Aggregated Spot vs Perp Volume (% Change)Aggregated Spot vs Perp Volume (% Change)

Description

The "Aggregated Spot vs Perp Volume (% Change)" indicator helps crypto traders compare the momentum of spot and perpetual futures (perp) trading volumes across 12 major exchanges. It calculates the percentage change in volume from one bar to the next, highlighting divergences and showing which market—spot or perp—is leading a move. By focusing on relative changes, it eliminates the issue of absolute volume differences, making trends clear.

The indicator aggregates data from Binance, Bybit, OKX, Coinbase, Bitget, MEXC, Phemex, BingX, WhiteBIT, BitMEX, Kraken, and HTX. Users can toggle exchanges and choose to measure volume in coin units (e.g., BTC) or USD.

How It Works

Volume Aggregation:

Fetches spot and perp volume data for the selected crypto (e.g., BTC) from up to 12 exchanges.

Spot volume is included only if perp volume is available for the same pair, ensuring consistency.

Volume can be measured in coin units or USD (volume × spot price).

Percentage Change:

Calculates the percentage change in spot and perp volumes from the previous bar:

Percentage Change = ((Current Volume − Previous Volume) / Previous Volume) ×100

This focuses on relative momentum, making spot and perp volumes directly comparable.

Visualization:

Spot volume % change is plotted as a blue line, and perp volume % change as a red line, both with a linewidth of 1.

Who Should Use It

Crypto Traders: To understand spot vs. perp market dynamics across exchanges.

Momentum Traders: To spot which market is driving price moves via volume divergences.

Scalpers/Day Traders: For identifying short-term shifts in market activity.

Analysts: To study liquidity and sentiment in crypto markets.

How to Use It

Blue line: Spot volume % change.

Red line: Perp volume % change.

Look for divergences (e.g., a sharp rise in the red line but not the blue line suggests perp markets are leading).

Combine with Price:

Use alongside price charts to confirm trends or spot potential reversals.

Context

Spot markets reflect actual asset trading, while perp markets, with leverage, attract speculative activity and often show higher volumes. This indicator uses percentage change to compare their momentum, helping traders identify market leadership and divergences. For example, a 50% increase in both spot and perp volumes plots at the same level, making it easy to see relative shifts across exchanges.

"西布罗姆vs伯恩利" için komut dosyalarını ara

Dynamic Spot vs Perp Spread### **Description for TradingView Publication**

---

**Dynamic Spot vs Perp Spread**

(For USDT-Spot and USDT.P-Perp)

Summary of Usefulness:

This indicator is a valuable tool for traders who want to monitor and capitalize on the relationship between spot and perpetual futures (perp) prices. When the spot price exceeds the perp price, it's often a leading signal that the perp price will follow, creating potential trading opportunities. While this behavior doesn't happen every time, divergences between spot and perp prices can frequently signal significant market movements.

What it Does:

This indicator calculates and displays the price spread (percentage difference) between the spot price and perpetual futures (perp) price of a cryptocurrency asset. It dynamically adjusts to the instrument being viewed, ensuring that spot dominance (spot price higher) is plotted above the zero line and perp dominance (perp price higher) is plotted below the zero line. Additionally, the indicator accounts for symbols with multipliers (e.g., `1000SHIBUSDT.P`) to ensure accurate calculations.

Key features include:

- Automatic symbol detection and adjustment for Spot/Perp pairs.

- Dynamic handling of price multipliers for assets with prefixes like `1000`.

- Visualization of spread with a histogram and optional smoothing using an EMA (Exponential Moving Average).

- Configurable alerts for significant spread changes and spread flips.

- No repainting: the indicator uses the `barmerge.lookahead_off` setting to ensure stable, non-repainting values.

---

### **How to Use**

1. **Add the Indicator:**

- Search for "Dynamic Spot vs Perp Spread" in the TradingView Indicators library and add it to your chart.

2. **Understand the Visualization:**

- A positive spread (green histogram) indicates that the spot price is higher than the perp price (spot dominance).

- A negative spread (red histogram) indicates that the perp price is higher than the spot price (perp dominance).

3. **Customize Settings:**

- **EMA Length:** Use the input field to smooth the spread data over a chosen number of periods.

