ninu3q merged//@version=6

indicator("Ultimate Trend + Momentum + Volume Pro (merged)", overlay=true,

max_boxes_count=700, max_lines_count=300, max_labels_count=300)

// -----------------------------

// 1) EMA Trend + VWAP Layer (combined)

// -----------------------------

ema200 = ta.ema(close, 200)

ema50 = ta.ema(close, 50)

vwap = ta.vwap

ema200Plot = plot(ema200, "EMA 200", color=color.red, linewidth=2, style=plot.style_line)

ema50Plot = plot(ema50, "EMA 50", color=color.teal, linewidth=1, style=plot.style_line)

vwapPlot = plot(vwap, "VWAP", color=color.orange, linewidth=1, style=plot.style_line)

// Trick: combine them into a group so TradingView counts less

plot(na) // placeholder, only one is really required

// -----------------------------

// 2) UT Bot Alerts

// -----------------------------

utAtrPeriod = input.int(10, "UT ATR Period")

utAtrMultiplier = input.float(2.0, "UT ATR Multiplier")

utAtr = ta.atr(utAtrPeriod)

utUpper = close + utAtrMultiplier * utAtr

utLower = close - utAtrMultiplier * utAtr

utBuy = ta.crossover(close, utUpper)

utSell = ta.crossunder(close, utLower)

plotshape(utBuy, "UT Buy", location=location.belowbar, color=color.green, style=shape.labelup, text="BUY")

plotshape(utSell, "UT Sell", location=location.abovebar, color=color.red, style=shape.labeldown, text="SELL")

// -----------------------------

// 3) Volume Profile (anchored to last N bars)

// -----------------------------

barsBack = input.int(150, "Bars Back", minval=1, maxval=5000)

cols = input.int(35, "Columns", minval=5, maxval=200)

vaPct = input.float(70.0, "Value Area %", minval=40.0, maxval=99.0)

histWidth = input.int(24, "Histogram Width (bars)", minval=6, maxval=200)

direction = input.string("Into chart (left)", "Histogram Direction", options= )

// Block/line styles

blockFillColor = input.color(#B0B0B0, "Volume Block Fill Color")

blockFillOpacity = input.int(70, "Volume Block Fill Opacity %", minval=0, maxval=100)

blockBorderColor = input.color(#000000, "Volume Block Border Color")

blockBorderOpacity = input.int(0, "Volume Block Border Opacity %", minval=0, maxval=100)

showPOC = input.bool(true, "Show POC Line")

pocColor = input.color(#FF0000, "POC Color")

pocWidth = input.int(2, "POC Width", minval=1, maxval=6)

showVA = input.bool(false, "Show VAH/VAL Lines")

vaColor = input.color(#FFA500, "VA Color")

vaWidth = input.int(1, "VA Width", minval=1, maxval=6)

showVWAP = input.bool(false, "Show AVWAP Line")

vwapColor = input.color(#0000FF, "AVWAP Color")

vwapWidth = input.int(1, "AVWAP Width", minval=1, maxval=6)

showLabels = input.bool(false, "Show Line Labels")

priceForBin = hlcc4

// Draw registries

var boxesArr = array.new_box()

var linesArr = array.new_line()

var labelsArr = array.new_label()

f_wipe() =>

while array.size(boxesArr) > 0

box.delete(array.pop(boxesArr))

while array.size(linesArr) > 0

line.delete(array.pop(linesArr))

while array.size(labelsArr) > 0

label.delete(array.pop(labelsArr))

if barstate.islast

f_wipe()

eff = math.min(barsBack, bar_index + 1)

if eff > 1

float pMin = na

float pMax = na

float pvSum = 0.0

float vSum = 0.0

for look = 0 to eff - 1

lo = low

hi = high

pMin := na(pMin) ? lo : math.min(pMin, lo)

pMax := na(pMax) ? hi : math.max(pMax, hi)

pvSum += priceForBin * volume

vSum += volume

anchoredVWAP = vSum > 0 ? pvSum / vSum : na

if not na(pMin) and not na(pMax) and pMax > pMin

step = (pMax - pMin) / cols

step := step == 0.0 ? syminfo.mintick : step

var vols = array.new_float()

var lows = array.new_float()

var highs = array.new_float()

array.clear(vols), array.clear(lows), array.clear(highs)

for i = 0 to cols - 1

array.push(vols, 0.0)

lo = pMin + i * step

hi = lo + step

array.push(lows, lo)

array.push(highs, hi)

for look = 0 to eff - 1

pr = priceForBin

vol = volume

idx = int(math.floor((pr - pMin) / step))

idx := idx < 0 ? 0 : idx > cols - 1 ? cols - 1 : idx

array.set(vols, idx, array.get(vols, idx) + vol)

pocIdx = 0

pocVol = 0.0

totalVol = 0.0

for i = 0 to cols - 1

v = array.get(vols, i)

totalVol += v

if v > pocVol

pocVol := v

pocIdx := i

targetVol = totalVol * (vaPct / 100.0)

left = pocIdx

right = pocIdx

cumVA = array.get(vols, pocIdx)

while cumVA < targetVol and (left > 0 or right < cols - 1)

vLeft = left > 0 ? array.get(vols, left - 1) : -1.0

vRight = right < cols - 1 ? array.get(vols, right + 1) : -1.0

if vRight > vLeft

right += 1

cumVA += array.get(vols, right)

else if vLeft >= 0

left -= 1

cumVA += array.get(vols, left)

else

break

VAH = array.get(highs, right)

VAL = array.get(lows, left)

profileStart = bar_index - (eff - 1)

rightStart = bar_index + 1

rightEnd = bar_index + 1 + histWidth

intoChart = direction == "Into chart (left)"

for i = 0 to cols - 1

v = array.get(vols, i)

len = pocVol > 0 ? (v / pocVol) : 0.0

px = int(math.round(len * histWidth))

x1 = intoChart ? (rightEnd - px) : rightStart

x2 = intoChart ? rightEnd : (rightStart + px)

y1 = array.get(lows, i)

y2 = array.get(highs, i)

b = box.new(x1, y2, x2, y1, xloc=xloc.bar_index, border_color=color.new(blockBorderColor, blockBorderOpacity))

box.set_bgcolor(b, color.new(blockFillColor, 100 - blockFillOpacity))

array.push(boxesArr, b)

if showPOC

pocPrice = (array.get(lows, pocIdx) + array.get(highs, pocIdx)) / 2.0

lnPOC = line.new(profileStart, pocPrice, rightEnd, pocPrice, xloc=xloc.bar_index, extend=extend.right, color=pocColor, width=pocWidth)

array.push(linesArr, lnPOC)

if showLabels

lbPOC = label.new(rightEnd, pocPrice, "POC", xloc=xloc.bar_index, style=label.style_label_right, textcolor=color.white, color=pocColor)

array.push(labelsArr, lbPOC)

if showVA

lnVAL = line.new(profileStart, VAL, rightEnd, VAL, xloc=xloc.bar_index, extend=extend.right, color=vaColor, width=vaWidth)

lnVAH = line.new(profileStart, VAH, rightEnd, VAH, xloc=xloc.bar_index, extend=extend.right, color=vaColor, width=vaWidth)

array.push(linesArr, lnVAL)

array.push(linesArr, lnVAH)

if showLabels

lbVAH = label.new(rightEnd, VAH, "VAH", xloc=xloc.bar_index, style=label.style_label_right, textcolor=color.white, color=vaColor)

lbVAL = label.new(rightEnd, VAL, "VAL", xloc=xloc.bar_index, style=label.style_label_right, textcolor=color.white, color=vaColor)

array.push(labelsArr, lbVAH)

array.push(labelsArr, lbVAL)

if showVWAP and not na(anchoredVWAP)

lnVW = line.new(profileStart, anchoredVWAP, rightEnd, anchoredVWAP, xloc=xloc.bar_index, extend=extend.right, color=vwapColor, width=vwapWidth)

array.push(linesArr, lnVW)

if showLabels

lbVW = label.new(rightEnd, anchoredVWAP, "AVWAP", xloc=xloc.bar_index, style=label.style_label_right, textcolor=color.white, color=vwapColor)

array.push(labelsArr, lbVW)

// placeholder plot

plot(na)

"摩根纳斯达克100基金风险大吗" için komut dosyalarını ara

EMRVA//@version=5

indicator("EMRVA", overlay=true)

// === الإعدادات ===

emaLength = input.int(200, "EMA Length")

rsiLength = input.int(14, "RSI Length")

volLength = input.int(20, "Volume MA Length")

adxLength = input.int(14, "ADX Length")

adxFilter = input.int(20, "ADX Minimum Value") // فلتر الاتجاه

// === EMA200 ===

ema200 = ta.ema(close, emaLength)

plot(ema200, color=color.orange, linewidth=2, title="EMA 200")

// === MACD ===

macdLine = ta.ema(close, 12) - ta.ema(close, 26)

signalLine = ta.ema(macdLine, 9)

// === RSI ===

rsi = ta.rsi(close, rsiLength)

// === Volume Confirmation ===

volMA = ta.sma(volume, volLength)

volCond = volume > volMA

// === ADX Manual Calculation ===

upMove = high - high

downMove = low - low

plusDM = na(upMove) ? na : (upMove > downMove and upMove > 0 ? upMove : 0)

minusDM = na(downMove) ? na : (downMove > upMove and downMove > 0 ? downMove : 0)

tr = ta.rma(ta.tr, adxLength)

plusDI = 100 * ta.rma(plusDM, adxLength) / tr

minusDI = 100 * ta.rma(minusDM, adxLength) / tr

dx = 100 * math.abs(plusDI - minusDI) / (plusDI + minusDI)

adx = ta.rma(dx, adxLength)

adxCond = adx > adxFilter

// === شروط الدخول والخروج ===

longCond = close > ema200 and macdLine > signalLine and rsi > 50 and volCond and adxCond

shortCond = close < ema200 and macdLine < signalLine and rsi < 50 and volCond and adxCond

