Daily Session Windows background highlight indicatorIn intraday studies of stock indexes and Forex I have this weird habit of highlighting premarket, core session, lunch break and extended session with different backgrounds. If done by hand, this is tedious work that has to be repeated daily.

I think this feature should be built-in in TradingView. But it isn't.

For a few months now, I have been using this tiny indicator that does precisely that job. It saved me literally hours of focus time and mistakes. I have decided to revamp it and release it. I'm sure it can be useful to others.

Features:

Background color highlighting for premarket , core session , lunch hour and extended session of the trading day.

Session timing preset to match US session, but can be customized.

Can be enabled or disabled on a day of the week basis, including week-end.

Timezone is selectable, matches the chart's instrument but can be set independently to track a different timezone.

Not affected by the timezone you decided to assign to the chat's time scale.

Ready for stock indexes, but can be used to highlight Forex sessions too.

Komut dosyalarını "wind+芯片行业+市盈率+财经数据" için ara

Week Window AlgorithmWeek Window Algorithm

The Week Window Algorithm is an advanced intraday trading overlay built for precision session tracking and key level visualization.

🔹 Features:

1. Time Lines

Automatically plots vertical lines 30 minutes ahead of specific London times (07, 08, 09, 13, 14, 15UK), with adjustable height in pips and custom color.

2. Session Boxes

Draws price range boxes for:

Asia (22:00–06:00 UK)

Europe AM (08:00–09:00 UK)

Europe PM (14:00–15:00 UK)

Each box auto-updates during the session and fades after 3 days. Fill color is fully customizable via settings.

3. Yesterday’s High/Low Levels

Captures and plots yesterday’s high and low at 23:00 UK. Lines extend through today and highlight first-time hits.

🛠️ Customization:

Enable/disable sessions individually

Set pip size for early lines

Choose colors for each session box and line style

🕒 Recommended Timeframes:

Optimized for 1–15 minute charts. Works best on intraday setups.

Highlight Trading Window (Simple Hours / Time of Day Filter)As the name says this is a straightforward way to highlight the times of day that you are interested in studying.

Like to trade just a market open, or highlight a full session?

Could also be used negatively to "block out" a window of time each day.

Usage:

Just set your preferred time zone and then your time window (start and end).

Hope you find it useful! 😁

Ehlers Hann Moving Average [CC]The Hann Moving Average is an original script but a slightly modified version of the Hann Window Filter created by John Ehlers. I am using the same length but changed the default data source to use the new Weighted Close that tv added after I requested it awhile ago so thank you tv! The big strength of this moving average/filter is that it creates an extremely smooth filter with the added benefit of very little lag to smooth ratio. The weakness of this moving average/filter is that it does have a decent amount of lag which means it isn't as useful during choppy periods but does work well for sustained uptrends or downtrends. Feel free to experiment and let me know what settings work better for you. I have included strong buy and sell signals in addition to normal ones so strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators or scripts you would like to see me publish!

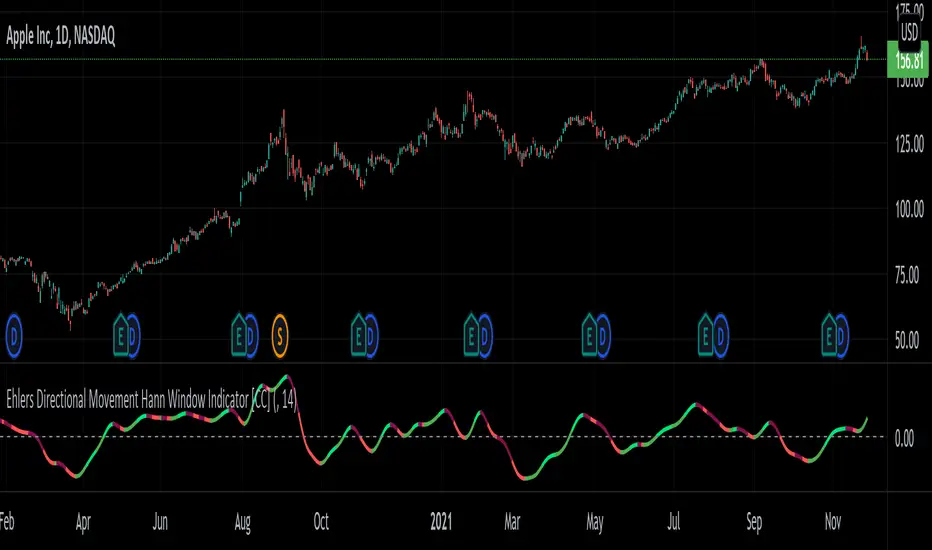

Ehlers Directional Movement Hann Window Indicator [CC]The Directional Movement Hann Window Indicator was created by John Ehlers (Stocks and Commodities Dec 2021 pgs 17-18) and this is his updated version of the classic Directional Movement indicator created by J. Welles Wilder. Ehlers uses the Hann Window Filtering after using an exponential moving average to smooth the classic directional movement indicator. This helps significantly with the lag and lack of smoothing which are both issues with the classic indicator. I have included strong buy and sell signals in addition to the normal ones so strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators you would like to see me publish!

Dollar Cost Average (Data Window Edition)Hi everyone

Hope you had a nice weekend and you're all excited for the week to come. At least I am (thanks to a few coffee but that still counts !!!)

This indicator is inspired from Dollar-Cost-Average-Cost-Basis

EDUCATIONAL POST

The educational post is coming a bit later this afternoon explaining how to use the indicator so I would advise to follow me so that you'll get updated in real-time :) (shameless self-advertising)

1 - What is Dollar-Cost Averaging (DCA)?

Dollar-Cost Averaging is a strategy that allows an investor to buy the same dollar amount of an investment on regular intervals. The purchases occur regardless of the asset's price.

I hope you're hungry because that one is a biggie and gave me a few headaches. Happy that it's getting out of my way finally and I can offer it

This indicator will analyse for the defined date range, how a dollar cost average (DCA) method would have performed vs investing all the hard earnt money at the beginning

2- What's on the menu today ?

Please check this screenshot to understand what you're supposed to see : CLICK ME I'M A SCREENSHOT (I'll repeat this URL one more time below as I noticed some don't read the information on my description and then will come pinging me saying "sir me no understand your indicator, itz buggy sir"

(yes I finally thought about a way to share screenshots on TradingView, took me 4 weeks, I'm slow to understand things apparently)

My indicator works with all asset classes and with the daily/weekly/monthly timeframes

As always, let's review quickly the different fields so that you'll understand how to use it (and I won't get spammed with questions in DM ^^)

- Use current resolution : if checked will use the resolution of the chart

- Timeframe used for DCA : different timeframe to be used if Use current resolution is unchecked

- Amount invested in your local currency : The amount in Fiat money that will be invested at each period selected above

- Starting Date

- Ending Date

- Select a candle level for the desired timeframe : If you want to use the open or close of the selected period above. Might make a diffence when the timeframe is weekly or monthly

3 - Specifications used

I got the idea from this website dcabtc.com and the result shown by this website and my indicator are very interesting in general and for your own trading

The formula used for the DCA calculation is that one : Investopedia Dollar Cost Average

4 - How to interpret the results

"But sir which results ??"...... those ones : CLICK ME I'M A SCREENSHOT :) (strike #2 with the screenshot)

It will draw all the plots and will give you some nice data to analyze in the Data Window section of TradingView

I'm not completely satisfied with the tool yet but the results are very closed to the dcabtc website mentioned above

If you're trading a very bullish asset class (who said crypto ?), it's very interesting to see what a DCA strategy could bring in term of performance. But DCA is not magic, there is a time component which is the day/week/month you'll start to invest (those who invested in crypto beginning of 2018 in altcoins know what I'm talking about and ..............will hate me for this joke)

5 - What's next ?

As said, the educational post is coming next but not only.

