GBTC Premium to CoinbaseThe BTC ETF premium indicator for TradingView is a specialized tool designed to measure and visualize the premium or discount of the Grayscale Bitcoin Trust (GBTC), an investment vehicle that holds Bitcoin, relative to the actual price of Bitcoin on the Coinbase exchange. This indicator can be particularly insightful for traders interested in the BTC securities market and those analyzing the demand for Bitcoin as reflected by institutional investment products.

#### Description:

The BTC ETF premium indicator in TradingView leverages an advanced Pine Script algorithm to calculate the premium (or discount) percentage of GBTC compared to the spot price of Bitcoin (BTC/USD) on Coinbase. The premium is a critical insight that reflects market sentiment and potentially arbitrage opportunities between the trust's share price and the underlying cryptocurrency asset.

Here's how the indicator works:

1. **Calculation Methodology:**

- **Implied Bitcoin Price of GBTC:** We determine the implied price of Bitcoin within GBTC by dividing the GBTC closing price by the known ratio of Bitcoin per share.

- **GBTC Premium to Coinbase:** The percentage premium is then calculated as:

$$\text{GBTC Premium} = \frac{(\text{Implied Bitcoin Price of GBTC} - \text{Actual Bitcoin Price on Coinbase})}{\text{Actual Bitcoin Price on Coinbase}} \times 100$$

- This calculation is performed using the closing prices on a per-minute basis to ensure timely and accurate analysis.

2. **Visualization:** The indicator plots the premium as a step line chart, making it easy to visualize changes over time. A dynamic label accompanies the plot, displaying the implied Bitcoin price, the actual percentage premium or discount, and whether the premium is trending up or down compared to the previous day's value.

3. **Usage Scenario:** Traders can use this indicator to monitor the live premium 24/7 and analyze how it behaves during different market conditions, including when the equity market, where GBTC is traded, is closed.

#### Additional Features:

- **Color-Coding:** The premium is color-coded in green when positive (premium) and in red when negative (discount), aiding quick visual assessment.

- **Zero-Line Reference:** A horizontal line is drawn at zero to easily identify when GBTC is trading at par with the spot price of Bitcoin.

- **Real-Time Label Updates:** The label updates in real time with the latest premium/discount information and includes an arrow to signify the trend direction.

#### Access and Usage:

The indicator can be favorited or added to your TradingView charts. You are also welcome to use the source code as a foundation for further customization to suit your trading strategies.

#### Notes:

Please consider that the GBTC has specific trading hours, and the indicator can show live changes even when its market is closed, which might lead to discrepancies from official static data. For best performance, use this indicator alongside the GBTC candlestick chart on TradingView.

"电脑桌面显示BTC" için komut dosyalarını ara

Real Dominance//Due to incompliance with TV rules, I re-publish this indicator once again. Hope this time it's complaint.

Indicator shows dominance of main coin (BTC by default) after deduction of all stablecoins marketcaps and compares it to dominance that provides TradingView (BTC.D by default). The reason of writing this indicator is to deduct all stablecoins' caps from bitcoin dominance and show dominance without impact of other stablecoins. It means, that if crypto cap equals to, let's say 100, stablecoins' cap will be part of it (something between 10 and 20), but generally stablecoins are not crypto and it's caps are generally not limited, so we can't clearly see what is real dominance of BTC in compare with altcoins.

Notes:

1. dominance for timeframes lower than 1D could be calculated only on tariffs Pro+ or Premium (TV limitation)

2. you may change any and all tickers in indicator's setup menu

3. at the moment of publication (03.06.2023), TV doesn't offer market cap tickers for all stablecoins. Therefore in case it will be added in the future you may add it in the setup menu. There are placeholders for stablecoins that has market cap in amount of more than 5mil USD as of today.

Индикатор показывает доминацию главной монеты (по умолчанию BTC) за вычетом доли всех стейблкоинов в сравнении к доминации, которую показывает TradingView (по умолчанию BTC.D). Причиной написания данного индикатора является необходимость вычесть влияние стейблов на доминацию, так как важно смотреть доминацию именно в сравнении BTC/altcoins, и не учитывать стейблкойны, объем которых по большому счету не ограничен.

Особенности работы:

1. на тарифах кроме Pro+ и Premium, доминация может быть рассчитана только на дневном таймфрейме и выше (ограничения TradingView).

2. все тикеры, включая главную и сравниваемую монеты можно менять по желанию в настройках. Стиль линий настраивается на соответствующей вкладке в настройках.

3. к сожалению, на момент публикации индикатора (03.06.2023), TradingView предоставляет данные капитализации для ограниченного количества стейблкойнов. В настройки добавлены заглушки для последующего добавления других стейблкойнов. В список внесены монеты, капитализация которых на момент публикации индикатора составляла более 5 млн долларов.

Active AddressesIndicator Overview

By comparing the 28 day change in price (%) with the 28 day change in active addresses (%) for Bitcoin we are able to create a short-term sentiment indicator called AASI (Active Address Sentiment Indicator).

Grey lines on the chart show the change in active addresses.

On the outer boundaries of those grey lines are standard deviation bands.

Dotted red line = upper boundary

Dotted green line = lower boundary

Orange line is the 28 day price change (%).

When the orange line reaches the upper boundary (red dotted line) it is indicating that short term market sentiment is overheated. Because the rate of increase in price is outstripping the rate of increase in active addresses.

Zooming in on the chart (left click and drag) we can see that this often corresponds with CRYPTOCAP:BTC price (blue line) stalling and/or retracing.

The opposite is true when the 28 day price change hits the lower boundary (green dotted line). Here market sentiment is overly bearish and we often see CRYPTOCAP:BTC price then increasing thereafter.

In extreme market conditions the 28 day price change (orange line) aggressively breaks out beyond the dotted red and green bands. This is typically in a major market crash or in the latter stages of a bull market. I may add additional standard deviation bands to catch these moves but for now have left them off to keep the chart clean.

Pre 2015 data is quite volatile and messy so this charts starts at 01 January 2015.

Bitcoin Price Prediction Using This Tool

Unlike many of the other Bitcoin live charts, this live chart examines lower time frames and attempts to provide a Bitcoin price prediction in terms of directional moves on weekly timeframes. So it tries to do a Bitcoin price forecast by highlighting where price may pullback or where it may bounce using price and active address data.

KINSKI USDT Market Cap DominanceUSDT dominance charts are rare to find as almost everyone is fixated on BTC dominance. Bitcoin dominance gives us insight into investors' preferences when they have a choice between BTC and thousands of altcoins.

