/IFR period for calculation basis

OrigemIFR : Source of RSI/IFR for calculation basis

Returns: Float with the RSI/IFR value for the period

calculoAlavancagemFuturos(margem, alavancagemMaxima)

Returns the number of contracts to work based on margin

Parameters:

margem : Margin for contract unit

alavancagemMaxima : Maximum number of contracts to work

Returns: Integer with the number of contracts suggested for trading

calculoAlavancagemAcoes(alavancagemMaxima)

Returns the number of batches to work based on the margin

Parameters:

alavancagemMaxima : Maximum number of batches to work

Returns: Integer with the amount of lots suggested for trading

bandasBollinger(periodoBB, origemBB, desvioPadrao)

Returns the value of bollinger bands

Parameters:

periodoBB : Period of bollinger bands for calculation basis

origemBB : Origin of bollinger bands for calculation basis

desvioPadrao : Standard Deviation of bollinger bands for calculation basis

Returns: Two-position array with upper and lower band values respectively

theRoc(periodoROC, origemROC)

Returns the value of Rate Of Change

Parameters:

periodoROC : Period for calculation basis

origemROC : Source of calculation basis

Returns: Float with the value of Rate Of Change

How to use Leverage in PineScriptI believe there are many friends who have been confused by the leverage problem of TradingView strategy, when backtesting, it is always unable to bring its own leverage, so it is impossible to do leverage sustained compounding, this key point, and many friends are looking forward to solve. In particular, the default_qty_value = 100, where 100 is the upper limit.

Here I have used the official RSI strategy for demonstration, using the qty to place orders. Through strategy.equity, leverage and close price, and rounding, directly calculate the specific number of contracts need to be opened.

I hope you can enjoy solving the leverage problem, and I look forward to your pointing out my problems and shortcomings to me. Thank you.

Leverage and contracts toolThis script is more like a tool than an indicator.

The script determinates the amount of contracts and the leverage needed to do one trade.

You must specify the following parameters:

Entry price

Stop Loss price

Stop Loss risk. It's the capital that you will loss if the price hit the SL price.

Operation equity. It's the whole capital involved in the operation.

No matter what side of operation is, it works in both ways (short and long).

To determine the levels could be useful use the short-long position tool of TradingView.

ATR SL + Position Size Calculator [DoctaBot]Props to @Veryfid for his original script 'ATR Stop Loss Finder'.

The concept is simple. We use the average true range to determine an appropriate stop loss distance based on recent volatility. The original script calculated the stop loss offset from the current candle's high or low. Here, I've added the option to offset stop loss from the recent local low or local high (a better way in my opinion).

I have also added a feature to automatically calculate position size by either dollar amount or as a percent of your account size to suit your risk profile (percent of account at risk per trade). This calculator supports use of leverage to calculate the amount of margin required to open desired position size.

Hulk Strategy x35 Leverage 5m chart w/Alerts This strategy is a pullback strategy that utilizes 2 EMAs as a way of identifying trend, MACD as an entry signal, and RSI and ADX to filter bad trades. By using the confirmation of all of these indicators the strategy attempts to catch pullbacks, and it is optimized to wait for high probability setups. Take not that the strategy is optimized for use on BTCUSDT along with 35 times leverage(Using leverage is risky). The Hulk Strategy waits for strong trend confirmation and then attempts to identify pullbacks using MACD and RSI. By using these it identifies strong short term movement against the trend(hence the name Hulk). To use the strategy wait for the strategy to make an entry, and then enter with a stop loss of 1.1% and a take profit of 1.35% with respect to if it is a long or short position. The trade frequency of this strategy is high as it is made for use on the 5m timeframe. But this does not mean you will have to be staring at your computer constantly as an average of 1 trade takes place each day. This will vary a lot though, somedays the strategy enters up to 4 times. I wish you good trading and hope that you like this strategy!

