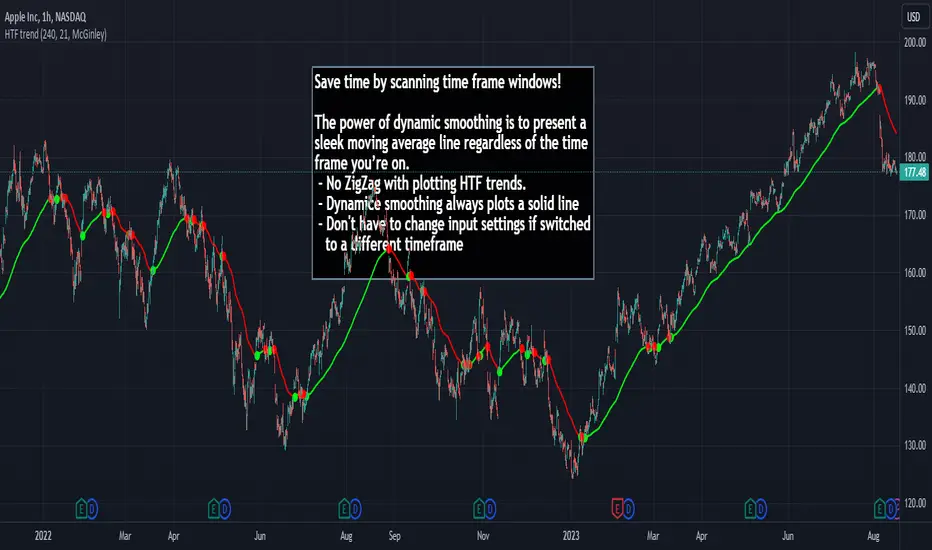

HTF Trend Filter - Dynamic SmoothingSummary of the HTF Trend Filter

The Higher Time Frame (HTF) Trend Filter is a cutting-edge tool crafted for traders who want to scan moving average trend lines time efficiently. At its core, it harnesses the power of dynamic smoothing to present a sleek moving average line regardless of the time frame you’re on. Here's a glimpse of the advantages you unlock with the HTF trend filter:

Dynamic Smoother: Ever been irked by jagged lines on your chart? With the dynamic smoother, those days are gone. The smoother streamlines HTF moving average line on your current lower time frame chart.

Time Efficiency: Time is of the essence in trading. With this tool, you can nimbly toggle between time charts without the hassle of readjusting input parameters, ensuring your screening process remains unhindered.

Features of the Script

Variety of Moving Averages: The script caters to different trading styles by offering a plethora of moving average types, ranging from the classic SMA and EMA to the innovative Hull and McGinley Dynamic MAs.

Dynamic Smoothing: This is the script's pièce de résistance. The dynamic smoothing factor is ingeniously derived by taking the ratio of minutes of the higher time frame to the current time frame. This ensures the moving average remains fluid and consistent across different time frames, eliminating the common pitfalls of jagged moving averages.

Reversal Indicators: It includes a reversal indicator. Green circles pinpoint the start of a potential uptrend, while red ones signify a potential downtrend.

Customizable Alerts: To ensure you never miss a beat, the script is equipped with customizable alert conditions.

Trading Idea

The essence of trading lies in confirming assumptions and validating trends. The HTF Trend Dynamic Smoother positions itself as a potential game-changer in this domain. One could consider using the HTF trend dynamic smoother as a supplementary confirmation tool alongside other primary indicators. For instance, if you're plotting a moving average on a lower time frame, toggling the HTF smoother can offer a broader perspective of the trend from a higher time frame. By ensuring alignment between these perspectives, you could potentially trade with increased confidence, reinforcing your lower time frame strategies with higher time frame confirmations. It's worth noting, however, that while this method can offer additional layers of information and validation, it doesn't replace due diligence. Every trade decision should be the culmination of thorough analysis, and no tool should be solely relied upon for decision-making.

Limitations

While the HTF Trend Filter is an exceptional tool, like all tools, it has its constraints. Lower Time Frame Dependency: For the indicator to function optimally, it's paramount to ensure that the time frame open is always lower (or equal) than the one selected in the input parameters. This limitation is crucial to remember as the dynamic smoother's accuracy hinges on this condition.

In conclusion, the HTF Trend Filter - Dynamic Smoothing is a remarkable blend of innovation and efficiency, tailored for traders who demand fast screening of higher time frame MA trends. Due to it simplistic design it gives a user-friendly experience. However, always remember the golden rule of trading: utilize tools as part of a comprehensive strategy, never in isolation.

Komut dosyalarını "欧易PI币开盘价格" için ara

Wave Generator (WG)Pine Script Wave Generator Utility

Introduction:

The Pine Script Wave Generator Utility is a versatile tool that creates different wave patterns. The script provides the user with four different wave styles to choose from (Sine, Triangle, Saw, Square) with customizable parameters for the wave height, duration, number of harmonics, and phase shift.

Technical Details:

The script utilizes the mathematical functions sin, pi, and array.avg to generate wave patterns. The wave height and duration are the main inputs, and the number of harmonics and phase shift are additional inputs that add fine-tuning to the wave pattern.

The wave styles are created using different combinations of sine waves and are normalized so that the resulting wave always lies within a range of -1 to 1.

Usage:

The user can adjust the wave parameters using the input options in the script. The user can choose the wave style from the “Wave Select” option and set the wave height, wave duration, number of harmonics and phase shift by adjusting the corresponding input options.

Conclusion:

The Pine Script Wave Generator Utility is an efficient and effective tool for generating wave patterns. It can be used for a variety of purposes such as creating wave patterns for technical analysis, simulation, and testing purposes. The user can easily adjust the wave parameters to create custom wave patterns, making it a flexible and valuable tool.

