Ehlers 2 Pole Butterworth Filter V2 [CC]The 2 Pole Butterworth Filter was created by John Ehlers (Cycle Analytics For Traders pg 32) and this is an updated version of his original 2 pole Butterworth Filter script that seems to follow the price even closer. Buy when the indicator line turns green and sell when it turns red.

Let me know if there are other scripts you would like to see me publish or if you want something custom done!

Filtering

Time Series Lag Reduction Filter by CryptorhythmsTime Series Lag Reduction Filter by Cryptorhythms

Description

A little filter to reduce lag on any time series data. Here we use an EMA to demonstrate how it works, but you could use it in many different ways/appications.

This method can cause overshoot if you get too aggressive with the "lagReduce" setting. In this case lower the lagReduce variable.

👍 We hope you enjoyed this indicator and find it useful! We post free crypto analysis, strategies and indicators regularly. This is our 76th script on Tradingview!

Blackman Filter - The Smoother The BetterIntroduction

Who doesn't like smooth things? I'd like a smooth market price for christmas! But i can't get it, instead its so noisy...so you apply a filter to smooth it, such filters are called low-pass filters, they smooth and its great but they have lag, so nobody really use them, but they are pretty to look at.

Its on a childish note that i will introduce this indicator, so what it is all about? I propose a new FIR filter using a blackman function as filter kernel for financial time-series smoothing, do you prefer the childish tone ? Fear not its surprisingly easy!

The Blackman Function

The blackman function look like a bell shaped curve, look:

The blackman function will produce such curve. This function is called a cosine sum function because she is based on the sum of cosine functions, here only 2.

0.42 - 0.5 * cos(2 * pi * k) + 0.08 * cos(4 * pi * k)

Originally you use this function for windowing , what does it means? In signal processing you have a function called sync function , if you use this function as filter kernel you would get the ideal frequency domain response filter, sometime called brickwall filter, it would be extremely smooth.

Above the optimal low pass filter frequency response.

However the sync function has no ending values and goes on forever, therefore we can't use it for convolution, expect if we apply windowing. Filters using windowing are called windowed-sinc filters, i will describe the procedure below :

1 - Create a sync function = sin(pi*n)/(pi*n)

2 - Truncate it = I only keep the first length points of the sync function.

This create a abrupt end, the frequency of a filter using step 1 as kernel would contain ripples in the pass band and stop band, this is bad! The frequency response would look like this :

3 - I multiply my values of step 2 by a window function, it can the blackman window, i no longer have an abrupt end, its smooth!

The frequency response of the filter using this kernel would no longer have ripples! This is the power of windowing functions.

Here we are not using such thing, but we could in the future. Here instead we use the blackman function as filter kernel, because this function is bell shaped this mean that the filter will certainly be smooth (symmetrical weighting is a rule of thumb for kernels when we want really smooth filters).

The Filter

This filter is quite smooth, unlike the gaussian filter this filter give less weights to recent and past values, this is because the blackman function has fatter tails than the gaussian one. I could make a comparison of both, however they are quite alike, if you often use a gaussian filter its up to you to decide which one you prefer.

The filter can do a better job than the moving average when it comes to preserve the frequency components that constitute the cycles/trend.

We can see that the filter has a greater performance when it comes to keep the shape of the market price, thus it has a slightly better fit.

Conclusion

Ok so in this post you learned a bit about the sync function and windowing, those are basic subjects in signal processing, they allow us to approximate the filter with the ideal frequency response, i also showed you that those windowing function could be used as kernel and that they where pretty smooth on their own, there are many others, but the one i prefer is the blackman windowing function.

I know what you are thinking, "we want trailing stops, alerts, colors, arrows!", and i understand you pal, but sometimes its cool to take a break from all this stuff. However i can tell that i'am working on a side project that aim to estimate rolling maximum/minimum as fast as possible, any experiments will be published here, and i can ensure you that those indicators will make your day quite brighter, we will see that soon.

I hope you learned something from this post! I'am a bit tired (look i'am disappearing !)

