MTF Commodity Oddity Index (CCI+)MTF Commodity Oddity Index (CCI+)

This chart overlay indicator is based upon the Commodity Channel Index (CCI) and can signal multiple triple-timeframe CCI overbought and oversold confluences directly onto your chart, intended for use as a confluence either for reversal trade entries, or potential trade exits, indicating where price may be probable to reverse.

Features include:

- Primary set of fully configurable triple-timeframe overbought and oversold signals, indicating where 3 selected timeframes are all overbought or all oversold at the same time. Enabled by default.

- Secondary set of fully configurable triple-timeframe overbought and oversold signals, indicating where 3 selected timeframes are all overbought or all oversold at the same time. Enabled by default.

- Optional drawing of background colours and/or ribbon seen at bottom of the chart image.

- The default primary MTF #1 timeframes are set to 1 minute, 5 minute and 15 minute. These are highly suitable for low timeframe scalpers trading on < 5m charts, and can often pin point price reversals.

- The default Secondary MTF #2 timeframes are set to 15 minute, 30 minute and 120 minute. These are suitable for both low timeframe scalpers and considerably higher timeframe traders.

- Independent alerts for MTF #1 and MTF #2 triple-timeframe confluences, including options for alerting MTF overbought and MTF oversold individually, as well as an option for alerting either overbought or oversold in a single combined alert.

- Also includes standard configurable CCI options, including CC length and source type.

Note: The features listed above are accurate at the time of publishing but maybe updated or added to in future.

A similar MTF CCI indicator is also available as a panel indicator here .

This indicator is based upon the original MTF Fantastic Stochastic (FS+) available here .

What is the Commodity Channel Index (CCI)?

Investopedia has described the popular oscillator as follows:

“The Commodity Channel Index (CCI) is a momentum-based oscillator used to help determine when an investment vehicle is reaching a condition of being overbought or oversold.

Developed by Donald Lambert, this technical indicator assesses price trend direction and strength, allowing traders to determine if they want to enter or exit a trade, refrain from taking a trade, or add to an existing position. In this way, the indicator can be used to provide trade signals when it acts in a certain way.”

You can read more about the CCI , its use cases and calculations here .

How do traders use overbought and oversold levels in their trading?

The oversold level, that is traditionally when the CCI is above the 100 level is typically interpreted as being 'overbought', and below the -100 level is typically considered 'oversold'. Traders will often use the CCI at an overbought level as a confluence for entry into a short position, and the CCI at an oversold level as a confluence for an entry into a long position. These levels do not mean that price will necessarily reverse at those levels in a reliable way, however. This is why this version of the CCI employs the triple timeframe overbought and oversold confluence, in an attempt to add a more confluence and reliability to this usage of the CCI . While traditionally, the overbought and oversold levels are below -100 for oversold, and above 100 for overbought, the default threshold settings of this indicator have been increased to provide fewer, stronger signals, especially suited to the low timeframes and highly volatile assets.

"股票开盘前15分钟交易规则" için komut dosyalarını ara

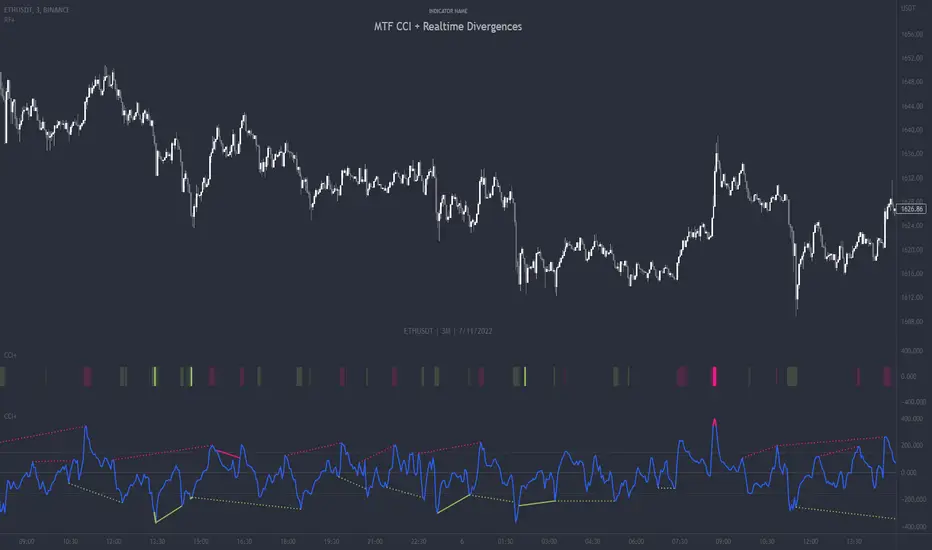

MTF CCI + Realtime DivergencesMulti-timeframe Commodity Channel Index (CCI) + Realtime Divergences + Alerts

This version of the CCI includes the following features:

- Optional 2x sets of triple-timeframe overbought and oversold signals with fully configurable timeframes and overbought and oversold thresholds, can indicate where 3 selected timeframes are all overbought or all oversold at the same time, with alert option.

- Optional divergence lines drawn directly onto the oscillator in realtime, with alert options.

- Configurable pivot periods to fine tune the divergences drawn in order to suit different trading styles and timeframes, including the ability to enable automatic adjustment of pivot period per chart timeframe.

- Alternate timeframe feature allows you to configure the oscillator to use data from a different timeframe than the chart it is loaded on.

- 'Hide oscillator' feature allows traders to hide the oscillator itself, leaving only the background colours indicating the overbought and oversold periods and/or MTF overbought and oversold confluences, as seen in the chart image.

- Also includes standard configurable CCI options, including CCI length and source type. Defaults set to length 20, and hlc3 source type.

- Optional Flip oscillator feature, allows users to flip the oscillator upside down, for use with Tradingviews 'Flip chart' feature (Alt+i), for the purpose of manually spotting divergences, where the trader has a strong natural bias in one direction, so that they can flip both the chart and the oscillator.

- Optional 'Fade oscillator' feature, which will fade out all but the most recent period, reducing visual noise on the chart.

While this version of the CCI has the ability to draw divergences in realtime along with related alerts so you can be notified as divergences occur without spending all day watching the charts, the main purpose of this indicator was to provide the triple-timeframe overbought and oversold confluence signals, in an attempt to add more confluence, weight and reliability to the single timeframe overbought and oversold states, commonly used for trade entry confluence. It's primary purpose is intended for scalping reversal trades on lower timeframes, typically between 1-15 minutes, which can be used in conjunction with the regular divergences the indicator can highlight. The triple timeframe overbought can often indicate near term reversals to the downside, with the triple timeframe oversold often indicating neartime reversals to the upside. The default timeframes for this confluence are set to check the 1m, 5m and 15m timeframes together, ideal for scalping the < 15 minute charts. The default settings for the MTF #1 timeframes (1m, 5m and 15m) are best used on a <5 minute chart.

Its design and use case is based upon the original MTF Stoch RSI + Realtime Divergences found here .

Commodity Channel Index (CCI)

Investopedia has described the popular oscillator as follows:

“The Commodity Channel Index (CCI) is a momentum-based oscillator used to help determine when an investment vehicle is reaching a condition of being overbought or oversold.

Developed by Donald Lambert, this technical indicator assesses price trend direction and strength, allowing traders to determine if they want to enter or exit a trade, refrain from taking a trade, or add to an existing position. In this way, the indicator can be used to provide trade signals when it acts in a certain way.”

You can read more about the CCI, its use cases and calculations here .

How do traders use overbought and oversold levels in their trading?

The oversold level, that is traditionally when the CCI is above the 100 level is typically interpreted as being 'overbought', and below the -100 level is typically considered 'oversold'. Traders will often use the CCI at an overbought level as a confluence for entry into a short position, and the CCI at an oversold level as a confluence for an entry into a long position. These levels do not mean that price will necessarily reverse at those levels in a reliable way, however. This is why this version of the CCI employs the triple timeframe overbought and oversold confluence, in an attempt to add a more confluence and reliability to this usage of the CCI. While traditionally, the overbought and oversold levels are below -100 for oversold, and above 100 for overbought, he default threshold settings of this indicator have been increased to provide fewer, stronger signals, especially suited to the low timeframes and highly volatile assets.

What are divergences?

Divergence is when the price of an asset is moving in the opposite direction of a technical indicator, such as an oscillator, or is moving contrary to other data. Divergence warns that the current price trend may be weakening, and in some cases may lead to the price changing direction.

There are 4 main types of divergence, which are split into 2 categories;

regular divergences and hidden divergences. Regular divergences indicate possible trend reversals, and hidden divergences indicate possible trend continuation.

Regular bullish divergence: An indication of a potential trend reversal, from the current downtrend, to an uptrend.

