Implied Range from Options [SS]I have been promising to post this for a while, but I just needed to make sure that a) there were no similar indicators already available and b) make it a bit more user friendly.

So here it is, a basic indicator that will display the implied range from options.

In addition to displaying the implied range from options, it will provide some secondary information to help add context to the implied range. Those are shown in the chart below:

The indicator will list various precents at each point to the upside and to the downside. This is the percent move required, based on the current close price, to obtain any point in the implied move range.

In addition, the indicator will display the average move from open to high and open to low over a user defined period (default to 14 candle period) as well as the previous open to high and open to low move from the previous day.

This is to give you context of:

a) How much of a % increase or decrease is required to reach the implied ranges; and

b) How does the implied range compare to the ticker's average moves.

An increased implied range that exceeds the ticker's average move can alert you that the market is pricing in an above average move. This can be helpful and alert you to potential news releases or other fundamental things that have the potential to move the market.

How to Use the indicator:

So unfortunately, this indicator requires a bit of manual input. I was going to do an auto IV calculcation using Black-Scholes Model but just to be more rigorous in accuracy, I decided to, for now, leave it at a manual input. So when you launch the settings menu, this is what you will see:

You can collect all of this required information from your broker. Inversely, you can collect it online for free from various services such as Barchart or COBE's exchange website. The easiest way is to just pull it from your broker though.

Make sure, if you are doing weekly options to see the weekly range, you set the timeframe to 1 week. The timeframe function will calculate the average move over the desired timeframe length. So if you are doing a 0 dte for the next day, you want to see the intra-day range and will select the 1 day timeframe. It will then present to you the range averages and information on the daily timeframe for you to compare to the implied options range.

Same for the weekly, monthly, yearly, etc.

Additional options:

The indicator provides the midline average and midway points, to add static targets if you are trading the implied range.

These can be toggled on or off in the settings menu:

As well, as you can see, you can also toggle off the range labels.

There is also an offset option. This allows you to extend the range into the future:

Simply select how many candles you would like to plot the range in advance.

Closing remarks

That is the indicator. Its very simple, but it is handy. I was never one to pay attention to option pricing data, but I have been plotting it out daily and weekly these past few weeks and it does add a bit of context in terms of what the market is thinking. So I do recommend actually adding it to your repertoire of analyses going into the weeks and months, and really just paying attention to how the average ranges compare to what the market is pricing in.

One quick suggestion, select the strike price that aligns with the closing price of the ticker. This gives you a better representation of the range.

Safe trades everyone and leave your comments, questions and suggestions below!

"weekly" için komut dosyalarını ara

Buying Selling Volume StrategyFirst I would like to give the original credit and thanks to @ceyhun for his amazing volume script.

The way I decided to convert it into a strategy is divided into multiple types.

First, I decided in order to smooth out the values and make it more accurate to adapt the values to multiple timeframes.

After that I took the initial values from the buyers and sellers , and made a rest operation between them to have a flat difference between the power of both sides.

WIth that later on I decided to to apply a volatility filter,in this case bollinger bands, in order to find out potential leading trends.

At the same time in order to filter even more, I decided to make use as well for weekly VWAP values of the asset used.

Lastly I added a dynamic risk management into it , based on the ATR Daily values of the asset values.

As for the rules used, for example for long, I am looking that the price of the asset is above the weekly VWAP, after that I am checking that the MTF volume rest operation is both bullish and above the upper side of the bollinger.

For short we would want the asset to be below the weekly VWAP, and the volume to be bearish and above the upper side of bollinger.

The exit is either based on daily ATR values multipliers, or if we have a reverse condition.

If you have any questions, please let me know !

Buy/Sell EMA CandleThis indicator is designed to display various technical indicators, candle patterns, and trend directions on a price chart. Let's break down the code and explain its different sections:

Exponential Moving Averages (EMA):

The code calculates and plots five EMAs of different lengths (13, 21, 55, 90, and 200) on the price chart. These EMAs are used to identify trends and potential crossovers.

Engulfing Candle Patterns:

The code identifies and highlights potential bullish and bearish engulfing candle patterns. It checks if the current candle's body size is larger than the combined body sizes of the previous and subsequent four candles. If this condition is met, it marks the pattern on the chart.

s3.tradingview.com

EMA Crossovers:

The code identifies and highlights points where the shorter EMA (ema1) crosses above or below the longer EMA (ema2). It plots circles to indicate these crossover points.

Candle Direction and RSI Trend:

The code determines the trend direction of the last candle based on whether it closed higher or lower than its open price. It also calculates the RSI (Relative Strength Index) and determines its trend direction (overbought, oversold, or neutral) based on predefined thresholds.

s3.tradingview.com

Table Display:

The code creates a table displaying trend directions for different timeframes (monthly, weekly, daily, 4-hour, and 1-hour) for candle direction and RSI trends. The trends are labeled with "L" for long, "S" for short, and "N/A" for not applicable.

