Real-Fast Fourier Transform of Price w/ Linear Regression [Loxx]Real-Fast Fourier Transform of Price w/ Linear Regression is a indicator that implements a Real-Fast Fourier Transform on Price and modifies the output by a measure of Linear Regression. The solid line is the Linear Regression Trend of the windowed data, The green/red line is the Real FFT of price.

What is the Discrete Fourier Transform?

In mathematics, the discrete Fourier transform (DFT) converts a finite sequence of equally-spaced samples of a function into a same-length sequence of equally-spaced samples of the discrete-time Fourier transform (DTFT), which is a complex-valued function of frequency. The interval at which the DTFT is sampled is the reciprocal of the duration of the input sequence. An inverse DFT is a Fourier series, using the DTFT samples as coefficients of complex sinusoids at the corresponding DTFT frequencies. It has the same sample-values as the original input sequence. The DFT is therefore said to be a frequency domain representation of the original input sequence. If the original sequence spans all the non-zero values of a function, its DTFT is continuous (and periodic), and the DFT provides discrete samples of one cycle. If the original sequence is one cycle of a periodic function, the DFT provides all the non-zero values of one DTFT cycle.

What is the Complex Fast Fourier Transform?

The complex Fast Fourier Transform algorithm transforms N real or complex numbers into another N complex numbers. The complex FFT transforms a real or complex signal x in the time domain into a complex two-sided spectrum X in the frequency domain. You must remember that zero frequency corresponds to n = 0, positive frequencies 0 < f < f_c correspond to values 1 ≤ n ≤ N/2 −1, while negative frequencies −fc < f < 0 correspond to N/2 +1 ≤ n ≤ N −1. The value n = N/2 corresponds to both f = f_c and f = −f_c. f_c is the critical or Nyquist frequency with f_c = 1/(2*T) or half the sampling frequency. The first harmonic X corresponds to the frequency 1/(N*T).

The complex FFT requires the list of values (resolution, or N) to be a power 2. If the input size if not a power of 2, then the input data will be padded with zeros to fit the size of the closest power of 2 upward.

What is Real-Fast Fourier Transform?

Has conditions similar to the complex Fast Fourier Transform value, except that the input data must be purely real. If the time series data has the basic type complex64, only the real parts of the complex numbers are used for the calculation. The imaginary parts are silently discarded.

Inputs:

src = source price

uselreg = whether you wish to modify output with linear regression calculation

Windowin = windowing period, restricted to powers of 2: "4", "8", "16", "32", "64", "128", "256", "512", "1024", "2048"

Treshold = to modified power output to fine tune signal

dtrendper = adjust regression calculation

barsback = move window backward from bar 0

mutebars = mute bar coloring for the range

Further reading:

Real-valued Fast Fourier Transform Algorithms IEEE Transactions on Acoustics, Speech, and Signal Processing, June 1987

Related indicators utilizing Fourier Transform

Fourier Extrapolator of Variety RSI w/ Bollinger Bands

Fourier Extrapolation of Variety Moving Averages

Fourier Extrapolator of Price w/ Projection Forecast

Komut dosyalarını "wind+芯片行业+市盈率+财经数据" için ara

vol_boxA simple script to draw a realized volatility forecast, in the form of a box. The script calculates realized volatility using the EWMA method, using a number of periods of your choosing. Using the "periods per year", you can adjust the script to work on any time frame. For example, if you are using an hourly chart with bitcoin, there are 24 periods * 365 = 8760 periods per year. This setting is essential for the realized volatility figure to be accurate as an annualized figure, like VIX.

By default, the settings are set to mimic CBOE volatility indices. That is, 252 days per year, and 20 period window on the daily timeframe (simulating a 30 trading day period).

Inside the box are three figures:

1. The current realized volatility.

2. The rank. E.g. "10%" means the current realized volatility is less than 90% of realized volatility measures.

3. The "accuracy": how often price has closed within the box, historically.

Inputs:

stdevs: the number of standard deviations for the box

periods to project: the number of periods to forecast

window: the number of periods for calculating realized volatility

periods per year: the number of periods in one year (e.g. 252 for the "D" timeframe)

Levels Of Fear [AstrideUnicorn]"Buy at the level of maximum fear when everyone is selling." - says a well-known among traders wisdom. If an asset's price declines significantly from the most recent highest value or established range, traders start to worry. The higher the drawdown gets, the more fear market participants experience. During a sell-off, a feedback loop arises, in which the escalating fear and price decline strengthen each other.

The Levels Of Fear indicator helps analyze price declines and find the best times to buy an asset after a sell-off. In finance, volatility is a term that describes the degree of variation of an asset price over time. It is usually denoted by the letter σ (sigma) and estimated as the standard deviation of the asset price or price returns. The Levels Of Fear indicator helps measure the current price decline in the standard deviation units. It plots seven levels at distances of 1, 2, 3, 4, 5, 6, and 7 standard deviations (sigmas) below the base price (the recent highest price or upper bound of the established range). In what follows, we will refer to these levels as levels of fear.

HOW TO USE

When the price in its decline reaches a certain level of fear, it means that it has declined from its recent highest value by a corresponding number of standard deviations. The indicator helps traders see the minimum levels to which the price may fall and estimate the potential depth of the current decline based on the cause of the actual market shock. Five-seven sigma declines are relatively rare events and correspond to significant market shocks. In the lack of information, 5-7 sigma levels are good for buying an asset. Because when the price falls that deep, it corresponds to the maximum fear and pessimism in the market when most people are selling. In such situations, contrarian logic becomes the best decision.

SETTINGS

Window: the averaging window or period of the indicator. The algorithm uses this parameter to calculate the base level and standard deviations. Higher values are better for measuring deeper and longer declines.

Levels Stability: the parameter used in the decline detection. The higher the value is, the more stable and long the fear levels are, but at the same time, the lag increases. The lower it is, the faster the indicator responds to the price changes, but the fear levels are recalculated more frequently and are less stable. This parameter is mostly for fine-tuning. It does not change the overall picture much.

Mode: the parameter that defines the style for the labels. In the Cool Guys Mode , the indicator displays the labels as emojis. In the Serious Guys Mode , labels show the distance from the base level measured in standard deviation units or sigmas.

Sentiment Estimator [AstrideUnicorn]Sentiment Estimator is an indicator that estimates market sentiment using only its pricing data. It counts bullish and bearish candles in a rolling window and calculates their relative values as percentages of the total amount of candles in the window. Market sentiment shows the direction in which the market is biased to move or the current trend direction. Extreme values of the market sentiment are contrarian signals. When the market sentiment is too bullish, it is time to sell and vice versa.

HOW TO USE

Sentiment Estimator plots a pair of green and red circles for each candle. They represent bullish and bearish sentiments, respectively.

The vertical positions of the circles show corresponding sentiment values in percentage units. For example, if a green circle's height is 60, the market is 60% bullish. In this case, the red circle's height will be 40, as bullish and bearish parts of the market sentiment sum to 100%.

The blue line plotted at the 50% level shows the neutral sentiment level. If a green circle is above the blue line, the prevailing market sentiment at that time is bullish, and the market is biased to move up. If a red one is above, the market has predominantly bearish sentiment and is prone to move down.

The red level shows extreme sentiment level. If a green or red circle is above this line, it means that the market is extremely bullish or bearish, respectively. It is a contrarian signal, and one can expect a reversal soon. In this case, a blue label with the text "reversal expected" is shown.

SETTINGS

Timeframe - allows choosing a timeframe other than the chart's one for the indicator calculation.

Look-Back Window - sets the historical window length used to perform the calculations. You can adjust the window to get the best results for a particular market or timeframe.

