BTC and ETH Long strategy - version 1I will start with a small introduction about myself. I'm now trading cryto currencies manually for almost 2 years. I decided to start after watching a documentary on the TV showing people who made big money during the Bitcoin pump which happened at the end of 2017.

The next day, I asked myself "Why should I not give it a try and learn how to trade".

This was in February 2018 and the price of Bitcoin was around 11500USD.

I didn't know how to trade. In fact, I didn't know the trading industry at all.

So, my first step into trading was to open an account with a broken. Then I directly bought 200$ worst of BTC . At that time, I saw the graph and thought "This can only go back in the upward direction!" :)

I didn't know anything about Stop loss, Take profit and Risk management.

Today, almost 2 years after, I think that I know how to trade and can also confirm that I still hold this bag of 200$ of bitcoin from 2018 :)

I did spend the 2 last years to learn technical analysis , risk management and leverage trading.

Today (14/05/2020), I know what I'm doing and I'm happy to see that the 2 last years have been positive in terms of gains. Of course, I did not make crazy money with my saving but at least I made more than if I would have kept it in my bank account.

Even if I like trading, I have a full time job which requires my full energy and lots of focus, so, the biggest problem I had is that I didn't have enough time to look at the charts.

Also, I realized that sometimes, neither technical analysis , nor fundamentals worked with crypto currency (at least for short time trading). So, as I have a developer background I decided to try to have a look at algo trading.

The goal for me was neither to make complex algos nor to beat the market but just to automate my trading with simple bot catching the big waves.

I then started to take a look at TV pine script and played with it.

I did my first LONG script in February 2020 to Long the BTC Market. It has some limitations but works well enough for me for the time being. Even if the real trades will bring me half of what the back testing shows, this will still be a lot more than what I was used to win during the last 2 years with my manual trading.

So, here we are! Below you will find some details about my first LONG script. I'm happy to share it with you.

Feel free to play with it, give your comments and bring improvements to it.

But please note that it only works fine with the candle size and crypto pair that I have mentioned below. If you use other settings this algo might loose money!

- Crypto pairs : XBTUSD and ETHXBT

- Candle size: 2 Hours

- Indicator used: Volatility , MACD (12, 26, 7), SMA (100), SMA (200), EMA (20)

- Default StopLoss: -1.5%

- Entry in position if: Volatility < 2%

AND MACD moving up

AND AME (20) moving up

AND SMA (100) moving up

AND SMA (200) moving up

AND EMA (20) > SAM (100)

AND SMA (100) > SMA (200)

- Exit the postion if: Stoploss is reached

OR EMA (20) crossUnder SMA (100)

Here is a summary of the results for this script:

XBTUSD : 01/01/2019 --> 14/05/2020 = +107%

ETHXBT : 01/01/2019 --> 14/05/2020 = +39%

ETHUSD : 01/01/2019 --> 14/05/2020 = +112%

It is far away from being perfect. There are still plenty of things which can be done to improve it but I just wanted to share it :) .

Enjoy playing with it....

Komut dosyalarını "米哈游2018年股票价格" için ara

Realized Volatility IIR Filters with BandsDISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The following indicator was made for NON LUCRATIVE ACTIVITIES and must remain as is following TradingView's regulations. Use of indicator and their code are published by Invitation Only for work and knowledge sharing. All access granted over it, their use, copy or re-use should mention authorship(s) and origin(s).

WARNING NOTICE!

THE INCLUDED FUNCTION MUST BE CONSIDERED AS TESTING. The models included in the indicator have been taken from open sources on the web and some of them has been modified by the author, problems could occur at diverse data sceneries.

WHAT'S THIS...?

Work derived by previous own research for study:

This is mainly an INFINITE IMPULSE RESPONSE FILTERING INDICATOR , it's purpose is to catch trend given by the nature of lag given by a VOLATILITY ESTIMATION ALGORITHM as it's coefficient. It provides as well an INFINITE IMPULSE RESPONSE DEVIATION FILTER that uses the same coefficients of the main filter to plot deviation bands as an auxiliary tool.

The given Filter based indicator provides my own Multi Volatility-Estimators Function with only 3 models:

ELASTIC VOLUME WEIGHTED VOLATILITY : This is a Modified Daigler & Padungsaksawasdi "Volume Weighted Volatility" as on DOI: 10.1504/IJBAAF.2018.089423 but with Elastic Volume Weighted Moving Average instead of VWAP (intraday) for faster (but inaccurate) calculation. A future version is planned on the way using intra-bar inspection for intraday timeframe as described in original paper.

GARMAN & KLASS / YANG-ZANG EXTENSION : As one of the best range based (OHLC) with open gaps inclusion in a single bar.

PETER MARTIN'S ULCER INDEX : This is a better approach to measure realized volatility than standard deviation of log returns given it's proven convex risk metric for DrawDowns as shown in Chekhlov et al. (2005) . Regarding this particular model, I take a different approach to use it as coefficient feed: Given that the UI only takes in consideration DrawDawns, I code myself the inverse of this to compute Draw-Ups as well and use both of them to filter minimums volatility levels in order to create a SLOW version of the IIR filter, and maximums of both to calculate as FAST variation. This approach can be used as a better proxy instead of any other common moving average given that with NO COMPOUND IN TIME AT ALL (N=1) or only using as long as N=3 bars of compund, the filter can catch a trend easily, making the indicator nearly a NON PARAMETRIC FILTER.

NOTES:

This version DO NOT INCLUDE ALERTS.

This version DO NOT INCLUDE STRATEGY: ALL Feedback welcome.

DERIVED WORK:

Incremental calculation of weighted mean and variance by Tony Finch (fanf2@cam. ac .uk) (dot@dotat.at), 2009.

Volume weighted volatility: empirical evidence for a new realised volatility measure by Chaiyuth Padungsaksawasdi & Robert T. Daigler, 2018.

Basic DSP Tips & Trics by TradingView user @alexgrover

CHEERS!

@XeL_Arjona 2020.

.BXBT IndexThe current .BXBT index weighted as close as possible to BitMEX's with updates as BitMEX refreshes their index.

Difference between this and the script titled '2020 March 27 .BXBT Index': this one will receive updates because it doesn't have a date in its title.

Methodology

www.bitmex.com

"BitMEX Index Weights, assuming no constituent exchanges have been excluded due to Index Protection Rules, last updated 27 December 2019 at 12:00:05 UTC."

Binance: -

Bitstamp: 10.61%

Bittrex: 2.53%

Coinbase: 52.30%

Gemini: 6.89%

Huobi: -

Itbit: 4.21%

Kraken: 23.46%

Poloniex: -

ItBit's weight is combined with Gemini's due to ItBit not being on TradingView as of now. BITTREX:BTCUSD substituted with BITTREX:BTCUSDT*POLONIEX:USDTUSD to backfill because Bittrex only recently (late 2018) started to offer a fiat BTC/USD pair. Not that it matters since the index used in 2018 didn't include Bittrex if I remember correctly.

What is actually used for 27/12/2019 to 27/03/2020:

Binance: -

Bitstamp: 10.61%

Bittrex: 2.53%

Coinbase: 52.30%

Gemini: 11.10%

Huobi: -

Itbit: -

Kraken: 23.46%

Poloniex: -

Options:

Toggle candlesticks or close line

Change price source to be used for indicators

To be added: Change quarter to show indexes for different times, with labels that apply to the appropriate index used

Reasons to use this vs. the index itself: (not many)

It is helpful as a reference for other indicators or creation of an index.

Stability Max OverloadStability Max Overload was created in another script I have been working on found below.

I have broken the code down to only display the Stability features.

What this is:

I was trying to find a way that could in some form display the Stability or Instability of the US Treasuries Bond Market. To try and help me do that, I came up with 3 values.

*Stability

*Stability Overload

*Stability Max Overload.

I started with STABILITY. This value is generated based off the number of side by side inversions in the Bond Market. I wanted this value to range between 0 and 1 while 1 equaling all Bonds inverted and 0 equaling no Bonds inverted and any number of inversions in between would equal a percentage value based off the actual number.

STABILITY OVERLOAD was created based off the average of each inversion.

