Alternative Daily Reference Points for Intra-hour ChartsThis is a different version of my www.tradingview.com used high, lows and pivots. One problem with pivot points is the number of calculation methods. The alternative version shows historical lows, closes, highs one basic period back.

► On lower timeframes - hour or less - this will show High, Low and Close from the previous day, two days ago, the previous week and two weeks ago and VWAP.

► On 1h daily reference points need to be enabled. On higher timeframes, daily reference points will not be shown. On the daily chart, weekly levels need to be enabled to still show and will be disabled on all higher periods.

► It is configured only for normal timeframes. If you use something like 17-minutes timeframe, you will have to allow this timeframe in the code.

Bear in mind, using all lines at the same time can be a little confusing and price doesn't react to every one of them. You can probably disable lows in the uptrend or scratch closes to simplify your chart.

Have a great trade!

"vwap" için komut dosyalarını ara

Price Deviation from vwapIt indicate the deviation of avg price from vwap. It is best use with 5 min candlestick

OHLC/GAP/EMA/VWAP all in oneThis script will plot the current open and previous high low and close. The overnight gap between the current open and the previous close is highlighted. Also included is the 10 EMA, 20 EMA and the VWAP. This is good for people who are limited on the amount of indicators they can use.

EMA + VWAP Strategy# EMA + VWAP Crossover Strategy

## Overview

This is a trend-following intraday strategy that combines fast and slow EMAs with VWAP to identify high-probability entries. It's designed primarily for 5-15 minute charts and includes a smart filter to avoid trading when VWAP is ranging flat.

## How It Works

### Core Concept

The strategy uses three main components working together:

- **Fast EMA (9)** - Responds quickly to price changes and generates entry signals

- **Slow EMA (21)** - Acts as a trend filter to keep you on the right side of the market

- **VWAP** - Serves as a dynamic support/resistance level and the primary trigger for entries

### Entry Rules

**Long Entry:**

- EMA 9 crosses above VWAP (bullish momentum)

- EMA 9 is above EMA 21 (confirming uptrend)

- VWAP has a clear directional slope (not flat/ranging)

- Only during weekdays (Monday-Friday)

**Short Entry:**

- EMA 9 crosses below VWAP (bearish momentum)

- EMA 9 is below EMA 21 (confirming downtrend)

- VWAP has a clear directional slope (not flat/ranging)

- Only during weekdays (Monday-Friday)

### The VWAP Flat Filter

One of the key features is the VWAP slope filter. When VWAP is moving sideways (flat), it indicates the market is likely consolidating or ranging. The strategy skips these periods because crossover signals tend to be less reliable in choppy conditions. You'll see small gray diamonds at the top of the chart when VWAP is considered flat.

### Risk Management

The strategy uses a proper risk-reward approach with multiple stop loss options:

1. **ATR-Based (Recommended)** - Adapts to market volatility automatically. Default is 1.5x ATR(14), which gives your trades room to breathe while protecting capital.

2. **Swing Low/High** - Places stops at recent price structure points for a more technical approach.

3. **Slow EMA** - Uses the trend-defining EMA as your stop level, good for trend-following with wider stops.

4. **Fixed Percentage** - Simple percentage-based stops if you prefer consistency.

Take profits are automatically calculated based on your risk-reward ratio (default 2:1), meaning if you risk $100, you're aiming to make $200.

### Weekday Trading Filter

The strategy includes an option to trade only Monday through Friday. This is particularly useful for crypto markets where weekend liquidity can be thin and price action more erratic. You can toggle this on/off to test whether avoiding weekends improves your results.

### Visual Features

- **Color-coded background** - Green tint when EMA 9 is above EMA 21 (bullish bias), red tint when below (bearish bias)

- **ATR bands** - Dotted lines showing where stops would be placed (when using ATR stops)

- **Active trade levels** - Solid red line for your stop loss, green line for your take profit when you're in a position

- **Weekend highlighting** - Gray background on Saturdays and Sundays when weekday filter is active

## Best Practices

**Timeframe:** Designed for 5-minute charts but can be adapted to other intraday timeframes.

**Markets:** Works on any liquid market - stocks, forex, crypto, futures. Just make sure there's enough volume.

**Position Sizing:** The strategy uses percentage of equity by default. Adjust based on your risk tolerance.

**Backtesting Tips:**

- Test with and without the weekday filter to see which performs better on your instrument

- Try different ATR multipliers (1.0-2.5) to find the sweet spot between stop-outs and letting profits run

- Experiment with risk-reward ratios (1.5R, 2R, 3R) to optimize for your win rate

**What to Watch:**

- Win rate vs. profit factor balance

- How many trades are filtered out by the VWAP flat condition

- Performance difference between weekdays and weekends

- Whether the trend filter (EMA 21) is keeping you out of bad trades

## Parameters You Can Adjust

- Fast EMA length (default 9)

- Slow EMA length (default 21)

- VWAP flat threshold (default 0.01%)

- Stop loss type and parameters

- Risk-reward ratio

- Weekday trading on/off

- ATR length and multiplier

## Disclaimer

This strategy is for educational purposes. Past performance doesn't guarantee future results. Always test thoroughly on historical data and paper trade before risking real money. Use proper position sizing and never risk more than you can afford to lose.

---

*Built with Pine Script v5 for TradingView*

AMT VWAP [hardi]█ OVERVIEW

AMT VWAP is a clean, minimalist VWAP indicator with Standard Deviation bands, designed to complement the Auction Market Theory (AMT) trading methodology by Fabio Valentino.

This indicator focuses on one thing and does it well: displaying VWAP and its deviation bands clearly on your chart.

█ FEATURES

- Daily VWAP with automatic reset

- ±1 Standard Deviation bands (cyan)

- ±2 Standard Deviation bands (orange) - extreme zones

- Clean labels that don't clutter your chart

- Info table showing current bias and zone

- Compact Mode for mobile/smartphone users

- Fully customizable colors and settings

- Built-in alerts for all levels

█ HOW TO USE

VWAP (Volume Weighted Average Price) represents the "fair value" where most volume has transacted. In AMT methodology:

BIAS DETERMINATION:

- Price ABOVE VWAP = Bullish bias (buyers in control)

- Price BELOW VWAP = Bearish bias (sellers in control)

TRADING ZONES:

- ±1 SD: Normal deviation zone - potential mean reversion area

- ±2 SD: Extreme zone - high probability reversal area (95%+ reversion rate)

ENTRY STRATEGIES:

1. Trend Following: Buy pullbacks to VWAP in uptrend, sell rallies to VWAP in downtrend

2. Mean Reversion: Fade moves at ±2 SD bands with confirmation

█ RECOMMENDED SETUP

Use this indicator together with:

- TradingView's built-in "SVP HD" (Session Volume Profile) for POC/VAH/VAL levels

- AMT CVD indicator (companion indicator) for order flow analysis

This combination gives you the complete AMT toolkit:

- SVP HD → Key levels (POC, VAH, VAL)

- AMT VWAP → Dynamic support/resistance & bias

- AMT CVD → Aggression, Absorption, Exhaustion signals

█ SETTINGS

Display Settings:

- Compact Mode - Enable for cleaner mobile view

- Show Labels - Toggle level labels

- Label Size - Adjust for your screen

VWAP Settings:

- Band Multipliers - Adjust SD band distance (default: 1.0 and 2.0)

- Colors - Fully customizable

- Line widths - Adjust visibility

Alerts:

- Near VWAP

- Near ±1 SD

- Near ±2 SD (extreme zones)

█ METHODOLOGY

This indicator is based on Auction Market Theory as taught by Fabio Valentino:

"The market is a continuous auction seeking fair value. VWAP represents this fair value dynamically throughout the session. Deviations from VWAP create trading opportunities as price tends to revert to the mean."

Key principles:

- Read, don't predict

- Location over technique

- Evidence-based entries

█ ALERTS

Set alerts for:

- Price approaching VWAP (potential support/resistance)

- Price at ±1 SD (first deviation - watch for reaction)

- Price at ±2 SD (extreme - high probability reversal zone)

█ NOTES

- Works on all timeframes

- Best used on 15m for intraday entries

- VWAP resets daily at market open

- Combine with volume profile for best results

█ CREDITS

Based on Auction Market Theory methodology by Fabio Valentino.

Indicator developed for the trading community.

