Mxwll Price Action Suite [Mxwll]Introducing the Mxwll Price Action Suite!

The Mxwll Price Action Suite is an all-in-one analysis indicator incorporating elements of SMC and also ideas extending beyond the trading methodology!

Features

Internal structures

External structures

Customizable Sensitivities

BoS/CHoCH

Order Blocks

HH/LH/LL/LH Areas

Rolling TF highs/lows

Rolling Volume Comparisons

Auto Fibs

And more!

The image above shows the indicator's market structure identification capabilities. Internal BoS and CHoCH structures in addition to overarching market structures are available with customizable sensitivities.

The image above shows the indicator identifying order blocks! Additionally, HH/LH/LL/LH areas are also identified.

The image above shows a rolling area of interest. These areas can be compared to supply/demand zones, where traders might consider a bargain long/short/sell area.

The indicator displays a rolling 4hr high/low and 1D high/low, alongside auto fibonacci levels with a customizable sensitivity.

Finally, the Mxwll Price Action Suite shows relevant session information.

Table information

Current Session

Countdown to session close

Next Session

Countdown to next session open

Rolling 4-Hr volume intensity

Rolling 24-Hr volume intensity

Introducing the Mxwll SMC Suite!

The Mxwll SMC Suite is an all-in-one analysis indicator incorporating elements of SMC and also ideas extending beyond the trading methodology!

Features

Internal structures

External structures

Customizable Sensitivities

BoS/CHoCH

Order Blocks

HH/LH/LL/LH Areas

Rolling TF highs/lows

Rolling Volume Comparisons

Auto Fibs

And more!

The image above shows the indicator's market structure identification capabilities. Internal BoS and CHoCH structures in addition to overarching market structures are available with customizable sensitivities.

The image above shows the indicator identifying order blocks! Additionally, HH/LH/LL/LH areas are also identified.

The image above shows a rolling area of interest. These areas can be compared to supply/demand zones, where traders might consider a bargain long/short/sell area.

The indicator displays a rolling 4hr high/low and 1D high/low, alongside auto fibonacci levels with a customizable sensitivity.

Finally, the Mxwll Price Action Suite shows relevant session information.

Table information

Current Session

Countdown to session close

Next Session

Countdown to next session open

Rolling 4-Hr volume intensity

Rolling 24-Hr volume intensity

Expanded Features of Mxwll Price Action Suite

Internal and External Structures

Internal Structures: These elements refer to the price formations and patterns that occur within a smaller scope or a specific trading session. The suite can detect intricate details like minor support/resistance levels or short-term trend reversals.

External Structures: These involve larger, more significant market patterns and trends spanning multiple sessions or time frames. This capability helps traders understand overarching market directions.

Customizable Sensitivities

Adjusting sensitivity settings allows users to tailor the indicator's responsiveness to market changes. Higher sensitivity can catch smaller fluctuations, while lower sensitivity might focus on more significant, reliable market moves.

Break of Structure (BoS) and Change of Character (CHoCH)

BoS: This feature identifies points where the price breaks a significant structure, potentially indicating a new trend or a trend reversal.

CHoCH: Detects subtle shifts in the market's behavior, which could suggest the early stages of a trend change before they become apparent to the broader market.

Order Blocks and Market Phases

Order Blocks: These are essentially price levels or zones where significant trading activities previously occurred, likely pointing to the positions of smart money.

HH/LH/LL/LH Areas: Identifying Higher Highs (HH), Lower Highs (LH), Lower Lows (LL), and Lower Highs (LH) helps in understanding the trend and market structure, aiding in predictive analysis.

Rolling Timeframe Highs/Lows and Volume Comparisons

Tracks highs and lows over specified rolling periods, providing dynamic support and resistance levels.

Compares volume data across different timeframes to assess the strength or weakness of the current price movements.

Auto Fibonacci Levels

Automatically calculates and plots Fibonacci retracement levels, a popular tool among traders to identify potential reversal points based on past movements.

Session Data and Volume Intensity

Session Information: Displays current and upcoming trading sessions along with countdown timers, which is crucial for day traders and those trading on session overlaps.

Volume Intensity: Measures and compares the volume within the last 4 hours and 24 hours to gauge market activity and potential breakout/breakdown movements.

Visualizations and Practical Use

Dynamic Visuals: The suite provides dynamic visual aids, such as real-time updating of high/low markers and Fibonacci levels, which adjust as new data comes in. This feature is critical in fast-paced markets.

Strategic Entry/Exit Points: By identifying order blocks and using Fibonacci levels, traders can pinpoint strategic entry and exit points, maximizing potential returns.

Risk Management: Enhanced features like session countdowns and volume intensity help in better risk management by providing traders with more data on market sentiment and potential volatility.

Komut dosyalarını "豪24配债" için ara

SOLANA Performance & Volatility Analysis BB%Overview:

The script provides an in-depth analysis of Solana's performance and volatility. It showcases Solana's price, its inverse relationship, its own volatility, and even juxtaposes it against Bitcoin's 24-hour historical volatility. All of these are presented using the Bollinger Bands Percentage (BB%) methodology to normalise the price and volatility values between 0 and 1.

Key Components:

Inputs:

SOLANA PRICE (SOLUSD): The price of Solana.

SOLANA INVERSE (SOLUSDT.3S): The inverse of Solana's price.

SOLANA VOLATILITY (SOLUSDSHORTS): Volatility for Solana.

BITCOIN 24 HOUR HISTORICAL VOLATILITY (BVOL24H): Bitcoin's volatility over the past 24 hours.

BB Calculations:

The script uses the Bollinger Bands methodology to calculate the mean (SMA) and the standard deviation of the prices and volatilities over a certain period (default is 20 periods). The calculated upper and lower bands help in normalising the values to the range of 0 to 1.

Normalised Metrics Plotting:

For better visualisation and comparative analysis, the normalised values for:

Solana Price

Solana Inverse

Solana Volatility

Bitcoin 24hr Volatility

are plotted with steplines.

Band Plotting:

Bands are plotted at 20%, 40%, 60%, and 80% levels to serve as reference points. The area between the 40% and 60% bands is shaded to highlight the median region.

Colour Coding:

Different colours are used for easy differentiation:

Solana Price: Blue

Solana Inverse: Red

Solana Volatility: Green

Bitcoin 24hr Volatility: White

Licence & Creator:

The script adheres to the Mozilla Public Licence 2.0 and is credited to the author, "Volatility_Vibes".

Works well with Breaks and Retests with Volatility Stop

Futures Exchange SessionsIn the 24-hour trading of the futures market, this indicator provides the user with full customization concerning the most important factor: time. This indicator is centered around three main visualizations: labels, backgrounds, and lines that minimalistically allows the user to keep track of the many time intervals that occur during a futures market 24-hour trading cycle. It also artfully displays the previous days highs and lows. And everything can be individually toggled and configured so the user can get exactly what they want.

Labels

There are three main futures market sessions in a 24-hour period: the London, New York, and Asian Sessions. Each session is given an independent label for the open and close times. The six labels (LO, LC, NYO, NYC, AO, AC) can be individually toggled on or off, the label background color changed, the text switched between black or white, and the height can be lowered or raised. These customizations are intended to give the user full control of the session they are interested in at the moment.

Backgrounds

Backgrounds are the heart of this indicator. There are different colored transparent backgrounds for each of the futures sessions. So the user can clearly see the session they want to highlight without cluttering their chart and getting in the way of analyzing the candles.

If you are familiar with the London and New York killzones, these backgrounds are each individually configured.

If you are familiar with the Inner Circle Trader’s (ICT) NY Morning and Afternoon sessions, these are available. Also, most times weird price action occurs during the lunch hour of these sessions. The London and New York have a background for their respective lunch hours so the user is never caught of guard during these periods.

Lines

The markets are constantly looking for liquidity. To help the user see runs on liquidity, this indicator projects the previous days highs and lows on to the current day with a line and a price label. The line make it very easy to see where price may be headed. See the image below for the perfect example of this phenomenon. Each of the lines can be independently controlled by color, style, and width. And even the labels can be toggled on or off if the user would prefer just to see the lines. Lastly, there is a line that marks the midnight open price in EST.

Special Notes

This indicator is specifically designed for futures tickers.

All of the backgrounds are not designed to be turned on a once (there are many that overlap). They are designed to give the user ultimate control over exactly what timeframe backgrounds to display on their charts.

The labels only appear when timeframe is 1 hour or less.

Relative Volume (rVol), Better Volume, Average Volume ComparisonThis is the best version of relative volume you can find a claim which is based on the logical soundness of its calculation.