Regular bearish divergence: An indication of a potential trend reversal, from the current uptrend, to a downtrend.

Hidden bullish divergence: An indication of a potential uptrend continuation.

Hidden bearish divergence: An indication of a potential downtrend continuation.

How do traders use divergences in their trading?

A divergence is considered a leading indicator in technical analysis , meaning it has the ability to indicate a potential price move in the short term future.

Hidden bullish and hidden bearish divergences, which indicate a potential continuation of the current trend are sometimes considered a good place for traders to begin, since trend continuation occurs more frequently than reversals, or trend changes.

When trading regular bullish divergences and regular bearish divergences, which are indications of a trend reversal, the probability of it doing so may increase when these occur at a strong support or resistance level . A common mistake new traders make is to get into a regular divergence trade too early, assuming it will immediately reverse, but these can continue to form for some time before the trend eventually changes, by using forms of support or resistance as an added confluence, such as when price reaches a moving average, the success rate when trading these patterns may increase.

Typically, traders will manually draw lines across the swing highs and swing lows of both the price chart and the oscillator to see whether they appear to present a divergence, this indicator will draw them for you, quickly and clearly, and can notify you when they occur.

Setting alerts.

With this indicator you can set alerts to notify you when any/all of the above types of divergences occur, on any chart timeframe you choose, and also when the triple timeframe overbought and oversold confluences occur.

Configurable pivot period.

You can adjust the default pivot period values to suit your prefered trading style and timeframe. If you like to trade a shorter time frame, lowering the default lookback values will make the divergences drawn more sensitive to short term price action. By default, this indicator has enabled the automatic adjustment of the pivot periods for 4 configurable timeframes, in a bid to optimise the divergences drawn when the indicator is loaded onto any of the 4 timeframes. These timeframes and the auto adjusted pivot periods on each of them can also be reconfigured within the settings menu.

Disclaimer: This script includes code adapted from the Divergence for Many Indicators v4 by LonesomeTheBlue . With special thanks.

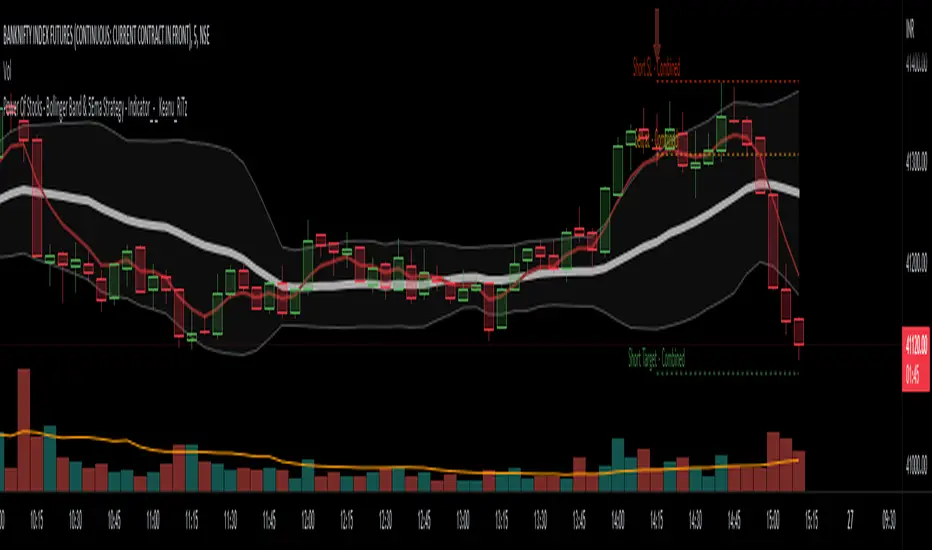

Power Of Stocks - Bollinger Band & 5Ema Indicator - Keanu_RiTz

Power of Stocks - Bollinger band & 5ema Strategy

In this script you get to take Buy/Sell trades using the 3 options mentioned below.(Alerts with price levels for buy/sell at , SL & Target are included in this one)

1. Combined Strategy :- uses confirmation from both strategies to trade.

2. Bollinger band Strategy :- use the Bollinger band Strategy to trade.

3. 5ema Strategy :- use the 5ema Strategy to trade.

1. Combined Strategy :-

for Selling :- we will go short/sell only when conditions of both strategies are satisfied.

i.e. when a candle is completely above the upper Bollinger band & completely above the 5ema then it will be our Alert Candle.

We Short/Sell only when the low of the Alert candle is broken or when the candle closes below the close of the Alert Candle.

SL will be above high of the Alert Candle. Target will be minimum 1:3 or as per your emotions.

for Buying:- we will go Long/Buy only when conditions of both strategies are satisfied.

i.e. when a candle is completely below the lower Bollinger band & completely below the 5ema then it will be our Alert Candle.

We go Long/Buy only when the high of the Alert candle is broken or when the candle closes above the close of the Alert Candle.

SL will be below low of the Alert Candle. Target will be minimum 1:3 or as per your emotions.

2. Power of Stocks - Bollinger Band Strategy :-

Bollinger band with standard deviation = 1.5

when a candle is completely above the upper Bollinger band, that candle will be called a signal/alert candle.

Initiate a Sell trade when that alert candles low is broken. SL will be above high of that alert candle.

Risk to reward ratio will be 1:4 i.e. target will be 4 times the SL.

when a candle is completely below the lower Bollinger band, that candle will be called a signal/alert candle.

Initiate a Buy trade when that alert candles high is broken. SL will be below low of that alert candle.

Risk to reward ratio will be 1:4 i.e. target will be 4 times the SL.

other rules for Options buying:- minimum 15min timeframe

The day you initiate the position , you should be in profit above 10%-15% then only you should carry forward that position overnight, otherwise squareoff your trade on that day only.

Buy ATM or slightly OTM, SL max 100 points , target 1:4

for Long-term/Investing :- Minimum Weekly

If candle is outside the lower band then initiate a Buy trade when that candles High is broken. Sl will be below Low of that candle.

for Long-term Target will be according to your emotions.

3. Power of Stocks - 5ema Strategy (target minimum 1:3)

Timeframe -

5 min for Selling (Sell Futures/index/stocks or buy Put)

15 min for Buying (Buy Futures/index/stocks or sell Put)

for selling stocks :-

you should enter trade within 10am , don't look for entries after that time. take only 2 entries a day.

for selling Index(Banknifty) :-

you can take trade at anytime of the day whenever conditions get satisfied. you can take multiple entries in banknifty as it is very volatile.

for options choose atm strikes: selling trade

sl for premium between 200-300 :- 20-30 points SL

sl for premium between 400-500 :- 40-50 points SL

sl for premium between 500-600 :- 50-60 points SL

Subhashish Pani's (power of stocks) 5 EMA Strategy:-

It plots 5 EMA and Buy/Sell signals with Target & Stoploss levels.

What is Subhashish Pani's (power of stocks) 5 EMA Strategy :-

His strategy is very simple to understand. for intraday use 5 minutes timeframe for selling. You can sell futures, sell call or buy Puts in selling strategy.

What this strategy tries to do is , it tries to catch the tops, so when you sell at top & it turns out to be a reversal point then you can get good profit.

this will hit stop losses often, but stop losses are small and minimum target should be 1:3. but if you stay with the trend you can get big profits.

According to Subhashish Pani this strategy has 60% success rate.

Strategy for Selling (Short future/Call/stock or buy Put)

When ever a Candle closes completely above 5 ema (no part of candle should be touching the 5ema), then that candle should be considered as Alert Candle.

If the next candle is also completely above 5 ema and it has not broken the low of previous alert candle, Then the previous Alert Candle should be ignored and the new candle should be considered as new Alert Candle.

so if this goes on then continue shifting the Alert Candle, but whenever the next candle breaks the low of the Alert Candle we should take the Short trade (Short future/Call/stock or buy Put).

Stoploss will be above high of the Alert Candle and minimum target will be 1:3.

Strategy for Buying (Buy future/Call/stock or sell Put)

When ever a Candle closes completely below 5 ema (no part of candle should be touching the 5ema), then that candle should be considered as Alert Candle.

If the next candle is also completely below 5 ema and it has not broken the high of previous alert candle, Then the previous Alert Candle should be ignored and the new candle should be considered as new Alert Candle.

so if this goes on then continue shifting the Alert Candle, but whenever the next candle breaks the high of the Alert Candle we should take the Long trade (Buy future/Call/stock or sell Put).

Stoploss will be below low of the Alert Candle and minimum target will be 1:3.

Buy/Sell with extra conditions :

it just adds 1 more condition to buying/selling

1. checks if closing of current candle is lower than alert candles closing for Selling & checks if closing of current candle is higher than alert candles closing for Buyling.

