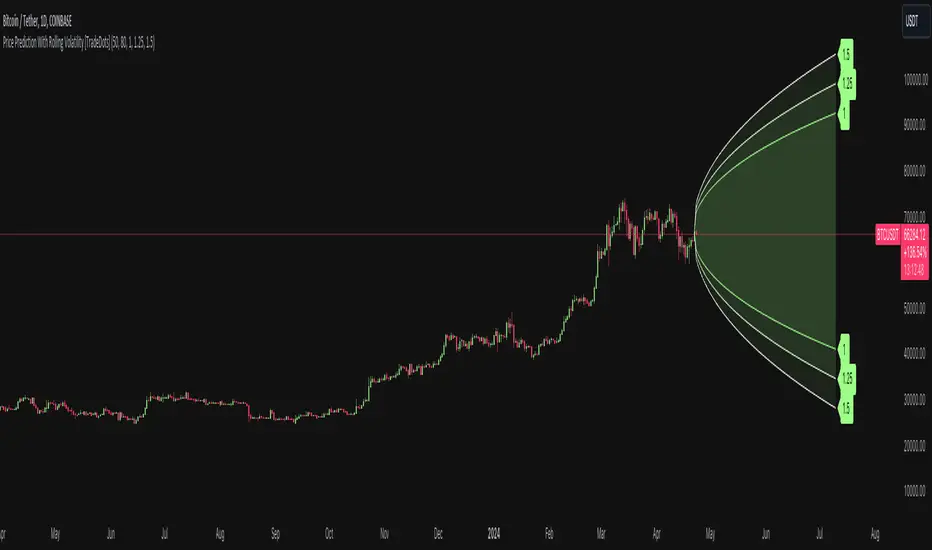

Price Prediction With Rolling Volatility [TradeDots]The "Price Prediction With Rolling Volatility" is a trading indicator that estimates future price ranges based on the volatility of price movements within a user-defined rolling window.

HOW DOES IT WORK

This indicator utilizes 3 types of user-provided data to conduct its calculations: the length of the rolling window, the number of bars projecting into the future, and a maximum of three sets of standard deviations.

Firstly, the rolling window. The algorithm amasses close prices from the number of bars determined by the value in the rolling window, aggregating them into an array. It then calculates their standard deviations in order to forecast the prospective minimum and maximum price values.

Subsequently, a loop is initiated running into the number of bars into the future, as dictated by the second parameter, to calculate the maximum price change in both the positive and negative direction.

The third parameter introduces a series of standard deviation values into the forecasting model, enabling users to dictate the volatility or confidence level of the results. A larger standard deviation correlates with a wider predicted range, thereby enhancing the probability factor.

APPLICATION

The purpose of the indicator is to provide traders with an understanding of the potential future movement of the price, demarcating maximum and minimum expected outcomes. For instance, if an asset demonstrates a substantial spike beyond the forecasted range, there's a significantly high probability of that price being rejected and reversed.

However, this indicator should not be the sole basis for your trading decisions. The range merely reflects the volatility within the rolling window and may overlook significant historical price movements. As with any trading strategies, synergize this with other indicators for a more comprehensive and reliable analysis.

Note: In instances where the number of predicted bars is exceedingly high, the lines may become scattered, presumably due to inherent limitations on the TradingView platform. Consequently, when applying three SD in your indicator, it is advised to limit the predicted bars to fewer than 80.

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

Komut dosyalarını "wind+芯片行业+市盈率+财经数据" için ara

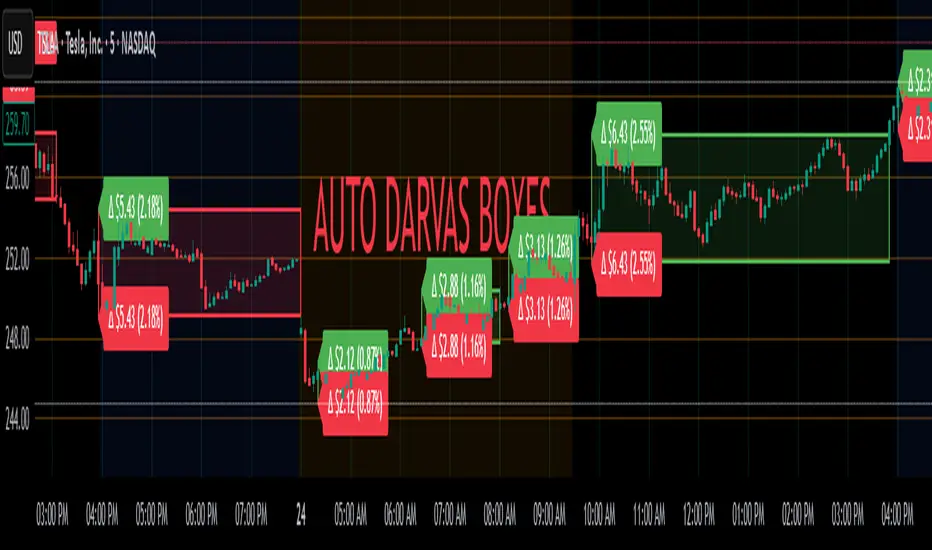

Auto Darvas Boxes## AUTO DARVAS BOXES

---

### OVERVIEW

**Auto Darvas Boxes** is a fully-automated, event-driven implementation of Nicolas Darvas’s 1950s box methodology.

The script tracks consolidation zones in real time, verifies that price truly “respects” those zones for a fixed validation window, then waits for the first decisive range violation to mark a directional breakout.

Every box is plotted end-to-end—from the first candle of the sideways range to the exact candle that ruptures it—giving you an on-chart, visually precise record of accumulation or distribution and the expansion that follows.

---

### HISTORICAL BACKGROUND

* Nicolas Darvas was a professional ballroom dancer who traded U.S. equities by telegram while touring the world.

* Without live news or Level II, he relied exclusively on **price** to infer institutional intent.

* His core insight: true market-moving entities leave footprints in the form of tight ranges; once their buying (or selling) is complete, price erupts out of the “box.”

* Darvas’s original procedure was manual—he kept notebooks, drew rectangles around highs and lows, and entered only when price punched out of the roof of a valid box.

* This indicator distills that logic into a rolling, self-resetting state machine so you never miss a box or breakout on any timeframe.

---

### ALGORITHM DETAIL (FOUR-STATE MACHINE)

**STATE 0 – RANGE DEFINITION**

• Examine the last *N* candles (default 7).

• Record `rangeHigh = highest(high, N) + tolerance`.

• Record `rangeLow = lowest(low, N) – tolerance`.

• Remember the index of the earliest bar in this window (`startBar`).

• Immediately transition to STATE 1.

**STATE 1 – RANGE VALIDATION**

• Observe the next *N* candles (again default 7).

• If **any** candle prints `high > rangeHigh` or `low < rangeLow`, the validation fails and the engine resets to STATE 0 **beginning at the violating candle**—no halfway boxes, no overlap.

• If all *N* candles remain inside the range, the box becomes **armed** and we transition to STATE 2.

**STATE 2 – ARMED (LIVE VISUAL FEEDBACK)**

• Draw a **green horizontal line** at `rangeHigh`.

• Draw a **red horizontal line** at `rangeLow`.

• Lines are extended in real time so the user can see the “live” Darvas ceiling and floor.

• Engine waits indefinitely for a breakout candle:

– **Up-Breakout** if `high > rangeHigh`.

– **Down-Breakout** if `low < rangeLow`.

**STATE 3 – BREAKOUT & COOLDOWN**

• Upon breakout the script:

1. Deletes the live range lines.

2. Draws a **filled rectangle (box)** from `startBar` to the breakout bar.

◦ **Green fill** when price exits above the ceiling.

◦ **Red fill** when price exits below the floor.

3. Optionally prints two labels at the left edge of the box:

◦ Dollar distance = `rangeHigh − rangeLow`.

◦ Percentage distance = `(rangeHigh − rangeLow) / rangeLow × 100 %`.

• After painting, the script waits a **user-defined cooldown** (default = 7 bars) before reverting to STATE 0. The cooldown guarantees separation between consecutive tests and prevents overlapping rectangles.

---

### INPUT PARAMETERS (ALL ADJUSTABLE FROM THE SETTINGS PANEL)

* **BARS TO DEFINE RANGE** – Number of candles used for both the definition and validation windows. Classic Darvas logic uses 7 but feel free to raise it on higher timeframes or volatile instruments.

* **OPTIONAL TOLERANCE** – Absolute price buffer added above the ceiling and below the floor. Use a small tolerance to ignore single-tick spikes or data-feed noise.

* **COOLDOWN BARS AFTER BREAKOUT** – How long the engine pauses before hunting for the next consolidation. Setting this equal to the range length produces non-overlapping, evenly spaced boxes.