// === منطق الإشارة عند بداية الاتجاه فقط ===

var inLong = false

var inShort = false

buySignal = longCond and not inLong

sellSignal = shortCond and not inShort

if buySignal

inLong := true

inShort := false

if sellSignal

inShort := true

inLong := false

// === إشارات ثابتة ===

plotshape(buySignal, title="Buy Signal", location=location.belowbar,

color=color.green, style=shape.labelup, text="BUY")

plotshape(sellSignal, title="Sell Signal", location=location.abovebar,

color=color.red, style=shape.labeldown, text="SELL")

// === تنبيهات ===

alertcondition(buySignal, title="Buy Alert", message="📈 إشارة شراء مؤكدة مع فلتر ADX")

alertcondition(sellSignal, title="Sell Alert", message="📉 إشارة بيع مؤكدة مع فلتر ADX")

// === رسم ADX للتأكيد ===

plot(adx, title="ADX", color=color.blue)

hline(adxFilter, "ADX Filter", color=color.red)

Candle Suite PRO – Engulf + Pin + Regime Filters + Trigger//@version=5

indicator("Candle Suite PRO – Engulf + Pin + Regime Filters + Trigger", overlay=true, max_labels_count=500)

//===================== Inputs =====================

grpPtn = "Patterns"

useEngulf = input.bool(true, "Enable Engulfing", group=grpPtn)

usePin = input.bool(true, "Enable Pin Bar", group=grpPtn)

pinRatio = input.float(2.0, "PinBar shadow >= body ×", group=grpPtn, step=0.1, minval=1)

minBodyP = input.float(0.15, "Min Body% of Range (0~1)", group=grpPtn, step=0.01, minval=0, maxval=1)

coolBars = input.int(3, "Cooldown bars", group=grpPtn, minval=0)

grpReg = "Regime Filters"

useHTF = input.bool(true, "Use HTF EMA50 Filter", group=grpReg)

htfTF = input.timeframe("60", "HTF timeframe", group=grpReg) // 5m/15m → 60 권장

useADX = input.bool(true, "Use ADX Trend Filter", group=grpReg)

adxLen = input.int(14, "ADX Length", group=grpReg, minval=5)

adxMin = input.int(18, "ADX Min Threshold", group=grpReg, minval=5)

useVOL = input.bool(true, "Use Volume Filter (> SMA×k)",group=grpReg)

volMult = input.float(1.10, "k for Volume", group=grpReg, step=0.05)

emaPinchPc = input.float(0.15, "No-Trade if |EMA20-50| < %", group=grpReg, step=0.05)/100.0

maxDistATR = input.float(1.5, "No-Trade if |Close-EMA20| > ATR×", group=grpReg, step=0.1)

useVWAP = input.bool(true, "Require close above/below VWAP", group=grpReg)

//===================== Helpers ====================

ema20 = ta.ema(close, 20)

ema50 = ta.ema(close, 50)

atr14 = ta.atr(14)

vwap = ta.vwap(hlc3)

rng = high - low

body = math.abs(close - open)

upper = high - math.max(open, close)

lower = math.min(open, close) - low

bull = close > open

bear = close < open

bodyOK = rng > 0 ? (body / rng) >= minBodyP : false

//===================== Patterns ===================

prevOpen = open

prevClose = close

prevBull = prevClose > prevOpen

prevBear = prevClose < prevOpen

bullEngulf_raw = useEngulf and prevBear and bull and (open <= prevClose) and (close >= prevOpen) and bodyOK

bearEngulf_raw = useEngulf and prevBull and bear and (open >= prevClose) and (close <= prevOpen) and bodyOK

bullPin_raw = usePin and (lower >= pinRatio * body) and (upper <= body) and bodyOK // Hammer

bearPin_raw = usePin and (upper >= pinRatio * body) and (lower <= body) and bodyOK // Shooting Star

//================= Regime & No-trade ===============

// HTF trend (EMA50 on higher TF)

emaHTF50 = request.security(syminfo.tickerid, htfTF, ta.ema(close, 50))

htfLong = not useHTF or close > emaHTF50

htfShort = not useHTF or close < emaHTF50

// ADX (manual, version-safe)

len = adxLen

upMove = high - high

downMove = low - low

plusDM = (upMove > downMove and upMove > 0) ? upMove : 0.0

minusDM = (downMove > upMove and downMove > 0) ? downMove : 0.0

trur = ta.rma(ta.tr(true), len)

plusDI = 100 * ta.rma(plusDM, len) / trur

minusDI = 100 * ta.rma(minusDM, len) / trur

dx = 100 * math.abs(plusDI - minusDI) / math.max(plusDI + minusDI, 1e-10)

adxVal = ta.rma(dx, len)

trendOK = not useADX or adxVal >= adxMin

// Volume

volOK = not useVOL or (volume >= ta.sma(volume, 20) * volMult)

// Alignment & slope

slopeUp = ema20 > ema20

slopeDown = ema20 < ema20

alignLong = ema20 > ema50 and slopeUp

alignShort = ema20 < ema50 and slopeDown

// Chop / distance / VWAP

pinch = math.abs(ema20 - ema50) / close < emaPinchPc

tooFar = math.abs(close - ema20) / atr14 > maxDistATR

vwapOKL = not useVWAP or close > vwap

vwapOKS = not useVWAP or close < vwap

//================= Final Setups ====================

longSetup_raw = bullEngulf_raw or bullPin_raw

shortSetup_raw = bearEngulf_raw or bearPin_raw

longSetup = longSetup_raw and alignLong and htfLong and trendOK and volOK and not pinch and not tooFar and vwapOKL

shortSetup = shortSetup_raw and alignShort and htfShort and trendOK and volOK and not pinch and not tooFar and vwapOKS

// Trigger: 다음 봉이 전봉의 고/저 돌파 + 종가 확인

longTrig = longSetup and high > high and close > ema20

shortTrig = shortSetup and low < low and close < ema20

// Cooldown & final signals

var int lastLong = na

var int lastShort = na

canLong = na(lastLong) or (bar_index - lastLong > coolBars)

canShort = na(lastShort) or (bar_index - lastShort > coolBars)

finalLong = longTrig and canLong

finalShort = shortTrig and canShort

if finalLong

lastLong := bar_index

if finalShort

lastShort := bar_index

//==================== Plots ========================

plot(ema20, "EMA 20", color=color.new(color.orange, 0))

plot(ema50, "EMA 50", color=color.new(color.blue, 0))

plot(useVWAP ? vwap : na, "VWAP", color=color.new(color.purple, 0))

plotshape(finalLong, title="LONG ▶", style=shape.labelup, location=location.belowbar, text="Long▶", color=color.new(color.blue, 0), size=size.tiny)

plotshape(finalShort, title="SHORT ▶", style=shape.labeldown, location=location.abovebar, text="Short▶", color=color.new(color.red, 0), size=size.tiny)

// Alerts

alertcondition(finalLong, "LONG ▶", "Long trigger")

alertcondition(finalShort, "SHORT ▶", "Short trigger")

// 시각적 노트레이드 힌트

bgcolor(pinch ? color.new(color.gray, 92) : na)

Bollinger Bands Difference Score

Bollinger Bands Difference Score (TradingView – Pine Script v6)

The **Bollinger Bands Difference Score** is a volatility-based scoring system designed to help traders quickly assess whether a stock is in a **strong trend, neutral zone, or weak setup**. It transforms the raw **Bollinger Band Width (BB-Diff)** into a **normalized score (0–100)** and classifies conditions with intuitive thresholds.

---

### 🔹 What is Bollinger Bands Difference (BB-Diff)?

* **Bollinger Bands** are built from a moving average with upper and lower bands set by standard deviations.

* The **difference (or width)** between the bands reflects market volatility.

* A **high difference** = wide bands = strong volatility (breakout/trend).

* A **low difference** = narrow bands = low volatility (consolidation).

This indicator standardizes BB-Diff into a score and smooths it for cleaner signals.

---

### 🔹 Key Features

1. **BB-Diff Scoring System**

* Converts Bollinger Band width into a **0–100 normalized score**.

* Higher score → higher volatility/trend strength.

* Lower score → consolidation or weaker momentum.

2. **Signal Levels**

* **Strong Zone (≥ 70):** Indicates strong trend strength or expansion in volatility.

* **Neutral Zone (40–70):** Sideways or undecided price action.

* **Weak Zone (≤ 20):** Suggests very low volatility, potential upcoming squeeze.

3. **Score Smoothing**

* Applies a moving average to reduce noise.

* Helps avoid false signals during choppy markets.

4. **Visual Enhancements**

* Plots the score as a line (0–100 scale).

* Adds horizontal reference lines for **Strong**, **Neutral**, and **Weak** levels.

* Background colors automatically highlight **bullish strength (green)** or **weakness (red)**.

---

### 🔹 How to Use

* **Trend Confirmation:**

Look for scores **above 70** → suggests trend continuation or volatility breakout.

* **Consolidation Watch:**

Scores in the **20 or below** zone may precede volatility squeezes → breakout setups.

* **Neutral Zone:**

Scores between **40–70** suggest sideways price action; avoid aggressive trades.

* **Combine with Price Action:**

Use with support/resistance, candlestick patterns, or momentum indicators for confirmation.

---

### 🔹 Best Practices

* Great as a **volatility filter** before entries.

* Use in combination with **RSI, MACD, or OBV** for directional bias.

* Works well for **breakout trading** (when score rises from low levels).

* Monitor on multiple timeframes for alignment.

---

✅ **In summary:** The **Bollinger Bands Difference Score** is a simple yet powerful tool that quantifies volatility strength into an actionable score, making it easier to spot strong trends, consolidation phases, and potential breakout opportunities.

