SNL Popular Moving Averages MTFSNL△ Popular Moving Averages MTF

Short title: PopMAs

These are popular moving averages used by various traders and they are multi-timeframe, i.e. you can see

the 200 day SMA on a 15 minute chart.

Four moving averages are also included for the current timeframe (20, 50, 100 and 200 EMA).

Not all moving averages are enabled by default. You can turn individual moving averges on or off in the

"Style" tab of the indicator's settings.

The way I see moving averages is that they do not represent a magic mathematical truth, but are simply the

result of many people agreeing on the same parameters. I guess the origin were five working days in a week

and therefore a month would be four times five, i.e. a 20 day SMA. 200 days are probably an estimate of

the work days in a year and the 50 day SMA represents a quarter year.

There are many indicators on TradingView that offer various adjustable moving averages, including

combinations and multi-timeframe. But my interest was to have an indicator with the most popular moving

averages and it should be multi-timeframe capable. By design I did not want to make the periods adjustable,

but you could add this easily if you like.

Here are some examples of poplular moving averages:

20 unit EMA : support on 4h BTC chart, Carl the Moon

20, 50, 100, 200 day SMA : classic trading all charts, Benjamin Cowen, Tone Vays

20, 50, 100, 200 week SMA: Benjamin Cowen

21 week EMA: well known BTC support, Benjamin Cowen

800 hour EMA: Traders Reality -> not possible in TradingView, represented as 33 day EMA

Known problems:

- I have not found a way to turn off floating labels according to a plot's state chosen in the "Style"

tab. So you will still see the label floating around even if you have turned off the moving average's

line. But you can always turn of all the floating labels in the settings.

- I have observed unexpected differences on multi-timeframe values: For example, looking at the true 20

week SMA on a weekly BTC chart showed a present time value of 43821 USD, but the value was 43908 USD

for the result of this call used in this script: security(syminfo.tickerid, "W", sma(close, 20))

The difference went away when switching my chart to weekly and back to 15 minutes.

Please comment if you know of other moving averages that are often and successfully used or if you find

that one of the included moving averages is irrelevant and should be removed from this script.

And I would very much appreciate any input regarding the mentioned known problems.

"富时中国50三倍做空" için komut dosyalarını ara

Six Moving Averages Study (use as a manual strategy indicator)I made this based on a really interesting conversation I had with a good friend of mine who ran a long/short hedge fund for seven years and worked at a major hedge fund as a manager for 20 years before that. This is an unconventional approach and I would not recommend it for bots, but it has worked unbelievably well for me over the last few weeks in a mixed market.

The first thing to know is that this indicator is supposed to work on a one minute chart and not a one hour, but TradingView will not allow 1m indicators to be published so we have to work around that a little bit. This is an ultra fast day trading strategy so be prepared for a wild ride if you use it on crypto like I do! Make sure you use it on a one minute chart.

The idea here is that you get six SMA curves which are:

1m 50 period

1m 100 period

1m 200 period

5m 50 period

5m 100 period

5m 200 period

The 1m 50 period is a little thicker because it's the most important MA in this algo. As price golden crosses each line it becomes a stronger buy signal, with added weight on the 1m 50 period MA. If price crosses all six I consider it a strong buy signal though your mileage may vary.

*** NOTE *** The screenshot is from a 1h chart which again, is not the correct way to use this. PLEASE don't use it on a one hour chart.

Multi HMA Lines by NB(ENG)

The Hull Moving Average (HMA) line responds quickly to volatile markets,

sometimes it provides more accurate information than the Exponancital Moving Average (EMA).

In particular, the 200 HMA line is easy to decide the overall trend of the market,

and it serves the basis entry position.

So I made indicator that provides these HMA lines into various periods so that they can be checked in one.

In addition, a custom TimeFrame HMA line function has been added so that you can check

not only the TimeFrame that meets your trading standards, but also the HMA of the other TimeFrame that you custome sets.

For example, if you want to see the 200 HMA of the 60-minute bar, you can select and set the different TimeFrame in the Multi TF section below.

For reference, 200 HMA at the 15-minute bar is the same value as 50 HMA at the 1-hour bar, so as shown in the following chart,

I use 4 HMA lines at the 15-minute bar : 20 HMA, 50 HMA, 200 HMA, and 200 HMA from 60-minute TimeFrame.

We hope it will help you in your trading. :)

(KOR)

HMA(Hull Moving Average) 라인은 변동성이 심한 시장에 빠르게 반응하며,

때때로 EMA(Exponancital Moving Average)보다 더 정확한 정보를 제공하곤 합니다.

특히 200HMA 라인은 시장의 전반적인 추세를 판단하기에 용이하며,

큰 틀에서의 포지션 진입 근거의 기반이 됩니다.

이러한 HMA 라인을 다양한 기간으로 나누어 하나의 지표에서 확인 할 수 있도록 만들어 보았습니다.

아울러, 자신의 매매 기준에 맞는 타임 프레임은 물론, 다른 타임 프레임의 HMA도 확인 할 수 있도록

커스텀 타임 프레임 HMA 라인 기능을 추가로 넣었습니다.

예를 들어, 15분 타임 프레임이 본인 매매 기준표이지만, 60분 봉의 200 HMA도 보고 싶다면

밑의 Multi TF 항목에서 해당 타임 프레임을 선택 후 설정하시면 됩니다.