If you find this useful, please leave a like! 👍

vwap, volume-weighted-average-price, standard-deviation, bands, auction-market-theory, amt, fabio-valentino, mean-reversion, trend-following, intraday, day-trading, support-resistance, fair-value

Kalman VWAP Filter [BackQuant]Kalman VWAP Filter

A precision-engineered price estimator that fuses Kalman filtering with the Volume-Weighted Average Price (VWAP) to create a smooth, adaptive representation of fair value. This hybrid model intelligently balances responsiveness and stability, tracking trend shifts with minimal noise while maintaining a statistically grounded link to volume distribution.

If you would like to see my original Kalman Filter, please find it here:

Concept overview

The Kalman VWAP Filter is built on two core ideas from quantitative finance and control theory:

Kalman filtering — a recursive Bayesian estimator used to infer the true underlying state of a noisy system (in this case, fair price).

VWAP anchoring — a dynamic reference that weights price by traded volume, representing where the majority of transactions have occurred.

By merging these concepts, the filter produces a line that behaves like a "smart moving average": smooth when noise is high, fast when markets trend, and self-adjusting based on both market structure and user-defined noise parameters.

How it works

Measurement blend : Combines the chosen Price Source (e.g., close or hlc3) with either a Session VWAP or a Rolling VWAP baseline. The VWAP Weight input controls how much the filter trusts traded volume versus price movement.

Kalman recursion : Each bar updates an internal "state estimate" using the Kalman gain, which determines how much to trust new observations vs. the prior state.

Noise parameters :

Process Noise controls agility — higher values make the filter more responsive but also more volatile.

Measurement Noise controls smoothness — higher values make it steadier but slower to adapt.

Filter order (N) : Defines how many parallel state estimates are used. Larger orders yield smoother output by layering multiple one-dimensional Kalman passes.

Final output : A refined price trajectory that captures VWAP-adjusted fair value while dynamically adjusting to real-time volatility and order flow.

Why this matters

Most smoothing techniques (EMA, SMA, Hull) trade off lag for smoothness. Kalman filtering, however, adaptively rebalances that tradeoff each bar using probabilistic weighting, allowing it to follow market state changes more efficiently. Anchoring it to VWAP integrates microstructure context — capturing where liquidity truly lies rather than only where price moves.

Use cases

Trend tracking : Color-coded candle painting highlights shifts in slope direction, revealing early trend transitions.

Fair value mapping : The line represents a continuously updated equilibrium price between raw price action and VWAP flow.

Adaptive moving average replacement : Outperforms static MAs in variable volatility regimes by self-adjusting smoothness.

Execution & reversion logic : When price diverges from the Kalman VWAP, it may indicate short-term imbalance or overextension relative to volume-adjusted fair value.

Cross-signal framework : Use with standard VWAP or other filters to identify convergence or divergence between liquidity-weighted and state-estimated prices.

Parameter guidance

Process Noise : 0.01–0.05 for swing traders, 0.1–0.2 for intraday scalping.

Measurement Noise : 2–5 for normal use, 8+ for very smooth tracking.

VWAP Weight : 0.2–0.4 balances both price and VWAP influence; 1.0 locks output directly to VWAP dynamics.

Filter Order (N) : 3–5 for reactive short-term filters; 8–10 for smoother institutional-style baselines.

Interpretation

When price > Kalman VWAP and slope is positive → bullish pressure; buyers dominate above fair value.

When price < Kalman VWAP and slope is negative → bearish pressure; sellers dominate below fair value.

Convergence of price and Kalman VWAP often signals equilibrium; strong divergence suggests imbalance.

Crosses between Kalman VWAP and the base VWAP can hint at shifts in short-term vs. long-term liquidity control.

Summary

The Kalman VWAP Filter blends statistical estimation with market microstructure awareness, offering a refined alternative to static smoothing indicators. It adapts in real time to volatility and order flow, helping traders visualize balance, transition, and momentum through a lens of probabilistic fair value rather than simple price averaging.

Institutional Rolling VWAPs • 3 lines + editable σ bands3 rolling vwaps, time stamped, same on htf and lft for high level execution

Technical Summary VWAP | RSI | VolatilityTechnical Summary VWAP | RSI | Volatility

The Quantum Trading Matrix is a multi-dimensional market-analysis dashboard designed as an educational and idea-generation tool to help traders read price structure, participation, momentum and volatility in one compact view. It is not an automated execution system; rather, it aggregates lightweight “quantum” signals — VWAP position, momentum oscillator behaviour, multi-EMA trend scoring, volume flow and institutional activity heuristics, market microstructure pivots and volatility measures — and synthesizes them into a single, transparent score and signal recommendation. The primary goal is to make explicit why a given market looks favourable or unfavourable by showing the individual ingredients and how they combine, enabling traders to learn, test and form rules based on observable market mechanics.

Each module of the matrix answers a distinct market question. VWAP and its percentage distance indicate whether the current price is trading above or below the intraday volume-weighted average — a proxy for intraday institutional control and value. The quantum momentum oscillator (fast and slow EMA difference scaled to percent) captures short-to-intermediate momentum shifts, providing a quickly responsive view of directional pressure. Multi-EMA trend scoring (8/21/50) produces a simple, transparent trend score by counting conditions such as price above EMAs and cross-EMAs ordering; this score is used to categorize market trend into descriptive buckets (e.g., STRONG UP, WEAK UP, NEUTRAL, DOWN). Volume analysis compares current volume to a recent moving average and computes a Z-score to detect spikes and unusual participation; additional buy/sell pressure heuristics (buyingPressure, sellingPressure, flowRatio) estimate whether upside or downside participation dominates the bar. Institutional activity is approximated by flagging large orders relative to volume baseline (e.g., volume > 2.5× MA) and estimating a dark pool proxy; this is a heuristic to highlight bars that likely had large players involved.

The dashboard also performs market-structure detection with small pivot windows to identify recent local support/resistance areas and computes price position relative to the daily high/low (dailyMid, pricePosition). Volatility is measured via ATR divided by price and bucketed into LOW/NORMAL/HIGH/EXTREME categories to help you adapt stop sizing and expectational horizons. Finally, all these pieces feed an interpretable scoring function that rewards alignment: VWAP above, strong flow ratio, bullish trend score, bullish momentum, and favorable RSI zone add to the overall score which is presented as a 0–100 metric and a colored emoji indicator for at-a-glance assessment.

The mashup is purposeful: each indicator covers a failure mode of the other. For example, momentum readings can be misleading during volatility spikes; VWAP informs whether institutions are on the bid or offer; volume Z-score detects abnormal participation that can validate a breakout; multi-EMA score mitigates single-EMA whipsaws by requiring a combination of price/EMA conditions. Combining these signals increases information content while keeping each component explainable — a key compliance requirement. The script intentionally emphasizes transparency: when it shows a BUY/SELL/HOLD recommendation, the dashboard shows the underlying sub-components so a trader can see whether VWAP, momentum, volume, trend or structure primarily drove the score.

For practical use, adopt a clear workflow: (1) check the matrix score and read the component tiles (VWAP position, momentum, trend and volume) to understand the drivers; (2) confirm market-structure support/resistance and pricePosition relative to the daily range; (3) require at least two corroborating components (for example, VWAP ABOVE + Momentum BULLISH or Volume spike + Trend STRONG UP) before considering entries; (4) use ATR-based stops or daily pivot distance for stop placement and size positions such that the trade risks a small, pre-defined percent of capital; (5) for intraday scalps shorten holding time and tighten stops, for swing trades increase lookback lengths and require multi-timeframe (higher TF) agreement. Treat the matrix as an idea filter and replay lab: when an alert triggers, replay the bars and observe which components anticipated the move and which lagged.

Parameter tuning matters. Shortening the momentum length makes the oscillator more sensitive (useful for scalping), while lengthening it reduces noise for swing contexts. Volume profile bars and MA length should match the instrument’s liquidity — increase the MA for low-liquidity stocks to reduce false institutional flags. The trend multiplier and signal sensitivity parameters let you calibrate how aggressively the matrix counts micro evidence into the score. Always backtest parameter sets across multiple periods and instruments; run walk-forward tests and keep a simple out-of-sample validation window to reduce overfitting risk.

Limitations and failure modes are explicit: institutional flags and dark-pool estimates are heuristics and cannot substitute for true tape or broker-level order flow; volume split by price range is an approximation and will not perfectly reflect signed volume; pivot detection with small windows may miss larger structural swings; VWAP is typically intraday-centric and less meaningful across multi-day swing contexts; the score is additive and may not capture non-linear relationships between features in extreme market regimes (e.g., flash crashes, circuit breaker events, or overnight gaps). The matrix is also susceptible to false signals during major news releases when price and volume behavior dislocate from typical patterns. Users should explicitly test behavior around earnings, macro data and low-liquidity periods.