Will probably post a strategy tomorrow using this indicator so that you can compare what's performing best between your trading and a dollar cost average method

I'll publish as a protected source this time a more advanced version of that one including DCA forecasts

6 - Suggested alternative (but I'll you doing it)

If you don't want to have this panel in the bottom with the plots and analyze the results in the data window, you can always create an infopanel like shown here Risk-Reward-InfoPanel/ and display all the data there

Hope you'll like it, like me, love it, love me, tip me :)

____________________________________________________________

Feel free to hit the thumbs up as it shows me that I'm not doing this for nothing and will motivate to deliver more quality content in the future. (Meaning... a few likes only = no indicators = Dave enjoying the beach)

- I'm an offically approved PineEditor/LUA/MT4 approved mentor on codementor. You can request a coaching with me if you want and I'll teach you how to build kick-ass indicators and strategies

Jump on a 1 to 1 coaching with me

- You can also hire for a custom dev of your indicator/strategy/bot/chrome extension/python

Candle Height - Data Window Onlya simple script showing the height of a candle in the data window when howering about it.

Kijun Sen Separate WindowThis indicator works the same as a regular Kijun Sen but it is on a separate window to allow for other on chart indicators.

I tend to use this as a filter for when to go long/short.

When it is green, I only take longs. When it is red, I only take shorts. Combine with other indicators of your choice.

How To Auto Set Date RangeExample how to automatically set the date range window to be backtested from X days or weeks ago to present. Additional options are also included to manually set the date range or to show entire range available.

Normally when you change chart period it changes the number of days being backtested, which means as you increase the chart period (for example from 5min to 15min), you also increase the number of days traded. So you can not compare apples to apples for which period would yield best performance for your strategy.

By incorporating this code with your own strategy's logic (replacing buy and sell), it will allow you to compare results of different period backtests over the same duration of time.

Date Range: ALL uses entire history.

Date Range: DAYS uses number you set in # Days or Weeks

Date Range: WEEKS uses number you set in # Days or Weeks

Date Range: MANUAL uses manual dates you set in From and To fields

Much gratitude to @pinechrix for suggesting this improvement to me, and to @Gesundheit for pointing me in the right direction on the original example I published previously. Thank you both!

NOTICE: This is an example script and not meant to be used as an actual strategy. By using this script or any portion thereof, you acknowledge that you have read and understood that this is for research purposes only and I am not responsible for any financial losses you may incur by using this script!

How To Set Backtest Date RangeExample how to select and set date range window to be backtested. Normally when you change chart period it changes the number of days being backtested which means as you increas the chart period (for example from 5min to 15min) you also increase the number of days traded, so you can not compare apples to apples for which period would yield best returns for your strategy. Now you can. Incorporate this code replacing buy and sell with your strategy, then simply input the From and To dates in Format -> Inputs, and then change the chart period to view updated results.

NOTE: There is a limit in backtesting to 2000 orders, so please be aware of this when setting your date ranges. If you set your range too high, you may be exceeding this limit on some periods and not on others, so this would yield incorrect comparison of returns per period. If you see in your backtesting results that you are nearing this limit for one of your periods you are testing, then reduce the date range to a smaller number of days.

Enjoy!

(Thanks to @Gesundheit "Adeel" for pointing me in the right direction on this!)

Shadow TradingThis is a very simple script that identify daily candles with big tails and enter the market if the lower or the higher price of the same candle is violated... this is the idea behind I hope you will find it usefull ;)

Swing Hull/rsi/EMA StrategyA Swing trading strategy that use a combination of indicators, Hull average to get the trend direction, ema and rsi do the rest, use it are your own risk expecially at the end of any hull trend

Past Performance Does Not Guarantee Future Results

DTC Intra+DTC Intra+

Complete Indian Intraday Trading Indicator

What This Indicator Does:

DTC Intra+ is a comprehensive intraday trading indicator designed specifically for Indian markets. It provides real-time session analysis, volume profiling, and technical insights that work consistently across all timeframes.

Key Features:

Multi-Timeframe Data Consistency

Solves the common problem where indicators show different values on different timeframes

Gap percentage, ADR (Average Daily Range), and Burst values remain consistent whether viewing 1-minute or daily charts

Uses proprietary algorithms to fetch daily data and apply it accurately to intraday calculations

Intelligent Session Detection

Automatically detects and displays three Indian market sessions: Morning (9:15-11:00 AM), Mid-Day (11:00-1:30 PM), Afternoon (1:30-3:30 PM)

Creates visual session boxes that extend dynamically and finalize at session boundaries

Each session maintains distinct colors and labels for easy identification

Advanced Volume Analysis

Calculates Relative Volume (RVol) using 21-period moving average for volume strength assessment

Colors candles based on volume strength: high/moderate bullish and bearish volume patterns

Customizable volume thresholds (150% and 200% of average volume) for precise signal generation

Pattern Recognition System

Identifies mini-coil consolidation patterns with customizable styling options

Maintains visual persistence across timeframes and chart updates

Configurable lookback periods and pattern validation algorithms

Technical Analysis Tools

Four customizable Moving Averages (10, 20, 50, 200) with multiple calculation types (SMA, EMA, WMA, HMA)

VWAP integration with theme-adaptive styling

Gap analysis with customizable thresholds (1% and 2%+) and visual alerts

Theme-Adaptive Interface

Automatically detects and adapts to dark or light chart themes

Professional color schemes optimized for both theme types

Customizable transparency and styling for all visual elements

Information Dashboard

Dynamic information table displaying Gap %, RVol, ADR, Burst, Sector, Industry, Theme, and Session data

Real-time sector and industry classification from TradingView data

Burst Ranker with descriptive labels (GREAT, GOOD, LOW) based on historical performance analysis

How It Works:

Session Management:

The indicator uses time-based detection algorithms to identify Indian market sessions, creating visual boxes that extend dynamically and finalize at session boundaries. Each session maintains its own color scheme and label system.

Data Consistency Engine:

Proprietary cross-timeframe calculation system ensures that daily metrics display consistently across all timeframes by fetching daily data and applying it to intraday calculations.

Volume Profiling:

Custom volume analysis algorithms calculate relative volume strength and apply color coding to candles based on volume thresholds and price direction, providing immediate visual feedback on market activity.

Pattern Detection:

Advanced consolidation pattern recognition system that identifies mini-coil formations using customizable parameters and maintains visual persistence across chart updates.

How To Use:

Apply to any Indian stock chart (BSE, NSDL) on intraday timeframes

Session times are pre-configured for Indian markets but can be customized

Moving Averages can be adjusted to your preferred lengths and calculation types

Volume thresholds can be modified based on your trading strategy

Monitor the information panel for real-time market insights

Use session boxes to identify optimal trading windows

Who This Is For:

Indian intraday traders seeking comprehensive market analysis

Traders who need consistent data across multiple timeframes

Volume-based traders requiring real-time volume strength analysis

Technical analysts needing session-based market structure insights

Busy professionals who want market insights without constant chart monitoring

What Makes It Unique:

Unlike basic session indicators, DTC Intra+ provides cross-timeframe data consistency, advanced volume profiling, and comprehensive Indian market analysis in a single, theme-adaptive interface. The proprietary algorithms ensure accurate daily metrics on intraday charts, making it essential for serious Indian market traders who need reliable, consistent data across all timeframes.

The Bottom Line:

This indicator transforms how you view Indian intraday markets by providing consistent, reliable data across all timeframes while offering advanced session analysis, volume profiling, and pattern recognition. It's designed specifically for Indian market characteristics and trading patterns, giving you the tools to trade with confidence and precision.

EdgeFlow Pullback [CHE]EdgeFlow Pullback \ — Icon & Visual Guide (Deep Dive)

TL;DR (1-minute read)

⏳ Hourglass = Pending verdict. A countdown runs from the signal bar until your Evaluation Window ends.

✔ Checkmark (green) = OK. After the evaluation window, price (HLC3) is on the correct side of the EMA144 for that signal’s direction.

✖ Cross (red) = Fail. After the evaluation window, price (HLC3) is on the wrong side of the EMA144.