Fourier Extrapolator of 'Caterpillar' SSA of Price [Loxx]Fourier Extrapolator of 'Caterpillar' SSA of Price is a forecasting indicator that applies Singular Spectrum Analysis to input price and then injects that transformed value into the Quinn-Fernandes Fourier Transform algorithm to generate a price forecast. The indicator plots two curves: the green/red curve indicates modeled past values and the yellow/fuchsia dotted curve indicates the future extrapolated values.

What is the Fourier Transform Extrapolator of price?

Fourier Extrapolator of Price is a multi-harmonic (or multi-tone) trigonometric model of a price series xi, i=1..n, is given by:

xi = m + Sum( a*Cos(w*i) + b*Sin(w*i), h=1..H )

Where:

xi - past price at i-th bar, total n past prices;

m - bias;

a and b - scaling coefficients of harmonics;

w - frequency of a harmonic ;

h - harmonic number;

H - total number of fitted harmonics.

Fitting this model means finding m, a, b, and w that make the modeled values to be close to real values. Finding the harmonic frequencies w is the most difficult part of fitting a trigonometric model. In the case of a Fourier series, these frequencies are set at 2*pi*h/n. But, the Fourier series extrapolation means simply repeating the n past prices into the future.

Quinn-Fernandes algorithm find sthe harmonic frequencies. It fits harmonics of the trigonometric series one by one until the specified total number of harmonics H is reached. After fitting a new harmonic , the coded algorithm computes the residue between the updated model and the real values and fits a new harmonic to the residue.

see here: A Fast Efficient Technique for the Estimation of Frequency , B. G. Quinn and J. M. Fernandes, Biometrika, Vol. 78, No. 3 (Sep., 1991), pp . 489-497 (9 pages) Published By: Oxford University Press

Fourier Transform Extrapolator of Price inputs are as follows:

npast - number of past bars, to which trigonometric series is fitted;

nharm - total number of harmonics in model;

frqtol - tolerance of frequency calculations.

What is Singular Spectrum Analysis ( SSA )?

Singular spectrum analysis ( SSA ) is a technique of time series analysis and forecasting. It combines elements of classical time series analysis, multivariate statistics, multivariate geometry, dynamical systems and signal processing. SSA aims at decomposing the original series into a sum of a small number of interpretable components such as a slowly varying trend, oscillatory components and a ‘structureless’ noise. It is based on the singular value decomposition ( SVD ) of a specific matrix constructed upon the time series. Neither a parametric model nor stationarity-type conditions have to be assumed for the time series. This makes SSA a model-free method and hence enables SSA to have a very wide range of applicability.

For our purposes here, we are only concerned with the "Caterpillar" SSA . This methodology was developed in the former Soviet Union independently (the ‘iron curtain effect’) of the mainstream SSA . The main difference between the main-stream SSA and the "Caterpillar" SSA is not in the algorithmic details but rather in the assumptions and in the emphasis in the study of SSA properties. To apply the mainstream SSA , one often needs to assume some kind of stationarity of the time series and think in terms of the "signal plus noise" model (where the noise is often assumed to be ‘red’). In the "Caterpillar" SSA , the main methodological stress is on separability (of one component of the series from another one) and neither the assumption of stationarity nor the model in the form "signal plus noise" are required.

"Caterpillar" SSA

The basic "Caterpillar" SSA algorithm for analyzing one-dimensional time series consists of:

Transformation of the one-dimensional time series to the trajectory matrix by means of a delay procedure (this gives the name to the whole technique);

Singular Value Decomposition of the trajectory matrix;

Reconstruction of the original time series based on a number of selected eigenvectors.

This decomposition initializes forecasting procedures for both the original time series and its components. The method can be naturally extended to multidimensional time series and to image processing.

The method is a powerful and useful tool of time series analysis in meteorology, hydrology, geophysics, climatology and, according to our experience, in economics, biology, physics, medicine and other sciences; that is, where short and long, one-dimensional and multidimensional, stationary and non-stationary, almost deterministic and noisy time series are to be analyzed.

"Caterpillar" SSA inputs are as follows:

lag - How much lag to introduce into the SSA algorithm, the higher this number the slower the process and smoother the signal

ncomp - Number of Computations or cycles of of the SSA algorithm; the higher the slower

ssapernorm - SSA Period Normalization

numbars =- number of past bars, to which SSA is fitted

Included:

Bar coloring

Alerts

Signals

Loxx's Expanded Source Types

Related Fourier Transform Indicators

Real-Fast Fourier Transform of Price w/ Linear Regression

Fourier Extrapolator of Variety RSI w/ Bollinger Bands

Fourier Extrapolator of Price w/ Projection Forecast

Related Projection Forecast Indicators

Itakura-Saito Autoregressive Extrapolation of Price

Helme-Nikias Weighted Burg AR-SE Extra. of Price

Related SSA Indicators

End-pointed SSA of FDASMA

End-pointed SSA of Williams %R

STD-Filtered, N-Pole Gaussian Filter [Loxx]This is a Gaussian Filter with Standard Deviation Filtering that works for orders (poles) higher than the usual 4 poles that was originally available in Ehlers Gaussian Filter formulas. Because of that, it is a sort of generalized Gaussian filter that can calculate arbitrary (order) pole Gaussian Filter and which makes it a sort of a unique indicator. For this implementation, the practical mathematical maximum is 15 poles after which the precision of calculation is useless--the coefficients for levels above 15 poles are so high that the precision loss actually means very little. Despite this maximal precision utility, I've left the upper bound of poles open-ended so you can try poles of order 15 and above yourself. The default is set to 5 poles which is 1 pole greater than the normal maximum of 4 poles.

The purpose of the standard deviation filter is to filter out noise by and by default it will filter 1 standard deviation. Adjust this number and the filter selections (price, both, GMA, none) to reduce the signal noise.

