Adaptive Trend FinderAdaptive Trend Finder - The Ultimate Trend Detection Tool

Introducing Adaptive Trend Finder, the next evolution of trend analysis on TradingView. This powerful indicator is an enhanced and refined version of Adaptive Trend Finder (Log), designed to offer even greater flexibility, accuracy, and ease of use.

What’s New?

Unlike the previous version, Adaptive Trend Finder allows users to fully configure and adjust settings directly within the indicator menu, eliminating the need to modify chart settings manually. A major improvement is that users no longer need to adjust the chart's logarithmic scale manually in the chart settings; this can now be done directly within the indicator options, ensuring a smoother and more efficient experience. This makes it easier to switch between linear and logarithmic scaling without disrupting the analysis. This provides a seamless user experience where traders can instantly adapt the indicator to their needs without extra steps.

One of the most significant improvements is the complete code overhaul, which now enables simultaneous visualization of both long-term and short-term trend channels without needing to add the indicator twice. This not only improves workflow efficiency but also enhances chart readability by allowing traders to monitor multiple trend perspectives at once.

The interface has been entirely redesigned for a more intuitive user experience. Menus are now clearer, better structured, and offer more customization options, making it easier than ever to fine-tune the indicator to fit any trading strategy.

Key Features & Benefits

Automatic Trend Period Selection: The indicator dynamically identifies and applies the strongest trend period, ensuring optimal trend detection with no manual adjustments required. By analyzing historical price correlations, it selects the most statistically relevant trend duration automatically.

Dual Channel Display: Traders can view both long-term and short-term trend channels simultaneously, offering a broader perspective of market movements. This feature eliminates the need to apply the indicator twice, reducing screen clutter and improving efficiency.

Fully Adjustable Settings: Users can customize trend detection parameters directly within the indicator settings. No more switching chart settings – everything is accessible in one place.

Trend Strength & Confidence Metrics: The indicator calculates and displays a confidence score for each detected trend using Pearson correlation values. This helps traders gauge the reliability of a given trend before making decisions.

Midline & Channel Transparency Options: Users can fine-tune the visibility of trend channels, adjusting transparency levels to fit their personal charting style without overwhelming the price chart.

Annualized Return Calculation: For daily and weekly timeframes, the indicator provides an estimate of the trend’s performance over a year, helping traders evaluate potential long-term profitability.

Logarithmic Adjustment Support: Adaptive Trend Finder is compatible with both logarithmic and linear charts. Traders who analyze assets like cryptocurrencies, where log scaling is common, can enable this feature to refine trend calculations.

Intuitive & User-Friendly Interface: The updated menu structure is designed for ease of use, allowing quick and efficient modifications to settings, reducing the learning curve for new users.

Why is this the Best Trend Indicator?

Adaptive Trend Finder stands out as one of the most advanced trend analysis tools available on TradingView. Unlike conventional trend indicators, which rely on fixed parameters or lagging signals, Adaptive Trend Finder dynamically adjusts its settings based on real-time market conditions. By combining automatic trend detection, dual-channel visualization, real-time performance metrics, and an intuitive user interface, this indicator offers an unparalleled edge in trend identification and trading decision-making.

Traders no longer have to rely on guesswork or manually tweak settings to identify trends. Adaptive Trend Finder does the heavy lifting, ensuring that users are always working with the strongest and most reliable trends. The ability to simultaneously display both short-term and long-term trends allows for a more comprehensive market overview, making it ideal for scalpers, swing traders, and long-term investors alike.

With its state-of-the-art algorithms, fully customizable interface, and professional-grade accuracy, Adaptive Trend Finder is undoubtedly one of the most powerful trend indicators available.

Try it today and experience the future of trend analysis.

This indicator is a technical analysis tool designed to assist traders in identifying trends. It does not guarantee future performance or profitability. Users should conduct their own research and apply proper risk management before making trading decisions.

// Created by Julien Eche - @Julien_Eche

Band

Volatility Price FlowCapitalize on market volatility with our new volatility price flow indicator. We have designed this indicator to process historical price movements and indicate when price may have reached exhaustion in the context of current volatility.

This is achieved by taking the price deviation from a user defined moving average, and applying a weighting to the deviations from the candle body and candle wick on both buy side and sell side, over a user defined period. The period of the base moving average, type of moving average and the period of the historical price deviations can all be modified. This creates a typical 'band' style indicator, though with a unique characteristic that the buy and sell side vary independently as well as the band expansion being based on weighted variables tied to the actual price changes, rather than just a standard deviation the moves uniformly.

Additionally, these bands can be merged with an anchored vwap - we do this so that the deviations of price from the moving average can include a more volume based approach to identifying potential pivots.

The end result is an indicator that reflects the current market price movements, identifies and capitalizes on impulsive or beginning moves to indicate potential tops / bottoms / reversals.

The signals are simple - anytime price closes within a band, having been outside the band, a signal is displayed. As a basic guide to setting the indicator up for the first time, we suggest reducing all of the multipliers to a value less than 1. Then gradually increase each one, until the signals reduce in quantity and improve in quality, starting with the price deviation multiplier, then the volatility multiplier and finally the expansion multiplier.

