RSI ModifiedThe RSI is an excellent indicator for determining when equities are overbought/oversold. Though I believe there is a shortcoming in using the 70/30 levels since they are static and do not adjust for when an equity is trending. It stands to reason that in a downtrend, the overbought might be less than 70 and the oversold less than 30—Vice versa for a bull trend. Using the built-in function of pivots, I have attempted to create overbought/oversold lines that adjust with the trend. Leaving the 70/30 lines on the indicator also helps visualize the equity trend. All pivot settings are adjustable in the input menu. The pivot limits serve as a filter for recording pivot points. For example, with an upper pivot limit of 60, only pivots greater than 60 will be recorded into the array used to determine overbought. The crosses represent which values are used to determine overbought/oversold and do not provide timely indications.

"美元汇率30天走势" için komut dosyalarını ara

Commodity Channel Relative StrengthNew concept(I think atleast) I've joined the Standard RSI and CCI at the hip with another plotcandle, which gives a picture of a larger candle With more interesting movement imo. Includes Fib Retracement Levels, High/Low and a couple of coppock curves for more confirmation. Broadening candles seem to indicate a weakening of trend strength (from what i've seen atleast) although exceptions do occur. Vice versa for tapering to a lesser degree I imagine. RSI has been shifted down to 0 to align the center point with the CCI , so the usual 30/70 RSI Levels are now -20/20 (although I have 30/-30 instead for the hlines).

SPY Volume Weighted CloseHey everyone!

Deciding to make this indicator public and open access.

This is a volume weighted close indicator for SPY. It is a statistics based indicator.

How it works:

It uses volume data mixed with some price action data to prospectively predict where SPY's price will close within a 30 minute interval.

As such, its different from other indicators in the sense that its not reactive, it proactive and actively predicts the price that SPY will see within the next 30 minutes and where SPY will most likely close at.

It has 3 bands. The main centre band (blue, but colour can be changed) is the most likely price that SPY will close at within the next 30 minutes.

The Upper Level Confidence and Lower Level Confidence bands are the expected range that the analysis thinks SPY will remain confined in based on current volume and price action.

How to Use it:

I personally use this in place of VWAP, but the applications are infinite. Take a look at the chart below:

Applications:

This is specifically programmed for SPY but I have used it with other stocks such as QQQ, UPRO and DIA. However, using it with those stocks, the upper and lower confidence bands are not helpful. But YMMV with other stocks. This is specifically designed for SPY.

Let me know your questions and thoughts!

Thanks for reading and checking this out!

Customizable OCC Non Repainting Scalper Bot v7.0bThis strategy is intended to be used on an automated trading platform and should be run on a one minute chart for fastest confirmations and signal relay to crypto automation platform. The strategy has been modded to only go long at this time to focus on profitability for one direction. The open long and close long text fields allow you to use your own webhook message for this purpose.

I have spent quite a bit of time and I figured I would put it out to the community to share the work and also get some feedback.

Ok, so let me say that I have done absolutely everything I can to make the strategy not repaint while still maintaining it's profitability. It has been a challenge so I am publishing this to the community to help test this.

What I have observed: the strategy will not repaint in real time. That is, if you have the chart open and keep it open, the signals are the same as the ones that are sent out by the strategy. In certain cases, when I reload the chart- the signals might be off from what was sent. In some ways, that is repainting, but it is repainting based on losing the real time data and recalculating from a different set of bars- since I am running it on a one minute chart then the start becomes different when you refresh.

To address repainting while keeping the strategy calculating as quickly as possibly I have altered the logic in the following ways:

I have made an assumption which might not work for everyone- at the first tick of the next bar, you can almost safefly assume in crypto that if you are looking at the previous bar for information, the open of the current bar was the close of the previous bar. This for the most part holds true in crypto with good liquidity. If you are trading a pair that jumps around due to low volume- this might not be the strategy to use. I might publish a different version with a different logic.

I have altered the security repaint to use isbarconfirmed, so at the very end of the bar (as soon as the bar is confirmed), we recalculate to the higher time frames. So as soon as the data is available, it is at that point that we can then safely calculate higher time frames. This is unique and experimental, but seems to do well at creating good signals for entry.

I have employed my own intervals by utilizing the resolution as an integer (used by the previous authors)- but in this case, I use the interval to take a snapshot of the higher time frame. With open close cross, the different moving averages can cause the repainting as they change to show the exact point of the cross. The interval feature I created minimizes this by utilizing the previous bar info until the interval is closed and then we recalculate the variants. You can use the interval offset feature to denote which minute is the one that starts and ends the interval. So for instance, Trading View uses minue 1 and minute 31 for 30 minute intervals. If you offset your 30 minute interval would start on minute 16 and do its calculations based on the last 30 minutes,

As with most of my scripts, I have started using filters and a "show data" feature that will give you the ability to see the values of indicators that you cannot plot in the overlay. This allows you to figure out how to filter losing trades or market conditions.

I have also added a trailing stop and created a fixed stop loss as seems to perform better than the original occ strategy. The original one seemed to repaint enough that it would close too quickly and not give the posiition enough time to become profitable. In certain cases where there was a large move, it would perform well, but for the most part the trades would not close profitably even though the backtest said that it did - probably due to the delay in execution and pinescript not having a confirmation on what the actual position price was.