This can sometimes save you from false moves but by using this, you can also miss out on big moves as you'll enter trade after candle closing instead of entering at break of high/low.

Note :- According to Subhashish Pani Timeframe for intraday buying should be 15 minutes Timeframe.

If you haven't understood the strategy by reading above description, then search for "Subhashish Pani's (power of stocks) 5 EMA Strategy" on YouTube to get a deeper understanding.

Note:- This is not only for Intraday trading , you can use this strategy for Positional/Swing trading as well. If you use this on Monthly Timeframe then it can be very good for Long Term Investing as well.

Rules will be same for all types of trades & Timeframes.

[ChasinAlts] SuppRe-me ZonesHello fellow tradeurs, I couldn't find one similar on TV so wanted to make it.. Took me a little while to figure some things out as I am in new coding territory with this script. I had a hard time finding ways to make only a partial zone/box disappear if price only crossed part of it. Nonetheless, I figured it out so I hope you enjoy the outcome. Now, allow me to take a second to first explain the utility that is this script...or at least expose my reasoning when I decided to go ahead with this little project and take the precious time necessary to learn parts of pine that I did not previously know how to deal with. Ultimately, I built this for the 1s-15s TF(except for the "Consecutive Bars/Large Bars" Boxes...Those were meant to use on both these second TFs and Higher TFs.... ). The reasoning behind all of this was to give me a more definitive answer to all of my questions regarding the speed at which it would take price to revisit areas that it very abruptly went to/left on a VERY short TF (like the 1sec charts)...or even if it EVER would). To determine this I wanted to draw lines starting at the end of large wicks, draw boxes spanning the entire span of large wicks, and lastly to draw boxes spanning the entire span of very large bodies. For this last one, not only did I want to draw a box on a single candle that possessed a large body but also if there were consecutive red candles in a row, their bodies could be summed up and if this summation exceeds the minimum body % threshold then it too counts just like a single large candled body would if it was larger than the threshold. All in all I really enjoyed this script and most importantly the data that it produces. What I found after coding the script was that (again on the 1 sec- 15 sec charts) was that price very quickly (relatively speaking I suppose) came back over these box/zoned areas and that the lines drawn from the tip of the large wicks would at some point in the near future act as very good support and resistance for price to either bounce off of or breakout from.

Now, with each of these objects you can choose to delete them when price crosses the object or have them continuously drawn on the chart...your call...but it gets awful messy sometimes if you let them continue printing.

Peace and love people...peace and love,

-ChasinAlts

7EMA_6MA + Fill EMA++- You can add 7 EMAs and 6 SMAs to the chart

- You can fix the timeframe to display any moving average (for example, you can fix the EMA-20 for the daily timeframe and switch to a shorter time frame, for example, 15 minutes, while you will see the moving average for the daily chart),

- You can fill in the color of the cloud between the selected groups of moving averages, which serves as a good visualization of a trend change

- Вы можете добавить на график до 7 EMA и до 6 SMA одновременно

- Вы можете фиксировать таймфрейм для отображения любой скользящей (например, вы можете зафиксировать ЕМА-20 для дневного таймфрейма и переключиться на более короткий ТФ, например, на 15 минут, при этом вы будете видеть дневную скользящую),

- Вы можете заливать цветом облако между выбранными группами скользящих, что служит хорошей визуализацией изменения тренда

STD/C-Filtered, N-Order Power-of-Cosine FIR Filter [Loxx]STD/C-Filtered, N-Order Power-of-Cosine FIR Filter is a Discrete-Time, FIR Digital Filter that uses Power-of-Cosine Family of FIR filters. This is an N-order algorithm that turns the following indicator from a static max 16 orders to a N orders, but limited to 50 in code. You can change the top end value if you with to higher orders than 50, but the signal is likely too noisy at that level. This indicator also includes a clutter and standard deviation filter.

See the static order version of this indicator here:

STD/C-Filtered, Power-of-Cosine FIR Filter

Amplitudes for STD/C-Filtered, N-Order Power-of-Cosine FIR Filter:

What are FIR Filters?

In discrete-time signal processing, windowing is a preliminary signal shaping technique, usually applied to improve the appearance and usefulness of a subsequent Discrete Fourier Transform. Several window functions can be defined, based on a constant (rectangular window), B-splines, other polynomials, sinusoids, cosine-sums, adjustable, hybrid, and other types. The windowing operation consists of multipying the given sampled signal by the window function. For trading purposes, these FIR filters act as advanced weighted moving averages.

What is Power-of-Sine Digital FIR Filter?

Also called Cos^alpha Window Family. In this family of windows, changing the value of the parameter alpha generates different windows.

f(n) = math.cos(alpha) * (math.pi * n / N) , 0 ≤ |n| ≤ N/2

where alpha takes on integer values and N is a even number

General expanded form:

alpha0 - alpha1 * math.cos(2 * math.pi * n / N)

+ alpha2 * math.cos(4 * math.pi * n / N)

- alpha3 * math.cos(4 * math.pi * n / N)

+ alpha4 * math.cos(6 * math.pi * n / N)

- ...

Special Cases for alpha:

alpha = 0: Rectangular window, this is also just the SMA (not included here)

alpha = 1: MLT sine window (not included here)

alpha = 2: Hann window (raised cosine = cos^2)

alpha = 4: Alternative Blackman (maximized roll-off rate)

This indicator contains a binomial expansion algorithm to handle N orders of a cosine power series. You can read about how this is done here: The Binomial Theorem

What is Pascal's Triangle and how was it used here?

In mathematics, Pascal's triangle is a triangular array of the binomial coefficients that arises in probability theory, combinatorics, and algebra. In much of the Western world, it is named after the French mathematician Blaise Pascal, although other mathematicians studied it centuries before him in India, Persia, China, Germany, and Italy.

The rows of Pascal's triangle are conventionally enumerated starting with row n = 0 at the top (the 0th row). The entries in each row are numbered from the left beginning with k=0 and are usually staggered relative to the numbers in the adjacent rows. The triangle may be constructed in the following manner: In row 0 (the topmost row), there is a unique nonzero entry 1. Each entry of each subsequent row is constructed by adding the number above and to the left with the number above and to the right, treating blank entries as 0. For example, the initial number in the first (or any other) row is 1 (the sum of 0 and 1), whereas the numbers 1 and 3 in the third row are added to produce the number 4 in the fourth row.

Rows of Pascal's Triangle

0 Order: 1

1 Order: 1 1

2 Order: 1 2 1

3 Order: 1 3 3 1

4 Order: 1 4 6 4 1

5 Order: 1 5 10 10 5 1

6 Order: 1 6 15 20 15 6 1

7 Order: 1 7 21 35 35 21 7 1

8 Order: 1 8 28 56 70 56 28 8 1

9 Order: 1 9 36 34 84 126 126 84 36 9 1

10 Order: 1 10 45 120 210 252 210 120 45 10 1

11 Order: 1 11 55 165 330 462 462 330 165 55 11 1

12 Order: 1 12 66 220 495 792 924 792 495 220 66 12 1

13 Order: 1 13 78 286 715 1287 1716 1716 1287 715 286 78 13 1

For a 12th order Power-of-Cosine FIR Filter

1. We take the coefficients from the Left side of the 12th row

1 13 78 286 715 1287 1716 1716 1287 715 286 78 13 1

2. We slice those in half to

1 13 78 286 715 1287 1716

3. We reverse the array

1716 1287 715 286 78 13 1

This is our array of alphas: alpha1, alpha2, ... alphaN

4. We then pull alpha one from the previous order, order 11, the middle value

11 Order: 1 11 55 165 330 462 462 330 165 55 11 1

The middle value is 462, this value becomes our alpha0 in the calculation

5. We apply these alphas to the cosine calculations

example: + alpha4 * math.cos(6 * math.pi * n / N)

6. We then divide by the sum of the alphas to derive our final coefficient weighting kernel

**This is only useful for orders that are EVEN, if you use odd ordering, the following are the coefficient outputs and these aren't useful since they cancel each other out and result in a value of zero. See below for an odd numbered oder and compare with the amplitude of the graphic posted above of the even order amplitude:

What is a Standard Deviation Filter?

If price or output or both don't move more than the (standard deviation) * multiplier then the trend stays the previous bar trend. This will appear on the chart as "stepping" of the moving average line. This works similar to Super Trend or Parabolic SAR but is a more naive technique of filtering.

What is a Clutter Filter?

For our purposes here, this is a filter that compares the slope of the trading filter output to a threshold to determine whether to shift trends. If the slope is up but the slope doesn't exceed the threshold, then the color is gray and this indicates a chop zone. If the slope is down but the slope doesn't exceed the threshold, then the color is gray and this indicates a chop zone. Alternatively if either up or down slope exceeds the threshold then the trend turns green for up and red for down. Fro demonstration purposes, an EMA is used as the moving average. This acts to reduce the noise in the signal.