What is Ehlers Gaussian filter?

This filter can be used for smoothing. It rejects high frequencies (fast movements) better than an EMA and has lower lag. published by John F. Ehlers in "Rocket Science For Traders".

A Gaussian filter is one whose transfer response is described by the familiar Gaussian bell-shaped curve. In the case of low-pass filters, only the upper half of the curve describes the filter. The use of gaussian filters is a move toward achieving the dual goal of reducing lag and reducing the lag of high-frequency components relative to the lag of lower-frequency components.

A gaussian filter with...

One Pole: f = alpha*g + (1-alpha)f

Two Poles: f = alpha*2g + 2(1-alpha)f - (1-alpha)2f

Three Poles: f = alpha*3g + 3(1-alpha)f - 3(1-alpha)2f + (1-alpha)3f

Four Poles: f = alpha*4g + 4(1-alpha)f - 6(1-alpha)2f + 4(1-alpha)3f - (1-alpha)4f

and so on...

For an equivalent number of poles the lag of a Gaussian is about half the lag of a Butterworth filters: Lag = N*P / pi^2, where,

N is the number of poles, and

P is the critical period

Special initialization of filter stages ensures proper working in scans with as few bars as possible.

From Ehlers Book: "The first objective of using smoothers is to eliminate or reduce the undesired high-frequency components in the eprice data. Therefore these smoothers are called low-pass filters, and they all work by some form of averaging. Butterworth low-pass filters can do this job, but nothing comes for free. A higher degree of filtering is necessarily accompanied by a larger amount of lag. We have come to see that is a fact of life."

References John F. Ehlers: "Rocket Science For Traders, Digital Signal Processing Applications", Chapter 15: "Infinite Impulse Response Filters"

Included

Loxx's Expanded Source Types

Signals

Alerts

Bar coloring

Related indicators

STD-Filtered, Gaussian Moving Average (GMA)

STD-Filtered, Gaussian-Kernel-Weighted Moving Average

One-Sided Gaussian Filter w/ Channels

Fisher Transform w/ Dynamic Zones

R-sqrd Adapt. Fisher Transform w/ D. Zones & Divs .

Fourier Extrapolation of Variety Moving Averages [Loxx]Fourier Extrapolation of Variety Moving Averages is a Fourier Extrapolation (forecasting) indicator that has for inputs 38 different types of moving averages along with 33 different types of sources for those moving averages. This is a forecasting indicator of the selected moving average of the selected price of the underlying ticker. This indicator will repaint, so past signals are only as valid as the current bar. This indicator allows for up to 1500 bars between past bars and future projection bars. If the indicator won't load on your chart. check the error message for details on how to fix that, but you must ensure that past bars + futures bars is equal to or less than 1500.

Fourier Extrapolation using the Quinn-Fernandes algorithm is one of several (5-10) methods of signals forecasting that I'l be demonstrating in Pine Script.

What is Fourier Extrapolation?

This indicator uses a multi-harmonic (or multi-tone) trigonometric model of a price series xi, i=1..n, is given by:

xi = m + Sum( a*Cos(w*i) + b*Sin(w*i), h=1..H )

Where:

xi - past price at i-th bar, total n past prices;

m - bias;

a and b - scaling coefficients of harmonics;

w - frequency of a harmonic ;

h - harmonic number;

H - total number of fitted harmonics.

Fitting this model means finding m, a, b, and w that make the modeled values to be close to real values. Finding the harmonic frequencies w is the most difficult part of fitting a trigonometric model. In the case of a Fourier series, these frequencies are set at 2*pi*h/n. But, the Fourier series extrapolation means simply repeating the n past prices into the future.

This indicator uses the Quinn-Fernandes algorithm to find the harmonic frequencies. It fits harmonics of the trigonometric series one by one until the specified total number of harmonics H is reached. After fitting a new harmonic , the coded algorithm computes the residue between the updated model and the real values and fits a new harmonic to the residue.

see here: A Fast Efficient Technique for the Estimation of Frequency , B. G. Quinn and J. M. Fernandes, Biometrika, Vol. 78, No. 3 (Sep., 1991), pp . 489-497 (9 pages) Published By: Oxford University Press

The indicator has the following input parameters:

src - input source

npast - number of past bars, to which trigonometric series is fitted;

Nfut - number of predicted future bars;

nharm - total number of harmonics in model;

frqtol - tolerance of frequency calculations.

Included:

Loxx's Expanded Source Types

Loxx's Moving Averages

Other indicators using this same method

Fourier Extrapolator of Variety RSI w/ Bollinger Bands

Fourier Extrapolator of Price w/ Projection Forecast

Fourier Extrapolator of Price

Loxx's Moving Averages: Detailed explanation of moving averages inside this indicator

Loxx's Expanded Source Types: Detailed explanation of source types used in this indicator

Fourier Extrapolator of Variety RSI w/ Bollinger Bands [Loxx]Fourier Extrapolator of Variety RSI w/ Bollinger Bands is an RSI indicator that shows the original RSI, the Fourier Extrapolation of RSI in the past, and then the projection of the Fourier Extrapolated RSI for the future. This indicator has 8 different types of RSI including a new type of RSI called T3 RSI. The purpose of this indicator is to demonstrate the Fourier Extrapolation method used to model past data and to predict future price movements. This indicator will repaint. If you wish to use this for trading, then make sure to take a screenshot of the indicator when you enter the trade to save your analysis. This is the first of a series of forecasting indicators that can be used in trading. Due to how this indicator draws on the screen, you must choose values of npast and nfut that are equal to or less than 200. this is due to restrictions by TradingView and Pine Script in only allowing 500 lines on the screen at a time. Enjoy!