Extremum Range MA Crossover Strategy1. Principle of Work & Strategy Logic ⚙️📈

Main idea: The strategy tries to catch the moment of a breakout from a price consolidation range (flat) and the start of a new trend. It combines two key elements:

Moving Average (MA) 📉: Acts as a dynamic support/resistance level and trend filter.

Range Extremes (Range High/Low) 🔺🔻: Define the borders of the recent price channel or consolidation.

The strategy does not attempt to catch absolute tops and bottoms. Instead, it enters an already formed move after the breakout, expecting continuation.

Type: Trend-following, momentum-based.

Timeframes: Works on different TFs (H1, H4, D), but best suited for H4 and higher, where breakouts are more meaningful.

2. Justification of Indicators & Settings ⚙️

A. Moving Average (MA) 📊

Why used: Core of the strategy. It smooths price fluctuations and helps define the trend. The price (via extremes) must cross the MA → signals a potential trend shift or strengthening.

Parameters:

maLength = 20: Default length (≈ one trading month, 20-21 days). Good balance between sensitivity & smoothing.

Lower TF → reduce (10–14).

Higher TF → increase (50).

maSource: Defines price source (default = Close). Alternatives (HL2, HLC3) → smoother, less noisy MA.

maType: Default = EMA (Exponential MA).

Why EMA? Faster reaction to recent price changes vs SMA → useful for breakout strategies.

Other options:

SMA 🟦 – classic, slowest.

WMA 🟨 – weights recent data stronger.

HMA 🟩 – near-zero lag, but “nervous,” more false signals.

DEMA/TEMA 🟧 – even faster & more sensitive than EMA.

VWMA 🔊 – volume-weighted.

ZLEMA ⏱ – reduced lag.

👉 Choice = tradeoff between speed of reaction & false signals.

B. Range Extremes (Previous High/Low) 📏

Why used: Define borders of recent trading range.

prevHigh = local resistance.

prevLow = local support.

Break of these levels on close = trigger.

Parameters:

lookbackPeriod = 5: Searches for highest high / lowest low of last 5 candles. Very recent range.

Higher value (10–20) → wider, stronger ranges but rarer signals.

3. Entry & Exit Rules 🎯

Long signals (BUY) 🟢📈

Condition (longCondition): Previous Low crosses MA from below upwards.

→ Price bounced from the bottom & strong enough to push range border above MA.

Execution: Auto-close short (if any) → open long.

Short signals (SELL) 🔴📉

Condition (shortCondition): Previous High crosses MA from above downwards.

→ Price rejected from the top, upper border failed above MA.

Execution: Auto-close long (if any) → open short.

Exit conditions 🚪

Exit Long (exitLongCondition): Close below prevLow.

→ Uptrend likely ended, range shifts down.

Exit Short (exitShortCondition): Close above prevHigh.

→ Downtrend likely ended, range shifts up.

⚠️ Important: Exit = only on candle close beyond extremes (not just wick).

4. Trading Settings ⚒️

overlay = true → indicators shown on chart.

initial_capital = 10000 💵.

default_qty_type = strategy.cash, default_qty_value = 100 → trades fixed $100 per order (not lots). Can switch to % of equity.

commission_type = strategy.commission.percent, commission_value = 0.1 → default broker fee = 0.1%. Adjust for your broker!

slippage = 3 → slippage = 3 ticks. Adjust to asset liquidity.

currency = USD.

margin_long = 100, margin_short = 100 → no leverage (100% margin).

5. Visualization on Chart 📊

The strategy draws 3 lines:

🔵 MA line (thickness 2).

🔴 Previous High (last N candles).

🟢 Previous Low (last N candles).

Also: entry/exit arrows & equity curve shown in backtest.

Disclaimer ⚠️📌

Risk Warning: This description & code are for educational purposes only. Not financial advice. Trading (Forex, Stocks, Crypto) carries high risk and may lead to full capital loss. You trade at your own risk.

Testing: Always backtest & demo test first. Past results ≠ future profits.

Responsibility: Author of this strategy & description is not responsible for your trading decisions or losses.

IV Rank (tasty-style) — VIXFix / HV ProxyIV Rank (tasty-style) — VIXFix / HV Proxy

Overview

This indicator replicates tastytrade’s IV Rank calculation—but built entirely inside TradingView.

Because TradingView does not expose live option-chain implied volatility, the script lets you choose between two widely used price-based IV proxies:

VIXFix (Williams VIX Fix): a fast-reacting volatility estimate derived from price extremes.

HV(30): 30-day annualized historical volatility of daily log returns.

The goal is to approximate the “rich vs. cheap” option volatility environment that traders use to decide whether to sell or buy premium.

Formula

IV Rank answers the question: Where is current implied volatility relative to its own 1-year range?

𝐼

𝑉

𝑅

=

𝐼

𝑉

𝑐

𝑢

𝑟

𝑟

𝑒

𝑛

𝑡

−

𝐼

𝑉

1

𝑦

𝐿

𝑜

𝑤

𝐼

𝑉

1

𝑦

𝐻

𝑖

𝑔

ℎ

−

𝐼

𝑉

1

𝑦

𝐿

𝑜

𝑤

×

100

IVR=

IV

1yHigh

−IV

1yLow

IV

current

−IV

1yLow

×100

IVcurrent: Current value of the chosen IV proxy.

IV1yHigh/Low: Highest and lowest proxy values over the user-defined lookback (default 252 trading days ≈ 1 year).

IVR = 0 → Current IV equals its 1-year low

IVR = 100 → Current IV equals its 1-year high

IVR ≈ 50 → Current IV sits mid-range

How to Use

High IV Rank (≥50–60%)

Options are relatively expensive → short-premium strategies (credit spreads, iron condors, straddles) may be more attractive.

Low IV Rank (≤20%)

Options are relatively cheap → long-premium strategies (debit spreads, calendars, diagonals) may offer better risk/reward.

Combine with your own analysis, liquidity checks, and risk management.

Inputs & Customization

IV Source: Choose “VIXFix” or “HV(30)” as the volatility proxy.

IVR Lookback: Rolling window for 1-year high/low (default 252 trading days).

VIXFix Parameters: Length and stdev multiplier to fine-tune sensitivity.

Info Label: Optional on-chart label displays current IV proxy, 1-year high/low, and IV Rank.

Alerts: Optional alerts when IVR crosses 50, falls below 20, or rises above 80.

Notes & Limitations

This indicator does not pull real option-chain IV.

It provides a close structural analogue to tastytrade’s IV Rank using price-derived proxies for markets where options data is not directly available.

For live option IV, use broker platforms or third-party data feeds alongside this script.

Tags: IV Rank, Implied Volatility, Tastytrade, VIXFix, Historical Volatility, Options, Premium Selling, Debit Spreads, Market Volatility

3-Level DCA Buy Strategy🎯 3-Level DCA Buy Strategy - Smart Dollar Cost Averaging

Professional DCA strategy that systematically accumulates positions during market dips. Enhanced with daily trend analysis for intelligent accumulation.

🚀 Key Features

- 3-Level Buying System: Automatic purchases at 5%, 10%, 15% drops from cycle highs

- Daily Trend Analysis: 1-day timeframe trend confirmation

- Smart Peak Detection: 100-period lookback for meaningful peaks

- Volume Filter: Optional volume confirmation system

- USD-Based Positions: Fixed dollar amounts per level

- Never Sells: Pure accumulation philosophy (buy-only)

📊 How It Works

1. Peak Identification: Detects highest price in last 100 periods

2. Daily Trend Check: Confirms price above 50 SMA on 1D timeframe

3. Drop Tracking: Calculates percentage drops from cycle high

4. Systematic Buying: Executes predetermined amounts at each level

5. Cycle Reset: Renews buy permissions when new peaks form

⚙️ Default Settings

- Buy Levels: 5%, 10%, 15% drops

- Position Sizes: $100, $150, $200

- Peak Period: 100 bars

- Higher Timeframe: 1 Day (1D)

- Pyramiding: 500 order capacity

🎨 Visual Elements

- Orange Circles: Mark cycle highs

- Colored Lines: Green/Blue/Red buy levels

- Triangle Signals: Buy point indicators

- Live Panel: Real-time statistics

- Background Colors: Trend and drop level indicators

🔔 Alert System

- Instant notifications for each buy level

- New peak detection alerts

- Major drop warnings (>20%)

- Daily trend change notifications

💡 Ideal Use Cases

- Crypto Accumulation: Bitcoin, Ethereum and major altcoins

- Stock DCA: Long-term portfolio building

- Volatile Markets: Capitalizing on price fluctuations

- Emotional Trading Prevention: Automated and disciplined buying

📈 Strategy Logic

This strategy follows the "buy the dip" philosophy. It waits during market rises and systematically builds positions during declines. Only buys when daily trend is bullish, providing protection during major bear markets.

⚠️ Important Notes

- Buy-only strategy - never sells positions

- Requires sufficient capital for multiple entries

- Most effective in trending and volatile markets

- Always backtest before live trading

- Risk management is your responsibility

🛠️ Customization Options

All parameters are fully customizable: drop percentages, position amounts, timeframes, visual elements and more. Suitable for both beginner and experienced investors.

🎯 Publishing Feature

Note: Strategy includes temporary 1-day sell cycle for TradingView publishing requirements. This feature can be disabled for normal DCA mode operation.

⭐ If you find this strategy helpful, please like and follow! Visit the profile for more trading tools.

Bar Index & TimeLibrary to convert a bar index to a timestamp and vice versa.

Utilizes runtime memory to store the 𝚝𝚒𝚖𝚎 and 𝚝𝚒𝚖𝚎_𝚌𝚕𝚘𝚜𝚎 values of every bar on the chart (and optional future bars), with the ability of storing additional custom values for every chart bar.

