Honey CypherHoney Cypher Aims to do 4 things

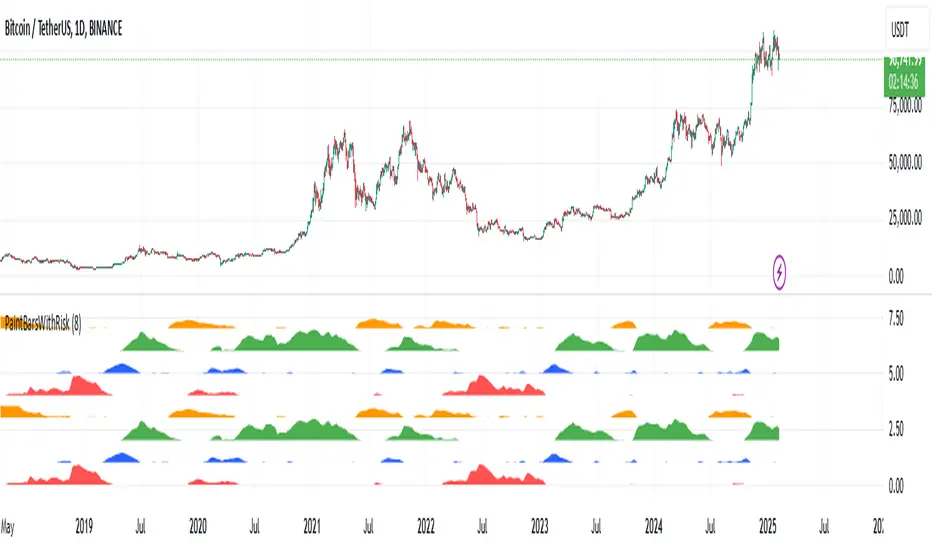

Momentum

Trend Strength

Overbought and oversold zones

Being the most beautiful indicator you ever see

Momentum

The big yellow honey waves primary use is to see the momentum of the market, they can be used in a similar way you would use a MACD or Chaikin Money Flow

On this image you see the honey waves being plotted to the 30 minute timeframe while on the 5 minute chart to have an understanding of longer time momentum in the chart.

Trend Strength

Most tools of the indicator can be used for that but the yellow and purple slope strength lines are made specificaly for this. When you see them curl down you know trend is strengthening towards the downside.

The candle color is based on the amount of Honey waves sloping in one direction. This might be the best tool in the indicator to find Trend Strength. Bright yellow candles mean strong bears while the bright blue candles mean strong bulls.

Overbought and oversold zones

By analysing the waves on a chart you start to learn how big waves can get before a reversal or consolidation period arrives.

You can become profitable with the indicator. But to be honest, my primary focus in making this indicator was find ways to visualise alot of data in a clear and beautiful way.

You should use the indicator with some out of the box ideas instead of just trusting the signals.

examples:

Find a head and shoulders pattern on the top of a huge honey wave.

Find a bottom small wave while the others honey waves are in the opposite direction for entering a pullback.

Use the honey for direction but the yellow and purple slope line crosses for entrys.

Comment your own strategys, I made this open source to be able to get community feedback.

The Honey Cypher waves are calculated in a similar way as the MACD histogram. I've combined MACD formula with some of the lazybear formula. It looks for the distance between 2 moving averages to find trend strength. After that the end results get's smoothed out. It is very satisfying to change that as you can see the honey waves create a melting like motion on each change of smoothing.

Below a preview of the honey cypher moving average lines, all lines have a length that is based on the fibonacci number sequence. Honey cypher measures the distance between for example length 5-8 averages.

I hope this inspires coders to create very beautiful scripts.

"wave" için komut dosyalarını ara

Pragmatic risk managementINTRO

The indicator is calculating multiple moving averages on the value of price change %. It then combines the normalized (via arctan function) values into a single normalized value (via simple average).

The total error from the center of gravity and the angle in which the error is accumulating represented by 4 waves:

BLUE = Good for chance for price to go up

GREEN = Good chance for price to continue going up

ORANGE = Good chance for price to go down

RED = Good chance for price to continue going down

A full cycle of ORANGE\RED\BLUE\GREEN colors will ideally lead to the exact same cycle, if not, try to understand why.

NOTICE-

This indicator is calculating large time-windows so It can be heavy on your device. Tested on PC browser only.

My visual setup:

1. Add two indicators on-top of each other and merge their scales (It will help out later).

2. Zoom out price chart to see the maximum possible data.

3. Set different colors for both indicators for simple visual seperation.

4. Choose 2 different values, one as high as possible and one as low as possible.

(Possible - the indicator remains effective at distinguishing the cycle).

Manual calibration:

0. Select a fixed chart resolution (2H resolution minimum recommended).

1. Change the "mul2" parameter in ranges between 4-15 .

2. Observe the "Turning points" of price movement. (Typically when RED\GREEN are about to switch.)

2. Perform a segmentation of time slices and find cycles. No need to be exact!

3. Draw a square on price movement at place and color as the dominant wave currently inside the indicator.

This procedure should lead to a full price segmentation with easier anchoring.

[blackcat] L2 Ehlers Autocorrelation IndicatorLevel: 2

Background

John F. Ehlers introduced Autocorrelation Indicator in his "Cycle Analytics for Traders" chapter 8 on 2013.

Function

If we correlate a waveform composed of perfectly random numbers by itself, the correlation will be perfect. However, if we lag one of the data streams by just one bar, the correlation will be dramatically reduced. In a long memory process with normally distributed random numbers the autocorrelation follows the power law.

One of the underlying principles of technical analysis is that market data do not follow this power law of an efficient market, and we therefore can extract information from the partial correlation of the autocorrelation function. For example, assume the data being examined is a perfect sine wave whose period is 20 bars. The autocorrelation with zero lag, averaged over one full period of the sine wave, is unity. That is, the correlation is perfect. Introducing a lag of one bar in the autocorrelation process causes the average correlation to be decreased slightly. Introducing another bar of lag further decreases the average correlation, and so on. That is, until a lag of 10 bars is reached. In this case, the positive alternation of the sine wave is correlated with the negative alternation of the lagged waveform and the negative alternation of the sine wave is correlated with the positive alternation of the lagged waveform, with the result that perfect anticorrelation has been reached. Continued lag increases causes the average correlation to increase until a lag of 20 bars is reached. When the lag is equal to the period of the sine wave waveform, the correlation is again perfect. In this theoretical example, the correlation values as a function of lag vary exactly as a sine wave.

Market data are considerably messier than purely random numbers or perfect sine waves but contain features of both. However, the characteristics that are uncovered by autocorrelation offer unique trading perspectives. Aside from appearing psychedelic, there are two distinct characteristics of the autocorrelation indicator using minimum averaging. First, there is a sharp reversal from red to yellow and from yellow to red at the timing of price reversals for all periods of lag. Second, there is a variation of the thickness of the bars and the number of bars over the vertical range of the indicator as a function of time.

Key Signal

Corr --> Pearson correlation data array

Pros and Cons

I am sorry this script is NOT 100% as original Ehlers works but I modified it accordingly which demostrated with better visual effect.

Remarks

The 47th script for Blackcat1402 John F. Ehlers Week publication.

Courtesy of @RicardoSantos for RGB functions.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

Momentum ArrowsThis simple indicators paints the Momentum based on Stochastic, RSI or WaveTrend onto the Price Chart by showing Green or Red arrows.

In the settings it can be selected which indicator is used, Stochastic is selected by default.

Length of the arrows is determined by the strength of the momentum:

Stochastic: Difference between D and K

RSI: Difference from RSI-50

WaveTrend: Difference between the Waves

(Thanks to @LazyBear for the WaveTrend inspiration)

PS:

If anyone has an idea how to conditionally change the color of the arrows, then please let me know - that would be the icing on the cake. Then it would be possible to indicate Overbought/Oversold levels with different colors.

Unfortunately it currently seems not to be possible to dynamically change the arrow colour.