This is still in beta mode, so please forward test first and use at your own risk.

If you spot repaint issues, please send me a message and try to explain the situation.

Ichimoku Kinko HyoThis indicator is adding to the original indicator Ichimoku Cloud some visual informations.

Be aware of settings that are by default 10, 30, 60, while in the original indicator, default settings are 9, 26, 52. These are commonly consider like "crypto settings".

Tenkan = blue line

Kijun = orange line

SSB = red line

This indicator display three categories of signals that are given by the Ichimoku indicator:

- tenkan / kijun crosses ;

- breaks of mid prices for the different time horizon ;

- bar coloring depending of the trend

Let's review more in deep each of these elements.

Tenkan / Kijun crosses

When the tenkan crossover the kijun, this is called gold cross and it's display by a green triangle at the bottom of the chart.

When the tenkan crossunder the kijun, this is called death cross and it's display by a red triangle at the top of the chart.

I advise to not enter long or short only on this signal because it can be fake, especially during ranges.

To confirm the signal, we need to wait for a movement of the kijun in the same side of the cross. See first arrow on the chart.

Breaks of mid prices

Ichimoku is composed of three han-le lines that displays mid-price of the last candles depending on the settings (10, 30, 60).

Tenkan show us the mid-price of the last 10 candles (short term)

Kijun show us the mid-price of the last 30 candles (mid term)

SSB show us the mid-price of the last 60 candles (long term)

Break of tenkan by the price is the first signal that Ichimoku gives us before a reversal of the trend. This signal is display by a blue triangle.

Then, happened the break of kijun line follow by the break of the SSB. These are display respectively by an orange triangle and a red triangle.

Same advise, don't enter long or short only on break of these lines.

However, tenkan and kijun breaks can be used as exit point.

Bar coloring

The bar coloring display the strength of the trend:

- green candle: strong bullish trend - this happen when the current price is above tenkan, kijun and SSB ;

- blue candle: potential starting of a bullish trend - this happen when the current price is above tenkan and kijun but below the SSB ;

- no colored candle: no trend, market is in a range - this happen when the current price is above tenkan and below kijun and SSB or when the current price is below tenkan and above kijun and SSB ;

- orange candle: potential starting of a bearish trend - this happen when the current price is below tenkan and kijun but above SSB ;

- red candle: strong bearish trend - this happen when the current price is below tenkan, kijun and SSB

How to use to enter / exit trades

First of all, we need confirmations to enter in the side of the trend.

The first signal that the indicator gives us is the break of tenkan, follow by the break of kijun. Candles becomes blue / orange depending of the side.

Then, we wait for a cross of tenkan and kijun. This cross has to be confirmed by a movement of kijun. A flat kijun tell us this is a fake cross.

When the movement of kijun happened in the same side of the cross it is possible to enter a trade if you are aggresive.

Otherwise, you can wait for the third signal to take place: break of SSB, candle become green / red, depending on the side.

You can then enter a trade.

Then hold the position and wait to exit for break of tenkan or kijun, depending on your horizon (short / mid term).

If you have other questions or some features that are missing, pm me. Thanks.

MME MTF CCIHi All,

This is a Dual/Multi TF CCI script to be used for Intraday as well as positional system.

Intraday:

Chart TF : 5 mins

Underlying Trend CCI : CCI 34 of 30 mins TF

Immediate Trend CCI : CCI 34 of 5 mins TF

Execution CCI : CCI 8 of 5 mins TF

The CCIs are used for entry, exit during momentum breakouts or pullbacks.

General Long Setup:

Buy at CCI-8 5m below -135, when CCI-34 30 mins is > +100. Long exit when CCI 34 5 min < -60

General Short Setup:

Sell at CCI-8 5m above -135, when CCI-34 30 mins is < -100. Short exit when CCI 34 5 min > +60

The same CCI settings can be used for positional or investment per appropriate timeframes one is interested to trade, along with HTF above in ratio 1:5.

Hope its helpful!

MTF Stochastic ScannerThis Stochastic scanner can be use to identify overbought and oversold of 10 symbols over multiple timeframes

it will give you a quick overview which pair is more overbough or more oversold and also signals tops and bottoms in the AVG row

light red/green cell = weak bearish (Stoch = 30-20) / bullish (Stoch = 70-80)

medium red/green cell = bearish (Stoch = 20-10) / bullish (Stoch = 80-90)

dark red/green cell = strong bearish (Stoch <= 10) / bullish (Stoch >= 90)

gray cell = neutral (Stoch = 30-70)

Usage

If AVG (average of all 4 timeframes) falls below 20, the cell will get green, indicating a good time to enter long (buy)

If AVG (average of all 4 timeframes) rises above 80, the cell will get red, indicating a good time to enter short (sell)

Use the "MTF Stochastic Scanner" in combination with the " MTF RSI Scanner "

to find tops (RSI MTF avg >=70 AND Stochastic MTF avg >= 80)

or bottoms (RSI MTF avg <= 30 AND Stochastic MTF avg <= 20)

Here is how the two MTF scanners looked on Nov 08 2021 (ATH) »

and here how the MTF scanners looked on June 21 2022

use TradingViews Replay function to check how it would have worked in the past and when not.