High Volume Bars (HVB):

The code identifies and colors bars with above-average volume as either bullish or bearish based on whether the price closed higher or lower than it opened. The color and conditions for high volume bars can be customized.

s3.tradingview.com

Doji Candle Pattern:

The code identifies and marks doji candle patterns, where the open and close prices are very close to each other within a certain percentage of the candle's high-low range.

RSI-Based Candle Coloring:

The code adjusts the color of the candles based on the RSI value. If the RSI value is above the overbought threshold or below the oversold threshold, the candles are colored yellow.

Usage and Interpretation:

Traders can use this indicator to identify potential trend changes based on EMA crossovers and candle patterns like engulfing and doji.

The RSI trend direction can provide additional insight into potential overbought or oversold conditions.

High volume bars can indicate potential price reversals or continuation patterns.

The table provides an overview of trend directions on different timeframes for both candle direction and RSI trends.

Keep in mind that this is a complex indicator with multiple features. Users should carefully evaluate its performance and consider combining it with other indicators and analysis methods for more accurate trading decisions.

The table is designed to provide a consolidated view of trend directions and other indicators across multiple timeframes. It is displayed on the chart and organized into rows and columns. Each row corresponds to a specific aspect of analysis, and each column corresponds to a different timeframe.

Here's a breakdown of the components of the table:

Row 1: Separation.

Row 2 (Header Row): This row contains the headers for the columns. The headers represent the different timeframes being analyzed, such as Monthly (M), Weekly (W), Daily (D), 4-hour (4h), and 1-hour (1h).

Row 3 (Content Row): This row contains labels indicating the types of information being displayed in the columns. The labels include "T" for Trend, "C" for Current Candle, and "R" for RSI Trend.

Row 4 and Onwards: These rows display the actual data for each aspect of analysis across different timeframes.

For each aspect of analysis (Trend, Current Candle, RSI Trend), the corresponding rows display the following information:

Monthly (M): The trend direction for the given aspect on the monthly timeframe.

Weekly (W): The trend direction for the given aspect on the weekly timeframe.

Daily (D): The trend direction for the given aspect on the daily timeframe.

4-hour (4h): The trend direction for the given aspect on the 4-hour timeframe.

1-hour (1h): The trend direction for the given aspect on the 1-hour timeframe.

The trend directions are represented by labels such as "L" for Long, "S" for Short, or "N/A" for Not Applicable.

The table's purpose is to provide a quick overview of trend directions and related information across multiple timeframes, aiding traders in making informed decisions based on the analysis of trend changes and other indicators.

MACDh with divergences & impulse system (overlayed on prices)-----------------------------------------------------------------

General Description:

This indicator ( the one on the top panel above ) consists on some lines, arrows and labels drawn over the price bars/candles indicating the detection of regular divergences between price and the classic MACD histogram (shown on the low panel). This script is special because it can be adjusted to fit several criteria when trading divergences filtering them according to the "height" and "width" of the patterns. The script also includes the "extra features" Impulse System and Keltner Channels, which you will hardly find anywhere else in similar classic MACD histogram divergence indicators.

The indicator helps to find trend reversals, and it works on any market, any instrument, any timeframe, and any market condition (except against really strong trends that do not show any other sign of reversion yet).

Please take on consideration that divergences should be taken with caution.

-----------------------------------------------------------------

Definition of classic Bullish and Bearish divergences:

* Bearish divergences occur in uptrends identifying market tops. A classical or regular bearish divergence occurs when prices reach a new high and then pull back, with an oscillator (MACD histogram in this case) dropping below its zero line. Prices stabilize and rally to a higher high, but the oscillator reaches a lower peak than it did on a previous rally.

In the chart above (weekly charts of NKE, Nike, Inc.), in area X (around August 2021), NKE rallied to a new bull market high and MACD-Histogram rallied with it, rising above its previous peak and showing that bulls were extremely strong. In area Y, MACD-H fell below its centerline and at the same time prices punched below the zone between the two moving averages. In area Z, NKE rallied to a new bull market high, but the rally of MACD-H was feeble, reflecting the bulls’ weakness. Its downtick from peak Z completed a bearish divergence, giving a strong sell signal and auguring a nasty bear market.

* Bullish divergences , in the other hand, occur towards the ends of downtrends identifying market bottoms. A classical (also called regular) bullish divergence occurs when prices and an oscillator (MACD histogram in this case) both fall to a new low, rally, with the oscillator rising above its zero line, then both fall again. This time, prices drop to a lower low, but the oscillator traces a higher bottom than during its previous decline.

In the example in the chart above (weekly charts of NKE, Nike, Inc.), you see a bearish divergence that signaled the October 2022 bear market bottom, giving a strong buy signal right near the lows. In area A, NKE (weekly charts) appeared in a free fall. The record low A of MACD-H indicated that bears were extremely strong. In area B, MACD-H rallied above its centerline. Notice the brief rally of prices at that moment. In area C, NKE slid to a new bear market low, but MACD-H traced a much more shallow low. Its uptick completed a bullish divergence, giving a strong buy signal.

