ArrayGenerateLibrary "ArrayGenerate"

Functions to generate arrays.

sequence_int(start, end, step) returns a sequence of int numbers.

Parameters:

start : int, begining of sequence range.

end : int, end of sequence range.

step : int, step, default=1 .

Returns: int , array.

sequence_float(start, end, step) returns a sequence of float numbers.

Parameters:

start : float, begining of sequence range.

end : float, end of sequence range.

step : float, step, default=1.0 .

Returns: float , array.

sequence_from_series(src, length, shift, direction_forward) Creates a array from a series sample range.

Parameters:

src : series, any kind.

length : int, window period in bars to sample series.

shift : int, window period in bars to shift backwards the data sample, default=0.

direction_forward : bool, sample from start to end or end to start order, default=true.

Returns: float array

normal_distribution(size, mean, dev) Generate normal distribution random sample.

Parameters:

size : int, size of array

mean : float, mean of the sample, (default=0.0).

dev : float, deviation of the sample from the mean, (default=1.0).

Returns: float array.

log_spaced(length, start_exp, stop_exp) Generate a base 10 logarithmically spaced sample sequence.

Parameters:

length : int, length of the sequence.

start_exp : float, start exponent.

stop_exp : float, stop exponent.

Returns: float array.

linear_range(stop, start) Generate a linearly spaced sample vector within the inclusive interval (start, stop) and step 1.

Parameters:

stop : float, stop value.

start : float, start value, (default=0.0).

Returns: float array.

periodic_wave(length, sampling_rate, frequency, amplitude, phase, delay) Create a periodic wave.

Parameters:

length : int, the number of samples to generate.

sampling_rate : float, samples per time unit (Hz). Must be larger than twice the frequency to satisfy the Nyquist criterion.

frequency : float, frequency in periods per time unit (Hz).

amplitude : float, the length of the period when sampled at one sample per time unit. This is the interval of the periodic domain, a typical value is 1.0, or 2*Pi for angular functions.

phase : float, optional phase offset.

delay : int, optional delay, relative to the phase.

Returns: float array.

sinusoidal(length, sampling_rate, frequency, amplitude, mean, phase, delay) Create a Sine wave.

Parameters:

length : int, The number of samples to generate.

sampling_rate : float, Samples per time unit (Hz). Must be larger than twice the frequency to satisfy the Nyquist criterion.

frequency : float, Frequency in periods per time unit (Hz).

amplitude : float, The maximal reached peak.

mean : float, The mean, or DC part, of the signal.

phase : float, Optional phase offset.

delay : int, Optional delay, relative to the phase.

Returns: float array.

periodic_impulse(length, period, amplitude, delay) Create a periodic Kronecker Delta impulse sample array.

Parameters:

length : int, The number of samples to generate.

period : int, impulse sequence period.

amplitude : float, The maximal reached peak.

delay : int, Offset to the time axis. Zero or positive.

Returns: float array.

"wave" için komut dosyalarını ara

ZigZag Chart with SupertrendHello All,

This script creates Zigzag Chart by using Zigzag waves, so it's timeless chart meaning that no time dependency on X-axis. Optionally it can calculate & show Zigzag Supertrend or Simple Moving Average. Also it can change bar colors of the main chart by trend direction of Zigzag Supertrend.

As seen below, each zigzag wave is a candle on Zigzag chart:

You have a few options and using these options you can find best settings for the securities/timeframes.

You can change Zigzag period, if you change Zigzag Period then all zigzag and the chart is recalculated/reconstructed.

You have option to show Zigzag Supertrend or Zigzag Moving Average, the options you have;

- You can change ATR Length and ATR multiplier for supertrend

- You can change Length for Simple Moving Average

You can change Zigzag candle & wick colors using options. Also you have option to change bar colors according to Zigzag Supertrend direction.

As it's timeless chart, below you can see how/when bar colors and Zigzag Supertrend change:

You can see Simple Moving Average of the Zigzag Candles:

You can play with ATR length and multiplier to find best supertrend:

You can play with the candle & wick colors:

Enjoy!

TASC 2021.10 - Cycle/Trend AnalyticsPresented here is code for the "Cycle/Trend Analytics" indicator originally conceived by John Ehlers. This is another one of TradingView's first code releases published in the October 2021 issue of Trader's Tips by Technical Analysis of Stocks & Commodities (TASC) magazine.

This indicator, referred to as "CTA" in later explanations, has a companion indicator that is discussed in the article entitled MAD Moving Average Difference , authored by John Ehlers. He's providing an innovative double dose of indicator code for the month of October 2021.

Modes of Operation

CTA has two modes defined as "trend" and "cycle". Ehlers' intention from what can be gathered from the article is to portray "the strength of the trend" in trend mode on real data. Cycle mode exhibits the response of the bank of calculations when a hypothetical sine wave is utilized as price. When cycle mode is chosen, two other lines will be displayed that are not shown in trend mode. A more detailed explanation of the indicator's technical functionality and intention can be found in the original Cycle/Trend Analytics And The MAD Indicator article, which requires a subscription.