- **Alert Threshold:** Set a threshold to receive alerts when the spread exceeds a specific percentage.

4. **Receive Alerts:**

- Enable alerts for spread flips (when dominance shifts between spot and perp) or when the spread exceeds the defined threshold.

5. **Use Case Examples:**

- **Spot vs. Perp Arbitrage:** Traders can monitor significant deviations between spot and perp prices to identify potential arbitrage opportunities.

- **Market Sentiment Analysis:** Persistent spot dominance may indicate stronger buying interest in the spot market, while perp dominance may suggest futures market speculation.

---

### **Repainting Behavior**

This indicator **does not repaint** because it uses `barmerge.lookahead_off` for all calculations, ensuring that data from the comparison symbol (spot or perp) is locked to the currently completed candle. This means the values plotted and alerts triggered are reliable and do not change retrospectively.

Repainting occurs when an indicator uses future-looking or incomplete data for calculations. By design, this indicator avoids such practices, making it suitable for live trading and analysis.

---

Cantom Chart - CL CTG vs BKDEnglish : This Pine Script indicator, named "Cantom Chart - CL CTG vs BKD," uniquely analyzes the immediate state of oil futures contracts to determine if they are in contango or backwardation. The script uses the price ratio between the nearest (CL1) and the next nearest (CL2) NYMEX crude oil futures contracts. It multiplies this ratio by 100 for clarity and scales fluctuations for enhanced visibility.

Key Features:

Dynamic Ratio Calculation: Computes the ratio (CL1/CL2 * 100) to determine the immediate market state.

Market State Interpretation: A ratio above 100 indicates backwardation, suggesting higher demand than supply, while a ratio below 100 indicates contango, suggesting higher supply than demand.

Volatility Adjustment: Amplifies market state changes by tripling the deviation from the baseline of 100, making it easier to observe subtle shifts.

Anomaly Detection: Caps the adjusted ratio at 125 for highs and 75 for lows, maintaining these limits until the ratio returns to normal levels.

Usage: This indicator is especially useful for traders analyzing supply-demand dynamics and inflationary pressures in the oil market. To apply it, simply add the script to your TradingView chart and adjust the 'Lower Threshold' and 'Upper Threshold' lines as needed based on your trading strategy.

-----

日本語 : この「Cantom Chart - CL CTG vs BKD」Pine Scriptインジケーターは、直近の原油先物契約がコンタンゴまたはバックワーデーションにあるかを特定するための独自の分析を提供します。最近の(CL1)と次の(CL2)NYMEX原油先物契約間の価格比を使用し、この比率に100を掛けて明確性を高め、変動の視認性を向上させます。

主要機能:

動的比率計算: 市場の即時状態を判断するために比率(CL1/CL2 * 100)を計算します。

市場状態の解釈: 比率が100を超える場合はバックワーデーション(需要が供給を上回る)、100未満の場合はコンタンゴ(供給が需要を上回る)を示します。

変動調整: 基準値100からの偏差を3倍にして、微妙な変化を容易に観察できるようにします。

異常値検出: 調整された比率を高値で125、低値で75に制限し、通常のレベルに戻るまでこれらの限界を維持します。

使用方法: このインジケーターは、原油市場における需給ダイナミクスとインフレ圧力を分析するトレーダーにとって特に有用です。使用するには、このスクリプトをTradingViewチャートに追加し、トレーディング戦略に基づいて「Lower Threshold」と「Upper Threshold」のラインを必要に応じて調整します。

Bearish vs Bullish ArgumentsThe Bearish vs Bullish Arguments Indicator is a tool designed to help traders visually assess and compare the number of bullish and bearish arguments based on their custom inputs. This script enables users to input up to five bullish and five bearish arguments, dynamically displaying the bias on a clean and customizable table on the chart. This provides traders with a clear, visual representation of the market sentiment they have identified.

Key Features:

Customizable Inputs: Users can input up to five bullish and five bearish arguments, which are displayed in a table on the chart.

Bias Calculation: The script calculates the bias (Bullish, Bearish, or Neutral) based on the number of bullish and bearish arguments provided.

