Forex Dynamic Lot Size CalculatorForex Dynamic Lot Size Calculator for Forex. Works on USD Base and USD Quote pairs. Provides real-time data based on stop-loss location. Allows you to know in real-time how the number of lots you need to purchase to match your risk %.

Number of Lots is calculated based on total risk. Total risk is calculated based on Stop-Loss + Commission + Spread Fees + Slippage measured in pips. Also includes data such as break-even pips, net take profit, margin required, buying power used, and a few others. All are real-time and anchored to the current price.

The intention of creating this indicator is to help with risk management. You know exactly how many lots you need to get this very moment to have your total risk at lets say $250, which includes commission fees, spread fees, and slippage.

To put it simply, if I was to enter the trade right now and willing to risk exactly $250, how many lots will I need to get right this second?

---

- To use adjust Account Settings along with other variables.

- Stop Loss Mode can be Manual or Dynamic. If you select Dynamic, then you will have to adjust Stop Loss Level to where you can see the reference line on the screen. It is at 1.1 by default. Just enter current price and the line will appear. Adjust it by dragging it to where you want your stop loss to be.

- Take Profit Mode can also be Manual or Dynamic. I just keep my TP at Manual and use Quick Access to set Quick RR levels.

- Adjust Spreads and Slippage to your liking. I tried to have TV calculate current spread, but it seem like it doesn't have access to real-life data for me like MT5 does. I just use average instead. Both are optional, depending on your broker and type of account you use.

- Pip Value for the current pair, Return on Margin, and Break-even line can be turned on and off, based on your needs. I just get the Break-even value in pips from the pannel and use that as reference where I need to relocate my stop loss to break-ever (commission + spreds + slippage).

- Panel is fully customizable based on your liking. Important fields are highlighted along with reference lines.

"tp" için komut dosyalarını ara

Idan Moskoבאי/סאייל - עידן מוסקו

אלגוריתם חכם לאיתותי BUY/SELL בלבד על הגרף ✅❌

משלב: ICT (BOS/CHOCH, Order Blocks, Liquidity), FVG/IFVG, Premium/Discount, EMA/MCB, תבניות נרות, וסינון תנודתיות.

איך זה עובד?

➡️ מזהה שבירת מבנה + דחיפה (Displacement)

➡️ בודק אזורי נזילות/OB + מיקום PD (Premium/Discount)

➡️ מאשר עם EMA/MCB/תבניות → מציג BUY או SELL בלבד

טיפים:

לטיימפריים מהירים → Profile: Aggressive

עובד על: 1m / 5m / 15m / 30m / 1H / 4H / 1D

התראות:

🔔 יש התראות מוכנות: “BUY v3” / “SELL v3”

הערה: אין ייעוץ השקעות. מומלץ לאשר עם ניהול סיכונים (SL/TP) 📉📈

Idan Mosko – BUY/SELL

Smart BUY/SELL only ✅❌ using ICT (BOS/CHOCH, OB, Liquidity) + FVG/IFVG, PD, EMA/MCB, and candle patterns.

Modes:

Close-confirmed ✔️ safer

Realtime ⚡ earlier entries

Tips:

Aggressive → more signals • Conservative → cleaner signals.

Works on 1m–1D. Alerts: “BUY v3” / “SELL v3”.

Not financial advice; use proper risk management.

XAUUSD 5m — CET 13:00→01:00 Supertrend + RSI (1:2 RR) — $240KThis strategy is designed for XAUUSD (Gold) on the 5-minute chart, optimized for trading during the most active hours (13:00–01:00 CET).

It combines a Supertrend direction filter with RSI crossovers for precise entries, and applies a 1:2 risk–reward ratio for consistent risk management.

🧠 Logic Overview:

Buy Signal: RSI crosses above 55 while Supertrend is bullish

Sell Signal: RSI crosses below 45 while Supertrend is bearish

Trading Hours: 13:00 → 01:00 CET (corresponding to 07:00 → 19:00 New York time)

Risk Management: Fixed 1:2 RR (TP = 2× SL distance from Supertrend line)

Session Management: Automatically closes all trades after 01:00 CET

Order Size: $240,000 notional exposure per position

💡 Best used for:

Scalping or intraday trading on XAUUSD during high-volatility hours.

The setup works best when combined with strong price action or volume confirmation.

⚠️ Disclaimer:

This script is for educational and testing purposes only.

Past performance does not guarantee future results.

Always test on demo before using live funds.

Trendline Breakout Strategy Strategy should place entries & exits so that it can be backtested (use strategy.entry and strategy.exit with explicit stop and limit prices). Include an option for fixed percent position sizing and an option for fixed contract size. Draw the trendline on the chart (with option to hide/show) and add labels that show: bias (Bull/Bear), trendline slope, entry price, SL, TP and the reason (e.g., "Trendline Breakout"). Provide user inputs for: EMA length (default 200), lookback for pivot detection, pivot sensitivity (left/right bars), quantity mode (percent / contracts), risk percent or fixed size, enable/disable backtest prints, and enable alerts. Avoid repainting: use confirmed pivot logic (pivot detection must use completed bars) and only take entry after breakout confirmed on close. Document any limitations (for example, trendline using two highest/highest bars inside lookback is approximate). Add clear comments, helpful variable names, and include example alertcondition lines for entry and exit signals.