This oscillator gives insight into the state of the coin market. When people exchange their digital currencies like BTC and Altcoins for USDT, there is low confidence in the market. The opposite is true when BTC and Altcoins are bought because market sentiment is high.

So when USDT dominance rises, cryptocurrency prices fall, but when their dominance falls, cryptocurrency prices rise.

Features

Can be displayed as a moving average (default) or histogram.

Choice between 'CRYPTOCAP:USDT', 'CRYPTOCAP:USDT.D', 'CRYPTOCAP:OTHERS.D' => CRYPTOCAP:USDT.D is default.

Smoothing types Selectable

Upward and downward trend of MA line can be activated

Extensive style settings

60-Day Accumulated Increasing RateIs this Bitcoin bull run still driven by new investors and new funds? Definitely. That’s why the 60-day accumulative increasing rate is so important and it can even determine everything. The only thing that can be trusted is the math. In history, each capital inflow uptrend bull run has ended once the 60-day accumulative increasing rate reached a high level and when the short-term euphoric investors push BTC price to rise at a fast speed and use up all kinds of leverages. At that point, there’s no time for new investors and new funds to flow in, thus the cryptocurrency market will crash from the global top.

In that sense, the crashes on 4th September, 2017 and 19th May, 2021 didn’t end the bull run, instead,they lengthened the bull run span.The last bull run cycle (2017) might have ended prematurely when BTC reached $10,000, recording 150% accumulated increase over 60 days. Then BTC won’t be pumped up to $20,000 if the course wasn’t interrupted by September 4th, 2017 incident.

Technical analysts(they are far from trustworthy, full of bollocks) call the correction of BTC: “consolidation or wipeout”, just like that diabetes is called as Liver Qi Stagnation, weight lossing, being thirsty and other symptoms. It’s quite fun to watch so many people explaining it in a false concept. Everyone knows what the maths is. That’s enough.

PS: This indicator can only be applied to Bitcoin daily chart!

Compare (RSI) Ticker 3x by fikiraHi!

Here I've created an indicator which compares 1 Ticker with 1 or 2 other Tickers.

The basis is RSI (Source & Length is adjustable), but the main objective is NOT to concentrate on the RSI, but on the comparison between the 2 or 3 Tickers.

I've used RSI because in this way high priced Tickers (for example BTC, now $8500) can easily be compared with low priced Tickers (for example BTT, now $0,00042)

In this example I have NEO/USDT (Binance) as my initial Ticker, you can see the candlesticks of NEO/USDT.

In the "Compare" indicator, the 'close' of NEO appears as a white line.

The second line (blue) is a chosen second Ticker, in this case BTC/USDT (Binance)

In "Settings" > "Inputs" you can enable/disable the second or third Ticker

- The second Ticker has multiple choices

- The third you can type any Ticker you want, for example CRYPTOCAP:BNB, BINANCE:ETHUSDT, NASDAQ_DLY:NDX or whatever,

just start typing and you'll see the possibilities (You also can choose between "Cryptocurrencies", "Index", "Forex", ...)

You can also plot 2 EMA's, a Short and a Long period (Length is adjustable).

The EMA's have the same colour as the Tickers (Ticker 1 = white, 2 = blue, 3 = red, of course all adjustable)

- EMA Ticker 1 crossover Ticker 2/3 > Green cloud

- EMA Ticker 1 crossunder Ticker 2/3 > Red cloud

For example:

NEO/USDT (1, white) & BTC/USDT (2, blue) with Long Period EMA

NEO/USDT (1, white) & BNB/USDT (3, red) with Long Period EMA

NEO/USDT (1, white) & BNB/USDT (3, red) with Short Period EMA

When the second chosen Ticker is the same as the first Ticker, of course you will be seeing lines

(because there is no difference between the 2 Tickers, the EMA is visible though)

Example :

Both BTC/USDT

(The second indicator is my "Compare (RSI) MACD", a MACD of this indicator, which in this case is obviously flat)

GBTCGBTC created BTC's leading indicator theory.

Is it difficult to understand with the GBTC / BTC MACD created earlier? That's why I tried simply overlapping.

Since it is forcibly matched with the multiple option, it seems that fine adjustment is always necessary.

GBTCはBTCの先行指標説を信じて作成しました。

先に作成したGBTC/BTC MACDではいまいちわかりにくい?というわけで単純に重ね合わせてみました。

multipleオプションで強引に合わせているので、常に微調整は必要と思われます

Ichimoku + VWAP + OBV + ATR Full System (NQ Daytrade)This script provides optimized scalping signals for BTC, designed mainly for the 15-minute timeframe.

Long/short entries are generated using VWAP band position and trend confirmation logic.

OBV momentum is used as a secondary filter to validate breakout or reversal conditions.

Exit signals are displayed when volatility compression or mean-reversion conditions occur.

Simple visual markers (triangles and circles) are included for easy decision-making.

롱/숏 삼각형 시그널

동그라미 청산 시그널

VWAP 밴드 기반 방향성

OBV 보조지표

이름 (Name)

BTC Scalping Signal – VWAP + OBV

짧은 설명 (Short Description)

VWAP 밴드와 OBV를 기반으로 방향성, 진입·청산 시그널을 제공하는 스캘핑 지표입니다.

긴 설명 (Long Description)

이 지표는 BTC 단기 스캘핑을 위해 설계된 것으로, 특히 15분봉 환경에 최적화되어 있습니다.

VWAP 밴드의 위치와 추세 판별 로직을 기반으로 롱·숏 진입 신호를 제공합니다.

OBV 모멘텀을 보조 필터로 사용하여 돌파 및 되돌림 가능성을 판단합니다.

시장 변동성이 축소되거나 평균회귀 신호가 감지될 때 청산 시그널을 표시합니다.

삼각형(진입), 원형(청산) 등 직관적 시각 요소를 통해 빠른 의사결정을 지원합니다.

Single AHR DCA (HM) — AHR Pane (customized quantile)Customized note

The log-regression window LR length controls how long a long-term fair value path is estimated from historical data.

The AHR window AHR window length controls over which historical regime you measure whether the coin is “cheap / expensive”.

When you choose a log-regression window of length L (years) and an AHR window of length A (years), you can intuitively read the indicator as:

“Within the last A years of this regime, relative to the long-term trend estimated over the same A years, the current price is cheap / neutral / expensive.”

Guidelines:

In general, set the AHR window equal to or slightly longer than the LR window:

If the AHR window is much longer than LR, you mix different baselines (different LR regimes) into one distribution.

If the AHR window is much shorter than LR, quantiles mostly reflect a very local slice of history.

For BTC / ETH and other BTC-like assets, you can use relatively long horizons (e.g. LR ≈ 3–5 years, AHR window ≈ 3–8 years).