WWV_LB pivotfix histogram jayy

This is a modification of LazyBear's WWV_LB which plots cumulative volume of waves. The reversal points are defined through relative closing prices. I made adjustments to the script to show waves turning on actual/true low or high pivots as opposed to the bar/candle identified in the LazyBear script. What I mean by that is that the actual/true low or high pivots are in fact the true WWV_LB pivots. The original WWV_LB script calculates cumulative volume from reversal confirmation bar to reversal confirmation bar as opposed to the true WWV_LB pivot bar to pivot bar. As such the waves can have slightly different start and end points. As such the cumulative volume can also be different from te WWV_LB script. This is because confirmation of a wave reversal can lag a few bars after the true reversal pivot bar. In the script notes, you will see the original key WWV_LB script lines that identify the true high or low pivots and confirm the wave direction has reversed. I have taken these lines from LazyBear's original script. I have included the LazyBear script within the script notes so that the original can be compared to what I have added/changed. Instead of "trendDetectionLength" I have inserted "Trend Detection Length". You can of course change the descriptor to what you wish by editing script line 33 to the original term or whatever you wish. You might also wish to set the default to the value "2" as per the original script. I have set the default to "3". This script should be used in conjunction with "WWV-LB zigzag pivot fix jayy" script which is shown on this screen for comparison.

Here is a link to the original LazyBear histogram script which can be used for comparison. The differences are subtle, however, the histograms will regularly be different by a bar or two:

The lowest panel has the original LazyBear WWV_LB script for comparison. All three scripts have been set to a Trend Detection Length of 3.jayy

Vegas tunnelHi all,

This is the first step in putting together a more comprehensive suite of indicators and strategies based around the original Vegas tunnel method.

You will need to know what that is before trying to use this indicator. I would implore you to take the time to read the document. It's free to the universe and is a very valuable piece of work in my opinion.

Here is the link to the original documentation dl.fxf1.com

This indicator is set up to use the original levels as described by Vegas. Future releases will allow for more custom levels.

A note on the target waves. Vegas gives us the levels of 55, 89 and 233...all in FX pips. You will need to adjust that for your instrument and it is your personal preference. If you are using BTC , you might use $55, $89 etc, for ETH $5.50, $8.90 etc, for S+P 55, 89, 233 or for FX, the number might be 0.0055 etc

The indicator has been left blank so you can fill the target waves in yourself.

A note on the templates

The original template is simply as Vegas described it in his document, change it as you wish

The TD template comes from where I first was introduced to the concept. I can't mention the full source here, but some of you will know to what I am referring to. A massive thanks to TD for all the material they have provided the world.

The HH (Hero Hedge) template is just my way of looking at the wave. It's green when the faster MA is above the slower MA and red for the opposite. It doesn't really mean much, it's just a visual reference. Perhaps you can use it to filter signals if you so wish.

Finally, some of you may notice that I am an amateur coder at best. If you think you can improve or tidy up the code, then by all means, please reach out and collaborate with me.

I am trying to produce something to the benefit of all. I hope this can help you. If it does, then please pay it forward as I am trying to do.

Hero Hedge.

Vegas tunnelHi all,

This is the first step in putting together a more comprehensive suite of indicators and strategies based around the original Vegas tunnel method.

You will need to know what that is before trying to use this indicator. I would implore you to take the time to read the document. It's free to the universe and is a very valuable piece of work in my opinion.

Here is the link to the original documentation dl.fxf1.com

This indicator is set up to use the original levels as described by Vegas. Future releases will allow for more custom levels.

A note on the target waves. Vegas gives us the levels of 55, 89 and 233...all in FX pips. You will need to adjust that for your instrument and it is your personal preference. If you are using BTC , you might use $55, $89 etc, for ETH $5.50, $8.90 etc, for S+P 55, 89, 233 or for FX, the number might be 0.0055 etc

The indicator has been left blank so you can fill the target waves in yourself.

A note on the templates

The original template is simply as Vegas described it in his document, change it as you wish

The TD template comes from where I first was introduced to the concept. I can't mention the full source here, but some of you will know to what I am referring to. A massive thanks to TD for all the material they have provided the world.

The HH (Hero Hedge) template is just my way of looking at the wave. It's green when the faster MA is above the slower MA and red for the opposite. It doesn't really mean much, it's just a visual reference. Perhaps you can use it to filter signals if you so wish.

Finally, some of you may notice that I am an amateur coder at best. If you think you can improve or tidy up the code, then by all means, please reach out and collaborate with me.

I am trying to produce something to the benefit of all. I hope this can help you. If it does, then please pay it forward as I am trying to do.

Hero Hedge.

Master Crypto Overlay [R2D2]The Gemini Master Crypto Overlay: User Guide

1. Introduction

The Gemini Master Crypto Overlay is a professional-grade TradingView script designed to consolidate six powerful institutional indicators into a single, clean "heads-up display" (HUD).

Instead of cluttering your chart with multiple sub-windows (which shrinks your view of the price), this script uses smart overlays and a data dashboard to provide actionable data instantly. It is optimized for the Daily timeframe as requested, but functions on all timeframes.

Included Indicators:

Ichimoku Cloud: Identifies the primary trend and support/resistance zones.

MACD (Custom Crypto Settings): Optimized (3-10-16) for catching fast crypto moves.

WaveTrend Oscillator: Visual signals for Overbought/Oversold entries.

Supertrend: A trailing stop-loss line to keep you in profitable trades.

Ultimate RSI (MTF): Multi-timeframe analysis to ensure you are trading with the higher trend.

Volume Reference (VWAP): An on-chart proxy for Volume Profile to spot fair value.

2. Installation Instructions

Step 1: Open Pine Editor

Launch your chart on TradingView.

At the bottom of the screen, click the tab labeled Pine Editor.

Step 2: Paste the Code

Delete any text currently in the editor window.

Copy the code block at the bottom of this response.

Paste it into the editor.

Step 3: Save and Add

Click "Save" (top right of the editor) and name it "Master Crypto Overlay".

Click "Add to chart".

Note: You may hide the "Pine Editor" panel now by clicking the arrow at the bottom center of the screen.

3. How to Use the Interface

The script is designed to be intuitive. Here is what you are looking at:

A. The Dashboard (Bottom Right)

This is your "Confluence Checker." It summarizes the status of the major indicators in real-time.

GREEN: Bullish (Buy/Hold)

RED: Bearish (Sell/Short)

GRAY: Neutral/Choppy (Stay out)

Pro Tip: Do not enter a trade unless at least 3 out of 4 signals on the dashboard match your direction.

B. On-Chart Signals

Clouds (Red/Green): If the cloud is Green and rising, only look for Long trades. If Red, only look for Short trades.

Supertrend Line: This continuous line trails the price. If price is above it (Green line), you are safe. If price closes below it, the trend has reversed.

MACD Labels: Small "MACD" text appears when momentum flips.

WaveTrend Circles:

Blue Circle (Bottom): Price is "Oversold." Good time to buy if the trend is up.

Orange Circle (Top): Price is "Overbought." Good time to take profit.

4. Strategy: Maximizing Trading Returns

To make money with this script, you need a rule-based system. Do not just blindly click when you see a label. Use this "Trend & Trigger" strategy:

The "Golden Entry" (High Probability Long)

Trend Check: Ensure price is ABOVE the Ichimoku Cloud.

Dashboard Check: Verify the RSI Status says "BULL (>50)".

The Trigger: Wait for a pullback where price touches the Supertrend Line (Green) or the top of the Cloud.

The Entry: Enter the trade when a Blue WaveTrend Circle appears OR a MACD Buy Label prints.

Stop Loss: Place your stop loss slightly below the Supertrend line.

The "Exit Strategy" (Protecting Profits)

Conservative: Sell half your position when an Orange WaveTrend Circle appears.

Trend Follower: Hold the rest of your position until the Supertrend Line turns RED.

MLExtensionsLibrary "MLExtensions"

A set of extension methods for a novel implementation of a Approximate Nearest Neighbors (ANN) algorithm in Lorentzian space.

normalizeDeriv(src, quadraticMeanLength)

Returns the smoothed hyperbolic tangent of the input series.

Parameters:

src (float) : The input series (i.e., the first-order derivative for price).

quadraticMeanLength (int) : The length of the quadratic mean (RMS).

Returns: nDeriv The normalized derivative of the input series.

normalize(src, min, max)

Rescales a source value with an unbounded range to a target range.

Parameters:

src (float) : The input series

min (float) : The minimum value of the unbounded range

max (float) : The maximum value of the unbounded range

Returns: The normalized series

rescale(src, oldMin, oldMax, newMin, newMax)

Rescales a source value with a bounded range to anther bounded range

Parameters:

src (float) : The input series

oldMin (float) : The minimum value of the range to rescale from

oldMax (float) : The maximum value of the range to rescale from

newMin (float) : The minimum value of the range to rescale to

newMax (float) : The maximum value of the range to rescale to

Returns: The rescaled series

getColorShades(color)

Creates an array of colors with varying shades of the input color

Parameters:

color (color) : The color to create shades of

Returns: An array of colors with varying shades of the input color

getPredictionColor(prediction, neighborsCount, shadesArr)

Determines the color shade based on prediction percentile

Parameters:

prediction (float) : Value of the prediction

neighborsCount (int) : The number of neighbors used in a nearest neighbors classification

shadesArr (array) : An array of colors with varying shades of the input color

Returns: shade Color shade based on prediction percentile

color_green(prediction)

Assigns varying shades of the color green based on the KNN classification

Parameters:

prediction (float) : Value (int|float) of the prediction

Returns: color

color_red(prediction)

Assigns varying shades of the color red based on the KNN classification

Parameters:

prediction (float) : Value of the prediction

Returns: color

tanh(src)

Returns the the hyperbolic tangent of the input series. The sigmoid-like hyperbolic tangent function is used to compress the input to a value between -1 and 1.