Computational Functionality

The CTA indicator only has one adjustment in the indicator "Settings" for choice of modes. The default mode of operation is "trend". Trend mode applies raw price data to the bank of plots, while the cycle mode employs a sinusoidal oscillator set to a cycle period of 30 bars. These are passed to multiple SMAs, which are then subtracted from the original source data. The result is a fascinating display of plots embellished with vivid array of gradient color on real data or the hypothetical sine wave.

Related Information

• SMA

• color.rgb()

Join TradingView

Chips MasterChips Master, a way to tell potential chips accumulation.

There are a couple of situation where Chips Master's Yellow Bars will show up.

Firstly,

When an uptrend trend completed Dow's 12345 waves, moving into ABC waves, yellow bars will show up between MA21 and MA60

if we refer to Granville rules, it is in the vicinity of buy point number 4.

Secondly,

During a down trend, when new low is created, potentially, yellow bars will show up, an indication of chips accumulation at low price.

Feel free to provide inputs to further improve the accuracy to benefit users.

Disclaimer : Purely for Technical Analysis study. No suggestion on buy/sell.

Financial Astrology True Lilith (Black Moon) LongitudeTrue Lilith (Black Moon) represents the wildly perturbed Moon apogee orbit, is not averaged (as Mean Lilith) and shows an erratic path with constant change of direction and speed. This Lilith uses the actual, real orbit rather than the average used by Mean Lilith. This perturbations are caused due to the gravitational pull of the Sun and the change of the orbit center which is the Earth-Moon Barycenter. The move of this apogee point toward all the Zodiac signs takes around 9 years to complete and as we can observe, the True Lilith moves back and forward within two consecutive zodiac signs during a prolonged period. In this erratic motion we can note that the peaks and valleys of this waves usually present a swing trade opportunities, is really impressive to note how a full or half True Lilith wave period correlates with short term local peaks and valleys in the BTCUSD price.

Note: The True Lilith (Black Moon) longitude indicator is based on an ephemeris array that covers years 2010 to 2030, prior or after this years the data is not available, this daily ephemeris are based on UTC time so in order to align properly with the price bars times you should set UTC as your chart timezone.

Multi ZigZag EW - ImpulseSimilar to the previous script on Elliot Wave Impulse:

But, here we are trying to use multiple zigzags instead of just one.

You can select upto 4 different Zigzags and set different length, line color, line width and style for each. Parameters ShowZigZag , ZigZag Length, ZigZag Color, ZigZag Width, ZigZag Style can be used for adjusting these.

ErrorPercent lets you set error threshold calculation of ratios for pattern identification

EntryPercent is used for marking Entry and T.Stop (Tight Stoploss) based on the length of Wave 2.

Target of the script is same as before. We are trying to identify Wave 1 and 2 of Elliot Impulese Wave and then project Wave 3. Chances of price following the pattern are there. Hence, we set Stoploss based on levels which fails the pattern.

Ratios are taken from below link: elliottwave-forecast.com - Section 3.1 Impulse

Wave 2 is 50%, 61.8%, 76.4%, or 85.4% of wave 1 - used for identifying the pattern.

Wave 3 is 161.8%, 200%, 261.8%, or 323.6% of wave 1-2 - used for setting the targets

Since we use multiple zigzags, labels can be quite messy at times. In such scenarios, just disable one of the zigzag length causing label overlaps.

Zig Zag Channels [LuxAlgo]The Zig Zag indicator is a useful indicator when it comes to visualizing past underlying trends in the price and can make the process of using drawing tools easier. The indicator consists of a series of lines connecting points where the price deviates more than a specific percentage from a maximum/minimum point ultimately connecting local peaks and troughs.

This indicator by its very nature backpaints by default, meaning that the displayed components are offset in the past.

🔶 USAGE

The Zig Zag indicator is commonly used to returns points of references for the usage of specific drawing tools, such as Fibonacci retracements, fans, squares...etc.

The proposed indicator estimates peaks and troughs by using rolling maximums/minimums with a window size determining their significance. This window size approach allows us to have an indicator that works with a certain regularity no matter the scale of the price, something the percentage-based approach struggles with. Additionally, one upper and lower extremity are displayed, highlighting the price point that deviates the most from the Zig Zag lines.

A common usage also includes the easy determination of Elliot wave patterns in the price.

The Zig Zag indicator above highlights a downtrending motive wave.

🔹 Extremities

The novel approach taken by this Zig Zag indicator is the addition of two extremities derived from the distance between the price and the Zig Zag line, thus returning channels. It is uncommon seeing extremities in Zig Zag indicators since the line connecting peaks and troughs has rarely any other utility than seeing trend variations with more clarity and is not meant to provide an accurate estimate of underlying local trends in the price.