STABILITY MAX OVERLOAD was then created based off the total of each inversion.

The most stable Yield Curve would have no inversions and therefore would generate a 0 for Stability, Stability Overload and Stability Max Overload. The more inversions the Yield Curve has the higher in value Stability itself would have as Stability is weighted more per inversion. With each inversion, data is taken based off the amount with which the Yields are inverted.

This display shows where we currently stand since Dec 2018. It's a telling story so say the least. I do plan on continuing the mentioned above script but again wanted to release a standalone of the data generated.

Hope you enjoy,

OpptionsOnly

Filtered Waves [NXT2017] #Linda Raschke #basics on Arthur MerrilHI BIG PLAYERS,

this script I wrote for an enquiry of a tradingview-user. It should represent the Filtered Waves idea from Arthur Merril and used by Linda Raschke.

It's similar like a visualization of Elliott Waves.

On YouTube title "MTA UK Chapter Presentation with Linda Raschke" between 34-36 minutes Linda Raschke shows the rules for her Filterd Waves.

Any questions? Ask me!

King regards

NXT2017

========

TO MY PERSON

I'm the second winner of the official German Forex Trading Competition in 2018.

Look here to the ranks:

deutsche-trading-meisterschaften.de

I speak german, english and russian.

My strength in trading are Wolfe Wave pattern.

Big 9 Volume - Volume indicator from exchanges with real volumeHere is a very basic indicator combining the volumes of the 9 biggest exchanges trading BTC/USD or BTC/USDT. These 9 exchanges were chosen based on the report by Bitwise Invest stating that 95% of the volume on CoinMarketCap is fake. On these 9 exchanges, however, volume data appears to be reliable. Please note BitFlyer was not included because it does not trade in USD. Please note also that data on all 9 exchanges is only available from June 2018.

Anyone is welcome to modify this and make it more elegant, this was just a quick implementation.

ATR Volatility Spectrum

This indicator estimates price volatility and it is based on ATR only.

The advantage of this indicator is that it can be used with any pair, any time frame.

The fluctuations of a short period ATR with respect to a gently ATR with high period

are calculated.

The only parameters are the periods of the reference ATR and fast ATR, which could be

safely let untouched and modified by experts.

RED areas depict low volatility

GREEN areas depict high volatility.

When the clouds are outside the region delimited by the aqua lines we have

extreme conditions:

Extremely low volatility = red cloud outside the aqua bands

Extremely high volatility = green cloud outside the aqua bands

Vitelot/yanez/Vts December 2018.

Hitting the like button is free act of gratitude

Synergy StatsSynergy Stats

This indicator is intended to complement the Synergy indicator. It provides the following statistics:

A percentage showing how often the two assets move in the opposite direction over a given lookback period.

Similarly, another percentage showing how often the two assets move in the same direction over the same lookback period.

Count the number of times (occurrences) when the two assets move in the same direction for more than 4 bars.

Count the number of times the alternative asset moves more than x%

Count the number of times that chart asset moved in the same direction of the alternative asset when the alternative asset moved more than x%

Both indicators were developed for use in an investigation/tutorial using Pine Script to analyse Gold and US Dollar Index correlation.

The full free post can be found here: backtest-rookies.com

SynergySynergy

This indicator was developed for use in an investigation/tutorial using Pine Script to analyse Gold and US Dollar Index correlation.

The first indicator shall measure the percentage change between the open and close of each bar and compare it to the same percentage change of an alternative asset. Additionally, we shall color the background when the two assets move in the same direction. This should allow us to more easily see when the two assets move together and spot trends in their moment.

The yellow bars show use the percentage change in the price of gold. The blue bars show the percentage change in the price of the US Dollar index. If the bar is above zero, it means that the asset closed up. Conversely, if it is below zero, it means the asset closed down. Finally, the grey bars show bars in which the two assets closed in the same direction.

It can be used in conjunction with a second indicator (to be published soon) that provides statistics generated from this indicator.

The full free post can be found here: backtest-rookies.com

Yope BTC tops channelAn empiric channel function that has held BTCUSD price from the beginning up to 2018. Possible extrapolation to the future.

Best used with the BLX ticker.

[astropark] MACD & RSI+//******************************************************************************

// Copyright by astropark v2.0

// RSI+

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

//******************************************************************************

@WACC Volatility Weighted PUT/CALL Positions [SPX]This indicator is based on Volatility and Market Sentiment. When volatility is high, and market sentiment is positive, the indicator is in a low or 'buy state'. When volatility is low and market sentiment is poor, the indicator is high.

The indicator uses the VIX as it's volatility input.

The indicator uses the spread between the Call Volume on SPX/SPY and the Put Volume.

This is pulled from CVSPX and PVSPX.

When volatility and put/call reaches a critical level, such as the levels present in a crisis or a sell off, the line will be green. See Sept 2015, 2008, and Feb 2018.

This level can be edited in the source code.

As the indicator is based on Put/Call, the indicator works best on larger time frames as the put/call ratio becomes a more discernible measure of sentiment over time.

Build A BotThis is the Robot we built during the 60 Minute Build-A-Bot webinar on September 12, 2018. We had a great time, and a lot of participation and the best part was that we finished up this robot and even ran a backtest in exactly 60 minutes! We built this robot based on recommendations and suggestions from those who were attending live. Lots of pieces in this robot, but you can always tinker with it, remove stuff, add things, whatever you want!

This version uses the CCI as a trigger for trade entry. The other version uses the Hull Moving Average as a trigger for trade entry.

Build A Bot Hull TriggerThis is the automated trading system we built during the 60-Minute Build-A-Bot webinar on September 12, 2018. We had a lot of fun, and implemented a TON of indicators LIVE during this webinar! And the best part is that as a group we researched, designed, and built a profitable robot in exactly 60 minutes!

We started by voting on the type of trading system, and this is a trend following system because it got the most votes. Then, the attendees in the webinar sent in their suggestions for indicators and settings during the live webinar (still counting toward the 60 minutes). Once we had the indicators on the chart, and we discussed various settings we could use, we got to work building the robot, and ran the first strategy test...and it was profitable!

This version uses the Hull Moving Average as a trigger for initiating the trade, and everything else is the same for the filters. The other version uses the CCI as a trigger for the trade, and many other indicators as filters.

Bollinger Bands + RSI Double Strategy (by SlumdogTrader)

// SlumdogTrader's Bollinger Bands + RSI Double Strategy - Profit Trailer

//

// Version 1.0

// Script by SlumdogTrader on July Fri 13(!), 2018.

//

// This strategy uses a normalise Bollinger Bands + RSI.

//

// Bollinger Band triggers

// SELL - when the price is above the upper band.

// BUY - when the price is below the lower band.

//

// RSI triggers

// SELL - when the price is above 55.

// BUY - when the price is below 45.

//

// This simple strategy only triggers when

// both the BB and the RSI

// indicators, at the same time, are in

// a overbought or oversold condition.

//

// Visit my TradingView work at:

// www.tradingview.com

//

// Visit my website at:

// www.slumdogtrader.com

boot2thrill - Pivot Reversal Strategy with Alert//Notes:

//Version by boot2thrill on 04-16-2018.

//Version includes "BUY" and "SELL" uppercase text with directional triangle shape indicators.

//Based on original PRS.

//***Recommended use on BTCUSD 1h/4h/1d chart.***

ETCUSDSHORTS ETCUSDLONGS - Bitfinex ETC Shorts & Longs// Created by titanlyy

// This script was inspired by @autemox who created the BTC version of this.

// Expecting the coinbase pump in Q3 2018, I was looking for an easy indicator script to display ETC Longs vs Shorts

// Hope this helps. Peace out.