Last of all, alerts can be created based on the current chart timeframe and indicator settings, simply by adding an alert that uses the built in buy or sell signal.

Note: We cannot guarantee the accuracy of the signals provided, since the user creates the signals by modifying the settings, and as such we can take no responsibility for any trading losses incurred using the indicator and highly encourage all users to manage their risk and only risk what you can afford to lose.

Standard Deviation-Based Fibonacci Band by zdmre This indicator is designed to better understand market dynamics by focusing on standard deviation and the Fibonacci sequence. This indicator includes the following components to assist investors in analyzing price movements:

Weighted Moving Average (WMA) : The indicator creates a central band by utilizing the weighted moving average of standard deviation. WMA provides a more current and accurate representation by giving greater weight to recent prices. This central band offers insights into the general trend of the market, helping to identify potential buying and selling opportunities.

Fibonacci Bands : The Fibonacci bands located above and below the central band illustrate potential support and resistance levels for prices. These bands enable investors to pinpoint areas where the price may exhibit indecisiveness. When prices move within these bands, it may be challenging for investors to discern the market's preferred direction.

Indecisiveness Representation : When prices fluctuate between the Fibonacci bands, they may reflect a state of indecisiveness. This condition is critical for identifying potential reversal points and trend changes. Investors can evaluate these periods of indecisiveness to develop suitable buying and selling strategies.

This indicator is designed to assist investors in better analyzing market trends and supporting their decision-making processes. The integration of standard deviation and the Fibonacci sequence offers a new perspective on understanding market movements.

#DYOR

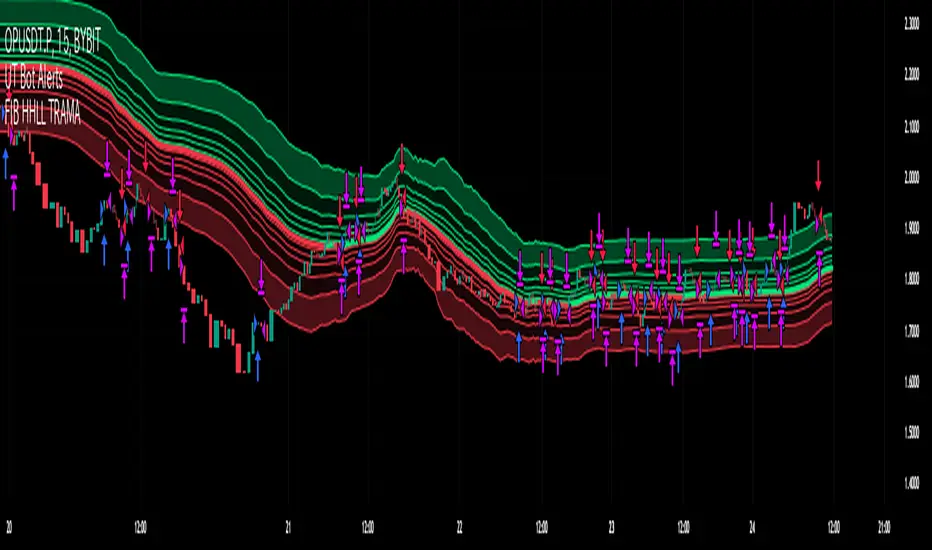

Fibonacci HH LL TRAMA BandLuxAlgo's Trend Moving Adaptive Moving Average was used as a reference to create bands by reading the highest and lowest prices of past bars based on Fibonacci numbers and then multiplying them by the Fibonacci ratio.

LuxAlgo/ LuxAlgo/

In particular, the so-called TRAMA is characterized by its adaptation to the average of the highest and lowest prices over a specific period of time and is used to identify support/resistance.

In order to apply this feature to the maximum extent possible, I used the high or low prices as the source of input, rather than the closing price.

For example,

src = high

not original like

src = close

In addition, I created 6 levels by multiplying the Fibonacci ratio

//Midline

mah = ama1

mal = ama2

m = (mah + mal)/2

//Half Mean Range

dist = (mah - mal)/2

//Levels

h6 = m + dist * 11.089

h5 = m + dist * 6.857

h4 = m + dist * 4.235

h3 = m + dist * 2.618

h2 = m + dist * 1.618

h1 = m + dist * 0.618

l1 = m - dist * 0.618

l2 = m - dist * 1.618

l3 = m - dist * 2.618

l4 = m - dist * 4.235

l5 = m - dist * 6.857

l6 = m - dist * 11.089

If you want to use it for scalping, such as 15 minutes, you can include Fibonacci numbers such as 21,34,55 for a quick reaction type to detect the trend. Also, by including Fibonacci numbers such as 89,144,233, you can see where you stand in the larger trend. Some examples are included below.