█ PREFACE

This library aims to tackle some problems that pine coders (from beginners to advanced) often come across, such as:

I'm trying to draw an object with a 𝚋𝚊𝚛_𝚒𝚗𝚍𝚎𝚡 that is more than 10,000 bars into the past, but this causes my script to fail. How can I convert the 𝚋𝚊𝚛_𝚒𝚗𝚍𝚎𝚡 to a UNIX time so that I can draw visuals using xloc.bar_time ?

I have a diagonal line drawing and I want to get the "y" value at a specific time, but line.get_price() only accepts a bar index value. How can I convert the timestamp into a bar index value so that I can still use this function?

I want to get a previous 𝚘𝚙𝚎𝚗 value that occurred at a specific timestamp. How can I convert the timestamp into a historical offset so that I can use 𝚘𝚙𝚎𝚗 ?

I want to reference a very old value for a variable. How can I access a previous value that is older than the maximum historical buffer size of 𝚟𝚊𝚛𝚒𝚊𝚋𝚕𝚎 ?

This library can solve the above problems (and many more) with the addition of a few lines of code, rather than requiring the coder to refactor their script to accommodate the limitations.

█ OVERVIEW

The core functionality provided is conversion between xloc.bar_index and xloc.bar_time values.

The main component of the library is the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object, created via the 𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() function which basically stores the 𝚝𝚒𝚖𝚎 and 𝚝𝚒𝚖𝚎_𝚌𝚕𝚘𝚜𝚎 of every bar on the chart, and there are 3 more overloads to this function that allow collecting and storing additional data. Once a 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object is created, use any of the exported methods:

Methods to convert a UNIX timestamp into a bar index or bar offset:

𝚝𝚒𝚖𝚎𝚜𝚝𝚊𝚖𝚙𝚃𝚘𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡(), 𝚐𝚎𝚝𝙽𝚞𝚖𝚋𝚎𝚛𝙾𝚏𝙱𝚊𝚛𝚜𝙱𝚊𝚌𝚔()

Methods to retrieve the stored data for a bar index:

𝚝𝚒𝚖𝚎𝙰𝚝𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡(), 𝚝𝚒𝚖𝚎𝙲𝚕𝚘𝚜𝚎𝙰𝚝𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡(), 𝚟𝚊𝚕𝚞𝚎𝙰𝚝𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡(), 𝚐𝚎𝚝𝙰𝚕𝚕𝚅𝚊𝚛𝚒𝚊𝚋𝚕𝚎𝚜𝙰𝚝𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡()

Methods to retrieve the stored data at a number of bars back (i.e., historical offset):

𝚝𝚒𝚖𝚎(), 𝚝𝚒𝚖𝚎𝙲𝚕𝚘𝚜𝚎(), 𝚟𝚊𝚕𝚞𝚎()

Methods to retrieve all the data points from the earliest bar (or latest bar) stored in memory, which can be useful for debugging purposes:

𝚐𝚎𝚝𝙴𝚊𝚛𝚕𝚒𝚎𝚜𝚝𝚂𝚝𝚘𝚛𝚎𝚍𝙳𝚊𝚝𝚊(), 𝚐𝚎𝚝𝙻𝚊𝚝𝚎𝚜𝚝𝚂𝚝𝚘𝚛𝚎𝚍𝙳𝚊𝚝𝚊()

Note: the library's strong suit is referencing data from very old bars in the past, which is especially useful for scripts that perform its necessary calculations only on the last bar.

█ USAGE

Step 1

Import the library. Replace with the latest available version number for this library.

//@version=6

indicator("Usage")

import n00btraders/ChartData/

Step 2

Create a 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object to collect data on every bar. Do not declare as `var` or `varip`.

chartData = ChartData.collectChartData() // call on every bar to accumulate the necessary data

Step 3

Call any method(s) on the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object. Do not modify its fields directly.

if barstate.islast

int firstBarTime = chartData.timeAtBarIndex(0)

int lastBarTime = chartData.time(0)

log.info("First `time`: " + str.format_time(firstBarTime) + ", Last `time`: " + str.format_time(lastBarTime))

█ EXAMPLES

• Collect Future Times

The overloaded 𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() functions that accept a 𝚋𝚊𝚛𝚜𝙵𝚘𝚛𝚠𝚊𝚛𝚍 argument can additionally store time values for up to 500 bars into the future.

//@version=6

indicator("Example `collectChartData(barsForward)`")

import n00btraders/ChartData/1

chartData = ChartData.collectChartData(barsForward = 500)

var rectangle = box.new(na, na, na, na, xloc = xloc.bar_time, force_overlay = true)

if barstate.islast

int futureTime = chartData.timeAtBarIndex(bar_index + 100)

int lastBarTime = time

box.set_lefttop(rectangle, lastBarTime, open)

box.set_rightbottom(rectangle, futureTime, close)

box.set_text(rectangle, "Extending box 100 bars to the right. Time: " + str.format_time(futureTime))

• Collect Custom Data

The overloaded 𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() functions that accept a 𝚟𝚊𝚛𝚒𝚊𝚋𝚕𝚎𝚜 argument can additionally store custom user-specified values for every bar on the chart.

//@version=6

indicator("Example `collectChartData(variables)`")

import n00btraders/ChartData/1

var map variables = map.new()

variables.put("open", open)

variables.put("close", close)

variables.put("open-close midpoint", (open + close) / 2)

variables.put("boolean", open > close ? 1 : 0)

chartData = ChartData.collectChartData(variables = variables)

var fgColor = chart.fg_color

var table1 = table.new(position.top_right, 2, 9, color(na), fgColor, 1, fgColor, 1, true)

var table2 = table.new(position.bottom_right, 2, 9, color(na), fgColor, 1, fgColor, 1, true)

if barstate.isfirst

table.cell(table1, 0, 0, "ChartData.value()", text_color = fgColor)

table.cell(table2, 0, 0, "open ", text_color = fgColor)

table.merge_cells(table1, 0, 0, 1, 0)

table.merge_cells(table2, 0, 0, 1, 0)

for i = 1 to 8

table.cell(table1, 0, i, text_color = fgColor, text_halign = text.align_left, text_font_family = font.family_monospace)

table.cell(table2, 0, i, text_color = fgColor, text_halign = text.align_left, text_font_family = font.family_monospace)

table.cell(table1, 1, i, text_color = fgColor)

table.cell(table2, 1, i, text_color = fgColor)

if barstate.islast

for i = 1 to 8

float open1 = chartData.value("open", 5000 * i)

float open2 = i < 3 ? open : -1

table.cell_set_text(table1, 0, i, "chartData.value(\"open\", " + str.tostring(5000 * i) + "): ")

table.cell_set_text(table2, 0, i, "open : ")

table.cell_set_text(table1, 1, i, str.tostring(open1))

table.cell_set_text(table2, 1, i, open2 >= 0 ? str.tostring(open2) : "Error")

• xloc.bar_index → xloc.bar_time

The 𝚝𝚒𝚖𝚎 value (or 𝚝𝚒𝚖𝚎_𝚌𝚕𝚘𝚜𝚎 value) can be retrieved for any bar index that is stored in memory by the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object.

//@version=6

indicator("Example `timeAtBarIndex()`")

import n00btraders/ChartData/1

chartData = ChartData.collectChartData()

if barstate.islast

int start = bar_index - 15000

int end = bar_index - 100

// line.new(start, close, end, close) // !ERROR - `start` value is too far from current bar index

start := chartData.timeAtBarIndex(start)

end := chartData.timeAtBarIndex(end)

line.new(start, close, end, close, xloc.bar_time, width = 10)

• xloc.bar_time → xloc.bar_index

Use 𝚝𝚒𝚖𝚎𝚜𝚝𝚊𝚖𝚙𝚃𝚘𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡() to find the bar that a timestamp belongs to.

If the timestamp falls in between the close of one bar and the open of the next bar,

the 𝚜𝚗𝚊𝚙 parameter can be used to determine which bar to choose:

𝚂𝚗𝚊𝚙.𝙻𝙴𝙵𝚃 - prefer to choose the leftmost bar (typically used for closing times)

𝚂𝚗𝚊𝚙.𝚁𝙸𝙶𝙷𝚃 - prefer to choose the rightmost bar (typically used for opening times)

𝚂𝚗𝚊𝚙.𝙳𝙴𝙵𝙰𝚄𝙻𝚃 (or 𝚗𝚊) - copies the same behavior as xloc.bar_time uses for drawing objects

//@version=6

indicator("Example `timestampToBarIndex()`")

import n00btraders/ChartData/1

startTimeInput = input.time(timestamp("01 Aug 2025 08:30 -0500"), "Session Start Time")

endTimeInput = input.time(timestamp("01 Aug 2025 15:15 -0500"), "Session End Time")

chartData = ChartData.collectChartData()

if barstate.islastconfirmedhistory

int startBarIndex = chartData.timestampToBarIndex(startTimeInput, ChartData.Snap.RIGHT)

int endBarIndex = chartData.timestampToBarIndex(endTimeInput, ChartData.Snap.LEFT)

line1 = line.new(startBarIndex, 0, startBarIndex, 1, extend = extend.both, color = color.new(color.green, 60), force_overlay = true)

line2 = line.new(endBarIndex, 0, endBarIndex, 1, extend = extend.both, color = color.new(color.green, 60), force_overlay = true)

linefill.new(line1, line2, color.new(color.green, 90))

// using Snap.DEFAULT to show that it is equivalent to drawing lines using `xloc.bar_time` (i.e., it aligns to the same bars)

startBarIndex := chartData.timestampToBarIndex(startTimeInput)

endBarIndex := chartData.timestampToBarIndex(endTimeInput)

line.new(startBarIndex, 0, startBarIndex, 1, extend = extend.both, color = color.yellow, width = 3)

line.new(endBarIndex, 0, endBarIndex, 1, extend = extend.both, color = color.yellow, width = 3)

line.new(startTimeInput, 0, startTimeInput, 1, xloc.bar_time, extend.both, color.new(color.blue, 85), width = 11)

line.new(endTimeInput, 0, endTimeInput, 1, xloc.bar_time, extend.both, color.new(color.blue, 85), width = 11)

• Get Price of Line at Timestamp

The pine script built-in function line.get_price() requires working with bar index values. To get the price of a line in terms of a timestamp, convert the timestamp into a bar index or offset.