What is Fourier Extrapolation?

This indicator uses a multi-harmonic (or multi-tone) trigonometric model of a price series xi, i=1..n, is given by:

xi = m + Sum( a*Cos(w*i) + b*Sin(w*i), h=1..H )

Where:

xi - past price at i-th bar, total n past prices;

m - bias;

a and b - scaling coefficients of harmonics;

w - frequency of a harmonic ;

h - harmonic number;

H - total number of fitted harmonics.

Fitting this model means finding m, a, b, and w that make the modeled values to be close to real values. Finding the harmonic frequencies w is the most difficult part of fitting a trigonometric model. In the case of a Fourier series, these frequencies are set at 2*pi*h/n. But, the Fourier series extrapolation means simply repeating the n past prices into the future.

This indicator uses the Quinn-Fernandes algorithm to find the harmonic frequencies. It fits harmonics of the trigonometric series one by one until the specified total number of harmonics H is reached. After fitting a new harmonic , the coded algorithm computes the residue between the updated model and the real values and fits a new harmonic to the residue.

see here: A Fast Efficient Technique for the Estimation of Frequency , B. G. Quinn and J. M. Fernandes, Biometrika, Vol. 78, No. 3 (Sep., 1991), pp . 489-497 (9 pages) Published By: Oxford University Press

The indicator has the following input parameters:

src - input source

npast - number of past bars, to which trigonometric series is fitted;

Nfut - number of predicted future bars;

nharm - total number of harmonics in model;

frqtol - tolerance of frequency calculations.

Included:

Loxx's Expanded Source Types

Loxx's Variety RSI

Other indicators using this same method

Fourier Extrapolator of Price w/ Projection Forecast

Fourier Extrapolator of Price

Fourier Extrapolator of Price w/ Projection Forecast [Loxx]Due to popular demand, I'm pusblishing Fourier Extrapolator of Price w/ Projection Forecast.. As stated in it's twin indicator, this one is also multi-harmonic (or multi-tone) trigonometric model of a price series xi, i=1..n, is given by:

xi = m + Sum( a*Cos(w*i) + b*Sin(w*i), h=1..H )

Where:

xi - past price at i-th bar, total n past prices;

m - bias;

a and b - scaling coefficients of harmonics;

w - frequency of a harmonic ;

h - harmonic number;

H - total number of fitted harmonics.

Fitting this model means finding m, a, b, and w that make the modeled values to be close to real values. Finding the harmonic frequencies w is the most difficult part of fitting a trigonometric model. In the case of a Fourier series, these frequencies are set at 2*pi*h/n. But, the Fourier series extrapolation means simply repeating the n past prices into the future.

This indicator uses the Quinn-Fernandes algorithm to find the harmonic frequencies. It fits harmonics of the trigonometric series one by one until the specified total number of harmonics H is reached. After fitting a new harmonic , the coded algorithm computes the residue between the updated model and the real values and fits a new harmonic to the residue.

see here: A Fast Efficient Technique for the Estimation of Frequency , B. G. Quinn and J. M. Fernandes, Biometrika, Vol. 78, No. 3 (Sep., 1991), pp . 489-497 (9 pages) Published By: Oxford University Press

The indicator has the following input parameters:

src - input source

npast - number of past bars, to which trigonometric series is fitted;

Nfut - number of predicted future bars;

nharm - total number of harmonics in model;

frqtol - tolerance of frequency calculations.

The indicator plots two curves: the green/red curve indicates modeled past values and the yellow/fuchsia curve indicates the modeled future values.

The purpose of this indicator is to showcase the Fourier Extrapolator method to be used in future indicators.

Fourier Extrapolator of Price [Loxx]Fourier Extrapolator of Price is a multi-harmonic (or multi-tone) trigonometric model of a price series xi, i=1..n, is given by:

xi = m + Sum( a *Cos(w *i) + b *Sin(w *i), h=1..H )

Where:

xi - past price at i-th bar, total n past prices;

m - bias;

a and b - scaling coefficients of harmonics;

w - frequency of a harmonic;

h - harmonic number;

H - total number of fitted harmonics.

Fitting this model means finding m, a , b , and w that make the modeled values to be close to real values. Finding the harmonic frequencies w is the most difficult part of fitting a trigonometric model. In the case of a Fourier series, these frequencies are set at 2*pi*h/n. But, the Fourier series extrapolation means simply repeating the n past prices into the future.

This indicator uses the Quinn-Fernandes algorithm to find the harmonic frequencies. It fits harmonics of the trigonometric series one by one until the specified total number of harmonics H is reached. After fitting a new harmonic, the coded algorithm computes the residue between the updated model and the real values and fits a new harmonic to the residue.

see here: A Fast Efficient Technique for the Estimation of Frequency , B. G. Quinn and J. M. Fernandes, Biometrika, Vol. 78, No. 3 (Sep., 1991), pp. 489-497 (9 pages) Published By: Oxford University Press

The indicator has the following input parameters:

src - input source

npast - number of past bars, to which trigonometric series is fitted;

nharm - total number of harmonics in model;

frqtol - tolerance of frequency calculations.

The indicator plots the modeled past values

The purpose of this indicator is to showcase the Fourier Extrapolator method to be used in future indicators. While this method can also prediction future price movements, for our purpose here we will avoid doing.

tickerTracker MFI OscillatorDid you ever want to have a neat indicator window in line with your chart showing a different ticker? tickerTracker is a Money Flow Index (MFI) oscillator. The Money Flow Index (MFI) is a technical oscillator that uses price and volume for identifying overbought or oversold conditions in an asset. More or less, everything is connected in the market. The tickerTracker lets you see what is happening with another ticker that you have connected a correlation between them. For my example here, I'm using COIN in the main chart with the tickerTracker displaying BTC, QQQ and COIN Money Flow Index (MFI) in its window. As the end user, you can customize the colors, the length input and the ticker. Like any other indicator, the shorter length input, the more quickly responsive and the longer the length input, the smoother curve print.