As always… there NOT a single indicator that can show to the top & bottom 100% every single time. So use with caution, with other indicators and/or deeper understanding of technicals analysis ☝️☝️☝️

Settings

You can change the timeframes, symbols, Stochastic settings, overbought/oversold levels and colors to your liking

Drag the table onto the price chart, if you want to use it as an overlay.

NOTE:

Because of the 4x10 security requests, it can take up to 1 minute for changed settings to take effect! Please be patient 🙃

If you have any idea on how to optimise the code, please feel free to share 🙏

*** Inspired by "Binance CHOP Dashboard" from @Cazimiro and "RSI MTF Table" from @mobester16 ***

ATR vs Day Trading Range and PercentageThis indicator displays the Current Daily ATR vs the current Day Range and displays the percentage.

For example if the Daily ATR is $5 and the current range of the day is $10 this would be 200% the original move.

It is color coded (and can be modified) to change color when the Daily range is over 100% the ATR.

The time frame can be changed from Daily just be aware you must be on a lower timeframe then selected. So if you want to compare the current 30 minute ATR to the current 30 minute range you will need to be showing a 30 min chart or lower for it to calculate correctly.

MTF Bullish/Bearish IndicatorThe script plots a bullish/bearish indicator by evaluating a variety of moving averages for a security across multiple timeframes. It's derived from built in Technical Analysis indicator published by TradingView. The result of evaluation is plotted on the chart in green light/red light format in a configurable location.

evaluated moving averages include

- SMA 10, 20, 30, 50, 100, 200

- EMA 10, 20, 30, 50, 100, 200

- Hull MA 9

- VWMA 20

- Ichimoku Cloud

moving averages are evaluated at chart timeframes and 5 min, 15 min, 30 min, 120 min, 240 min, and daily by default but can be customized.

vol_premiaThis script shows the volatility risk premium for several instruments. The premium is simply "IV30 - RV20". Although Tradingview doesn't provide options prices, CBOE publishes 30-day implied volatilities for many instruments (most of which are VIX variations). CBOE calculates these in a standard way, weighting at- and out-of-the-money IVs for options that expire in 30 days, on average. For realized volatility, I used the standard deviation of log returns. Since there are twenty trading periods in 30 calendar days, IV30 can be compared to RV20. The "premium" is the difference, which reflects market participants' expectation for how much upcoming volatility will over- or under-shoot recent volatility.

The script loads pretty slow since there are lots of symbols, so feel free to delete the ones you don't care about. Hopefully the code is straightforward enough. I won't list the meaning of every symbols here, since I might change them later, but you can type them into tradingview for data, and read about their volatility index on CBOE's website. Some of the more well-known ones are:

ES: S&P futures, which I prefer to the SPX index). Its implied volatility is VIX.

USO: the oil ETF representing WTI future prices. Its IV is OVX.

GDX: the gold miner's ETF, which is usually more volatile than gold. Its IV is VXGDX.

FXI: a china ETF, whose volatility is VXFXI.

And so on. In addition to the premium, the "percentile" column shows where this premium ranks among the previous 252 trading days. 100 = the highest premium, 0 = the lowest premium.

Strat Assistant Hour FlipStrat Assistant Hour Flip

----------------------------

█ OVERVIEW

This script is intended to provide a vertical line indicator for the hourly "flips" to easily indicate when the hour turns. Ideally used in timeframes less than an hour.

Input

----------

Hour Color: the color of the line and the text for the hourly indicator

Four Hour Color: the color of the line and the text for the four hour indicator

Show Label Text?: an on/off (active/inactive) flag to display the text (new 30s/60s). I can't figure out how to get a label vertical, so sometimes it gets in the way.

Output

----------

Vertical Dotted Line Indicator: vertical lines that allow a user to quickly see when the hour flips

Hour Flip Labels: quick visual labels with the same color as the lines that will display new 4h/60s/30s

Best Practices

----------

Trading view may limit the number of lines drawn, so probably not best to be use in larger time frames (like days/month worth of data on the chart) for smaller intervals

Best if used for intervals under 30 minutes

RSI band with Signal alert//th/en

//th

สวัสดีครับท่านสมาชิก

ก่อนอื่นต้องขอเกริ่นก่อนเลยว่า Indicator ตัวนี้ถูกสร้างขึ้นมาบนพื้นฐานของ RSI จริง เพียงแต่ใช้ค่า EMA27 ในการสร้าง เนื่องจากผมยังไม่สามารถเขียน RSI band ที่โยงกับราคาได้ในส่วนนี้เองได้

แต่ทั้งนี้ขอให้ท่านใจเย็น ๆ และฟังผมสักหน่อย เนื่องจากก่อนหน้านี้ผมได้สังเกตเห็นว่า EMA27 นั้นมีค่าเท่ากับ RSI14 ที่ค่า 50 พอดี ดังนั้นผมจึงเลือกที่จะสร้างมันขึ้นมาด้วย EMA27 เพราะง่ายต่อการเขียน

วิธีการใช้งานมีดังต่อไปนี้

Indicator ตัวนี้ใช้งานเหมือน RSI14 วิธีการอ่านคือให้นับเส้น EMA27 เป็นค่า 50 ของ RSI14 ดังนั้นให้เราพิจารณาการซื้อขายดังต่อไปนี้ (โดยหลังจากนี้ผมจะเรียก EMA27 ที่สร้างขึ้นว่า RSI band)