For Investors

BTCUSDT 1day Chart Fibonacci number "55"

For Daytraders

BTCUSDT 4hour Chart Fibonacci number "34"

For Scalpers

BTCUSDT 15min Chart Fibonacci number "55"

BTCUSDT 15min Chart Fibonacci number "89"

BTCUSDT 15min Chart Fibonacci number "233"

Fibonacci numbers are 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, etc.,

Fibonacci ratios are 0.618, 1.618, 2.618, 4.236, 6.854, 11.089, etc.,

Bollinger Bands Heatmap (BBH)The Bollinger Bands Heatmap (BBH) Indicator provides a unique visualization of Bollinger Bands by displaying the full distribution of prices as a heatmap overlaying your price chart. Unlike traditional Bollinger Bands, which plot the mean and standard deviation as lines, BBH illustrates the entire statistical distribution of prices based on a normal distribution model.

This heatmap indicator offers traders a visually appealing way to understand the probabilities associated with different price levels. The lower the weight of a certain level, the more transparent it appears on the heatmap, making it easier to identify key areas of interest at a glance.

Key Features

Dynamic Heatmap: Changes in real-time as new price data comes in.

Fully Customizable: Adjust the scale, offset, alpha, and other parameters to suit your trading style.

Visually Engaging: Uses gradients of colors to distinguish between high and low probabilities.

Settings

Scale

Tooltip: Scale the size of the heatmap.

Purpose: The 'Scale' setting allows you to adjust the dimensions of each heatmap box. A higher value will result in larger boxes and a more generalized view, while a lower value will make the boxes smaller, offering a more detailed look at price distributions.

Values: You can set this from a minimum of 0.125, stepping up by increments of 0.125.

Scale ATR Length

Tooltip: The ATR used to scale the heatmap boxes.

Purpose: This setting is designed to adapt the heatmap to the instrument's volatility. It determines the length of the Average True Range (ATR) used to size the heatmap boxes.

Values: Minimum allowable value is 5. You can increase this to capture more bars in the ATR calculation for greater smoothing.

Offset

Tooltip: Offset mean by ATR.

Purpose: The 'Offset' setting allows you to shift the mean value by a specified ATR. This could be useful for strategies that aim to capitalize on extreme price movements.

Values: The value can be any floating-point number. Positive values shift the mean upward, while negative values shift it downward.

Multiplier

Tooltip: Bollinger Bands Multiplier.

Purpose: The 'Multiplier' setting determines how wide the Bollinger Bands are around the mean. A higher value will result in a wider heatmap, capturing more extreme price movements. A lower value will tighten the heatmap around the mean price.

Values: The minimum is 0, and you can increase this in steps of 0.2.

Length

Tooltip: Length of Simple Moving Average (SMA).

Purpose: This setting specifies the period for the Simple Moving Average that serves as the basis for the Bollinger Bands. A higher value will produce a smoother average, while a lower value will make it more responsive to price changes.

Values: Can be set to any integer value.

Heat Map Alpha

Tooltip: Opacity level of the heatmap.

Purpose: This controls the transparency of the heatmap. A lower value will make the heatmap more transparent, allowing you to see the price action more clearly. A higher value will make the heatmap more opaque, emphasizing the bands.

Values: Ranges from 0 (completely transparent) to 100 (completely opaque).

Color Settings

High Color & Low Color: These settings allow you to customize the gradient colors of the heatmap.

Purpose: Use contrasting colors for better visibility or colors that you prefer. The 'High Color' is used for areas with high density (high probability), while the 'Low Color' is for low-density areas (low probability).

Usage Scenarios for Settings

For Volatile Markets: Increase 'Scale ATR Length' for better smoothing and set a higher 'Multiplier' to capture wider price movements.

For Trend Following: You might want to set a larger 'Length' for the SMA and adjust 'Scale' and 'Offset' to focus on more probable price zones.

These are just recommendations; feel free to experiment with these settings to suit your specific trading requirements.

How To Interpret

The heatmap gives a visual representation of the range within which prices are likely to move. Areas with high density (brighter color) indicate a higher probability of the price being in that range, whereas areas with low density (more transparent) indicate a lower probability.

Bright Areas: Considered high-probability zones where the price is more likely to be.

Transparent Areas: Considered low-probability zones where the price is less likely to be.

Tips For Use

Trend Confirmation: Use the heatmap along with other trend indicators to confirm the strength and direction of a trend.

Volatility: Use the density and spread of the heatmap as an indication of market volatility.

Entry and Exit: High-density areas could be potential support and resistance levels, aiding in entry and exit decisions.

Caution

The Bollinger Bands Heatmap assumes a normal distribution of prices. While this is a standard assumption in statistics, it is crucial to understand that real-world price movements may not always adhere to a normal distribution.

Conclusion

The Bollinger Bands Heatmap Indicator offers traders a fresh perspective on Bollinger Bands by transforming them into a visual, real-time heatmap. With its customizable settings and visually engaging display, BBH can be a useful tool for traders looking to understand price probabilities in a dynamic way.

Feel free to explore its features and adjust the settings to suit your trading strategy. Happy trading!

[DIP] Inverse BB/Bollinger highlight for barsThis indicator allows you to highlight the area outside of the Bollinger Bands in order to draw more attention to it. This is especially useful for those who only trade when we are outside of the bands.