I have amalgamated various volume analysis into one synergistic script. I wasn't going to opensource it. But, as one of the lucky few winners of TradingClue 2. I felt obligated to give something back to the community.

Relative volume traditionally compares current volume to prior bar volume or SMA of volume. This has drawbacks. The question of relative volume is "Volume relative to what?" In the traditional scripts you'll find it displays current volume relative to the last number of bars. But, is that the best way to compare volume. On a daily chart, possibly. On a daily chart this can work because your units of time are uniform. Each day represents a full cycle of volume. However, on an intraday chart? Not so much.

Example: If you have a lookback of 9 on an hourly chart in a 24 hour market, you are then comparing the average volume from Midnight - 9 AM to the 9 AM volume. What do you think you'll find? Well at 9:30 when NY exchanges open the volume should be consistently and predictably higher. But though rVol is high relative to the lookback period, its actually just average or maybe even below average compared to prior NY session opens. But prior NY session opens are not included in the lookback and thus ignored.

This problem is the most visibly noticed when looking at the volume on a CME futures chart or some equivalent. In a 24 hour market, such as crypto, there are website's like skew can show you the volume disparity from time of day. This led me to believe that the traditional rVol calculation was insufficient. A better way to calculate it would be to compare the 9:30 am 30m bar today to the last week's worth of 9:30 am 30m bars. Then I could know whether today's volume at 9:30 am today is high or low based on prior 9:30 am bars. This seems to be a superior method on an intraday basis and is clearly superior in markets with irregular volume

This led me to other problems, such as markets that are open for less than 24 hours and holiday hours on traditional market exchanges. How can I know that the script is accurately looking at the correct prior relevant bars. I've created and/or adapted solutions to all those problems and these calculations and code snippets thus have value that extend beyond this rVol script for other pinecoders.

The Script

This rVol script looks back at the bars of the same time period on the viewing timeframe. So, as we said, the last 9:30 bars. Averages those, then divides the: . The result is a percentage expressed as x.xxx. Thus 1.0 mean current volume is equal to average volume. Below 1.0 is below the average and above 1.0 is above the average.

This information can be viewed on its own. But there are more levels of analysis added to it.

Above the bars are signals that correlate to the "Better Volume Indicator" developed by, I believe, the folks at emini-watch and originally adapted to pinescript by LazyBear. The interpretation of these symbols are in a table on the right of the indicator.

The volume bars can also be colored. The color is defined by the relationship between the average of the rVol outputs and the current volume. The "Average rVol" so to speak. The color coding is also defined by a legend in the table on the right.

These can be researched by you to determine how to best interpret these signals. I originally got these ideas and solid details on how to use the analysis from a fellow out there, PlanTheTrade.

I hope you find some value in the code and in the information that the indicator presents. And I'd like to thank the TradingView team for producing the most innovative and user friendly charting package on the market.

(p.s. Better Volume is provides better information with a longer lookback value than the default imo)

Credit for certain code sections and ideas is due to:

LazyBear - Better Volume

Grimmolf (From GitHub) - Logic for Loop rVol

R4Rocket - The idea for my rVol 1 calculation

And I can't find the guy who had the idea for the multiples of volume to the average. Tag him if you know him

Final Note: I'd like to leave a couple of clues of my own for fellow seekers of trading infamy.

Indicators: indicators are like anemometers (The things that measure windspeed). People talk bad about them all the time because they're "lagging." Well, you can't tell what the windspeed is unless the wind is blowing. anemometers are lagging indicators of wind. But forecasters still rely on them. You would use an indicator, which I would define as a instrument of measure, to tell you the windspeed of the markets. Conversely, when people talk positively about indicators they say "This one is great and this one is terrible." This is like a farmer saying "Shovels are great, but rakes are horrible." There are certain tools that have certain functions and every good tool has a purpose for a specific job. So the next time someone shares their opinion with you about indicators. Just smile and nod, realizing one day they'll learn... hopefully before they go broke.

How to forecast: Prediction is accomplished by analyzing the behavior of instruments of measure to aggregate data (using your anemometer). The data is then assembled into a predictive model based on the measurements observed (a trading system). That predictive model is tested against reality for it's veracity (backtesting). If the model is predictive, you can optimize your decision making by creating parameter sets around the prediction that are synergistic with the implications of the prediction (risk, stop loss, target, scaling, pyramiding etc).

<3

Advanced Volume ProfileTHIS SCRIPT CURRENTLY ONLY WORKS FOR ASSETS THAT TRADE 24/7 OR CBOE FUTURES HOURS!

This script plots volume relative to an asset's historical volume profile.

Usage:

As a companion to my "Unusual Time Frame Volume" (UTF Volume) script, this plots volume against the same historical volume profile used for UTF Volume.

The same high volume (relative to historical) threshold alert is available (yellow bar).

Likewise, if the volume exceeds the historical threshold, but is below the alert threshold, the bar color is orange.

At the top of the chart is an indicator which is green if a bar has higher volume than the previous bar.

You can also set a threshold for this such that if the volume of a bar exceeds the previous bar by a certain multiplier which will turn the indicator yellow.

For example, if the threshold is set to "1.5", then the indicator will be yellow (instead of green) on an increase in volume over the previous bar of 1.5x.

NOTES:

Again, this script currently only works for assets that trade 24/7 or CBOE Futures hours!

Make sure you set the "Asset Mode" and "Time Frame (minutes)" to values that match your asset and chart setting.

For example, if you are trading Futures on a 2m chart, set the Asset Mode to Futures and Time Frame to 2m.

If you are trading crypto on a 5m chart, set the Asset Mode to 24/7 and Time Frame to 5m.

If the settings are not set appropriately, the output will be incorrect/invalid.

If you choose a "Look-back (Days)" setting that is too far back given the time frame, the script will produce an error.

I suggest playing with settings from "1" (compares volume to the previous day's volume) to the highest number that doesn't break the script.

For example, at a 2m time frame, the maximum look-back will be "6" or "7" depending on which mode you are using.

Longer chart time settings allow larger look-back values.

I find that the default value ("6") does a decent job in general.

Please feel free to reuse or further develop this script.

I would greatly appreciate it if you would send me a message below if you find it useful.

Bar Balance [LucF]Bar Balance extracts the number of up, down and neutral intrabars contained in each chart bar, revealing information on the strength of price movement. It can display stacked columns representing raw up/down/neutral intrabar counts, or an up/down balance line which can be calculated and visualized in many different ways.

WARNING: This is an analysis tool that works on historical bars only. It does not show any realtime information, and thus cannot be used to issue alerts or for automated trading. When realtime bars elapse, the indicator will require a browser refresh, a change to its Inputs or to the chart's timeframe/symbol to recalculate and display information on those elapsed bars. Once a trader understands this, the indicator can be used advantageously to make discretionary trading decisions.

Traders used to work with my Delta Volume Columns Pro will feel right at home in this indicator's Inputs . It has lots of options, allowing it to be used in many different ways. If you value the bar balance information this indicator mines, I hope you will find the time required to master the use of Bar Balance well worth the investment.

█ OVERVIEW

The indicator has two modes: Columns and Line .

Columns

• In Columns mode you can display stacked Up/Down/Neutral columns.

• The "Up" section represents the count of intrabars where `close > open`, "Down" where `close < open` and "Neutral" where `close = open`.

• The Up section always appears above the centerline, the Down section below. The Neutral section overlaps the centerline, split halfway above and below it.

The Up and Down sections start where the Neutral section ends, when there is one.

• The Up and Down sections can be colored independently using 7 different methods.

• The signal line plotted in Line mode can also be displayed in Columns mode.

Line

• Displays a single balance line using a zero centerline.

• A variable number of independent methods can be used to calculate the line (6), determine its color (5), and color the fill (5).

You can thus evaluate the state of 3 different components with this single line.

• A "Divergence Levels" feature will use the line to automatically draw expanding levels on divergence events.

Features available in both modes

• The color of all components can be selected from 15 base colors, with 16 gradient levels used for each base color in the indicator's gradients.

• A zero line can show a 6-state aggregate value of the three main volume balance modes.

• The background can be colored using any of 5 different methods.

• Chart bars can be colored using 5 different methods.

• Divergence and large neutral count ratio events can be shown in either Columns or Line mode, calculated in one of 4 different methods.

• Markers on 6 different conditions can be displayed.