P.S. The indicators on my chart are visualizations of the indicators used in the strategy, they are not necessary for the strategy to work though. Also the colored in cloud on the price chart is an EMA cloud and it comes with the strategy when you add it to your chart. This EMA cloud consists of two EMAs a 50 and a 200 EMA.

Position Sizing CalculatorThis is an intuitive risk management tool with a minimalist design.

This calculator will determine your position size per trade, profit, loss, risk/reward ratio and leverage if any.

It will calculate your leverage if you are trading financial instruments e.g. Mini Futures , Turbo Warrants etc. that have a financing level.

Tip: Use this as a complement to the Long/Short Position tool.

Provide the following inputs to get a calculation:

- Position type

- Account balance

- Risk per trade percentage

- Financing level (if any for leveraged instruments), else let it be 0

- Entry price

- Target price

- Stopp loss price

You can also choose the color of the output text, its background and position in the chart window.

Enjoy!

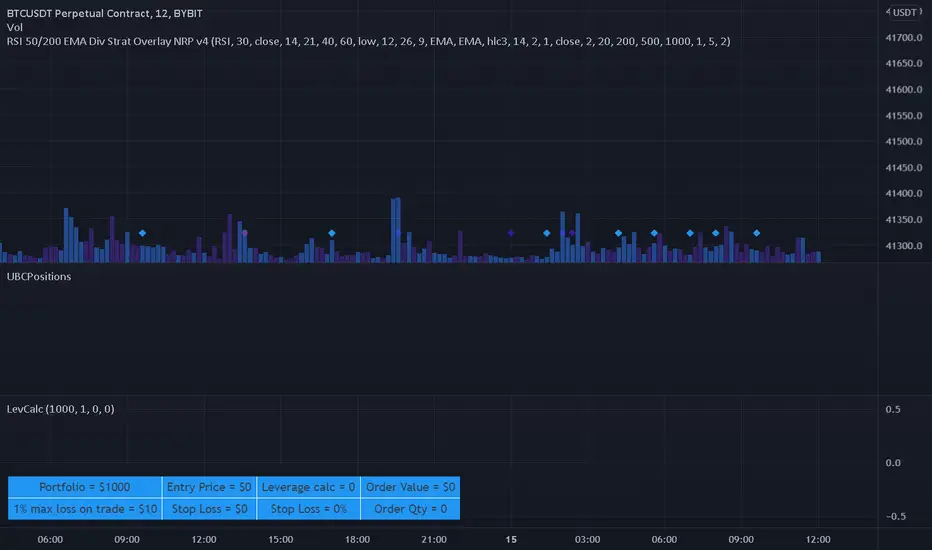

Leverage CalculatorThis script is intended to be used as a risk management calculator.

It will calculate the best leverage to use based on the maximum percentage of loss you are willing to incur on your trading portfolio.

Also calculates the order value and order qty based on your inputs.

Please note this calculator does not take into account any trading fees imposed by the exchange you are using.

*** Only risking 1% to 5% of your portfolio is considered good risk management ***

*** Not financial advice ***

------ Settings Inputs -----------------------------------------------------------------------------------------------------

"Portfolio Size" -- enter your portfolio balance

"% Willing to lose on this trade" -- enter the percent of your portfolio you are willing to lose if the stop loss is hit

"Entry Price" -- enter the price at which you will enter the trade

"Stop Loss Price" -- enter the price at which your stop loss will be set

----------------------------------------------------------------------------------------------------------------------------

------ Outputs -------------------------------------------------------------------------------------------------------------

"Portfolio" -- displays the portfolio balance entered in settings

"max loss on trade" -- displays the % loss entered in settings and the corresponding amount of your portfolio

"Entry Price" -- displays the entry price entered in settings

"Stop Loss Price" -- displays the stop loss price entered in settings

"Stop Loss %" -- displays the calculated percentage loss from the entry price

"Leverage calc" -- displays the calculated leverage based on your max loss and stop loss settings

"Order Value" -- displays the value of the order based on the calculated leverage

"Order Qty" -- displays the calculated order qty based on the calculated leverage

Elevated Leverage index System - ELiSELEVATED LEVERAGE index SYSTEM (ELiS) tries to solve the problem of adjusting meaningful leverage in futures and margin trading.