This channel can be useful to study the potential relationship between underlying trends and the Zig Zag line. A low width between the Zig Zag and the upper extremity indicates price variations mostly located below the Zig Zag while equal width indicates more linear trends.

When the indicator is extended to the last line, the extremities provide potential support and resistances, thus making this indicator able to forecast price variations.

🔶 SETTINGS

Length: Determines the significance of the detected peaks and troughs.

Extend To Last Bar: Extend the most recent line to the most recent closing price value.

Show Extremities: Displays the extremities.

Show Labels: Display labels highlighting the high/low prices located at peaks and troughs.

🔹 Style

Upper Extremity Color: Color of the upper extremity displayed by the indicator.

Zig Zag Color: Color of the ZigZag lines.

Lower Extremity Color: Color of the lower extremity displayed by the indicator.

Relative VolatilityRelative volatility highlights large changes in price. This was designed to be used with my relative volume indicator so that traders can see the effect of volume on price action. It is also a good tool to analyse breakout patterns to identify best entry points and waves.

Above shows relative volatility and relative volume working together.

Boom HunterEvery "boom" begins with a pullback... This indicator will help traders find bottoms and perfect entries into a pump. It combines two indicators, Dr. John Ehlers Early Onset Trend (EOT) and the infamous Stochastic RSI. The indicator features a built in dump and dip detector which usually picks up signals a few candles before it happens. The blue wave (EOT) shows trend, when waves travel up so does the price. Likewise for the opposite. Low points are revealed when EOT bottoms out and flat lines. Traders can then use the Stochastic RSI crossover to enter a trade. As the EOT lines get closer together there is more movement in price action, so as they get wider traders can expect sideways action. This indicator works on all timeframes but has had excellent results on hourly chart.

Entry zones are marked with a green dot at top of indicator. This signals a bottom is being formed and traders should look for an entry.

Exit points are marked with a red dot at top of indicator. This signals a peak and great time to exit.

Dips and dumps are indicated in red at bottom of indicator.

FAJ Dogepack Combines EMA + RSI indicator

Dieses Script ist eine einfache Kombination aus RSI und EMA.

Es erlaubt euch zu erkennen in welche Richtung der Trend in dem aktuellen

TimeFrame geht und wie stark dieser aktuell ist.

Außerdem zeigt es euch ob gerade eher die Bullen oder die Bären den Markt

dominieren. Mit Hilfe des Indikators lassen sich Top und Bottom des aktuellen

Time Frames erkennen.

Ich Empfehle nur eine Nutzung bei BTC um Wellen besser zu erkennen.

Erinnert euch daran, das ist nur eine Beta und gibt immer noch viele Fehlsignale aus, also testet es für euch selber in verschiedenen TimeFrames.

This script is a simple combination of RSI and EMA.

It allows you to see in which direction the trend is going in the current

time frame and how strong it is currently. It also shows you whether the

bulls or the bears are dominating the market. With the help of the indicator,

the top and bottom of the current time frame can be recognized.

recommended only use in BTC to better detect waves.

remember that it is in beta and still sends many false signals so you have to test it well in several time periods.

[blackcat] L2 Ehlers Dominant Cycle Tuned Bandpass FilterLevel: 2

Background

John F. Ehlers introuced his Dominant Cycle Tuned Bandpass Filter Strategy in Mar, 2008.

Function

In "Measuring Cycle Periods", author John Ehlers presents a very interesting technique of measuring dominant market cycle periods by means of multiple bandpass filtering. By utilizing an approach similar to audio equalizers, the signal (here, the price series) is fed into a set of simple second-order infinite impulse response bandpass filters. Filters are tuned to 8,9,10,...,50 periods. The filter with the highest output represents the dominant cycle. A full-featured formula that implements a high-pass filter and a six-tap low-pass Fir filter on input, then 42 parallel Iir band-pass filters.

I've coded John Ehlers' filter bank to measure the dominant cycle (DC) and the sine and cosine filter components in pine v4 for TradingView, based on John Ehlers' article in this issue, "Measuring Cycle Periods." The CycleFilterDC function plots and returns the DC series and its components, so it's a trivial matter to make use of them in a trading strategy.

Based on John Ehlers' article, "Measuring Cycle Periods," he chose to implement the dominant cycle-tuned bandpass filter response to test Ehlers' suggestion to use the sine and cosine crossovers as buy and sell signals. If the sine closely follows the price pattern as suggested, and the cosine is an effective leading function of the sine, then it seems to make sense that a crossover implementation would work well (Personally, what I observed this is not so accurated as his claims).