Color Customization: Users can customize the colors for the table background, text, and headers, ensuring the table fits seamlessly into their charting environment.

Reset Functionality: A reset switch allows users to clear all input arguments with a single click, making it easy to start fresh.

How It Works:

Input Fields: The script provides input fields for up to five bullish and five bearish arguments. Each input is a simple text field where users can describe their arguments.

Bias Calculation: The script counts the number of non-empty bullish and bearish arguments and determines the overall bias. The bias is displayed in the table with a dynamically changing color to indicate whether the market sentiment is bullish, bearish, or neutral.

Customizable Table: The table is positioned on the chart according to the user's preference (top-left, top-right, bottom-left, bottom-right) and can be customized in terms of background color and text color.

How to Use:

Add the Indicator: Add the Bearish vs Bullish Arguments Indicator to your chart.

Input Arguments: Enter up to five bullish and five bearish arguments in the provided input fields in the script settings.

Customize Appearance: Adjust the table's background color, text color, and position on the chart to fit your preferences.

Example Use Case:

A trader might use this indicator to visually balance their arguments for and against a particular trade setup. By entering their reasons for a bullish outlook in the bullish argument fields and their reasons for a bearish outlook in the bearish argument fields, they can quickly see which side has more supporting points and make a more informed trading decision.

This script was inspired by Arjoio's concepts

VIX: Backwardation Vs ContangoVIX: Backwardation Vs Contango

Quickly visualize Contango vs Backwardation in the S&P 500 Volatility Index by plotting the prices of the futures contracts over the next 9 months

Note: indicator does not map to time axis in the same way as price; it simply plots the progression of contract months out into the future; left to right; so timeframe DOESN'T MATTER for this plot

TO UPDATE(every few months recommended): in REQUEST CONTRACTS section, delete old contracts (top) and add new ones (bottom). Then in PLOTTING section, Delete old contract labels (bottom); add new contract labels (top); adjust the X in 'bar_index-(X+_historical)' numbers accordingly

This is one of several similar indicators: Meats | Metals | Grains | VIX

Tips:

-Right click and reset chart if you can't see the plot; or if you have trouble with the scaling.

-Right click and pin to Scale A to plot on the same scale as price

--Added historical input: input days back in time; to see the historical shape of the Futures curve via selecting 'days back' snapshot

updated 15th June 2022

© twingall

ROC vs BTCThis is a modification of my Rate of Change Percentile script, used to compare the current ticker (e.g. Altcoins) to BTC.

Essentially we are looking at (Current Ticker ROC percentile) vs (Bitcoin ROC percentile).

In other words, we are using the ROC value of both the current ticker and BTC, and ranking each based on their previous ROC.

We compare the rankings to gauge the relative overperformance or underperformance of the current ticker vs BTC.

The blue line is BTC, the columns are the current ticker.

Green columns above the blue line indicate positive ROC and current ticker has higher ROC ranking than BTC.

Red columns below the blue line indicate negative ROC and current ticker has a higher ROC ranking than BTC.

*** PLEASE LEAVE A LIKE AND FOLLOW IF YOU ENJOY THE SCRIPT ***

Any questions, comments or feedback I'd love to hear from you below!

Percentile - Price vs FundamentalsThis is done in the same lines of below scripts

Drawdown-Price-vs-Fundamentals

Drawdown-Range

Instead of using drawdown, here we are only plotting percentile of drawdown. Also added few more fundamental stats to the indicator. Also using part of the code from Random-Color-Generator/ to automatically generate colors. This in turn uses code from @RicardoSantos for convering color based on HSL to RGB

This is how the study can be used:

Study plots percentile of price and each of the listed fundamentals based on history. History can be chose All time or particular window. If any fundamental or price is near 100 - which means it is nearer to its peak. And if something is near its bottom, it is nearer to its 0th percentile.

Price of the stock is considered undervalued based on historical levels when it is below most of the fundamentals. Price is considered overvalued based on historical levels when it is above all the fundamentals. Please note, being undervalued does not guarantee immediate mean reversion. Stocks can stay undervalued for prolonged time and can go further down. Similarly overvalued stock can stay overvalued for prolonged time before correcting itself or justifying the position. Hence, further discretion needs to be used while using this study.