* **SHOW BOX DISTANCE LABELS** – Toggle on/off. When on, each completed box displays its vertical size in both dollars and percentage, anchored at the box’s left edge.

---

### REAL-TIME VISUALISATION

* During the **armed** phase you see two extended, colour-coded guide-lines showing the exact high/low that must hold.

* When the breakout finally occurs, those lines vanish and the rectangle instantly appears, coloured to match the breakout direction.

* This immediate visual feedback turns any chart into a live Darvas tape—no manual drawing, no lag.

---

### PRACTICAL USE-CASES & BEST-PRACTICE WORKFLOWS

* **INTRADAY MOMENTUM** – Drop the script on 1- to 15-minute charts to catch tight coils before they explode. The coloured box marks the precise origin of the expansion; stops can sit just inside the opposite side of the box.

* **SWING & POSITION TRADING** – On 4-hour or daily charts, boxes often correspond to accumulation bases or volatility squeezes. Waiting for the box-validated breakout filters many false signals.

* **MEAN-REVERSION OR “FADE” STRATEGIES** – If a breakout immediately fails and price re-enters the box, you may have trapped momentum traders; fading that failure can be lucrative.

* **RISK MANAGEMENT** – Box extremes provide objective, structure-based stop levels rather than arbitrary ATR multiples.

* **BACK-TEST RESEARCH** – Because each box is plotted from first range candle to breakout candle, you can programmatically measure hold time, range height, and post-breakout expectancy for any asset.

---

### CUSTOMISATION IDEAS FOR POWER USERS

* **VOLATILITY-ADAPTIVE WINDOW** – Replace the fixed 7-bar length with a dynamic value tied to ATR percentile so the consolidation window stretches or compresses with volatility.

* **MULTI-TIMEFRAME LOGIC** – Only arm a 5-minute box if the 1-hour trend is aligned.

* **STRATEGY WRAPPER** – Convert the indicator to a full `strategy{}` script, automate entries on breakouts, and benchmark performance across assets.

* **ALERTS** – Create TradingView alerts on both up-breakout and down-breakout conditions; route them to webhook for broker automation.

---

### FINAL THOUGHTS

**Auto Darvas Boxes** packages one of the market’s oldest yet still potent price-action frameworks into a modern, self-resetting indicator. Whether you trade equities, futures, crypto, or forex, the script highlights genuine contraction-expansion sequences—Darvas’s original “boxes”—with zero manual effort, letting you focus solely on execution and risk.

Walk Forward PatternsINTRO

In Euclidean geometry, every mathematical output has a planar projection. 'Walk Forward Patterns' can be considered a practical example of this concept. On the other hand, this indicator might also be viewed as an experiment in 'how playing with Lego as a child contributes to time series analysis' :)

OVERVIEW

This script dynamically generates the necessary optimization and testing ranges for Walk Forward Analysis based on user-defined bar count and length inputs. It performs automatic calculations for each step, offers 8 different window options depending on the inputs, and visualizes the results dynamically. I should also note that most of the window models consist of original patterns I have created.

ADDITIONAL INFO : WHAT IS WALK FORWARD ANALYSIS?

Although it is not the main focus of this indicator, providing a brief definition of Walk Forward Analysis can be helpful in correctly interpreting the results it generates. Walk Forward Analysis (WFA) is a systematic method for optimizing parameters and validating trading strategies. It involves dividing historical data into variable segments, where a strategy is first optimized on an in-sample period and then tested on an out-of-sample period. This process repeats by shifting the windows forward, ensuring that each test evaluates the strategy on unseen data, helping to assess its robustness and adaptability in real market conditions.

ORIGINALITY

There are very few studies on Walk Forward Analysis in TradingView. Even worse, there are no any open-source studies available. Someone has to start somewhere, I suppose. And in my personal opinion, determining the optimization and backtest intervals is the most challenging part of WFA. These intervals serve as a prerequisite for automated parameter optimization. I felt the need to publish this pattern module, which I use in my own WFA models, partly due to this gap on community scripts.

INDICATOR MECHANICS

To use the indicator effectively, you only need to perform four simple tasks:

Specify the total number of bars in your chart in the 'Bar Index' parameter.

Define the optimization (In-Sample Test) length.

Define the testing (Out-Of-Sample Test) length.

Finally, select the window type.

The indicator automatically models everything else (including the number of steps) based on your inputs. And the result; you now have a clear idea of which bars to use for your Walk Forward tests!

A COMMONLY USED WINDOW SELECTION METHOD: ROLLING

A more concrete definition of Walk Forward Analysis, specifically for the widely used Rolling method, can be described as follows:

Parameters that have performed well over a certain period are identified (Optimization: In-Sample).

These parameters are then tested on a shorter, subsequent period (Backtest: Out-of-Sample).

The process is repeated forward in time (At each step, the optimization and backtest periods are shifted by the backtest length).

If the cumulative percentage profit obtained from the backtest results is greater than half of the historical optimization profit, the strategy is considered "successful."

If the strategy is successful, the most recent (untested) optimization values are used for live trading.

OTHER WINDOW OPTIONS

ANCHORED: That's a pattern based on progressively expanding optimization ranges at each step. Backtest ranges move forward in a staircase-like manner.

STATIC: Optimization ranges remain fixed, while backtest ranges are shifted forward.

BLOCKED: Optimization ranges are shifted forward in groups of three blocks. Backtest ranges are also shifted in a staircase manner, even at the cost of creating gaps from the optimization end bars.

TRIANGULAR: Optimization ranges are shifted forward in triangular regions, while backtest ranges move in a staircase pattern.

RATIO: The optimization length increases by 25% of the initial step’s fixed length at each step. In other words, the length grows by 25% of the first step's length incrementally. Backtest ranges always start from the bar where the optimization ends.

FIBONACCI: A variation of the Ratio method, where the optimization shift factor is set to 0.618

RANDOM WALK

Unlike the window models explained above, we can also generate optimization and backtest ranges completely randomly—offering almost unlimited variations! When you select the "Random" option in the "Window" parameter on the indicator interface, random intervals are generated based on various trigonometric calculations. By changing the numerical value in the '🐒' parameter, you can create entirely unique patterns.

WHY THE 🐒 EMOJI?

Two reasons.

First, I think that as humanity, we are a species of tailless primates who become happy when we understand things :). At least evolutionarily. The entire history of civilization is built on the effort to express the universe in a scale we can comprehend. 'Knowledge' is an invention born from this effort, which is why we feel happiness when we 'understand'. Second, I can't think of a better metaphor for randomness than a monkey sitting at a keyboard. See: Monkey Test.

Anyway, I’m rambling :)

NOTES

The indicator generates results for up to 100 steps. As the number of steps increases, the table may extend beyond the screen—don’t forget to zoom out!

FINAL WORDS

I haven’t published a Walk Forward script yet . However, there seem to be examples that can perform parameter optimization in the true sense of the word, producing more realistic results without falling into overfitting in my library. Hopefully, I’ll have the chance to publish one in the coming weeks. Sincerely thanks to Kıvanç Özbilgiç, Robert Pardo, Kevin Davey, Ernest P. Chan for their inspiring publishments.

DISCLAIMER

That's just a script, nothing more. I hope it helps everyone. Do not forget to manage your risk. And trade as safely as possible. Best of luck!

© dg_factor

RSI from Rolling VWAP [CHE]Introducing the RSI from Rolling VWAP Indicator

Elevate your trading strategy with the RSI from Rolling VWAP —a cutting-edge indicator designed to provide unparalleled insights and enhance your decision-making on TradingView. This advanced tool seamlessly integrates the Relative Strength Index (RSI) with a Rolling Volume-Weighted Average Price (VWAP) to deliver precise and actionable trading signals.

Why Choose RSI from Rolling VWAP ?

- Clear Trend Detection: Our enhanced algorithms ensure accurate identification of bullish and bearish trends, allowing you to capitalize on market movements with confidence.

- Customizable Time Settings: Tailor the time window in days, hours, and minutes to align perfectly with your unique trading strategy and market conditions.

- Flexible Moving Averages: Select from a variety of moving average types—including SMA, EMA, WMA, and more—to smooth the RSI, providing clearer trend analysis and reducing market noise.

- Threshold Alerts: Define upper and lower RSI thresholds to effortlessly spot overbought or oversold conditions, enabling timely and informed trading decisions.

- Visual Enhancements: Enjoy a visually intuitive interface with color-coded RSI lines, moving averages, and background fills that make interpreting market data straightforward and efficient.

- Automatic Signal Labels: Receive immediate bullish and bearish labels directly on your chart, signaling potential trading opportunities without the need for constant monitoring.