What he discovered in his tests was that crossovers happened at frequent intervals, even when price has not moved significantly. This leads to a higher percentage of losing trades, particularly when spread, slippage, and commissions are accounted for. Nevertheless, the cosine crossover was quite effective at identifying reversals very early in many cases, so this indicator could prove quite effective when used alongside other indicators. In particular, the use of an indicator to confirm a certain level of recent volatility, as well as an indicator to confirm significant rate of change, could prove quite helpful.

Key Signal

CosineLine--> Ehlers Dominant Cycle Tuned Bandpass Filter Strategy fast line

SineLine--> Ehlers Dominant Cycle Tuned Bandpass Filter Strategy slow line

Pros and Cons

100% John F. Ehlers definition translation, even variable names are the same. This help readers who would like to use pine to read his book.

Remarks

The 72th script for Blackcat1402 John F. Ehlers Week publication.

NOTE: Although Dr. Ehlers think high of Cosine and Sine wave indicator and trading strategy, my study and trading experience indicated it did not work that well as many other oscillator indicators. However, I would like to keep the original code of Dr. Ehlers for anyone who want to make a deep dive into this kind of indicator or strategy with Cosine and Sine wave.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

[blackcat] L2 Ehlers Hilbert Transformer IndicatorLevel: 2

Background

John F. Ehlers introuced Hilbert Transformer Indicator in his "Cycle Analytics for Traders" chapter 14 on 2013.

Function

Basically, the real component moves with the general direction of the prices, and the imaginary component is a predictive indicator for the real component in the same sense that a cosine wave is a predictor of a sine wave. Although the default LPPeriod input is set to 20 bars in an attempt to smooth the indicator the imaginary component is still too erratic to be useful.

Key Signal

Imag --> Quadrature phase output signal

Real --> In-phase output signal

Pros and Cons

100% John F. Ehlers definition translation, even variable names are the same. This help readers who would like to use pine to read his book.

Remarks

The 58th script for Blackcat1402 John F. Ehlers Week publication.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

True Momentum Oscillator"TMO calculates momentum using the delta of price. Giving a much better picture of trend, trend reversals and divergence than momentum oscillators using price". This is comparable to the WaveTrend Oscillator, gives more or less better or worse signals depending on the time frame and markets. This is a free and open source indicator found in many platforms, now ported to TV.

This indicator uses the closing and opening of the price in a way that reminds me of the Qstick indicator but it seems different. It's an oscillator with overbought and oversold zones and crossovers for entry and exits. I included the option of changing the moving averages from the standard exponential types used in its 3 functions to calculate the main and signal lines just in case the settings need to be changed further or if anyone wants to experiment to find better settings on top of just changing the lengths for each length type. I added dots for when the Main line crosses the Signal line. The Main line is darkened in case anyone needs to see it better.

Buy/Sell IndicatorBased on logic from many top contributors here, the script utilizes LazyBear's WaveTrend Oscillator Indicator along with custom code to plot a few key components for daily trading;

Boundaries for entry and exit points which are based on a 6-day trend in OPEN/HIGH and OPEN/LOW prices.

Daily HIGH and LOW points to establish a good view of stock's movements

Entry and exit points with confidence levels. These can be treated as entry points for short to medium term investments

Entry points come in the colours of White and Lime, where white is slightly confident and lime is extremely confident

Exit points come in the colours of Maroon, and Red, where maroon is slightly confident and red is extremely confident

Each Entry and Exit point also comes without text, or with a M or H above it, where M indicates medium confidence on the point and an O indicates overconfidence.

Use Case:

The best possible use case is to enter a trade on a LIME point with O text, this means that is an overconfident entry point.

The trade should be exited on a RED point with O text, this means that is an overconfident exit point.

But you can do with the indicators as you please.

In addition to LazyBear's code, the following existing models and indicators are taken into account:

RSI of closing price over a period of 25

EMA of RSI

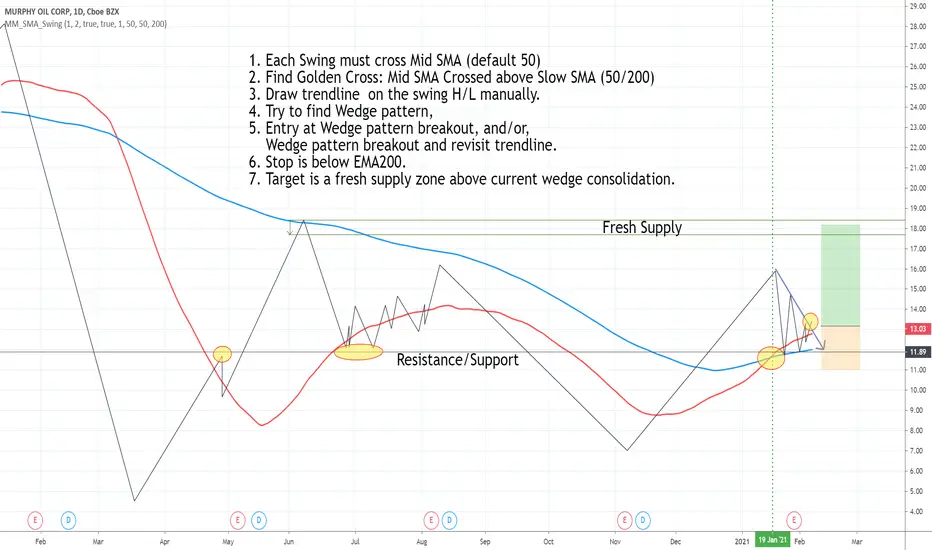

Draw swing Lines based on SMA// Draw swing Lines based on SMA

// Each swing line must cross SMA

// ---------------------------------------------------

// Input:

