FunctionBaumWelchLibrary "FunctionBaumWelch"

Baum-Welch Algorithm, also known as Forward-Backward Algorithm, uses the well known EM algorithm

to find the maximum likelihood estimate of the parameters of a hidden Markov model given a set of observed

feature vectors.

---

### Function List:

> `forward (array pi, matrix a, matrix b, array obs)`

> `forward (array pi, matrix a, matrix b, array obs, bool scaling)`

> `backward (matrix a, matrix b, array obs)`

> `backward (matrix a, matrix b, array obs, array c)`

> `baumwelch (array observations, int nstates)`

> `baumwelch (array observations, array pi, matrix a, matrix b)`

---

### Reference:

> en.wikipedia.org

> github.com

> en.wikipedia.org

> www.rdocumentation.org

> www.rdocumentation.org

forward(pi, a, b, obs)

Computes forward probabilities for state `X` up to observation at time `k`, is defined as the

probability of observing sequence of observations `e_1 ... e_k` and that the state at time `k` is `X`.

Parameters:

pi (float ) : Initial probabilities.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing

states given a state matrix is size (M x M) where M is number of states.

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. Given

state matrix is size (M x O) where M is number of states and O is number of different

possible observations.

obs (int ) : List with actual state observation data.

Returns: - `matrix _alpha`: Forward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first

dimension refers to the state and the second dimension to time.

forward(pi, a, b, obs, scaling)

Computes forward probabilities for state `X` up to observation at time `k`, is defined as the

probability of observing sequence of observations `e_1 ... e_k` and that the state at time `k` is `X`.

Parameters:

pi (float ) : Initial probabilities.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing

states given a state matrix is size (M x M) where M is number of states.

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. Given

state matrix is size (M x O) where M is number of states and O is number of different

possible observations.

obs (int ) : List with actual state observation data.

scaling (bool) : Normalize `alpha` scale.

Returns: - #### Tuple with:

> - `matrix _alpha`: Forward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first

dimension refers to the state and the second dimension to time.

> - `array _c`: Array with normalization scale.

backward(a, b, obs)

Computes backward probabilities for state `X` and observation at time `k`, is defined as the probability of observing the sequence of observations `e_k+1, ... , e_n` under the condition that the state at time `k` is `X`.

Parameters:

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

obs (int ) : Array with actual state observation data.

Returns: - `matrix _beta`: Backward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first dimension refers to the state and the second dimension to time.

backward(a, b, obs, c)

Computes backward probabilities for state `X` and observation at time `k`, is defined as the probability of observing the sequence of observations `e_k+1, ... , e_n` under the condition that the state at time `k` is `X`.

Parameters:

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

obs (int ) : Array with actual state observation data.

c (float ) : Array with Normalization scaling coefficients.

Returns: - `matrix _beta`: Backward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first dimension refers to the state and the second dimension to time.

baumwelch(observations, nstates)

**(Random Initialization)** Baum–Welch algorithm is a special case of the expectation–maximization algorithm used to find the

unknown parameters of a hidden Markov model (HMM). It makes use of the forward-backward algorithm

to compute the statistics for the expectation step.

Parameters:

observations (int ) : List of observed states.

nstates (int)

Returns: - #### Tuple with:

> - `array _pi`: Initial probability distribution.

> - `matrix _a`: Transition probability matrix.

> - `matrix _b`: Emission probability matrix.

---

requires: `import RicardoSantos/WIPTensor/2 as Tensor`

baumwelch(observations, pi, a, b)

Baum–Welch algorithm is a special case of the expectation–maximization algorithm used to find the

unknown parameters of a hidden Markov model (HMM). It makes use of the forward-backward algorithm

to compute the statistics for the expectation step.

Parameters:

observations (int ) : List of observed states.

pi (float ) : Initial probaility distribution.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

Returns: - #### Tuple with:

> - `array _pi`: Initial probability distribution.

> - `matrix _a`: Transition probability matrix.

> - `matrix _b`: Emission probability matrix.

---

requires: `import RicardoSantos/WIPTensor/2 as Tensor`

Komut dosyalarını "欧易PI币开盘价格" için ara

pymath█ OVERVIEW

This library ➕ enhances Pine Script's built-in types (`float`, `int`, `array`, `array`) with mathematical methods, mirroring 🪞 many functions from Python's `math` module. Import this library to overload or add to built-in capabilities, enabling calls like `myFloat.sin()` or `myIntArray.gcd()`.

█ CONCEPTS

This library wraps Pine's built-in `math.*` functions and implements others where necessary, expanding the mathematical toolkit available within Pine Script. It provides a more object-oriented approach to mathematical operations on core data types.

█ HOW TO USE

• Import the library: i mport kaigouthro/pymath/1

• Call methods directly on variables: myFloat.sin() , myIntArray.gcd()

• For raw integer literals, you MUST use parentheses: `(1234).factorial()`.

█ FEATURES

• **Infinity Handling:** Includes `isinf()` and `isfinite()` for robust checks. Uses `POS_INF_PROXY` to represent infinity.

• **Comprehensive Math Functions:** Implements a wide range of methods, including trigonometric, logarithmic, hyperbolic, and array operations.

• **Object-Oriented Approach:** Allows direct method calls on `int`, `float`, and arrays for cleaner code.

• **Improved Accuracy:** Some functions (e.g., `remainder()`) offer improved accuracy compared to default Pine behavior.

• **Helper Functions:** Internal helper functions optimize calculations and handle edge cases.

█ NOTES

This library improves upon Pine Script's built-in `math` functions by adding new ones and refining existing implementations. It handles edge cases such as infinity, NaN, and zero values, enhancing the reliability of your Pine scripts. For Speed, it wraps and uses built-ins, as thy are fastest.

█ EXAMPLES

//@version=6

indicator("My Indicator")

// Import the library

import kaigouthro/pymath/1

// Create some Vars

float myFloat = 3.14159

int myInt = 10

array myIntArray = array.from(1, 2, 3, 4, 5)

// Now you can...

plot( myFloat.sin() ) // Use sin() method on a float, using built in wrapper

plot( (myInt).factorial() ) // Factorial of an integer (note parentheses)

plot( myIntArray.gcd() ) // GCD of an integer array

method isinf(self)

isinf: Checks if this float is positive or negative infinity using a proxy value.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) value to check.

Returns: (bool) `true` if the absolute value of `self` is greater than or equal to the infinity proxy, `false` otherwise.

method isfinite(self)

isfinite: Checks if this float is finite (not NaN and not infinity).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The value to check.

Returns: (bool) `true` if `self` is not `na` and not infinity (as defined by `isinf()`), `false` otherwise.

method fmod(self, divisor)

fmod: Returns the C-library style floating-point remainder of `self / divisor` (result has the sign of `self`).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Dividend `x`.

divisor (float) : (float) Divisor `y`. Cannot be zero or `na`.

Returns: (float) The remainder `x - n*y` where n is `trunc(x/y)`, or `na` if divisor is 0, `na`, or inputs are infinite in a way that prevents calculation.

method factorial(self)

factorial: Calculates the factorial of this non-negative integer.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) The integer `n`. Must be non-negative.

Returns: (float) `n!` as a float, or `na` if `n` is negative or overflow occurs (based on `isinf`).

method isqrt(self)

isqrt: Calculates the integer square root of this non-negative integer (floor of the exact square root).

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) The non-negative integer `n`.

Returns: (int) The greatest integer `a` such that a² <= n, or `na` if `n` is negative.

method comb(self, k)

comb: Calculates the number of ways to choose `k` items from `self` items without repetition and without order (Binomial Coefficient).

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) Total number of items `n`. Must be non-negative.

k (int) : (int) Number of items to choose. Must be non-negative.

Returns: (float) The binomial coefficient nCk, or `na` if inputs are invalid (n<0 or k<0), `k > n`, or overflow occurs.

method perm(self, k)

perm: Calculates the number of ways to choose `k` items from `self` items without repetition and with order (Permutations).

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) Total number of items `n`. Must be non-negative.

k (simple int) : (simple int = na) Number of items to choose. Must be non-negative. Defaults to `n` if `na`.

Returns: (float) The number of permutations nPk, or `na` if inputs are invalid (n<0 or k<0), `k > n`, or overflow occurs.

method log2(self)

log2: Returns the base-2 logarithm of this float. Input must be positive. Wraps `math.log(self) / math.log(2.0)`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be positive.