Key Features

- Inspired by Proven Tools: Building upon the robust foundation of TradingView's Rolling VWAP, our indicator offers enhanced functionality and greater precision.

- Volume-Weighted Insights: By incorporating volume into the VWAP calculation, gain a deeper understanding of price movements and market strength.

- User-Friendly Configuration: Easily adjust settings to match your trading preferences, whether you're a novice trader or an experienced professional.

- Hypothesis-Driven Analysis: Utilize hypothetical results to backtest strategies, understanding that past performance does not guarantee future outcomes.

How It Works

1. Data Integration: Utilizes the `hlc3` (average of high, low, and close) as the default data source, with customization options available to suit your trading needs.

2. Dynamic Time Window: Automatically calculates the optimal time window based on an auto timeframe or allows for fixed time periods, ensuring flexibility and adaptability.

3. Rolling VWAP Calculation: Accurately computes the Rolling VWAP by balancing price and volume over the specified time window, providing a reliable benchmark for price action.

4. RSI Analysis: Measures momentum through RSI based on Rolling VWAP changes, smoothed with your chosen moving average for enhanced trend clarity.

5. Actionable Signals: Detects and labels bullish and bearish conditions when RSI crosses predefined thresholds, offering clear indicators for potential market entries and exits.

Seamless Integration with Your TradingView Experience

Adding the RSI from Rolling VWAP to your TradingView charts is straightforward:

1. Add to Chart: Simply copy the Pine Script code into TradingView's Pine Editor and apply it to your desired chart.

2. Customize Settings: Adjust the Source Settings, Time Settings, RSI Settings, MA Settings, and Color Settings to align with your trading strategy.

3. Monitor Signals: Watch for RSI crossings above or below your set thresholds, accompanied by clear labels indicating bullish or bearish trends.

4. Optimize Your Trades: Leverage the visual and analytical strengths of the indicator to make informed buy or sell decisions, maximizing your trading potential.

Disclaimer:

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Get Started Today

Transform your trading approach with the RSI from Rolling VWAP indicator. Experience the synergy of momentum and volume-based analysis, and unlock the potential for more accurate and profitable trades.

Download now and take the first step towards a more informed and strategic trading journey!

For further inquiries or support, feel free to contact

Best regards

Chervolino

Inspired by the acclaimed Rolling VWAP by TradingView

Volatility Breaker Blocks [BigBeluga]The Volatility Breaker Blocks indicator identifies key market levels based on significant volatility at pivot highs and lows. It plots blocks that act as potential support and resistance zones, marked in green (support) and blue (resistance). Even after a breakout, these blocks leave behind shadow boxes that continue to impact price action. The sensitivity of block detection can be adjusted in the settings, allowing traders to customize the identification of volatility breakouts. The blocks print triangle labels (up or down) after breakouts, indicating potential areas of interest.

🔵 IDEA

The Volatility Breaker Blocks indicator is designed to highlight key areas in the market where volatility has created significant price action. These blocks, created at pivot highs and lows with increased volatility, act as potential support and resistance levels.

The idea is that even after price breaks through these blocks, the remaining shadow boxes continue to influence price movements. By focusing on volatility-driven pivot points, traders can better anticipate how price may react when it revisits these areas. The indicator also captures the natural tendency for price to retest broken resistance or support levels.

🔵 KEY FEATURES & USAGE

◉ High Volatility Breaker Blocks:

The indicator identifies areas of high volatility at pivot highs and lows, plotting blocks that represent these zones. Green blocks represent support zones (identified at pivot lows), while blue blocks represent resistance zones (identified at pivot highs).

Support:

Resistance:

◉ Shadow Blocks after Breakouts:

When price breaks through a block, the block doesn't disappear. Instead, it leaves behind a shadow box, which can still influence future price action. These shadow blocks act as secondary support or resistance levels.

If the price crosses these shadow blocks, the block stops extending, and the right edge of the box is fixed at the point where the price crosses it. This feature helps traders monitor important price levels even after the initial breakout has occurred.

◉ Triangle Labels for Breakouts:

After the price breaks through a volatility block, the indicator prints triangle labels (up or down) at the breakout points.

◉ Support and Resistance Retests:

One of the key concepts in this indicator is the retesting of broken blocks. After breaking a resistance block, price often returns to the shadow box, which then acts as support. Similarly, after breaking a support block, price tends to return to the shadow box, which becomes a resistance level. This concept of price retesting and bouncing off these levels is essential for understanding how the indicator can be used to identify potential entries and exits.

The natural tendency of price to retest broken resistance or support levels.

Additionaly indicator can display retest signals of broken support or resistance

◉ Customizable Sensitivity:

The sensitivity of volatility detection can be adjusted in the settings. A higher sensitivity captures fewer but more significant breakouts, while a lower sensitivity captures more frequent volatility breakouts. This flexibility allows traders to adapt the indicator to different trading styles and market conditions.

🔵 CUSTOMIZATION

Calculation Window: Defines the window of bars over which the breaker blocks are calculated. A larger window will capture longer-term levels, while a smaller window focuses on more recent volatility areas.

Volatility Sensitivity: Adjusts the threshold for volatility detection. Lower sensitivity captures smaller breakouts, while higher sensitivity focuses on larger, more significant moves.

Retest Signals: Display or hide retest signals of shadow boxes

Indicators OverlayHello All,

This script shows the indicators in separate windows on the main chart. Included indicators are RSI, CCI, OBV, Stochastic, Money Flow Index, Average True Range and Chande Momentum Oscillator. indicator windows are located at the top or bottom of the chart according to last moves of the Closing price. Different colors are used for each indicator. Horizontal levels are shown as dashed line and label as well.

Using the options;

You can enable/disable the indicators you want to see or not

You can change source and length for each indicator

You can set window length. using this length indicator windows are located on the chart

After you added this indicator to your chart I recommend: right click on any of the indicator windows => "Visual Order" => "Bring to front" as seen screenshot below:

in this example only 3 indicators enabled and period is set as 80:

indicator windows moves to the top or bottom of the chart according to the close price:

P.S. if you want to see any other indicator in the options then leave a comment under the indicator ;)

Enjoy!

Great Expectations [LucF]Great Expectations helps traders answer the question: What is possible? It is a powerful question, yet exploration of the unknown always entails risk. A more complete set of questions better suited to traders could be:

What opportunity exists from any given point on a chart?

What portion of this opportunity can be realistically captured?

What risk will be incurred in trying to do so, and how long will it take?

Great Expectations is the result of an exploration of these questions. It is a trade simulator that generates visual and quantitative information to help strategy modelers visually identify and analyse areas of optimal expectation on charts, whether they are designing automated or discretionary strategies.

WARNING: Great Expectations is NOT an indicator that helps determine the current state of a market. It works by looking at points in the past from which the future is already known. It uses one definition of repainting extensively (i.e. it goes back in the past to print information that could not have been know at the time). Repainting understood that way is in fact almost all the indicator does! —albeit for what I hope is a noble cause. The indicator is of no use whatsoever in analyzing markets in real-time. If you do not understand what it does, please stay away!

This is an indicator—not a strategy that uses TradingView’s backtesting engine. It works by simulating trades, not unlike a backtest, but with the crucial difference that it assumes a trade (either long or short) is entered on all bars in the historic sample. It walks forward from each bar and determines possible outcomes, gathering individual trade statistics that in turn generate precious global statistics from all outcomes tested on the chart.

Great Expectations provides numbers summarizing trade results on all simulations run from the chart. Those numbers cannot be compared to backtest-produced numbers since all non-filtered bars are examined, even if an entry was taken on the bar immediately preceding the current one, which never happens in a backtest. This peculiarity does NOT invalidate Great Expectations calculations; it just entails that results be considered under a different light. Provided they are evaluated within the indicator’s context, they can be useful—sometimes even more than backtesting results, e.g. in evaluating the impact of parameter-fitting or variations in entry, exit or filtering strats.

Traders and strategy modelers are creatures of hope often suffering from blurred vision; my hope is that Great Expectations will help them appraise the validity of their setup and strat intuitions in a realistic fashion, preventing confirmation bias from obstructing perspective—and great expectations from turning into financial great deceptions.

USE CASES

You’ve identified what looks like a promising setup on other indicators. You load Great Expectations on the chart and evaluate if its high-expectation areas match locations where your setup’s conditions occur. Unless today is your lucky day, chances are the indicator will help you realize your setup is not as promising as you had hoped.

You want to get a rough estimate of the optimal trade duration for a chart and you don’t mind using the entry and exit strategies provided with the indicator. You use the trade length readouts of the indicator.

You’re experimenting with a new stop strategy and want to know how long it will keep you in trades, on average. You integrate your stop strategy in the indicator’s code and look at the average trade length it produces and the TST ratio to evaluate its performance.