Parameters:

src (float) : The input series (i.e., the normalized derivative).

Returns: tanh The hyperbolic tangent of the input series.

dualPoleFilter(src, lookback)

Returns the smoothed hyperbolic tangent of the input series.

Parameters:

src (float) : The input series (i.e., the hyperbolic tangent).

lookback (int) : The lookback window for the smoothing.

Returns: filter The smoothed hyperbolic tangent of the input series.

tanhTransform(src, smoothingFrequency, quadraticMeanLength)

Returns the tanh transform of the input series.

Parameters:

src (float) : The input series (i.e., the result of the tanh calculation).

smoothingFrequency (int)

quadraticMeanLength (int)

Returns: signal The smoothed hyperbolic tangent transform of the input series.

n_rsi(src, n1, n2)

Returns the normalized RSI ideal for use in ML algorithms.

Parameters:

src (float) : The input series (i.e., the result of the RSI calculation).

n1 (simple int) : The length of the RSI.

n2 (simple int) : The smoothing length of the RSI.

Returns: signal The normalized RSI.

n_cci(src, n1, n2)

Returns the normalized CCI ideal for use in ML algorithms.

Parameters:

src (float) : The input series (i.e., the result of the CCI calculation).

n1 (simple int) : The length of the CCI.

n2 (simple int) : The smoothing length of the CCI.

Returns: signal The normalized CCI.

n_wt(src, n1, n2)

Returns the normalized WaveTrend Classic series ideal for use in ML algorithms.

Parameters:

src (float) : The input series (i.e., the result of the WaveTrend Classic calculation).

n1 (simple int)

n2 (simple int)

Returns: signal The normalized WaveTrend Classic series.

n_adx(highSrc, lowSrc, closeSrc, n1)

Returns the normalized ADX ideal for use in ML algorithms.

Parameters:

highSrc (float) : The input series for the high price.

lowSrc (float) : The input series for the low price.

closeSrc (float) : The input series for the close price.

n1 (simple int) : The length of the ADX.

regime_filter(src, threshold, useRegimeFilter)

Parameters:

src (float)

threshold (float)

useRegimeFilter (bool)

filter_adx(src, length, adxThreshold, useAdxFilter)

filter_adx

Parameters:

src (float) : The source series.

length (simple int) : The length of the ADX.

adxThreshold (int) : The ADX threshold.

useAdxFilter (bool) : Whether to use the ADX filter.

Returns: The ADX.

filter_volatility(minLength, maxLength, useVolatilityFilter)

filter_volatility

Parameters:

minLength (simple int) : The minimum length of the ATR.

maxLength (simple int) : The maximum length of the ATR.

useVolatilityFilter (bool) : Whether to use the volatility filter.

Returns: Boolean indicating whether or not to let the signal pass through the filter.

backtest(high, low, open, startLongTrade, endLongTrade, startShortTrade, endShortTrade, isEarlySignalFlip, maxBarsBackIndex, thisBarIndex, src, useWorstCase)

Performs a basic backtest using the specified parameters and conditions.

Parameters:

high (float) : The input series for the high price.

low (float) : The input series for the low price.

open (float) : The input series for the open price.

startLongTrade (bool) : The series of conditions that indicate the start of a long trade.

endLongTrade (bool) : The series of conditions that indicate the end of a long trade.

startShortTrade (bool) : The series of conditions that indicate the start of a short trade.

endShortTrade (bool) : The series of conditions that indicate the end of a short trade.

isEarlySignalFlip (bool) : Whether or not the signal flip is early.

maxBarsBackIndex (int) : The maximum number of bars to go back in the backtest.

thisBarIndex (int) : The current bar index.

src (float) : The source series.

useWorstCase (bool) : Whether to use the worst case scenario for the backtest.

Returns: A tuple containing backtest values

init_table()

init_table()

Returns: tbl The backtest results.

update_table(tbl, tradeStatsHeader, totalTrades, totalWins, totalLosses, winLossRatio, winrate, earlySignalFlips)

update_table(tbl, tradeStats)

Parameters:

tbl (table) : The backtest results table.

tradeStatsHeader (string) : The trade stats header.

totalTrades (float) : The total number of trades.

totalWins (float) : The total number of wins.

totalLosses (float) : The total number of losses.

winLossRatio (float) : The win loss ratio.

winrate (float) : The winrate.

earlySignalFlips (float) : The total number of early signal flips.

Returns: Updated backtest results table.

Ultimate Multi-Asset Correlation System by able eiei Ultimate Multi-Asset Correlation System - User Guide

Overview

This advanced TradingView indicator combines WaveTrend oscillator analysis with comprehensive multi-asset correlation tracking. It helps traders understand market relationships, identify regime changes, and spot high-probability trading opportunities across different asset classes.

Key Features

1. WaveTrend Oscillator

Main Signal Lines: WT1 (blue) and WT2 (red) plot momentum and its moving average

Overbought/Oversold Zones: Default levels at +60/-60

Cross Signals:

🟢 Bullish: WT1 crosses above WT2 in oversold territory

🔴 Bearish: WT1 crosses below WT2 in overbought territory

Higher Timeframe (HTF) Analysis: Shows WT1 from 4H, Daily, and Weekly timeframes for trend confirmation

2. Multi-Asset Correlation Tracking

Monitors relationships between:

Major Assets: Gold (XAUUSD), Dollar Index (DXY), US 10-Year Yield, S&P 500

Crypto Assets: Bitcoin, Ethereum, Solana, BNB

Cross-Asset Analysis: Correlation between traditional markets and crypto

3. Market Regime Detection

Automatically identifies market conditions:

Risk-On: High correlation + positive sentiment (🟢 Green background)

Risk-Off: High correlation + negative sentiment (🔴 Red background)

Crypto-Risk-On: Strong crypto correlations (🟠 Orange background)

Low-Correlation: Divergent market behavior (⚪ Gray background)

Neutral: Mixed signals (🟡 Yellow background)

How to Use

Basic Setup

Add to Chart: Apply the indicator to any chart (works on all timeframes)

Choose Display Mode (Display Options):

All: Shows everything (recommended for comprehensive analysis)

WaveTrend Only: Focus on momentum signals

Correlation Only: View market relationships

Heatmap Only: Simplified correlation view

Enable Asset Groups:

✅ Major Assets: Traditional markets (stocks, bonds, commodities)

✅ Crypto Assets: Digital currencies

Mix and match based on your trading focus

Reading the Charts

WaveTrend Section (Bottom Panel)

Above 0 = Bullish momentum

Below 0 = Bearish momentum

Above +60 = Overbought (potential reversal)

Below -60 = Oversold (potential bounce)

Lighter lines = Higher timeframe trends

Correlation Histogram (Colored Bars)

Blue bars: Major asset correlations

Orange bars: Crypto correlations

Purple bars: Cross-asset correlations

Bar height: Correlation strength (-50 to +50 scale)

Background Color

Intensity reflects correlation strength

Color shows market regime

Dashboard Elements

🎯 Market Regime Analysis (Top Left)

Current Regime: Overall market condition

Average Correlation: Strength of relationships (0-1 scale)

Risk Sentiment: -100% (risk-off) to +100% (risk-on)

HTF Alignment: Multi-timeframe trend agreement

Signal Quality: Confidence level for current signals

📊 Correlation Matrix (Top Right)

Shows correlation values between asset pairs:

1.00: Perfect positive correlation

0.75+: Strong correlation (🟢 Green)

0.50+: Medium correlation (🟡 Yellow)

0.25+: Weak correlation (🟠 Orange)

Below 0.25: Negative/no correlation (🔴 Red)

🔥 Correlation Heatmap (Bottom Right)

Visual matrix showing:

Gold vs. DXY, BTC, ETH

DXY vs. BTC, ETH

BTC vs. ETH

Color-coded strength

📈 Performance Tracker (Bottom Left)

