3 Leg Short Strangle BandsDraws 3 leg bands along with safe zone(green lines) based on input

1) Input ATR, Week Day, Current Market Close

2) Input ATR - Previous day 1H Max ATR

3) ADX < 25

4) Input Current Market Close

5) Trading Day - Mon/Tue/Wed/Thu/Fri - Bands distance calculated based on day M/Tu/F 2*(Max ATR), W/Th 1.5(ATR)

6) Safe zone green lines - CMPCls +/- (1.5 * Max ATR)

7) Leg 1 Upper Lower Legs - M/Tu/F - CMPCls +/-(2 * Max ATR), W/Th - CMPCls +/-(1.5 * ATR)

8) Leg 2 & 3 Calculates based on Leg 2 = Leg 1 +/- 100 pts distance, Leg 3 = Leg 2 +/- 100 pts distance'

9) All figures rounded to nearest 100's

10) Safe zone broken exit all positions

This is a popular technic used by Profitable traders on sideway markets for Intraday

One can keep 3K as SL per 1 set of 3 legs for better R:R

"马斯克+100万" için komut dosyalarını ara

HeatbandsWhat you see is the 100 day moving average (blue line in the middle) with percentage bands attached to it.

Each color has a 5% range.

The brightest green color is 20%-25% below the 100 day moving average.

The brightest red color is 20%-25% above the 100 day moving average.

The behaviour of the stock price between the bands could give you trading ideas.

The moving average length is adjustable.

The range between the bands is not adjustable (maybe in future updates).

Enjoy:)

Spread for VSAЭтот индикатор сравнивает спрэд (расстояние от закрытия предыдущего бара до закрытия текущего бара или индикатор Momentum = 1) на периоде для сравнения.

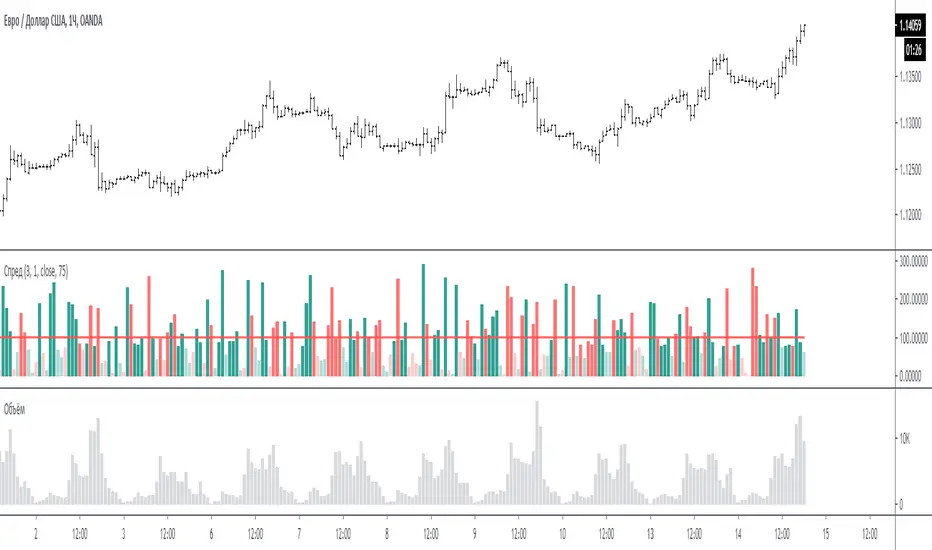

На графике за 100 % принимается среднее значение спрэда за период для сравнения - красная линия. (по умолчанию период сравнения равен 3 - то есть три последних бара)

Размер бара на графике равен текущему спрэду по отношению к 100 %.

Если бар меньше 100 % то он ниже среднего, и наоборот если больше 100% то он больше среднего.

Если бар красный - спрэд отрицательный (текущее закрытие меньше предыдущего закрытия)

Если бар зелёный - спрэд положительный (текущее закрытие больше предыдущего закрытия)

Если бар меньше 75% то он будет окрашен в тусклый цвет (этот процент можно менять в настройках)

Если в настройках период спрэда указать больше 1, например 2, то спрэд будет равен закрытие мину закрытие через 1 бар назад. (это для экспериментов).