You have put together your own entry and exit criteria and are looking for a filter that will help you improve backtesting results. You visually ascertain the suitability of your filter by looking at its results on the charts with great Expectations, to see if your filter is choosing its areas correctly.

You have a strategy that shows backtested trades on your chart. Great Expectations can help you evaluate how well your strategy is benefitting from high-opportunity areas while avoiding poor expectation spots.

You want more complete statistics on your set of strategies than what backtesting will provide. You use Great Expectations, knowing that it tests all bars in the sample that correspond to your criteria, as opposed to backtesting results which are limited to a subset of all possible entries.

You want to fool your friends into thinking you’ve designed the holy grail of indicators, something that identifies optimal opportunities on any chart; you show them the P&L cloud.

FEATURES

For one trade

At any given point on the chart, assuming a trade is entered there, Great Expectations shows you information specific to that trade simulation both on the chart and in the Data Window.

The chart can display:

the P & L Cloud which shows whether the trade ended profitably or not, and by how much,

the Opportunity & Risk Cloud which the maximum opportunity and risk the simulation encountered. When superimposed over the P & L cloud, you will see what I call the managed opportunity and risk, i.e the portion of maximum opportunity that was captured and the portion of the maximum risk that was incurred,

the target and if it was reached,

a background that uses a gradient to show different levels of trade length, P&L or how frequently the target was reached during simulation.

The Data Window displays more than 40 values on individual trades and global results. For any given trade you will know:

Entry/Exit levels, including slippage impact,

It’s outcome and duration,

P/L achieved,

The fraction of the maximum opportunity/risk managed by the trade.

For all trades

After going through all the possible trades on the chart, the indicator will provide you with a rare view of all outcomes expressed with the P&L cloud, which allows us to instantly see the most/least profitable areas of a chart using trade data as support, while also showing its relationship with the opportunity/risk encountered during the simulation. The difference between the two clouds is the managed opportunity and risk.

The Data Window will present you with numbers which we will go through later. Some of them are: average stop size, P/L, win rate, % opportunity managed, trade lengths for different types of trade outcomes and the TST (Target:Stop Travel) ratio.

Let’s see Great Expectations in action… and remember to open your Data Window!

INPUTS

Trade direction : You must first choose if you wish to look at long or short trades. Because of the way the indicator works and the amount of visual information on the chart, it is only practical to look at one type of trades at a time. The default is Longs.

Maximum trade Length (MaxL) : This is the maximum walk forward distance the simulator will go in analyzing outcomes from any given point in the past. It also determines the size of the dead zone among the chart’s last bars. A red background line identifies the beginning of the dead zone for which not enough bars have elapsed to analyze outcomes for the maximum trade length defined. If an ATR-based entry stop is used, that length is added to the wait time before beginning simulations, so that the first entry starts with a clean ATR value. On a sample of around 16000 bars, my tests show that the indicator runs into server errors at lengths of around 290, i.e. having completed ~4,6M simulation loop iterations. That is way too high a length anyways; 100 will usually be amply enough to ring out all the possibilities out of a simulation, and on shorter time frames, 30 can be enough. While making it unduly small will prevent simulations of expressing the market’s potential, the less you use, the faster the indicator will run. The default is 40.

Unrealized P&L base at End of Trade (EOT) : When a simulation ends and the trade is still open, we calculate unrealized P&L from an exit order executed from either the last in-trade stop on the previous bar, or the close of the last bar. You can readily see the impact of this selection on the chart, with the P&L cloud. The default is on the close.

Display : The check box besides the title does nothing.

Show target : Shows a green line displaying the trade’s target expressed as a multiple of X, i.e. the amplitude of the entry stop. I call this value “X” and use it as a unit to express profit and loss on a trade (some call it “R”). The line is highlighted for trades where the close reached the target during the trade, whether the trade ended in profit or loss. This is also where you specify the multiple of X you wish to use in calculating targets. The multiple is used even if targets are not displayed.

Show P&L Cloud : The cloud allows traders to see right away the profitable areas of the chart. The only line printed with the cloud is the “end of trade line” (EOT). The EOT line is the only way one can see the level where a trade ended on the chart (in the Data Window you can see it as the “Exit Fill” value). The EOT level for the trade determines if the trade ended in a profit or a loss. Its value represents one of the following:

- fill from order executed at close of bar where stop is breached during trade (which produces “Realized P/L”),

- simulation of a fill pseudo-fill at the user-defined EOT level (last close or stop level) if the trade runs its course through MaxL bars without getting stopped (producing Unrealized P/L).

The EOT line and the cloud fill print in green when the trade’s outcome is profitable and in red when it is not. If the trade was closed after breaching the stop, the line appears brighter.

Show Opportunity&Risk Cloud : Displays the maximum opportunity/risk that was present during the trade, i.e. the maximum and minimum prices reached.

Background Color Scheme : Allows you to choose between 3 different color schemes for the background gradients, to accommodate different types of chart background/candles. Select “None” if you don’t want a background.

Background source : Determines what value will be used to generate the different intensities of the gradient. You can choose trade length (brighter is shorter), Trade P&L (brighter is higher) or the number of times the target was reached during simulation (brighter is higher). The default is Trade Length.

Entry strat : The check box besides the title does nothing. The default strat is All bars, meaning a trade will be simulated from all bars not excluded by the filters where a MaxL bars future exists. For fun, I’ve included a pseudo-random entry strat (an indirect way of changing the seed is to vary the starting date of the simulation).

Show Filter State : Displays areas where the combination of filters you have selected are allowing entries. Filtering occurs as per your selection(s), whether the state is displayed or not. The effect of multiple selections is additive. The filters are:

1. Bar direction: Longs will only be entered if close>open and vice versa.

2. Rising Volume: Applies to both long and shorts.

3. Rising/falling MA of the length you choose over the number of bars you choose.

4. Custom indicator: You can feed your own filtering signal through this from another indicator. It must produce a signal of 1 to allow long entries and 0 to allow shorts.

Show Entry Stops :

1. Multiple of user-defined length ATR.

2. Fixed percentage.

3. Fixed value.

All entry stops are calculated using the entry fill price as a reference. The fill price is calculated from the current bar’s open, to which slippage is added if configured. This simulates the case where the strategy issued the entry signal on the previous bar for it to be executed at the next bar’s open.

The entry stop remains active until the in-trade stop becomes the more aggressive of the two stops. From then on, the entry stop will be ignored, unless a bar close breaches the in-trade stop, in which case the stop will be reset with a new entry stop and the process repeats.

Show In-trade stops : Displays in bright red the selected in-trade stop (be sure to read the note in this section about them).

1. ATR multiple: added/subtracted from the average of the two previous bars minimum/maximum of open/close.

2. A trailing stop with a deviation expressed as a multiple of entry stop (X).

3. A fixed percentage trailing stop.

Trailing stops deviations are measured from the highest/lowest high/low reached during the trade.

Note: There is a twist with the in-trade stops. It’s that for any given bar, its in-trade stop can hold multiple values, as each successive pass of the advancing simulation loops goes over it from a different entry points. What is printed is the stop from the loop that ended on that bar, which may have nothing to do with other instances of the trade’s in-trade stop for the same bar when visited from other starting points in previous simulations. There is just no practical way to print all stop values that were used for any given bar. While the printed entry stops are the actual ones used on each bar, the in-trade stops shown are merely the last instance used among many.

Include Slippage : if checked, slippage will be added/subtracted from order price to yield the fill price. Slippage is in percentage. If you choose to include slippage in the simulations, remember to adjust it by considering the liquidity of the markets and the time frame you’ll be analyzing.

Include Fees : if checked, fees will be subtracted/added to both realized an unrealized trade profits/losses. Fees are in percentage. The default fees work well for crypto markets but will need adjusting for others—especially in Forex. Remember to modify them accordingly as they can have a major impact on results. Both fees and slippage are included to remind us of their importance, even if the global numbers produced by the indicator are not representative of a real trading scenario composed of sequential trades.

Date Range filtering : the usual. Just note that the checkbox has to be selected for date filtering to activate.

DATA WINDOW

Most of the information produced by this indicator is made available in the Data Window, which you bring up by using the icon below the Watchlist and Alerts buttons at the right of the TV UI. Here’s what’s there.

Some of the information presented in the Data Window is standard trade data; other values are not so standard; e. g. the notions of managed opportunity and risk and Target:Stop Travel ratio. The interplay between all the values provided by Great Expectations is inherently complex, even for a static set of entry/filter/exit strats. During the constant updating which the habitual process of progressive refinement in building strategies that is the lot of strategy modelers entails, another level of complexity is no doubt added to the analysis of this indicator’s values. While I don’t want to sound like Wolfram presenting A New Kind of Science , I do believe that if you are a serious strategy modeler and spend the time required to get used to using all the information this indicator makes available, you may find it useful.