// sma(Number): Default 50;

// showSMA: Default 'true'; if showSMA ='false', do not show SMA line;

// Deviation(%): Default "1"; To draw a new swing line, Price must cross SMA more than (n% of SMA)

// In weekly chart, better use "2" or more to avoid small ZigZag;

// ---------------------------------------------------

// This swing Lines could be used:

// 1. Verify reversal pattern, such as, double tops;

// 2. Help to draw accurate trend line, avoid noice; Set showSMA=false, to see trend line clearly;

// 3. Use two of this study together with different SMA, Set showSMA=false,

// Such as, SMA20 and SMA200, to see small waves in bigger wave

// ---------------------------------------------------

// In this sample Chart -- AMD 1h (Feb to Jun 2020)

// Added this study with SMA(50),

// Hide price chart and SMA line, to show the Swing line only,

// I drew some sample trend lines, and identified one Double top;

BTC and ETH Long strategy - version 1I will start with a small introduction about myself. I'm now trading cryto currencies manually for almost 2 years. I decided to start after watching a documentary on the TV showing people who made big money during the Bitcoin pump which happened at the end of 2017.

The next day, I asked myself "Why should I not give it a try and learn how to trade".

This was in February 2018 and the price of Bitcoin was around 11500USD.

I didn't know how to trade. In fact, I didn't know the trading industry at all.

So, my first step into trading was to open an account with a broken. Then I directly bought 200$ worst of BTC . At that time, I saw the graph and thought "This can only go back in the upward direction!" :)

I didn't know anything about Stop loss, Take profit and Risk management.

Today, almost 2 years after, I think that I know how to trade and can also confirm that I still hold this bag of 200$ of bitcoin from 2018 :)

I did spend the 2 last years to learn technical analysis , risk management and leverage trading.

Today (14/05/2020), I know what I'm doing and I'm happy to see that the 2 last years have been positive in terms of gains. Of course, I did not make crazy money with my saving but at least I made more than if I would have kept it in my bank account.

Even if I like trading, I have a full time job which requires my full energy and lots of focus, so, the biggest problem I had is that I didn't have enough time to look at the charts.

Also, I realized that sometimes, neither technical analysis , nor fundamentals worked with crypto currency (at least for short time trading). So, as I have a developer background I decided to try to have a look at algo trading.

The goal for me was neither to make complex algos nor to beat the market but just to automate my trading with simple bot catching the big waves.

I then started to take a look at TV pine script and played with it.

I did my first LONG script in February 2020 to Long the BTC Market. It has some limitations but works well enough for me for the time being. Even if the real trades will bring me half of what the back testing shows, this will still be a lot more than what I was used to win during the last 2 years with my manual trading.

So, here we are! Below you will find some details about my first LONG script. I'm happy to share it with you.

Feel free to play with it, give your comments and bring improvements to it.

But please note that it only works fine with the candle size and crypto pair that I have mentioned below. If you use other settings this algo might loose money!

- Crypto pairs : XBTUSD and ETHXBT

- Candle size: 2 Hours

- Indicator used: Volatility , MACD (12, 26, 7), SMA (100), SMA (200), EMA (20)

- Default StopLoss: -1.5%

- Entry in position if: Volatility < 2%

AND MACD moving up

AND AME (20) moving up

AND SMA (100) moving up

AND SMA (200) moving up

AND EMA (20) > SAM (100)

AND SMA (100) > SMA (200)

- Exit the postion if: Stoploss is reached

OR EMA (20) crossUnder SMA (100)

Here is a summary of the results for this script:

XBTUSD : 01/01/2019 --> 14/05/2020 = +107%

ETHXBT : 01/01/2019 --> 14/05/2020 = +39%

ETHUSD : 01/01/2019 --> 14/05/2020 = +112%

It is far away from being perfect. There are still plenty of things which can be done to improve it but I just wanted to share it :) .

Enjoy playing with it....

Squeeze Momentum Indicator [LazyBear] vHMAThis is a remake of the famous LazyBear Indicator, the Squeeze Momentum Indicator.

All i did was take out the SMA's and replace them with HMA's. HMA is a more responsive moving average.

Hull Moving Average.

