WLSMA: fast approximation🙏🏻 Sup TV & @alexgrover

O(N) algocomplexity, just one loop inside. No, you can't do O(1) @ updates in moving window mode, only expanding window will allow that.

Now I have time series & stats models of my own creation, nowhere else available, just TV and my github for now, ain’t no legacy academic industry I always have fun about, but back in 2k20 when I consciously ain’t known much about quant, I remember seeing post by @alexgrover recreating Moving Regression Endpoint dropped on price chart (called LSMA here) as a linear filter combination of filters (yea yeah DSP terms) as 3WMA - 2SMA. Now it’s my time to do smth alike aye?

...

This script is remake of my 1st degree WLSMA via linear filter combo. It’s much faster, we aint calculate moving regression per se, we just match its freq response. You can see it on the screen (WLSMAfa) almost perfectly matching the original one (WLSMA).

...

While humans like to overfit, I fw generalizations. So your lovely WMA is actually just one case of a more general weight pattern: pow(len - i, e), where pow is the power function and e is the exponent itself. So:

- If e = 0, then we have SMA (every number in 0th power is one)

- If e = 1, we get WMA

- If e = 2, we get quadratic weights.

We can recreate WLSMA freq response then by combining 2 filters with e = 1 and e = 2.

This is still an approximation, even tho enormously precise for the tasks you’ve shared with me. Due to the non-linear nature of the thing it’s all we can do, and as window size grows, even this small discrepancy converges with true WLSMA value, so we’re all good. Pls don’t try to model this 0.00xxxx discrepancy, it’s not natural.

...

DSP approach is unnatural for prices, but you can put this thing on volume delta and be happy, or on other metrics of yours, if for some reason u dont wanna estimate thresholds by fitting a distro.

All good TV

∞

P.S.: strangely, the first script made & dropped in the location in Saint P where my actual quant way has started ~5 years ago xD, very thankful

"如何用wind搜索股票的发行价和份数" için komut dosyalarını ara

Support and Resistance Profile with Volatility ClusteringThe indicator begins by looking at recent volatility behavior in the market: it measures the average true range over your chosen “Length” and compares it to the average true range over ten times that period. When volatility over the short window is high relative to longer-term volatility, we mark that period as a “cluster.” As price moves through these clusters—whether in a quiet period or a sudden burst of activity—the script isolates each cluster and examines the sequence of closing prices within it.

Within every cluster, the algorithm next finds the points along the price path that matter most to a human eye, smoothing out minor wobbles and highlighting the peaks and valleys that define the cluster’s shape. It does this by drawing a straight line between the beginning and end of the cluster, then repeatedly snapping the single point that deviates most from that line back onto it and re-interpolating, until it has identified a fixed number of perceptually important points. Those points capture where price really turned or accelerated, stripping away noise so that you see the genuine memory-markers in each volatility episode.

Each of those important points inherits a “weight” based on the cluster’s normalized volatility—essentially how large the average true range in that cluster was relative to its average close. Over your “Main Length for Profile” window, every time one of these weighted points occurs at a particular price level, it adds to a running total in that level’s bin. At the end of the window you see a silhouette of boxes extending to the right of the chart: where boxes are wide, many important points (with high volatility weight) have happened there in the past; where boxes are thin or absent, price memory is light.

For a trader, the value of this profile lies in spotting zones where the market has repeatedly “remembered” price extremes during volatile episodes—those are areas where support or resistance is likely to be strongest. Conversely, gaps in the profile—price levels with little weighted history—suggest frictionless zones. If price enters such a gap, it may move swiftly until it encounters another region of heavy memory. You can use this in several ways: as a filter on breakouts and breakdowns (only trade through a gap when you see sufficient momentum), as a guide for scaling into positions (add when price enters a low-memory zone and tighten stops where memory boxes thicken), or to anticipate where price might pause or reverse (when it reaches a band of wide boxes). By turning raw volatility clusters into a human-readable map of price memory, this tool helps you see at a glance where the market is likely to push or pause—and plan entries, exits, and risk targets accordingly.

Reflexivity Resonance Factor (RRF) - Quantum Flow Reflexivity Resonance Factor (RRF) – Quantum Flow

See the Feedback Loops. Anticipate the Regime Shift.

What is the RRF – Quantum Flow?

The Reflexivity Resonance Factor (RRF) – Quantum Flow is a next-generation market regime detector and energy oscillator, inspired by George Soros’ theory of reflexivity and modern complexity science. It is designed for traders who want to visualize the hidden feedback loops between market perception and participation, and to anticipate explosive regime shifts before they unfold.

Unlike traditional oscillators, RRF does not just measure price momentum or volatility. Instead, it models the dynamic feedback between how the market perceives itself (perception) and how it acts on that perception (participation). When these feedback loops synchronize, they create “resonance” – a state of amplified reflexivity that often precedes major market moves.

Theoretical Foundation

Reflexivity: Markets are not just driven by external information, but by participants’ perceptions and their actions, which in turn influence future perceptions. This feedback loop can create self-reinforcing trends or sudden reversals.

Resonance: When perception and participation align and reinforce each other, the market enters a high-energy, reflexive state. These “resonance” events often mark the start of new trends or the climax of existing ones.

Energy Field: The indicator quantifies the “energy” of the market’s reflexivity, allowing you to see when the crowd is about to act in unison.

How RRF – Quantum Flow Works

Perception Proxy: Measures the rate of change in price (ROC) over a configurable period, then smooths it with an EMA. This models how quickly the market’s collective perception is shifting.

Participation Proxy: Uses a fast/slow ATR ratio to gauge the intensity of market participation (volatility expansion/contraction).

Reflexivity Core: Multiplies perception and participation to model the feedback loop.

Resonance Detection: Applies Z-score normalization to the absolute value of reflexivity, highlighting when current feedback is unusually strong compared to recent history.

Energy Calculation: Scales resonance to a 0–100 “energy” value, visualized as a dynamic background.

Regime Strength: Tracks the percentage of bars in a lookback window where resonance exceeded the threshold, quantifying the persistence of reflexive regimes.

Inputs:

🧬 Core Parameters

Perception Period (pp_roc_len, default 14): Lookback for price ROC.

Lower (5–10): More sensitive, for scalping (1–5min).

Default (14): Balanced, for 15min–1hr.

Higher (20–30): Smoother, for 4hr–daily.

Perception Smooth (pp_smooth_len, default 7): EMA smoothing for perception.

Lower (3–5): Faster, more detail.

Default (7): Balanced.

Higher (10–15): Smoother, less noise.

Participation Fast (prp_fast_len, default 7): Fast ATR for immediate volatility.

5–7: Scalping.

7–10: Day trading.

10–14: Swing trading.

Participation Slow (prp_slow_len, default 21): Slow ATR for baseline volatility.

Should be 2–4x fast ATR.

Default (21): Works with fast=7.

⚡ Signal Configuration

Resonance Window (res_z_window, default 50): Z-score lookback for resonance normalization.

20–30: More reactive.

50: Medium-term.

100+: Very stable.

Primary Threshold (rrf_threshold, default 1.5): Z-score level for “Active” resonance.

1.0–1.5: More signals.

1.5: Balanced.

2.0+: Only strong signals.

Extreme Threshold (rrf_extreme, default 2.5): Z-score for “Extreme” resonance.

2.5: Major regime shifts.

3.0+: Only the most extreme.

Regime Window (regime_window, default 100): Lookback for regime strength (% of bars with resonance spikes).

Higher: More context, slower.

Lower: Adapts quickly.

🎨 Visual Settings

Show Resonance Flow (show_flow, default true): Plots the main resonance line with glow effects.

Show Signal Particles (show_particles, default true): Circular markers at active/extreme resonance points.

Show Energy Field (show_energy, default true): Background color based on resonance energy.

Show Info Dashboard (show_dashboard, default true): Status panel with resonance metrics.

Show Trading Guide (show_guide, default true): On-chart quick reference for interpreting signals.

Color Mode (color_mode, default "Spectrum"): Visual theme for all elements.

“Spectrum”: Cyan→Magenta (high contrast)

“Heat”: Yellow→Red (heat map)

“Ocean”: Blue gradients (easy on eyes)

“Plasma”: Orange→Purple (vibrant)

Color Schemes

Dynamic color gradients are used for all plots and backgrounds, adapting to both resonance intensity and direction:

Spectrum: Cyan/Magenta for bullish/bearish resonance.