Returns: (float) The base-2 logarithm, or `na` if input <= 0.

method trunc(self)

trunc: Returns this float with the fractional part removed (truncates towards zero).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The integer part, or `na` if input is `na` or infinite.

method abs(self)

abs: Returns the absolute value of this float. Wraps `math.abs()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The absolute value, or `na` if input is `na`.

method acos(self)

acos: Returns the arccosine of this float, in radians. Wraps `math.acos()`. Input must be between -1 and 1.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be between -1 and 1.

Returns: (float) Angle in radians , or `na` if input is outside or `na`.

method asin(self)

asin: Returns the arcsine of this float, in radians. Wraps `math.asin()`. Input must be between -1 and 1.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be between -1 and 1.

Returns: (float) Angle in radians , or `na` if input is outside or `na`.

method atan(self)

atan: Returns the arctangent of this float, in radians. Wraps `math.atan()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) Angle in radians , or `na` if input is `na`.

method ceil(self)

ceil: Returns the ceiling of this float (smallest integer >= self). Wraps `math.ceil()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The ceiling value, or `na` if input is `na` or infinite.

method cos(self)

cos: Returns the cosine of this float (angle in radians). Wraps `math.cos()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The cosine, or `na` if input is `na`.

method degrees(self)

degrees: Converts this float from radians to degrees. Wraps `math.todegrees()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The angle in degrees, or `na` if input is `na`.

method exp(self)

exp: Returns e raised to the power of this float. Wraps `math.exp()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The exponent.

Returns: (float) `e**self`, or `na` if input is `na`.

method floor(self)

floor: Returns the floor of this float (largest integer <= self). Wraps `math.floor()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The floor value, or `na` if input is `na` or infinite.

method log(self)

log: Returns the natural logarithm (base e) of this float. Wraps `math.log()`. Input must be positive.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be positive.

Returns: (float) The natural logarithm, or `na` if input <= 0 or `na`.

method log10(self)

log10: Returns the base-10 logarithm of this float. Wraps `math.log10()`. Input must be positive.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be positive.

Returns: (float) The base-10 logarithm, or `na` if input <= 0 or `na`.

method pow(self, exponent)

pow: Returns this float raised to the power of `exponent`. Wraps `math.pow()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The base.

exponent (float) : (float) The exponent.

Returns: (float) `self**exponent`, or `na` if inputs are `na` or lead to undefined results.

method radians(self)

radians: Converts this float from degrees to radians. Wraps `math.toradians()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in degrees.

Returns: (float) The angle in radians, or `na` if input is `na`.

method round(self)

round: Returns the nearest integer to this float. Wraps `math.round()`. Ties are rounded away from zero.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The rounded integer, or `na` if input is `na` or infinite.

method sign(self)

sign: Returns the sign of this float (-1, 0, or 1). Wraps `math.sign()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) -1 if negative, 0 if zero, 1 if positive, `na` if input is `na`.

method sin(self)

sin: Returns the sine of this float (angle in radians). Wraps `math.sin()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The sine, or `na` if input is `na`.

method sqrt(self)

sqrt: Returns the square root of this float. Wraps `math.sqrt()`. Input must be non-negative.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be non-negative.

Returns: (float) The square root, or `na` if input < 0 or `na`.

method tan(self)

tan: Returns the tangent of this float (angle in radians). Wraps `math.tan()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The tangent, or `na` if input is `na`.

method acosh(self)

acosh: Returns the inverse hyperbolic cosine of this float. Input must be >= 1.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be >= 1.

Returns: (float) The inverse hyperbolic cosine, or `na` if input < 1 or `na`.

method asinh(self)

asinh: Returns the inverse hyperbolic sine of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The inverse hyperbolic sine, or `na` if input is `na`.

method atanh(self)

atanh: Returns the inverse hyperbolic tangent of this float. Input must be between -1 and 1 (exclusive).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be between -1 and 1 (exclusive).

Returns: (float) The inverse hyperbolic tangent, or `na` if input is outside (-1, 1) or `na`.

method cosh(self)

cosh: Returns the hyperbolic cosine of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The hyperbolic cosine, or `na` if input is `na`.

method sinh(self)

sinh: Returns the hyperbolic sine of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The hyperbolic sine, or `na` if input is `na`.

method tanh(self)

tanh: Returns the hyperbolic tangent of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The hyperbolic tangent, or `na` if input is `na`.

method atan2(self, dx)

atan2: Returns the angle in radians between the positive x-axis and the point (dx, self). Wraps `math.atan2()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The y-coordinate `y`.

dx (float) : (float) The x-coordinate `x`.

Returns: (float) The angle in radians , result of `math.atan2(self, dx)`. Returns `na` if inputs are `na`. Note: `math.atan2(0, 0)` returns 0 in Pine.

Optimization: Use built-in math.atan2()

method cbrt(self)

cbrt: Returns the cube root of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The value to find the cube root of.

Returns: (float) The real cube root. Handles negative inputs correctly, or `na` if input is `na`.

method exp2(self)

exp2: Returns 2 raised to the power of this float. Calculated as `2.0.pow(self)`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The exponent.

Returns: (float) `2**self`, or `na` if input is `na` or results in non-finite value.

method expm1(self)

expm1: Returns `e**self - 1`. Calculated as `self.exp() - 1.0`. May offer better precision for small `self` in some environments, but Pine provides no guarantee over `self.exp() - 1.0`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The exponent.

Returns: (float) `e**self - 1`, or `na` if input is `na` or `self.exp()` is `na`.

method log1p(self)

log1p: Returns the natural logarithm of (1 + self). Calculated as `(1.0 + self).log()`. Pine provides no specific precision guarantee for self near zero.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Value to add to 1. `1 + self` must be positive.

Returns: (float) Natural log of `1 + self`, or `na` if input is `na` or `1 + self <= 0`.

method modf(self)

modf: Returns the fractional and integer parts of this float as a tuple ` `. Both parts have the sign of `self`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The number `x` to split.

Returns: ( ) A tuple containing ` `, or ` ` if `x` is `na` or non-finite.

method remainder(self, divisor)

remainder: Returns the IEEE 754 style remainder of `self` with respect to `divisor`. Result `r` satisfies `abs(r) <= 0.5 * abs(divisor)`. Uses round-half-to-even.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Dividend `x`.

divisor (float) : (float) Divisor `y`. Cannot be zero or `na`.

Returns: (float) The IEEE 754 remainder, or `na` if divisor is 0, `na`, or inputs are non-finite in a way that prevents calculation.

method copysign(self, signSource)

copysign: Returns a float with the magnitude (absolute value) of `self` but the sign of `signSource`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Value providing the magnitude `x`.

signSource (float) : (float) Value providing the sign `y`.

Returns: (float) `abs(x)` with the sign of `y`, or `na` if either input is `na`.

method frexp(self)

frexp: Returns the mantissa (m) and exponent (e) of this float `x` as ` `, such that `x = m * 2^e` and `0.5 <= abs(m) < 1` (unless `x` is 0).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The number `x` to decompose.

Returns: ( ) A tuple ` `, or ` ` if `x` is 0, or ` ` if `x` is non-finite or `na`.

method isclose(self, other, rel_tol, abs_tol)

isclose: Checks if this float `a` and `other` float `b` are close within relative and absolute tolerances.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) First value `a`.

other (float) : (float) Second value `b`.

rel_tol (simple float) : (simple float = 1e-9) Relative tolerance. Must be non-negative and less than 1.0.

abs_tol (simple float) : (simple float = 0.0) Absolute tolerance. Must be non-negative.

Returns: (bool) `true` if `abs(a - b) <= max(rel_tol * max(abs(a), abs(b)), abs_tol)`. Handles `na`/`inf` appropriately. Returns `na` if tolerances are invalid.

method ldexp(self, exponent)

ldexp: Returns `self * (2**exponent)`. Inverse of `frexp`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Mantissa part `x`.

exponent (int) : (int) Exponent part `i`.

Returns: (float) The result of `x * pow(2, i)`, or `na` if inputs are `na` or result is non-finite.

method gcd(self)

gcd: Calculates the Greatest Common Divisor (GCD) of all integers in this array.

Namespace types: array

Parameters:

self (array) : (array) An array of integers.

Returns: (int) The largest positive integer that divides all non-zero elements, 0 if all elements are 0 or array is empty. Returns `na` if any element is `na`.

method lcm(self)

lcm: Calculates the Least Common Multiple (LCM) of all integers in this array.

Namespace types: array

Parameters:

self (array) : (array) An array of integers.