DrawIndicatorOnTheChartLibrary "DrawIndicatorOnTheChart"

this library is used to show an indicator (such RSI, CCI, MOM etc) on the main chart with indicator's horizontal lines in a window. Location of the window is calculated dynamically by last price movemements

drawIndicator(indicatorName, indicator, indicatorcolor, period, indimax_, indimin_, levels, precision, xlocation) draws the related indicator on the chart

Parameters:

indicatorName : is the indicator name as string such "RSI", "CCI" etc

indicator : is the indicator you want to show, such rsi(close, 14), mom(close, 10) etc

indicatorcolor : is the color of indicator line

period : is the length of the window to show

indimax_ : is the maximum value of the indicator, for example for RSI it's 100.0, if the indicator (such CCI, MOM etc) doesn't have maximum value then use "na"

indimin_ : is the minimum value of the indicator, for example for RSI it's 0.0, if the indicator (such CCI, MOM etc)doesn't have maximum value then use "na"

levels : is the levels of the array for the horizontal lines. for example if you want horizontal lines at 30.0, and 70.0 then use array.from(30.0, 70.0). if no horizontal lines then use array.from(na)

precision : is the precision/number of decimals that is used to show indicator values, for example for RSI set it 2

xlocation : is end location of the indicator window, for example if xlocation = 0 window is created on the index of the last bar/candle

Returns: none

Liquidity Levels [LuxAlgo]The Peak Activity Levels indicator displays support and resistance levels from prices accompanied by significant volume. The indicator includes a histogram returning the frequency of closing prices falling between two parallel levels, each bin shows the number of bullish candles within the levels.

1. Settings

Length: Lookback for the detection of volume peaks.

Number Of Levels: Determines the number of levels to display.

Levels Color Mode: Determines how the levels should be colored. "Relative" will color the levels based on their location relative to the current price. "Random" will apply a random color to each level. "Fixed" will use a single color for each level.

Levels Style: Style of the displayed levels. Styles include solid, dashed, and dotted.

1.1 Histogram

Show Histogram: Determines whether to display the histogram or not.

Histogram Window: Lookback period of the histogram calculation.

Bins Colors: Control the color of the histogram bins.

2. Usage

The indicator can be used to display ready-to-use support and resistance. These are constructed from peaks in volume. When a peak occurs, we take the price where this peak occurred and use it as the value for our level.

If one of the levels was previously tested, we can hypothesize that the level might be used as support/resistance in the future. Additional analysis using volume can be done in order to confirm a potential bounce.

The histogram can return various information to the user. It can show if the price stayed within two levels for a long time and if the price within two levels was mostly made of bullish or bearish candles.

In the chart above, we can see that over the most recent 200 bars (determined by Histogram Window) 68 closing prices fall between levels A and B, with 27 bars being bullish.

Additionally, the width of a bin and its length can sometimes give information about the volatility of a specific price variation. If a bin is very wide but short (a low number of closing prices fallen within the levels) then we can conclude a most of the movement was done on a short amount of time.

vol_signalNote: This description is copied from the script comments. Please refer to the comments and release notes for updated information, as I am unable to edit and update this description.

----------

USAGE

This script gives signals based on a volatility forecast, e.g. for a stop

loss. It is a simplified version of my other script "trend_vol_forecast", which incorporates a trend following system and measures performance. The "X" labels indicate when the price touches (exceeds) a forecast. The signal occurs when price crosses "fcst_up" or "fcst_down".

There are only three parameters:

- volatility window: this is the number of periods (bars) used in the

historical volatility calculation. smaller number = reacts more

quickly to changes, but is a "noisier" signal.

- forecast periods: the number of periods for projecting a volatility

forecast. for example, "21" on a daily chart means the plots will

show the forecast from 21 days ago.

- forecast stdev: the number of standard deviations in the forecast.

for example, "2" means that price is expected to remain within

the forecast plot ~95% of the time. A higher number produces a

wider forecast.

The output table shows:

- realized vol: the volatility over the previous N periods, where N =

"volatility window".

- forecast vol: the realized volatility from N periods ago, where N =

"forecast periods"

- up/down fcst (level): the price level of the forecast for the next

N bars, where N = "forecast periods".

- up/down fcst (%): the difference between the current and forecast

price, expressed as a whole number percentage.

The plots show:

- blue/red plot: the upper/lower forecast from "forecast periods" ago.

- blue/red line: the upper/lower forecast for the next

"forecast periods".

- red/blue labels: an "X" where the price touched the forecast from

"forecast periods" ago.

+ NOTE: pinescript only draws a limited number of labels.

They will not appear very far into the past.

RSI Stochastic AlignmentRSI Stochastic Alignment input RSI and Stochastic into 1 windows and align them to find bullish and bearish divergence.

A. The Line display in windows:

1. Fast RSI (green line) is RSI(close,3)

2. Slow Rsi (red line) is Linear Regession of Fast RSI with 5 period and offset 0 = linreg(rsi,5,0)

3. Fast Stochastic (blue line) is %K of Stochastic

4. Slow Stochastic (aqua line) is %D of Stochastic

B. Alignment and Divergence Detect

1. Bearish Divergence:

* Slow RSI at top

* Fast Stochastic at bottom

* Fast RSI over overbought level (default = 70)

* Slow Stochastic under overbought level minus a constant value (Divergence Power value, default this value = 1)

2. Bullish Divergence:

* Fast Stochastic at top

* Slow RSI at bottom

* Fast RSI under oversold level (default = 30)

* Slow Stochastic over oversold level plus a constant value (Divergence Power value, default this value = 1)

C. Script Option

1. RSI value adjustable

2. Stochastic value adjustable

3. Overbought and Oversold Level adjustable

4. Enable/Disable Level line

5. Enable/Disable Divergence Column

6. Enable/Disable Key Bar Colored

Narrow Bandpass FilterIn technical analysis most bandpass filters like the MACD, TRIX, AO, or COG will have a non-symmetrical frequency response, in fact, this one is generally right-skewed. As such these oscillators will not fully remove lower and higher frequency components from the input signal, the following indicator is a bandpass filter with a more symmetrical frequency response with the possibility to have a narrow bandwidth, this allows the indicator to potentially isolate sinusoids from the input signal.

Indicator & Settings

The filter is calculated via convolution, if we take into account that the frequency response of a filter is the Fourier transform of its weighting function we can deduce that we can get a narrow response by using a sinusoid sin(2𝛑nf) as the weighting function, with the peak of the frequency response being equal to f , this makes the filter quite easy to control by the user, as this one can choose the frequency to be isolated. The length of the weighting function controls the bandwidth of the frequency response, with a higher length returning an ever-smaller frequency response width.

In the indicator settings the "Cycle Period" determine the period of the sinusoid used as a weighting function, while "Bandwidth" determine the filter passband width, with higher values returning a narrower passband, this setting also determine the length of the convolution, because the sum of the weights must add to 0 we know that the length of the convolution must be a multiple of "Cycle Period", so the length of the convolution is equal to "Cycle Period × Bandwidth".

Finally, the windowing option determines if a window is applied to the weighting function, a weighting function allow to remove ripples in the filter frequency response

Above both indicators have a Cycle period of 100 and a Bandwidth of 4, we can see that the indicator with no windowing don't fully remove the trend component in the price, this is due to the presence of ripples allowing lower frequency components to pass, this is not the case for the windowed version.

In theory, an ultra-narrow passband would allow to fully isolate pure sinusoids, below the cycle period of interest is 20

using a bandwidth equal to 10 allow to retain that sinusoid, however, note that this sinusoid is subject to phase shift and that it might not be a dominant frequency in the price.

Decaying Rate of Change Non Linear FilterThis is a potential solution to dealing with the inherent lag in most filters especially with instruments such as BTC and the effects of long periods of low volatility followed by massive volatility spikes as well as whipsaws/barts etc.

We can try and solve these issues in a number of ways, adaptive lengths, dynamic weighting etc. This filter uses a non linear weighting combined with an exponential decay rate.