Default Values:

MFI Length = 13

Chart ticker = white

SPY = white

QQQ = blue

IWM = yellow

DIA = orange

BTC/USD = yellow

ETH/USD = green

SOL/USD = purple

ADA/USD = red

Do your own due diligence, your risk is 100% your responsibility. This is for educational and entertainment purposes only. You win some or you learn some. Consider being charitable with some of your profit to help humankind. Good luck and happy trading friends...

*3x lucky 7s of trading*

7pt Trading compass:

Price action, entry/exit

Volume average/direction

Trend, patterns, momentum

Newsworthy current events

Revenue

Earnings

Balance sheet

7 Common mistakes:

+5% portfolio trades, capital risk management

Beware of analyst's motives

Emotions & Opinions

FOMO : bad timing, the market is ruthless, be shrewd

Lack of planning & discipline

Forgetting restraint

Obdurate repetitive errors, no adaptation

7 Important tools:

Trading View app!, Brokerage UI

Accurate indicators & settings

Wide screen monitor/s

Trading log (pencil & graph paper)

Big, organized desk

Reading books, playing chess

Sorted watch-list

Checkout my indicators:

Fibonacci VIP - volume

Fibonacci MA7 - price

pi RSI - trend momentum

TTC - trend channel

AlertiT - notification

tickerTracker - MFI Oscillator

www.tradingview.com

Number FrameNumber frame for any number input between 0 - 10, to 5 decimal places (you can change these limits in the code).

Default value pi = 3.14159

Feli DMAs + WMAs + BBsThe idea of this indicator is to have in the same place:

- Moving Averages

- Bollinger Bands

- Important crossings of MAs (golden cross, death cross, Pi Cycle)

Notes:

- The indicator has a main resolution that applies to all the elements and three independent resolutions for the MAs. Why? E.g. You want to see the real-time 20WMA but you're looking at a 1h chart. Normally, the last value of that MA would show on the last sunday at close and would update the next sunday close, but if you are looking at the same 1h chart but select a general resolution of 1h the 20WMA will be updated with the closing price of the last hour. Not sure if there's a best solution but it works for me.

Hope it helps! :)

Alino Forex SystemInizia a fare qualche spiccio con il forex.

Un indicatore di swing trading è uno strumento di analisi tecnica utilizzato per identificare nuove opportunità. Gli swing trader vogliono trarre profitto dai mini trend che sorgono tra alti e bassi (e viceversa). Per fare ciò, devono identificare il nuovo slancio il più rapidamente possibile, quindi utilizzano indicatori.

Ci sono due tipi di opportunità che uno swing trader utilizzerà per identificare gli indicatori: tendenze e breakout. Le tendenze sono movimenti di mercato a lungo termine che contengono oscillazioni a breve termine. I breakout segnano l'inizio di una nuova tendenza.

Gli swing trader potrebbero utilizzare indicatori su quasi tutti i mercati: inclusi forex , indici e azioni .

Gherkinit Futures Cycle█ OVERVIEW

Presented here is code for the " NYSE:GME Futures cycle theory" originally conceived by Gherkinit (Pi-Fi) and his quantitative analysts which is still under peer review.

This theory was built upon the knowledge that many intelligent investors on Reddit accrued over the past year in regards to the Mother Of All Short Squeezes this stock has to offer.

Up until now, what happened in January 2021 was considered an anomaly brought on by FOMO and retail interest but it's starting to look like unfair market makers and similar went to cover and ran head on into retail FOMO which is why they cut off the buying at that time. In order to understand what happened and what's to come, visualizing the theory with ease is essential.

█ WHAT THE SETTINGS MEAN

- Enable Draw | Visual Clean up

(True/False) Quarterly dates : Enables or disables the quarterly dates that repeat every "cycle".

(True/False) Roll dates : Enables or disables the roll dates that repeat every "cycle".

(True/False) Expiration dates : Enables or disables the expiration dates that repeat every "cycle".

(True/False) Run dates : Enables or disables the run dates that repeat every "cycle".

- Date Colors | Making things look good

(Color) Quarterly : Color for the respective date.

(Color) Roll : Color for the respective date.

(Color) Expiration : Color for the respective date.

(Color) Run : Color for the respective date.

- Extended Cycle | Look into the future

(Integer) Extended line height multiplier : A multiplier value for the height of the lines representing the selected "future" cycle.

(Dollar Amount) Extended line height : The height value in dollars of the lines representing the selected "future" cycle.

(Integer) Extended line width : The width of the lines representing the selected "future" cycle.

(Integer) Extended cycle ID : The cycle you want to see "ahead" or in the "future". For example if you set the value to "0" you'll only see cycles from the past up until the present (already occurred). If you set the value to "1" you will see the estimated dates for the specific cycle in the future i.e. 1 cycle ahead of the last completed/visible cycle on the chart.

█ EXTRA INFO

This indicator was simply made by a bored CS student who didn't want to endlessly mark dates on a graph after learning more about the theory.

Hope this help whoever uses this. To the moon fellow apes!

- Winter ;)

P.s. Pickle 4 Life

ArrayGenerateLibrary "ArrayGenerate"

Functions to generate arrays.

sequence_int(start, end, step) returns a sequence of int numbers.

Parameters:

start : int, begining of sequence range.

end : int, end of sequence range.

step : int, step, default=1 .

Returns: int , array.

sequence_float(start, end, step) returns a sequence of float numbers.

Parameters:

start : float, begining of sequence range.

end : float, end of sequence range.

step : float, step, default=1.0 .