█ CONCEPTS

Intrabar inspection

Intrabar inspection means the indicator looks at lower timeframe bars ( intrabars ) making up a given chart bar to gather its information. If your chart is on a 1-hour timeframe and the intrabar resolution determined by the indicator is 5 minutes, then 12 intrabars will be analyzed for each chart bar and the count of up/down/neutral intrabars among those will be tallied.

Bar Balances and calculation methods

The indicator uses a variety of methods to evaluate bar balance and to derive other calculations from them:

1. Balance on Bar : Uses the relative importance of instant Up and Down counts on the bar.

2. Balance Averages : Uses the difference between the EMAs of Up and Down counts.

3. Balance Momentum : Starts by calculating, separately for both Up and Down counts, the difference between the same EMAs used in Balance Averages and an SMA of double the period used for the EMAs. These differences are then aggregated and finally, a bounded momentum of that aggregate is calculated using RSI.

4. Markers Bias : It sums the bull/bear occurrences of the four previous markers over a user-defined period (the default is 14).

5. Combined Balances : This is the aggregate of the instant bull/bear bias of the three main bar balances.

6. Dual Up/Down Averages : This is a display mode showing the EMA calculated for each of the Up and Down counts.

Interpretation of neutral intrabars

What do neutral intrabars mean? When price does not change during a bar, it can be because there is simply no interest in the market, or because of a perfect balance between buyers and sellers. The latter being more improbable, Bar Balance assumes that neutral bars reveal a lack of interest, which entails uncertainty. That is the reason why the option is provided to interpret ratios of neutral intrabars greater than 50% as divergences. It is also the rationale behind the option to dampen signal lines on the inverse ratio of neutral intrabars, so that zero intrabars do not affect the signal, and progressively larger proportions of neutral intrabars will reduce the signal's amplitude, as the balance calcs using the up/down counts lose significance. The impact of the dampening will vary with markets. Weaker markets such as cryptos will often contain greater numbers of neutral intrabars, so dampening the Line in that sector will have a greater impact than in more liquid markets.

█ FEATURES

1 — Columns

• While the size of the Up/Down columns always represents their respective importance on the bar, their coloring mode is independent. The default setup uses a standard coloring mode where the Up/Down columns over/under the zero line are always in the bull/bear color with a higher intensity for the winning side. Six other coloring modes allow you to pack more information in the columns. When choosing to color the top columns using a bull/bear gradient on Balance Averages, for example, you will end up with bull/bear colored tops. In order for the color of the bottom columns to continue to show the instant bar balance, you can then choose the "Up/Down Ratio on Bar — Dual Solid Colors" coloring mode to make those bars the color of the winning side for that bar.

• Line mode shows only the line, but Columns mode allows displaying the line along with it. If the scale of the line is different than that of the scale of the columns, the line will often appear flat. Traders may find even a flat line useful as its bull/bear colors will be easily distinguishable.

2 — Line

• The default setup for Line mode uses a calculation on "Balance Momentum", with a fill on the longer-term "Balance Averages" and a line color based on the "Markers Bias". With the background set on "Line vs Divergence Levels" and the zero line on the hard-coded "Combined Bar Balances", you have access to five distinct sources of information at a glance, to which you can add divergences, divergences levels and chart bar coloring. This provides powerful potential in displaying bar balance information.

• When no columns are displayed, Line mode can show the full scale of whichever line you choose to calculate because the columns' scale no longer interferes with the line's scale.

• Note that when "Balance on Bar" is selected, the Neutral count is also displayed as a ratio of the balance line. This is the only instance where the Neutral count is displayed in Line mode.

• The "Dual Up/Down Averages" is an exception as it displays two lines: one average for the Up counts and another for the Down counts. This mode will be most useful when Columns are also displayed, as it provides a reference for the top and bottom columns.

3 — Zero Line

The zero line can be colored using two methods, both based on the Combined Balances, i.e., the aggregate of the instant bull/bear bias of the three main bar balances.

• In "Six-state Dual Color Gradient" mode, a dot appears on every bar. Its color reflects the bull/bear state of the Combined Balances, and the dot's brightness reflects the tally of balance biases.

• In "Dual Solid Colors (All Bull/All Bear Only)" a dot only appears when all three balances are either bullish or bearish. The resulting pattern is identical to that of Marker 1.

4 — Divergences

• Divergences are displayed as a small circle at the top of the scale. Four different types of divergence events can be detected. Divergences occur whenever the bull/bear bias of the method used diverges with the bar's price direction.

• An option allows you to include in divergence events instances where the count of neutral intrabars exceeds 50% of the total intrabar count.

• The divergence levels are dynamic levels that automatically build from the line's values on divergence events. On consecutive divergences, the levels will expand, creating a channel. This implementation of the divergence levels corresponds to my view that divergences indicate anomalies, hesitations, points of uncertainty if you will. It excludes any association of a pre-determined bullish/bearish bias to divergences. Accordingly, the levels merely take note of divergence events and mark those points in time with levels. Traders then have a reference point from which they can evaluate further movement. The bull/bear/neutral colors used to plot the levels are also congruent with this view in that they are determined by price's position relative to the levels, which is how I think divergences can be put to the most effective use.

5 — Background

• The background can show a bull/bear gradient on four different calculations. You can adjust its brightness to make its visual importance proportional to how you use it in your analysis.

6 — Chart bars

• Chart bars can be colored using five different methods.

• You have the option of emptying the body of bars where volume does not increase, as does my TLD indicator, the idea behind this being that movement on bars where volume does not increase is less relevant.

7 — Intrabar Resolution

You can choose between three modes. Two of them are automatic and one is manual:

a) Fast, Longer history, Auto-Steps (~12 intrabars) : Optimized for speed and deeper history. Uses an average minimum of 12 intrabars.

b) More Precise, Shorter History Auto-Steps (~24 intrabars) : Uses finer intrabar resolution. It is slower and provides less history. Uses an average minimum of 24 intrabars.

c) Fixed : Uses the fixed resolution of your choice.

Auto-Steps calculations vary for 24/7 and conventional markets in order to achieve the proper target of minimum intrabars.

You can choose to view the intrabar resolution currently used to calculate delta volume. It is the default.

The proper selection of the intrabar resolution is important. It must achieve maximal granularity to produce precise results while not unduly slowing down calculations, or worse, causing runtime errors.

8 — Markers

Six markers are available:

1. Combined Balances Agreement : All three Bar Balances are either bullish or bearish.

2. Up or Down % Agrees With Bar : An up marker will appear when the percentage of up intrabars in an up chart bar is greater than the specified percentage. Conditions mirror to down bars.

3. Divergence confirmations By Price : One of the four types of balance calculations can be used to detect divergences with price. Confirmations occur when the bar following the divergence confirms the balance bias. Note that the divergence events used here do not include neutral intrabar events.

4. Balance Transitions : Bull/bear transitions of the selected balance.

5. Markers Bias Transitions : Bull/bear transitions of the Markers Bias.

6. Divergence Confirmations By Line : Marks points where the line first breaches a divergence level.

Markers appear when the condition is detected, without delay. Since nothing is plotted in realtime, markers do not appear on the realtime bar.

9 — Settings

• Two modes can be selected to dampen the line on the ratio of neutral intrabars.

• A distinct weight can be attributed to the count of the latter half of intrabars, on the assumption that later intrabars may be more important in determining the outcome of chart bars.

• Allows control over the periods of the different moving averages used in calculations.

• The default periods used for the various calculations define the following hierarchy from slow to fast:

Balance Averages: 50,

Balance Momentum: 20,

Dual Up/Down Averages: 20,

Marker Bias: 10.

█ LIMITATIONS

• This script uses a special characteristic of the `security()` function allowing the inspection of intrabars—which is not officially supported by TradingView.

• The method used does not work on the realtime bar—only on historical bars.

• The indicator only works on some chart resolutions: 3, 5, 10, 15 and 30 minutes, 1, 2, 4, 6, and 12 hours, 1 day, 1 week and 1 month. The script’s code can be modified to run on other resolutions, but chart resolutions must be divisible by the lower resolution used for intrabars and the stepping mechanism could require adaptation.

• When using the "Line vs Divergence Levels — Dual Color Gradient" color mode to fill the line, background or chart bars, keep in mind that a line calculation mode must be defined for it to work, as it determines gradients on the movement of the line relative to divergence levels. If the line is hidden, it will not work.

• When the difference between the chart’s resolution and the intrabar resolution is too great, runtime errors will occur. The Auto-Steps selection mechanisms should avoid this.

• Alerts do not work reliably when `security()` is used at intrabar resolutions. Accordingly, no alerts are configured in the indicator.