Keep in mind this indicator only works on bars, not on candles.

Ultimate Trend ChannelThe "Ultimate Trend Channel" indicator is a comprehensive trend analysis tool that calculates and displays a series of upper and lower bands based on user-defined input lengths. It uses linear regression and standard deviation to determine these bands for each of the 21 different group lengths. The indicator then computes the averages of these upper and lower bands, as well as the average of all the bands combined.

The visualization on the chart includes the plotting of the average upper and lower bands, with the space between these bands shaded for easy visualization of the overall trend. Additionally, the average of all the bands, referred to as the "Ultimate Trend Line," is also plotted on the chart.

This indicator provides a robust way of assessing market trends and volatility over varying periods, which can be extremely useful for both short-term and long-term trading strategies.

(Very promising) [Abdullah Ahmed] Momentum indicator V.1Description: MOM-LRC is a powerful technical analysis indicator designed to provide traders with signals based on the momentum of an asset's price and its deviation from its mean value. The indicator calculates the exponential RSI and uses a custom function to determine the percentage change from the mean. The upper and lower bands of the momentum channel are then calculated using linear regression of the rate of change from the mean. The channel multiplier can be adjusted to increase or decrease the sensitivity of the indicator.

How to use :

1 - Using MOM-LRC , look for buy signals when the price of the asset is below the lower border of the channel and retracing up. The opposite is true in the case of sell signals.

2 - It is also used in the case of negative and positive divergences, just as you use RSI

The indicator can be used on any time frame and any asset, making it a versatile tool for traders of all levels.

features:

Calculates exponential RSI and percentage change from the mean

Uses linear regression to calculate upper and lower bands of momentum channel

Adjustable channel multiplier for increased sensitivity

Suitable for any time frame and any asset

Happy trading!

Faytterro Bandswhat is Faytterro Bands?

it is a channel indicator like "Bollinger Bands".

what it does?

creates a channel using standard deviations and means. thus giving users an idea about the expensive and cheap zones. It uses a special weighted moving average different from standard bollinger bands, it also averages not only price but also deviations.

how it does it?

it uses this formulas:

how to use it?

its usage is the same as "bollinger band".

length represents the number of candles to be taken into account, source represents the source of those candles and stdev represents the coefficient of the standard deviation.

you can use it with other indicators:

Chebyshevs BandsThis script calculates upper and lower bands using Chebyshev's inequality formula.

The main pros.: the band doesn't depend on particular distribution. It fits to any type of random variables. Also it allows to calculate bands for instruments with extremely high volatility.

Cons.: formula provides a rough estimation in some special cases like lognormal distribution.

Band of Filtered RS by Mustafa ÖZVERBand of Filtered RS by Mustafa ÖZVER

This code shows a range (max-min values) price may get if we get strong movements. These values is based on RSI (Relative Strange Index). And also these are calculated using RSI, if we get trades to make rsi is equal to 25 (or rsi down limit) or 75 (rsi up limit) or any value you set, how much will price value get? This code calculate these and shows these to you on graph.

This price are between these band limits because we expect cross reaction to hard movements on price.

For scalping, we can use these values as

long signal when price under down limit,

short signal when price over up limit,

But only these values can not guarantee good results for trading. BE CAREFUL

Z Score BandThis is a band based on Z Score. What is Z Score? In layman's terms it's a method of finding outliers within a sequence of numbers. It's highly effective to quantify pump and dumps in the crypto market.

The middle line is a simple Exponential Moving Average, you can configure this with whatever period you prefer. It comes default with a period of 247 to which I find suitable for my style of trading. The upper and lower bound are determined by the standard deviation you choose in the settings, it comes with a default of 1.69 although I've heard people saying 2.5 is a better number to really pinpoint outliers.

Trading with this indicator is like trading with any band based indicator. The main difference is that this indicator's sole purpose when I wrote it is to help me find shorting positions in the futures market. On the contrary though, longs are also achievable although I rarely long the futures market.

If prices hit the upper bound and get rejected, it's probably because the move was an outlier, it doesn't happen often and when it does usually it reveals crypto's nature of buying spot and hedging short in the futures market. When prices stay above the upper bound, switch to a higher timeframe until we can see that it's still have some ways upwards.

What's true about using this as a shorting tool is also true with longs. However, it might not be as effective, I'd like to be proven wrong.

