Blockunity Excess Index (BEI)Identify excess zones resulting in market reversals by visualizing price deviations from an average.

The Excess Index (BEI) is designed to identify excess zones resulting in reversals, based on price deviations from a moving average. This moving average is fully customizable (type, period to be taken into account, etc.). This indicator also multiplies the moving average with a configurable coefficient, to give dynamic support and resistance levels. Finally, the BEI also provides reversal signals to alert you to any risk of trend change, on any asset.

The Idea

The goal is to provide the community with a visual and customizable tool for analyzing large price deviations from an average.

How to Use

Very simple to use, this indicator plots colored zones according to the price's deviation from the moving average. Moving average extensions also provide dynamic support and resistance. Finally, signals alert you to potential reversal points.

Elements

The Moving Average

The Moving Average, which defaults to a gray line over 200 periods, serves as a stable reference point. It is accompanied by an Index, whose color varies from yellow to orange to red, offering an overview of market conditions.

Extensions

These dynamic lines can be used to determine effective supports and resistances.

Signals

Green and red triangles serve as clear indicators for buy and sell signals.

Settings

Mainly, the type of moving average is configurable. The default is an SMA.

A Simple Moving Average (SMA) calculates the average of a selected range of prices by the number of periods in that range.

But you can also, for example, switch the mode to EMA.

The Exponential Moving Average (EMA) is a moving average that places a greater weight and significance on the most recent data points:

You also have WMA.

A Weighted Moving Average (WMA) gives more weight on recent data and less on past data:

And finally, the possibility of having a PCMA.

PCMA takes into account the highest and lowest points in the lookback period and divides this by two to obtain an average:

You can change other parameters such as lookback periods, as well as the coefficient used to define extension lines.

You can refer to the tooltips directly in the indicator parameters.

For those who prefer a minimalist display, you can activate a "Bar Color" in the settings (You must also uncheck "Borders" and "Wick" in your Chart Settings), and deactivate all other elements as you wish:

Finally, you can customize all the different colors, as well as the parameters of the table that indicates the Index value and the asset trend.

How it Works

The Index is calculated using the following method:

abs_distance = math.abs(close - base_ma)

bei = (abs_distance - ta.lowest(abs_distance, lookback_norm)) / (ta.highest(abs_distance, lookback_norm) - ta.lowest(abs_distance, lookback_norm)) * 100

Signals are triggered according to the following conditions:

A Long (buy) signal is triggered when the Index falls below 100, when the closing price is lower than 5 periods ago, and when the price is under the moving average.

A Short (sell) signal is triggered when the Index falls below 100, when the closing price is greater than 5 periods ago, and when the price is above the moving average.

"摩根纳斯达克100基金风险大吗" için komut dosyalarını ara

Margin/Leverage CalculationMargin

This library calculates margin liquidation prices and quantities for long and short positions in your strategies.

Usage example

// ############################################################

// # INVESTMENT SETTINGS / INPUT

// ############################################################

// Get the investment capital from the properties tab of the strategy settings.

investment_capital = strategy.initial_capital

// Get the leverage from the properties tab of the strategy settings.

// The leverage is calculated from the order size for example: (300% = x3 leverage)

investment_leverage = margin.leverage()

// The maintainance rate and amount.

investment_leverage_maintenance_rate = input.float(title='Maintanance Rate (%)', defval=default_investment_leverage_maintenance_rate, minval=0, maxval=100, step=0.1, tooltip=tt_investment_leverage_maintenance_rate, group='MARGIN') / 100

investment_leverage_maintenance_amount = input.float(title='Maintanance Amount (%)', defval=default_investment_leverage_maintenance_amount, minval=0, maxval=100, step=0.1, tooltip=tt_investment_leverage_maintenance_amount, group='MARGIN')

// ############################################################

// # LIQUIDATION PRICES

// ############################################################

leverage_liquidation_price_long = 0.0

leverage_liquidation_price_long := na(leverage_liquidation_price_long ) ? na : leverage_liquidation_price_long

leverage_liquidation_price_short = 0.0

leverage_liquidation_price_short := na(leverage_liquidation_price_short ) ? na : leverage_liquidation_price_short

leverage_liquidation_price_long := margin.liquidation_price_long(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

leverage_liquidation_price_short := margin.liquidation_price_short(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

Get the qty for margin long or short position.

margin.qty_long(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

margin.qty_short(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

Get the price and qty for margin long or short position.

= margin.qty_long(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

= margin.qty_short(investment_capital, strategy.position_avg_price, investment_leverage, investment_leverage_maintenance_rate, investment_leverage_maintenance_amount)

Fear & Greed Index (Zeiierman)█ Overview

The Fear & Greed Index is an indicator that provides a comprehensive view of market sentiment. By analyzing various market factors such as market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility, and safe haven demand, the Index can depict the overall emotions driving market behavior, categorizing them into two main sentiments: Fear and Greed.

Fear: Indicates a market scenario where investors are scared, possibly leading to a sell-off or a stagnant market. In such conditions, the indicator helps in identifying potential buying opportunities as assets may be undervalued.

Greed: Represents a state where investors are overly confident and buying aggressively, which can lead to inflated asset prices. The indicator in such cases can signal overbought conditions, advising caution or potential short opportunities.

█ How It Works

The Fear & Greed Index is an aggregate of seven distinct indicators, each gauging a specific dimension of stock market activity. These indicators include market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility, and safe haven demand. The Index assesses the deviation of each individual indicator from its average, in relation to its typical fluctuations. In compiling the final score, which ranges from 0 to 100, the Index assigns equal weight to each indicator. A score of 100 denotes the highest level of Greed, while a score of 0 represents the utmost level of fear.

S&P 500's Momentum: The Index monitors the S&P 500's position relative to its 125-day moving average. Positive momentum (price above the average) signals growing confidence among investors (Greed), while negative momentum (price below the average) indicates rising fear.

Stock Price Strength: By comparing the number of stocks hitting 52-week highs to those at 52-week lows on the NYSE, the Index gauges market breadth. An extreme number of highs indicates Greed, whereas an extreme number of lows suggests Fear.

Stock Price Breadth (Market Volume): Using the McClellan Volume Summation Index, which considers the volume of advancing versus declining stocks, the Index assesses whether the market is broadly participating in a trend, or if a smaller subset of stocks is driving it.

Put and Call Options: The put/call ratio helps gauge investor sentiment. A rising ratio, particularly above 1, indicates increasing fear, as more investors are buying puts to protect against a decline. A falling ratio suggests growing confidence.

Market Volatility (VIX): The VIX measures expected market volatility. Higher values generally indicate Fear, while lower values point to Greed. The Fear & Greed Index compares the VIX to its 50-day moving average to understand its trend.

Safe Haven Demand: The performance of stocks versus bonds over a 20-day period helps understand where investors are putting their money. Bonds outperforming stocks is a sign of Fear, while the opposite suggests Greed.

Junk Bond Demand: By comparing the yields on junk bonds to safer investment-grade bonds, the Index gauges risk appetite. A narrower yield spread suggests Greed (investors are taking more risk), while a wider spread indicates Fear.

The Fear & Greed Index combines these components, scales, and averages them to produce a single value between 0 (Extreme Fear) and 100 (Extreme Greed).

█ How to Use

The Fear & Greed Index serves as a tool to evaluate the prevailing sentiments in the market. Investors, often driven by emotions, can react impulsively, and sentiment indicators like the Fear & Greed Index aim to highlight these emotional states, helping investors recognize personal biases that might impact their investment choices. When integrated with fundamental analysis and additional analytical instruments, the Index becomes a valuable resource for understanding and interpreting market moods and tendencies.