참고로 15분 봉에서의 200 HMA은 1시간 봉에서의 50 HMA과 동일한 값이므로 저는 다음 차트 그림과 같이

15분 봉에서 20 HMA, 50 HMA, 200 HMA, 그리고 1시간 봉에서 200 HMA 이렇게 4개의 라인을 참고 하고 있습니다.

여러분 거래에 도움이 되기를 바랍니다. :)

How to use Leverage and Margin in PineScriptEn route to being absolutely the best and most complete trading platform out there, TradingView has just closed 2 gaps in their PineScript language.

It is now possible to create and backtest a strategy for trading with leverage.

Backtester now produces Margin Calls - so recognizes mid-trade drawdown and if it is too big for the broker to maintain your trade, some part of if will be instantly closed.

New additions were announced in official blogpost , but it lacked code examples, so I have decided to publish this script. Having said that - this is purely educational stuff.

█ LEVERAGE

Let's start with the Leverage. I will discuss this assuming we are always entering trades with some percentage of our equity balance (default_qty_type = strategy.percent_of_equity), not fixed order quantity.

If you want to trade with 1:1 leverage (so no leverage) and enter a trade with all money in your trading account, then first line of your strategy script must include this parameter:

default_qty_value = 100 // which stands for 100%

Now, if you want to trade with 30:1 leverage, you need to multipy the quantity by 30x, so you'd get 30 x 100 = 3000:

default_qty_value = 3000 // which stands for 3000%

And you can play around with this value as you wish, so if you want to enter each trade with 10% equity on 15:1 leverage you'd get default_qty_value = 150.

That's easy. Of course you can modify this quantity value not only in the script, but also afterwards in Script Settings popup, "Properties" tab.

█ MARGIN

Second newly released feature is Margin calculation together with Margin Calls. If the market goes against your trades and your trading account cannot maintain mid-trade drawdown - those trades will be closed in full or partly. Also, if your trading account cannot afford to open more trades (pyramiding those trades), Margin mechanism will prevent them from being entered.

I will not go into details about how Margin calculation works, it was all explainged in above mentioned blogpost and documentation .

All you need to do is to add two parameters to the opening line of your script:

margin_long = 1./30*50, margin_short = 1./30*50

Whereas "30" is a leverage scale as in 30:1, and "50" stands for 50% of Margin required by your broker. Personally the Required Margin number I've met most often is 50%, so I'm using value 50 here, but there are literally 1000+ brokers in this world and this is individual decision by each of them, so you'd better ask yourself.

--------------------

Please note, that if you ever encounter a strategy which triggers Margin Call at least once, then it is probably a very bad strategy. Margin Call is a last resort, last security measure - all the risks should be calculated by the strategy algorithm before it is ever hit. So if you see a Margin Call being triggred, then something is wrong with risk management of the strategy. Therefore - don't use it!

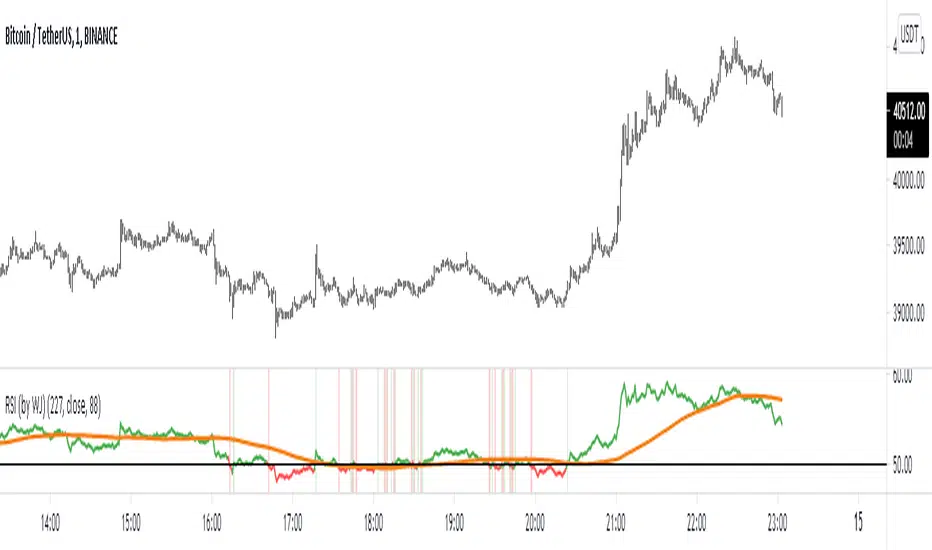

Relative Strength Index w/ 3 Levels & 0 Line Colour (by WJ)NOTE:

// RSI CODE TAKEN FROM DEFAULT INDICATOR

// I HAVE ONLY MADE SOME ADJUSTMENTS FOR VISUAL AID

// I MADE THIS FOR MY OWN USE BUT HAVE DECIDED TO PUBLISH AND SHARE IN CASE ANYBODY WANTS TO USE IT

This is the normal default built-in RSI indicator which I have added some stuff for visual aid:

Added middle line (50)

RSI turns green when crossed above 50

RSI turns red when crossed below 50

RSI background turns green and red on crossover candle based on whether RSI just crossed over or below 50 respectively

Alert notification on the crossover candle

Baz: Mcdx HeatmapThis indicator is to detect buying and selling momentum based on volume and price action with multiple timeframe mcdx.

