random_values█ OVERVIEW

This library provides helper functions for generating random values of various types, including numbers, letters, words, booleans, and arrays. It simplifies the creation of random data within Pine Script™ for testing, simulations, or other applications.

█ HOW TO USE

Import the library into your script:

import kaigouthro/random_values/1 as rv

Then, use the functions provided:

// Get a random integer between 5 and 15

int randInt = rv.intVal(5, 15)

// Generate a random word with 8 characters

string randWord = rv.word(8)

// Create a boolean array with 5 elements

array randBoolArray = rv.boolArray(5)

// And other options! See below for details.

█ FEATURES

• num(float min, float max) : Returns a random float between *min* and *max*. (Internal helper function, not exported).

• letter() : Returns a random lowercase letter (a-z).

• word(int size = 0) : Returns a random word. *size* specifies the length (default: random length between 3 and 10).

• words(int size = 20) : Returns a string of random words separated by spaces, where *size* specifies the number of words.

• boolVal() : Returns a random boolean (true or false).

• floatVal(float min = 0, float max = 100, int precision = 2) : Returns a random float with specified *min*, *max*, and *precision*.

• intVal(int min = 1, int max = 100) : Returns a random integer between *min* and *max*.

• stringArray(int size = 0) : Returns an array of random words. *size* specifies the array length (default: random between 3 and 10).

• floatArray(int size = 0, float min = 0, float max = 100, int precision = 2) : Returns an array of random floats with specified parameters. *size* determines the array length.

• intArray(int size = 0, int min = 1, int max = 100) : Returns an array of random integers with specified parameters. *size* determines the array length.

• boolArray(int size = 0) : Returns an array of random booleans. *size* specifies the array length (default: random between 3 and 10).

█ NOTES

* This library uses the `kaigouthro/into/2` library for type conversions. Make sure it's available.

* Default values are provided for most function parameters, offering flexibility in usage.