Included

Bar coloring

Loxx's Expanded Source Types

Signals

Alerts

Variety N-Tuple Moving Averages w/ Variety Stepping [Loxx]Variety N-Tuple Moving Averages w/ Variety Stepping is a moving average indicator that allows you to create 1- 30 tuple moving average types; i.e., Double-MA, Triple-MA, Quadruple-MA, Quintuple-MA, ... N-tuple-MA. This version contains 2 different moving average types. For example, using "50" as the depth will give you Quinquagintuple Moving Average. If you'd like to find the name of the moving average type you create with the depth input with this indicator, you can find a list of tuples here: Tuples extrapolated

Due to the coding required to adapt a moving average to fit into this indicator, additional moving average types will be added as they are created to fit into this unique use case. Since this is a work in process, there will be many future updates of this indicator. For now, you can choose from either EMA or RMA.

This indicator is also considered one of the top 10 forex indicators. See details here: forex-station.com

Additionally, this indicator is a computationally faster, more streamlined version of the following indicators with the addition of 6 stepping functions and 6 different bands/channels types.

STD-Stepped, Variety N-Tuple Moving Averages

STD-Stepped, Variety N-Tuple Moving Averages is the standard deviation stepped/filtered indicator of the following indicator

Last but not least, a big shoutout to @lejmer for his help in formulating a looping solution for this streamlined version. this indicator is speedy even at 50 orders deep. You can find his scripts here: www.tradingview.com

How this works

Step 1: Run factorial calculation on the depth value,

Step 2: Calculate weights of nested moving averages

factorial(depth) / (factorial(depth - k) * factorial(k); where depth is the depth and k is the weight position

Examples of coefficient outputs:

6 Depth: 6 15 20 15 6

7 Depth: 7 21 35 35 21 7

8 Depth: 8 28 56 70 56 28 8

9 Depth: 9 36 34 84 126 126 84 36 9

10 Depth: 10 45 120 210 252 210 120 45 10

11 Depth: 11 55 165 330 462 462 330 165 55 11

12 Depth: 12 66 220 495 792 924 792 495 220 66 12

13 Depth: 13 78 286 715 1287 1716 1716 1287 715 286 78 13

Step 3: Apply coefficient to each moving average

For QEMA, which is 5 depth EMA , the calculation is as follows

ema1 = ta. ema ( src , length)

ema2 = ta. ema (ema1, length)

ema3 = ta. ema (ema2, length)

ema4 = ta. ema (ema3, length)

ema5 = ta. ema (ema4, length)

In this new streamlined version, these MA calculations are packed into an array inside loop so Pine doesn't have to keep all possible series information in memory. This is handled with the following code:

temp = array.get(workarr, k + 1) + alpha * (array.get(workarr, k) - array.get(workarr, k + 1))

array.set(workarr, k + 1, temp)

After we pack the array, we apply the coefficients to derive the NTMA:

qema = 5 * ema1 - 10 * ema2 + 10 * ema3 - 5 * ema4 + ema5

Stepping calculations

First off, you can filter by both price and/or MA output. Both price and MA output can be filtered/stepped in their own way. You'll see two selectors in the input settings. Default is ATR ATR. Here's how stepping works in simple terms: if the price/MA output doesn't move by X deviations, then revert to the price/MA output one bar back.

ATR

The average true range (ATR) is a technical analysis indicator, introduced by market technician J. Welles Wilder Jr. in his book New Concepts in Technical Trading Systems, that measures market volatility by decomposing the entire range of an asset price for that period.

Standard Deviation

Standard deviation is a statistic that measures the dispersion of a dataset relative to its mean and is calculated as the square root of the variance. The standard deviation is calculated as the square root of variance by determining each data point's deviation relative to the mean. If the data points are further from the mean, there is a higher deviation within the data set; thus, the more spread out the data, the higher the standard deviation.

Adaptive Deviation

By definition, the Standard Deviation (STD, also represented by the Greek letter sigma σ or the Latin letter s) is a measure that is used to quantify the amount of variation or dispersion of a set of data values. In technical analysis we usually use it to measure the level of current volatility .

Standard Deviation is based on Simple Moving Average calculation for mean value. This version of standard deviation uses the properties of EMA to calculate what can be called a new type of deviation, and since it is based on EMA , we can call it EMA deviation. And added to that, Perry Kaufman's efficiency ratio is used to make it adaptive (since all EMA type calculations are nearly perfect for adapting).

The difference when compared to standard is significant--not just because of EMA usage, but the efficiency ratio makes it a "bit more logical" in very volatile market conditions.

See how this compares to Standard Devaition here:

Adaptive Deviation

Median Absolute Deviation

The median absolute deviation is a measure of statistical dispersion. Moreover, the MAD is a robust statistic, being more resilient to outliers in a data set than the standard deviation. In the standard deviation, the distances from the mean are squared, so large deviations are weighted more heavily, and thus outliers can heavily influence it. In the MAD, the deviations of a small number of outliers are irrelevant.

Because the MAD is a more robust estimator of scale than the sample variance or standard deviation, it works better with distributions without a mean or variance, such as the Cauchy distribution.

For this indicator, I used a manual recreation of the quantile function in Pine Script. This is so users have a full inside view into how this is calculated.

Efficiency-Ratio Adaptive ATR

Average True Range (ATR) is widely used indicator in many occasions for technical analysis . It is calculated as the RMA of true range. This version adds a "twist": it uses Perry Kaufman's Efficiency Ratio to calculate adaptive true range

See how this compares to ATR here:

ER-Adaptive ATR

Mean Absolute Deviation

The mean absolute deviation (MAD) is a measure of variability that indicates the average distance between observations and their mean. MAD uses the original units of the data, which simplifies interpretation. Larger values signify that the data points spread out further from the average. Conversely, lower values correspond to data points bunching closer to it. The mean absolute deviation is also known as the mean deviation and average absolute deviation.

This definition of the mean absolute deviation sounds similar to the standard deviation (SD). While both measure variability, they have different calculations. In recent years, some proponents of MAD have suggested that it replace the SD as the primary measure because it is a simpler concept that better fits real life.

For Pine Coders, this is equivalent of using ta.dev()

Bands/Channels

See the information above for how bands/channels are calculated. After the one of the above deviations is calculated, the channels are calculated as output +/- deviation * multiplier

Signals

Green is uptrend, red is downtrend, yellow "L" signal is Long, fuchsia "S" signal is short.

Included:

Alerts

Loxx's Expanded Source Types

Bar coloring

Signals

6 bands/channels types

6 stepping types

Related indicators

3-Pole Super Smoother w/ EMA-Deviation-Corrected Stepping

STD-Stepped Fast Cosine Transform Moving Average

ATR-Stepped PDF MA

STD-Stepped, Variety N-Tuple Moving Averages [Loxx]STD-Stepped, Variety N-Tuple Moving Averages is the standard deviation stepped/filtered indicator of the following indicator

Variety N-Tuple Moving Averages is a moving average indicator that allows you to create 1- 30 tuple moving average types; i.e., Double-MA, Triple-MA, Quadruple-MA, Quintuple-MA, ... N-tuple-MA. This version contains 5 different moving average types including T3. A list of tuples can be found here if you'd like to name the order of the moving average by depth: Tuples extrapolated

STD-Stepped, You'll notice that this is a lot of code and could normally be packed into a single loop in order to extract the N-tuple MA, however due to Pine Script limitations and processing paradigm this is not possible ... yet.

If you choose the EMA option and select a depth of 2, this is the classic DEMA ; EMA with a depth of 3 is the classic TEMA , and so on and so forth this is to help you understand how this indicator works. This version of NTMA is restricted to a maximum depth of 30 or less. Normally this indicator would include 50 depths but I've cut this down to 30 to reduce indicator load time. In the future, I'll create an updated NTMA that allows for more depth levels.