Tracks individual asset momentum:

WT1 Values: Current momentum reading

Status: OB (overbought) / OS (oversold) / Normal

Trading Strategies

1. High-Probability Trend Following

✅ Entry Conditions:

WaveTrend bullish/bearish cross

HTF Alignment matches signal direction

Signal Quality > 70%

Correlation supports direction

2. Regime Change Trading

🎯 Watch for regime shifts:

Risk-Off → Risk-On = Consider long positions

High correlation → Low correlation = Reduce position size

Crypto-Risk-On = Focus on crypto longs

3. Divergence Trading

🔍 Look for:

Strong correlation breakdown = Potential volatility

Cross-asset correlation surge = Follow the leader

Volume-price correlation extremes = Trend confirmation

4. Overbought/Oversold Reversals

⚡ Trade reversals when:

WT crosses in extreme zones (-60/+60)

HTF alignment shows opposite trend weakening

Correlation confirms mean reversion setup

Customization Tips

Fine-Tuning Parameters

WaveTrend Core:

Channel Length (10): Lower = more sensitive, Higher = smoother

Average Length (21): Adjust for your timeframe

Correlation Settings:

Length (50): Longer = more stable, Shorter = more responsive

Smoothing (5): Reduce noise in correlation readings

Market Regime:

Risk-On Threshold (0.6): Lower = earlier regime signals

High Correlation Threshold (0.75): Adjust sensitivity

Custom Asset Selection

Replace default symbols with your preferred markets:

Major Assets: Any forex, indices, bonds

Crypto: Any digital currencies

Must use correct exchange prefix (e.g., BINANCE:BTCUSDT)

Alert System

Enable "Advanced Alerts" to receive notifications for:

✅ Market regime changes

✅ Correlation breakdowns/surges

✅ Strong signals with high correlation

✅ Extreme volume-price correlation

✅ Complete HTF alignment

Correlation Interpretation Guide

ValueMeaningTrading Implication+0.75 to +1.0Strong positiveAssets move together+0.5 to +0.75Moderate positiveGenerally aligned+0.25 to +0.5Weak positiveLoose relationship-0.25 to +0.25No correlationIndependent movements-0.5 to -0.25Weak negativeSlight inverse relationship-0.75 to -0.5Moderate negativeTend to move opposite-1.0 to -0.75Strong negativeStrongly inversely correlated

Best Practices

Use Multiple Timeframes: Check HTF alignment before trading

Confirm with Correlation: Strong signals work best with supportive correlations

Watch Regime Changes: Adjust strategy based on market conditions

Volume Matters: Enable volume-price correlation for confirmation

Quality Over Quantity: Trade only high-quality setups (>70% signal quality)

Common Patterns to Watch

🔵 Risk-On Environment:

Gold-BTC positive correlation

DXY negative correlation with risk assets

High crypto correlations

🔴 Risk-Off Environment:

Flight to safety (Gold up, stocks down)

DXY strength

Correlation breakdowns

🟡 Transition Periods:

Low correlation across assets

Mixed HTF signals

Use caution, reduce position sizes

Technical Notes

Calculation Period: Uses HLC3 (average of high, low, close)

Correlation Window: Rolling correlation over specified length

HTF Data: Accurately calculated using security() function

Performance: Optimized for real-time calculation on all timeframes

Support

For optimal performance:

Use on 15-minute to daily timeframes

Enable only needed asset groups

Adjust correlation length based on trading style

Combine with your existing strategy for confirmation

Enjoy comprehensive multi-asset analysis! 🚀

Cora Combined Suite v1 [JopAlgo]Cora Combined Suite v1 (CCSV1)

This is an 2 in 1 indicator (Overlay & Oscillator) the Cora Combined Suite v1 .

CCSV1 combines a price-pane Overlay for structure/trend with a compact Oscillator for timing/pressure. It’s designed to be clear, beginner-friendly, and largely automatic: you pick a profile (Scalp / Intraday / Swing), choose whether to run as Overlay or Oscillator, and CCSV1 tunes itself in the background.

What’s inside — at a glance

1) Overlay (price pane)

CoRa Wave: a smooth trend line based on a compound-ratio WMA (CRWMA).

Green when the slope rises (bull bias), Red when it falls (bear bias).

Asymmetric ATR Cloud around the CoRa Wave

Width expands more up when buyer pressure dominates and more down when seller pressure dominates.

Fill is intentionally light, so candlesticks remain readable.

Chop Guard (Range-Lock Gate)

When the cloud stays very narrow versus ATR (classic “dead water”), pullback alerts are muted to avoid noise.

Visuals don’t change—only the alerting logic goes quiet.

Typical Overlay reads

Trend: Follow the CoRa color; green favors long setups, red favors shorts.

Value: Pullbacks into/through the cloud in trend direction are higher-quality than chasing breaks far outside it.

Dominance: A visibly asymmetric cloud hints which side is funding the move (buyers vs sellers).

2) Oscillator (subpane or inline preview)

Stretch-Z (columns): how far price is from the CoRa mean (mean-reversion context), clipped to ±clip.

Near 0 = equilibrium; > +2 / < −2 = stretched/extended.

Slope-Z (line): z-score of CoRa’s slope (momentum of the trend line).

Crossing 0 upward = potential bullish impulse; downward = potential bearish impulse.

VPO (stepline): a normalized Volume-Pressure read (positive = buyers funding, negative = sellers).

Rendered as a clean stepline to emphasize state changes.

Event Bands ±2 (subpane): thin reference lines to spot extension/exhaustion zones fast.

Floor/Ceiling lines (optional): quiet boundaries so the panel doesn’t feel “bottomless.”

Inline vs Subpane

Inline (overlay): the oscillator auto-anchors and scales beneath price, so it never crushes the price scale.

Subpane (raw): move to a new pane for the classic ±clip view (with ±2 bands). Recommended for systematic use.

Why traders like it

Two in one: Structure on the chart, timing in the panel—built to complement each other.

Retail-first automation: Choose Scalp / Intraday / Swing and let CCSV1 auto-tune lengths, clips, and pressure windows.

Robust statistics: On fast, spiky markets/timeframes, it prefers outlier-resistant math automatically for steadier signals.

Optional HTF gate: You can require higher-timeframe agreement for oscillator alerts without changing visuals.

Quick start (simple playbook)

Run As

Overlay for structure: assess trend direction, where value is (the cloud), and whether chop guard is active.

Oscillator for timing: move to a subpane to see Stretch-Z, Slope-Z, VPO, and ±2 bands clearly.

Profile

Scalp (1–5m), Intraday (15–60m), or Swing (4H–1D). CCSV1 adjusts length/clip/pressure windows accordingly.

Overlay entries

Trade with CoRa color.

Prefer pullbacks into/through the cloud (trend direction).

If chop guard is active, wait; let the market “breathe” before engaging.

Oscillator timing

Look for Funded Flips: Slope-Z crossing 0 in the direction of VPO (i.e., momentum + funded pressure).

Use ±2 bands to manage risk: stretched conditions can stall or revert—better to scale or wait for a clean reset.

Optional HTF gate

Enable to green-light only those oscillator alerts that align with your chosen higher timeframe.

What each signal means (plain language)

CoRa turns green/red (Overlay): trend bias shift on your chart.

Cloud width tilts asymmetrically: one side (buyers/sellers) is dominating; extensions on that side are more likely.

Stretch-Z near 0: fair value around CoRa; pullback timing zone.

Stretch-Z > +2 / < −2: extended; watch for slowing momentum or scale decisions.

Slope-Z cross up/down: new impulse starting; combine with VPO sign to avoid unfunded crosses.

VPO positive/negative: net buying/selling pressure funding the move.

Alerts included

Overlay

Pullback Long OK

Pullback Short OK

Oscillator

Funded Flip Up / Funded Flip Down (Slope-Z crosses 0 with VPO agreement)

Pullback Long Ready / Pullback Short Ready (near equilibrium with aligned momentum and pressure)

Exhaustion Risk (Long/Short) (Stretch-Z beyond ±2 with weakening momentum or pressure)

Tip: Keep chart alerts concise and use strategy rules (TP/SL/filters) in your trade plan.

Best practices

One glance workflow

Read Overlay for direction + value.

Use Oscillator for trigger + confirmation.

Pairing

Combine with S/R or your preferred execution framework (e.g., your JopAlgo setups).

The suite is neutral: it won’t force trades; it highlights context and quality.

Markets

Works on crypto, indices, FX, and commodities.

Where real volume is available, VPO is strongest; on synthetic volume, treat VPO as a soft filter.