// 12th July 2018

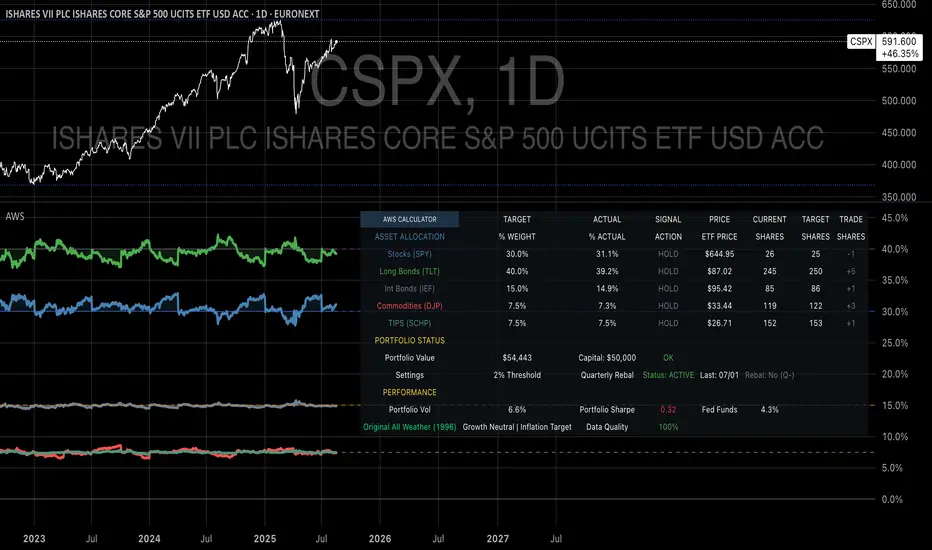

Ray Dalio's All Weather Strategy - Portfolio CalculatorTHE ALL WEATHER STRATEGY INDICATOR: A GUIDE TO RAY DALIO'S LEGENDARY PORTFOLIO APPROACH

Introduction: The Genesis of Financial Resilience

In the sprawling corridors of Bridgewater Associates, the world's largest hedge fund managing over 150 billion dollars in assets, Ray Dalio conceived what would become one of the most influential investment strategies of the modern era. The All Weather Strategy, born from decades of market observation and rigorous backtesting, represents a paradigm shift from traditional portfolio construction methods that have dominated Wall Street since Harry Markowitz's seminal work on Modern Portfolio Theory in 1952.

Unlike conventional approaches that chase returns through market timing or stock picking, the All Weather Strategy embraces a fundamental truth that has humbled countless investors throughout history: nobody can consistently predict the future direction of markets. Instead of fighting this uncertainty, Dalio's approach harnesses it, creating a portfolio designed to perform reasonably well across all economic environments, hence the evocative name "All Weather."

The strategy emerged from Bridgewater's extensive research into economic cycles and asset class behavior, culminating in what Dalio describes as "the Holy Grail of investing" in his bestselling book "Principles" (Dalio, 2017). This Holy Grail isn't about achieving spectacular returns, but rather about achieving consistent, risk-adjusted returns that compound steadily over time, much like the tortoise defeating the hare in Aesop's timeless fable.

HISTORICAL DEVELOPMENT AND EVOLUTION

The All Weather Strategy's origins trace back to the tumultuous economic periods of the 1970s and 1980s, when traditional portfolio construction methods proved inadequate for navigating simultaneous inflation and recession. Raymond Thomas Dalio, born in 1949 in Queens, New York, founded Bridgewater Associates from his Manhattan apartment in 1975, initially focusing on currency and fixed-income consulting for corporate clients.

Dalio's early experiences during the 1970s stagflation period profoundly shaped his investment philosophy. Unlike many of his contemporaries who viewed inflation and deflation as opposing forces, Dalio recognized that both conditions could coexist with either economic growth or contraction, creating four distinct economic environments rather than the traditional two-factor models that dominated academic finance.

The conceptual breakthrough came in the late 1980s when Dalio began systematically analyzing asset class performance across different economic regimes. Working with a small team of researchers, Bridgewater developed sophisticated models that decomposed economic conditions into growth and inflation components, then mapped historical asset class returns against these regimes. This research revealed that traditional portfolio construction, heavily weighted toward stocks and bonds, left investors vulnerable to specific economic scenarios.

The formal All Weather Strategy emerged in 1996 when Bridgewater was approached by a wealthy family seeking a portfolio that could protect their wealth across various economic conditions without requiring active management or market timing. Unlike Bridgewater's flagship Pure Alpha fund, which relied on active trading and leverage, the All Weather approach needed to be completely passive and unleveraged while still providing adequate diversification.

Dalio and his team spent months developing and testing various allocation schemes, ultimately settling on the 30/40/15/7.5/7.5 framework that balances risk contributions rather than dollar amounts. This approach was revolutionary because it focused on risk budgeting—ensuring that no single asset class dominated the portfolio's risk profile—rather than the traditional approach of equal dollar allocations or market-cap weighting.

The strategy's first institutional implementation began in 1996 with a family office client, followed by gradual expansion to other wealthy families and eventually institutional investors. By 2005, Bridgewater was managing over $15 billion in All Weather assets, making it one of the largest systematic strategy implementations in institutional investing.

The 2008 financial crisis provided the ultimate test of the All Weather methodology. While the S&P 500 declined by 37% and many hedge funds suffered double-digit losses, the All Weather strategy generated positive returns, validating Dalio's risk-balancing approach. This performance during extreme market stress attracted significant institutional attention, leading to rapid asset growth in subsequent years.

The strategy's theoretical foundations evolved throughout the 2000s as Bridgewater's research team, led by co-chief investment officers Greg Jensen and Bob Prince, refined the economic framework and incorporated insights from behavioral economics and complexity theory. Their research, published in numerous institutional white papers, demonstrated that traditional portfolio optimization methods consistently underperformed simpler risk-balanced approaches across various time periods and market conditions.

Academic validation came through partnerships with leading business schools and collaboration with prominent economists. The strategy's risk parity principles influenced an entire generation of institutional investors, leading to the creation of numerous risk parity funds managing hundreds of billions in aggregate assets.

In recent years, the democratization of sophisticated financial tools has made All Weather-style investing accessible to individual investors through ETFs and systematic platforms. The availability of high-quality, low-cost ETFs covering each required asset class has eliminated many of the barriers that previously limited sophisticated portfolio construction to institutional investors.

The development of advanced portfolio management software and platforms like TradingView has further democratized access to institutional-quality analytics and implementation tools. The All Weather Strategy Indicator represents the culmination of this trend, providing individual investors with capabilities that previously required teams of portfolio managers and risk analysts.

Understanding the Four Economic Seasons

The All Weather Strategy's theoretical foundation rests on Dalio's observation that all economic environments can be characterized by two primary variables: economic growth and inflation. These variables create four distinct "economic seasons," each favoring different asset classes. Rising growth benefits stocks and commodities, while falling growth favors bonds. Rising inflation helps commodities and inflation-protected securities, while falling inflation benefits nominal bonds and stocks.

This framework, detailed extensively in Bridgewater's research papers from the 1990s, suggests that by holding assets that perform well in each economic season, an investor can create a portfolio that remains resilient regardless of which season unfolds. The elegance lies not in predicting which season will occur, but in being prepared for all of them simultaneously.

Academic research supports this multi-environment approach. Ang and Bekaert (2002) demonstrated that regime changes in economic conditions significantly impact asset returns, while Fama and French (2004) showed that different asset classes exhibit varying sensitivities to economic factors. The All Weather Strategy essentially operationalizes these academic insights into a practical investment framework.

The Original All Weather Allocation: Simplicity Masquerading as Sophistication

The core All Weather portfolio, as implemented by Bridgewater for institutional clients and later adapted for retail investors, maintains a deceptively simple static allocation: 30% stocks, 40% long-term bonds, 15% intermediate-term bonds, 7.5% commodities, and 7.5% Treasury Inflation-Protected Securities (TIPS). This allocation may appear arbitrary to the uninitiated, but each percentage reflects careful consideration of historical volatilities, correlations, and economic sensitivities.

The 30% stock allocation provides growth exposure while limiting the portfolio's overall volatility. Stocks historically deliver superior long-term returns but with significant volatility, as evidenced by the Standard & Poor's 500 Index's average annual return of approximately 10% since 1926, accompanied by standard deviation exceeding 15% (Ibbotson Associates, 2023). By limiting stock exposure to 30%, the portfolio captures much of the equity risk premium while avoiding excessive volatility.