Примечание:

по умолчанию период для сравнения равен 3, но также интересен график и при значениях 15 и больше. Экспериментируйте.

По вопросам и предложениям пишите в комментариях.

Automatic translation google translate.

This indicator compares the spread (the distance from the closing of the previous bar to the closing of the current bar or the Momentum indicator = 1) on the period for comparison.

On the chart, the average spread value for the period for comparison is the red line, taken as 100%. (by default, the comparison period is 3 - that is, the last three bars)

The size of the bar on the chart is equal to the current spread with respect to 100%.

If the bar is less than 100%, then it is below average, and vice versa, if more than 100%, then it is more than average.

If the bar is red, the spread is negative (the current close is less than the previous close)

If the bar is green, the spread is positive (the current close is greater than the previous close)

If the bar is less than 75%, then it will be painted in a dull color (this percentage can be changed in the settings)

If in the settings the period of the spread is specified more than 1, for example 2, then the spread will be equal to closing mine closing after 1 bar back. (this is for experimentation).

Note:

the default period for comparison is 3, but the chart is also interesting for values of 15 or more. Experiment.

For questions and suggestions, write in the comments.

[LunaOwl] 強度指數 (Num-Day Strength Index, NDSI)The Num-Day Strength Index was published by Mr.George Angel. low percentage represent bear, high percentage represent bull, and the 50 level is a watershed. In fact, you should adjust the length according to the market, timeframe and trading day. the default is 100 universal.

原本Num-Day Strength Index是指N日內的強度指數,由喬治安傑爾先生提出,可以衡量市場強度,根據50水平線區分多空,事實上,您應該根據自己所在的市場、時框以及每週交易日調整參數。預設值是100。

--------------------------*

Formula - 公式

NDSI =

( last close - lowest since period x ) * 100 /

( highest since period x - lowest since period )

--------------------------*

Indicator Style - 指標樣式

Take a simple and bright style at a glance.

簡潔的風格,一目了然。

--------------------------*

Market Example - 市場範例

1. TAIEX , Taiwan SE Weighted Index, 4 hour

2. EUR/USD , Forex Market, 1 hour

3. S&P 500 E-mini futures, 15 min

LUBEThis is a chart meant for 30m BTCUSD but could be used for many other assets, and there are inputs to play with.

I decided on the strange title "LUBE" because I was measuring how many of the previous 500 bars had the current price level already been in. I wanted to discover when the price was in a new zone or an area that it hadn't spent much time in recently... the LUBE zone.

Think of the blue line as showing you the current level friction. If the blue line is high, price is quagmired and not moving quickly. Price could trend sideways for a while before breaking out. A high blue line is a high traffic zone for trading. When the blue line dips low, it's encountering a price zone the asset has not been observed in recently, and this could mean price could break out and move more freely and quickly when it does. We get a trade entry signal if the blue line dips below the bottom white line. The bottom white line is currently set to -10. Think about the lowest the blue line has been recently as 0, and the highest as 100. It is set by default (for BTCUSD 30m chart) to -10 meaning the blue line has to dip a little (-10%) below the lowest it has experienced recently to initiate a trade. This is the LUBE zone. The bottom white line shows that level. Again this is a level lower than the lowest amount of friction experienced in price action for the last 100 bars, but offset by 5 bars showing where that level was at 5 bars ago. We want to dip below that to initiate a trade.

The direction to trade in is determined by a very quick moving weighted moving average (variable name is "fir") to see if the recent trend is up or down. To end a trade, an arbitrary number between 0 and 100 is picked telling us when we are experiencing enough friction again to end the trade. I have it preset to 50 (think of it as 50/100 or half way between the white bars. At a 50% friction level it's time to get out of the trade.

Some shortcomings are missing the bulk of big moves, and experiencing whipsaws where price action zips up and then comes straight back down. Overall the backtest looks sweet enough to use on 2x leverage, experiencing a 17.78% max drawdown at the time of publishing. I wouldn't push the leverage any higher.

To get alerts change the word "strategy" to "study" and delete lines 60-67.