Timeframes

Use the Profile preset closest to your style; feel free to fine-tune later.

For multi-TF trading, enable the HTF gate on the oscillator alerts only.

Inputs you’ll actually use (the rest can stay on Auto)

Run As: Overlay or Oscillator.

Profile: Scalp / Intraday / Swing.

Oscillator Render: “Subpane (raw)” for a classic panel; “Inline (overlay)” only for a quick preview.

HTF gate (optional): require higher-timeframe Slope-Z agreement for oscillator alerts.

Everything else ships with sensible defaults and auto-logic.

Limitations & tips

Not a strategy: CCSV1 is a decision support tool; you still need your entry/exit rules and risk management.

Non-repainting design: Signals finalize on bar close; intrabar graphics can adjust during the bar (Pine standard).

Very flat sessions: If price and volume are extremely quiet, expect fewer alerts; that restraint is intentional.

Who is this for?

Beginners who want one clean overlay for structure and one simple oscillator for timing—without wrestling settings.

Intermediates seeking a coherent trend/pressure framework with HTF confirmation.

Advanced users who appreciate robust stats and clean engineering behind the visuals.

Disclaimer: Educational purposes only. Not financial advice. Trading involves risk. Use at your own discretion.

WT + Stoch RSI Reversal Combo📊MR.Z RSI : WT + Stochastic RSI Reversal Combo

This custom indicator combines WaveTrend oscillator and Stochastic RSI to detect high-confidence market reversal points, filtering signals so they only appear when both indicators align.

🔍 Core Components:

✅ WaveTrend Oscillator

Based on smoothed deviation from EMA (similar to TCI logic)

Plots:

WT1 (main line)

WT2 (signal line = SMA of WT1)

Uses overbought/oversold thresholds (default: ±53) to filter signals

✅ Stochastic RSI

Momentum oscillator based on RSI's stochastic value

Plots:

%K: smoothed Stoch of RSI

%D: smoothed version of %K

Adjustable oversold/overbought thresholds (default: 20/80)

🔁 Combined Reversal Signal Logic:

🔼 Buy Signal

WT1 crosses above WT2 below WT oversold level (e.g., -53)

%K crosses above %D below Stoch RSI oversold level (e.g., 20)

🔽 Sell Signal

WT1 crosses below WT2 above WT overbought level (e.g., 53)

%K crosses below %D above Stoch RSI overbought level (e.g., 80)

🔔 Signals are only plotted and alerted if both conditions are true.

📌 Features:

Toggle on/off:

WaveTrend lines and histogram

Stochastic RSI

Combined Buy/Sell signals

Horizontal reference lines (±100, OB/OS)

Fully customizable smoothing lengths and thresholds

Signal plots:

✅ Green up-triangle = Combo Buy

✅ Red down-triangle = Combo Sell

Optional: Circle/cross markers for WT-only and Stoch-only signals

🔔 Built-in alerts for Buy/Sell signals

📈 Use Cases:

Reversal Trading: Wait for both indicators to confirm momentum shift

Entry Filter: Use in combination with trend indicators (like EMA)

Scalping or Swing: Works on intraday and higher timeframes

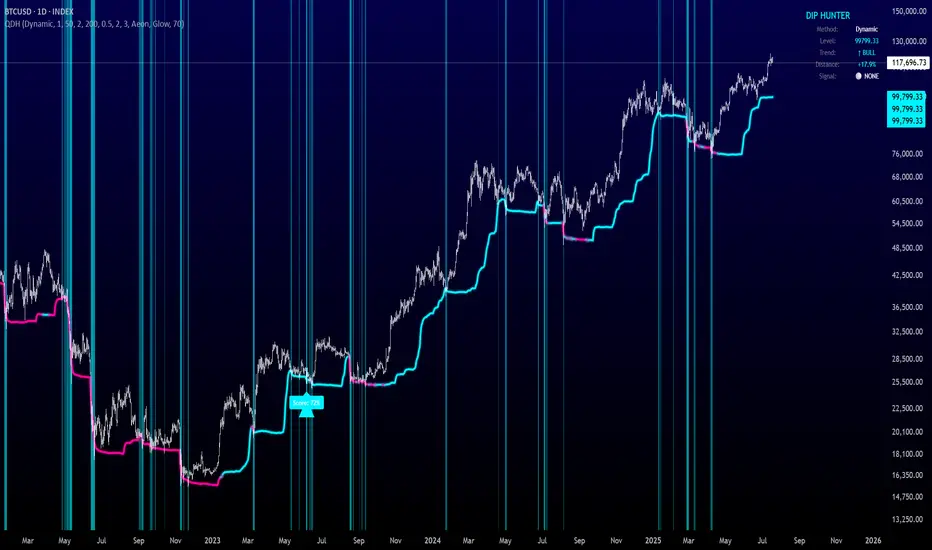

Quantum Dip Hunter | AlphaNattQuantum Dip Hunter | AlphaNatt

🎯 Overview

The Quantum Dip Hunter is an advanced technical indicator designed to identify high-probability buying opportunities when price temporarily dips below dynamic support levels. Unlike simple oversold indicators, this system uses a sophisticated quality scoring algorithm to filter out low-quality dips and highlight only the best entry points.

"Buy the dip" - but only the right dips. Not all dips are created equal.

⚡ Key Features

5 Detection Methods: Choose from Dynamic, Fibonacci, Volatility, Volume Profile, or Hybrid modes

Quality Scoring System: Each dip is scored from 0-100% based on multiple factors

Smart Filtering: Only signals above your quality threshold are displayed

Visual Effects: Glow, Pulse, and Wave animations for the support line

Risk Management: Automatic stop-loss and take-profit calculations

Real-time Statistics: Live dashboard showing current market conditions

📊 How It Works

The indicator calculates a dynamic support line using your selected method

When price dips below this line, it evaluates the dip quality

Quality score is calculated based on: trend alignment (30%), volume (20%), RSI (20%), momentum (15%), and dip depth (15%)

If the score exceeds your minimum threshold, a buy signal arrow appears

Stop-loss and take-profit levels are automatically calculated and displayed

🚀 Detection Methods Explained

Dynamic Support

Adapts to recent price action

Best for: Trending markets

Uses ATR-adjusted lowest points

Fibonacci Support

Based on 61.8% and 78.6% retracement levels

Best for: Pullbacks in strong trends

Automatically switches between fib levels

Volatility Support

Uses Bollinger Band methodology

Best for: Range-bound markets

Adapts to changing volatility

Volume Profile Support

Finds high-volume price levels

Best for: Identifying institutional support

Updates dynamically as volume accumulates

Hybrid Mode

Combines all methods for maximum accuracy

Best for: All market conditions

Takes the most conservative support level

⚙️ Key Settings

Dip Detection Engine

Detection Method: Choose your preferred support calculation

Sensitivity: Higher = more sensitive to price movements (0.5-3.0)

Lookback Period: How far back to analyze (20-200 bars)

Dip Depth %: Minimum dip size to consider (0.5-10%)

Quality Filters

Trend Filter: Only buy dips in uptrends when enabled

Minimum Dip Score: Quality threshold for signals (0-100%)

Trend Strength: Required trend score when filter is on

📈 Trading Strategies

Conservative Approach

Use Dynamic method with Trend Filter ON

Set minimum score to 80%

Risk:Reward ratio of 2:1 or higher

Best for: Swing trading

Aggressive Approach

Use Hybrid method with Trend Filter OFF

Set minimum score to 60%

Risk:Reward ratio of 1:1

Best for: Day trading

Scalping Setup

Use Volatility method

Set sensitivity to 2.0+

Focus on Target 1 only

Best for: Quick trades

🎨 Visual Customization

Color Themes:

Neon: Bright cyan/magenta for dark backgrounds

Ocean: Cool blues and teals

Solar: Warm yellows and oranges

Matrix: Classic green terminal look

Gradient: Smooth color transitions

Line Styles:

Solid: Clean, simple line

Glow: Adds depth with glow effect

Pulse: Animated breathing effect

Wave: Oscillating wave pattern

💡 Pro Tips

Start with the Trend Filter ON to avoid catching falling knives

Higher quality scores (80%+) have better win rates but fewer signals

Use Volume Profile method near major support/resistance levels

Combine with your favorite momentum indicator for confirmation

The pulse animation can help draw attention to key levels

⚠️ Important Notes

This indicator identifies potential entries, not guaranteed profits

Always use proper risk management

Works best on liquid instruments with good volume

Backtest your settings before live trading

Not financial advice - use at your own risk

📊 Statistics Panel

The live statistics panel shows:

Current detection method

Support level value

Trend direction

Distance from support

Current signal status

🤝 Support

Created by AlphaNatt

For questions or suggestions, please comment below!