Returns: (int) The smallest positive integer that is a multiple of all non-zero elements, 0 if any element is 0, 1 if array is empty. Returns `na` on potential overflow or if any element is `na`.

method dist(self, other)

dist: Returns the Euclidean distance between this point `p` and another point `q` (given as arrays of coordinates).

Namespace types: array

Parameters:

self (array) : (array) Coordinates of the first point `p`.

other (array) : (array) Coordinates of the second point `q`. Must have the same size as `p`.

Returns: (float) The Euclidean distance, or `na` if arrays have different sizes, are empty, or contain `na`/non-finite values.

method fsum(self)

fsum: Returns an accurate floating-point sum of values in this array. Uses built-in `array.sum()`. Note: Pine Script does not guarantee the same level of precision tracking as Python's `math.fsum`.

Namespace types: array

Parameters:

self (array) : (array) The array of floats to sum.

Returns: (float) The sum of the array elements. Returns 0.0 for an empty array. Returns `na` if any element is `na`.

method hypot(self)

hypot: Returns the Euclidean norm (distance from origin) for this point given by coordinates in the array. `sqrt(sum(x*x for x in coordinates))`.

Namespace types: array

Parameters:

self (array) : (array) Array of coordinates defining the point.

Returns: (float) The Euclidean norm, or 0.0 if the array is empty. Returns `na` if any element is `na` or non-finite.

method prod(self, start)

prod: Calculates the product of all elements in this array.

Namespace types: array

Parameters:

self (array) : (array) The array of values to multiply.

start (simple float) : (simple float = 1.0) The starting value for the product (returned if the array is empty).

Returns: (float) The product of array elements * start. Returns `na` if any element is `na`.

method sumprod(self, other)

sumprod: Returns the sum of products of values from this array `p` and another array `q` (dot product).

Namespace types: array

Parameters:

self (array) : (array) First array of values `p`.

other (array) : (array) Second array of values `q`. Must have the same size as `p`.

Returns: (float) The sum of `p * q ` for all i, or `na` if arrays have different sizes or contain `na`/non-finite values. Returns 0.0 for empty arrays.

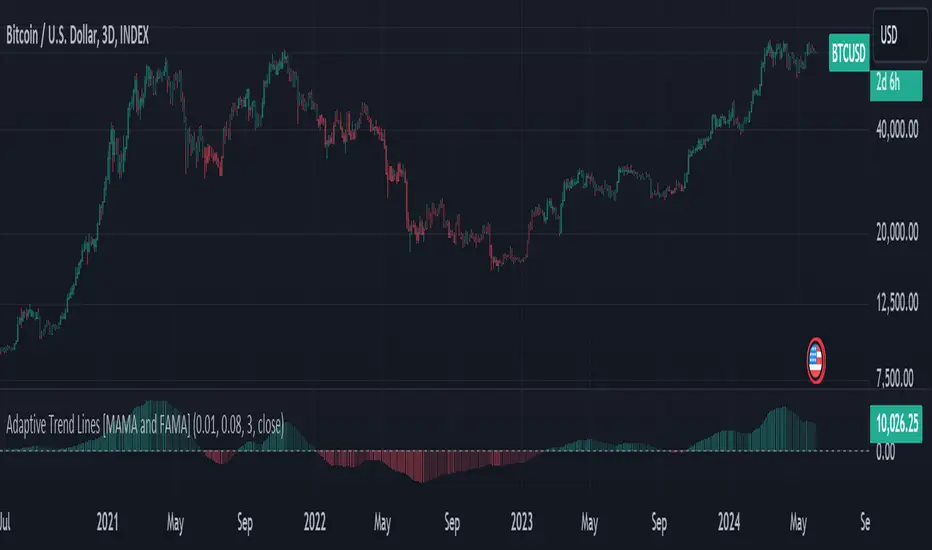

EMA Oracle and RSIEMA Oracle

- “See the market’s structure through the eyes of exponential wisdom.”

combines classic EMA stacks with Pi-based logic to reveal high-probability buy/sell zones and trend bias across timeframes

Multi-EMA Trend & Pi Signal Indicator

This advanced indicator combines classic trend analysis with Pi-based signal logic to help traders identify optimal entry and exit zones across multiple timeframes.

Core Features

EMA Trend Structure: Displays EMAs 9, 13, 20, 50, and 200 to visualize short-term and long-term trend orientation. Bullish momentum is indicated when shorter EMAs are stacked above longer ones.

Pi-Based Signal Logic: Inspired by the Pi Indicator, it includes EMA111 and EMA700 (350×2) on the daily chart:

Buy Zone: When price is trading below EMA111, it signals potential accumulation for spot or low-leverage position trades.

Sell Zone: When price is above EMA700, it suggests potential distribution or exit zones.

Trend Cross Alerts: Detects EMA crossovers and crossunders to highlight shifts in market structure and generate buy/sell signals.

Multi-Timeframe Analysis: Evaluates trend direction across selected timeframes (e.g., 15m, 30m, 1h, 4h, 1D), offering a broader market perspective.

RSI Integration: Combines Relative Strength Index (RSI) readings with EMA positioning to assess momentum and overbought/oversold conditions.

Trend Table Display: A dynamic table summarizes the asset’s trend status per timeframe, showing:

RSI values

EMA alignment

Overall trend bias (bullish, bearish, neutral)

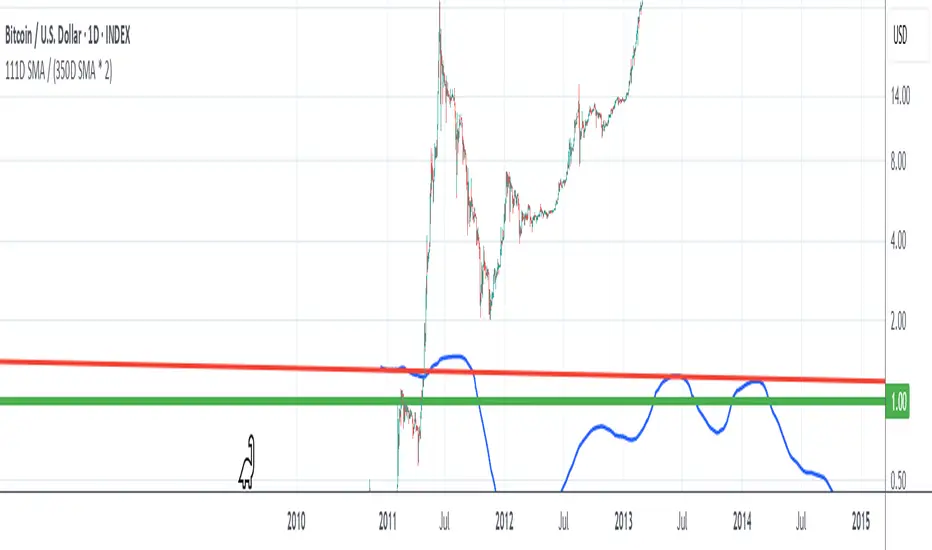

Intellect_city - World Cycle - Ath - Timeframe 1D and 1WIndicator Overview

The Pi Cycle Top Indicator has historically been effective in picking out the timing of market cycle highs within 3 days.

It uses the 111 day moving average (111DMA) and a newly created multiple of the 350 day moving average, the 350DMA x 2.

Note: The multiple is of the price values of the 350DMA, not the number of days.

For the past three market cycles, when the 111DMA moves up and crosses the 350DMA x 2 we see that it coincides with the price of Bitcoin peaking.

It is also interesting to note that 350 / 111 is 3.153, which is very close to Pi = 3.142. In fact, it is the closest we can get to Pi when dividing 350 by another whole number.

It once again demonstrates the cyclical nature of Bitcoin price action over long time frames. However, in this instance, it does so with a high degree of accuracy over Bitcoin's adoption phase of growth.

Bitcoin Price Prediction Using This Tool

The Pi Cycle Top Indicator forecasts the cycle top of Bitcoin’s market cycles. It attempts to predict the point where Bitcoin price will peak before pulling back. It does this on major high time frames and has picked the absolute tops of Bitcoin’s major price moves throughout most of its history.

How It Can Be Used

Pi Cycle Top is useful to indicate when the market is very overheated. So overheated that the shorter-term moving average, which is the 111-day moving average, has reached an x2 multiple of the 350-day moving average. Historically, it has proved advantageous to sell Bitcoin around this time in Bitcoin's price cycles.