Improve version of mcdx to let you see clearly real-time changes in 15mins, 30mins, 1h, 2h, 4h, 1D of the mcdx value.

Heatmap:

Green > Yellow > Orange > Red = Retailer shifting to banker

How it works?

The color subsides based on the resolution of chart, for example

We should focus on larger timeframe, which is >50 on the heatmap. Giving a clear signal that banker is still involved.

For value <50 on heatmap, you get faster signal without changing to smaller timeframe getting all the mcdx value, which save us a lot of time to look at bigger picture what is going on.

For example,

Lets check on each timeframe chart, starting from 15mins

For 15mins and 30min chart, mcdx is < 50

For 1H chart, mcdx is about 50

For 2H, 4H 1D, mcdx > 90

Color Changing Moving Average

Hello everybody!

I'm not much of a coder but I do make indicators for myself for fun sometimes and found this one super cool. Hope it helps!

Basically it's a moving average that changes colors based on the trend. How does it do it, you may ask? Simply put, it checks and makes sure that the open and close price is above the moving average, then it checks and sees if the 50-period RSI (length adjustable) is above 50. If both conditions are met, the moving average turns green. Simple as that.

If the price is below the moving average and the RSI is below 50, the moving average turns red.

If the price is above the moving average but the RSI is below 50, the line is grey and I advise to simply waiting for the trend direction to be decided. Likewise, if the price is below the moving average, but the RSI is above 50, the line is also grey.

This is NOT a comprehensive system, and the changing color of the moving average does not indicate a buy or sell signal. It simply indicates that the price is trending. You should use your own entry and exit strategy, such as the MACD, Wave Trend, Schaff Trend Cycle, etc.

As well, I would recommend waiting for confirmation of a trend change when the color changes, since in a range price can cross multiple times before deciding on the right direction.

The slope of the moving average can help too, since in a range the moving average is typically flat.

I would recommend using a fixed risk to reward ratio, to limit emotions. But, this would also help with a trend-following strategy due to the trend filter functionality.

The length of the moving average is adjustable, as well as the RSI period- though I wouldn't recommend selecting an RSI lower than 30 because it will whipsaw more. Disabling the EMA option will give you an SMA that does the same thing as the EMA. You can also disable the RSI filter and simply have a moving average that changes color when the price is above/below- but that's pretty boring, huh?

Anyways, hope this helps, happy trading everybody :)

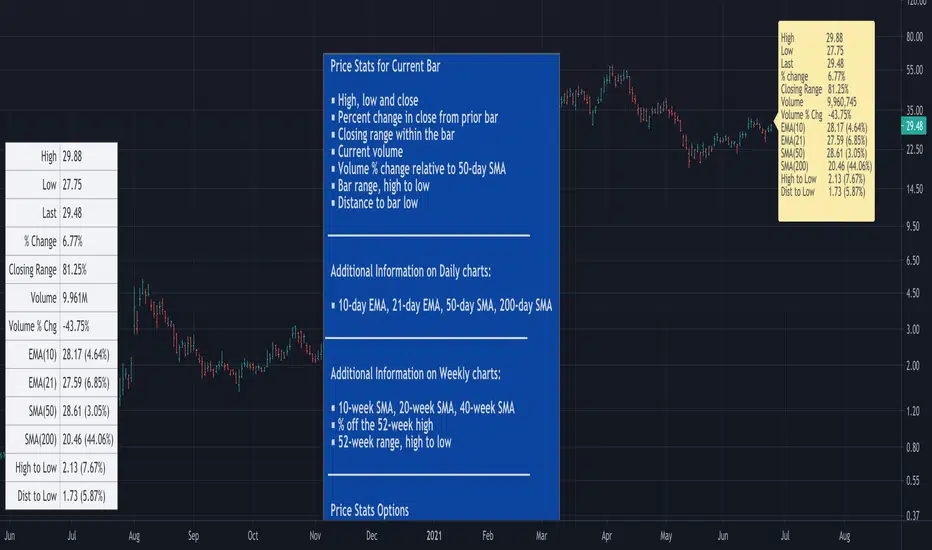

Price Stats / Price Data [LevelUp]Introduction

Price Stats is an indicator based on the statistics shown in MarketSmith charting software when viewing the Track Price information, also known as the "yellow box."

The following stats are available for the most recent price bar:

■ High price

■ Low price

■ Last price

■ Percent change in price from prior bar

■ Closing range within the bar

■ Current volume

■ Volume % change relative to the 50-day moving average volume

For daily charts:

■ 21-day EMA and % offset of price

■ 50-day SMA and % offset of price

■ 200-day SMA and % offset of price

Here's how to interpret the moving averages:

In the image below the 50-day SMA is 74.58 (8.04%). 74.58 represents the value of the 50-day SMA. 8.04% indicates that the current price is 8.04% above the SMA. A negative % would indicate the current price is the specified % below the SMA.

Combined Momentum MA (Equal-Length EMA/SMA Crossover)Overview:

This momentum and trend-following strategy captures the majority of any trending move, and works well on high timeframes.

It uses an equal-period EMA and SMA crossover to detect trend acceleration/deceleration, since an EMA places a greater weight and significance on the most recent data.

To reduce noise and optimize entries, we combined this with an overall trend bias for further confluence.