Bot traders using alerts: beware the alert conditions. If a trade goes directly from long to short (which happens rarely), without closing a trade first, it might not act properly. If you use bots to trade, for "LONG" please close any old trades first before putting in instructions to open a leveraged long. To go "SHORT" please remember to close any old trade first as well, and things *should* work out just fine.

Good luck, have fun, and feel free to mess up and butcher this code to your own liking. I'm not responsible if anything bad that happens to you if you use this trading system, or for any bugs you may encounter.

IKAKOver2(LITE雲なし)

change point

I tried to make the operation lighter by removing the display of the Ichimoku balance table.

We have set a period such as EMA to use 5 minute bars and the first band is period 60 and 100 EMA . The color of the belt changes according to the position of the period 5EMA-25EMA-50EMA. The second sash is based on a 60- and 100-EMA period of 15 minutes. The change in the color of the obi is also a 15-minute specification.

Since the above period can be changed, I think that there are customs such as 1 hour and 4 hours.

Buying and selling signs are shown in green for buying and red for selling. (More frequent)

For the time being, it is also possible to display the Ichimoku balance table.

As for my usage method, when both the 15-minute and 5-minute bars have an uptrend (downtrend ), when each trading sign is confirmed, spread the limit just below the price. . (Because there is a commission in the market)

If the color of the obi becomes yellow, the trend may be over, so wait for the signature to reach the bundle of 15 minutes instead of 5 minutes, and after the signature is confirmed, it is the same as 5 minutes.

The loss cut line is often the latest low. Or when the obi is broken. .

I am still studying about profitability. Sometimes we use indicators, sometimes we reach the target horizon. I think each way is good.

It is a discretionary aid, and the head and tail are cut off, and the image is about 10 to 100 $.

IKAKOver2change point

Improve the accuracy of reverse sign

Adding a signature using only RCI

変更点

逆張りのサインと順張りのサインを区別し、逆張りのサインは騙しができるだけ少なくなるように精度を上げました。

逆張りか順張りかは10emaと100emaの位置関係だけで区別しています。

また、RCIのみを利用した、レンジ相場用のサインを追加しました。

We have set a period such as EMA to use 5 minute bars and the first band is period 60 and 100 EMA . The color of the belt changes according to the position of the period 5EMA-25EMA-50EMA. The second sash is based on a 60- and 100-EMA period of 15 minutes. The change in the color of the obi is also a 15-minute specification.

Since the above period can be changed, I think that there are customs such as 1 hour and 4 hours.

Buying and selling signs are shown in green for buying and red for selling. (More frequent)

For the time being, it is also possible to display the Ichimoku balance table.

As for my usage method, when both the 15-minute and 5-minute bars have an uptrend (downtrend ), when each trading sign is confirmed, spread the limit just below the price. . (Because there is a commission in the market)

If the color of the obi becomes yellow, the trend may be over, so wait for the signature to reach the bundle of 15 minutes instead of 5 minutes, and after the signature is confirmed, it is the same as 5 minutes.

The loss cut line is often the latest low. Or when the obi is broken. .

I am still studying about profitability. Sometimes we use indicators, sometimes we reach the target horizon. I think each way is good.

It is a discretionary aid, and the head and tail are cut off, and the image is about 10 to 100 $.

IKAKOWe have set a period such as EMA to use 5 minute bars and the first band is period 60 and 100 EMA. The color of the belt changes according to the position of the period 5EMA-25EMA-50EMA. The second sash is based on a 60- and 100-EMA period of 15 minutes. The change in the color of the obi is also a 15-minute specification.

Since the above period can be changed, I think that there are customs such as 1 hour and 4 hours.

Buying and selling signs are shown in green for buying and red for selling. (More frequent)

For the time being, it is also possible to display the Ichimoku balance table.

As for my usage method, when both the 15-minute and 5-minute bars have an uptrend (downtrend ), when each trading sign is confirmed, spread the limit just below the price. . (Because there is a commission in the market)

If the color of the obi becomes yellow, the trend may be over, so wait for the signature to reach the bundle of 15 minutes instead of 5 minutes, and after the signature is confirmed, it is the same as 5 minutes.