Thanks for reading !

Setting-Less Trend-Step FilteringIntroduction

Indicators settings have been a major concern in trading strategies, in order to provide the best results each indicators involved in the strategy must have its settings optimized, when using only 1 indicator this task can easily be achieved, but an increasing number of indicators involve more slower computations, lot of softwares will use brute force for indicators settings optimization, this involve testing each indicator settings and see which setting/combination maximize the equity, in order to fasten this process softwares can use a user defined range for the indicator settings. Nonetheless the combination that maximize the equity at time t might be different at time t+1...n .

Therefore i propose an indicator without any numerical setting that aim to filter small price variations using the architecture of the T-step lsma, such indicator can provide robust filtering and can therefore be used as input for other indicators.

Robustness Vs Non Robustness

Robustness is often defined as the ability of certain statistical tools to be less affected by outliers, outliers are defined as huge variations in a data-set, high volatility movements and large gaps might be considered as outliers. However here we define robustness as the ability of an indicator to be non affected by price variations that are not correlated with the main trend, which can be defined in technical analysis as pullbacks.

Some small pullbacks in INTEL, the indicator is not affected by them, which allow the indicator to filter the price in a "smart" way.

This effect is made possible by using exponential averaging in the indicator, exponential averaging is defined as y = sc*x + (1-sc)*y , with 1 > sc > 0 . Here sc is calculated in a similar way as the kalman gain, which is in the form of a/(a + b) , in our case this is done with :

sc = abs(input - nz(b ))/(abs(input - nz(b )) + nz(a ))

Non Robust Version Of The Indicator

The user is allowed to use the non robust version of the indicator by unchecking "robust" in the setting panel, this allow a better fit with the price at the cost of less filtering.

robust checked

robust unchecked

Conclusion

I proposed a technical indicator that aim to filter short frequencies without the use of parameters, the indicator proven to be robust to various pullbacks and therefore was able to follow the main trend, although using the term trend for such small price variations might be wrong. Removing high frequencies is always beneficial in trading, noisy series are harder to manipulate, this is why you'll see a lot of indicators using median price often defined as hl2 instead of the closing price.

Like previous settings-less indicators i published this one can behave differently depending on the time frame selected by the user, lower time frames will make the indicator filter more. I'll try to make more setting-less indicators that will correct this effect.

Acknowledgements

The support and interest of the community is only thing that allowed me to be where i'am today, i'am thankful. Special thanks to the tv staff, LucF, and my family who may not have believed in this project but are still proud of their son.

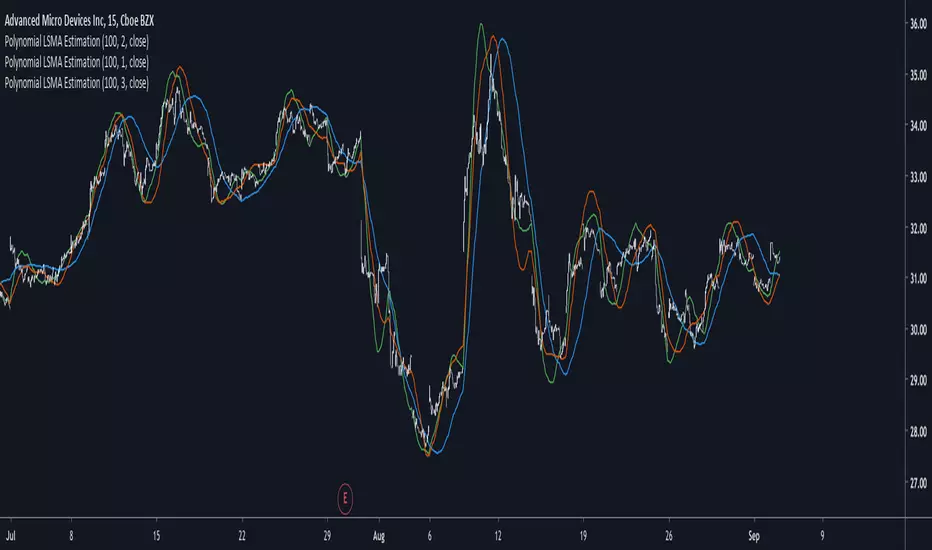

Polynomial LSMA Estimation - Estimating An LSMA Of Any DegreeIntroduction

It was one of my most requested post, so here you have it, today i present a way to estimate an LSMA of any degree by using a kernel based on a sine wave series, note that this is originally a paper that i posted that you can find here figshare.com , in the paper you will be able to find the frequency response of the filter as well as both python and pinescript code.