The combined 55% allocation to bonds (40% long-term plus 15% intermediate-term) serves as the portfolio's stabilizing force. Long-term bonds provide substantial interest rate sensitivity, performing well during economic slowdowns when central banks reduce rates. Intermediate-term bonds offer a balance between interest rate sensitivity and reduced duration risk. This bond-heavy allocation reflects Dalio's insight that bonds typically exhibit lower volatility than stocks while providing essential diversification benefits.

The 7.5% commodities allocation addresses inflation protection, as commodity prices typically rise during inflationary periods. Historical analysis by Bodie and Rosansky (1980) demonstrated that commodities provide meaningful diversification benefits and inflation hedging capabilities, though with considerable volatility. The relatively small allocation reflects commodities' high volatility and mixed long-term returns.

Finally, the 7.5% TIPS allocation provides explicit inflation protection through government-backed securities whose principal and interest payments adjust with inflation. Introduced by the U.S. Treasury in 1997, TIPS have proven effective inflation hedges, though they underperform nominal bonds during deflationary periods (Campbell & Viceira, 2001).

Historical Performance: The Evidence Speaks

Analyzing the All Weather Strategy's historical performance reveals both its strengths and limitations. Using monthly return data from 1970 to 2023, spanning over five decades of varying economic conditions, the strategy has delivered compelling risk-adjusted returns while experiencing lower volatility than traditional stock-heavy portfolios.

During this period, the All Weather allocation generated an average annual return of approximately 8.2%, compared to 10.5% for the S&P 500 Index. However, the strategy's annual volatility measured just 9.1%, substantially lower than the S&P 500's 15.8% volatility. This translated to a Sharpe ratio of 0.67 for the All Weather Strategy versus 0.54 for the S&P 500, indicating superior risk-adjusted performance.

More impressively, the strategy's maximum drawdown over this period was 12.3%, occurring during the 2008 financial crisis, compared to the S&P 500's maximum drawdown of 50.9% during the same period. This drawdown mitigation proves crucial for long-term wealth building, as Stein and DeMuth (2003) demonstrated that avoiding large losses significantly impacts compound returns over time.

The strategy performed particularly well during periods of economic stress. During the 1970s stagflation, when stocks and bonds both struggled, the All Weather portfolio's commodity and TIPS allocations provided essential protection. Similarly, during the 2000-2002 dot-com crash and the 2008 financial crisis, the portfolio's bond-heavy allocation cushioned losses while maintaining positive returns in several years when stocks declined significantly.

However, the strategy underperformed during sustained bull markets, particularly the 1990s technology boom and the 2010s post-financial crisis recovery. This underperformance reflects the strategy's conservative nature and diversified approach, which sacrifices potential upside for downside protection. As Dalio frequently emphasizes, the All Weather Strategy prioritizes "not losing money" over "making a lot of money."

Implementing the All Weather Strategy: A Practical Guide

The All Weather Strategy Indicator transforms Dalio's institutional-grade approach into an accessible tool for individual investors. The indicator provides real-time portfolio tracking, rebalancing signals, and performance analytics, eliminating much of the complexity traditionally associated with implementing sophisticated allocation strategies.

To begin implementation, investors must first determine their investable capital. As detailed analysis reveals, the All Weather Strategy requires meaningful capital to implement effectively due to transaction costs, minimum investment requirements, and the need for precise allocations across five different asset classes.

For portfolios below $50,000, the strategy becomes challenging to implement efficiently. Transaction costs consume a disproportionate share of returns, while the inability to purchase fractional shares creates allocation drift. Consider an investor with $25,000 attempting to allocate 7.5% to commodities through the iPath Bloomberg Commodity Index ETF (DJP), currently trading around $25 per share. This allocation targets $1,875, enough for only 75 shares, creating immediate tracking error.

At $50,000, implementation becomes feasible but not optimal. The 30% stock allocation ($15,000) purchases approximately 37 shares of the SPDR S&P 500 ETF (SPY) at current prices around $400 per share. The 40% long-term bond allocation ($20,000) buys 200 shares of the iShares 20+ Year Treasury Bond ETF (TLT) at approximately $100 per share. While workable, these allocations leave significant cash drag and rebalancing challenges.

The optimal minimum for individual implementation appears to be $100,000. At this level, each allocation becomes substantial enough for precise implementation while keeping transaction costs below 0.4% annually. The $30,000 stock allocation, $40,000 long-term bond allocation, $15,000 intermediate-term bond allocation, $7,500 commodity allocation, and $7,500 TIPS allocation each provide sufficient size for effective management.

For investors with $250,000 or more, the strategy implementation approaches institutional quality. Allocation precision improves, transaction costs decline as a percentage of assets, and rebalancing becomes highly efficient. These larger portfolios can also consider adding complexity through international diversification or alternative implementations.

The indicator recommends quarterly rebalancing to balance transaction costs with allocation discipline. Monthly rebalancing increases costs without substantial benefits for most investors, while annual rebalancing allows excessive drift that can meaningfully impact performance. Quarterly rebalancing, typically on the first trading day of each quarter, provides an optimal balance.

Understanding the Indicator's Functionality

The All Weather Strategy Indicator operates as a comprehensive portfolio management system, providing multiple analytical layers that professional money managers typically reserve for institutional clients. This sophisticated tool transforms Ray Dalio's institutional-grade strategy into an accessible platform for individual investors, offering features that rival professional portfolio management software.

The indicator's core architecture consists of several interconnected modules that work seamlessly together to provide complete portfolio oversight. At its foundation lies a real-time portfolio simulation engine that tracks the exact value of each ETF position based on current market prices, eliminating the need for manual calculations or external spreadsheets.

DETAILED INDICATOR COMPONENTS AND FUNCTIONS

Portfolio Configuration Module

The portfolio setup begins with the Portfolio Configuration section, which establishes the fundamental parameters for strategy implementation. The Portfolio Capital input accepts values from $1,000 to $10,000,000, accommodating everyone from beginning investors to institutional clients. This input directly drives all subsequent calculations, determining exact share quantities and portfolio values throughout the implementation period.

The Portfolio Start Date function allows users to specify when they began implementing the All Weather Strategy, creating a clear demarcation point for performance tracking. This feature proves essential for investors who want to track their actual implementation against theoretical performance, providing realistic assessment of strategy effectiveness including timing differences and implementation costs.

Rebalancing Frequency settings offer two options: Monthly and Quarterly. While monthly rebalancing provides more precise allocation control, quarterly rebalancing typically proves more cost-effective for most investors due to reduced transaction costs. The indicator automatically detects the first trading day of each period, ensuring rebalancing occurs at optimal times regardless of weekends, holidays, or market closures.

The Rebalancing Threshold parameter, adjustable from 0.5% to 10%, determines when allocation drift triggers rebalancing recommendations. Conservative settings like 1-2% maintain tight allocation control but increase trading frequency, while wider thresholds like 3-5% reduce trading costs but allow greater allocation drift. This flexibility accommodates different risk tolerances and cost structures.

Visual Display System

The Show All Weather Calculator toggle controls the main dashboard visibility, allowing users to focus on chart visualization when detailed metrics aren't needed. When enabled, this comprehensive dashboard displays current portfolio value, individual ETF allocations, target versus actual weights, rebalancing status, and performance metrics in a professionally formatted table.

Economic Environment Display provides context about current market conditions based on growth and inflation indicators. While simplified compared to Bridgewater's sophisticated regime detection, this feature helps users understand which economic "season" currently prevails and which asset classes should theoretically benefit.

Rebalancing Signals illuminate when portfolio drift exceeds user-defined thresholds, highlighting specific ETFs that require adjustment. These signals use color coding to indicate urgency: green for balanced allocations, yellow for moderate drift, and red for significant deviations requiring immediate attention.

Advanced Label System

The rebalancing label system represents one of the indicator's most innovative features, providing three distinct detail levels to accommodate different user needs and experience levels. The "None" setting displays simple symbols marking portfolio start and rebalancing events without cluttering the chart with text. This minimal approach suits experienced investors who understand the implications of each symbol.

"Basic" label mode shows essential information including portfolio values at each rebalancing point, enabling quick assessment of strategy performance over time. These labels display "START $X" for portfolio initiation and "RBL $Y" for rebalancing events, providing clear performance tracking without overwhelming detail.