The Fear & Greed Index operates on the principle that excessive fear can result in stocks trading well below their intrinsic values,

while uncontrolled Greed can push prices above what they should be.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

[blackcat] L3 Inverted VixFix Indicator with RSI ScalingThis pine script that creates a custom indicator called the Inverted VixFix Indicator with RSI Scaling. This indicator combines two well-known technical indicators - the VixFix and the RSI - to create a more comprehensive view of market conditions.

The VixFix is a technical indicator that helps identify market trends and volatility. It is based on the highest close of the past 22 bars and the lowest low of the same period. The VixFix is calculated as 100 times the difference between the highest close and the current low divided by the highest close. The indicator is inverted, meaning that high values indicate low volatility and low values indicate high volatility.

The RSI (Relative Strength Index) is a momentum indicator that measures the strength of price action in a given period. It is calculated based on the closing prices of the selected asset. The RSI is scaled to a range between 0 and 100, with values above 70 indicating overbought conditions and values below 30 indicating oversold conditions.

The Inverted VixFix Indicator with RSI Scaling combines these two indicators to give a more comprehensive view of market conditions. The RSI is first scaled to a range between 0 and 100 using the RSI Length, RSI Overbought, and RSI Oversold inputs. The Inverted VixFix is then scaled to the same range as the RSI using the RSI Overbought and RSI Oversold inputs. The two indicators are then combined to create the Inverted VixFix Indicator with RSI Scaling.

To smooth out the RSI, the script also uses the ALMA (Arnaud Legoux Moving Average) function. This function is a type of moving average that uses a variable smoothing factor to give more weight to recent price action. In this script, the ALMA is applied to the scaled RSI with a length of 3, a offset of 0.58, and a sigma of 6.

To help visualize the indicator, the script also creates visual elements such as threshold lines and fills. The Bull Threshold line is drawn at the RSI Overbought level and the Bear Threshold line is drawn at the RSI Oversold level. A fill is then created between these two lines using the color purple and opacity set to 70%.

Overall, the Inverted VixFix Indicator with RSI Scaling is a useful tool for traders looking for a more comprehensive view of market conditions. By combining the VixFix and RSI indicators, this script provides a more nuanced view of market trends and volatility.

Median of Means Estimator Median of Means (MoM) is a measure of central tendency like mean (average) and median. However, it could be a better and robust estimator of central tendency when the data is not normal, asymmetric, have fat tails (like stock price data) and have outliers. The MoM can be used as a robust trend following tool and in other derived indicators.

Median of means (MoM) is calculated as follows, the MoM estimator shuffles the "n" data points and then splits them into k groups of m data points (n= k*m). It then computes the Arithmetic Mean of each group (k). Finally, it calculate the median over the resulting k Arithmetic Means. This technique diminishes the effect that outliers have on the final estimation by splitting the data and only considering the median of the resulting sub-estimations. This preserves the overall trend despite the data shuffle.

Below is an example to illustrate the advantages of MoM

Set A Set B Set C

3 4 4

3 4 4

3 5 5

3 5 5

4 5 5

4 5 5

5 5 5

5 5 5

6 6 8

6 6 8

7 7 10

7 7 15

8 8 40

9 9 50

10 100 100

Median 5 5 5

Mean 5.5 12.1 17.9

MoM 5.7 6.0 17.3

For all three sets the median is the same, though set A and B are the same except for one outlier in set B (100) it skews the mean but the median is resilient. However, in set C the group has several high values despite that the median is not responsive and still give 5 as the central tendency of the group, but the median of means is a value of 17.3 which is very close to the group mean 17.9. In all three cases (set A, B and C) the MoM provides a better snapshot of the central tendency of the group. Note: The MoM is dependent on the way we split the data initially and the value might slightly vary when the randomization is done sevral time and the resulting value can give the confidence interval of the MoM estimator.

Laguerre RSI - non repaintingIt seems that the traditional Laguerre* functions repaint due to the gamma parameter.

That goes even for the editorial pick here.

But one could use calculation period instead of "gamma" parameter. This gives us a non-repainting Laguerre RSI fit for scalping trends.

At first glance, I haven't seen anyone do this with a pine script, but I could be wrong because it's not a big deal.

So here is a variation of Laguerre RSI, without repainting. It's a little bit more insensitive, but this is not of great importance, since only the extreme values are used for confirmation.

( * Laguerre RSI is based on John EHLERS' Laguerre Filter to avoid the noise of RSI.)

And if you implement this indicator into a strategy (like I do) I can give you a trick.

Traditionaly the condition is at follows:

LaRSI = cd == 0 ? 100 : cu / (cu + cd)

(this is the final part of the indicator before the plotting)

LongLaguerre= LaRSIupb

It's fine for the short (ot exit long), but for the long is better to make a swich between the CD and CU parameters, as follows:

LaRSI1 = cd == 0 ? 100 : cu / (cu + cd)

LaRSI2 = cu == 0 ? 100 : cu / (cu + cd)

LongLaguerre= LaRSI2upb

[blackcat] L1 Larry Williams VixFix IndicatorLevel : L1

Larry Williams, had this idea to create a synthetic VIX for more than just the main stock indices. Check out the formula for Williams VixFix:

```

VIX Fix Formula = (Highest(Close, 22) – Low) / (Highest(Close, 22)) * 100

```

What does this even mean? In normal person terms, here's what it's all about:

1. Find the highest close over the last 22 days and subtract today's low (or the current bar).

2. Divide that by the highest close of the past 22 days.

3. Multiply the result by 100 to "normalize" the indicator.

Why 22 days, you ask? That's how long the normal month of trading days is.

So, you see, the formula is pretty chill. It's just a way to measure the price volatility of the last 22 trading days. It's a bit of a lagging indicator, but it gets the job done.

Here my version of this scriptcreates a custom technical indicator called "L1 Larry Williams VixFix" that measures the distance between the highest high and the lowest low of a security's price over a specified period.

The user can adjust the period length and source price used in the VixFix calculation. The period length is set to 22 by default, but can be modified by the user with the "Length" input parameter. The source price is set to "close" by default, meaning it will use the closing price of each bar to calculate the VixFix. However, the user can also choose a different type of price data, such as open, high, or low.

The VixFix is calculated as a percentage of the difference between the highest close and the lowest low over the specified period. This percentage is then multiplied by 100 to create a more readable value.

Finally, the code plots the VixFix line on the chart with a yellow color and a thickness of 2. This allows the user to easily visualize the VixFix value and incorporate it into their trading decisions.

Overall, this script provides a powerful tool for technical analysis that can help traders identify potential trend changes and market reversals.

Fib TSIFib TSI = Fibonacci True Strength Index

The Fib TSI indicator uses Fibonacci numbers input for the True Strength Index moving averages. Then it is converted into a stochastic 0-100 scale.

The Fibonacci sequence is the series of numbers where each number is the sum of the two preceding numbers. 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610...

TSI uses moving averages of the underlying momentum of a financial instrument.

Stochastic is calculated by a formula of high and low over a length of time on a scale of 0-100.

How to use Fib TSI:

100 = overbought

0 = oversold

Rising = bullish

Falling = bearish

crossover 50 = bullish

crossunder 50 = bearish

The default input settings are:

2 = Stoch D smoothing

3 = TSI signal

TSI uses 2 moving averages compared with each other.