Happy dip hunting! 🎯

Not financial advice, always do your own research

Color█ OVERVIEW

This library is a Pine Script® programming tool for advanced color processing. It provides a comprehensive set of functions for specifying and analyzing colors in various color spaces, mixing and manipulating colors, calculating custom gradients and schemes, detecting contrast, and converting colors to or from hexadecimal strings.

█ CONCEPTS

Color

Color refers to how we interpret light of different wavelengths in the visible spectrum . The colors we see from an object represent the light wavelengths that it reflects, emits, or transmits toward our eyes. Some colors, such as blue and red, correspond directly to parts of the spectrum. Others, such as magenta, arise from a combination of wavelengths to which our minds assign a single color.

The human interpretation of color lends itself to many uses in our world. In the context of financial data analysis, the effective use of color helps transform raw data into insights that users can understand at a glance. For example, colors can categorize series, signal market conditions and sessions, and emphasize patterns or relationships in data.

Color models and spaces

A color model is a general mathematical framework that describes colors using sets of numbers. A color space is an implementation of a specific color model that defines an exact range (gamut) of reproducible colors based on a set of primary colors , a reference white point , and sometimes additional parameters such as viewing conditions.

There are numerous different color spaces — each describing the characteristics of color in unique ways. Different spaces carry different advantages, depending on the application. Below, we provide a brief overview of the concepts underlying the color spaces supported by this library.

RGB

RGB is one of the most well-known color models. It represents color as an additive mixture of three primary colors — red, green, and blue lights — with various intensities. Each cone cell in the human eye responds more strongly to one of the three primaries, and the average person interprets the combination of these lights as a distinct color (e.g., pure red + pure green = yellow).

The sRGB color space is the most common RGB implementation. Developed by HP and Microsoft in the 1990s, sRGB provided a standardized baseline for representing color across CRT monitors of the era, which produced brightness levels that did not increase linearly with the input signal. To match displays and optimize brightness encoding for human sensitivity, sRGB applied a nonlinear transformation to linear RGB signals, often referred to as gamma correction . The result produced more visually pleasing outputs while maintaining a simple encoding. As such, sRGB quickly became a standard for digital color representation across devices and the web. To this day, it remains the default color space for most web-based content.

TradingView charts and Pine Script `color.*` built-ins process color data in sRGB. The red, green, and blue channels range from 0 to 255, where 0 represents no intensity, and 255 represents maximum intensity. Each combination of red, green, and blue values represents a distinct color, resulting in a total of 16,777,216 displayable colors.

CIE XYZ and xyY

The XYZ color space, developed by the International Commission on Illumination (CIE) in 1931, aims to describe all color sensations that a typical human can perceive. It is a cornerstone of color science, forming the basis for many color spaces used today. XYZ, and the derived xyY space, provide a universal representation of color that is not tethered to a particular display. Many widely used color spaces, including sRGB, are defined relative to XYZ or derived from it.

The CIE built the color space based on a series of experiments in which people matched colors they perceived from mixtures of lights. From these experiments, the CIE developed color-matching functions to calculate three components — X, Y, and Z — which together aim to describe a standard observer's response to visible light. X represents a weighted response to light across the color spectrum, with the highest contribution from long wavelengths (e.g., red). Y represents a weighted response to medium wavelengths (e.g., green), and it corresponds to a color's relative luminance (i.e., brightness). Z represents a weighted response to short wavelengths (e.g., blue).

From the XYZ space, the CIE developed the xyY chromaticity space, which separates a color's chromaticity (hue and colorfulness) from luminance. The CIE used this space to define the CIE 1931 chromaticity diagram , which represents the full range of visible colors at a given luminance. In color science and lighting design, xyY is a common means for specifying colors and visualizing the supported ranges of other color spaces.

CIELAB and Oklab

The CIELAB (L*a*b*) color space, derived from XYZ by the CIE in 1976, expresses colors based on opponent process theory. The L* component represents perceived lightness, and the a* and b* components represent the balance between opposing unique colors. The a* value specifies the balance between green and red , and the b* value specifies the balance between blue and yellow .

The primary intention of CIELAB was to provide a perceptually uniform color space, where fixed-size steps through the space correspond to uniform perceived changes in color. Although relatively uniform, the color space has been found to exhibit some non-uniformities, particularly in the blue part of the color spectrum. Regardless, modern applications often use CIELAB to estimate perceived color differences and calculate smooth color gradients.

In 2020, a new LAB-oriented color space, Oklab , was introduced by Björn Ottosson as an attempt to rectify the non-uniformities of other perceptual color spaces. Similar to CIELAB, the L value in Oklab represents perceived lightness, and the a and b values represent the balance between opposing unique colors. Oklab has gained widespread adoption as a perceptual space for color processing, with support in the latest CSS Color specifications and many software applications.

Cylindrical models

A cylindrical-coordinate model transforms an underlying color model, such as RGB or LAB, into an alternative expression of color information that is often more intuitive for the average person to use and understand.

Instead of a mixture of primary colors or opponent pairs, these models represent color as a hue angle on a color wheel , with additional parameters that describe other qualities such as lightness and colorfulness (a general term for concepts like chroma and saturation). In cylindrical-coordinate spaces, users can select a color and modify its lightness or other qualities without altering the hue.

The three most common RGB-based models are HSL (Hue, Saturation, Lightness), HSV (Hue, Saturation, Value), and HWB (Hue, Whiteness, Blackness). All three define hue angles in the same way, but they define colorfulness and lightness differently. Although they are not perceptually uniform, HSL and HSV are commonplace in color pickers and gradients.

For CIELAB and Oklab, the cylindrical-coordinate versions are CIELCh and Oklch , which express color in terms of perceived lightness, chroma, and hue. They offer perceptually uniform alternatives to RGB-based models. These spaces create unique color wheels, and they have more strict definitions of lightness and colorfulness. Oklch is particularly well-suited for generating smooth, perceptual color gradients.

Alpha and transparency

Many color encoding schemes include an alpha channel, representing opacity . Alpha does not help define a color in a color space; it determines how a color interacts with other colors in the display. Opaque colors appear with full intensity on the screen, whereas translucent (semi-opaque) colors blend into the background. Colors with zero opacity are invisible.

In Pine Script, there are two ways to specify a color's alpha:

• Using the `transp` parameter of the built-in `color.*()` functions. The specified value represents transparency (the opposite of opacity), which the functions translate into an alpha value.

• Using eight-digit hexadecimal color codes. The last two digits in the code represent alpha directly.

A process called alpha compositing simulates translucent colors in a display. It creates a single displayed color by mixing the RGB channels of two colors (foreground and background) based on alpha values, giving the illusion of a semi-opaque color placed over another color. For example, a red color with 80% transparency on a black background produces a dark shade of red.

Hexadecimal color codes

A hexadecimal color code (hex code) is a compact representation of an RGB color. It encodes a color's red, green, and blue values into a sequence of hexadecimal ( base-16 ) digits. The digits are numerals ranging from `0` to `9` or letters from `a` (for 10) to `f` (for 15). Each set of two digits represents an RGB channel ranging from `00` (for 0) to `ff` (for 255).

Pine scripts can natively define colors using hex codes in the format `#rrggbbaa`. The first set of two digits represents red, the second represents green, and the third represents blue. The fourth set represents alpha . If unspecified, the value is `ff` (fully opaque). For example, `#ff8b00` and `#ff8b00ff` represent an opaque orange color. The code `#ff8b0033` represents the same color with 80% transparency.

Gradients

A color gradient maps colors to numbers over a given range. Most color gradients represent a continuous path in a specific color space, where each number corresponds to a mix between a starting color and a stopping color. In Pine, coders often use gradients to visualize value intensities in plots and heatmaps, or to add visual depth to fills.

The behavior of a color gradient depends on the mixing method and the chosen color space. Gradients in sRGB usually mix along a straight line between the red, green, and blue coordinates of two colors. In cylindrical spaces such as HSL, a gradient often rotates the hue angle through the color wheel, resulting in more pronounced color transitions.

Color schemes

A color scheme refers to a set of colors for use in aesthetic or functional design. A color scheme usually consists of just a few distinct colors. However, depending on the purpose, a scheme can include many colors.

A user might choose palettes for a color scheme arbitrarily, or generate them algorithmically. There are many techniques for calculating color schemes. A few simple, practical methods are:

• Sampling a set of distinct colors from a color gradient.