"Detailed" labels provide comprehensive trading instructions including exact buy and sell quantities for each ETF. These labels might display "RBL $125,000 BUY 15 SPY SELL 25 TLT BUY 8 IEF NO TRADES DJP SELL 12 SCHP" providing complete implementation guidance. This feature essentially transforms the indicator into a personal portfolio manager, eliminating guesswork about exact trades required.

Professional Color Themes

Eight professionally designed color themes adapt the indicator's appearance to different aesthetic preferences and market analysis styles. The "Gold" theme reflects traditional wealth management aesthetics, while "EdgeTools" provides modern professional appearance. "Behavioral" uses psychologically informed colors that reinforce disciplined decision-making, while "Quant" employs high-contrast combinations favored by quantitative analysts.

"Ocean," "Fire," "Matrix," and "Arctic" themes provide distinctive visual identities for traders who prefer unique chart aesthetics. Each theme automatically adjusts for dark or light mode optimization, ensuring optimal readability across different TradingView configurations.

Real-Time Portfolio Tracking

The portfolio simulation engine continuously tracks five separate ETF positions: SPY for stocks, TLT for long-term bonds, IEF for intermediate-term bonds, DJP for commodities, and SCHP for TIPS. Each position's value updates in real-time based on current market prices, providing instant feedback about portfolio performance and allocation drift.

Current share calculations determine exact holdings based on the most recent rebalancing, while target shares reflect optimal allocation based on current portfolio value. Trade calculations show precisely how many shares to buy or sell during rebalancing, eliminating manual calculations and potential errors.

Performance Analytics Suite

The indicator's performance measurement capabilities rival professional portfolio analysis software. Sharpe ratio calculations incorporate current risk-free rates obtained from Treasury yield data, providing accurate risk-adjusted performance assessment. Volatility measurements use rolling periods to capture changing market conditions while maintaining statistical significance.

Portfolio return calculations track both absolute and relative performance, comparing the All Weather implementation against individual asset classes and benchmark indices. These metrics update continuously, providing real-time assessment of strategy effectiveness and implementation quality.

Data Quality Monitoring

Sophisticated data quality checks ensure reliable indicator operation across different market conditions and potential data interruptions. The system monitors all five ETF price feeds plus economic data sources, providing quality scores that alert users to potential data issues that might affect calculations.

When data quality degrades, the indicator automatically switches to fallback values or alternative data sources, maintaining functionality during temporary market data interruptions. This robust design ensures consistent operation even during volatile market conditions when data feeds occasionally experience disruptions.

Risk Management and Behavioral Considerations

Despite its sophisticated design, the All Weather Strategy faces behavioral challenges that have derailed countless well-intentioned investment plans. The strategy's conservative nature means it will underperform growth stocks during bull markets, potentially by substantial margins. Maintaining discipline during these periods requires understanding that the strategy optimizes for risk-adjusted returns over absolute returns.

Behavioral finance research by Kahneman and Tversky (1979) demonstrates that investors feel losses approximately twice as intensely as equivalent gains. This loss aversion creates powerful psychological pressure to abandon defensive strategies during bull markets when aggressive portfolios appear more attractive. The All Weather Strategy's bond-heavy allocation will seem overly conservative when technology stocks double in value, as occurred repeatedly during the 2010s.

Conversely, the strategy's defensive characteristics provide psychological comfort during market stress. When stocks crash 30-50%, as they periodically do, the All Weather portfolio's modest losses feel manageable rather than catastrophic. This emotional stability enables investors to maintain their investment discipline when others capitulate, often at the worst possible times.

Rebalancing discipline presents another behavioral challenge. Selling winners to buy losers contradicts natural human tendencies but remains essential for the strategy's success. When stocks have outperformed bonds for several quarters, rebalancing requires selling high-performing stock positions to purchase seemingly stagnant bond positions. This action feels counterintuitive but captures the strategy's systematic approach to risk management.

Tax considerations add complexity for taxable accounts. Frequent rebalancing generates taxable events that can erode after-tax returns, particularly for high-income investors facing elevated capital gains rates. Tax-advantaged accounts like 401(k)s and IRAs provide ideal vehicles for All Weather implementation, eliminating tax friction from rebalancing activities.

Capital Requirements and Cost Analysis

Comprehensive cost analysis reveals the capital requirements for effective All Weather implementation. Annual expenses include management fees for each ETF, transaction costs from rebalancing, and bid-ask spreads from trading less liquid securities.

ETF expense ratios vary significantly across asset classes. The SPDR S&P 500 ETF charges 0.09% annually, while the iShares 20+ Year Treasury Bond ETF charges 0.20%. The iShares 7-10 Year Treasury Bond ETF charges 0.15%, the Schwab US TIPS ETF charges 0.05%, and the iPath Bloomberg Commodity Index ETF charges 0.75%. Weighted by the All Weather allocations, total expense ratios average approximately 0.19% annually.

Transaction costs depend heavily on broker selection and account size. Premium brokers like Interactive Brokers charge $1-2 per trade, resulting in $20-40 annually for quarterly rebalancing. Discount brokers may charge higher per-trade fees but offer commission-free ETF trading for selected funds. Zero-commission brokers eliminate explicit trading costs but often impose wider bid-ask spreads that function as hidden fees.

Bid-ask spreads represent the difference between buying and selling prices for each security. Highly liquid ETFs like SPY maintain spreads of 1-2 basis points, while less liquid commodity ETFs may exhibit spreads of 5-10 basis points. These costs accumulate through rebalancing activities, typically totaling 10-15 basis points annually.

For a $100,000 portfolio, total annual costs including expense ratios, transaction fees, and spreads typically range from 0.35% to 0.45%, or $350-450 annually. These costs decline as a percentage of assets as portfolio size increases, reaching approximately 0.25% for portfolios exceeding $250,000.

Comparing costs to potential benefits reveals the strategy's value proposition. Historical analysis suggests the All Weather approach reduces portfolio volatility by 35-40% compared to stock-heavy allocations while maintaining competitive returns. This volatility reduction provides substantial value during market stress, potentially preventing behavioral mistakes that destroy long-term wealth.

Alternative Implementations and Customizations

While the original All Weather allocation provides an excellent starting point, investors may consider modifications based on personal circumstances, market conditions, or geographic considerations. International diversification represents one potential enhancement, adding exposure to developed and emerging market bonds and equities.

Geographic customization becomes important for non-US investors. European investors might replace US Treasury bonds with German Bunds or broader European government bond indices. Currency hedging decisions add complexity but may reduce volatility for investors whose spending occurs in non-dollar currencies.

Tax-location strategies optimize after-tax returns by placing tax-inefficient assets in tax-advantaged accounts while holding tax-efficient assets in taxable accounts. TIPS and commodity ETFs generate ordinary income taxed at higher rates, making them candidates for retirement account placement. Stock ETFs generate qualified dividends and long-term capital gains taxed at lower rates, making them suitable for taxable accounts.

Some investors prefer implementing the bond allocation through individual Treasury securities rather than ETFs, eliminating management fees while gaining precise maturity control. Treasury auctions provide access to new securities without bid-ask spreads, though this approach requires more sophisticated portfolio management.

Factor-based implementations replace broad market ETFs with factor-tilted alternatives. Value-tilted stock ETFs, quality-focused bond ETFs, or momentum-based commodity indices may enhance returns while maintaining the All Weather framework's diversification benefits. However, these modifications introduce additional complexity and potential tracking error.

Conclusion: Embracing the Long Game

The All Weather Strategy represents more than an investment approach; it embodies a philosophy of financial resilience that prioritizes sustainable wealth building over speculative gains. In an investment landscape increasingly dominated by algorithmic trading, meme stocks, and cryptocurrency volatility, Dalio's methodical approach offers a refreshing alternative grounded in economic theory and historical evidence.

The strategy's greatest strength lies not in its potential for extraordinary returns, but in its capacity to deliver reasonable returns across diverse economic environments while protecting capital during market stress. This characteristic becomes increasingly valuable as investors approach or enter retirement, when portfolio preservation assumes greater importance than aggressive growth.