Few examples:

AMZN seems to be trading in range and so are the fundamentals:

MSFT at peak along with half of the fundamentals. But, debt levels are going up along with margins reducing.

LPX is trading at 15% discount whereas most of the fundamentals are at the peak.

FLGT price seems to have gone down further whereas fundamentals look pretty healthy.

DTR vs ATRThis script shows DTR vs ATR (Today's True Range vs 14 days Avg True Range) along with percentage. The label automatically changes color based on percent value. <=70 is GREEN, >=90 is RED and between 70 & 90 is ORANGE.

The location of the script not stick to one place. There is no such a functionality to keep it static at one location (like top right corner). But I think that feature is coming soon. I may be wrong.

Altcoin Cap vs Bitcoin Cap RSIFollowing Willy Woo study of Altcoin Cap vs Bitcoin Cap RSI

charts.woobull.com

Euro Area vs US10YThe Euro Area GDP-Weighted Yield vs US10Y Spread is a macroeconomic indicator designed for forex traders and institutional investors who want to monitor the fundamental interest rate differential between the Eurozone and the United States. This tool aggregates sovereign bond yields from the major Eurozone member states using a weighted methodology based on outstanding government debt, providing a comprehensive view of the Euro Area’s fixed income market dynamics.

This indicator calculates a composite 10-year government bond yield for the Eurozone by combining data from seven major member countries: Germany, France, Italy, Spain, Netherlands, Belgium, and Austria. The weights are based on the proportion of government debt outstanding in each country, reflecting the actual composition of the European sovereign bond market rather than just GDP size.

The indicator then compares this Euro Area weighted yield against the US 10-Year Treasury yield (US10Y), producing a yield spread that serves as a powerful leading indicator for EUR/USD price movements.

Effort vs Result TRFxThe Effort vs Result (EVR) indicator is designed to identify high-probability reversal signals based on volume and price action dynamics. It highlights points where the market “effort” (high volume) does not correspond to an immediate “result” (price continuation), providing actionable trade setups for both bullish and bearish scenarios.

Features:

Detects bullish EVR signals when a previous high-volume sell candle is followed by a strong bullish candle that sweeps the previous low.

Detects bearish EVR signals when a previous high-volume buy candle is followed by a strong bearish candle that sweeps the previous high.

Sticky arrows plot automatically above or below the candle, ensuring the signal moves with the price bar.

Considers inside bars, wick size, and relative volume to filter low-quality setups.

Fully compatible with multiple timeframes.

Inputs:

Volume Multiplier: Sets how much higher the current candle’s volume should be compared to the previous candle to count as high volume.

Min Wick % of Candle: Minimum wick size relative to the candle body to filter insignificant bars.

Max Inside Bars to Ignore: Number of inside bars between the previous candle and the EVR candle to ignore minor consolidations.

Usage:

(Green Arrow): Enter long when a green arrow appears below the candle. Place stop-loss slightly below the previous swing low.

(Red Arrow): Enter short when a red arrow appears above the candle. Place stop-loss slightly above the previous swing high.

Can be combined with support/resistance levels, trendlines, or other technical indicators for higher accuracy.

Benefits:

Simple and clean visual signals with tiny arrows that move with candles.

Helps traders identify high-probability reversal points based on volume and price action.

Ideal for intraday and swing trading strategies.

Buyer vs Seller ControlBuyer vs Seller Control Analysis

Technical indicator measuring market participation through candlestick wick analysis

Overview:

This indicator analyzes the relationship between closing prices and candlestick wicks to measure buying and selling pressure. It calculates two key metrics and displays their moving averages to help identify market sentiment shifts.

Calculation Method:

The indicator measures two distinct values for each candle:

Buyer Control Value: Distance from candle low to closing price (close - low)

Seller Control Value: Distance from candle high to closing price (high - close)

Both values are then smoothed using a Simple Moving Average (default period: 20) to reduce noise and show clearer trends.

Visual Components:

Lime Line: 20-period SMA of buyer control values

Fuchsia Line: 20-period SMA of seller control values

Area Fill: Colored region between the two lines

Histogram: Difference between buyer and seller control SMAs

Zero Reference Line: Horizontal line at zero level

Information Table: Current numerical values (optional display)

Interpretation:

When the lime line (buyer control) is above the fuchsia line (seller control), it indicates that recent candles have been closing closer to their highs than to their lows on average.