▲ / ▼ Triangles = the actual PB Long/Short signal bar (sequence completed in time).

Small lime/red crosses = visual markers when HLC3 crosses EMA144 (context, not trade signals).

Orange line = EMA144 (baseline/trend filter).

T3 line color = Context signal: green when T3 is below HLC3, red when T3 is above HLC3.

Icon Glossary (What each symbol means)

1) ⏳ Hourglass — “Pending / Countdown”

Appears immediately when a PB signal fires (Long or Short).

Shows `⏳ currentBars / EvaluationBars` (e.g., `⏳ 7/30`).

The label stays anchored at the signal bar and its original price level (it does not drift with price).

During ⏳ you get no verdict yet. It’s simply the waiting period before grading.

2) ✔ Checkmark (green) — “Condition met”

Appears after the Evaluation Window completes.

Logic:

Long signal: HLC3 (typical price) is above EMA144 → ✔

Short signal: HLC3 is below EMA144 → ✔

The label turns green and text says “✔ … Condition met”.

This is rules-based grading, not PnL. It tells you if the post-signal structure behaved as expected.

3) ✖ Cross (red) — “Condition failed”

Appears after the Evaluation Window completes if the condition above is not met.

Label turns red with “✖ … Condition failed”.

Again: rules-based verdict, not a guarantee of profit or loss.

4) ▲ “PB Long” triangle (below bar)

Marks the exact bar where the 4-step Long sequence completed within the allowed window.

That bar is your signal bar for Long setups.

5) ▼ “PB Short” triangle (above bar, red)

Same as above, for Short setups.

6) Lime/Red “+” crosses (tiny cross markers)

Lime cross (below bar): HLC3 crosses above EMA144 (crossover).

Red cross (above bar): HLC3 crosses below EMA144 (crossunder).

These crosses are context markers; they’re not entry signals by themselves.

The Two Clocks (Don’t mix them up)

There are two different time windows at play:

1. Signal Window — “Max bars for full sequence”

A pullback signal (Long or Short) only fires if the 4-step sequence completes within this many bars.

If it takes too long: reset (no signal, no triangle, no label).

Purpose: avoid stale setups.

2. Evaluation Window — “Evaluation window after signal (bars)”

Starts after the signal bar. The label shows an ⏳ countdown.

When it reaches the set number of bars, the indicator checks whether HLC3 is on the correct side of EMA144 for the signal direction.

Then it stamps the signal with ✔ (OK) or ✖ (Fail).

Timeline sketch (Long example):

```

→ ▲ PB Long at bar t0

Label shows: ⏳ 0/EvalBars

t0+1, t0+2, ... t0+EvalBars-1 → still ⏳

At t0+EvalBars → Check HLC3 vs EMA144

Result → ✔ (green) or ✖ (red)

(Label remains anchored at t0 / signal price)

```

What Triggers the PB Signal (so you know why triangles appear)

LONG sequence (4 steps in order):

1. T3 falling (the pullback begins)

2. HLC3 crosses under EMA144

3. T3 rising (pullback ends)

4. HLC3 crosses over EMA144 → PB Long triangle

SHORT sequence (mirror):

1. T3 rising

2. HLC3 crosses over EMA144

3. T3 falling

4. HLC3 crosses under EMA144 → PB Short triangle

If steps 1→4 don’t complete in time (within Max bars for full sequence), the sequence is abandoned (no signal).

Lines & Colors (quick interpretation)

EMA144 (orange): your baseline trend filter.

T3 (green/red):

Green when T3 < HLC3 (price above the smoothed path; often supportive in up-moves)

Red when T3 > HLC3 (price below the smoothed path; often pressure in down-moves)

HLC3 (gray): the typical price the logic uses ( (H+L+C)/3 ).

Label Behavior (anchoring & cleanup)

Each signal creates one label at the signal bar with ⏳.

The label is position-locked: it stays at the same bar index and y-price it was born at.

After the evaluation check, the label text and color update to ✔/✖, but position stays fixed.

The indicator keeps only the last N labels (your “Show only the last N labels” input). Older ones are deleted to reduce clutter.

What You Can (and Can’t) Infer from ✔ / ✖

✔ OK: Structure behaved as intended during the evaluation window (HLC3 finished on the correct side of EMA144).

Inference: The pullback continued in the expected direction post-signal.

✖ Fail: Structure ended up opposite the expectation.

Inference: The pullback did not continue cleanly (chop, reversal, or insufficient follow-through).

> Important: ✔/✖ is not profit or loss. It’s an objective rule check. Use it to identify market regimes where your entries perform best.

Input Settings — How they change the visuals

T3 length:

Shorter → faster turns, more signals (and more noise).

Longer → smoother turns, fewer but cleaner sequences.

T3 volume factor (0–1, default 0.7):

Higher → more curvature/smoothing.

Typical sweet spot: 0.5–0.9.

EMA length (baseline) default 144:

Smaller → faster baseline, more cross events, more aggressive signals.

Larger → slower, stricter trend confirmation.

Max bars for full sequence (signal window):

Smaller → only fresh, snappy pullbacks can signal.

Larger → allows slower pullbacks to complete.

Evaluation window (after signal):

Smaller → verdict arrives quickly (less tolerance).

Larger → gives the trade more time to prove itself structurally.

Show only the last N labels:

Controls chart clutter. Increase for more history, decrease for focus.

(FYI: The “Debug” toggle exists but doesn’t draw extra overlays in this version.)

Practical Reading Flow (how to use visuals in seconds)

1. Triangles catch your eye: ▲ for Long, ▼ for Short. That’s the setup completion.

2. ⏳ label starts—don’t judge yet; let the evaluation run.

3. Watch EMA slope and T3 color for context (trend + pressure).

4. After the window: ✔/✖ stamps the outcome. Log what the market was like when you got ✔.

Common “Why did…?” Questions

Q: Why did I get no triangle even though T3 turned and EMA crossed?

A: The 4 steps must happen in order and within the Signal Window. If timing breaks, the sequence resets.

Q: Why did my label stay ⏳ for so long?

A: That’s by design until the Evaluation Window completes. The verdict only happens at the end of that window.

Q: Why is ✔/✖ different from my PnL?

A: It’s a structure check, not a profit check. It doesn’t know your entries/exits/stops.

Q: Do the small lime/red crosses mean buy/sell?

A: No. They’re context markers for HLC3↔EMA crosses, useful inside the sequence but not standalone signals.

Pro Tips (turn visuals into decisions)

Entry: Use the ▲/▼ triangle as your trigger, in trend direction (check EMA slope/market structure).

Stop: Behind the pullback swing around the signal bar.

Exit: Structure levels, R-multiples, or a reverse HLC3↔EMA cross as a trailing logic.

Tuning:

Intraday/volatile: shorter T3/EMA + tighter Signal Window.

Swing/slow: default 144 EMA + moderate windows.

Learn quickly: Filter your chart to show only ✔ or only ✖ windows in your notes; see which sessions, assets, and volatility regimes suit the system.

Disclaimer

No indicator guarantees profits. Sweep2Trade Pro \ is a decision aid; always combine with solid risk management and your own judgment. Backtest, forward test, and size responsibly.

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence 🚀

Happy trading

Chervolino

J12Matic Builder by galgoomA flexible Renko/tick strategy that lets you choose between two entry engines (Multi-Source 3-way or QBand+Moneyball), with a unified trailing/TP exit engine, NY-time trading windows with auto-flatten, daily profit/loss and trade-count limits (HALT mode), and clean webhook routing using {{strategy.order.alert_message}}.

Highlights

Two entry engines

Multi-Source (3): up to three long/short sources with Single / Dual / Triple logic and optional lookback.

QBand + Moneyball: Gate → Trigger workflow with timing windows, OR/AND trigger modes, per-window caps, optional same-bar fire.

Unified exit engine: Trailing by Bricks or Ticks, plus optional static TP/SL.