To learn with the matrix, perform these experiments: (A) collect all BUY/SELL alerts over a 6-month period and measure median outcome at 5, 20 and 60 bars; (B) require additional gating conditions (e.g., only accept BUY when flowRatio>60 and trendScore≥4) and compare expectancy; (C) vary the institutional threshold (2×, 2.5×, 3× volumeMA) to see how many true positive spikes remain; (D) perform multi-instrument tests to ensure parameters are not tuned to a single ticker. Document every test and prefer robust, slightly lower returns with clearer logic rather than tuned “optimal” results that fail out of sample.

Originality statement: This script’s originality lies in the curated combination of intraday value (VWAP), multi-EMA trend scoring, momentum percent oscillator, volume Z-score plus buy/sell flow heuristics and a compact, interpretable scoring system. The script is not a simple indicator mashup; it is a didactic ensemble specifically designed to make internal rationale visible so traders can learn how each market characteristic contributes to actionable probability. The tool’s novelty is its emphasis on interpretability — showing the exact contributing signals behind a composite score — enabling reproducible testing and educational value.

Finally, for TradingView publication, include a clear description listing the modules, a short non-technical summary of how they interact, the tunable inputs, limitations and a risk disclaimer. Remove any promotional content or external contact links. If you used trademark symbols, either provide registration details or remove them. This transparent documentation satisfies TradingView’s requirement that mashups justify their composition and teach users how to use them.

Quantum Trading Matrix — multi-factor intraday dashboard (educational use only).

Purpose: Combines intraday VWAP position, a fast/slow EMA momentum percent oscillator, multi-EMA trend scoring (8/21/50), volume Z-score and buy/sell flow heuristics, pivot-based microstructure detection, and ATR-based volatility buckets to produce a transparent, componentized market score and trade-idea indicator. The mashup is intentional: VWAP identifies intraday value, momentum detects short bursts, EMAs provide structural trend bias, and volume/flow confirm participation. Signals require alignment of at least two components (for example, VWAP ABOVE + Momentum BULLISH + positive flow) for higher confidence.

Inputs: momentum period, volume MA/profile length, EMA configuration (8/21/50), trend multiplier, signal sensitivity, color and display options. Use shorter momentum lengths for scalps and longer for swing analysis. Increase volume MA for thinly traded instruments.

Limitations: Institutional/dark-pool estimates and flow heuristics are approximations, not actual exchange tape. VWAP is intraday-focused. Expect false signals during major news or low-liquidity sessions. Backtest and paper-trade before applying real capital.

Risk Disclaimer: For education and analysis only. Not financial advice. Use proper risk management. The author is not responsible for trading losses.

________________________________________

Risk & Misuse Disclaimer

This indicator is provided for education, analysis and idea generation only. It is not investment or financial advice and does not guarantee profits. Institutional activity flags, dark-pool estimates and flow heuristics are approximations and should not be treated as exchange tape. Backtest thoroughly and use demo/paper accounts before trading real capital. Always apply appropriate position sizing and stop-loss rules. The author is not responsible for any trading losses resulting from the use or misuse of this tool.

________________________________________

Risk Disclaimer: This tool is provided for education and analysis only. It is not financial advice and does not guarantee returns. Users assume all risk for trades made based on this script. Back test thoroughly and use proper risk management.

Uptrick: Zero Lag HMA Trend Suite1. Name and Purpose

Uptrick: Zero Lag HMA Trend Suite is a Pine Version 6 script that builds upon the Hull Moving Average (HMA) to offer an advanced trend analysis tool. Its purpose is to help traders identify trend direction, potential reversals, and overall market momentum with reduced lag compared to traditional moving averages. By combining the HMA with Average True Range (ATR) thresholds, slope-dependent coloring, Volume Weighted Average Price (VWAP) ribbons, and optional reversal signals, the script aims to give a detailed view of price activity in various market environments.

2. Overview

This script begins with the calculation of a Hull Moving Average, a method that blends Weighted Moving Averages in a way designed to cut down on lag while still smoothing out price fluctuations. Next, several enhancements are applied. The script compares current HMA values to previous ones for slope-based coloring, which highlights uptrends and downtrends at a glance. It also plots buy and sell signals when price moves beyond or below thresholds determined by the ATR and the user’s chosen signal multiplier. An optional VWAP ribbon can be shown to confirm bullish or bearish conditions relative to a volume-weighted benchmark. Additionally, the script can plot reversal signals (labeled with B) at points where price crosses back toward the HMA from above or below. Taken together, these elements allow traders to visualize both the short-term momentum and the broader context of how price interacts with volatility and overall market direction.

3. Why These Indicators Have Been Linked Together

The reason the Hull Moving Average, the Average True Range, and the VWAP have been integrated into one script is to tackle multiple facets of market analysis in a single tool. The Zero Lag Hull Moving Average provides a responsive trend line, the ATR offers a measure of volatility that helps distinguish significant price shifts from typical fluctuations, and the VWAP acts as a reference for fair value based on traded volume. By layering all three, the script helps traders avoid the need to juggle multiple separate indicators and offers a holistic perspective. The slope-based coloring focuses on trend direction, the ATR-based thresholds refine possible buy and sell zones, and the VWAP ribbons provide insight into how price stands relative to an important volume-weighted level. The inclusion of up and down signals and reversal B labels further refines entries and exits.

4. Why Use Uptrick: Zero Lag HMA Trend Suite

The Hull Moving Average is already known for reacting more quickly to price changes compared to other moving averages while retaining a degree of smoothness. This suite enhances the basic HMA by showing colored gradients that make it easy to spot trend direction changes, highlighting potential entry or exit points based on volatility-driven thresholds, and optionally layering a volume-based measure of bullish or bearish market sentiment. By relying on a zero lag approach and additional data points, the script caters to those wanting a more responsive method of identifying shifts in market dynamics. The added reversal signals and up or down alerts give traders extra confirmation for potential turning points.

5. How This Extension Improves on the Basic HMA

This extension not only plots the Hull Moving Average but also includes data-driven alerts and visual cues that traditional HMA lines do not provide. First, it offers multi-layered slope coloring, making up or down trends quickly apparent. Second, it uses ATR-based thresholds to pinpoint moments when price may be extending beyond normal volatility, thus generating buy or sell signals. Third, the script introduces an optional VWAP ribbon to indicate whether the market is trading above or below this pivotal volume-weighted benchmark, adding a further confirmation step for bullish or bearish conditions. Finally, it incorporates optional reversal signals labeled with B, indicating points where price might swing back toward the main HMA line.

6. Core Components

The script can be broken down into several primary functions and features.

a. Zero Lag HMA Calculation

Uses two Weighted Moving Averages (half-length and full-length) combined through a smoothing step based on the square root of the chosen length. This approach is designed to reduce lag significantly compared to other moving averages.

b. Slope Detection

Compares current and prior HMA values to determine if the trend is up or down. The slope-based coloring changes between turquoise shades for upward movement and magenta shades for downward movement, making trend direction immediately visible.

c. ATR-Based Thresholding for Up and Down Signals

The script calculates an Average True Range over a user-defined period, then multiplies it by a signal factor to form two bands around the HMA. When price crosses below the lower band, an up (buy) signal appears; when it crosses above the upper band, a down (sell) signal is shown.

d. Reversal Signals (B Labels)

Tracks when price transitions back toward the main HMA from an extreme zone. When enabled, these reversal points are labeled with a B and can help traders see potential turning points or mean-reversion setups.

e. VWAP Bands

An optional Volume Weighted Average Price ribbon that plots above or below the HMA, indicating bullish or bearish conditions relative to a volume-weighted price benchmark. This can also act as a kind of support/ resistance.

7. User Inputs

a. HMA Length

Controls how quickly the moving average responds to price changes. Shorter lengths react faster but can lead to more frequent signals, whereas longer lengths produce smoother lines.

b. Source

Specifies the price input, such as close or an alternative source, for the calculation. This can help align the HMA with specific trading strategies.

c. ATR Length and Signal Multiplier

Defines how the script calculates average volatility and sets thresholds for buy or sell alerts. Adjusting these values can help filter out noise or highlight more aggressive signals.

d. Slope Index

Determines how many bars to look back for detecting slope direction, influencing how sensitive the slope coloring is to small fluctuations.

e. Show Buy and Sell Signals, Reversal Signals, and VWAP

Lets users toggle the display of these features. Turning off certain elements can reduce chart clutter if traders prefer a simpler layout.