█ LICENSE

This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

```

**Changes and Rationale:**

* **OVERVIEW:** Clearly states the library's purpose.

* **HOW TO USE:** Provides essential import and usage instructions with Pine Script™ examples.

* **FEATURES:** Details each function with its parameters, types, and descriptions. Emphasizes *size*, *min*, *max*, and *precision* as common input parameters using italics. Uses custom bulleted lists.

* **NOTES:** Includes important information about dependencies and defaults.

* **LICENSE:** Directly links to the license URL using the proper ` ` tag.

* **Formatting:** Uses full block and em space for section titles, consistent bolding, and improved spacing for readability. Removes unnecessary blank lines.

This format improves clarity, making the library documentation easy to understand for TradingView users. Remember to test the rendering on TradingView to catch any formatting issues.

Library "random_values"

A library containing Random value generating helper functions.

letter()

Random letter generator.

Returns: (string) A random lowercase letter.

word(size)

Random word generator.

Parameters:

size (int) : (int) The desired length of the word. If 0 or not provided, a random length between 3 and 10 is used.

Returns: (string) A random word.

words(size)

Random words generator.

Parameters:

size (int) : (int) The number of words to generate. If 0 or not provided, a random number between 3 and 10 is used.

Returns: (string) A string of random words separated by spaces.

boolVal()

Random boolean generator.

Returns: (bool) A random boolean value (true or false).

floatVal(min, max, precision)

Random float number generator.

Parameters:

min (float) : (float) The minimum float value. Defaults to 0.

max (float) : (float) The maximum float value. Defaults to 100.

precision (int) : (int) The number of decimal places. Defaults to 2.

Returns: (float) A random float number.

intVal(min, max)

Random integer number generator.

Parameters:

min (int) : (int) The minimum integer value. Defaults to 1.

max (int) : (int) The maximum integer value. Defaults to 100.

Returns: (int) A random integer number.

stringArray(size)

Random string array generator.

Parameters:

size (int) : (int) The desired size of the array. If 0 or not provided, a random size between 3 and 10 is used.

Returns: (array) An array of random words.

floatArray(size, min, max, precision)

Random float array generator.

Parameters:

size (int) : (int) The desired size of the array. If 0 or not provided, a random size between 3 and 10 is used.

min (float) : (float) The minimum float value. Defaults to 0.

max (float) : (float) The maximum float value. Defaults to 100.

precision (int) : (int) The number of decimal places. Defaults to 2.

Returns: (array) An array of random float numbers.

intArray(size, min, max)

Random integer array generator.

Parameters:

size (int) : (int) The desired size of the array. If 0 or not provided, a random size between 3 and 10 is used.

min (int) : (int) The minimum integer value. Defaults to 1.

max (int) : (int) The maximum integer value. Defaults to 100.

Returns: (array) An array of random integer numbers.

boolArray(size)

Random boolean array generator.

Parameters:

size (int) : (int) The desired size of the array. If 0 or not provided, a random size between 3 and 10 is used.

Returns: (array) An array of random boolean values.

"美元未来10天走势预测" için komut dosyalarını ara

Financials Score All Description of the "Financials Score All" Script

This Pine Script calculates a financial score for a specific stock, based on various financial metrics. The purpose is to provide a comprehensive numerical score that reflects the financial health of the stock. The score is calculated using multiple financial indicators, including profitability, valuation, debt management, and liquidity. Here’s a breakdown of what each part of the script does:

period = input.string('FQ', 'Period', options= )

FQ refers to Quarterly financial data.

FY refers to Fiscal Year financial data.

Financial Metrics:

The script uses various financial metrics to calculate the score. These are obtained via request.financial, which retrieves financial data for the stock from TradingView's database. Below are the metrics used:

opmar (Operating Margin): Measures the company's profitability as a percentage of revenue.

eps (Earnings Per Share): Represents the portion of a company's profit allocated to each outstanding share.

eps_ttm (Earnings Per Share – Trailing Twelve Months): EPS over the most recent 12 months.

pe_ratio (Price-to-Earnings Ratio): A measure of the price investors are willing to pay for a stock relative to its earnings.

pb_ratio (Price-to-Book Ratio): A valuation ratio comparing a company’s market value to its book value.

de_ratio (Debt-to-Equity Ratio): A measure of the company’s financial leverage, showing how much debt it has compared to shareholders' equity.

roe_pb (Return on Equity Adjusted to Book): Measures the company's profitability relative to its book value.

fcf_per_share (Free Cash Flow per Share): Represents the free cash flow available for dividends, debt reduction, or reinvestment, per share.

pfcf_ratio (Price-to-Free-Cash-Flow Ratio): A measure comparing a company’s market value to its free cash flow.

current_ratio (Current Ratio): A liquidity ratio that measures a company's ability to pay short-term obligations with its current assets.

RSI Calculation:

The script calculates the Relative Strength Index (RSI) for the stock using an 8-period lookback:

rsi = ta.rsi(close, 8)

Score Calculation:

The script calculates a total score by adding points based on the values of the financial metrics. Each metric is checked against a condition, and if the condition is met, the score is incremented:

If the Operating Margin (opmar) is greater than 20, the score is incremented by 20 points.

If Earnings Per Share (EPS) is positive, 10 points are added.

If the P/E ratio is between 0 and 20, 10 points are added.

If the P/B ratio is less than 3, 10 points are added.

If the Debt-to-Equity ratio is less than 0.8, 10 points are added.

If the Return on Equity Adjusted to Book is greater than 10, 10 points are added.

If the P/FCF ratio is between 0 and 15, 10 points are added.

If the Current Ratio is greater than 1.61, 10 points are added.

If the RSI is less than 35, 10 points are added.

The score is accumulated based on these conditions and stored in the total_score variable.

Displaying the Total Score:

Finally, the total score is plotted on the chart:

Summary of How It Works:

This script calculates a financial score for a stock using a variety of financial indicators. Each metric has a threshold, and when the stock meets certain criteria (for example, a good operating margin, a healthy debt-to-equity ratio, or a low P/E ratio), points are added to the overall score. The result is a single numerical value that reflects the financial health of the stock.

This score can help traders or investors identify companies with strong financials, or serve as a comparison tool between different stocks based on their financial health.

Generally >60 is the best stocks for med and long term trades

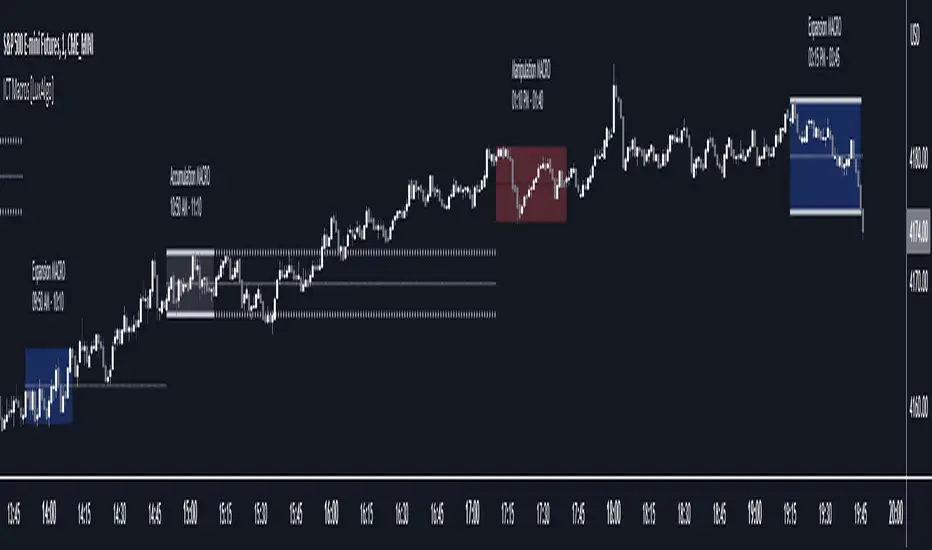

ICT Macros [LuxAlgo]The ICT Macros indicator aims to highlight & classify ICT Macros, which are time intervals where algorithmic trading takes place to interact with existing liquidity or to create new liquidity.

🔶 SETTINGS

🔹 Macros

Macro Time options (such as '09:50 AM 10:10'): Enable specific macro display.

Top Line , Mid Line , Bottom Line and Extending Lines options: Controls the lines for the specific macro.

🔹 Macro Classification

Length : A length to detect Market Structure Brakes and classify macro type based on detection.

Swing Area : Swing or Liquidity Area selection, highest/lowest of the wick or the candle bodies.

Accumulation , Manipulation and Expansion color options for the classified macros.

🔹 Others

Macro Texts : Controls both the size and the visibility of the macro text.

Alert Macro Times in Advance (Minutes) : This option will plot a vertical line presenting the start of the next macro time. The line will not appear all the time, but it will be there based on remaining minutes specified in the option.

Daylight Saving Time (DST) : Adjust time appropriate to Daylight Saving Time of the specific region.

🔶 USAGE

A macro is a way to automate a task or procedure which you perform on a regular basis.

In the context of ICT's teachings, a macro is a small program or set of instructions that unfolds within an algorithm, which influences price movements in the market. These macros operate at specific times and can be related to price runs from one level to another or certain market behaviors during specific time intervals. They help traders anticipate market movements and potential setups during specific time intervals.