With the non linear weighting the filter can become very responsive to sudden volatility spikes. We can use a short length absolute rate of change as a method to improve weighting of relative high volatility.

c1 = abs(close - close ) / close

Which gives us a fairly simple filter :

filter = sum(c1 * close,periods) / sum(c1,periods)

At this point if we want to control the relative magnitude of the ROC coefficients we can do so by raising it to a power.

c2 = pow(c1, x)

Where x approaches zero the coefficient approaches 1 or a linear filter. At x = 1 we have an unmodified coefficient and higher values increase the relative magnitude of the response. As an extreme example with x = 10 we effectively isolate the highest ROC candle within the window (which has some novel support resistance horizontals as those closes are often important). This controls the degree of responsiveness, so we can magnify the responsiveness, but with the trade off of overshoot/persistence.

So now we have the problem whereby that a highly weighted data point from a high volatility event persists within the filter window. And to a possibly extreme degree, if a reversal occurs we get a potentially large "overshoot" and in a way actually induced a large amount of lag for future price action.

This filter compensates for this effect by exponentially decaying the abs(ROC) coefficient over time, so as a high volatility event passes through the filter window it receives exponentially less weighting allowing more recent prices to receive a higher relative weighting than they would have.

c3 = c2 * pow(1 - percent_decay, periods_back)

This is somewhat similar to an EMA, however with an EMA being recursive that event will persist forever (to some degree) in the calculation. Here we are using a fixed window, so once the event is behind the window it's completely removed from the calculation

I've added Ehler's Super Smoother as an optional smoothing function as some highly non linear settings benefit from smoothing. I can't remember where I got the original SS code snippet, so if you recognize it as yours msg me and I'll link you here.

Volume-Weighted Money Flow [sgbpulse]Overview

The VWMF indicator is an advanced technical analysis tool that combines and summarizes five leading momentum and volume indicators (OBV, PVT, A/D, CMF, MFI) into one clear oscillator. The indicator helps to provide a clear picture of market sentiment by measuring the pressure from buyers and sellers. Unlike single indicators, VWMF provides a comprehensive view of market money flow by weighting existing indicators and presenting them in a uniform and understandable format.

Indicator Components

VWMF combines the following indicators, each normalized to a range of 0 to 100 before being weighted:

On-Balance Volume (OBV): A cumulative indicator that measures positive and negative volume flow.

Price-Volume Trend (PVT): Similar to OBV, but incorporates relative price change for a more precise measure.

Accumulation/Distribution Line (A/D): Used to identify whether an asset is being bought (accumulated) or sold (distributed).

Chaikin Money Flow (CMF): Measures the money flow over a period based on the close price's position relative to the candle's range.

Money Flow Index (MFI): A momentum oscillator that combines price and volume to measure buying and selling pressure.

Understanding the Normalized Oscillators

The indicator combines the five different momentum indicators by normalizing each one to a uniform range of 0 to 100 .

Why is Normalization Important?

Indicators like OBV, PVT, and the A/D Line are cumulative indicators whose values can become very large. To assess their trend, we use a Moving Average as a dynamic reference line . The Moving Average allows us to understand whether the indicator is currently trending up or down relative to its average behavior over time.

How Does Normalization Work?

Our normalization fully preserves the original trend of each indicator.

For Cumulative Indicators (OBV, PVT, A/D): We calculate the difference between the current indicator value and its Moving Average. This difference is then passed to the normalization process.

- If the indicator is above its Moving Average, the difference will be positive, and the normalized value will be above 50.

- If the indicator is below its Moving Average, the difference will be negative, and the normalized value will be below 50.

Handling Extreme Values: To overcome the issue of extreme values in indicators like OBV, PVT, and the A/D Line , the function calculates the highest absolute value over the selected period. This value is used to prevent sharp spikes or drops in a single indicator from compromising the accuracy of the normalization over time. It's a sophisticated method that ensures the oscillators remain relevant and accurate.

For Bounded Indicators (CMF, MFI): These indicators already operate within a known range (for example, CMF is between -1 and 1, and MFI is between 0 and 100), so they are normalized directly without an additional reference line.

Reference Line Settings:

Moving Average Type: Allows the user to choose between a Simple Moving Average (SMA) and an Exponential Moving Average (EMA).

Volume Flow MA Length: Allows the user to set the lookback period for the Moving Average, which affects the indicator's sensitivity.

The 50 line serves as the new "center line." This ensures that, even after normalization, the determination of whether a specific indicator supports a bullish or bearish trend remains clear.

Settings and Visual Tools

The indicator offers several customization options to provide a rich analysis experience:

VWMF Oscillator (Blue Line): Represents the weighted average of all five indicators. Values above 50 indicate bullish momentum, and values below 50 indicate bearish momentum.

Strength Metrics (Bullish/Bearish Strength %): Two metrics that appear on the status line, showing the percentage of indicators supporting the current trend. They range from 0% to 100%, providing a quick view of the strength of the consensus.

Dynamic Background Colors: The background color of the chart automatically changes to bullish (a blue shade by default) or bearish (a default brown-gray shade) based on the trend. The transparency of the color shows the consensus strength—the more opaque the background, the more indicators support the trend.

Advanced Settings:

- Background Color Logic: Allows the user to choose the trigger for the background color: Weighted Value (based on the combined oscillator) or Strength (based on the majority of individual indicators).

- Weights: Provides full control over the weight of each of the five indicators in the final oscillator.

Using the Data Window

TradingView provides a useful Data Window that allows you to see the exact numerical values of each normalized oscillator separately, in addition to the trend strength data.

You can use this window to:

Get more detailed information on each indicator: Viewing the precise numerical data of each of the five indicators can help in making trading decisions.

Calibrate weights: If you want to manually adjust the indicator weights (in the settings menu), you can do so while tracking the impact of each indicator on the weighted oscillator in the Data Window.

The indicator's default setting is an equal weight of 20% for each of the five indicators.

Alert Conditions

The indicator comes with a variety of built-in alerts that can be configured through the TradingView alerts menu:

VWMF Cross Above 50: An alert when the VWMF oscillator crosses above the 50 line, indicating a potential bullish momentum shift.

VWMF Cross Below 50: An alert when the VWMF oscillator crosses below the 50 line, indicating a potential bearish momentum shift.

Bullish Strength: High But Not Absolute Consensus: An alert when the bullish trend strength reaches 60% or more but is less than 100%, indicating a high but not absolute consensus.

Bullish Strength at 100%: An alert when all five indicators (MFI, OBV, PVT, A/D, CMF) show bullish strength, indicating a full and absolute consensus.

Bearish Strength: High But Not Absolute Consensus: An alert when the bearish trend strength reaches 60% or more but is less than 100%, indicating a high but not absolute consensus.

Bearish Strength at 100%: An alert when all five indicators (MFI, OBV, PVT, A/D, CMF) show bearish strength, indicating a full and absolute consensus.

Summary

The VWMF indicator is a powerful, all-in-one tool for analyzing market momentum, money flow, and sentiment. By combining and normalizing five different indicators into a single oscillator, it offers a holistic and accurate view of the market's underlying trend. Its dynamic visual features and customizable settings, including the ability to adjust indicator weights, provide a flexible experience for both novice and experienced traders. The built-in alerts for momentum shifts and trend consensus make it an effective tool for spotting trading opportunities with confidence. In essence, VWMF distills complex market data into clear, actionable signals.

Important Note: Trading Risk

This indicator is intended for educational and informational purposes only and does not constitute investment advice or a recommendation for trading in any form whatsoever.

Trading in financial markets involves significant risk of capital loss. It is important to remember that past performance is not indicative of future results. All trading decisions are your sole responsibility. Never trade with money you cannot afford to lose.