The least squares moving average or LSMA is a filter that best fit a polynomial function through the price by using the method of least squares, by default the LSMA best fit a line through the input by using the following formula : ax + b where x is often a linear series 1,2,3...etc and a/b are parameters, the LSMA is made by finding a and b such that their values minimize the sum of squares between the lsma and the input.

Now a LSMA of 2nd degree (quadratic) is in the form of ax^2 + bx + c , although the first order LSMA is not hard to make the 2nd order one is way more heavy in term of codes since we must find optimal values for a , b and c , therefore we may want to find alternatives if the goal is simply data smoothing.

Estimation By Convolution

The LSMA is a FIR filter which posses various characteristics, the impulse response of an LSMA of degree n is a polynomial of the same degree, and its step response is a polynomial of degree n+1, estimating those step response is done by the described sine wave series :

f(x) =>

sum = 0.

b = 0.

pi = atan(1)*4

a = x*x

for i = 1 to d

b := 1/i * sin(x*i*pi)

sum := sum + b

pol = a + iff(d == 0,0,sum)

which is simple the sum of multiple sine waves of different frequency and amplitude + the square of a linear function. We then differentiate this result and apply convolution.

The Indicator

length control the filter period while degree control the degree of the filter, higher degree's create better fit with the input as seen below :

Now lets compare our estimate with actual LSMA's, below a lsma in blue and our estimate in orange of both degree 1 and period 100 :

Below a LSMA of degree 2 (quadratic) and our estimate with degree 2 with both period 100 :

It can be seen that the estimate is doing a pretty decent job.

Now we can't make comparisons with higher degrees of lsma's but thats not a real necessity.

Conclusion

This indicator wasn't intended as a direct estimate of the lsma but it was originally based on the estimation of polynomials using sine wave series, which led to the proposed filter showcased in the article. So i think we can agree that this is not a bad estimate although i could have showcased more statistics but thats to many work, but its not that interesting to use higher degree's anyways so sticking with degree 1, 2 and 3 might be for the best.

Hope you like and thanks for reading !

Smart Labelling - Candlestick ChartingThis is a full-fledged implementation of a system presented in an unique research paper 'Profitability of Candlestick Charting Patterns in the Stock Exchange of Thailand' (2017) on candlestick charting, candlestick patterns, trend identification methods, and testing.

You can easily find this paper in the Web. For example, visit: www.researchgate.net

This script is best suited for middle-to-higher time frames. Possible future developments: trend identification and factor calculation techniques.

Donate: PayPal (paypal.me)

HMA-Kahlman Trend, DifferenceFilter & TrendlinesThis update to the previous HMA-Kahlman Trend, Clipping & Trendlines script features the same structure with the three modules:

- Trendlines module,

- NEW Winsorizing submodule using difference-based filtering.

- HMA-Kahlman Trend module.

The Winsorizing submodule filters signals by a volume level, eliminating the ones with the volume below a threshold. This module substitutes the previous 'low-level' filtering implementation. This time it filters out based on difference between scaled volume and its moving average.

Tested with BTCUSD.

Edge-Preserving FilterIntroduction

Edge-preserving smoothing is often used in image processing in order to preserve edge information while filtering the remaining signal. I introduce two concepts in this indicator, edge preservation and an adaptive cumulative average allowing for fast edge-signal transition with period increase over time. This filter have nothing to do with classic filters for image processing, those filters use kernels convolution and are most of the time in a spatial domain.