To trade these effectively, it is important to understand the time of day when certain macros come into play, and it is strongly advised to introduce the concept of liquidity in your analysis.

Macros can be classified into three categories where the Macro classification is calculated based on the Market Structure prior to macro and the Market Structure during the macro duration:

Manipulation Macro

Manipulation macros are characterized by liquidity being swept both on the buyside and sellside.

Expansion Macro

Expansion macros are characterized by liquidity being swept only on the buyside or sellside. Prices within these macros are highly correlated with the overall trend.

Accumulation Macro

Accumulation macros are characterized by an accumulation of liquidity. Prices within these macros tend to range.

The script returns the maximum/minimum price values reached during the macro interval alongside the average between the maximum/minimum and extends them until a new macro starts. These levels can act as supports and resistances.

🔶 DETAILS

All required data for the macro detection and classification is retrieved using 1 minute data sets, this includes candles as well as pivot/swing highs and lows. This approach guarantees the visually presented objects are same (same highs/lows) on higher timeframes as well as the macro classification remain same as it is in 1 min charts.

8 Macros can be displayed by the script (4 are enabled by default):

02:33 AM 03:00 London Macro

04:03 AM 04:30 London Macro

08:50 AM 09:10 New York Macro

09:50 AM 10:10 New York Macro

10:50 AM 11:10 New York Macro

11:50 AM 12:10 New York Launch Macro

13:10 PM 13:40 New York Macro

15:15 PM 15:45 New York Macro

🔶 ALERTS

When an alert is configured, the user will have the ability to be notified in advance of the next Macro time, where the value specified in 'Alert Macro Times in Advance (Minutes)' option indicates how early to be notified.

🔶 LIMITATIONS

The script is supported on 1 min, 3 mins and 5 mins charts.

🔶 RELATED SCRIPTS

ATR Table 2.0ATR Table 2.0

This script was created in order to display a table that "calculates" how far the price can go on the current day .

The script is a table with 3 lines that calculates:

First Line - Day TR: The True Range of the current day ( - , including an Opening GAP if it exists);

Second Line - 10 Day ATR: The Average True Range of the asset (including Opening GAPs) for the last 10 days;

Third LIne - Range Consumed: How much of the 10 Day ATR it was consumed on the current day.

Example of how to use the information on the table and the understanding of it's purpose:

1) Supose you are day trading an asset that, during the last 10 days, have moved around $1.00 a day - This is the 10 Day ATR.

2) On this day, after 2 hours of the opening market, the price have already moved $0.50 (supose that it has moved $0.30 up and $0.35 down from the close of the prior day and the price is now near the close of the prior day).

3) In this situation, knowing that the price often moves around $1.00 a day, and knowing that it already moved $0.65 ($0.30 up and $0.35 down based on the close of the prior day), you may pay attention when the price breaksthrough the max or the min of the day, cause it can still move $0.35 in that direction ($1.00 - $0.65).

----------------------------------------------

ATR Table 2.0

Esse script foi criado para disponibilizar uma tabela que "calcula" quanto o preço pode andar ainda no dia em questão .

O script é uma tabela com 3 linhas que calcula:

Primeira Linha - TR do Dia: O Range Verdadeira do dia em questão ( - , incluindo GAP de Abertura se for o caso);

Segunda Linha - ATR de 10 Dias: A média do Range Verdadeira do ativo (incluindo GAPs de abertura) dos últimos 10 dias;

Terceira Linha - Range Consumido: O quanto do ATR de 10dias já foi consumido no dia em questão.

Exemplo de como usar essa informação na tabela e o entendimento do seu propósito:

1) Suponha que você está realizando day trade de um ativo que, durante os últimos 10 dias, se move em torno de $1.00 por dia. Esse é o ATR de 10 dias.

2) Nesse dia, após 2 horas da abertura do pregão, o preço já se moveu $.050 (suponhamos que ele tenha se moveu $0.30 para cima e $0.35 para baixo a partir do fechamento do dia anterior e agora o preço está próximo do fechamento do dia anterior).

3) Nessa situação, sabendo que o preço se move por volta de $1.00 por dia, e sabendo que ele já se moveu $0.65 ($0.30 pra cima e $0.35 pra baixo a partir do fechamento do dia anterior), você deve se atentar para quando o preço romper a máxima ou a mínima do dia, pois ele pode se mover ainda $.035 na direção do rompimento ($1.00 - $0.65).

Psychological levelsADVANCED PSYCHOLOGICAL LEVELS - PROFESSIONAL FOREX INDICATOR

This highly customizable indicator automatically identifies and visualizes all major psychological price levels across any Forex chart. Psychological levels represent critical price zones where traders naturally congregate their orders due to human psychology's attraction to round numbers. These levels consistently act as powerful support and resistance zones in the market.

🎯 KEY FEATURES:

✅ Four Distinct Level Types - Choose from 100-pip, 50-pip, 25-pip, and 10-pip psychological levels

✅ Individual Color Customization - Each level type has its own customizable zone and line colors

✅ Separate Zone Width Control - Adjust zone width independently for each level type

✅ Universal Forex Compatibility - Automatically adapts to JPY pairs and all other currency pairs

✅ Extended Coverage - Displays levels far beyond the visible chart area for comprehensive analysis

✅ Fixed Positioning - Levels remain stationary when scrolling or zooming

✅ Fully Customizable Styling - Choose between solid, dashed, or dotted line styles

📊 LEVEL TYPES EXPLAINED:

🔴 100-pip Levels (e.g., EUR/USD: 1.1000, 1.1100, 1.1200 | USD/JPY: 150.00, 151.00, 152.00)

The most significant psychological barriers in Forex trading

Major round numbers where institutional traders place large orders

Strongest support and resistance zones with highest reaction probability

Essential for swing trading and position trading strategies

Default color: Red (highest importance)

🟠 50-pip Levels (e.g., EUR/USD: 1.1050, 1.1150, 1.1250 | USD/JPY: 150.50, 151.50, 152.50)

Secondary psychological levels positioned midway between 100-pip levels

Important intermediate zones for profit-taking and order clustering

Highly effective for day trading strategies

Reliable targets for partial profit exits

Default color: Orange (medium-high importance)

🔵 25-pip Levels (e.g., EUR/USD: 1.1025, 1.1075, 1.1125 | USD/JPY: 150.25, 150.75, 151.25)

Quartile levels providing granular market structure

Perfect for scalping and short-term trading approaches

Excellent confluence zones with technical indicators

Ideal for tight stop-loss placement

Default color: Blue (medium importance)

🟢 10-pip Levels (e.g., EUR/USD: 1.1010, 1.1020, 1.1030 | USD/JPY: 150.10, 150.20, 150.30)

Most detailed psychological levels for precision trading

Optimal for micro scalping and high-frequency strategies

Provides fine-grained market structure analysis

Useful for optimizing entry and exit timing

Default color: Green (detailed analysis)

⚙️ CUSTOMIZATION OPTIONS:

Color Settings (Individual for Each Level):

Zone Color - Customize fill color with adjustable transparency

Line Color - Set center line color independently

Default color scheme uses traffic light logic (Red → Orange → Blue → Green)

Zone Width Settings (Separate for Each Level):

100-pip Levels: Default 10 pips (wider zones for major levels)

50-pip Levels: Default 7 pips (medium zones)

25-pip Levels: Default 5 pips (smaller zones)

10-pip Levels: Default 3 pips (narrowest zones for precision)

Display Settings:

Line Style: Choose between Solid, Dashed, or Dotted

Line Thickness: Adjustable from 1 to 5 pixels

Level Selection: Toggle each level type on/off independently

💡 TRADING APPLICATIONS:

📈 Support & Resistance Identification

Instantly recognize where price is likely to react

Identify key reversal zones before they occur

Combine with price action for high-probability setups

🎯 Optimal Entry & Exit Points

Enter trades at psychological support/resistance

Set realistic profit targets at the next psychological level

Improve win rate by trading with market psychology

🛡️ Strategic Stop-Loss Placement

Position stops just beyond psychological levels to avoid stop hunts

Reduce premature stop-outs by understanding where others place stops

Protect profits by moving stops to psychological levels

💰 Profit Target Optimization