• The color model used in the indicator provides for fancy visuals that come at a price; when you change values in Inputs , it can take 20 seconds for the changes to materialize. Luckily, once your color setup is complete, the color model does not have a large performance impact, as in normal operation the `security()` calls will become the most important factor in determining response time. Also, once in a while a runtime error will occur when you change inputs. Just making another change will usually bring the indicator back up.

█ RAMBLINGS

Is this thing useful?

I'll let you decide. Bar Balance acts somewhat like an X-Ray on bars. The intrabars it analyzes are no secret; one can simply change the chart's resolution to see the same intrabars the indicator uses. What the indicator brings to traders is the precise count of up/down/neutral intrabars and, more importantly, the calculations it derives from them to present the information in a way that can make it easier to use in trading decisions.

How reliable is Bar Balance information?

By the same token that an up bar does not guarantee that more up bars will follow, future price movements cannot be inferred from the mere count of up/down/neutral intrabars. Price movement during any chart bar for which, let's say, 12 intrabars are analyzed, could be due to only one of those intrabars. One can thus easily see how only relying on bar balance information could be very misleading. The rationale behind Bar Balance is that when the information mined for multiple chart bars is aggregated, it can provide insight into the history behind chart bars, and thus some bias as to the strength of movements. An up chart bar where 11/12 intrabars are also up is assumed to be stronger than the same up bar where only 2/12 intrabars are up. This logic is not bulletproof, and sometimes Bar Balance will stray. Also, keep in mind that balance lines do not represent price momentum as RSI would. Bar Balance calculations have no idea where price is. Their perspective, like that of any historian, is very limited, constrained that it is to the narrow universe of up/down/neutral intrabar counts. You will thus see instances where price is moving up while Balance Momentum, for example, is moving down. When Bar Balance performs as intended, this indicates that the rally is weakening, which does necessarily imply that price will reverse. Occasionally, price will merrily continue to advance on weakening strength.

Divergences

Most of the divergence detection methods used here rely on a difference between the bias of a calculation involving a multi-bar average and a given bar's price direction. When using "Bar Balance on Bar" however, only the bar's balance and price movement are used. This is the default mode.

As usual, divergences are points of interest because they reveal imbalances, which may or may not become turning points. I do not share the overwhelming enthusiasm traders have for the purported ability of bullish/bearish divergences to indicate imminent reversals.

Superfluity

In "The Bed of Procrustes", Nassim Nicholas Taleb writes: To bankrupt a fool, give him information . Bar Balance can display lots of information. While learning to use a new indicator inevitably requires an adaptation period where we put it through its paces and try out all its options, once you have become used to Bar Balance and decide to adopt it, rigorously eliminate the components you don't use and configure the remaining ones so their visual prominence reflects their relative importance in your analysis. I tried to provide flexible options for traders to control this indicator's visuals for that exact reason—not for window dressing.

█ NOTES

For traders

• To avoid misleading traders who don't read script descriptions, the indicator shows nothing in the realtime bar.

• The Data Window shows key values for the indicator.

• All gradients used in this indicator determine their brightness intensities using advances/declines in the signal—not their relative position in a fixed scale.

• Note that because of the way gradients are optimized internally, changing their brightness will sometimes require bringing down the value a few steps before you see an impact.

• Because this indicator does not use volume, it will work on all markets.

For coders

• For those interested in gradients, this script uses an advanced version of the Advance/Decline gradient function from the PineCoders Color Gradient (16 colors) Framework . It allows more precise control over the range, steps and min/max values of the gradients.

• I use the PineCoders Coding Conventions for Pine to write my scripts.

• I used functions modified from the PineCoders MTF Selection Framework for the selection of timeframes.

█ THANKS TO:

— alexgrover who helped me think through the dampening method used to attenuate signal lines on high ratios of neutral intrabars.

— A guy called Kuan who commented on a Backtest Rookies presentation of their Volume Profile indicator . The technique I use to inspect intrabars is derived from Kuan's code.

— theheirophant , my partner in the exploration of the sometimes weird abysses of `security()`’s behavior at intrabar resolutions.

— midtownsk8rguy , my brilliant companion in mining the depths of Pine graphics. He is also the co-author of the PineCoders Color Gradient Frameworks .

Price Action and 3 EMAs Momentum plus Sessions FilterThis indicator plots on the chart the parameters and signals of the Price Action and 3 EMAs Momentum plus Sessions Filter Algorithmic Strategy. The strategy trades based on time-series (absolute) and relative momentum of price close, highs, lows and 3 EMAs.

I am still learning PS and therefore I have only been able to write the indicator up to the Signal generation. I plan to expand the indicator to Entry Signals as well as the full Strategy.

The strategy works best on EURUSD in the 15 minutes TF during London and New York sessions with 1 to 1 TP and SL of 30 pips with lots resulting in 3% risk of the account per trade. I have already written the full strategy in another language and platform and back tested it for ten years and it was profitable for 7 of the 10 years with average profit of 15% p.a which can be easily increased by increasing risk per trade. I have been trading it live in that platform for over two years and it is profitable.

Contributions from experienced PS coders in completing the Indicator as well as writing the Strategy and back testing it on Trading View will be appreciated.

STRATEGY AND INDICATOR PARAMETERS

Three periods of 12, 48 and 96 in the 15 min TF which are equivalent to 3, 12 and 24 hours i.e (15 min * period / 60 min) are the foundational inputs for all the parameters of the PA & 3 EMAs Momentum + SF Algo Strategy and its Indicator.

3 EMAs momentum parameters and conditions

• FastEMA = ema of 12 periods

• MedEMA = ema of 48 periods

• SlowEMA = ema of 96 periods

• All the EMAs analyse price close for up to 96 (15 min periods) equivalent to 24 hours

• There’s Upward EMA momentum if price close > FastEMA and FastEMA > MedEMA and MedEMA > SlowEMA

• There’s Downward EMA momentum if price close < FastEMA and FastEMA < MedEMA and MedEMA < SlowEMA

PA momentum parameters and conditions

• HH = Highest High of 48 periods from 1st closed bar before current bar

• LL = Lowest Low of 48 periods from 1st closed bar from current bar

• Previous HH = Highest High of 84 periods from 12th closed bar before current bar

• Previous LL = Lowest Low of 84 periods from 12th closed bar before current bar

• All the HH & LL and prevHH & prevLL are within the 96 periods from the 1st closed bar before current bar and therefore indicative of momentum during the past 24 hours

• There’s Upward PA momentum if price close > HH and HH > prevHH and LL > prevLL

• There’s Downward PA momentum if price close < LL and LL < prevLL and HH < prevHH

Signal conditions and Status (BuySignal, SellSignal or Neutral)

• The strategy generates Buy or Sell Signals if both 3 EMAs and PA momentum conditions are met for each direction and these occur during the London and New York sessions

• BuySignal if price close > FastEMA and FastEMA > MedEMA and MedEMA > SlowEMA and price close > HH and HH > prevHH and LL > prevLL and timeinrange (LDN&NY) else Neutral

• SellSignal if price close < FastEMA and FastEMA < MedEMA and MedEMA < SlowEMA and price close < LL and LL < prevLL and HH < prevHH and timeinrange (LDN&NY) else Neutral

Entry conditions and Status (EnterBuy, EnterSell or Neutral)(NOT CODED YET)

• ENTRY IS NOT AT THE SIGNAL BAR but at the current bar tick price retracement to FastEMA after the signal

• EnterBuy if current bar tick price <= FastEMA and current bar tick price > prevHH at the time of the Buy Signal

• EnterSell if current bar tick price >= FastEMA and current bar tick price > prevLL at the time of the Sell Signal

[BTX] Triple TRIX + MAsThis indicator suggest a strategy, which is quite similar to multiple MA or multiple RSI strategies.

This indicator can be used for all timeframes, all markets.

This indicator can help detect the market trend and momentum.

Default values are TRIX - 6, 12, and 24 periods and MA(8) for each TRIX line. You can choose what type of MA to be used (EMA or SMA).

How to exploit this indicator?

- When all of the lower TRIXs are ABOVE the higher one: TRIX(6) is above TRIX(12), and TRIX(12) is above TRIX(24), there is a BULLISH market.

- When all of the lower TRIXs are BELOW the higher one: TRIX(6) is below TRIX(12), and TRIX(12) is below TRIX(24), there is a BEARISH market.

- A crossover of the lower TRIX to the higher one indicates a BUY signal.

- A crossunder of the lower TRIX to the higher one indicates a SELL signal.

- TRIX crossover the Zero line can be considered as a STRONG bullish signal.

- TRIX crossunder the Zero line can be considered as a STRONG bearish signal.