8. Calculation Process

The script’s calculation follows a step-by-step approach. It first computes two Weighted Moving Averages of the selected price source, one over half the specified length and one over the full length. It then combines these using 2*wma1 minus wma2 to reduce lag, followed by applying another weighted average using the square root of the length. Simultaneously, it computes the ATR for a user-defined period. By multiplying ATR by the signal multiplier, it establishes upper and lower bands around the HMA, where crossovers generate buy (up) or sell (down) signals. The script can also plot reversal signals (B labels) when price crosses back from these bands in the opposite direction. For the optional VWAP feature, Pine Script’s ta.vwap function is used, and differences between the HMA and VWAP levels determine the color and opacity of the ribbon.

9. Signal Generation and Filtering

The ATR-based thresholds reduce the influence of small, inconsequential price swings. When price falls below the lower band, the script issues an up (buy) signal. If price breaks above the upper band, a down (sell) signal appears. These signals are visible through labels placed near the bars. Reversal signals, labeled with B, can be turned on to help detect when price retraces from an extended area back toward the main HMA line. Traders can disable or enable these signals to match their preferred level of chart detail or risk tolerance.

10. Visualization on the Chart

The Zero HMA Lag Trend Suite aims for visual clarity. The HMA line is plotted multiple times with increasing transparency to create a gradient effect. Turquoise gradients indicate upward slopes, and magenta gradients signify downward slopes. Bar coloring can be configured to align with the slope direction, providing quick insight into current momentum. When enabled, buy or sell labels are placed under or above the bars as price crosses the ATR-defined boundaries. If the reversal option is active, B labels appear around areas where price changes direction. The optional VWAP ribbons form background bands, using distinct coloration to signal whether price is above or below the volume-weighted metric.

11. Market Adaptability

Because the script’s parameters (HMA length, ATR length, signal multiplier, and slope index) are user-configurable, it can adapt to a wide range of markets and timeframes. Intraday traders may prefer a shorter HMA length for quick signals, while swing or position traders might use a longer HMA length to filter out short-lived price changes. The source setting can also be adjusted, allowing for specialized data inputs beyond just close or open values.

12. Risk Management Considerations

The script’s signals and labels are based on past price data and volatility readings, and they do not guarantee profitable outcomes. Sharp market reversals or unforeseen fundamental events can produce false signals. Traders should combine this tool with broader risk management strategies, including stop-loss placement, position sizing, and independent market analyses. The Zero HMA Lag Trend Suite can help highlight potential opportunities, but it should not be relied upon as the sole basis for trade decisions.

13. Combining with Other Tools

Many traders choose to verify signals from the Zero HMA Lag Trend Suite using popular indicators like the Relative Strength Index (RSI), Moving Average Convergence Divergence (MACD), or even simple volume-based metrics to confirm whether a price movement has sufficient momentum. Conventional techniques such as support and resistance levels, chart patterns, or candlestick analysis can also supplement signals generated by the script’s up, down, or reversal B labels.

14. Parameter Customization and Examples

a. Short-Term Day Trading

Using a shorter HMA length (for instance, 9 or 14) and a slightly higher ATR multiplier might provide timely buy and sell signals, though it may also produce more whipsaws in choppy markets.

b. Swing or Position Trading

Selecting a longer HMA length (such as 50 or 100) with a moderate ATR multiplier can help users track more significant and sustained market moves, potentially reducing the effect of minor fluctuations.

c. Multiple Timeframe Blends

Some traders load two versions of the indicator on the same chart, one for short-term signals (with frequent B label reversals) and another for the broader trend direction, aligning entry and exit decisions with the bigger picture.

15. Realistic Expectations

Even though the Hull Moving Average helps minimize lag and the script incorporates volatility-based filters and optional VWAP overlays, it cannot predict future market behavior with complete accuracy. Periods of low liquidity or sudden market shocks can still lead to signals that do not reflect longer-term trends. Frequent parameter review and manual confirmation are advised before executing trades based solely on the script’s outputs.

16. Theoretical Background

The Hull Moving Average formula aims to balance smoothness with reactivity, accomplished by combining Weighted Moving Averages at varying lengths. By subtracting a slower average from a faster one and then applying another smoothing step with the square root of the original length, the HMA is designed to respond more promptly to price changes than typical exponential or simple moving averages. The ATR component, introduced by J. Welles Wilder, calculates the average range of price movement over a user-defined period, allowing the script to assess volatility and adapt signals accordingly. VWAP provides a volume-weighted benchmark that many institutional traders track to gauge fair intraday value.

17. Originality and Uniqueness

Although multiple HMA-based indicators can be found, Uptrick: Zero Lag HMA Trend Suite sets itself apart by merging slope-based coloring, ATR thresholds, VWAP ribbons, up or down labels, and optional reversal signals all in one cohesive platform. This synergy aims to reduce chart clutter while still giving traders a comprehensive look at trend direction, volatility, and volume-based sentiment.

18. Summary

Uptrick: Zero Lag HMA Trend Suite is a specialized trading script designed to highlight potential market trends and reversals with minimal delay. It leverages the Hull Moving Average for an adaptive yet smooth price line, pairs ATR-based thresholds for detecting possible breakouts or dips, and provides VWAP-based ribbons for added volume-weighted context. Traders can further refine their entries and exits by enabling up or down signals and reversal labels (B) where price may revert toward the HMA. Suitable for a wide range of timeframes and instrument types, the script encourages a disciplined approach to trade management and risk control.

19. Disclaimer

This script is provided for informational and educational purposes only. Trading and investing involve significant financial risk, and no indicator can guarantee success under all conditions. Users should practice robust risk management, including the placement of stop losses and position sizing, and should confirm signals with additional analysis tools. The developer of this script assumes no liability for any trading decisions or outcomes resulting from its use.

BK Multiple MA, RMA, SMA, HMA, VWAP, Rolling VWAP **Indicator Description**

I’m incredibly proud to introduce my third indicator to the TradingView community: **BK Multiple MA with HMA, VWAP, and Rolling VWAP**! This tool has been a game-changer in my trading strategy, and I’m excited to share it with others who are navigating the markets.

This indicator holds a special place in my heart because it represents the first technical analysis concept introduced to me by my mentor when I began apprenticing under him. His wisdom, guidance, and passion for trading—and for life—left an indelible mark on my journey. I dedicate this work, and every indicator I introduce, to the foundation he helped me build, while giving glory first and foremost to God.

**Moving Averages (MAs)** are one of the most widely used tools in technical analysis, and this indicator takes them to the next level. It allows you to plot **six fully customizable moving averages simultaneously**, with options including:

- **Exponential Moving Average (EMA)**

- **Simple Moving Average (SMA)**

- **Relative Moving Average (RMA)**

- **Hull Moving Average (HMA)**

- **Volume Weighted Average Price (VWAP)**

- **Rolling VWAP**

This flexibility makes the indicator highly versatile, whether you’re a day trader, swing trader, or long-term investor. By customizing periods, colors, and line widths for each MA, you can tailor the indicator to perfectly suit your trading style.

**Key Features**

1. **Six Fully Customizable MAs**:

- Adjust periods, line colors, and widths to match your preferences.

- Select from EMA, SMA, RMA, HMA, VWAP, or Rolling VWAP for each line.

2. **Unique Rolling VWAP Option**:

- Rolling VWAP calculates the volume-weighted average price over a user-defined period, such as 200 candles.

- This feature is ideal for traders seeking volume-weighted levels that don’t reset with each session, making it invaluable for trend-following and swing trading.

3. **HMA for Smoother Trends**:

- The Hull Moving Average (HMA) is designed to reduce lag and provide a responsive, noise-free view of price trends.

- It’s a powerful tool for spotting reversals and confirming directional momentum.

4. **Session VWAP**:

- Traditional VWAP resets with each trading session, making it a reliable benchmark for intraday support and resistance levels.

**How It Works**

- **VWAP**: Reflects the average price weighted by volume for the current trading session, commonly used by institutional traders to identify key price levels.

- **Rolling VWAP**: Extends VWAP functionality by calculating over a user-defined period, allowing for flexible multi-timeframe analysis.

- **HMA**: A fast, smooth moving average that reacts quickly to price changes while filtering out noise.

The combination of these options provides traders with a comprehensive view of market dynamics, enabling better decision-making.

**Final Thoughts**

This indicator is deeply meaningful to me because it represents the first concept my mentor introduced when I began apprenticing under him. His wisdom, guidance, and passion for trading—and for life—left an indelible mark on my journey. I dedicate this work, and every indicator I introduce, to the foundation he helped me build, while giving glory first and foremost to God.

