Mahnam BTC with breake outThis strategy is designed and coded specifically for trading Bitcoin in the 15-minute timeframe.

Of course, those who are skilled in coding can use it in other timeframes and currencies by changing its codes and personalizing it.

Of course, it is strongly recommended that people who want to use it first perform the necessary backtests or test this strategy on demo sites and then trade on the Tetri platform.

In this strategy, it only checks the entry and exit conditions and connects to the exchange using the API code and trades completely automatically.

This strategy determines the stop loss and take profit points on the exchange at the same time as entering the transaction and sets them.

///////////////////////// Code ////////////////////////////////

//@version=5

// Copyright (c) 2021-present, Alex Orekhov (everget)

//indicator('HalfTrend and TMA', overlay=true , max_lines_count = 500, max_labels_count = 500)

strategy(title='Mahnam BTC with breake out', overlay=true , max_bars_back=5000 , max_labels_count= 500 , max_boxes_count = 500,max_lines_count = 500, initial_capital=1000, currency = currency.USDT, default_qty_type=strategy.cash )

import PineCoders/Time/4

/////////////////////////////////////////////////////////////////////////////////////////////////////////////////

newyork = '0000-2400' // input.session(title='Session', defval='0000-2400')

time_newyork = time(timeframe.period, newyork)

///////////////////////////////////////////////////////////////////////////////////////////////////////////

// تعیین تاریخ شروع و پایان (بر حسب timestamp یونیکس)

// تنظیمات Input برای تاریخ شروع و پایان

startDate = input.time(timestamp('01 Jan 2025 00:00 UTC'), "📅 تاریخ شروع معاملات", inline="dateRange")

endDate = input.time(timestamp('31 Dec 2025 23:59 UTC'), "📅 تاریخ پایان معاملات", inline="dateRange")

// بررسی اینکه آیا زمان فعلی در بازه مجاز است یا خیر

isTradeEnabled = (time >= startDate) //and (time <= endDate)

///////////////////////////////////////////////////////////////////////////////////////////

// currentTime = time("15", "GMT+0")

// hourOfDay = hour(currentTime)

// notrade_hours1 = input.(12 , minval = 0 , maxval = 24 , title = "Hours Friday")

// notrade_hours2 = input.int(12 , minval = 0 , maxval = 24 , title = "Hours Monday")

////////////////////////////////////////////////////////////Holidays/////////////////////

// تعریف روزهای هفته

isSaturday = dayofweek == dayofweek.saturday //and hourOfDay > 12

isSunday = dayofweek == dayofweek.sunday

// isMonday = dayofweek == dayofweek.monday and hourOfDay < notrade_hours1

// isFriday = dayofweek == dayofweek.friday and hourOfDay > notrade_hours2

// رنگآمیزی پسزمینه برای شنبه (آبی کمرنگ) و یکشنبه (نارنجی کمرنگ)

bgcolor(isSaturday ? color.new(color.blue, 90) : isSunday ? color.new(color.orange, 90) : na)

//bgcolor(isMonday ? color.new(color.white, 90) : isFriday ? color.new(color.green, 90) : na)

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

//تنظیمات پوزیشن

leverage = input.int(defval = 10 , title = "leverage" , minval = 1 , maxval = 20,step = 5 , group="Posistion Settings==========================================")

quantity = input.float(defval = 500 , title = "quantity" , minval = 1, group="Posistion Settings==========================================")

sl_manager = input.float(defval = 0.5 , step = 0.1 , title = "Risk Percent Of Capital", group="Posistion Settings==========================================")

persent_fee = input.float(defval = 0.05 , title = "Persent Fee Eexchange" , minval = 0 , maxval = 1,step = 0.01 , group="Posistion Settings==========================================")

position_type = input.string(defval = "Buy_And_Sell" , title = "Position_type" , options = , group="Posistion Settings==========================================" )

r_r_long = input.float(defval = 2 , step = 0.1 , title = "R - R =>", group="Posistion Settings==========================================")

r_r_short = r_r_long // input.float(defval = 1.8 , step = 0.1 , title = "r_r Short =>")

//////////////////////////////////////////////////////// END ROC /////////////////////////////////////

day_of_week = input.bool(false , title = "Trade in 7 days", group="Posistion Settings==========================================")

show_tp_sl_ent = true // input.bool(defval=true, title= "Show Tp Sl Ent Box", group="Posistion Settings==========================================")

show_qty = true // input.bool(defval = true , title = "Show Qty Label", group="Posistion Settings==========================================")

//////////////////////////////////////////////////////// Information Position ////////////////////////////////////////////////////

var short_is_open = false

var long_is_open = false

//variant for sell position

var sl1 = 0.0

var tp1 = 0.0

var ent1 = 0.0

var equity1 = 0.0

var qty1 = ""

//variant for buy position

var sl3 = 0.0

var qty2 = ""

var tp3 = 0.0

var ent2 = 0.0

var equity2 = 0.0

symbol = str.tostring(syminfo.basecurrency + "-" + syminfo.currency )

////////////////////////////////////////////////////////////////////////////////////////////////////////

var long_condition = false

var short_condition = false

persent_candel = 0.7 // input.float(defval = 0.7 , step = 0.1 , title = "درصد حرکت آخرین کندل", group="CANDEL Settings==========================================")

////////////////////////////////////////////////////////////////////////////////////////////////////////

amplitude = 2 // input.int(title='Amplitude', defval=2)

channelDeviation =2 //input.int(title='Channel Deviation', defval=2)

showChannels =true // input.bool(title='Show Channels', defval=true)

var int trend = 0

var int nextTrend = 0

var float maxLowPrice = nz(low , low)

var float minHighPrice = nz(high , high)

var float up = 0.0

var float down = 0.0

float atrHigh = 0.0

float atrLow = 0.0

float arrowUp = na

float arrowDown = na

len_atr = 130 // input.int(130 , title = "Len Half Trend")

atr2 = ta.atr(len_atr) / 2

dev = channelDeviation * atr2

highPrice = high

lowPrice = low

highma = ta.sma(high, amplitude)

lowma = ta.sma(low, amplitude)

if nextTrend == 1

maxLowPrice := math.max(lowPrice, maxLowPrice)

if highma < maxLowPrice and close < nz(low , low)

trend := 1

nextTrend := 0

minHighPrice := highPrice

minHighPrice

else

minHighPrice := math.min(highPrice, minHighPrice)

if lowma > minHighPrice and close > nz(high , high)

trend := 0

nextTrend := 1

maxLowPrice := lowPrice

maxLowPrice

if trend == 0

if not na(trend ) and trend != 0

up := na(down ) ? down : down

arrowUp := up - atr2

arrowUp

else

up := na(up ) ? maxLowPrice : math.max(maxLowPrice, up )

up

atrHigh := up + dev

atrLow := up - dev

atrLow

else

if not na(trend ) and trend != 1

down := na(up ) ? up : up

arrowDown := down + atr2

arrowDown

else

down := na(down ) ? minHighPrice : math.min(minHighPrice, down )

down

atrHigh := down + dev

atrLow := down - dev

atrLow

//////////////////////////////////////////////////////////////////////////////////////////////////////////

len_rsi = 14 // input.int(14, group = "RSI Setting=================================")

rsi = ta.rsi(close , len_rsi)

//////////////////////////////////////////////////////////////////////////////////

// محاسبات مربوط به تعیین خطوط حمایت و مقاومت و شکست آنها

show_ATR = input.bool(false)

lookback_15 = 4 // input.int(4, title = "====>Look Back 1H=====>", inline = "2", group = "Setting Pivot======================", tooltip = "Drawing support and resistance in time frame 15 min in selected look back")

pl60 = fixnan(ta.pivotlow( low , lookback_15 , lookback_15 ))

ph60 = fixnan(ta.pivothigh( high , lookback_15 , lookback_15 ))

plot(show_ATR ? pl60 : na , color = color.red)

plot(show_ATR ? ph60 : na , color = color.green)

//////////////////////////////////////////////////////////////////////////////////////////////////////////

/////////////////////////////////////////////////////////////

len_ema_fast_long = 2 // input.int(2)

sorce_tma_long = low // input.source(low)

ema_fast_long = ta.ema(sorce_tma_long , len_ema_fast_long)

len_ema_slow_long = 25 // input.int(25)

ema_slow_long = ta.ema(sorce_tma_long , len_ema_slow_long)

//**********************************

len_ema_fast_short = 2 // input.int(2)

sorce_tma_short = high // input.source(close)

ema_fast_short = ta.ema(sorce_tma_short , len_ema_fast_short)

len_ema_slow_short = 25 // input.int(25)

ema_slow_short = ta.ema(sorce_tma_short , len_ema_slow_short)

///////////////////////////////////////////////////////////////////////////////////////////////////////////

bars = 2 // input.int(9,title="Volume Previous bars to check")

//one_side = input.bool(false, title="Positive values only")

float volume_up = 0

float volume_down = 0

for i = 0 to bars

if (close >open )

volume_up:=volume_up+volume

else

volume_down:=volume_down+volume

total_up_down_vol= volume_up-volume_down

vol_bb = 8 // input.int(8)

vol_aa = 2 // input.int(2)

pivot_high_vol = fixnan(ta.pivothigh(total_up_down_vol , vol_bb , vol_aa ))

pivot_low_vol = fixnan(ta.pivotlow(total_up_down_vol , vol_bb , vol_aa ))