-----------------------------------------------------------------

Some cool features included in this indicator:

1. This indicator also includes the “ Impulse System ”. The Impulse System is based on two indicators, a 13-day exponential moving average and the MACD-Histogram, and identifies inflection points where a trend speeds up or slows down. The moving average identifies the trend, while the MACD-Histogram measures momentum. This unique indicator combination is color coded into the price bars for easy reference.

Calculation:

Green Price Bar: (13-period EMA > previous 13-period EMA) and

(MACD-Histogram > previous period's MACD-Histogram)

Red Price Bar: (13-period EMA < previous 13-period EMA) and

(MACD-Histogram < previous period's MACD-Histogram)

Price bars are colored blue when conditions for a Red Price Bar or Green Price Bar are not met. The MACD-Histogram is based on MACD(12,26,9).

The Impulse System works more like a censorship system. Green price bars show that the bulls are in control of both trend and momentum as both the 13-day EMA and MACD-Histogram are rising (you don't have permission to sell). A red price bar indicates that the bears have taken control because the 13-day EMA and MACD Histogram are falling (you don't have permission to buy). A blue price bar indicates mixed technical signals, with neither buying nor selling pressure predominating (either both buying or selling are permitted).

2. Another "extra feature" included here is the " Keltner Channels ". Keltner Channels are volatility-based envelopes set above and below an exponential moving average.

3. It were also included a couple of EMAs.

Everything can be removed from the chart any time.

-----------------------------------------------------------------

Options/adjustments for this indicator:

*Horizontal Distance (width) between two tops/bottoms criteria.

Refers to the horizontal distance between the MACH histogram peaks involved in the divergence

*Height of tops/bottoms criteria (for Histogram).

Refers to the difference/relation/vertical distance between the MACH HISTOGRAM peaks involved in the divergence: 1st Histogram Peak is X times the 2nd.

*Height/Vertical deviation of tops/bottoms criteria (for Price).

Deviation refers to the difference/relation/vertical distance between the PRICE peaks involved in the divergence.

*Plot Regular Bullish Divergences?.

*Plot Regular Bearish Divergences?.

*Delete Previous Cancelled Divergences?.

*Shows a pair of EMAs.

*Shows Keltner Channels (using ATR)

Keltner Channels are volatility-based envelopes set above and below an exponential moving average.

*This indicator also has the option to show the Impulse System over the price bars/candles.

MACDh with divergences & impulse system-----------------------------------------------------------------

General Description:

This indicator ( the one on the low panel ) is a classic MACD that also shows regular divergences between its histogram and the prices. This script is special because it can be adjusted to fit several criteria when trading divergences filtering them according to the "height" and "width" of the patterns. The script also includes the "extra feature" Impulse System, which you will hardly find anywhere else in similar classic MACD histogram divergence indicators.

The indicator helps to find trend reversals, and it works on any market, any instrument, any timeframe, and any market condition (except against really strong trends that do not show any other sign of reversion yet).

Please take on consideration that divergences should be taken with caution.

-----------------------------------------------------------------

Definition of classic Bullish and Bearish divergences:

* Bearish divergences occur in uptrends identifying market tops. A classical or regular bearish divergence occurs when prices reach a new high and then pull back, with an oscillator (MACD histogram in this case) dropping below its zero line. Prices stabilize and rally to a higher high, but the oscillator reaches a lower peak than it did on a previous rally.

In the chart above (weekly charts of NKE, Nike, Inc.), in area X (around August 2021), NKE rallied to a new bull market high and MACD-Histogram rallied with it, rising above its previous peak and showing that bulls were extremely strong. In area Y, MACD-H fell below its centerline and at the same time prices punched below the zone between the two moving averages. In area Z, NKE rallied to a new bull market high, but the rally of MACD-H was feeble, reflecting the bulls’ weakness. Its downtick from peak Z completed a bearish divergence, giving a strong sell signal and auguring a nasty bear market.

* Bullish divergences , in the other hand, occur towards the ends of downtrends identifying market bottoms. A classical (also called regular) bullish divergence occurs when prices and an oscillator (MACD histogram in this case) both fall to a new low, rally, with the oscillator rising above its zero line, then both fall again. This time, prices drop to a lower low, but the oscillator traces a higher bottom than during its previous decline.

In the example in the chart above (weekly charts of NKE, Nike, Inc.), you see a bearish divergence that signaled the October 2022 bear market bottom, giving a strong buy signal right near the lows. In area A, NKE (weekly charts) appeared in a free fall. The record low A of MACD-H indicated that bears were extremely strong. In area B, MACD-H rallied above its centerline. Notice the brief rally of prices at that moment. In area C, NKE slid to a new bear market low, but MACD-H traced a much more shallow low. Its uptick completed a bullish divergence, giving a strong buy signal.

-----------------------------------------------------------------

Extra feature: Impulse System

This indicator also includes the “ Impulse System ”. The Impulse System is based on two indicators, a 13-day exponential moving average and the MACD-Histogram, and identifies inflection points where a trend speeds up or slows down. The moving average identifies the trend, while the MACD-Histogram measures momentum. This unique indicator combination is color coded into the price bars or macd histogram bars for easy reference.