Trade Information

Entry Order : This is the open of the bar where simulation starts. We suppose that an entry signal was generated at the previous bar.

Entry Fill (including slip.) : The actual entry price, including slippage. This is the base price from which other values will be calculated.

Exit Order : When a stop is breached, an exit order is executed from the close of the bar that breached the stop. While there is no “In-trade stop” value included in the Data Window (other than the End of trade Stop previously discussed), this “Exit Order” value is how we can know the level where the trade was stopped during the simulation. The “Trade Length” value will then show the bar where the stop was breached.

Exit Fill (including slip.) : When the exit order is simulated, slippage is added to the order level to create the fill.

Chart: Target : This is the target calculated at the beginning of the simulation. This value also appear on the chart in teal. It is controlled by the multiple of X defined under the “Show Target” checkbox in the Inputs.

Chart: Entry Stop : This value also appears on the chart (the red dots under points where a trade was simulated). Its value is controlled by the Entry Strat chosen in the Inputs.

X (% Fill, including Fees) and X (currency) : This is the stop’s amplitude (Entry Fill – Entry Stop) + Fees. It represents the risk incurred upon entry and will be used to express P&L. We will show R expressed in both a percentage of the Entry Fill level (this value), and currency (the next value). This value represents the risk in the risk:reward ratio and is considered to be a unit of 1 so that RR can be expressed as a single value (i.e. “2” actually meaning “1:2”).

Trade Length : If trade was stopped, it’s the number of bars elapsed until then. The trade is then considered “Closed”. If the trade ends without being stopped (there is no profit-taking strat implemented, so the stop is the only exit strat), then the trade is “Open”, the length is MaxL and it will show in orange. Otherwise the value will print in green/red to reflect if the trade is winning/losing.

P&L (X) : The P&L of the trade, expressed as a multiple of X, which takes into account fees paid at entry and exit. Given our default target setting at 2 units of “X”, a trade that closes at its target will have produced a P&L of +2.0, i.e. twice the value of X (not counting fees paid at exit ). A trade that gets stopped late 50% further that the entry stop’s level will produce a P&L of -1.5X.

P&L (currency, including Fees) : same value as above, but expressed in currency.

Target first reached at bar : If price closed above the target during the trade (even if it occurs after the trade was stopped), this will show when. This value will be used in calculating our TST ratio.

Times Stop/Target reached in sim. : Includes all occurrences during the complete simulation loop.

Opportunity (X) : The highest/lowest price reached during a simulation, i.e. the maximum opportunity encountered, whether the trade was previously stopped or not, expressed as a multiple of X.

Risk (X) : The lowest/highest price reached during a simulation, i.e. the maximum risk encountered, whether the trade was previously stopped or not, expressed as a multiple of X.

Risk:Opportunity : The greater this ratio, the greater Opportunity is, compared to Risk.

Managed Opportunity (%) : The portion of Opportunity that was captured by the highest/low stop position, even if it occurred after a previous stop closed the trade.

Managed Risk (%) : The portion of risk that was protected by the lowest/highest stop position, even if it occurred after a previous stop closed the trade. When this value is greater than 100%, it means the trade’s stop is protecting more than the maximum risk, which is frequent. You will, however, never see close to those values for the Managed Opportunity value, since the stop would have to be higher than the Maximum opportunity. It is much easier to alleviate the risk than it is to lock in profits.

Managed Risk:Opportunity : The ratio of the two preceding values.

Managed Opp. vs. Risk : The Managed Opportunity minus the Managed Risk. When it is negative, which is most often is, it means your strat is protecting a greater portion of the risk than it captures opportunity.

Global Numbers

Win Rate(%) : Percentage of winning trades over all entries. Open trades are considered winning if their last stop/close (as per user selection) locks in profits.

Avg X%, Avg X (currency) : Averages of previously described values:.

Avg Profitability/Trade (APPT) : This measures expectation using: Average Profitability Per Trade = (Probability of Win × Average Win) − (Probability of Loss × Average Loss) . It quantifies the average expectation/trade, which RR alone can’t do, as the probabilities of each outcome (win/lose) must also be used to calculate expectancy. The APPT combine the RR with the win rate to yield the true expectancy of a strategy. In my usual way of expressing risk with X, APPT is the equivalent of the average P&L per trade expressed in X. An APPT of -1.5 means that we lose on average 1.5X/trade.

Equity (X), Equity (currency) : The cumulative result of all trade outcomes, expressed as a multiple of X. Multiplied by the Average X in currency, this yields the Equity in currency.

Risk:Opportunity, Managed Risk:Opportunity, Managed Opp. vs. Risk : The global values of the ones previously described.

Avg Trade Length (TL) : One of the most important values derived by going through all the simulations. Again, it is composed of either the length of stopped trades, or MaxL when the trade isn’t stopped (open). This value can help systems modelers shape the characteristics of the components they use to build their strategies.

Avg Closed Win TL and Avg Closed Lose TL : The average lengths of winning/losing trades that were stopped.

Target reached? Avg bars to Stop and Target reached? Avg bars to Target : For the trades where the target was reached at some point in the simulation, the number of bars to the first point where the stop was breached and where the target was reached, respectively. These two values are used to calculate the next value.

TST (Target:Stop Travel Ratio) : This tracks the ratio between the two preceding values (Bars to first stop/Bars to first target), but only for trades where the target was reached somewhere in the loop. A ratio of 2 means targets are reached twice as fast as stops.

The next values of this section are counts or percentages and are self-explanatory.

Chart Plots

Contains chart plots of values already describes.

NOTES

Optimization/Overfitting: There is a fine line between optimizing and overfitting. Tools like this indicator can lead unsuspecting modelers down a path of overfitting that often turns strategies into over-specialized beasts that do not perform elegantly when confronted to the real-world. Proven testing strategies like walk forward analysis will go a long way in helping modelers alleviate this risk.

Input tuning: Because the results generated by the indicator will vary with the parameters used in the active entry, filtering and exit strats, it’s important to realize that although it may be fun at first, just slapping the default settings on a chart and time frame will not yield optimal nor reliable results. While using ATR as often as possible (as I do in this indicator) is a good way to make strat parametrization adaptable, it is not a foolproof solution.

There is no data for the last MaxL bars of the chart, since not enough trade future has elapsed to run a simulation from MaxL bars back.

Modifying the code: I have tried to structure the code modularly, even if that entails a larger code base, so that you can adapt it to your needs. I’ve included a few token components in each of the placeholders designed for entry strategies, filters, entry stops and in-trade stops. This will hopefully make it easier to add your own. In the same spirit, I have also commented liberally.

You will find in the code many instances of standard trade management tasks that can be lifted to code TV strategies where, as I do in mine, you manage everything yourself and don’t rely on built-in Pine strategy functions to act on your trades.

Enjoy!

THANKS

To @scarf who showed me how plotchar() could be used to plot values without ruining scale.

To @glaz for the suggestion to include a Chandelier stop strat; I will.

To @simpelyfe for the idea of using an indicator input for the filters (if some day TV lets us use more than one, it will be useful in other modules of the indicator).

To @RicardoSantos for the random generator used in the random entry strat.

To all scripters publishing open source on TradingView; their code is the best way to learn.

To my trading buddies Irving and Bruno; who showed me way back how pro traders get it done.

SMC - Institutional Confidence Oscillator [PhenLabs]📊 Institutional Confidence Oscillator

Version: PineScript™v6

📌 Description

The Institutional Confidence Oscillator (ICO) revolutionizes market analysis by automatically detecting and evaluating institutional activity at key support and resistance levels using our own in-house detection system. This sophisticated indicator combines volume analysis, volatility measurements, and mathematical confidence algorithms to provide real-time readings of institutional sentiment and zone strength.

Using our advanced thin liquidity detection, the ICO identifies high-volume, narrow-range bars that signal institutional zone formation, then tracks how these zones perform under market pressure. The result is a dual-wave confidence oscillator that shows traders when institutions are actively defending price levels versus when they’re abandoning positions.

The indicator transforms complex institutional behavior patterns into clear, actionable confidence percentiles, helping traders align with smart money movements and avoid common retail trading pitfalls.

🚀 Points of Innovation

Automated thin liquidity zone detection using volume threshold multipliers and zone size filtering

Dual-sided confidence tracking for both support and resistance levels simultaneously

Sigmoid function processing for enhanced mathematical accuracy in confidence calculations

Real-time institutional defense pattern analysis through complete test cycles

Advanced visual smoothing options with multiple algorithmic methods (EMA, SMA, WMA, ALMA)

Integrated momentum indicators and gradient visualization for enhanced signal clarity

🔧 Core Components

Volume Threshold System: Analyzes volume ratios against baseline averages to identify institutional activity spikes

Zone Detection Algorithm: Automatically identifies thin liquidity zones based on customizable volume and size parameters

Confidence Lifecycle Engine: Tracks institutional defense patterns through complete observation windows

Mathematical Processing Core: Uses sigmoid functions to convert raw market data into normalized confidence percentiles

Visual Enhancement Suite: Provides multiple smoothing methods and customizable display options for optimal chart interpretation

🔥 Key Features

Auto-Detection Technology: Automatically scans for institutional zones without manual intervention, saving analysis time

Dual Confidence Tracking: Simultaneously monitors both support and resistance institutional activity for comprehensive market view

Smart Zone Validation: Evaluates zone strength through volume analysis, adverse excursion measurement, and defense success rates

Customizable Parameters: Extensive input options for volume thresholds, observation windows, and visual preferences

Real-Time Updates: Continuously processes market data to provide current institutional confidence readings

Enhanced Visualization: Features gradient fills, momentum indicators, and information panels for clear signal interpretation

🎨 Visualization

Dual Oscillator Lines: Support confidence (cyan) and resistance confidence (red) plotted as percentage values 0-100%

Gradient Fill Areas: Color-coded regions showing confidence dominance and strength levels

Reference Grid Lines: Horizontal markers at 25%, 50%, and 75% levels for easy interpretation

Information Panel: Real-time display of current confidence percentiles with color-coded dominance indicators

Momentum Indicators: Rate of change visualization for confidence trends

Background Highlights: Extreme confidence level alerts when readings exceed 80%

📖 Usage Guidelines

Auto-Detection Settings

Use Auto-Detection

Default: true

Description: Enables automatic thin liquidity zone identification based on volume and size criteria

Volume Threshold Multiplier

Default: 6.0, Range: 1.0+

Description: Controls sensitivity of volume spike detection for zone identification, higher values require more significant volume increases

Volume MA Length

Default: 15, Range: 1+

Description: Period for volume moving average baseline calculation, affects volume spike sensitivity

Max Zone Height %

Default: 0.5%, Range: 0.05%+

Description: Filters out wide price bars, keeping only thin liquidity zones as percentage of current price

Confidence Logic Settings

Test Observation Window

Default: 20 bars, Range: 2+

Description: Number of bars to monitor zone tests for confidence calculation, longer windows provide more stable readings

Clean Break Threshold

Default: 1.5 ATR, Range: 0.1+

Description: ATR multiple required for zone invalidation, higher values make zones more persistent

Visual Settings

Smoothing Method

Default: EMA, Options: SMA/EMA/WMA/ALMA

Description: Algorithm for signal smoothing, EMA responds faster while SMA provides more stability

Smoothing Length

Default: 5, Range: 1-50

Description: Period for smoothing calculation, higher values create smoother lines with more lag

✅ Best Use Cases

Trending market analysis where institutional zones provide reliable support/resistance levels

Breakout confirmation by validating zone strength before position entry

Divergence analysis when confidence shifts between support and resistance levels

Risk management through identification of high-confidence institutional backing

Market structure analysis for understanding institutional sentiment changes

⚠️ Limitations

Performs best in liquid markets with clear institutional participation

May produce false signals during low-volume or holiday trading periods

Requires sufficient price history for accurate confidence calculations

Confidence readings can fluctuate rapidly during high-impact news events

Manual fallback zones may not reflect actual institutional activity

💡 What Makes This Unique

Automated Detection: First Pine Script indicator to automatically identify thin liquidity zones using sophisticated volume analysis

Dual-Sided Analysis: Simultaneously tracks institutional confidence for both support and resistance levels

Mathematical Precision: Uses sigmoid functions for enhanced accuracy in confidence percentage calculations

Real-Time Processing: Continuously evaluates institutional defense patterns as market conditions change

Visual Innovation: Advanced smoothing options and gradient visualization for superior chart clarity

🔬 How It Works

1. Zone Identification Process:

Scans for high-volume bars that exceed the volume threshold multiplier

Filters bars by maximum zone height percentage to identify thin liquidity conditions

Stores qualified zones with proximity threshold filtering for relevance

2. Confidence Calculation Process:

Monitors price interaction with identified zones during observation windows

Measures volume ratios and adverse excursions during zone tests

Applies sigmoid function processing to normalize raw data into confidence percentiles

3. Real-Time Analysis Process:

Continuously updates confidence readings as new market data becomes available

Tracks institutional defense success rates and zone validation patterns

Provides visual and numerical feedback through the oscillator display

💡 Note:

The ICO works best when combined with traditional technical analysis and proper risk management. Higher confidence readings indicate stronger institutional backing but should be confirmed with price action and volume analysis. Consider using multiple timeframes for comprehensive market structure understanding.

ATAI Volume Pressure Analyzer V 1.0 — Pure Up/DownATAI Volume Pressure Analyzer V 1.0 — Pure Up/Down

Overview

Volume is a foundational tool for understanding the supply–demand balance. Classic charts show only total volume and don’t tell us what portion came from buying (Up) versus selling (Down). The ATAI Volume Pressure Analyzer fills that gap. Built on Pine Script v6, it scans a lower timeframe to estimate Up/Down volume for each host‑timeframe candle, and presents “volume pressure” in a compact HUD table that’s comparable across symbols and timeframes.

1) Architecture & Global Settings

Global Period (P, bars)

A single global input P defines the computation window. All measures—host‑TF volume moving averages and the half‑window segment sums—use this length. Default: 55.

Timeframe Handling

The core of the indicator is estimating Up/Down volume using lower‑timeframe data. You can set a custom lower timeframe, or rely on auto‑selection:

◉ Second charts → 1S

◉ Intraday → 1 minute

◉ Daily → 5 minutes

◉ Otherwise → 60 minutes

Lower TFs give more precise estimates but shorter history; higher TFs approximate buy/sell splits but provide longer history. As a rule of thumb, scan thin symbols at 5–15m, and liquid symbols at 1m.

2) Up/Down Volume & Derived Series

The script uses TradingView’s library function tvta.requestUpAndDownVolume(lowerTf) to obtain three values:

◉ Up volume (buyers)

◉ Down volume (sellers)

◉ Delta (Up − Down)

From these we define:

◉ TF_buy = |Up volume|

◉ TF_sell = |Down volume|

◉ TF_tot = TF_buy + TF_sell

◉ TF_delta = TF_buy − TF_sell

A positive TF_delta indicates buyer dominance; a negative value indicates selling pressure. To smooth noise, simple moving averages of TF_buy and TF_sell are computed over P and used as baselines.

3) Key Performance Indicators (KPIs)

Half‑window segmentation

To track momentum shifts, the P‑bar window is split in half:

◉ C→B: the older half

◉ B→A: the newer half (toward the current bar)

For each half, the script sums buy, sell, and delta. Comparing the two halves reveals strengthening/weakening pressure. Example: if AtoB_delta < CtoB_delta, recent buying pressure has faded.

[ 4) HUD (Table) Display /i]

Colors & Appearance

Two main color inputs define the theme: a primary color and a negative color (used when Δ is negative). The panel background uses a translucent version of the primary color; borders use the solid primary color. Text defaults to the primary color and flips to the negative color when a block’s Δ is negative.

Layout

The HUD is a 4×5 table updated on the last bar of each candle:

◉ Row 1 (Meta): indicator name, P length, lower TF, host TF

◉ Row 2 (Host TF): current ↑Buy, ↓Sell, ΔDelta; plus Σ total and SMA(↑/↓)

◉ Row 3 (Segments): C→B and B→A blocks with ↑/↓/Δ

◉ Rows 4–5: reserved for advanced modules (Wings, α/β, OB/OS, Top

5) Advanced Modules

5.1 Wings

“Wings” visualize volume‑driven movement over C→B (left wing) and B→A (right wing) with top/bottom lines and a filled band. Slopes are ATR‑per‑bar normalized for cross‑symbol/TF comparability and converted to angles (degrees). Coloring mirrors HUD sign logic with a near‑zero threshold (default ~3°):

◉ Both lines rising → blue (bullish)

◉ Both falling → red (bearish)

◉ Mixed/near‑zero → gray

Left wing reflects the origin of the recent move; right wing reflects the current state.

5.2 α / β at Point B

We compute the oriented angle between the two wings at the midpoint B:

β is the bottom‑arc angle; α = 360° − β is the top‑arc angle.

◉ Large α (>180°) or small β (<180°) flags meaningful imbalance.

◉ Intuition: large α suggests potential selling pressure; small β implies fragile support. HUD cells highlight these conditions.