When the fuchsia line is above the lime line, recent candles have been closing closer to their lows than to their highs on average.

Fill Color Logic:

Lime (green) fill appears when buyer control SMA > seller control SMA

Fuchsia (red) fill appears when seller control SMA > buyer control SMA

Fill transparency adjusts based on the magnitude of difference between the two SMAs

Stronger differences result in more opaque fills

Settings:

Moving Average Period: Adjustable from 1-200 periods (default: 20)

Show Info Table: Toggle to display/hide the numerical values table

Technical Notes:

The indicator works on any timeframe

Values are displayed in the same units as the underlying asset's price

The histogram shows the mathematical difference between the two SMA lines

Transparency calculation uses a 50-period lookback for dynamic scaling

This indicator provides a quantitative approach to analyzing candlestick patterns by focusing on where prices close relative to their intraday ranges.

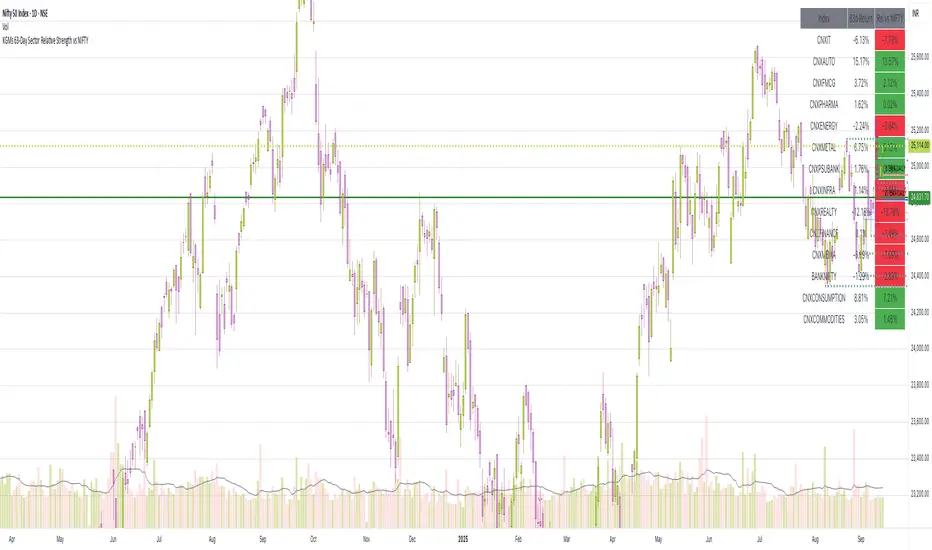

63-Day Sector Relative Strength vs NIFTYThis script calculates and displays the 63-day returns of major NSE sectoral indices and their relative strength versus the NIFTY 50.

It,

Covered Indices: CNXIT, CNXAUTO, CNXFMCG, CNXPHARMA, CNXENERGY, CNXMETAL, CNXPSUBANK, CNXINFRA, CNXREALTY, CNXFINANCE, CNXMEDIA, BANKNIFTY, CNXCONSUMPTION, CNXCOMMODITIES

How to use this: Quickly identify which sectors are outperforming or underperforming relative to the NIFTY over the past 63 trading sessions (approx. 3 months).

EMA 9 vs 21 Spread VarianceEMA 9 vs 21 Spread Variance

What it does

Tracks the distance between EMA 9 and EMA 21, then measures how volatile that distance has been over your chosen lookback. The indicator plots the EMA spread around zero and a rolling variance of that spread. Rising variance signals expanding dispersion between the fast and slow EMAs, which often precedes momentum bursts or regime shifts. Falling variance points to compression and mean-reversion conditions.

How it is calculated

Fast EMA and slow EMA are computed on the selected source.

Spread = EMA9 minus EMA21, plotted around zero.

Variance = rolling variance of the spread over Variance Lookback. Variance is always non-negative.

For readability you can show the variance either on its raw scale, or fitted to the spread’s recent range so both lines are comparable in one pane.