This is considered one of the top ten indicators in forex. You can read more about it here: forex-station.com

How this works

Step 1: Run factorial calculation on the depth value,

Step 2: Calculate weights of nested moving averages

factorial(nemadepth) / (factorial(nemadepth - k) * factorial(k); where nemadepth is the depth and k is the weight position

Examples of coefficient outputs:

6 Depth: 6 15 20 15 6

7 Depth: 7 21 35 35 21 7

8 Depth: 8 28 56 70 56 28 8

9 Depth: 9 36 34 84 126 126 84 36 9

10 Depth: 10 45 120 210 252 210 120 45 10

11 Depth: 11 55 165 330 462 462 330 165 55 11

12 Depth: 12 66 220 495 792 924 792 495 220 66 12

13 Depth: 13 78 286 715 1287 1716 1716 1287 715 286 78 13

Step 3: Apply coefficient to each moving average

For QEMA, which is 5 depth EMA , the caculation is as follows

ema1 = ta. ema ( src , length)

ema2 = ta. ema (ema1, length)

ema3 = ta. ema (ema2, length)

ema4 = ta. ema (ema3, length)

ema5 = ta. ema (ema4, length)

qema = 5 * ema1 - 10 * ema2 + 10 * ema3 - 5 * ema4 + ema5

Included:

Alerts

Loxx's Expanded Source Types

Bar coloring

Signals

Standard deviation stepping

Variety N-Tuple Moving Averages [Loxx]Variety N-Tuple Moving Averages is a moving average indicator that allows you to create 1- 30 tuple moving average types; i.e., Double-MA, Triple-MA, Quadruple-MA, Quintuple-MA, ... N-tuple-MA. This version contains 5 different moving average types including T3. A list of tuples can be found here if you'd like to name the order of the moving average by depth: Tuples extrapolated

You'll notice that this is a lot of code and could normally be packed into a single loop in order to extract the N-tuple MA, however due to Pine Script limitations and processing paradigm this is not possible ... yet.

If you choose the EMA option and select a depth of 2, this is the classic DEMA; EMA with a depth of 3 is the classic TEMA, and so on and so forth this is to help you understand how this indicator works. This version of NTMA is restricted to a maximum depth of 30 or less. Normally this indicator would include 50 depths but I've cut this down to 30 to reduce indicator load time. In the future, I'll create an updated NTMA that allows for more depth levels.

This is considered one of the top ten indicators in forex. You can read more about it here: forex-station.com

How this works

Step 1: Run factorial calculation on the depth value,

Step 2: Calculate weights of nested moving averages

factorial(nemadepth) / (factorial(nemadepth - k) * factorial(k); where nemadepth is the depth and k is the weight position

Examples of coefficient outputs:

6 Depth: 6 15 20 15 6

7 Depth: 7 21 35 35 21 7

8 Depth: 8 28 56 70 56 28 8

9 Depth: 9 36 34 84 126 126 84 36 9

10 Depth: 10 45 120 210 252 210 120 45 10

11 Depth: 11 55 165 330 462 462 330 165 55 11

12 Depth: 12 66 220 495 792 924 792 495 220 66 12

13 Depth: 13 78 286 715 1287 1716 1716 1287 715 286 78 13

Step 3: Apply coefficient to each moving average

For QEMA, which is 5 depth EMA, the caculation is as follows

ema1 = ta.ema(src, length)

ema2 = ta.ema(ema1, length)

ema3 = ta.ema(ema2, length)

ema4 = ta.ema(ema3, length)

ema5 = ta.ema(ema4, length)

qema = 5 * ema1 - 10 * ema2 + 10 * ema3 - 5 * ema4 + ema5

Included:

Alerts

Loxx's Expanded Source Types

Bar coloring

HDT CloudsHDT Clouds combines custom clouds such as the 200EMA/MA cloud indicator to create high confluence bounce zones when combined with VWAP. The HDT indicator combines various clouds with the Volume Weighted Average Price indicator and Standard Deviations which allow users to identify areas on the chart where the stock may reverse.

On smaller time frames, like the 5/15/30minute, the 200ema/ma cloud and VWAP (when sitting in the same relative area) creates pockets of supply or demand.

In addition, the various moving average clouds, such as the 8/9ema cloud and the 34/50ema cloud, create areas of supply and demand depending on the overall trend. If the stock is trending very strongly to the upside, the 8/9ema can be used as a potential bounce area. Whereas, if the stock is trending, but not quite as strong, the stock may have demand at the 34-50ema where the stock could see a potential bounce to the upside. What sets this indicator apart from other moving average clouds is the incorporation of VWAP/Standard Deviation and the combining of a 200EMA/MA indicator which creates a strong pocket of demand even on lower time frames such as the 5 or 15 minute time frame.

CFB-Adaptive CCI w/ T3 Smoothing [Loxx]CFB-Adaptive CCI w/ T3 Smoothing is a CCI indicator with adaptive period inputs and T3 smoothing. Jurik's Composite Fractal Behavior is used to created dynamic period input.

What is Composite Fractal Behavior ( CFB )?

All around you mechanisms adjust themselves to their environment. From simple thermostats that react to air temperature to computer chips in modern cars that respond to changes in engine temperature, r.p.m.'s, torque, and throttle position. It was only a matter of time before fast desktop computers applied the mathematics of self-adjustment to systems that trade the financial markets.

Unlike basic systems with fixed formulas, an adaptive system adjusts its own equations. For example, start with a basic channel breakout system that uses the highest closing price of the last N bars as a threshold for detecting breakouts on the up side. An adaptive and improved version of this system would adjust N according to market conditions, such as momentum, price volatility or acceleration.

Since many systems are based directly or indirectly on cycles, another useful measure of market condition is the periodic length of a price chart's dominant cycle, (DC), that cycle with the greatest influence on price action.

The utility of this new DC measure was noted by author Murray Ruggiero in the January '96 issue of Futures Magazine. In it. Mr. Ruggiero used it to adaptive adjust the value of N in a channel breakout system. He then simulated trading 15 years of D-Mark futures in order to compare its performance to a similar system that had a fixed optimal value of N. The adaptive version produced 20% more profit!

This DC index utilized the popular MESA algorithm (a formulation by John Ehlers adapted from Burg's maximum entropy algorithm, MEM). Unfortunately, the DC approach is problematic when the market has no real dominant cycle momentum, because the mathematics will produce a value whether or not one actually exists! Therefore, we developed a proprietary indicator that does not presuppose the presence of market cycles. It's called CFB (Composite Fractal Behavior) and it works well whether or not the market is cyclic.

CFB examines price action for a particular fractal pattern, categorizes them by size, and then outputs a composite fractal size index. This index is smooth, timely and accurate

Essentially, CFB reveals the length of the market's trending action time frame. Long trending activity produces a large CFB index and short choppy action produces a small index value. Investors have found many applications for CFB which involve scaling other existing technical indicators adaptively, on a bar-to-bar basis.

What is Jurik Volty used in the Juirk Filter?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

What is the T3 moving average?

Better Moving Averages Tim Tillson

November 1, 1998

Tim Tillson is a software project manager at Hewlett-Packard, with degrees in Mathematics and Computer Science. He has privately traded options and equities for 15 years.

Introduction

"Digital filtering includes the process of smoothing, predicting, differentiating, integrating, separation of signals, and removal of noise from a signal. Thus many people who do such things are actually using digital filters without realizing that they are; being unacquainted with the theory, they neither understand what they have done nor the possibilities of what they might have done."

This quote from R. W. Hamming applies to the vast majority of indicators in technical analysis . Moving averages, be they simple, weighted, or exponential, are lowpass filters; low frequency components in the signal pass through with little attenuation, while high frequencies are severely reduced.

"Oscillator" type indicators (such as MACD , Momentum, Relative Strength Index ) are another type of digital filter called a differentiator.

Tushar Chande has observed that many popular oscillators are highly correlated, which is sensible because they are trying to measure the rate of change of the underlying time series, i.e., are trying to be the first and second derivatives we all learned about in Calculus.

We use moving averages (lowpass filters) in technical analysis to remove the random noise from a time series, to discern the underlying trend or to determine prices at which we will take action. A perfect moving average would have two attributes:

It would be smooth, not sensitive to random noise in the underlying time series. Another way of saying this is that its derivative would not spuriously alternate between positive and negative values.

It would not lag behind the time series it is computed from. Lag, of course, produces late buy or sell signals that kill profits.

The only way one can compute a perfect moving average is to have knowledge of the future, and if we had that, we would buy one lottery ticket a week rather than trade!

Having said this, we can still improve on the conventional simple, weighted, or exponential moving averages. Here's how:

Two Interesting Moving Averages

We will examine two benchmark moving averages based on Linear Regression analysis.

In both cases, a Linear Regression line of length n is fitted to price data.

I call the first moving average ILRS, which stands for Integral of Linear Regression Slope. One simply integrates the slope of a linear regression line as it is successively fitted in a moving window of length n across the data, with the constant of integration being a simple moving average of the first n points. Put another way, the derivative of ILRS is the linear regression slope. Note that ILRS is not the same as a SMA ( simple moving average ) of length n, which is actually the midpoint of the linear regression line as it moves across the data.

We can measure the lag of moving averages with respect to a linear trend by computing how they behave when the input is a line with unit slope. Both SMA (n) and ILRS(n) have lag of n/2, but ILRS is much smoother than SMA .