5.3 OB/OS Spike

OverBought/OverSold (OB/OS) labels appear when directional volume spikes align with a 7‑oscillator vote (RSI, Stoch, %R, CCI, MFI, DeMarker, StochRSI).

◉ OB label (red): unusually high sell volume + enough OB votes

◉ OS label (teal): unusually high buy volume + enough OS votes

Minimum votes and sync window are user‑configurable; dotted connectors can link labels to the candle wick.

5.4 Top3 Volume Peaks

Within the P window the script ranks the top three BUY peaks (B1–B3) and top three SELL peaks (S1–S3).

◉ B1 and S1 are drawn as horizontal resistance (at B1 High) and support (at S1 Low) zones with adjustable thickness (ticks/percent/ATR).

◉ The HUD dedicates six cells to show ↑/↓/Δ for each rank, and prints the exact High (B1) and Low (S1) inline in their cells.

6) Reading the HUD — A Quick Checklist

◉ Meta: Confirm P and both timeframes (host & lower).

◉ Host TF block: Compare current ↑/↓/Δ against their SMAs.

◉ Segments: Contrast C→B vs B→A deltas to gauge momentum change.

◉ Wings: Right‑wing color/angle = now; left wing = recent origin.

◉ α / β: Look for α > 180° or β < 180° as imbalance cues.

◉ OB/OS: Note labels, color (red/teal), and the vote count.

◉Top3: Keep B1 (resistance) and S1 (support) on your radar.

Use these together to sketch scenarios and invalidation levels; never rely on a single signal in isolation.

[ 7) Example Highlights (What the table conveys) /i]

◉ Row 1 shows the indicator name, the analysis length P (default 55), and both TFs used for computation and display.

◉ B1 / S1 blocks summarize each side’s peak within the window, with Δ indicating buyer/seller dominance at that peak and inline price (B1 High / S1 Low) for actionable levels.

◉ Angle cells for each wing report the top/bottom line angles vs. the horizontal, reflecting the directional posture.

◉ Ranks B2/B3 and S2/S3 extend context beyond the top peak on each side.

◉ α / β cells quantify the orientation gap at B; changes reflect shifting buyer/seller influence on trend strength.

Together these visuals often reveal whether the “wings” resemble a strong, upward‑tilted arm supported by buyer volume—but always corroborate with your broader toolkit

8) Practical Tips & Tuning

◉ Choose P by market structure. For daily charts, 34–89 bars often works well.

◉ Lower TF choice: Thin symbols → 5–15m; liquid symbols → 1m.

◉ Near‑zero angle: In noisy markets, consider 5–7° instead of 3°.

◉ OB/OS votes: Daily charts often work with 3–4 votes; lower TFs may prefer 4–5.

◉ Zone thickness: Tie B1/S1 zone thickness to ATR so it scales with volatility.

◉ Colors: Feel free to theme the primary/negative colors; keep Δ<0 mapped to the negative color for readability.

Combine with price action: Use this indicator alongside structure, trendlines, and other tools for stronger decisions.

Technical Notes

Pine Script v6.

◉ Up/Down split via TradingView/ta library call requestUpAndDownVolume(lowerTf).

◉ HUD‑first design; drawings for Wings/αβ/OBOS/Top3 align with the same sign/threshold logic used in the table.

Disclaimer: This indicator is provided solely for educational and analytical purposes. It does not constitute financial advice, nor is it a recommendation to buy or sell any security. Always conduct your own research and use multiple tools before making trading decisions.

Signal Stack MeterWhat it is

A lightweight “go or no‑go” meter that combines your manual read of Structure, Location, and Momentum with automatic context from volatility and macro timing. It surfaces a single, tradeable answer on the chart: OK to engage or Standby.

Why traders like it

You keep your discretion and nuance, and the meter adds guardrails. It prevents good trade ideas from being executed in the wrong conditions.

What it measures

Manual buckets you set each day: Structure, Location, Momentum from 0 to 2

Volatility from VIX, term structure, ATR 5 over 60, and session gaps

Time windows for CPI, NFP, and FOMC with ET inputs and an exchange‑offset

Total score and a simple gate: threshold plus a “strong bucket” rule you choose

How to use in 30 seconds

Pick a preset for your market.

Set Structure, Location, Momentum to 0, 1, or 2.

Leave defaults for the auto metrics while you get a feel.

Read the header. When it says OK to engage, you have both your read and the context.

Defaults we recommend

OK threshold: 5

Strong bucket rule: Either Structure or Location equals 2

VIX triggers: 22 and 1.25× the 20‑SMA

Term mode: Diff at 0.00 tolerance. Ratio mode at 1.00+ is available

ATR 5/60 defense: 1.25. Offense cue: 0.85 or lower

ATR smoothing: 1

Gap mode: RTH with 0.60× ATR5 wild gap. ON wild range at 0.80× ATR5

CPI window 08:25 to 08:40 ET. FOMC window 13:50 to 14:30 ET

ET to exchange offset: −60 for CME index futures. Set to 0 for NYSE symbols like SPY

Alert cadence: Once per RTH session. Snooze first 30 minutes optional

New since the last description

Parity with Defense Mode for presets, sessions, ratio vs diff term mode, ATR smoothing, RTH‑key cadence, and snooze options

Event windows in ET with a simple offset to your exchange time

Alternate row backgrounds and full color control for readability

Exposed series for automation: EngageOK(1=yes) plus TotalScore

Debug toggle to see ATR ratio, term, and gap measurements directly

Notes

Dynamic alerts require “Any alert() function call”.

The meter is designed to sit opposite Defense Mode on the chart. Use the position input to avoid overlap.

9:45am NIFTY TRADINGTime Frame: 15 Minutes | Reference Candle Time: 9:45 AM IST | Valid Trading Window: 3 Hours

📌 Introduction

This document outlines a structured trading strategy for NIFTY & BANKNIFTY Options based on a 15-minute timeframe with a 9:45 AM IST reference candle. The strategy incorporates technical indicators, probability analysis, and strict trading rules to optimize entries and exits.

📊 Core Features

1. Reference Time Trading System

9:45 AM IST Candle acts as the reference for the day.

All signals (Buy/Sell/Reversal) are generated based on price action relative to this candle.

The valid trading window is 3 hours after the reference candle.

2. Signal Generation Logic

Signal Condition

Buy (B) Price breaks above reference candle high with confirmation

Sell (S) Price breaks below reference candle low with confirmation

Reversal (R) Early trend reversal signal (requires strict confirmation)

3. Probability Analysis System

The strategy calculates Win Probability (%) using 4 components:

Component Weight Calculation

Body Win Probability 30% Based on candle body strength (body % of total range)

Volume Win Probability 30% Current volume vs. average volume strength

Trend Win Probability 40% EMA crossover + RSI momentum alignment

Composite Probability - Weighted average of all 3 components

Probability Color Coding:

🟢 Green (High Probability): ≥70%

🟠 Orange (Medium Probability): 50-69%

🔴 Red (Low Probability): <50%

4. Timeframe Enforcement

Strictly 15-minute charts only (no other timeframes allowed).

System auto-disables signals if the wrong timeframe is selected.

📈 Technical Analysis Components

1. EMA System (Trend Analysis)

Short EMA (9) – Fast trend indicator

Middle EMA (20) – Intermediate trend

Long EMA (50) – Long-term trend confirmation

Rules:

Buy Signal: Price > 9 EMA > 20 EMA > 50 EMA (Bullish trend)

Sell Signal: Price < 9 EMA < 20 EMA < 50 EMA (Bearish trend)

2. Multi-Timeframe RSI (Momentum)

5M, 15M, 1H, 4H, Daily RSI values are compared for divergence/confluence.

Overbought (≥70) / Oversold (≤30) conditions help in reversal signals.

3. Volume Analysis

Volume Strength (%) = (Current Volume / Avg. Volume) × 100

Strong Volume (>120% Avg.) confirms breakout/breakdown.

4. Body Percentage (Candle Strength)

Body % = (Close - Open) / (High - Low) × 100

Strong Bullish Candle: Body > 60%

Strong Bearish Candle: Body < 40%

📊 Visual Elements

1. Information Tables

Reference Data Table (9:45 AM Candle High/Low/Close)

RSI Values Table (5M, 15M, 1H, 4H, Daily)

Signal Legend (Buy/Sell/Reversal indicators)

2. Chart Overlays

Reference Lines (9:45 AM High & Low)

EMA Lines (9, 20, 50)

Signal Labels (B, S, R)

3. Color Coding

High Probability (Green)

Medium Probability (Orange)

Low Probability (Red)

⚠️ Important Usage Guidelines

✅ Best Practices:

Trade only within the 3-hour window (9:45 AM - 12:45 PM IST).

Wait for confirmation (closing above/below reference candle).

Use probability score to filter high-confidence trades.