///////////////////////////////////////////////////////////////////////////////////////////////////////////

//////////////////////////////////////////////////////////////////////////////////

CLOSE = close

LOW = low

HIGH = high

//////////////////////////////////////////////////////////////////////////////////

//

//reg_trend_on = input(true, 'Activate Reg Trend Line')

length_bull_bear = 4 // input.int(defval= 4, title='🔹 Length Reg Trend line=', minval=1)

//

BullTrend_hist = 0.0

BearTrend_hist = 0.0

BullTrend = (CLOSE - ta.lowest(LOW, length_bull_bear)) / (ta.sma(ta.tr(true), length_bull_bear ))

BearTrend = (ta.highest(HIGH, length_bull_bear) - CLOSE) / (ta.sma(ta.tr(true), length_bull_bear ))

BearTrend2 = -1 * BearTrend

Trend = BullTrend - BearTrend

// plot columun

if BullTrend < 2

BullTrend_hist := BullTrend - 2

BullTrend_hist

if BearTrend2 > -2

BearTrend_hist := BearTrend2 + 2

BearTrend_hist

//alexgrover-Regression Line Formula

x = bar_index

y = Trend

x_ = ta.sma(x, length_bull_bear)

y_ = ta.sma(y, length_bull_bear)

mx = ta.stdev(x, length_bull_bear)

my = ta.stdev(y, length_bull_bear)

c = ta.correlation(x, y, length_bull_bear)

slope = c * (my / mx)

inter = y_ - slope * x_

reg_trend = x * slope + inter

/////////////////////////////////////////////////

long2 = true

short2 = true

close_H = request.security("" , "" , close )

open_H = request.security("" , "" , open )

if close_H > open_H and close_H > open_H

short2 := false

if close_H < open_H and close_H < open_H

long2 := false

nnn = 1.4 // input.float(1.4 , step = 0.1)

long_1 = BullTrend > nnn and ta.sma(reg_trend , 4 ) > ta.sma(reg_trend , 8 )

short_1 = BearTrend2 < -nnn and ta.sma(reg_trend , 4 ) < ta.sma(reg_trend , 8 )

///////////////////////////////////////////////////

lensig_mdi = 8 // input.int(8, title="ADX Smoothing", minval=1)

len_mdi = 2 // input.int(2, minval=1, title="DI Length")

up_mdi = ta.change(high)

down_mdi = -ta.change(low)

plusDM = na(up_mdi) ? na : (up_mdi > down_mdi and up_mdi > 0 ? up_mdi : 0)

minusDM = na(down_mdi) ? na : (down_mdi > up_mdi and down_mdi > 0 ? down_mdi : 0)

trur_mdi = ta.rma(ta.tr, len_mdi)

plus_mdi = fixnan(100 * ta.rma(plusDM, len_mdi) / trur_mdi)

minus_mdi = fixnan(100 * ta.rma(minusDM, len_mdi) / trur_mdi)

sum = plus_mdi + minus_mdi

adx = 100 * ta.rma(math.abs(plus_mdi - minus_mdi) / (sum == 0 ? 1 : sum), lensig_mdi)

/////////////////////////////////////////////////////////////////////////////////////////////////////////////

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// تنظیمات SuperTrend

atrPeriod = 28 // input(28, title="ATR Period Super Trend")

factor = 3 // input(3.0, title="Multiplier")

= ta.supertrend(factor, atrPeriod)

// تعریف تایمفریمهای بالاتر

htf0 = "30" // input.timeframe("30", title="تایمفریم تأیید اول (1H)")

htf1 = "60" // input.timeframe("60", title=" ایمفریم تأیید دوم (1H)")

htf2 = "240" // input.timeframe("240", title="تایمفریم تأیید سوم (4H)")

// محاسبه SuperTrend در تایمفریمهای بالاتر

supertrend1 = request.security(syminfo.tickerid, htf0, supertrend)

direction1 = request.security(syminfo.tickerid, htf0, direction)

supertrend1H = request.security(syminfo.tickerid, htf1, supertrend )

direction1H = request.security(syminfo.tickerid, htf1, direction)

supertrend4H = request.security(syminfo.tickerid, htf2, supertrend )

direction4H = request.security(syminfo.tickerid, htf2, direction)

// شرایط ورود

Condition_supertrend_long = (direction1H > 0 or direction4H > 0 or direction1 > 0) and volume > fixnan(ta.pivotlow(volume , 16 , 2 ))

Condition_supertrend_short = (direction1H < 0 or direction4H < 0 or direction1 < 0) and volume > fixnan(ta.pivotlow(volume , 16 , 2 ))

//////////////////////////////////////////////////////////////////////////////////////////////////////////

open_4h = request.security("" , "240" , open )

close_4h = request.security("" , "240" , close )

//////////////////////////////////////////////////////////////////////////////////

//////////////////////////////////////////////////////////////////////////////////////////////////////////////

if day_of_week == false

if isTradeEnabled == true and time == time_newyork and not isSaturday and not isSunday //and not isFriday and not isMonday

long_condition := long_is_open == false and short_is_open == false and total_up_down_vol > pivot_low_vol and rsi > 51 and rsi < 80

and math.abs(close - open) < (persent_candel/100) * close and ema_fast_long > ema_slow_long and high > ph60 and open < ph60 and long_1 == true and long2 == true

and plus_mdi > minus_mdi and Condition_supertrend_long == true and high > close_4h and close > atrHigh

short_condition := long_is_open == false and short_is_open == false and total_up_down_vol > pivot_low_vol and rsi < 49 and rsi > 20

and math.abs(close - open) < (persent_candel/100) * close and ema_fast_short < ema_slow_short and low < pl60 and open > pl60 and short_1 == true and short2 == true

and plus_mdi < minus_mdi and Condition_supertrend_short == true and low < close_4h and close < atrLow

if day_of_week == true

if isTradeEnabled == true and time == time_newyork

long_condition := long_is_open == false and short_is_open == false and total_up_down_vol > pivot_low_vol and rsi > 51 and rsi < 80

and math.abs(close - open) < (persent_candel/100) * close and ema_fast_long > ema_slow_long and high > ph60 and open < ph60 and long_1 == true and long2 == true

and plus_mdi > minus_mdi and Condition_supertrend_long == true and high > close_4h and close > atrHigh

short_condition := long_is_open == false and short_is_open == false and total_up_down_vol > pivot_low_vol and rsi < 49 and rsi > 20

and math.abs(close - open) < (persent_candel/100) * close and ema_fast_short < ema_slow_short and low < pl60 and open > pl60 and short_1 == true and short2 == true

and plus_mdi < minus_mdi and Condition_supertrend_short == true and low < close_4h and close < atrLow

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

//تنظیمات استاپ سل پوزیشن شورت و لانگ بر اساس ATR

length_atr = 2 // input.int(title='Length', defval=2, minval=1, group = "StopLoss Setting=================================")

m = 0.9 // input.float(0.9,step = 0.1,title = 'Multiplier', group = "StopLoss Setting=================================")

show_atr = false // input.bool(false, group = "StopLoss Setting=================================")

src1_atr = high //input(high , title = "Stoploss Short")

src2_atr = low //input(low ,title = "Stoploss Long")

collong_atr = color.rgb(0,255,0,0)

colshort_atr = color.rgb(255,0,0,0)

a1 = (ta.sma(ta.tr(true), length_atr) * m) / 2 + (ta.wma(ta.tr(true), length_atr) * m) / 2

stop_loss_short = src1_atr + a1

stop_loss_long = src2_atr - a1

p1_atr1 = plot(show_atr ? stop_loss_long : na, title='ATR Short Stop Loss', color=colshort_atr, style=plot.style_circles)

p2_atr1 = plot(show_atr ? stop_loss_short : na, title='ATR Long Stop Loss', color=collong_atr, style=plot.style_circles)

/////////////////////////////////////////////////////////////////Start Stop Loss///////////////////////////////////////////////

/////////////////////////////////////////////////////////////////END Stop Loss///////////////////////////////////////////////

var total_long_trade = 0

var loss_long = 0

var profit_long = 0

var sood_pos_long = 0.00

var zarar_pos_long = 0.00

var kol_sood_long = 0.00

var total_short_trade = 0

var loss_short = 0

var profit_short = 0

var sood_pos_short = 0.00

var zarar_pos_short = 0.00

var kol_sood_short = 0.00

/////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// ━━━━━━━━━━━━━━━━━━ تنظیمات ورودی ━━━━━━━━━━━━━━━━━━

var int candlesToWait = 12 // input.int(1, "تعداد کندلهای انتظار پس از معامله", minval=1)

// ━━━━━━━━━━━━━━━━━━ شناسایی آخرین معامله ━━━━━━━━━━━━━━━━━━

var int lastTradeCloseBar = na

var bool isCoolDownOver = true

// اگر معاملهای بسته شد، شماره کندل آن را ذخیره کن

if strategy.closedtrades > 0 and (na(lastTradeCloseBar) or strategy.closedtrades != strategy.closedtrades )

lastTradeCloseBar := bar_index

isCoolDownOver := false

// بررسی آیا تعداد کندلهای موردنظر گذشته است؟

if not na(lastTradeCloseBar) and (bar_index - lastTradeCloseBar) >= candlesToWait

isCoolDownOver := true

bgcolor(isCoolDownOver ? na : color.new(color.red, 90), title="Cooldown Status")