It is also worth noting that this indicator has worked during Bitcoin's adoption growth phase, the first 15 years or so of Bitcoin's life. With the launch of Bitcoin ETF's and Bitcoin's increased integration into the global financial system, this indicator may cease to be relevant at some point in this new market structure.

111D SMA / (350D SMA * 2)Indicator: Pi Cycle Ratio

This custom technical indicator calculates a ratio between two moving averages that are used for the PI Cycle Top indicator. The PI Cycle Top indicator triggers when the 111-day simple moving average (111D SMA) crosses up with the 350-day simple moving average (350D SMA *2).

The line value is ratio is calculated as:

Line Value = 111DSMA / (350D SMA × 2)

When the 111D SMA crosses with the 350D SMA triggering the PI Cycle Top, the value of the ratio between the two lines is 1.

This visualizes the ratio between the two moving averages into a single line. This indicator can be used for technical analysis for historical and future moves.

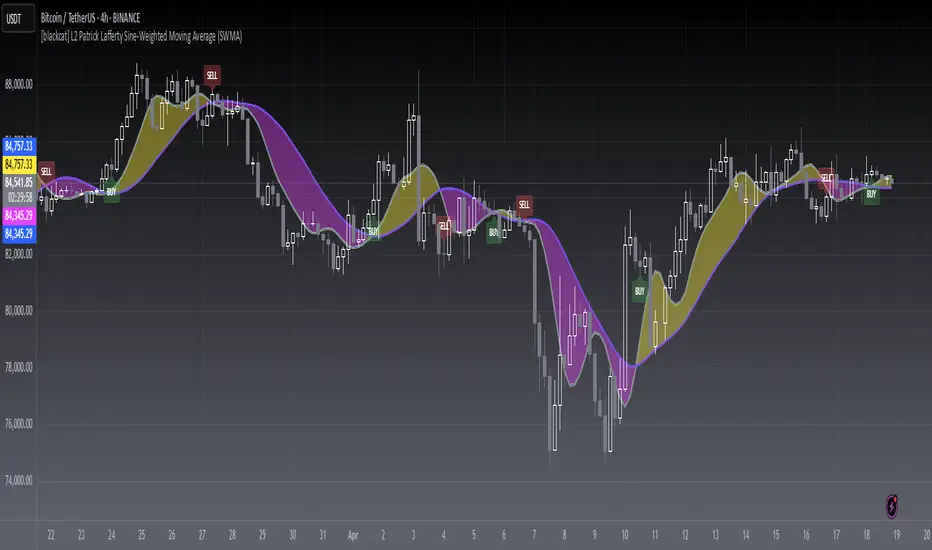

Bitcoin Cycle High/Low with functional Alert [heswaikcrypt]Introduction

Just as machines are fine-tuned for maximum efficiency, trading indicators must evolve to meet the demands of ever-changing markets.

Credit goes to the initial author, @NoCreditsLeft I only improved the existing Pi-cycle indicator with a functional alert and included a bull mode indicator in the script. The alert can help you get a live alert at candle close when the cycle tops, bottoms, and the potential bull phase switch occurs.

Philip Swift’s Pi Cycle Top Indicator is a brilliant example of leveraging mathematical relationships to signal critical turning points in Bitcoin’s price cycles. Historically, it has identified market and local tops with some relative accuracy, often within three days, as demonstrated in all the previous bull run cycles.

At its core, the Pi Cycle Indicator derives its name from the mathematical constant π (pi), achieved by using simple moving averages (MAs) in a specific ratio: 𝜋 = Long MA/short MA

The Bull mode switch is calculated using a crossover of the short exponentia moving average and the long moving average.

.

.

.

Knowing when Bitcoin reaches its top—and receiving timely alerts about it—is crucial for successful trading. The indicator is designed to signal;

Potential Bitcoin tops: Purple label

Potential Bitcoin bottoms : green Label, and

Parabolic swing : Yellow diamond shape (relating to the market switching to a potential bull mode)

"Please note: This indicator is tailored for Bitcoin using historical data analysis and should not be considered definitive. However accurate it might be."

Setting alerts

To set the alert conditions, select any alert function call to get alert whenever the conditions are met. The script is configured on dialy TF; you can set it on 1D or weekly TF.

Enjoy and Trade smartly

Bitcoin Macro Trend Map [Ox_kali]

## Introduction

__________________________________________________________________________________

The “Bitcoin Macro Trend Map” script is designed to provide a comprehensive analysis of Bitcoin’s macroeconomic trends. By leveraging a unique combination of Bitcoin-specific macroeconomic indicators, this script helps traders identify potential market peaks and troughs with greater accuracy. It synthesizes data from multiple sources to offer a probabilistic view of market excesses, whether overbought or oversold conditions.

This script offers significant value for the following reasons:

1. Holistic Market Analysis : It integrates a diverse set of indicators that cover various aspects of the Bitcoin market, from investor sentiment and market liquidity to mining profitability and network health. This multi-faceted approach provides a more complete picture of the market than relying on a single indicator.

2. Customization and Flexibility : Users can customize the script to suit their specific trading strategies and preferences. The script offers configurable parameters for each indicator, allowing traders to adjust settings based on their analysis needs.

3. Visual Clarity : The script plots all indicators on a single chart with clear visual cues. This includes color-coded indicators and background changes based on market conditions, making it easy for traders to quickly interpret complex data.

4. Proven Indicators : The script utilizes well-established indicators like the EMA, NUPL, PUELL Multiple, and Hash Ribbons, which are widely recognized in the trading community for their effectiveness in predicting market movements.

5. A New Comprehensive Indicator : By integrating background color changes based on the aggregate signals of various indicators, this script essentially creates a new, comprehensive indicator tailored specifically for Bitcoin. This visual representation provides an immediate overview of market conditions, enhancing the ability to spot potential market reversals.

Optimal for use on timeframes ranging from 1 day to 1 week , the “Bitcoin Macro Trend Map” provides traders with actionable insights, enhancing their ability to make informed decisions in the highly volatile Bitcoin market. By combining these indicators, the script delivers a robust tool for identifying market extremes and potential reversal points.

## Key Indicators

__________________________________________________________________________________

Macroeconomic Data: The script combines several relevant macroeconomic indicators for Bitcoin, such as the 10-month EMA, M2 money supply, CVDD, Pi Cycle, NUPL, PUELL, MRVR Z-Scores, and Hash Ribbons (Full description bellow).

Open Source Sources: Most of the scripts used are sourced from open-source projects that I have modified to meet the specific needs of this script.

Recommended Timeframes: For optimal performance, it is recommended to use this script on timeframes ranging from 1 day to 1 week.

Objective: The primary goal is to provide a probabilistic solution to identify market excesses, whether overbought or oversold points.

## Originality and Purpose

__________________________________________________________________________________

This script stands out by integrating multiple macroeconomic indicators into a single comprehensive tool. Each indicator is carefully selected and customized to provide insights into different aspects of the Bitcoin market. By combining these indicators, the script offers a holistic view of market conditions, helping traders identify potential tops and bottoms with greater accuracy. This is the first version of the script, and additional macroeconomic indicators will be added in the future based on user feedback and other inputs.

## How It Works

__________________________________________________________________________________

The script works by plotting each macroeconomic indicator on a single chart, allowing users to visualize and interpret the data easily. Here’s a detailed look at how each indicator contributes to the analysis:

EMA 10 Monthly: Uses an exponential moving average over 10 monthly periods to signal bullish and bearish trends. This indicator helps identify long-term trends in the Bitcoin market by smoothing out price fluctuations to reveal the underlying trend direction.Moving Averages w/ 18 day/week/month.

Credit to @ryanman0

M2 Money Supply: Analyzes the evolution of global money supply, indicating market liquidity conditions. This indicator tracks the changes in the total amount of money available in the economy, which can impact Bitcoin’s value as a hedge against inflation or economic instability.

Credit to @dylanleclair

CVDD (Cumulative Value Days Destroyed): An indicator based on the cumulative value of days destroyed, useful for identifying market turning points. This metric helps assess the Bitcoin market’s health by evaluating the age and value of coins that are moved, indicating potential shifts in market sentiment.

Credit to @Da_Prof

Pi Cycle: Uses simple and exponential moving averages to detect potential sell points. This indicator aims to identify cyclical peaks in Bitcoin’s price, providing signals for potential market tops.

Credit to @NoCreditsLeft

NUPL (Net Unrealized Profit/Loss): Measures investors’ unrealized profit or loss to signal extreme market levels. This indicator shows the net profit or loss of Bitcoin holders as a percentage of the market cap, helping to identify periods of significant market optimism or pessimism.