Our second benchmark moving average is well known, called EPMA or End Point Moving Average. It is the endpoint of the linear regression line of length n as it is fitted across the data. EPMA hugs the data more closely than a simple or exponential moving average of the same length. The price we pay for this is that it is much noisier (less smooth) than ILRS, and it also has the annoying property that it overshoots the data when linear trends are present.

However, EPMA has a lag of 0 with respect to linear input! This makes sense because a linear regression line will fit linear input perfectly, and the endpoint of the LR line will be on the input line.

These two moving averages frame the tradeoffs that we are facing. On one extreme we have ILRS, which is very smooth and has considerable phase lag. EPMA has 0 phase lag, but is too noisy and overshoots. We would like to construct a better moving average which is as smooth as ILRS, but runs closer to where EPMA lies, without the overshoot.

A easy way to attempt this is to split the difference, i.e. use (ILRS(n)+EPMA(n))/2. This will give us a moving average (call it IE /2) which runs in between the two, has phase lag of n/4 but still inherits considerable noise from EPMA. IE /2 is inspirational, however. Can we build something that is comparable, but smoother? Figure 1 shows ILRS, EPMA, and IE /2.

Filter Techniques

Any thoughtful student of filter theory (or resolute experimenter) will have noticed that you can improve the smoothness of a filter by running it through itself multiple times, at the cost of increasing phase lag.

There is a complementary technique (called twicing by J.W. Tukey) which can be used to improve phase lag. If L stands for the operation of running data through a low pass filter, then twicing can be described by:

L' = L(time series) + L(time series - L(time series))

That is, we add a moving average of the difference between the input and the moving average to the moving average. This is algebraically equivalent to:

2L-L(L)

This is the Double Exponential Moving Average or DEMA , popularized by Patrick Mulloy in TASAC (January/February 1994).

In our taxonomy, DEMA has some phase lag (although it exponentially approaches 0) and is somewhat noisy, comparable to IE /2 indicator.

We will use these two techniques to construct our better moving average, after we explore the first one a little more closely.

Fixing Overshoot

An n-day EMA has smoothing constant alpha=2/(n+1) and a lag of (n-1)/2.

Thus EMA (3) has lag 1, and EMA (11) has lag 5. Figure 2 shows that, if I am willing to incur 5 days of lag, I get a smoother moving average if I run EMA (3) through itself 5 times than if I just take EMA (11) once.

This suggests that if EPMA and DEMA have 0 or low lag, why not run fast versions (eg DEMA (3)) through themselves many times to achieve a smooth result? The problem is that multiple runs though these filters increase their tendency to overshoot the data, giving an unusable result. This is because the amplitude response of DEMA and EPMA is greater than 1 at certain frequencies, giving a gain of much greater than 1 at these frequencies when run though themselves multiple times. Figure 3 shows DEMA (7) and EPMA(7) run through themselves 3 times. DEMA^3 has serious overshoot, and EPMA^3 is terrible.

The solution to the overshoot problem is to recall what we are doing with twicing:

DEMA (n) = EMA (n) + EMA (time series - EMA (n))

The second term is adding, in effect, a smooth version of the derivative to the EMA to achieve DEMA . The derivative term determines how hot the moving average's response to linear trends will be. We need to simply turn down the volume to achieve our basic building block:

EMA (n) + EMA (time series - EMA (n))*.7;

This is algebraically the same as:

EMA (n)*1.7-EMA( EMA (n))*.7;

I have chosen .7 as my volume factor, but the general formula (which I call "Generalized Dema") is:

GD (n,v) = EMA (n)*(1+v)-EMA( EMA (n))*v,

Where v ranges between 0 and 1. When v=0, GD is just an EMA , and when v=1, GD is DEMA . In between, GD is a cooler DEMA . By using a value for v less than 1 (I like .7), we cure the multiple DEMA overshoot problem, at the cost of accepting some additional phase delay. Now we can run GD through itself multiple times to define a new, smoother moving average T3 that does not overshoot the data:

T3(n) = GD ( GD ( GD (n)))

In filter theory parlance, T3 is a six-pole non-linear Kalman filter. Kalman filters are ones which use the error (in this case (time series - EMA (n)) to correct themselves. In Technical Analysis , these are called Adaptive Moving Averages; they track the time series more aggressively when it is making large moves.

Included:

Bar coloring

Signals

Alerts

Price Pivots for NSE Index & F&O StocksPrice Pivots for NSE Index & F&O Stocks

What is this Indicator?

• This indicator calculates the price range a Stock or Index can move in a Day, Week or Month.

Advantages of this Indicator

• This is a Leading indicator, not Dynamic or Repaint.

• Helps to identify the tight range of price movement.

• Can easily identify the Options strike price.

• The levels are more reliable and authentic than Gann Square of 9 Levels.

• Develops a discipline in placing Targets.

Disadvantages of this Indicator

• The indicator is specifically made for National Stock Exchange of India (NSE) listed index and stocks.

• The indicator is calculated only for index NIFTY, BANKNIFTY, FINNIFTY, MIDCPNIFTY and Stocks listed in Futures and Options.

• The indicator shows nothing for other indexes and stocks other than above mentioned.

• The data need to be entered manually.

• The data need to be updated manually when the F&O listed stocks are updated.

Who to use?

Highly beneficial for Day Traders, it can be used for Swing and Positions as well.

What timeframe to use?

• Any timeframe.

• The highlighted levels in Red and Green will not show correct levels in 1 minute timeframe.

• 5min is recommended for Day Traders.

When to use?

• Wait for proper swing to form.

• Recommended to avoid 1st 1 hour or market open, that is 9.15am to 10.15 or 10.30am.

• Within this time a proper swing will be formed.

How to use?

Entry

• Enter when the Price reach closer to the Blue line.

• Enter Long when the Price takes a pullback or breakout at the Red lines.

Exit

• Exit position when the Price reach closer to the Red lines in Long positions.

What are the Lines?

Gray Lines:

• Every lines with price labels are the Strike Prices in the Option Chain from NSE website.

• Price moves from 1 Strike Price level to another.

• The dashed lines are average levels of 2 Strike Prices.

Red & Green Lines:

• The Red and Green Lines will appear only after the first 1 hour.

• The levels are calculated based on the 1st 1 hour.

• Red Lines are important Resistance levels, these are strong Bearish reversal points. It is also a breakout level, this need to be figured out from the past levels, trend, percentage change and consolidation.

• Green Lines are important Support levels, these are strong Bullish reversal points. It is also a breakdown level, this need to be figured out from the past levels, trend, percentage change and consolidation.

What are the Labels?

• First Number: Price of that level.

• Numbers in (): Percentage change and Change of price from LTP(Last Traded Price) to that Level.

How to use?

Entry:

• Enter when price is closer to the Red or Green lines.

• Enter after considering previous Swing and Trend.

• Note the 50% of previous Swing.

• Enter Short when price reverse from each level.

• If 50% of swing and the pivot level is closer it can be a good entry.

Exit:

• Use the logic of Entry, each level can be a target.

• Exit when price is closer to the Red or Green lines.

Indicator Menu

Source

• Custom: Enter the price manually after choosing the Source as Custom to show the Pivots at that price.

• LTP: Pivot is calculated based on Last Traded Price.

• Day Open: Pivot is calculated based on current day opening price.

• PD Close: Pivot is calculated based on previous day closing price.

• PD HL2: Pivot is calculated based on previous day average of High and Low.

• PD HLC3: Pivot is calculated based on previous day average of High, Low and Close.

"Time (IST) (Vertical)"

• This is a marker of every 1 hour.

• Usually major price movement happen between previous day last 1 hour (2:15 pm) to today first 1 hour (10:15 pm).

• Two swings can happen between first 2 hour of current day.

• At the end of the day last 1 hour from 2.15 pm another important movement will happen.

• Usually rest of the time won't show any interesting movement.

To the Users

• Certain symbols may show the levels as a single line. For such symbols choose a different Source or Timeframe from the indicator menu.

• Please inform if any of the Symbol's price levels don't react to the pivots, include the Symbol a well.

• Also inform if you notice any wrong values, errors or abnormal behavior in the indicator.

• Feel free to suggest or adding new features and options.

General Tips

• It is good if Stock trend is same as that of NIFTY trend.

• Lots of indicators creates lots of confusion.

• Keep the chart simple and clean.

• Buy Low and Sell High.

• Master averages or 50%.

• Previous Swing High and Swing Low are crucial.

psk 15min levels This indicator plots 15 minute high low values . It also plots 15 minute range mid point and other levels.

Singular and Cumulative Volume Delta (SVD+CVD)This a Volume Delta indicator with Cumulative Volume Delta.

I have been studying Volume Delta and CVD trading strategies and indicator styles.

This implementation was developed to test a basic trailing window / oscillator approach.

Script has been republished as public and searchable.

Changelog from private era follows.