- The MA of TRIX acts as a confirmation, it can be used as SELL signals.

- High slopes of TRIX lines can point out the high momentum of the current trend.

- Divergence patterns can be used with this indicator.

- And many more tricks.

MTF CMO (Chande Momentum Oscillator)Simple Multi-Timeframe version of the Chande Momentum Oscillator . Many thanks to HPotter whos script I used as a starting point. This displays 1, 2, 3, 4, and 24 period CMOs on the graph. 1, 2, 3, and 4 periods are smoothed by using their simple moving averages. 24 period is unsmoothed. I prefer to set my chart to a 1 hour timeframe and look for bottoming or topping patterns in the momentum. Strongest topping or bottoming patterns are when all timeframes roll over including the 24 period.

Ease of Movement WatcherHere’s a handy Ease of Movement(EMV) Indicator. I tried to include detailed comments so that anyone that’s learning pine can follow along.

The Ease of Movement Indicator is a volume based oscillator that is designed to measure the ease (or movability) of price movement for a security. The EMV is a centered oscillator, meaning that values can fluctuate above and below zero.

To understand how to use and interpret the EMV Indicator, its crucial to first understand its two main calculations :

Distance Moved = ((high + low) / 2) - ((high + low ) / 2)

-This is the difference between the current period’s midpoint and the previous period’s

midpoint.

Box Ratio = (volume / 100,000) / (high - low)

-When calculating the Box Ratio, it is common to divide the volume by 100,000 for a clearer visualization of the data. However, users can choose

to modify this value with the ‘volumeDiv’ input.

The Ease of Movement Value is then pretty simple to calculate:

EMV = (Distance Moved / Box Ratio)

The indicator then plots a SMA of the previous 24 EMV Values.

Looking at the formula, we know that combining low volume with a large {high, low} range will result in a relatively small box ratio value. Thus, we know that the EMV value for that period will be higher since EMV is found by dividing the Distance Moved by the Box Ratio.

Here’s a simple guide to interpreting the EMV:

- If (EMV > 0)

then price is increasing with relative ease.

-If (EMV < 0)

then price is decreasing with relative ease.

- If high-low range is large and volume is low

then ease of movement is high.

-If high-low range is small and volume is high

then ease of movement is low.

The Chart:

-The histogram represents the Simple Moving Average of EMV Values. The default length is 24, but users can adjust this value at the inputs menu(I've

found 24 works best).

-The teal and pink dotted lines represent the standard deviation of the SMA of EMV values multiplied by 2.5.

-The histogram turns dark green when the EMV SMA is greater than the top teal dotted standard deviations line.

-The histogram turns maroon when the EMV SMA falls below the bottom pink standard deviation line.

How To Use:

Enter a long position when the most recent EMV SMA value was below the lower pink stand. dev. line and the current EMV SMA value rises above that

same pink line. That means the previous bar was maroon and the current bar is not.

If the user enables the option to show entry points, a green dot will be plotted when it is time to enter a long position.

Exit the long position when the most recent EMV SMA value was above the upper green standard deviation line and the current EMV SMA value falls

below that same line. If this is true, then the previous bar will be dark green, and the current will be light green.

If the ‘showExits’ option is enabled, then a red dot will be plotted when it is time to exit the long position.

Input Options:

- 'volumeDiv' : Integer. Used in the calculation of Box Ratio.

- 'lenSMA' : Integer. The length of the Simple Moving Average of Ease of Movement Values.

- 'showStDev' : Bool. If true, dotted green and red lines will be shown at values equal to 2.5 * standard deviation of emvSMA and -2.5 * standard deviation of

emvSMA.

- 'showEntries' and 'showExits' : Bool. If true, a green circle will be plotted at long entry points and a red circle will be plotted at long exit points.

- 'changeBgColor': Bool. If true, the background color will change to green when it is time to enter a long position and red when it is time to exit.

Alerts:

- When it is time to enter a long position, an alert with the message "EMV Tracker - Enter Long" is sent.

- When it is time to exit a long position, an alert with the message "EMV Tracker - Exit Long" is sent.

NOTE:

- I usually use this indicator to confirm signals from other indicators rather than relying on it solely.

- Most accurate signals are generated on 30 minutes with the default input values I've set in the script.

Shoot me a message if you have any ideas for modifications or questions.

~ Happy Trading ~

The Daily Bias Dashboard📜 Overview

This indicator is a powerful statistical tool designed to provide traders with a probable Daily Bias based on historical price action. It is built upon the concepts of Quarterly Theory, which divides the 24-hour trading day into 4 distinct sessions to analyze market behavior.

This tool analyzes how the market has behaved in the past to give you a statistical edge. It answers the question: "Based on the last X number of days, what is the most likely way the price will move during the Newyork AM & PM Sessions based on Asian & London Sessions?"

⚙️ How It Works

The indicator divides the 24-hour day (based on the America/New_York timezone) into two 12-hour halves:

First Half - 12 Hour Candle: The Accumulation/Manipulation or Asian/London Sessions (6 PM to 6 AM NY Time)

This period covers the Asian session and the start of the London session.

The indicator's only job here is to identify the highest high and lowest low of this 12-hour block, establishing the initial daily range.

Second Half - 12 Hour Candle: The Distribution/Continuation or NY AM/PM Sessions (6 AM to 6 PM NY Time)

This period covers the main London session and the full New York session.

The indicator actively watches to see if, and in what order, the price breaks out of the range established in Session 1 (FIrst Half of the day).

By tracking this behavior over hundreds of days, the indicator compiles statistics on four possible daily scenarios.

📊 The Four Scenarios & The Dashboard

The indicator presents its findings in a clean, easy-to-read dashboard, calculating the historical probability of each of the following scenarios:

↓ Low, then ↑ High: The price first breaks the low of Session 1 (often a liquidity sweep or stop hunt) before reversing to break the high of Session 1. This suggests a "sweep and reverse" bullish day.

↑ High, then ↓ Low: The price first breaks the high of Session 1 before reversing to break the low of Session 1. This suggests a "sweep and reverse" bearish day.

One-Sided Breakout: The price breaks only one of the boundaries (either the high or the low) and continues in that direction without taking the other side. This indicates a strong, trending day.

No Breakout (Inside Bar): The price fails to break either the high or the low of Session 1, remaining contained within its range. This indicates a day of consolidation and low volatility.

🧠 How to Use This Indicator

This is a confluence tool, not a standalone trading system. Its purpose is to help you frame a high-probability narrative for the trading day.

Establish a Bias: Start checking the dashboard at 06:00 AM Newyork time, which is the start of next half day trading session. If one scenario has a significantly higher probability (e.g., "One-Sided Breakout" at 89%), you have a statistically-backed directional bias in the direction of Breakout.

🔧 Features & Settings

Historical Days to Analyze: Set how many past days the indicator should use for its statistical analysis (default is 500).

Session Timezone : The calculation is locked to America/New_York as it is central to the Quarterly Theory concept, but this setting ensures correct alignment.

Dashboard Display: Fully customize the on-screen table, including its position and text size, or hide it completely.

⚠️ Important Notes

For maximum accuracy, use this indicator on hourly (H1) or lower timeframes.

The statistical probabilities are based on past performance and are not a guarantee of future results.

This tool is designed to sharpen your analytical skills and provide a robust, data-driven framework for your daily trading decisions. Use it to build confidence in your directional bias and to better understand the rhythm of the market.

Disclaimer: This indicator is for educational and informational purposes only and does not constitute financial advice. All trading involves risk.

Return Volatility (σ) — auto-annualized [v6]Overview

This indicator calculates and visualizes the return-based volatility (standard deviation) of any asset, automatically adjusting for your chart's timeframe to provide both absolute and annualized volatility values.

It’s designed for traders who want to filter trades, adjust position sizing, and detect volatility events based on statistically significant changes in market activity.

Key Features

Absolute Volatility (abs σ%) – Standard deviation of returns for the current timeframe (e.g., 1H, 4H, 1D).

Annualized Volatility (ann σ%) – Converts abs σ% into an annualized figure for easier cross-timeframe and cross-asset comparison.

Relative Volatility (rel σ) – Ratio of current volatility to the long-term average (default: 120 periods).

Z-Score – Number of standard deviations the current volatility is above or below its historical average.

Auto-Timeframe Adjustment – Detects your chart’s bar size (seconds per bar) and calculates bars/year automatically for crypto’s 24/7 market.

Highlight Mode – Optional yellow background when volatility exceeds set thresholds (rel σ ≥ threshold OR z-score ≥ threshold).