Credit to @Da_Prof

PUELL Multiple: Assesses mining profitability relative to historical averages to indicate buying or selling opportunities. This indicator compares the daily issuance value of Bitcoin to its yearly average, providing insights into when the market is overbought or oversold based on miner behavior.

Credit to @Da_Prof

MRVR Z-Scores: Compares market value to realized value to identify overbought or oversold conditions. This metric helps gauge the overall market sentiment by comparing Bitcoin’s market value to its realized value, identifying potential reversal points.

Credit to @Pinnacle_Investor

Hash Ribbons: Uses hash rate variations to signal buying opportunities based on miner capitulation and recovery. This indicator tracks the health of the Bitcoin network by analyzing hash rate trends, helping to identify periods of miner capitulation and subsequent recoveries as potential buying opportunities.

Credit to @ROBO_Trading

## Indicator Visualization and Interpretation

__________________________________________________________________________________

For each horizontal line representing an indicator, a legend is displayed on the right side of the chart. If the conditions are positive for an indicator, it will turn green, indicating the end of a bearish trend. Conversely, if the conditions are negative, the indicator will turn red, signaling the end of a bullish trend.

The background color of the chart changes based on the average of green or red indicators. This parameter is configurable, allowing adjustment of the threshold at which the background color changes, providing a clear visual indication of overall market conditions.

## Script Parameters

__________________________________________________________________________________

The script includes several configurable parameters to customize the display and behavior of the indicators:

Color Style:

Normal: Default colors.

Modern: Modern color style.

Monochrome: Monochrome style.

User: User-customized colors.

Custom color settings for up trends (Up Trend Color), down trends (Down Trend Color), and NaN (NaN Color)

Background Color Thresholds:

Thresholds: Settings to define the thresholds for background color change.

Low/High Red Threshold: Low and high thresholds for bearish trends.

Low/High Green Threshold: Low and high thresholds for bullish trends.

Indicator Display:

Options to show or hide specific indicators such as EMA 10 Monthly, CVDD, Pi Cycle, M2 Money, NUPL, PUELL, MRVR Z-Scores, and Hash Ribbons.

Specific Indicator Settings:

EMA 10 Monthly: Options to customize the period for the exponential moving average calculation.

M2 Money: Aggregation of global money supply data.

CVDD: Adjustments for value normalization.

Pi Cycle: Settings for simple and exponential moving averages.

NUPL: Thresholds for unrealized profit/loss values.

PUELL: Adjustments for mining profitability multiples.

MRVR Z-Scores: Settings for overbought/oversold values.

Hash Ribbons: Options for hash rate moving averages and capitulation/recovery signals.

## Conclusion

__________________________________________________________________________________

The “Bitcoin Macro Trend Map” by Ox_kali is a tool designed to analyze the Bitcoin market. By combining several macroeconomic indicators, this script helps identify market peaks and troughs. It is recommended to use it on timeframes from 1 day to 1 week for optimal trend analysis. The scripts used are sourced from open-source projects, modified to suit the specific needs of this analysis.

## Notes

__________________________________________________________________________________

This is the first version of the script and it is still in development. More indicators will likely be added in the future. Feedback and comments are welcome to improve this tool.

## Disclaimer:

__________________________________________________________________________________

Please note that the Open Interest liquidation map is not a guarantee of future market performance and should be used in conjunction with proper risk management. Always ensure that you have a thorough understanding of the indicator’s methodology and its limitations before making any investment decisions. Additionally, past performance is not indicative of future results.

Prometheus Polarized Fractal Efficiency (PFE)This indicator uses market data to calculate Polarized Fractal Efficiency (PFE) on an asset, so traders can have a better idea of which direction it may go.

Users can control the lookback length for the fractal calculation, the lookback length for the Exponential Moving Average (EMA), and whether or not to display lines at the -50 and 50 level, or -25 and 25 level.

Polarized Fractal Efficiency:

The Polarized Fractal Efficiency (PFE) indicator is a value between -100 and 100 with 0 as a midpoint.

A PFE above 0 indicates the asset may trend higher, a PFE below 0 indicates the asset may trend lower.

There are many ways to trade with PFE, the intuitive trend riding as described above, or reversals.

Even when the PFE is above 0, if it gets high enough, it may also be an indication of a reversal. A PFE of 90 - 100, or -100 - -90, may indicate price is ready to revert the other direction. Furthermore, traders already in a position may look to breaks of other levels to be their take profit or stop out spot.

Calculation:

Pi = 100 x (Price - Price )2 + N2 / Summation, j= 0, to N-2 (Price - Price )2 + 1

If Close < Close Pi = -Pi

PFEi = EMA(Pi, M)

Where:

N = period of indicator

M = smoothing period

Citation: www.investopedia.com

Scenarios:

Inputs are (9, 5) and every display option is on.

Trend example

Step 1: A short trade appears as PFE crosses below -25. We reach a safe take profit as PFE crosses below -50. Traders can use these levels to exit as well as enter.

Step 2: On the cross above 25 there is a safe long. As the PFE value breaks 0 a safe, early take profit could be appropriate for this trade. No guarantee we would see 50.

Step 3: Long scenario at break of 25, straight to 50. Simple, straightforward setup.

Step 4: This long results in a stop loss. Once again entry as PFE crosses 25, but as we cross the 0 line it is for a loss.

Step 5: The last trade in this example is reminiscent of step 3. This is a short trade entry at break of 25 and exit at break of 50.

Traders have liberty to use the PFE value to determine spots to enter and exit trades, long or short. 25 and 50 were chosen arbitrarily, values like 10 and 60 may work as well, we encourage traders to use their own discretion along with tools.

Reversal example

Step 1: PFE is around -100, crossing below it at one point! Strong zone for a potential reversal.

Step 2: PFE crosses above 25 adding conviction.

Step 3: Option to exit at 70.

Step 4: Option to exit at 90.

There is no “one size fits all method”, this approach may be more intuitive for some users and is just as feasible as the first.

Longer trend example

Step 1: Using -50 and 50 this time instead of -25 and 25 to be safer on our entries we see a short here. Was a good entry and as the value gets closer to -70 we can safely close.

Step 2: On this candle we see a long for the break of 50. On the next candle we break the 0 line, but because of our safe entry at 50, we could hold this and only stop out at a break of -25. We get close but stay in it and close at 70.

Step 3: Break of 50 for a long once again. This time the break of 0 line occurs as we are in profit, not letting a green trade go red is a golden rule of trading, so an early exit here.

Step 4: Same at step 2, break of 50 to long and stay in it, not stopping out at break of 0 line. The PFE value eventually reaches 70 and there is a good exit.

Quicker Reversal example

Step 1: Notice a close with PFE below -90, enter long for the reversal. Then close for profit when the PFE crosses above 70.

Step 2: When the PFE breaks above 90 we have a short entry. Like the long closing it when it crosses below -70.

Step 3: This step is the same setup as step 2. As PFE breaks above 90 we have a short entry. Closing it when it crosses below -70.

Recap:

Described above are 4 different examples with many different trades. Both trend and reversal trades. The PFE value is an indicator that can be used by traders in many different ways and Prometheus encourages traders to use their own discretion along with tools and not follow indicators blindly.

Options:

Users can control the input for the lookback of the indicator. The default is 9.

The smoothing factor for the EMA is also changeable, default is 5.

Users have options to display lines at -50, -25, 25, and 50.

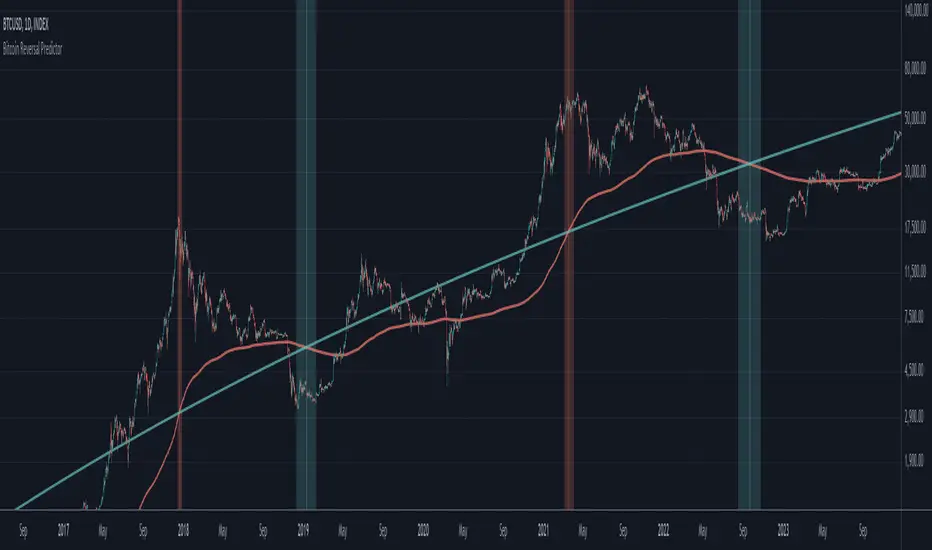

Intelle_city - World Cycle - Ath & Atl - Logarithmic - Strategy.Overview

Indicators: Strategy !