• Generating monochromatic variants of a color (i.e., tints, tones, or shades with matching hues).

• Computing color harmonies — such as complements, analogous colors, triads, and tetrads — from a base color.

This library includes functions for all three of these techniques. See below for details.

█ CALCULATIONS AND USE

Hex string conversion

The `getHexString()` function returns a string containing the eight-digit hexadecimal code corresponding to a "color" value or set of sRGB and transparency values. For example, `getHexString(255, 0, 0)` returns the string `"#ff0000ff"`, and `getHexString(color.new(color.red, 80))` returns `"#f2364533"`.

The `hexStringToColor()` function returns the "color" value represented by a string containing a six- or eight-digit hex code. The `hexStringToRGB()` function returns a tuple containing the sRGB and transparency values. For example, `hexStringToColor("#f23645")` returns the same value as color.red .

Programmers can use these functions to parse colors from "string" inputs, perform string-based color calculations, and inspect color data in text outputs such as Pine Logs and tables.

Color space conversion

All other `get*()` functions convert a "color" value or set of sRGB channels into coordinates in a specific color space, with transparency information included. For example, the tuple returned by `getHSL()` includes the color's hue, saturation, lightness, and transparency values.

To convert data from a color space back to colors or sRGB and transparency values, use the corresponding `*toColor()` or `*toRGB()` functions for that space (e.g., `hslToColor()` and `hslToRGB()`).

Programmers can use these conversion functions to process inputs that define colors in different ways, perform advanced color manipulation, design custom gradients, and more.

The color spaces this library supports are:

• sRGB

• Linear RGB (RGB without gamma correction)

• HSL, HSV, and HWB

• CIE XYZ and xyY

• CIELAB and CIELCh

• Oklab and Oklch

Contrast-based calculations

Contrast refers to the difference in luminance or color that makes one color visible against another. This library features two functions for calculating luminance-based contrast and detecting themes.

The `contrastRatio()` function calculates the contrast between two "color" values based on their relative luminance (the Y value from CIE XYZ) using the formula from version 2 of the Web Content Accessibility Guidelines (WCAG) . This function is useful for identifying colors that provide a sufficient brightness difference for legibility.

The `isLightTheme()` function determines whether a specified background color represents a light theme based on its contrast with black and white. Programmers can use this function to define conditional logic that responds differently to light and dark themes.

Color manipulation and harmonies

The `negative()` function calculates the negative (i.e., inverse) of a color by reversing the color's coordinates in either the sRGB or linear RGB color space. This function is useful for calculating high-contrast colors.

The `grayscale()` function calculates a grayscale form of a specified color with the same relative luminance.

The functions `complement()`, `splitComplements()`, `analogousColors()`, `triadicColors()`, `tetradicColors()`, `pentadicColors()`, and `hexadicColors()` calculate color harmonies from a specified source color within a given color space (HSL, CIELCh, or Oklch). The returned harmonious colors represent specific hue rotations around a color wheel formed by the chosen space, with the same defined lightness, saturation or chroma, and transparency.

Color mixing and gradient creation

The `add()` function simulates combining lights of two different colors by additively mixing their linear red, green, and blue components, ignoring transparency by default. Users can calculate a transparency-weighted mixture by setting the `transpWeight` argument to `true`.

The `overlay()` function estimates the color displayed on a TradingView chart when a specific foreground color is over a background color. This function aids in simulating stacked colors and analyzing the effects of transparency.

The `fromGradient()` and `fromMultiStepGradient()` functions calculate colors from gradients in any of the supported color spaces, providing flexible alternatives to the RGB-based color.from_gradient() function. The `fromGradient()` function calculates a color from a single gradient. The `fromMultiStepGradient()` function calculates a color from a piecewise gradient with multiple defined steps. Gradients are useful for heatmaps and for coloring plots or drawings based on value intensities.

Scheme creation

Three functions in this library calculate palettes for custom color schemes. Scripts can use these functions to create responsive color schemes that adjust to calculated values and user inputs.

The `gradientPalette()` function creates an array of colors by sampling a specified number of colors along a gradient from a base color to a target color, in fixed-size steps.

The `monoPalette()` function creates an array containing monochromatic variants (tints, tones, or shades) of a specified base color. Whether the function mixes the color toward white (for tints), a form of gray (for tones), or black (for shades) depends on the `grayLuminance` value. If unspecified, the function automatically chooses the mix behavior with the highest contrast.

The `harmonyPalette()` function creates a matrix of colors. The first column contains the base color and specified harmonies, e.g., triadic colors. The columns that follow contain tints, tones, or shades of the harmonic colors for additional color choices, similar to `monoPalette()`.

█ EXAMPLE CODE

The example code at the end of the script generates and visualizes color schemes by processing user inputs. The code builds the scheme's palette based on the "Base color" input and the additional inputs in the "Settings/Inputs" tab:

• "Palette type" specifies whether the palette uses a custom gradient, monochromatic base color variants, or color harmonies with monochromatic variants.

• "Target color" sets the top color for the "Gradient" palette type.

• The "Gray luminance" inputs determine variation behavior for "Monochromatic" and "Harmony" palette types. If "Auto" is selected, the palette mixes the base color toward white or black based on its brightness. Otherwise, it mixes the color toward the grayscale color with the specified relative luminance (from 0 to 1).

• "Harmony type" specifies the color harmony used in the palette. Each row in the palette corresponds to one of the harmonious colors, starting with the base color.

The code creates a table on the first bar to display the collection of calculated colors. Each cell in the table shows the color's `getHexString()` value in a tooltip for simple inspection.

Look first. Then leap.

█ EXPORTED FUNCTIONS

Below is a complete list of the functions and overloads exported by this library.

getRGB(source)

Retrieves the sRGB red, green, blue, and transparency components of a "color" value.

getHexString(r, g, b, t)

(Overload 1 of 2) Converts a set of sRGB channel values to a string representing the corresponding color's hexadecimal form.

getHexString(source)

(Overload 2 of 2) Converts a "color" value to a string representing the sRGB color's hexadecimal form.

hexStringToRGB(source)

Converts a string representing an sRGB color's hexadecimal form to a set of decimal channel values.

hexStringToColor(source)

Converts a string representing an sRGB color's hexadecimal form to a "color" value.

getLRGB(r, g, b, t)

(Overload 1 of 2) Converts a set of sRGB channel values to a set of linear RGB values with specified transparency information.

getLRGB(source)

(Overload 2 of 2) Retrieves linear RGB channel values and transparency information from a "color" value.

lrgbToRGB(lr, lg, lb, t)

Converts a set of linear RGB channel values to a set of sRGB values with specified transparency information.

lrgbToColor(lr, lg, lb, t)

Converts a set of linear RGB channel values and transparency information to a "color" value.

getHSL(r, g, b, t)

(Overload 1 of 2) Converts a set of sRGB channels to a set of HSL values with specified transparency information.

getHSL(source)

(Overload 2 of 2) Retrieves HSL channel values and transparency information from a "color" value.

hslToRGB(h, s, l, t)

Converts a set of HSL channel values to a set of sRGB values with specified transparency information.

hslToColor(h, s, l, t)

Converts a set of HSL channel values and transparency information to a "color" value.

getHSV(r, g, b, t)

(Overload 1 of 2) Converts a set of sRGB channels to a set of HSV values with specified transparency information.

getHSV(source)

(Overload 2 of 2) Retrieves HSV channel values and transparency information from a "color" value.

hsvToRGB(h, s, v, t)

Converts a set of HSV channel values to a set of sRGB values with specified transparency information.

hsvToColor(h, s, v, t)

Converts a set of HSV channel values and transparency information to a "color" value.

getHWB(r, g, b, t)

(Overload 1 of 2) Converts a set of sRGB channels to a set of HWB values with specified transparency information.

getHWB(source)

(Overload 2 of 2) Retrieves HWB channel values and transparency information from a "color" value.

hwbToRGB(h, w, b, t)

Converts a set of HWB channel values to a set of sRGB values with specified transparency information.

hwbToColor(h, w, b, t)

Converts a set of HWB channel values and transparency information to a "color" value.

getXYZ(r, g, b, t)

(Overload 1 of 2) Converts a set of sRGB channels to a set of XYZ values with specified transparency information.

getXYZ(source)

(Overload 2 of 2) Retrieves XYZ channel values and transparency information from a "color" value.

xyzToRGB(x, y, z, t)

Converts a set of XYZ channel values to a set of sRGB values with specified transparency information

xyzToColor(x, y, z, t)

Converts a set of XYZ channel values and transparency information to a "color" value.

getXYY(r, g, b, t)