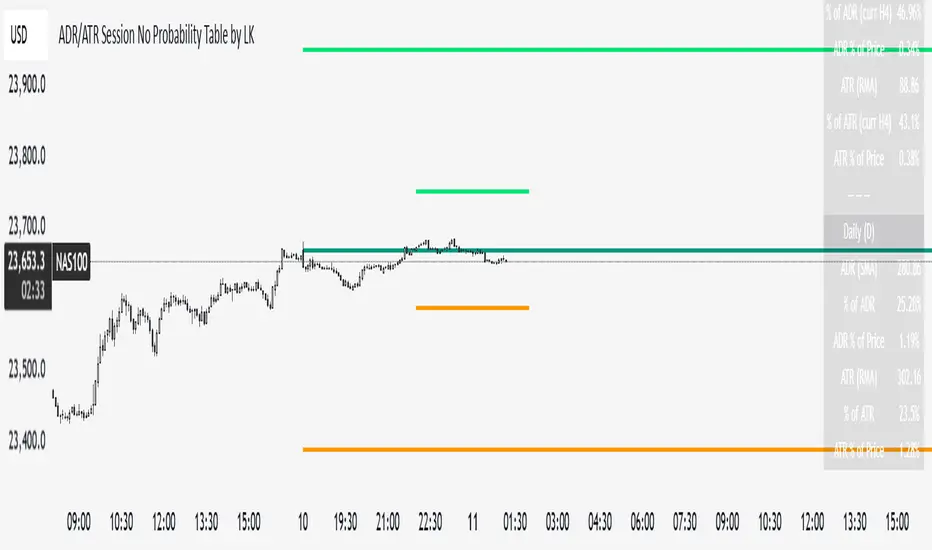

ADR/ATR Session No Probability Table by LKHere you go—clear, English docs you can drop into your script’s description or share with teammates.

ADR/ATR Session by LK — Overview

This indicator summarizes Average Daily Range (ADR) and Average True Range (ATR) for two horizons:

• Session H4 (e.g., 06:00–13:00 on a 4‑hour chart)

• Daily (D)

It shows:

• Current ADR/ATR values (using your chosen smoothing method)

• How much of ADR/ATR today/this bar has already been consumed (% of ADR/ATR)

• ADR/ATR as a percent of price

• Optional probability blocks: likelihood that %ADR will exceed user‑defined thresholds over a lookback window

• Optional on‑chart lines for the current H4 and Daily candles: Open, ADR High, ADR Low

⸻

What the metrics mean

• ADR (H4 / D): Moving average of the bar range (high - low).

• ATR (H4 / D): Moving average of True Range (max(hi-lo, |hi-close |, |lo-close |)).

• % of ADR (curr H4): (H4 range of the current H4 bar) / ADR(H4) × 100. Updates live even if the current time is outside the session.

• % of ADR (Daily): (today’s intra‑day range) / ADR(D) × 100.

• % of ATR (curr H4 / Daily): TR / ATR × 100 for that horizon.

• ADR % of Price / ATR % of Price: ADR or ATR divided by current price × 100 (a quick “volatility vs. price” gauge).

Session logic (H4): ADR/ATR(H4) only update on bars that fall inside the configured session window; outside the window the values hold steady (no recalculation “bleed”).

Daily range tracking: The indicator tracks today’s high/low in real‑time and resets at the day change.

⸻

Inputs (quick reference)

Core

• Length (ADR/ATR): smoothing length for ADR/ATR (default 21).

• Wait for Higher TF Bar Close: if true, updates ADR/ATR only after the higher‑TF bar closes when using request.security.

Timeframes

• Session Timeframe (H4): default 240.

• Daily Timeframe: default D.

Session time

• Session Timezone: “Chart” (default) or a fixed timezone.

• Session Start Hour, End Hour (minutes are fixed to 0 in this version).

Smoothing methods

• H4 ADR Method / H4 ATR Method: SMA/EMA/RMA/WMA.

• Daily ADR Method / Daily ATR Method: SMA/EMA/RMA/WMA.

Table appearance

• Table BG, Table Text, Table Font Size.

Lines (optional)

• Show current H4 segments, Show current Daily segments

• Line colors for Open / ADR High / ADR Low

• Line width

Probability

• H4 Probability Lookback (bars): number of H4 bars to examine (e.g., 300).

• Daily Probability Lookback (days): number of D bars (e.g., 180).

• ADR thresholds (%): CSV list of thresholds (e.g., 25,50,55,60,65,70,75,80,85,90,95,100,125,150).

The table will show the % of lookback bars where %ADR ≥ threshold.

Tip: If you want probabilities only for session H4 bars (not every H4 bar), ask and I can add a toggle to filter by inSess.

⸻

How to read the table

H4 block

• ADR (method) / ATR (method): the session‑aware averages.

• % of ADR (curr H4): live progress of this H4 bar toward the session ADR.

• ADR % of Price: ADR(H4) relative to price.

• % of ATR (curr H4) and ATR % of Price: same idea for ATR.

H4 Probability (lookback N bars)

• Rows like “≥ 80% ADR” show the fraction (in %) of the last N H4 bars that reached at least 80% of ADR(H4).

Daily block

• Mirrors the H4 block, but for Daily.

Daily Probability (lookback M days)

• Rows like “≥ 100% ADR” show the fraction of the last M daily bars whose daily range reached at least 100% of ADR(D).

⸻

Practical usage

• Use % of ADR (curr H4 / Daily) to judge exhaustion or room left in the day/session.

E.g., if Daily %ADR is already 95%, be cautious with momentum continuation trades.

• The probability tables give a quick historical context:

If “≥ 125% ADR” is ~18%, the market rarely stretches that far; your trade sizing/targets can reflect that.

• ADR/ATR % of Price helps normalize volatility between instruments.

⸻

Troubleshooting

• If probability rows are blank: ensure lookback windows are large enough (and that the chart has enough history).

• If ADR/ATR show … (NA): usually you don’t have enough bars for the chosen length/TF yet.

• If line segments are missing: verify you’re on a chart with visible current H4/D bars and the toggles are enabled.

⸻

Notes & customization ideas

• Add a toggle to count only session bars in H4 probability.

• Add separate thresholds for H4 vs Daily.

• Let users pick minutes for session start/end if needed.

• Add alerts when %ADR crosses specified thresholds.

If you want me to bundle any of the “ideas” above into the code, say the word and I’ll ship a clean patch.

Opening Range Breakout🧭 Overview

The Open Range Breakout (ORB) indicator is designed to capture and display the initial price range of the trading day (typically the first 15 minutes), and help traders identify breakout opportunities beyond this range. This is a popular strategy among intraday and momentum traders.

🔧 Features

📊 ORB High/Low Lines

Plots horizontal lines for the session’s high and low

🟩 Breakout Zones

Background highlights when price breaks above or below the range

🏷️ Breakout Labels

Text labels marking breakout events

🧭 Session Control

Customizable session input (default: 09:15–09:30 IST)

📍 ORB Line Labels

Text labels anchored to the ORB high and low lines (aligned right)

🔔 Alerts

Configurable alerts for breakout events

⚙️ Adjustable Settings

Show/hide background, labels, session window, etc.

⏱️ Session Logic

• The ORB range is calculated during a defined session window (default: 09:15–09:30).

• During this window, the highest high and lowest low are recorded as ORB High and ORB Low.

📈 Breakout Detection

• Breakout Above: Triggered when price crosses above the ORB High.

• Breakout Below: Triggered when price crosses below the ORB Low.

• Each breakout can trigger:

• A background highlight (green/red)

• A text label (“Breakout ↑” / “Breakout ↓”)

• An optional alert

🔔 Alerts

Two built-in alert conditions:

1. Breakout Above ORB High

• Message: "🔼 Price broke above ORB High: {{close}}"

2. Breakout Below ORB Low

• Message: "🔽 Price broke below ORB Low: {{close}}"

You can create alerts in TradingView by selecting these from the Add Alert window.