The biggest problem for traders is adjusting the leverage level manually.

Concerning about the volatilities it's very hard to set a meaningful leverage level.

ELiS includes 4 different volatility component which are:

1- nATR: Normalized Average True Range which is actually ATR/price to stabilize ATR's value differences when price changes are high on long term periods.

2- Standard Deviation

3- Kairi based nATR

4- Bollinger %B

which are scaled from 0 to 100 and takes different averages with different combinations & ratios and combines them as an index.

This index calculates an average volatility to set the true leverage level when trading futures especially in Crypto and FX markets.

There are 5 risk levels of "GEARS" like on automobiles to set the max leverage for risk management.

Gear 1 - CONSERVATIVE: max leverage level can be 20 for swing traders and beginners

Gear 2 - STANDARD: max leverage level can be 25 (default) for day traders

Gear 3 - AVERAGE: max leverage level can be 33 for day traders

Gear 4 - RISKY: max leverage level can be 50 for scalpers

Gear 5 - AGRESSIVE: max leverage level can be 100 for advanced scalpers

default length for ATR, Standard Deviation and %B are all 50

Simply:

When markets aren't volatile: ELiS indicateshigher leverage values to maximize profits.

When markets are volatile enough: ELiS indicates lower values to reduce risk level.

hope you all enjoy ELiS on profitable trades.

Alferow_pnl_up_longThis script allows you to determine the leverage required to enter one position based on the set entry price, the price of the expected take profit, stop loss and risk per transaction. It also allows you to schedule this transaction for 5 possible transactions, with different shoulders and a martingale coefficient for each subsequent gain at the same risk, allowing you to qualitatively improve the pnl of the transaction with price fluctuations after entering the transaction. The script is designed for long positions.

money managementthis indicator has been designed to make your calculations easier and faster.

you can use this indicator to set tp and sl prices based on your entry price, balance,risk and leverage.

it has been designed only for cryptocurrency market and it is not recommended to use it in other markets!

1- enter your balance in the setting of the indicator.

2- enter risk percentage of your balance.

3- enter your sl percentage.

4- enter your tp percentage.

5- set your leverage if you are trading in futures market.

6- and at last set your entry price.

your position size both in spot market and futures market and the exact price of tp and sl , will be shown top right of the screen.

caution: before using this indicator in real market, please make sure that you understand this indicator's behavior and test it.

--------------------------------------------------------------------

این اندیکاتور برای تسریع محاسبات مدیریت سرمایه و سهولت رعایت آن طراحی شده است.

شما میتوانید با وارد کردن پارامترهاقیمت ورودی، سرمایه کل، ریسک و اهرم، قیمت حد سود و ضرر خود را محاسبه کنید.

همچنین اندازه حجم معاملات شما توسط این اندیکاتور محاسبه خواهد شد.

این اندیکاتور برای بازار کریپتوکارنسی طراحی شده است و استفاده از آن در سایر بازارها پیشنهاد نمیشود.

از بخش تنظیمات اندیکاتورمراحل زیر را انجام دهید:

1- میزان سرمایه خود را در قسمت بالانس وارد کنید

2- میزان ریسک سرمایه در هر معامله را مشخص کنید (به درصد)

3- میزان حد ضرر خود را مشخص کنید (به درصد)

4- میزان حد سود خود را مشخص کنید (به درصد)

5- عدد اهرم خود را وارد کنید

6- قیمت ورود به معامله را وارد کنید

توجه: قبل از استفاده این اندیکاتور در بازار لایو لطفا آن را تست کنید و از کارکرد صحیح آن با مدیریت سرمایه خود اطمینان حاصل فرمایید.