5 = TSI fastest

TSI uses 2 moving averages compared with each other.

Default value is 3/5.

color = white

8 = TSI fast

TSI uses 2 moving averages compared with each other.

Default value is 5/8.

color = blue

13 = TSI mid

TSI uses 2 moving averages compared with each other.

Default value is 8/13.

color = orange

21 = TSI slow

TSI uses 2 moving averages compared with each other.

Default value is 13/21.

color = purple

34 = TSI slowest

TSI uses 2 moving averages compared with each other.

Default value is 21/34.

color = yellow

55 = Stoch K length

All total / 5 = All TSI

color rising above 50 = bright green

color falling above 50 = mint green

color falling below 50 = bright red

color rising below 50 = pink

Up bullish reversal = green arrow up

bullish trend = green dots

Down bearish reversal = red arrow down

bearish trend = red dots

Horizontal lines:

100

75

50

25

0

2 different visual options example snapshot:

Short Term IndeXThe Short-Term Index (STIX) is a simple market indicator designed to assess short-term overbought or oversold conditions in the stock market. Leveraging a combination of advancing and declining issues, STIX provides valuable insights into market sentiment and potential reversals. To enhance its interpretability and reveal the underlying trend with greater clarity, STIX has been refined through a Heiken-Ashi transformation, ensuring a smoother representation of market dynamics.

Calculation and Methodology:

stix = ta.ema(adv / (adv + dec) * 100, len)

STIX is calculated by dividing the difference between the sum of advancing issues (ADV) by the total number of issues traded (ADV + DEC). This quotient is multiplied by 100 to express the result as a percentage. The STIX index ranges from 0 to 100, where extreme values indicate potential overbought (mainly above 60) or oversold (mainly below 40) market conditions.

Heiken-Ashi Transformation:

By applying a Heiken-Ashi transformation to STIX, the indicator gains improved visual clarity and noise reduction. This transformation enhances the ability to identify trend shifts and potential reversal points, making it an even more valuable tool for traders and investors.

Utility and Use Cases:

-The Short-Term Index (STIX) offers a range of practical applications-

1. Overbought/Oversold Conditions: STIX provides a clear indication of short-term overbought or oversold conditions, helping traders anticipate potential market reversals.

2. Reversal Points: STIX can help pinpoint potential reversal points in short-term market trends, providing traders with opportunities to enter or exit positions.

3. Trend Analysis: By observing STIX values over time, traders can assess the strength and sustainability of short-term trends, aiding in trend-following strategies.

The Short-Term Index (STIX), enhanced by its Heiken-Ashi transformation, equips traders and investors with a tool for assessing short-term market conditions, confirming price movements, and identifying potential reversal points. Its robust methodology and refined presentation contribute to a more comprehensive understanding of short-term market dynamics, enabling traders to make well-informed trading decisions.

See Also:

- Other Market Breadth Indicators-

Strategy - Relative Volume GainersStrategy - Relative Volume Gainers

Overview:

This trading strategy, called "Relative Volume Gainers," is designed for Long Entry opportunities in the stock market. The strategy aims to identify potential trading candidates based on specific technical conditions, including volume, price movements, and indicator alignments.

Strategy Rules:

The strategy is focused solely on Long Entry positions.

The volume for the current trading day must be greater than or equal to the volume of the previous day.

The percentage change in price must be greater than or equal to 2.5%.

The Last Traded Price (LTP) must be greater than or equal to the Exponential Moving Average (EMA) 200.

The Relative Volume for the current trading day (calculated over the last 30 days) must be greater than or equal to the Simple Moving Average (SMA) of Relative Volume over the same 30 days.

The current candle on the chart should be Green or Bullish, indicating positive price movement.

The price difference between bid and ask prices should be kept to a minimum.

It's recommended to also analyze market depth for better insights.

Strategy Requirements:

Add the Exponential Moving Average (EMA) 200 to your trading chart.

This strategy can be applied on charts of any timeframe.

For intraday trading, particularly for early entry, consider using a 1-minute timeframe.

It is advisable to create a screener to identify potential trades in real-time market conditions.

Risk Warning:

Stocks that meet the strategy criteria might exhibit high volatility and a high beta, making them inherently risky to trade. Exercise caution and adhere to predetermined risk management strategies.

Determine your trading quantity based on your entry price and stop loss in order to manage risk effectively.

Quantity Calculation Formula:

Quantity calculation is crucial to manage risk and position sizing. The following formulas can be used based on your trading scenario:

Quantity with Leverage:

Quantity = (((Using Capital / 100) * Risk Percent) / (Entry Price - Stop Loss)) * Leverage

Eg: Quantity = (((10000 / 100) * 0.2) / (405.5 - 398.5)) * 5

Quantity = 14

Risk = Rs.100 (Rs.100 is 1% of Rs.10000. So the risk is 1%, means we lose only Rs.100 when the SL is hit. If SL is increased the Quantity will get reduced to maintain a fixed risk of Rs.100)

Quantity without Leverage:

Quantity = (((Using Capital / 100) * Risk Percent) / (Entry Price - Stop Loss))

Note:

Always stay informed about market conditions and be prepared for potential rapid price movements when trading stocks that meet the strategy criteria. Strictly adhere to your predefined risk management strategy to safeguard your capital.

adaptive_mfi

█ Description

Money flow an indexed value-based price and volume for the specified input length (lookback period). In summary, a momentum indicator that attempt to measure the flow of money (identify buying/selling pressure) through the asset within a specified period of time. MFI will oscillate between 0 to 100, oftentimes comprehend the analysis with oversold (20) or overbought (80) level, and a divergence that spotted to signaling a further change in trend/direction. As similar to many other indicators that use length (commonly a fixed value) as an input parameter, can be optimized by applied an adaptive filter (Ehlers), to solve the measuring cycle period. In this indicator, the adaptive measure of dominant cycle as an input parameter for the lookback period/n, will be applied to the money flow index.

█ Money Flow Index

mfi = 100 - (100/(1 + money_flow_ratio))

where:

n = int(dominant_cycle)

money_flow_ratio = n positive raw_money_flow / n negative raw_money_flow

raw_money_flow = typical_price * volume

typical_price = hlc3

█ Feature

The indicator will have a specified default parameter of: hp_period = 48; source = ohlc4

Horizontal line indicates positive/negative money flow

MFI Color Scheme: Solid; Normalized

CNTLibraryLibrary "CNTLibrary"

Custom Functions To Help Code In Pinescript V5

Coded By Christian Nataliano

First Coded In 10/06/2023

Last Edited In 22/06/2023

Huge Shout Out To © ZenAndTheArtOfTrading and his ZenLibrary V5, Some Of The Custom Functions Were Heavily Inspired By Matt's Work & His Pine Script Mastery Course

Another Shout Out To The TradingView's Team Library ta V5

//====================================================================================================================================================

// Custom Indicator Functions

//====================================================================================================================================================

GetKAMA(KAMA_lenght, Fast_KAMA, Slow_KAMA)

Calculates An Adaptive Moving Average Based On Perry J Kaufman's Calculations

Parameters:

KAMA_lenght (int) : Is The KAMA Lenght

Fast_KAMA (int) : Is The KAMA's Fastes Moving Average

Slow_KAMA (int) : Is The KAMA's Slowest Moving Average

Returns: Float Of The KAMA's Current Calculations

GetMovingAverage(Source, Lenght, Type)