Session control (NY time): Evening / Overnight / NY Session windows; auto-flatten at end of any enabled window.

Day controls: Profit/Loss (USD) and Trade-count limits. When hit, strategy HALTS new entries, shows an on-chart label/background.

Alert routing designed for webhooks: Every order sets alert_message= so you can run alerts with:

Condition: this strategy

Notify on: Order fills only

Message: {{strategy.order.alert_message}}

Default JSONs or Custom payloads: If a Custom field is blank, a sensible default JSON is sent. Fill a field to override.

How to set up alerts (the 15-second version)

Create a TradingView alert with this strategy as Condition.

Notify on: Order fills only.

Message: {{strategy.order.alert_message}} (exactly).

If you want your own payloads, paste them into Inputs → 08) Custom Alert Payloads.

Leave blank → the strategy sends a default JSON.

Fill in → your text is sent as-is.

Note: Anything you type into the alert dialog’s Message box is ignored except the {{strategy.order.alert_message}} token, which forwards the payload supplied by the strategy at order time.

Publishing notes / best practices

Renko users: Make sure “Renko Brick Size” in Inputs matches your chart’s brick size exactly.

Ticks vs Bricks: Exit distances switch instantly when you toggle Exit Units.

Same-bar flips: If enabled, a new opposite signal will first close the open trade (with its exit payload), then enter the new side.

HALT mode: When day profit/loss limit or trade-count limit triggers, new entries are blocked for the rest of the session day. You’ll see a label and a soft background tint.

Session end flatten: Auto-closes positions at window ends; these exits use the “End of Session Window Exit” payload.

Bar magnifier: Strategy is configured for on-close execution; you can enable Bar Magnifier in Properties if needed.

Default JSONs (used when a Custom field is empty)

Open: {"event":"open","side":"long|short","symbol":""}

Close: {"event":"close","side":"long|short|flat","reason":"tp|sl|flip|session|limit_profit|limit_loss","symbol":""}

You can paste any text/JSON into the Custom fields; it will be forwarded as-is when that event occurs.

Input sections — user guide

01) Entries & Signals

Entry Logic: Choose Multi-Source (3) or QBand + Moneyball (pick one).

Enable Long/Short Signals: Master on/off switches for entering long/short.

Flip on opposite signal: If enabled, a new opposite signal will close the current position first, then open the other side.

Signal Logic (Multi-Source):

Single: any 1 of the 3 sources > 0

Dual: Source1 AND Source2 > 0

Triple (default): 1 AND 2 AND 3 > 0

Long/Short Signal Sources 1–3: Provide up to three series (often indicators). A positive value (> 0) is treated as a “pulse”.

Use Lookback: Keeps a source “true” for N bars after it pulses (helps catch late triggers).

Long/Short Lookback (bars): How many bars to remember that pulse.

01b) QBands + Moneyball (Gate -> Trigger)

Allow same-bar Gate->Trigger: If ON, a trigger can fire on the same bar as the gate pulse.

Trigger must fire within N bars after Gate: Size of the gate window (in bars).

Max signals per window (0 = unlimited): Cap the number of entries allowed while a gate window is open.

Buy/Sell Source 1 – Gate: Gate pulse sources that open the buy/sell window (often a regime/zone, e.g., QBands bull/bear).

Trigger Pulse Mode (Buy/Sell): How to detect a trigger pulse from the trigger sources (Change / Appear / Rise>0 / Fall<0).

Trigger A/B sources + Extend Bars: Primary/secondary triggers plus optional extension to persist their pulse for N bars.

Trigger Mode: Pick S2 only, S3 only, S2 OR S3, or S2 AND S3. AND mode remembers both pulses inside the window before firing.

02) Exit Units (Trailing/TP)

Exit Units: Choose Bricks (Renko) or Ticks. All distances below switch accordingly.

03) Tick-based Trailing / Stops (active when Exit Units = Ticks)

Initial SL (ticks): Starting stop distance from entry.

Start Trailing After (ticks): Start trailing once price moves this far in your favor.

Trailing Distance (ticks): Offset of the trailing stop from peak/trough once trailing begins.

Take Profit (ticks): Optional static TP distance.

Stop Loss (ticks): Optional static SL distance (overrides trailing if enabled).

04) Brick-based Trailing / Stops (active when Exit Units = Bricks)

Renko Brick Size: Must match your chart’s brick size.

Initial SL / Start Trailing After / Trailing Distance (bricks): Same definitions as tick mode, measured in bricks.

Take Profit / Stop Loss (bricks): Optional static distances.

05) TP / SL Switch

Enable Static Take Profit: If ON, closes the trade at the fixed TP distance.

Enable Static Stop Loss (Overrides Trailing): If ON, trailing is disabled and a fixed SL is used.

06) Trading Windows (NY time)

Use Trading Windows: Master toggle for all windows.

Evening / Overnight / NY Session: Define each session in NY time.

Flatten at End of : Auto-close any open position when a window ends (sends the Session Exit payload).

07) Day Controls & Limits

Enable Profit Limits / Profit Limit (Dollars): When daily net PnL ≥ limit → auto-flatten and HALT.

Enable Loss Limits / Loss Limit (Dollars): When daily net PnL ≤ −limit → auto-flatten and HALT.

Enable Trade Count Limits / Number of Trades Allowed: After N entries, HALT new entries (does not auto-flatten).

On-chart HUD: A label and soft background tint appear when HALTED; a compact status table shows Day PnL, trade count, and mode.

08) Custom Alert Payloads (used as strategy.order.alert_message)

Long/Short Entry: Payload sent on entries (if blank, a default open JSON is sent).

Regular Long/Short Exit: Payload sent on closes from SL/TP/flip (if blank, a default close JSON is sent).

End of Session Window Exit: Payload sent when any enabled window ends and positions are flattened.

Profit/Loss/Trade Limit Close: Payload sent when daily profit/loss limit causes auto-flatten.

Tip: Any tokens you include here are forwarded “as is”. If your downstream expects variables, do the substitution on the receiver side.

Known limitations

No bracket orders from Pine: This strategy doesn’t create OCO/attached brackets on the broker; it simulates exits with strategy logic and forwards your payloads for external automation.

alert_message is per order only: Alerts fire on order events. General status pings aren’t sent unless you wire a separate indicator/alert.

Renko specifics: Backtests on synthetic Renko can differ from live execution. Always forward-test on your instrument and settings.

Quick checklist before you publish

✅ Brick size in Inputs matches your Renko chart

✅ Exit Units set to Bricks or Ticks as you intend

✅ Day limits/Windows toggled as you want

✅ Custom payloads filled (or leave blank to use defaults)

✅ Your alert uses Order fills only + {{strategy.order.alert_message}}

Goertzel Browser [Loxx]As the financial markets become increasingly complex and data-driven, traders and analysts must leverage powerful tools to gain insights and make informed decisions. One such tool is the Goertzel Browser indicator, a sophisticated technical analysis indicator that helps identify cyclical patterns in financial data. This powerful tool is capable of detecting cyclical patterns in financial data, helping traders to make better predictions and optimize their trading strategies. With its unique combination of mathematical algorithms and advanced charting capabilities, this indicator has the potential to revolutionize the way we approach financial modeling and trading.

█ Brief Overview of the Goertzel Browser

The Goertzel Browser is a sophisticated technical analysis tool that utilizes the Goertzel algorithm to analyze and visualize cyclical components within a financial time series. By identifying these cycles and their characteristics, the indicator aims to provide valuable insights into the market's underlying price movements, which could potentially be used for making informed trading decisions.

The primary purpose of this indicator is to:

1. Detect and analyze the dominant cycles present in the price data.

2. Reconstruct and visualize the composite wave based on the detected cycles.

3. Project the composite wave into the future, providing a potential roadmap for upcoming price movements.

To achieve this, the indicator performs several tasks:

1. Detrending the price data: The indicator preprocesses the price data using various detrending techniques, such as Hodrick-Prescott filters, zero-lag moving averages, and linear regression, to remove the underlying trend and focus on the cyclical components.

