Keltner Channel Backtest The Keltner Channel, a classic indicator

of technical analysis developed by Chester Keltner in 1960.

The indicator is a bit like Bollinger Bands and Envelopes.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Backtest

Moving Average Convergence/Divergence MaCD BackestingMade this to backtest simple macd trading strategy, had to set it to open long and short positions because i'm not sure how you get it to calculate otherwise.

Cyatophilum Trend Indicator [BACKTEST][STRATEGY]HOW IT WORKS

Based on my Cyatophilum Trend Indicator, this Strategy performs simple Buy and Sell orders when an alert from the Indicator triggers. The goal is to find the best Time Frame and Trend Parameter in order to make the most profit. The indicator turns the candles green for a Long trade/Buy and red for a Short trade/Sell.

ABOUT THE STRATEGY

The Net Profit (Gross profit - Gross loss) is calculated with a commission of 0.05% on each order.

Each trade is made with 1 BTC : The backtest buys 1 BTC and sells 1 BTC.

It clearly outperforms the Buy & Hold line, meaning it is more profitable to use this strategy than to just hold Bitcoin.

If you decided to Short or Long, profits can be higher, but trade at your own risk.

To use this strategy on a BTC market (for trading altcoins), change the default Order Size from 1 Contract to 100% of Equity.

MY PERSONNAL ADVICE

This is a Trend Indicator, meaning the least profitable trades are made during flat markets. Keep an eye on News and Volume to indentify a possible breakout and avoid trades during those flat periods. Do not trade during a Triangle since the commissions will rekt you.

Get This Indicator Today!

Purchase at blockchainfiesta.com

NOTE

If you purchase the Indicator you will get both the Alert Setup and the Backtest Strategy.

Find, discuss and request more backtesting on my discord!

discord.gg

Volatility Backtest The Volatility function measures the market volatility by plotting a

smoothed average of the True Range. It returns an average of the TrueRange

over a specific number of bars, giving higher weight to the TrueRange of

the most recent bar.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

08-18 EMA Watson [BACKTEST][STRATEGY] BTC/USDTHello, it has been a while since I published something, I have been working on webdev in the last months but Here I Am again with a brand new strategy, I called it EMA Watson lol (no I'm not a fan)!

Recently Bitcoin has been outperforming almost all altcoins so I made a script for trading Bitcoin against USDT. This script should be used on a pair that is in an uptrend, just like BTC/USDT today. The script is coded in such a way that it won't make any trade if the trend goes bearish.

This is a simple buy and sell strategy, that can be used for manual trading or for a trading bot. The strategy is based upon the Exponential Moving Average trading rules, and I added my personnal touch of course.

I give access for free, just leave a comment.

More info about the script, such as inputs description, how to configure the script, strategy explanation, alert configuration can be found here : blockchainfiesta.com

The Alert Setup (indicator) script should be uploaded soon on my profile.

--------------------------------------------------------------------------------------------------------------

Commission Work: TradingView development, Reverse Engineering, Pine Script. contact@blockchainfiesta.com. You can also send me a message in TradingView or Discord

If you have too much crypto and want to help me out:

BTC address: 19sVQvCDmVfEACq7BiMnWSMqFPZ8qfSQ2K

ETH address: 0xc8a5d3a63a05db0c2363ea1c08b37a01cce9ebfb

Smart Money Index (SMI) Backtest Attention:

If you would to use this indicator on the ES, you should have intraday data 60min in your account.

Smart money index (SMI) or smart money flow index is a technical analysis indicator demonstrating investors sentiment.

The index was invented and popularized by money manager Don Hays. The indicator is based on intra-day price patterns.

The main idea is that the majority of traders (emotional, news-driven) overreact at the beginning of the trading day

because of the overnight news and economic data. There is also a lot of buying on market orders and short covering at the opening.

Smart, experienced investors start trading closer to the end of the day having the opportunity to evaluate market performance.

Therefore, the basic strategy is to bet against the morning price trend and bet with the evening price trend. The SMI may be calculated

for many markets and market indices (S&P 500, DJIA, etc.)

The SMI sends no clear signal whether the market is bullish or bearish. There are also no fixed absolute or relative readings signaling

about the trend. Traders need to look at the SMI dynamics relative to that of the market. If, for example, SMI rises sharply when the

market falls, this fact would mean that smart money is buying, and the market is to revert to an uptrend soon. The opposite situation

is also true. A rapidly falling SMI during a bullish market means that smart money is selling and that market is to revert to a downtrend

soon. The SMI is, therefore, a trend-based indicator.

Some analysts use the smart money index to claim that precious metals such as gold will continually maintain value in the future.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

High and Low Levels Backtest This script shows a high and low period value.

Width - width of lines

SelectPeriod - Day or Week or Month and etc.