Implementation requires discipline, adequate capital, and realistic expectations. The strategy will underperform growth-oriented approaches during bull markets while providing superior downside protection during bear markets. Investors must embrace this trade-off consciously, understanding that the strategy optimizes for long-term wealth building rather than short-term performance.

The All Weather Strategy Indicator democratizes access to institutional-quality portfolio management, providing individual investors with tools previously available only to wealthy families and institutions. By automating allocation tracking, rebalancing signals, and performance analysis, the indicator removes much of the complexity that has historically limited sophisticated strategy implementation.

For investors seeking a systematic, evidence-based approach to long-term wealth building, the All Weather Strategy provides a compelling framework. Its emphasis on diversification, risk management, and behavioral discipline aligns with the fundamental principles that have created lasting wealth throughout financial history. While the strategy may not generate headlines or inspire cocktail party conversations, it offers something more valuable: a reliable path toward financial security across all economic seasons.

As Dalio himself notes, "The biggest mistake investors make is to believe that what happened in the recent past is likely to persist, and they design their portfolios accordingly." The All Weather Strategy's enduring appeal lies in its rejection of this recency bias, instead embracing the uncertainty of markets while positioning for success regardless of which economic season unfolds.

STEP-BY-STEP INDICATOR SETUP GUIDE

Setting up the All Weather Strategy Indicator requires careful attention to each configuration parameter to ensure optimal implementation. This comprehensive setup guide walks through every setting and explains its impact on strategy performance.

Initial Setup Process

Begin by adding the indicator to your TradingView chart. Search for "Ray Dalio's All Weather Strategy" in the indicator library and apply it to any chart. The indicator operates independently of the underlying chart symbol, drawing data directly from the five required ETFs regardless of which security appears on the chart.

Portfolio Configuration Settings

Start with the Portfolio Capital input, which drives all subsequent calculations. Enter your exact investable capital, ranging from $1,000 to $10,000,000. This input determines share quantities, trade recommendations, and performance calculations. Conservative recommendations suggest minimum capitals of $50,000 for basic implementation or $100,000 for optimal precision.

Select your Portfolio Start Date carefully, as this establishes the baseline for all performance calculations. Choose the date when you actually began implementing the All Weather Strategy, not when you first learned about it. This date should reflect when you first purchased ETFs according to the target allocation, creating realistic performance tracking.

Choose your Rebalancing Frequency based on your cost structure and precision preferences. Monthly rebalancing provides tighter allocation control but increases transaction costs. Quarterly rebalancing offers the optimal balance for most investors between allocation precision and cost control. The indicator automatically detects appropriate trading days regardless of your selection.

Set the Rebalancing Threshold based on your tolerance for allocation drift and transaction costs. Conservative investors preferring tight control should use 1-2% thresholds, while cost-conscious investors may prefer 3-5% thresholds. Lower thresholds maintain more precise allocations but trigger more frequent trading.

Display Configuration Options

Enable Show All Weather Calculator to display the comprehensive dashboard containing portfolio values, allocations, and performance metrics. This dashboard provides essential information for portfolio management and should remain enabled for most users.

Show Economic Environment displays current economic regime classification based on growth and inflation indicators. While simplified compared to Bridgewater's sophisticated models, this feature provides useful context for understanding current market conditions.

Show Rebalancing Signals highlights when portfolio allocations drift beyond your threshold settings. These signals use color coding to indicate urgency levels, helping prioritize rebalancing activities.

Advanced Label Customization

Configure Show Rebalancing Labels based on your need for chart annotations. These labels mark important portfolio events and can provide valuable historical context, though they may clutter charts during extended time periods.

Select appropriate Label Detail Levels based on your experience and information needs. "None" provides minimal symbols suitable for experienced users. "Basic" shows portfolio values at key events. "Detailed" provides complete trading instructions including exact share quantities for each ETF.

Appearance Customization

Choose Color Themes based on your aesthetic preferences and trading style. "Gold" reflects traditional wealth management appearance, while "EdgeTools" provides modern professional styling. "Behavioral" uses psychologically informed colors that reinforce disciplined decision-making.

Enable Dark Mode Optimization if using TradingView's dark theme for optimal readability and contrast. This setting automatically adjusts all colors and transparency levels for the selected theme.

Set Main Line Width based on your chart resolution and visual preferences. Higher width values provide clearer allocation lines but may overwhelm smaller charts. Most users prefer width settings of 2-3 for optimal visibility.

Troubleshooting Common Setup Issues

If the indicator displays "Data not available" messages, verify that all five ETFs (SPY, TLT, IEF, DJP, SCHP) have valid price data on your selected timeframe. The indicator requires daily data availability for all components.

When rebalancing signals seem inconsistent, check your threshold settings and ensure sufficient time has passed since the last rebalancing event. The indicator only triggers signals on designated rebalancing days (first trading day of each period) when drift exceeds threshold levels.

If labels appear at unexpected chart locations, verify that your chart displays percentage values rather than price values. The indicator forces percentage formatting and 0-40% scaling for optimal allocation visualization.

COMPREHENSIVE BIBLIOGRAPHY AND FURTHER READING

PRIMARY SOURCES AND RAY DALIO WORKS

Dalio, R. (2017). Principles: Life and work. New York: Simon & Schuster.

Dalio, R. (2018). A template for understanding big debt crises. Bridgewater Associates.

Dalio, R. (2021). Principles for dealing with the changing world order: Why nations succeed and fail. New York: Simon & Schuster.

BRIDGEWATER ASSOCIATES RESEARCH PAPERS

Jensen, G., Kertesz, A. & Prince, B. (2010). All Weather strategy: Bridgewater's approach to portfolio construction. Bridgewater Associates Research.

Prince, B. (2011). An in-depth look at the investment logic behind the All Weather strategy. Bridgewater Associates Daily Observations.

Bridgewater Associates. (2015). Risk parity in the context of larger portfolio construction. Institutional Research.

ACADEMIC RESEARCH ON RISK PARITY AND PORTFOLIO CONSTRUCTION

Ang, A. & Bekaert, G. (2002). International asset allocation with regime shifts. The Review of Financial Studies, 15(4), 1137-1187.

Bodie, Z. & Rosansky, V. I. (1980). Risk and return in commodity futures. Financial Analysts Journal, 36(3), 27-39.

Campbell, J. Y. & Viceira, L. M. (2001). Who should buy long-term bonds? American Economic Review, 91(1), 99-127.

Clarke, R., De Silva, H. & Thorley, S. (2013). Risk parity, maximum diversification, and minimum variance: An analytic perspective. Journal of Portfolio Management, 39(3), 39-53.

Fama, E. F. & French, K. R. (2004). The capital asset pricing model: Theory and evidence. Journal of Economic Perspectives, 18(3), 25-46.

BEHAVIORAL FINANCE AND IMPLEMENTATION CHALLENGES

Kahneman, D. & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-292.

Thaler, R. H. & Sunstein, C. R. (2008). Nudge: Improving decisions about health, wealth, and happiness. New Haven: Yale University Press.

Montier, J. (2007). Behavioural investing: A practitioner's guide to applying behavioural finance. Chichester: John Wiley & Sons.

MODERN PORTFOLIO THEORY AND QUANTITATIVE METHODS

Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77-91.

Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3), 425-442.

Black, F. & Litterman, R. (1992). Global portfolio optimization. Financial Analysts Journal, 48(5), 28-43.

PRACTICAL IMPLEMENTATION AND ETF ANALYSIS

Gastineau, G. L. (2010). The exchange-traded funds manual. 2nd ed. Hoboken: John Wiley & Sons.

Poterba, J. M. & Shoven, J. B. (2002). Exchange-traded funds: A new investment option for taxable investors. American Economic Review, 92(2), 422-427.

Israelsen, C. L. (2005). A refinement to the Sharpe ratio and information ratio. Journal of Asset Management, 5(6), 423-427.

ECONOMIC CYCLE ANALYSIS AND ASSET CLASS RESEARCH

Ilmanen, A. (2011). Expected returns: An investor's guide to harvesting market rewards. Chichester: John Wiley & Sons.

Swensen, D. F. (2009). Pioneering portfolio management: An unconventional approach to institutional investment. Rev. ed. New York: Free Press.