2. Applying the Goertzel algorithm: The indicator applies the Goertzel algorithm to the detrended price data, identifying the dominant cycles and their characteristics, such as amplitude, phase, and cycle strength.

3. Constructing the composite wave: The indicator reconstructs the composite wave by combining the detected cycles, either by using a user-defined list of cycles or by selecting the top N cycles based on their amplitude or cycle strength.

4. Visualizing the composite wave: The indicator plots the composite wave, using solid lines for the past and dotted lines for the future projections. The color of the lines indicates whether the wave is increasing or decreasing.

5. Displaying cycle information: The indicator provides a table that displays detailed information about the detected cycles, including their rank, period, Bartel's test results, amplitude, and phase.

This indicator is a powerful tool that employs the Goertzel algorithm to analyze and visualize the cyclical components within a financial time series. By providing insights into the underlying price movements and their potential future trajectory, the indicator aims to assist traders in making more informed decisions.

█ What is the Goertzel Algorithm?

The Goertzel algorithm, named after Gerald Goertzel, is a digital signal processing technique that is used to efficiently compute individual terms of the Discrete Fourier Transform (DFT). It was first introduced in 1958, and since then, it has found various applications in the fields of engineering, mathematics, and physics.

The Goertzel algorithm is primarily used to detect specific frequency components within a digital signal, making it particularly useful in applications where only a few frequency components are of interest. The algorithm is computationally efficient, as it requires fewer calculations than the Fast Fourier Transform (FFT) when detecting a small number of frequency components. This efficiency makes the Goertzel algorithm a popular choice in applications such as:

1. Telecommunications: The Goertzel algorithm is used for decoding Dual-Tone Multi-Frequency (DTMF) signals, which are the tones generated when pressing buttons on a telephone keypad. By identifying specific frequency components, the algorithm can accurately determine which button has been pressed.

2. Audio processing: The algorithm can be used to detect specific pitches or harmonics in an audio signal, making it useful in applications like pitch detection and tuning musical instruments.

3. Vibration analysis: In the field of mechanical engineering, the Goertzel algorithm can be applied to analyze vibrations in rotating machinery, helping to identify faulty components or signs of wear.

4. Power system analysis: The algorithm can be used to measure harmonic content in power systems, allowing engineers to assess power quality and detect potential issues.

The Goertzel algorithm is used in these applications because it offers several advantages over other methods, such as the FFT:

1. Computational efficiency: The Goertzel algorithm requires fewer calculations when detecting a small number of frequency components, making it more computationally efficient than the FFT in these cases.

2. Real-time analysis: The algorithm can be implemented in a streaming fashion, allowing for real-time analysis of signals, which is crucial in applications like telecommunications and audio processing.

3. Memory efficiency: The Goertzel algorithm requires less memory than the FFT, as it only computes the frequency components of interest.

4. Precision: The algorithm is less susceptible to numerical errors compared to the FFT, ensuring more accurate results in applications where precision is essential.

The Goertzel algorithm is an efficient digital signal processing technique that is primarily used to detect specific frequency components within a signal. Its computational efficiency, real-time capabilities, and precision make it an attractive choice for various applications, including telecommunications, audio processing, vibration analysis, and power system analysis. The algorithm has been widely adopted since its introduction in 1958 and continues to be an essential tool in the fields of engineering, mathematics, and physics.

█ Goertzel Algorithm in Quantitative Finance: In-Depth Analysis and Applications

The Goertzel algorithm, initially designed for signal processing in telecommunications, has gained significant traction in the financial industry due to its efficient frequency detection capabilities. In quantitative finance, the Goertzel algorithm has been utilized for uncovering hidden market cycles, developing data-driven trading strategies, and optimizing risk management. This section delves deeper into the applications of the Goertzel algorithm in finance, particularly within the context of quantitative trading and analysis.

Unveiling Hidden Market Cycles:

Market cycles are prevalent in financial markets and arise from various factors, such as economic conditions, investor psychology, and market participant behavior. The Goertzel algorithm's ability to detect and isolate specific frequencies in price data helps trader analysts identify hidden market cycles that may otherwise go unnoticed. By examining the amplitude, phase, and periodicity of each cycle, traders can better understand the underlying market structure and dynamics, enabling them to develop more informed and effective trading strategies.

Developing Quantitative Trading Strategies:

The Goertzel algorithm's versatility allows traders to incorporate its insights into a wide range of trading strategies. By identifying the dominant market cycles in a financial instrument's price data, traders can create data-driven strategies that capitalize on the cyclical nature of markets.

For instance, a trader may develop a mean-reversion strategy that takes advantage of the identified cycles. By establishing positions when the price deviates from the predicted cycle, the trader can profit from the subsequent reversion to the cycle's mean. Similarly, a momentum-based strategy could be designed to exploit the persistence of a dominant cycle by entering positions that align with the cycle's direction.

Enhancing Risk Management:

The Goertzel algorithm plays a vital role in risk management for quantitative strategies. By analyzing the cyclical components of a financial instrument's price data, traders can gain insights into the potential risks associated with their trading strategies.

By monitoring the amplitude and phase of dominant cycles, a trader can detect changes in market dynamics that may pose risks to their positions. For example, a sudden increase in amplitude may indicate heightened volatility, prompting the trader to adjust position sizing or employ hedging techniques to protect their portfolio. Additionally, changes in phase alignment could signal a potential shift in market sentiment, necessitating adjustments to the trading strategy.

Expanding Quantitative Toolkits:

Traders can augment the Goertzel algorithm's insights by combining it with other quantitative techniques, creating a more comprehensive and sophisticated analysis framework. For example, machine learning algorithms, such as neural networks or support vector machines, could be trained on features extracted from the Goertzel algorithm to predict future price movements more accurately.

Furthermore, the Goertzel algorithm can be integrated with other technical analysis tools, such as moving averages or oscillators, to enhance their effectiveness. By applying these tools to the identified cycles, traders can generate more robust and reliable trading signals.

The Goertzel algorithm offers invaluable benefits to quantitative finance practitioners by uncovering hidden market cycles, aiding in the development of data-driven trading strategies, and improving risk management. By leveraging the insights provided by the Goertzel algorithm and integrating it with other quantitative techniques, traders can gain a deeper understanding of market dynamics and devise more effective trading strategies.

█ Indicator Inputs

src: This is the source data for the analysis, typically the closing price of the financial instrument.

detrendornot: This input determines the method used for detrending the source data. Detrending is the process of removing the underlying trend from the data to focus on the cyclical components.

The available options are:

hpsmthdt: Detrend using Hodrick-Prescott filter centered moving average.

zlagsmthdt: Detrend using zero-lag moving average centered moving average.

logZlagRegression: Detrend using logarithmic zero-lag linear regression.

hpsmth: Detrend using Hodrick-Prescott filter.

zlagsmth: Detrend using zero-lag moving average.

DT_HPper1 and DT_HPper2: These inputs define the period range for the Hodrick-Prescott filter centered moving average when detrendornot is set to hpsmthdt.

DT_ZLper1 and DT_ZLper2: These inputs define the period range for the zero-lag moving average centered moving average when detrendornot is set to zlagsmthdt.

DT_RegZLsmoothPer: This input defines the period for the zero-lag moving average used in logarithmic zero-lag linear regression when detrendornot is set to logZlagRegression.

HPsmoothPer: This input defines the period for the Hodrick-Prescott filter when detrendornot is set to hpsmth.

ZLMAsmoothPer: This input defines the period for the zero-lag moving average when detrendornot is set to zlagsmth.

MaxPer: This input sets the maximum period for the Goertzel algorithm to search for cycles.

squaredAmp: This boolean input determines whether the amplitude should be squared in the Goertzel algorithm.

useAddition: This boolean input determines whether the Goertzel algorithm should use addition for combining the cycles.

useCosine: This boolean input determines whether the Goertzel algorithm should use cosine waves instead of sine waves.