INTELLECT_city - World Cycle - ATH & ATL - Timeframe 1D and 1W - Logarithmic - Strategy - The Pi Cycle Top and Bottom Oscillator is an adaptation of the original Pi Cycle Top chart. It compares the 111-Day Moving Average circle and the 2 * 350-Day Moving Average circle of Bitcoin’s Price. These two moving averages were selected as 350 / 111 = 3.153; An approximation of the important mathematical number Pi.

When the 111-Day Moving Average circle reaches the 2 * 350-Day Moving Average circle, it indicates that the market is becoming overheated. That is because the mid time frame momentum reference of the 111-Day Moving Average has caught up with the long timeframe momentum reference of the 2 * 350-Day Moving Average.

Historically this has occurred within 3 days of the very top of each market cycle.

When the 111 Day Moving Average circle falls back beneath the 2 * 350 Day Moving Average circle, it indicates that the market momentum of that cycle is significantly cooling down. The oscillator drops down into the lower green band shown where the 111 Day Moving Average is moving at a 75% discount relative to the 2 * 350 Day Moving Average.

Historically, this has highlighted broad areas of bear market lows.

IMPORTANT: You need to set a LOGARITHMIC graph. (The function is located at the bottom right of the screen)

IMPORTANT: The INTELLECT_city indicator is made for a buy-sell strategy; there is also a signal indicator from INTELLECT_city

IMPORTANT: The Chart shows all cycles, both buying and selling.

IMPORTANT: Suitable timeframes are 1 daily (recommended) and 1 weekly

-----------------------------

Описание на русском:

-----------------------------

Обзор индикатора

INTELLECT_city - World Cycle - ATH & ATL - Timeframe 1D and 1W - Logarithmic - Strategy - Логарифмический - Сигнал - Осциллятор вершины и основания цикла Пи представляет собой адаптацию оригинального графика вершины цикла Пи. Он сравнивает круг 111-дневной скользящей средней и круг 2 * 350-дневной скользящей средней цены Биткойна. Эти две скользящие средние были выбраны как 350/111 = 3,153; Приближение важного математического числа Пи.

Когда круг 111-дневной скользящей средней достигает круга 2 * 350-дневной скользящей средней, это указывает на то, что рынок перегревается. Это происходит потому, что опорный моментум среднего временного интервала 111-дневной скользящей средней догнал опорный момент импульса длинного таймфрейма 2 * 350-дневной скользящей средней.

Исторически это происходило в течение трех дней после вершины каждого рыночного цикла.

Когда круг 111-дневной скользящей средней опускается ниже круга 2 * 350-дневной скользящей средней, это указывает на то, что рыночный импульс этого цикла значительно снижается. Осциллятор опускается в нижнюю зеленую полосу, показанную там, где 111-дневная скользящая средняя движется со скидкой 75% относительно 2 * 350-дневной скользящей средней.

Исторически это высветило широкие области минимумов медвежьего рынка.

ВАЖНО: Выставлять нужно ЛОГАРИФМИЧЕСКИЙ график. (Находиться функция с правой нижней части экрана)

ВАЖНО: Индикатор INTELLECT_city сделан для стратегии покупок продаж, есть также и сигнальный от INTELLECT_сity

ВАЖНО: На Графике видны все циклы, как на покупку так и на продажу.

ВАЖНО: Подходящие таймфреймы 1 дневной (рекомендовано) и 1 недельный

-----------------------------

Beschreibung - Deutsch

-----------------------------

Indikatorübersicht

INTELLECT_city – Weltzyklus – ATH & ATL – Zeitrahmen 1T und 1W – Logarithmisch – Strategy – Der Pi-Zyklus-Top- und Bottom-Oszillator ist eine Anpassung des ursprünglichen Pi-Zyklus-Top-Diagramms. Er vergleicht den 111-Tage-Gleitenden-Durchschnittskreis und den 2 * 350-Tage-Gleitenden-Durchschnittskreis des Bitcoin-Preises. Diese beiden gleitenden Durchschnitte wurden als 350 / 111 = 3,153 ausgewählt; eine Annäherung an die wichtige mathematische Zahl Pi.

Wenn der 111-Tage-Gleitenden-Durchschnittskreis den 2 * 350-Tage-Gleitenden-Durchschnittskreis erreicht, deutet dies darauf hin, dass der Markt überhitzt. Das liegt daran, dass der Momentum-Referenzwert des 111-Tage-Gleitenden-Durchschnitts im mittleren Zeitrahmen den Momentum-Referenzwert des 2 * 350-Tage-Gleitenden-Durchschnitts im langen Zeitrahmen eingeholt hat.

Historisch gesehen geschah dies innerhalb von 3 Tagen nach dem Höhepunkt jedes Marktzyklus.

Wenn der Kreis des 111-Tage-Durchschnitts wieder unter den Kreis des 2 x 350-Tage-Durchschnitts fällt, deutet dies darauf hin, dass die Marktdynamik dieses Zyklus deutlich nachlässt. Der Oszillator fällt in das untere grüne Band, in dem der 111-Tage-Durchschnitt mit einem Abschlag von 75 % gegenüber dem 2 x 350-Tage-Durchschnitt verläuft.

Historisch hat dies breite Bereiche mit Tiefstständen in der Baisse hervorgehoben.

WICHTIG: Sie müssen ein logarithmisches Diagramm festlegen. (Die Funktion befindet sich unten rechts auf dem Bildschirm)

WICHTIG: Der INTELLECT_city-Indikator ist für eine Kauf-Verkaufs-Strategie konzipiert; es gibt auch einen Signalindikator von INTELLECT_city

WICHTIG: Das Diagramm zeigt alle Zyklen, sowohl Kauf- als auch Verkaufszyklen.

WICHTIG: Geeignete Zeitrahmen sind 1 täglich (empfohlen) und 1 wöchentlich

intellect_city - World Cycle - Ath & Atl - Logarithmic - Signal.Indicator Overview

INTELLECT_city - World Cycle - ATH & ATL - Timeframe 1D and 1W - Logarithmic - Signal - The Pi Cycle Top and Bottom Oscillator is an adaptation of the original Pi Cycle Top chart. It compares the 111-Day Moving Average circle and the 2 * 350-Day Moving Average circle of Bitcoin’s Price. These two moving averages were selected as 350 / 111 = 3.153; An approximation of the important mathematical number Pi.

When the 111-Day Moving Average circle reaches the 2 * 350-Day Moving Average circle, it indicates that the market is becoming overheated. That is because the mid time frame momentum reference of the 111-Day Moving Average has caught up with the long timeframe momentum reference of the 2 * 350-Day Moving Average.

Historically this has occurred within 3 days of the very top of each market cycle.

When the 111 Day Moving Average circle falls back beneath the 2 * 350 Day Moving Average circle, it indicates that the market momentum of that cycle is significantly cooling down. The oscillator drops down into the lower green band shown where the 111 Day Moving Average is moving at a 75% discount relative to the 2 * 350 Day Moving Average.

Historically, this has highlighted broad areas of bear market lows.

IMPORTANT: You need to set a LOGARITHMIC graph. (The function is located at the bottom right of the screen)

IMPORTANT: The INTELLECT_city indicator is made for signal purchases of sales, there is also a strategic one from INTELLECT_city

IMPORTANT: The Chart shows all cycles, both buying and selling.

IMPORTANT: Suitable timeframes are 1 daily (recommended) and 1 weekly

-----------------------------

Описание на русском:

-----------------------------

Обзор индикатора

INTELLECT_city - World Cycle - ATH & ATL - Timeframe 1D and 1W - Logarithmic - Signal - Логарифмический - Сигнал - Осциллятор вершины и основания цикла Пи представляет собой адаптацию оригинального графика вершины цикла Пи. Он сравнивает круг 111-дневной скользящей средней и круг 2 * 350-дневной скользящей средней цены Биткойна. Эти две скользящие средние были выбраны как 350/111 = 3,153; Приближение важного математического числа Пи.