Heat: Yellow/Red for bullish, Blue/Purple for bearish.

Ocean: Blue gradients for both directions.

Plasma: Orange/Purple for high-energy states.

Glow and aura effects: The resonance line is layered with multiple glows for depth and signal strength.

Background energy field: Darker = higher energy = stronger reflexivity.

Visual Logic

Main Resonance Line: Shows the smoothed resonance value, color-coded by direction and intensity.

Glow/Aura: Multiple layers for visual depth and to highlight strong signals.

Threshold Zones: Dotted lines and filled areas mark “Active” and “Extreme” resonance zones.

Signal Particles: Circular markers at each “Active” (primary threshold) and “Extreme” (extreme threshold) event.

Dashboard: Top-right panel shows current status (Dormant, Building, Active, Extreme), resonance value, energy %, and regime strength.

Trading Guide: Bottom-right panel explains all states and how to interpret them.

How to Use RRF – Quantum Flow

Dormant (💤): Market is in equilibrium. Wait for resonance to build.

Building (🌊): Resonance is rising but below threshold. Prepare for a move.

Active (🔥): Resonance exceeds primary threshold. Reflexivity is significant—consider entries or exits.

Extreme (⚡): Resonance exceeds extreme threshold. Major regime shift likely—watch for trend acceleration or reversal.

Energy >70%: High conviction, crowd is acting in unison.

Above 0: Bullish reflexivity (positive feedback).

Below 0: Bearish reflexivity (negative feedback).

Regime Strength: % of bars in “Active” state—higher = more persistent regime.

Tips:

- Use lower lookbacks for scalping, higher for swing trading.

- Combine with price action or your own system for confirmation.

- Works on all assets and timeframes—tune to your style.

Alerts

RRF Activation: Resonance crosses above primary threshold.

RRF Extreme: Resonance crosses above extreme threshold.

RRF Deactivation: Resonance falls below primary threshold.

Originality & Usefulness

RRF – Quantum Flow is not a mashup of existing indicators. It is a novel oscillator that models the feedback loop between perception and participation, then quantifies and visualizes the resulting resonance. The multi-layered color logic, energy field, and regime strength dashboard are unique to this script. It is designed for anticipation, not confirmation—helping you see regime shifts before they are obvious in price.

Chart Info

Script Name: Reflexivity Resonance Factor (RRF) – Quantum Flow

Recommended Use: Any asset, any timeframe. Tune parameters to your style.

Disclaimer

This script is for research and educational purposes only. It does not provide financial advice or direct buy/sell signals. Always use proper risk management and combine with your own strategy. Past performance is not indicative of future results.

Trade with insight. Trade with anticipation.

— Dskyz , for DAFE Trading Systems

VWAP Double Touch Alert (Timeframe-Aware)📌 VWAP Double Touch Alert — Smart Re-entry Signal for Precision Traders

Take your VWAP trading to the next level with this intelligent indicator that filters out the noise and zeroes in on high-probability re-entry setups.

💡 How it works:

This script tracks every time price touches the VWAP line and alerts you when it happens twice within a defined window of time (adjustable per your timeframe). This is often a sign of smart money accumulation, potential reversals, or explosive breakouts.

🔍 Why Traders Love It:

✅ Filters out weak signals — only alerts on confirmed double touches

✅ Fully adjustable VWAP zone sensitivity

✅ Selectable timeframe profiles or custom window (1m, 5m, 15m, 30m, etc.)

✅ Clean visual cues with minimal chart clutter

✅ Perfect for scalping, intraday reversals, or VWAP mean-reversion strategies

⚙️ Customization:

VWAP zone width (in %)

Time window in bars or automatic based on timeframe

Custom alert messages

Alert only triggers once per double-touch event to avoid spamming

🎯 Best For:

Crypto scalpers & day traders

VWAP bounce and mean-reversion traders

Traders who want clean, conclusive entry alerts without lag

[Stop!Loss] ADR Signal ADR Signal - a technical indicator located in a separate window, which displays by default the 80%-level , as well as the 100%-level of the average daily range (ADR) for the last 10 days and compares it with the current intraday range. The indicator helps not only with the use of a mathematical-statistical method to identify a potential reversal at the moment during intraday trading, but can also serves as an effective assistant in risk management.

👉 Basic mechanics of the indicator

Firstly, this indicator tracks the performance of the standard ATR indicator on the daily chart, in other words, ADR (Average Daily Range).

Important ❗️The ATR (Average True Range) indicator was created by J. Welles Wilder Jr. He first introduced ATR in his book "New Concepts in Technical Trading Systems", published in 1978. Wilder developed this indicator to measure market volatility to help traders estimate the range of price movements. This indicator is built into TradingView, more details can be found by link: www.tradingview.com

Like ATR , ADR calculates the average true range for a specified period. In this case, the distance in points from the maximum of each day to its minimum is calculated, after which the arithmetic mean is calculated - this is ADR .

👉 Visualization

ADR Signal is located in a separate window on the chart and has 3 levels:

1) "ADR level" (green line) - the same parameter, the calculations of which are briefly described above. There is 100%-level of ATR on the daily chart (ADR).

2) "Current level" (red line) - this is the current price passage within the day, calculated in points. At the start of a new day, this parameter is reset. Therefore, in the indicator window, this line has sharp drops at the start of a new trading day: "A new trading day - the instrument's power reserve is renewed again".

3) "Signal level" (blue line) - this is an individually customized value that demonstrates a certain part of the ADR parameter.

👉 Inputs

1) - is responsible for the ATR indicator period, the value of which will always be calculated on the daily chart. The default value is "10", that is, ATR is calculated for the last 10 days (not including the current one).

2) - signal level (in %). The default value is "0.8", that is, 80%-level of the ADR parameter (set earlier) is calculated.

👉 Style

1) - by default, this level is colored "blue".

2) - by default, this level is colored "red".

3) - by default, this level is colored "green".

👉 How to use this indicator

Important❗️ The two methods of the use of the ADR Signal indicator described below will be most effective when trading intraday (which is highlighted quite well below), so it is more logical to use the indicator information on time periods H1 and below.

1) Identifying potential reversals during intraday trading:

The ADR Signal indicator can be used as a potential individual reversal strategy.

Important ❗️It should be noted that using it in it without additional confirming analysis tools will be a rather aggressive trading approach. Therefore, it is best to support the entry point in particular with other methods.

In this case, the crossing of the red line (the number of points passed within the current day, that is, from the minimum of the current day to its maximum) and the blue line (color of the Signal level based on the default settings), indicates that the trading instrument has passed 80% (based on the default settings for the "Signal level") of its average distance from the maximum to the minimum over the past 10 days (based on the default settings for the "ADR Length"). Such a situation in the context of the mathematical-statistical approach indicates a probable reversal, since the "power reserve" of this instrument is mostly exhausted, so one can expect with a higher probability, at least, a price stop and possibly a reversal. In case of crossing of the red line and the green one (ADR level), it says again that based on the mathematical-statistical approach, this trading instrument has completely exhausted its intraday "power reserve". In this situation, a stop or reversal of the price will be even more likely.

Of course, using the "Signal level" parameter, one can filter out even more reliable situations for potential price reversals within a day, namely, by specifying, for example, 1.5 in the field of this parameter. Under such conditions, in the case of crossing the red and blue lines (based on the default style settings), to say that the trading instrument has passed 150% of its average distance over the last 10 days (based on the default style settings "ADR length"). In this case, the probability of a stop or reversal of the price increases even more.

2) Use in risk management:

In terms of risk management, this indicator is more applicable to open trades. For example, if one had an open Buy-position (especially if it is an intraday trade) and the price has raised significantly during the day, then the crossing of the red line with the blue line , and especially the red line with the green line , may indicate that the price will most likely stop growing, since the "power reserve" is almost or completely exhausted for this instrument within the current day. In this case, one can, at a minimum, move the trade to breakeven or even partially fix the profit.

We will continue to discuss the methods of using this indicator and strategies based on it here. And we are always waiting for your reactions and feedback on this topic 💬.

Thank you for your support 🚀

VWAP 2.0 with desv + Initial Balance by RiotWolftrading🌟 Overview

This powerful tool is designed for traders who want to harness the power of the Volume Weighted Average Price (VWAP) alongside session-based ranges to make informed trading decisions. Whether you're a day trader or a swing trader, this indicator provides a clean and effective way to identify support, resistance, and market trends—all in one place! 💡

✨ Key Features

Auto-Anchored VWAP 📊

Automatically calculates the VWAP based on a user-defined anchor period (e.g., Daily, Weekly, Monthly).

Resets at the start of each period (e.g., daily for a Daily anchor).

Displays a customizable VWAP line with standard deviation bands to highlight key price levels.

Standard Deviation Bands 📏

Plots up to three sets of standard deviation bands above and below the VWAP (multipliers: 1.0, 2.0, 3.0).

Includes volume percentage labels to show where trading volume is concentrated. 📉

Session High/Low Range 🕒

Identifies the high and low prices within a customizable session (default: 12:00 to 15:31).

Draws horizontal lines at the session high and low, with dotted deviation lines for additional reference points.

Perfect for spotting key levels during your trading session! 🔑

Time-Based Range Box ⏰

Highlights a specific time window (default: 15:40 to 15:50) with a colored box showing the high and low prices.

Ideal for tracking price action during high-impact events like news releases or market opens. 📅

Alerts 🚨

Set up alerts for when the price crosses above or below the VWAP—never miss a potential trading opportunity!

⚙️ Settings

Customize the indicator to fit your trading style with these easy-to-use settings:

VWAP Settings

Timezone 🌍: Select your timezone (default: GMT+2) to align calculations with your local time.

VWAP Source 📈: Choose the price source for VWAP (default: hlc3 - average of high, low, close).

Std Deviation Multipliers 📐: Adjust the multipliers for the bands (default: 1.0, 2.0, 3.0).

Line Width ✏️: Set the thickness of the VWAP and band lines (default: 1).

Session Time ⏳: Define the session window for VWAP calculations (default: 08:00-18:00, all days).

Show Upper/Lower Bands 👀: Toggle visibility for each set of bands (default: Band 1 visible, Bands 2 & 3 hidden).

Range Settings

Range Start/End Time 🕙: Set the time window for the range box (default: 15:40 to 15:50).

Box Color 🎨: Customize the border color (default: blue).

Box Background Color 🖌️: Adjust the background color (default: light aqua, 90% transparency).

I created this indicator to provide a streamlined, clutter-free tool for traders who rely on VWAP and session-based analysis. It focuses on the essentials—VWAP, standard deviation bands, session high/low, and range box—without unnecessary overlays. I hope it helps you in your trading journey! If you have feedback or suggestions, feel free to share—I’d love to hear from you! 😊

Dkoderweb repainting issue fix strategyHarmonic Pattern Recognition Trading Strategy

This TradingView strategy called "Dkoderweb repainting issue fix strategy" is designed to identify and trade harmonic price patterns with optimized entry and exit points using Fibonacci levels. The strategy implements various popular harmonic patterns including Bat, Butterfly, Gartley, Crab, Shark, ABCD, and their anti-patterns.

Key Features

Pattern Recognition: Identifies 17+ harmonic price patterns including standard and anti-patterns

Fibonacci-Based Entries and Exits: Uses customizable Fibonacci levels for precision entries, take profits, and stop losses

Alternative Timeframe Analysis: Option to use higher timeframes for pattern identification

Heiken Ashi Support: Optional use of Heiken Ashi candles instead of regular candlesticks

Visual Indicators:

Pattern visualization with ZigZag indicator

Buy/sell signal markers

Color-coded background to highlight active trade zones

Customizable Fibonacci level display

How It Works

The strategy uses a ZigZag-based pattern identification system to detect pivot points

When a valid harmonic pattern forms, the strategy calculates the optimal entry window using the specified Fibonacci level (default 0.382)

Entries trigger when price returns to the entry window after pattern completion

Take profit and stop loss levels are automatically set based on customizable Fibonacci ratios

Visual alerts notify you of entries and exits

The strategy tracks active trades and displays them with background color highlights

Customizable Settings

Trade size

Entry window Fibonacci level (default 0.382)

Take profit Fibonacci level (default 0.618)

Stop loss Fibonacci level (default -0.618)

Alert messages for entries and exits

Display options for specific Fibonacci levels

Alternative timeframe selection

This strategy is designed to fix repainting issues that are common in harmonic pattern strategies, ensuring more reliable signals and backtesting results.

Dskyz Adaptive Futures Elite (DAFE)Dskyz Adaptive Futures Edge (DAFE)

imgur.com

A Dynamic Futures Trading Strategy

DAFE adapts to market volatility and price action using technical indicators and advanced risk management. It’s built for high-stakes futures trading (e.g., MNQ, BTCUSDT.P), offering modular logic for scalpers and swing traders alike.

Key Features

Adaptive Moving Averages

Dynamic Logic: Fast and slow SMAs adjust lengths via ATR, reacting to momentum shifts and smoothing in calm markets.

Signals: Long entry on fast SMA crossing above slow SMA with price confirmation; short on cross below.

RSI Filtering (Optional)

Momentum Check: Confirms entries with RSI crossovers (e.g., above oversold for longs). Toggle on/off with custom levels.

Fine-Tuning: Adjustable lookback and thresholds (e.g., 60/40) for precision.

Candlestick Pattern Recognition

Eng|Enhanced Detection: Identifies strong bullish/bearish engulfing patterns, validated by volume and range strength (vs. 10-period SMA).

Conflict Avoidance: Skips trades if both patterns appear in the lookback window, reducing whipsaws.

Multi-Timeframe Trend Filter

15-Minute Alignment: Syncs intrabar trades with 15-minute SMA trends; optional for flexibility.

Dollar-Cost Averaging (DCA) New!

Scaling: Adds up to a set number of entries (e.g., 4) on pullbacks/rallies, spaced by ATR multiples.

Control: Caps exposure and resets on exit, enhancing trend-following potential.

Trade Execution & Risk Management

Entry Rules: Prioritizes moving averages or patterns (user choice), with volume, volatility, and time filters.

Stops & Trails:

Initial Stop: ATR-based (2–3.5x, volatility-adjusted).

Trailing Stop: Locks profits with configurable ATR offset and multiplier.

Discipline

Cooldown: Pauses post-exit (e.g., 0–5 minutes).

Min Hold: Ensures trades last a set number of bars (e.g., 2–10).

Visualization & Tools

Charts: Overlays MAs, stops, and signals; trend shaded in background.

Dashboard: Shows position, P&L, win rate, and more in real-time.

Debugging: Logs signal details for optimization.

Input Parameters

Parameter Purpose Suggested Use

Use RSI Filter - Toggle RSI confirmation *Disable 4 price-only

trading

RSI Length - RSI period (e.g., 14) *7–14 for sensitivity

RSI Overbought/Oversold - Adjust for market type *Set levels (e.g., 60/40)

Use Candlestick Patterns - Enables engulfing signals *Disable for MA focus

Pattern Lookback - Pattern window (e.g., 19) *10–20 bars for balance

Use 15m Trend Filter - Align with 15-min trend *Enable for trend trades

Fast/Slow MA Length - Base MA lengths (e.g., 9/19) *10–25 / 30–60 per

timeframe

Volatility Threshold - Filters volatile spikes *Max ATR/close (e.g., 1%)

Min Volume - Entry volume threshold *Avoid illiquid periods

(e.g., 10)

ATR Length - ATR period (e.g., 14) *Standard volatility

measure

Trailing Stop ATR Offset - Trail distance (e.g., 0.5) *0.5–1.5 for tightness

Trailing Stop ATR Multi - Trail multiplier (e.g., 1.0) *1–3 for trend room

Cooldown Minutes - Post-exit pause (e.g., 0–5) *Prevents overtrading

Min Bars to Hold - Min trade duration (e.g., 2) *5–10 for intraday

Trading Hours - Active window (e.g., 9–16) *Focus on key sessions

Use DCA - Toggle DCA *Enable for scaling

Max DCA Entries - Cap entries (e.g., 4) *Limit risk exposure

DCA ATR Multiplier Entry spacing (e.g., 1.0) *1–2 for wider gaps

Compliance

Realistic Testing: Fixed quantities, capital, and slippage for accurate backtests.

Transparency: All logic is user-visible and adjustable.

Risk Controls: Cooldowns, stops, and hold periods ensure stability.

Flexibility: Adapts to various futures and timeframes.

Summary

DAFE excels in volatile futures markets with adaptive logic, DCA scaling, and robust risk tools. Currently in prop account testing, it’s a powerful framework for precision trading.

Caution

DAFE is experimental, not a profit guarantee. Futures trading risks significant losses due to leverage. Backtest, simulate, and monitor actively before live use. All trading decisions are your responsibility.

BTC Trading RobotOverview

This Pine Script strategy is designed for trading Bitcoin (BTC) by placing pending orders (BuyStop and SellStop) based on local price extremes. The script also implements a trailing stop mechanism to protect profits once a position becomes sufficiently profitable.

________________________________________

Inputs and Parameter Setup

1. Trading Profile:

o The strategy is set up specifically for BTC trading.

o The systemType input is set to 1, which means the strategy will calculate trade parameters using the BTC-specific inputs.

2. Common Trading Inputs:

o Risk Parameters: Although RiskPercent is defined, its actual use (e.g., for position sizing) isn’t implemented in this version.

o Trading Hours Filter:

SHInput and EHInput let you restrict trading to a specific hour range. If these are set (non-zero), orders will only be placed during the allowed hours.

3. BTC-Specific Inputs:

o Take Profit (TP) and Stop Loss (SL) Percentages:

TPasPctBTC and SLasPctBTC are used to determine the TP and SL levels as a percentage of the current price.

o Trailing Stop Parameters:

TSLasPctofTPBTC and TSLTgrasPctofTPBTC determine when and by how much a trailing stop is applied, again as percentages of the TP.

4. Other Parameters:

o BarsN is used to define the window (number of bars) over which the local high and low are calculated.

o OrderDistPoints acts as a buffer to prevent the entry orders from being triggered too early.

________________________________________

Trade Parameter Calculation

• Price Reference:

o The strategy uses the current closing price as the reference for calculations.

• Calculation of TP and SL Levels:

o If the systemType is set to BTC (value 1), then:

Take Profit Points (Tppoints) are calculated by multiplying the current price by TPasPctBTC.

Stop Loss Points (Slpoints) are calculated similarly using SLasPctBTC.

A buffer (OrderDistPoints) is set to half of the take profit points.

Trailing Stop Levels:

TslPoints is calculated as a fraction of the TP (using TSLTgrasPctofTPBTC).

TslTriggerPoints is similarly determined, which sets the profit level at which the trailing stop will start to activate.

________________________________________

Time Filtering

• Session Control:

o The current hour is compared against SHInput (start hour) and EHInput (end hour).

o If the current time falls outside the allowed window, the script will not place any new orders.

________________________________________

Entry Orders

• Local Price Extremes:

o The strategy calculates a local high and local low using a window of BarsN * 2 + 1 bars.

• Placing Stop Orders:

o BuyStop Order:

A long entry is triggered if the current price is less than the local high minus the order distance buffer.

The BuyStop order is set to trigger at the level of the local high.

o SellStop Order:

A short entry is triggered if the current price is greater than the local low plus the order distance buffer.

The SellStop order is set to trigger at the level of the local low.

Note: Orders are only placed if there is no current open position and if the session conditions are met.

________________________________________

Trailing Stop Logic

Once a position is open, the strategy monitors profit levels to protect gains:

• For Long Positions:

o The script calculates the profit as the difference between the current price and the average entry price.

o If this profit exceeds the TslTriggerPoints threshold, a trailing stop is applied by placing an exit order.

o The stop price is set at a distance below the current price, while a limit (profit target) is also defined.

• For Short Positions:

o The profit is calculated as the difference between the average entry price and the current price.

o A similar trailing stop exit is applied if the profit exceeds the trigger threshold.

________________________________________

Summary

In essence, this strategy works by:

• Defining entry levels based on recent local highs and lows.

• Placing pending stop orders to enter the market when those levels are breached.

• Filtering orders by time, ensuring trades are only taken during specified hours.

• Implementing a trailing stop mechanism to secure profits once the trade moves favorably.

This approach is designed to automate BTC trading based on price action and dynamic risk management, although further enhancements (like dynamic position sizing based on RiskPercent) could be added for a more complete risk management system.

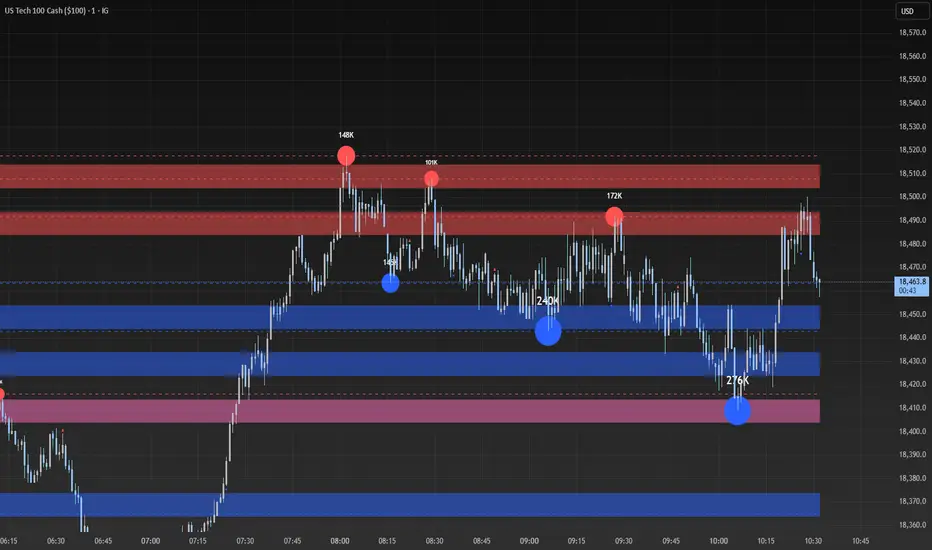

Liquidity Heatmap SwiftEdgeDescription

Liquidity Heatmap with Buy/Sell Side (Blue/Red) is a technical analysis tool designed to help traders identify potential liquidity zones in the market by combining swing high/low detection with volume analysis, visualized as a heatmap overlay on the chart. This script highlights areas where significant buying or selling pressure may exist, often acting as support or resistance levels, and provides a clear visual representation of these zones using color-coded heatmap boxes and labeled bubbles.

What It Does

The script identifies key price levels (swing highs and lows) where liquidity is likely to be concentrated, such as stop-loss clusters or pending orders. These levels are then grouped into a heatmap, with blue zones representing potential buy-side liquidity (below the current price) and red zones indicating sell-side liquidity (above the current price). Each zone is marked with a bubble showing the estimated liquidity amount, derived from volume data, to help traders gauge the strength of the level.

How It Works

The script combines three main components to create a comprehensive liquidity visualization:

Swing Highs and Lows Detection:

The script uses the ta.pivothigh and ta.pivotlow functions to identify swing highs and lows over a user-defined lookback period (Swing Length). These levels often represent areas where price has reversed, indicating potential liquidity zones where stop-losses or pending orders may be placed.

Volume Analysis:

Volume data at each swing high/low is captured and averaged over a specified period (Volume Average Length). This volume is then scaled using a multiplier (Volume Multiplier for Liquidity) to estimate the liquidity amount at each level, displayed in thousands (e.g., "10K") on the chart via labeled bubbles.

Heatmap Visualization:

The identified levels are grouped into price bins to form a heatmap. The price range is divided into a user-defined number of bins (Number of Heatmap Bins), and each bin is drawn as a colored box (blue for buy-side, red for sell-side). The transparency of the heatmap boxes can be adjusted (Heatmap Transparency) to ensure they do not obscure the price action.

Why Combine These Components?

The combination of swing highs/lows, volume analysis, and a heatmap provides a powerful way to visualize liquidity in the market. Swing highs and lows are natural points where liquidity tends to accumulate, as they often coincide with areas where traders place stop-losses or pending orders. By incorporating volume data, the script quantifies the potential strength of these levels, giving traders insight into the magnitude of liquidity present. The heatmap visualization then aggregates these levels into a clear, color-coded overlay, making it easy to see where buy-side and sell-side liquidity is concentrated without cluttering the chart.

This mashup is particularly useful because it bridges price action (swing levels), market activity (volume), and visual clarity (heatmap), offering a holistic view of potential support and resistance zones that might influence price movements.

How to Use It

Add the Indicator to Your Chart:

Apply the script to your chart by adding it from the Pine Script library. It will overlay directly on your price chart.

Interpret the Heatmap:

Blue Zones (Buy-Side Liquidity): These appear below the current price and indicate levels where buying pressure or stop-losses from short positions may be located.

Red Zones (Sell-Side Liquidity): These appear above the current price and indicate levels where selling pressure or stop-losses from long positions may be located.