Jun 9 (2022)

Release Notes:

Added option to use EMA/SMA based cumulation. This will not scale well with singular data, so default view is still SUM.

Jun 9 (2022)

Release Notes:

Outdated comment correction.

Jun 9 (2022)

Release Notes:

Added default option to normalilze visual scale of MA cumulation types. The averaging creates a singular value sized results, instead of a range-sums. This multiples that candle result by the range length to get a range-sum sized result.

Added option to scale the cumulation size relative to the volume size. 1-to-1 scaling creates singular deltas that can be hard to see with all options on. This allows you to beef them up for visual or weighting purposes.

Jun 15 (2022)

Release Notes: * Added break even level for current delta. Tells where current delta must land for cumulative delta to stay flat.

* Added comparison of historical cumulative levels to current level. The historical levels are the initial values going into current accumulation window.

* Changed title of indicator to be more generic, clear, and searchable.

Jun 15 (2022)

Release Notes: * Added option to have the cumulation cutoff line AFTER or OVER the end of the cumulation window. This change is to ensure the indicator clearly documents it's behavior and avoids confusion on this / last cumulation window semantics.

* Bugfix: Initial levels were pulled from cumulation line which was AFTER end of window. This has been changed to the initial values INSIDE the cumulation window.

* Code cleanup.

June 17th (2022)

Release Notes: Marked as beta because TV confirmed they no longer allow private scripts to be changed to public. (Despite lingering documentation that says otherwise.

June 17th (2022)

Re-published as public.

sm trend analyzer█ OVERVIEW

This script is intended to provide full time frame continuity information for almost all time frames (3, 5, 15, 30, 60, 4H, Day, Week, Month, Quarter, Year)

When added, the script provides a visual indicator/table to the bottom right of the screen to view the different performance at each time frame.

----------

Output

Time Frames: 3min, 5min, 15min, 30min, 60min, 4 Hour, Day, Week, Month Quarter, Year

Time Frame Labels: 3, 5, 15, 30, H, 4H, D, W, M, Q, Y

Colors: Will display the colors in RED if it's a down time frame (close/current < prior close) or a GREEN if it's a up time frame (close/current > prior close), the color will be more opaque/the opacity will increase the stronger it's levels are for the time frame.

Percentage: The percentages will also display, to give you a quick visual indicator or how strong a time frame is one way or the other.

Best Practices

----------

Had to decouple this from the other scripts because TV limits how much you can plot/show

May be a little slow at times, analyzing a lot of time periods/data be patient.

Used to indicate who is in control, buyers or sellers.

Jul 28, 2021

Release Notes: Fix study name, add some padding (high percentages are hard to get one the whole table)

Jul 28, 2021

Release Notes: Add more space... fix logic. It's open and close not close and prior close for FTC.

Jul 28, 2021

Release Notes: Set the width to ensure the whole percentage is shown. Also stack the cells (2 rows of 6) so it's more compressed and easier to read. Added in the 2H indicator as well.

Aug 2, 2021

Release Notes: Changes: added the ability to disable/hide each box and the ability to change the time frame of each box. The boxes are sequentially numbered, 1 - 12, left to right, top to bottom. So the first box, or 1, would be the top left, 2 would be the next box, all the way to 12 at the bottom right.

Customizable Non-Repainting HTF MACD MFI Scalper Bot Strategy v2Customizable Non-Repainting HTF MACD MFI Scalper Bot Strategy v2

This script was originally shared by Wunderbit as a free open source script for the community to work with. This is my second published iteration of this idea.

WHAT THIS SCRIPT DOES:

It is intended for use on an algorithmic bot trading platform but can be used for scalping and manual trading.

This strategy is based on the trend-following momentum indicator . It includes the Money Flow index as an additional point for entry.

This is a new and improved version geared for lower timeframes (15-5 minutes), but can be run on larger ones as well. I am testing it live as my high frequency trader.

HOW IT DOES IT:

It uses a combination of MACD and MFI indicators to create entry signals. Parameters for each indicator have been surfaced for user configurability.

Take profits are now trailing profits, and the stop loss is now fixed. Why? I found that the trailing stop loss with ATR in the previous version yields very good results for back tests but becomes very difficult to deploy live due to transaction fees. As you can see the average trade is a higher profit percentage than the previous version.

HOW IS MY VERSION ORIGINAL:

Now instead of using ATR stop loss, we have a fixed stop loss - counter intuitively to what some may believe this performs better in live trading scenarios since it gives the strategy room to move. I noticed that the ATR trailing stop was stopping out too fast and was eating away balance due to transaction fees.

The take profit on the other hand is now a trailing profit with a customizable deviation. This ensures that you can have a minimum profit you want to take in order to exit.

I have depracated the old ATR trailing stop as it became too confusing to have those as different options. I kept the old version for others that want to experiment with it. The source code still requires some cleanup, but its fully functional.

I added in a way to show RSI values and ATR values with a checkbox so that you can use the new an improved ATR Filter (and grab the right RSI values for the RSI filter). This will help to filter out times of very low volatility where we are unlikely to find a profitable trade. Use the "Show Data" checkbox to see what the values are on the indicator pane, then use those values to gauge what you want to filter out.

Both versions

Delayed Signals : The script has been refactored to use a time frame drop down. The higher time frame can be run on a faster chart (recommended on one minute chart for fastest signal confirmation and relay to algotrading platform.)

Repainting Issues : All indicators have been recoded to use the security function that checks to see if the current calculation is in realtime, if it is, then it uses the previous bar for calculation. If you are still experiencing repainting issues based on intended (or non intended use), please provide a report with screenshot and explanation so I can try to address.

Filtering : I have added to additional filters an ABOVE EMA Filter and a BELOW RSI Filter (both can be turned on and off)

Customizable Long and Close Messages : This allows someone to use the script for algorithmic trading without having to alter code. It also means you can use one indicator for all of your different alterts required for your bots.

HOW TO USE IT:

It is intended to be used in the 5-30 minute time frames, but you might be able to get a good configuration for higher time frames. I welcome feedback from other users on what they have found.

Find a pair with high volatility (example KUCOIN:ETH3LUSDT ) - I have found it works particularly well with 3L and 3S tokens for crypto. although it the limitation is that confrigurations I have found to work typically have low R/R ratio, but very high win rate and profit factor.

Ideally set one minute chart for bots, but you can use other charts for manual trading. The signal will be delayed by one bar but I have found configurations that still test well.

Select a time frame in configuration for your indicator calculations.

Select the strategy config for time frame (resolution). I like to use 5 and 15 minutes for scalping scenarios, but I am interested in hearing back from other community memebers.

Optimize your indicator without filters : customize your settings for MACD and MFI that are profitable with your chart and selected time frame calculation. Try different Take Profits (try about 2-5%) and stop loss (try about 5-8%). See if your back test is profitable and continue to optimize.

Use the Trend, RSI, ATR Filter to further refine your signals for entry. You will get less entries but you can increase your win ratio.

You can use the open and close messages for a platform integration, but I choose to set mine up on the destination platform and let the platform close it. With certain platforms you cannot be sure what your entry point actually was compared to Trading View due to slippage and timing, so I let the platform decide when it is actually profitable.

Limitations: this works rather well for short term, and does some good forward testing but back testing large data sets is a problem when switching from very small time frame to large time frame. For instance, finding a configuration that works on a one minute chart but then changing to a 1 hour chart means you lose some of your intra bar calclulations. There are some new features in pine script which might be able to address, this, but I have not had a chance to work on that issue.

Everything Bitcoin [Kioseff Trading]Hello!

This script retrieves most of the available Bitcoin data published by Quandl; the script utilizes the new request.security_lower_tf() function.

Included statistics,

True price

Volume

Difficulty

My Wallet # Of Users

Average Block Size

api.blockchain size

Median Transaction Confirmation Time

Miners' Revenue

Hash Rate

Cost Per Transaction

Cost % of Transaction Volume

Estimated Transaction Volume USD

Total Output Volume

Number Of Transactions Per Block

# of Unique BTC Addresses

# of BTC Transactions Excluding Popular Addresses

Total Number of Transactions

Daily # of Transactions

Total Transaction Fees USD

Market Cap

Total BTC

Retrieved data can be plotted as line graphs; however, the data is initially split between two tables.

The image above shows how the requested Bitcoin data is displayed.

However, in the user inputs tab, you can modify how the data is displayed.

For instance, you can append the data displayed in the floating statistics box to the stagnant statistics box.

The image above exemplifies the instance.

You can hide any and all data via the user inputs tab.

In addition to data publishing, the script retrieves lower timeframe price/volume/indicator data, to which the values of the requested data are appended to center-right table.

The image above shows the script retrieving one-minute bar data.