For major altcoins (BNB / SOL / XRP and similar high-beta assets), it is recommended to use equal or slightly shorter horizons, e.g. LR ≈ 2–3 years, AHR window ≈ 2–3 years.

1. Price series & windows

Working timeframe: daily (1D).

Let the daily close of the current symbol on day t be P_t .

Main length parameters:

HM window: L_HM = maLen (default 200 days)

Log-regression window: L_LR = lrLen (default 1095 days ≈ 3 years)

AHR window (regime window): W = windowLen (default 1095 days ≈ 3 years)

2. Harmonic moving average (HM)

On a window of length L_HM, define the harmonic mean:

HM_t = ^(-1)

Here eps = 1e-10 is used to avoid division by zero.

Intuition: HM is more sensitive to low prices – an extremely low price inside the window will drag HM down significantly.

3. Log-regression baseline (LR)

On a window of length L_LR, perform a linear regression on log price:

Over the last L_LR bars, build the series

x_k = log( max(P_k, eps) ), for k = t-L_LR+1 ... t, and fit

x_k ≈ a + b * k.

The fitted value at the current index t is

log_P_hat_t = a + b * t.

Exponentiate to get the log-regression baseline:

LR_t = exp( log_P_hat_t ).

Interpretation: LR_t is the long-term trend / fair value path of the current regime over the past L_LR days.

4. HM-based AHR (valuation ratio)

At each time t, build an HM-based AHR (valuation multiple):

AHR_t = ( P_t / HM_t ) * ( P_t / LR_t )

Interpretation:

P_t / HM_t : deviation of price from the mid-term HM (e.g. 200-day harmonic mean).

P_t / LR_t : deviation of price from the long-term log-regression trend.

Multiplying them means:

if price is above both HM and LR, “expensiveness” is amplified;

if price is below both, “cheapness” is amplified.

Typical reading:

AHR_t < 1 : price is below both mid-term mean and long-term trend → statistically cheaper.

AHR_t > 1 : price is above both mid-term mean and long-term trend → statistically more expensive.

5. Empirical quantile thresholds (Opp / Risk)

On each new day, whenever AHR_t is valid, add it into a rolling array:

A_t_window = { AHR_{t-W+1}, ..., AHR_t } (at most W = windowLen elements)

On this empirical distribution, define two quantiles:

Opportunity quantile: q_opp (default 15%)

Risk quantile: q_risk (default 65%)

Using standard percentile computation (order statistics + linear interpolation), we get:

Opp threshold:

theta_opp = Percentile( A_t_window, q_opp )

Risk threshold:

theta_risk = Percentile( A_t_window, q_risk )

We also compute the percentile rank of the current AHR inside the same history:

q_now = PercentileRank( A_t_window, AHR_t ) ∈

This yields three valuation zones:

Opportunity zone: AHR_t <= theta_opp

(corresponds to roughly the cheapest ~q_opp% of historical states in the last W days.)

Neutral zone: theta_opp < AHR_t < theta_risk

Risk zone: AHR_t >= theta_risk

(corresponds to roughly the most expensive ~(100 - q_risk)% of historical states in the last W days.)

All quantiles are purely empirical and symbol-specific: they are computed only from the current asset’s own history, without reusing BTC thresholds or assuming cross-asset similarity.

6. DCA simulation (lightweight, rolling window)

Given:

a daily budget B (input: budgetPerDay), and

a DCA simulation window H (input: dcaWindowLen, default 900 days ≈ 2.5 years),

The script applies the following rule on each new day t:

If thresholds are unavailable or AHR_t > theta_risk

→ classify as Risk zone → buy = 0

If AHR_t <= theta_opp

→ classify as Opportunity zone → buy = 2B (double size)

Otherwise (Neutral zone)

→ buy = B (normal DCA)

Daily invested cash:

C_t ∈ {0, B, 2B}

Daily bought quantity:

DeltaQ_t = C_t / P_t

The script keeps rolling sums over the last H days:

Cumulative position:

Q_H = sum_{k=t-H+1..t} DeltaQ_k

Cumulative invested cash:

C_H = sum_{k=t-H+1..t} C_k

Current portfolio value:

PortVal_t = Q_H * P_t

Cumulative P&L:

PnL_t = PortVal_t - C_H

Active days:

number of days in the last H with C_k > 0.

These results are only used to visualize how this AHR-quantile-driven DCA rule would have behaved over the recent regime, and do not constitute financial advice.

Bitcoin Lagging (N Days)This indicator overlays Bitcoin’s price on any chart with a user-defined N-day lag. You can select the BTC symbol and timeframe (daily recommended), choose which price source to use (open, high, low, close, hlc3, ohlc4), and shift the series by a chosen number of days. An option to normalize the series to 100 at the first visible value is also available, along with the ability to display the original BTC line for comparison.

It is designed for traders and researchers who want to test lagging relationships between Bitcoin and other assets, observe correlation changes, or visualize how BTC’s past prices might align with current market movements. The lagging is calculated based on daily candles, so even if applied on intraday charts, the shift remains in daily units.

이 지표는 비트코인 가격을 원하는 차트 위에 N일 지연된 상태로 표시해 줍니다. 심볼과 타임프레임(일봉 권장)을 선택할 수 있으며, 가격 소스(시가, 고가, 저가, 종가, hlc3, ohlc4)도 설정 가능합니다. 또한 시리즈를 첫 값 기준으로 100에 맞춰 정규화하거나, 원래의 비트코인 가격선을 함께 표시할 수도 있습니다.

비트코인과 다른 자산 간의 시차 효과를 분석하거나 상관관계 변화를 관찰할 때 유용하게 활용할 수 있습니다. 지연은 일봉 기준으로 계산되므로, 분·시간 차트에 적용해도 항상 일 단위로 반영됩니다.

Crypto Market Dominance Stacked with LabelsA professional stacked area chart showing the dominance of major crypto market segments: BTC, ETH, Top 100 Altcoins, and #101+ Altcoins. Each layer is color-coded for clarity and includes dynamic labels with the current dominance percentage. Provides a clear visual representation of market share trends for traders, analysts, and crypto enthusiasts.

Features:

Stacked visualization of BTC, ETH, Top 100, and small-cap altcoins (#101+).

Color-coded areas for easy identification.

Dynamic labels showing each category’s current dominance percentage.

Horizontal reference lines for percentage levels.

Approximates top 100 and #101+ altcoins using TOTAL2 and TOTAL3 market cap tickers.

Use Case:

Track how market share shifts between BTC, ETH, large altcoins, and smaller altcoins over time. Ideal for analyzing trends, spotting dominance changes, and visualizing overall crypto market structure.