How it works:

Signals are determined by the crossover of an EMA and SMA of the same length, e.g. EMA-50 and SMA-50.

The overall trend bias is determined using a slower SMA golden/death cross, e.g. SMA-50 and SMA-100.

The signal is stronger when it occurs in confluence with the overall trend bias, e.g. when EMA-50 crosses over SMA-50, while above the SMA-100. This is analogous to only opening long positions in a bull market.

Indicator description:

GREEN: Up Trend (EMA is above SMA, while EMA is above BIAS_MA. This shows a bullish confluence.)

YELLOW: No Trend (EMA/SMA crossover and BIAS_MA are not in confluence.)

RED = Down Trend (EMA is below SMA, while EMA is below BIAS_MA. This shows a bearish confluence.)

Equal-Length EMA/SMA Crossover Momentum StrategyOverview:

This momentum and trend-following strategy captures the majority of any trending move, and works well on high timeframes.

It uses an equal-period EMA and SMA crossover to detect trend acceleration/deceleration, since an EMA places a greater weight and significance on the most recent data.

This version is optimized for longs, and designed to cut your losses quickly and let your winners run.

To reduce noise and optimize entries, we combined this with an overall trend bias for further confluence.

How it works:

Signals are determined by the crossover of an EMA and SMA of the same length, e.g. EMA-50 and SMA-50.

The overall trend bias is determined using a slower SMA golden/death cross, e.g. SMA-50 and SMA-100.

The signal is stronger when it occurs in confluence with the overall trend bias, e.g. when EMA-50 crosses over SMA-50, while above the SMA-100. This is analogous to only opening long positions in a bull market.

Signal description:

Trend Buy: EMA crosses above SMA, and overall trend bias is bullish. Buying is in confluence with the overall trend bias.

Risky Buy: EMA crosses above SMA, and overall trend bias is bearish. Buying is early, more risky, and not in confluence with the overall trend bias.

Late Buy: SMA crosses above BIAS_SLOW. This gives further confirmation of bullish trend, but signal comes later.

Sell: EMA crosses under SMA.

Strategy entry and exit conditions:

This version enters a Long when "TREND BUY" is signalled.

This version has Sell/Shorts disabled because UP ONLY.

Long entry: Strategy enters Long when EMA is above SMA, while overall trend bias is bullish.

Long exit: Close long when EMA crosses under SMA.

Equal-Length EMA/SMA Crossover Momentum Signal V1Overview:

This momentum and trend-following strategy captures the majority of any trending move, and works well on high timeframes.

It uses an equal-period EMA and SMA crossover to detect trend acceleration/deceleration, since an EMA places a greater weight and significance on the most recent data.

This version is optimized for longs, and designed to cut your losses quickly and let your winners run.

To reduce noise and optimize entries, we combined this with an overall trend bias for further confluence.

How it works:

Signals are determined by the crossover of an EMA and SMA of the same length, e.g. EMA-50 and SMA-50.

The overall trend bias is determined using a slower SMA golden/death cross, e.g. SMA-50 and SMA-100.

The signal is stronger when it occurs in confluence with the overall trend bias, e.g. when EMA-50 crosses over SMA-50, while above the SMA-100. This is analogous to only opening long positions in a bull market.

Signal description:

Trend Buy: EMA crosses above SMA, and overall trend bias is bullish. Buying is in confluence with the overall trend bias.

Risky Buy: EMA crosses above SMA, and overall trend bias is bearish. Buying is early, more risky, and not in confluence with the overall trend bias.

Late Buy: SMA crosses above BIAS_SLOW. This gives further confirmation of bullish trend, but signal comes later.

Sell: EMA crosses under SMA.

Everything RSIThis indicator includes:

RSI Candles set to the default 14 length (un check Borders in the Style tab to see the candlesticks better)

I like using the wicks as an early warning for a possible trend change, which is generally in the opposite direction of the wicks.

It's also easier for me to draw trend lines using the RSI Candles vs the rsi plot line.

40 ema of the RSI Candles

2nd RSI set to the 20 length , which plots just inside the wicks of the RSI Candles. This RSI also highlights Oversold and Overbought levels.

I sometimes leave the RSI Candle Borders checked and use the 20 RSI plot with the wicks of the RSI Candles

Signals to look for Short or Long opportunities , which use the 5 sma of the RSI Candles crossing under the overbought and over the

oversold levels. If you'd like to plot the 5 sma, remove the // at the beginning of the code on line 72.

3nd RSI set to the default 14 length which can be set to a different timeframe as the current chart. Default setting is the 1h.

This RSI plots a + at the top of the indicator when it's above the 50 level and an x at the bottom of the indicator when it's below the 50 level.

For me, this is just a visual aid when I'm scalping on lower timeframes.

If the 1h RSI is above the 50 level, I focus on long scalps. If the 1h RSI is below the 50 level, I focus on short scalps.

RSI Cloud which is formed by filling in the area between the 14 ema of both the 7 RSI and 28 RSI.

I used part of @FnM_Capital 's Trend-Sniper script for my RSI Candles. Thank you! You're extremely talented and deserve all of the credit for your work.

I'd also like to thank @SeanNance for answering all of my random coding questions!!!

I've added the indicator to the example twice to show a couple of the ways I view the RSI's.

The top indicator shows the RSI Candle Borders "un checked" and without the 2nd RSI plot.

The bottom indicator shows RSI Candle Borders "checked", using 2nd RSI plot with the RSI Candle Wicks.

CyclesThis is a modified Stochastic indicator. Modifications include:

1. The output is now centered on "0" and the scale is from -50 to +50, so that histograms and columns can be used to plot the output.

2. Added visual trade setup triggers. A trigger to the up side is a cycle high and indicates a "sell signal". A trigger to the down side is a cycle low and indicates a "buy" signal.

3. Added an alert trigger to be used to setup alerts. Selecting "Alert" to be Greater Than (>) Value = 0.00 will trigger an alert if either the buy or sell triggers occur.

4. Added a force indicator output. This indicates the rate of change in "D", or mathematically "dD/dt", as was done in the Power Analyzer indicator. When Force and D are in-phase, the maximum power is achieved.

5. Added "Slow Average Momentum" and "Slow Average Force" as was done in the Power Analyzer indicator.

6. Added an internal MACD and EMA as part of the trade setup trigger equation. There is a new input variable for the EMA length.

7. Added an input variable for the "Trigger Threshold", which ranges from -50 to 50, to be used as a screening filter.

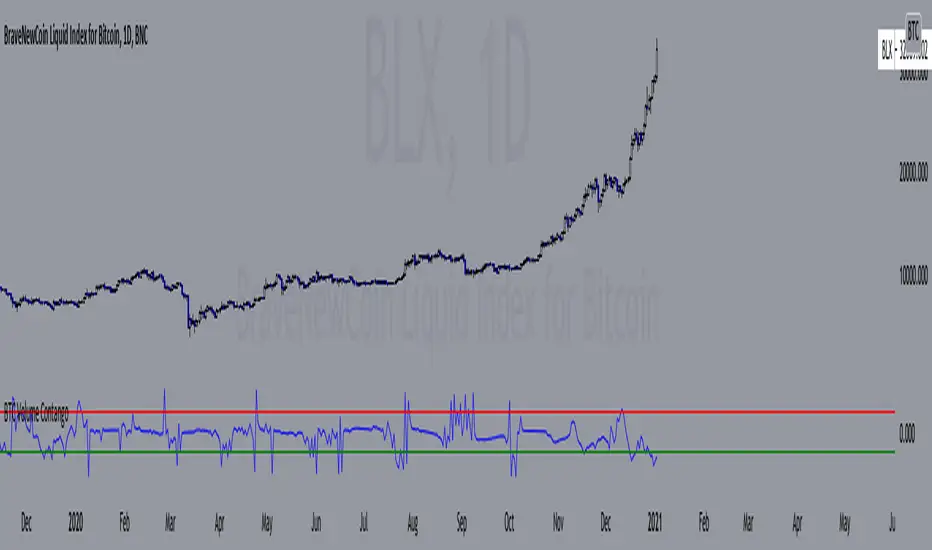

BTC Volume Contango IndexBased on my previous script "BTC Contango Index" which was inspired by a Twitter post by Byzantine General:

This is a script that shows the contango between spot and futures volumes of Bitcoin to identify overbought and oversold conditions. When a market is in contango, the volume of a futures contract is higher than the spot volume. Conversely, when a market is in backwardation, the volume of the futures contract is lower than the spot volume.

The aggregate daily volumes on top exchanges are taken to obtain Total Spot Volume and Total Futures Volume. The script then plots (Total Futures Volume/Total Spot Volume) - 1 to illustrate the percent difference (contango) between spot and futures volumes of Bitcoin. This data by itself is useful, but because aggregate futures volumes are so much larger than spot volumes, no negative values are produced. To correct for this, the Z-score of contango is taken. The Z-score (z) of a data item x measures the distance (in standard deviations StdDev) and direction of the item from its mean (U):

Z-score = (x - U) / StDev

A value of zero indicates that the data item x is equal to the mean U, while positive or negative values show that the data item is above or below the mean (x Values of +2 and -2 show that the data item is two standard deviations above or below the chosen mean, respectively, and over 95.5% of all data items are contained within these two horizontal references). We substitute x with volume contango C, the mean U with simple moving average ( SMA ) of n periods (50), and StdDev with the standard deviation of closing contango for n periods (50), so the above formula becomes: Z-score = (C - SMA (50)) / StdDev(C,50).

When in contango, Bitcoin may be overbought.

When in backwardation, Bitcoin may be oversold.

The current bar calculation will always look incorrect due to TV plotting the Z-score before the bar closes.

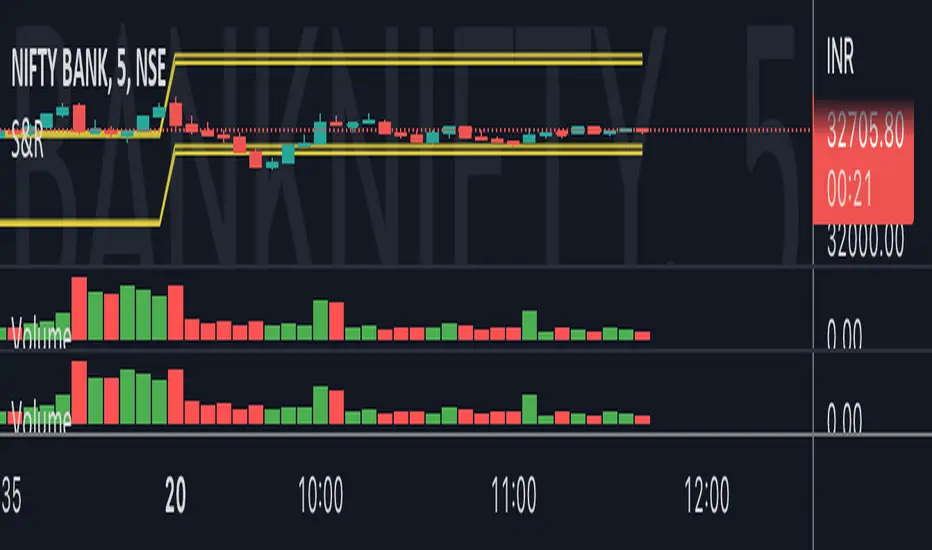

Bank Nifty VolumeWhy this Script : Nifty 50 does not provide volume and some time it is really useful to understand the volume .

This is the pine script which calculate the nifty 50 volume .

Logic :

Take each stock contribute to nifty 50 and find it's volume .

Multiply the same with contribution percentage of the same on Nifty 50

Add up all of them and find the total volume .

I took the open source code from @daytraderph script called, Custom Volume

I will make sure I will update the contribution percentage of all stocks my self instead o you update using input methods. This is the difference. Some people don't know where to look at this to update the value, so for them this script might be useful. And this is the only difference comparing to Custom Volume script.

Probability: Bull/Bear Dominance | Ratio | Bar CountIntro

What's the probability of the next bar being red? How about green? Well, there are many ways to quantify the probability but I am presenting just one stupidly simple (but generally accurate) way to measure it.

Strangely... no one has done this before that I can find. I try to check if someone else has done it first (Pro Tip: Plz do this. We honestly don't need the 5 trillionth "MTF MAs" script.)

Indicator

Its a basic counting script, but the nice thing about this script is you choose the time range. It starts counting from a specified point of your choosing. It counts up the bull bars and bear bars separately.

Bull Bar = Close > Open

Bear Bar = Open > Close

You can look at them in sum or as a ratio of Green Bars : Red Bars

I know, it's almost too simple. But, here's some interesting food for thought from a layman to fellow laymen.

Analysis/Edge

Between the time of candle open and candle close, the price can do one of three things, close higher, close lower, or close equal to.

'Equal to' is rare on higher timeframes in liquid markets and it provides no useful information. Thus, we'll nix it for purposes of this conversation.

So boil it down. The next candle is going to be a red candle or a green candle.

It is popular to refer to the general probability of most candles as 50/50, with trader's mission in life being to seek an edge that tilts the probabilities slightly in their favor.

The truth is the odds are probably never actually 50/50, but knowing the precisely correct probability is unknowable, just like the accuracy of a weather forecast is inherently unknowable. What we're trying to do as traders is develop systems that give us predictive probabilistic outcomes that correspond with future realities based on various ways of measuring the market (most often heavily dependent on the past).

The reality is that the market can be measured in many, many different ways. The important thing is that you measure it in a way that is accurate, relevant, and universally applicable.

So look at this indicator here:

You start from a point in time on a chosen timeframe and you put red bars in the red column, green in the green column, and count them all up.

Then you make a ratio, in this case, Green : Red.

What the ratio shows you is the percentage of green bars compared to red bars . At the time of this screenshot, the 4h on the SPX starting from the 2020 bottom is showing a ratio of 1.2.

This means there have been 20% more green bars than there have been red bars.

Now there are 1,000 directions you can take this discussion. What is the overall volatility picture, the size of the red bars vs the green bars, what happens if you miss out on the 5 biggest green bars... so many more variables that you would need to take into account to develop a true edge from this idea. But, the bottom line fact (which is what I like about this) is that we can take this data and say with a certain level of confidence that on the SPX you have a 20% better shot at making money (otherwise stated there's a 60/40 chance) if you open a LONG trade at the beginning of a 4h candle than if you open a short.

That's useful information. One could argue that it's not a complete strategy in and of itself (although I bet it could be with a couple of additional parameters). But I can tell you, based on the 4h candles in the 2020 rally if you open a short, the deck is stacked against you from this perspective. And we can actually somewhat demonstrate this to be true for our dataset because we can look at the price history and see who likely made more money. The SPX is up 1000pts off the bottom. So, thus far, for this dataset, it rings true; Bulls have been doing way better in the latter part of 2020 than the bears.

Conclusion

Predictive systems with a small number of variables tend to be more robust than a system with many variables when applied to a complex system. I may keep updating this script if people like it and determine aspects like population vs sample size, confidence intervals, volatility, and exclusion of outliers. For now, this is just an opening foray into the basic idea of how we can establish an edge in the markets. It really can be this simple.

Thanks for Reading.

WR% VARIATIONThis indicator plot the change of the William R%.

We have 3 hlines, 50, 0, -50

You can use this as a confirmation indicator for different entries:

ENTRIES

When change is higher than 50 we have a strong LONG signal

When change is lower than -50 we have a strong SHORT signal

CONTINUATION TRADES

When we are in a Bull Market, candle is red and change crossover the 0 line, we have a LONG continuation trade

When we are in a Bear Market, candle is green and change crossunder the 0 line, we have a SHORT continuation trade

EXITS

When we are in a Bull Market, candle is green and change crossunder the 0 line, we have an Exit, or a Reversal

When we are in a Bear Market, candle is read and change crossover the 0 line, we have an Exit, or a Reversal

RISK-OFF.RISK.ON-ppxdf.v3======================================= RISK-OFF & RISK ON INDEX ================================================

1. Stock Price Momentum: Measuring the Standard & Poor's 500 Index ( S&P 500 ) versus its 125-day moving average (MA)

2. Stock Price Strength: Calculating the number of stocks hitting 52-week highs versus those hitting 52-week lows on the New York Stock Exchange (NYSE)

3. Stock Price Breadth: Analyzing trading volumes in rising stocks against declining stocks

4. Put and Call Options: How much do put options lag behind call options, signifying greed, or surpass them, indicating fear

5. Junk Bond Demand: Gauging appetite for higher risk strategies by measuring the spread between yields on investment-grade bonds and junk bonds

6. Market Volatility: CNN measures the Chicago Board Options Exchange Volatility Index ( VIX ), concentrating on a 50-day MA

7. Safe Haven Demand: The difference in returns for stocks versus treasuries

Each of these seven indicators is measured on a scale from 0 to 100, with the index being computed by taking an equal-weighted average of each of them.

A reading of 50 is deemed NEUTRAL.

Above 50 signals the market with RISK-ON. (GREED)

Below 50, Signals the market with RISK-OFF (FEAR)

8

Ultimate Moving Average Package (17 MA's)Included is the:

VWAP

Current time frame 10 EMA

Current time frame 20 EMA

Current time frame 50 EMA

Current time frame 10 SMA

Current time frame 20 SMA

Current time frame 50 SMA

Daily 10 EMA

Daily 20 EMA

Daily 50 EMA

Daily 50 SMA

Daily 100 SMA

Daily 200 SMA

Weekly 100 SMA

Weekly 200 SMA

Monthly 100 SMA

Monthly 200 SMA

All Daily/Weekly/Monthly MA's can be seen on intraday charts. Current time frame MA's change depending on your time frame. Obviously you dont need all 17 on your chart but you can pick the ones you like and disable the rest.

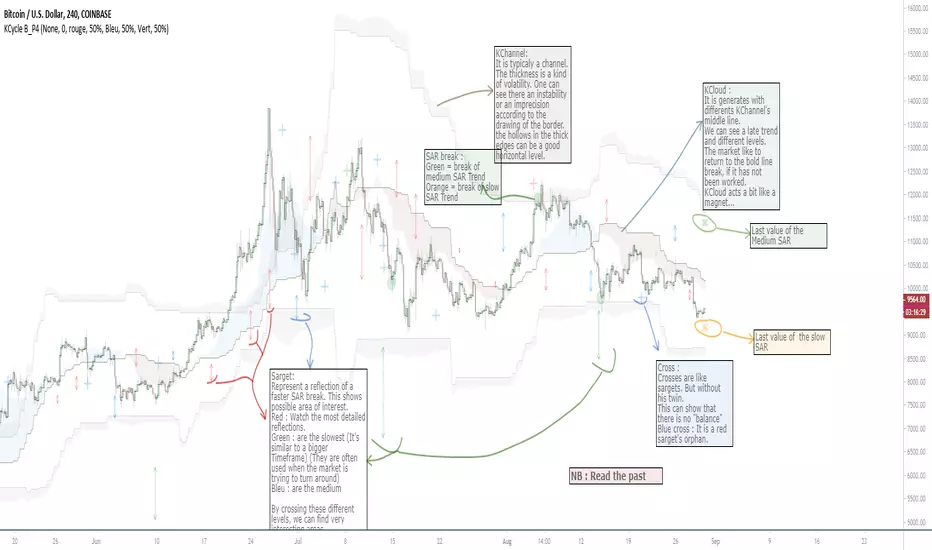

OVL_Kikoocycle Beta_Pine3This script use :

- A custom Chande Kroll Stop for generate the channel

- Some custom Parabolic S.A.R for generate cycles

This script can be separated into 3 categories:

- Channel Kroll generator : one layer for the actual interval and a layer for a Large Timeframe .(with ratio)

- "Range" generator : one layer for actual Interval and a layer for a Large Timeframe.(with automique ratio)

-Targets generator : one layer for actual interval with different trend.

"Channel Kroll" :

- I "hijack" the Chande Kroll Stop formula with custom parameters for generate this channel. Overall, it works like other types of channels like BB, etc... A midline and two borders. The thickness of the borders are relatively important here. A thick border shows some resistance of the area. And so the probability of seeing the market return to its first contact is stronger. While a very thin and vertical border would rather play the role of a breach, a bit like the idea of gaps. Often the market seems to want to go after several cycles.

You can activate its Large TimeFrame version, its midline is strong and fine borders helps to judge the risk.

SARget + "SAR Limited" :

- (S.A.R + targets) The philosophy of this function is simple... When a small cycle is broken, it creates a mark on a higher cycle. So on until the SAR called "SAR Limited". For simplicity, imagine a fractal image but inverted ... Break the small figure, it will mark the larger figure at this time but to get there you still have to make the way to the small figure.

Targets are : cross ("+") for fast targets(hidden by default because, theire work only on lower interval), squares (for medium trend), Xcross(for large trend) and red cross(they try to find a large contexte). When a target proc, it is for later (market need some cycles for going to, but it is relative to your interval). This gives you speculative goals.

Why 2 targets for a same type and a triangle with a 90deg angle : This give a potential area for management.The triangle help to visualize the SAR and to juge the market reaction. You need to adapte your trade with that...

Targets may be slightly too far because I am a bad coder... Currently the targets appear at the moment of rupture but it would be necessary to wait for the end of the breaking movement. Which can bring a positional error if the break is violent.

RnG and LTF RnG :

- Attempt to generate a Fibo range for each cycle and see interressing areas to enter or exit. This is played with the same philosophy as the Fibo extensions and retracement.

When a new RnG is generated, do not rush. It appears showing 50/50 for both sides. When a new RnG is generated, do not rush. It appears showing 50/50 for both sides. As long as the market is out of the middle zone (the 3 lines) keep in mind the past RnG.

When the market is out of range, you can use the FibRetracement tool for have extensions. One point at each end, as on the presentation graph. (Values 1.14, 1.272, 1.414, 1.618, 1.786, 2, 2.4 and 4 work well.) If too extrem you can active the LTF version.

Never fomo a break, market like to pull a level... Observe and be patient.

It's easier to use than to explain xD

NB : Do not use the LTF as context. For this, it is better to look at a higher interval.

I invite you to look in the style tab of the script and deselect the plots named UNCHECKEME, this will ease your browser.

Amazing Crossover System - 100+ pips per day!I got the main concept for this system on another site. While I have made one important change, I must stress that the heart of this system was created by someone else! We must give credit where credit is due!

Y'all know baby pips. @ForexPhantom published about this system and did both back and forward test around 10 years ago.

I found it on the sit and now I put it to code to see how it performs. I assume 10 points spread for every trade. I use Renesource or AxiTrader to get the low spreads.

There are 2 mods, the single trades and constant trading on the direction.

Main concept

Indicators

5 EMA -- YELLOW

10 EMA -- RED

RSI (10 - Apply to Median Price: HL/2) -- One level at 50.

TIME FRAME

1 Hour Only (very important!)

PAIRS

Virtually any pair seems to work as this is strictly technical analysis.

I recommend sticking to the main currencies and avoiding cross currencies (just his preference).

WHEN TO ENTER A TRADE

Enter LONG when the Yellow EMA crosses the Red EMA from underneath.

RSI must be approaching 50 from the BOTTOM and cross 50 to warrant entry.

Enter SHORT when the Yellow EMA crosses the Red EMA from the top.

RSI must be approaching 50 from the TOP and cross 50 to warrant entry.

I've attached a picture which demonstrates all these conditions.

That's it!

f.bpcdn.co

MFIww MFI/RSI_v2[wozdux]A new version of the indicator Mfi_v2. Added new control parameters.

tt - the averaging period of the volume.

Len - the period for calculating the MPI.

nn-averaging period MFI (blue line). level-critical levels from below and above (black horizontal lines).

Level 0 or 50 - switch between different histogram views with the middle at either level 50 or level 0.

key level-key to remove black critical levels.

key ema (MFI, nn) - key to remove mfi averaging (blue line).

key color-key to remove histogram coloring.

key colomns a-line - key switching modes represent the mfi histrogram or line.

---------------------------

Новая версия индикатора MFIww_v2. Добавлены новые управляющие параметры.

tt- период усреднения объема.

Len - период вычисления MFI.

nn- период усреднения MFI (голубая линия).

level- критические уровни снизу и сверху (черные горизонтальные линии).

Level 0 or 50 - переключение между разными представлениями гистрограммы с серединой либо на уровне 50 , либо на уровне 0.

key level- ключ убрать черные критические уровни.

key ema(mfi,nn) - ключ убрать усреднение mfi (голубая линия).

key color- ключ убрать расцветку гистрограммы.

key colomns-line - ключ переключения режимов представления mfi гистрограммой или линией.

GoTiT|Simple Auto Fib v1.0Simple Auto Fib!

Notes:

1. Always set the trend manually! Don't rely on the auto trend detection.

2. The first parameter Length sets the number of candles back (left) to search for highs and lows from the current candle.

3. The High Offset parameter sets the number of candles back (left) to ignore/skip before searching for highs.

4. The Low Offset parameter sets the number of candles back (left) to ignore/skip before searching for lows.

5. The offset parameters change the behavior of the Length parameter.

Example 1:

Length = 100

High Offset = 0

Low Offset = 0

This is the default behavior, and the search for highs and lows occurs on the last 100 candles.

Example 2:

Length = 50

High Offset = 20 (Ignore the last 20 candles, and search for highs starting at candle 21 to 71 (or 50 candles back)

Low Offset = 15 (Ignore the last 15 candles, and search for lows starting at candle 16 to 66 (or 50 candles back)

In example 2, search starts on candle 21 for highs, and candle 16 for lows and extends 50 candles further back from there.

6. The Trend Detection parameter sets the number of candles back (left) to use in the trend calculations. Larger values give better "marco trend" detection. Smaller values give better "micro trend" detection. See note #1.

7. The white fib line is fib0. Assuming you correctly set the trend manually (or the trend is auto detected correctly), in a downtrend fib0 should be bellow the red fib line, and in an uptrend fib0 should be above the red fib line.