Get Custom Moving Averages Values

Parameters:

Source (float) : Of The Moving Average, Defval = close

Lenght (simple int) : Of The Moving Average, Defval = 50

Type (string) : Of The Moving Average, Defval = Exponential Moving Average

Returns: The Moving Average Calculation Based On Its Given Source, Lenght & Calculation Type (Please Call Function On Global Scope)

GetDecimals()

Calculates how many decimals are on the quote price of the current market © ZenAndTheArtOfTrading

Returns: The current decimal places on the market quote price

Truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places © ZenAndTheArtOfTrading

Parameters:

number (float)

decimalPlaces (simple float)

Returns: The given number truncated to the given decimalPlaces

ToWhole(number)

Converts pips into whole numbers © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

ToPips(number)

Converts whole numbers back into pips © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

GetPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period © ZenAndTheArtOfTrading

Parameters:

value1 (float)

value2 (float)

lookback (int)

BarsAboveMA(lookback, ma)

Counts how many candles are above the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are above the MA

BarsBelowMA(lookback, ma)

Counts how many candles are below the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are below the EMA

BarsCrossedMA(lookback, ma)

Counts how many times the EMA was crossed recently © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many times price recently crossed the EMA

GetPullbackBarCount(lookback, direction)

Counts how many green & red bars have printed recently (ie. pullback count) © ZenAndTheArtOfTrading

Parameters:

lookback (int)

direction (int)

Returns: The bar count of how many candles have retraced over the given lookback & direction

GetSwingHigh(Lookback, SwingType)

Check If Price Has Made A Recent Swing High

Parameters:

Lookback (int) : Is For The Swing High Lookback Period, Defval = 7

SwingType (int) : Is For The Swing High Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing High

GetSwingLow(Lookback, SwingType)

Check If Price Has Made A Recent Swing Low

Parameters:

Lookback (int) : Is For The Swing Low Lookback Period, Defval = 7

SwingType (int) : Is For The Swing Low Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing Low

//====================================================================================================================================================

// Custom Risk Management Functions

//====================================================================================================================================================

CalculateStopLossLevel(OrderType, Entry, StopLoss)

Calculate StopLoss Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLoss (float) : Is The Custom StopLoss Distance, Defval = 2x ATR Below Close

Returns: Float - The StopLoss Level In Actual Price As A

CalculateStopLossDistance(OrderType, Entry, StopLoss)

Calculate StopLoss Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

StopLoss (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The StopLoss Value In Pips

CalculateTakeProfitLevel(OrderType, Entry, StopLossDistance, RiskReward)

Calculate TakeProfit Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLossDistance (float)

RiskReward (float)

Returns: Float - The TakeProfit Level In Actual Price

CalculateTakeProfitDistance(OrderType, Entry, TakeProfit)

Get TakeProfit Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

TakeProfit (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The TakeProfit Value In Pips

CalculateConversionCurrency(AccountCurrency, SymbolCurrency, BaseCurrency)

Get The Conversion Currecny Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

AccountCurrency (simple string) : Is For The Account Currency Used

SymbolCurrency (simple string) : Is For The Current Symbol Currency (Front Symbol)

BaseCurrency (simple string) : Is For The Current Symbol Base Currency (Back Symbol)

Returns: Tuple Of A Bollean (Convert The Currency ?) And A String (Converted Currency)

CalculateConversionRate(ConvertCurrency, ConversionRate)

Get The Conversion Rate Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

ConvertCurrency (bool) : Is To Check If The Current Symbol Needs To Be Converted Or Not

ConversionRate (float) : Is The Quoted Price Of The Conversion Currency (Input The request.security Function Here)

Returns: Float Price Of Conversion Rate (If In The Same Currency Than Return Value Will Be 1.0)

LotSize(LotSizeSimple, Balance, Risk, SLDistance, ConversionRate)

Get Current Lot Size

Parameters:

LotSizeSimple (bool) : Is To Toggle Lot Sizing Calculation (Simple Is Good Enough For Stocks & Crypto, Whilst Complex Is For Forex)

Balance (float) : Is For The Current Account Balance To Calculate The Lot Sizing Based Off

Risk (float) : Is For The Current Risk Per Trade To Calculate The Lot Sizing Based Off

SLDistance (float) : Is The Current Position StopLoss Distance From Its Entry Price

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - Position Size In Units

ToLots(Units)

Converts Units To Lots

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots

ToUnits(Lots)

Converts Lots To Units

Parameters:

Lots (float) : Is For How Many Lots Need To Be Converted Into Units (Minimun 0.01 Units)

Returns: Int - Position Size In Units

ToLotsInUnits(Units)

Converts Units To Lots Than Back To Units

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots That Were Rounded To Units

ATRTrail(OrderType, SourceType, ATRPeriod, ATRMultiplyer, SwingLookback)

Calculate ATR Trailing Stop

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

SourceType (int) : Is To Determine Where To Calculate The ATR Trailing From, Defval = close

ATRPeriod (simple int) : Is To Change Its ATR Period, Defval = 20

ATRMultiplyer (float) : Is To Change Its ATR Trailing Distance, Defval = 1

SwingLookback (int) : Is To Change Its Swing HiLo Lookback (Only From Source Type 5), Defval = 7

Returns: Float - Number Of The Current ATR Trailing

DangerZone(WinRate, AvgRRR, Filter)

Calculate Danger Zone Of A Given Strategy

Parameters:

WinRate (float) : Is The Strategy WinRate

AvgRRR (float) : Is The Strategy Avg RRR

Filter (float) : Is The Minimum Profit It Needs To Be Out Of BE Zone, Defval = 3

Returns: Int - Value, 1 If Out Of Danger Zone, 0 If BE, -1 If In Danger Zone

IsQuestionableTrades(TradeTP, TradeSL)

Checks For Questionable Trades (Which Are Trades That Its TP & SL Level Got Hit At The Same Candle)

Parameters:

TradeTP (float) : Is The Trade In Question Take Profit Level

TradeSL (float) : Is The Trade In Question Stop Loss Level

Returns: Bool - True If The Last Trade Was A "Questionable Trade"

//====================================================================================================================================================

// Custom Strategy Functions

//====================================================================================================================================================

OpenLong(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Long Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Long"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Long Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

OpenShort(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Short Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Short"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Short Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

TP_SLExit(FromID, TPLevel, SLLevel, PercentageClose, Comment, CommentValue)

Exits Based On Predetermined TP & SL Levels

Parameters:

FromID (string) : Is The Trade ID That The TP & SL Levels Be Palced

TPLevel (float) : Is The Take Profit Level

SLLevel (float) : Is The StopLoss Level

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

CloseLong(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Long Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Long"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

CloseShort(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Short Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Short"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

BrokerCheck(Broker)

Checks Traded Broker With Current Loaded Chart Broker

Parameters:

Broker (string) : Is The Current Broker That Is Traded

Returns: Bool - True If Current Traded Broker Is Same As Loaded Chart Broker

OpenPC(LicenseID, OrderType, UseLimit, LimitPrice, SymbolPrefix, Symbol, SymbolSuffix, Risk, SL, TP, OrderComment, Spread)

Compiles Given Parameters Into An Alert String Format To Open Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Open

UseLimit (bool) : Is If We Want To Enter The Position At Exactly The Previous Closing Price

LimitPrice (float) : Is The Limit Price Of The Trade (Only For Pending Orders)

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Risk (float) : Is The Trade Risk Per Trade / Fixed Lot Sizing