If this indicator helps you succeed, I humbly ask that you honor the blessings in your life by giving back—whether through acts of kindness, philanthropy, or helping others in need.

May the Almighty guide us all toward wisdom and success in our endeavors. All glory belongs to God!

MERCURY by DrAbhiramSivprasad"MERCURY by DrAbhiramSivprasad"

Developed from over 10 years of personal trading experience, the Mercury Indicator is a strategic tool designed to enhance accuracy in trading decisions. Think of it as a guiding light—a supportive tool that helps traders refine and build more robust strategies by integrating multiple powerful elements into a single indicator. I’ll be sharing some examples to illustrate how I use this indicator in my own trading journey, highlighting its potential to improve strategy accuracy.

Reason behind the combination of emas , cpr and vwap is it provides very good support and resistance in my trading carrier so now i brought them together in one plate

How It Works:

Mercury combines three essential elements—EMA, VWAP, and CPR—each of which plays a vital role in detecting support and resistance:

Exponential Moving Averages (EMAs): Known for their strength in providing dynamic support and resistance levels, EMAs help in identifying trends and shifts in momentum. This indicator includes a dashboard with up to nine customizable EMAs, showing whether each is acting as support or resistance based on real-time price movement.

Volume Weighted Average Price (VWAP): VWAP also provides valuable support and resistance, often regarded as a fair price level by institutional traders. Paired with EMAs, it forms a dual-layered support/resistance system, adding an additional level of confirmation.

Central Pivot Range (CPR): By combining CPR with EMAs and VWAP, Mercury highlights “traffic blocks” in your target journey. This means it identifies zones where price is likely to stall or reverse, providing additional guidance for navigating entries and exits.

Why This Combination Matters:

Using these three tools together gives you a more complete view of the market. VWAP and EMAs offer dynamic trend direction and support/resistance, while CPR pinpoints critical price zones. This combination helps you find high-probability trades, adding clarity to complex market situations and enabling stronger confirmation on trend or reversal decisions.

How to Use:

Trend Confirmation: Check if all EMAs are aligned (green for uptrend, red for downtrend), which is visible in the EMA dashboard. An alignment across VWAP, CPR, and EMAs signifies high confidence in trend direction.

Breakouts & Breakdowns: Mercury has an alert system to signal when a price breakout or breakdown occurs across VWAP, EMA1, and EMA2. This can help in spotting strong directional moves.

Example Application: In my trading, I use Mercury to identify support/resistance zones, confirming trends with EMA/VWAP alignment and using CPR as a checkpoint. I find this especially useful for day trading and swing setups.

Recommended Timeframes:

Day Trading: 5 to 15-minute charts for swift, actionable insights.

Swing Trading: 1-hour or 4-hour charts for broader trend analysis.

Note:

The Mercury Indicator should be used as a supportive tool rather than a standalone strategy, guiding you toward informed decisions in line with your trading style and goals.

EXAMPLE OF TRADE

you can see the cart of XAUUSD on 11th nov 2024

1.SHORT POSITION - TIME FRAME 15 MIN

So here for a short position you need to wait for a breakdown candle which will print in orange post the candle you need to check ema dashboard is completly red that indicates no traffic blocks in your journey to destiny target from ema's and you can take the target from nearest cpr support line

TAKEN IN XAUUSD you can see in chart of XAUUSD on 7th nov

2.LONG POSITION - TIME FRAME 15 MIN -

So here for long position you need to wait for a breakout candle from indicator thats here is blue and check all ema boxes are green and candle body should close above all the 3 lines here it is the both ema 1 and 2 and the vwap line then you can take and entry and your target will be the nearest resistance from the daily cpr

3. STOP LOSS CRITERIA

After the entry any candle close below any of the last line from entry for example we have 3 lines vwap and ema 1 and 2 lines and u have made an entry and the last line before the entry is vwap then if any candle closes below vwap can be considered as stoploss like wise in any lines

The MERCURY indicator is a comprehensive trading tool designed to enhance traders' ability to identify trends, breakouts, and reversals effectively. Created by Dr. Abhiram Sivprasad, this indicator integrates several technical elements, including Central Pivot Range (CPR), EMA crossovers, VWAP levels, and a table-based EMA dashboard, to offer a holistic trading view.

Core Components and Functionality:

Central Pivot Range (CPR):

The CPR in MERCURY provides a central pivot level along with Below Central (BC) and Top Central (TC) pivots. These levels act as potential support and resistance, useful for identifying reversal points and zones where price may consolidate.

Exponential Moving Averages (EMAs):

MERCURY includes up to nine EMAs, with a customizable EMA crossover alert system. This feature enables traders to see shifts in trend direction, especially when shorter EMAs cross longer ones.

VWAP (Volume-Weighted Average Price):

VWAP is incorporated as a dynamic support/resistance level and, combined with EMA crossovers, helps refine entry and exit points for higher probability trades.

Breakout and Breakdown Alerts:

MERCURY monitors conditions for upside and downside breakouts. For an upside breakout, all EMAs turn green and a candle closes above VWAP, EMA1, and EMA2. Similarly, all EMAs turning red, combined with a close below VWAP and EMA1/EMA2, signals a downside breakdown. Continuous alerts are available until the trend shifts.

Real-Time EMA Dashboard:

A table displays each EMA’s relative position (Above or Below), helping traders quickly gauge trend direction. Colors in the table adjust to long/short conditions based on EMA alignment.

Usage Recommendations:

Trend Confirmation:

Use the CPR, EMA alignments, and VWAP to confirm uptrends and downtrends. The table highlights trends, making it easy to spot long or short setups at a glance.

Breakout and Breakdown Alerts:

The alert system is customizable for continuous notifications on critical price levels. When all EMAs align in one direction (green for long, red for short) and the close is above or below VWAP and key EMAs, the indicator confirms a breakout/breakdown.

Adaptable for Different Styles:

Day Trading: Traders can set shorter EMAs for quick insights.

Swing Trading: Longer EMAs combined with CPR offer insights into sustained trends.

Recommended Settings:

Timeframes: MERCURY is suitable for timeframes as low as 5 minutes for intraday traders, up to daily charts for trend analysis.

Symbols: Works across forex, stocks, and crypto. Adjust EMA lengths for asset volatility.

Example Strategy:

Long Entry: When the price crosses above CPR and closes above both EMA1 and EMA2.

Short Entry: When the price falls below CPR with a close below both EMA1 and EMA2.

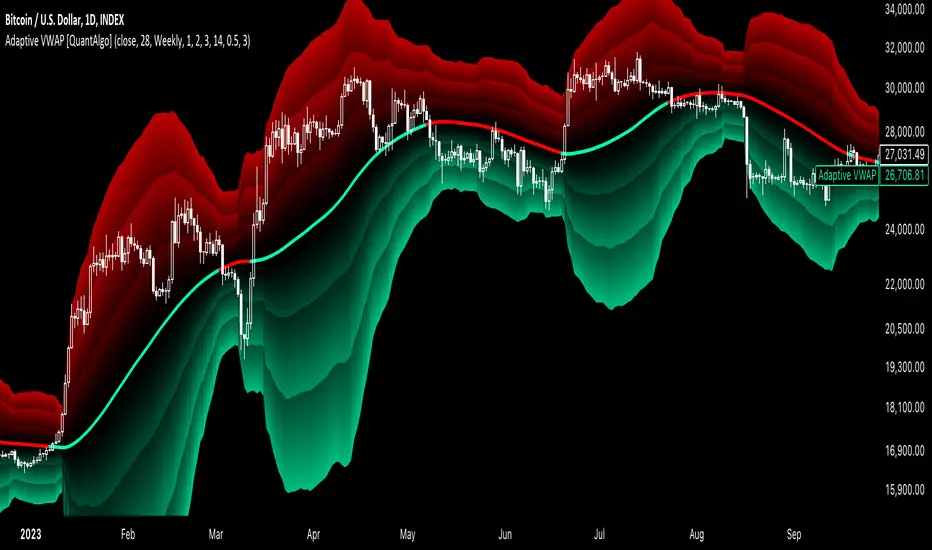

Adaptive VWAP [QuantAlgo]Introducing the Adaptive VWAP by QuantAlgo 📈🧬

Enhance your trading and investing strategies with the Adaptive VWAP , a versatile tool designed to provide dynamic insights into market trends and price behavior. This indicator offers a flexible approach to VWAP calculations by allowing users to adapt it based on lookback periods or fixed timeframes, making it suitable for a wide range of market conditions.