Edge Detection Method

We want to minimize smoothing when an edge is detected, so our first goal is to detect an edge. An edge will be considered as being a peak or a valley, if you recall there is one of my indicator who aim to detect peaks and valley (reference at the bottom of the post) , since this estimation return binary outputs we will use it to tell our filter when to stop filtering.

Filtering Increase By Using Multi Steps Cumulative Average

The edge detection is a binary output, using a exponential smoothing could be possible and certainly more efficient but i wanted instead to try using a cumulative average approach because it smooth more and is a bit more original to use an adaptive architecture using something else than exponential averaging. A cumulative average is defined as the sum of the price and the previous value of the cumulative average and then this result is divided by n with n = number of data points. You could say that a cumulative average is a moving average with a linear increasing period.

So lets call CMA our cumulative average and n our divisor. When an edge is detected CMA = close price and n = 1 , else n is equal to previous n+1 and the CMA act as a normal cumulative average by summing its previous values with the price and dividing the sum by n until a new edge is detected, so there is a "no filtering state" and a "filtering state" with linear period increase transition, this is why its multi-steps.

The Filter

The filter have two parameters, a length parameter and a smooth parameter, length refer to the edge detection sensitivity, small values will detect short terms edges while higher values will detect more long terms edges. Smooth is directly related to the edge detection method, high values of smooth can avoid the detection of some edges.

smooth = 200

smooth = 50

smooth = 3

Conclusion

Preserving the price edges can be useful when it come to allow for reactivity during important price points, such filter can help with moving average crossover methods or can be used as a source for other indicators making those directly dependent of the edge detection.

Rsi with a period of 200 and our filter as source, will cross triggers line when an edge is detected

Feel free to share suggestions ! Thanks for reading !

References

Peak/Valley estimator used for the detection of edges in price.

Ehlers Decycler OscillatorThis indicator was originally developed by John F. Ehlers (Stocks & Commodities , V.33:10 (September, 2015): "Decyclers").

The idea is still the same as for the Simple Decycler.

Mr. Ehlers suggested to virtually eliminate lag by getting rid of the very low-frequency components. So, he applied the high-pass filter to the simple decycler.

Mr. Ehlers recommended to use two instances of the Decycler Oscillator with different parameters (high-pass filter period and multiplier). As a result, he got the Decycler Oscillator pair.

The first oscillator (red line) has a period of 125 bars, the second one (yellow line) has a period of 100 bars.

The interpretation is straightforward:

When the yellow line crosses over the red line, a trend reversal to the upside is indicated.

When the yellow line crosses under the red line, a trend reversal to the downside is indicated.

Ehlers Simple DecyclerThis indicator was originally developed by John F. Ehlers (Stocks & Commodities, V.33:10 (September, 2015): "Decyclers").

Mr. Ehlers suggested a way to improve trend identification using high-pass filters. The basic smoothers like SMA, low-pass filters, have considerable lag in their display. Mr. Ehlers applied the high-pass filter and subtracted the high-pass filter output from the time series input. Doing these steps he removed high-frequency short-wavelength components (the ones causing the wiggles) from the time series.

As a result he got a special series of the low-frequency components with virtually no lag - the Decycler.

The Decycler is plotted with two additional lines (the percent-shifts of Decycler) and together they form a hysteresis band.

If the prices are above the upper hysteresis line, then the market is in an uptrend . If the prices are below the low hysteresis line, then the market is in a downtrend . Prices within the hysteresis band are trend-neutral .

1LC-LSMA (1 line code lsma with 3 functions)Even Shorter Estimation

I know that i'am insistent with the lsma but i really like it and i'm happy to deconstruct it like a mad pinescript user. But if you have an idea about some kind of indicator then dont hesitate to contact me, i would be happy to help you if its feasible.

My motivation for such indicator was to use back the correlation function (that i had putted aside in the ligh-lsma code) and provide a shorter code than the estimation using the line rescaling method (see : Approximating A Least Square Moving Average In Pine) .