SL (float) : Is The Trade SL In Price / In Pips

TP (float) : Is The Trade TP In Price / In Pips

OrderComment (string) : Is The Executed Trade Comment

Spread (float) : is The Maximum Spread For Execution

Returns: String - Pine Connector Order Syntax Alert Message

ClosePC(LicenseID, OrderType, SymbolPrefix, Symbol, SymbolSuffix)

Compiles Given Parameters Into An Alert String Format To Close Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Close

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Returns: String - Pine Connector Order Syntax Alert Message

//====================================================================================================================================================

// Custom Backtesting Calculation Functions

//====================================================================================================================================================

CalculatePNL(EntryPrice, ExitPrice, LotSize, ConversionRate)

Calculates Trade PNL Based On Entry, Eixt & Lot Size

Parameters:

EntryPrice (float) : Is The Trade Entry

ExitPrice (float) : Is The Trade Exit

LotSize (float) : Is The Trade Sizing

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - The Current Trade PNL

UpdateBalance(PrevBalance, PNL)

Updates The Previous Ginve Balance To The Next PNL

Parameters:

PrevBalance (float) : Is The Previous Balance To Be Updated

PNL (float) : Is The Current Trade PNL To Be Added

Returns: Float - The Current Updated PNL

CalculateSlpComm(PNL, MaxRate)

Calculates Random Slippage & Commisions Fees Based On The Parameters

Parameters:

PNL (float) : Is The Current Trade PNL

MaxRate (float) : Is The Upper Limit (In Percentage) Of The Randomized Fee

Returns: Float - A Percentage Fee Of The Current Trade PNL

UpdateDD(MaxBalance, Balance)

Calculates & Updates The DD Based On Its Given Parameters

Parameters:

MaxBalance (float) : Is The Maximum Balance Ever Recorded

Balance (float) : Is The Current Account Balance

Returns: Float - The Current Strategy DD

CalculateWR(TotalTrades, LongID, ShortID)

Calculate The Total, Long & Short Trades Win Rate

Parameters:

TotalTrades (int) : Are The Current Total Trades That The Strategy Has Taken

LongID (string) : Is The Order ID Of The Long Trades Of The Strategy

ShortID (string) : Is The Order ID Of The Short Trades Of The Strategy

Returns: Tuple Of Long WR%, Short WR%, Total WR%, Total Winning Trades, Total Losing Trades, Total Long Trades & Total Short Trades

CalculateAvgRRR(WinTrades, LossTrades)

Calculates The Overall Strategy Avg Risk Reward Ratio

Parameters:

WinTrades (int) : Are The Strategy Winning Trades

LossTrades (int) : Are The Strategy Losing Trades

Returns: Float - The Average RRR Values

CAGR(StartTime, StartPrice, EndTime, EndPrice)

Calculates The CAGR Over The Given Time Period © TradingView

Parameters:

StartTime (int) : Is The Starting Time Of The Calculation

StartPrice (float) : Is The Starting Price Of The Calculation

EndTime (int) : Is The Ending Time Of The Calculation

EndPrice (float) : Is The Ending Price Of The Calculation

Returns: Float - The CAGR Values

//====================================================================================================================================================

// Custom Plot Functions

//====================================================================================================================================================

EditLabels(LabelID, X1, Y1, Text, Color, TextColor, EditCondition, DeleteCondition)

Edit / Delete Labels

Parameters:

LabelID (label) : Is The ID Of The Selected Label

X1 (int) : Is The X1 Coordinate IN BARINDEX Xloc

Y1 (float) : Is The Y1 Coordinate IN PRICE Yloc

Text (string) : Is The Text Than Wants To Be Written In The Label

Color (color) : Is The Color Value Change Of The Label Text

TextColor (color)

EditCondition (int) : Is The Edit Condition of The Line (Setting Location / Color)

DeleteCondition (bool) : Is The Delete Condition Of The Line If Ture Deletes The Prev Itteration Of The Line

Returns: Void

EditLine(LineID, X1, Y1, X2, Y2, Color, EditCondition, DeleteCondition)

Edit / Delete Lines

Parameters:

LineID (line) : Is The ID Of The Selected Line

X1 (int) : Is The X1 Coordinate IN BARINDEX Xloc

Y1 (float) : Is The Y1 Coordinate IN PRICE Yloc

X2 (int) : Is The X2 Coordinate IN BARINDEX Xloc

Y2 (float) : Is The Y2 Coordinate IN PRICE Yloc

Color (color) : Is The Color Value Change Of The Line

EditCondition (int) : Is The Edit Condition of The Line (Setting Location / Color)

DeleteCondition (bool) : Is The Delete Condition Of The Line If Ture Deletes The Prev Itteration Of The Line

Returns: Void

//====================================================================================================================================================

// Custom Display Functions (Using Tables)

//====================================================================================================================================================

FillTable(TableID, Column, Row, Title, Value, BgColor, TextColor, ToolTip)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

Column (int) : Is The Current Column Of The Table That Wants To Be Edited

Row (int) : Is The Current Row Of The Table That Wants To Be Edited

Title (string) : Is The String Title Of The Current Cell Table

Value (string) : Is The String Value Of The Current Cell Table

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

ToolTip (string) : Is The ToolTip Of The Current Cell In The Table

Returns: Void

DisplayBTResults(TableID, BgColor, TextColor, StartingBalance, Balance, DollarReturn, TotalPips, MaxDD)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

StartingBalance (float) : Is The Account Starting Balance

Balance (float)

DollarReturn (float) : Is The Account Dollar Reture

TotalPips (float) : Is The Total Pips Gained / loss

MaxDD (float) : Is The Maximum Drawdown Over The Backtesting Period

Returns: Void

DisplayBTResultsV2(TableID, BgColor, TextColor, TotalWR, QTCount, LongWR, ShortWR, InitialCapital, CumProfit, CumFee, AvgRRR, MaxDD, CAGR, MeanDD)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

TotalWR (float) : Is The Strategy Total WR In %

QTCount (int) : Is The Strategy Questionable Trades Count

LongWR (float) : Is The Strategy Total WR In %

ShortWR (float) : Is The Strategy Total WR In %

InitialCapital (float) : Is The Strategy Initial Starting Capital

CumProfit (float) : Is The Strategy Ending Cumulative Profit

CumFee (float) : Is The Strategy Ending Cumulative Fee (Based On Randomized Fee Assumptions)

AvgRRR (float) : Is The Strategy Average Risk Reward Ratio

MaxDD (float) : Is The Strategy Maximum DrawDown In Its Backtesting Period

CAGR (float) : Is The Strategy Compounded Average GRowth In %

MeanDD (float) : Is The Strategy Mean / Average Drawdown In The Backtesting Period

Returns: Void

//====================================================================================================================================================

// Custom Pattern Detection Functions

//====================================================================================================================================================

BullFib(priceLow, priceHigh, fibRatio)

Calculates A Bullish Fibonacci Value (From Swing Low To High) © ZenAndTheArtOfTrading

Parameters:

priceLow (float)

priceHigh (float)

fibRatio (float)

Returns: The Fibonacci Value Of The Given Ratio Between The Two Price Points

BearFib(priceLow, priceHigh, fibRatio)

Calculates A Bearish Fibonacci Value (From Swing High To Low) © ZenAndTheArtOfTrading

Parameters:

priceLow (float)

priceHigh (float)

fibRatio (float)

Returns: The Fibonacci Value Of The Given Ratio Between The Two Price Points

GetBodySize()