❌ Avoid:

Trading outside the 15-minute timeframe.

Ignoring volume & RSI divergence.

Overtrading – Stick to 1-2 high-probability setups per day.

🎯 Conclusion

This NIFTY Trading Strategy is optimized for 15-minute charts with a 9:45 AM IST reference candle. It combines EMA trends, RSI momentum, volume analysis, and probability scoring to generate high-confidence signals.

🚀 Key Takeaways:

✔ Reference candle defines the day’s bias.

✔ Probability system filters best trades.

✔ Strict 15M timeframe ensures consistency.

Happy Trading! 📈💰

Vertical Time Marker Configurable (VTMC)# Vertical Time Marker Configurable (VTMC)

## Overview

The Vertical Time Marker Configurable (VTMC) is a powerful PineScript v6 indicator designed to help traders quickly identify key market times across their entire chart history. Instead of hovering over candles to check timestamps, VTMC draws clear vertical lines with customizable labels at your specified times, making it easy to spot important market sessions, news events, or personal trading windows at a glance.

## Key Features

### ⏰ Flexible Time Selection

- Set any time using an intuitive time picker (defaults to 8:30 AM Central Time)

- Automatically draws lines at your specified time across all historical data

- Perfect for marking market opens, closes, news releases, or personal trading times

### 🎨 Full Visual Customization

- **Line Color**: Choose any color (defaults to white for maximum visibility)

- **Line Style**: Solid, dashed, or dotted options

- **Line Width**: Adjustable from 1-10 pixels

- **Opacity Control**: Precise opacity slider (0-100%) for both line and text

### 🏷️ Smart Text Labels

- **Preset Options**: New York Open, New York Close, London Open, London Close, Asia Open, Asia Close

- **Custom Labels**: Enter any text for personalized marking (news events, trading windows, etc.)

- **Configurable Text**: Adjustable size (8-20px), color, and opacity

- **Smart Positioning**: Text appears just above the price action for clear visibility

### 📊 Professional Display

- Lines extend fully from top to bottom of chart

- Clean, non-intrusive design that doesn't clutter your analysis

- Works on any timeframe and market

- Historical lines persist across all chart data

## Perfect For

### Market Session Traders

- Mark key session opens and closes

- Identify overlap periods between major markets

- Track session-specific price behavior patterns

### News Traders

- Mark important economic releases (FOMC, NFP, etc.)

- Create visual reminders for scheduled events

- Track market reaction patterns around news times

### Institutional Flow Traders

- Identify key institutional activity times

- Mark order block formation periods

- Track smart money movement windows

### Personal Trading Systems

- Mark your optimal trading hours

- Create visual discipline for trading windows

- Track performance during specific time periods

## Why VTMC?

Unlike hardcoded session indicators that only work for specific markets, VTMC gives you complete flexibility to mark ANY time that matters to your trading strategy. Whether you're tracking "MY Trading Window" from 9:30-10:30 AM or marking custom news events, VTMC adapts to your specific needs.

The indicator eliminates the constant need to hover over candles to check times, instead providing instant visual reference points across your entire chart. This makes pattern recognition, backtesting, and trade timing significantly more efficient.

## Usage Tips

- Use multiple instances for different time zones or events

- Combine with other indicators for comprehensive market timing

- Customize colors to match your chart theme

- Use custom labels for personalized trading reminders

*Built with precision in PineScript v6 for reliable performance and modern TradingView compatibility.*

Institutional Momentum Scanner [IMS]Institutional Momentum Scanner - Professional Momentum Detection System

Hunt explosive price movements like the professionals. IMS identifies maximum momentum displacement within 10-bar windows, revealing where institutional money commits to directional moves.

KEY FEATURES:

▪ Scans for strongest momentum in rolling 10-bar windows (institutional accumulation period)

▪ Adaptive filtering reduces false signals using efficiency ratio technology

▪ Three clear states: LONG (green), SHORT (red), WAIT (gray)

▪ Dynamic volatility-adjusted thresholds (8% ATR-scaled)

▪ Visual momentum flow with glow effects for signal strength

BASED ON:

- Pocket Pivot concept (O'Neil/Morales) applied to price momentum

- Adaptive Moving Average principles (Kaufman KAMA)

- Market Wizards momentum philosophy

- Institutional order flow patterns (5-day verification window)

HOW IT WORKS:

The scanner finds the maximum price displacement in each 10-bar window - where the market showed its hand. An adaptive filter (5-bar regression) separates real moves from noise. When momentum exceeds the volatility-adjusted threshold, states change.

IDEAL FOR:

- Momentum traders seeking explosive moves

- Swing traders (especially 4H timeframe)

- Position traders wanting institutional footprints

- Anyone tired of false breakout signals

Default parameters (10,5) optimized for 4H charts but adaptable to any timeframe. Remember: The market rewards patience and punishes heroes. Wait for clear signals.

"The market is honest. Are you?"

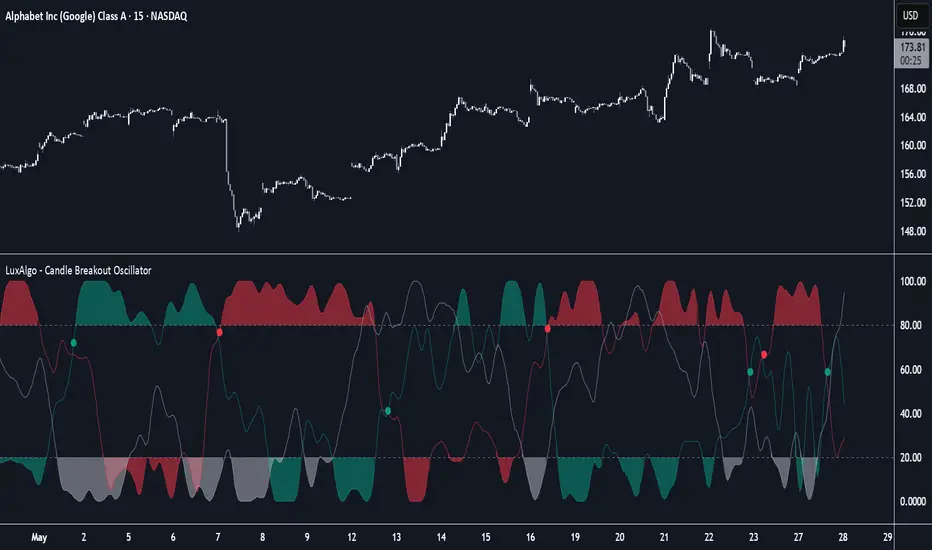

Candle Breakout Oscillator [LuxAlgo]The Candle Breakout Oscillator tool allows traders to identify the strength and weakness of the three main market states: bullish, bearish, and choppy.

Know who controls the market at any given moment with an oscillator display with values ranging from 0 to 100 for the three main plots and upper and lower thresholds of 80 and 20 by default.

🔶 USAGE

The Candle Breakout Oscillator represents the three main market states, with values ranging from 0 to 100. By default, the upper and lower thresholds are set at 80 and 20, and when a value exceeds these thresholds, a colored area is displayed for the trader's convenience.

This tool is based on pure price action breakouts. In this context, we understand a breakout as a close above the last candle's high or low, which is representative of market strength. All other close positions in relation to the last candle's limits are considered weakness.

So, when the bullish plot (in green) is at the top of the oscillator (values above 80), it means that the bullish breakouts (close below the last candle low) are at their maximum value over the calculation window, indicating an uptrend. The same interpretation can be made for the bearish plot (in red), indicating a downtrend when high.

On the other hand, weakness is indicated when values are below the lower threshold (20), indicating that breakouts are at their minimum over the last 100 candles. Below are some examples of the possible main interpretations:

There are three main things to look for in this oscillator:

Value reaches extreme

Value leaves extreme

Bullish/Bearish crossovers

As we can see on the chart, before the first crossover happens the bears come out of strength (top) and the bulls come out of weakness (bottom), then after the crossover the bulls reach strength (top) and the bears weakness (bottom), this process is repeated in reverse for the second crossover.

The other main feature of the oscillator is its ability to identify periods of sideways trends when the sideways values have upper readings above 80, and trending behavior when the sideways values have lower readings below 20. As we just saw in the case of bullish vs. bearish, sideways values signal a change in behavior when reaching or leaving the extremes of the oscillator.

🔶 DETAILS

🔹 Data Smoothing

The tool offers up to 10 different smoothing methods. In the chart above, we can see the raw data (smoothing: None) and the RMA, TEMA, or Hull moving averages.

🔹 Data Weighting

Users can add different weighting methods to the data. As we can see in the image above, users can choose between None, Volume, or Price (as in Price Delta for each breakout).

🔶 SETTINGS