The Method

Fairly simple, lets name y our estimation, we calculate it as follow:

y = x̄ + r*o*1.7

where x̄ is the price moving average, r the correlation between the price and a line (or n) and o the standard deviation. If plotted against a classic lsma the difference would be meaningless at first glance so lets plot the absolute value between the difference of the lsma and our estimation of both period 100.

The difference is under 0.0000 on eurusd, its really low.

In general the longer the period of the estimation, the lower the difference between a normal lsma, but when using shorter period they can differ a little bit.

Why 1.7 ?

We need to multiply the standard deviation by a constant in order to match the overshoot and the rise-time of the original lsma. The constant 1.7 is one that work well but actually this constant should be dependant of the length period of the filter to make the estimation more accurate.

More About Step-Response

Most of the time when a filter have less lag, it mean that he induce overshoot in order to decrease the rise-time . Rise-time is the time the output take to match the target input, its related to the lag. Overshoot mean that the output exceed the target input, you can clearly see those concept in the image above.

Conclusion

I've showed that its possible to be even more concise about the code it take to estimate an lsma. I've also briefly explained the concept of rise-time and overshoot, concepts really important to signal processing and particularly in filter design. I'm sure that it can be even more simplified and i have some ideas for such estimate.

Thanks for reading !

Filtered ATRThis script defines an average true range where extreme events are filtered out.

Extreme events are those bars with a true range larger than 3*sigma+average,

where average and standard deviation are estimated from the last 200 bars.

In this way the ATR is not altered by exceptional events (e.g. the flash crash of Jan 3rd 2019)

and can still be used safely for Stop Losses and Take Profits.

Hitting the like button is a free sign of gratitude, thanks.

Adaptive StochasticAdapt To The Right Situation

There are already some Adaptive Stochastic scripts out there, but i didn't see the concept of using different periods highest/lowest for their calculations. What we want

for such oscillator is to be active when price is trending and silent during range periods. Like that the information we will see will be clear and easy to use.

Switching between a long term highest/lowest during range periods and a short term highest/lowest during trending periods is what will create the adaptive stochastic.

The switching is made thanks to the Efficiency Ratio , the period of the efficiency ratio is determined by the length parameter.

The period of the highest and lowest will depend on the slow and fast parameters, if our efficiency ratio is close to one (trending market) then the indicator will use highest and lowest of period fast , making the indicator more reactive, if our efficiency ratio is low (ranging market) then the indicator will use highest and lowest of period slow , making the indicator less reactive.

The source of the indicator is a running line ( lsma ) of period slow-fast .

it is also possible to switch the parameters values, making the indicator reactive during ranging market and less reactive during trending ones.

Hope you enjoy

For any questions/demands feel free to pm me, i would be happy to help you

One Dimensional Parametric Kalman FilterA One Dimensional Kalman Filter, the particularity of Kalman Filtering is the constant recalculation of the Error between the measurements and the estimate.This version is modified to allow more/less filtering using an alternative calculation of the error measurement.

Camparison of the Kalman filter Red with a moving average Black of both period 50

Can be used as source for others indicators such as stochastic/rsi/moving averages...etc

For any questions/suggestions feel free to contact me

Swing FilterSwing Filter allows you to identify market swings and use the settings to filter out the noise.

The concept is the same as Pine Script's built in pivothigh() and pivotlow(), except with a command center full of controls. Do you to only see swings that are a certain amount higher or lower than their neighboring candles? Want to filter out flash-crashes or freak-spikes? Do you want to count swing-highs or lows that are formed by multiple bars? ...how many? ...how strict? Do you only want swings that are already confirmed or do you want swings that are probably about to be confirmed? You get the idea.

Swing Filter was designed to be plugged into other tools. Swings are used to figure Support and Resistance in Technical Analysis (TA), so you'll find that it is swing filter working in the background of my Support & Resistance Indicator. The creator of this indicator would be happy to help you implement Swing Filter into your workflow, and even can unlock rewiring features that allow Trading View Premium customers to use outputs from other indicators as inputs to swing filter (indicator layering).