Gets The Current Candle Body Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Body Size IN POINTS

GetTopWickSize()

Gets The Current Candle Top Wick Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Top Wick Size IN POINTS

GetBottomWickSize()

Gets The Current Candle Bottom Wick Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Bottom Wick Size IN POINTS

GetBodyPercent()

Gets The Current Candle Body Size As A Percentage Of Its Entire Size Including Its Wicks © ZenAndTheArtOfTrading

Returns: The Current Candle Body Size IN PERCENTAGE

GetTopWickPercent()

Gets The Current Top Wick Size As A Percentage Of Its Entire Body Size

Returns: Float - The Current Candle Top Wick Size IN PERCENTAGE

GetBottomWickPercent()

Gets The Current Bottom Wick Size As A Percentage Of Its Entire Bodu Size

Returns: Float - The Current Candle Bottom Size IN PERCENTAGE

BullishEC(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Engulfing Candle

Parameters:

Allowance (int) : To Give Flexibility Of Engulfing Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bullsih Engulfing Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bullish Engulfing Candle

BearishEC(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bearish Engulfing Candle

Parameters:

Allowance (int) : To Give Flexibility Of Engulfing Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bearish Engulfing Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing High, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bearish Engulfing Candle

Hammer(Fib, ColorMatch, NearSwings, SwingLookBack, ATRFilterCheck, ATRPeriod)

Checks If The Current Bar Is A Hammer Candle

Parameters:

Fib (float) : To Specify Which Fibonacci Ratio To Use When Determining The Hammer Candle, Defval = 0.382 Ratio

ColorMatch (bool) : To Filter Only Bullish Closed Hammer Candle Pattern, Defval = false

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

ATRFilterCheck (float) : To Filter Smaller Hammer Candles That Might Be Better Classified As A Doji Candle, Defval = 1

ATRPeriod (simple int) : To Change ATR Period Of The ATR Filter, Defval = 20

Returns: Bool - True If The Current Bar Matches The Requirements of a Hammer Candle

Star(Fib, ColorMatch, NearSwings, SwingLookBack, ATRFilterCheck, ATRPeriod)

Checks If The Current Bar Is A Hammer Candle

Parameters:

Fib (float) : To Specify Which Fibonacci Ratio To Use When Determining The Hammer Candle, Defval = 0.382 Ratio

ColorMatch (bool) : To Filter Only Bullish Closed Hammer Candle Pattern, Defval = false

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

ATRFilterCheck (float) : To Filter Smaller Hammer Candles That Might Be Better Classified As A Doji Candle, Defval = 1

ATRPeriod (simple int) : To Change ATR Period Of The ATR Filter, Defval = 20

Returns: Bool - True If The Current Bar Matches The Requirements of a Hammer Candle

Doji(MaxWickSize, MaxBodySize, DojiType, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Doji Candle

Parameters:

MaxWickSize (float) : To Specify The Maximum Lenght Of Its Upper & Lower Wick, Defval = 2

MaxBodySize (float) : To Specify The Maximum Lenght Of Its Candle Body IN PERCENT, Defval = 0.05

DojiType (int)

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing High / Low (Only In Dragonlyf / Gravestone Mode), Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High / Low (Only In Dragonlyf / Gravestone Mode), Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Doji Candle

BullishIB(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Harami Candle

Parameters:

Allowance (int) : To Give Flexibility Of Harami Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bullsih Harami Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bullish Harami Candle

BearishIB(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Harami Candle

Parameters:

Allowance (int) : To Give Flexibility Of Harami Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bearish Harami Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing High, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bearish Harami Candle

//====================================================================================================================================================

// Custom Time Functions

//====================================================================================================================================================

BarInSession(sess, useFilter)

Determines if the current price bar falls inside the specified session © ZenAndTheArtOfTrading

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls within the given time session

BarOutSession(sess, useFilter)

Determines if the current price bar falls outside the specified session © ZenAndTheArtOfTrading

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls outside the given time session

DateFilter(startTime, endTime)

Determines if this bar's time falls within date filter range © ZenAndTheArtOfTrading

Parameters:

startTime (int)

endTime (int)

Returns: A boolean - true if the current bar falls within the given dates

DayFilter(monday, tuesday, wednesday, thursday, friday, saturday, sunday)

Checks if the current bar's day is in the list of given days to analyze © ZenAndTheArtOfTrading

Parameters:

monday (bool)

tuesday (bool)

wednesday (bool)

thursday (bool)

friday (bool)

saturday (bool)

sunday (bool)

Returns: A boolean - true if the current bar's day is one of the given days

AUSSess()

Checks If The Current Australian Forex Session In Running

Returns: Bool - True If Currently The Australian Session Is Running

ASIASess()

Checks If The Current Asian Forex Session In Running

Returns: Bool - True If Currently The Asian Session Is Running

EURSess()

Checks If The Current European Forex Session In Running

Returns: Bool - True If Currently The European Session Is Running

USSess()

Checks If The Current US Forex Session In Running

Returns: Bool - True If Currently The US Session Is Running

UNIXToDate(Time, ConversionType, TimeZone)

Converts UNIX Time To Datetime

Parameters:

Time (int) : Is The UNIX Time Input

ConversionType (int) : Is The Datetime Output Format, Defval = DD-MM-YYYY

TimeZone (string) : Is To Convert The Outputed Datetime Into The Specified Time Zone, Defval = Exchange Time Zone

Returns: String - String Of Datetime

Fibonacci Levels on Any Indicator [By MUQWISHI]▋ INTRODUCTION :

A “Fibonacci Levels on Any Indicator” can be applied to any indicator to draw Fibonacci levels based on provided conditions of two price points to produce a sequence of horizontal line levels starting from 0% to 100% in addition to extension levels. The 0% level is measured as the start of retracement, while the 100% level is the beginning of the extension levels. This tool was developed to be easy to add to any indicator, and it could be valuable to some traders in terms of managing trades by setting targets and reducing risk in the trend direction.

_______________________

▋ USAGE:

➤ NEEDS TO IDENTIFY 4 ELEMENTS:

1. Starting Point. What’re the conditions / When will the drawing of the Fibonacci levels begin?

2. Ending Point. What’re the conditions / When will the drawing of the Fibonacci levels end?

3. High Point. What is the price for a 100% Fibonacci level (0% for the downside)?

4. Low Point. What is the price for a 0% Fibonacci level (100% for the downside)?

➤ STARTING & ENDING POINTS CONDITIONS:

Need to specify the condition when the drawing of Fibonacci levels starts and ends, and the indicator shows different prepared conditions.

New Phase: Import a value (plot) from an existing indicator, where its status changes from NaN to a real number.

Crosses Above/Below: Import a value(1) (plot) from an existing indicator, where it crosses above/below value(2).

Reversal Up/Down: Import a value(1) (plot) from an existing indicator, where it rises/decreases than the previous value(1).

First/Last Bar: Useful to draw stationary Fibonacci levels.

➤ UPPER & LOWER PIVOTS (0% & 100%):

Need to specify the two price points representing 0% & 100% Fibonacci levels to expose the sequence of Fibonacci lines.

Upper Pivot. By default, the ATR Upper Band. It’s possible to import a custom value from an existing indicator.

Lower Pivot. By default, the ATR Lower Band. It’s possible to import a custom value from an existing indicator.

➤ FIBONACCI STYLING OPTIONS:

Ability to customize line & label style, color, reverse, and hide/show levels.