/////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// تنظیمات دستورات لازم برای ارسال به صرافی جهت پوزیشن لانگ

//ADD_quantity = 1.5 // input.float(2 , title = "در صورت واگرایی ماجین رو چند بابر کنم؟")

if position_type == "Buy" or position_type == "Buy_And_Sell"

if long_condition and isCoolDownOver

ent2 := close

sl3 :=stop_loss_long - (stop_loss_long * (0.5 / leverage) / 100 )

tp3 := ent2 + ((ent2 - sl3) * r_r_long)

number_coin = ((quantity * leverage * sl_manager) / ((ent2 - sl3) *100))

equity2 := math.round ((number_coin * close ) , 3)

if equity2 > quantity * leverage

equity2 := quantity * leverage

//////////////////////////////////////////////////////////////////////////////////

if show_qty

label.new(bar_index , low , str.tostring(equity2) + "$" , color = color.rgb(0, 255, 0,0) , size = size.normal , style = label.style_label_up)

strategy.entry(id="buy", direction = strategy.long , qty=(equity2/close) )

if close >= 10 and close < 500

qty2 := str.tostring(math.round(equity2/close , 2))

else

qty2 := str.tostring(math.round(equity2/close , 0))

if close > 500

qty2 := str.tostring(math.round(equity2/close , 3 ))

if symbol == "AAVEUSDT"

qty2 := str.tostring(math.round(equity2/close , 1))

// ================/ برای باز کردن پوزیشن از این مقدار استفاده میکند /======================

message1 = '{"symbol":"'+symbol+'","type":"MARKET", "side":"BUY", "positionSide": "LONG", "quantity":"'+qty2+'","leverage": "'+str.tostring(leverage)+'","marginMode": "Isolated","botmix-action":"open-market-order-v2"}'

// message1 = '{ "side":"Ask","symbol":"'+symbol+'","tradeType":"Market","entrustVolume":"'+qty1+'","action":"Open","marginMode":"Isolated","leverage":"'+str.tostring(leverage)+'", "takerProfitPrice":"'+str.tostring(tp1)+'","stopLossPrice":"'+str.tostring(sl1)+'","botmix-action":"open-market-order" }'

// message1 = '{ "batchOrders": ,"botmix-action":"open-multiple-order" }'

alert(message1 , alert.freq_once_per_bar)

message2 = '{"symbol":"'+symbol+'","type":"LIMIT","side":"SELL", "positionSide": "LONG","delay": 5 ,"quantity":"'+qty2+'","price": "'+str.tostring(tp3)+'", "botmix-action":"open-market-order-v2"}'

alert(message2 , alert.freq_once_per_bar)

message3 = '{"symbol":"'+symbol+'","type":"STOP_MARKET","side":"SELL","positionSide": "LONG","delay": 10 ,"quantity":"'+qty2+'","price": "'+str.tostring(sl3)+'", "stopPrice": "'+str.tostring(sl3)+'","botmix-action":"open-market-order-v2"}'

alert(message3 , alert.freq_once_per_bar)

long_is_open := true

if show_tp_sl_ent

line.new(bar_index, tp3, bar_index + 15, tp3, xloc= xloc.bar_index, color= color.rgb(0, 255, 0,0 ), width = 1)

box.new(bar_index , tp3 , bar_index + 15 , ent2 ,bgcolor = color.rgb(0, 255, 0 , 90) , border_color = color.rgb(0, 255, 0 , 80) )

line.new(bar_index, (tp3 - ((tp3 - ent2) /2)), bar_index + 15, (tp3 - ((tp3 - ent2) /2)), xloc= xloc.bar_index, color= color.rgb(0, 17, 255), width = 2 , style = line.style_dashed)

line.new(bar_index, sl3, bar_index + 15, sl3, xloc= xloc.bar_index, color= color.rgb(255, 0, 0,0), width = 1)

box.new(bar_index , sl3 , bar_index + 15 , ent2 ,bgcolor = color.rgb(255, 0, 0, 90) , border_color = color.rgb(255, 0, 0 , 80) )

line.new(bar_index , ent2 , bar_index + 15 , ent2 , color = color.rgb(255, 255, 0, 0))

/////////////////////////////////////////////////////////

total_long_trade := total_long_trade + 1

if low <= sl3 and long_is_open == true

loss_long := loss_long + 1

zarar_pos_long := zarar_pos_long + (((ent2 - sl3) / ent2) * equity2)

if high >= tp3 and long_is_open == true

profit_long := profit_long + 1

sood_pos_long := sood_pos_long +(((tp3 - ent2) / ent2) * equity2)

kol_sood_long := sood_pos_long - zarar_pos_long

/////////////////////////////////////////////////////////////

if (low <= sl3 or high >= tp3) and long_is_open == true

long_is_open := false

strategy.exit( id = "buy" , from_entry = "buy" , limit = tp3 , stop = sl3 , qty_percent = 100 , comment_profit = "tp" , comment_loss = "sl" )

color_kol_pos_long = kol_sood_long >0 ? color.rgb(0,255,0) : color.rgb(255,0,0)

// //////////////////////LONG___ENNNDD//////////////////////////////////////////////////////////

// تظیمات دستورات لازم برای ارسال به صرافی جهت پوزیشن شورت

if position_type == "Sell" or position_type == "Buy_And_Sell"

if short_condition and isCoolDownOver

ent1 := close

sl1 :=stop_loss_short + (stop_loss_short * (0.5 / leverage) / 100 )

tp1 := ent1 - ((sl1 - ent1 ) * r_r_short)

number_coin = ((quantity * leverage * sl_manager) / ((sl1 - ent1) *100))

equity1 := math.round ((number_coin * close ) , 3)

if equity1 > quantity * leverage

equity1 := quantity * leverage

/////////////////////////////////////////////////////////////////////////////////////////

if show_qty

label.new(bar_index , high , str.tostring(equity1) + "$" , color = color.rgb(255, 0, 0,0) , size = size.normal , style = label.style_label_down)

strategy.entry(id="sell", direction = strategy.short, qty=(equity1/close) )

if close >= 10 and close < 500

qty1 := str.tostring(math.round(equity1/close , 2))

else

qty1 := str.tostring(math.round(equity1/close , 0))

if close > 500

qty1 := str.tostring(math.round(equity1/close , 3))

if symbol == "AAVEUSDT"

qty1 := str.tostring(math.round(equity1/close , 1))

// ================/ برای باز کردن پوزیشن از این مقدار استفاده میکند /======================

message1 = '{"symbol":"'+symbol+'","type":"MARKET", "side":"SELL", "positionSide": "SHORT", "quantity":"'+qty1+'","leverage": "'+str.tostring(leverage)+'","marginMode": "Isolated","botmix-action":"open-market-order-v2"}'

// message1 = '{ "side":"Ask","symbol":"'+symbol+'","tradeType":"Market","entrustVolume":"'+qty1+'","action":"Open","marginMode":"Isolated","leverage":"'+str.tostring(leverage)+'", "takerProfitPrice":"'+str.tostring(tp1)+'","stopLossPrice":"'+str.tostring(sl1)+'","botmix-action":"open-market-order" }'

// message1 = '{ "batchOrders": ,"botmix-action":"open-multiple-order" }'

alert(message1 , alert.freq_once_per_bar)

message2 = '{"symbol":"'+symbol+'","type":"LIMIT","side":"BUY", "positionSide": "SHORT","delay": 5 ,"quantity":"'+qty1+'","price": "'+str.tostring(tp1)+'", "botmix-action":"open-market-order-v2"}'

alert(message2 , alert.freq_once_per_bar)

message3 = '{"symbol":"'+symbol+'","type":"STOP_MARKET","side":"BUY","positionSide": "SHORT","delay": 10 ,"quantity":"'+qty1+'","price": "'+str.tostring(sl1)+'", "stopPrice": "'+str.tostring(sl1)+'","botmix-action":"open-market-order-v2"}'

alert(message3 , alert.freq_once_per_bar)

short_is_open := true

if show_tp_sl_ent

line.new(bar_index, tp1, bar_index + 15, tp1, xloc= xloc.bar_index, color= color.rgb(0, 255, 0,0 ), width = 1)

box.new(bar_index , tp1 , bar_index + 15 , ent1 ,bgcolor = color.rgb(0, 255, 0 , 90) , border_color = color.rgb(0, 255, 0 , 80) )

line.new(bar_index, (tp1+((ent1 - tp1)/2)), bar_index + 15, (tp1+((ent1 - tp1)/2)), xloc= xloc.bar_index, color= color.rgb(4, 0, 255), width = 2 , style= line.style_dashed)

line.new(bar_index, sl1, bar_index + 15, sl1, xloc= xloc.bar_index, color= color.rgb(255, 0, 0,50), width = 1)

box.new(bar_index , sl1 , bar_index + 15 , ent1 ,bgcolor = color.rgb(255, 0, 0, 90) , border_color = color.rgb(255, 0, 0 , 80) )

line.new(bar_index , ent1 , bar_index + 15 , ent1 , color = color.rgb(255, 255, 0,0))