LookBack - Shift levels 0 - current period, 1 - previous and etc.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Floor Pivot Points Backtest The name ‘Floor-Trader Pivot,’ came from the fact that Pivot points can

be calculated quickly, on the fly using price data from the previous day

as an input. Although time-frames of less than a day can be used, Pivots are

commonly plotted on the Daily Chart; using price data from the previous day’s

trading activity.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

[STRATEGY]Kagi Emulator OCC & SLTP V3It is a Kagi candle emulator without resolution multiplier.

Also with take profit and stop loss.

Modify the value of "reversal" according to current symbol.

It's the backtest, coming soon, same script but with no-repainting alerts

Enjoy!

CMOaDisparity Index Backtest The related article is copyrighted materialfrom Stocks & Commodities Dec 2009

My strategy modification.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Dual Timeframe SMA Ribbon Crossover Backtest// Backtesting Dual SMA Ribbon Crossover Strategy

// see f.bpcdn.co

// including time limiting

Turned this study into a backtest.

The Falcon - My BTC/USDT Strategy 5 min UTHello,

I made a custom indicator, I called it The Falcon because it reacts quickly and knows how to take perspective of the market.

This kind of indicator can be used for manual trading or bots.

About the indicator

In short, it will help you :

Make profit when the market is in trading range

Get in/Get out when a rally begins

Never go against the trend

I based my algorithm on several technical tools such as RSI , emas , for a total of 3 boolean conditions mixed together with AND and OR gates, resulting in those entry/exit points (arrows).

About the Strategy

I only used long entries and exits. No shorting.

It is tested on the last 18 days (the maximum TradingView allows for a 5 min range)

I set a 0.05% commission on each order.

I will grant access to people willing to make a small donation.

Here is my BTC address : 19sVQvCDmVfEACq7BiMnWSMqFPZ8qfSQ2K

If you prefer ETH : 0xc8a5d3a63a05db0c2363ea1c08b37a01cce9ebfb

Send me a Private Message with the ID of the transaction

If you want to do some forward testing first, send me a message.

This script comes with an Alert Setup.

I am also taking commissions if you want me to code something for you, or do some reverse engineering.

Also you can ask me anything in the comments.

Thanks and see you next time !

The Falcon - My Custom Indicator and Alert SetupHello,

I made a custom indicator, I called it The Falcon because it reacts quickly and knows how to take perspective of the market. It switches entry and exit conditions depending on wether we are in trading range or in a bullish/bearish trend (difference between green/blue arrows and between red/orange arrows).

This kind of indicator can be used for manual trading or bots.

I will grant access to people willing to make a small donation.

Here is my BTC address : 19sVQvCDmVfEACq7BiMnWSMqFPZ8qfSQ2K

If you prefer ETH : 0xc8a5d3a63a05db0c2363ea1c08b37a01cce9ebfb

Send me a Private Message with the ID of the transaction

If you want to do some forward testing first, send me a message.

I will upload soon a Strategy version of The Falcon with backtesting results.

I am also taking commissions if you want me to code something for you, or do some reverse engineering.

Also you can ask me anything in the comments.

Thanks and see you next time !

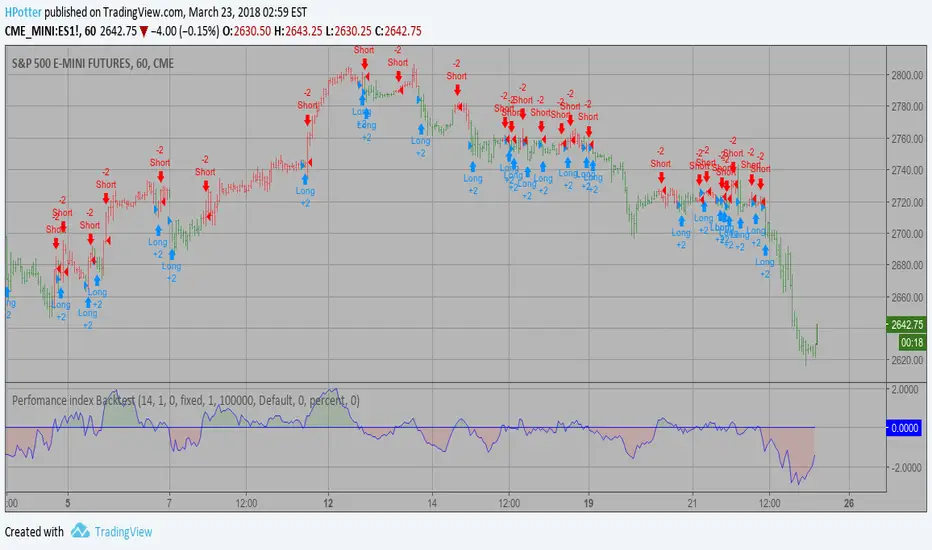

Perfomance index Backtest The Performance indicator or a more familiar term, KPI (key performance indicator),

is an industry term that measures the performance. Generally used by organizations,

they determine whether the company is successful or not, and the degree of success.