Market Cap Landscape 3DHello, traders and creators! 👋

Market Cap Landscape 3D. This project is more than just a typical technical analysis tool; it's an exploration into what's possible when code meets artistry on the financial charts. It's a demonstration of how we can transcend flat, two-dimensional lines and step into a vibrant, three-dimensional world of data.

This project continues a journey that began with a previous 3D experiment, the T-Virus Sentiment, which you can explore here:

The Market Cap Landscape 3D builds on that foundation, visualizing market data—particularly crypto market caps—as a dynamic 3D mountain range. The entire landscape is procedurally generated and rendered in real-time using the powerful drawing capabilities of polyline.new() and line.new() , pushed to their creative limits.

This work is intended as a guide and a design example for all developers, born from the spirit of learning and a deep love for understanding the Pine Script™ language.

---

🧐 Core Concept: How It Works

The indicator synthesizes multiple layers of information into a single, cohesive 3D scene:

The Surface: The mountain range itself is a procedurally generated 3D mesh. Its peaks and valleys create a rich, textured landscape that serves as the canvas for our data.

Crypto Data Integration: The core feature is its ability to fetch market cap data for a list of cryptocurrencies you provide. It then sorts them in descending order and strategically places them onto the 3D surface.

The Summit: The highest point on the mountain is reserved for the asset with the #1 market cap in your list, visually represented by a flag and a custom emblem.

The Mountain Labels: The other assets are distributed across the mountainside, with their rank determining their general elevation. This creates an intuitive visual hierarchy.

The Leaderboard Pole: For clarity, a dedicated pole in the back-right corner provides a clean, ranked list of the symbols and their market caps, ensuring the data is always easy to read.

---

🧐 Example of adjusting the view

To evoke the feeling of flying over mountains

To evoke the feeling of looking at a mountain peak on a low plain

🧐 Example of predefined colors

---

🚀 How to Use

Getting started with the Market Cap Landscape 3D:

Add to Chart: Apply the "Market Cap Landscape 3D" indicator to your active chart.

Open Settings: Double-click anywhere on the 3D landscape or click the "Settings" icon next to the indicator's name.

Customize Your Crypto List: The most important setting is in the Crypto Data tab. In the "Symbols" text area, enter a comma-separated list of the crypto tickers you want to visualize (e.g., BTC,ETH,SOL,XRP ). The indicator supports up to 40 unique symbols.

> Important Note: This indicator exclusively uses TradingView's `CRYPTOCAP` data source. To find valid symbols, use the main symbol search bar on your chart. Type `CRYPTOCAP:` (including the colon) and you will see a list of available options. For example, typing `CRYPTOCAP:BTC` will confirm that `BTC` is a valid ticker for the indicator's settings. Using symbols that do not exist in the `CRYPTOCAP` index will result in a script error. or, to display other symbols, simply type CRYPTOCAP: (including the colon) and you will see a list of available options.

Adjust Your View: Use the settings in the Camera & Projection tab to rotate ( Yaw ), tilt ( Pitch ), and scale the landscape until you find a view you love.

Explore & Customize: Play with the color palettes, flag design, and other settings to make the landscape truly your own!

---

⚙️ Settings & Customization

This indicator is highly customizable. Here’s a breakdown of what each setting does:

#### 🪙 Crypto Data

Symbols: Enter the crypto tickers you want to track, separated by commas. The script automatically handles duplicates and case-insensitivity.

Show Market Cap on Mountain: When checked, it displays the full market cap value next to the symbol on the mountain. When unchecked, it shows a cleaner look with just the symbol and a colored circle background.

#### 📷 Camera & Projection

Yaw (°): Rotates the camera view horizontally (side to side).

Pitch (°): Tilts the camera view vertically (up and down).

Scale X, Y, Z: Stretches or compresses the landscape in width, depth, and height, respectively. Fine-tune these to get the perfect perspective.

#### 🏞️ Grid / Surface

Grid X/Y resolution: Controls the detail level of the 3D mesh. Higher values create a smoother surface but may use more resources.

Fill surface strips: Toggles the beautiful color gradient on the surface.

Show wireframe lines: Toggles the visibility of the grid lines.

Show nodes (markers): Toggles the small dots at each grid intersection point.

#### 🏔️ Peaks / Mountains

Fill peaks volume: Draws vertical lines on high peaks, giving them a sense of volume.

Fill peaks surface: Draws a cross-hatch pattern on the surface of high peaks.

Peak height threshold: Defines the minimum height for a peak to receive the fill effect.

Peak fill color/density: Customizes the appearance of the fill lines.

#### 🚩 Flags (3D)

Show Flag on Summit: A master switch to show or hide the flag and emblem entirely.

Flag height, width, etc.: Provides full control over the dimensions and orientation of the flag on the highest peak.

#### 🎨 Color Palette

Base Gradient Palette: Choose from 13 stunning, pre-designed color themes for the landscape, from the classic SUNSET_WAVE to vibrant themes like NEON_DREAM and OCEANIC .

#### 🛡️ Emblem / Badge Controls

This section gives you granular control over every element of the custom emblem on the flag. Tweak rotation, offsets, and scale to design your unique logo.

---

👨💻 Developer's Corner: Modifying the Core Logic

If you're a developer and wish to customize the indicator's core data source, this section is for you. The script is designed to be modular, making it easy to change what data is being ranked and visualized.

The heart of the data retrieval and ranking logic is within the f_getSortedCryptoData() function. Here’s how you can modify it:

1. Changing the Data Source (from Market Cap to something else):

The current logic uses request.security("CRYPTOCAP:" + syms.get(i), ...) to fetch market capitalization data. To change this, you need to modify this line.

Example: Ranking by RSI (14) on the Daily timeframe.

First, you'll need a function to calculate RSI. Add this function to the script:

f_getRSI(symbol, timeframe, length) =>

request.security(symbol, timeframe, ta.rsi(close, length))

Then, inside f_getSortedCryptoData() , find the `for` loop that populates the `caps` array and replace the `request.security` call:

// OLD LINE:

// caps.set(i, request.security("CRYPTOCAP:" + syms.get(i), timeframe.period, close))

// NEW LINE for RSI:

// Note: You'll need to decide how to format the symbol name (e.g., "BINANCE:" + syms.get(i) + "USDT")

caps.set(i, f_getRSI("BINANCE:" + syms.get(i) + "USDT", "D", 14))

2. Changing the Data Formatting:

The ranking values are formatted for display using the f_fmtCap() function, which currently formats large numbers into "M" (millions), "B" (billions), etc.