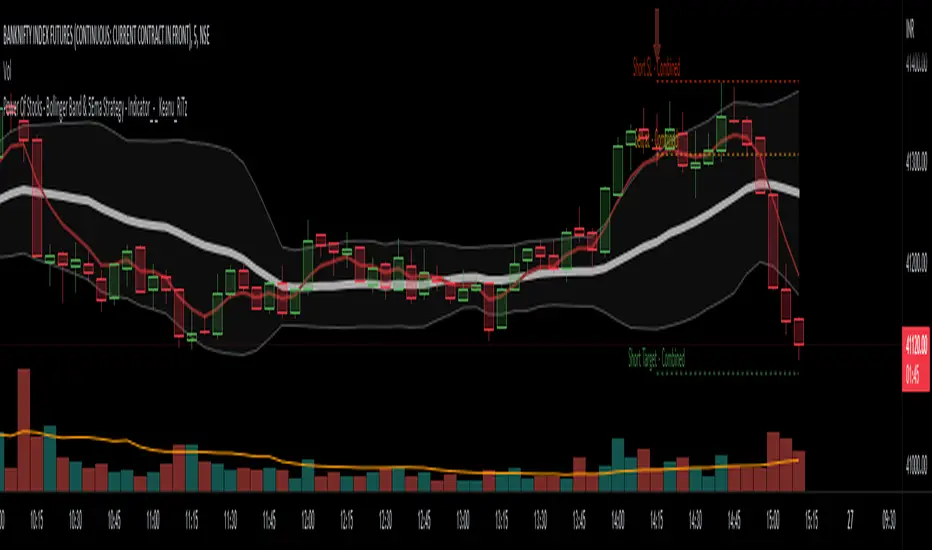

Power Of Stocks - Bollinger Band & 5Ema Indicator - Keanu_RiTz

Power of Stocks - Bollinger band & 5ema Strategy

In this script you get to take Buy/Sell trades using the 3 options mentioned below.(Alerts with price levels for buy/sell at , SL & Target are included in this one)

1. Combined Strategy :- uses confirmation from both strategies to trade.

2. Bollinger band Strategy :- use the Bollinger band Strategy to trade.

3. 5ema Strategy :- use the 5ema Strategy to trade.

1. Combined Strategy :-

for Selling :- we will go short/sell only when conditions of both strategies are satisfied.

i.e. when a candle is completely above the upper Bollinger band & completely above the 5ema then it will be our Alert Candle.

We Short/Sell only when the low of the Alert candle is broken or when the candle closes below the close of the Alert Candle.

SL will be above high of the Alert Candle. Target will be minimum 1:3 or as per your emotions.

for Buying:- we will go Long/Buy only when conditions of both strategies are satisfied.

i.e. when a candle is completely below the lower Bollinger band & completely below the 5ema then it will be our Alert Candle.

We go Long/Buy only when the high of the Alert candle is broken or when the candle closes above the close of the Alert Candle.

SL will be below low of the Alert Candle. Target will be minimum 1:3 or as per your emotions.

2. Power of Stocks - Bollinger Band Strategy :-

Bollinger band with standard deviation = 1.5

when a candle is completely above the upper Bollinger band, that candle will be called a signal/alert candle.

Initiate a Sell trade when that alert candles low is broken. SL will be above high of that alert candle.

Risk to reward ratio will be 1:4 i.e. target will be 4 times the SL.

when a candle is completely below the lower Bollinger band, that candle will be called a signal/alert candle.

Initiate a Buy trade when that alert candles high is broken. SL will be below low of that alert candle.

Risk to reward ratio will be 1:4 i.e. target will be 4 times the SL.

other rules for Options buying:- minimum 15min timeframe

The day you initiate the position , you should be in profit above 10%-15% then only you should carry forward that position overnight, otherwise squareoff your trade on that day only.

Buy ATM or slightly OTM, SL max 100 points , target 1:4

for Long-term/Investing :- Minimum Weekly

If candle is outside the lower band then initiate a Buy trade when that candles High is broken. Sl will be below Low of that candle.

for Long-term Target will be according to your emotions.

3. Power of Stocks - 5ema Strategy (target minimum 1:3)

Timeframe -

5 min for Selling (Sell Futures/index/stocks or buy Put)

15 min for Buying (Buy Futures/index/stocks or sell Put)

for selling stocks :-

you should enter trade within 10am , don't look for entries after that time. take only 2 entries a day.

for selling Index(Banknifty) :-

you can take trade at anytime of the day whenever conditions get satisfied. you can take multiple entries in banknifty as it is very volatile.

for options choose atm strikes: selling trade

sl for premium between 200-300 :- 20-30 points SL

sl for premium between 400-500 :- 40-50 points SL

sl for premium between 500-600 :- 50-60 points SL

Subhashish Pani's (power of stocks) 5 EMA Strategy:-

It plots 5 EMA and Buy/Sell signals with Target & Stoploss levels.

What is Subhashish Pani's (power of stocks) 5 EMA Strategy :-

His strategy is very simple to understand. for intraday use 5 minutes timeframe for selling. You can sell futures, sell call or buy Puts in selling strategy.

What this strategy tries to do is , it tries to catch the tops, so when you sell at top & it turns out to be a reversal point then you can get good profit.

this will hit stop losses often, but stop losses are small and minimum target should be 1:3. but if you stay with the trend you can get big profits.

According to Subhashish Pani this strategy has 60% success rate.

Strategy for Selling (Short future/Call/stock or buy Put)

When ever a Candle closes completely above 5 ema (no part of candle should be touching the 5ema), then that candle should be considered as Alert Candle.