Up arrows reflect an increase in the more recent value, relative to the immediately preceding value.

Down arrows reflect a decrease in the more recent value relative to the immediately preceding value.

The ascending minute column reflects the number of minutes/hours (ago) the displayed value occurred.

For instance, 15 minutes means the displayed value occurred 15 minutes prior to the current time (value).

Volume, price, and indicator data can be retrieved on lower timeframe charts ranging from 1 minute to 1440 minutes.

The image above shows retrieved 5-minute volume data.

Several built-in indicators are included, to which lower timeframe values can be retrieved.

The image above shows LTF VWAP data. Also distinguished are increases/decreases for sequential values.

The image above shows a dynamic regression channel. The channel terminates and resets each fiscal quarter. Previous channels remain on the chart.

Lastly, you can plot any of the requested data.

The new request.security_lower_tf() function is immensely advantageous - be sure to try it in your scripts!

Time FunctionsLibrary "TimeFunctions"

Utility functions to handle time in Pine Script

TimeframetoInt()

Returns an int that corresponds to a timeframe string:

"1" => 1

"5" => 5

"10" => 10

"15" => 15

"30" => 30

"60" => 60

"H1" => 60

"H4" => 240

"1D" => 1440

BarsSinceOpen()

Returns the number of bars that have passed since the opening of the New York Session.

Weighted Relative Strength IndexWRSI uses 3 different user defined time frames with user defined weight on each time frame to give a final RSI value

Default values:

RSI 1 = 5 minute timeframe with a weightage of 9:14

RSI 2 = 15 minute timeframe with a weightage of 4:14

RSI 1 = 60 minute timeframe with a weightage of 1:14

Works best on a 15 min chart.

Please note this indicator will show exactly same values on all time frame charts so if you are looking at a daily chart you may want to change to 60 min, Daily & Weekly RSI time frame in settings.

The weights used here are basically sqaures of 1,2,& 3, you may choose any numbers that work for you.

The RSI length taken here is 27 (count of nakshatras)

The RSI MA length taken here is 28 (count of nakshatras + Abhijit Nakshatra)

You can obviously change it to what works best for you.

Leg/Base & GAP CandlesThis script, redraws the Minute, Hourly, Daily, Weekly, Monthly candles for gap up and gap down situation. Also this candle marks the LEG candles and BASE Candles with different colors to mark the supply and demand zone.

This script is only for Indian NSE markets (09:15 to 15:30) for GAP up/GAP down redraw.

This script is most beneficial for TradeLegend students.

This script is originally made by me, and no code has been modified or copied from anywhere else except Pinescript documentation.

JaeRSI+What is JaeRSI++

🥇 It is an indicator that detects and displays the RSI of the upper frame one step at a time

- It is no different from normal RSI but, u can see the RSI of the upper frame together

- Works based on 5m 15m 1h 4h 1d 1w

🥇Also, if the RSI is (over 70↗️) or (less than 30↘️), changes the background color

- If the background color is continuous, it is recommended to check the frame one step higher

🥇 Meaning of table (table)

- "🌈", RSI, Main, Danger in order

- RSI: It is divided into 5, 15, 60, 240 and indicates the current RSI of each frame (the background color is different from RSI : 33.0 below / 67.0 above)

- Main: Estimate the mainframe

If the previous 14 candles have entered the Danger zone (RSI : below 33.0 / above 67.0) or oversold/number, the corresponding frame is marked as the main frame.

- Danger: If abnormal RSI motion is detected (beam shape) due to sudden surge/fall in a frame, it warns that the frame may be the main frame.

==================================================================================

JaeRSI++란?

🥇 상위 프레임의 RSI를 추가로 표시해 주는 RSI 지표입니다

- 일반 RSI와 알고리즘의 차이가 없으나 상위 프레임의 RSI를 함께 볼 수 있습니다 (빨간 선으로 표시)

- 5m 15m 1h 4h 1d 1w 기준으로 작동합니다

🥇또한 RSI가 (70 이상↗️) 또는 (30↘️)인 경우 배경색을 변경합니다

- 배경색이 연속적인 경우 프레임을 한 단계 높게 확인하는 것이 좋습니다

🥇표(테이블)의 의미

- 순서대로 시간프레임 , RSI , 메인 , 위험

- RSI : 5, 15, 60, 240으로 나뉘어져 각각 프레임의 현재 RSI를 나타낸다 (33.0 아래 / 67.0 위 부터 배경색이 달라짐)

- 메인 : 메인프레임을 추정한다

이전 14개 캔들안에 꺵판존(33.0 아래 / 67.0 위) or 과매도/수에 들어간 적이 있다면 해당 프레임을 메인프레임으로 표시한다

- 위험 : 어떤 프레임에서 급등/급락하여 비 정상적인 RSI의 움직임이 감지된다면(빔 형태) 해당 프레임이 메인 프레임일 수 있다고 경고한다

Heikin Ashi CountObjective:

This indicator aims to obtain an oscillator indicating the trend of a market by minimizing noise through the use of Heikin Ashi candles.

The idea is to make the oscillator tend towards 100 at each bullish Heikin Ashi candle, and inversely towards 0 when bearish.

The advantage is that this indicator has little noise compared to the RSI, but also little lag compared to the Schaff Trend Cycle, which are the two indicators that inspired me to create this one.

Usage:

As a general rule, below 15, HA Count indicates an oversell and above 85 an overbuy.

Setting the length for the candle count results in an indicator that is less sensitive when close to 1 and more sensitive when it is at 2 or higher.

Chosen as the default value, 1.15 seems to give the best indications, regardless of the market or time period.

Also it looks very similar to the values that the RSI could give set over 14 periods, so it can be used in the same way. Especially with regard to divergences.

---- FR ----

Objectif :

Cet indicateur vise à obtenir un oscillateur indicant la tendance d'un marché en minimisant le bruit grace à l'utilisation des bougies Heikin Ashi.

L'idée est de faire tendre l'oscillateur vers 100 à chaque bougie Heikin Ashi haussière, et inversement vers 0 lorsque baissière.

L'avantage est que cet indicateur a peu de bruit comparé au RSI, mais peu de lag aussi comparé au Schaff Trend Cycle, qui sont les deux indicateurs qui m'ont inspiré pour la création de celui-ci.

Utilisation :

En régle général, en dessous de 15 HA Count indique une sur-vente et au-dessus de 85 un sur-achat.

Le paramétrage de la longueur pour le comptage de bougie permet d'obtenir un indicateur moins sensible lorsque proche de 1 et plus sensible lorsqu'il est à 2 ou supérieur.

Choisie comme valeur par défaut, 1.15 semble donner les meilleures indications, peu importe le marché ou la période de temps.

En outre cela ressemble beaucoup aux valeurs que pourrait donner le RSI régler sur 14 périodes, ainsi il peut être utilisé de la même manière. Notamment pour ce qui est des divergences.

Volatility Risk Premium GOLD & SILVER 1.0ENGLISH

This indicator (V-R-P) calculates the (one month) Volatility Risk Premium for GOLD and SILVER.

V-R-P is the premium hedgers pay for over Realized Volatility for GOLD and SILVER options.

The premium stems from hedgers paying to insure their portfolios, and manifests itself in the differential between the price at which options are sold (Implied Volatility) and the volatility GOLD and SILVER ultimately realize (Realized Volatility).

I am using 30-day Implied Volatility (IV) and 21-day Realized Volatility (HV) as the basis for my calculation, as one month of IV is based on 30 calendaristic days and one month of HV is based on 21 trading days.

At first, the indicator appears blank and a label instructs you to choose which index you want the V-R-P to plot on the chart. Use the indicator settings (the sprocket) to choose one of the precious metals (or both).

Together with the V-R-P line, the indicator will show its one year moving average within a range of +/- 15% (which you can change) for benchmarking purposes. We should consider this range the “normalized” V-R-P for the actual period.

The Zero Line is also marked on the indicator.

Interpretation

When V-R-P is within the “normalized” range, … well... volatility and uncertainty, as it’s seen by the option market, is “normal”. We have a “premium” of volatility which should be considered normal.

When V-R-P is above the “normalized” range, the volatility premium is high. This means that investors are willing to pay more for options because they see an increasing uncertainty in markets.

When V-R-P is below the “normalized” range but positive (above the Zero line), the premium investors are willing to pay for risk is low, meaning they see decreasing uncertainty and risks in the market, but not by much.

When V-R-P is negative (below the Zero line), we have COMPLACENCY. This means investors see upcoming risk as being lower than what happened in the market in the recent past (within the last 30 days).

CONCEPTS :

Volatility Risk Premium

The volatility risk premium (V-R-P) is the notion that implied volatility (IV) tends to be higher than realized volatility (HV) as market participants tend to overestimate the likelihood of a significant market crash.