Calculation:

Green Price Bar: (13-period EMA > previous 13-period EMA) and

(MACD-Histogram > previous period's MACD-Histogram)

Red Price Bar: (13-period EMA < previous 13-period EMA) and

(MACD-Histogram < previous period's MACD-Histogram)

Histogram bars are colored blue when conditions for a Red Histogram Bar or Green Histogram Bar are not met. The MACD-Histogram is based on MACD(12,26,9).

The Impulse System works more like a censorship system. Green histogram bars show that the bulls are in control of both trend and momentum as both the 13-day EMA and MACD-Histogram are rising (you don't have permission to sell). A red histogram bar indicates that the bears have taken control because the 13-day EMA and MACD Histogram are falling (you don't have permission to buy). A blue histogram bar indicates mixed technical signals, with neither buying nor selling pressure predominating (either both buying or selling are permitted).

The impulse system can be removed from the chart any time.

-----------------------------------------------------------------

Options/adjustments for this indicator:

*Horizontal Distance (width) between two tops/bottoms criteria.

Refers to the horizontal distance between the MACH histogram peaks involved in the divergence

*Height of tops/bottoms criteria (for Histogram).

Refers to the difference/relation/vertical distance between the MACH HISTOGRAM peaks involved in the divergence: 1st Histogram Peak is X times the 2nd.

*Height/Vertical deviation of tops/bottoms criteria (for Price).

Deviation refers to the difference/relation/vertical distance between the PRICE peaks involved in the divergence.

*Plot Regular Bullish Divergences?.

*Plot Regular Bearish Divergences?.

*Delete Previous Cancelled Divergences?.

*This indicator also has the option to show the Impulse System over the MACD histogram bars

Buy Only Strategy with Dynamic Re-Entry and ExitThe strategy aims to create a simple buy-only trading system based on moving average crossovers and the Weekly Commodity Channel Index (CCI) or Weekly Average Directional Index (ADX). It generates buy signals when the fast-moving average crosses above the slow-moving average and when the Weekly CCI and or Weekly ADX meet the specified conditions.

The strategy also allows for dynamic re-entry, which means it can open new long positions if the price goes above the three moving averages after an exit. However, the strategy will exit the long position if the price closes below the third moving average.

ENTRY CONDITIONS

The script defines the conditions for generating buy signals. It checks for two conditions for a valid buy signal:

• If the fast-moving average crosses above the slow-moving average -THERE IS Dynamic Re-Entry also

• If the user chooses HE OR SHE CAN FILTER TRADES BY USING CCI OR ADX

Dynamic Re-Entry:

the script allows for dynamic re-entry. If there is no active long position and the price is above all three moving averages a new long position is opened.

Exit Conditions

The script defines the exit condition for closing a long position. If the price closes below the third moving average, the script closes the long position.

IMPORTANT NOTICE

ONLY DAILY TIME FRAME

THERE WOULD BE WHIPSAW USE YOUR OWN ACCUMEN TO MINIMISE THEM

ITS ONLY BUY STRATEGY

EXIT CAN BE STRATEGY BASED OR SET PROFIT AND TARGETS AS PER RISK APETITE /RISK MANAGEMENT

DONT TRADE OPTIONS ON THIS

SUITABLE FOR STOCKS OF USA AND INDIAN MARKETS

ALWAYS REMEMBER TO DO YOUR OWN RESEARCH BEFORE TRADING AND INVESTING

HTF FVG D/W/M 25%/50%/75% [MK]Do you use HTF FVG (fair value gaps) in your trading strategy? Do you monitor price on the 25%/50%/75% levels within the FVG on a lower timeframe?

This script will allow the user to display either Daily, Weekly or Monthly FVGs on a lower timeframe chart. The script will then also show the 25%/50%/75% levels within the HTF FVG so traders can see how price reacts in the FVG.

For example, a Weekly FVG may be chosen by the trader as a possible reversal point, or somewhere to add to an existing position. The trader might want to see the FVG almost fully filled, then watch price climb up/down out of the Weekly FVG

before taking the trade.

Previously traders would draw the FVG to the chart, then use maybe the tradingview fib tool to display the 25%/50%/75% levels. The problem with this is that its easy to accidently move the fib while dragging the chart around.

Chart below shows example of price almost filling a D FVG, then using the 25%/50%/75% levels as it climbs out of the FVG and reverses to the upside.

TimeLy Moving Average - TMAHello traders, I'm Only Fibonacci.

With this indicator, you will see the averages according to the hourly, weekly and monthly price movements in many periods on the chart.

This will show you the moving average values of the price over different periods in a progressive manner on the chart that is open to you.

Options and Usage

To see the hourly average, your chart's time range must be less than or equal to 60 minutes, otherwise it will produce a NaN value.

In order to see the daily average, your chart must be open for any minute period or (even if the second is open, it must be greater than 6 seconds). Otherwise, it does not produce any value.

Your chart must be larger than the second chart to see the weekly average. In other words, you can see the weekly average with at least 1 minute chart open.

In order to see the monthly average, your chart time interval must be above 10 minutes, otherwise you will not be able to see data again.

Settings

You choose the moving average type and the time interval value you want to see from the indicator settings.