If you change the data source to something like RSI, you'll want to change the formatting. You can modify f_fmtCap() or create a new formatting function.

Example: Formatting for RSI.

// Modify f_fmtCap or create f_fmtRSI

f_fmtRSI(float v) =>

str.tostring(v, "#.##") // Simply format to two decimal places

Remember to update the calls to this function in the main drawing loop where the labels are created (e.g., str.format("{0}: {1}", crypto.symbol, f_fmtCap(crypto.cap)) ).

By modifying these key functions ( f_getSortedCryptoData and f_fmtCap ), you can adapt the Market Cap Landscape 3D to visualize and rank almost any dataset you can imagine, from technical indicators to fundamental data.

---

We hope you enjoy using the Market Cap Landscape 3D as much as we enjoyed creating it. Happy charting! ✨

Alt Season vs USDT Flow DashboardWhat the script tells you (the signals)

It builds four “alt vs stables” lenses and colors the background when they agree.

ALT ex-ETH / STABLES (TOTAL3 / (USDT+USDC+DAI))

Think: “How much alt cap per $1 of dry-powder stables?”

Bullish when price is above its 200-day SMA and rising → risk appetite expanding toward smaller alts.

ALT Share of Risk-On ((TOTAL − STABLES − BTC − ETH) / (TOTAL − STABLES))

Of the non-stable crypto pie, how much is flowing to ex-BTC/ETH alts?

Uptrend = broadening alt participation (late-early to mid alt-season behavior).

Dominance Spread ((TOTAL3 / TOTAL) − (STABLES / TOTAL))

Alts’ share minus stables’ share.

Widening spread means stables are being converted into alts (not just into BTC).

Flow Ratio ROC(TOTAL3, N) / ROC(STABLES, N) (default N=30 days)

Compares alts’ growth rate to stable supply growth.

> 1 and sustained → alts expanding faster than new “dry powder” is appearing.

The background color (“regime”)

Green (ALT-on) when all three conditions align:

ALT/Stable > its SMA

Dominance Spread > its SMA

Flow Ratio > 1

Red (ALT-off) when the opposite holds.

No color = mixed/chop.

How to read it (quick playbook)

Early alt-season tell:

BTC.D starts to slip, total market cap (TOTAL) rising.

ALT/Stable breaks above its 200-SMA and stays there.

Dominance Spread climbs (alts gaining share, stables losing share).

Flow Ratio > 1 for a few weeks.

Maturing phase: ALT Share of Risk-On rises (money broadens from ETH/L1s → mid/small caps).

Exhaustion/false start: Flow Ratio dips < 1 or ALT/Stable loses the 200-SMA while BTC.D stabilizes or rises.

Practical tips

Timeframes: Make calls on 1D. Use 1W to avoid whipsaw; use 4H only for entries once the 1D regime is green.

Smoothing: If you see noisy spikes from market-cap revisions, add a light smoother (e.g., 7D SMA on the plotted lines).

Parameters:

Try ROC length 21–45 days.

Try SMA 150–250 days (200 is a good middle).

Confluence: Keep BTC.D and ETH.D in another pane. Best alt windows: BTC.D trending down, ETH.D flat-to-up initially, then ETH.D flattens as TOTAL3 momentum spreads to mid/small caps.

Risk checks: If USDT.D/USDC.D (stable dominance) spike up while your signals are green, that’s a caution flag (capital retreating to stables).

FUMO 200 MagnetWhat it does

FUMO Magnet measures how far price has stretched away from its long-term “magnet” — a blended EMA/SMA moving average (200 by default).

It plots a logarithmic deviation (optionally normalized) as an oscillator around zero.

Above 0** → price is above the magnet (stretched up)

Below 0** → price is below the magnet (stretched down)

Guide levels** highlight potential overbought/oversold zones

---

Why log deviation?

Log returns make extremes comparable across cycles and compress exponential trends — especially useful for BTC and other crypto assets.

Normalization modes further adjust the scale, keeping the oscillator readable on any chart.

---

Inputs

**Base**

* Source (default: Close)

* Base Length (default: 200 EMA/SMA)

* EMA vs SMA weight (%) — 0% = pure SMA, 100% = pure EMA, 50% = blended

* EMA smoothing of deviation — acts as a noise filter

**Normalization**

* None (Log Deviation) — raw log stretch in % terms

* Z-score — deviation in standard deviations (σ)

* Robust Z (MAD) — deviation vs median absolute deviation, resistant to outliers

* Tanh squash — smooth nonlinear squash of extremes for compact scale

* Normalization window (for Z / MAD)

* Tanh scale (lower = stronger squash)

* Clamp after normalization — hard cap at ±X

**Levels**

* Guide levels (Upper / Lower) — visual thresholds (default ±12)

* Zero line toggle

---

### How to read it

* **Trend bias**: sustained time above 0 = uptrend, below 0 = downtrend

* **Stretch / mean reversion**: the farther from 0, the higher the reversion risk

* **Cross-checks**: combine with structure (HH/HL, LH/LL), volume, or momentum (RSI, MACD)

---

### Recommended settings by timeframe

**Long-term (1D / 1W)**

* Normalization: None (Log Deviation)

* Base Length: 200

* EMA vs SMA weight: 50% (adjust 35–65% for faster/slower magnet)

* Deviation smoothing: 20 (10–30 range)

* Guide levels: ±12 to ±20

* Use case: cycle extremes, portfolio rebalancing, trim/add logic

**Swing (4H – 1D)**

* Normalization: Z-score

* Window: 200 (100–250)

* Smoothing: 14–20

* Guide levels: ±2σ to ±3σ

* Use case: stretched conditions across regimes; ±3σ is rare, often mean-reverts

**Intraday / Active swing (1H – 4H)**

* Normalization: Robust Z (MAD)

* Window: 200 (150 for faster response)

* Smoothing: 10–16

* Guide levels: ±3 to ±4 (robust units)

* Use case: handles spikes better than σ, fewer false overbought/oversold signals

**Scalping / Universal readability (15m – 1H)**

* Normalization: Tanh squash

* Tanh scale: 6–10 (start with 8)

* Smoothing: 8–12

* Guide levels: ±8 to ±12

* Use case: compact panel across assets and timeframes; not % or σ, but visually consistent

---

### Optional

* Clamp: enable ±20 (or ±25) for strict bounded range (useful for public charts)

---

### Quick setups

**BTC Daily (“cycle view”)**

* Normalization: None

* Blend: 50%

* Smooth: 20

* Levels: ±12–15

**BTC 4H (“swing”)**

* Normalization: Z-score

* Window: 200

* Smooth: 16

* Levels: ±2.5σ to ±3σ

**Alts 1H (“volatile”)**

* Normalization: Robust Z (MAD)