If the next candle is also completely above 5 ema and it has not broken the low of previous alert candle, Then the previous Alert Candle should be ignored and the new candle should be considered as new Alert Candle.

so if this goes on then continue shifting the Alert Candle, but whenever the next candle breaks the low of the Alert Candle we should take the Short trade (Short future/Call/stock or buy Put).

Stoploss will be above high of the Alert Candle and minimum target will be 1:3.

Strategy for Buying (Buy future/Call/stock or sell Put)

When ever a Candle closes completely below 5 ema (no part of candle should be touching the 5ema), then that candle should be considered as Alert Candle.

If the next candle is also completely below 5 ema and it has not broken the high of previous alert candle, Then the previous Alert Candle should be ignored and the new candle should be considered as new Alert Candle.

so if this goes on then continue shifting the Alert Candle, but whenever the next candle breaks the high of the Alert Candle we should take the Long trade (Buy future/Call/stock or sell Put).

Stoploss will be below low of the Alert Candle and minimum target will be 1:3.

Buy/Sell with extra conditions :

it just adds 1 more condition to buying/selling

1. checks if closing of current candle is lower than alert candles closing for Selling & checks if closing of current candle is higher than alert candles closing for Buyling.

This can sometimes save you from false moves but by using this, you can also miss out on big moves as you'll enter trade after candle closing instead of entering at break of high/low.

Note :- According to Subhashish Pani Timeframe for intraday buying should be 15 minutes Timeframe.

If you haven't understood the strategy by reading above description, then search for "Subhashish Pani's (power of stocks) 5 EMA Strategy" on YouTube to get a deeper understanding.

Note:- This is not only for Intraday trading , you can use this strategy for Positional/Swing trading as well. If you use this on Monthly Timeframe then it can be very good for Long Term Investing as well.

Rules will be same for all types of trades & Timeframes.

Bollinger BandsThis strategy is inspired from Power of Stock aka Subhasish Panni.

Target is minimum 1:3 when you get this setup right.

Buy when:

1) Low is greater than upper band of BB and next candle breaks high of that candle, SL is Low of previous candle which is has low above upper band.

2) High is lower than lower band of BB and next candle breaks high of that candle, SL is low of previous candle which has high lower than lower band.

Sell when:

1) Low is greater than upper band of BB and next candle breaks low of that candle, SL is high of previous candle which is has low above upper band.

2) High is lower than lower band of BB and next candle breaks high of that candle, SL is high of previous candle which has high lower than lower band.

Disclaimer: this setup will cause many small stoploss hit, you have to accept that loss but you will be profitable because of R:R.

PBSimple moving average based percentage band. Think it as a reaction zone. Not useful when market is trending.

Pivot-Based Channels & Bands [Misu]█ This Indicator is based on Pivot detection to show bands and channels.

The pivot price is similar to a resistance or support level. If the pivot level is breached, the price should continue in that direction. Or the price could reverse at or near this level.

█ Usages:

Use channels as a support & resistance zone.

Use bands as a support & resistance zone. It is also very powerfull to use it as a breakout.

Use mid bands & mid channels as a trend direction or trade filter as a more usual moving average.

█ Parameters:

Show Pivot Bands: show bands.

Show Pivot Mid Band: show mid bands.

Show Pivot Channels: show channels.

Show Pivot Mid Channel: show mid channels.

Deviation: deviation used to calculate pivot points.

Depth: depth used to calculate pivot points.

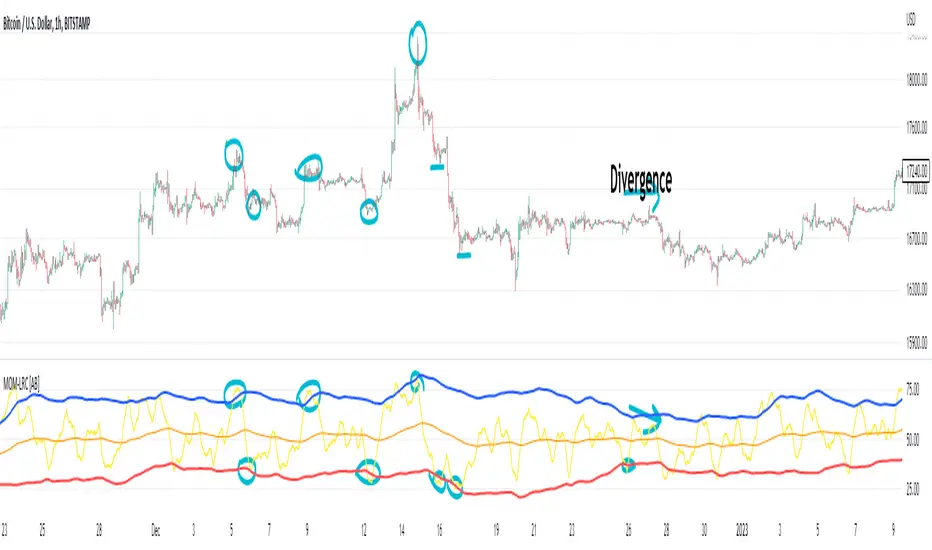

RAS.V2 Strength Index OscillatorHeavily modified version of my previous "Relative Aggregate Strength Oscillator" -Added high/low lines, alma curves,, lrc bands, changed candle calculations + other small things. Replaces the standard RSI indicator with something a bit more insightful.