This is a derivative of John Carter's "TTM Squeeze" volatility indicator, as discussed in his book "Mastering the Trade" (chapter 11).

Black crosses on the midline show that the market just entered a squeeze ( Bollinger Bands are with in Keltner Channel). This signifies low volatility , market preparing itself for an explosive move (up or down). Gray crosses signify "Squeeze release".

Mr.Carter suggests waiting till the first gray after a black cross, and taking a position in the direction of the momentum (for ex., if momentum value is above zero, go long). Exit the position when the momentum changes (increase or decrease --- signified by a color change). My (limited) experience with this shows, an additional indicator like ADX / WaveTrend, is needed to not miss good entry points. Also, Mr.Carter uses simple momentum indicator , while I have used a different method (linreg based) to plot the histogram.

More info:

- Book: Mastering The Trade by John F Carter

Here is the original version:

Stochastic RibbonA series of highs and lows of different lengths to create a ribbon-like indicator to emulate the stochastic oscillator's top (100), middle (50) and bottom (0). Traders can determine the strength of the support and resistance by the number of converging lines, choose price points and visualise momentum waves.

Inputs:

Theme: multiple colours/themes (theme 2)

Length: high/low length (14)

Start: plot number to start ribbon on (1)

PlotNumber: number of plots to show; maximum 10 per top, middle, bottom (10)

Example:

Length: 14

Start: 5

PlotNumber: 10

Patient Trendfollower (7)(alpha)Patient Trendfollower consists of 21 and 55 EMA, Commodity Channel Index and Supertrend indicator. It confirms a trend and gives you a signal on a pullback. Original creation worked on 1h EURUSD chart.

►Long setup:

• 21 EMA is above 55 EMA, which is above the Supertrend indicator.

• Commodity Channel Index is an oscillator, which prints into the chart if extreme levels are reached. Green is for a level above 100 or below -100, red is above 140 or below -140 and black is above 180 or below -180.

• If 21 EMA > 55EMA > Supertrend and an oversold signal appear, you can buy into the trend.

• When backtesting on 1h EURUSD, profit target 400 pips worked best with a stop-loss below Supertrend's bottom and the size of your spread.

• A picture shows two valid entries.

: This part still malfunctions and shows red dots over some green ones. It is important to disable red ones in the settings to see green ones.

Some more long signals:

Some short signals:

►Backtesting data with default settings and trading only green CCI signals with mentioned risk management strategy:

• 212 closed trades

• 58.96% profitable with average win trade 348 USD and average loss trade 263 USD when only green signals are followed.

• Profit factor 1.903, Sharpee 0.792

• 20 bars is average for all trades, short trades were 18 bars long on average.

With given data, you can see the strategy is profitable by itself. However, original risk management settings do work only on 1h charts of EURUSD and would need to be adjusted for other instruments based on average volatility.

Even though the profitability is low, you can increase your odds by a great margin, if you properly use price action (impulsive and corrective moves, patterns, bar analysis), if you trade when major exchanges are open, you may also use wave analysis such as Elliot Waves or Market Profiles to predict whether the next day might be a trending day. My backtesting program didn't consider these ideas.

Unfortunately, I won't be making backtesting strategy public with it anytime soon, because it still has some parts that do not work. I am ok with that since I understand the code and know what does malfunction and how. Then, there are parts which I am not sure how to fix yet. This is why the indicator is still considered alpha.

In the future when a strategy is published, you will also be able to set your own overbought/oversold values without entering the code itself and probably some other features. But I am not in a hurry for that. You can give me feedback on UX and try to figure out the best setups for other symbols, it might help to improve the automatic testing script when I know what I should achieve. My main point is to make this public for friends who can already be using it on EURUSD at least.

Close doesn't always have to be 400 pips, you might want to close on a logical level such as strong resistance or a trendline too.

Thanks to:

• @everget for providing Supertrend solution.

• Satik FX who hand-tested the system by hand and reported results in this article . He is my main inspiration for creating the complete indicator as one because I want to be able to show and hide it with a single click. My future scripts will also work as a whole strategy each by itself.

• The number in the script's name comes from Satik's numbering. A mentioned article was his seventh shared strategy.