You can also select a source for moving averages.

Enjoy it, you can make improvements on it.

Please do not forget to comment for various bug reports.

ICT TGIF_V2 [MK]The ICT T.G.I.F (Thank God Its Friday) works on the following strategy:

1. Friday makes the High/Low of the Week.

2. The Weekly High/Low range is used to calculate 20-30% levels. (see chart above)

3. Trades are taken in the Friday PM session (NY EST) with the idea that price may retrace to the 20-30% level.

The indicator plots the following levels:

1. Week High

2. Week Low

3. Week Open

3. 20-30% level in upper part of weekly range (only shows if Friday has made the high of the week)

4. 20-30% level in lower part of weekly range (only shows if Friday has made the low of the week)

It is possible to show all historical levels listed above for the purpose of back-testing the TGIF strategy.

Also it is possible to disable all the historical and current levels, in which case only the 20-30% levels will show when Friday has made the Week High/Low (the 20-30% level only shows from 1200-1600 on Friday to keep charts as clean as possible.

Users of this script, and any script for that matter, should always do proper back-testing before taking any trades.

Many thanks should be given to ICT (The Inner Circle Trader) for bringing this strategy to the trading community.

Below shows indicator with all levels turned ON

Below shows indicator with all levels turned OFF (this allows for cleaner charts)

Correlation Coefficient - DXY & XAUPublishing my first indicator on TradingView. Essentially a modification of the Correlation Coefficient indicator, that displays a 2 ticker symbols' correlation coefficient vs, the chart presently loaded.. You can modify the symbols, but the default uses DXY and XAU, which have been displaying strong negative correlation.

As with the built-in CC (Correlation Coefficient) indicator, readings are taken the same way:

Positive Correlation = anything above 0 | stronger as it moves up towards 1 | weaker as it moves back down towards 0

Negative Correlation = anything below 0 | stronger moving down towards -1 | weaker moving back up towards 0

This is primarily created to work with the Bitcoin weekly chart, for comparing DXY and Gold (XAU) price correlations (in advance, when possible). If you change the chart timeframe to something other than weekly, consider playing with the Length input, which is set to 35 by default where I think it best represents correlations with Bitcoin's weekly timeframe for DXY and Gold.

The intention is that you might be able to determine future direction of Bitcoin based on positive or negative correlations of Gold and/or the US Dollar Index. DXY has been making peaks and valleys prior to Bitcoin since after March 2020 black swan event, where it peaked just after instead. In the future, it may flip over again and Bitcoin may hit major highs or lows prior to DXY, again. So, keep an eye on the charts for all 3, as well as the indicator correlations.

Currently, we've moved back into negative correlation between Bitcoin and DXY, and positive correlation with Bitcoin and Gold:

Negative Correlation b/w Bitcoin and DXY - if DXY moves up, Bitcoin likely moves down, or if DXY moves down, Bitcoin likely moves up (or if Bitcoin were to move first before DXY, as it did on March 2020, instead)

Positive Correlation b/w Bitcoin and Gold - Bitcoin and Gold will likely move up or down with each other.

DXY is represented by the green histogram and label, Gold is represented by the yellow histogram and label. Again, you can modify the tickers you want to check against, and you can modify the colors for their histograms / labels.

The inspiration from came from noticing areas of same date or delayed negative correlation between Bitcoin and DXY, here is one of my most recent posts about that:

Please let me know if you have any questions, or would like to see updates to the indicator to make it easier to use or add more useful features to it.

I hope this becomes useful to you in some way. Thank you for your support!

Cheers,

dudebruhwhoa :)

DB Support Resistance LevelsDB Support Resistance Levels

This indicator plots historic lines for high, low and close prices. The settings allow up to 3 periods to be configured based on the current timeframe. Users can toggle the display of high, low or close values for each period along with customizing the period line color. The indicator does not use the security function. Instead, it's designed to use a period multiplier. Each period allows the user to configure a lookback length and multiplier.

For Example on Weekly

A period lookback of 12 with a multiplier value of 12 on weekly would produce historic high, low and close lines for the last 12 weeks.

A period lookback of 10 with a multiplier value of 4 on weekly would produce historic high, low and close lines for the last 4, 4-week months.

A period lookback of 8 with a multiplier value of 13 on weekly would produce historic high, low and close lines for the last 8, 13-week quarters.

Why not use security with higher timeframe?

The goal was to have the lines start at the precise high, low and close points for the current chart timeframe to allow the user to visually trace the start of the line.

What else does this do?

This indicator also plots the pivot points using TradingView's built-in "pivot_point_levels" feature.

How should I use this indicator?

Traders may use this indicator to gain a visual reference of support and resistance levels from higher periods of time. You can then compare these historic levels against the pivot point levels. In most cases, historic high, low and close levels act as support and resistance levels which can be helpful for judging future market pivot points.

Additional Notes

This indicator does increase the max total lines allowed which may impact performance depending on device specs. No alerts or signals for now. Perhaps coming soon...

Previous Levels With Custom TimeZoneThe Previous Levels With Custom TimeZone indicator shows to users specifics price area which can be liquidity to take.