Credits to @wolneyyy - 'Mean Deviation Detector - Throw Out All Other Indicators ' And @algomojo - 'Responsive Coppock Curve'

And the default Relative Strength Index

The candles are the average of the MFI ,CCI ,MOM and RSI candles, they seemed similar enough in style to me so I created candles out of each and the took the sum of all the candle's OHLC values and divided by 4 to get an average, same as v1 but with some tweaks. Previous Peaks and Potholes visible with the blue horizontal lines which adjust when a new boundary is established. Toggle alma waves or smalrc curves or both to your liking. This indicator is great for calling out peaks and troughs in realtime, although is best when combined with other trusted indicators to get a consensus.

Cryptogrithm's Secret Momentum and Volatility IndicatorThis indicator is hard-coded for Bitcoin, but you may try it on other asset classes/coins. I have not updated this indicator in over 3 years, but it seems to still work very well for Bitcoin.

This indicator is NOT for beginners and is directed towards intermediate/advanced traders with a sensibility to agree/disagree with what this indicator is signalling (common sense).

This indicator was developed back in 2018 and I has not been maintained since, which is the reason why I am releasing it. (It still works great though! At the time of this writing of May 2022).

How to use:

Terms:

PA (Price Action): Literally the candlestick formations on your chart (and the trend formation). If you don't know how to read and understand price action, I will make a fast-track video/guide on this later (but in the meanwhile, you need to begin by learning Order-Flow Analysis, please google it first before asking).

CG Level (Cryptogrithm Level/Yellow Line): PA level above = bullish, PA level below = bearish

CG Bands (Cryptogrithm Bands): This is similar to how bollingers work, you can use this the same was as bollinger bands. The only difference is that the CG bands are more strict with the upper and lower levels as it uses different calculations to hug the price tighter allowing it to be more reactive to drastic price changes (earlier signals for oversold/overbought).

CG Upper Band (Red Upper Line): Above this upper bound line means overbought.

CG Middle Band (Light Blue Line): If PA trades above this line, the current PA trend is bullish continuing in the uptrend. If PA trades below this line, the current PA trend is bearish continuing in the downtrend. This band should only be used for short-term trends.

CG Lower Band (Green Lower Line): Below this lower bound line means oversold.

What the CG Level (yellow line) tells you:

PA is trading above CG Level = Bullish

PA is trading below CG Level = Bearish

Distance between CG Level and price = Momentum

What this means is that the further away the price is from the CG Level, the greater the momentum of the current PA trend. An increasing gap between the CG Level and PA indicates the price's strength (momentum) towards the current upward/downward trend. Basically when the PA and CG Level diverge, it means that the momentum is increasing in the current trend and when they converge, the current trend is losing momentum and the direction of the PA trend may flip towards the other direction (momentum flip).

PA+CG Level Momentum:

To use the CG Level as a momentum indicator, you need to pay attention to how the price and the CG level are moving away/closer from each other:

PA + CG Level Diverges = Momentum Increasing

PA + CG Level Converges = Momentum Decreasing

Examples (kind of common sense, but just for clarity):

Case 1: Bullish Divergence (Bullish): The PA is ABOVE and trending AWAY above from the CG Level = very bullish, this means that momentum is increasing towards the upside and larger moves will come (increasing gap between the price and CG Level)

Case 2: Bearish Convergence (Bearish): - The PA is ABOVE the CG Level and trending TOWARDS the CG Level = bearish, there is a possibility that the upward trend is ending. Look to start closing off long positions until case 1 (divergence) occurs again.

Case 3: Neutral - The PA is trading on the CG Level (no clear divergence or convergence between the PA and CG Level) = Indicates a back and forth (tug of war) between bears and bulls. Beware of choppy price patterns as the trend is undecisive until either supply/liquidity is dried out and a winner between bull/bear is chosen. This is a no trade zone, but do as you wish.

Case 4: Bearish Divergence (Bearish): The PA is BELOW and trending AWAY BELOW from the CG Level = very bearish, this means that momentum is increasing towards the downside and larger downward moves will come (increasing gap between the price and CG Level).

Case 5: Bullish Convergence (Bullish): - The PA is BELOW the CG Level and trending TOWARDS the CG Level = bullish, there is a possibility that the downward trend is ending and a trend flip is occuring. Look to start closing off short positions until case 4 (divergence) occurs again.

CG Bands + CG Level: You can use the CG bands instead of the PA candles to get a cleaner interpretation of reading the momentum. I won't go into detail as this is pretty self-explanatory. It is the same explanation as PA+CG Level Momentum, but you are replacing the PA candles with the CG Bands for interpretation. So instead of the PA converging/diverging from the CG Level, the Upper and Lower Bound levels are converging/diverging from the CG level instead.

Convergence: CG Level (yellow line) trades inside the CG bands

Divergence: CG Level (yellow line) trades outside the CG bands

Bullish/Bearish depends on whether the CG Band is trading below or above the CG level. If CG Band is above the CG Level, this is bullish. If CG Band is below the CG level, this is bearish.