📌 Best Use Cases

• Intraday momentum trading

• Breakout and scalping strategies

• First 15-minute range traders (NSE, BSE markets)

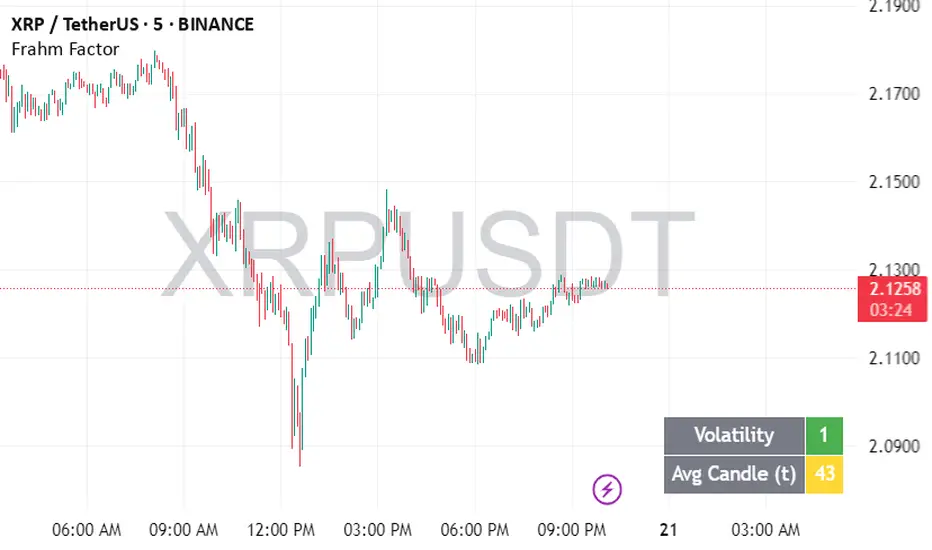

Frahm FactorIntended Usage of the Frahm Factor Indicator

The Frahm Factor is designed to give you a rapid, at-a-glance assessment of how volatile the market is right now—and how large the average candle has been—over the most recent 24-hour window. Here’s how to put it to work:

Gauge Volatility Regimes

Volatility Score (1–10)

A low score (1–3, green) signals calm seas—tight ranges, low risk of big moves.

A mid score (4–6, yellow) warns you that volatility is picking up.

A high score (7–10, red) tells you to prepare for disorderly swings or breakout opportunities.

How to trade off it

In low-volatility periods, you might favor mean-reversion or range-bound strategies.

As the score climbs into the red zone, consider widening stops, scaling back position size, or switching to breakout momentum plays.

Monitor Average Candle Size

Avg Candle (ticks) cell shows you the mean true-range of each bar over that 24h window in ticks.

When candles are small, you know the market is consolidating and liquidity may be thin.

When candles are large, momentum and volume are driving strong directional bias.

The optional dynamic color ramp (green→yellow→red) immediately flags when average bar size is unusually small or large versus its own 24h history.

Customize & Stay Flexible

Timeframes: Works on any intraday chart—from 1-minute scalping to 4-hour swing setups—because it always looks back exactly 24 hours.

Toggles:

Show or hide the Volatility and Avg-Candle cells to keep your screen uncluttered.

Turn on the dynamic color ramp only when you want that extra visual cue.

Alerts: Built-in alerts fire automatically at meaningful thresholds (Volatility ≥ 8 or ≤ 3), so you’ll never miss regime shifts, even if you step away.

Real-World Applications

Risk Management: Automatically adjust your stop-loss distances or position sizing based on the current volatility band.

Strategy Selection: Flip between range-trading and momentum strategies as the volatility regime changes.

Session Analysis: Pinpoint when during the day volatility typically ramps—perfect for doorway sessions like London opening or the US midday news spikes.

Bottom line: the Frahm Factor gives you one compact dashboard to see the pulse of the market—so you can make choices with conviction, dial your risk in real time, and never be caught off guard by sudden volatility shifts.

Logic Behind the Frahm Factor Indicator

24-Hour Rolling Window

On every intraday bar, we append that bar’s True Range (TR) and timestamp to two arrays.

We then prune any entries older than 24 hours, so the arrays always reflect exactly the last day of data.

Volatility Score (1–10)

We count how many of those 24 h TR values are less than or equal to the current bar’s TR.

Dividing by the total array size gives a percentile (0–1), which we scale and round into a 1–10 score.

Average Candle Size (ticks)

We sum all TR values in the same 24 h window, divide by array length to get the mean TR, then convert that price range into ticks.

Optionally, a green→yellow→red ramp highlights when average bar size is unusually small, medium or large versus its own 24 h history.

Color & Alerts

The Volatility cell flips green (1–3), yellow (4–6) or red (7–10) so you see regime shifts at a glance.

Built-in alertcondition calls fire when the score crosses your high (≥ 8) or low (≤ 3) thresholds.

Modularity

Everything—table location, which cells to show, dynamic coloring—is controlled by simple toggles, so you can strip it back or layer on extra visual cues as needed.

That’s the full recipe: a true 24 h look-back, a percentile-ranked volatility gauge, and a mean-bar-size meter, all wrapped into one compact dashboard.

Volume PercentileThis Pine Script indicator highlights bars where the current volume exceeds a configurable percentile threshold (e.g., 80th percentile) based on a rolling window of historical volume data.

🔍 Key Features:

Calculates a user-defined volume percentile (e.g., 75th, 80th, 90th) over a rolling window.

Marks candles where current volume is higher than the selected percentile.

Helps detect volume spikes, breakouts, or unusual activity.

Works directly on the main chart window for easier analysis.

🛠️ Inputs:

Window Length: Number of bars used to calculate the percentile (default = 20).

Percentile: The percentile threshold to trigger a high-volume signal (default = 80).

🖥️ Visualization:

Displays a red triangle marker below bars with volume above the selected percentile.

Double Top/Bottom DetectorDouble Top/Bottom Detector Indicator Description

Overview

The Double Top/Bottom Detector is a technical analysis tool designed to automatically identify and label potential double top and double bottom patterns on price charts. By combining pivot point detection with configurable height tolerance and pullback depth criteria, this indicator helps traders visually spot possible trend reversal zones without manual drawing or guesswork.

Key Features

• Pivot Point Identification

The indicator uses a symmetric window approach to find true highs and lows. A pivot high is confirmed only when a bar’s high exceeds the highs of a specified number of bars both before and after it. Likewise, a pivot low is established when a bar’s low is the lowest in its surrounding window.

• Double Top and Double Bottom Detection

– Height Tolerance: Ensures that the two pivot points forming the pattern are within a user-defined percentage of each other.

– Pullback Depth: Measures the drop (for a double top) or the rise (for a double bottom) between the two pivot points and confirms that it meets a minimum percentage threshold.

• Automatic Drawing and Labeling

When a valid double top is detected, a red line connects the two pivot highs and a “Double Top” label is centered above the line. For a double bottom, a green line connects the two pivot lows and a “Double Bottom” label appears below the midpoint.

• Pivot Visualization for Debugging

Small red and green triangles mark every detected pivot high and pivot low on the chart, making it easy to verify and fine-tune settings.

Parameters

Height Tolerance (%) – The maximum allowable percentage difference between the two pivot heights (default 2.0).

Pullback Minimum (%) – The minimum required percentage pullback (for tops) or rebound (for bottoms) between the two pivots (default 5.0).

Pivot Lookback – The number of bars to look back and forward for validating pivot points (default 5).

Window Length – The number of bars over which to compute pullback extrema, equal to twice the pivot lookback plus one (default derived from pivot lookback).

Usage Instructions

1. Copy the Pine Script code into TradingView’s editor and select version 6.

2. Adjust the parameters based on the asset’s volatility and timeframe. A larger lookback window yields fewer but more reliable pivots; tighter height tolerance produces more precise pattern matches.