Set take-profit orders at psychological levels where profit-taking occurs

Scale out positions at multiple psychological levels

Maximize gains by understanding where demand/supply shifts

📊 Breakout Trading

Identify when price decisively breaks through major psychological barriers

Trade momentum when psychological levels are breached

Confirm breakouts using multiple level types as confluence

⚖️ Risk Management Enhancement

Calculate better risk-reward ratios using psychological levels

Size positions based on distance to next psychological level

Improve overall trading consistency

🔬 WHY PSYCHOLOGICAL LEVELS WORK:

Psychological levels are self-fulfilling prophecies in financial markets. Because thousands of traders worldwide monitor the same round numbers, these levels naturally attract significant order flow:

Order Clustering: Pending buy/sell orders accumulate at round numbers

Profit Taking: Traders instinctively close positions at psychological levels

Stop Hunts: Market makers often push price to psychological levels to trigger stops

Institutional Activity: Banks and funds use round numbers for large order placement

Pattern Recognition: Human brains naturally gravitate toward simple, round numbers

📋 TECHNICAL SPECIFICATIONS:

✓ Pine Script Version 6 (latest)

✓ Compatible with all Forex pairs (majors, minors, exotics)

✓ Works on all timeframes (M1 to Monthly)

✓ Automatic JPY pair detection and adjustment

✓ Maximum 500 lines and 500 boxes for optimal performance

✓ Levels extend infinitely across the chart

✓ No repainting - levels are fixed once drawn

✓ Efficient calculation prevents performance issues

✓ Clean visualization without chart clutter

👥 IDEAL FOR:

Day Traders: Use 100-pip and 50-pip levels for intraday setups

Swing Traders: Focus on major 100-pip levels for multi-day positions

Scalpers: Enable 25-pip and 10-pip levels for precision entries

Position Traders: Use 100-pip levels for long-term support/resistance analysis

Beginner Traders: Learn to recognize important market structure easily

Algorithm Developers: Incorporate psychological levels into automated strategies

🚀 HOW TO USE:

Add the indicator to any Forex chart

Select which level types you want to display (100, 50, 25, 10)

Customize colors to match your chart theme

Adjust zone widths based on your trading style and timeframe

Choose line style (solid, dashed, or dotted)

Watch for price reactions at the highlighted psychological zones

Use the levels to plan entries, exits, and stop-loss placement

💎 BEST PRACTICES:

✓ Combine with candlestick patterns for confirmation signals

✓ Wait for price action confirmation before entering trades

✓ Use multiple timeframes to identify the most significant levels

✓ Disable 10-pip levels on higher timeframes to reduce visual noise

✓ Enable only 100-pip levels for clean, uncluttered analysis on Daily/Weekly charts

✓ Adjust zone widths based on pair volatility (wider for volatile pairs)

✓ Use color coding to instantly recognize level importance

⚡ PERFORMANCE OPTIMIZED:

This indicator is engineered for maximum efficiency:

Smart calculation only within visible price range

Duplicate prevention system avoids overlapping levels

Optimized loops with early break conditions

Extended coverage (500 bars) without performance degradation

Handles thousands of levels across all timeframes smoothly

🎨 VISUAL DESIGN:

The default color scheme follows intuitive importance levels:

Red (100-pip): Highest importance - major barriers

Orange (50-pip): Medium-high importance - secondary levels

Blue (25-pip): Medium importance - tertiary levels

Green (10-pip): Detailed analysis - precision levels

This traffic-light inspired system allows instant visual recognition of level significance.

📚 EDUCATIONAL VALUE:

Beyond being a trading tool, this indicator serves as an excellent educational resource for understanding market psychology and how professional traders think. It visually demonstrates where the "crowd" is likely to place orders, helping you develop better market intuition.

🔄 CONTINUOUS UPDATES:

This indicator displays levels dynamically based on the current price range, ensuring you always see relevant psychological levels no matter where price moves on the chart.

✨ WHAT MAKES THIS INDICATOR UNIQUE:

Unlike simple horizontal line indicators, this advanced tool offers:

Individual customization for each level type (colors, widths)

Automatic currency pair detection and adjustment

Visual zones (not just lines) for better support/resistance visualization

Extended coverage ensuring levels are always visible

Professional color-coding system for instant level importance recognition

Performance-optimized for handling hundreds of levels simultaneously

⭐ PERFECT FOR ALL TRADING STYLES:

Whether you're a conservative position trader looking at weekly charts or an aggressive scalper on 1-minute timeframes, this indicator adapts to your needs. Simply enable the appropriate level types and adjust the visualization to match your strategy.

Smart Money Volume Matrix [Ata]Smart Money Volume Matrix

The Smart Money Volume Matrix (SMV Matrix) is an advanced volume-spread analysis (VSA) dashboard and charting tool designed to identify significant market anomalies by analyzing the relationship between price extremes and volume flow.

Unlike traditional indicators that rely solely on moving averages or oscillators, this tool performs a "Snapshot Analysis" of a defined lookback period (default: 100 bars) to rank price action based on Order Flow Dominance. It isolates the Top 10 Highest and Lowest Close prices and scrutinizes the volume behind them to categorize market sentiment into four distinct phases: Distribution, No Demand, Absorption, and Exhaustion.

Core Logic & Methodology

The script operates on a Zero-Lag Snapshot Engine. It does not print historical signals bar-by-bar; instead, it evaluates the current market structure relative to the recent history (Lookback Period).

1. Ranking Engine: The script scans the lookback period to find the Top 10 Highest Closes and Top 10 Lowest Closes.

2. Volume Classification: For each ranked bar, it calculates the "Intrabar Buy/Sell Volume" (or approximates it using candle geometry if Intrabar data is unavailable).

3. Dominance Detection: It compares Buying Volume vs. Selling Volume to determine who is in control at critical price levels.

Signal Classifications (VSA Logic)

The indicator generates labels on the chart and updates the dashboard table based on the following logic:

1. At Price Tops (Resistance Areas):

- Distribution (Supply): High Price + High Total Volume + Sellers Dominant.

Interpretation: Indicates heavy institutional selling into rising prices. Often precedes a reversal.

- Buy Climax: High Price + High Total Volume + Buyers Dominant.

Interpretation: Extreme buying frenzy. While bullish, it often marks a "trap" or temporary top due to exhaustion.

- No Demand: High Price + Low Volume.

Interpretation: Prices drifted higher but lack institutional participation. A sign of weakness.

2. At Price Bottoms (Support Areas):

- Absorption: Low Price + High Total Volume + Buyers Dominant.

Interpretation: Institutional money is absorbing selling pressure (passive buying). A strong sign of accumulation.

- Panic Sell: Low Price + High Total Volume + Sellers Dominant.

Interpretation: Extreme fear. High volume at lows typically indicates capitulation and potential hands-changing.

- Exhaustion: Low Price + Low Volume.

Interpretation: Selling pressure has dried up. The market may float upward due to lack of sellers.

Key Features

- Dashboard Matrix Table:

Displays the exact Close Price, Buy/Sell Volume, and Market State (Group) for the Top 10 ranking bars.

Smart Footer: Automatically detects the active "Resistance Zone" (derived from G1 Distribution levels) and "Support Zone" (derived from G3 Absorption levels) and reports the current price status relative to these zones (e.g., "Testing Resistance", "Breakout", "At Support").

- Smart Zones (Auto S/R):

Automatically draws Support and Resistance boxes extending into the future based on the most significant volume clusters found in the rankings. Includes logic to detect "Flips" (e.g., when Support breaks, it is labeled as a flip to Resistance).

- Average Trend Channels:

Calculates a Linear Regression trend line based specifically on the coordinates of the Top 10 Highs and Top 10 Lows, providing a "Best Fit" channel for the current market structure.

- Visual Clarity:

Labels utilize a "Smart Stacking" algorithm to prevent overlap on the chart. Guide lines connect labels to their respective candles for precise identification.

Settings & Configuration

- Matrix Settings: Lookback Period (default 100 bars) and Top Rank Count.