_______________________

▋ IMPLEMENTATION:

Here are some examples of implementing the indicator.

Note: All presented examples below are for demonstration purposes, and they're not trading suggestions.

# Example 1: (Reversal Up/Down)

We want to implement Fibonacci levels on the Hull MA by mohamed982 . Our requirements are as follows:

Fibonacci levels start when the Hull MA reverses up.

Fibonacci levels end when the Hull MA reverses down.

Upper Pivot is the ATR Upper Band.

Lower Pivot is the ATR Lower Band.

After adding the required indicator (Hull MA), here’re the implementation and results

# Example 2: (Crosses Above/Below)

We want to implement Fibonacci Level on the Squeeze Momentum by LazyBear . Our requirements are as follows:

Fibonacci levels start when the Squeeze Momentum histogram crosses above 0.

Fibonacci levels end when the Squeeze Momentum histogram crosses below 0.

Upper Pivot is the Bollinger Upper Band.

Lower Pivot is the Bollinger Lower Band.

After adding the required indicators (Squeeze Momentum & Bollinger Band), here’re the implementation and results

# Example 3: (Crosses Above/Below)

We want to implement Fibonacci Level on the Crossing Moving Averages. Our requirements are as follows:

Fibonacci levels start when the 20-EMA crosses above 100-MA.

Fibonacci levels end when the 20-EMA crosses below 100-MA.

Upper Pivot is the ATR Upper Band.

Lower Pivot is the ATR Lower Band.

After adding the required indicators (20-EMA & 100-MA), here’re the implementation and results

# Example 4: (New Phase: When the previous value is NaN, and the current value is a real number.)

We want to implement Fibonacci Level on the Supertrend. Our requirements are as follows:

Fibonacci levels start when an up-Supertrend (green) line shows up.

Fibonacci levels end when a down-Supertrend (red) line shows up.

Upper Pivot is the down-Supertrend.

Lower Pivot is the up-Supertrend.

After adding the required indicator (Supertrend), here’re the implementation and results

# Example 5: (First/Last Bar)

We want to implement Fibonacci Level between two points, 330 & 300. Our requirements are as follows:

Fibonacci levels start at first bar on the chart.

Fibonacci levels end at last bar on the chart.

Upper Pivot is 330.

Lower Pivot is 300.

Here’re the implementation and results.

To customize the number of bars back (like 50 bars)

_______________________

▋ Final Comments:

The “Fibonacci Levels on Any Indicator” is made to apply on other indicators for planning Fibonacci Levels.

It can be implemented in different ways, along with presented examples.

This indicator does not work with plots that were developed by drawing classes.

Please let me know if you have any questions.

Thank you.

4H RangeThis script visualizes certain key values based on a 4-hour timeframe of the selected market on the chart. These values include the High, Mid, and Low price levels during each 4-hour period.

These levels can be helpful to identify inside range price action, chop, and consolidation. They can sometimes act as pivots and can be a great reference for potential entries and exits if price continues to hold the same range.

Here's a step-by-step overview of what this indicator does:

1. Inputs: At the beginning of the script, users are allowed to customize some inputs:

Choose the color of lines and labels.

Decide whether to show labels on the chart.

Choose the size of labels ("tiny", "small", "normal", or "large").

Choose whether to display price values in labels.

Set the number of bars to offset the labels to the right.

Set a threshold for the number of ticks that triggers a new calculation of high, mid, and low values.

* Tick settings may need to be increased on equity charts as one tick is usually equal to one cent.

For example, if you want to clear the range when there is a close one point/one dollar above or below the range high/low then on ES

that would be 4 ticks but one whole point on AAPL would be 100 ticks. 100 ticks on an equity chart may or may not be ideal due to

different % change of 100 ticks might be too excessive depending on the price per share.

So be aware that user preferred thresholds can vary greatly depending on which chart you're using.

2. Retrieving Price Data: The script retrieves the high, low, and closing price for every 4-hour period for the current market.

The script also calculates the mid-price of each 4-hour period (the average of the high and low prices).

3. Line Drawing: At the start of the script (first run), it draws three lines (high, mid, and low) at the levels corresponding to the high,

mid, and low prices. Users can also change transparency settings on historical lines to view them. Default setting for historical lines

is for them to be hidden.

4. Updating Lines and Labels: For each subsequent 4-hour period, the script checks whether the close price of the period has gone

beyond a certain threshold (set by user input) above the previous high or below the previous low. If it has, the script deletes the

previous lines and labels, draws new lines at the new high, mid, and low levels, and creates new labels (if the user has opted to

show labels).

5. Displaying Values in the Data Window: In addition to the visual representation on the chart, the script also plots the high, mid, and

low prices. These plotted values appear in the Data Window of TradingView, allowing users to see the exact price levels even when

they're not directly labeled on the chart.

6. Updating Lines and Labels Position: At the end of each period, the script moves the lines and labels (if they're shown) to the right,

keeping them aligned with the current period.

Please note: This script operates based on a 4-hour timeframe, regardless of the timeframe selected on the chart. If a shorter timeframe is selected on the chart, the lines and labels will appear to extend across multiple bars because they represent 4-hour price levels. If a longer timeframe is selected, the lines and labels may not accurately represent high, mid, and low levels within that longer timeframe.

Pure Morning 2.0 - Candlestick Pattern Doji StrategyThe new "Pure Morning 2.0 - Candlestick Pattern Doji Strategy" is a trend-following, intraday cryptocurrency trading system authored by devil_machine.

The system identifies Doji and Morning Doji Star candlestick formations above the EMA60 as entry points for long trades.

For best results we recommend to use on 15-minute, 30-minute, or 1-hour timeframes, and are ideal for high-volatility markets.

The strategy also utilizes a profit target or trailing stop for exits, with stop loss set at the lowest low of the last 100 candles. The strategy's configuration details, such as Doji tolerance, and exit configurations are adjustable.

In this new version 2.0, we've incorporated a new selectable filter. Since the stop loss is set at the lowest low, this filter ensures that this value isn't too far from the entry price, thereby optimizing the Risk-Reward ratio.

In the specific case of ALPINE, a 9% Take-Profit and and Stop-Loss at Lowest Low of the last 100 candles were set, with an activated trailing-stop percentage, Max Loss Filter is not active.

Name : Pure Morning 2.0 - Candlestick Pattern Doji Strategy

Author : @devil_machine

Category : Trend Follower based on candlestick patterns.

Operating mode : Spot or Futures (only long).

Trades duration : Intraday

Timeframe : 15m, 30m, 1H

Market : Crypto

Suggested usage : Short-term trading, when the market is in trend and it is showing high volatility .

Entry : When a Doji or Morning Doji Star formation occurs above the EMA60.

Exit : Profit target or Trailing stop, Stop loss on the lowest low of the last 100 candles.

Configuration :

- Doji Settings (tolerances) for Entry Condition

- Max Loss Filter (Lowest Low filter)

- Exit Long configuration

- Trailing stop

Backtesting :

⁃ Exchange: BINANCE

⁃ Pair: ALPINEUSDT

⁃ Timeframe: 30m

⁃ Fee: 0.075%

⁃ Slippage: 1

- Initial Capital: 10000 USDT

- Position sizing: 10% of Equity

- Start: 2022-02-28 (Out Of Sample from 2022-12-23)

- Bar magnifier: on

Disclaimer : Risk Management is crucial, so adjust stop loss to your comfort level. A tight stop loss can help minimise potential losses. Use at your own risk.