พิจารณาเข้าซื้อ : เมื่อราคาทะลุ RSI band ขึ้นไปและย่อตัวทำ Higher Low เหนือเส้น RSI band

พิจารณาขายออก : เมื่อราคาทะลุ RSI band ลงมาและรีบาวน์ทำ Lower High ใต้เส้น RSI band

# ทั้งนี้ผมได้ทำสีแท่งเทียนไว้เพื่อให้ง่ายต่อการสังเกต โดยการนำไปใช้อาจนำสีของเส้นขอบแท่งเทียนออก แล้วในส่วนของไส้แท่งเทียนให้ใช้สีที่ไม่เจาะจงราคาบวกลบอย่างสี #434651

โดยเราสามารถดู Divergence โดยการเทียบความต่างระหว่างราคาและ RSI band ได้ดังนี้

ในแนวโน้มขาลง : ให้เปรียบเทียบความต่างระหว่างราคากับ RSI band ของ Lower Low ปัจจุบันกับ Low ก่อนหน้า โดยถ้าความต่างของ Low ลดลงเรื่อย ๆ จนราคาเข้าใกล้เส้น RSI band ให้พิจารณาเข้าซื้อ

ในแนวโน้มขาขึ้น : ให้เปรียบเทียบความต่างระหว่างราคากับ RSI band ของ Higher High ปัจจุบันกับ High ก่อนหน้า โดยถ้าความต่างของ High ดลงเรื่อย ๆ จนราคาเข้าใกล้เส้น RSI band ให้พิจารณาขายออก

ทั้งนี้ผมได้สร้าง Signal alert ไว้เพื่อให้ง่ายต่อการสังเกต โดยสร้างมาจากเงื่อนไขดังนี้ (ห้ามทำการซื้อขายตาม Signal alert เด็ดขาด เพราะเค้าแค่บอกจุดตามเงื่อนไขที่ตั้งไว้ บางทีอาจมีสัญญาณซื้อแล้วให้ซื้อต่อโดยไม่มีสัญญาณขายเลยก็ได้)

Buy : เมื่อ RSI14 ตัดขึ้นที่ค่า 50 พร้อมกับ RSI14 ตัดขึ้น Signal ที่ผมตั้งไว้ (ผมใช้ EMA7 ของ RSI14)

Prepare to Sell : เมื่อ RSI14 ตัดลง Signal ในขณะที่ RSI14 นั้น มีค่ามากกว่า 70

Sell/Short Top : เมื่อ RSI14 ตัดลงที่ค่า 70 พร้อมกับ RSI14 ตัดลง Signal (จะมีขึ้นแสดงว่า Peak ในกราฟ)

Buy : เมื่อ RSI14 ตัดลงที่ค่า 50 พร้อมกับ RSI14 ตัดลง Signal

Prepare to Buy : เมื่อ RSI14 ตัดขึ้น Signal ในขณะที่ RSI14 นั้น มีค่าน้อยกว่า 30

TP Short/Buy Bottom : เมื่อ RSI14 ตัดขึ้นที่ค่า 30 พร้อมกับ RSI14 ตัดขึ้น Signal (จะมีขึ้นแสดงว่า Deep ในกราฟ)

# สาเหตุที่ใส่ข้อความใน Signal alert เพียงแค่ตอน Sell/Short Top และ TP Short/Buy Bottom เพื่อลดโอกาสเกิดการแพนิคที่เกิดจากการสังเกตได้ โดยในสัญญาณตัวอื่นจะมีแค่เครื่องหมาย * เพียงอย่างเดียว

ขอให้โชคดีครับ

Firstssk

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

//en (Google Translate)

Hello, Trader

First of all, I have to say that this indicator is built on the basis of a real RSI, just using the EMA27 value to create it, since I still can't write an RSI band that is tied to the price in this section.

But please be patient and listen to me a bit. Since I previously noticed that EMA27 is exactly equal to RSI14 at 50, so I chose to build it with EMA27 because it's easier to write.

Here's how to use it:

This indicator works like RSI14. The reading method is to count the EMA27 line as the 50 value of RSI14, so let's consider the following trading. (After this I will call the created EMA27 RSI band)

Consider buying : When the price breaks the RSI band up and makes a Higher low above the RSI band.

Consider selling : When the price breaks the RSI band down and rebounds to make a Lower high below the RSI band.

# However, I have colored the candlesticks to make them easier to spot. By applying it may remove the color of the candlestick border. Then for the wick part, use a color that does not specify the price plus and minus color #434651

We can see the divergence by comparing the difference between the price and the RSI band as follows.

In a downtrend : Compare the difference between the price and the RSI band of the current Lower Low and the previous Low. If the divergence of the Low continues to decrease until the price approaches the RSI band, consider buying.

In an uptrend : Compare the price difference between the RSI band of the current Higher High and the previous high. If the divergence of the High continues to decrease until the price approaches the RSI band, consider selling.

I have created a Signal alert for easy observation. It was created from the following conditions: (Do not trade according to Signal alert strictly because they just tell the point according to the conditions set There may be a buy signal and then buy again without a sell signal.)

Buy : When RSI14 crosses above 50 with RSI14 crosses up the signal I set (I use EMA7 of RSI14).