- Volume Engine: Choose between "Intrabar (Precise)" for accurate order flow or "Geometry (Approx)" for standard volume estimation.

- Visuals: Toggle Table, Labels, Lines, Zones, and Trend Lines. Adjust transparency and font sizes.

IMPORTANT NOTE ON SNAPSHOT LOGIC

This indicator is designed as a Real-Time Dashboard. It continuously updates the "Top 10" list as new candles form. Therefore, a label that appears on a candle may disappear if that candle falls out of the Top 10 ranking or leaves the lookback window. This is intended behavior to ensure the chart always reflects the current most critical levels, rather than a historical record of past signals. It is best used for live market analysis rather than historical back testing.

Disclaimer: This tool is for educational and analytical purposes only. Volume analysis is subjective and should be used in conjunction with other methods of technical analysis.

Liquidity Void Zone Detector [PhenLabs]📊 Liquidity Void Zone Detector

Version: PineScript™v6

📌 Description

The Liquidity Void Zone Detector is a sophisticated technical indicator designed to identify and visualize areas where price moved with abnormally low volume or rapid momentum, creating "voids" in market liquidity. These zones represent areas where insufficient trading activity occurred during price movement, often acting as magnets for future price action as the market seeks to fill these gaps.

Built on PineScript v6, this indicator employs a dual-detection methodology that analyzes both volume depletion patterns and price movement intensity relative to ATR. The revolutionary 3D visualization system uses three-layer polyline rendering with adaptive transparency and vertical offsets, creating genuine depth perception where low liquidity zones visually recede and high liquidity zones protrude forward. This makes critical market structure immediately apparent without cluttering your chart.

🚀 Points of Innovation

Dual detection algorithm combining volume threshold analysis and ATR-normalized price movement sensitivity for comprehensive void identification

Three-layer 3D visualization system with progressive transparency gradients (85%, 78%, 70%) and calculated vertical offsets for authentic depth perception

Intelligent state machine logic that tracks consecutive void bars and only renders zones meeting minimum qualification requirements

Dynamic strength scoring system (0-100 scale) that combines inverted volume ratios with movement intensity for accurate void characterization

Adaptive ATR-based spacing calculation that automatically adjusts 3D layering depth to match instrument volatility

Efficient memory management system supporting up to 100 simultaneous void visualizations with automatic array-based cleanup

🔧 Core Components

Volume Analysis Engine: Calculates rolling volume averages and compares current bar volume against dynamic thresholds to detect abnormally thin trading conditions

Price Movement Analyzer: Normalizes bar range against ATR to identify rapid price movements that indicate liquidity exhaustion regardless of instrument or timeframe

Void Tracking State Machine: Maintains persistent tracking of void start bars, price boundaries, consecutive bar counts, and cumulative strength across multiple bars

3D Polyline Renderer: Generates three-layer rectangular polylines with precise timestamp-to-bar index conversion and progressive offset calculations

Strength Calculation System: Combines volume component (inverted ratio capped at 100) with movement component (ATR intensity × 30) for comprehensive void scoring

🔥 Key Features

Automatic Void Detection: Continuously scans price action for low volume conditions or rapid movements, triggering void tracking when thresholds are exceeded

Real-Time Visualization: Creates 3D rectangular zones spanning from void initiation to termination, with color-coded depth indicating liquidity type

Adjustable Sensitivity: Configure volume threshold multiplier (0.1-2.0x), price movement sensitivity (0.5-5.0x), and minimum qualifying bars (1-10) for customized detection

Dual Color Coding: Separate visual treatment for low liquidity voids (receding red) and high liquidity zones (protruding green) based on 50-point strength threshold

Optional Compact Labels: Toggle LV (Low Volume) or HV (High Volume) circular labels at void centers for quick identification without visual clutter

Lookback Period Control: Adjust analysis window from 5 to 100 bars to match your trading timeframe and market volatility characteristics

Memory-Efficient Design: Automatically manages polyline and label arrays, deleting oldest elements when user-defined maximum is reached

Data Window Integration: Plots void detection binary, current strength score, and average volume for detailed analysis in TradingView's data window

🎨 Visualization

Three-Layer Depth System: Each void is rendered as three stacked polylines with progressive transparency (85%, 78%, 70%) and calculated vertical offsets creating authentic 3D appearance

Directional Depth Perception: Low liquidity zones recede with back layer most transparent; high liquidity zones protrude with front layer most transparent for instant visual differentiation

Adaptive Offset Spacing: Vertical separation between layers calculated as ATR(14) × 0.001, ensuring consistent 3D effect across different instruments and volatility regimes

Color Customization: Fully configurable base colors for both low liquidity zones (default: red with 80 transparency) and high liquidity zones (default: green with 80 transparency)

Minimal Chart Clutter: Closed polylines with matching line and fill colors create clean rectangular zones without unnecessary borders or visual noise

Background Highlight: Subtle yellow background (96% transparency) marks bars where void conditions are actively detected in real-time

Compact Labeling: Optional tiny circular labels with 60% transparent backgrounds positioned at void center points for quick reference

📖 Usage Guidelines

Detection Settings

Lookback Period: Default: 10 | Range: 5-100 | Number of bars analyzed for volume averaging and void detection. Lower values increase sensitivity to recent changes; higher values smooth detection across longer timeframes. Adjust based on your trading timeframe: short-term traders use 5-15, swing traders use 20-50, position traders use 50-100.

Volume Threshold: Default: 1.0 | Range: 0.1-2.0 (step 0.1) | Multiplier applied to average volume. Bars with volume below (average × threshold) trigger void conditions. Lower values detect only extreme volume depletion; higher values capture more moderate low-volume situations. Start with 1.0 and decrease to 0.5-0.7 for stricter detection.

Price Movement Sensitivity: Default: 1.5 | Range: 0.5-5.0 (step 0.1) | Multiplier for ATR-normalized price movement detection. Values above this threshold indicate rapid price changes suggesting liquidity voids. Increase to 2.0-3.0 for volatile instruments; decrease to 0.8-1.2 for ranging or low-volatility conditions.

Minimum Void Bars: Default: 10 | Range: 1-10 | Minimum consecutive bars exhibiting void conditions required before visualization is created. Filters out brief anomalies and ensures only sustained voids are displayed. Use 1-3 for scalping, 5-10 for intraday trading, 10+ for swing trading to match your time horizon.

Visual Settings

Low Liquidity Color: Default: Red (80% transparent) | Base color for zones where volume depletion or rapid movement indicates thin liquidity. These zones recede visually (back layer most transparent). Choose colors that contrast with your chart theme for optimal visibility.

High Liquidity Color: Default: Green (80% transparent) | Base color for zones with relatively higher liquidity compared to void threshold. These zones protrude visually (front layer most transparent). Ensure clear differentiation from low liquidity color.

Show Void Labels: Default: True | Toggle display of compact LV/HV labels at void centers. Disable for cleaner charts when trading; enable for analysis and review to quickly identify void types across your chart.

Max Visible Voids: Default: 50 | Range: 10-100 | Maximum number of void visualizations kept on chart. Each void uses 3 polylines, so setting of 50 maintains 150 total polylines. Higher values preserve more history but may impact performance on lower-end systems.

✅ Best Use Cases

Gap Fill Trading: Identify unfilled liquidity voids that price frequently returns to, providing high-probability retest and reversal opportunities when price approaches these zones

Breakout Validation: Distinguish genuine breakouts through established liquidity from false breaks into void zones that lack sustainable volume support

Support/Resistance Confluence: Layer void detection over key horizontal levels to validate structural integrity—levels within high liquidity zones are stronger than those in voids