////////////////////////////////////////////////////////////////////////////////////

total_short_trade := total_short_trade + 1

if high >= sl1 and short_is_open == true

loss_short := loss_long + 1

zarar_pos_short := zarar_pos_short + (((sl1 - ent1) / ent1) * equity1)

if low <= tp1 and short_is_open == true

profit_short := profit_short + 1

sood_pos_short := sood_pos_short +(((ent1 - tp1) / ent1) * equity1)

kol_sood_short := sood_pos_short - zarar_pos_short

///////////////////////////////////////////////////////////////////////////////////

if (high >= sl1 or low <= tp1 ) and short_is_open == true

short_is_open := false

strategy.exit( id = "sellext1" , from_entry = "sell" , limit = tp1 , stop = sl1 , qty_percent = 100 , comment_profit = "tp" , comment_loss = "sl" )

color_kol_pos_short = kol_sood_short > 0 ? color.rgb(0,255,0) : color.rgb(255,0,0)

////////////////////////////////////////////////////////////////////////////////////////////

kol_trade = loss_short + loss_long + profit_long + profit_short

/////////////////////SHORT___ENNNDD//////////////////////////////////////////////////////

closed_trades = (loss_short + loss_long + profit_long + profit_short) // strategy.closedtrades

kolfee = (closed_trades * quantity * leverage * persent_fee) / 100

net_profit = math.round((kol_sood_short + kol_sood_long) , 2 ) - kolfee

net_percent = math.round((net_profit / quantity) * 100 , 2)

win_rate = math.round(((profit_long + profit_short) / kol_trade) * 100 , 2) //math.round((strategy.wintrades / strategy.closedtrades) * 100 , 2)

ending = math.round((quantity + net_profit) , 2)

profit_factor = math.round((sood_pos_long + sood_pos_short) / math.abs(zarar_pos_long + zarar_pos_short) , 2)

drow_down = math.round((strategy.max_drawdown / quantity) * 100, 2 )

show_reportTabel = input.bool(true)

if show_reportTabel

table_color = color.rgb(0, 0, 0)

var table result_table = table.new(position.top_right, 30, 40, bgcolor=color.rgb(255,255,255,0), frame_color=color.rgb(0, 0, 0,0), frame_width=1, border_width=2)

table.cell(result_table , column = 0 , row = 0 , text = "TEST BTC with breake out: " + str.tostring(kol_trade) , bgcolor = table_color , text_color = color.rgb(255,255,255,0))

table.cell(result_table , column = 1 , row = 0 , text = "starting: " + str.tostring(quantity) + "$" , bgcolor = table_color, text_color = color.rgb(255,255,255,0))

table.cell(result_table , column = 2 , row = 0 , text = "Net Profit: " + str.tostring(net_profit) + "$: " + " fee = " + str.tostring(kolfee) , bgcolor = table_color, text_color = net_profit > 0 ? color.rgb(0,255,0,0) : color.rgb(255,0,0,0))

table.cell(result_table , column = 0 , row = 1 , text = "Win Rate: " + str.tostring(win_rate) + "%" , bgcolor = table_color, text_color = color.rgb(255,255,255,0))

table.cell(result_table , column = 1 , row = 1 , text = "Ending: " + str.tostring(ending) + "$" , bgcolor = table_color, text_color = color.rgb(255,255,255,0))

table.cell(result_table , column = 2 , row = 1 , text = "Profit Factor: " + str.tostring(profit_factor) , bgcolor = table_color, text_color = color.rgb(255,255,255,0))

table.cell(result_table , column = 3 , row = 0 , text = "Net Percent: " + str.tostring(net_percent) + "%" , bgcolor = table_color, text_color = net_percent > 0 ? color.rgb(0,255,0,0) : color.rgb(255,0,0,0))

table.cell(result_table , column = 3 , row = 1 , text = "Draw Down: " + str.tostring(drow_down) + "%" , bgcolor = table_color, text_color = color.rgb(255,255,255,0))

table.cell(result_table , column = 4 , row = 0 , text = "Stop: " + "Short =" + str.tostring(loss_short)+ " " +"Long =" + str.tostring(loss_long) , bgcolor = table_color, text_color = color.rgb(255,0,0,0))

table.cell(result_table , column = 4 , row = 1 , text = "TP: " + "Short =" + str.tostring(profit_short)+ " " +"Long =" + str.tostring(profit_long) , bgcolor = table_color, text_color = color.rgb(0,255,0,0))

table.cell(result_table , column = 5 , row = 0 , text = "Short: " + "sood =" + str.tostring(math.round(sood_pos_short,2)) + " " + "Zarar =" + str.tostring(math.round(zarar_pos_short,2)) , bgcolor = table_color, text_color = color.rgb(0,255,0,0))

table.cell(result_table , column = 5 , row = 1 , text = "Long: " + "sood =" + str.tostring(math.round(sood_pos_long,2)) + " " + "Zarar =" + str.tostring(math.round(zarar_pos_long,2)) , bgcolor = table_color, text_color = color.rgb(0,255,0,0))

table.cell(result_table , column = 6 , row = 0 , text = "Kol Sood Short: " + "Short =" + str.tostring(math.round(kol_sood_short,2)) , bgcolor = table_color, text_color = color_kol_pos_short)

table.cell(result_table , column = 6 , row = 1 , text = "Kol Sood Long: " + "LONG =" + str.tostring(math.round(kol_sood_long,2)) , bgcolor = table_color, text_color = color_kol_pos_long)

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// //////////////////////////////////////////////////////////////////////////////////////////////////////

// // ********** تنظیمات **********

// show_monthly_Report = input.bool(false, "نمایش گزارش ماهیانه")

// exchange_fee_percent = 0.05 / 100 // input.float(0.05, "کارمزد صرافی (%)", step=0.01) / 100

// indicator_name = 'BTC with breake out' // input.string("تحلیلگر حرفه ای - گزارش ماهیانه", "عنوان اندیکاتور")

// show_total_row = true // input.bool(true, "نمایش سطر جمع کل")

// // ********** ایجاد جدول **********

// var table monthlyReport = table.new(position = position.top_right, columns = 6,rows = 21,bgcolor = color.rgb(33, 33, 33),

// border_width = 2,border_color = color.rgb(80, 80, 80),frame_width = 1,frame_color = color.rgb(50, 50, 50))

// // ********** متغیرهای ماهیانه **********

// var int currentMonth = na

// var int monthTrades = 0

// var int monthWinningTrades = 0

// var float totalFees = 0.0

// var float monthNetProfit = 0.0

// // ********** متغیرهای جمع کل **********

// var float totalAllTrades = 0.0

// var float totalAllFees = 0.0

// var float totalAllNetProfit = 0.0

// var int totalAllWinningTrades = 0

// var int totalAllMonths = 0

// // ********** تشخیص تغییر ماه **********

// isNewMonth = ta.change(month) or ta.change(year)

// // ********** محاسبات معاملات **********

// tradeClosed = strategy.closedtrades > strategy.closedtrades

// if tradeClosed

// lastTradeIndex = strategy.closedtrades - 1

// tradeSize = math.abs(strategy.closedtrades.size(lastTradeIndex) * strategy.closedtrades.exit_price(lastTradeIndex))

// tradeFee = tradeSize * exchange_fee_percent

// totalFees := totalFees + tradeFee

// tradeProfit = strategy.closedtrades.profit(lastTradeIndex)

// monthNetProfit := monthNetProfit + tradeProfit

// monthTrades := monthTrades + 1

// if tradeProfit > 0

// monthWinningTrades := monthWinningTrades + 1

// // ********** مدیریت گزارش ماهیانه **********

// if isNewMonth and show_monthly_Report and not na(currentMonth)

// // محاسبات ماهانه

// grossProfit = monthNetProfit

// netProfit = grossProfit - totalFees

// winRate = monthTrades > 0 ? (monthWinningTrades/monthTrades)*100 : 0

// // به روزرسانی جمع کل

// totalAllTrades := totalAllTrades + monthTrades

// totalAllFees := totalAllFees + totalFees

// totalAllNetProfit := totalAllNetProfit + netProfit

// totalAllWinningTrades := totalAllWinningTrades + monthWinningTrades

// totalAllMonths := totalAllMonths + 1

// // نمایش در جدول

// row = (month % 12 == 0 ? 12 : month % 12) + 2 // +2 برای جا دادن سطرهای عنوان

// monthName = str.tostring(year ) + "-" + str.tostring(month , "00")

// table.cell(monthlyReport, 0, row, monthName, text_color=color.white)

// table.cell(monthlyReport, 1, row, str.tostring(monthTrades), text_color=color.white)

// table.cell(monthlyReport, 2, row, str.tostring(grossProfit, "0.00") + " $")

// table.cell(monthlyReport, 3, row, str.tostring(totalFees, "0.00") + " $")

// table.cell(monthlyReport, 4, row, str.tostring(netProfit, "0.00") + " $")

// table.cell(monthlyReport, 5, row, str.tostring(winRate, "1.0") + "%")

// // رنگ آمیزی سود/زیان

// textColor = netProfit >= 0 ? color.rgb(0, 200, 0) : color.rgb(200, 0, 0)