How to read it

Spread near zero with variance rising suggests an impending expansion from balance.

Large positive spread with elevated variance confirms a strong up-trend that is still dynamic.

Large negative spread with elevated variance confirms a strong down-trend that is still dynamic.

Variance rolling over after a run warns that momentum dispersion is cooling and that a consolidation or pullback is likely.

The horizontal zero line applies to the spread only. Variance does not cross zero.

Inputs

Source: price series for EMAs.

Fast EMA Length and Slow EMA Length: defaults 9 and 21.

Variance Lookback: window for the spread variance, common ranges 20 to 100 on intraday charts and 50 to 200 on higher timeframes.

Show spread line and Fit variance to spread scale: display controls.

Suggested use

Combine with your breakout logic. Look for variance expansion from low levels as a filter before taking continuation entries.

Use as a volatility context for EMA cross systems. Crosses that occur with rising variance tend to travel farther than crosses that occur during compression.

Caveats

Variance reacts to spikes in the spread, so it can jump around news bars. Smoothing reduces noise but adds lag. Consider pairing with ATR or session filters if you only want signals during liquid hours.

Global Liquidity Proxy vs BitcoinGlobal Liquidity Proxy vs Bitcoin. Helps to understand the cycles with liquidty.

Stop Loss vs Take Profit Probability and EVThis stop loss and take profit calculator uses a Monte Carlo simulation to calculate the probability of hitting your Stop Loss or Take Profit levels across different time horizons (expressed in bars).

It provides data-driven insights to optimize your risk management and position sizing by showing Expected Value for each scenario.

As a quant, I love using statistical data to help my decisions and get better EV from my trades.

🔬 How It's Calculated

Monte Carlo Simulation: Runs 1,000-10,000 price simulations using a random walk model

Volatility Analysis: Combines ATR-based and Historical Volatility for accurate price movement modeling

Expected Value: Calculates profit/loss expectation using formula: (TP_Probability × Reward) - (SL_Probability × Risk)

Time Horizons: Tests multiple timeframes (1, 5, 10, 20, 50 bars) to find optimal holding periods

Risk/Reward Ratios: Automatically calculates and displays R:R ratios for quick assessment

💡 Use Cases

Position Sizing - Determine optimal risk per trade based on Expected Value

Time Horizon Optimization - Find the best holding period for your strategy

Stop Loss Placement - Validate SL levels using probability analysis

Take Profit Optimization - Set TP levels with statistical backing

Strategy Backtesting - Compare different R:R setups before entering trades

Risk Management - Avoid trades with negative Expected Value

Swing vs Day Trading - Choose timeframes with highest success probability

🎯 How to Use

Setup Trade: Enter your entry price, stop loss, and take profit levels

You can add or remove time horizons denominated in bars. Say you are looking at 1h candles, adding a 24-bar time horizon means you are looking into 24 hours

Choose Direction: Select Long or Short position

Review Table

Analyze Expected Value: Focus on positive EV scenarios (green background)

Optimize Timing: Select time horizons with best risk/reward profile

Adjust Parameters: Modify volatility calculation method and simulation count if needed

Examples

Here's how you can read the tables.

Example 1:

In this chart, we are analyzing the TP and SL probabilities as well as the EV (expected value) for a stock. I want to check what the likelihood is that my SL and TP get triggered over the next 5 days. The stock market is open for 6.5 hours per day, which is 13 bars in this 30-minute bar chart. 26 bars is 2 days, 39 bars is 3 days and so on.

Although this trade is more likely to trigger my SL than my TP, in some of the time horizons we have a positive expected value because of the risk/reward of our trade (i.e. distance of the SL and TP from the price) and the probability of hitting SL and TP.

Example 2:

In this example, we have applied the indicator to gold. Because the TP is much closer to the price, the probability of hitting the TP is much higher.

We can also observe that the expected Value in the shorter time frames is better than in the longer ones. This can give us some clues to set up our trade. If we know that the EV is positive, we can allocate more to that specific trade.