Users can determine the desired time zone to retrieve the correct daily, weekly and monthly values.

Several price area are shown with with indicator which are :

Daily Open Price

Daily Low Price

Daily High Price

Previous Daily Low Price

Previous Daily High Price

Previous Weekly Low Price

Previous Weekly High Price

Previous Monthly Low Price

Previous Monthly High Price

All price area are configurable to let user have specific color or line style for each area.

Here's some example :

Daily Open / High / Low

Previous Daily High / Low

Previous Weekly High / Low

Previous Monthly High / Low

MTF TMOTMO - (T)rue (M)omentum (O)scillator) MTF (Higher Aggregation) Version

TMO calculates momentum using the DELTA of price. Giving a much better picture of the trend, reversals & divergences than most momentum oscillators using price. Aside from the regular TMO, this study combines four different TMO aggregations into one indicator for an even better picture of the trend. Once you look deeper into this study you will realize how complex this tool is. This version also produce much more information like crosses, divergences, overbought / oversold signals, higher aggregation fades etc. It is probably not even possible to explain them all, there could easily be an entire e-book about this study.

I have been using this tool for a couple of years now, and this is what i have learned so far:

Favorite Time Frame Variations:

1. 1m / 5m / 30m - Great for intraday futures or options scalps. 30m TMO serves as the overall trend gauge for the day. 5min dictates the longer term intraday moves as well as direction of the 1min. 1min is for the scalps. When the 5min TMO is sloping higher focus should be on 1min buy signals (red to green cross) and vice versa for the 5min agg. sloping down.

2. 5m / 30m / 60m - Also an interesting variation for day trading the 3-5 min charts. Producing more cleaner & beginner-friendly signals that lasts couple of minutes instead of seconds.

3. 120m / Day / 2 Day - For the 30m to 1H or 2H timeframes. Daily & 2 Day dictates the overall trend. 120 min for the signals. Great for a multi-day swings.

4. Day / 2 Day / Week - Good for the daily charts, swing trading analysis as the weekly dictates the overall trend, daily dictates the signals and the 2 day cleans out the daily signals. If the daily & 2 day are not aligned togather, daily signal means nothing. Weekly dictates 2 day - 2 day dictates daily.

5. Week / Month / 3 Month - Same thing as the previous variation but for the weekly charts.

TMO Length:

The default vanilla settings are 14,5,3. Some traders prefer 21,5,3 as the TMO length is litle higher = TMO will potenially last little longer which could teoretically produce less false signals but slower crosses which means signals will lag more behind price. The lower the length, the faster the oscillator oscillates. It is the noice vs. the lag debate. The Length can be changed, but i would not personally touch the other two. Few points up or down on length will not drastically change much. But changes on Calc Length and Smooth Length can produce totally different signals from the original.

Tips & Tricks:

1. Observe

- This is the best tip & trick I can give you. The #1 best way to learn how any study operates is to just observe how it works in certain situations from the past. MTF TMO is not

an exception.

2. The Power of the Higher Aggregation

- The higher aggregation ALWAYS dictates the lower one. Best way to see this? Just 2x the current timeframe aggregation = so on daily chart, plot the daily & two day TMOs and you will notice how the higher agg. smooths out the current agg. The higher the aggregation is, the smoother (but slower) will the TMO turn. The real power kicks in when the 3 or 4 aggregations are aligned togather in one direction.

3. Position of the Higher Aggregation in Relation to the Extremes

- Overbought / oversold signals might not really work on the current aggregation. But pay attention to the higher aggregations in relation to the extremes. Ex: on the daily chart - daily TMO inside the OB / OS extremes might not mean much. But once the higher aggregations such as 3 day or Weekly TMO enters OB/OS zone togather with the daily, this can be a very powerful signal for a TMO reversion to the zeroline.

4. Crosses

- Yes, crosses do work. Personally, I never really focused on them. The thing about the crosses is that it is crucial to pick the right higher aggregation to the combination of the current one that would be reliable but also print enough signals. The closer the cross is to the OB / OS extremes, the more bigger move can occur. Crosses around the zero line can be considered as less quality crosses.

5. Divergences

- TMO can print awesome divergences. The best divergences are on the current aggregation (TMO agg. same as the chart) since the current agg. oscillates fast, it can usually produce lower lows & higher highs faster then any higher aggregations. Easy setup: wait for the higher aggregation to reach the OB / OS extremes and watch the current (chart) aggregation to print a divergence.

6. Three is Enough

- I personally find more than three aggregations messy and hard to read. But there is always the option to turn on the 4th one. Just switch the TMO 4 Main, TMO 4 Signal and TMO 4 Fill in the style settings.

Hope it helps.