UseCycleStrength: This boolean input determines whether the Goertzel algorithm should compute the cycle strength, which is a normalized measure of the cycle's amplitude.

WindowSizePast and WindowSizeFuture: These inputs define the window size for past and future projections of the composite wave.

FilterBartels: This boolean input determines whether Bartel's test should be applied to filter out non-significant cycles.

BartNoCycles: This input sets the number of cycles to be used in Bartel's test.

BartSmoothPer: This input sets the period for the moving average used in Bartel's test.

BartSigLimit: This input sets the significance limit for Bartel's test, below which cycles are considered insignificant.

SortBartels: This boolean input determines whether the cycles should be sorted by their Bartel's test results.

UseCycleList: This boolean input determines whether a user-defined list of cycles should be used for constructing the composite wave. If set to false, the top N cycles will be used.

Cycle1, Cycle2, Cycle3, Cycle4, and Cycle5: These inputs define the user-defined list of cycles when 'UseCycleList' is set to true. If using a user-defined list, each of these inputs represents the period of a specific cycle to include in the composite wave.

StartAtCycle: This input determines the starting index for selecting the top N cycles when UseCycleList is set to false. This allows you to skip a certain number of cycles from the top before selecting the desired number of cycles.

UseTopCycles: This input sets the number of top cycles to use for constructing the composite wave when UseCycleList is set to false. The cycles are ranked based on their amplitudes or cycle strengths, depending on the UseCycleStrength input.

SubtractNoise: This boolean input determines whether to subtract the noise (remaining cycles) from the composite wave. If set to true, the composite wave will only include the top N cycles specified by UseTopCycles.

█ Exploring Auxiliary Functions

The following functions demonstrate advanced techniques for analyzing financial markets, including zero-lag moving averages, Bartels probability, detrending, and Hodrick-Prescott filtering. This section examines each function in detail, explaining their purpose, methodology, and applications in finance. We will examine how each function contributes to the overall performance and effectiveness of the indicator and how they work together to create a powerful analytical tool.

Zero-Lag Moving Average:

The zero-lag moving average function is designed to minimize the lag typically associated with moving averages. This is achieved through a two-step weighted linear regression process that emphasizes more recent data points. The function calculates a linearly weighted moving average (LWMA) on the input data and then applies another LWMA on the result. By doing this, the function creates a moving average that closely follows the price action, reducing the lag and improving the responsiveness of the indicator.

The zero-lag moving average function is used in the indicator to provide a responsive, low-lag smoothing of the input data. This function helps reduce the noise and fluctuations in the data, making it easier to identify and analyze underlying trends and patterns. By minimizing the lag associated with traditional moving averages, this function allows the indicator to react more quickly to changes in market conditions, providing timely signals and improving the overall effectiveness of the indicator.

Bartels Probability:

The Bartels probability function calculates the probability of a given cycle being significant in a time series. It uses a mathematical test called the Bartels test to assess the significance of cycles detected in the data. The function calculates coefficients for each detected cycle and computes an average amplitude and an expected amplitude. By comparing these values, the Bartels probability is derived, indicating the likelihood of a cycle's significance. This information can help in identifying and analyzing dominant cycles in financial markets.

The Bartels probability function is incorporated into the indicator to assess the significance of detected cycles in the input data. By calculating the Bartels probability for each cycle, the indicator can prioritize the most significant cycles and focus on the market dynamics that are most relevant to the current trading environment. This function enhances the indicator's ability to identify dominant market cycles, improving its predictive power and aiding in the development of effective trading strategies.

Detrend Logarithmic Zero-Lag Regression:

The detrend logarithmic zero-lag regression function is used for detrending data while minimizing lag. It combines a zero-lag moving average with a linear regression detrending method. The function first calculates the zero-lag moving average of the logarithm of input data and then applies a linear regression to remove the trend. By detrending the data, the function isolates the cyclical components, making it easier to analyze and interpret the underlying market dynamics.

The detrend logarithmic zero-lag regression function is used in the indicator to isolate the cyclical components of the input data. By detrending the data, the function enables the indicator to focus on the cyclical movements in the market, making it easier to analyze and interpret market dynamics. This function is essential for identifying cyclical patterns and understanding the interactions between different market cycles, which can inform trading decisions and enhance overall market understanding.

Bartels Cycle Significance Test:

The Bartels cycle significance test is a function that combines the Bartels probability function and the detrend logarithmic zero-lag regression function to assess the significance of detected cycles. The function calculates the Bartels probability for each cycle and stores the results in an array. By analyzing the probability values, traders and analysts can identify the most significant cycles in the data, which can be used to develop trading strategies and improve market understanding.

The Bartels cycle significance test function is integrated into the indicator to provide a comprehensive analysis of the significance of detected cycles. By combining the Bartels probability function and the detrend logarithmic zero-lag regression function, this test evaluates the significance of each cycle and stores the results in an array. The indicator can then use this information to prioritize the most significant cycles and focus on the most relevant market dynamics. This function enhances the indicator's ability to identify and analyze dominant market cycles, providing valuable insights for trading and market analysis.

Hodrick-Prescott Filter:

The Hodrick-Prescott filter is a popular technique used to separate the trend and cyclical components of a time series. The function applies a smoothing parameter to the input data and calculates a smoothed series using a two-sided filter. This smoothed series represents the trend component, which can be subtracted from the original data to obtain the cyclical component. The Hodrick-Prescott filter is commonly used in economics and finance to analyze economic data and financial market trends.

The Hodrick-Prescott filter is incorporated into the indicator to separate the trend and cyclical components of the input data. By applying the filter to the data, the indicator can isolate the trend component, which can be used to analyze long-term market trends and inform trading decisions. Additionally, the cyclical component can be used to identify shorter-term market dynamics and provide insights into potential trading opportunities. The inclusion of the Hodrick-Prescott filter adds another layer of analysis to the indicator, making it more versatile and comprehensive.

Detrending Options: Detrend Centered Moving Average:

The detrend centered moving average function provides different detrending methods, including the Hodrick-Prescott filter and the zero-lag moving average, based on the selected detrending method. The function calculates two sets of smoothed values using the chosen method and subtracts one set from the other to obtain a detrended series. By offering multiple detrending options, this function allows traders and analysts to select the most appropriate method for their specific needs and preferences.

The detrend centered moving average function is integrated into the indicator to provide users with multiple detrending options, including the Hodrick-Prescott filter and the zero-lag moving average. By offering multiple detrending methods, the indicator allows users to customize the analysis to their specific needs and preferences, enhancing the indicator's overall utility and adaptability. This function ensures that the indicator can cater to a wide range of trading styles and objectives, making it a valuable tool for a diverse group of market participants.

The auxiliary functions functions discussed in this section demonstrate the power and versatility of mathematical techniques in analyzing financial markets. By understanding and implementing these functions, traders and analysts can gain valuable insights into market dynamics, improve their trading strategies, and make more informed decisions. The combination of zero-lag moving averages, Bartels probability, detrending methods, and the Hodrick-Prescott filter provides a comprehensive toolkit for analyzing and interpreting financial data. The integration of advanced functions in a financial indicator creates a powerful and versatile analytical tool that can provide valuable insights into financial markets. By combining the zero-lag moving average,

█ In-Depth Analysis of the Goertzel Browser Code

The Goertzel Browser code is an implementation of the Goertzel Algorithm, an efficient technique to perform spectral analysis on a signal. The code is designed to detect and analyze dominant cycles within a given financial market data set. This section will provide an extremely detailed explanation of the code, its structure, functions, and intended purpose.

Function signature and input parameters:

The Goertzel Browser function accepts numerous input parameters for customization, including source data (src), the current bar (forBar), sample size (samplesize), period (per), squared amplitude flag (squaredAmp), addition flag (useAddition), cosine flag (useCosine), cycle strength flag (UseCycleStrength), past and future window sizes (WindowSizePast, WindowSizeFuture), Bartels filter flag (FilterBartels), Bartels-related parameters (BartNoCycles, BartSmoothPer, BartSigLimit), sorting flag (SortBartels), and output buffers (goeWorkPast, goeWorkFuture, cyclebuffer, amplitudebuffer, phasebuffer, cycleBartelsBuffer).