How you or we can improve? Source code is open so share your ideas!

Leave a comment and smash the boost button!

Thanks for your attention, happy to support the TradingView community.

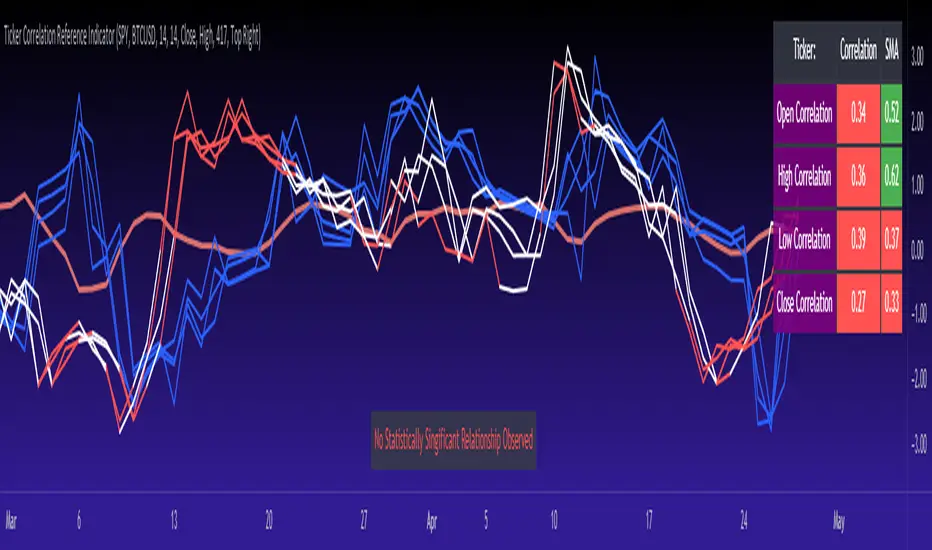

Ticker Correlation Reference IndicatorHello,

I am super excited to be releasing this Ticker Correlation assessment indicator. This is a big one so let us get right into it!

Inspiration:

The inspiration for this indicator came from a similar indicator by Balipour called the Correlation with P-Value and Confidence Interval. It’s a great indicator, you should check it out!

I used it quite a lot when looking for correlations; however, there were some limitations to this indicator’s functionality that I wanted. So I decided to make my own indicator that had the functionality I wanted. I have been using this for some time but decided to actual spruce it up a bit and make it user friendly so that I could share it publically. So let me get into what this indicator does and, most importantly, the expanded functionality of this indicator.

What it does:

This indicator determines the correlation between 2 separate tickers. The user selects the two tickers they wish to compare and it performs a correlation assessment over a defaulted 14 period length and displays the results. However, the indicator takes this much further. The complete functionality of this indicator includes the following:

1. Assesses the correlation of all 4 ticker variables (Open, High, Low and Close) over a user defined period of time (defaulted to 14);

2. Converts both tickers to a Z-Score in order to standardize the data and provide a side by side comparison;

3. Displays areas of high and low correlation between all 4 variables;

4. Looks back over the consistency of the relationship (is correlation consistent among the two tickers or infrequent?);

5. Displays the variance in the correlation (there may be a statistically significant relationship, but if there is a high variance, it means the relationship is unstable);

6. Permits manual conversion between prices; and

7. Determines the degree of statistical significance (be it stable, unstable or non-existent).

I will discuss each of these functions below.

Function 1: Assesses the correlation of all 4 variables.

The only other indicator that does this only determines the correlation of the close price. However, correlation between all 4 variables varies. The correlation between open prices, high prices, low prices and close prices varies in statistically significant ways. As such, this indicator plots the correlation of all 4 ticker variables and displays each correlation.

Assessing this matters because sometimes a stock may not have the same magnitude in highs and lows as another stock (one stock may be more bullish, i.e. attain higher highs in comparison to another stock). Close price is helpful but does not pain the full picture. As such, the indicator displays the correlation relationship between all 4 variables (image below):

Function 2: Converts both tickers to Z-Score

Z-Score is a way of standardizing data. It simply measures how far a stock is trading in relation to its mean. As such, it is a way to express both tickers on a level playing field. Z-Score was also chosen because the Z-Score Values (0 – 4) also provide an appropriate scale to plot correlation lines (which range from 0 to 1).

The primary ticker (Ticker 1) is plotted in blue, the secondary comparison ticker (Ticker 2) is plotted in a colour changing format (which will be discussed below). See the image below:

Function 3: Displays areas of high and low correlation

While Ticker 1 is plotted in a static blue, Ticker 2 (the comparison ticker) is plotted in a dynamic, colour changing format. It will display areas of high correlation (i.e. areas with a P value greater than or equal to 0.9 or less than and equal to -0.9) in green, areas of moderate correlation in white. Areas of low correlation (between 0.4 and 0 or -0.4 and 0) are in red. (see image below):

Function 4: Checks consistency of relationship

While at the time of assessing a stock there very well maybe a high correlation, whether that correlation is consistent or not is the question. The indicator employs the use of the SMA function to plot the average correlation over a defined period of time. If the correlation is consistently high, the SMA should be within an area of statistical significance (over 0.5 or under -0.5). If the relationship is inconsistent, the SMA will read a lower value than the actual correlation.

You can see an example of this when you compare ETH to Tezos in the image below:

You can see that the correlation between ETH and Tezo’s on the high level seems to be inconsistent. While the current correlation is significant, the SMA is showing that the average correlation between the highs is actually less than 0.5.

The indicator also tells the user narratively the degree of consistency in the statistical relationship. This will be discussed later.

Function 5: Displays the variance

When it comes to correlation, variance is important. Variance simply means the distance between the highest and lowest value. The indicator assess the variance. A high degree of variance (i.e. a number surpassing 0.5 or greater) generally means the consistency and stability of the relationship is in issue. If there is a high variance, it means that the two tickers, while seemingly significantly correlated, tend to deviate from each other quite extensively.

The indicator will tell the user the variance in the narrative bar at the bottom of the chart (see image below):

Function 6: Permits manual conversion of price

One thing that I frequently want and like to do is convert prices between tickers. If I am looking at SPX and I want to calculate a price on SPY, I want to be able to do that quickly. This indicator permits you to do that by employing a regression based formula to convert Ticker 1 to Ticker 2.

The user can actually input which variable they would like to convert, whether they want to convert Ticker 1 Close to Ticker 2 Close, or Ticker 1 High to Ticker 2 High, or low or open.

To do this, open the settings and click “Permit Manual Conversion”. This will then take the current Ticker 1 Close price and convert it to Ticker 2 based on the regression calculations.

If you want to know what a specific price on Ticker 1 is on Ticker 2, simply click the “Allow Manual Price Input” variable and type in the price of Ticker 1 you want to know on Ticker 2. It will perform the calculation for you and will also list the standard error of the calculation.

Below is an example of calculating a SPY price using SPX data:

Above, the indicator was asked to convert an SPX price of 4,100 to a SPY price. The result was 408.83 with a standard error of 4.31, meaning we can expect 4,100 to fall within 408.83 +/- 4.31 on SPY.

Function 7: Determines the degree of statistical significance

The indicator will provide the user with a narrative output of the degree of statistical significance. The indicator looks beyond simply what the correlation is at the time of the assessment. It uses the SMA and the highest and lowest function to make an assessment of the stability of the statistical relationship and then indicates this to the user. Below is an example of IWM compared to SPY: