15-Minute ORB by @RhinoTradezOverview

Hey traders, ready to jump on the morning breakout train? The 15-Minute ORB by @RhinoTradez

is your go-to pal for rocking the Opening Range Breakout (ORB) scene, zeroing in on the first 15 minutes of the U.S. market day—9:30 to 9:45 AM Eastern Time. Picture this: sleek orange lines mark the high and low of that opening rush, but they only hang out during regular trading hours (9:30 AM-4:00 PM ET) and reset fresh each day—no old baggage here! Built in Pine Script v6 for that cutting-edge feel, it’s loaded with breakout signals and alerts to keep your trading game strong—ideal for SPY, QQQ, or any ticker you love.

Crafted by @RhinoTradez

to fuel your daily grind—let’s hit those breakouts running!

What It Does

The ORB strategy is all about that early market spark: the 9:30-9:45 AM range sets the battlefield, and breakouts signal the charge. Here’s the rundown:

Captures the Range : Snags the high and low from the 9:30-9:45 AM ET candle—U.S. market kickoff, locked in.

Daily Refresh : Wipes yesterday’s lines at 9:30 AM ET each day—today’s all that matters.

Regular Hours Focus : Orange lines shine from 9:45 AM to 4:00 PM ET, vanishing outside those hours.

Breakout Signals : Green triangles for upside breaks, red for downside, all within regular hours.

Alerts You : Chimes in with “Price broke above 15-min ORB High: 597” (or below the low) when the move hits.

It’s your morning breakout blueprint—simple, focused, and trader-ready.

Functionality Breakdown:

15-Minute ORB Snap:

Locks the high and low of the 9:30-9:45 AM ET candle on a 15-minute chart (EST/EDT auto-adjusted).

Resets daily at 9:30 AM ET—yesterday’s range is outta here.

Regular Hours Only:

Lines glow from 9:45 AM to 4:00 PM ET, keeping pre-market and after-hours clean.

Breakout Flags:

Marks price busting above the ORB high (green triangle below bar) or below the low (red triangle above), only during 9:30 AM-4:00 PM.

Alert Action:

Drops a custom alert with the breakout price (e.g., “Price broke below 15-min ORB Low: 594”)—stay in the know, hands-free.

Customization Options

Keep it chill with one slick tweak:

ORB Line Color : Starts at orange—vibrant and trader-cool! Flip it to blue, purple, or any shade you dig in the settings. Make it yours.

How to Use It

Pop It On: Add it to a 15-minute chart—SPY, QQQ, or your hot pick works like a dream.

Time It Right: Set your chart to “America/New_York” time (Chart Settings > Time Zone) to sync with 9:30 AM ET.

Choose Your Color: Dive into the indicator settings and pick your ORB line color—orange kicks it off, but you’re in charge.

Set Alerts: Right-click the indicator, add an alert with “Any alert() function call,” and catch breakouts live.

Ride the Wave: Green triangle? Upward vibe. Red? Downside alert. Mix with volume or candles for extra punch.

Pro Tips

15-Minute Only : Tailored for that 9:30-9:45 AM ET candle—other timeframes won’t sync up.

Daily Reset : Lines refresh at 9:30 AM ET—always today’s play.

Breakout Boost : High volume or RSI can seal the deal on those triangle signals.

No Clutter : Lines stick to 9:30 AM-4:00 PM ET—your chart stays tidy.

Brought to you by @RhinoTradez

in Pine Script v6, this ORB script’s your morning breakout wingman. Slap it on, pick a color, and let’s chase those moves together! Happy trading!

"博时黄金ETF联接C基金同类基金的最大回撤率、波动率、夏普比率对比数据" için komut dosyalarını ara

Volume Width Based Candles

Overview

This indicator reimagines traditional candlestick charts by adjusting the horizontal width of each candle based on the bar’s trading volume. In other words, candles with higher volume appear wider, while those with lower volume are drawn narrower. This extra visual dimension can help traders quickly identify bars with significant volume relative to a defined lookback period.

Key Components

Volume Normalization:

The script calculates the highest volume over a user-defined lookback period (default is 100 bars).

Each bar’s volume is then normalized by dividing it by this maximum value. The result is a value between 0 and 1 that represents how the current volume compares to the maximum over the lookback.

Variable Candle Width Calculation:

A base multiplier (default set to 0.4) is used to control how much the volume influences the candle width.

The normalized volume is multiplied by this multiplier to compute an offset value.

Instead of using timestamps (which could lead to drawing objects too far into the future), the script uses the bar_index (the sequential index of bars) to determine the left and right positions of each candle.

The left and right x–positions are calculated by subtracting and adding the offset from the current bar index, respectively.

Candle Body & Wick Drawing:

Candle Body:

The body is drawn using box.new as a rectangle.

The top and bottom of the box are determined by the higher and lower values of the open and close prices.

The color of the candle is set based on whether the bar is bullish (green) or bearish (red).

Wicks:

The upper wick is drawn from the high of the bar down to the top of the body.

The lower wick is drawn from the low up to the bottom of the body.

These are created using line.new at the current bar index.

Handling Edge Cases:

The indicator includes conditions to avoid drawing errors on the very first bar (or any bar where prior data is unavailable).

It also converts the calculated x–coordinates (which are derived from the bar index plus a floating point offset) to integers since box.new requires integer values for positioning.

What It Tells the Trader

Volume Visualization:

Wider candles indicate bars where trading volume is high relative to recent history, potentially highlighting periods of increased market activity.

Narrower candles suggest lower volume, which can signal less interest or participation during that bar.

Contextual Price Action:

By integrating volume into the visual representation of each candle, traders get an immediate sense of the strength behind price movements.

This can be particularly useful for spotting potential breakouts, reversals, or confirming trends when analyzed alongside traditional price-based indicators.

Customization Options

Volume Lookback Period:

You can adjust the number of bars considered when determining the maximum volume. A shorter period may be more responsive to recent changes, while a longer period provides a broader context.

Base Width Multiplier:

Adjusting this multiplier changes how pronounced the effect of volume is on the candle’s width. Increasing it will make high-volume candles even wider, and decreasing it will reduce the difference between high and low volume candles.

Final Thoughts

This indicator is a creative way to overlay volume information directly onto the price chart without the need for separate volume bars. It provides an at-a-glance understanding of market activity and can be a valuable addition to a trader’s toolkit, especially for those who prefer visual cues integrated with price action. However, due to limitations (like the maximum number of drawn boxes), it’s best used on charts with a moderate amount of historical data or with appropriate adjustments to manage performance.

Capitulation Volume Detector by @RhinoTradezOverview

Hey traders, want to catch the market when it’s totally losing it? The Capitulation Volume Detector is your go-to buddy for spotting those wild moments when panic selling takes over. Picture this: prices plummet, volume explodes, and everyone’s bailing out—that’s capitulation, and it might just signal a turning point. This script throws a bright marker on your chart whenever the chaos hits, so you can decide if it’s time to jump in or sit tight. Built fresh in Pine Script v6, it’s sleek, customizable, and packs an alert to keep you posted—perfect for stocks, indices like SPY, or even crypto chaos.

Inspired by epic sell-offs like March 2020’s COVID crash, this tool’s here to help you navigate the storm with a smile (and maybe a profit).

What It Does

Capitulation volume is that “everyone’s out!” moment: a steep price drop meets a massive volume surge, hinting that sellers are tapped out. It’s not a guaranteed reversal—sometimes the bleeding continues—but it’s a loud clue that fear’s peaked. Here’s the magic:

Volume Check : Measures current volume against a customizable average (default: 20 bars).

Price Plunge : Tracks the percentage drop from the last close.

Capitulation Cal l: When volume rockets past your threshold (e.g., 2x average) and price tanks (e.g., -5%), you get a red triangle above the bar.

Stay Alert : Fires off a detailed message (e.g., “Volume 300M > 200M, Drop -10%”) so you’re never caught off guard.

Think of it as your market meltdown radar—simple, effective, and ready to roll.

Functionality Breakdown

Volume Surge Spotter :

Uses a 20-bar Simple Moving Average (SMA) of volume as your baseline.

Flags any bar where volume exceeds this average by your chosen multiplier (default: 2x).

Price Drop Detector :

Calculates the percentage change from the prior close.

Triggers when the drop’s bigger than your set limit (default: -5%).

Capitulation Marker:

Combines both signals: high volume + sharp drop = capitulation.

Slaps a red triangle above the bar for instant “whoa, there it is!” vibes.

Real-Time Alerts :

Sends a custom alert with volume and drop details, keeping you in the loop without babysitting the chart.

Customization Options

Tune it to your trading style with these easy settings:

Volume Multiplier (x Avg): Starts at 2.0 (2x average volume). Bump it to 3.0 for only the wildest spikes or dial it to 1.5 for more frequent catches. Range: 1.0-10.0, step 0.1.

Price Drop Threshold (%): Default 5.0 (a -5% drop). Go big with 10.0 for crash-level falls or ease to 3.0 for lighter dips. Range: 1.0-20.0, step 0.1.

Average Volume Period: Default 20 bars. Stretch it to 50 for a broader view or shrink to 10 for quick reactions. Range: 1-100.

Capitulation Marker Color: Red by default—because panic’s loud! Switch it to blue, green, or pink to match your chart’s personality.

How to Use It

Drop It On : Add it to any chart with volume data—SPY daily for market moves, /ES 15-minute for intraday action, or your go-to stock.

Play with Settings : Hit the indicator’s config gear and tweak the multiplier, drop threshold, period, or marker color to fit your vibe.

Set an Alert : Right-click the indicator, add an alert with “Any alert() function call,” and get pinged when capitulation strikes.

Watch the Action : Look for those red triangles on big drop days—pair with your favorite reversal signals for extra oomph.

Pro Tips

Daily Charts : Catch market-wide capitulations like March 23, 2020 (SPY: -10%, 3x volume).

Intraday : Spot flash crashes or sector sell-offs on 15-minute or 5-minute bars.

Context Matters : High volume alone isn’t enough—check the VIX or candlestick patterns (e.g., hammers) to confirm a bottom.

TestMA-STATEOverview:

This Pine Script (version 6) is designed to generate trading events based on moving average (MA) behavior and dynamically calculated percentiles. It leverages a custom state machine library (version 7) from decrypt_capital to track and manage state transitions related to MA conditions, and it triggers alerts (and optionally, chart labels) when specific state transitions occur.

Key Components:

License & Metadata:

The script is distributed under the Mozilla Public License 2.0.

It carries copyright by decrypt_capital.

The title ("TestMA-STATE") and short title ("MA-STATE") are defined, and the script runs on an overlay with extended backtracking and drawing limits.

State Machine Integration:

The script imports the lib_statemachine_modified library (version 7) using the alias modSM.

A persistent state machine instance (MovingAverageDirection_SM) is created to manage various MA-related states.

Several state constants are defined to represent different market conditions, such as:

MA_SHORT_ABOVE_OVERBOUGHT: When the short MA low is above the overbought threshold.

MA_SHORT_CROSSUNDER_MID & MA_SHORT_CROSSUNDER_BIG: Conditions for bearish crossunders.

MA_SHORT_BELOW_OVERSOLD: When the short MA high is below the oversold threshold.

MA_SHORT_CROSSOVER_MID & MA_SHORT_CROSSOVER_BIG: Conditions for bullish crossovers.

Inputs & MA Calculation:

Users can choose the type of moving average (EMA, SMA, WMA, VWMA) and adjust lengths for short, mid, and big MAs.

Additional inputs include lookback length for percentile calculations and percentile thresholds for determining overbought and oversold boundaries.

The script computes:

Short MA Low and High: Based on the low and high series.

Mid MA and Big MA: Based on the average price (ohlc4).

Dynamic Percentile Boundaries:

Two functions (f_getPercentile() and f_getPercentileArr()) calculate dynamic percentile values from the MA data.

These functions determine the oversold and overbought boundaries used in the state transition conditions.

Timestamp & Alert Header Formatting:

A helper function (f_formatTimestamp()) formats timestamps into a human-readable form (e.g., "Tue 12 Mar 16:30").

This formatted time, along with ticker information and other details, is used to build an alert header.

State Transitions & Alerts:

The script calls the state machine’s step() method multiple times with conditions based on the relationship between MA values and the percentile boundaries.

For example:

A bullish condition is triggered when the short MA low moves above the overbought threshold.

A bearish condition is triggered when the short MA high falls below the oversold boundary.

Transitions are further refined by checking if the MA is rising or falling.

When specific state transitions occur (e.g., MA_SHORT_CROSSOVER_MID after MA_SHORT_BELOW_OVERSOLD), the script:

Checks that the transition is recent (using the barsSinceState() method).

Optionally creates a label on the chart.

Triggers an alert with a descriptive message.

Chart Plotting:

The script plots the calculated moving averages (short, mid, and optionally big) on the chart.

It also plots the dynamic percentile boundaries for visual reference.

Purpose & Usage:

Trading Signal Generation:

The primary goal is to monitor key MA conditions and trigger alerts when significant crossovers or crossunders occur. These events—such as bullish crossovers when the market recovers from oversold conditions or bearish crossunders when the market retracts from overbought conditions—can be used as trading signals.

Visualization:

Users have options to display the various moving averages and percentile boundaries directly on the chart, as well as optional labels that mark when an alert is generated.

Alerting:

When specific state transitions are detected, the script constructs and sends an alert message with a timestamp, ticker, and descriptive text, aiding traders in making timely decisions.

THE Bucknut test PARI (SPY)📌 THE Bucknut Test PARI – Market Momentum & Volatility Gauge

🔹 Description

THE Bucknut Test PARI Indicator is a momentum and volatility-based market gauge designed to provide clear, actionable insights on price movement. This indicator calculates a Price Action Relative Index (PARI) score to help traders evaluate risk and potential market reversals.

It utilizes exponential moving average (EMA)-based momentum, standard deviation volatility, and SPY correlation to generate a PARI score between 1-100. The score is then categorized into risk zones, helping traders identify when conditions are favorable for entries or caution is needed.

Ideal for intraday traders, options traders (including SPX 0DTE), and swing traders looking to gauge volatility-driven market shifts.

🔥 Features & Functionality

✅ Momentum Calculation via EMA Filtering – Ensures smooth, responsive signals.

✅ Volatility-Based Adjustments – Uses standard deviation-based volatility scaling.

✅ SPY Correlation Filtering – Helps align momentum signals with market sentiment.

✅ User-Defined Timeframe Settings – Adjusts dynamically based on selected time intervals.

✅ Customizable Risk Thresholds – Allows traders to define high-risk, neutral, and low-risk zones.

✅ Non-Repainting Algorithm – Ensures reliable, static signals without revision.

⚙️ Settings & Adjustments

Setting Default Value Description

Time Frame Mode "5m-15m" Choose between 1m-3m, 5m-15m, or 1H-Daily. Affects smoothing values.

Scaling Factor 10 Adjusts PARI score sensitivity. Higher values amplify movement.

Background Color Black Custom background for the indicator panel.

Background Transparency 85 Controls indicator panel opacity (0 = solid, 100 = invisible).

High-Risk Threshold 80 Above this level, market is in overbought/high-risk conditions.

Low-Risk Threshold 20 Below this level, market is oversold/low-risk for potential reversals.

Neutral Level 50 Middle ground where price action is balanced.

📈 How to Use THE Bucknut Test PARI

🔴 Above 80 (High-Risk Zone)

Market may be overheated, strong momentum may fade or reverse soon.

Caution with calls; potential put opportunities.

🟢 Below 20 (Low-Risk Zone)

Market is oversold, potential reversal or bounce incoming.

Consider long entries or avoiding shorts.

⚪ Between 20-80 (Neutral Zone)

Market is in equilibrium; follow primary trend direction.

No extreme risk, trend-following strategies preferred.

🔍 Example Use Cases

✔ Intraday Traders → Gauge market strength on short-term charts (1m-15m).

✔ SPX 0DTE Options Traders → Time high-confidence call/put setups.

✔ Swing Traders → Identify periods of excessive momentum or exhaustion.

VIX/VIX3M Ratio計算並顯示 CBOE:VIX 和 CBOE:VIX3M 的比率,幫助交易者評估市場的波動性。

當比率超過設定的高水平或低於低水平時,指標將顯示為紅色,提示潛在的市場異常情況。

Calculates and displays the ratio of CBOE:VIX to CBOE:VIX3M, helping traders assess market volatility.

When the ratio exceeds the set high level or falls below the low level, the indicator will be displayed in red, signaling potential market anomalies.

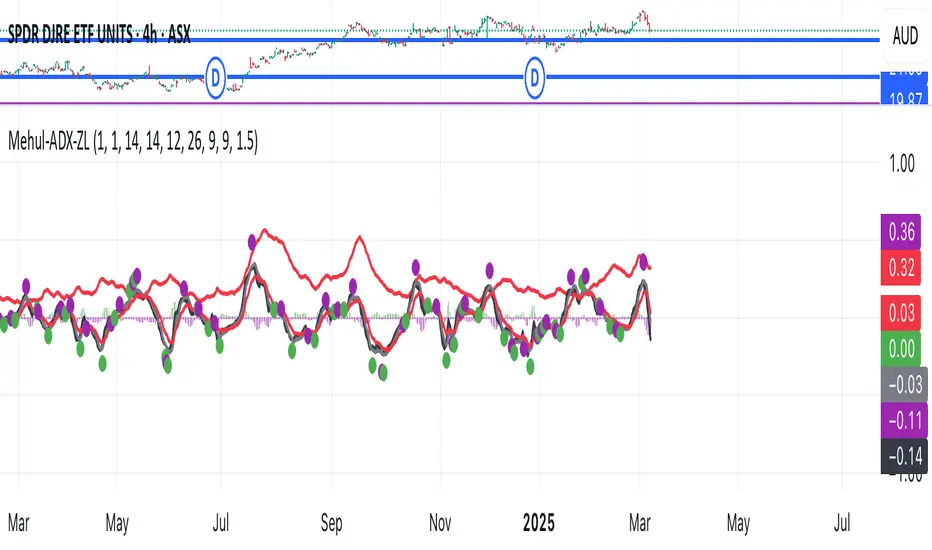

Mehul - ADX Zero LagThis script combines two popular technical indicators into a single visualization:

1. **Average Directional Index (ADX)**:

- Measures trend strength on a scale from 0-100 (now normalized to 0-1 by dividing by 100)

- Displayed as a red line

- Adjustable smoothing and length parameters

2. **Zero Lag MACD (Modified Moving Average Convergence Divergence)**:

- An enhanced version of the traditional MACD with reduced lag

- Shows the relationship between fast and slow moving averages

- Main components include:

- MACD line (black)

- Signal line (gray)

- Histogram (green for positive, purple for negative)

- EMA of the MACD line (red)

- Optional crossing dots

Key features of the combined indicator:

- **Scale Adjustment**: Both indicators can be scaled independently (adxScale and macdScale parameters)

- **Visibility Toggles**: Each indicator can be shown or hidden

- **Advanced Customization**: Parameters for both indicators can be fine-tuned

- **Algorithm Selection**: Option to choose between the "Glaz" algorithm or the "real" zero lag algorithm

- **Display Options**: Toggles for visualization elements like crossing dots

The most significant technical aspect is that both indicators are displayed in the same pane with compatible scaling, achieved by normalizing the ADX values and applying user-defined scale factors to both indicators.

This combined indicator is designed to give traders a comprehensive view of both trend strength (from ADX) and momentum/direction (from Zero Lag MACD) in a single, easy-to-read visualization.

Time Box Breakout IndicatorPlots Boxes with breakout signals on whatever timeframe the user selects.

Allows for users to see higher timeframe ranges on lower timeframes.

Useful for scalpers taking advantage of momentum, combined with support and resistance on higher timeframes.

Aids in visualizing risk, ranges and trends.

Dynamic Timeframe Trend AnalyzerPurpose and Core Logic

This indicator automatically adjusts its calculations based on the current chart’s timeframe, allowing traders to analyze trends, momentum, and mean reversion opportunities without manually changing indicator settings for each interval. It detects potential long or short setups by combining several techniques:

Dynamic Timeframe Factor

The script compares the current timeframe to a base (e.g., 5 minutes) and calculates a “factor” to scale certain parameters, such as EMA lengths or ATR settings. This reduces the need to reconfigure indicators when switching timeframes.

Regime Detection

It uses ADX (Average Directional Index) to classify the market as strongly trending, moderately trending, choppy, or in a potential mean-reversion phase.

RSI (Relative Strength Index) is also monitored for extreme levels (e.g., overbought/oversold) to detect potential reversal zones.

Volume is compared to a moving average to confirm or refute volatility conditions.

Trend & Mean Reversion Signals

EMA Alignment (8/21/55) helps identify bullish or bearish phases (strong bull if all EMAs align upward, strong bear if aligned downward).

For mean reversion opportunities, the script checks if ADX is sufficiently low (indicating weak or no trend) while price and RSI are at extreme levels—suggesting a snapback or countertrend move may occur.

Dynamic Stop Loss & Take Profit

Uses ATR (Average True Range) to set initial stop-loss (SL) and take-profit (TP) levels, then adjusts these levels further with “regime multipliers” based on whether the market is in a high-volatility trend or a quieter mean-reversion environment.

This approach aims to place stops and targets in a more adaptive way, reflecting current market conditions rather than a one-size-fits-all approach.

Visual Aids

Color-coded chart backgrounds (e.g., greenish for bullish trend, red for bearish, yellow/orange for mean reversion).

Triangles to show recent bullish/bearish signals.

A status table in the top-right corner (optional) displaying key metrics like ADX, RSI, dynamic thresholds, current SL/TP levels, and whether a stop loss has been hit.

How It Works Internally

ADX & Dynamic Thresholds:

A moving average (adx_mean) and standard deviation (adx_std) of the ADX are calculated over a lookback period to define “strong” vs. “weak” ADX thresholds.

This allows the script to adapt to changing volatility and trend strength in different markets or timeframes.

Mean Reversion Criteria:

The indicator checks if price deviates significantly from its own moving average, alongside RSI extremes. If ADX suggests no strong directional push (i.e., the market is “quiet”), it may classify conditions as mean-reverting.

Regime Multipliers:

Once the script identifies the market regime (e.g., strong uptrend, choppy, mean reversion), it applies different multipliers to the user-defined base values for stop-loss and take-profit. For instance, strong trending conditions might allow for wider stops to handle volatility, while mean reversion signals use tighter exits to capture quick reversals.

How to Use It

Timeframe Agnostic

Simply apply it to any timeframe (from 1-minute up to daily or weekly). The “Dynamic Timeframe Factor” will scale the indicator parameters automatically.

Look for Buy/Sell Triangles

When the script detects a valid bullish trend shift or a mean-reversion long setup, it plots a green triangle under the price bar. Conversely, it plots a red triangle above the price bar for bearish or mean-reversion short setups.

Check the Status Table

The table in the top-right corner summarizes the indicator’s current readings: ADX, RSI, volume trends, and the market regime classification.

The table also shows if a stop loss has been hit (SL Hit) and displays recommended SL/TP levels if a signal is active.

Stop Loss & Take Profit

The script plots lines for SL and TP on your chart after a new signal. These lines are automatically adjusted based on ATR, volume conditions, and ADX-derived multipliers.

Mean Reversion vs. Trend-Following

If you see a “Mean Rev” state in the table or the background turning yellow/orange, it suggests potential countertrend trades. Conversely, “STRONG BULL” or “STRONG BEAR” states favor momentum-based entries in the prevailing direction.

Originality & Benefits

Adaptive to Timeframe: Many indicators require reconfiguration when switching from short to long timeframes. This script automates that process using the “timeframe factor” logic.

Regime-Based SL/TP: Instead of fixed risk parameters, the script dynamically tunes stop and target levels depending on whether the market is trending or reverting.

Comprehensive Market View: It combines multiple factors—ADX, RSI, volume, moving averages, and volatility measurements—into a single, integrated framework that categorizes the market regime in real time.

Best Practices & Notes

Timeframes: It typically performs well on intraday timeframes (5m, 15m, 1H) but can also be used for swing trading on 4H or Daily charts.

Settings: The defaults are a good starting point, but you can adjust the base ATR multiplier or ADX lookbacks if you prefer a different balance between sensitivity and stability.

Risk Management: This indicator is not a guarantee of any specific results. Always use proper risk management (position sizing, stop-losses, and diversified strategies).

Alert Conditions: Built-in alert conditions can notify you when a new long or short signal appears, or when a stop loss is triggered.

ID 10 Second BarsEnters numbers 1, 3 and 5 under the appropriate bars on the 10 second chart and permits you to adjust the colors of each number.

QSL Upside/DownsideThe QSL Upside/Downside Indicator helps traders estimate potential gains and losses using Conditional Value at Risk (cVaR), a statistical measure that assesses both downside risk and upside potential beyond standard volatility. Instead of fixed timeframes (daily, weekly, etc.), traders can set a custom lookback period (in days) to analyze market behavior over their preferred time frame.

How It Works

The indicator calculates cVaR over the chosen period to determine how much an investment could move up or down based on past price behavior. It does this by:

• Mean Return – The average price movement over the period.

• Standard Deviation – Measures price fluctuations from the average.

• cVaR Confidence Interval (95%) – Estimates worst-case losses, meaning the downside projection reflects the worst 5% of expected losses.

• Upside Potential (Best 5%) – Instead of only considering risk, this indicator also calculates the potential upside by measuring returns in the top 5% of past price movements.

This provides a more complete view of what traders can expect—both in terms of risk and potential reward.

Key Features

✅ Custom Lookback Period – Set any number of days to analyze.

✅ cVaR Calculation (95% Confidence Interval) – Identifies extreme downside risks.

✅ Upside Potential (Best 5%) – Estimates how much an investment could rise in a best-case scenario.

✅ Clear Table Display – Quickly see projected best and worst-case portfolio values.

Understanding Probabilities: Upside & Downside Potential

Most traders focus on risk, but it’s equally important to understand potential gains. This indicator provides a probability-based view of expected market moves:

• 95% Confidence Interval (Downside cVaR) – There’s a 5% chance that losses could exceed this level.

• 95% Confidence Interval (Upside cVaR) – There’s a 5% chance that gains could be greater than this level.

• The remaining 90% of expected returns fall between these two extremes.

By knowing both potential losses and gains, traders can make more balanced, data-driven decisions rather than only focusing on worst-case scenarios.

Why Use This Indicator?

🔹 Better Risk & Reward Assessment – Understand both downside risk and upside potential.

🔹 More Realistic Market Projections – Uses probabilities instead of simple historical averages.

🔹 Flexible & Customizable – Works with any asset and any time period.

With this tool, QSL members can strategically plan trades, knowing the expected best and worst-case outcomes with a 95% probability range. 🚀

QSL Rolling Annualized VolatilityThis script calculates the rolling annualized volatility of an asset, helping traders measure how much its returns fluctuate over time. It uses logarithmic daily returns and computes the standard deviation over a custom lookback period (default: 252 trading days = 1 year) to capture historical volatility. The result is scaled to an annualized figure by multiplying by √252, making it comparable across different timeframes.

🔹 Key Features:

Customizable Lookback Period: Set in days to fit different trading strategies.

Annualized Output: Expresses volatility in yearly terms for consistency with financial models.

Rolling Calculation: Continuously updates to reflect recent market conditions.

Clear Visualization: Plots volatility as a time-series indicator and displays the latest value with a label.

This tool is ideal for risk management, position sizing, and strategy optimization in quantitative trading. 🚀

MM Labelled AVWAPTradingView provides a tool to show anchored VWAP plots on your screen, but there is no way to label the plots to add additional context to the level. Instead, users are forced to use the plot style (color, line style, line thickness, etc) to indicate what the plots are for and then they have to remember that meaning when looking at different charts. It also means that for key market-wide moments, users will need to add the plot for every symbol.

Now, for the first time on TradingView, you can create anchored VWAP plots with labels on them so you can understand the meaning behind the key moments you care about and don't need to remember what they mean by using styles like color or thickness. You can use this indicator to track key moments like the 2022 market bottom, or the Aug 9, 2024 "Carry Trade Unwind" bottom. The labelled AVWAP plots are visible on every chart by default. If you have an AVWAP moment that is only relevant to a small number of symbols, you can configure the indicator to only appear on those symbols.

Bollinger Bands MTF & Kalman Filter | Flux Charts📈 Multi-Timeframe Kalman Filtered Bollinger Bands Indicator

Introducing our MTF Kalman Filtered Bollinger Bands – a powerful multi-timeframe Bollinger Bands (BB) indicator enhanced with Kalman filtering for superior smoothing and trend analysis. This indicator dynamically adapts Bollinger Bands across multiple timeframes while incorporating volume-based gradient transparency to highlight significant price movements. This indicator is better optimized for lower timeframes.

❓ How to Interpret the Bands & Volume Gradient:

Our indicator combines Lower Timeframe (LTF) and Higher Timeframe (HTF) Bollinger Bands to provide a comprehensive trend analysis. It applies Kalman filtering to the LTF bands, ensuring smoother, noise-reduced signals. The color gradient and relative volume-based transparency offer deeper insights into price strength.

🔹 LTF Bollinger Bands: Shorter-period bands filtered with a Kalman smoothing algorithm, reducing lag and noise.

🔹 HTF Bollinger Bands: Traditional Bollinger Bands plotted on a higher timeframe, offering macro trend analysis.

🔹 Volume Gradient Transparency: The bands adjust their opacity based on relative buy/sell volume, allowing traders to assess momentum strength.

📌 How Does It Work?

1️⃣ Multi-Timeframe Bollinger Bands Calculation

The LTF BB uses Kalman filtering for a smoother price representation, helping to reduce false signals.

The HTF BB is EMA-smoothed for improved trend clarity.

2️⃣ Adaptive Gradient Transparency

The opacity of the fill color between the bands is determined by relative buy/sell volume.

Higher buy volume = stronger bullish signal (greener bands).

Higher sell volume = stronger bearish signal (redder bands).

3️⃣ Dynamic Trend Signals & Breakouts

Buy Signal: When price breaks below the HTF lower band and LTF bands start rising.

Sell Signal: When price breaks above the HTF upper band and LTF bands start falling.

⚙️ Settings & Customization:

🛠 LTF and HTF Bollinger Bands Settings:

Multiplier: The multiplier applied to the BB to determine the upper and lower bands

Length: Define the number of bars determines the BB calculations.

Custom Timeframe Selection: Choose from predefined options (e.g., 5m, 15m, 1H, 4H, etc).

🎨 Gradient & Transparency Settings:

Bullish/Bearish Color Options: Customize colors for uptrend and downtrend conditions.

Max & Min Opacity: Adjust the transparency levels based on volume intensity.

Solid vs. Gradient Mode: Choose between a gradient fill or a solid color mode for clarity.

📌 Recommended Settings for Optimal Use:

1️⃣ Timeframe Selection (LTF -> HTF):

1 min -> 5 min

2 min -> 5 min

3 min -> 15 min

5 min -> 15 min

15 min -> 1 hr

1 hr -> 4 hr

4 hr -> 1 day

2️⃣ Multiplier: Use 2.0 for LTF and 2.25 for HTF

3️⃣Length: Use a length of 20 - 30 bars

🚀 Why Use This Indicator?

✅ Multi-Timeframe Bollinger Bands with Kalman Filtering – Ideal for traders looking for reduced lag and clearer trend signals.

✅ Volume-Based Transparency – See momentum shifts instantly with adaptive opacity.

✅ Dynamic Buy & Sell Signals – Alerts based on price action + volume trends.

✅ Customizable for Any Strategy – Adjust colors, timeframes, and filtering options for personalized trading.

AntoQQE - HistogramThis script displays a QQE-based momentum histogram, derived from the RSI line’s deviation around a neutral 50 level. It uses a smoothed RSI, monitors volatility with a dynamically adjusted multiplier, and then plots a color-coded histogram that helps traders see when the RSI is entering strong bullish or bearish territory:

• Smoothed RSI Calculation

The script calculates RSI for a user-defined period and then smooths it with an EMA. This reduces noise in the indicator’s readings.

• Dynamic Average Range (DAR)

The script computes volatility by taking the absolute change of the smoothed RSI, applying two EMAs, and multiplying by a QQE factor. This produces a band around the RSI that adapts to changes in market volatility.

• Histogram Centering and Thresholds

Rather than plotting the RSI itself, the script subtracts 50 from the RSI to center it around zero. Columns are plotted for each bar:

Blue when momentum is significantly above zero (over a threshold value).

Red when momentum is significantly below zero (under a negative threshold).

Gray when momentum is within a neutral range.

• Usage

By observing when columns turn blue or red—and how far they extend above or below zero—traders can quickly gauge the market’s momentum. The horizontal threshold lines (dashed by default) provide clear breakout levels for bullish or bearish conditions, which can help confirm entries or exits based on shifting market sentiment. It is best paired with the AntoQQE - Bars indicator for better chart visualization.

AntoQQE - BarsThis script is a variation on the QQE (Quantitative Qualitative Estimation) concept applied to RSI. It calculates a smoothed RSI line, then determines a “Dynamic Average Range” around that line. By tracking the RSI’s movement relative to these upper (shortBand) and lower (longBand) levels, it determines when price momentum shifts enough to suggest a possible trend flip. The script plots color-coded candles based on these momentum conditions:

• RSI Calculation and Smoothing

An RSI value is obtained over a specified period, then smoothed by an EMA. This smoothed RSI serves as the core measure of momentum.

• Dynamic Average Range (DAR)

The script computes the volatility of the smoothed RSI using two EMAs of its bar-to-bar movements. It multiplies this volatility factor by a QQE multiplier to create upper and lower bands that adapt to changes in RSI volatility.

• Trend Flips

When the smoothed RSI crosses above or below its previous band level (shortBand or longBand), the script interprets this as a shift in momentum and sets a trend state accordingly (long or short).

• Candle Coloring

Finally, the script colors each candle according to how far the smoothed RSI is from a neutral baseline of 50:

Candles turn green when the RSI is sufficiently above 50, suggesting bullish momentum.

Candles turn red when the RSI is sufficiently below 50, indicating bearish momentum.

Candles turn orange when they are near the 50 level, reflecting a more neutral or transitional phase.

Traders can use these colored candles to quickly see when the RSI’s momentum has moved into overbought/oversold zones—or is shifting between bullish and bearish conditions—without needing to consult a separate oscillator window. The adaptive nature of the band calculations can help in spotting significant shifts in market sentiment and volatility.

NFP High/Low Levels PlusNFP High/Low Levels Plus

Description:

This indicator stores the 12 most recent NFP (Non-Farm-Payroll) days and their values.

Values are captured from 0830 (NFP Release) until close of market

The High and Low values for each NFP month are drawn on the chart with horizontal lines.

- Labels indicating the month's high or low line are placed after the line

- Optionally the high/low price can be displayed additionally

Support and Resistance boxes can be drawn at the closest NFP level above and below the

current price.

- Boxes will automatically update as prices cross the NFP value

Macro Indicator

- This option displays a small table in the top right corner that says "Up" or " Down"

- The Macro Indicator can be used to judge the potential direction for the current month

- Macro direction is calculated by the following:

- UP: If two consecutive days both open and close above the most recent NFP High level

- DOWN: If two consecutive days both open and close below the most recent NFP Low level

Micro Indicator

- This option displays a small table in the top right corner that says "Up" or " Down"

- The Micro Indicator can be used to judge the potential direction for low timeframes 1H or

lower

- Micro direction is calculated by the following:

- UP: If two consecutive 10m candles close above the 20EMA

- DOWN: If two consecutive 10m candles close below the 20EMA

NFP Session Bars

- This feature draws an arrow at the bottom of the chart for each candle that falls within the

NFP session day

- This is useful for identifying NFP Days

Support / Resistance Table

- This displays a table bottom center showing the nearest high and low NFP line level

What is an NFP Day and why is it useful to add to my chart?

- NFP Days are one of the most important data releases monthly

- NFP (Non-Farm-Payroll) is the official release of 80% of the US workforce employed in

manufacturing, construction, and goods

- It does not include those who work on farms, private households, non-profit and

government workers

- Historically these high/low levels for the day create strong support and resistance levels

- Having them displayed on the chart can help identify potential strong levels and pivot points

Full Indicator with all options enabled and identified

Easily update NFP Release Days in the indicator settings

Modify various options: Show/Hide lines, labels, directional indicator tables, values tables

Adjust line width, offsets, colors, font sizes, box widths

Enable individual Directional Indicators and modify colors

Example of full indicator enabled

You can find a list of the NFP Release Schedule on the official US Bureau of Labor Statistics website. This is useful for updating the indicator settings with the correct dates

Volume Pressure Histogram (Normalized)Overview

The Volume Pressure Histogram is designed to help traders analyze buying and selling pressure using real volume data.

Unlike traditional momentum indicators that rely solely on price movements, VPH measures the strength of bullish and bearish volume, providing insights into market participation.

How It Works

The histogram represents the difference between buying and selling volume over a selected period.

Green bars indicate strong buying pressure, while red bars signal strong selling pressure.

Lime and orange bars (if enabled) represent moderate buying and selling activity.

A white signal line smooths volume data to track momentum shifts over time.

How to Use It

Trend Confirmation: When price is rising and green bars increase, the trend is supported by real buying pressure.

Reversal Detection: If price makes a new high but green bars shrink, buyers may be losing strength.

Breakout Strength: A breakout with rising volume pressure confirms strong participation, while weak volume pressure suggests a potential fake move.

Divergence Signals: If price moves higher, but volume pressure declines, the move may lack conviction and could reverse.

Customization Options

Threshold Multiplier (default = 20) controls when green and red bars appear, filtering out weaker signals.

Log Scale Option helps normalize extreme volume spikes.

Adjustable Smoothing Length for both the histogram and signal line.

Why Use This Indicator

Provides a volume-based approach to analyzing market trends.

Can confirm or contradict price movements, helping identify strong or weak trends.

Works across multiple markets, including stocks, forex, crypto, and indices.

This indicator is designed for educational and informational purposes only and does not provide financial advice.

Volume Stack US Top 40 [Pt]█ Overview

Volume Stack US Top 40 is a versatile TradingView indicator designed to give you an at-a-glance view of market sentiment and volume dynamics across the top 40 U.S. large-cap stocks. Inspired by the popular Saty Volume Stack, this enhanced version aggregates essential volume and price strength data from major tickers on both the NYSE and NASDAQ, and works seamlessly on all timeframes.

█ Key Features

Dynamic Buy / Sell Volume Stack: This indicator dynamically stacks the volume bars so that the side with higher volume appears on top. For example, green over red signals more buy-side volume, while red over green indicates greater sell-side volume.

Cross-Market Analysis: Easily toggle between NYSE and NASDAQ to analyze the most influential U.S. stocks. The indicator automatically loads the correct set of tickers based on your selection.

Flexible Coverage: Choose from Top 10, Top 20, Top 30, or Top 40 tickers to tailor the tool to your desired scope of analysis.

Dynamic Table Display: A neat on-chart table lists the selected ticker symbols along with visual cues that reflect each stock’s strength. You can even remove exchange prefixes for a cleaner look.

█ Inputs & Settings

Market Selector: Choose whether to view data from the NYSE or NASDAQ; the indicator automatically loads the corresponding list of top tickers.

Number of Tickers: Select from ‘Top 10’, ‘Top 20’, ‘Top 30’, or ‘Top 40’ stocks to define the breadth of your analysis.

Color Options: Customize the colors for bullish and bearish histogram bars to suit your personal style.

Table Preferences: Adjust the on-chart table’s display style (grid or one row), text size, and decide whether to show exchange information alongside ticker symbols.

█ Usage & Benefits

Volume Stack US Top 40 is ideal for traders and investors who need a clear yet powerful tool to gauge overall market strength. By combining volume and price action data across multiple major stocks, it helps you:

Quickly assess whether the market sentiment is bullish or bearish.

Confirm trends by comparing volume patterns against intraday price movements.

Enhance your trading decisions with a visual representation of market breadth and dynamic buy/sell volume stacking.

Its intuitive design means you spend less time adjusting complex settings and more time making confident, informed decisions.

Asset Allocation CalculatorOverview

This script is a tool that automatically calculates asset allocation for your investment portfolio. Users can set the weight of multiple assets and monitor the portfolio value in real time based on price fluctuations.

Key Features

Supports input of asset allocation percentages

Dynamic allocation calculation based on real-time price data

Automatically calculates allocated amounts for each asset based on the total investment amount

User-friendly interface with intuitive visual feedback

Settings

Total Capital : Enter the total capital, including the value of assets.

Quantity rounding : Using the rounding function may cause the target allocation to exceed 100%.

Tickers, Weight, Holdings :

To retrieve accurate asset prices, specify both the exchange and the ticker.

If you want to include cash in your portfolio, use $.

Ensure that the total allocation sums to 100%.

Refer to the pre-filled example for the correct format.

Table Settings : You can adjust the table's position, height, font size, and background color.

How to Use

By buying or selling the quantity shown in the Buy column, you can continuously maintain your target allocation.

Hold - Current holdings

Buy - Quantity to buy or sell to reach the target allocation

Target - Quantity aimed for after buying or selling

Caution

It can only calculate for a single currency, so do not mix multiple currency markets.

자산 배분 계산기

소개

이 스크립트는 투자 포트폴리오의 자산 배분을 자동으로 계산해주는 도구입니다. 사용자는 여러 자산의 비중을 설정할 수 있으며, 가격 변동에 따라 포트폴리오 가치를 실시간으로 모니터링할 수 있습니다.

주요 기능

자산 배분 비율 입력 지원

실시간 가격 데이터를 기반으로 한 동적 배분 계산

총 투자 금액을 기준으로 각 자산에 할당된 금액 자동 계산

직관적인 시각적 피드백을 제공하는 사용자 친화적인 인터페이스

설정

Total Capital : 자산 가치를 포함한 총 자본금을 입력하세요.

Quantity rounding : 반올림 기능을 사용하면 목표 비중이 100%를 초과할 수 있습니다.

Tickers, Weight, Holdings :

정확한 자산 가격을 불러오기 위해 거래소와 티커를 함께 입력하세요.

포트폴리오에 현금을 포함하려면 '$'를 사용하세요.

비중 합계가 반드시 100%가 되도록 설정하세요.

예제 형식을 참고하여 올바르게 입력하세요.

한국(원화) 시장을 위한 입력 예시입니다.

KRX:360750, 17.5, 100

KRX:310960, 17.5, 120

KRX:148070, 25, 20

KRX:305080, 25, 10

KRX:139320, 10, 150

UPBIT:BTCKRW, 5, 0.002

$,0,5000000

Table Settings : 테이블의 위치, 높이, 글자 크기 및 배경색을 조정할 수 있습니다.

사용 방법

Buy 열에 표시된 수량만큼 매수 또는 매도하면 목표 비중을 지속적으로 유지할 수 있습니다.

Hold - 현재 보유 수량

Buy - 목표 비중을 맞추기 위해 매수 또는 매도해야 하는 수량

Target - 매수, 매도 후 목표로 하는 수량

주의

한 가지 통화로만 계산할 수 있으니 여러 통화 시장을 혼용하지 마세요.

Average Daily Range ProjectionsCreates a trailing high and low projection based on the Average Daily Range.

Track the Session High and Low to determine the Daily Range.

Average the Daily Range by a fixed Period to create an Average Daily Range .

Track the Prior Daily Range .

Track the Current Daily Range .

Track the % of Range completion relative to the CDR & ADR(P).

From the Session Low, project an Average Daily Range High by adding the ADR.

From the Session High, project an Average Daily Range Low by subtracting the ADR.

When %R reaches 100% or greater, the ADR HI & LO will lock, showing the range break out or break down. As the Session High and Low create the Daily Range, observe the reaction of price as it reaches the limit of the expected daily range.

On strongly trending days, CDR is likely greater than PDR and ADR(P). Price can break away.

On ranging days, %R may fail to reach 100% and CDR may be lesser than PDR and ADR(P). Price can bounce around within the bounds of ADR HI & LO.

Market Snap Shot with Pine ScreenerMarket Snap Shot

The Market Snap Shot is a comprehensive technical analysis tool designed to track and display key price metrics across multiple timeframes, including daily, weekly, monthly, quarterly, and yearly data. This script provides a range of essential calculations for traders and investors, enabling them to assess price action, volatility, and market trends at a glance.

Features:

Daily Metrics: Includes the daily percentage change, closing range relative to the daily high/low.

Weekly Metrics: Tracks weekly open, close, range, and calculates week-to-date performance for a broader market view.

Monthly Metrics: Provides similar calculations for monthly price action, offering insights into monthly performance.

Quarter-to-Date (QTD): Displays performance for the current quarter, offering insights into quarterly price movements.

Year-to-Date (YTD): Calculates year-to-date price change, helping users track performance relative to the start of the year.

52-Week High/Low: Displays the current price's distance from the 52-week high and low, giving context to long-term price levels.

Usage:

Traders can use this screener to quickly assess the current market position and make informed decisions based on short-term and long-term trends.

Investors can leverage the 52-week and YTD metrics to gauge the overall strength of an asset in the market.

The tool is versatile for both active traders looking for real-time performance data and for those focusing on longer-term market trends.

Instructions:

This script displays multiple metrics such as percentage changes and range data for daily, weekly, monthly, quarterly, and yearly timeframes. It is designed to be used as a screener tool to assess price action and monitor performance across these key time periods.

Warning:

The "Market Snap Shot" does not provide buy or sell signals but rather serves as a performance tracking tool. Users are encouraged to use this data in conjunction with other technical and fundamental analysis tools.

Mile Runner - Swing Trade LONGMile Runner - Swing Trade LONG Indicator - By @jerolourenco

Overview

The Mile Runner - Swing Trade LONG indicator is designed for swing traders who focus on LONG positions in stocks, BDRs (Brazilian Depositary Receipts), and ETFs. It provides clear entry signals, stop loss, and take profit levels, helping traders identify optimal buying opportunities with a robust set of technical filters. The indicator is optimized for daily candlestick charts and combines multiple technical analysis tools to ensure high-probability trades.

Key Features

Entry Signals: Visualized as green triangles below the price bars, indicating a potential LONG entry.

Stop Loss and Take Profit Levels: Automatically plotted on the chart for easy reference.

Stop Loss: Based on the most recent pivot low (support level).

Take Profit: Calculated using a Fibonacci-based projection from the entry price to the stop loss.

Trend and Momentum Filters: Ensures trades align with the prevailing trend and have sufficient momentum.

Volume and Volatility Confirmation: Verifies market interest and price movement potential.

How It Works

The indicator uses a combination of technical tools to filter and confirm trade setups:

Exponential Moving Averages (EMAs):

A short EMA (default: 9 periods) and a long EMA (default: 21 periods) identify the trend.

A bullish crossover (EMA9 crosses above EMA21) signals a potential upward trend.

Money Flow Index (MFI):

Confirms buying pressure when MFI > 50.

Average True Range (ATR):

Ensures sufficient volatility by checking if ATR exceeds its 20-period moving average.

Volume:

Confirms market interest when volume exceeds its 20-period moving average.

Pivot Lows:

Identifies recent support levels (pivot lows) to set the stop loss.

Ensures the pivot low is recent (within the last 10 bars by default).

Additional Trend Filter:

Confirms the long EMA is rising, reinforcing the bullish trend.

Inputs and Customization

The indicator is highly customizable, allowing traders to tailor it to their strategies:

EMA Periods: Adjust the short and long EMA lengths.

ATR and MFI Periods: Modify lookback periods for volatility and momentum.

Pivot Lookback: Control the sensitivity of pivot low detection.

Fibonacci Level: Adjust the Fibonacci retracement level for take profit.

Take Profit Multiplier: Fine-tune the aggressiveness of the take profit target.

Max Pivot Age: Set the maximum bars since the last pivot low for relevance.

Usage Instructions

Apply the Indicator:

Add the "Mile Runner - Swing Trade LONG" indicator to your TradingView chart.

Best used on daily charts for swing trading.

Look for Entry Signals:

A green triangle below the price bar signals a potential LONG entry.

Set Stop Loss and Take Profit:

Stop Loss: Red dashed line indicating the stop loss level.

Take Profit: Purple dashed line showing the take profit level.

Monitor the Trade:

The entry price is marked with a green dashed line for reference.

Adjust trade management based on the plotted levels.

Set Alerts:

Use the built-in alert condition to get notified of new LONG entry signals.

Important Notes

For LONG Positions Only : Designed exclusively for swing trading LONG positions.

Timeframe: Optimized for daily charts but can be tested on other timeframes.

Asset Types: Works best with stocks, BDRs, and ETFs.

Risk Management: Always align stop loss and take profit levels with your risk tolerance.

Why Use Mile Runner?

The Mile Runner indicator simplifies swing trading by integrating trend, momentum, volume, and volatility filters into one user-friendly tool. It helps traders:

Identify high-probability entry points.

Establish clear stop loss and take profit levels.

Avoid low-volatility or low-volume markets.

Focus on assets with strong buying pressure and recent support.

By following its signals and levels, traders can make informed decisions and enhance their swing trading performance. Customize the inputs and test it on your favorite assets—happy trading!