3. Observe the chart for red and green triangles marking pivot highs and lows. When two qualifying pivots occur, the indicator draws a connecting line and displays a descriptive label.

4. To extend the number of visible historical lines and labels, increase the max\_lines\_count and max\_labels\_count settings in the indicator declaration.

Customization Ideas

• Add volume or moving average filters to reduce false signals.

• Encapsulate pivot logic into reusable functions for cleaner code.

• Incorporate alert conditions to receive notifications when new double top or bottom patterns form.

This indicator is well suited for medium- to long-term analysis and can be combined with risk management rules to enhance decision making.

Volume-Weighted Pivot BandsThe Volume-Weighted Pivot Bands are meant to be a dynamic, rolling pivot system designed to provide traders with responsive support and resistance levels that adapt to both price volatility and volume participation. Unlike traditional daily pivot levels, this tool recalculates levels bar-by-bar using a rolling window of volume-weighted averages, making it highly relevant for intraday traders, scalpers, swing traders, and algorithmic systems alike.

-- What This Indicator Does --

This tool calculates a rolling VWAP-based pivot level, and surrounds that central pivot with up to five upper bands (R1–R5) and five lower bands (S1–S5). These act as dynamic zones of potential resistance (R) and support (S), adapting in real time to price and volume changes.

Rather than relying on static session or daily data, this indicator provides continually evolving levels, offering more relevant levels during sideways action, trending periods, and breakout conditions.

-- How the Bands Are Calculated --

Pivot (VWAP Pivot):

The core of this system is a rolling Volume-Weighted Average Price, calculated over a user-defined window (default 20 bars). This ensures that each bar’s price impact is weighted by its volume, giving a more accurate view of fair value during the selected lookback.

Volume-Weighted Range (VW Range):

The highest high and lowest low over the same window are used to calculate the volatility range — this acts as a spread factor.

Support & Resistance Bands (S1–S5, R1–R5):

The bands are offset above and below the pivot using multiples of the VW Range:

R1 = Pivot + (VW Range × multiplier)

R2 = R1 + (VW Range × multiplier)

R3 = R2 + (VW Range x multiplier)

...

S1 = Pivot − (VW Range × multiplier)

S2 = S1 − (VW Range × multiplier)

S3 = S2 - (VW Range x multiplier)

...

You can control the multiplier manually (default is 0.25), to widen or tighten band spacing.

Smoothing (Optional):

To prevent erratic movements, you can optionally toggle on/off a simple moving average to the pivot line (default length = 20), providing a smoother trend base for the bands.

-- How to Use It --

This indicator can be used for:

Support and resistance identification:

Price often reacts to R1/S1, and the outer bands (R4/R5 or S4/S5) act as overshoot zones or strong reversal areas.

Trend context:

If price is respecting upper bands (R2–R3), the trend is likely bullish. If price is pressing into S3 or lower, it may indicate sustained selling pressure or a breakdown.

Volatility framing:

The distance between bands adjusts based on price range over the rolling window. In tighter markets, the bands compress — in volatile moves, they expand. This makes the indicator self-adaptive.

Mean reversion trades:

A move into R4/R5 or S4/S5 without continuation can be a sign of exhaustion — potential for reversal toward the pivot.

Alerting:

Built-in alerts are available for crosses of all major bands (R1–R5, S1–S5), enabling trade automation or scalp alerts with ease.

-- Visual Features --

Fuchsia Lines: Mark all Resistance (R1–R5) levels.

Lime Lines: Mark all Support (S1–S5) levels.

Gray Circle Line: Marks the rolling pivot (VWAP-based).

-- Customizable Settings --

Rolling Length: Number of bars used to calculate VWAP and VW Range.

Multiplier: Controls how wide the bands are spaced.

Smooth Pivot: Toggle on/off to smooth the central pivot.

Pivot Smoothing Length: Controls how many bars to average when smoothing is enabled.

Offset: Visually shift all bands forward/backward in time.

-- Why Use This Over Standard Pivots? --

Traditional pivots are based on previous session data and remain fixed. That’s useful for static setups, but may become irrelevant as price action evolves. In contrast:

This system updates every bar, adjusting to current price behavior.

It includes volume — a key feature missing from most static pivots.

It shows multiple bands, giving a full view of compression, breakout potential, or trend exhaustion.

-- Who Is This For? --

This tool is ideal for:

Day traders & scalpers who need relevant intraday levels.

Swing traders looking for evolving areas of confluence.

Algorithmic/systematic traders who rely on quantifiable, volume-aware support/resistance.

Traders on all assets: works on crypto, stocks, futures, forex — any chart that has volume.

[blackcat] L3 Trendmaster XOVERVIEW

The L3 Trendmaster X is an advanced trend-following indicator meticulously crafted to assist traders in identifying and capitalizing on market trends. This sophisticated tool integrates multiple technical factors, including Average True Range (ATR), volume dynamics, and price spreads, to deliver precise buy and sell signals. By plotting dynamic trend bands directly onto the chart, it offers a comprehensive visualization of potential trend directions, enabling traders to make informed decisions swiftly and confidently 📊↗️.

FEATURES

Customizable Input Parameters: Tailor the indicator to match your specific trading needs with adjustable settings:

Trendmaster X Multiplier: Controls the sensitivity of the ATR-based levels.

Trendmaster X Period: Defines the period over which the ATR is calculated.

Window Length: Specifies the length of the moving window for standard deviation calculations.

Volume Averaging Length: Determines how many periods are considered for averaging volume.

Volatility Factor: Adjusts the impact of volatility on the trend bands.

Core Technical Metrics:

Dynamic Range: Measures the range between high and low prices within each bar.

Candle Body Size: Evaluates the difference between open and close prices.

Volume Average: Assesses the cumulative On-Balance Volume relative to the dynamic range.

Price Spread: Computes the standard deviation of the price ranges over a specified window.

Volatility Factor: Incorporates volatility into the calculation of trend bands.

Advanced Trend Bands Calculation:

Upper Level: Represents potential resistance levels derived from the ATR multiplier.

Lower Level: Indicates possible support levels using the same ATR multiplier.

High Band and Low Band: Dynamically adjust to reflect current trend directions, offering a clear view of market sentiment.

Visual Representation:

Plots distinct green and red trend lines representing bullish and bearish trends respectively.

Fills the area between these trend lines and the middle line for enhanced visibility.

Displays clear buy ('B') and sell ('S') labels on the chart for immediate recognition of trading opportunities 🏷️.

Alert System:

Generates real-time alerts when buy or sell conditions are triggered, ensuring timely action.

Allows customization of alert messages and frequencies to align with individual trading strategies 🔔.

HOW TO USE

Adding the Indicator:

Open your TradingView platform and navigate to the "Indicators" section.

Search for " L3 Trendmaster X" and add it to your chart.

Adjusting Settings:

Fine-tune the input parameters according to your preferences and trading style.

For example, increase the Trendmaster X Multiplier for higher sensitivity during volatile markets.

Decrease the Window Length for shorter-term trend analysis.

Monitoring Trends:

Observe the plotted trend bands and labels on the chart.

Look for buy ('B') labels at potential support levels and sell ('S') labels at resistance levels.

Setting Up Alerts:

Configure alerts based on the generated buy and sell signals.

Choose notification methods (e.g., email, SMS) and set alert frequencies to stay updated without constant monitoring 📲.

Combining with Other Tools:

Integrate the Trendmaster X with other technical indicators like Moving Averages or RSI for confirmation.

Utilize fundamental analysis alongside the indicator for a holistic approach to trading.

Backtesting and Optimization:

Conduct thorough backtests on historical data to evaluate performance.

Optimize parameters based on backtest results to enhance accuracy and reliability.

Real-Time Application:

Apply the optimized settings to live charts and monitor real-time signals.