Alert Conditions – Alerts trigger when relative volatility or z-score exceed defined limits.

How It Works

Return Calculation

Log returns: ln(Pt / Pt-1) (default)

or Simple returns: (Pt / Pt-1) – 1

Volatility Measurement

Standard deviation of returns over the lookback period N (default: 20 bars).

Absolute volatility = σ × 100 (% per bar).

Annualization

Uses: σₐₙₙ = σ × √(bars/year) × 100 (%)

Bars/year auto-calculated based on timeframe:

1H = 8,760 bars/year

4H ≈ 2,190 bars/year

1D = 365 bars/year

Relative and Statistical Context

Relative σ = Current σ / Historical average σ (baseLen, default: 120)

Z-score = (Current σ – Historical average σ) / Std. dev. of σ over baseLen

Trading Applications

Volatility Filter – Only allow trade entries when volatility exceeds historical norms (trend traders often benefit from this).

Risk Management – Reduce position size during high volatility spikes to manage risk; increase size in low-volatility trending environments.

Market Scanning – Identify assets with the highest relative volatility for momentum or breakout strategies.

Event Detection – Highlight significant volatility surges that may precede large moves.

Suggested Settings

Lookback (N): 20 bars for short/medium-term trading.

Base Length (M): 120 bars to establish long-term volatility baseline.

Relative Threshold: 1.5× baseline σ.

Z-score Threshold: ≥ 2.0 for statistically significant volatility shifts.

Use Log Returns: Recommended for more consistent scaling across prices.

Notes & Limitations

Volatility measures movement magnitude, not direction. Combine with trend or momentum filters for directional bias.

Very low volatility may still produce false breakouts; combine with volume and market structure analysis.

Crypto markets trade 24/7 — annualization assumes no market closures; adjust for other asset classes if needed.

💡 Best Practice: Use this indicator as a pre-trade filter for breakout or trend-following strategies, or as a risk control overlay in mean-reversion systems.

Tradeable Candle Detection By Raja SaienTradeable Candle Detection By Raja Saien

Overview:

This advanced candle detection tool is designed to help traders identify high-quality trade setups and avoid fake moves, based on candle structure, volume, and RSI conditions. Unlike many indicators that are limited to specific sessions, this script works across all market sessions, giving you full flexibility to trade 24/7.

🔍 Key Features:

All Session Support (24/7 Trading)

Detects tradeable setups during any time of the day, including Asian, London, New York, and overlapping hours.

No restriction to any specific session — trade when the opportunity is there!

Fake Move Detection 🚫

Identifies candles with long wicks, small bodies, and low volume — typical signs of manipulation or indecision.

Displays a “No Trade Zone – Fake Move” label to help you avoid poor entries.

Real Move Detection ✅

Highlights candles with strong bodies, short wicks, and high volume — ideal conditions for trade entries.

Helps you focus only on high-probability, momentum-driven moves.

RSI-Based Confirmation

Uses RSI to ensure trade entries align with momentum:

Bullish Entry Allowed: Candle is bullish + RSI between 50–75.

Bearish Entry Allowed: Candle is bearish + RSI between 25–50.

Avoid Trades: RSI is overbought/oversold or showing divergence.

Divergence Detection

Detects bearish divergence in bullish setups and bullish divergence in bearish setups — warns against risky entries.

Visual Zones & Candle Highlights

Plots horizontal lines at candle highs/lows and extended zones based on candle range.

Dominant candles are highlighted in black for quick visual spotting.

⚙️ Custom Inputs:

Minimum Body Size Threshold

Wick-to-Body Ratio for Fake Move

Volume Strength Multiplier

Candle Dominance Precision (% of range)

RSI Period and Source

Optional session filter (can be turned off to enable all-session detection)

🛎️ Alerts Included:

✅ Long Entry Confirmed – Strong bullish candle with supporting RSI

✅ Short Entry Confirmed – Strong bearish candle with supporting RSI

🚫 Fake Move Detected – Weak structure + low volume, no trade

🧠 How to Use:

Wait for a dominant black candle to appear.

Read the label to understand:

✅ Green = Trade Allowed

⚠️ Orange = Avoid (due to RSI or divergence)

🚫 Red = Fake Move (stay out)

Combine with support/resistance, SMC, or price action strategy for confluence.

🟢 "Trade any session, any time – with confidence, precision, and control. Powered by Raja Saien."

Built for traders who value smart entries and reliable signals across all time zones.

FEDFUNDS Rate Divergence Oscillator [BackQuant]FEDFUNDS Rate Divergence Oscillator

1. Concept and Rationale

The United States Federal Funds Rate is the anchor around which global dollar liquidity and risk-free yield expectations revolve. When the Fed hikes, borrowing costs rise, liquidity tightens and most risk assets encounter head-winds. When it cuts, liquidity expands, speculative appetite often recovers. Bitcoin, a 24-hour permissionless asset sometimes described as “digital gold with venture-capital-like convexity,” is particularly sensitive to macro-liquidity swings.

The FED Divergence Oscillator quantifies the behavioural gap between short-term monetary policy (proxied by the effective Fed Funds Rate) and Bitcoin’s own percentage price change. By converting each series into identical rate-of-change units, subtracting them, then optionally smoothing the result, the script produces a single bounded-yet-dynamic line that tells you, at a glance, whether Bitcoin is outperforming or underperforming the policy backdrop—and by how much.

2. Data Pipeline

• Fed Funds Rate – Pulled directly from the FRED database via the ticker “FRED:FEDFUNDS,” sampled at daily frequency to synchronise with crypto closes.

• Bitcoin Price – By default the script forces a daily timeframe so that both series share time alignment, although you can disable that and plot the oscillator on intraday charts if you prefer.

• User Source Flexibility – The BTC series is not hard-wired; you can select any exchange-specific symbol or even swap BTC for another crypto or risk asset whose interaction with the Fed rate you wish to study.

3. Math under the Hood

(1) Rate of Change (ROC) – Both the Fed rate and BTC close are converted to percent return over a user-chosen lookback (default 30 bars). This means a cut from 5.25 percent to 5.00 percent feeds in as –4.76 percent, while a climb from 25 000 to 30 000 USD in BTC over the same window converts to +20 percent.

(2) Divergence Construction – The script subtracts the Fed ROC from the BTC ROC. Positive values show BTC appreciating faster than policy is tightening (or falling slower than the rate is cutting); negative values show the opposite.

(3) Optional Smoothing – Macro series are noisy. Toggle “Apply Smoothing” to calm the line with your preferred moving-average flavour: SMA, EMA, DEMA, TEMA, RMA, WMA or Hull. The default EMA-25 removes day-to-day whips while keeping turning points alive.

(4) Dynamic Colour Mapping – Rather than using a single hue, the oscillator line employs a gradient where deep greens represent strong bullish divergence and dark reds flag sharp bearish divergence. This heat-map approach lets you gauge intensity without squinting at numbers.

(5) Threshold Grid – Five horizontal guides create a structured regime map:

• Lower Extreme (–50 pct) and Upper Extreme (+50 pct) identify panic capitulations and euphoria blow-offs.

• Oversold (–20 pct) and Overbought (+20 pct) act as early warning alarms.

• Zero Line demarcates neutral alignment.

4. Chart Furniture and User Interface

• Oscillator fill with a secondary DEMA-30 “shader” offers depth perception: fat ribbons often precede high-volatility macro shifts.

• Optional bar-colouring paints candles green when the oscillator is above zero and red below, handy for visual correlation.

• Background tints when the line breaches extreme zones, making macro inflection weeks pop out in the replay bar.

• Everything—line width, thresholds, colours—can be customised so the indicator blends into any template.

5. Interpretation Guide

Macro Liquidity Pulse

• When the oscillator spends weeks above +20 while the Fed is still raising rates, Bitcoin is signalling liquidity tolerance or an anticipatory pivot view. That condition often marks the embryonic phase of major bull cycles (e.g., March 2020 rebound).

• Sustained prints below –20 while the Fed is already dovish indicate risk aversion or idiosyncratic crypto stress—think exchange scandals or broad flight to safety.

Regime Transition Signals

• Bullish cross through zero after a long sub-zero stint shows Bitcoin regaining upward escape velocity versus policy.

• Bearish cross under zero during a hiking cycle tells you monetary tightening has finally started to bite.

Momentum Exhaustion and Mean-Reversion

• Touches of +50 (or –50) come rarely; they are statistically stretched events. Fade strategies either taking profits or hedging have historically enjoyed positive expectancy.