The loss cut line is often the latest low. Or when the obi is broken. .

I am still studying about profitability. Sometimes we use indicators, sometimes we reach the target horizon. I think each way is good.

It is a discretionary aid, and the head and tail are cut off, and the image is about 10 to 100 $.

7EMA_5MA (G/D + Bias + 12/26 Signal)This script alow you to survey multiple crossing signals as Golden/Death cross (MA50/200), Institutional Bias (EMA9/18), or EMA 12/26 crossing. You can show/hide all EMAs/MAs and show/hide all signals. Default config displays EMA 50/100/200 and MA 20. Full script includes display of EMA 9/18/12/26/50/100/200 and MA 20/21/50/100/200.

Point and Figure (PnF) ChartThis is live and non-repainting Point and Figure Charting tool. The tool has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

Chart Style: There are 3 options for chart style: “Candle”, “Area” or “Don’t show”.

As Area:

As Candle:

X/O Column Style: it can show all columns from opening price or only last Xs/Os.

Color Theme: different themes exist => Green/Red, Yellow/Blue, White/Yellow, Orange/Blue, Lime/Red, Blue/Red

Show Breakouts is the option to show Breakouts

This tool detects & shows following Breakouts:

Triple Top/Bottom,

Triple Top Ascending,

Triple Bottom Descending,

Simple Buy/Sell (Double Top/Bottom),

Simple Buy With Rising Bottom,

Simple Sell With Declining Top

Catapult bullish/bearish

Show Horizontal Count Targets: Finds the congestion or consolidation pattern and if there is breakout then it calculates the Target by using Horizontal Count method (based on the width of congestion pattern). It shows how many column exist on congestion area. There is no guarantee that prices will reach the target.

Show Vertical Count Targets: When Triple Top/Bottom Breakouts occured the script calculates the target by using Vertical Count Method (based on the length of the column). There is no guarantee that prices will reach the target.

For both methods there is auto target cancellation if price goes below congestion bottom or above congestion top.

trend is calculated by EMA of closing price of the P&F

Whipsaw protection:

Last options are “Show info panel” and Labeling Offset. Script shows current box size, reversal, and recommanded minimum and maximum box size. And also it shows the price level to reverse the column (Xs <-> Os) and the price level to add at least 1 more box to column. This is the option to put these labels 10, 20, 30, 50 or 100 bars away from the last bar. Labeling content and color change according to X/O column.

do not hesitate to comment.

Technical Analysis - Panel Info//A. Oscillators & B. Moving Averages base on TradingView's Technical Analysis by ThiagoSchmitz

//C.Pivot base on Ultimate Pivot Points Alerts by elbartt

//D. Summary & Panel info by anhnguyen14

Panel Info base on these indicators:

A. Oscillators

1. Rsi (14)

2. Stochastic (14,3,3)

3. CCI (20)

4. ADX (14)

5. AO

6. Momentum (10)

7. MACD (12,26)

8. Stoch RSI (3,3,14,14)

9. %R (14)

10. Bull bear

11. UO (7,14,28)

B. Moving Averages

1. SMA & EMA: 5-10-20-30-50-100-200

2. Ichimoku Cloud - Baseline (26)

3. Hull MA (9)

C. Pivot

1. Traditional

2. Fibonacci

3. Woodie

4. Camarilla

D. Summary

Sum_red=A_red+B_red+C_red

Sum_blue=A_blue+B_blue+C_blue

sell_point=(Sum_red/32)*100

buy_point=(Sum_blue/32)*100

sell =

Sum_red>Sum_blue

and sell_point>50

Strong_sell =

A_red>A_blue

and B_red>B_blue

and C_red>C_blue

and sell_point>50

and not crossunder(sell_point,75)

buy =

Sum_red>Sum_blue

and buy_point>50

Strong_buy =

A_red50

and not crossunder(buy_point,75)

neutral = not sell and not Strong_sell and not buy and not Strong_buy

CCI RiderThis is my thank you to the TradingView community, for the people who are sharing their scripts, which allowed me to learn Pine Script.