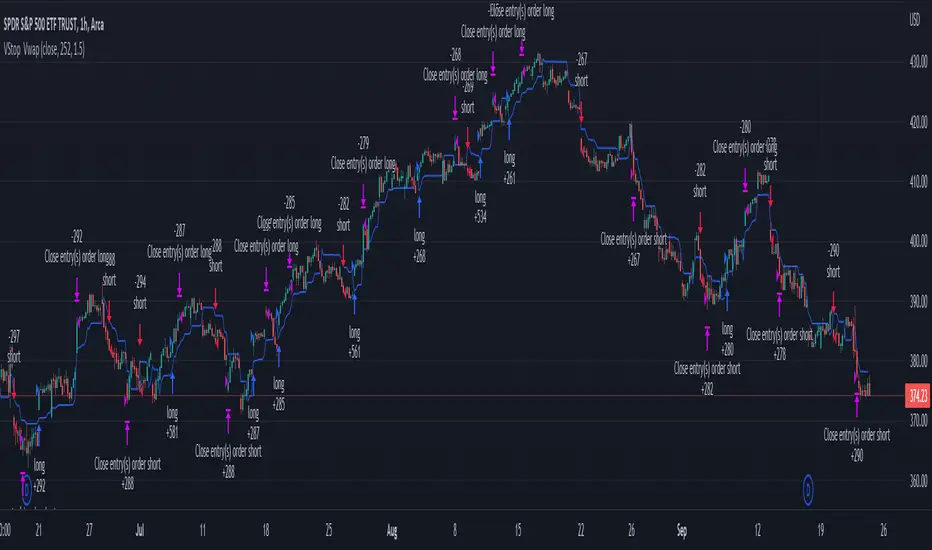

Volatility Stop with Vwap StrategyFirst the credits goes to @TradingView for their release of the volatility stop mtf indicator.

I have took it, and inside I have added a weekly vwap for a better trend direction and at the same time I have added a dynamic risk managment which is calculated from the distance between the volatility line to the close of the candle.

The rules for entry are simple:

For long:We enter when our close of the candle is above the volatility stop line and at the same time the close of the candle is above weekly vwap

For short we enter when our close of the candle is below the volatility stop line and at the same time the close of the candle is below weekly vwap.

We exit when we either have a reverse signal than the one we enterred, or based on the TP/SL which is calculated with the distance from vwap to the close of the candle.

If you have any questions please let me know !

CPR with MAs, Super Trend & VWAP by MackraniThis script will allow to add CPR with Standard Pivots and 4 Indicators.

Standard Pivot has 9 levels of support and 9 levels of resistance lines. It has CPR , 3 levels of Day-wise pivots , 3 levels of Weekly pivots and 3 Levels of Monthly Pivots .

In Addition to the CPR and Pivot , this script will allow user to Add 4 more Indicators - SMA , EMA , VWAP and SuperTrend as well.

All the Support and resistance levels can be enabled / disabled from settings. It will allow to select multiple combinations of support and resistance levels across 3 levels at any of the 3 time-frames individually and combined.

All 4 Indicators can be can be enabled / disabled from settings. This will allow the indicators to be plotted individually and combined along with any combination of CPR & Pivots .

These number of combinations will allow user to visualize the charts with desired indicators, pivot support & resistance levels on all or any of the 3 time frames.

For Ease of access, listed few points on how the script works..

- CPR and day-wise level 1 & 2 (S1 & R1) enabled by default and can be changed from settings

- Day-wise Level 2 & 3 (S2, R2, S3 & L3) can be enabled from settings

- Weekly 3 levels and Monthly 3 levels can be enabled from settings

- CPR & pivot levels colored in blue lines

- All support levels colored in Green

- All resistance levels Colored in Red

- Day-wise pivot , support & resistance are straight lines

- Weekly pivot , support & resistance are cross (+) lines

- Weekly pivot , support & resistance are circle (o) lines

- SMA , EMA , VWAP and SuperTrend Enabled by Default

- SMA Colored in Orange

- EMA Colored in Red

- EMA Colored in Teal

- SuperTrend Colored in standard Red & Green with triangle arrows

- Any combinations can be selected from settings-> Inputs & style

Day_Week_High_LowPlot lines for Daily weekly high and low. It helps to find support and resistance for weekly option trading. Weekly high low acts as Support and resistance.

Intraday Power 3 VisualDescription

This indicator draws a dynamic "Open High Low Close" type visual on intraday charts so the trader can easily keep track of the daily/weekly movement. This indicator was inspired by the Inner Circle Trader’s (ICT) “Power 3” concept, which is Accumulation, Manipulation, and Distribution of price on a daily timeframe.

Visual

This indicator plots the chosen timeframes opening price along with a live line for the current price. This makes it very easy to identify the daily/weekly range along it’s open. And the user can combine this indicator with my other indicator “Futures Exchange Sessions” to plot the midnight EST & 8:30 AM EST lines to get a great summation of over night price action.

Inputs and Style

In the Input section the user can dynamically switch between Daily and Weekly timeframes. Built in ability to move the entire Visual to the right makes preventing indicator overlap a breeze. All of the lines can be configured: color, style, and width. Independently toggle ON/OFF the Power 3 labels (Accumulation, Manipulation, Range Extension, Distribution) and can change labels color. The labels dynamically move and switch positions based upon bear or bull daily/weekly range.