Enjoy, and please let me know your feedback! 😊🥂

EMA 3 vs EMA 21 % Difference AdjustableTitle: EMA 3 vs EMA 21 % Difference with Adjustable Labels

Description:

This script calculates the percentage difference between EMA 3 and EMA 21 and displays it directly on the chart as a label. Labels are shown only when the difference exceeds a user-defined threshold, helping traders easily spot significant deviations.

Features:

Calculates EMA 3 and EMA 21.

Displays percentage difference as labels above or below candles.

Adjustable label style and size.

User-defined percentage threshold for label visibility.

Plots EMA lines for visual reference.

Ideal for traders who want to monitor short-term EMA divergence relative to a longer-term trend in a clean and customizable way.

1H Candlestick vs EMA Crossover# Description — 1H Candlestick vs EMA Crossover (Pine Script)

This indicator is built in **TradingView Pine Script v5** and is designed to track the relationship between the **1‑hour candlestick close** and the **1‑hour Exponential Moving Average (EMA)**. It works on any chart timeframe but always pulls in **1H data** using `request. security`.

### Core Features

* **Customizable EMA length** (default = 200)

* **Plots the 1H EMA** as an orange line on your chart

* Optionally shows the **1H close** as a faint gray line for reference

* Detects and highlights when the **1H candle close crosses above or below the 1H EMA**

* **Arrows**: Green triangles appear below the bar when a bullish crossover happens (1H close > EMA); red triangles appear above the bar when a bearish crossover happens (1H close < EMA)

* **Alerts**: Built‑in `alert condition` statements let you create TradingView alerts whenever a crossover occurs

### How to Use

1. Adjust the EMA length if you want a faster or slower moving average.

2. Enable alerts: Right‑click the chart → Add Alert → choose this indicator and select either “crossed ABOVE EMA” or “crossed BELOW EMA.”

### Trading Applications

* **Trend Confirmation**: Use the 1H EMA as a higher‑timeframe filter while trading on lower timeframes.

* **Entry/Exit Signals**: Crossovers can mark potential entry points for trend continuation or reversals.

* **Scalping/Intraday**: Even on a 5m or 15m chart, you can overlay the 1H EMA to align your trades with the bigger trend.

This makes the indicator a simple yet powerful tool for aligning trades with higher‑timeframe momentum and avoiding false signals from lower‑timeframe noise.

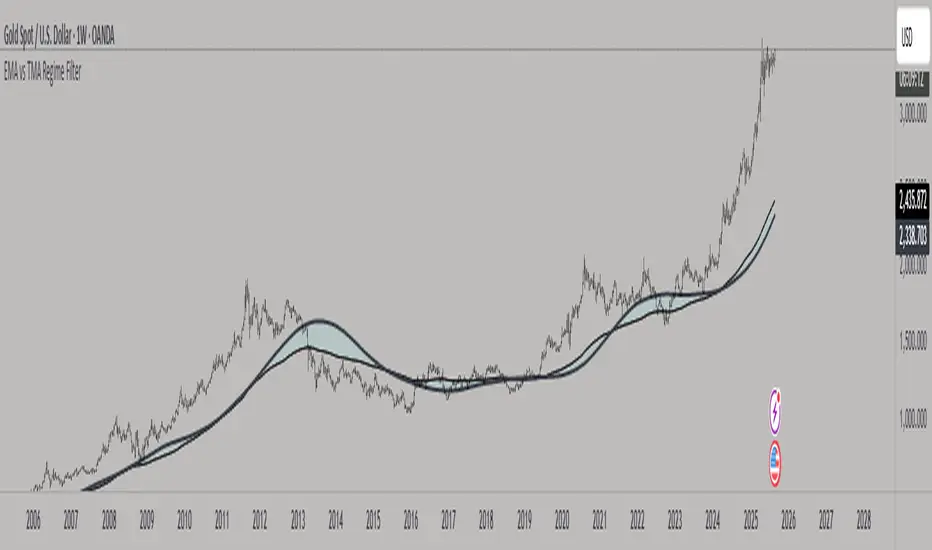

EMA vs TMA Regime FilterEMA vs TMA Regime Filter

This indicator is built as a visual study tool to compare the behavior of the Exponential Moving Average (EMA) and the Triangular Moving Average (TMA).