• Inside-bar candlestick patterns or lower-timeframe bearish engulfings simultaneously with an extreme overbought print make high-probability short scalp setups, especially near weekly resistance. The same logic mirrors for oversold.

Pair Trading / Relative Value

• Combine the oscillator with spreads like BTC versus Nasdaq 100. When both the FED Divergence oscillator and the BTC–NDQ relative-strength line roll south together, the cross-asset confirmation amplifies conviction in a mean-reversion short.

• Swap BTC for miners, altcoins or high-beta equities to test who is the divergence leader.

Event-Driven Tactics

• FOMC days: plot the oscillator on an hourly chart (disable ‘Force Daily TF’). Watch for micro-structural spikes that resolve in the first hour after the statement; rapid flips across zero can front-run post-FOMC swings.

• CPI and NFP prints: extremes reached into the release often mean positioning is one-sided. A reversion toward neutral in the first 24 hours is common.

6. Alerts Suite

Pre-bundled conditions let you automate workflows:

• Bullish / Bearish zero crosses – queue spot or futures entries.

• Standard OB / OS – notify for first contact with actionable zones.

• Extreme OB / OS – prime time to review hedges, take profits or build contrarian swing positions.

7. Parameter Playground

• Shorten ROC Lookback to 14 for tactical traders; lengthen to 90 for macro investors.

• Raise extreme thresholds (for example ±80) when plotting on altcoins that exhibit higher volatility than BTC.

• Try HMA smoothing for responsive yet smooth curves on intraday charts.

• Colour-blind users can easily swap bull and bear palette selections for preferred contrasts.

8. Limitations and Best Practices

• The Fed Funds series is step-wise; it only changes on meeting days. Rapid BTC oscillations in between may dominate the calculation. Keep that perspective when interpreting very high-frequency signals.

• Divergence does not equal causation. Crypto-native catalysts (ETF approvals, hack headlines) can overwhelm macro links temporarily.

• Use in conjunction with classical confirmation tools—order-flow footprints, market-profile ledges, or simple price action to avoid “pure-indicator” traps.

9. Final Thoughts

The FEDFUNDS Rate Divergence Oscillator distills an entire macro narrative monetary policy versus risk sentiment into a single colourful heartbeat. It will not magically predict every pivot, yet it excels at framing market context, spotting stretches and timing regime changes. Treat it as a strategic compass rather than a tactical sniper scope, combine it with sound risk management and multi-factor confirmation, and you will possess a robust edge anchored in the world’s most influential interest-rate benchmark.

Trade consciously, stay adaptive, and let the policy-price tension guide your roadmap.

CE XAU/USDT Strategy📌 Auto-Trading Strategy Using CE on XAU/USDT (5M)

Indicator: CE

Parameters:

• ATR Period: 1

• ATR Multiplier: 1.85

Timeframe: 5 minutes

Instrument: Gold (XAU/USD)

🔁 Logic:

• Buy signal → Close short, open long

• Sell signal → Close long, open short

⚙️ Automation:

1. CE indicator on TradingView generates signals

2. Signals are sent via webhook to a Python bot

3. The bot opens/closes trades in MT5 accordingly

✅ Advantages:

• Full automation

• Operates 24/7 without manual intervention

⚠️ Important:

• Always test on a demo account

• Manage risk and position size properly

📌 Стратегия автоторговли по CE на XAU/USDT (5М)

Индикатор: CE

Параметры:

• ATR Period: 1

• ATR Множитель: 1.85

Таймфрейм: 5 минут

Инструмент: Золото (XAU/USD)

🔁 Логика:

• Buy сигнал → закрыть шорт, открыть лонг

• Sell сигнал → закрыть лонг, открыть шорт

⚙️ Автоматизация:

1. CE в TradingView генерирует сигналы

2. Webhook отправляет их в Python-бот

3. Бот открывает/закрывает сделки в MT5

✅ Плюсы:

• Полная автоматизация

• Работа 24/7 без вмешательства

⚠️ Важно:

• Тестируй на демо

• Управляй рисками и лотами

Time Range Marker By BCB ElevateThe Time Range Marker is a simple yet powerful visual tool for traders who want to focus on specific time intervals within the trading day. This indicator highlights a custom time range on your chart using a background color, helping you visually isolate key trading sessions or event windows such as:

Market open/close hours

News release periods

High-volatility trading zones

Personal strategy testing windows

⚙️ Key Features:

Customizable start and end time (hour & minute)

Works across all intraday timeframes

Adjustable highlight color to match your chart theme

Built using Pine Script v5 for speed and flexibility

🔧 Settings:

Start Hour / Minute – Set the beginning of the time range (in 24-hour format)

End Hour / Minute – Define when the range ends

Highlight Color – Choose the background color for better visibility

🕒 Timezone Note:

The indicator uses UTC time by default to ensure accuracy across markets. If your broker uses a different timezone (like EST, IST, etc.), the script can be adjusted to reflect your local market hours.

✅ How to Use the Time Range Marker Indicator

This indicator is used to visually highlight a specific time window each trading day, such as:

Market open or close sessions (e.g., NYSE, London, Tokyo)

High-impact news release periods

Custom time slots for strategy testing or scalping

🛠️ Installation Steps

Open TradingView and go to any chart.

Click on Pine Editor at the bottom of the screen.

Copy and paste the full Pine Script (shared above) into the editor.

Click the “Add to Chart” ▶️ button.

The indicator will appear on the chart with a highlighted background during the time range you set.

⚙️ How to Customize the Time Range

After adding the indicator:

Click the gear icon ⚙️ next to the indicator’s name on the chart.

Adjust the following settings:

Start Hour / Start Minute: The beginning of your time range (in 24-hour format).

End Hour / End Minute: When the highlight should stop.

Highlight Color: Pick a color and transparency for visual clarity.

Click OK to apply changes.

🕒 Timezone Consideration

By default, the indicator uses UTC (Coordinated Universal Time).

To match your broker’s timezone (e.g., EST, IST, etc.), you'll need to adjust the script by changing:

sessStart = timestamp("Etc/UTC", ...)

sessEnd = timestamp("Etc/UTC", ...)

to your correct timezone, like "Asia/Kolkata" for IST or "America/New_York" for EST.

Let me know your broker or local timezone, and I’ll update it for you.

📈 Tips for Traders

Combine this with volume, price action, or breakout indicators to focus your strategy on high-probability time windows.

Use multiple versions of this script if you want to highlight more than one time range in a day.

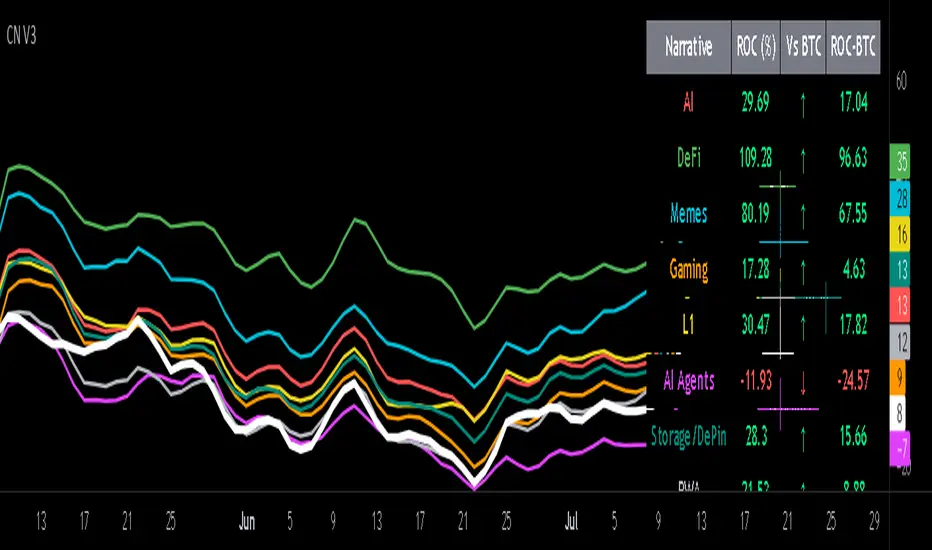

Crypto Narratives: Relative Strength V2Simple Indicator that displays the relative strength of 8 Key narratives against BTC as "Spaghetti" chart. The chart plots an aggregated RSI value for the 5 highest Market Cap cryopto's within each relevant narrative. The chart plots a 14 period SMA RSI for each narrative.