Crosses (PA or CG Band crosses with CG level): This typically indicates volatility is incoming.

There are MANY MANY MANY other ways to use this indicator that is not explained here and even other undiscovered methods. Use some common sense as to how this indicator works (it is a momentum indicator and volatility predictor). You can get pretty creative and apply your own methods / knowledge to it and look for patterns that occur. Feel free to comment and share what you came up with!

Smarter MACD BandThe Smarter MACD displayed as a band instead of an oscillator. A classic MACD with average peak and dip lines. The lighter green and red horizontal lines are the average peak and dip of the entire span, respectively. The second, bolder of the two lines are the averages of the peaks and dips above and below the overall peak and dip averages. The filled in color is to help visualize these averages and possible trade setups.

SuperJump Turn Back Bollinger BandThis is a simple indicator using bolinger band return.

After the candle's bolinger band broke out,

Turn back inside BB is the entry point.

Usually there are more than two triangles, so you can wait after ordering a better price.

As you already know about it, it is very dangerous for the bolinger band to enter in the reverse direction when a strong trend is created.

That's why I made the Red Line. It is calculated by ATR and will suggest you an appropriate StopLoss value.

BB Order BlocksUsing the Bollinger Band to mark areas of Support and Resistance

The scrip finds the highest and lowest levels of the bands to mark up futures areas of interest.

If the High/Lows are being broken on the Bollinger band, or if the look back range has expired without finding new levels, the script will stop plotting them until new levels are found

I have found many combinations which work well

Changing the band length to to levels 20,50,100 or 200 seem to give interesting results

Aswell as this changing the standard deviation to 3 instead of 2 marks up key levels.

The look back range seems to show better levels on 50,100 and 200

Let me know any changes or updates you think you could make an impact , this was just a quick basic script I wanted to share.

Bar By Bar ATR [upslidedown]After seeing strategy after strategy refer to calculating ATR values using a "calculator" (how barbaric!), I thought I'd take a stab at one possible solution to the "problem" as an overlay indicator on the main chart that replaces traditional standard ATR bands. This indicator presents ATR within a channel with a slick trick: invisible hover-able tooltips for you to know the ATR value for your strategy from bar to bar. Just zoom in and hover over the high ATR range and you'll see take profit and stop loss values for whatever strategy you might be running. I defaulted the indicator to a 1:1.5 ATR standard setup because that is good for many strategies but this is as configurable as you'd like to make it. One notable improvement for this indicator over standard ATR bands is that many existing ATR bands only use integers and this one uses a float value, so you can endlessly customize based on whatever strategy you might be running.

Note: Because labels are limited by default, the best way to historically see ATR values is to use TV's replay feature. I did this on purpose to limit resource usage. One could certainly print more labels but I felt it unnecessary to go beyond the default number of labels.

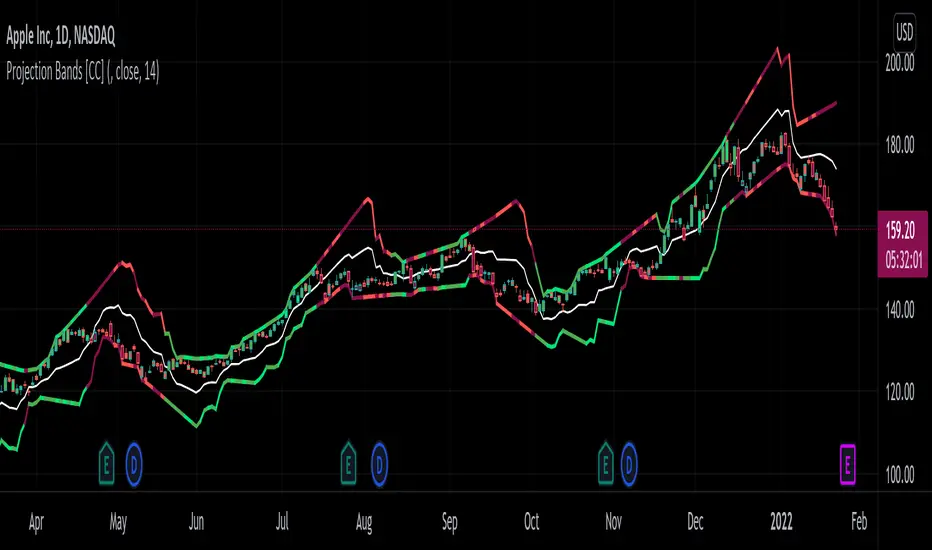

Projection Bands [CC]The Projection Bands were created by Mel Widner (Stocks and Commodities Jul 1995) and this indicator and the other two that rely on this one (I will publish them later) are very underappreciated in my humble opinion. The biggest strength of this indicator is the fact that it is a leading indicator for dramatic price movements. As you can see in my example chart it consistently gives great exit points before a downturn. I have included strong buy and sell signals in addition to normal ones so strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators or scripts you would like to see me publish!