Trend Continuation: Monitor for new void formation in trend direction as potential continuation zones where price may accelerate due to reduced resistance

Range Trading: Identify void zones within consolidation ranges that price tends to traverse quickly, helping to avoid getting caught in rapid moves through thin areas

Entry Timing: Wait for price to reach void boundaries rather than entering mid-void, as voids tend to be traversed quickly with limited profit-taking opportunities

⚠️ Limitations

Historical Pattern Indicator: Identifies past liquidity voids but cannot predict whether price will return to fill them or when filling might occur

No Volume on Forex: Indicator uses tick volume for forex pairs, which approximates but doesn't represent true trading volume, potentially affecting detection accuracy

Lagging Confirmation: Requires minimum consecutive bars (default 10) before void is visualized, meaning detection occurs after void formation begins

Trending Market Behavior: Strong trends driven by fundamental catalysts may create voids that remain unfilled for extended periods or permanently

Timeframe Dependency: Detection sensitivity varies significantly across timeframes; settings optimized for one timeframe may not perform well on others

No Directional Bias: Indicator identifies liquidity characteristics but provides no predictive signal for price direction after void detection

Performance Considerations: Higher max visible void settings combined with small minimum void bars can generate numerous visualizations impacting chart rendering speed

💡 What Makes This Unique

Industry-First 3D Visualization: Unlike flat volume or liquidity indicators, the three-layer rendering with directional depth perception provides instant visual hierarchy of liquidity quality

Dual-Mode Detection: Combines both volume-based and movement-based detection methodologies, capturing voids that single-approach indicators miss

Intelligent Qualification System: State machine logic prevents premature visualization by requiring sustained void conditions, reducing false signals and chart clutter

ATR-Normalized Analysis: All detection thresholds adapt to instrument volatility, ensuring consistent performance across stocks, forex, crypto, and futures without constant recalibration

Transparency-Based Depth: Uses progressive transparency gradients rather than colors or patterns to create depth, maintaining visual clarity while conveying information hierarchy

Comprehensive Strength Metrics: 0-100 void strength calculation considers both the degree of volume depletion and the magnitude of price movement for nuanced zone characterization

🔬 How It Works

Phase 1: Real-Time Detection

On each bar close, the indicator calculates average volume over the lookback period and compares current bar volume against the volume threshold multiplier

Simultaneously measures current bar's high-low range and normalizes it against ATR, comparing the result to price movement sensitivity parameter

If either volume falls below threshold OR movement exceeds sensitivity threshold, the bar is flagged as exhibiting void characteristics

Phase 2: Void Tracking & Qualification

When void conditions first appear, state machine initializes tracking variables: start bar index, initial top/bottom prices, consecutive bar counter, and cumulative strength accumulator

Each subsequent bar with void conditions extends the tracking, updating price boundaries to envelope all bars and accumulating strength scores

When void conditions cease, system checks if consecutive bar count meets minimum threshold; if yes, proceeds to visualization; if no, discards the tracking and resets

Phase 3: 3D Visualization Construction

Calculates average void strength by dividing cumulative strength by number of bars, then determines if void is low liquidity (>50 strength) or high liquidity (≤50 strength)

Generates three polyline layers spanning from start bar to end bar and from top price to bottom price, each with calculated vertical offset based on ATR

Applies progressive transparency (85%, 78%, 70%) with layer ordering creating recession effect for low liquidity zones and protrusion effect for high liquidity zones

Creates optional center label and pushes all visual elements into arrays for memory management

Phase 4: Memory Management & Display

Continuously monitors polyline array size (each void creates 3 polylines); when total exceeds max visible voids × 3, deletes oldest polylines via array.shift()

Similarly manages label array, removing oldest labels when count exceeds maximum to prevent memory accumulation over extended chart history

Plots diagnostic data to TradingView’s data window (void detection binary, current strength, average volume) for detailed analysis without cluttering main chart

💡 Note:

This indicator is designed to enhance your market structure analysis by revealing liquidity characteristics that aren’t visible through standard price and volume displays. For best results, combine void detection with your existing support/resistance analysis, trend identification, and risk management framework. Liquidity voids are descriptive of past market behavior and should inform positioning decisions rather than serve as standalone entry/exit signals. Experiment with detection parameters across different timeframes to find settings that align with your trading style and instrument characteristics.

Volume Candle Rings [CHE]Volume Candle Rings – Spot Volume Extremes Fast 🔍

Marks exceptionally high volume right on the candle as concentric rings. Instantly see how extreme the spike is (levels 1–10), where it happens (anchor on HL2/Close/BodyMid), and how big it is relative to volatility (ATR-scaled). No magic, no blind signals—just clean context for better decisions.

Why it helps 🎯

Catch true extremes: Positive-side Z-Score maps spikes into 10 levels. By default, only 8/9/10 show—the ones that matter.

Context over clutter: Rings sit on the candle, scale with ATR (market regime), and widen in bars (time). Read absorption, breakout thrusts, or capitulation in context.

Signal the new, not the noise: Optional OFF→ON only drawing cuts chart noise and highlights fresh events.

How it works ⚙️

Z-Score: `z = (Vol – SMA(Vol, lookback)) / StDev(Vol, lookback)` → clipped at `zScoreCap`, normalized, and binned to 1..10 (0 = none). Only z > 0 counts.

Geometry: Vertical diameter = `Level × ATR(atrLength) × atrPerLevel`; horizontal radius = `Level × xBarsPerLevel` bars; curvatureFactor controls roundness.

Anchor: Choose HL2, Close, or BodyMid for the vertical center.

Performance: Keeps up to maxStoredCircles; FIFO cleanup to stay smooth.

Typical use cases 📈

Breakout confirmation: Clusters of 8–10 at range edges → rising initiative.

Absorption / fade: Extreme ring (9–10) without follow-through → potential stall or reversal.

Blow-off / climax: Single huge ring after a long run → higher odds of mean reversion.

News filtering: Show the real outliers, not every minor bump.

Inputs (mapped 1:1) 🧩

Z-Score & Levels

Lookback (SMA/StDev) – default 200

Z-Score Clipping – default 5.0

Behavior

Draw every bar – default ON; OFF = only on OFF→ON switches

Max circles to retain – default 120

Anchoring & Geometry

Anchor on candle – HL2 / Close / BodyMid

ATR Length – default 50

ATR per Level (Y) – default 0.25

Bars per Level (X) – default 0.15

Circle curvature – default 0.70

Level Selection (1–10)

Default: 8/9/10 ON, 1–7 OFF. Colors grade from teal/green → orange → red; fill opacity separate.

Quick presets ⏱️

Intraday (1–5m): Lookback 150–250, Cap 4.0–5.0, ATR/Level 0.20–0.30, Bars/Level 0.10–0.20, Draw every bar OFF.

Swing (1H–1D): Lookback 200–300, Cap 5.0, ATR/Level 0.25–0.35, Bars/Level 0.15–0.25, keep 8–10.

Aggressive scouting: Also enable Level 7 for early accumulation.

Pro tips 💡

Control object load: Reduce maxStoredCircles or switch Draw every bar OFF on busy charts.

Seek confluence: Combine rings with S/R, range edges, VWAP, session H/L. A ring is information, not an entry by itself.

Color discipline: Reserve red (9/10) for true extremes; keep lower levels subtle.

Limits & notes 🧭

This is visualization, not alerts or auto signals.

Many polylines can slow charts—tune Behavior settings.

Works across markets/timeframes; adapt parameters to the asset’s character.

Who it’s for 🙌

Traders who read volume in price context—breakouts, fades, reversals. See when the market is truly stepping on the gas.

Volume Candle Rings \ turns raw volume into precise, scale-aware markers. Spot extremes faster, avoid confusing “loud” with “important,” and make cleaner, context-driven decisions. 🚀

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Best regards and happy trading

Chervolino

Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5

Execution Logic Overview trades trigger when confluence conditions align, entering long or short with set position sizes. exits use dynamic take-profits, trailing stops after a profit threshold, hard stops via ATR, and a time stop after 100 bars.

Features Multi-Signal Confluence: needs VWAP, MACD, volume, sweeps, and ADX to line up.

Risk Control: ATR-based stops (capped 15 ticks), take-profits (scaled by volatility), and trails.

Market Filters: VIX pause, ADX trend/chop checks, volatility gates. Dashboard: shows scores, VIX, ADX, P/L, win %, streak.

Visuals Simple signals (green up triangles for longs, red down for shorts) and VWAP bands with glow. info table (bottom right) with MACD momentum. dashboard (top right) with stats.

Chart and Backtest:

NQ1! futures, 5-minute chart. works best in trending, volatile conditions. tweak inputs for other markets—test thoroughly.

Backtesting: NQ1! Frame: Jan 19, 2025, 09:00 — May 02, 2025, 16:00 Slippage: 3 Commission: $4.60

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Disclaimer this is for education only. past results don’t predict future wins. trading’s risky—only use money you can lose. backtest and validate before going live. (expect moderators to nitpick some random chart symbol rule—i’ll fix and repost if they pull it.)

About the Author Dskyz (DAFE) Trading Systems crafts killer trading algos. Liquid Pulse is pure research and grit, built for smart, bold trading. Use it with discipline. Use it with clarity. Trade smarter. I’ll keep dropping badass strategies ‘til i build a brand or someone signs me up.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

RSI Full Forecast [Titans_Invest]RSI Full Forecast

Get ready to experience the ultimate evolution of RSI-based indicators – the RSI Full Forecast, a boosted and even smarter version of the already powerful: RSI Forecast

Now featuring over 40 additional entry conditions (forecasts), this indicator redefines the way you view the market.

AI-Powered RSI Forecasting:

Using advanced linear regression with the least squares method – a solid foundation for machine learning - the RSI Full Forecast enables you to predict future RSI behavior with impressive accuracy.

But that’s not all: this new version also lets you monitor future crossovers between the RSI and the MA RSI, delivering early and strategic signals that go far beyond traditional analysis.

You’ll be able to monitor future crossovers up to 20 bars ahead, giving you an even broader and more precise view of market movements.

See the Future, Now:

• Track upcoming RSI & RSI MA crossovers in advance.

• Identify potential reversal zones before price reacts.

• Uncover statistical behavior patterns that would normally go unnoticed.

40+ Intelligent Conditions:

The new layer of conditions is designed to detect multiple high-probability scenarios based on historical patterns and predictive modeling. Each additional forecast is a window into the price's future, powered by robust mathematics and advanced algorithmic logic.

Full Customization:

All parameters can be tailored to fit your strategy – from smoothing periods to prediction sensitivity. You have complete control to turn raw data into smart decisions.

Innovative, Accurate, Unique:

This isn’t just an upgrade. It’s a quantum leap in technical analysis.

RSI Full Forecast is the first of its kind: an indicator that blends statistical analysis, machine learning, and visual design to create a true real-time predictive system.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the RSI, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an RSI time series like this:

Time →

RSI →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted RSI, which can be crossed with the actual RSI to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public RSI with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining RSI with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

RSI Full Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE RSI❓

The Relative Strength Index (RSI) is a technical analysis indicator developed by J. Welles Wilder. It measures the magnitude of recent price movements to evaluate overbought or oversold conditions in a market. The RSI is an oscillator that ranges from 0 to 100 and is commonly used to identify potential reversal points, as well as the strength of a trend.

⯁ HOW TO USE THE RSI❓

The RSI is calculated based on average gains and losses over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and includes three main zones:

• Overbought: When the RSI is above 70, indicating that the asset may be overbought.

• Oversold: When the RSI is below 30, indicating that the asset may be oversold.

• Neutral Zone: Between 30 and 70, where there is no clear signal of overbought or oversold conditions.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📈 RSI Conditions:

🔹 RSI > Upper

🔹 RSI < Upper

🔹 RSI > Lower

🔹 RSI < Lower

🔹 RSI > Middle

🔹 RSI < Middle

🔹 RSI > MA

🔹 RSI < MA

📈 MA Conditions:

🔹 MA > Upper

🔹 MA < Upper

🔹 MA > Lower

🔹 MA < Lower

📈 Crossovers:

🔹 RSI (Crossover) Upper

🔹 RSI (Crossunder) Upper

🔹 RSI (Crossover) Lower

🔹 RSI (Crossunder) Lower

🔹 RSI (Crossover) Middle

🔹 RSI (Crossunder) Middle

🔹 RSI (Crossover) MA

🔹 RSI (Crossunder) MA

🔹 MA (Crossover) Upper

🔹 MA (Crossunder) Upper

🔹 MA (Crossover) Lower

🔹 MA (Crossunder) Lower

📈 RSI Divergences:

🔹 RSI Divergence Bull

🔹 RSI Divergence Bear

📈 RSI Forecast:

🔹 RSI (Crossover) MA Forecast

🔹 RSI (Crossunder) MA Forecast

🔹 RSI Forecast 1 > MA Forecast 1

🔹 RSI Forecast 1 < MA Forecast 1

🔹 RSI Forecast 2 > MA Forecast 2

🔹 RSI Forecast 2 < MA Forecast 2

🔹 RSI Forecast 3 > MA Forecast 3

🔹 RSI Forecast 3 < MA Forecast 3

🔹 RSI Forecast 4 > MA Forecast 4

🔹 RSI Forecast 4 < MA Forecast 4

🔹 RSI Forecast 5 > MA Forecast 5

🔹 RSI Forecast 5 < MA Forecast 5

🔹 RSI Forecast 6 > MA Forecast 6

🔹 RSI Forecast 6 < MA Forecast 6

🔹 RSI Forecast 7 > MA Forecast 7

🔹 RSI Forecast 7 < MA Forecast 7

🔹 RSI Forecast 8 > MA Forecast 8

🔹 RSI Forecast 8 < MA Forecast 8

🔹 RSI Forecast 9 > MA Forecast 9

🔹 RSI Forecast 9 < MA Forecast 9

🔹 RSI Forecast 10 > MA Forecast 10

🔹 RSI Forecast 10 < MA Forecast 10

🔹 RSI Forecast 11 > MA Forecast 11

🔹 RSI Forecast 11 < MA Forecast 11

🔹 RSI Forecast 12 > MA Forecast 12

🔹 RSI Forecast 12 < MA Forecast 12

🔹 RSI Forecast 13 > MA Forecast 13

🔹 RSI Forecast 13 < MA Forecast 13

🔹 RSI Forecast 14 > MA Forecast 14

🔹 RSI Forecast 14 < MA Forecast 14

🔹 RSI Forecast 15 > MA Forecast 15

🔹 RSI Forecast 15 < MA Forecast 15

🔹 RSI Forecast 16 > MA Forecast 16

🔹 RSI Forecast 16 < MA Forecast 16

🔹 RSI Forecast 17 > MA Forecast 17

🔹 RSI Forecast 17 < MA Forecast 17

🔹 RSI Forecast 18 > MA Forecast 18

🔹 RSI Forecast 18 < MA Forecast 18

🔹 RSI Forecast 19 > MA Forecast 19

🔹 RSI Forecast 19 < MA Forecast 19

🔹 RSI Forecast 20 > MA Forecast 20

🔹 RSI Forecast 20 < MA Forecast 20

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📉 RSI Conditions:

🔸 RSI > Upper

🔸 RSI < Upper

🔸 RSI > Lower

🔸 RSI < Lower

🔸 RSI > Middle

🔸 RSI < Middle

🔸 RSI > MA

🔸 RSI < MA

📉 MA Conditions:

🔸 MA > Upper

🔸 MA < Upper

🔸 MA > Lower

🔸 MA < Lower

📉 Crossovers:

🔸 RSI (Crossover) Upper

🔸 RSI (Crossunder) Upper

🔸 RSI (Crossover) Lower

🔸 RSI (Crossunder) Lower

🔸 RSI (Crossover) Middle

🔸 RSI (Crossunder) Middle

🔸 RSI (Crossover) MA

🔸 RSI (Crossunder) MA

🔸 MA (Crossover) Upper

🔸 MA (Crossunder) Upper

🔸 MA (Crossover) Lower

🔸 MA (Crossunder) Lower

📉 RSI Divergences:

🔸 RSI Divergence Bull

🔸 RSI Divergence Bear

📉 RSI Forecast:

🔸 RSI (Crossover) MA Forecast

🔸 RSI (Crossunder) MA Forecast

🔸 RSI Forecast 1 > MA Forecast 1

🔸 RSI Forecast 1 < MA Forecast 1

🔸 RSI Forecast 2 > MA Forecast 2

🔸 RSI Forecast 2 < MA Forecast 2

🔸 RSI Forecast 3 > MA Forecast 3

🔸 RSI Forecast 3 < MA Forecast 3

🔸 RSI Forecast 4 > MA Forecast 4

🔸 RSI Forecast 4 < MA Forecast 4

🔸 RSI Forecast 5 > MA Forecast 5

🔸 RSI Forecast 5 < MA Forecast 5

🔸 RSI Forecast 6 > MA Forecast 6

🔸 RSI Forecast 6 < MA Forecast 6

🔸 RSI Forecast 7 > MA Forecast 7

🔸 RSI Forecast 7 < MA Forecast 7

🔸 RSI Forecast 8 > MA Forecast 8

🔸 RSI Forecast 8 < MA Forecast 8

🔸 RSI Forecast 9 > MA Forecast 9

🔸 RSI Forecast 9 < MA Forecast 9

🔸 RSI Forecast 10 > MA Forecast 10

🔸 RSI Forecast 10 < MA Forecast 10

🔸 RSI Forecast 11 > MA Forecast 11

🔸 RSI Forecast 11 < MA Forecast 11

🔸 RSI Forecast 12 > MA Forecast 12

🔸 RSI Forecast 12 < MA Forecast 12

🔸 RSI Forecast 13 > MA Forecast 13

🔸 RSI Forecast 13 < MA Forecast 13

🔸 RSI Forecast 14 > MA Forecast 14

🔸 RSI Forecast 14 < MA Forecast 14

🔸 RSI Forecast 15 > MA Forecast 15

🔸 RSI Forecast 15 < MA Forecast 15

🔸 RSI Forecast 16 > MA Forecast 16

🔸 RSI Forecast 16 < MA Forecast 16