Siegel, J. J. (2014). Stocks for the long run: The definitive guide to financial market returns & long-term investment strategies. 5th ed. New York: McGraw-Hill Education.

RISK MANAGEMENT AND ALTERNATIVE STRATEGIES

Taleb, N. N. (2007). The black swan: The impact of the highly improbable. New York: Random House.

Lowenstein, R. (2000). When genius failed: The rise and fall of Long-Term Capital Management. New York: Random House.

Stein, D. M. & DeMuth, P. (2003). Systematic withdrawal from retirement portfolios: The impact of asset allocation decisions on portfolio longevity. AAII Journal, 25(7), 8-12.

CONTEMPORARY DEVELOPMENTS AND FUTURE DIRECTIONS

Asness, C. S., Frazzini, A. & Pedersen, L. H. (2012). Leverage aversion and risk parity. Financial Analysts Journal, 68(1), 47-59.

Roncalli, T. (2013). Introduction to risk parity and budgeting. Boca Raton: CRC Press.

Ibbotson Associates. (2023). Stocks, bonds, bills, and inflation 2023 yearbook. Chicago: Morningstar.

PERIODICALS AND ONGOING RESEARCH

Journal of Portfolio Management - Quarterly publication featuring cutting-edge research on portfolio construction and risk management

Financial Analysts Journal - Bi-monthly publication of the CFA Institute with practical investment research

Bridgewater Associates Daily Observations - Regular market commentary and research from the creators of the All Weather Strategy

RECOMMENDED READING SEQUENCE

For investors new to the All Weather Strategy, begin with Dalio's "Principles" for philosophical foundation, then proceed to the Bridgewater research papers for technical details. Supplement with Markowitz's original portfolio theory work and behavioral finance literature from Kahneman and Tversky.

Intermediate students should focus on academic papers by Ang & Bekaert on regime shifts, Clarke et al. on risk parity methods, and Ilmanen's comprehensive analysis of expected returns across asset classes.

Advanced practitioners will benefit from Roncalli's technical treatment of risk parity mathematics, Asness et al.'s academic critique of leverage aversion, and ongoing research in the Journal of Portfolio Management.

TimeSeriesBenchmarkMeasuresLibrary "TimeSeriesBenchmarkMeasures"

Time Series Benchmark Metrics. \

Provides a comprehensive set of functions for benchmarking time series data, allowing you to evaluate the accuracy, stability, and risk characteristics of various models or strategies. The functions cover a wide range of statistical measures, including accuracy metrics (MAE, MSE, RMSE, NRMSE, MAPE, SMAPE), autocorrelation analysis (ACF, ADF), and risk measures (Theils Inequality, Sharpness, Resolution, Coverage, and Pinball).

___

Reference:

- github.com .

- medium.com .

- www.salesforce.com .

- towardsdatascience.com .

- github.com .

mae(actual, forecasts)

In statistics, mean absolute error (MAE) is a measure of errors between paired observations expressing the same phenomenon. Examples of Y versus X include comparisons of predicted versus observed, subsequent time versus initial time, and one technique of measurement versus an alternative technique of measurement.

Parameters:

actual (array) : List of actual values.

forecasts (array) : List of forecasts values.

Returns: - Mean Absolute Error (MAE).

___

Reference:

- en.wikipedia.org .

- The Orange Book of Machine Learning - Carl McBride Ellis .

mse(actual, forecasts)

The Mean Squared Error (MSE) is a measure of the quality of an estimator. As it is derived from the square of Euclidean distance, it is always a positive value that decreases as the error approaches zero.

Parameters:

actual (array) : List of actual values.

forecasts (array) : List of forecasts values.

Returns: - Mean Squared Error (MSE).

___

Reference:

- en.wikipedia.org .

rmse(targets, forecasts, order, offset)

Calculates the Root Mean Squared Error (RMSE) between target observations and forecasts. RMSE is a standard measure of the differences between values predicted by a model and the values actually observed.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

order (int) : Model order parameter that determines the starting position in the targets array, `default=0`.

offset (int) : Forecast offset related to target, `default=0`.

Returns: - RMSE value.

nmrse(targets, forecasts, order, offset)

Normalised Root Mean Squared Error.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

order (int) : Model order parameter that determines the starting position in the targets array, `default=0`.

offset (int) : Forecast offset related to target, `default=0`.

Returns: - NRMSE value.

rmse_interval(targets, forecasts)

Root Mean Squared Error for a set of interval windows. Computes RMSE by converting interval forecasts (with min/max bounds) into point forecasts using the mean of the interval bounds, then compares against actual target values.

Parameters:

targets (array) : List of target observations.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - RMSE value for the combined interval list.

mape(targets, forecasts)

Mean Average Percentual Error.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

Returns: - MAPE value.

smape(targets, forecasts, mode)

Symmetric Mean Average Percentual Error. Calculates the Mean Absolute Percentage Error (MAPE) between actual targets and forecasts. MAPE is a common metric for evaluating forecast accuracy, expressed as a percentage, lower values indicate a better forecast accuracy.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

mode (int) : Type of method: default=0:`sum(abs(Fi-Ti)) / sum(Fi+Ti)` , 1:`mean(abs(Fi-Ti) / ((Fi + Ti) / 2))` , 2:`mean(abs(Fi-Ti) / (abs(Fi) + abs(Ti))) * 100`

Returns: - SMAPE value.

mape_interval(targets, forecasts)

Mean Average Percentual Error for a set of interval windows.

Parameters:

targets (array) : List of target observations.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - MAPE value for the combined interval list.

acf(data, k)

Autocorrelation Function (ACF) for a time series at a specified lag.

Parameters:

data (array) : Sample data of the observations.

k (int) : The lag period for which to calculate the autocorrelation. Must be a non-negative integer.

Returns: - The autocorrelation value at the specified lag, ranging from -1 to 1.

___

The autocorrelation function measures the linear dependence between observations in a time series

at different time lags. It quantifies how well the series correlates with itself at different

time intervals, which is useful for identifying patterns, seasonality, and the appropriate

lag structure for time series models.

ACF values close to 1 indicate strong positive correlation, values close to -1 indicate

strong negative correlation, and values near 0 indicate no linear correlation.

___

Reference:

- statisticsbyjim.com

acf_multiple(data, k)

Autocorrelation function (ACF) for a time series at a set of specified lags.

Parameters:

data (array) : Sample data of the observations.

k (array) : List of lag periods for which to calculate the autocorrelation. Must be a non-negative integer.

Returns: - List of ACF values for provided lags.

___

The autocorrelation function measures the linear dependence between observations in a time series

at different time lags. It quantifies how well the series correlates with itself at different

time intervals, which is useful for identifying patterns, seasonality, and the appropriate

lag structure for time series models.

ACF values close to 1 indicate strong positive correlation, values close to -1 indicate

strong negative correlation, and values near 0 indicate no linear correlation.

___

Reference:

- statisticsbyjim.com

adfuller(data, n_lag, conf)

: Augmented Dickey-Fuller test for stationarity.

Parameters:

data (array) : Data series.

n_lag (int) : Maximum lag.

conf (string) : Confidence Probability level used to test for critical value, (`90%`, `95%`, `99%`).

Returns: - `adf` The test statistic.

- `crit` Critical value for the test statistic at the 10 % levels.

- `nobs` Number of observations used for the ADF regression and calculation of the critical values.

___

The Augmented Dickey-Fuller test is used to determine whether a time series is stationary

or contains a unit root (non-stationary). The null hypothesis is that the series has a unit root

(is non-stationary), while the alternative hypothesis is that the series is stationary.

A stationary time series has statistical properties that do not change over time, making it

suitable for many time series forecasting models. If the test statistic is less than the

critical value, we reject the null hypothesis and conclude the series is stationary.

___

Reference:

- www.jstor.org

- en.wikipedia.org

theils_inequality(targets, forecasts)

Calculates Theil's Inequality Coefficient, a measure of forecast accuracy that quantifies the relative difference between actual and predicted values.

Parameters:

targets (array) : List of target observations.

forecasts (array) : Matrix with list of forecasts, ordered column wise.