So here is my first creation, feel free to experiment, modify and use it as you wish.

It is a CCI(default value is 100, can be changed), combined with an EMA of that CCI(default 21,changeable) that then colors the background according to the strength of the signal(if selected to do so).

To generate strong signals, it also uses Bollinger Bands to prevent whipsaws in high volatility situations.

The best signals are generated when the CCI crosses the limits set by the user (default is 100/-100), and is above/belov its EMA.

Exit signals are indicated, when the CCI crosses its EMA.

Unfortunately in strong trends, this exit signal is sometimes premature, using a 3x resolution of the indicator will improve this, maybe I will implement this in a later version.

I use it mostly in 15min charts and higher, I found in shorter timeframes still a lot of whipsaws, maybe experimenting with different lengths and levels will improve this.

As the Indicator allows the user to experiment with different lenghts and levels, and the colors will change according the setting, I find it a nice tool to search for the best mixture for different securities and timeframes.

See below an example of a nice signal.

I do suggest to use it in combination with other indicators.

Yield Curve Version 2.55.2Welcome to Yield Curve Version 2.55.2

US10Y-US02Y

* Please read description to help understand the information displayed.

* NOTE - This script requires 1 real time update before accurate information is displayed, therefore WILL NOT display the correct information if the Bond Market is Closed over the Weekend.

* NOTE - When values are changed Via Input setting they do take a bit to display based off all the information that is required to display this script.

**FEATURES**

* Input Features let you view the information the way YOU like via Input Settings

* Displays Current Version Title - Toggleable On/Off via Input Settings - Default On

* Plots the Yield Curve of the Bonds listed (Middle Green and Red Line)

* Displays the Spread for each Bond (Top Green and Red Labels) - Toggleable On/Off via Input Settings - Change Size via Input Settings - Default On

* Displays the current Yield for each Bond (Bottom Green and Red Labels) - Toggleable On/Off via Input Settings - Change Size via Input Settings - Default On - Large Size

* Plots the Average of the Entire Yield Curve (BLUE Line within the Yield Curve) - Toggleable On/Off via Input Settings - Default On

* Displays messages based off Yield Inversions (Orange Text) - Toggleable On/Off via Input Settings - Default On if Applicable

* Displays 2 10 Inversion Warning Message (Orange Text) - Toggleable On/Off via Input Settings - Default On if Applicable

* Plots Column Data at the Bottom that tries to help determine the Stability of the Yield Curve (More information Below about Stability) - Toggleable On/Off via Input Settings - Default On

* Plots the 7,20 and 100 SMA of the STABILITY MAX OVERLOAD (More information Below about Stability Max Overload) - Toggleable On/Off via Input Settings - Default On for 100 SMA , 20 SMA and 7 SMA

* Ability to Display Indicator Name and Value via Input Settings - Default On - Displays Stability Max Overload SMA Labels. Toggleable to Non SMA Values. See Below.

**Bottom Columns are all about STABILITY**

* I have tried to come up with an algorithm that helps understand the Stability of the Yield Curve. There are 3 Sections to the Bottom Columns.

* Section 1 - STABILITY (Displayed as the lightest Green or Red Column) Values range from 0 to 1 where 1 equals the MOST UNSTABLE Curve and 0 equals the MOST STABLE Curve

* Section 2 - STABILITY OVERLOAD (Displayed just above the Stability Column a shade darker Green or Red Column)

* Section 3 - STABILITY MAX OVERLOAD (Displayed just above the Stability Overload Column a shade darker Green or Red Column)

What this section tries to do is help understand the Stability of the Curve based on the inversions data. Lower values represent a MORE STABLE curve. If the Yield Curve currently has 0 Inversions all Stability factors should equal 0 and therefore not plot any lower columns. As the Yield Curve becomes more inverted each section represents a value based off that data. GREEN columns represent a MORE Stable Curve from the resolution prior and vise versa.

(S SO SMO)

STABILITY - tests the current Stability of the Curve itself again ranging from 0 to 1 where 0 equals the MOST Stable Curve and 1 equals the MOST Unstable Curve.

STABILIY OVERLOAD - adds a value to STABLITY based off STABILITY itself.