* Window: 200

* Smooth: 12

* Levels: ±3.5 to ±4.5

**Mixed assets 15m (“compact panel”)**

* Normalization: Tanh squash

* Scale: 8

* Smooth: 10

* Levels: ±8–12

* Clamp: ±20

Supertrend EMA Vol Strategy V5### Supertrend EMA Strategy V5

**Overview**

This is a trend-following strategy designed for cryptocurrency markets like BTC/USD on daily timeframes, combining the Supertrend indicator for dynamic trailing stops with an EMA filter for trend confirmation. It aims to capture strong uptrends while avoiding counter-trend trades, with optional volume filtering for high-conviction entries and ATR-based stop-loss to manage risk. Ideal for long-only setups in bullish assets, it visually highlights trends with green/red bands and fills for easy interpretation. Backtested on BTC from 2024-2025, it shows potential for outperforming buy-and-hold in trending markets, but always use with proper risk management—past performance isn't indicative of future results.

**Key Features**

- **Supertrend Core**: Uses ATR to plot adaptive uptrend (green) and downtrend (red) lines, flipping on closes beyond prior bands for buy/sell signals.

- **EMA Trend Filter**: Entries require price above the EMA (default 21-period) for longs, ensuring alignment with the broader trend.

- **Volume Confirmation**: Optional filter only allows entries when volume exceeds its EMA (default 20-period), reducing false signals in low-activity periods.

- **Risk Controls**: Built-in ATR-multiplier stop-loss (default 2x) to cap losses; exits on Supertrend flips for trailing profits.

- **Visuals**: Green/red lines and highlighter fills for up/down trends, plus buy/sell labels and circles for signals.

- **Customizable Inputs**: Tweak ATR period (default 10), multiplier (default 3), EMA length, start date, long/short toggles, SL, and volume filter.

- **Alerts**: Built-in for buy/sell and direction changes.

**How to Use**

1. Add to your TradingView chart (e.g., BTC/USD 1D).

2. Adjust inputs: Start with defaults for trend-following; increase multiplier for fewer trades/higher win rate. Enable volume filter for volatile assets.

3. Monitor signals: Green "Buy" for long entries (if close > EMA and conditions met); red "Sell" for exits.

4. Backtest in Strategy Tester: Focus on equity curve, win rate (~50-60% in tests), and drawdown (<15% with SL).

5. Live Trading: Use small position sizes (1-2% risk per trade); combine with your analysis. Shorts disabled by default for bull-biased markets.

Sat Stacking Strategies Simulation (SSSS)Sat Stacking Strategies Simulation (SSSS)

This indicator simulates and compares different Bitcoin stacking strategies over time, allowing you to visualize performance, cost basis, and stacking behavior directly on your chart.

Core Features:

Three Stacking Strategies

• Trend-Based – Stack only when price is above/below a long-term SMA.

• Stack the Dip – Buy during sharp pullbacks or oversold conditions.

• Price Zone – Stack only in “cheap”, “fair”, or “expensive” zones based on a simulated Short-Term Holder (STH) cost basis.

Always Stack Benchmark

Compare your chosen strategy against a simple “Always Stack” approach for a real-world DCA reference.

Performance Metrics Table

Track:

• Total Fiat Added

• Total BTC Accumulated

• Current Value

• Average Cost per BTC

• PnL %

• CAGR

• Sharpe Ratio & Stdev

• Stack Events & Time Underwater

Advanced Options

• Simulate cash-secured puts on unused fiat.

• Simulate covered calls on BTC holdings.

• Roll over unused stacking amounts for future buys.

This tool is designed for Bitcoiners, stackers, and DCA enthusiasts who want to backtest and visualize their stacking plan—whether you keep it simple or go full quant.

Sometimes the best alpha is just showing up every week with your wallet open… and occasionally wearing a helmet. 🪖💰

🇰🇷 Kim'in Kim'out — Korean Premium TrackerKim’in Kim’out is a premium-tracking TradingView indicator that reveals Korean market sentiment by comparing real-time asset prices on Upbit (KRW) and Binance (USDT).

It detects when Korean traders are spot accumulating (Kim’in) or spot distributing (Kim’out) — enhanced by volume confirmation and trend context.

Perfect for crypto scalpers, swing traders, and arbitrage hunters.

⚙️ How It Works

Kimchi Premium: Measures how much more (or less) Koreans are paying on Upbit compared to Binance.

Volume Confirmation: Filters signals by comparing Upbit volume vs its moving average.

Signal Logic:

🔼 Kim’in: Premium exceeds the buy threshold + high volume

🔽 Kim’out: Premium drops below the sell threshold + high volume

Trend Context: Premium trend line gives insight into sustained interest/disinterest.

🎛️ Settings Overview

Input Description

Select Cryptocurrency Choose from supported coins (BTC, ETH, SOL, etc.)

Buy Threshold (%) How high the premium must be to trigger a Kim’in signal

Sell Threshold (%) How low the premium must be to trigger a Kim’out signal

Volume MA Period The number of candles for volume average

Volume Multiplier Volume spike ratio needed to confirm a signal

Show Info Table Toggle detailed premium stats in a side panel

Show Premium Zones Visual background zones (green/red/yellow)

Debug Mode Shows extra signals that trigger without volume confirmation

✅ How to Use It

Add the indicator to any chart (e.g. BTC/USDT)

Choose a coin from the dropdown (BTC, ETH, etc.)

Watch for:

Green Triangle Up (Kim’in) = Korean spot buy pressure confirmed

Red Triangle Down (Kim’out) = Korean selloff or disinterest

Use the Info Table (top-right) to see:

Premium %

Volume confirmation

Real-time KRW-USD exchange rate

Upbit vs Binance price comparison

Set Alerts:

Right-click on a signal → Add Alert on "Kim’in" or "Kim’out"

Or use the prebuilt alertconditions

🔔 Alert Messages

🇰🇷 Korean Premium BUY signal detected → Kim’in

🇰🇷 Korean Premium SELL signal detected → Kim’out

🧪 Best Practices

Use on 1H or 4H timeframe for best results

Confirm with broader market structure or confluence tools

Spot divergences between Binance and Upbit to predict regional flow shifts

🚫 Limitations

Works only with coins that have both Binance USDT & Upbit KRW pairs

Premium may be delayed by low liquidity or FX rate fluctuations (USDKRW)

Not suitable for lowcaps not listed on Upbit

Created by UKMC Crypto

The Great Anchors: Dual AVWAP Powered by RSI

The Great Anchors

*Dual Anchored Volume Weighted Average Price Powered by RSI*

---

📌 Overview

The Great Anchors is a dual AVWAP-based indicator that resets dynamically using RSI extremes — either from the current asset or a master symbol (e.g., BTCUSDT). It identifies meaningful shifts in price structure and momentum using these "anchored" levels.