Prepare to Sell : When RSI14 crosses signal while RSI14 is greater than 70.

Sell/Short Top : When RSI14 crosses down at 70 with RSI14 crosses down Signal (it will show "Peak" on the chart)

Buy : When RSI14 crosses down to 50 with RSI14 crosses down signal.

Prepare to Buy : When RSI14 crosses signal while RSI14 is less than 30.

TP Short/Buy Bottom : When RSI14 crosses above 30 with RSI14 crosses up signal (it will show "Deep" in the chart).

# The reason why I put the message in Signal alert only at Sell/Short Top and TP Short/Buy Bottom to reduce the chance of panic occurring from observation. In other signals, there will only be a * sign.

Good luck.

Firstssk

MACD, RSI, & RVOL Strategy

This strategy combines the use of MACD (12, 26, 9), RSI (14, 30, 70), and RVOL (14) to create Long Buy and Sell signals. This works well with many different time intervals but was developed with 15-minute intervals in mind.

Using MACD as a reference, the strategy identifies when the MACD line crosses over (a factor in a buy signal) and under (a factor in a Sell signal) the Signal line. This shows a shift in positive (cross over) and negative (cross under) of a security.

Using the Relative Strength Index ( RSI ) as an indicator, the strategy notices when the velocity and magnitude of the directional price movements cross over the Oversold signal (30) and crosses under the Overbought signal (70) as a factor in creating a Buy and Sell signal.

Using Relative Volume (RVOL) as an indicator, the strategy calculates when the current volume has crossed over the 2x average volume indicator over a given period and is then used as a factor in creating a Buy signal. RVOL is also used when the change in volume crosses under a set RVOL number (in this strategy, it is set to a RVOL of 5).

RVOL = Current Volume / Average Volume over a certain period

This strategy indicates a Buy signal when 2/3 conditions are met:

- RSI Cross Over the Over Sold signal (default 30)

- MACD Cross Over of Signal ( MACD > Signal)

- RVOL Cross Over of 2 (RVOL > 2)

This strategy indicates a Sell signal when 2/3 conditions are met:

- RSI Cross Under the Over Bought signal (default 70)

- MACD Cross Under of Signal ( MACD < Signal)

- RVOL Cross Under 5 (RVOL < 5)

Enjoy and leave feedback!

Multiple Screeners with AlertsI already published few version of my custom screeners. Unfortunately, because of TradingView's security function call limit you can't use more than 40 stocks in 1 screener.

Fortunately, you can compute multiple values in your function and screen few indicators at once.

In this script I show how you can compute 5 indicators at the same time for 40 instruments. I display then in different labels.

Every label consist of list of instruments satisfying current indicator conditions and a value for it. It can be absolute value as for RSI or -1/1 representing Bullish/Bearish event.

Also you can create 1 alert with result of all screeners inside.

In this example I took 5 indicators with following conditions:

RSI - "RSI < 30" or "RSI > 70"

TSI - "TSI < -30" or "RSI >30"

ADX - "ADX > 40"

MACD - "MACD Bullish Cross" or "MACD Bearish Cross" (1 and -1 in screener)

AO - "AO Crosses 0 UP" or "AO Crosses 0 DOWN" (1 and -1 in screener)

Params

- bars_apart - this parameter define how may bars apart you labels are on your chart. If you see labels overlapping, increase this number.

- Parameters for all used indicators

- 40 symbol inputs for instruments you want to use in this screener

Alerts

You can create an alert from it easily by selecting screener name from the list and then selecting "Any alert() function call".

No additional configuration is required, message and alert on close is generated in the code.

You should better change default name for your alert. Sometimes because of big amount of inputs you might receive an error.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as good as in historical backtesting.

This post and the script don’t provide any financial advice.

RSI Classic Strategy (by Coinrule)One of the questions hobbyist traders more often ask is: what is the perfect trading indicator?

Every indicator is just a tool, so its efficiency is proportional to your ability to read its signals and translate them into an actionable trading strategy. The RSI is likely the most flexible and easy to use among the technical indicators.

This trading strategy tries to catch short-term swings on the coins of your choice with a simple yet profitable setup.

Buy when the RSI is lower than 30 (you can adjust it to 35 in times of steep uptrend).

Sell when the RSI is greater than 65 (the target may range between 60 and 75 depending on the volatility of the coin).

Note that the buy signal comes when the indicator crosses below 30 and not when it crosses above 30 as it happens on the built-in RSI strategy on Tradingview.

The present script overperforms the built-in strategy, even adding trading fees and using a lower amount of capital for each trade (30%). That means that the system can deliver higher net-profits with lower risk levels.

A typical example of market conditions where this strategy works perfectly is as follows.

The first initial breakout indicates that a new leg up in the trend may start. Bitcoin starts to trade within a range which you can identify when it reaches the point 3. That is the perfect time to start the rule because

- trading within a channel anticipates possible swings up and down

- the trend is on the upside, providing low downside risk in buying the dips.

This strategy works well with selected coins of your choice, and it's a great fit on leverage exchanges like Binance Futures.

If you prefer to run it across all available coins on the market, instead, you may choose an optimized version.