Returns: float , array.

sequence_from_series(src, length, shift, direction_forward) Creates a array from a series sample range.

Parameters:

src : series, any kind.

length : int, window period in bars to sample series.

shift : int, window period in bars to shift backwards the data sample, default=0.

direction_forward : bool, sample from start to end or end to start order, default=true.

Returns: float array

normal_distribution(size, mean, dev) Generate normal distribution random sample.

Parameters:

size : int, size of array

mean : float, mean of the sample, (default=0.0).

dev : float, deviation of the sample from the mean, (default=1.0).

Returns: float array.

log_spaced(length, start_exp, stop_exp) Generate a base 10 logarithmically spaced sample sequence.

Parameters:

length : int, length of the sequence.

start_exp : float, start exponent.

stop_exp : float, stop exponent.

Returns: float array.

linear_range(stop, start) Generate a linearly spaced sample vector within the inclusive interval (start, stop) and step 1.

Parameters:

stop : float, stop value.

start : float, start value, (default=0.0).

Returns: float array.

periodic_wave(length, sampling_rate, frequency, amplitude, phase, delay) Create a periodic wave.

Parameters:

length : int, the number of samples to generate.

sampling_rate : float, samples per time unit (Hz). Must be larger than twice the frequency to satisfy the Nyquist criterion.

frequency : float, frequency in periods per time unit (Hz).

amplitude : float, the length of the period when sampled at one sample per time unit. This is the interval of the periodic domain, a typical value is 1.0, or 2*Pi for angular functions.

phase : float, optional phase offset.

delay : int, optional delay, relative to the phase.

Returns: float array.

sinusoidal(length, sampling_rate, frequency, amplitude, mean, phase, delay) Create a Sine wave.

Parameters:

length : int, The number of samples to generate.

sampling_rate : float, Samples per time unit (Hz). Must be larger than twice the frequency to satisfy the Nyquist criterion.

frequency : float, Frequency in periods per time unit (Hz).

amplitude : float, The maximal reached peak.

mean : float, The mean, or DC part, of the signal.

phase : float, Optional phase offset.

delay : int, Optional delay, relative to the phase.

Returns: float array.

periodic_impulse(length, period, amplitude, delay) Create a periodic Kronecker Delta impulse sample array.

Parameters:

length : int, The number of samples to generate.

period : int, impulse sequence period.

amplitude : float, The maximal reached peak.

delay : int, Offset to the time axis. Zero or positive.

Returns: float array.

PI_GRM Bitcoin Golden Ratio Multipier [wozdux]Golden Ratio Multiplier

Formula GRM=MA350(BTC USD) * (1.6;2;3;5;8;13;21)

The multiplier examines medium-and long-term time cycles.

For this, a multiple of 350 MA is used to determine the areas of potential resistance.

Additionally, fibo levels from the main line.

version 2021 year modification

Scalp ProScalp Pro is a scalping tool that uses the MACD mechanism. MACD lines are smoothed using fibonacci numbers and pi numbers. In this way, the noise on the signal is reduced. A " BUY " signal is generated when the lines cross upwards. If the lines cross down, a " SELL " signal is generated. The logic is very simple and the Indicator is very useful.

I wish you many profitable trades.

[EG] MA ATR ChannelsGreetings - the aim of this indicator was to code a single indicator with a selectable moving average, so I could examine price relationships to MA's and Average True Range (ATR) bollinger type bands. You can obviously approach this tool in so many different ways so I am going to share first an overview of moving averages and a short overview of how I use this this indicator.

Simple ( SMA ) – A simple average of the past N (length) prices. Just add the price data for each N (bar) and divide the total by N.

Exponential ( EMA ) – An exponential moving average with a greater weight for recent prices. The weighting is exponential. An N-period EMA takes more than N data points into account and gradually dilutes past data’s effect.

Double Exponential ( DEMA ) - Same as an EMA , the Double exponential moving average , or DEMA , is a measure of a security's trending average price that gives the even more weight to recent price data. Aimed to help reduce lag.

Triple Exponential ( TEMA ) - Same as an EMA , the Triple exponential moving average , or TEMA , is a measure of a security's trending average price that gives the even more weight to recent price data than EMA or DEMA . Aimed to help reduce lag.

Weighted ( WMA ) – An average of the past N prices with a linear weighting, again giving greater weight to more recent prices.

Hull ( HMA ) - The Hull Moving Average (developed by Alan Hull) has the purpose of reducing lag, increasing responsiveness while at the same time eliminating noise. It emphasises recent prices over older ones, resulting in a fast-acting yet smooth moving average that can be used to identify the prevailing market trend.

Wilder's (RMA) - Wilder's smoothing is a type of exponential moving average . It takes one parameter, the period n, and price. Larger values for n will have a greater smoothing effect on the input data but will also create more lag. It is equivalent to a 2n-1 Exponential Moving Average . For example, a 10 period Wilder's smoothing is the same as a 19 period exponential moving average .

Symmetrically Weighted ( SWMA ) - Weight distribution starts from median of given period and it's reduced linearly to the sides so the ending and starting point of period have the least weight. It's smooth and fast but reacts late to trend changes on higher lengths (lookback).

Arnaud Legoux ( ALMA ) - Arnaud Legoux Moving Average removes small price fluctuations and enhances trend via applying a moving average twice, once from left to right, and once from right to left and combines both. At the end of this process the phase shift (price lag) commonly associated with moving averages is significantly reduced.

Volume-Weighted ( VWMA ) - A Volume-Weighted Moving Average gives a different weight to each closing price and this weight depends on the volume of that period. For example, the closing price of a day with high volume will have a greater weight on the moving average value.