Когда круг 111-дневной скользящей средней достигает круга 2 * 350-дневной скользящей средней, это указывает на то, что рынок перегревается. Это происходит потому, что опорный моментум среднего временного интервала 111-дневной скользящей средней догнал опорный момент импульса длинного таймфрейма 2 * 350-дневной скользящей средней.

Исторически это происходило в течение трех дней после вершины каждого рыночного цикла.

Когда круг 111-дневной скользящей средней опускается ниже круга 2 * 350-дневной скользящей средней, это указывает на то, что рыночный импульс этого цикла значительно снижается. Осциллятор опускается в нижнюю зеленую полосу, показанную там, где 111-дневная скользящая средняя движется со скидкой 75% относительно 2 * 350-дневной скользящей средней.

Исторически это высветило широкие области минимумов медвежьего рынка.

ВАЖНО: Выставлять нужно ЛОГАРИФМИЧЕСКИЙ график. (Находиться функция с правой нижней части экрана)

ВАЖНО: Индикатор INTELLECT_city сделан для сигнальных покупок продаж, есть также и стратегический от INTELLECT_сity

ВАЖНО: На Графике видны все циклы, как на покупку так и на продажу.

ВАЖНО: Подходящие таймфреймы 1 дневной (рекомендовано) и 1 недельный

-----------------------------

Beschreibung - Deutsch

-----------------------------

Indikatorübersicht

INTELLECT_city – Weltzyklus – ATH & ATL – Zeitrahmen 1T und 1W – Logarithmisch – Signal – Der Pi-Zyklus-Top- und Bottom-Oszillator ist eine Anpassung des ursprünglichen Pi-Zyklus-Top-Diagramms. Er vergleicht den 111-Tage-Gleitenden-Durchschnittskreis und den 2 * 350-Tage-Gleitenden-Durchschnittskreis des Bitcoin-Preises. Diese beiden gleitenden Durchschnitte wurden als 350 / 111 = 3,153 ausgewählt; eine Annäherung an die wichtige mathematische Zahl Pi.

Wenn der 111-Tage-Gleitenden-Durchschnittskreis den 2 * 350-Tage-Gleitenden-Durchschnittskreis erreicht, deutet dies darauf hin, dass der Markt überhitzt. Das liegt daran, dass der Momentum-Referenzwert des 111-Tage-Gleitenden-Durchschnitts im mittleren Zeitrahmen den Momentum-Referenzwert des 2 * 350-Tage-Gleitenden-Durchschnitts im langen Zeitrahmen eingeholt hat.

Historisch gesehen geschah dies innerhalb von 3 Tagen nach dem Höhepunkt jedes Marktzyklus.

Wenn der Kreis des 111-Tage-Durchschnitts wieder unter den Kreis des 2 x 350-Tage-Durchschnitts fällt, deutet dies darauf hin, dass die Marktdynamik dieses Zyklus deutlich nachlässt. Der Oszillator fällt in das untere grüne Band, in dem der 111-Tage-Durchschnitt mit einem Abschlag von 75 % gegenüber dem 2 x 350-Tage-Durchschnitt verläuft.

Historisch hat dies breite Bereiche mit Tiefstständen in der Baisse hervorgehoben.

WICHTIG: Sie müssen ein logarithmisches Diagramm festlegen. (Die Funktion befindet sich unten rechts auf dem Bildschirm)

WICHTIG: Der INTELLECT_city-Indikator dient zur Signalisierung von Käufen oder Verkäufen, es gibt auch einen strategischen Indikator von INTELLECT_city

WICHTIG: Das Diagramm zeigt alle Zyklen, sowohl Kauf- als auch Verkaufszyklen.

WICHTIG: Geeignete Zeitrahmen sind 1 täglich (empfohlen) und 1 wöchentlich

Vector2Library "Vector2"

Representation of two dimensional vectors or points.

This structure is used to represent positions in two dimensional space or vectors,

for example in spacial coordinates in 2D space.

~~~

references:

docs.unity3d.com

gist.github.com

github.com

gist.github.com

gist.github.com

gist.github.com

~~~

new(x, y)

Create a new Vector2 object.

Parameters:

x : float . The x value of the vector, default=0.

y : float . The y value of the vector, default=0.

Returns: Vector2. Vector2 object.

-> usage:

`unitx = Vector2.new(1.0) , plot(unitx.x)`

from(value)

Assigns value to a new vector `x,y` elements.

Parameters:

value : float, x and y value of the vector.

Returns: Vector2. Vector2 object.

-> usage:

`one = Vector2.from(1.0), plot(one.x)`

from(value, element_sep, open_par, close_par)

Assigns value to a new vector `x,y` elements.

Parameters:

value : string . The `x` and `y` value of the vector in a `x,y` or `(x,y)` format, spaces and parentesis will be removed automatically.

element_sep : string . Element separator character, default=`,`.

open_par : string . Open parentesis character, default=`(`.

close_par : string . Close parentesis character, default=`)`.

Returns: Vector2. Vector2 object.

-> usage:

`one = Vector2.from("1.0,2"), plot(one.x)`

copy(this)

Creates a deep copy of a vector.

Parameters:

this : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = Vector2.new(1.0) , b = a.copy() , plot(b.x)`

down()

Vector in the form `(0, -1)`.

Returns: Vector2. Vector2 object.

left()

Vector in the form `(-1, 0)`.

Returns: Vector2. Vector2 object.

right()

Vector in the form `(1, 0)`.

Returns: Vector2. Vector2 object.

up()

Vector in the form `(0, 1)`.

Returns: Vector2. Vector2 object.

one()

Vector in the form `(1, 1)`.

Returns: Vector2. Vector2 object.

zero()

Vector in the form `(0, 0)`.

Returns: Vector2. Vector2 object.

minus_one()

Vector in the form `(-1, -1)`.

Returns: Vector2. Vector2 object.

unit_x()

Vector in the form `(1, 0)`.

Returns: Vector2. Vector2 object.

unit_y()

Vector in the form `(0, 1)`.

Returns: Vector2. Vector2 object.

nan()

Vector in the form `(float(na), float(na))`.

Returns: Vector2. Vector2 object.

xy(this)

Return the values of `x` and `y` as a tuple.

Parameters:

this : Vector2 . Vector2 object.

Returns: .

-> usage:

`a = Vector2.new(1.0, 1.0) , = a.xy() , plot(ax)`

length_squared(this)

Length of vector `a` in the form. `a.x^2 + a.y^2`, for comparing vectors this is computationaly lighter.

Parameters:

this : Vector2 . Vector2 object.

Returns: float. Squared length of vector.

-> usage:

`a = Vector2.new(1.0, 1.0) , plot(a.length_squared())`

length(this)

Magnitude of vector `a` in the form. `sqrt(a.x^2 + a.y^2)`

Parameters:

this : Vector2 . Vector2 object.

Returns: float. Length of vector.

-> usage:

`a = Vector2.new(1.0, 1.0) , plot(a.length())`

normalize(a)

Vector normalized with a magnitude of 1, in the form. `a / length(a)`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = normalize(Vector2.new(3.0, 2.0)) , plot(a.y)`

isNA(this)

Checks if any of the components is `na`.

Parameters:

this : Vector2 . Vector2 object.

Returns: bool.

usage:

p = Vector2.new(1.0, na) , plot(isNA(p)?1:0)

add(a, b)

Adds vector `b` to `a`, in the form `(a.x + b.x, a.y + b.y)`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = one() , c = add(a, b) , plot(c.x)`

add(a, b)

Adds vector `b` to `a`, in the form `(a.x + b, a.y + b)`.

Parameters:

a : Vector2 . Vector2 object.

b : float . Value.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = 1.0 , c = add(a, b) , plot(c.x)`

add(a, b)

Adds vector `b` to `a`, in the form `(a + b.x, a + b.y)`.

Parameters:

a : float . Value.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = 1.0 , b = one() , c = add(a, b) , plot(c.x)`

subtract(a, b)

Subtract vector `b` from `a`, in the form `(a.x - b.x, a.y - b.y)`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = one() , c = subtract(a, b) , plot(c.x)`

subtract(a, b)

Subtract vector `b` from `a`, in the form `(a.x - b, a.y - b)`.