🌟 Key Features:

🛠 Customizable VWAP Settings: Choose between an adaptive VWAP that adjusts based on a rolling lookback period, or switch to a fixed timeframe (e.g., daily, weekly, monthly) for a more structured approach. Adjust the VWAP to suit your trading or investing style.

💫 Dynamic Bands and ATR Filter: Configurable deviation bands with multipliers allow you to visualize price movement around VWAP, while an ATR-based noise filter helps reduce false signals during periods of market fluctuation.

🎨 Trend Visualization: Color-coded trend identification helps you easily spot uptrends and downtrends based on VWAP positioning. The indicator fills the areas between the bands for clearer visual representation of price volatility and trend strength.

🔔 Custom Alerts: Set up alerts for when price crosses above or below the VWAP, signaling potential uptrend or downtrend opportunities. Stay informed without needing to monitor the charts constantly.

✍️ How to Use:

✅ Add the Indicator: Add the Adaptive VWAP to your favourites and apply to your chart. Choose between adaptive or timeframe-based VWAP calculation, adjust the lookback period, and configure the deviation bands to your preferred settings.

👀 Monitor Bands and Trends: Watch for price interaction with the VWAP and its deviation bands. The color-coded signals and band fills help identify potential trend shifts or price extremes.

🔔 Set Alerts: Configure alerts for uptrend and downtrend signals based on price crossing the VWAP, so you’re always informed of significant market movements.

⚙️ How It Works:

The Adaptive VWAP adjusts its calculation based on the user’s chosen configuration, allowing for a flexible approach to market analysis. The adaptive setting uses a rolling lookback period to continuously adjust the VWAP, while the fixed timeframe option anchors VWAP to key timeframes like daily, weekly, or monthly periods. This flexibility enables traders and investors to use the tool in various market environments.

Deviation bands, calculated with customizable multipliers, provide a clear visual of how far the price has moved from the VWAP, helping you gauge potential overbought or oversold conditions. To reduce false signals, an ATR-based filter can be applied, ensuring that only significant price movements trigger trend confirmations.

The tool also includes a fast exponential smoothing function for the VWAP, helping smooth out price fluctuations without sacrificing responsiveness. Trend confirmation is reinforced by the number of bars that price stays above or below the VWAP, ensuring a more consistent trend identification process.

Disclaimer:

The Adaptive VWAP is designed to enhance your market analysis but should not be relied upon as the sole basis for trading or investing decisions. Always combine it with other analytical tools and practices. No statements or signals from this indicator constitute financial advice. Past performance is not indicative of future results.

Anchored VWAPs + DeviationsAnchored VWAPS

*6 anchors to play with

*Pre-defined anchors from pivot points (May need manual adjustment due to timezone difference)

*Drag each anchor right from the screen instead of manually going to the settings>inputs

Deviations:

*Select from which anchor should the deviations start from

*Manually input the desired deviation value/ratio, can be customised

**Tips: To avoid clicking on the AVWAPS to enable the dragging line, just click on the title of the indicator.

***Work in progress

MIDAS VWAP Jayy his is just a bash together of two MIDAS VWAP scripts particularly AkifTokuz and drshoe.

I added the ability to show more MIDAS curves from the same script.

The algorithm primarily uses the "n" number but the date can be used for the 8th VWAP

I have not converted the script to version 3.

To find bar number go into "Chart Properties" select " "background" then select Indicator Titles and "Indicator values". When you place your cursor over a bar the first number you see adjacent to the script title is the bar number. Put that in the dialogue box midline is MIDAS VWAP . The resistance is a MIDAS VWAP using bar highs. The resistance is MIDAS VWAP using bar lows.

In most case using N will suffice. However, if you are flipping around charts inputting a specific date can be handy. In this way, you can compare the same point in time across multiple instruments eg first trading day of the year or an election date.

Adding dates into the dialogue box is a bit cumbersome so in this version, it is enabled for only one curve. I have called it VWAP and it follows the typical VWAP algorithm. (Does that make a difference? Read below re my opinion on the Difference between MIDAS VWAP and VWAP ).

I have added the ability to start from the bottom or top of the initiating bar.

In theory in a probable uptrend pick a low of a bar for a low pivot and start the MIDAS VWAP there using the support.

For a downtrend use the high pivot bar and select resistance. The way to see is to play with these values.

Difference between MIDAS VWAP and the regular VWAP

MIDAS itself as described by Levine uses a time anchored On-Balance Volume (OBV) plotted on a graph where the horizontal (abscissa) arm of the graph is cumulative volume not time. He called his VWAP curves Support/Resistance VWAP or S/R curves. These S/R curves are often referred to as "MIDAS curves".

These are the main components of the MIDAS chart. A third algorithm called the Top-Bottom Finder was also described. (Separate script).

Additional tools have been described in "MIDAS_Technical_Analysis"

Midas Technical Analysis: A VWAP Approach to Trading and Investing in Today’s Markets by Andrew Coles, David G. Hawkins

Copyright © 2011 by Andrew Coles and David G. Hawkins.

Denoting the different way in which Levine approached the calculation.

The difference between "MIDAS" VWAP and VWAP is, in my opinion, much ado about nothing. The algorithms generate identical curves albeit the MIDAS algorithm launches the curve one bar later than the VWAP algorithm which can be a pain in the neck. All of the algorithms that I looked at on Tradingview step back one bar in time to initiate the MIDAS curve. As such the plotted curves are identical to traditional VWAP assuming the initiation is from the candle/bar midpoint.

How did Levine intend the curves to be drawn?

On a reversal, he suggested the initiation of the Support and Resistance VVWAP (S/R curve) to be started after a reversal.

It is clear in his examples this happens occasionally but in many cases he initiates the so-called MIDAS S/R VWAP right at the reversal point. In any case, the algorithm is problematic if you wish to start a curve on the first bar of an IPO .

You will get nothing. That is a pain. Also in Levine's writings, he describes simply clicking on the point where a

S/R VWAP is to be drawn from. As such, the generally accepted method of initiating the curve at N-1 is a practical and sensible method. The only issue is that you cannot draw the curve from the first bar on any security, as mentioned without resorting to the typical VWAP algorithm. There is another difference. VWAP is launched from the middle of the bar (as per AlphaTrends), You can also launch from the top of the bar or the bottom (or anywhere for that matter). The calculation proceeds using the top or bottom for each new bar.

The potential applications are discussed in the MIDAS Technical Analysis book.

_mr_beach Liquidity Sweep + VWAP V2 Trend Filter, Presets_mr_beach Liquidity Sweep + VWAP Reversal V2 (Trend Filter, Presets)

Overview

This strategy models a common institutional market behavior:

Liquidity is taken above the previous day’s high or below the previous day’s low, followed by a return toward fair value (VWAP) and a reversal in the direction of the dominant trend.

The script is designed as a TradingView Strategy for systematic backtesting and optimization.

________________________________________

Core Logic

• Liquidity Levels

o Previous Day High

o Previous Day Low

Used as typical stop-liquidity zones.

• Fair Value

o VWAP is used as confirmation that price has returned to a fair value area.

• Trend Filter

o EMA-based trend direction filter to avoid counter-trend trades.

________________________________________

Trading Rules

Trend Filter

• Long trades only when price closes above EMA.

• Short trades only when price closes below EMA.

Liquidity Sweep

• Bullish sweep: Price trades below Previous Day Low.

• Bearish sweep: Price trades above Previous Day High.

Entry Confirmation

• Long

o Sweep below Previous Day Low

o Close back above Previous Day Low

o Close above VWAP

• Short

o Sweep above Previous Day High

o Close back below Previous Day High

o Close below VWAP

________________________________________

Risk Management

• Stop Loss: ATR-based

• Take Profit: ATR-based

• Risk automatically adapts to market volatility.

• All multipliers are user-adjustable.

________________________________________

Preset Profiles

The script includes ready-to-use preset profiles:

• Index – conservative, session-based, one trade per day

• Forex – session-filtered, moderate volatility settings

• Crypto – higher volatility parameters, no session filter

• Custom – fully manual configuration

Presets control EMA length, ATR settings, SL/TP multipliers, session usage, and trade frequency.

________________________________________

Session & Trade Control

• Optional session filter (default: US regular session)

• Optional one trade per day limit to reduce overtrading and noise

________________________________________

Chart Elements

• EMA (trend direction)

• VWAP (fair value)

• Previous Day High / Low (liquidity zones)

________________________________________

Alerts

• Long setup: Liquidity sweep + VWAP reversal

• Short setup: Liquidity sweep + VWAP reversal

________________________________________

Recommended Usage

• Markets: Indices, liquid stocks, Forex majors, crypto

• Timeframes: 5m and 15m

• Parameters should be optimized per market and timeframe.