It’s designed to help traders spot trend continuations, momentum inflection points, and entry signals aligned with overbought/oversold conditions — but only when the market confirms through volume-weighted price direction.

---

🛠 Core Logic

• AVWAP 1 (favwap): Anchored when RSI reaches overbought levels (top anchor)

• AVWAP 2 (savwap): Anchored when RSI reaches oversold levels (bottom anchor)

• AVWAPs are recalculated each time a new OB/OS condition is triggered — acting like "fresh anchors" at key market turning points.

---

⚙️ Key Features

🔁 Auto or Manual RSI Thresholds

→ Automatically determines dynamic RSI OB/OS levels based on past peaks and troughs, or lets you set fixed levels.

🧠 Master Symbol Control

→ Use the RSI of a separate asset (like BTCUSDT, ETHUSDT, SOLUSDT, BNBUSDT, SUPRAUSDT) or indices (like TOTAL, TOTAL2, BFR) to control resets — ideal for tracking how BTC/major coins impacts altcoins/others.

🔍 Trend-Filtering Signal Logic

→ Signals are filtered for less noise and are triggered when:

- Both AVWAPs are rising (bullish) or falling (bearish)

- Price action confirms the structure

🎯 Visual Markers & Alerts

→ "💥" for bullish signals and "🔥" for bearish ones. Alerts included for automation or push notifications.

---

🎯 How to Use It

1. Add the indicator to your chart.

2. Choose whether to use RSI from the current symbol or a master symbol (e.g., BTC).

3. Select auto-adjusted or manual OB/OS levels.

4. Watch for:

- AVWAP(s) making a significant change (at this point it's one of the AVWAPs resetting)

- Check if price flip it upwards or downwards

- If price goes above both AVWAPs thats a likely bullish trend

- If price can't go above both AVWAPs up and fall bellow both that's a likely bearish trend

- Price retesting upper AVWAP and bounce

- likely bullish continuation

- Price retesting lower AVWAP and dip

- likely bearish continuation

- Signal icons on chart ("💥 - Bullish" or "🔥- Bearish")

Best suited for:

• Swing traders

• Momentum traders

• Traders timing altcoin entries using BTC/Major asset's RSI

---

🔔 Signal Explanation

💥 Bullish Signal =

• Both AVWAPs rising

• Higher lows in price structure

• Bullish candle close

• Triggered from overbought RSI reset

🔥 Bearish Signal =

• Both AVWAPs falling

• Lower highs in price structure

• Bearish candle close

• Triggered from oversold RSI reset

Signals reset by opposite signals to prevent noise or overfitting.

---

⚠️ Tips & Notes

• Use AVWAPs as dynamic support/resistance, even without signal triggers

• Pair with volume or divergence tools for stronger confirmation

---

🧩 Credits & Philosophy

This tool is built with a simple philosophy:

"Anchor your trades to meaningful moments in price — not arbitrary time."

The dual AVWAP concept helps you see how price reacts after momentum peaks, giving you a cleaner bias and more precise trade setups.

---

4 diffs (CB & IBIT Premium)📊 Script Name: 4 diffs (CB & IBIT Premium)

Version: Pine Script® v6

Overlay: Yes (table displayed on chart)

🧠 What it Does:

This script tracks four important Bitcoin price differentials to monitor spot/perpetual/futures price inefficiencies and ETF premium/discounts, and displays them in a live table on the chart. It helps traders identify arbitrage opportunities or institutional pricing signals.

📈 Displayed Metrics:

Coinbase Premium

→ Difference between Coinbase spot and Binance spot prices.

→ Use case: US vs. offshore spot market divergence.

Coinbase Spot vs Binance Perpetual

→ Difference between Coinbase spot and Binance perpetual price.

→ Use case: Spot-perp basis, often used for funding rate insights or market stress.

Bybit vs Binance Perpetual

→ Difference between Bybit perp and Binance perp price.

→ Use case: Compare derivative pricing across major offshore exchanges.

IBIT Premium (CME vs ETF-implied)

→ Compares CME futures price vs. IBIT’s implied spot BTC value

→ IBIT implied BTC = IBIT ETF price ÷ (BTC held / shares outstanding)

→ Use case: Gauge institutional premium/discount and ETF arbitrage clues.

🛠️ Customization:

Text color of the table is adjustable via the input setting.

📌 Visual Output:

A fixed 2×4 table appears in the top-right corner of the chart.

Each row shows a label and the live price difference in USD.

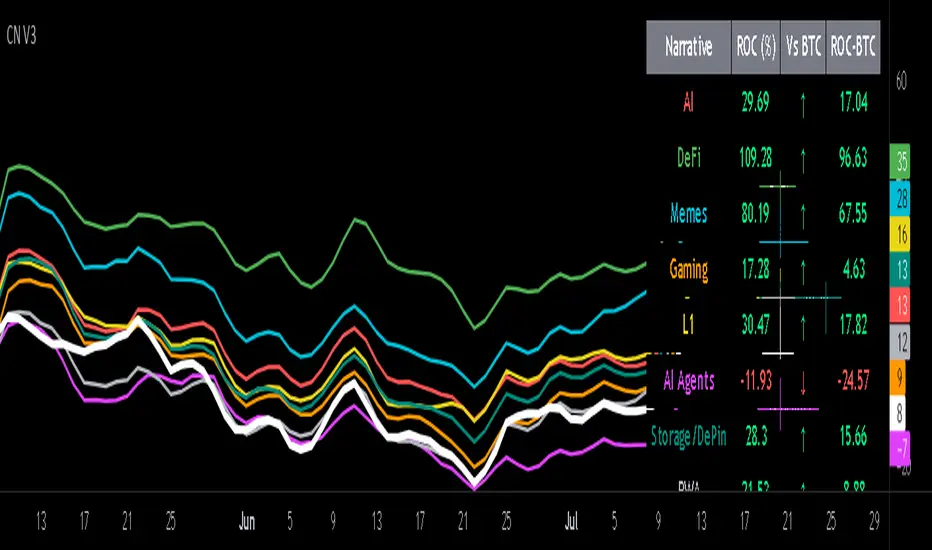

Crypto Narratives: Relative Strength V2Simple Indicator that displays the relative strength of 8 Key narratives against BTC as "Spaghetti" chart. The chart plots an aggregated RSI value for the 5 highest Market Cap cryopto's within each relevant narrative. The chart plots a 14 period SMA RSI for each narrative.