Volume Weighted Average Price ( VWAP ) - Though not necessarily a MA - Volume-weighted average price ( VWAP ) is a ratio of the cumulative share price to the cumulative volume traded over a given time period and so I thought would be useful as an ATR tool. The VWAP is calculated using the opening price for each day and adjusting in real time right up until the close of the session. Thus, the calculation uses intraday data only.

So what is Average True Range ?

Average True Range is a measure of volatility . It's an area that represents roughly how much you can expect a security to change in price over a time period. Average true range is usually calculated by applying Wilders Smoothing to True Range. If you want regular ATR - use RMA as the input for the ATR. The ATR is then divided into periods based on derivatives of Phi (3.14) and Fibs (0.618, 1.618 etc.) You will notice price bounces off the lines. Look for patterns.

The indicator - consisting of 3 parts:

Price/Fast MA - this is an MA anywhere between 3-20 periods that is reflective of very recent price action. It is red when price is below - and green when above. Recommendations : SMA , EMA , WMA , HMA

Trend/Medium MA - this is a slower MA that you could set anywhere between 30 - 100 periods that is reflective of overall bull/bear market trend depending on both it's direction and whether the Price MA / price is lower or higher. Recommendations: EMA , WMA , VWMA , RMA, ALMA

Average True Range - this is a way to measure and visualise range the price may be capable of in - if it is towards or below the 2.1 multiplier - a bull reversal is more likely and vice versea. The multi's are set to factors of Pi and Fibonacci ratio's. Green channel means bullish, red channel means bearish. Gold means sign of a likely reversal. If the PMA enters the channel - it is likely the reversal is cancelled for a short period more.

Recommendations : RMA, EMA , VWMA , ALMA , SWMA , VWAP

How I use it :

First of all - Consider longs when channel is green - or going to bounce on a support line - and consider shorts based on the opposite. This is not a buy/sell indicator - this is a MAP to PRICE to give reference and meaning to price movements across multiple time frames - very useful when using with a volume indicator and an RSI. I personally use it on the 3m chart but change the TFM to 5 for 15m data.

If you wish to see any other more exotic or interesting MA's added please feel free to request them in the comments ! And thanks for checking out my first indicator

Euler Cubes - CubᵋI give you the "Euler Cubes", inspired by the mathematical number 'e' (Euler's number).

It is suggested (fibonacci ratios analogy) that price/e ratio can give Support/Resistance area's.

The first cube is made by a low/high of choice, for example:

You set the 'source low'/'source high' in position:

Then you choose the 'e ratio' (x times 'e')

This multiplies the distance 'high-low' times '0.271828' times 'the set number' .

For example, choosing 5 gives 5 x 0.271828 = 1.35914, the distance 'high-low' hereby multiplied by 1.35914, the following cubes multiply the previous distance by 1.35914.

(Settings below 5 will give cubes smaller than the 'high-low' distance)

In the case of x times 'e' = 5:

You can extend the lines:

Now you can give it an angle:

Do mind, using it over very little bars and using an angle can cause some lines to not align as intended, because for now, it is not possible to plot in between bars.

There are also 'Euler' SMA and EMA available with following length's:

27, 54, 82,109, 136, 163, 190 and 217

Cheers!

AlertiTI can't be glued to all charts on all tickers all the time. I have a life you know, lol.

So in the spirit of getting fresh air, running errands, working and having fun with family & friends, I setup this AlertiT script.

Three indicators: RSI, SMA and Momentum are used in this script alert.

The alert will be triggered if any of the indicators crosses a specified input.

The message will contain the name of the indicator and its current value.

The default is 13 SMA, 9 RSI +75:-25 and 11 Momentum.

I provided an input in the dialogue box so the variables can be adjusted to suit your needs.

Source is open, high, low, close.

Do your own due diligence, your risk is 100% your responsibility. You win some or you learn some. Consider being charitable with some of your profit to help humankind. Small incremental steps work : If you double a penny a day for a month it = $5,368,709. Good luck and happy trading friends...

*3x lucky 7s of trading*

7pt Trading compass:

Price action, entry/exit

Volume average/direction

Trend, patterns, momentum

Newsworthy current events

Revenue

Earnings

Balance sheet

7 Common mistakes:

+5% portfolio trades, risk management

Beware of analysts motives

Emotions & Opinions

FOMO : bad timing

Lack of planning & discipline

Forgetting restraint

Obdurate repetitive errors, no adaptation

7 Important tools:

Trading View app!, Brokerage UI

Accurate indicators & settings

Wide screen monitor/s

Trading log (pencil & graph paper)

Big organized desk

Reading books, playing chess

Sorted watch-list

Checkout my indicators:

Fibonacci VIP - volume

Fibonacci MA7 - price

pi RSI - trend momentum

TTC - trend channel

AlertiT - notification

www.tradingview.com

TTC: Triangular Trend ChannelTTC: Triangular Trend Channel is a script to dynamically create a trend channel on the move. It uses open, high, low, close, simple moving average inputs for it's plot lines.

Default color coded in top to bottom price order:

green = top

orange

blue

white = center (9sma)

purple

yellow

red = bottom

The base sma is 9, but all default settings can be changed to suit your needs in the dialogue box. Depending on the time frame chart, you can dial in the accuracy by adjusting the default settings.

Do your own due diligence, your risk is 100% your responsibility. You win some or you learn some. Consider being charitable with some of your profit to help humankind. Small incremental steps work : If you double a penny for a month it = $5,368,709. Good luck and happy trading friends...