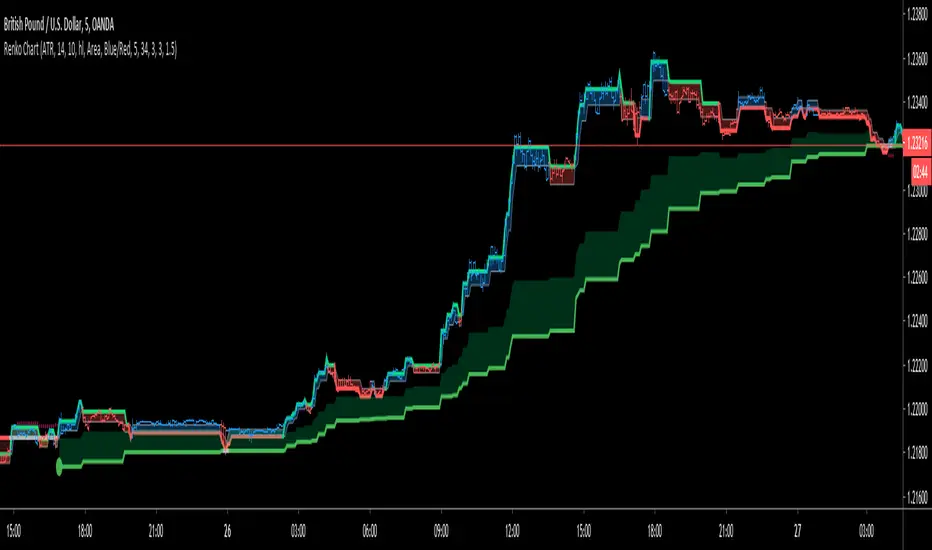

Renko ChartHello All. This is live and non-repainting Renko Charting tool. The tool has it’s own engine and not using integrated function of Trading View.

Renko charts ignore time and focus solely on price changes that meet a minimum requirement. Time is not a factor on Renko chart but as you can see with this script Renko chart created on time chart.

Renko chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

in the script Renko Trend Line with threshold area is included. and also there is protection from whipsaws, so you can catch big waves with very good entry points. Trend line is calculated by EMA of Renko closing price.

As source Closing price or High/Low can be used. Traditional or ATR can be used for scaling. If ATR is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and brick size (ATR/Percentage) is 0.00124 then box size becomes 0.001. And also while using dynamic brick size (ATR), box size changes only when Renko closing price changed.

Renko bar can be seen as area or candle and also optionally bar color changes when Renko trend changed.

Soon other Renko scripts (Renko RSI, Renko Weis Wave, Renko MACD etc) are coming ;)

ENJOY!

Trading Public School ST1This is a derivative of Trading Public School "TTM Squeeze" volatility indicator, as discussed in his book "Mastering the Trade" (chapter 11).

Black crosses on the midline show that the market just entered a squeeze ( Bollinger Bands are with in Keltner Channel). This signifies low volatility , market preparing itself for an explosive move (up or down). Gray crosses signify "Squeeze release".

Mr.Carter suggests waiting till the first gray after a black cross, and taking a position in the direction of the momentum (for ex., if momentum value is above zero, go long). Exit the position when the momentum changes (increase or decrease --- signified by a color change). My (limited) experience with this shows, an additional indicator like ADX / WaveTrend, is needed to not miss good entry points. Also, Mr.Carter uses simple momentum indicator , while I have used a different method (linreg based) to plot the histogram. 100% Profit & loss 10% Only

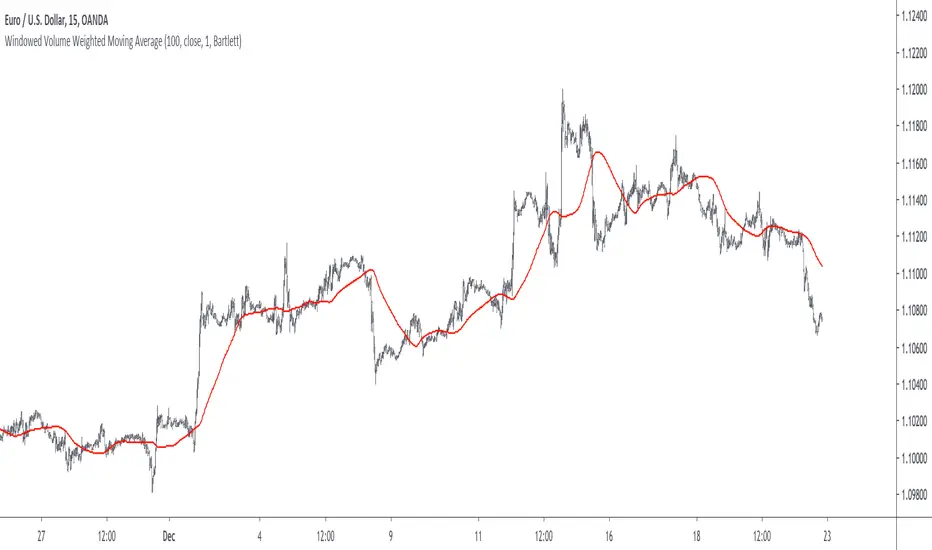

Windowed Volume Weighted Moving AverageIntroduction

The concept of windowing was briefly introduced in the Blackman filter post, however windowing is more than just some window functions, and isn't exclusively used in filter design.

Today we will use windowing with the volume weighted moving average, a moving average that weight the price with volume in order to be more reactive when volume is high, that is the moving average is more reactive when the market is more active. The use of windowing in the vwma allow to enhance its performance in the frequency domain which result in a smoother output.