Multi Time Frame Buy the Dips (by Coinrule)Buying the dips is a relatively easy automated trading strategy that can return impressive profits, especially during uptrend times. Not all price drops are for buying, though. This trading system is based on a multi time frame buy-the-dip approach to optimize each trade.

The strategy catches sudden price drops on a 1-hr time frame when the price increases significantly in the last 12 hours. During steep uptrends, profit-taking price actions result in flash crashes that provide great opportunity to enter at convenient prices.

Buy Condition

The setup of the script is optimized on a 30 min time frame. You can adjust the parameters to fit different time frames.

The system gets a buy signal when

- the price drops 1% from the two previous candles (1 hour time frame = two 30-min candles)

- the price is up 3% from the last 12 hours (twenty-four 30-min candles equal the desired time frame)

Sell Condition

Each trade comes with a stop loss of 3% and a take profit of 4%.

This setup has been optimized, running over 150 backtests on more than 20 different crypto trading pairs.

The strategy assumes each order to trade 30% of the available capital. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

Easy Loot Golden CrossGolden/Death Cross Moving Average Indicator

30, 100 & 200 period Simple Moving Average (SMA).

30 = Yellow

100 = Green

200 = Black

Black crosses mark the 'golden crosses' as well as the 'death crosses'. These black crosses appear when the 30 crosses the 100 & when the 100 crosses the 200. These black crosses don't tell you when to buy/sell, but simply indicate interest in the market.

This code is open-source so feel free to add this indicator to your chart and play around with the different moving average timeframes & color schemes.

Golden Cross

The golden cross occurs when a short-term moving average crosses over a major long-term moving average to the upside and is interpreted by analysts and traders as signaling a definitive upward turn in a market. Basically, the short-term average trends up faster than the long-term average, until they cross.

There are three stages to a golden cross:

A downtrend that eventually ends as selling is depleted

A second stage where the shorter moving average crosses up through the longer moving average

Finally, the continuing uptrend, hopefully leading to higher prices

Death Cross

Conversely, a similar downside moving average crossover constitutes the death cross and is understood to signal a decisive downturn in a market. The death cross occurs when the short term average trends down and crosses the long-term average, basically going in the opposite direction of the golden cross.

The death cross preceded the economic downturns in 1929, 1938, 1974, and 2008.

Traders Dynamic Index(RSI) w/ Bull&Bear Control ZonesMomentum (RSI) is one of the most commonly used indicators for trading, but the vast majority of traders who use it, simply apply it as an oscillator to measure overbought and oversold conditions. However, momentum is much more complex than that and using a basic RSI fails to highlight these complexities.

What this highlights are some of the areas/zones that many people may not even know about or are unaware what the RSI can actually reveal about a particular trend.

What this indicator is showing:

Fast moving RSI (Green) - 1 period

Slow moving RSI (Red) - 9 period

Bollinger Bands

Relative Strength: 1 - 100

Bearish Control Zone: 30(Below) - 45

Bullish Control Zone: 60 - 70 (Above)

How this identifies trends:

Bear Market(Bearish Control Zone):

-Support: 20(Below) - 30

-Resistance: 55 - 65

-Momentum will test resistance but will fail to hold support at 50

Bull Market(Bullish Control Zone):

-Support: 45 - 50

-Resistance: 80 - 90(Above)

-Momentum will test support but will not continue past the 45 support

How this identifies reversals:

If a market is bullish, but loses support at 45 and tests 30, it has begun reversal. If a market is bearish, but breaks 60 and tests 70, it has begun reversal.

-A bull market reversal is confirmed if it finds resistance at 60 after testing bearish support

-A bear market reversal is confirmed if it finds support at 50 after testing bullish resistance

Slow & Fast RSI w/ Boll Bands:

-The Slow and Fast RSI crossovers will act as Intermediate trends within the Macro trend - Fast crosses slow, bullish. Slow cross fast, bearish.

-Use in confluence with the Macro trend.

-While under Bearish Control, the Slow RSI will act as resistance for the Fast RSI.

-While under Bullish Control, the Slow RSI will act as support for the Fast RSI.

-The two will have an impulsive crossover when the Macro trend reverses.

-The Bollinger Bands will act as a volatility gauge for potential approaching tests of Support & Resistances. (Expansions & Contractions)

This is an analog of TDIGM (GoldMinds)

-Added Bullish/Bearish Control Zones.

-Changed Fast RSI to Green and Slow RSI to Red.

50ema + 105emaIf price action is above the 50ema + 105ema on the 30-minute chart, be bullish.

If price action is below the 50ema + 105ema on the 30-minute chart, be bearish.

If price action is in-between buy off the lower when it acts like support and sell near the top ema which will act like resistance.

The purpose of this indicator is to show these 30-minute moving averages -- regardless of timeframe. This will only appear if you are using an intraday timeframe.