STABILITY MAX OVERLOAD - adds the Entire value to STABILITY derived again from STABILITY.

This section also allows us to see the 7,20 and 100 SMA of the STABILITY MAX OVERLOAD which should always be the GREATEST of ALL STABILTY VALUES.

*Indicator Labels How to use*

Indicator Labels by default are turned On and will display Name and Value Labels for Stability Max Overload SMA values. To switch to (S SO SMO) Labels, toggle "Indicator Labels / SMO SMA Labels", via Input Settings. This button allows you to switch between the two Indicator Label Display options. You must have "Indicators" turned On to view the Labels and therefore is turned On by Default. To turn all of the Indicator Labels Off, simply disable "Indicators" via Input Settings.

Remember - All information displayed can be tuned On or Off besides the Curve itself. There are also other Features Accessible Via the Input Settings.

I will continue to update this script as there is more information I would like to gather and display!

I hope you enjoy,

OpptionsOnly

Ultimate Moving Average Package (17 MA's)Included is the:

VWAP

Current time frame 10 EMA

Current time frame 20 EMA

Current time frame 50 EMA

Current time frame 10 SMA

Current time frame 20 SMA

Current time frame 50 SMA

Daily 10 EMA

Daily 20 EMA

Daily 50 EMA

Daily 50 SMA

Daily 100 SMA

Daily 200 SMA

Weekly 100 SMA

Weekly 200 SMA

Monthly 100 SMA

Monthly 200 SMA

All Daily/Weekly/Monthly MA's can be seen on intraday charts. Current time frame MA's change depending on your time frame. Obviously you dont need all 17 on your chart but you can pick the ones you like and disable the rest.

Bilateral Stochastic Oscillator - For The Sake Of EfficiencyIntroduction

The stochastic oscillator is a feature scaling method commonly used in technical analysis, this method is the same as the running min-max normalization method except that the stochastic oscillator is in a range of (0,100) while min-max normalization is in a range of (0,1). The stochastic oscillator in itself is efficient since it tell's us when the price reached its highest/lowest or crossed this average, however there could be ways to further develop the stochastic oscillator, this is why i propose this new indicator that aim to show all the information a classical stochastic oscillator would give with some additional features.

Min-Max Derivation

The min-max normalization of the price is calculated as follow : (price - min)/(max - min) , this calculation is efficient but there is alternates forms such as :

price - (max - min) - min/(max - min)

This alternate form is the one i chosen to make the indicator except that both range (max - min) are smoothed with a simple moving average, there are also additional modifications that you can see on the code.

The Indicator

The indicator return two main lines, in blue the bull line who show the buying force and in red the bear line who show the selling force.

An orange line show the signal line who represent the moving average of the max(bull,bear), this line aim to show possible exit/reversals points for the current trend.

Length control the highest/lowest period as well as the smoothing amount, signal length control the moving average period of the signal line, the pre-filtering setting indicate which smoothing method will be used to smooth the input source before applying normalization.

The default pre-filtering method is the sma.

The ema method is slightly faster as you can see above.

The triangular moving average is the moving average of another moving average, the impulse response of this filter is a triangular function hence its name. This moving average is really smooth.

The lsma or least squares moving average is the fastest moving average used in this indicator, this filter try to best fit a linear function to the data in a certain window by using the least squares method.

No filtering will use the source price without prior smoothing for the indicator calculation.

Relationship With The Stochastic Oscillator

The crosses between the bull and bear line mean that the stochastic oscillator crossed the 50 level. When the Bull line is equal to 0 this mean that the stochastic oscillator is equal to 0 while a bear line equal to 0 mean a stochastic oscillator equal to 100.

The indicator and below a stochastic oscillator of both period 100

Using Levels

Unlike a stochastic oscillator who would clip at the 0 and 100 level the proposed indicator is not heavily constrained in a range like the stochastic oscillator, this mean that you can apply levels to trigger signals

Possible levels could be 1,2,3... even if the indicator rarely go over 3.

Its then possible to create strategies using such levels as support or resistance one.