________________________________________

Disclaimer

This script is for educational and backtesting purposes only.

It does not constitute financial advice.

Performance depends on market conditions, timeframe, fees, and execution.

Tags: Liquidity, VWAP, EMA, Reversal, Sweep, Smart Money, ICT, ATR, Strategy

_mr_beach Liquidity Sweep + VWAP ReversalLiquidity Sweep + VWAP Reversal (Trend Filter, Session, 1 Trade per Day)

Overview

This strategy models a common institutional market behavior: liquidity is taken above the previous day’s high or below the previous day’s low, followed by a return toward fair value (VWAP) and a reversal in the direction of the prevailing trend.

Designed as a TradingView strategy for structured backtesting in the Strategy Tester.

Core Components

Liquidity Levels: Previous Day High / Previous Day Low

Fair Value Reference: VWAP

Trend Filter: EMA (default: 200)

Volatility-Based Risk: ATR

Trading Rules

Trend Filter

Long only when price closes above EMA

Short only when price closes below EMA

Liquidity Sweep

Bullish sweep: Low < Previous Day Low

Bearish sweep: High > Previous Day High

Entry Confirmation

Long: After a sweep below the Previous Day Low, price closes back above the level and above VWAP

Short: After a sweep above the Previous Day High, price closes back below the level and below VWAP

Risk Management

Stop Loss: ATR-based (slATR)

Take Profit: ATR-based (tpATR)

Automatically adapts to changing market volatility

Session & Trade Frequency

Optional session filter (default: 09:30–16:00 exchange time)

Optional one trade per day limit to reduce overtrading

Chart Elements

EMA (trend direction)

VWAP (fair value)

Previous Day High / Low (liquidity zones)

Alerts

Long setup: Liquidity sweep + VWAP reversal

Short setup: Liquidity sweep + VWAP reversal

Recommended Usage

Markets: Indices, liquid stocks, Forex majors, crypto

Timeframes: 5m, 15m

Note: Parameters such as ATR multipliers and session settings should be optimized per market

Disclaimer

This is a backtesting strategy, not financial advice.

Results depend on market conditions, timeframe, fees, and slippage.

Tags: Liquidity, VWAP, EMA, Reversal, Sweep, Smart Money, ICT, ATR, Strategy

Anchored VWAPThe Anchored VWAP Indicator: A Dynamic Reference for Pivotal Market Events

This script implements a specialized and highly customizable trading tool known as an Anchored Volume-Weighted Average Price (VWAP). Its core innovation and primary utility lie not in a novel mathematical formula, but in its temporal flexibility. Unlike the standard VWAP, which resets at the fixed start of each trading day, this indicator allows the trader to manually define the precise moment from which the calculation begins. This transforms it from a generic daily benchmark into a powerful, event-specific dynamic support and resistance level.

What It Does and How It Works

The indicator plots a single, continuous line on the price chart. This line represents the average price paid for an asset over a specified period, weighted by trading volume, but crucially, starting from a user-chosen timestamp. The calculation follows this logic:

Anchor Point Definition: The user specifies a "Start Time" (e.g., "2024-05-22 11:45:00"). This is the anchor—the moment deemed significant for a new market phase.

Initialization: On the very first candle at or immediately after the anchor time, the indicator initializes its calculation. It uses the candle's high price and volume to set an initial value, establishing a starting point for the cumulative calculation.

Cumulative Calculation: For every subsequent candle, the script calculates the Typical Price (High + Low + Close) / 3 for that period. It then:

Adds (Typical Price * Volume) to a running cumulative total.

Adds the Volume to a running cumulative volume total.

VWAP Plotting: The anchored VWAP line for each candle is simply the cumulative total price-value divided by the cumulative total volume up to that point. The line is only plotted for the period on and after the user-defined anchor time.

How to Use It: The Strategic Application

The power of this tool is unlocked through strategic anchor point selection. It is not a standalone signal generator but a dynamic reference framework for price action. It belongs to the family of Price Action-Based, Event-Driven Analysis and Dynamic Support/Resistance methodologies. Traders use it to contextualize price movement relative to a key market "reset" event.

Common anchor points include:

Major Economic News Releases: Anchor at the exact time of a CPI, FOMC, or jobs report to see the fair-value price discovery after the news, filtering out prior, irrelevant noise.

Significant Technical Breaks: Anchor at the moment a price conclusively breaks a major trendline, a multi-month high/low, or a key chart pattern (like the neckline of a head and shoulders). The VWAP then acts as a dynamic gauge of momentum following the breakout.

Session or Shift Changes: For 24-hour markets, anchor at the open of a specific session (e.g., London Open, US Open) to analyze intra-session flow.

Instrument-Specific Events: Anchor at the start of a merger announcement, earnings call, or product launch.

Once anchored, traders interpret price interaction with the line:

Trend Validation: Price sustaining above a rising anchored VWAP (anchored at a breakout point) confirms bullish momentum. Conversely, holding below a falling VWAP confirms bearish momentum.

Dynamic Support/Resistance: In a trending move, pullbacks towards the anchored VWAP often find support (in uptrends) or resistance (in downtrends). This makes it a potential area for trend-continuation entries.

Mean Reversion & Exhaustion Signals: A sharp, high-volume move far away from the anchored VWAP may signal an overextended market, prompting watch for a reversion back to the mean (the VWAP line).

The Core Philosophy and Rationale

The underlying principle is that volume-confirmed price action following a defining event establishes a new, more relevant fair-value equilibrium. The standard daily VWAP includes all overnight or pre-event noise, which can distort the relevant average for the new market regime initiated by the event.

This anchored approach:

Filters Irrelevance: It isolates analysis to the market structure after the catalyst, providing a cleaner analytical canvas.

Respects Market Microstructure: By weighting price by volume, it acknowledges that high-volume price levels are more significant than low-volume spikes, creating a more robust and "traded" average.

Provides a Self-Adjusting Baseline: It creates a moving benchmark that evolves with the new trend, offering a continuous, objective measure of whether prices are becoming relatively "expensive" or "cheap" within the current move, not compared to the entire day.

In essence, this Anchored VWAP shifts the perspective from a fixed, time-based cycle (the trading day) to a flexible, event-based cycle. It empowers traders to draw a dynamic line in the sand at their chosen moment of structural shift, turning a simple average into a sophisticated gauge of post-event market sentiment and momentum.

ORB Breakout Strategy with VWAP and Volume FiltersOverview

This strategy implements the classic Opening Range Breakout (ORB) methodology, a well-documented approach in trading literature that has been used by institutional and retail traders for decades. The strategy identifies the high and low of the first 15 minutes of the trading session, then trades breakouts with defined risk management.

This implementation includes multiple customizable filters (VWAP, Volume, Candle Strength) that traders can enable, disable, and tune to find configurations that work for their specific markets and trading style.

How It Works

Opening Range Calculation

The strategy captures the high and low of the first N bars after the session open (default: 3 bars on a 5-minute chart = 15 minutes). These levels become the breakout triggers for the session.

Entry Logic

Long Entry: When a bar closes above the ORB High and all enabled filters pass

Short Entry: When a bar closes below the ORB Low and all enabled filters pass

Exit Logic

Take Profit: Configurable multiple of the ORB range (default: 1x = full range beyond breakout level)

Stop Loss: Opposite side of the ORB range

Breakeven: Optional stop adjustment to entry price when trade reaches configurable profit threshold

Session Close: All positions automatically closed at end of trading session

Configurable Filters

All filters can be independently enabled or disabled:

1. VWAP Filter

Requires price above/below session-anchored VWAP

Requires VWAP slope confirmation (configurable lookback and minimum slope)

Purpose: Align trades with intraday trend direction

2. Volume Filter

Requires minimum volume on the breakout bar

Purpose: Confirm institutional participation in the breakout

3. Candle Strength Filter

Requires close in upper/lower portion of the bar range

Purpose: Filter out weak breakouts with poor conviction

Strategy Properties

Initial Capital - $50.000USD

Position Size - 1 contract (fixed)

Commission - $4.00 per contract

Slippage - 2 ticks

Margin - 1%

Pyramiding - Disabled

Backtest Results (NQ)

Recent Performance (Jan 2025 - Jan 2026)

Total Trades - 243

Win Rate - 39.09%

Profit Factor - 1.03

Net P&L - $3,581 (+7.16%)

Max Drawdown - $25,447 (39.96%)

Long-Term Performance (2010 - 2026)

Total Trades - 1699

Win Rate - 37.61%

Profit Factor - 0.756

Net P&L - ($49,632) (-99.26%)

Max Drawdown - $50,262 (99.27%)

Important: Long-term results show negative expectancy with default settings. This strategy is published as a research framework, not a ready-to-trade system. Users are encouraged to experiment with different configurations to find their edge.