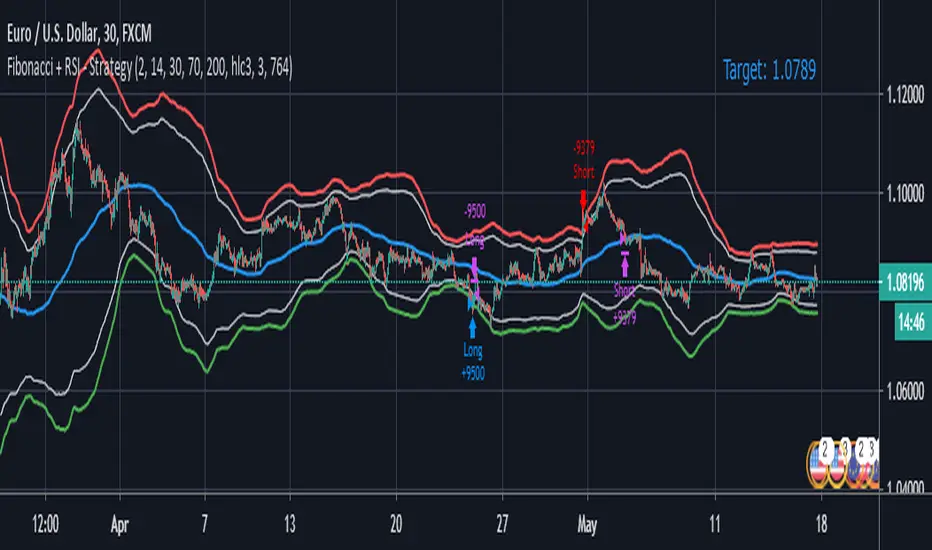

Fibonacci + RSI - StrategyStrategy: Fibonacci + RSI:

- Intraday trading strategy (Scalping).

Time Frames Tested with best Results:

30 Minutes.

5 Minutes.

15 Minutes.

1 Minute

Indicators Used:

RSI (30 / 70)

Fibonacci (1 - 0.784)

How it Works:

Once the Price Hits the 1 or -1 Fibonacci Level and bounces a little bit, It checks the RSI if Over Bought or Over Sold According to 30 - 70.

If both conditions are satisfied, it triggers a Long or Short Positions.

Further Notes:

- I have put a Stop-loss with a 2% just for further upgrades.

- Not advised to use in High Volatility Markets.

- No Repaint was observed during a 2-Weeks Tests.

If you have any suggestions or modifications please contact to add.

If you have observed any bad behavior please contact to fix.

Trade wisely.

[LunaOwl] 智慧型RSI (Smart RSI - a handy tool with less noise)Relative Strength Index is a common technical analysis tool, it is classified as a momentum oscillator, measuring the velocity and magnitude of directional price movements. it is most typically used on a 14-period timeframe, measured on a scale from 0 to 100, with high and low levels marked at 70 and 30.

相對強弱指標是常見的技術分析工具,它被歸類為動量振盪器,用於測量定向價格運動的速度和幅度,通常會使用14期數,擺盪範圍在0到100間,超買超賣分別標記成70、30。

after simple improvement and addition of logical judgment, it becomes a passive judge from subjective judgments, avoid the shortcomings of peoples in watching passivation, and the trade can be more consistent.

經過簡單的改良與添加邏輯判斷,能夠使RSI指標的使用,從主觀的判斷成為被動的確認指標,有效避免人們判斷指標鈍化的主觀缺失,並能夠使得交易更加一致。

--------------------------*

1) parameter

RSI period 1 - default is 14, same as general RSI.

RSI period 2 - default is 5, due to its own formula, the amplitude of the oscillator will become larger and more agile or fast. When the parameter is small.

exponential moving avg of RSI - using the result of RSI period 1 as the source of Ema's formula, the default length is 14, which can filter the excessive agility of RSI period 2 to reduce noise, and compared to using the baseline as the criterion for long and short judgments, The characteristics of exponential moving avg are more suitable to become flexible filtering standards.

Overbought - default is 70, you can set your overbought level.

Oversold - same as above, the default is 30.

2) Options

Open Candle color(開啟蠟燭線趨勢) - choose whether to start the color of the candle.

Open background color(開啟指標背景色) - the default is false, you can turn on.

--------------------------*

1. 設置參數

RSI期數1:預設值是14,是普通的RSI指標。

RSI期數2:預設值是5,由於RSI公式的算法,造成參數愈小擺盪幅度就會變大,反應比較快。

指數平均化的RSI期數1:將RSI期數1的結果帶入指數移動平均公式,預設值14,它能過濾RSI期數2過度敏捷的缺點,減少雜訊,相較於單純使用基準線作為多空判斷標準,用EMA的判斷標準更加因時制宜。

超買線:預設值是70,可以隨意調。

超賣線:預設值是30,一樣的。

2. 設定選項

開啟蠟燭線趨勢:顧名思義。已經幫您開好了。

開啟指標背景色:顏色太淺的話可以調深一點。

--------------------------*

ver.2- adjust new style design and create two options.

修改2: 調整新的樣式設計與建立兩個選項。

--------------------------*

ver.3- Create alert condition. maybe I should refer to the Alert Creation Framework,

there is also room for improvement.

修改3: 建立快訊選項。我應該參考警報創建框架,還有進步空間。

--------------------------*

Indicator Style - 指標樣式

The design uses casual light color style, light gray between overbought and oversold.

--------------------------*

Market Example - 市場範例

1. Bitcoin/Tether, Binance, 1 day

2. Bitcoin/USD, Coinbase, 4 hour

3. EUR/USD, Forex Market, 4 hour

4. GBP/USD, Forex Market, 30 min

5. TAIEX, Taiwan SE Weighted Index, 1 week

--------------------------*

postscript - 後記感想

The purpose of publishing Chinese Scripts is to make Pine close to more Chinese user.