Execute trades based on confirmed signals while considering risk management principles.

LIMITATIONS

Market Conditions: The indicator might produce false signals in highly volatile or sideways-trending markets due to increased noise and lack of clear direction 🌪️.

Complementary Analysis: Traders should use this indicator in conjunction with other analytical tools to validate signals and reduce the likelihood of false positives.

Asset-Specific Performance: Effectiveness can vary across different assets and timeframes; therefore, testing on diverse instruments is recommended.

NOTES

Data Requirements: Ensure adequate historical data availability for accurate calculations and reliable signal generation.

Demo Testing: Thoroughly test the indicator on demo accounts before deploying it in live trading environments to understand its behavior under various market scenarios.

Parameter Customization: Regularly review and adjust parameters based on evolving market conditions and personal trading objectives.

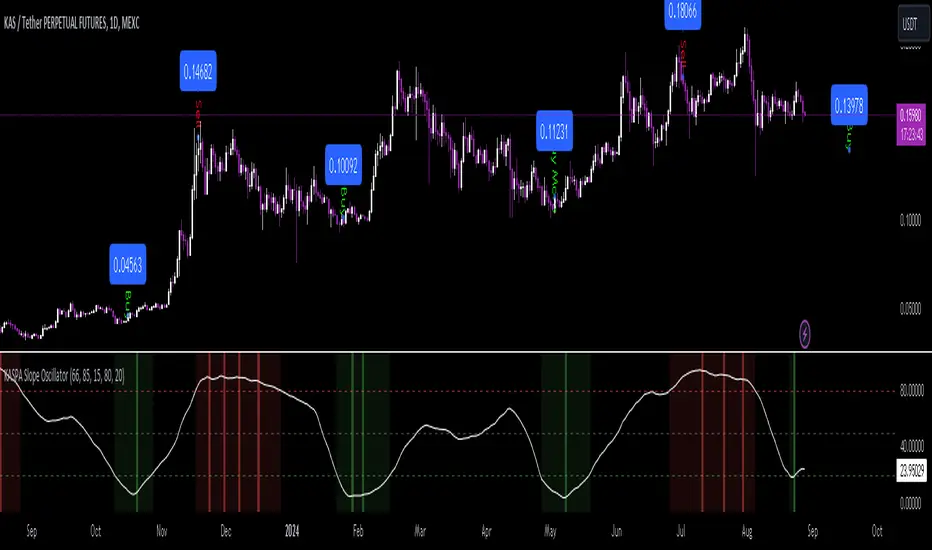

KASPA Slope OscillatorKASPA Slope Oscillator for analyzing KASPA on the 1D (daily) chart.

The indicator is plotted in a separate pane below the price chart and uses a mathematical approach to calculate and visualize the momentum or "slope" of KASPA's price movements.

Input Parameters:

Slope Window (days):

Defines the period (66 days by default) over which the slope is calculated.

Normalization Window (days):

The window size (85 days) for normalizing the slope values between 0 and 100.

Smoothing Period:

The number of days (15 days) over which the slope values are smoothed to reduce noise.

Overbought and Oversold Levels:

Threshold levels set at 80 (overbought) and 20 (oversold), respectively.

Calculation of the Slope:

Logarithmic Price Calculation:

Converts the close price of KASPA into a logarithmic scale to account for exponential growth or decay.

Rolling Slope:

Computes the rate of change in logarithmic prices over the defined slope window.

Normalization:

The slope is normalized between 0 and 100, allowing easier identification of extreme values.

Smoothing and Visualization:

Smoothing the Slope:

A Simple Moving Average (SMA) is applied to the normalized slope for the specified smoothing period.

Plotting the Oscillator:

The smoothed slope is plotted on the oscillator chart. Horizontal lines indicate overbought (80), oversold (20), and the mid-level (50).

Background Color Indications:

Background colors (red or green) indicate when the slope crosses above the overbought or below the oversold levels, respectively, signaling potential buy or sell conditions.

Detection of Local Maxima and Minima:

The code identifies local peaks (maxima) above the overbought level and troughs (minima) below the oversold level.

Vertical background lines are highlighted in red or green at these points, signaling potential reversals.

Short Summary:

The oscillator line fluctuates between 0 and 100, representing the normalized momentum of the price.

Red background areas indicate periods when the oscillator is above the overbought level (80), suggesting a potential overbought condition or a sell signal.

Green background areas indicate periods when the oscillator is below the oversold level (20), suggesting a potential oversold condition or a buy signal.

The vertical lines on the background mark local maxima and minima where price reversals may occur.

(I also want to thank @ForgoWork for optimizing visuality and cleaning up the source code)

Option Pair ZigzagOptions Pair Zigzag:

Though we can split the chart window and view multiple charts, this indicator is useful when we view options charts.

How this indicator works:

The indicator works in non-overlay mode.

The indicator will find other option pair symbol and load it’s chart in indicator window. It will also draw a zigzag on both the charts. It will also fetch the SPOT symbol and display SPOT Close price of latest candle.

Useful information:

A. Support resistance: Higher High (HH) and Lower Low (LL) markings can be treated as strong support and or resistance and LH, HL markings can be treated as weak support and or resistance.

B. Trend identification: Easy identification of trend based on trend lines and trend markings i.e. Higher High (HH), Lower Low (LL), Lower High (LH), Higher Low (HL)

C. Use of Rate of change (ROC )– Labels drawn on swing points are equipped with ROC% between swing points. ROC% between Call and Put option charts can be compared and used to identify strong and weak moves.

Example:

1. User loads a call option chart of ‘NIFTY240620C23500’ (NIFTY 50 INDEX OPTIONS 20 JUN 2024 CALL 23500)

2. Since user has selected CALL Option, Indicator rules/logic will find PUT Option symbol of same strike and expiry

3. PUT Option chart would then shown in the indicator window

4. Draw zigzag on both the charts

5. Plot labels on both the charts

6. Labels are equipped with a tooltip showing rate of change between 2 pivot points

Input Parameters:

Left bars – Parameter required for plotting zigzag

Right bars – Parameter required for plotting zigzag

Plot HHLL Labels – Enable/disable plotting of labels

Use cases:

Refer to chart snapshots:

1. Buy Call Option or Sell Put Option - How one can trade on formation of a consolidation range

2. Breakdown of Swing structure - One can observe Swing structure (Zigzag) formed on a SPOT chart and trade on break of swing structure

3. Triangle formation - Observe the patterns formed on the SPOT chart and trade either Call or Put options. Example snapshot shows trade based on triangle pattern

Chart Snapshot:

One can split chart window and load base symbol chart which will help to review bases symbol and options chart at the same time.

Buy Call Option or Sell Put Option

Breakdown of Swing structure

Triangle formation

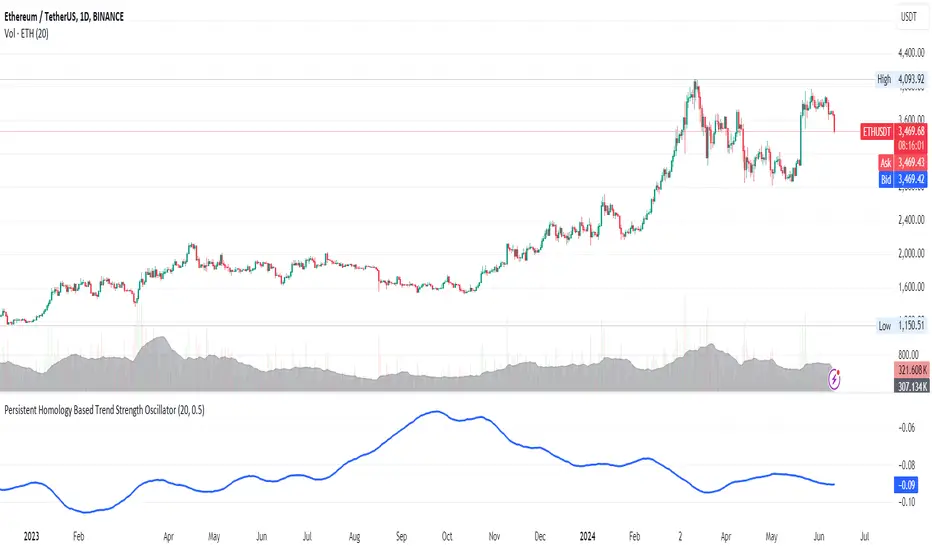

Persistent Homology Based Trend Strength OscillatorPersistent Homology Based Trend Strength Oscillator

The Persistent Homology Based Trend Strength Oscillator is a unique and powerful tool designed to measure the persistence of market trends over a specified rolling window. By applying the principles of persistent homology, this indicator provides traders with valuable insights into the strength and stability of uptrends and downtrends, helping to inform better trading decisions.