It is used on a business’ different levels, to quantify the progress or regress of a

department, of an employee or even of a certain program or activity. For a manager

it’s extremely important to determine which KPIs are relevant for his activity, and

what is important almost always depends on which department he wants to measure the

performance for. So the indicators set for the financial team will be different than

the ones for the marketing department and so on.

Similar to the KPIs companies use to measure their performance on a monthly, quarterly

and yearly basis, the stock market makes use of a performance indicator as well, although

on the market, the performance index is calculated on a daily basis. The stock market

performance indicates the direction of the stock market as a whole, or of a specific stock

and gives traders an overall impression over the future security prices, helping them decide

the best move. A change in the indicator gives information about future trends a stock could

adopt, information about a sector or even on the whole economy. The financial sector is the

most relevant department of the economy and the indicators provide information on its overall

health, so when a stock price moves upwards, the indicators are a signal of good news. On the

other hand, if the price of a particular stock decreases, that is because bad news about its

performance are out and they generate negative signals to the market, causing the price to go

downwards. One could state that the movement of the security prices and consequently, the movement

of the indicators are an overall evaluation of a country’s economic trend.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Chande Forecast Oscillator Backtest The Chande Forecast Oscillator developed by Tushar Chande The Forecast

Oscillator plots the percentage difference between the closing price and

the n-period linear regression forecasted price. The oscillator is above

zero when the forecast price is greater than the closing price and less

than zero if it is below.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Fractal Chaos Bands Backtest The FCB indicator looks back in time depending on the number of time periods trader selected

to plot the indicator. The upper fractal line is made by plotting stock price highs and the

lower fractal line is made by plotting stock price lows. Essentially, the Fractal Chaos Bands

show an overall panorama of the price movement, as they filter out the insignificant fluctuations

of the stock price.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

How To Set Backtest Date RangeExample how to select and set date range window to be backtested. Normally when you change chart period it changes the number of days being backtested which means as you increas the chart period (for example from 5min to 15min) you also increase the number of days traded, so you can not compare apples to apples for which period would yield best returns for your strategy. Now you can. Incorporate this code replacing buy and sell with your strategy, then simply input the From and To dates in Format -> Inputs, and then change the chart period to view updated results.

NOTE: There is a limit in backtesting to 2000 orders, so please be aware of this when setting your date ranges. If you set your range too high, you may be exceeding this limit on some periods and not on others, so this would yield incorrect comparison of returns per period. If you see in your backtesting results that you are nearing this limit for one of your periods you are testing, then reduce the date range to a smaller number of days.

Enjoy!

(Thanks to @Gesundheit "Adeel" for pointing me in the right direction on this!)

MACD Crossover Backtest MACD – Moving Average Convergence Divergence. The MACD is calculated

by subtracting a 26-day moving average of a security's price from a

12-day moving average of its price. The result is an indicator that

oscillates above and below zero. When the MACD is above zero, it means

the 12-day moving average is higher than the 26-day moving average.

This is bullish as it shows that current expectations (i.e., the 12-day

moving average) are more bullish than previous expectations (i.e., the

26-day average). This implies a bullish, or upward, shift in the supply/demand

lines. When the MACD falls below zero, it means that the 12-day moving average

is less than the 26-day moving average, implying a bearish shift in the

supply/demand lines.

A 9-day moving average of the MACD (not of the security's price) is usually

plotted on top of the MACD indicator. This line is referred to as the "signal"

line. The signal line anticipates the convergence of the two moving averages

(i.e., the movement of the MACD toward the zero line).

Let's consider the rational behind this technique. The MACD is the difference

between two moving averages of price. When the shorter-term moving average rises

above the longer-term moving average (i.e., the MACD rises above zero), it means

that investor expectations are becoming more bullish (i.e., there has been an

upward shift in the supply/demand lines). By plotting a 9-day moving average of

the MACD, we can see the changing of expectations (i.e., the shifting of the

supply/demand lines) as they occur.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Kaufman Moving Average Adaptive (KAMA) Backtest Everyone wants a short-term, fast trading trend that works without large

losses. That combination does not exist. But it is possible to have fast

trading trends in which one must get in or out of the market quickly, but

these have the distinct disadvantage of being whipsawed by market noise

when the market is volatile in a sideways trending market. During these

periods, the trader is jumping in and out of positions with no profit-making

trend in sight. In an attempt to overcome the problem of noise and still be

able to get closer to the actual change of the trend, Kaufman developed an

indicator that adapts to market movement. This indicator, an adaptive moving

average (AMA), moves very slowly when markets are moving sideways but moves

swiftly when the markets also move swiftly, change directions or break out of

a trading range.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Backtest History Setup 1.0Script of strategy component to setup the backtext lookback. You setup the maximum days back in the history, which will be used for backtest.

15 Minute Gold Trend-Following StrategyThis is the main strategy that I will be forward testing on demo for a month or two, then making it an EA in MetaTrader4

You can see the code for yourself this time, all the strategy is, is a crossover of various moving averages.

Commission included, $10,000 account.

Results over the past 3 months, beginning in January 2017.