Conclusion

I've showed a modified stochastic oscillator who aim to show additional information to the user while keeping all the information a classical stochastic oscillator would give. The proposed indicator is no longer constrained in an hard range and posses more liberty to exploit its scale which in return allow to create strategies based on levels.

For pinescript users what you can learn from this is that alternates forms of specific formulas can be extremely interesting to modify, changes can be really surprising so if you are feeling stuck, modifying alternates forms of know indicators can give great results, use tools such as sympy gamma to get alternates forms of formulas.

Thanks for reading !

If you are looking for something or just want to say thanks try to pm me :)

High/Low bandsGives good idea about trend.

In last 100 days the lowest price was this.

In last 100 days the highest price was this.

Price makes new 100 days high! (uptrend)

Chaikin MF% (CMFP) w. Alerts, Bells & Whistles [LucF]This is Chaikin’s Money Flow indicator on a 0-100 scale with buy/sell signals, alerts and other bells & whistles.

It includes:

- a fast EMA (16 periods by default),

- a slow MA (64 periods by default),

- histograms,

- 3 different sorts of crosses,

- big swings identification,

- buy/sell signals on CMFP crossing back from outside user-defined levels,

- buy/sell signals on the slow MA pivots above/below user-defined levels,

- alerts on big swings and buy/sells.

This indicator started with @LazyBear code (VAPI) at:

@cI8DH then changed the scale to 0-100, which I find very useful:

I then added the rest.

The chart above shows both clean and busy versions of the indicator.

Note that the default length is 10 rather than the commonly used 20. I use CMFP in conjunction with VFI and like the fact that it is faster than VFI. The default inputs show the way I normally use this indicator, with the slow MA shown in histogram mode. I find it gives good context to the signal line. Crosses between the two are often useful.

The buy/sell signals aren’t the main attraction of this indicator, and nothing to write home about. Like the big swing markers, I think it’s more realistic to view them as pointers to potentially interesting areas on charts. Their nature makes them more suited to identifying reversals. They certainly aren’t reliable enough to turn this study into a strategy and I normally don’t use them. The levels pre-defined for the buy/sell signals on CMFP are most useful on short intervals. The buy/sell signals on the slow MA pivots work on a more complete range of intervals. Optimization for your specific instruments and intervals will improve their reliability.

As usual when defining alerts, be sure you already have defined proper inputs and that you are on the intended interval, as they will be used when triggering alerts.

3 of SlowStochastics

스토캐스틱 3개를 한번에 볼수 있습니다. 천장과 바닥은 각 100의 위치마다 존재합니다

You can see three slow stochastics at once. The ceiling and floor are located at each 100 (0 - 100 - 200- 300)

Percentage Price Oscillator (PPO)The Percentage Price Oscillator (PPO) is a momentum oscillator that measures the difference between two moving averages as a percentage of the larger moving average. As with its cousin, MACD, the Percentage Price Oscillator is shown with a signal line, a histogram and a centerline. Signals are generated with signal line crossovers, centerline crossovers, and divergences. First, PPO readings are not subject to the price level of the security. Second, PPO readings for different securities can be compared, even when there are large differences in the price.

Calculations

PPO: {(12-day EMA - 26-day EMA)/26-day EMA} x 100

Signal Line: 9-day EMA of PPO

PPO Histogram: PPO - Signal Line

While MACD measures the absolute difference between two moving averages, PPO makes this a relative value by dividing the difference by the slower moving average (26-day EMA). PPO is simply the MACD value divided by the longer moving average. The result is multiplied by 100 to move the decimal place two spots.

Interpretation

As with MACD, the PPO reflects the convergence and divergence of two moving averages. PPO is positive when the shorter moving average is above the longer moving average. The indicator moves further into positive territory as the shorter moving average distances itself from the longer moving average. This reflects strong upside momentum. The PPO is negative when the shorter moving average is below the longer moving average. Negative readings grow when the shorter moving average distances itself from the longer moving average (goes further negative). This reflects strong downside momentum. The histogram represents the difference between PPO and its 9-day EMA, the signal line. The histogram is positive when PPO is above its 9-day EMA and negative when PPO is below its 9-day EMA. The PPO-Histogram can be used to anticipate signal line crossovers in the PPO.