(Overload 1 of 2) Converts a set of sRGB channels to a set of xyY values with specified transparency information.

getXYY(source)

(Overload 2 of 2) Retrieves xyY channel values and transparency information from a "color" value.

xyyToRGB(xc, yc, y, t)

Converts a set of xyY channel values to a set of sRGB values with specified transparency information.

xyyToColor(xc, yc, y, t)

Converts a set of xyY channel values and transparency information to a "color" value.

getLAB(r, g, b, t)

(Overload 1 of 2) Converts a set of sRGB channels to a set of CIELAB values with specified transparency information.

getLAB(source)

(Overload 2 of 2) Retrieves CIELAB channel values and transparency information from a "color" value.

labToRGB(l, a, b, t)

Converts a set of CIELAB channel values to a set of sRGB values with specified transparency information.

labToColor(l, a, b, t)

Converts a set of CIELAB channel values and transparency information to a "color" value.

getOKLAB(r, g, b, t)

(Overload 1 of 2) Converts a set of sRGB channels to a set of Oklab values with specified transparency information.

getOKLAB(source)

(Overload 2 of 2) Retrieves Oklab channel values and transparency information from a "color" value.

oklabToRGB(l, a, b, t)

Converts a set of Oklab channel values to a set of sRGB values with specified transparency information.

oklabToColor(l, a, b, t)

Converts a set of Oklab channel values and transparency information to a "color" value.

getLCH(r, g, b, t)

(Overload 1 of 2) Converts a set of sRGB channels to a set of CIELCh values with specified transparency information.

getLCH(source)

(Overload 2 of 2) Retrieves CIELCh channel values and transparency information from a "color" value.

lchToRGB(l, c, h, t)

Converts a set of CIELCh channel values to a set of sRGB values with specified transparency information.

lchToColor(l, c, h, t)

Converts a set of CIELCh channel values and transparency information to a "color" value.

getOKLCH(r, g, b, t)

(Overload 1 of 2) Converts a set of sRGB channels to a set of Oklch values with specified transparency information.

getOKLCH(source)

(Overload 2 of 2) Retrieves Oklch channel values and transparency information from a "color" value.

oklchToRGB(l, c, h, t)

Converts a set of Oklch channel values to a set of sRGB values with specified transparency information.

oklchToColor(l, c, h, t)

Converts a set of Oklch channel values and transparency information to a "color" value.

contrastRatio(value1, value2)

Calculates the contrast ratio between two colors values based on the formula from version 2 of the Web Content Accessibility Guidelines (WCAG).

isLightTheme(source)

Detects whether a background color represents a light theme or dark theme, based on the amount of contrast between the color and the white and black points.

grayscale(source)

Calculates the grayscale version of a color with the same relative luminance (i.e., brightness).

negative(source, colorSpace)

Calculates the negative (i.e., inverted) form of a specified color.

complement(source, colorSpace)

Calculates the complementary color for a `source` color using a cylindrical color space.

analogousColors(source, colorSpace)

Calculates the analogous colors for a `source` color using a cylindrical color space.

splitComplements(source, colorSpace)

Calculates the split-complementary colors for a `source` color using a cylindrical color space.

triadicColors(source, colorSpace)

Calculates the two triadic colors for a `source` color using a cylindrical color space.

tetradicColors(source, colorSpace, square)

Calculates the three square or rectangular tetradic colors for a `source` color using a cylindrical color space.

pentadicColors(source, colorSpace)

Calculates the four pentadic colors for a `source` color using a cylindrical color space.

hexadicColors(source, colorSpace)

Calculates the five hexadic colors for a `source` color using a cylindrical color space.

add(value1, value2, transpWeight)

Additively mixes two "color" values, with optional transparency weighting.

overlay(fg, bg)

Estimates the resulting color that appears on the chart when placing one color over another.

fromGradient(value, bottomValue, topValue, bottomColor, topColor, colorSpace)

Calculates the gradient color that corresponds to a specific value based on a defined value range and color space.

fromMultiStepGradient(value, steps, colors, colorSpace)

Calculates a multi-step gradient color that corresponds to a specific value based on an array of step points, an array of corresponding colors, and a color space.

gradientPalette(baseColor, stopColor, steps, strength, model)

Generates a palette from a gradient between two base colors.

monoPalette(baseColor, grayLuminance, variations, strength, colorSpace)

Generates a monochromatic palette from a specified base color.

harmonyPalette(baseColor, harmonyType, grayLuminance, variations, strength, colorSpace)

Generates a palette consisting of harmonious base colors and their monochromatic variants.

Topological Market Stress (TMS) - Quantum FabricTopological Market Stress (TMS) - Quantum Fabric

What Stresses The Market?

Topological Market Stress (TMS) represents a revolutionary fusion of algebraic topology and quantum field theory applied to financial markets. Unlike traditional indicators that analyze price movements linearly, TMS examines the underlying topological structure of market data—detecting when the very fabric of market relationships begins to tear, warp, or collapse.

Drawing inspiration from the ethereal beauty of quantum field visualizations and the mathematical elegance of topological spaces, this indicator transforms complex mathematical concepts into an intuitive, visually stunning interface that reveals hidden market dynamics invisible to conventional analysis.

Theoretical Foundation: Topology Meets Markets

Topological Holes in Market Structure

In algebraic topology, a "hole" represents a fundamental structural break—a place where the normal connectivity of space fails. In markets, these topological holes manifest as:

Correlation Breakdown: When traditional price-volume relationships collapse

Volatility Clustering Failure: When volatility patterns lose their predictive power

Microstructure Stress: When market efficiency mechanisms begin to fail

The Mathematics of Market Topology

TMS constructs a topological space from market data using three key components:

1. Correlation Topology

ρ(P,V) = correlation(price, volume, period)

Hole Formation = 1 - |ρ(P,V)|

When price and volume decorrelate, topological holes begin forming.

2. Volatility Clustering Topology

σ(t) = volatility at time t

Clustering = correlation(σ(t), σ(t-1), period)

Breakdown = 1 - |Clustering|

Volatility clustering breakdown indicates structural instability.

3. Market Efficiency Topology

Efficiency = |price - EMA(price)| / ATR

Measures how far price deviates from its efficient trajectory.

Multi-Scale Topological Analysis

Markets exist across multiple temporal scales simultaneously. TMS analyzes topology at three distinct scales:

Micro Scale (3-15 periods): Immediate structural changes, market microstructure stress

Meso Scale (10-50 periods): Trend-level topology, medium-term structural shifts

Macro Scale (50-200 periods): Long-term structural topology, regime-level changes

The final stress metric combines all scales:

Combined Stress = 0.3×Micro + 0.4×Meso + 0.3×Macro

How TMS Works

1. Topological Space Construction

Each market moment is embedded in a multi-dimensional topological space where:

- Price efficiency forms one dimension

- Correlation breakdown forms another

- Volatility clustering breakdown forms the third

2. Hole Detection Algorithm

The indicator continuously scans this topological space for:

Hole Formation: When stress exceeds the formation threshold

Hole Persistence: How long structural breaks maintain

Hole Collapse: Sudden topology restoration (regime shifts)

3. Quantum Visualization Engine

The visualization system translates topological mathematics into intuitive quantum field representations:

Stress Waves: Main line showing topological stress intensity

Quantum Glow: Surrounding field indicating stress energy

Fabric Integrity: Background showing structural health

Multi-Scale Rings: Orbital representations of different timeframes

4. Signal Generation

Stable Topology (✨): Normal market structure, standard trading conditions

Stressed Topology (⚡): Increased structural tension, heightened volatility expected

Topological Collapse (🕳️): Major structural break, regime shift in progress

Critical Stress (🌋): Extreme conditions, maximum caution required

Inputs & Parameters

🕳️ Topological Parameters

Analysis Window (20-200, default: 50)

Primary period for topological analysis

20-30: High-frequency scalping, rapid structure detection

50: Balanced approach, recommended for most markets

100-200: Long-term position trading, major structural shifts only

Hole Formation Threshold (0.1-0.9, default: 0.3)

Sensitivity for detecting topological holes

0.1-0.2: Very sensitive, detects minor structural stress

0.3: Balanced, optimal for most market conditions

0.5-0.9: Conservative, only major structural breaks

Density Calculation Radius (0.1-2.0, default: 0.5)

Radius for local density estimation in topological space

0.1-0.3: Fine-grained analysis, sensitive to local changes

0.5: Standard approach, balanced sensitivity

1.0-2.0: Broad analysis, focuses on major structural features

Collapse Detection (0.5-0.95, default: 0.7)