INDICATOR SETTINGS:

SWING HIGH VISIBILITY - Show the location of all filtered swing-highs, marked with green "H"

Show Unconfirmed Swing Highs - Whereas a confirmed swing high is shown with a green H, unconfirmed swing highs are shown with an orange H. Sometimes you want to see what could become a swing high before the final right-neighboring candle closes and confirms it. As long as the final right-side candle still has a lower high, we can show an unconfirmed swing high. Once the final right-side candle closes with a lower high, then we have a confirmed swing high. When the "# of Lower Bars to Right of Swing High" setting is set to a number greater than 1, keep in mind that unconfirmed candles will only ever appear one candle prior to confirmation.

# of Lower Bars to Left of Swing High - Swing highs are calculated based on being higher than neighboring candles. How many candles do you want to check to the left-side of a swing high?

# of Lower Bars to Right of Swing High - Swing highs are calculated based on being higher than neighboring candles. How many candles do you want to check to the right-side of a swing high?

Must be This % Higher Than Left Bars - Filter out highs that aren't high enough. "0.5" would require your swing highs to be at least half a percent higher than the high of its confirming left-side bars.

Must be This % Higher Than Right Bars - Filter out highs that aren't high enough. "1" would require your swing highs to be at least one percent higher than the high of its confirming right-side bars.

Multibar Highs - # Bars Allowed to Form High - Filter out or allow highs that are formed at a transition from one bar to another. Especially on low spread exchanges like GDAX, highs may be formed by many consecutive bars, formed by persistant impenetrable buy/sell walls. When using multibar highs, they are counted as a single candle: the swing high will be marked on the right-most high of the multi-bar high, and then the left-side bars are counted from the left-most high of the multi-bar high.

Multibar Highs Strict-Mode - Some multibar highs are just the result of chance, meaning that the first candle reached it's high, went back down, then the second candle reached the same high at a later time. Strict mode will filter these out and only show multibar swing highs that were formed when a candle closed at its high and the next candle opened at its same high. How strict? It allows a one penny difference (for negligible spreads). It also doesn't care about the candles' lows, which leaves room for a future super-strict mode.

*For the complete list of settings and instructions see comments below (sorry they're listed in backwards order below, and the publishing rules won't let me put them all here (too long))

Auto-FilterA least squares filter using the Auto line as source, practical for noise removal without higher phase shift.

Its possible to create another parameter for the auto-line length, just add a parameter Period or whatever you want.

r = round(close/round)*round

dev = stdev(close,Period)

Hope you enjoy :)

Fractals and Levels by JustUncleLEven though there are a many other Fractal and Level indicators, this indicator has some unique features. The indicator will display Fractals, fractal levels and HH/LL points, they will only be drawn after they have completed. Also the indicator has options to :

Show Ideal Fractals Only.

Use Renko Style Fractals, where open/close values are used instead of high/low to find Fractals. This is used to show the correct Fractals when Renko Wicks are enabled.

Has an optional Filter to only display Fractals that are above/below a MA Ribbon.

References:

This code is based on Fractal Levels V8 by RicardoSantos

This is a Renko Chart with "Renko Style Fractals" enabled, notice that the wicks are ignored and only the true Bricks are used for Fractals:

Sawada Masu Moving AverageThe Sawada Masu Moving Average is a filtering technique invented by the japan engineer Sawada Masu with the help of the french trader Alex pierrefeu. This filter have 2 input, a lenght input, who modify the sensibility of the filter to market movement, and a alpha input who just smooth the filter.

The recommended inputs are : a length of 90 and a alpha of 50 for short period, a length of 140 or 200 and a alpha of 90 or 140 for medium period, and a length of 300 and a alpha of 90 for long terms.But feel free to experiment others configurations.

This moving average can be really interesting using it in collaboration with others indicators such another moving average

Hope you enjoy and have a good trades !

I apologize for orthographics or grammar error,i'm from japan and my english is really limited