//@version=6

indicator("Example `line.get_price()` at timestamp")

import n00btraders/ChartData/1

lineStartInput = input.time(timestamp("01 Aug 2025 08:30 -0500"), "Line Start")

chartData = ChartData.collectChartData()

var diagonal = line.new(na, na, na, na, force_overlay = true)

if time <= lineStartInput

line.set_xy1(diagonal, bar_index, open)

if barstate.islastconfirmedhistory

line.set_xy2(diagonal, bar_index, close)

if barstate.islast

int timeOneWeekAgo = timenow - (7 * timeframe.in_seconds("1D") * 1000)

// Note: could also use `timetampToBarIndex(timeOneWeekAgo, Snap.DEFAULT)` and pass the value directly to `line.get_price()`

int barsOneWeekAgo = chartData.getNumberOfBarsBack(timeOneWeekAgo)

float price = line.get_price(diagonal, bar_index - barsOneWeekAgo)

string formatString = "Time 1 week ago: {0,number,#}\n - Equivalent to {1} bars ago\n\n𝚕𝚒𝚗𝚎.𝚐𝚎𝚝_𝚙𝚛𝚒𝚌𝚎(): {2,number,#.##}"

string labelText = str.format(formatString, timeOneWeekAgo, barsOneWeekAgo, price)

label.new(timeOneWeekAgo, price, labelText, xloc.bar_time, style = label.style_label_lower_right, size = 16, textalign = text.align_left, force_overlay = true)

█ RUNTIME ERROR MESSAGES

This library's functions will generate a custom runtime error message in the following cases:

𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() is not called consecutively, or is called more than once on a single bar

Invalid 𝚋𝚊𝚛𝚜𝙵𝚘𝚛𝚠𝚊𝚛𝚍 argument in the 𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() function

Invalid 𝚟𝚊𝚛𝚒𝚊𝚋𝚕𝚎𝚜 argument in the 𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() function

Invalid 𝚕𝚎𝚗𝚐𝚝𝚑 argument in any of the functions that accept a number of bars back

Note: there is no runtime error generated for an invalid 𝚝𝚒𝚖𝚎𝚜𝚝𝚊𝚖𝚙 or 𝚋𝚊𝚛𝙸𝚗𝚍𝚎𝚡 argument in any of the functions. Instead, the functions will assign 𝚗𝚊 to the returned values.

Any other runtime errors are due to incorrect usage of the library.

█ NOTES

• Function Descriptions

The library source code uses Markdown for the exported functions. Hover over a function/method call in the Pine Editor to display formatted, detailed information about the function/method.

//@version=6

indicator("Demo Function Tooltip")

import n00btraders/ChartData/1

chartData = ChartData.collectChartData()

int barIndex = chartData.timestampToBarIndex(timenow)

log.info(str.tostring(barIndex))

• Historical vs. Realtime Behavior

Under the hood, the data collector for this library is declared as `var`. Because of this, the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object will always reflect the latest available data on realtime updates. Any data that is recorded for historical bars will remain unchanged throughout the execution of a script.

//@version=6

indicator("Demo Realtime Behavior")

import n00btraders/ChartData/1

var map variables = map.new()

variables.put("open", open)

variables.put("close", close)

chartData = ChartData.collectChartData(variables)

if barstate.isrealtime

varip float initialOpen = open

varip float initialClose = close

varip int updateCount = 0

updateCount += 1

float latestOpen = open

float latestClose = close

float recordedOpen = chartData.valueAtBarIndex("open", bar_index)

float recordedClose = chartData.valueAtBarIndex("close", bar_index)

string formatString = "# of updates: {0}\n\n𝚘𝚙𝚎𝚗 at update #1: {1,number,#.##}\n𝚌𝚕𝚘𝚜𝚎 at update #1: {2,number,#.##}\n\n"

+ "𝚘𝚙𝚎𝚗 at update #{0}: {3,number,#.##}\n𝚌𝚕𝚘𝚜𝚎 at update #{0}: {4,number,#.##}\n\n"

+ "𝚘𝚙𝚎𝚗 stored in memory: {5,number,#.##}\n𝚌𝚕𝚘𝚜𝚎 stored in memory: {6,number,#.##}"

string labelText = str.format(formatString, updateCount, initialOpen, initialClose, latestOpen, latestClose, recordedOpen, recordedClose)

label.new(bar_index, close, labelText, style = label.style_label_left, force_overlay = true)

• Collecting Chart Data for Other Contexts

If your use case requires collecting chart data from another context, avoid directly retrieving the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object as this may exceed memory limits .

//@version=6

indicator("Demo Return Calculated Results")

import n00btraders/ChartData/1

timeInput = input.time(timestamp("01 Sep 2025 08:30 -0500"), "Time")

var int oneMinuteBarsAgo = na

// !ERROR - Memory Limits Exceeded

// chartDataArray = request.security_lower_tf(syminfo.tickerid, "1", ChartData.collectChartData())

// oneMinuteBarsAgo := chartDataArray.last().getNumberOfBarsBack(timeInput)

// function that returns calculated results (a single integer value instead of an entire `ChartData` object)

getNumberOfBarsBack() =>

chartData = ChartData.collectChartData()

chartData.getNumberOfBarsBack(timeInput)

calculatedResultsArray = request.security_lower_tf(syminfo.tickerid, "1", getNumberOfBarsBack())

oneMinuteBarsAgo := calculatedResultsArray.size() > 0 ? calculatedResultsArray.last() : na

if barstate.islast

string labelText = str.format("The selected timestamp occurs 1-minute bars ago", oneMinuteBarsAgo)

label.new(bar_index, hl2, labelText, style = label.style_label_left, size = 16, force_overlay = true)

• Memory Usage

The library's convenience and ease of use comes at the cost of increased usage of computational resources. For simple scripts, using this library will likely not cause any issues with exceeding memory limits. But for large and complex scripts, you can reduce memory issues by specifying a lower 𝚌𝚊𝚕𝚌_𝚋𝚊𝚛𝚜_𝚌𝚘𝚞𝚗𝚝 amount in the indicator() or strategy() declaration statement.

//@version=6

// !ERROR - Memory Limits Exceeded using the default number of bars available (~20,000 bars for Premium plans)

//indicator("Demo `calc_bars_count` parameter")

// Reduce number of bars using `calc_bars_count` parameter

indicator("Demo `calc_bars_count` parameter", calc_bars_count = 15000)

import n00btraders/ChartData/1

map variables = map.new()

variables.put("open", open)

variables.put("close", close)

variables.put("weekofyear", weekofyear)

variables.put("dayofmonth", dayofmonth)

variables.put("hour", hour)

variables.put("minute", minute)

variables.put("second", second)

// simulate large memory usage

chartData0 = ChartData.collectChartData(variables)

chartData1 = ChartData.collectChartData(variables)

chartData2 = ChartData.collectChartData(variables)

chartData3 = ChartData.collectChartData(variables)

chartData4 = ChartData.collectChartData(variables)

chartData5 = ChartData.collectChartData(variables)

chartData6 = ChartData.collectChartData(variables)

chartData7 = ChartData.collectChartData(variables)

chartData8 = ChartData.collectChartData(variables)

chartData9 = ChartData.collectChartData(variables)

log.info(str.tostring(chartData0.time(0)))

log.info(str.tostring(chartData1.time(0)))

log.info(str.tostring(chartData2.time(0)))

log.info(str.tostring(chartData3.time(0)))

log.info(str.tostring(chartData4.time(0)))

log.info(str.tostring(chartData5.time(0)))

log.info(str.tostring(chartData6.time(0)))

log.info(str.tostring(chartData7.time(0)))

log.info(str.tostring(chartData8.time(0)))

log.info(str.tostring(chartData9.time(0)))

if barstate.islast

result = table.new(position.middle_right, 1, 1, force_overlay = true)

table.cell(result, 0, 0, "Script Execution Successful ✅", text_size = 40)

█ EXPORTED ENUMS

Snap

Behavior for determining the bar that a timestamp belongs to.

Fields:

LEFT : Snap to the leftmost bar.

RIGHT : Snap to the rightmost bar.

DEFAULT : Default `xloc.bar_time` behavior.

Note: this enum is used for the 𝚜𝚗𝚊𝚙 parameter of 𝚝𝚒𝚖𝚎𝚜𝚝𝚊𝚖𝚙𝚃𝚘𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡().

█ EXPORTED TYPES

Note: users of the library do not need to worry about directly accessing the fields of these types; all computations are done through method calls on an object of the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 type.

Variable

Represents a user-specified variable that can be tracked on every chart bar.

Fields:

name (series string) : Unique identifier for the variable.

values (array) : The array of stored values (one value per chart bar).

ChartData

Represents data for all bars on a chart.

Fields:

bars (series int) : Current number of bars on the chart.

timeValues (array) : The `time` values of all chart (and future) bars.

timeCloseValues (array) : The `time_close` values of all chart (and future) bars.

variables (array) : Additional custom values to track on all chart bars.

█ EXPORTED FUNCTIONS

collectChartData()

Collects and tracks the `time` and `time_close` value of every bar on the chart.

Returns: `ChartData` object to convert between `xloc.bar_index` and `xloc.bar_time`.

collectChartData(barsForward)

Collects and tracks the `time` and `time_close` value of every bar on the chart as well as a specified number of future bars.