// for i = 2 to 5

// table.cell_set_text_color(monthlyReport, i, row, textColor)

// // ********** سطر جمع کل **********

// if show_monthly_Report and show_total_row and totalAllMonths > 0

// totalWinRate = totalAllTrades > 0 ? (totalAllWinningTrades/totalAllTrades)*100 : 0

// table.cell(monthlyReport, 0, 15, "جمع کل (" + str.tostring(totalAllMonths) + " ماه)",

// text_color=color.yellow,

// bgcolor=color.rgb(50, 50, 50),

// width=6)

// table.cell(monthlyReport, 1, 15, str.tostring(totalAllTrades),

// text_color=color.yellow,

// bgcolor=color.rgb(50, 50, 50))

// table.cell(monthlyReport, 2, 15, str.tostring(totalAllNetProfit + totalAllFees, "0.00") + " $",

// text_color=color.yellow,

// bgcolor=color.rgb(50, 50, 50))

// table.cell(monthlyReport, 3, 15, str.tostring(totalAllFees, "0.00") + " $",

// text_color=color.yellow,

// bgcolor=color.rgb(50, 50, 50))

// table.cell(monthlyReport, 4, 15, str.tostring(totalAllNetProfit, "0.00") + " $",

// text_color = totalAllNetProfit >= 0 ? color.green : color.red,

// bgcolor=color.rgb(50, 50, 50))

// table.cell(monthlyReport, 5, 15, str.tostring(totalWinRate, "1.0") + "%",

// text_color=color.yellow,

// bgcolor=color.rgb(50, 50, 50))

// // ********** ریست ماهیانه **********

// if isNewMonth

// currentMonth := month

// monthTrades := 0

// monthWinningTrades := 0

// totalFees := 0.0

// monthNetProfit := 0.0

// // ********** عنوانهای جدول **********

// if barstate.isfirst and show_monthly_Report

// // عنوان اصلی (یکپارچه در سطر اول)

// table.cell(

// monthlyReport,

// column = 4, // ستون شروع (0 = اولین ستون)

// row = 0, // ردیف 0 (اولین ردیف)

// text = indicator_name,

// bgcolor = color.rgb(0, 0, 0),

// text_size = size.small,

// text_color = color.rgb(255,255,0),

// width = 12, // گسترش روی تمام 6 ستون

// height = 4 // ارتفاع بیشتر برای وضوح بهتر

// )

// // عنوان ستونها (در ردیف دوم)

// headers = array.from("ماه", "تعداد", "سود ناخالص", "کارمزد", "سود خالص", "نرخ برد")

// for i = 0 to 5

// table.cell(

// monthlyReport,

// column = i,

// row = 1, // ردیف بعد از عنوان اصلی

// text = array.get(headers, i),

// text_color = color.white,

// bgcolor = color.rgb(60, 60, 60),

// width = 1 // عرض معمولی برای هر ستون

// )

Yatırımcı Taahhüdü (COT)

Planting & Harvesting SeasonsHello all,

as a commodity trader, I use a lot of seasonal patterns in my analysis. Some time ago, I came up with the idea to develop a simple script that visually overlays the typical planting and harvesting periods for key agricultural futures directly on the chart.

This script automatically detects the underlying commodity based on the symbol (e.g. ZC, ZW, ZS, CT) and displays color-coded zones for each seasonal window. These zones are based on historical crop calendars and help identify when planting or harvesting typically takes place. The goal is to better align technical setups with fundamental seasonal factors.

This is a basic version and meant as a visual aid — not a trading signal in itself.

Hope you enjoy it and any feedback is highly appreciated!

High-Impact News Events with ALERTHigh-Impact News Events with ALERT

This indicator is builds upon the original by adding alert capabilities, allowing traders to receive notifications before and after economic events to manage risk effectively.

This indicator is updated version of the Live Economic Calendar by @toodegrees ( ) which allows user to set alert for the news events.

Key Features

Customizable Alert Selection: Users can choose which impact levels to restrict (High, Medium, Low).

User-Defined Restriction Timing: Set alerts to X minutes before or after the event.

Real-Time Economic Event Detection: Fetches live news data from Forex Factory.

Multi-Event Support: Detects and processes multiple news events dynamically.

Automatic Trading Restriction: user can use this script to stop trades in news events.

Visual Markers:

Vertical dashed lines indicate the start and end of restriction periods.

Background color changes during restricted trading times.

Alerts notify traders during the news events.

How It Works

The user selects which news impact levels should restrict trading.

The script retrieves real-time economic event data from Forex Factory.

Trading can be restricted for X minutes before and after each event.

The script highlights restricted periods with a background color.

Alerts notify traders all time during the news events is active as per the defined time to prevent unexpected volatility exposure.

Customization Options

Choose which news impact levels (High, Medium, Low) should trigger trading restrictions.

Define time limits before and after each news event for restriction.

Enable or disable alerts for restricted trading periods.

How to Use

Apply the indicator to any TradingView chart.

Configure the news event impact levels you want to restrict.

Set the pre- and post-event restriction durations as needed.

The indicator will automatically apply restrictions, plot visual markers, and trigger alerts accordingly.

Limitations

This script relies on Forex Factory data and may have occasional update delays.

TradingView does not support external API connections, so data is updated through internal methods.

The indicator does not execute trades automatically; it only provides visual alerts and restriction signals.

Reference & Credit

This script is based on the Live Economic Calendar by @toodegrees ( ), adding enhanced pre- and post-event alerting capabilities to help traders prepare for market-moving news.

Disclaimer

This script is for informational purposes only and does not constitute financial advice. Users should verify economic data independently and exercise caution when trading around news events. Past performance is not indicative of future results.

The Commitment of Traders (COT) IndexThe COT Index indicator is used to measure the positioning of different market participants (Large Traders, Small Traders, and Commercial Hedgers) relative to their historical positioning over a specified lookback period. It helps traders identify extreme positioning, which can signal potential reversals or trend continuations.

Key Features of the Indicator:

COT Data Retrieval

The script pulls COT report data from the TradingView COT Library TradingView/LibraryCOT/3).

It retrieves long and short positions for three key groups:

Large Traders (Non-commercial positions) – Speculators such as hedge funds.

Small Traders (Non-reportable positions) – Small retail traders.

Commercial Hedgers (Commercial positions) – Institutions that hedge real-world positions.

Threshold Zones for Extreme Positioning:

Upper Zone Threshold (Default: 90%)

Signals potential overbought conditions (excessive buying).

Lower Zone Threshold (Default: 10%)

Signals potential oversold conditions (excessive selling).

The indicator plots these zones using horizontal lines.

The COT Index should be used in conjunction with technical analysis (support/resistance, trends, etc.). A high COT Index does not mean the market will reverse immediately—it’s an indication of extreme sentiment.

Note:

If the script does not recognize or can't find the ticker currently viewed in the COT report, the COT indicator will default to U.S. Dollar.

Tims Smart Money COT-IndexThe **Tims Smart Money COT Index** analyzes the positions of different groups of market participants from the COT report (Commercials, Large Specs, Small Specs). It calculates their net positions and scales them relative to extremes of the last 24 weeks. It indicates bullish and bearish zones to identify market sentiments.

- Commercials (Smart Money)**: Often act against the trend, bullish from 80+.

- Large Specs (Retail Money)**: Trend-following, bullish from 80+.

- Small Specs**: Mostly impulsive, bullish from 80+.

The indicator helps to identify turning points in the market based on the behavior of the players.

Adjusted CoT IndexAdjusted COT Index

Improves upon: "COT Index Commercials vs large and small Speculators" by SystematicFutures

How: CoT Indexes are adjusted by Open Interest to normalise data over time, and threshold background colours are in-line with Larry Williams recommendations from his book.

Note: This indicator is **only** accurate on the Daily time-frame due to the mid-week release date for CoT data.

This script calculates and plots the Adjusted Commitment of Traders (COT) Index for Commercial, Large Speculator, and Retail (Small Speculator) categories.

The CoT Index is adjusted by Open Interest to normalise data through time, following the methodology of Larry Williams, providing insights into how these groups are positioned in the market with an arguably more historically accurate context.

COT Categories

-------------------

- Commercials (Producers/Hedgers): Large entities hedging against price changes in the underlying asset.

- Large Speculators (Non-commercials): Professional traders and funds speculating on price movements.

- Retail Traders (Nonreportable/Small Speculators): Small individual traders, typically less informed.

Features

----------

- Open Interest Adjustment

- The net positions for each category are normalized by Open Interest to account

for varying contract sizes.

- Customisable Look-back Period

- You can adjust the number of weeks for the index calculation to control the

historical range used for comparison.

- Thresholds for Extremes

- Upper and lower thresholds (configurable) are provided to mark overbought and

oversold conditions.

- Defaults

- Overbought: <=20

- Oversold: >= 80

- Hide Current Week Option

- Optionally hide the current week's data until market close for more accurate comparison.

- Visual Aids

- Plot the Commercials, Large Speculators, and Retail indexes, and optionally highlight extreme positioning.

Inputs

--------

- weeks

- Number of weeks for historical range comparison.

- upperExtreme and lowerExtreme

- Thresholds to identify overbought/oversold conditions (default 80/20).

- hideCurrentWeek

- Option to hide current week's data until market close.

- markExtremes

- Highlight extremes where any index crosses the upper or lower thresholds.

- Options to display or hide indexes for Commercials, Large Speculators, and Small Speculators.

Outputs

----------

- The script plots the COT Index for each of the three categories and highlights periods of extreme positioning with customisable thresholds.

Usage

-------

- This tool is useful for traders who want to track the positioning of different market participants over time.

- By identifying the extreme positions of Commercials, Large Speculators, and Retail traders, it can give insights into market sentiment and potential reversals.

- Reversals of trend can be confirmed with RSI Divergence (daily), for example

- Continuation can be confirmed with RSI overbought/oversold conditions (daily), and/or hidden RSI Hidden Divergence, for example

Cot Histogram | MercorCot Histogram | Mercor

Overview:

The Cot Histogram | Mercor indicator provides a comprehensive visualization of the Commitment of Traders (COT) report data using bar charts. This indicator is designed to help traders analyze the positions held by commercial traders and large speculators in various markets. By representing the data as histograms, traders can easily interpret the long and short positions, as well as the net positions of these market participants.

Originality:

What sets the Cot Histogram | Mercor indicator apart is its unique approach to visualizing COT data using bar charts instead of traditional line charts. This method offers a clearer representation of the data, making it easier for traders to spot trends and changes in market sentiment. Additionally, the indicator allows for customization of colors and bar widths, providing a tailored experience for each user.

Features:

Show Shorts as Negative Numbers: This option allows users to display short positions as negative values, providing a more intuitive visualization.

Invert Colors: Users can invert the default colors for long and short positions, enabling better contrast and visual preference.

Bar Width: Adjust the width of the histogram bars to suit personal preferences and chart aesthetics.

Concepts Underlying the Calculations:

The Commitment of Traders (COT) report is a weekly publication by the Commodity Futures Trading Commission (CFTC) that provides a breakdown of the open interest positions of market participants in futures markets. This indicator focuses on two main categories of traders:

Commercial Traders: These are entities involved in the production, processing, or merchandising of a commodity. Their positions are typically hedging-oriented.

Large Speculators: These include institutional investors, hedge funds, and other entities that take positions based on market trends and expectations, often for speculative purposes.

The indicator calculates and plots the following metrics:

Commercial Long: The number of long positions held by commercial traders.

Commercial Short: The number of short positions held by commercial traders.

Commercial Net: The difference between commercial long and short positions.

Large Speculators Long: The number of long positions held by large speculators.

Large Speculators Short: The number of short positions held by large speculators.

Large Speculators Net: The difference between long and short positions of large speculators.

How to Use:

Load the Indicator: Add the Cot Histogram | Mercor indicator to your TradingView chart.

Customize Settings: Adjust the settings according to your preferences:

Enable or disable the "Show Shorts as Negative Numbers" option.

Invert the colors if needed.

Adjust the bar width for better visual representation.

Interpret the Data: Use the histograms to analyze the market positions:

Commercial Long and Short: Observe the positions held by commercial traders. Increasing long positions may indicate hedging against potential price increases, while increasing short positions may suggest hedging against potential price decreases.

Large Speculators Long and Short: Monitor the positions of large speculators to gauge market sentiment. A rise in long positions by large speculators often indicates bullish sentiment, while a rise in short positions suggests bearish sentiment.

Net Positions: The net positions provide a clearer picture of the overall stance of commercial traders and large speculators.

Example:

If you notice that commercial traders are increasing their long positions while large speculators are increasing their short positions, it may indicate a divergence in market expectations between hedgers and speculators. This could be a signal to further investigate potential market reversals or confirm existing trends.

By leveraging the Cot Histogram | Mercor indicator, traders can gain valuable insights into market dynamics, improve their trading strategies, and make more informed decisions. Whether you are a long-term investor or a short-term trader, understanding the positions of different market participants can provide a significant edge in the markets.

COT Index Commercials vs large and small SpeculatorsThe COT reports for futures-only Commitments of Traders and for Futures and Options Combined Commitments of Traders are collected on Tuesdays and published every Friday at 3:30 p.m. Eastern time. The raw data is available free of charge on the Commodity Futures Trading Commission (CFTC) website.

Use it to get a better understanding on which side the smart money (producers, commercials) are trading on.

The COT index ranges from 0 to 100%. Extreme values are areas below 25% and above 75%. When the index reaches 0% or 100%, it means that the market participant has the most extreme net short or net long position in the last 26 weeks. Readings below 25% are considered as a short sentiment and readings above 75% are considered long sentiment. However the COT index is not a timing tool. It only shows the overall market sentiment of the smart money in relation over the past 26 weeks.

You can change the period to calculate the index, as well as the style, which lines to show and if you want to highlight the extreme arias.

COT | MERCORThis Pine Script is designed for use on the TradingView platform to visualize various Commitment of Traders (COT) data for trading analysis. The COT reports provide a breakdown of each Tuesday’s open interest in the futures markets, which is valuable for understanding market sentiment. This script specifically focuses on displaying the positions of commercial and noncommercial traders (large speculators), both in long and short positions, as well as their net positions. Here’s a breakdown of the script’s components and how to use it:

Script Components

Indicator Declaration: The script begins by declaring a custom indicator using indicator() function, naming it "COT | MERCOR", and setting a short title and precision.

Library Import: It imports a library TradingView/LibraryCOT/2 as cot, which is likely a mock representation for the purpose of this description, assuming a library that provides COT data functions.

User Inputs:

shortNegative: A boolean input that allows users to choose whether short positions are displayed as negative numbers.

invertColors: A boolean input for users to decide if they want to invert the default colors of the plot lines.

lineWidth: An integer input that lets users adjust the width of the plotted lines.

COT Data Requests: The script requests COT data for both commercial and noncommercial traders' long and short positions using cot.COTTickerid() function. This includes constructing identifiers for these data points based on the user's input and predefined criteria (like "Commercial Positions" or "Noncommercial Positions", and direction "Long" or "Short").

Data Plotting: The script plots the retrieved data points on the chart, using different colors and line styles to distinguish between commercial and noncommercial positions, as well as between long, short, and net positions. It includes options to adjust the appearance based on user inputs (like inverting colors or changing line width).

Zero Line: A horizontal line (hline) is plotted at zero to provide a baseline for comparison.

How to Use

Adding the Script to Your Chart:

On TradingView, open the Pine Editor.

Paste this script into the Pine Editor.

Save and add the script to your chart.

Customizing the Display:

You can toggle whether short positions are displayed as negative numbers through the "Show Shorts as Negative Numbers?" checkbox.

Use the "Invert Colors?" checkbox to swap the colors used for plotting the positions.

Adjust the "Line Width" option to change the thickness of the plotted lines according to your preference.

Analyzing the Data:

The plotted lines represent the long, short, and net positions of commercial and noncommercial traders.

Commercial positions are typically considered the positions of entities involved in the production, processing, or merchandising of a commodity, whereas noncommercial positions represent large speculators, such as hedge funds.

The net positions (long minus short) provide insight into the overall bullish or bearish sentiment among these trader categories.

By examining these positions, traders can gain insights into potential market moves based on the behaviors of key market participants.

This script is a powerful tool for traders who want to incorporate COT report data into their market analysis on TradingView. By visualizing the trading positions of significant market players, it aids in making informed trading decisions.

COT MCIThe COT MCI script is a market indicator based on the data from the Commitment of Traders Reports.

Integration of COT Report Data:

The script sources COT data from futures contracts, including:

Treasury Bonds (ZB), Dollar Index (DX), 10-Year Treasury Notes (ZN)

Commodities like Soybeans (ZS), Soy Meal (ZM), Soy Oil (ZL), Corn (ZC), Wheat (ZW), Kansas City Wheat (KE), Pork (HE), Cattle (LE)

Precious Metals such as Gold (GC), Silver (SI), Palladium (PA), Platinum (PL)

Industrial Metals like Copper (HG), Aluminum (AUP), Steel (HRC)

Energy Products like Crude Oil (CL), Heating Oil (HO), Gasoline (RB), Natural Gas (NG), Brent Crude (BB)

Currencies such as AUD (6A), GBP (6B), CAD (6C), EUR (6E), JPY (6J), CHF (6S), NZD (6N), BRL (6L), MXN (6M), RUB (6R), ZAR (6Z)

Others: Sugar (SB), Coffee (KC), Cocoa (CC), Cotton (CT), Ethanol (EH), Rice (ZR), Oats (ZO), Whey (DC), Orange Juice (OJ), Lumber (LBS), Livestock (GF), E-mini S&P 500 (ES), E-mini Russell 2000 (RTY), E-mini Dow Jones (YM), E-mini NASDAQ-100 (NQ), VIX Futures (VX), S&P 500 (SP), DJIA (DJIA)

Cryptocurrencies such as Bitcoin (BTC) and Ethereum (ETH)

Functions and Logic of the Script:

COT Calculation: Determines the net positions for commercial actors and large speculators. Also Available are short and long positions of commercials or large speculators.

Position Change Analysis: Analyzes the percentage changes in net positions and open interest data over a period of 6 weeks (Weekly Chart).

Average Value Calculation: Determines short-term and long-term trend averages.

Trend Analysis: Buy and sell signals (represented in colors) are based on linear regressions and average calculations.

Usage and Application Examples:

Ideal for traders looking for a detailed analysis of market dynamics and position changes in the futures market. Suitable for decision-making in transaction timing and assessing market sentiment.

Usage Notes:

Users should be familiar with the interpretation of COT data and basic concepts of futures trading. Particularly suitable for medium to long-term trading strategies.

COT CFTC Title: Enhanced COT CFTC Analysis Tool

Description:

Introducing the 'Enhanced COT CFTC Analysis Tool', meticulously designed to dissect the CFTC's Commitments of Traders (COT) data. This sophisticated tool aims to equip traders and investors with profound insights into market dynamics, utilizing the positions of Large Speculators, Commercials, and Non-Reportable Positions for a comprehensive market overview.

Key Features:

Large Speculators Analysis: Visualizes the net positions of large speculators, offering insights into speculative market sentiments.

Commercials Insights: Provides a deep dive into the trading activities of commercials, known for their strategic hedging practices.

Non-Reportable Positions Tracking: Displays the activities of smaller speculators, often considered as contrarian indicators.

Additional Plots:

Options Share: Allows selection between the proportion of options in the market.

Net, Short, and Long Positions: Offers options to view net, short, and long positions.

Percentage of Net Short and Long Positions: Displays the percentage of net short and long positions, either as raw data or as an index over a specified time period.

Extreme Value Indicators: Highlights extreme values in the market data, providing critical insights into market peaks and troughs.

This tool features an intuitive display with color-coded lines and charts, simplifying the complex data analysis process. It also includes an innovative 5% detector, highlighting extreme market positions for enhanced market understanding.

Spread Analysis: This feature provides an insightful visualization of the spread between various COT data points, enabling users to gauge the market’s depth and liquidity effectively.

Usage Tips:

Utilize divergence analysis between different groups to identify potential trend reversals.

Keep a close eye on the 5% detector for early indications of market overextensions.

The 'Enhanced COT CFTC Analysis Tool' is a vital addition to your trading arsenal, designed to enrich your trading strategy with precise and actionable market insights. It’s not just an indicator; it’s a comprehensive market analysis suite.

Disclaimer: This indicator is for educational purposes only. Trading decisions should always be approached with caution and based on thorough personal analysis.

Open Interest Chart [LuxAlgo]The Open Interest Chart displays Commitments of Traders %change of futures open interest , with a unique circular plotting technique, inspired from this publication Periodic Ellipses .

🔶 USAGE

Open interest represents the total number of contracts that have been entered by market participants but have not yet been offset or delivered. This can be a direct indicator of market activity/liquidity, with higher open interest indicating a more active market.

Increasing open interest is highlighted in green on the circular plot, indicating money coming into the market, while decreasing open interests highlighted in red indicates money coming out of the market.

You can set up to 6 different Futures Open interest tickers for a quick follow up:

🔶 DETAILS

Circles are drawn, using plot() , with the functions createOuterCircle() (for the largest circle) and createInnerCircle() (for inner circles).

Following snippet will reload the chart, so the circles will remain at the right side of the chart:

if ta.change(chart.left_visible_bar_time ) or

ta.change(chart.right_visible_bar_time)

n := bar_index

Here is a snippet which will draw a 39-bars wide circle that will keep updating its position to the right.

//@version=5

indicator("")

n = bar_index

barsTillEnd = last_bar_index - n

if ta.change(chart.left_visible_bar_time ) or

ta.change(chart.right_visible_bar_time)

n := bar_index

createOuterCircle(radius) =>

var int end = na

var int start = na

var basis = 0.

barsFromNearestEdgeCircle = 0.

barsTillEndFromCircleStart = radius

startCylce = barsTillEnd % barsTillEndFromCircleStart == 0 // start circle

bars = ta.barssince(startCylce)

barsFromNearestEdgeCircle := barsTillEndFromCircleStart -1

basis := math.min(startCylce ? -1 : basis + 1 / barsFromNearestEdgeCircle * 2, 1) // 0 -> 1

shape = math.sqrt(1 - basis * basis)

rad = radius / 2

isOK = barsTillEnd <= barsTillEndFromCircleStart and barsTillEnd > 0

hi = isOK ? (rad + shape * radius) - rad : na

lo = isOK ? (rad - shape * radius) - rad : na

start := barsTillEnd == barsTillEndFromCircleStart ? n -1 : start

end := barsTillEnd == 0 ? start + radius : end

= createOuterCircle(40)

plot(h), plot(l)

🔶 LIMITATIONS

Due to the inability to draw between bars, from time to time, drawings can be slightly off.

Bar-replay can be demanding, since it has to reload on every bar progression. We don't recommend using this script on bar-replay. If you do, please choose the lowest speed and from time to time pause bar-replay for a second. You'll see the script gets reloaded.

🔶 SETTINGS

🔹 TICKERS

Toggle :

• Enabled -> uses the first column with a pre-filled list of Futures Open Interest tickers/symbols

• Disabled -> uses the empty field where you can enter your own ticker/symbol

Pre-filled list : the first column is filled with a list, so you can choose your open interest easily, otherwise you would see COT:088691_F_OI aka Gold Futures Open Interest for example.

If applicable, you will see 3 different COT data:

• COT: Legacy Commitments of Traders report data

• COT2: Disaggregated Commitments of Traders report data

• COT3: Traders in Financial Futures report data

Empty field : When needed, you can pick another ticker/symbol in the empty field at the right and disable the toggle.

Timeframe : Commitments of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) and is published weekly. Therefore data won't change every day.

Default set TF is Daily

🔹 STYLE

From middle:

• Enabled (default): Drawings start from the middle circle -> towards outer circle is + %change , towards middle of the circle is - %change

• Disabled: Drawings start from the middle POINT of the circle, towards outer circle is + OR -

-> in both options, + %change will be coloured green , - %change will be coloured red .

-> 0 %change will be coloured blue , and when no data is available, this will be coloured gray .

Size circle : options tiny, small, normal, large, huge.

Angle : Only applicable if "From middle" is disabled!

-> sets the angle of the spike:

Show Ticker : Name of ticker, as seen in table, will be added to labels.

Text - fill

• Sets colour for +/- %change

Table

• Sets 2 text colours, size and position

Circles

• Sets the colour of circles, style can be changed in the Style section.

You can make it as crazy as you want:

ICT Commitment of Traders° by toodegreesDescription:

The Commitment of Traders (COT) is a valuable raw data report released weekly by the Commodity Futures Trading Commission (CFTC). This report offers insights into the current long and short positions of three key market entities:

Commercial Traders ( usually represented in red )

Large Traders ( typically depicted in green )

Small Speculator Traders ( commonly shown in blue )

The concept of utilizing the COT data as a strategic trading tool was first introduced by Larry Williams, who emphasized the importance of monitoring Commercial Speculators – large corporate producers or consumers of commodities.

The Inner Circle Trader (ICT) prompts us to delve deeper into this data. While we can easily determine their Net Position (also referred to as the Main Program) by subtracting Commercial Short Positions from the Commercial Long Positions, this calculation doesn't reveal their ongoing Hedge Program .

Merely following the Main Program won't provide a trading edge. Aligning with the Hedge Program can be an invaluable weapon in your trading arsenal.

The Commercial Speculators' Hedge Program can be unveiled by examining the highest and lowest reading of their Net Position over a chosen time period and setting a new "zero line" between these extremes. This process generates a novel "COT Graph" providing a detailed understanding of the Commercial Speculators' current market activity.

When the Hedge Program, Seasonality, and Open Interest are cross-referenced with Institutional Orderflow, a trader can construct a very clear medium-to-long-term market narrative.

Features:

Access COT Data for the Commercial Speculators via Tradingview's reliable data source

Automate calculations and display the 3-month, 6-month, 12-month, 2-year, and 3-year Hedge Program

Define your own Custom Time Range for the Hedge Program

Display the Main Program and all Hedge Programs in an easy-to-understand table format

Additionally, by following the included instructions, you can augment your table with COT data from multiple markets. This extra information can help monitor correlated markets and develop a more robust market narrative:

EURUSD COT Trend StrategyThis is a long term/investment type of strategy designed to have a good idea about where the big trend direction is headed.

Its logic, its made entirely on the COT report, mainly from looking into the net non comercial positions aka the speculators.

For bullish trend we look that the difference between long non comercial vs short non comercial is higher than 0

For bearish trend we look that the difference between long non comercial vs short non comercial is lower than 0.

This is mainly as an educational tool, for a full strategy, I recommend implement other things into it, like technical analysis or risk management.

If you have any questions, please let me know !