I hope English skills enhancement...staggered writing makes me feel hard.

發布中文腳本的目的,是希望可以讓 Pine 親近更多中文圈的使用者。希望我的英語進步,中英文交錯撰寫有一些困難。

--------------------------*

If you find my works useful, you can give me encouragement. I can buy more books to sophisticated themselves.

如果您發現我的作品有用,可以給我鼓勵。讓我可以買更多書籍來精進自己。

MacD (Future Known or Unknown) StrategyThis indicator/strategy is to be used as a way to baseline the top potential any strategy could have with other strategies and indicators.

What I have created literally shows the BEST moves possible you could have made in my opinion for SHORTING or LONGING using only the MacD values of the 4 hour while on the 30 minute chart.

To use this, try checking out XBTUSD on the 30 minute chart . It will work under different time frames but works best on the 30 minute chart in my opinion. It WILL NOT WORK Above 2 hours time frame.

DO NOT TRADE WITH THIS indicator . I can't emphasize this enough. These results only work because of the lookahead_on parameter. A lot of scam indicators and strategies use this to trick people on tradingView into buying their scripts.

This code is OPEN SOURCE and as such there is nothing to hide and no scam!

I like to use this as a comparison tool for how good I 'could' have traded and at what points those were. By knowing where the perfect trading positions are, you can create real indicators and scripts that try to find patterns in those positions.

This also shows that IF you could know the direction the MacD was going what amazing results you could get ^_~.

This is meant purely for entertainment purposes and for comparing against your own scripts.

I've included the options in the settings to allow ONLY LONG or ONLY SHORTS. By default it attempts both buy attempts. You can also change your starting ($) amount and commission percentage that is taken per trade as well.

Also included in the options is the ability to set the back testing time frame to see how it performs during just certain time periods.

Finally a color explanation

Red - MacD 4 hour going down

Green - MacD 4 hour going up

Purple - MacD 4 hour going down (from an up position)

Yellow - MacD 4 hour going up (from a down position)

Notice the program will always buy right before it turns into a yellow color since it knows the future.

In the options you can turn off 'use the future' to see the horrible results if you trade the moment you know which direction the MacD 4 hour is actually going. I will revise this script in the future with attempts to work without knowing the future as play options to get better results.

If you have any questions or comments, please do not hesitate to ask!

(JS)DMI BarsAlright - so this is my own version of John Carter's "10x Bars"... I have done multiple things that are different from his version so they are slightly different..

So first of all the main indicator is based off of the ADX and the DMI;

For those who aren't familiar with it, Directional Movement is what you'd pull up under "built-in's" from the indicators tab (if you want to check it out).

The standard interpretation of this however, is when the ADX is above 20 that suggests the trend is strong, whereas under 20 suggests it is weak.

Also, when the D+ is above the D- that suggests a bullish trend, and D- above D+ suggests a bearish trend.

These bars take away the need to have it at the bottom of your screen, and places the data on the bars on your chart instead.

=========================================================================================================================================

So here's what the colors stand for -

Yellow - The ADX is under 20, no strength in trend

Shades of green occur when the ADX is above 20 and there's a bullish trend (D+ higher than D-)

Bright Green (Lime) - Bullish trend, D+ above 30

Green - Bullish Trend

Yellow Green - Bullish trend, D+ below 15

Shades of red occur when the ADX is above 20 and there's a bearish trend (D- higher than D+)

Bright Red - Bearish trend, D- above 30

Red - Bearish Trend

Orange - Bearish trend, D- below 15

=========================================================================================================================================

I have also added multiple time frame labels (label script used is the one created by Ricardo Santos)

These labels are color coded the same as the bars/candles, and they appear off to the right of your screen using every built in time increment from TradingView.

The purpose is to show you in real time, and on any chart resolution, what the current trend is on every individual time frame.

So using just one single chart you'll see your current resolutions candles, but also on the labels you'll see:

1 Minute

3 Minute

5 Minute

15 Minute

30 Minute

45 Minute

1 Hour

2 Hour

3 Hour

4 Hour

Daily

Weekly

Monthly

There is an input I added that allows you to adjust where your labels appear on the side of your screen as well!

=========================================================================================================================================

Now onto the volume spike portion of the indicator. This will plot a blue dot under each bar that has a spike in volume which meets your specified criteria.

I have 500% as the default setting.

What that means is that this indicator looks back and gets the 50 bar volume average and then applies dots where volume is 500% above average.

=========================================================================================================================================

Now finally, the reversal arrows. This is another simple to understand concept that I first read in John Carter's book "Mastering the Trade" that he calls "HOLP/LOHP".

I have added the ability to change the look back period you'd like the indicator to watch for highs and lows on.

What that stands for is 'High of Low Period' and 'Low of High Period', and it is used like this-

Whenever a bar makes a new high the indicator watches the low on that highest bar. Then when a bar afterwards makes a lower low then the one on the high bar,

a reversal arrow is given. Apply this same concept in the other direction in for the highs on the lowest bars.

=========================================================================================================================================

Now, I didn't want to make a "set" or have a bunch of different indicators out there that are all intended for the same package, so I took the time to put them together,

and if there's a part of it you don't care for they can easily be turned off in the settings.

Enjoy!