Initializing variables and arrays:

The code initializes several float arrays (goeWork1, goeWork2, goeWork3, goeWork4) with the same length as twice the period (2 * per). These arrays store intermediate results during the execution of the algorithm.

Preprocessing input data:

The input data (src) undergoes preprocessing to remove linear trends. This step enhances the algorithm's ability to focus on cyclical components in the data. The linear trend is calculated by finding the slope between the first and last values of the input data within the sample.

Iterative calculation of Goertzel coefficients:

The core of the Goertzel Browser algorithm lies in the iterative calculation of Goertzel coefficients for each frequency bin. These coefficients represent the spectral content of the input data at different frequencies. The code iterates through the range of frequencies, calculating the Goertzel coefficients using a nested loop structure.

Cycle strength computation:

The code calculates the cycle strength based on the Goertzel coefficients. This is an optional step, controlled by the UseCycleStrength flag. The cycle strength provides information on the relative influence of each cycle on the data per bar, considering both amplitude and cycle length. The algorithm computes the cycle strength either by squaring the amplitude (controlled by squaredAmp flag) or using the actual amplitude values.

Phase calculation:

The Goertzel Browser code computes the phase of each cycle, which represents the position of the cycle within the input data. The phase is calculated using the arctangent function (math.atan) based on the ratio of the imaginary and real components of the Goertzel coefficients.

Peak detection and cycle extraction:

The algorithm performs peak detection on the computed amplitudes or cycle strengths to identify dominant cycles. It stores the detected cycles in the cyclebuffer array, along with their corresponding amplitudes and phases in the amplitudebuffer and phasebuffer arrays, respectively.

Sorting cycles by amplitude or cycle strength:

The code sorts the detected cycles based on their amplitude or cycle strength in descending order. This allows the algorithm to prioritize cycles with the most significant impact on the input data.

Bartels cycle significance test:

If the FilterBartels flag is set, the code performs a Bartels cycle significance test on the detected cycles. This test determines the statistical significance of each cycle and filters out the insignificant cycles. The significant cycles are stored in the cycleBartelsBuffer array. If the SortBartels flag is set, the code sorts the significant cycles based on their Bartels significance values.

Waveform calculation:

The Goertzel Browser code calculates the waveform of the significant cycles for both past and future time windows. The past and future windows are defined by the WindowSizePast and WindowSizeFuture parameters, respectively. The algorithm uses either cosine or sine functions (controlled by the useCosine flag) to calculate the waveforms for each cycle. The useAddition flag determines whether the waveforms should be added or subtracted.

Storing waveforms in matrices:

The calculated waveforms for each cycle are stored in two matrices - goeWorkPast and goeWorkFuture. These matrices hold the waveforms for the past and future time windows, respectively. Each row in the matrices represents a time window position, and each column corresponds to a cycle.

Returning the number of cycles:

The Goertzel Browser function returns the total number of detected cycles (number_of_cycles) after processing the input data. This information can be used to further analyze the results or to visualize the detected cycles.

The Goertzel Browser code is a comprehensive implementation of the Goertzel Algorithm, specifically designed for detecting and analyzing dominant cycles within financial market data. The code offers a high level of customization, allowing users to fine-tune the algorithm based on their specific needs. The Goertzel Browser's combination of preprocessing, iterative calculations, cycle extraction, sorting, significance testing, and waveform calculation makes it a powerful tool for understanding cyclical components in financial data.

█ Generating and Visualizing Composite Waveform

The indicator calculates and visualizes the composite waveform for both past and future time windows based on the detected cycles. Here's a detailed explanation of this process:

Updating WindowSizePast and WindowSizeFuture:

The WindowSizePast and WindowSizeFuture are updated to ensure they are at least twice the MaxPer (maximum period).

Initializing matrices and arrays:

Two matrices, goeWorkPast and goeWorkFuture, are initialized to store the Goertzel results for past and future time windows. Multiple arrays are also initialized to store cycle, amplitude, phase, and Bartels information.

Preparing the source data (srcVal) array:

The source data is copied into an array, srcVal, and detrended using one of the selected methods (hpsmthdt, zlagsmthdt, logZlagRegression, hpsmth, or zlagsmth).

Goertzel function call:

The Goertzel function is called to analyze the detrended source data and extract cycle information. The output, number_of_cycles, contains the number of detected cycles.

Initializing arrays for past and future waveforms:

Three arrays, epgoertzel, goertzel, and goertzelFuture, are initialized to store the endpoint Goertzel, non-endpoint Goertzel, and future Goertzel projections, respectively.

Calculating composite waveform for past bars (goertzel array):

The past composite waveform is calculated by summing the selected cycles (either from the user-defined cycle list or the top cycles) and optionally subtracting the noise component.

Calculating composite waveform for future bars (goertzelFuture array):

The future composite waveform is calculated in a similar way as the past composite waveform.

Drawing past composite waveform (pvlines):

The past composite waveform is drawn on the chart using solid lines. The color of the lines is determined by the direction of the waveform (green for upward, red for downward).

Drawing future composite waveform (fvlines):

The future composite waveform is drawn on the chart using dotted lines. The color of the lines is determined by the direction of the waveform (fuchsia for upward, yellow for downward).

Displaying cycle information in a table (table3):

A table is created to display the cycle information, including the rank, period, Bartel value, amplitude (or cycle strength), and phase of each detected cycle.

Filling the table with cycle information:

The indicator iterates through the detected cycles and retrieves the relevant information (period, amplitude, phase, and Bartel value) from the corresponding arrays. It then fills the table with this information, displaying the values up to six decimal places.

To summarize, this indicator generates a composite waveform based on the detected cycles in the financial data. It calculates the composite waveforms for both past and future time windows and visualizes them on the chart using colored lines. Additionally, it displays detailed cycle information in a table, including the rank, period, Bartel value, amplitude (or cycle strength), and phase of each detected cycle.

█ Enhancing the Goertzel Algorithm-Based Script for Financial Modeling and Trading

The Goertzel algorithm-based script for detecting dominant cycles in financial data is a powerful tool for financial modeling and trading. It provides valuable insights into the past behavior of these cycles and potential future impact. However, as with any algorithm, there is always room for improvement. This section discusses potential enhancements to the existing script to make it even more robust and versatile for financial modeling, general trading, advanced trading, and high-frequency finance trading.

Enhancements for Financial Modeling

Data preprocessing: One way to improve the script's performance for financial modeling is to introduce more advanced data preprocessing techniques. This could include removing outliers, handling missing data, and normalizing the data to ensure consistent and accurate results.

Additional detrending and smoothing methods: Incorporating more sophisticated detrending and smoothing techniques, such as wavelet transform or empirical mode decomposition, can help improve the script's ability to accurately identify cycles and trends in the data.

Machine learning integration: Integrating machine learning techniques, such as artificial neural networks or support vector machines, can help enhance the script's predictive capabilities, leading to more accurate financial models.

Enhancements for General and Advanced Trading

Customizable indicator integration: Allowing users to integrate their own technical indicators can help improve the script's effectiveness for both general and advanced trading. By enabling the combination of the dominant cycle information with other technical analysis tools, traders can develop more comprehensive trading strategies.

Risk management and position sizing: Incorporating risk management and position sizing functionality into the script can help traders better manage their trades and control potential losses. This can be achieved by calculating the optimal position size based on the user's risk tolerance and account size.

Multi-timeframe analysis: Enhancing the script to perform multi-timeframe analysis can provide traders with a more holistic view of market trends and cycles. By identifying dominant cycles on different timeframes, traders can gain insights into the potential confluence of cycles and make better-informed trading decisions.