Note that i made a similar indicator long ago, but at that time I was not great at all with math and pinescript in general and the indicator was therefore wrong, i want to remind to the community that i'am not a professional, only an enthusiast, I never claimed to be a master coder and i'am totally open to receive criticism, if I sounded like bragging in the past I apologize, at 20 years old it is still easy to act like a kid, the information contained in my posts is only shared in order to help others but also myself, since sharing is also a way to learn more effectively. That said lets go with the indicator.

Windowing

Windowing consist on applying a window function to a signal, by applying i mostly talk about multiplying, this process is mostly used with windowed sinc filters in order to reduce ripples in the pass/stop band, but can be used with any kind of filters in order to have better frequency domain performance, the only thing we need to do is to multiply the filter weights by a window function.

In order to understand windowing it is useful to visualize this process and understand spectral leakage. Remember that we can describe a signal as the sum of sine/cosine waves of different frequencies, amplitude and phase, leakage is an effect that appear with signals having discontinuities, that is when a signal non periodic.

This figure show a non periodic sine wave of frequency 0.1, a non periodic signal will have is last sample value different from its first sample value, if we where to do its fourier transform we wouldn't end up with a single bin at 0.1 but with more bins, this is spectral leakage, the discontinuities in the signal create additional frequency components. In order to reduce leakage we must make the signal approximately periodic, this is done by making use of window functions.

A window function is symmetric and relatively smooth, all we have to do is to multiply our first non periodic signal with the window function.

We end up with the following windowed signal :

The signal is approximately periodic and leakage has been reduced. Now that we have seen that, it might be useful to see why it is useful in filters.

Remember that the Fourier transform of the filter weights gives us its frequency response, if our weights introduce leakage we end up with ripples, so windowing the filter weights might help reduce the ripples in the frequency response, which result in a smoother filter output.

Volume Weighted Moving Average

A volume weighted moving average is a FIR filter who use volume as filter kernel, therefore the frequency response of this filter always change, it is therefore not wrong to qualify the vwma as an adaptive moving average. Higher volume mean higher weighting of the current closing price value, which therefore produce a more reactive output.

However the smoothness of the moving average is relatively poor.

Windowed Volume Weighted Moving Average

The proposed moving average has a length setting who control the moving average period, and various options that we will describe below. The first option is the type of window, there are many windows, certains more complex than others, here 3 windows are proposed, the famous Blackman window, the Bartlett, and finally the Hanning window, they provide each different level of smoothness. lets compare our moving average with period 100 with a vwma of the same period.

Our moving average in red, and the vwma in blue. As you can see the results are smoother.

The power parameter is used in order to give an even higher weighting to closing prices with high volume, this create a more boxy output. Below is a comparison with a vwma in blue and a powered vwma in red with power = 2 without windowing :

We can then apply a window, here i will choose the Blackman window :

Conclusion

A new moving average based on windowed volume weighting has been proposed. The result are smoother which might therefore reduce whipsaw trades. I wish i could have explained things better, unfortunately windowing isn't something i use much, i wanted to post this moving average earlier this year.

I will be off in France for 1 week, my flight is tomorrow in the morning, therefore i don't think i'll have the possibility to make other posts this year. I want to profit from this occasion to review my year in tradingview.

Many indicators have been posted, some being extremely bad and others really interesting, this year introduced my attempts on estimating the lsma efficiently, the linear channels, an attempt on making lines and remain the first indicator from the v4 i posted if i'am right. Then came the efficient auto-line, who gained some popularity quite fast. Then finally the %G oscillator and the recursive bands where posted, and remain some of the favorites indicators i made. I also wanted to leave this year due to studies, that i totally abandoned, i'am thankful that i chosen to stay.

I also want to express my apologies to any member that i could have offended, i think that i'am not a mean person but i certainly not contest the fact that i'am clumsy, even in my work, however my clumsiness is far greater when it comes to interact with other peoples or a group of peoples, i don't want to hurt anyone, if i made anything that made you feel bad then i'am sincerely sorry, and hope we can start this new year from 0.

Finally i thank the tradingview community for their interest and curiosity, i thank all the great coders who work on making pinescript a better scripting language, i also thank the tradingview staff for their work this year. I wish you all a merry christmas, and an happy new year.

Thanks for reading.

Zenith TraderWarning, all trading involves risk. Be sure to do your own research before placing in a trade and do not realize solely on this indicator.

Zenith Trader is made up of 3 parts

RSI , WaveTrend by LazyBear, & GMMA Oscillator by JustUncleL

It uses crosses of the 0 and/or 50 line on all indicators as a buy/sell indication

You can change which indicator is showing on the main screen in the settings.

You can all change the time frame when the alerts will pop up in order to customize your own time for alerts to go off.