The intensity of the color is controlled by the Heatmap Transparency setting—lower values make the zones more opaque, while higher values make them more transparent.

Analyze the Bubbles:

Each liquidity zone is marked with a bubble showing the estimated liquidity amount in thousands (e.g., "10K"). The size of the bubble is scaled by the Bubble Size Multiplier, with larger bubbles indicating higher liquidity.

Adjust Settings for Your Needs:

Liquidity Settings:

Swing Length: Controls the lookback period for detecting swing highs and lows. A smaller value (e.g., 10) is better for shorter timeframes like 1-minute charts, while a larger value (e.g., 50) suits higher timeframes.

Liquidity Threshold: Defines how close two levels must be to be considered the same, preventing duplicate zones.

Volume Average Length: Sets the period for averaging volume data at swing points.

Volume Multiplier for Liquidity: Scales the volume to estimate liquidity amounts shown in the bubbles.

Lookback Period (Hours): Limits how far back the script looks for liquidity zones.

Use Price Window Filter: If enabled, only shows zones within a price range defined by Liquidity Window (Points per Side).

Heatmap Settings:

Number of Heatmap Bins: Determines how many price bins the heatmap is divided into. More bins create a finer resolution but may clutter the chart.

Heatmap Bin Height (Points): Sets the vertical height of each heatmap box in price points.

Heatmap Transparency: Adjusts the transparency of the heatmap boxes (0 = fully opaque, 100 = fully transparent).

Display Settings:

Bubble Size Multiplier: Scales the size of the bubbles showing liquidity amounts.

Trading Application:

Use the heatmap to identify potential support (blue zones) and resistance (red zones) levels where price may react.

Pay attention to zones with larger bubbles, as they indicate higher liquidity and may have a stronger impact on price.

Combine with other analysis tools (e.g., trendlines, indicators) to confirm trade setups.

What Makes It Original?

This script stands out by integrating swing high/low detection with volume-based liquidity estimation and a heatmap visualization in a single tool. Unlike traditional support/resistance indicators that only plot static lines, this script dynamically aggregates liquidity zones into a heatmap, making it easier to see clusters of potential buying or selling pressure. The addition of volume-derived liquidity amounts in labeled bubbles provides a unique quantitative measure of each zone's strength, helping traders prioritize key levels. The color-coded buy/sell distinction further enhances its utility by visually separating zones based on their likely market impact.

Example Use Case

On a 1-minute chart of EUR/USD, you might set Swing Length to 10 to capture short-term pivots, Lookback Period (Hours) to 4 to focus on recent data, and Liquidity Window to 200 points (20 pips) to show only nearby zones. The heatmap will then display blue zones below the current price where buy-side liquidity may act as support, and red zones above where sell-side liquidity may act as resistance. A bubble showing "50K" at a blue zone indicates significant buy-side liquidity, suggesting a potential bounce if the price approaches that level.

VIDYA For-Loop | QuantEdgeB Introducing VIDYA For-Loop by QuantEdgeB

Overview

The VIDYA For-Loop indicator by QuantEdgeB is a dynamic trend-following tool that leverages Variable Index Dynamic Average (VIDYA) along with a rolling loop function to assess trend strength and direction. By utilizing adaptive smoothing and a recursive loop for threshold evaluation, this indicator provides a more responsive and robust signal framework for traders.

______

Key Components & Features

📌 VIDYA (Variable Index Dynamic Average)

- Adaptive Moving Average that adjusts its responsiveness based on market volatility.

- Uses a dynamic smoothing constant based on standard deviations.

- Allows for better trend detection compared to static moving averages.

📌 Loop Function (Rolling Calculation)

- A for-loop algorithm continuously compares VIDYA values over a defined lookback range.

- Measures the number of times price trends higher or lower within the rolling window.

- Generates a momentum-based score that helps quantify trend persistence.

📌 Trend Signal Calculation

- A long signal is triggered when the loop score exceeds the upper threshold.

- A short signal is triggered when the loop score falls below the lower threshold.

- The result is a clear directional bias that adapts to changing market conditions.

______

How It Works in Trading

✅ Detects Trend Strength – By measuring cumulative movements within a window.

✅ Filters Noise – Uses adaptive smoothing to avoid whipsaws.

✅ Dynamic Thresholds – Enables customized entry & exit conditions.

✅ Color-Coded Candles – Provides visual clarity for traders.

______

Visual Representation

Trend Signals:

🔵 Blue Candles – Strong Uptrend

🔴 Red Candles – Strong Downtrend

Thresholds:

📈 Long Threshold – Upper bound for bullish confirmation.

📉 Short Threshold – Lower bound for bearish confirmation.

Labels & Annotations (Optional):

✅ Long & Short Labels can be turned on or off for trade signal clarity.

📊 Display of entry & exit points based on loop calculations.

______

Settings:

VIDYA Length: 2 → Number of bars for VIDYA calculation.

SD Length: 5 → Standard deviation length for VIDYA calculation.

Source: Close → Defines the input data source (Close price).

Start Loop: 1 → Initial lookback period for the loop function.

End Loop: 60 → Maximum lookback range for trend scoring.

Long Threshold: 40 → Upper bound for a long signal.

Short Threshold: 10 → Lower bound for a short signal.

Extra Plots: True → Enables additional moving averages for visualization.

______

Conclusion

The VIDYA For-Loop by QuantEdgeB is a next-gen adaptive trend filter that combines dynamic smoothing with recursive trend evaluation, making it an invaluable tool for traders seeking precision and consistency in their strategies.

🔹 Who should use VIDYA For Loop :

📊 Trend-Following Traders – Helps identify sustained trends.

⚡ Momentum Traders – Captures strong price swings.

🚀 Algorithmic & Systematic Trading – Ideal for automated entries & exits.

🔹 Disclaimer: Past performance is not indicative of future results. No trading strategy can guarantee success in financial markets.

🔹 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

Moving Averages With Continuous Periods [macp]This script reimagines traditional moving averages by introducing floating-point period calculations, allowing for fractional lengths rather than being constrained to whole numbers. At its core, it provides SMA, WMA, and HMA variants that can work with any decimal length, which proves especially valuable when creating dynamic indicators or fine-tuning existing strategies.

The most significant improvement lies in the Hull Moving Average implementation. By properly handling floating-point mathematics throughout the calculation chain, this version reduces the overshoot tendencies that often plague integer-based HMAs. The result is a more responsive yet controlled indicator that better captures price action without excessive whipsaw.

The visual aspect incorporates a trend gradient system that can adapt to different trading styles. Rather than using fixed coloring, it offers several modes ranging from simple solid colors to more nuanced three-tone gradients that help identify trend transitions. These gradients are normalized against ATR to provide context-aware visual feedback about trend strength.

From a practical standpoint, the floating-point approach eliminates the subtle discontinuities that occur when integer-based moving averages switch periods. This makes the indicator particularly useful in systems where the MA period itself is calculated from market conditions, as it can smoothly transition between different lengths without artificial jumps.

At the heart of this implementation lies the concept of continuous weights rather than discrete summation. Traditional moving averages treat each period as a distinct unit with integer indexing. However, when we move to floating-point periods, we need to consider how fractional periods should behave. This leads us to some interesting mathematical considerations.

Consider the Weighted Moving Average kernel. The weight function is fundamentally a slope: -x + length where x represents the position in the averaging window. The normalization constant is calculated by integrating (in our discrete case, summing) this slope across the window. What makes this implementation special is how it handles the fractional component - when the length isn't a whole number, the final period gets weighted proportionally to its fractional part.

For the Hull Moving Average, the mathematics become particularly intriguing. The standard HMA formula HMA = WMA(2*WMA(price, n/2) - WMA(price, n), sqrt(n)) is preserved, but now each WMA calculation operates in continuous space. This creates a smoother cascade of weights that better preserves the original intent of the Hull design - to reduce lag while maintaining smoothness.

The Simple Moving Average's treatment of fractional periods is perhaps the most elegant. For a length like 9.7, it weights the first 9 periods fully and the 10th period at 0.7 of its value. This creates a natural transition between integer periods that traditional implementations miss entirely.

The Gradient Mathematics

The trend gradient system employs normalized angular calculations to determine color transitions. By taking the arctangent of price changes normalized by ATR, we create a bounded space between 0 and 1 that represents trend intensity. The formula (arctan(Δprice/ATR) + 90°)/180° maps trend angles to this normalized space, allowing for smooth color transitions that respect market volatility context.

This mathematical framework creates a more theoretically sound foundation for moving averages, one that better reflects the continuous nature of price movement in financial markets. The implementation recognizes that time in markets isn't truly discrete - our sampling might be, but the underlying process we're trying to measure is continuous. By allowing for fractional periods, we're creating a better approximation of this continuous reality.

This floating-point moving average implementation offers tangible benefits for traders and analysts who need precise control over their indicators. The ability to fine-tune periods and create smooth transitions makes it particularly valuable for automated systems where moving average lengths are dynamically calculated from market conditions. The Hull Moving Average calculation now accurately reflects its mathematical formula while maintaining responsiveness, making it a practical choice for both systematic and discretionary trading approaches. Whether you're building dynamic indicators, optimizing existing strategies, or simply want more precise control over your moving averages, this implementation provides the mathematical foundation to do so effectively.

Moving Average Hamming-RKMoving Average Hamming

Description:

A Moving Average using a Hamming window is a technique used in technical analysis to smooth price data. The Hamming window applies weighted smoothing, reducing sharp variations and edge effects in the data. This helps in identifying trends more effectively while minimizing noise.

It can be used in combination with other technical indicators for better market analysis.

Technical Use:

The Hamming Moving Average reduces high-frequency noise, making trends clearer.

It applies different weights to data points, giving more importance to the center of the window while reducing the impact of abrupt changes.

This method is particularly useful in trend-following strategies as it minimizes false breakouts.

It can also be integrated into algorithmic trading systems for improved price fluctuation filtering.

When to Take a Position:

Buy Signal: When the price crosses above the Hamming Moving Average, indicating a potential uptrend.

Sell Signal: When the price crosses below the Hamming Moving Average, signaling a possible downtrend.

Confirmation: Combine with other indicators like RSI or MACD to confirm the trend before entering a trade.

Avoid Choppy Markets: The indicator works best in trending markets; avoid using it in sideways or ranging conditions.

This approach helps traders refine their analysis, making informed decisions while reducing market noise.

Earnings Gap UpsBased on research conducted by John Pocorobba and Jason Thompson, the Earnings Gap Ups Indicator is designed to identify three types of earnings gaps, key levels, and the "alpha window"—a period when stocks often outperform following a gap. These gaps are frequently observed in high-performing stocks.

What is an Earnings Gap?

An earnings gap occurs when a stock's price makes a significant jump, after the company reports earnings signifying the street (institutions) were caught off guard.

The three different types of gaps are as follows: [/b

PEG (Power Earnings Gap)

Price gain of 10% or more

Volume is greater than 200% above the 50-day average

EPS surprise of at least 20%

Monster Gap

Price gain of 20% or more

Volume is greater than 300% above the 50-day average

No fundamental requirement

Monster Peg

Price Gain of 20% or more

Volume is greater than 300% above the 50-day average

EPS surprise of at least 20%

Key Levels and the Alpha Window

In addition to spotting these gaps, the indicator marks key levels on the chart and extends them through the alpha window, which represents the time period when the stock tends to outperform after the gap.

Key levels include:

High volume close: The closing price on a day with unusually high trading volume

High volume close minus 5%: A potential support level below the high volume close

Gap day high: The highest price reached on the gap day

Gap day low: The lowest price reached on the gap day

By understanding and tracking these gaps and levels, traders can map out a playbook for trading earnings gaps.

RS Cycles [QuantVue]The RS Cycles indicator is a technical analysis tool that expands upon traditional relative strength (RS) by incorporating Beta-based adjustments to provide deeper insights into a stock's performance relative to a benchmark index. It identifies and visualizes positive and negative performance cycles, helping traders analyze trends and make informed decisions.

Key Concepts:

Traditional Relative Strength (RS):

Definition: A popular method to compare the performance of a stock against a benchmark index (e.g., S&P 500).

Calculation: The traditional RS line is derived as the ratio of the stock's closing price to the benchmark's closing price.

RS=Stock Price/Benchmark Price

Usage: This straightforward comparison helps traders spot periods of outperformance or underperformance relative to the market or a specific sector.

Beta-Adjusted Relative Strength (Beta RS):

Concept: Traditional RS assumes equal volatility between the stock and benchmark, but Beta RS accounts for the stock's sensitivity to market movements.

Calculation:

Beta measures the stock's return relative to the benchmark's return, adjusted by their respective volatilities.

Alpha is then computed to reflect the stock's performance above or below what Beta predicts:

Alpha=Stock Return−(Benchmark Return×β)

Significance: Beta RS highlights whether a stock outperforms the benchmark beyond what its Beta would suggest, providing a more nuanced view of relative strength.

RS Cycles:

The indicator identifies positive cycles when conditions suggest sustained outperformance:

Short-term EMA (3) > Mid-term EMA (10) > Long-term EMA (50).

The EMAs are rising, indicating positive momentum.

RS line shows upward movement over a 3-period window.

EMA(21) > 0 confirms a broader uptrend.

Negative cycles are marked when the opposite conditions are met:

Short-term EMA (3) < Mid-term EMA (10) < Long-term EMA (50).

The EMAs are falling, indicating negative momentum.

RS line shows downward movement over a 3-period window.

EMA(21) < 0 confirms a broader downtrend.

This indicator combines the simplicity of traditional RS with the analytical depth of Beta RS, making highlighting true relative strength and weakness cycles.

Pulse DPO: Major Cycle Tops and Bottoms█ OVERVIEW

Pulse DPO is an oscillator designed to highlight Major Cycle Tops and Bottoms .

It works on any market driven by cycles. It operates by removing the short-term noise from the price action and focuses on the market's cyclical nature.

This indicator uses a Normalized version of the Detrended Price Oscillator (DPO) on a 0-100 scale, making it easier to identify major tops and bottoms.

Credit: The DPO was first developed by William Blau in 1991.

█ HOW TO READ IT

Pulse DPO oscillates in the range between 0 and 100. A value in the upper section signals an OverBought (OB) condition, while a value in the lower section signals an OverSold (OS) condition.

Generally, the triggering of OB and OS conditions don't necessarily translate into swing tops and bottoms, but rather suggest caution on approaching a market that might be overextended.

Nevertheless, this indicator has been customized to trigger the signal only during remarkable top and bottom events.

I suggest using it on the Daily Time Frame , but you're free to experiment with this indicator on other time frames.

The indicator has Built-in Alerts to signal the crossing of the Thresholds. Please don't act on an isolated signal, but rather integrate it to work in conjunction with the indicators present in your Trading Plan.

█ OB SIGNAL ON: ENTERING OVERBOUGHT CONDITION

When Pulse DPO crosses Above the Top Threshold it Triggers ON the OB signal. At this point the oscillator line shifts to OB color.

When Pulse DPO enters the OB Zone, please beware! In this Area the Major Players usually become Active Sellers to the Public. While the OB signal is On, it might be wise to Consider Selling a portion or the whole Long Position.

Please note that even though this indicator aims to focus on major tops and bottoms, a strong trending market might trigger the OB signal and stay with it for a long time. That's especially true on young markets and on bubble-mode markets.

█ OB SIGNAL OFF: EXITING OVERBOUGHT CONDITION

When Pulse DPO crosses Below the Top Threshold it Triggers OFF the OB signal. At this point the oscillator line shifts to its normal color.

When Pulse DPO exits the OB Zone, please beware because a Major Top might just have occurred. In this Area the Major Players usually become Aggressive Sellers. They might wind up any remaining Long Positions and Open new Short Positions.

This might be a good area to Open Shorts or to Close/Reverse any remaining Long Position. Whatever you choose to do, it's usually best to act quickly because the market is prone to enter into panic mode.

█ OS SIGNAL ON: ENTERING OVERSOLD CONDITION

When Pulse DPO crosses Below the Bottom Threshold it Triggers ON the OS signal. At this point the oscillator line shifts to OS color.

When Pulse DPO enters the OS Zone, please beware because in this Area the Major Players usually become Active Buyers accumulating Long Positions from the desperate Public.

While the OS signal is On, it might be wise to Consider becoming a Buyer or to implement a Dollar-Cost Averaging (DCA) Strategy to build a Long Position towards the next Cycle. In contrast to the tops, the OS state usually takes longer to resolve a major bottom.

█ OS SIGNAL OFF: EXITING OVERSOLD CONDITION

When Pulse DPO crosses Above the Bottom Threshold it Triggers OFF the OS signal. At this point the oscillator line shifts to its normal color.

When Pulse DPO exits the OS Zone, please beware because a Major Bottom might already be in place. In this Area the Major Players become Aggresive Buyers. They might wind up any remaining Short Positions and Open new Long Positions.

This might be a good area to Open Longs or to Close/Reverse any remaining Short Positions.

█ WHY WOULD YOU BE INTERESTED IN THIS INDICATOR?

This indicator is built over a solid foundation capable of signaling Major Cycle Tops and Bottoms across many markets. Let's see some examples:

Early Bitcoin Years: From 0 to 1242

This chart is in logarithmic mode in order to properly display various exponential cycles. Pulse DPO is properly signaling the major early highs from 9-Jun-2011 at 31.50, to the next one on 9-Apr-2013 at 240 and the epic top from 29-Nov-2013 at 1242.

Due to the massive price movements, the OB condition stays pinned during most of the exponential price action. But as you can see, the OB condition quickly vanishes once the Cycle Top has been reached. As the market matures, the OB condition becomes more exceptional and triggers much closer from the Cycle Top.

With regards to Cycle Bottoms, the early bottom of 2 after having peaked at 31.50 doesn’t get captured by the indicator. That is the only cycle bottom that escapes the Pulse DPO when the bottom threshold is set at a value of 5. In that event, the oscillator low reached 6.95.

Bitcoin Adoption Spreading: From 257 to 73k

This chart is in logarithmic mode in order to properly display various exponential cycles. Pulse DPO is properly signaling all the major highs from 17-Dec-2017 at 19k, to the next one on 14-Apr-2021 at 64k and the most recent top from 9-Nov-2021 at 68k.

During the massive run of 2017, the OB condition still stayed triggered for a few weeks on each swing top. But on the next cycles it started to signal only for a few days before each swing top actually happened. The OB condition during the last cycle top triggered only for 3 days. Therefore the signal grows in focus as the market matures.

At the time of publishing this indicator, Bitcoin printed a new All Time High (ATH) on 13-Mar-2024 at 73k. That run didn’t trigger the OB condition. Therefore, if the indicator is correct the Bitcoin market still has some way to grow during the next months.

With regards to Cycle Bottoms, the bottom of 3k after having peaked at19k got captured within the wide OS zone. The bottom of 15k after having peaked at 68k got captured too within the OS accumulation area.

Gold

Pulse DPO behaves surprisingly well on a long standing market such as Gold. Moving back to the 197x years it’s been signaling most Cycle Tops and Bottoms with precision. During the last cycle, it shows topping at 2k and bottoming at 1.6k.

The current price action is signaling OB condition in the range of 2.5k to 2.7k. Looking at past cycles, it tends to trigger on and off at multiple swing tops until reaching the final cycle top. Therefore this might indicate the first wave within a potential gold run.

Oil

On the Oil market, we can see that most of the cycle tops and bottoms since the 80s got signaled. The only exception being the low from 2020 which didn’t trigger.

EURUSD

On Forex markets the Pulse DPO also behaves as expected. Looking back at EURUSD we can see the marketing triggering OB and OS conditions during major cycle tops and bottoms from recent times until the 80s.

S&P 500

On the S&P 500 the Pulse DPO catched the lows from 2016 and 2020. Looking at present price action, the recent ATH didn’t trigger the OB condition. Therefore, the indicator is allowing room for another leg up during the next months.

Amazon

On the Amazon chart the Pulse DPO is mirroring pretty accurately the major swings. Scrolling back to the early 2000s, this chart resembles early exponential swings in the crypto space.

Tesla

Moving onto a younger tech stock, Pulse DPO captures pretty accurately the major tops and bottoms. The chart is shown in logarithmic scale to better display the magnitude of the moves.

█ SETTINGS

This indicator is ideal for identifying major market turning points while filtering out short-term noise. You are free to adjust the parameters to align with your preferred trading style.

Parameters : This section allows you to customize any of the Parameters that shape the Oscillator.

Oscillator Length: Defines the period for calculating the Oscillator.

Offset: Shifts the oscillator calculation by a certain number of periods, which is typically half the Oscillator Length.

Lookback Period: Specifies how many bars to look back to find tops and bottoms for normalization.

Smoothing Length: Determines the length of the moving average used to smooth the oscillator.

Thresholds : This section allows you to customize the Thresholds that trigger the OB and OS conditions.

Top: Defines the value of the Top Threshold.

Bottom: Defines the value of the Bottom Threshold.

Savitzky-Golay Z-Score [BackQuant]Savitzky-Golay Z-Score

The Savitzky-Golay Z-Score is a powerful trading indicator that combines the precision of the Savitzky-Golay filter with the statistical strength of the Z-Score. This advanced indicator is designed to detect trend shifts, identify overbought or oversold conditions, and highlight potential divergences in the market, providing traders with a unique edge in detecting momentum changes and trend reversals.

Core Concept: Savitzky-Golay Filter

The Savitzky-Golay filter is a widely-used smoothing technique that preserves important signal features such as peak detection while filtering out noise. In this indicator, the filter is applied to price data (default set to HLC3) to smooth out volatility and produce a cleaner trend line. By specifying the window size and polynomial degree, traders can fine-tune the degree of smoothing to match their preferred trading style or market conditions.

Z-Score: Measuring Deviation

The Z-Score is a statistical measure that indicates how far the current price is from its mean in terms of standard deviations. In trading, the Z-Score can be used to identify extreme price moves that are likely to revert or continue trending. A positive Z-Score means the price is above the mean, while a negative Z-Score indicates the price is below the mean.

This script calculates the Z-Score based on the Savitzky-Golay filtered price, enabling traders to detect moments when the price is diverging from its typical range and may present an opportunity for a trade.

Long and Short Conditions

The Savitzky-Golay Z-Score generates clear long and short signals based on the Z-Score value:

Long Signals : When the Z-Score is positive, indicating the price is above its smoothed mean, a long signal is generated. The color of the bars turns green, signaling upward momentum.

Short Signals : When the Z-Score is negative, indicating the price is below its smoothed mean, a short signal is generated. The bars turn red, signaling downward momentum.

These signals allow traders to follow the prevailing trend with confidence, using statistical backing to avoid false signals from short-term volatility.

Standard Deviation Levels and Extreme Levels

This indicator includes several features to help visualize overbought and oversold conditions:

Standard Deviation Levels: The script plots horizontal lines at +1, +2, -1, and -2 standard deviations. These levels provide a reference for how far the current price is from the mean, allowing traders to quickly identify when the price is moving into extreme territory.

Extreme Levels: Additional extreme levels at +3 and +4 (and their negative counterparts) are plotted to highlight areas where the price is highly likely to revert. These extreme levels provide important insight into market conditions that are far outside the norm, signaling caution or potential reversal zones.

The indicator also adapts the color shading of these extreme zones based on the Z-Score’s strength. For example, the area between +3 and +4 is shaded with a stronger color when the Z-Score approaches these values, giving a visual representation of market pressure.

Divergences: Detecting Hidden and Regular Signals

A key feature of the Savitzky-Golay Z-Score is its ability to detect bullish and bearish divergences, both regular and hidden:

Regular Bullish Divergence: This occurs when the price makes a lower low while the Z-Score forms a higher low. It signals that bearish momentum is weakening, and a bullish reversal could be near.

Hidden Bullish Divergence: This divergence occurs when the price makes a higher low while the Z-Score forms a lower low. It signals that bullish momentum may continue after a temporary pullback.

Regular Bearish Divergence: This occurs when the price makes a higher high while the Z-Score forms a lower high, signaling that bullish momentum is weakening and a bearish reversal may be near.

Hidden Bearish Divergence: This divergence occurs when the price makes a lower high while the Z-Score forms a higher high, indicating that bearish momentum may continue after a temporary rally.

These divergences are plotted directly on the chart, making it easier for traders to spot when the price and momentum are out of sync and when a potential reversal may occur.

Customization and Visualization

The Savitzky-Golay Z-Score offers a range of customization options to fit different trading styles:

Window Size and Polynomial Degree: Adjust the window size and polynomial degree of the Savitzky-Golay filter to control how much smoothing is applied to the price data.

Z-Score Lookback Period: Set the lookback period for calculating the Z-Score, allowing traders to fine-tune the sensitivity to short-term or long-term price movements.

Display Options: Choose whether to display standard deviation levels, extreme levels, and divergence labels on the chart.