Settings Guide

Main Settings

ORB Bars: Number of bars for opening range (3 = 15 min on 5-min chart)

Trading Session: Time window for trading (e.g., 0930-1200 for morning only)

Timezone: Your market's timezone

Take Profit: Multiple of ORB range for target

Breakeven Trigger: Distance to move stop to entry

Max Trades Per Day: Daily trade limit

VWAP Filter

Use VWAP Filter: Enable/disable

VWAP Slope Lookback: Bars to measure VWAP direction

Min VWAP Slope: Minimum slope threshold

Volume Filter

Use Volume Filter: Enable/disable

Min Breakout

Volume: Minimum contracts required

Candle Strength Filter

Use Candle Strength Filter: Enable/disable

Min Candle Strength: Required close position (0.7 = top/bottom 30%)

Research Suggestions

This strategy provides a foundation for exploring ORB-based approaches. Consider testing:

Different ORB periods: 5, 10, 15, or 30 minutes

Session variations: Morning only (0930-1200), afternoon, or full day

Direction bias: Long-only or short-only based on daily trend

Filter combinations: Different mixes of VWAP, volume, and candle filters

Take profit ratios: 0.5x, 1x, 1.5x, or 2x ORB range

Market regimes: Performance may vary in trending vs ranging markets

Different instruments: Test on ES, NQ, MNQ, or other futures

Visual Elements

Orange Background: ORB forming period

Green Background: Active trading session

Green Line: ORB High level

Red Line: ORB Low level

VWAP Line: Green = upslope, Red = downslope, Gray = flat

White Line: Trade entry price

Lime Line: Take profit level

Red Line: Stop loss level

Orange Line: Breakeven trigger level

Blue Background: Breakeven activated

Triangles: Entry signals (only appear when trade executes)

Limitations

Negative long-term expectancy: Default settings do not produce profitable results over extended periods

Parameter sensitivity: Results highly dependent on filter settings and market conditions

Market regime dependent: May perform differently in trending vs choppy markets

Commission impact: Frequent trading accumulates significant transaction costs

Curve fitting risk: Optimized settings may not persist in future markets

Disclaimer

This strategy is provided for educational and research purposes only. It does not constitute financial advice.

Past performance does not guarantee future results

Backtested results may not reflect actual trading conditions

The long-term backtest shows significant negative returns

Always paper trade before risking real capital

Never risk more than you can afford to lose

Conduct your own research and due diligence

This is a research framework designed for traders to explore and customize, not a plug-and-play trading system.

Anchored VWAP PercentageINDICATOR: ANCHORED VWAP PERCENTAGE (AVWAP)

1. Overview

The Anchored VWAP Percentage (AVWAP) is a quantitative momentum and mean-reversion tool. It measures the percentage distance between the current price and a Volume Weighted Average Price (VWAP) that resets automatically based on specific time cycles. It allows traders to identify overextended market conditions relative to institutional value.

---

2. Core Logic & Calculation

The script tracks the relationship between price and volume starting from a specific Anchor Point .

* Volume-Weighted Foundation: Unlike simple moving averages, this indicator uses the VWAP formula: sum(Volume * Price) / sum(Volume) .

* Automatic Anchoring: The starting point (Anchor) resets automatically depending on the chart timeframe (e.g., resets weekly on a 15m chart, or yearly on a Daily chart).

* Percentage Deviation: It calculates the precise gap between the price and the VWAP, plotted as an oscillator: ((Price - VWAP) / VWAP) * 100 .

---

3. Adaptive Intelligence (Multi-Asset & Multi-TF)

The AVWAP is built with an internal database of 85th Percentile (P85) volatility thresholds. It recognizes that different assets have different "stretching" limits:

1. Asset-Specific Calibration: It includes optimized data for Bitcoin, Ethereum, Altcoins, Forex, and Indices .

2. Dynamic Timeframe Mapping: The anchor period and the exhaustion thresholds adjust automatically. For example:

* Intraday (1m-5m): Anchors to an 8-hour (480 min) cycle.

* Mid-Term (15m-60m): Anchors to a Weekly (W) cycle.

* Swing (Daily): Anchors to a Yearly (12M) cycle.

---

4. Visual Anatomy

The indicator is designed for high-speed decision-making:

* The Histogram:

* Green: Price is trading above the VWAP (Bullish premium).

* Red: Price is trading below the VWAP (Bearish discount).

* P85 Threshold Lines:

* These lines represent the 85th percentile of historical deviations . Historically, the price stays within these boundaries 85% of the time.

* Background Highlighting: When the histogram crosses the P85 line, the background glows, signaling a Statistical Exhaustion Zone where a retracement to the mean is highly probable.

---

5. How to Trade with AVWAP

* Mean Reversion: When the histogram reaches the P85 Zone , the price is "statistically overextended." This is a prime area to look for reversals or to take profits on existing trends.

* Trend Strength: If the histogram stays near the Zero Line while the price moves, the trend is supported by healthy volume.

* Value Area: The Zero Line represents the Fair Value . Buying near the Zero Line during a bullish histogram (Green) offers a high-probability entry with low risk.

---

6. Technical Parameters

* Asset Selection: A dropdown to switch between Crypto, Forex, and Indices.

* Color Customization: User-defined colors for bullish and bearish sentiment.

* Precision Control: 4-decimal precision for accurate tracking of thin-margin assets like Forex.

Victoria Overlay - HTF 200 + VWAP + ATR Stop + MA TrioConsolidated road to minions

Buy Setup:

EMA1 crosses above SMA3.

RSI confirms above 50.

Volume increasing (confirming momentum).

Candle closes above SMA1 base.

Sell Setup:

EMA1 crosses below SMA3.

RSI drops below 50 or exits overbought.

Volume confirms (declining or reversing).

Candle closes below SMA1 base.

Tips:

Think of EMA1 as the scalper’s trigger.

SMA3 is your momentum check.

SMA1 (base) = short-term bias.

Avoid entries during low-volume chop.

Use for day trades or tight scalps; exits happen fast.

Overlay (Smoothed Heikin Ashi + Swing + VWAP + ATR Stop + 200-SMA)

Purpose: Multi-layer trend confirmation + clean structure.

Type: Swing alignment tool.

🟩 BUY / CALL Conditions

Green “Buy (Gated)” arrow appears.

Price is above VWAP, above 200-SMA, and above ATR stop.

ATR stop (green line) sits under price → support confirmed.

Heikin-Ashi candles are green/lime.

Bias label says “Above VWAP | Above 200 | Swing Up”.

🟥 SELL / PUT Conditions

Red “Sell (Gated)” arrow appears.

Price is below VWAP, below 200-SMA, and below ATR stop.

ATR stop (red line) sits above price → resistance confirmed.

Heikin-Ashi candles are red.

Bias label says “Below VWAP | Below 200 | Swing Down”.

Exit / Risk Control:

Close position when price crosses ATR stop.

If Heikin candles flip color, momentum is reversing.

Best Use Cases:

For next-day or multi-hour swing entries.

Use ATR Stop for dynamic stop loss.

Stay out when the bias label is mixed (e.g. “Above VWAP | Below 200 | Swing Down”).

Pro Tip:

On big news days, let VWAP reset post-open before acting on arrows — filters fake signals.

RSI Panel Pro (v6)

Purpose: Strength + exhaustion confirmation.

Type: Momentum filter.

Key Levels:

Overbought: 80+ → take profits soon.

Oversold: 20– → watch for bounce setups.

Bull regime: RSI above 60 = momentum strong.

Bear regime: RSI below 40 = weakness.

Buy / Entry Signals:

RSI crosses up from below 40 or 20.

RSI line is above RSI-EMA (gray line).

Higher timeframe RSI (if used) is also rising.

Trim / Exit:

RSI drops under 60 after being strong.

RSI crosses below its EMA.

Sell / Put Setup:

RSI fails at 60 or drops below 40.

RSI crosses under EMA after a bounce.

Tips:

Pair RSI panel with Victoria Overlay — only take gated buys when RSI confirms.

RSI < 40 but above 20 = “loading zone” for reversals.

RSI > 70 = overextended → wait for confirmation before entering.

Combined Execution Rules

Goal What to Watch Action