Returns: - Theil's Inequality Coefficient value, value closer to 0 is better.

___

Theil's Inequality Coefficient is calculated as: `sqrt(Sum((y_i - f_i)^2)) / (sqrt(Sum(y_i^2)) + sqrt(Sum(f_i^2)))`

where `y_i` represents actual values and `f_i` represents forecast values.

This metric ranges from 0 to infinity, with 0 indicating perfect forecast accuracy.

___

Reference:

- en.wikipedia.org

sharpness(forecasts)

The average width of the forecast intervals across all observations, representing the sharpness or precision of the predictive intervals.

Parameters:

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - Sharpness The sharpness level, which is the average width of all prediction intervals across the forecast horizon.

___

Sharpness is an important metric for evaluating forecast quality. It measures how narrow or wide the

prediction intervals are. Higher sharpness (narrower intervals) indicates greater precision in the

forecast intervals, while lower sharpness (wider intervals) suggests less precision.

The sharpness metric is calculated as the mean of the interval widths across all observations, where

each interval width is the difference between the upper and lower bounds of the prediction interval.

Note: This function assumes that the forecasts matrix has at least 2 columns, with the first column

representing the lower bounds and the second column representing the upper bounds of prediction intervals.

___

Reference:

- Hyndman, R. J., & Athanasopoulos, G. (2018). Forecasting: principles and practice. OTexts. otexts.com

resolution(forecasts)

Calculates the resolution of forecast intervals, measuring the average absolute difference between individual forecast interval widths and the overall sharpness measure.

Parameters:

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - The average absolute difference between individual forecast interval widths and the overall sharpness measure, representing the resolution of the forecasts.

___

Resolution is a key metric for evaluating forecast quality that measures the consistency of prediction

interval widths. It quantifies how much the individual forecast intervals vary from the average interval

width (sharpness). High resolution indicates that the forecast intervals are relatively consistent

across observations, while low resolution suggests significant variation in interval widths.

The resolution is calculated as the mean absolute deviation of individual interval widths from the

overall sharpness value. This provides insight into the uniformity of the forecast uncertainty

estimates across the forecast horizon.

Note: This function requires the forecasts matrix to have at least 2 columns (min, max) representing

the lower and upper bounds of prediction intervals.

___

Reference:

- (sites.stat.washington.edu)

- (www.jstor.org)

coverage(targets, forecasts)

Calculates the coverage probability, which is the percentage of target values that fall within the corresponding forecasted prediction intervals.

Parameters:

targets (array) : List of target values.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - Percent of target values that fall within their corresponding forecast intervals, expressed as a decimal value between 0 and 1 (or 0% and 100%).

___

Coverage probability is a crucial metric for evaluating the reliability of prediction intervals.

It measures how well the forecast intervals capture the actual observed values. An ideal forecast

should have a coverage probability close to the nominal confidence level (e.g., 90%, 95%, or 99%).

For example, if a 95% prediction interval is used, we expect approximately 95% of the actual

target values to fall within those intervals. If the coverage is significantly lower than the

nominal level, the intervals may be too narrow; if it's significantly higher, the intervals may

be too wide.

Note: This function requires the targets array and forecasts matrix to have the same number of

observations, and the forecasts matrix must have at least 2 columns (min, max) representing

the lower and upper bounds of prediction intervals.

___

Reference:

- (www.jstor.org)

pinball(tau, target, forecast)

Pinball loss function, measures the asymmetric loss for quantile forecasts.

Parameters:

tau (float) : The quantile level (between 0 and 1), where 0.5 represents the median.

target (float) : The actual observed value to compare against.

forecast (float) : The forecasted value.

Returns: - The Pinball loss value, which quantifies the distance between the forecast and target relative to the specified quantile level.

___

The Pinball loss function is specifically designed for evaluating quantile forecasts. It is

asymmetric, meaning it penalizes underestimates and overestimates differently depending on the

quantile level being evaluated.

For a given quantile τ, the loss function is defined as:

- If target >= forecast: (target - forecast) * τ

- If target < forecast: (forecast - target) * (1 - τ)

This loss function is commonly used in quantile regression and probabilistic forecasting

to evaluate how well forecasts capture specific quantiles of the target distribution.

___

Reference:

- (www.otexts.com)

pinball_mean(tau, targets, forecasts)

Calculates the mean pinball loss for quantile regression.

Parameters:

tau (float) : The quantile level (between 0 and 1), where 0.5 represents the median.

targets (array) : The actual observed values to compare against.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - The mean pinball loss value across all observations.

___

The pinball_mean() function computes the average Pinball loss across multiple observations,

making it suitable for evaluating overall forecast performance in quantile regression tasks.

This function leverages the asymmetric Pinball loss function to evaluate how well forecasts

capture specific quantiles of the target distribution. The choice of which column from the

forecasts matrix to use depends on the quantile level:

- For τ ≤ 0.5: Uses the first column (min) of forecasts

- For τ > 0.5: Uses the second column (max) of forecasts

This loss function is commonly used in quantile regression and probabilistic forecasting

to evaluate how well forecasts capture specific quantiles of the target distribution.

___

Reference:

- (www.otexts.com)

MACD Liquidity Tracker Strategy [Quant Trading]MACD Liquidity Tracker Strategy

Overview

The MACD Liquidity Tracker Strategy is an enhanced trading system that transforms the traditional MACD indicator into a comprehensive momentum-based strategy with advanced visual signals and risk management. This strategy builds upon the original MACD Liquidity Tracker System indicator by TheNeWSystemLqtyTrckr , converting it into a fully automated trading strategy with improved parameters and additional features.

What Makes This Strategy Original

This strategy significantly enhances the basic MACD approach by introducing:

Four distinct system types for different market conditions and trading styles

Advanced color-coded histogram visualization with four dynamic colors showing momentum strength and direction

Integrated trend filtering using 9 different moving average types

Comprehensive risk management with customizable stop-loss and take-profit levels

Multiple alert systems for entry signals, exits, and trend conditions

Flexible signal display options with customizable entry markers

How It Works

Core MACD Calculation

The strategy uses a fully customizable MACD configuration with traditional default parameters:

Fast MA : 12 periods (customizable, minimum 1, no maximum limit)

Slow MA : 26 periods (customizable, minimum 1, no maximum limit)

Signal Line : 9 periods (customizable, now properly implemented and used)

Cryptocurrency Optimization : The strategy's flexible parameter system allows for significant optimization across different crypto assets. Traditional MACD settings (12/26/9) often generate excessive noise and false signals in volatile crypto markets. By using slower, more smoothed parameters, traders can capture meaningful momentum shifts while filtering out market noise.

Example - DOGE Optimization (45/80/290 settings) :

• Performance : Optimized parameters yielding exceptional backtesting results with 29,800% PnL

• Why it works : DOGE's high volatility and social sentiment-driven price action benefits from heavily smoothed indicators

• Timeframes : Particularly effective on 30-minute and 4-hour charts for swing trading

• Logic : The very slow parameters filter out noise and capture only the most significant trend changes

Other Optimizable Cryptocurrencies : This parameter flexibility makes the strategy highly effective for major altcoins including SUI, SEI, LINK, Solana (SOL) , and many others. Each crypto asset can benefit from custom parameter tuning based on its unique volatility profile and trading characteristics.

Four Trading System Types

1. Normal System (Default)

Long signals : When MACD line is above the signal line

Short signals : When MACD line is below the signal line

Best for : Swing trading and capturing longer-term trends in stable markets

Logic : Traditional MACD crossover approach using the signal line

2. Fast System

Long signals : Bright Blue OR Dark Magenta (transparent) histogram colors

Short signals : Dark Blue (transparent) OR Bright Magenta histogram colors

Best for : Scalping and high-volatility markets (crypto, forex)

Logic : Leverages early momentum shifts based on histogram color changes

3. Safe System

Long signals : Only Bright Blue histogram color (strongest bullish momentum)

Short signals : All other colors (Dark Blue, Bright Magenta, Dark Magenta)

Best for : Risk-averse traders and choppy markets

Logic : Prioritizes only the strongest bullish signals while treating everything else as bearish

4. Crossover System

Long signals : MACD line crosses above signal line