Enhancements for High-Frequency Finance Trading

Algorithm optimization: To ensure the script's suitability for high-frequency finance trading, optimizing the algorithm for faster execution is crucial. This can be achieved by employing efficient data structures and refining the calculation methods to minimize computational complexity.

Real-time data streaming: Integrating real-time data streaming capabilities into the script can help high-frequency traders react to market changes more quickly. By continuously updating the cycle information based on real-time market data, traders can adapt their strategies accordingly and capitalize on short-term market fluctuations.

Order execution and trade management: To fully leverage the script's capabilities for high-frequency trading, implementing functionality for automated order execution and trade management is essential. This can include features such as stop-loss and take-profit orders, trailing stops, and automated trade exit strategies.

While the existing Goertzel algorithm-based script is a valuable tool for detecting dominant cycles in financial data, there are several potential enhancements that can make it even more powerful for financial modeling, general trading, advanced trading, and high-frequency finance trading. By incorporating these improvements, the script can become a more versatile and effective tool for traders and financial analysts alike.

█ Understanding the Limitations of the Goertzel Algorithm

While the Goertzel algorithm-based script for detecting dominant cycles in financial data provides valuable insights, it is important to be aware of its limitations and drawbacks. Some of the key drawbacks of this indicator are:

Lagging nature:

As with many other technical indicators, the Goertzel algorithm-based script can suffer from lagging effects, meaning that it may not immediately react to real-time market changes. This lag can lead to late entries and exits, potentially resulting in reduced profitability or increased losses.

Parameter sensitivity:

The performance of the script can be sensitive to the chosen parameters, such as the detrending methods, smoothing techniques, and cycle detection settings. Improper parameter selection may lead to inaccurate cycle detection or increased false signals, which can negatively impact trading performance.

Complexity:

The Goertzel algorithm itself is relatively complex, making it difficult for novice traders or those unfamiliar with the concept of cycle analysis to fully understand and effectively utilize the script. This complexity can also make it challenging to optimize the script for specific trading styles or market conditions.

Overfitting risk:

As with any data-driven approach, there is a risk of overfitting when using the Goertzel algorithm-based script. Overfitting occurs when a model becomes too specific to the historical data it was trained on, leading to poor performance on new, unseen data. This can result in misleading signals and reduced trading performance.

No guarantee of future performance: While the script can provide insights into past cycles and potential future trends, it is important to remember that past performance does not guarantee future results. Market conditions can change, and relying solely on the script's predictions without considering other factors may lead to poor trading decisions.

Limited applicability: The Goertzel algorithm-based script may not be suitable for all markets, trading styles, or timeframes. Its effectiveness in detecting cycles may be limited in certain market conditions, such as during periods of extreme volatility or low liquidity.

While the Goertzel algorithm-based script offers valuable insights into dominant cycles in financial data, it is essential to consider its drawbacks and limitations when incorporating it into a trading strategy. Traders should always use the script in conjunction with other technical and fundamental analysis tools, as well as proper risk management, to make well-informed trading decisions.

█ Interpreting Results

The Goertzel Browser indicator can be interpreted by analyzing the plotted lines and the table presented alongside them. The indicator plots two lines: past and future composite waves. The past composite wave represents the composite wave of the past price data, and the future composite wave represents the projected composite wave for the next period.

The past composite wave line displays a solid line, with green indicating a bullish trend and red indicating a bearish trend. On the other hand, the future composite wave line is a dotted line with fuchsia indicating a bullish trend and yellow indicating a bearish trend.

The table presented alongside the indicator shows the top cycles with their corresponding rank, period, Bartels, amplitude or cycle strength, and phase. The amplitude is a measure of the strength of the cycle, while the phase is the position of the cycle within the data series.

Interpreting the Goertzel Browser indicator involves identifying the trend of the past and future composite wave lines and matching them with the corresponding bullish or bearish color. Additionally, traders can identify the top cycles with the highest amplitude or cycle strength and utilize them in conjunction with other technical indicators and fundamental analysis for trading decisions.

This indicator is considered a repainting indicator because the value of the indicator is calculated based on the past price data. As new price data becomes available, the indicator's value is recalculated, potentially causing the indicator's past values to change. This can create a false impression of the indicator's performance, as it may appear to have provided a profitable trading signal in the past when, in fact, that signal did not exist at the time.

The Goertzel indicator is also non-endpointed, meaning that it is not calculated up to the current bar or candle. Instead, it uses a fixed amount of historical data to calculate its values, which can make it difficult to use for real-time trading decisions. For example, if the indicator uses 100 bars of historical data to make its calculations, it cannot provide a signal until the current bar has closed and become part of the historical data. This can result in missed trading opportunities or delayed signals.

█ Conclusion

The Goertzel Browser indicator is a powerful tool for identifying and analyzing cyclical patterns in financial markets. Its ability to detect multiple cycles of varying frequencies and strengths make it a valuable addition to any trader's technical analysis toolkit. However, it is important to keep in mind that the Goertzel Browser indicator should be used in conjunction with other technical analysis tools and fundamental analysis to achieve the best results. With continued refinement and development, the Goertzel Browser indicator has the potential to become a highly effective tool for financial modeling, general trading, advanced trading, and high-frequency finance trading. Its accuracy and versatility make it a promising candidate for further research and development.

█ Footnotes

What is the Bartels Test for Cycle Significance?

The Bartels Cycle Significance Test is a statistical method that determines whether the peaks and troughs of a time series are statistically significant. The test is named after its inventor, George Bartels, who developed it in the mid-20th century.

The Bartels test is designed to analyze the cyclical components of a time series, which can help traders and analysts identify trends and cycles in financial markets. The test calculates a Bartels statistic, which measures the degree of non-randomness or autocorrelation in the time series.

The Bartels statistic is calculated by first splitting the time series into two halves and calculating the range of the peaks and troughs in each half. The test then compares these ranges using a t-test, which measures the significance of the difference between the two ranges.

If the Bartels statistic is greater than a critical value, it indicates that the peaks and troughs in the time series are non-random and that there is a significant cyclical component to the data. Conversely, if the Bartels statistic is less than the critical value, it suggests that the peaks and troughs are random and that there is no significant cyclical component.

The Bartels Cycle Significance Test is particularly useful in financial analysis because it can help traders and analysts identify significant cycles in asset prices, which can in turn inform investment decisions. However, it is important to note that the test is not perfect and can produce false signals in certain situations, particularly in noisy or volatile markets. Therefore, it is always recommended to use the test in conjunction with other technical and fundamental indicators to confirm trends and cycles.

Deep-dive into the Hodrick-Prescott Fitler

The Hodrick-Prescott (HP) filter is a statistical tool used in economics and finance to separate a time series into two components: a trend component and a cyclical component. It is a powerful tool for identifying long-term trends in economic and financial data and is widely used by economists, central banks, and financial institutions around the world.

The HP filter was first introduced in the 1990s by economists Robert Hodrick and Edward Prescott. It is a simple, two-parameter filter that separates a time series into a trend component and a cyclical component. The trend component represents the long-term behavior of the data, while the cyclical component captures the shorter-term fluctuations around the trend.

The HP filter works by minimizing the following objective function:

Minimize: (Sum of Squared Deviations) + λ (Sum of Squared Second Differences)

Where:

The first term represents the deviation of the data from the trend.

The second term represents the smoothness of the trend.

λ is a smoothing parameter that determines the degree of smoothness of the trend.

The smoothing parameter λ is typically set to a value between 100 and 1600, depending on the frequency of the data. Higher values of λ lead to a smoother trend, while lower values lead to a more volatile trend.

The HP filter has several advantages over other smoothing techniques. It is a non-parametric method, meaning that it does not make any assumptions about the underlying distribution of the data. It also allows for easy comparison of trends across different time series and can be used with data of any frequency.

However, the HP filter also has some limitations. It assumes that the trend is a smooth function, which may not be the case in some situations. It can also be sensitive to changes in the smoothing parameter λ, which may result in different trends for the same data. Additionally, the filter may produce unrealistic trends for very short time series.