The EMA applies an exponential weighting to price data, giving stronger importance to the most recent values. This makes it a faster, more responsive line that reflects short-term momentum. The TMA, by contrast, applies a double-smoothing process (or in the “True TMA” option, a split SMA sequence), which produces a much slower curve. The TMA emphasizes balance over reactivity, often used for filtering noise and observing longer-term structure.

When both are plotted on the same chart, their differences become clear. The shaded region between them highlights times when short-term price dynamics diverge from longer-term smoothing. This is where the idea of “regime” comes in — not as a trading signal, but as a descriptive way of seeing whether market action is currently dominated by speed or by stability.

Users can customize:

Line styles, widths, and colors.

Cloud transparency for visual clarity.

Whether to color bars based on relative position (optional, purely visual).

The goal is not to create a system, but to help traders experiment, observe, and learn how different smoothing techniques can emphasize different aspects of price. By switching between the legacy and true TMA, or adjusting lengths, users can study how each approach interprets the same data differently.

Relative RSI vs Multi Benchmark (Equal Weight + RBI Rate)Relative RSI vs Multi Benchmark (Equal Weight + RBI Rate) - Select RSI or MACD

Alt Season vs USDT Flow DashboardWhat the script tells you (the signals)

It builds four “alt vs stables” lenses and colors the background when they agree.

ALT ex-ETH / STABLES (TOTAL3 / (USDT+USDC+DAI))

Think: “How much alt cap per $1 of dry-powder stables?”

Bullish when price is above its 200-day SMA and rising → risk appetite expanding toward smaller alts.

ALT Share of Risk-On ((TOTAL − STABLES − BTC − ETH) / (TOTAL − STABLES))

Of the non-stable crypto pie, how much is flowing to ex-BTC/ETH alts?

Uptrend = broadening alt participation (late-early to mid alt-season behavior).

Dominance Spread ((TOTAL3 / TOTAL) − (STABLES / TOTAL))

Alts’ share minus stables’ share.

Widening spread means stables are being converted into alts (not just into BTC).

Flow Ratio ROC(TOTAL3, N) / ROC(STABLES, N) (default N=30 days)

Compares alts’ growth rate to stable supply growth.

> 1 and sustained → alts expanding faster than new “dry powder” is appearing.

The background color (“regime”)

Green (ALT-on) when all three conditions align:

ALT/Stable > its SMA

Dominance Spread > its SMA

Flow Ratio > 1

Red (ALT-off) when the opposite holds.

No color = mixed/chop.

How to read it (quick playbook)

Early alt-season tell:

BTC.D starts to slip, total market cap (TOTAL) rising.

ALT/Stable breaks above its 200-SMA and stays there.

Dominance Spread climbs (alts gaining share, stables losing share).

Flow Ratio > 1 for a few weeks.

Maturing phase: ALT Share of Risk-On rises (money broadens from ETH/L1s → mid/small caps).

Exhaustion/false start: Flow Ratio dips < 1 or ALT/Stable loses the 200-SMA while BTC.D stabilizes or rises.

Practical tips

Timeframes: Make calls on 1D. Use 1W to avoid whipsaw; use 4H only for entries once the 1D regime is green.

Smoothing: If you see noisy spikes from market-cap revisions, add a light smoother (e.g., 7D SMA on the plotted lines).

Parameters:

Try ROC length 21–45 days.

Try SMA 150–250 days (200 is a good middle).

Confluence: Keep BTC.D and ETH.D in another pane. Best alt windows: BTC.D trending down, ETH.D flat-to-up initially, then ETH.D flattens as TOTAL3 momentum spreads to mid/small caps.

Risk checks: If USDT.D/USDC.D (stable dominance) spike up while your signals are green, that’s a caution flag (capital retreating to stables).

Relative Weighted Rate of Change (WROC) vs Nifty 50Relative Weighted Rate of Change (WROC) vs Nifty 50

ALTSEASON Monitor: Macro vs Crypto (normalized)ALTSEASON Monitor: Macro vs Crypto (normalized)

Set 1W or 1M timeframe for the macro picture.

If your provider does not have some symbols, change the tickers in the script settings (for example, ETHBTC from another exchange).

For detailed trading, keep this monitor on the second window and watch local entries on individual charts.