Bar Color: Color the price bars based on trend direction, with green for bullish trends and red for bearish trends, allowing traders to easily visualize the current momentum.

Divergences: Enable or disable divergence detection, and adjust the lookback periods for pivots used to detect regular and hidden divergences.

Alerts and Automation

To ensure you never miss an important signal, the indicator includes built-in alert conditions for the following events:

Positive Z-Score (Long Signal): Triggers an alert when the Z-Score crosses above zero, indicating a potential buying opportunity.

Negative Z-Score (Short Signal): Triggers an alert when the Z-Score crosses below zero, signaling a potential short opportunity.

Shifting Momentum: Alerts when the Z-Score is shifting up or down, providing early warning of changing market conditions.

These alerts can be configured to notify you via email, SMS, or app notification, allowing you to stay on top of the market without having to constantly monitor the chart.

Trading Applications

The Savitzky-Golay Z-Score is a versatile tool that can be applied across multiple trading strategies:

Trend Following: By smoothing the price and calculating the Z-Score, this indicator helps traders follow the prevailing trend while avoiding false signals from short-term volatility.

Mean Reversion: The Z-Score highlights moments when the price is far from its mean, helping traders identify overbought or oversold conditions and capitalize on potential reversals.

Divergence Trading: Regular and hidden divergences between the Z-Score and price provide early warning of trend reversals, allowing traders to enter trades at opportune moments.

Final Thoughts

The Savitzky-Golay Z-Score is an advanced statistical tool designed to provide a clearer view of market trends and momentum. By applying the Savitzky-Golay filter and Z-Score analysis, this indicator reduces noise and highlights key areas where the market may reverse or accelerate, giving traders a significant edge in understanding price behavior.

Whether you’re a trend follower or a reversal trader, this indicator offers the flexibility and insights you need to navigate complex markets with confidence.

Approximate Spectral Entropy-Based Market Momentum (SEMM)Overview

The Approximate Spectral Entropy-Based Market Momentum (SEMM) indicator combines the concepts of spectral entropy and traditional momentum to provide traders with insights into both the strength and the complexity of market movements. By measuring the randomness or predictability of price changes, SEMM helps traders understand whether the market is in a trending or consolidating state and how strong that trend or consolidation might be.

Key Features

Entropy Measurement: Calculates the approximate spectral entropy of price movements to quantify market randomness.

Momentum Analysis: Integrates entropy with rate-of-change (ROC) to highlight periods of strong or weak momentum.

Dynamic Market Insight: Provides a dual perspective on market behavior—both the trend strength and the underlying complexity.

Customizable Parameters: Adjustable window length for entropy calculation, allowing for fine-tuning to suit different market conditions.

Concepts Underlying the Calculations

The indicator utilizes Shannon entropy, a concept from information theory, to approximate the spectral entropy of price returns. Spectral entropy traditionally involves a Fourier Transform to analyze the frequency components of a signal, but due to Pine Script limitations, this indicator uses a simplified approach. It calculates log returns over a rolling window, normalizes them, and then computes the Shannon entropy. This entropy value represents the level of disorder or complexity in the market, which is then multiplied by traditional momentum measures like the rate of change (ROC).

How It Works

Price Returns Calculation: The indicator first computes the log returns of price data over a specified window length.

Entropy Calculation: These log returns are normalized and used to calculate the Shannon entropy, representing market complexity.

Momentum Integration: The calculated entropy is then multiplied by the rate of change (ROC) of prices to generate the SEMM value.

Signal Generation: High SEMM values indicate strong momentum with higher randomness, while low SEMM values indicate lower momentum with more predictable trends.

How Traders Can Use It

Trend Identification: Use SEMM to identify strong trends or potential trend reversals. Low entropy values can indicate a trending market, whereas high entropy suggests choppy or consolidating conditions.

Market State Analysis: Combine SEMM with other indicators or chart patterns to confirm the market's state—whether it's trending, ranging, or transitioning between states.

Risk Management: Consider high SEMM values as a signal to be cautious, as they suggest increased market unpredictability.

Example Usage Instructions

Add the Indicator: Apply the "Approximate Spectral Entropy-Based Market Momentum (SEMM)" indicator to your chart.

Adjust Parameters: Modify the length parameter to suit your trading timeframe. Shorter lengths are more responsive, while longer lengths smooth out the signal.

Analyze the Output: Observe the blue line for entropy and the red line for SEMM. Look for divergences or confirmations with price action to guide your trades.

Combine with Other Tools: Use SEMM alongside moving averages, support/resistance levels, or other indicators to build a comprehensive trading strategy.

Weekday Signal [QuantAlchemy]### Weekday Signal Indicator

#### Overview

The "Weekday Signal " indicator offers a method for triggering entry and exit signals based on specific weekdays and defined trading sessions. This allows traders to tailor their strategies to time slots and days, ensuring strategic execution and optimal trading periods.

Additionally, this indicator exposes signals for external use in other scripts, enabling integration with additional trading strategies or indicators, thereby enhancing its utility and flexibility for trading systems.

#### Definitions

- **Weekday Signal**: An indicator designed to trigger entry and exit signals based on specific weekdays within defined trading sessions.

- **Time Zone**: The local or preferred time zone setting to match market hours across global exchanges.

- **Trading Session**: The specific hours within a day when the trading signals are active.

#### Plots

- **Enter Signal**: Plots a signal when the conditions for entering a trade are met.

- **Exit Signal**: Plots a signal when the conditions for exiting a trade are met.

#### Properties

- **Flexible Time Zones**: Allows users to set their preferred time zone to align with global market hours.

- **Customizable Entry and Exit Days**: Users can select specific weekdays for entry and exit signals.

- **Defined Trading Sessions**: Users can define trading session hours to restrict signals to optimal market times.

- **Visual Indicators**: Provides clear visual plots and background colors on the chart to indicate when entry and exit criteria are met.

- **Dual Group Configuration**: Separate controls for entry and exit setups, offering flexibility in managing trading signals.

#### How to Read

1. **Green Background**: Indicates a potential entry signal.

2. **Red Background**: Indicates a potential exit signal.

3. **Status Line and Data Window**: Shows a value of 1 when an entry or exit condition is met and 0 otherwise.

#### Proposed Interpretations

- **Entry Signals**: When the background turns green and the status line/data window shows a value of 1, it indicates a potential time to enter a trade based on the selected weekday and session.

- **Exit Signals**: When the background turns red and the status line/data window shows a value of 1, it indicates a potential time to exit a trade based on the selected weekday and session.

#### Essential Knowledge

- **Weekdays and Trading Sessions**: Understanding the significance of specific trading days and sessions can help in optimizing trade timings.

- **Time Zones**: Correctly setting the time zone ensures alignment with market hours and accurate signal generation.

#### Deeper Concepts

- **Signal Filtering**: The script uses the `time_filter` library to determine if the current time falls within the defined entry or exit periods.

#### Typical Use Cases

- **Intraday Trading**: Traders who want to restrict their trades to specific weekdays and trading sessions.

- **Strategy Integration**: Users can integrate the signals from this indicator into broader trading strategies or other Pine Scripts using the signals as an external reference to an input.

#### Limitations

- **Time Zone Settings**: Incorrect time zone settings can lead to misaligned signals.

- **Trading Sessions**: Signals are limited to the defined trading session hours, which may not cover all market conditions.

#### Final Thoughts

The "Weekday Signal " indicator is a tool for traders looking to refine their entry and exit points based on specific days and sessions. By leveraging customizable time zones and trading sessions, traders can refine their strategic execution.

#### Disclaimer

This indicator is for educational purposes only and should not be construed as financial advice. Trading involves risk, and you should consult with a qualified financial advisor before making any trading decisions.

utilsLibrary "utils"

Provides a set of utility functions for use in strategies or indicators.

colorGreen(opacity)

Parameters:

opacity (int)

colorRed(opacity)

Parameters:

opacity (int)

colorTeal(opacity)

Parameters:

opacity (int)

colorBlue(opacity)

Parameters:

opacity (int)

colorOrange(opacity)

Parameters:

opacity (int)

colorPurple(opacity)

Parameters:

opacity (int)

colorPink(opacity)

Parameters:

opacity (int)

colorYellow(opacity)

Parameters:

opacity (int)

colorWhite(opacity)

Parameters:

opacity (int)

colorBlack(opacity)

Parameters:

opacity (int)

trendChangingUp(emaShort, emaLong)

Signals when the trend is starting to change in a positive direction.