*3x lucky 7s of trading*

7pt Trading compass:

Price action, entry/exit

Volume average/direction

Trend, patterns, momentum

Newsworthy current events

Revenue

Earnings

Balance sheet

7 Common mistakes:

+5% portfolio trades, risk management

Beware of analysts motives

Emotions & Opinions

FOMO : bad timing

Lack of planning & discipline

Forgetting restraint

Obdurate repetitive errors, no adaptation

7 Important tools:

Trading View app!, Brokerage UI

Accurate indicators & settings

Wide screen monitor/s

Trading log (pencil & graph paper)

Big organized desk

Reading books, playing chess

Sorted watch-list

Checkout my indicators:

Fibonacci VIP - volume

Fibonacci MA7 - price

pi RSI - trend momentum

TTC - trend channel

www.tradingview.com

Free Zen SMA CollectionWith this script/indicator you combine a couple of different plots based mainly on moving average function.

Plot functions:

1. Highlight Dates: Weekends, New Years and halvings. Just for a better orientation.

2. Add 2 custom MA's (SMA, EMA or RMA)

- observe the golden/death crossos of them

- observe the filled area between them

- observe the slope of the MA's based on the color of the lines

3. Plot the 350SMA daily and their golden ratio multiplier (BTC related)

4. Highlight the ATH cross based on Pi cycle (SMA(111) crosses SMA(350)*2)

5. Plot EMA Ribbons.

have fun guys and thanks to all others who contribute to this huge script community

[blackcat] L2 Ehlers Market Mode IdentifierLevel: 2

Background

John F. Ehlers introuced Market Mode Identifier in his "Rocket Science for Traders" chapter 11. The simplified model of the market, derived from the Drunkard's Walk problem, has only two modes-the Cycle Mode and the Trend Mode. Through the derivation of the Sinewave Indicator and the Instantaneous Trendline, Ehlers had shown several ways to estimate which mode the market may have for a given moment. As with most technical indicators, the decision point between modes is not clear-cut. In fact, trying to automate the decision often leads to a great deal of chatter and rapid back and

forth switching of decisions.

Function

blackcat L2 Ehlers Market Mode Identifier is used to identify market status is in Trend Mode or Cycle Mode.Since the Cycle Mode exists for the smallest fraction of time and since most traders make the most money following a trend rather than a cycle, it is best to assume that the market is in a Trend Mode unless some very specific criteria are met. There are only two criteria to establish a Cycle Mode. First, a Cycle Mode exists for the period of a half-dominant cycle after the crossing of the two Sinewave Indicator lines. Second, a Cycle Mode exists if the measured phase rate of change is more than two-thirds the phase rate of change of the dominant cycle (2*pi /Period) and is less

than 1.5 times the phase rate of change of the dominant cycle. There is another condition that defines a Trend Mode. This condition is derived from pragmatic observation, not theoretical considerations. When the market makes a major reversal, it often does this with great vigor. When this occurs, the prices have a wide separation from the Instantaneous Trendline. When the prices are widely separated from the Instantaneous Trendline, it is possible for the Cycle Mode conditions to be met-but the Cycle Mode identification is clearly incorrect. Dr. Ehlers have therefore inserted another overriding rule for these cases. That rule is that if the SmoothPrice (the 4-bar WMA of the Price) is separated by more than 1.5 percent from the Instantaneous Trendline, then the correct market mode is the Trend Mode.

Key Signal

Smooth --> 4 bar WMA w/ 1 bar lag

Detrender --> The amplitude response of a minimum-length HT can be improved by adjusting the filter coefficients by

trial and error. HT does not allow DC component at zero frequency for transformation. So, Detrender is used to remove DC component/ trend component.

Q1 --> Quadrature phase signal

I1 --> In-phase signal

Period --> Dominant Cycle in bars

SmoothPeriod --> Period with complex averaging

DCPeriod ---> Dominant Cycle Period

Trendline ---> IT fast line

SmoothPrice ---> IT slow line

Trend ---> Trend identifier: 1 for trend; 0 for cycle.

Pros and Cons

100% John F. Ehlers definition translation of original work, even variable names are the same. This help readers who would like to use pine to read his book. If you had read his works, then you will be quite familiar with my code style.

NOTE: I had tried several time frames, and found it did not work well for time frame < 1W.

Remarks

The 10th script for Blackcat1402 John F. Ehlers Week publication.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

[blackcat] L2 Ehlers Phase Accumulator Cycle Period MeasurerLevel: 2

Background

John F. Ehlers introuced Phase Accumulation technique of cycle period measurement in his "Rocket Science for Traders" chapter 7. It is perhaps the easiest to comprehend. In this technique, John Ehlers measures the phase at each sample by taking the arctangent of the ratio of the Quadrature component to the In-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample Dr. Ehlers then looks backward, adding up the delta phases. When the sum of the delta phases reaches 360 degrees (2*pi in tradingview), we must have passed through one full cycle, on average. The process is repeated for each new sample.

Function

blackcat L2 Ehlers Phase Accumulator Cycle Period Measurer is used to measure Dominant Cycle (DC). This is one of John Ehlers three major methods to measure DC. The Phase Accumulation method of cycle measurement always uses one full cycle’s worth of historical data. This is both an advantage and disadvantage. The advantage is the lag in obtaining the answer scales directly with the cycle period. That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. Longer averaging reduces the noise level compared to the signal. Therefore, shorter cycle periods necessarily have a higher output Signal-to-Noise Ratio (SNR).

Key Signal

Smooth --> 4 bar WMA w/ 1 bar lag

Detrender --> The amplitude response of a minimum-length HT can be improved by adjusting the filter coefficients by

trial and error. HT does not allow DC component at zero frequency for transformation. So, Detrender is used to remove DC component/ trend component.

Q1 --> Quadrature phase signal

I1 --> In-phase signal

Period --> Dominant Cycle in bars

Pros and Cons

100% John F. Ehlers definition translation of original work, even variable names are the same. This help readers who would like to use pine to read his book. If you had read his works, then you will be quite familiar with my code style.

Remarks

The 2nd script for Blackcat1402 John F. Ehlers Week publication.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.