Parameters:

barsForward (simple int) : Number of future bars to collect data for.

Returns: `ChartData` object to convert between `xloc.bar_index` and `xloc.bar_time`.

collectChartData(variables)

Collects and tracks the `time` and `time_close` value of every bar on the chart. Additionally, tracks a custom set of variables for every chart bar.

Parameters:

variables (simple map) : Custom values to collect on every chart bar.

Returns: `ChartData` object to convert between `xloc.bar_index` and `xloc.bar_time`.

collectChartData(barsForward, variables)

Collects and tracks the `time` and `time_close` value of every bar on the chart as well as a specified number of future bars. Additionally, tracks a custom set of variables for every chart bar.

Parameters:

barsForward (simple int) : Number of future bars to collect data for.

variables (simple map) : Custom values to collect on every chart bar.

Returns: `ChartData` object to convert between `xloc.bar_index` and `xloc.bar_time`.

█ EXPORTED METHODS

method timestampToBarIndex(chartData, timestamp, snap)

Converts a UNIX timestamp to a bar index.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

timestamp (series int) : A UNIX time.

snap (series Snap) : A `Snap` enum value.

Returns: A bar index, or `na` if unable to find the appropriate bar index.

method getNumberOfBarsBack(chartData, timestamp)

Converts a UNIX timestamp to a history-referencing length (i.e., number of bars back).

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

timestamp (series int) : A UNIX time.

Returns: A bar offset, or `na` if unable to find a valid number of bars back.

method timeAtBarIndex(chartData, barIndex)

Retrieves the `time` value for the specified bar index.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

barIndex (int) : The bar index.

Returns: The `time` value, or `na` if there is no `time` stored for the bar index.

method time(chartData, length)

Retrieves the `time` value of the bar that is `length` bars back relative to the latest bar.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

length (series int) : Number of bars back.

Returns: The `time` value `length` bars ago, or `na` if there is no `time` stored for that bar.

method timeCloseAtBarIndex(chartData, barIndex)

Retrieves the `time_close` value for the specified bar index.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

barIndex (series int) : The bar index.

Returns: The `time_close` value, or `na` if there is no `time_close` stored for the bar index.

method timeClose(chartData, length)

Retrieves the `time_close` value of the bar that is `length` bars back from the latest bar.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

length (series int) : Number of bars back.

Returns: The `time_close` value `length` bars ago, or `na` if there is none stored.

method valueAtBarIndex(chartData, name, barIndex)

Retrieves the value of a custom variable for the specified bar index.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

name (series string) : The variable name.

barIndex (series int) : The bar index.

Returns: The value of the variable, or `na` if that variable is not stored for the bar index.

method value(chartData, name, length)

Retrieves a variable value of the bar that is `length` bars back relative to the latest bar.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

name (series string) : The variable name.

length (series int) : Number of bars back.

Returns: The value `length` bars ago, or `na` if that variable is not stored for the bar index.

method getAllVariablesAtBarIndex(chartData, barIndex)

Retrieves all custom variables for the specified bar index.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

barIndex (series int) : The bar index.

Returns: Map of all custom variables that are stored for the specified bar index.

method getEarliestStoredData(chartData)

Gets all values from the earliest bar data that is currently stored in memory.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

Returns: A tuple:

method getLatestStoredData(chartData, futureData)

Gets all values from the latest bar data that is currently stored in memory.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

futureData (series bool) : Whether to include the future data that is stored in memory.

Returns: A tuple:

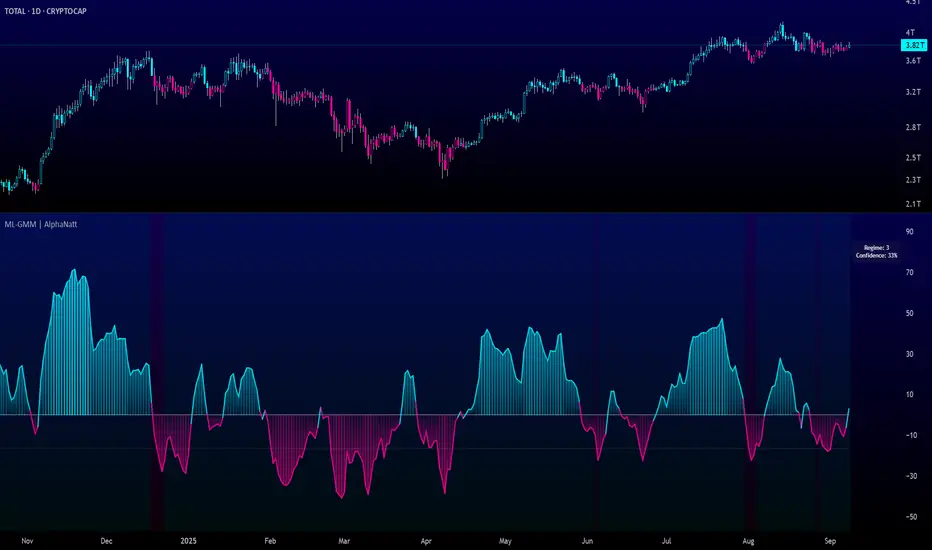

Machine Learning Gaussian Mixture Model | AlphaNattMachine Learning Gaussian Mixture Model | AlphaNatt

A revolutionary oscillator that uses Gaussian Mixture Models (GMM) with unsupervised machine learning to identify market regimes and automatically adapt momentum calculations - bringing statistical pattern recognition techniques to trading.

"Markets don't follow a single distribution - they're a mixture of different regimes. This oscillator identifies which regime we're in and adapts accordingly."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🤖 THE MACHINE LEARNING

Gaussian Mixture Models (GMM):

Unlike K-means clustering which assigns hard boundaries, GMM uses probabilistic clustering :

Models data as coming from multiple Gaussian distributions

Each market regime is a different Gaussian component

Provides probability of belonging to each regime

More sophisticated than simple clustering

Expectation-Maximization Algorithm:

The indicator continuously learns and adapts using the E-M algorithm:

E-step: Calculate probability of current market belonging to each regime

M-step: Update regime parameters based on new data

Continuous learning without repainting

Adapts to changing market conditions

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 THREE MARKET REGIMES

The GMM identifies three distinct market states:

Regime 1 - Low Volatility:

Quiet, ranging markets

Uses RSI-based momentum calculation

Reduces false signals in choppy conditions

Background: Pink tint

Regime 2 - Normal Market:

Standard trending conditions

Uses Rate of Change momentum

Balanced sensitivity

Background: Gray tint

Regime 3 - High Volatility:

Strong trends or volatility events

Uses Z-score based momentum

Captures extreme moves

Background: Cyan tint

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 KEY INNOVATIONS

1. Probabilistic Regime Detection:

Instead of binary regime assignment, provides probabilities:

30% Regime 1, 60% Regime 2, 10% Regime 3

Smooth transitions between regimes

No sudden indicator jumps

2. Weighted Momentum Calculation:

Combines three different momentum formulas

Weights based on regime probabilities

Automatically adapts to market conditions

3. Confidence Indicator:

Shows how certain the model is (white line)

High confidence = strong regime identification

Low confidence = transitional market state

Line transparency changes with confidence

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ PARAMETER OPTIMIZATION

Training Period (50-500):

50-100: Quick adaptation to recent conditions

100: Balanced (default)

200-500: Stable regime identification

Number of Components (2-5):

2: Simple bull/bear regimes

3: Low/Normal/High volatility (default)

4-5: More granular regime detection

Learning Rate (0.1-1.0):

0.1-0.3: Slow, stable learning

0.3: Balanced (default)

0.5-1.0: Fast adaptation

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING STRATEGIES

Visual Signals:

Cyan gradient: Bullish momentum

Magenta gradient: Bearish momentum

Background color: Current regime

Confidence line: Model certainty

1. Regime-Based Trading:

Regime 1 (pink): Expect mean reversion

Regime 2 (gray): Standard trend following

Regime 3 (cyan): Strong momentum trades

2. Confidence-Filtered Signals:

Only trade when confidence > 70%

High confidence = clearer market state

Avoid transitions (low confidence)

3. Adaptive Position Sizing:

Regime 1: Smaller positions (choppy)

Regime 2: Normal positions

Regime 3: Larger positions (trending)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🚀 ADVANTAGES OVER OTHER ML INDICATORS

vs K-Means Clustering:

Soft clustering (probabilities) vs hard boundaries

Captures uncertainty and transitions

More mathematically robust

vs KNN (K-Nearest Neighbors):

Unsupervised learning (no historical labels needed)

Continuous adaptation

Lower computational complexity

vs Neural Networks:

Interpretable (know what each regime means)

No overfitting issues

Works with limited data

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 PERFORMANCE CHARACTERISTICS

Best Market Conditions:

Markets with clear regime shifts

Volatile to trending transitions

Multi-timeframe analysis

Cryptocurrency markets (high regime variation)

Key Strengths:

Automatically adapts to market changes

No manual parameter adjustment needed

Smooth transitions between regimes

Probabilistic confidence measure

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔬 TECHNICAL BACKGROUND

Gaussian Mixture Models are used extensively in:

Speech recognition (Google Assistant)

Computer vision (facial recognition)

Astronomy (galaxy classification)

Genomics (gene expression analysis)

Finance (risk modeling at investment banks)

The E-M algorithm was developed at Stanford in 1977 and is one of the most important algorithms in unsupervised machine learning.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 PRO TIPS

Watch regime transitions: Best opportunities often occur when regimes change

Combine with volume: High volume + regime change = strong signal

Use confidence filter: Avoid low confidence periods

Multi-timeframe: Compare regimes across timeframes

Adjust position size: Scale based on identified regime

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ IMPORTANT NOTES

Machine learning adapts but doesn't predict the future

Best used with other confirmation indicators

Allow time for model to learn (100+ bars)

Not financial advice - educational purposes

Backtest thoroughly on your instruments

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🏆 CONCLUSION

The GMM Momentum Oscillator brings institutional-grade machine learning to retail trading. By identifying market regimes probabilistically and adapting momentum calculations accordingly, it provides:

Automatic adaptation to market conditions

Clear regime identification with confidence levels

Smooth, professional signal generation

True unsupervised machine learning

This isn't just another indicator with "ML" in the name - it's a genuine implementation of Gaussian Mixture Models with the Expectation-Maximization algorithm, the same technology used in:

Google's speech recognition

Tesla's computer vision

NASA's data analysis

Wall Street risk models

"Let the machine learn the market regimes. Trade with statistical confidence."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt | Machine Learning Trading Systems

Version: 1.0

Algorithm: Gaussian Mixture Model with E-M

Classification: Unsupervised Learning Oscillator

Not financial advice. Always DYOR.