Functionality:

The indicator calculates the average RSI values for the current leading tokens associated with ten different crypto narratives:

- AI (Artificial Intelligence)

- DeFi (Decentralized Finance)

- Memes

- Gaming

- Level 1 (Layer 1 Protocols)

- AI Agents

- Storage/DePin

- RWA (Real-World Assets)

- BTC

Usage Notes:

The 5 crypto coins should be regularly checked and updated (in the script) by overtyping the current values from Rows 24 - 92 to ensure that you are using the up to date list of highest marketcap coins (or coins of your choosing).

The 14 period SMA can be changed in the indicator settings.

The indicator resets every 24 hours and is set to UTC+10. This can be changed by editing the script line 19 and changing the value of "resetHour = 1" to whatever value works for your timezone.

There is also a Rate of Change table that details the % rate of change of each narrative against BTC

Horizontal lines have been included to provide an indication of overbought and oversold levels.

The upper and lower horizontal line (overbought and oversold) can be adjusted through the settings.

The line width, and label offset can be customised through the input options.

Alerts can be set to triggered when a narrative's RSI crosses above the overbought level or below the oversold level. The alerts include the narrative name, RSI value, and the RSI level.

Supply In Profit Z-ScoreZ-score of BTC Supply in Profit.

Supply in Profit is an On-Chain BTC indicator that shows the percentage of BTC in profit.

In this indicator you can choose to use a Z-Score or not.

NUPL-Z For Loop🧠 Overview

NUPL-Z For Loop is a trend-following indicator built on Bitcoin’s on-chain Net Unrealized Profit/Loss (NUPL) metric. It uses a Z-scored transformation of NUPL and a custom loop-based scoring system to measure the consistency of directional movement. Rather than identifying tops and bottoms, this tool is designed to track sustained trends and filter out short-term noise, making it ideal for momentum-aligned strategies.

🧩 Key Features

Loop-Based Trend Logic: Assesses trend strength by summing the number of upward vs. downward moves in Z-scored NUPL across a custom lookback.

Z-Score Normalization: Applies long-term statistical normalization to NUPL to emphasize deviation from average behavior over time.

Threshold-Based Regime Shifts: Custom input thresholds define when trend strength is significant enough to trigger long or short signals.

Directional Market State Tracking: Internally tracks bullish, bearish, or neutral conditions to guide trend entries.

BTC-Focused On-Chain Analysis: Tailored specifically for Bitcoin using Market Cap and Realized Cap inputs.

🔍 How It Works

NUPL Calculation: Derived as the percentage of net unrealized profit relative to market cap: (MC - RMC) / MC * 100.

Z-Scoring: NUPL is normalized using a rolling mean and standard deviation over a long window (default 1300 days) to create a smoothed trend signal.

Directional Loop: A custom loop iterates from the start_loop to the end_loop, comparing the current Z-score to past values.

Each instance where NUPL_Z > NUPL_Z adds +1 to the score; otherwise, it subtracts -1.

This cumulative score reflects how consistently NUPL-Z has been trending.

Signal Logic:

Long signal when loop score exceeds long_threshold.

Short signal when score falls below short_threshold.

CD State Engine: Maintains the current trend regime (1 for long, -1 for short), which drives plot coloring and overlays.

🔁 Use Cases & Applications

Momentum Trend Filter: Detects and confirms sustained directional strength in BTC’s profit/loss positioning.

Noise Suppression: Avoids reactive signals from one-off spikes or dips in NUPL by requiring a consistent trend before confirming bias.

Best Suited for BTC: Designed specifically for Bitcoin’s price and on-chain structure, using its unique NUPL dynamics.

✅ Conclusion

NUPL-Z For Loop transforms a traditionally mean-reverting indicator into a trend-following signal engine. By scoring the consistency of movement in normalized NUPL, this tool identifies trend strength rather than reversal potential — providing more reliable context for momentum-aligned trades on Bitcoin.

⚠️ Disclaimer

The content provided by this indicator is for educational and informational purposes only. Nothing herein constitutes financial or investment advice. Trading and investing involve risk, including the potential loss of capital. Always backtest and apply risk management suited to your strategy.

Bitcoin Open Interest [SAKANE]Bitcoin Open Interest

— Unveiling the True Flow of Capital

PurposeVisualize and compare Bitcoin open interest (OI) from CME and Binance, the leading derivatives exchanges, in a single intuitive chart, providing traders with clear insights into crypto market capital dynamics.

Background & MotivationIn the 24/7 crypto market, price movements alone reveal only part of the story. Open interest (OI)—the total outstanding futures contracts—offers critical clues to the market’s next move. Yet, accessing and interpreting OI data is challenging:

CME Constraints: Commitment of Traders (COT) reports are weekly, and standalone BTC1! or BTC2! OI is noisy due to contract rollovers, obscuring true OI changes.

Existing Tool Limitations: Most OI indicators are fixed to either USD or BTC, limiting flexible analysis.

This indicator overcomes these hurdles, enabling seamless comparison of CME and Binance OI to track the market’s “capital center of gravity” in real time.

Key Features

Synthetic CME OI: Combines BTC1! and BTC2! to deliver high-accuracy OI, eliminating rollover noise.

Multi-Timeframe Analysis: Displays daily CME OI as pseudo-candlestick (OHLC) on any timeframe (e.g., 4H), allowing intuitive capital flow tracking across timeframes.

CME/Binance One-Click Toggle: Instantly compare institutional-driven CME and retail-driven Binance OI.

USD/BTC Flexibility: Switch between BTC (real demand) and USD (margin) perspectives for OI analysis.

Robust Design: Concise, global-scope code ensures stability and adaptability to TradingView updates.

Insights & Use Cases

Holistic Market Sentiment: Analyze capital flows by region and exchange for a multidimensional view.

Signal Detection: E.g., a sharp drop in CME OI during a sell-off may signal institutional withdrawal.

Retail Trends: A surge in Binance OI suggests retail-driven inflows.

Event-Driven Insights: E.g., during a hypothetical April 2025 “Trump Tariff Shock,” instantly identify which exchange drives capital shifts.

Unique ValueUnlike price-centric indicators, this tool focuses on capital flow (OI). It’s the only indicator offering one-click multi-timeframe and multi-exchange OI comparison, empowering traders to uncover the market’s “true intent” and gain a strategic edge.

ConclusionBitcoin Open Interest makes the market’s hidden capital movements accessible to all. By capturing market dynamics and pinpointing the “leading forces” during events, it sets a new standard for traders seeking a revolutionary perspective.