MACD, PPO and Price

MACD levels are affected by the price of a security. A high-priced security will have higher or lower MACD values than a low-priced security, even if volatility is basically equal. This is because MACD is based on the absolute difference in the two moving averages. Because MACD is based on absolute levels, large price changes can affect MACD levels over an extended period of time. If a stock advances from 20 to 100, its MACD levels will be considerably smaller around 20 than around 100. The PPO solves this problem by showing MACD values in percentage terms.

Conclusions

The Percentage Price Oscillator (PPO) generates the same signals as the MACD, but provides an added dimension as a percentage version of MACD. The PPO levels of the Dow Industrials (price > 20K) can be compared against the PPO levels of IBM (price < 200) because the PPO “levels” the playing field. In addition, PPO levels in one security can be compared over extended periods of time, even if the price has doubled or tripled. This is not the case for the MACD.

Limitations

Despite its advantages, the PPO is still not the best oscillator to identify overbought or oversold conditions because movements are unlimited (in theory). Levels for RSI and the Stochastic Oscillator are limited and this makes them better suited to identify overbought and oversold levels.

Source: Stockcharts

Multiple Moving AveragesThis is really simple. But useful for me as I don't have a paid account. No-pro users can only use 3 indicators at once and because I rely heavily on simple moving averages it can be a real pain.

This one indicator features:

20 MA

50 MA

100 MA

200 MA

which I find are the most useful overall. The 20 and 50 over all time frame but in particular < 1 day, the 100 and 200 at > 4 hr time frames. In general I don't use the 100 MA that much. The daily 200 MA is a critical support for many assets like stocks and cryptos. I'm by no means a pro and if you are learning I recommend becoming familiar with moving averages right at the beginning.

If you want to deactivate some of the lines, you can do it via the indicator's settings icon.

Exponential Moving Average (Set of 3) [Krypt] + 13/34 EMAsI took Krypt's script and essentially added on to it.

the 20/50/100/200 EMAs should be used together as support and resistance as normal.

Wait for price to break 200 EMA

Wait for 50 EMA to cross 200 EMA

Wait for pullback to 50 EMA to open position

20 and 100 EMAs are for extra information about moving support and resistance

and 13/34 EMAs should be used in conjunction

When 13 EMA crosses 34 EMA, open position

When price gets far from 13/34, close position (because price will attempt to revert back to mean)

This is better for scalping and swing trades than the 20/50/100/200 setup.

Twitter: @AzorAhai06

Ichimoku Cloud Score v1.0This script calculates a simple Ichimoku Score based on the signals documented here , with a few additions. Each of the score components can be individually weighted via the script inputs . The output is a plot of the normalized Ichimoku score, in the range of -100 to 100.

This script has been heavily modified from 'Ichimoku Cloud Signal Score v2.0.0 '. Credit to user 'dashed' for the initial implementation.

This has been modified with several refinements:

Clean/Organized Code

Simplified Inputs

Improved Style

Scores normalized to a range (-100, 100)

Bugfixes and Improvements

Script Inputs: i.imgur.com

Volume RatioDefinition:

Volume ratio can be obtained in a similar way to RSI.

Volume Ratio (%) = 100 - 100/(1+vr)

The parameter "vr" is defined as

vr=(A+U/2)/(D+U/2)

A=Total volume of the periods when the price advanced

D=Total volume of the periods when the price declined

U=Total volume of the periods when the price unchanged

After substitution, following expression can be derived and the denominator represents total volume of all periods.

Volume Ratio (%) = 100 x (A+U/2)/(A+D+U)

Notes:

A similar method to interpret RSI can be employed.

1) Overbought level over 70% and oversold level under 30%. These levels need to be adjusted according to the periods, time frames and issues.

2) Bullish picture over 50% line and bearish picture under 50% line.

3) Crossing oversold level to the upside can be taken as a confirmation of bullish reversal. - and vice versa for a bearish reversal.

4) After a long-term bearish market, the increase of volume can happen in the early stage of a bullish market.

5) Buying opportunity can be suggested when the volume ratio is declining and the price is either advancing or leveling off.