Supertrend [TradingConToto]Supertrend — ADX/DI + EMA Gap + Breakout (with Mobile UI)

What makes it original

Supertrend combines trend strength (ADX/DI), multi-timeframe bias (EMA63 and EMA 200D equivalent), a structural filter based on the distance between EMA2400 and EMA4800 expressed in ATR units, and a momentum confirmation through a previous high breakout.

This is not a random mashup — it’s a sequence of filters designed to reduce trades in ranging markets and prioritize mature trends:

Direction: +DI > -DI (trend led by buyers).

Strength: ADX > mean(ADX) (avoids weak, choppy phases).

Short-term bias: Close > EMA63.

Long-term bias: Close > EMA4800 ≈ EMA200 daily on H1.

Momentum: Close > High (immediate breakout).

Structure: (EMA2400 − EMA4800) > k·ATR (ensures separation in ATR units, filters out flat phases).

Entries & exits

Entry: when all six conditions are met and no open position exists.

Exit: if +DI < -DI or Close < EMA63.

Visuals: EMA63 is painted green while in position and red otherwise, with a supertrend-style band; “BUY” labels appear below the green band and “SELL” labels above the red band.

UI: includes a compact table (mobile-friendly) showing the state of each condition.

Default parameters used in this publication

Initial capital: 10,000

Position size: 10% of equity (≤10% per trade is considered sustainable).

Commission: 0.01% per side (adjust to your broker/market).

Slippage: 1 tick

Pyramiding: 0 (only one position at a time)

Adjust commission/slippage to match your market. For US equities, commissions are often per share; for spot crypto, 0.10–0.20% total is common. I publish with 0.01% per side as a conservative example to avoid overestimating results.

Recommended backtest dataset

Timeframe: H1

Multi-cycle window (e.g. 2015–today)

Symbols with high liquidity (e.g. NASDAQ-100 large caps, or BTC/ETH spot) to generate 100+ trades. Avoid cherry-picked short windows.

Why each filter matters

+DI > -DI + ADX > mean: reduce counter-trend trades and weak signals.

Close > EMA63 + Close > EMA4800: enforce trend alignment in short and long horizons.

Breakout High : requires immediate momentum, avoids early entries.

EMA gap in ATR units: blocks flat or compressed structures where EMA200D aligns with price.

Limitations

The breakout filter may skip healthy pullbacks; the design prioritizes continuation over perfect entry price.

No fixed trailing stop/TP; exits depend on trend degradation via DI/EMA63.

Results vary with real costs (commissions, slippage, funding). Adjust defaults to your broker.

How to use

Apply it on a clean chart (no other indicators when publishing).

Keep in mind the default parameters above; if you change them, mention it in your notes and use the same values in the Strategy Tester.

Ensure your dataset produces 100+ trades for statistical validity.

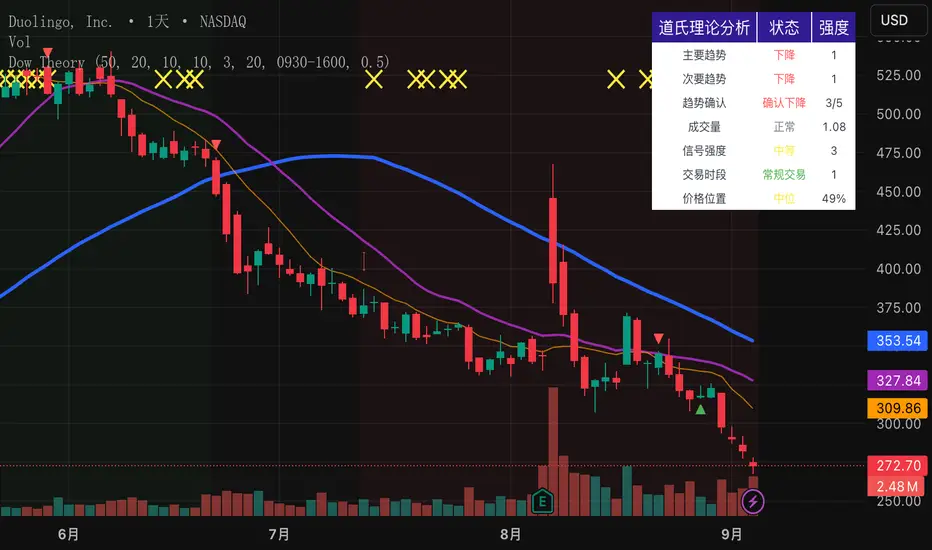

Dow Theory Indicator## 🎯 Key Features of the Indicator

### 📈 Complete Implementation of Dow Theory

- Three-tier trend structure: primary trend (50 periods), secondary trend (20 periods), and minor trend (10 periods).

- Swing point analysis: automatically detects critical swing highs and lows.

- Trend confirmation mechanism: strict confirmation logic based on consecutive higher highs/higher lows or lower highs/lower lows.

- Volume confirmation: ensures price moves are supported by trading volume.

### 🕐 Flexible Timeframe Parameters

All key parameters are adjustable, making it especially suitable for U.S. equities:

Trend analysis parameters:

- Primary trend period: 20–200 (default 50; recommended 50–100 for U.S. stocks).

- Secondary trend period: 10–100 (default 20; recommended 15–30 for U.S. stocks).

- Minor trend period: 5–50 (default 10; recommended 5–15 for U.S. stocks).

Dow Theory parameters:

- Swing high/low lookback: 5–50 (default 10).

- Trend confirmation bar count: 1–10 (default 3).

- Volume confirmation period: 10–100 (default 20).

### 🇺🇸 U.S. Market Optimizations

- Session awareness: distinguishes Regular Trading Hours (9:30–16:00 EST) from pre-market and after-hours.

- Pre/post-market weighting: adjustable weighting factor for signals during extended hours.

- Earnings season filter: automatically adjusts sensitivity during earnings periods.

- U.S.-optimized default parameters.

## 🎨 Visualization

1. Trend lines: three differently colored trend lines.

2. Background fill: green (uptrend) / red (downtrend) / gray (neutral).

3. Signal markers: arrows, labels, and warning icons.

4. Swing point markers: small triangles at key turning points.

5. Info panel: real-time display of eight key metrics.

## 🚨 Alert System

- Trend turning to up/down.

- Strong bullish/bearish signals (dual confirmation).

- Volume divergence warning.

- New swing high/low formed.

## 📋 How to Use

1. Open the Pine Editor in TradingView.

2. Copy the contents of dow_theory_indicator.pine.

3. Paste and click “Add to chart.”

4. Adjust parameters based on trading style:

- Long-term investing: increase all period parameters.

- Swing trading: use the default parameters.

- Short-term trading: decrease all period parameters.

## 💡 Parameter Tips for U.S. Stocks

- Large-cap blue chips (AAPL, MSFT): primary 60–80, secondary 25–30.

- Mid-cap growth stocks: primary 40–60, secondary 18–25.

- Small-cap high-volatility stocks: primary 30–50, secondary 15–20.

EMA20 Cross Strategy with countertrades and signalsEMA20 Cross Strategy Documentation

Overview

The EMA20 Cross Strategy with Counter-Trades and Instant Signals is a Pine Script (version 6) trading strategy designed for the TradingView platform. It implements an Exponential Moving Average (EMA) crossover system to generate buy and sell signals, with optional trend filtering, session-based trading, instant signal processing, and visual/statistical feedback. The strategy supports counter-trades (closing opposing positions before entering new ones) and operates with a fixed trade size in EUR.

Features

EMA Crossover Mechanism:

Uses a short-term EMA (configurable length, default: 1) and a long-term EMA (default: 20) to detect crossovers.

A buy signal is generated when the short EMA crosses above the long EMA.

A sell signal is generated when the short EMA crosses below the long EMA.

Instant Signals:

If enabled (useInstantSignals), signals are based on the current price crossing the short EMA, rather than waiting for the candle close.

This allows faster trade execution but may increase sensitivity to price fluctuations.

Trend Filter:

Optionally filters trades based on the trend direction (useTrendFilter).

Long trades are allowed only when the short EMA (or price, for instant signals) is above the long EMA.

Short trades are allowed only when the short EMA (or price) is below the long EMA.

Session Filter:

Restricts trading to specific market hours (sessionStart, default: 09:00–17:00) if enabled (useSessionFilter).

Ensures trades occur only during active market sessions, reducing exposure to low-liquidity periods.

Customizable Timeframe:

The EMA calculations can use a higher timeframe (e.g., 5m, 15m, 1H, 4H, 1D, default: 1H) via request.security.

This allows the strategy to base signals on longer-term trends while operating on a shorter-term chart.

Trade Management:

Fixed trade size of €100,000 per trade (tradeAmount), with a maximum quantity cap (maxQty = 10,000) to prevent oversized trades.