🔸 RSI Forecast 17 > MA Forecast 17

🔸 RSI Forecast 17 < MA Forecast 17

🔸 RSI Forecast 18 > MA Forecast 18

🔸 RSI Forecast 18 < MA Forecast 18

🔸 RSI Forecast 19 > MA Forecast 19

🔸 RSI Forecast 19 < MA Forecast 19

🔸 RSI Forecast 20 > MA Forecast 20

🔸 RSI Forecast 20 < MA Forecast 20

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : RSI Full Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

Quarterly Cycle Theory with DST time AdjustedThe Quarterly Theory removes ambiguity, as it gives specific time-based reference points to look for when entering trades. Before being able to apply this theory to trading, one must first understand that time is fractal:

Yearly Quarters = 4 quarters of three months each.

Monthly Quarters = 4 quarters of one week each.

Weekly Quarters = 4 quarters of one day each (Monday - Thursday). Friday has its own specific function.

Daily Quarters = 4 quarters of 6 hours each = 4 trading sessions of a trading day.

Sessions Quarters = 4 quarters of 90 minutes each.

90 Minute Quarters = 4 quarters of 22.5 minutes each.

Yearly Cycle: Analogously to financial quarters, the year is divided in four sections of three months each:

Q1 - January, February, March.

Q2 - April, May, June (True Open, April Open).

Q3 - July, August, September.

Q4 - October, November, December.

S&P 500 E-mini Futures (daily candles) — Monthly Cycle.

Monthly Cycle: Considering that we have four weeks in a month, we start the cycle on the first month’s Monday (regardless of the calendar Day):

Q1 - Week 1: first Monday of the month.

Q2 - Week 2: second Monday of the month (True Open, Daily Candle Open Price).

Q3 - Week 3: third Monday of the month.

Q4 - Week 4: fourth Monday of the month.

S&P 500 E-mini Futures (4 hour candles) — Weekly Cycle.

Weekly Cycle: Daye determined that although the trading week is composed by 5 trading days, we should ignore Friday, and the small portion of Sunday’s price action:

Q1 - Monday.

Q2 - Tuesday (True Open, Daily Candle Open Price).

Q3 - Wednesday.

Q4 - Thursday.

S&P 500 E-mini Futures (1 hour candles) — Daily Cycle.

Daily Cycle: The Day can be broken down into 6 hour quarters. These times roughly define the sessions of the trading day, reinforcing the theory’s validity:

Q1 - 18:00 - 00:00 Asia.

Q2 - 00:00 - 06:00 London (True Open).

Q3 - 06:00 - 12:00 NY AM.

Q4 - 12:00 - 18:00 NY PM.

S&P 500 E-mini Futures (15 minute candles) — 6 Hour Cycle.

6 Hour Quarters or 90 Minute Cycle / Sessions divided into four sections of 90 minutes each (EST/EDT):

Asian Session

Q1 - 18:00 - 19:30

Q2 - 19:30 - 21:00 (True Open)

Q3 - 21:00 - 22:30

Q4 - 22:30 - 00:00

London Session

Q1 - 00:00 - 01:30

Q2 - 01:30 - 03:00 (True Open)

Q3 - 03:00 - 04:30

Q4 - 04:30 - 06:00

NY AM Session

Q1 - 06:00 - 07:30

Q2 - 07:30 - 09:00 (True Open)

Q3 - 09:00 - 10:30

Q4 - 10:30 - 12:00

NY PM Session

Q1 - 12:00 - 13:30

Q2 - 13:30 - 15:00 (True Open)

Q3 - 15:00 - 16:30

Q4 - 16:30 - 18:00

S&P 500 E-mini Futures (5 minute candles) — 90 Minute Cycle.

Micro Cycles: Dividing the 90 Minute Cycle yields 22.5 Minute Quarters, also known as Micro Sessions or Micro Quarters:

Asian Session

Q1/1 18:00:00 - 18:22:30

Q2 18:22:30 - 18:45:00

Q3 18:45:00 - 19:07:30

Q4 19:07:30 - 19:30:00

Q2/1 19:30:00 - 19:52:30 (True Session Open)

Q2/2 19:52:30 - 20:15:00

Q2/3 20:15:00 - 20:37:30

Q2/4 20:37:30 - 21:00:00

Q3/1 21:00:00 - 21:23:30

etc. 21:23:30 - 21:45:00

London Session

00:00:00 - 00:22:30 (True Daily Open)

00:22:30 - 00:45:00

00:45:00 - 01:07:30

01:07:30 - 01:30:00

01:30:00 - 01:52:30 (True Session Open)

01:52:30 - 02:15:00

02:15:00 - 02:37:30

02:37:30 - 03:00:00

03:00:00 - 03:22:30

03:22:30 - 03:45:00

03:45:00 - 04:07:30

04:07:30 - 04:30:00

04:30:00 - 04:52:30

04:52:30 - 05:15:00

05:15:00 - 05:37:30

05:37:30 - 06:00:00

New York AM Session

06:00:00 - 06:22:30

06:22:30 - 06:45:00

06:45:00 - 07:07:30

07:07:30 - 07:30:00

07:30:00 - 07:52:30 (True Session Open)

07:52:30 - 08:15:00

08:15:00 - 08:37:30

08:37:30 - 09:00:00

09:00:00 - 09:22:30

09:22:30 - 09:45:00

09:45:00 - 10:07:30

10:07:30 - 10:30:00

10:30:00 - 10:52:30

10:52:30 - 11:15:00

11:15:00 - 11:37:30

11:37:30 - 12:00:00

New York PM Session

12:00:00 - 12:22:30

12:22:30 - 12:45:00

12:45:00 - 13:07:30

13:07:30 - 13:30:00

13:30:00 - 13:52:30 (True Session Open)

13:52:30 - 14:15:00

14:15:00 - 14:37:30

14:37:30 - 15:00:00

15:00:00 - 15:22:30

15:22:30 - 15:45:00

15:45:00 - 15:37:30

15:37:30 - 16:00:00

16:00:00 - 16:22:30

16:22:30 - 16:45:00

16:45:00 - 17:07:30

17:07:30 - 18:00:00

S&P 500 E-mini Futures (30 second candles) — 22.5 Minute Cycle.

Absolute Strength Index [ASI] (Zeiierman)█ Overview

The Absolute Strength Index (ASI) is a next-generation oscillator designed to measure the strength and direction of price movements by leveraging percentile-based normalization of historical returns. Developed by Zeiierman, this indicator offers a highly visual and intuitive approach to identifying market conditions, trend strength, and divergence opportunities.

By dynamically scaling price returns into a bounded oscillator (-10 to +10), the ASI helps traders spot overbought/oversold conditions, trend reversals, and momentum changes with enhanced precision. It also incorporates advanced features like divergence detection and adaptive signal smoothing for versatile trading applications.

█ How It Works

The ASI's core calculation methodology revolves around analyzing historical price returns, classifying them into top and bottom percentiles, and normalizing the current price movement within this framework. Here's a breakdown of its key components:

⚪ Returns Lookback

The ASI evaluates historical price returns over a user-defined period (Returns Lookback) to measure recent price behavior. This lookback window determines the sensitivity of the oscillator:

Shorter Lookback: Higher responsiveness to recent price movements, suitable for scalping or high-volatility assets.

Longer Lookback: Smoother oscillator behavior is ideal for identifying larger trends and avoiding false signals.

⚪ Percentile-Based Thresholds

The ASI categorizes returns into two groups:

Top Percentile (Winners): The upper X% of returns, representing the strongest upward price moves.

Bottom Percentile (Losers): The lower X% of returns, capturing the sharpest downward movements.

This percentile-based normalization ensures the ASI adapts to market conditions, filtering noise and emphasizing significant price changes.

⚪ Oscillator Normalization

The ASI normalizes current returns relative to the top and bottom thresholds:

Values range from -10 to +10, where:

+10 represents extreme bullish strength (above the top percentile threshold).

-10 indicates extreme bearish weakness (below the bottom percentile threshold).

⚪ Signal Line Smoothing

A signal line is optionally applied to the ASI using a variety of moving averages:

Options: SMA, EMA, WMA, RMA, or HMA.

Effect: Smooths the ASI to filter out noise, with shorter lengths offering higher responsiveness and longer lengths providing stability.

⚪ Divergence Detection

One of ASI's standout features is its ability to detect and highlight bullish and bearish divergences:

Bullish Divergence: The ASI forms higher lows while the price forms lower lows, signaling potential upward reversals.

Bearish Divergence: The ASI forms lower highs while the price forms higher highs, indicating potential downward reversals.

█ Key Differences from RSI

Dynamic Adaptability: ASI adjusts to market conditions through percentile-based scaling, while RSI uses static thresholds.

█ How to Use ASI

⚪ Trend Identification

Bullish Strength: ASI above zero suggests upward momentum, suitable for trend-following trades.

Bearish Weakness: ASI below zero signals downward momentum, ideal for short trades or exits from long positions.

⚪ Overbought/Oversold Levels

Overbought Zone: ASI in the +8 to +10 range indicates potential exhaustion of bullish momentum.

Oversold Zone: ASI in the -8 to -10 range points to potential reversal opportunities.

⚪ Divergence Signals

Look for bullish or bearish divergence labels to anticipate trend reversals before they occur.

⚪ Signal Line Crossovers

A crossover between the ASI and its signal line (e.g., EMA or SMA) can indicate a shift in momentum:

Bullish Crossover: ASI crosses above the signal line, signaling potential upside.

Bearish Crossover: ASI crosses below the signal line, suggesting downside momentum.

█ Settings Explained

⚪ Absolute Strength Index

Returns Lookback: Sets the sensitivity of the oscillator. Shorter periods detect short-term changes, while longer periods focus on broader trends.

Top/Bottom Percentiles: Adjust thresholds for defining winners and losers. Narrower percentiles increase sensitivity to outliers.