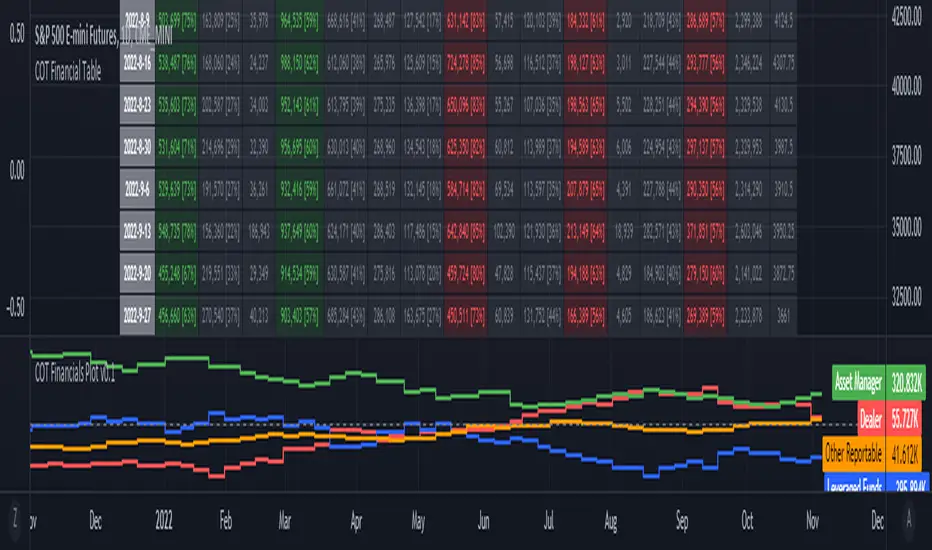

ILM COT Financials PlotUse this indicator on Daily Timeframe

Please refer to the below link for CFTC Financials

www.cftc.gov

This script is very similar to COT Financial Table indicator except that it plots the data (Longs - Shorts) instead of showing in a table.

COT Report IndicatorA COT Report Indicator that shows the Data for both currencies (base- and quotecurrency). It works in the forex market and on the Bitcoin Chart.

The table shows the Net-Contracts, Long and Short Percentage of the latest report. The line chart shows if the Commercials, Institutionals and Retail Traders are more long biased (value above 50) or more short biased (value below 50).

The COT Report is only published weekly. This should not be used as an entry indicator, but can help to find market bottoms/top and the trend of the market.

Bitfinex Shorts StratOverview

This strat applies the data from BITFINEX:USDSHORTS to the RSI indicator in order to provide SHORT/LONG entries as the number of contracts goes up and down. Although Bitfinex has lost relevance over the years its generally considered an exchange dominated by smart money rather than retail. I'd like to see if any insights can be gained by following their trading behaviour.

How to use

Select the underlying security you wish to trade and load the indicator. Select the appropriate short security by searching in the Bitfinex Short Symbol. RSI settings apply to short symbol not the actual asset. Strategy shorts the underlying asset when shorts rise and longs when they drop. The shorts symbol will follow the value of the loaded chart. Works best on 4 hour chart.

Why use shorts only rather than both long/shorts?

Bitfinex longs seem to be on a long-term uptrend accounting for 25x the number of shorts. Might be enormous confidence on part of the whales, but more likely reflects selling spot and buying perp. Given the size disparity and price action I don't think longs info is adding much.

Problems with script:

a) We don't really know the intentions of short players (e.g. speculation or hedging spot)

b) The script uses a decline in shorts as a long signal

c) RSI is a blunt tool there are probably better options for calculating high/lows in shorts

d) Shorts are accumulated both at highs and also when BTC price is already heavily trending down. This suggests some are speculative (at the highs) or protective/hedging during a decline

Takeaways:

Based on this strat Bitfinex whales are more wrong than right.

Results don't carry across well into altcoins using the accompanying short symbol. However, what is interesting is that applying the BITFINEX:BTCUSDSHORTS to altcoin charts does work pretty well.

Strat needs some refinement to control for entries under different circumstances.

Probably not a great idea to use this as a strategy in isolation, but highlights how Bitfinex whale behaviour is a good gauge to follow.

COT + ema + aux tickerPurpose: Create a script for backtesting the idea that COT can steer weekly Bias on Forex Market.

How does it works: the script use Commercials Delta Conctract, EMA of the selected ticker, EMA of 2 auxiliary tickers (e.g. correlated ticker) to generates buy and sell signals, it allows to include or not each of these.

If you use all the indicator, The buy or sell signals are generated following that rules:

(Example for buy signals on GBPCAD)

1) Commercials add net contract to GBP futures + remove net contract to CAD

2) EMA of GBPCAD is rising

3) EMA of 1st aux ticker is rising (or decline if select inv option)

4) EMA of 2nd aux ticker is rising (or decline if select inv option)

The scripts set the stop at low of the week for long orders and high of the week for shorts.

The exit strategy is to exit at first week of profit

How could you use it:

1) Choose your FX Ticker e.g. GBPCAD and set 1W TimeFrame

2) Select ticker in the strategy setting, remember to select the currency in right order, if you want to study GBP CAD 1st currency is GBP and 2nd CAD

3) Choose if you want to use EMA (and its period of calculation)

4) Choose if you want to use a aux ticker, the direction, and the relative ema period

What could be better;

1) you can just buy on begin of the week.

2) the exit strategy isn't best you can do

3) No level of delta contract is consider, its generate a buy signial also for 1 contract in the right direction

For any question, suggestion of improvemet, ideas, insult:) write to me

It all started from a script i find here on tradingview that extract COT data. Don't remember the name of that guy but Thanks a lot.

My English isn't perfect but i hope you can understand as well.

COT Report BTC Positions█ OVERVIEW

Showing the Commitments of Traders (COT) report(*) for BITCOIN Positions - CHICAGO MERCANTILE EXCHANGE (futures only) with COT charts on TradingView data.

* COT reports are released each Friday (except for U.S. holidays) by the CFTC.

* Each COT report release includes data from the previous Tuesday.

* Original data is www.cftc.gov

Data currently displayed are through April 12, 2022

█ FEATURES

You can switch the display for each of the following Positions :

Long

Short

You can switch the display for each of the following Categories :

Dealer

Asset manager

Leverage funds

Other reportable

Non reportable

█ HOW TO USE IT

This indicator allows you to see changes for each category within TradingView without having to refer directly to each report.

COT Net Positions BTC & ETH FO_ALLWeekly Commitment of Traders Report for Futures positions, as well as futures plus options positions.

This is only for Bitcoin and Ether.

OPEN INTEREST

DEALER

ASSET MANAGER

LEVERAGED FUNDS

OTHER REPORTABLE

TOTAL REPORTABLE

NON REPORTABLE

CoT data with OpenInterestDisplays COT data based on the "Disaggregated Commitments of Traders" report for Futures of the CFTC.

It does make accesible the following symbols:

ZB

ZN

ZS

ZM

ZL

ZC

ZW

KE

HE

LE

GC

SI

HG

CL

HO

RB

NG

6A

6B

6C

6E

6J

6S

SB

KC

CC

CT

ES

RTY

YM

NQ

PA

PL

AUP

HRC

EH

BB

ZR

ZO

DC

OJ

LBS

GF

SP

DJIA

6N

6L

VX

6M

6R

6Z

ZT

ZF

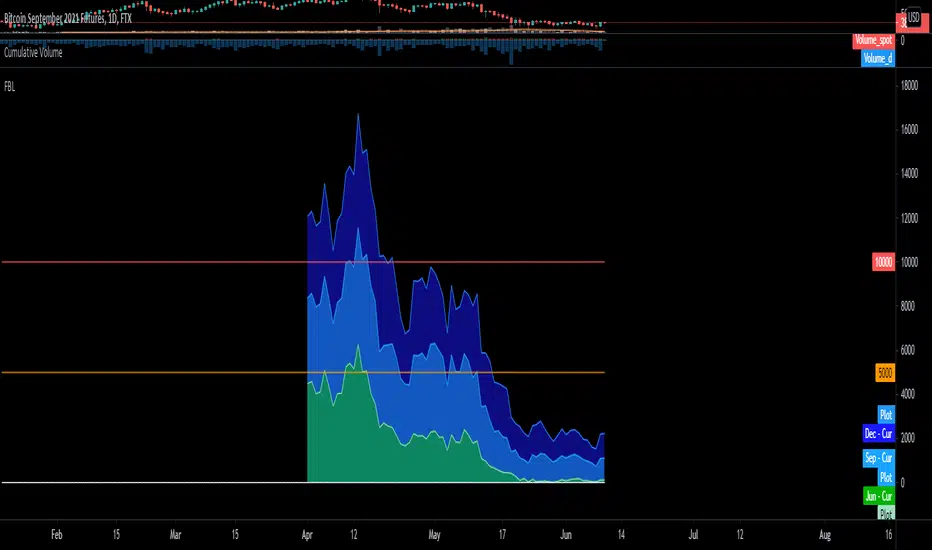

BTC FTX Futures PremiumsThis indicator shows the future BTC premiums on FTX.

The purple area is the Daily December Futures contract subtracted by the current price.

The blue area is the Daily September futures contract subtracted by the current price.

The green area is the Daily June futures contract subtracted by the current price.

You can use this to try and understand market sentiment.

If the current price dumps but the premium remains the same it likely means that sentiment is unchanged.

The opposite is true, if the price pumps and the premium is the same it means the market likely wasn't convinced by the movement.

The difference between the current price and the futures price can help determine how bullish or bearish a market or at extremes the level of euphoria.

Last Friday of MonthThis script marks the last Friday of the month in a daily chart because this is the day when BTC and ETH options expire according to Deribit.

I only found a script that highlights the 3rd Friday of the month, which is not what I wanted.

This script tries to figure out the correct number of days per month but is not aware of holidays which might displace the expiry date.