Counter-trades: Closes short positions before entering a long position and vice versa.

Trades are executed with a minimum quantity of 1 to ensure valid orders.

Visualization:

EMA Lines: The short EMA is colored based on the last signal (green for buy, red for sell, gray for neutral), and the long EMA is orange.

Signal Markers: Displays buy/sell signals as arrows (triangles) above/below candles if enabled (showSignalShapes).

Background/Candle Coloring: Optionally colors the chart background or candles green (bullish) or red (bearish) based on the trend (useColoredBars).

Statistics Display:

If enabled (useStats), a label on the chart shows:

Total closed trades

Open trades

Win rate (%)

Number of winning/losing trades

Profit factor (gross profit / gross loss)

Net profit

Maximum drawdown

Configuration Inputs

EMA Short Length (emaLength): Length of the short-term EMA (default: 1).

Trend EMA Length (trendLength): Length of the long-term EMA (default: 20).

Enable Trend Filter (useTrendFilter): Toggles trend-based filtering (default: true).

Color Candles (useColoredBars): Colors candles instead of the background (default: true).

Enable Session Filter (useSessionFilter): Restricts trading to specified hours (default: false).

Trading Session (sessionStart): Defines trading hours (default: 09:00–17:00).

Show Statistics (useStats): Displays performance stats on the chart (default: true).

Show Signal Arrows (showSignalShapes): Displays buy/sell signals as arrows (default: true).

Use Instant Signals (useInstantSignals): Generates signals based on live price action (default: false).

EMA Timeframe (emaTimeframe): Timeframe for EMA calculations (options: 5m, 15m, 1H, 4H, 1D; default: 1H).

Strategy Logic

Signal Generation:

Standard Mode: Signals are based on EMA crossovers (short EMA crossing long EMA) at candle close.

Instant Mode: Signals are based on the current price crossing the short EMA, enabling faster reactions.

Trade Execution:

On a buy signal, closes any short position and opens a long position.

On a sell signal, closes any long position and opens a short position.

Position size is calculated as the minimum of €100,000 or available equity, divided by the current price, capped at 10,000 units.

Filters:

Trend Filter: Ensures trades align with the trend direction (if enabled).

Session Filter: Restricts trades to user-defined market hours (if enabled).

Visual Feedback

EMA Lines: Provide a clear view of the short and long EMAs, with the short EMA’s color reflecting the latest signal.

Signal Arrows: Large green triangles (buy) below candles or red triangles (sell) above candles for easy signal identification.

Chart Coloring: Highlights bullish (green) or bearish (red) trends via background or candle colors.

Statistics Label: Displays key performance metrics in a label above the chart for quick reference.

Usage Notes

Initial Capital: €100,000 (configurable via initial_capital).

Currency: EUR (set via currency).

Order Processing: Orders are processed at candle close (process_orders_on_close=true) unless instant signals are enabled.

Dynamic Requests: Allows dynamic timeframe adjustments for EMA calculations (dynamic_requests=true).

Platform: Designed for TradingView, compatible with any market supported by the platform (e.g., stocks, forex, crypto).

Example Use Case

Scenario: Trading on a 5-minute chart with a 1-hour EMA timeframe, trend filter enabled, and session filter set to 09:00–17:00.

Behavior: The strategy will:

Calculate EMAs on the 1-hour timeframe.

Generate buy signals when the short EMA crosses above the long EMA (and price is above the long EMA).

Generate sell signals when the short EMA crosses below the long EMA (and price is below the long EMA).

Execute trades only during 09:00–17:00.

Display green/red candles and performance stats on the chart.

Limitations

Instant Signals: May lead to more frequent signals, increasing the risk of false positives in volatile markets.

Fixed Trade Size: Does not adjust dynamically based on market conditions beyond equity and max quantity limits.

Session Filter: Simplified and may not account for complex session rules or holidays.

Statistics: Displayed on-chart, which may clutter the view in smaller charts.

Customization

Adjust emaLength and trendLength to suit different market conditions (e.g., shorter for scalping, longer for swing trading).

Toggle useInstantSignals for faster or more stable signal generation.

Modify sessionStart to align with specific market hours.

Disable useStats or showSignalShapes for a cleaner chart.

This strategy is versatile for both manual and automated trading, offering flexibility for various markets and trading styles while providing clear visual and statistical feedback.

Live Market - Performance MonitorLive Market — Performance Monitor

Study material (no code) — step-by-step training guide for learners

________________________________________

1) What this tool is — short overview

This indicator is a live market performance monitor designed for learning. It scans price, volume and volatility, detects order blocks and trendline events, applies filters (volume & ATR), generates trade signals (BUY/SELL), creates simple TP/SL trade management, and renders a compact dashboard summarizing market state, risk and performance metrics.

Use it to learn how multi-factor signals are constructed, how Greeks-style sensitivity is replaced by volatility/ATR reasoning, and how a live dashboard helps monitor trade quality.

________________________________________

2) Quick start — how a learner uses it (step-by-step)

1. Add the indicator to a chart (any ticker / timeframe).

2. Open inputs and review the main groups: Order Block, Trendline, Signal Filters, Display.

3. Start with defaults (OB periods ≈ 7, ATR multiplier 0.5, volume threshold 1.2) and observe the dashboard on the last bar.

4. Walk the chart back in time (use the last-bar update behavior) and watch how signals, order blocks, trendlines, and the performance counters change.

5. Run the hands-on labs below to build intuition.

________________________________________

3) Main configurable inputs (what you can tweak)

• Order Block Relevant Periods (default ~7): number of consecutive candles used to define an order block.

• Min. Percent Move for Valid OB (threshold): minimum percent move required for a valid order block.

• Number of OB Channels: how many past order block lines to keep visible.

• Trendline Period (tl_period): pivot lookback for detecting highs/lows used to draw trendlines.

• Use Wicks for Trendlines: whether pivot uses wicks or body.

• Extension Bars: how far trendlines are projected forward.

• Use Volume Filter + Volume Threshold Multiplier (e.g., 1.2): requires volume to be greater than multiplier × average volume.

• Use ATR Filter + ATR Multiplier: require bar range > ATR × multiplier to filter noise.

• Show Targets / Table settings / Colors for visualization.

________________________________________

4) Core building blocks — what the script computes (plain language)

Price & trend:

• Spot / LTP: current close price.

• EMA 9 / 21 / 50: fast, medium, slow moving averages to define short/medium trend.

o trend_bullish: EMA9 > EMA21 > EMA50

o trend_bearish: EMA9 < EMA21 < EMA50

o trend_neutral: otherwise

Volatility & noise:

• ATR (14): average true range used for dynamic target and filter sizing.

• dynamic_zone = ATR × atr_multiplier: minimum bar range required for meaningful move.

• Annualized volatility: stdev of price changes × sqrt(252) × 100 — used to classify volatility (HIGH/MEDIUM/LOW).

Momentum & oscillators:

• RSI 14: overbought/oversold indicator (thresholds 70/30).

• MACD: EMA(12)-EMA(26) and a 9-period signal line; histogram used for momentum direction and strength.

• Momentum (ta.mom 10): raw momentum over 10 bars.

Mean reversion / band context:

• Bollinger Bands (20, 2σ): upper, mid, lower.

o price_position measures where price sits inside the band range as 0–100.

Volume metrics:

• avg_volume = SMA(volume, 20) and volume_spike = volume > avg_volume × volume_threshold

o volume_ratio = volume / avg_volume

Support & Resistance:

• support_level = lowest low over 20 bars

• resistance_level = highest high over 20 bars

• current_position = percent of price between support & resistance (0–100)

________________________________________

5) Order Block detection — concept & logic

What it tries to find: a bar (the base) followed by N candles in the opposite direction (a classical order block setup), with a minimum % move to qualify. The script records the high/low of the base candle, averages them, and plots those levels as OB channels.

How learners should think about it (conceptual):

1. An order block is a signature area where institutions (theory) left liquidity — often seen as a large bar followed by a sequence of directional candles.

2. This indicator uses a configurable number of subsequent candles to confirm that the pattern exists.

3. When found, it stores and displays the base candle’s high/low area so students can see how price later reacts to those zones.

Implementation note for learners: the tool keeps a limited history of OB lines (ob_channels). When new OBs exceed the count, the oldest lines are removed — good practice to avoid clutter.

________________________________________

6) Trendline detection — idea & interpretation

• The script finds pivot highs and lows using a symmetric lookback (tl_period and half that as right/left).

• It then computes a trendline slope from successive pivots and projects the line forward (extension_bars).

• Break detection: Resistance break = close crosses above the projected resistance line; Support break = close crosses below projected support.

Learning tip: trendlines here are computed from pivot points and time. Watch how changing tl_period (bigger = smoother, fewer pivots) alters the trendlines and break signals.

________________________________________

7) Signal generation & filters — step-by-step

1. Primary triggers:

o Bullish trigger: order block bullish OR resistance trendline break.

o Bearish trigger: bearish order block OR support trendline break.

2. Filters applied (both must pass unless disabled):

o Volume filter: volume must be > avg_volume × volume_threshold.

o ATR filter: bar range (high-low) must exceed ATR × atr_multiplier.

o Not in an existing trade: new trades only start if trade_active is false.

3. Trend confirmation:

o The primary trigger is only confirmed if trend is bullish/neutral for buys or bearish/neutral for sells (EMA alignment).

4. Result:

o When confirmed, a long or short trade is activated with TP/SL calculated from ATR multiples.

________________________________________

8) Trade management — what the tool does after a signal

• Entry management: the script marks a trade as trade_active and sets long_trade or short_trade flags.

• TP & SL rules:

o Long: TP = high + 2×ATR ; SL = low − 1×ATR

o Short: TP = low − 2×ATR ; SL = high + 1×ATR

• Monitoring & exit:

o A trade closes when price reaches TP or SL.