Functionality:

The indicator calculates the average RSI values for the current leading tokens associated with ten different crypto narratives:

- AI (Artificial Intelligence)

- DeFi (Decentralized Finance)

- Memes

- Gaming

- Level 1 (Layer 1 Protocols)

- AI Agents

- Storage/DePin

- RWA (Real-World Assets)

- BTC

Usage Notes:

The 5 crypto coins should be regularly checked and updated (in the script) by overtyping the current values from Rows 24 - 92 to ensure that you are using the up to date list of highest marketcap coins (or coins of your choosing).

The 14 period SMA can be changed in the indicator settings.

The indicator resets every 24 hours and is set to UTC+10. This can be changed by editing the script line 19 and changing the value of "resetHour = 1" to whatever value works for your timezone.

There is also a Rate of Change table that details the % rate of change of each narrative against BTC

Horizontal lines have been included to provide an indication of overbought and oversold levels.

The upper and lower horizontal line (overbought and oversold) can be adjusted through the settings.

The line width, and label offset can be customised through the input options.

Alerts can be set to triggered when a narrative's RSI crosses above the overbought level or below the oversold level. The alerts include the narrative name, RSI value, and the RSI level.

Frahm Factor Position Size CalculatorThe Frahm Factor Position Size Calculator is a powerful evolution of the original Frahm Factor script, leveraging its volatility analysis to dynamically adjust trading risk. This Pine Script for TradingView uses the Frahm Factor’s volatility score (1-10) to set risk percentages (1.75% to 5%) for both Margin-Based and Equity-Based position sizing. A compact table on the main chart displays Risk per Trade, Frahm Factor, and Average Candle Size, making it an essential tool for traders aligning risk with market conditions.

Calculates a volatility score (1-10) using true range percentile rank over a customizable look-back window (default 24 hours).

Dynamically sets risk percentage based on volatility:

Low volatility (score ≤ 3): 5% risk for bolder trades.

High volatility (score ≥ 8): 1.75% risk for caution.

Medium volatility (score 4-7): Smoothly interpolated (e.g., 4 → 4.3%, 5 → 3.6%).

Adjustable sensitivity via Frahm Scale Multiplier (default 9) for tailored volatility response.

Position Sizing:

Margin-Based: Risk as a percentage of total margin (e.g., $175 for 1.75% of $10,000 at high volatility).

Equity-Based: Risk as a percentage of (equity - minimum balance) (e.g., $175 for 1.75% of ($15,000 - $5,000)).

Compact 1-3 row table shows:

Risk per Trade with Frahm score (e.g., “$175.00 (Frahm: 8)”).

Frahm Factor (e.g., “Frahm Factor: 8”).

Average Candle Size (e.g., “Avg Candle: 50 t”).

Toggles to show/hide Frahm Factor and Average Candle Size rows, with no empty backgrounds.

Four sizes: XL (18x7, large text), L (13x6, normal), M (9x5, small, default), S (8x4, tiny).

Repositionable (9 positions, default: top-right).

Customizable cell color, text color, and transparency.

Set Frahm Factor:

Frahm Window (hrs): Pick how far back to measure volatility (e.g., 24 hours). Shorter for fast markets, longer for chill ones.

Frahm Scale Multiplier: Set sensitivity (1-10, default 9). Higher makes the score jumpier; lower smooths it out.

Set Margin-Based:

Total Margin: Enter your account balance (e.g., $10,000). Risk auto-adjusts via Frahm Factor.

Set Equity-Based:

Total Equity: Enter your total account balance (e.g., $15,000).

Minimum Balance: Set to the lowest your account can go before liquidation (e.g., $5,000). Risk is based on the difference, auto-adjusted by Frahm Factor.

Customize Display:

Calculation Method: Pick Margin-Based or Equity-Based.

Table Position: Choose where the table sits (e.g., top_right).

Table Size: Select XL, L, M, or S (default M, small text).

Table Cell Color: Set background color (default blue).

Table Text Color: Set text color (default white).

Table Cell Transparency: Adjust transparency (0 = solid, 100 = invisible, default 80).

Show Frahm Factor & Show Avg Candle Size: Check to show these rows, uncheck to hide (default on).

MC Geopolitical Tension Events📌 Script Title: Geopolitical Tension Events

📖 Description:

This script highlights key geopolitical and military tension events from 1914 to 2024 that have historically impacted global markets.

It automatically plots vertical dashed lines and labels on the chart at the time of each major event. This allows traders and analysts to visually assess how markets have responded to global crises, wars, and significant political instability over time.

🧠 Use Cases:

Historical backtesting: Understand how market responded to past geopolitical shocks.

Contextual analysis: Add macro context to technical setups.

🗓️ List of Geopolitical Tension Events in the Script

Date Event Title Description

1914-07-28 WWI Begins Outbreak of World War I following the assassination of Archduke Franz Ferdinand.

1929-10-24 Wall Street Crash Black Thursday, the start of the 1929 stock market crash.

1939-09-01 WWII Begins Germany invades Poland, starting World War II.

1941-12-07 Pearl Harbor Japanese attack on Pearl Harbor; U.S. enters WWII.

1945-08-06 Hiroshima Bombing First atomic bomb dropped on Hiroshima by the U.S.

1950-06-25 Korean War Begins North Korea invades South Korea.

1962-10-16 Cuban Missile Crisis 13-day standoff between the U.S. and USSR over missiles in Cuba.

1973-10-06 Yom Kippur War Egypt and Syria launch surprise attack on Israel.

1979-11-04 Iran Hostage Crisis U.S. Embassy in Tehran seized; 52 hostages taken.

1990-08-02 Gulf War Begins Iraq invades Kuwait, triggering U.S. intervention.

2001-09-11 9/11 Attacks Coordinated terrorist attacks on the U.S.

2003-03-20 Iraq War Begins U.S.-led invasion of Iraq to remove Saddam Hussein.

2008-09-15 Lehman Collapse Bankruptcy of Lehman Brothers; peak of global financial crisis.

2014-03-01 Crimea Crisis Russia annexes Crimea from Ukraine.

2020-01-03 Soleimani Strike U.S. drone strike kills Iranian General Qasem Soleimani.

2022-02-24 Ukraine Invasion Russia launches full-scale invasion of Ukraine.

2023-10-07 Hamas-Israel War Hamas launches attack on Israel, sparking war in Gaza.

2024-01-12 Red Sea Crisis Houthis attack ships in Red Sea, prompting Western naval response.

ES OHLC BASED ON 9:301. RTH Price Levels

YC (Yesterday's Close): Previous day's RTH closing price at 4:00 PM ET

0DTE-O (Today's Open): Current day's RTH opening price at 9:30 AM ET

T-E-M (Today's Europe-Asia Midpoint): Midpoint of overnight session high/low

T-E-R (Today's Europe-Asia Resistance): Overnight session high

T-E-S (Today's Europe-Asia Support): Overnight session low

Y-T-M (Yesterday-Today Midpoint): Midpoint between YC and 0DTE-O

2. Previous Bar Percentage Levels

Displays 50% retracement level for all bars

Shows 70% level for bullish bars (close > open)

Shows 30% level for bearish bars (close < open)

Lines automatically update with each new bar

3. Custom Support/Resistance Lines

Up to 4 customizable horizontal levels (2 resistance, 2 support)

Useful for marking key psychological levels or pivot points

4. VIX-Based Options Strategy Suggestions

Real-time VIX value display

Time Zone Handling

The indicator is configured for Central Time (CT) as Pine Script's default:

RTH Open: 8:30 AM CT (9:30 AM ET)

RTH Close: 3:00 PM CT (4:00 PM ET)

Overnight session: 7:00 PM CT to 8:30 AM CT next day

Usage Notes

Chart Requirement: This indicator only works on 5-minute timeframe charts

Auto-refresh: All lines and labels automatically refresh at each new trading day's RTH open

24-hour Market: Designed for ES futures which trade nearly 24 hours

Visual Clarity: Different line styles and colors for easy identification

Ideal For

Day traders focusing on ES futures

0DTE options traders needing key reference levels

Traders using overnight gaps and previous day's levels

Those incorporating VIX-based strategies in their trading

Aftershock by Session [SAKANE]■ Background & Motivation

In 24/7 markets like crypto, not all participants react simultaneously to major events.

Instead, reactions unfold across different regional trading sessions — Asia (APAC), Europe (EU), and the United States (US) — each with its own tempo and sentiment.

This indicator is designed to visualize which session drives the market after a key event — capturing the "aftershock" effect that ripples through time zones.

■ Key Features

Tracks price return (open → close) for each session: APAC / EU / US

Cumulative session returns are calculated and visualized

Smoothing options: SMA, EMA, or Ehlers SuperSmoother