Special Notes

The Futures market is open 23/5. It is closed everyday for 1-hour at 5pm EST and closed over the weekends. Because this Intraday Power 3 Visual is drawing in the 'future' on the users TradingView chart, when the visual is close or in a time when the market is closed, the visual doesn't behave properly. This is because TradingView doesn't display times when the Market is closed, thus the drawings cannot be displayed during those times. There is nothing wrong with the script. Please wait until the Market is open and the visual will be drawn normally.

This indicator is intended for use in the Futures Market

BTC NVM Ratio - Onchain AnalysisIt is an onchain oscillator and is designed to operate at weekly timeframes and is only for Bitcoin.

Network Value to Metcalfe Ratio (NVM Ratio) is defined as the ratio of the log of market capitalization divided by the log of the square of daily active addresses in the specified window.

This oscillator evaluates bitcoin price according to the Metcalfe Ratio to shows whether the current value of Bitcoin is higher or lower than the real price

I made this comparison using a moving average of 100. The areas that are red in the weekly timeframe indicate that bitcoin is Overvalued. and The areas that are blue in the weekly timeframe indicate that bitcoin is undervalued.

rsisma imkind dailyrsi 14

sma 8

time fram : weekly and daily

rsi 14

sma 8

time fram : weekly and daily

rsi 14

sma 8

time fram : weekly and daily

rsi 14

sma 8

time fram : weekly and daily

Cowen CorridorI'm reposting the Cowen Corridor that was originally developed by Benjamin Cowen of "Into the Cryptoverse"

This indicator was originally developed by Ben publicly on stream. It may be used to predict upper and lower bound limits for the price of Bitcoin .

I've set up this indicator for it to be used on the weekly timeframe as was intended.

The indicator plots in any BTCUSD spot, futures , BLX index and BTCEUR .

It paints in all time frames, but Weekly time frame is the correct one to interpret the 'official' read of it.

For that reason, I've enabled by default an option that forces the indicator to display on the Weekly value even though the time frame could be higher or lower.

Credit for this idea goes to Benjamin Cowen: @intocryptoverse

Saylor to Schiff RatioI'm reposting the Saylor to Schiff Ratio indicator that was originally developed by Michael Silva

This indicator may be used to predict key momentum shifts in the price of Bitcoin

I've set up this indicator for it to be used on the weekly timeframe as was intended.

The indicator plots in any BTCUSD spot, futures , BLX index and BTCEUR .

It paints in all time frames, but Weekly time frame is the correct one to interpret the 'official' read of it.

For that reason, I've enabled by default an option that forces the indicator to display on the Weekly value even though the time frame could be higher or lower.

Credit for this idea goes to Michael Silva: @mikepsilva

Wave Chart v1##Wave Chart v1##

For analyzing Neo-wave theory

Plot the market's highs and lows in real-time order.

Then connect the highs and lows

with a diagonal line. Next, the last plot of one day (or bar) is connected with a straight line to the

first plot of the next day (or bar).

##How To Use##

if you want a weekly chart you drop the time frame to the daily chart.

Then you set the range to 7(if the market opens 7 days per week).

Then you click "highlight the bar that runs to plot" and you must shift the highlight to the last day that the weekly chart bar close(Sunday / Friday)

##Example 1

Weekly chart BTCUSDT on BINANCE

first open daily chart, set range = 7 and Bars_shift = 3 (shift highlight to Sunday)

##Example 2

Weekly chart XAUUSD on FXOPEN

first open daily chart, set range = 5 (market open 5 days per week) and Bars_shift = 1 (shift highlight to Friday)

##Note##

If the market has a special holiday Wave Chart may be inaccurate.

Share market aasan hai CPR with MA & VWAP This script will allow to add CPR with Standard Pivots and 4 Indicators.

Standard Pivot has 9 levels of support and 9 levels of resistance lines. It has CPR , 3 levels of Day-wise pivots , 3 levels of Weekly pivots and 3 Levels of Monthly Pivots .

In Addition to the CPR and Pivot , this script will allow user to Add 4 more Indicators - SMA , EMA , VWAP and SuperTrend as well.

All the Support and resistance levels can be enabled / disabled from settings. It will allow to select multiple combinations of support and resistance levels across 3 levels at any of the 3 time-frames individually and combined.

All 4 Indicators can be can be enabled / disabled from settings. This will allow the indicators to be plotted individually and combined along with any combination of CPR & Pivots .

These number of combinations will allow user to visualize the charts with desired indicators, pivot support & resistance levels on all or any of the 3 time frames.

For Ease of access, listed few points on how the script works..

- CPR and day-wise level 1 & 2 (S1 & R1) enabled by default and can be changed from settings

- Day-wise Level 2 & 3 (S2, R2, S3 & L3) can be enabled from settings

- Weekly 3 levels and Monthly 3 levels can be enabled from settings

- CPR & pivot levels colored in blue lines

- All support levels colored in Green

- All resistance levels Colored in Red

- Day-wise pivot , support & resistance are straight lines

- Weekly pivot , support & resistance are cross (+) lines

- Weekly pivot , support & resistance are circle (o) lines

- SMA , EMA , VWAP and SuperTrend Enabled by Default

- SMA

- EMA

- SuperTrend