What Makes This Indicator Original?

This indicator's originality lies in its application of persistent homology , a method from topological data analysis, to financial markets. Persistent homology examines the shape and features of data across multiple scales, identifying patterns that persist as the scale changes. By adapting this concept, the oscillator tracks the persistence of uptrends and downtrends in price data, offering a novel approach to trend analysis.

Concepts Underlying the Calculations:

Persistent Homology: This method identifies features such as clusters, holes, and voids that persist as the scale changes. In the context of this indicator, it tracks the duration and stability of price trends.

Rolling Window Analysis: The oscillator uses a specified window size to calculate the average length of uptrends and downtrends, providing a dynamic view of trend persistence over time.

Threshold-Based Trend Identification: It differentiates between uptrends and downtrends based on specified thresholds for price changes, ensuring precision in trend detection.

How It Works:

The oscillator monitors consecutive changes in closing prices to identify uptrends and downtrends.

An uptrend is detected when the closing price increase exceeds a specified positive threshold.

A downtrend is detected when the closing price decrease exceeds a specified negative threshold.

The lengths of these trends are recorded and averaged over the chosen window size.

The Trend Persistence Index is calculated as the difference between the average uptrend length and the average downtrend length, providing a measure of trend persistence.

How Traders Can Use It:

Identify Trend Strength: The Trend Persistence Index offers a clear measure of the strength and stability of uptrends and downtrends. A higher value indicates stronger and more persistent uptrends, while a lower value suggests stronger and more persistent downtrends.

Spot Trend Reversals: Significant shifts in the Trend Persistence Index can signal potential trend reversals. For instance, a transition from positive to negative values might indicate a shift from an uptrend to a downtrend.

Confirm Trends: Use the Trend Persistence Index alongside other technical indicators to confirm the strength and duration of trends, enhancing the accuracy of your trading signals.

Manage Risk: Understanding trend persistence can help traders manage risk by identifying periods of high trend stability versus periods of potential volatility. This can be crucial for timing entries and exits.

Example Usage:

Default Settings: Start with the default settings to get a feel for the oscillator’s behavior. Observe how the Trend Persistence Index reacts to different market conditions.

Adjust Thresholds: Fine-tune the positive and negative thresholds based on the asset's volatility to improve trend detection accuracy.

Combine with Other Indicators: Use the Persistent Homology Based Trend Strength Oscillator in conjunction with other technical indicators such as moving averages, RSI, or MACD for a comprehensive analysis.

Backtesting: Conduct backtesting to see how the oscillator would have performed in past market conditions, helping you to refine your trading strategy.

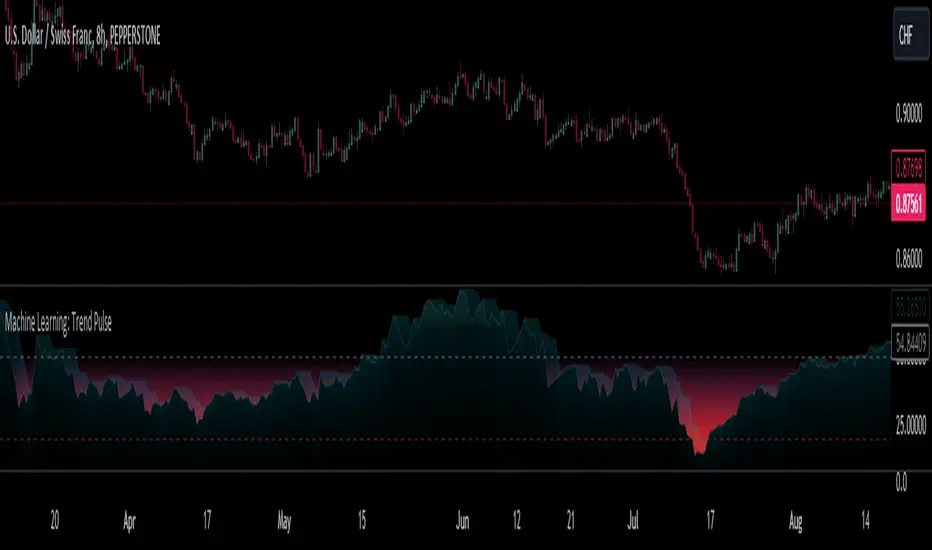

Machine Learning: Trend Pulse⚠️❗ Important Limitations: Due to the way this script is designed, it operates specifically under certain conditions:

Stocks & Forex : Only compatible with timeframes of 8 hours and above ⏰

Crypto : Only works with timeframes starting from 4 hours and higher ⏰

❗Please note that the script will not work on lower timeframes.❗

Feature Extraction : It begins by identifying a window of past price changes. Think of this as capturing the "mood" of the market over a certain period.

Distance Calculation : For each historical data point, it computes a distance to the current window. This distance measures how similar past and present market conditions are. The smaller the distance, the more similar they are.

Neighbor Selection : From these, it selects 'k' closest neighbors. The variable 'k' is a user-defined parameter indicating how many of the closest historical points to consider.

Price Estimation : It then takes the average price of these 'k' neighbors to generate a forecast for the next stock price.

Z-Score Scaling: Lastly, this forecast is normalized using the Z-score to make it more robust and comparable over time.

Inputs:

histCap (Historical Cap) : histCap limits the number of past bars the script will consider. Think of it as setting the "memory" of model—how far back in time it should look.

sampleSpeed (Sampling Rate) : sampleSpeed is like a time-saving shortcut, allowing the script to skip bars and only sample data points at certain intervals. This makes the process faster but could potentially miss some nuances in the data.

winSpan (Window Size) : This is the size of the "snapshot" of market data the script will look at each time. The window size sets how many bars the algorithm will include when it's measuring how "similar" the current market conditions are to past conditions.

All these variables help to simplify and streamline the k-NN model, making it workable within limitations. You could see them as tuning knobs, letting you balance between computational efficiency and predictive accuracy.

Relative slopeRelative slope metric

Description:

I was in need to create a simple, naive and elegant metric that was able to tell how strong is the trend in a given rolling window. While abstaining from using more complicated and arguably more precise approaches, I’ve decided to use Linearly Weighted Linear Regression slope for this goal. Outright values are useful, but the problem was that I wasn’t able to use it in comparative analysis, i.e between different assets & different resolutions & different window sizes, because obviously the outputs are scale-variant.

Here is the asset-agnostic, resolution-agnostic and window size agnostic version of the metric.

I made it asset agnostic & resolution agnostic by including spread information to the formula. In our case it's weighted stdev over differenced data (otherwise we contaminate the spread with the trend info). And I made it window size agnostic by adding a non-linear relation of length to the output, so finally it will be aprox in (-1, 1) interval, by taking square root of length, nothing fancy. All these / 2 and * 2 in unexpected places all around the formula help us to return the data to it’s natural scale while keeping the transformations in place.

Peace TV