Parameters:

a : Vector2 . vector2 object.

b : float . Value.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = 1.0 , c = subtract(a, b) , plot(c.x)`

subtract(a, b)

Subtract vector `b` from `a`, in the form `(a - b.x, a - b.y)`.

Parameters:

a : float . value.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = 1.0 , b = one() , c = subtract(a, b) , plot(c.x)`

multiply(a, b)

Multiply vector `a` with `b`, in the form `(a.x * b.x, a.y * b.y)`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = one() , c = multiply(a, b) , plot(c.x)`

multiply(a, b)

Multiply vector `a` with `b`, in the form `(a.x * b, a.y * b)`.

Parameters:

a : Vector2 . Vector2 object.

b : float . Value.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = 1.0 , c = multiply(a, b) , plot(c.x)`

multiply(a, b)

Multiply vector `a` with `b`, in the form `(a * b.x, a * b.y)`.

Parameters:

a : float . Value.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = 1.0 , b = one() , c = multiply(a, b) , plot(c.x)`

divide(a, b)

Divide vector `a` with `b`, in the form `(a.x / b.x, a.y / b.y)`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = from(2.0) , c = divide(a, b) , plot(c.x)`

divide(a, b)

Divide vector `a` with value `b`, in the form `(a.x / b, a.y / b)`.

Parameters:

a : Vector2 . Vector2 object.

b : float . Value.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = 2.0 , c = divide(a, b) , plot(c.x)`

divide(a, b)

Divide value `a` with vector `b`, in the form `(a / b.x, a / b.y)`.

Parameters:

a : float . Value.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = 3.0 , b = from(2.0) , c = divide(a, b) , plot(c.x)`

negate(a)

Negative of vector `a`, in the form `(-a.x, -a.y)`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = a.negate , plot(b.x)`

pow(a, b)

Raise vector `a` with exponent vector `b`, in the form `(a.x ^ b.x, a.y ^ b.y)`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = from(2.0) , c = pow(a, b) , plot(c.x)`

pow(a, b)

Raise vector `a` with value `b`, in the form `(a.x ^ b, a.y ^ b)`.

Parameters:

a : Vector2 . Vector2 object.

b : float . Value.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = 2.0 , c = pow(a, b) , plot(c.x)`

pow(a, b)

Raise value `a` with vector `b`, in the form `(a ^ b.x, a ^ b.y)`.

Parameters:

a : float . Value.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = 3.0 , b = from(2.0) , c = pow(a, b) , plot(c.x)`

sqrt(a)

Square root of the elements in a vector.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = sqrt(a) , plot(b.x)`

abs(a)

Absolute properties of the vector.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(-3.0) , b = abs(a) , plot(b.x)`

min(a)

Lowest element of a vector.

Parameters:

a : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = min(a) , plot(b)`

max(a)

Highest element of a vector.

Parameters:

a : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = max(a) , plot(b)`

vmax(a, b)

Highest elements of two vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 2.0) , b = new(2.0, 3.0) , c = vmax(a, b) , plot(c.x)`

vmax(a, b, c)

Highest elements of three vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

c : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 2.0) , b = new(2.0, 3.0) , c = new(1.5, 4.5) , d = vmax(a, b, c) , plot(d.x)`

vmin(a, b)

Lowest elements of two vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 2.0) , b = new(2.0, 3.0) , c = vmin(a, b) , plot(c.x)`

vmin(a, b, c)

Lowest elements of three vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

c : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 2.0) , b = new(2.0, 3.0) , c = new(1.5, 4.5) , d = vmin(a, b, c) , plot(d.x)`

perp(a)

Perpendicular Vector of `a`, in the form `(a.y, -a.x)`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = perp(a) , plot(b.x)`

floor(a)

Compute the floor of vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = floor(a) , plot(b.x)`

ceil(a)

Ceils vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = ceil(a) , plot(b.x)`

ceil(a, digits)

Ceils vector `a`.

Parameters:

a : Vector2 . Vector2 object.

digits : int . Digits to use as ceiling.

Returns: Vector2. Vector2 object.

round(a)

Round of vector elements.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = round(a) , plot(b.x)`

round(a, precision)

Round of vector elements.

Parameters:

a : Vector2 . Vector2 object.

precision : int . Number of digits to round vector "a" elements.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(0.123456, 1.234567) , b = round(a, 2) , plot(b.x)`

fractional(a)

Compute the fractional part of the elements from vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.123456, 1.23456) , b = fractional(a) , plot(b.x)`

dot_product(a, b)

dot_product product of 2 vectors, in the form `a.x * b.x + a.y * b.y.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = dot_product(a, b) , plot(c)`

cross_product(a, b)

cross product of 2 vectors, in the form `a.x * b.y - a.y * b.x`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = cross_product(a, b) , plot(c)`

equals(a, b)

Compares two vectors

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: bool. Representing the equality.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = equals(a, b) ? 1 : 0 , plot(c)`

sin(a)

Compute the sine of argument vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = sin(a) , plot(b.x)`

cos(a)

Compute the cosine of argument vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = cos(a) , plot(b.x)`

tan(a)

Compute the tangent of argument vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = tan(a) , plot(b.x)`

atan2(x, y)

Approximation to atan2 calculation, arc tangent of `y/x` in the range (-pi,pi) radians.

Parameters:

x : float . The x value of the vector.

y : float . The y value of the vector.

Returns: float. Value with angle in radians. (negative if quadrante 3 or 4)

-> usage:

`a = new(3.0, 1.5) , b = atan2(a.x, a.y) , plot(b)`

atan2(a)

Approximation to atan2 calculation, arc tangent of `y/x` in the range (-pi,pi) radians.

Parameters:

a : Vector2 . Vector2 object.

Returns: float, value with angle in radians. (negative if quadrante 3 or 4)

-> usage:

`a = new(3.0, 1.5) , b = atan2(a) , plot(b)`

distance(a, b)

Distance between vector `a` and `b`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = distance(a, b) , plot(c)`

rescale(a, length)

Rescale a vector to a new magnitude.

Parameters:

a : Vector2 . Vector2 object.

length : float . Magnitude.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = 2.0 , c = rescale(a, b) , plot(c.x)`

rotate(a, radians)

Rotates vector by a angle.

Parameters:

a : Vector2 . Vector2 object.

radians : float . Angle value in radians.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = 2.0 , c = rotate(a, b) , plot(c.x)`

rotate_degree(a, degree)

Rotates vector by a angle.

Parameters:

a : Vector2 . Vector2 object.

degree : float . Angle value in degrees.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = 45.0 , c = rotate_degree(a, b) , plot(c.x)`

rotate_around(this, center, angle)

Rotates vector `target` around `origin` by angle value.

Parameters:

this

center : Vector2 . Vector2 object.

angle : float . Angle value in degrees.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = rotate_around(a, b, 45.0) , plot(c.x)`

perpendicular_distance(a, b, c)

Distance from point `a` to line between `b` and `c`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

c : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(1.5, 2.6) , b = from(1.0) , c = from(3.0) , d = perpendicular_distance(a, b, c) , plot(d.x)`

project(a, axis)

Project a vector onto another.

Parameters:

a : Vector2 . Vector2 object.

axis : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = project(a, b) , plot(c.x)`

projectN(a, axis)

Project a vector onto a vector of unit length.

Parameters:

a : Vector2 . Vector2 object.

axis : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = projectN(a, b) , plot(c.x)`

reflect(a, axis)

Reflect a vector on another.

Parameters:

a : Vector2 . Vector2 object.

axis

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = reflect(a, b) , plot(c.x)`

reflectN(a, axis)

Reflect a vector to a arbitrary axis.

Parameters:

a : Vector2 . Vector2 object.

axis

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = reflectN(a, b) , plot(c.x)`

angle(a)

Angle in radians of a vector.

Parameters:

a : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = angle(a) , plot(b)`

angle_unsigned(a, b)

unsigned degree angle between 0 and +180 by given two vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = angle_unsigned(a, b) , plot(c)`

angle_signed(a, b)

Signed degree angle between -180 and +180 by given two vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = angle_signed(a, b) , plot(c)`

angle_360(a, b)

Degree angle between 0 and 360 by given two vectors

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = angle_360(a, b) , plot(c)`

clamp(a, min, max)

Restricts a vector between a min and max value.

Parameters:

a : Vector2 . Vector2 object.

min

max

Returns: Vector2. Vector2 object.

-> usage: