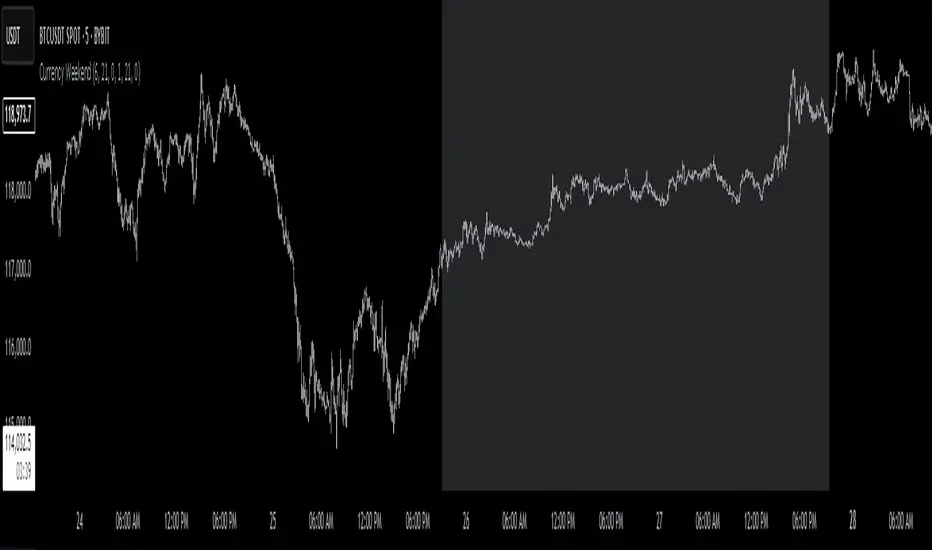

Currency Weekend - shading weekend trading// ─────────────────────────────────────────────────────────────────────────────

// © 2025, Steve / Steven Anthony – "Currency Weekend"

// This script highlights the low-liquidity weekend window that often affects

// both fiat currency markets and cryptocurrencies like Bitcoin.

//

// ╭─────────────────────────────── DESCRIPTION ───────────────────────────────╮

// | This indicator shades a customizable time window on your chart, |

// | originally set to highlight the **forex weekend lull** from |

// | **Friday 21:00 UTC to Sunday 21:00 UTC**, when traditional fiat |

// | currency markets close. |

// | |

// | Traders who observe Bitcoin, Ethereum, or other crypto assets may |

// | notice reduced liquidity or increased erratic moves during this time, |

// | due to overlapping behaviors from professional forex traders who |

// | trade both markets. |

// ╰──────────────────────────────────────────────────────────────────────────╯

//

// 🔧 Flexible Configuration:

// - Define your own start and end **day + time** for shading

// - Useful for shading other custom quiet periods or session transitions

//

// 💡 Use Cases:

// - Avoid trading during low-liquidity periods

// - Spot potential weekend traps or price gaps

// - Align crypto behavior with fiat market hours

//

// 📍 Default Settings:

// - Start: Friday 21:00 UTC

// - End: Sunday 21:00 UTC

//

// Timezone is normalized to the chart’s timezone for seamless integration.

//

// ─────────────────────────────────────────────────────────────────────────────

"如何用wind搜索股票的发行价和份数" için komut dosyalarını ara

Canonical Momenta Indicator [T1][T69]📌 Overview

The Canonical Momenta Indicator models trend pressure using a Lagrangian-based momentum engine combined with reflexivity theory to detect bursts in price movement influenced by herd behavior and volume acceleration.

🧠 Features

Lagrangian-based kinetic model combining velocity and acceleration

Reflexivity burst detection with directional scoring

Adaptive momentum-weighted output (adaptiveCMI)

Buy 🐋 / Sell 🐻 labels when reflexivity confirms direction

Fully parameterized for customization

⚙️ How to Use

This indicator helps traders:

Detect reflexive bursts in market activity driven by sharp price movement + volume spikes

Capture herd-driven directional moves early.

Gauge market pressure using a kinetic-potential energy model.

Suggested signals:

🐋 Reflexive Up: Strong bullish momentum spike confirmed by volume and positive lagrangian pressure

🐻 Reflexive Down: Strong bearish dump confirmed by volume and negative lagrangian burst

🔧 Configuration

MA Lookback Length - Smoothing for baseline price & energy calculation

Reflexivity Momentum Threshold - Price momentum trigger for burst detection

Reflexivity Lookback - Period over which bursts are counted

Reflexivity Window - Minimum burst sum to trigger signal label

Volume Spike Threshold - % above average volume to qualify as burst

📊 Behavior Description

The indicator computes a Lagrangian energy:

Kinetic Energy = (velocity² + 0.5 * acceleration²)

Potential Energy = deviation from moving average (distance²)

Lagrangian = Potential − Kinetic (higher = overextension)

Then, reflexive bursts are triggered when:

Price is rising or falling over short window (burstMvmnt)

Volume is above average by a user-defined multiple

Each bar gets a burst score:

+1 for up-burst

−1 for down-burst

0 otherwise

⚠️ Risk Profile Based on Lookback Settings

Risk Level | Description | Recommended Lookback

🟥 High | Extremely sensitive to bursts, prone to false signals | 7–10

🟨 Moderate | Balanced reflexivity with trend confirmation | 11–20

🟩 Low | Filters out most noise, slower to react | 21+

🧪 Advanced Tips

Combine with moving average slope for trend filtering

Use divergence between adaptiveCMI and price to detect exhaustion

Works well in crypto, commodities, and volatile assets

⚠️ Limitations

Sensitive to high volatility noise if volMult is too low

Designed for higher timeframes (1H, 4H, Daily) for reliability

Doesn’t confirm direction in sideways markets — pair with other filters

📝 Disclaimer

This tool is provided for educational and informational purposes. Always do your own backtesting and use proper risk management.

Trigonometric StochasticTrigonometric Stochastic - Mathematical Smoothing Oscillator

Overview

A revolutionary approach to stochastic oscillation using sine wave mathematical smoothing. This indicator transforms traditional stochastic calculations through trigonometric functions, creating an ultra-smooth oscillator that reduces noise while maintaining sensitivity to price changes.

Mathematical Foundation

Unlike standard stochastic oscillators, this version applies sine wave smoothing:

• Raw Stochastic: (close - lowest_low) / (highest_high - lowest_low) × 100

• Trigonometric Smoothing: 50 + 50 × sin(2π × raw_stochastic / 100)

• Result: Naturally smooth oscillator with mathematical precision

Key Features

Advanced Smoothing Technology

• Sine Wave Filter: Eliminates choppy movements while preserving signal integrity

• Natural Boundaries: Mathematically constrained between 0-100

• Reduced False Signals: Trigonometric smoothing filters market noise effectively

Traditional Stochastic Levels

• Overbought Zone: 80 level (dashed line)

• Oversold Zone: 20 level (dashed line)

• Midline: 50 level (dotted line) - equilibrium point

• Visual Clarity: Clean oscillator panel with clear level markings

Smart Signal Generation

• Anti-Repaint Logic: Uses confirmed previous bar values

• Buy Signals: Generated when crossing above 30 from oversold territory

• Sell Signals: Generated when crossing below 70 from overbought territory

• Crossover Detection: Precise entry/exit timing

Professional Presentation

• Separate Panel: Dedicated oscillator window (overlay=false)

• Price Format: Formatted as price indicator with 2-decimal precision

• Theme Adaptive: Automatically matches your chart color scheme

Parameters

• Cycle Length (5-200): Period for highest/lowest calculations

- Shorter periods = more sensitive, more signals

- Longer periods = smoother, fewer but stronger signals

Trading Applications

Momentum Analysis

• Overbought/Oversold: Clear visual identification of extreme levels

• Momentum Shifts: Early detection of momentum changes

• Trend Strength: Monitor oscillator position relative to midline

Signal Trading

• Long Entries: Buy when crossing above 30 (oversold bounce)

• Short Entries: Sell when crossing below 70 (overbought rejection)

• Confirmation Tool: Use with trend indicators for higher probability trades

Divergence Detection

• Bullish Divergence: Price makes lower lows, oscillator makes higher lows

• Bearish Divergence: Price makes higher highs, oscillator makes lower highs

• Early Warning: Spot potential trend reversals before they occur

Trading Strategies

Scalping (5-15min timeframes)

• Use cycle length 10-14 for quick signals

• Focus on 20/80 level bounces

• Combine with price action confirmation

Swing Trading (1H-4H timeframes)

• Use cycle length 20-30 for reliable signals

• Wait for clear crossovers with momentum

• Monitor divergences for reversal setups

Position Trading (Daily+ timeframes)

• Use cycle length 50+ for major signals

• Focus on extreme readings (below 10, above 90)

• Combine with fundamental analysis

Advantages Over Standard Stochastic

1. Smoother Action: Sine wave smoothing reduces whipsaws

2. Mathematical Precision: Trigonometric functions provide consistent behavior

3. Maintained Sensitivity: Smoothing doesn't compromise signal quality

4. Reduced Noise: Cleaner signals in volatile markets

5. Visual Appeal: More aesthetically pleasing oscillator movement

Best Practices

• Market Context: Consider overall trend direction

• Multiple Timeframe: Confirm signals on higher timeframes

• Risk Management: Always use proper position sizing

• Backtesting: Test parameters on your preferred instruments

• Combination: Works excellently with trend-following indicators

Built-in Alerts

• Buy Alert: Trigonometric stochastic oversold crossover

• Sell Alert: Trigonometric stochastic overbought crossunder

Technical Specifications

• Pine Script Version: v6

• Panel: Separate oscillator window

• Format: Price indicator with 2-decimal precision

• Performance: Optimized for all timeframes

• Compatibility: Works with all instruments

Free and open-source indicator. Modify, improve, and share with the community!

Educational Value: Perfect for traders wanting to understand how mathematical smoothing improves oscillators and trigonometric applications in technical analysis.

ORB Range Indicator with Fibonacci Targets

This script plots the Opening Range (ORB) high and low based on a configurable time window (5–45 minutes from the U.S. session open at 9:30 AM EST).

Once the ORB window closes, the indicator draws horizontal lines marking:

ORB High and Low

The size of the range in price and %

Fibonacci-based price targets above and below the range (0.382, 0.618, 1.000, 1.618, 2.000)

You can control:

Which Fibonacci levels to display

Whether to show long targets, short targets, or both

All drawings are automatically cleared at the start of each trading day.

Ideal for breakout traders using ORB and Fibonacci extensions for target planning.

Midnight 30min High/LowMidnight 30min High/Low — Overnight Liquidity Range Tracker

Capture the Overnight Session: A Strategic Level Identification Tool from Professional Trading Methodology

This indicator captures the high and low prices during the critical 30-minute midnight session (12:00-12:30 AM EST) and projects these levels forward as key support and resistance zones. These overnight ranges often contain significant liquidity and serve as crucial reference points for intraday price action, representing areas where institutional activity may have established important levels.

🔍 What This Script Does:

Identifies Critical Overnight Session Levels

- Automatically detects the 12:00-12:30 AM EST session window

- Captures the highest and lowest prices during this 30-minute period

- Projects these levels forward for multiple trading days

Creates Dynamic Support/Resistance Zones

- Extends midnight high/low levels as horizontal lines with customizable projection periods

- Fills the area between high and low to create a visual trading range

- Updates automatically each trading day with new overnight levels

Provides Clear Visual Reference Points

- Optional session start markers (●) highlight when the midnight session begins

- Color-coded lines distinguish between high and low levels

- Transparent fill area creates an easy-to-identify trading zone

Real-Time Level Tracking

- Updates levels in real-time during the active midnight session

- Maintains historical levels for reference and backtesting

- Compatible with data window for precise level values

⚙️ Customization Options:

Extend Days (1-30):** Control how many days forward the levels are projected (default: 5 days)

High Line Color:** Customize the midnight high line color (default: blue)

Low Line Color:** Customize the midnight low line color (default: orange)

Fill Color:** Adjust the transparency and color of the range area (default: light aqua, 80% transparency)

Show Session Markers:** Toggle yellow session start indicators on/off (default: enabled)

💡 How to Use:

Deploy on lower timeframes (1m-15m) for precise level identification and reaction monitoring**

Watch for key price interactions:

- Rejection at midnight high levels (potential resistance)

- Bounce from midnight low levels (potential support)

- Range-bound trading between the high and low levels

Combine with liquidity concepts:

- Monitor for stop hunts above/below these levels

- Look for false breakouts that snap back into the range

- Use as confluence with other ICT concepts like FVGs and Order Blocks

Strategic Applications:

- Range trading between midnight levels

- Breakout confirmation when price closes decisively outside the range

- Support/resistance validation for entry and exit planning

🔗 Combine With These Tools for Complete Market Structure Analysis:

✅ First FVG — Opening Range Fair Value Gap Detector.

✅ ICT Turtle Soup (Liquidity Reversal)— Spot stop hunts and false breakout scenarios

✅ ICT Macro Zones (Grey Box Version)- It tracks real-time highs and lows for each Silver Bullet session

✅ ICT SMC Liquidity Grabs and OBs- Liquidity Grabs, Order Block Zones, and Fibonacci OTE Levels, allowing traders to identify institutional entry models with clean, rule-based visual signals.

Together, these tools create a comprehensive Smart Money Concepts (SMC) framework — helping traders identify, anticipate, and capitalize on institutional-level price movements with precision and confidence during critical overnight sessions.

Initial Balance Wave MapThis indicator visualizes the Initial Balance (IB) range for any session, marking the first hour's high and low. It includes optional midpoints, extensions (e.g. 1.5x IB, 2x IB), and customizable time windows. Additional features allow users to display session open, high, low, close, and VWAP reference points. Designed to support price action and session structure analysis, it adapts to various global futures and FX market opens. All display elements are optional and fully configurable.

This updated indicator builds upon the open-source foundation by @noop-noop with enhancements and user-facing labels tailored for Auction Market Theory, scalping, and structure-based trade setups.

Key updated Featured: Multiple previous day's IB levels carry forward into the current day's chart, as opposed to just the previous day's levels carrying forward to the new IB time.

🙌 Credits:

This script builds upon the excellent open-source work by @noop-noop. Original script available here .

Alt Szn Oracle - Institutional GradeThe Alt Szn Oracle is a macro-level indicator built to help traders front-run altseason by tracking liquidity, dominance rotation, sentiment, and capital flows—all in one signal. It’s designed for those who don’t just chase pumps, but want to understand when the tide is turning and why. This tool doesn't predict specific coin breakouts—it tells you when the market as a whole is gearing up to rotate into higher beta assets like altcoins, including memes and microcaps.

The index consolidates ten macro inputs into a normalized, smoothed score from 0–100. These include Bitcoin and Ethereum dominance, ETH/BTC, altcoin market cap (Total3), relative volume flows, and stablecoin supply (USDT, USDC, DAI)—which act as proxies for risk-on appetite and dry powder entering the system. It also incorporates manually updated sentiment metrics from Google Trends and the Fear & Greed Index, giving it a behavioral edge that most indicators lack.

The logic is simple but powerful: when BTC dominance is falling, ETH/BTC is rising, altcoin volume increases relative to BTC/ETH, and stablecoins start moving—you're likely in the early innings of rotation. The index is also filtered through a volatility threshold and smoothed with an EMA to eliminate chop and fakeouts.

Use this indicator on macro charts like TOTAL3, TOTAL2, or ETHBTC to gauge market health, or overlay it on specific coins like PEPE, DOGE, or SOL to confirm if the tide is in your favor. Interpreting the score is straightforward: readings above 80 suggest euphoria and signal it’s time to de-risk, 60–80 indicates expansion and confirms altseason is underway, 40–60 is neutral, and 20–40 is a capitulation zone where smart money accumulates.

What sets this apart is that it doesn’t just track price—it reflects the flow of capital, the positioning of liquidity, and the sentiment of the crowd. Most altseason indicators are lagging, overfitted, or too simplistic. This one is modular, forward-looking, and grounded in real capital rotation theory.

If you're a trader who wants to time the cycle, not guess it, this is your tool. Refine it, fork it, or expand it to your niche—DeFi, NFTs, meme coins, or L1s. It’s a framework for reading the macro winds, not a signal service. Use it with discipline, and you’ll catch the wave while others drown in noise.

Staccked SMA - Regime Switching & Persistance StatisticsThis indicator is designed to identify the prevailing market regime by analyzing the behavior of a "stack" of Simple Moving Averages (SMAs). It helps you understand whether the market is currently trending, mean-reverting, or moving randomly.

Core Concept: SMA Correlation

At its heart, the indicator examines the relationship between a set of nine SMAs with different lengths (3, 5, 8, 13, 21, 34, 55, 89, 144) and the lengths themselves.

In a strong trending market (either up or down), the SMAs will be neatly "stacked" in order of their length. The shortest SMA will be furthest from the longest SMA, creating a strong, almost linear visual pattern. When we measure the statistical correlation between the SMA values and their corresponding lengths, we get a value close to +1 (perfect uptrend stack) or -1 (perfect downtrend stack). The absolute value of this correlation will be very high (close to 1).

In a mean-reverting or sideways market, the SMAs will be tangled and crisscrossing each other. There is no clear order, and the relationship between an SMA's length and its price value is weak. The correlation will be close to 0.

This indicator calculates this Pearson correlation on every bar, giving a continuous measure of how ordered or "trendy" the SMAs are. An absolute correlation above 0.8 is considered strongly trending, while a value between 0.4 and 0.8 suggests a mean-reverting character. Below 0.4, the market is likely random or choppy.

Regime Classification and Statistics

The indicator doesn't just look at the current correlation; it analyzes its behavior over a user-defined lookback window (default is 252 bars) to classify the overall market "regime."

It presents its findings in a clear table:

📊 |SMA Correlation| Regime Table: This main table provides a snapshot of the current market character.

Median: Shows the median absolute correlation over the lookback period, giving a central tendency of the market's behavior.

% > 0.80: The percentage of time the market was in a strong trend during the lookback period.

% < 0.80 & > 0.40: The percentage of time the market showed mean-reverting characteristics.

🧠 Regime: The final classification. It's labeled "📈 Trend-Dominant" if the median correlation is high and it has spent a significant portion of the time trending. It's labeled "🔄 Mean-Reverting" if the median is in the middle range and it has spent significant time in that state. Otherwise, it's considered "⚖️ Random/ Choppy".

📐 Regime Significance: This tells you how statistically confident you can be in the current regime classification, using a Z-score to compare its occurrence against random chance. ⭐⭐⭐ indicates high confidence (99%), while "❌ Not Significant" means the pattern could be random.

Regime Transition Probabilities

Optionally, a second table can be displayed that shows the historical probability of the market transitioning from one regime to another over different time horizons (t+5, t+10, t+15, and t+20 bars).

📈 → 🔄 → ⚖️ Transition Table: This table answers questions like, "If the market is trending now (From: 📈), what is the probability it will be mean-reverting (→ 🔄) in 10 bars?"

This provides powerful insights into the market's cyclical nature, helping you anticipate future behavior based on past patterns. For example, you might find that after a period of strong trending, a transition to a choppy state is more likely than a direct switch to a mean-reverting

Indicator Settings

Lookback Window for Regime Classification: This sets the number of recent bars (default is 252) the script analyzes to determine the current market regime (Trending, Mean-Reverting, or Random). A larger number provides a more stable, long-term view, while a smaller number makes the classification more sensitive to recent price action.

Show Regime Transition Table: A simple toggle (on/off) to show or hide the table that displays the probabilities of the market switching from one regime to another.

Lookback Offset for Starting Regime: This determines the "starting point" in the past for calculating regime transitions. The default is 20 bars ago. The script looks at the regime at this point and then checks what it became at later points.

Step 1, 2, 3, 4 Offset (bars): These define the future time intervals (5, 10, 15, and 20 bars by default) for the transition probability table. For example, the script checks the regime at the "Lookback Offset" and then sees what it transitioned to 5, 10, 15, and 20 bars later.

Significance Filter Settings

Use Regime Significance Filter: When enabled, this filter ensures that the regime transition statistics only count transitions that were "statistically significant." This helps to filter out noise and focus on more reliable patterns.

Min Stars Required (1=90%, 2=95%, 3=99%): This sets the minimum confidence level required for a regime to be included in the transition statistics when the significance filter is on.

1 ⭐: Requires at least 90% confidence.

2 ⭐⭐: Requires at least 95% confidence (default).

3 ⭐⭐⭐: Requires at least 99% confidence.

Time Period Highlighter V2This indicator highlights custom time periods on any intraday chart in TradingView, making it easier to visualize your preferred trading sessions.

You can define up to three separate time ranges per day, each with precise start and end times down to the minute (e.g., 08:30 - 12:15, 14:00 - 16:45, and 20:00 - 22:30). The indicator shades the background of your chart during these periods, helping you quickly identify when you're most active or when specific market conditions occur.

Key Features:

Set start and end times (hours and minutes) for up to three trading sessions.

Automatically highlights these periods across any intraday timeframe.

Uses 24-hour time format aligned with your TradingView chart timezone.

Perfect for day traders, scalpers, or anyone needing clear visual cues for their trading windows.

This tool is especially useful for reviewing trading strategies, backtesting, or ensuring you're focusing on high-probability market hours.

Tip: Double-check that your chart timezone matches your desired session times for accurate highlighting.

Greer Value Yields Line📈 Greer Value Yields Line – Valuation Signal Without the Clutter

Part of the Greer Financial Toolkit, this streamlined indicator tracks four valuation-based yield metrics and presents them clearly via the Data Window, GVY Score badge, and an optional Yield Table:

Earnings Yield (EPS ÷ Price)

FCF Yield (Free Cash Flow ÷ Price)

Revenue Yield (Revenue per Share ÷ Price)

Book Value Yield (Book Value per Share ÷ Price)

✅ Each yield is compared against its historical average

✅ A point is scored for each metric above average (0–4 total)

✅ Color-coded GVY Score badge highlights valuation strength

✅ Yield trend-lines Totals (TVAVG & TVPCT) help assess direction

✅ Clean layout: no chart clutter – just actionable insights

🧮 GVY Score Color Coding (0–4):

⬜ 0 = None (White)

⬜ 1 = Weak (Gray)

🟦 2 = Neutral (Aqua)

🟩 3 = Strong (Green)

🟨 4 = Gold Exceptional (All metrics above average)

Total Value Average Line Color Coding:

🟥 Red – Average trending down

🟩 Green – Average trending up

Ideal for long-term investors focused on fundamental valuation, not short-term noise.

Enable the table and badge for a compact yield dashboard — or keep it minimal with just the Data Window and trend-lines.

Range Bar Gaps DetectorRange Bar Gaps Detector

Overview

The Range Bar Gaps Detector identifies price gaps across multiple range bar sizes (12, 24, 60, and 120) on any trading instrument, helping traders spot potential support/resistance zones or breakout opportunities. Designed for Pine Script v6, this indicator detects gaps on range bars and exports data for use in companion scripts like Range Bar Gaps Overlap, making it ideal for multi-timeframe gap analysis.

Key Features

Multi-Range Gap Detection: Identifies gaps on 12, 24, 60, and 120-range bars, capturing both bullish (gap up) and bearish (gap down) price movements.

Customizable Sensitivity: Includes a user-defined minimum deviation (default: 10% of 14-period SMA) for 12-range gaps to filter out noise.

7-Day Lookback: Automatically prunes gaps older than 7 days to focus on recent, relevant price levels.

Data Export: Serializes up to 10 gaps per range (tops, bottoms, start bars, highest/lowest prices, and age) for seamless integration with overlap analysis scripts.

Debugging Support: Plots gap counts and aggregation data in the Data Window for easy verification of detected gaps.

How It Works

The indicator aggregates price movements to simulate higher range bars (24, 60, 120) from a base range bar chart. It detects gaps when the price jumps significantly between bars, ensuring gaps meet the minimum deviation threshold for 12-range bars. Gaps are stored in arrays, serialized for external use, and pruned after 7 days to maintain efficiency.

Usage

Add to your range bar chart (e.g., 12-range) to detect gaps across multiple ranges.

Use alongside the Range Bar Gaps Overlap indicator to visualize gaps and their overlaps as boxes on the chart.

Check the Data Window to confirm gap counts and sizes for each range (12, 24, 60, 120).

Adjust the "Minimal Deviation (%) for 12-Range" input to control gap detection sensitivity.

Settings

Minimal Deviation (%) for 12-Range: Set the minimum gap size for 12-range bars (default: 10% of 14-period SMA).

Range Sizes: Fixed at 24, 60, and 120 for higher range bar aggregation.

Notes

Ensure the script is published under your TradingView username (e.g., GreenArrow2005) for use with companion scripts.

Best used on range bar charts to maintain consistent gap detection.

For advanced overlap analysis, pair with the Range Bar Gaps Overlap indicator to highlight zones where gaps from different ranges align.

Ideal For

Traders seeking to identify key price levels for support/resistance or breakout strategies.

Multi-timeframe analysts combining gap data across various range bar sizes.

Developers building custom indicators that leverage gap data for advanced charting.

Frahm Factor Position Size CalculatorThe Frahm Factor Position Size Calculator is a powerful evolution of the original Frahm Factor script, leveraging its volatility analysis to dynamically adjust trading risk. This Pine Script for TradingView uses the Frahm Factor’s volatility score (1-10) to set risk percentages (1.75% to 5%) for both Margin-Based and Equity-Based position sizing. A compact table on the main chart displays Risk per Trade, Frahm Factor, and Average Candle Size, making it an essential tool for traders aligning risk with market conditions.

Calculates a volatility score (1-10) using true range percentile rank over a customizable look-back window (default 24 hours).

Dynamically sets risk percentage based on volatility:

Low volatility (score ≤ 3): 5% risk for bolder trades.

High volatility (score ≥ 8): 1.75% risk for caution.

Medium volatility (score 4-7): Smoothly interpolated (e.g., 4 → 4.3%, 5 → 3.6%).

Adjustable sensitivity via Frahm Scale Multiplier (default 9) for tailored volatility response.

Position Sizing:

Margin-Based: Risk as a percentage of total margin (e.g., $175 for 1.75% of $10,000 at high volatility).

Equity-Based: Risk as a percentage of (equity - minimum balance) (e.g., $175 for 1.75% of ($15,000 - $5,000)).

Compact 1-3 row table shows:

Risk per Trade with Frahm score (e.g., “$175.00 (Frahm: 8)”).

Frahm Factor (e.g., “Frahm Factor: 8”).

Average Candle Size (e.g., “Avg Candle: 50 t”).

Toggles to show/hide Frahm Factor and Average Candle Size rows, with no empty backgrounds.

Four sizes: XL (18x7, large text), L (13x6, normal), M (9x5, small, default), S (8x4, tiny).

Repositionable (9 positions, default: top-right).

Customizable cell color, text color, and transparency.

Set Frahm Factor:

Frahm Window (hrs): Pick how far back to measure volatility (e.g., 24 hours). Shorter for fast markets, longer for chill ones.

Frahm Scale Multiplier: Set sensitivity (1-10, default 9). Higher makes the score jumpier; lower smooths it out.

Set Margin-Based:

Total Margin: Enter your account balance (e.g., $10,000). Risk auto-adjusts via Frahm Factor.

Set Equity-Based:

Total Equity: Enter your total account balance (e.g., $15,000).

Minimum Balance: Set to the lowest your account can go before liquidation (e.g., $5,000). Risk is based on the difference, auto-adjusted by Frahm Factor.

Customize Display:

Calculation Method: Pick Margin-Based or Equity-Based.

Table Position: Choose where the table sits (e.g., top_right).

Table Size: Select XL, L, M, or S (default M, small text).

Table Cell Color: Set background color (default blue).

Table Text Color: Set text color (default white).

Table Cell Transparency: Adjust transparency (0 = solid, 100 = invisible, default 80).

Show Frahm Factor & Show Avg Candle Size: Check to show these rows, uncheck to hide (default on).

AZ Dynamic Trend Indicator with Heikin-Ashi### Dynamic Trend Indicator with Heikin-Ashi (v2.7)

**Effortlessly identify trends and reversals** with this versatile tool combining multi-timeframe analysis, adaptive moving averages, and Heikin-Ashi smoothing. Here's what it offers:

#### 🔍 **Core Features**

1. **Dual Timeframe Analysis**:

- Track trends on higher timeframes (e.g., 1H/D) while viewing signals on your current chart.

- Toggle between **Heikin-Ashi** or standard candles for cleaner trend visualization.

2. **8 Customizable MAs**:

- Choose from **ALMA, HMA, SMA, SWMA, VWMA, WMA, ZLEMA, or EMA** with adjustable periods.

- Unique "Trend Strength" metric: `(MA_Close - MA_Open) / (MA_High - MA_Low)` highlights momentum direction.

3. **Smart Signals**:

- **Entry/Exit**: Triangles mark crossovers between MA Close/Open.

- **Reversal Alerts**: Detects counter-trend moves within a user-defined window (default: 3 bars) after signals.

- Color-coded plots: Bullish (🟢), Bearish (🔴), Reversal Bull (🔵), Reversal Bear (🟠).

#### 🎨 **Visual Customization**

- Toggle **High/Low MA lines**, **Close line**, and **fill colors**.

- Adjust colors for all elements to match your chart theme.

- Hide signals or reversal markers as needed.

#### ⚙️ **Practical Use**

- **Trend Following**: Use the MA Close/Open crossover with trend fill colors to confirm direction.

- **Reversal Trading**: Capitalize on pullbacks with reversal signals (e.g., after a bearish signal, watch for Bull Reversal markers).

- **Multi-Timeframe Confirmation**: Avoid false signals by aligning higher-timeframe trends with your entries.

*Ideal for swing traders and trend riders!*

**Note**: Adjust `MA Period`, `Reversal Window`, and `Trend Timeframe` for your strategy. Disable Heikin-Ashi in choppy markets for faster reactions.

---

*Code v2.7 updates: Optimized reversal logic, added ALMA/ZLEMA support, and enhanced visual controls.*

BK AK-SILENCER🚨 Introducing BK AK-SILENCER — Volume Footprint Warfare, Right on the Price Bars 🚨

This isn’t a traditional indicator.

This is a tactical weapon — engineered to expose institutional behavior directly in the bar data, using volume logic, CVD divergence, and spike detection to pinpoint who’s really in control of the tape.

No panels. No clutter.

Just silent execution — built directly into price itself.

🔥 Why "SILENCER"?

Because real power moves in silence.

Institutions don’t chase — they build positions quietly, in size, beneath the surface.

BK AK-SILENCER gives you a real-time edge by visually revealing their footprints through color-coded bar behavior, divergence signals, and volume spike alerts — all directly on your chart.

🔹 “AK” honors my mentor A.K., whose training forged my trading discipline.

🔹 “SILENCER” represents the institutional mindset — high impact, low visibility. This tool lets you trade like them: without noise, without hesitation, with deadly clarity.

🧠 What Is BK AK-SILENCER?

A bar-level institutional detection tool, purpose-built to:

✅ Color-code bars based on volume aggression and close-location inside range

✅ Detect real-time bullish and bearish divergences between price and volume delta

✅ Tag volume spikes with a $ symbol to expose potential traps or silent position builds

✅ Overlay VWAP for real-time mean-reversion biasing

No extra windows.

No indicators talking over each other.

Just pure volume-logic weaponry embedded into price.

⚙️ What This Weapon Deploys

🔸 Bar Coloring Logic (Volume Footprint)

🟢 Power Buy = Strong close near highs on elevated volume

🟩 Accumulation = Weak close but still heavy volume

🔴 Power Sell = Strong close near lows on heavy selling

🟥 Distribution / Weakness = Low close without commitment

❗ Extreme Volume Spikes marked with $ — using standard deviation to highlight institutional bursts

🔸 CVD Divergence Detection

→ Tracks cumulative volume delta and compares it to price pivot behavior

Bullish Divergence = Price makes lower lows, CVD makes higher lows → hidden accumulation

Bearish Divergence = Price makes higher highs, CVD makes lower highs → hidden distribution

All plotted directly on bars with triangle markers.

🔸 VWAP Overlay (Optional)

→ Anchored VWAP gives immediate context for intraday bias — above VWAP = demand, below = supply

🎯 How to Use BK AK-SILENCER

🔹 Silent Reversal Detection

Bullish divergence + Power Buy bar + VWAP reclaim = sniper entry

Bearish divergence + Power Sell bar + VWAP rejection = trap confirmation

🔹 Volume-Based Entry Triggers

Look for Power Buy + $ spike after a pullback → watch for quiet reversal

Accumulation colors clustering? Institutions are likely loading silently

🔹 Institutional Trap Warnings

$ spike + red distribution bar at highs = time to exit or flip

Weakness bar below VWAP? Don’t chase the long.

🛡️ Why It Matters

✅ Clean — it integrates into price action, no separate panels

✅ Silent — tracks institutions who build without alerts or indicators

✅ Tactical — no fluff, no lag, just real-time behavior recognition

This tool is ideal for:

🔸 Scalpers reading bar-by-bar

🔸 Intraday swing traders using VWAP and structure

🔸 Professionals who need volume behavior decoded in real-time

🔸 Anyone who wants signal without clutter

🙏 Final Thoughts

This tool isn’t just about trading — it’s about tactical awareness.

🔹 Dedicated to my mentor A.K., whose wisdom runs deep in every logic tree.

🔹 Above all, I give thanks to Gd, the source of clarity, courage, and conviction.

Without Him, even the sharpest system is blind.

With Him, we execute with structure, purpose, and divine alignment.

⚡ No noise. No clutter. No delay. Just raw, silent execution.

🔥 BK AK-SILENCER — Bar-Level Volume Footprint Precision 🔥

Gd bless every step you take in this market.

Trade with clarity, move with intention. 🙏

Opening Range Breakout (ORB) with Fib RetracementOverview

“ORB with Fib Retracement” is a Pine Script indicator that anchors a full Fibonacci framework to the first minutes of the trading day (the opening-range breakout, or ORB).

After the ORB window closes the script:

Locks-in that session’s high and low.

Calculates a complete ladder of Fibonacci retracement levels between them (0 → 100 %).

Projects symmetric extension levels above and below the range (±1.618, ±2.618, ±3.618, ±4.618 by default).

Sub-divides every extension slice with additional 23.6 %, 38.2 %, 50 %, 61.8 % and 78.6 % mid-lines so each “zone” has its own inner fib grid.

Plots the whole structure and—optionally—extends every line into the future for ongoing reference.

**Session time / timezone** – Defines the ORB window (defaults 09:30–09:45 EST).

**Show All Fib Levels** – Toggles every retracement and extension line on or off.

**Show Extended Lines** – Draws dotted, extend-right projections of every level.

**Color group** – Assigns colors to buy-side (green), sell-side (red), and internal fibs (gray).

**Extension value inputs** – Allows custom +/- 1.618 to 4.618 fib levels for personalized projection zones.

S4_IBS_Mean_Rev_3candleExitOverview:

This is a rules-based, mean reversion strategy designed to trade pullbacks using the Internal Bar Strength (IBS) indicator. The system looks for oversold conditions based on IBS, then enters long trades , holding for a maximum of 3 bars or until the trade becomes profitable.

The strategy includes:

✅ Strict entry rules based on IBS

✅ Hardcoded exit conditions for risk management

✅ A clean visual table summarizing key performance metrics

How It Works:

1. Internal Bar Strength (IBS) Setup:

The IBS is calculated using the previous bar’s price range:

IBS = (Previous Close - Previous Low) / (Previous High - Previous Low)

IBS values closer to 0 indicate price is near the bottom of the previous range, suggesting oversold conditions.

2. Entry Conditions:

IBS must be ≤ 0.25, signaling an oversold setup.

Trade entries are only allowed within a user-defined backtest window (default: 2024).

Only one trade at a time is permitted (long-only strategy).

3. Exit Conditions:

If the price closes higher than the entry price, the trade exits with a profit.

If the trade has been open for 3 bars without showing profit, the trade is forcefully exited.

All trades are closed automatically at the end of the backtest window if still open.

Additional Features:

📊 A real-time performance metrics table is displayed on the chart, showing:

- Total trades

- % of profitable trades

- Total P&L

- Profit Factor

- Max Drawdown

- Best/Worst trade performance

📈 Visual markers indicate trade entries (green triangle) and exits (red triangle) for easy chart interpretation.

Who Is This For?

This strategy is designed for:

✅ Traders exploring systematic mean reversion approaches

✅ Those who prefer strict, rules-based setups with no subjective decision-making

✅ Traders who want built-in performance tracking directly on the chart

Note: This strategy is provided for educational and research purposes. It is a backtested model and past performance does not guarantee future results. Users should paper trade and validate performance before considering real capital.