Zero Lag Trend Signals (MTF) [Quant Trading] V7Overview

The Zero Lag Trend Signals (MTF) V7 is a comprehensive trend-following strategy that combines Zero Lag Exponential Moving Average (ZLEMA) with volatility-based bands to identify high-probability trade entries and exits. This strategy is designed to reduce lag inherent in traditional moving averages while incorporating dynamic risk management through ATR-based stops and multiple exit mechanisms.

This is a longer term horizon strategy that takes limited trades. It is not a high frequency trading and therefore will also have limited data and not > 100 trades.

How It Works

Core Signal Generation:

The strategy uses a Zero Lag EMA (ZLEMA) calculated by applying an EMA to price data that has been adjusted for lag:

Calculate lag period: floor((length - 1) / 2)

Apply lag correction: src + (src - src )

Calculate ZLEMA: EMA of lag-corrected price

Volatility bands are created using the highest ATR over a lookback period multiplied by a band multiplier. These bands are added to and subtracted from the ZLEMA line to create upper and lower boundaries.

Trend Detection:

The strategy maintains a trend variable that switches between bullish (1) and bearish (-1):

Long Signal: Triggers when price crosses above ZLEMA + volatility band

Short Signal: Triggers when price crosses below ZLEMA - volatility band

Optional ZLEMA Trend Confirmation:

When enabled, this filter requires ZLEMA to show directional momentum before entry:

Bullish Confirmation: ZLEMA must increase for 4 consecutive bars

Bearish Confirmation: ZLEMA must decrease for 4 consecutive bars

This additional filter helps avoid false signals in choppy or ranging markets.

Risk Management Features:

The strategy includes multiple stop-loss and take-profit mechanisms:

Volatility-Based Stops: Default stop-loss is placed at ZLEMA ± volatility band

ATR-Based Stops: Dynamic stop-loss calculated as entry price ± (ATR × multiplier)

ATR Trailing Stop: Ratcheting stop-loss that follows price but never moves against position

Risk-Reward Profit Target: Take-profit level set as a multiple of stop distance

Break-Even Stop: Moves stop to entry price after reaching specified R:R ratio

Trend-Based Exit: Closes position when price crosses EMA in opposite direction

Performance Tracking:

The strategy includes optional features for monitoring and analyzing trades:

Floating Statistics Table: Displays key metrics including win rate, GOA (Gain on Account), net P&L, and max drawdown

Trade Log Labels: Shows entry/exit prices, P&L, bars held, and exit reason for each closed trade

CSV Export Fields: Outputs trade data for external analysis

Default Strategy Settings

Commission & Slippage:

Commission: 0.1% per trade

Slippage: 3 ticks

Initial Capital: $1,000

Position Size: 100% of equity per trade

Main Calculation Parameters:

Length: 70 (range: 70-7000) - Controls ZLEMA calculation period

Band Multiplier: 1.2 - Adjusts width of volatility bands

Entry Conditions (All Disabled by Default):

Use ZLEMA Trend Confirmation: OFF - Requires ZLEMA directional momentum

Re-Enter on Long Trend: OFF - Allows multiple entries during sustained trends

Short Trades:

Allow Short Trades: OFF - Strategy is long-only by default

Performance Settings (All Disabled by Default):

Use Profit Target: OFF

Profit Target Risk-Reward Ratio: 2.0 (when enabled)

Dynamic TP/SL (All Disabled by Default):

Use ATR-Based Stop-Loss & Take-Profit: OFF

ATR Length: 14

Stop-Loss ATR Multiplier: 1.5

Profit Target ATR Multiplier: 2.5

Use ATR Trailing Stop: OFF

Trailing Stop ATR Multiplier: 1.5

Use Break-Even Stop-Loss: OFF

Move SL to Break-Even After RR: 1.5

Use Trend-Based Take Profit: OFF

EMA Exit Length: 9

Trade Data Display (All Disabled by Default):

Show Floating Stats Table: OFF

Show Trade Log Labels: OFF

Enable CSV Export: OFF

Trade Label Vertical Offset: 0.5

Backtesting Date Range:

Start Date: January 1, 2018

End Date: December 31, 2069

Important Usage Notes

Default Configuration: The strategy operates in its most basic form with default settings - using only ZLEMA crossovers with volatility bands and volatility-based stop-losses. All advanced features must be manually enabled.

Stop-Loss Priority: If multiple stop-loss methods are enabled simultaneously, the strategy will use whichever condition is hit first. ATR-based stops override volatility-based stops when enabled.

Long-Only by Default: Short trading is disabled by default. Enable "Allow Short Trades" to trade both directions.

Performance Monitoring: Enable the floating stats table and trade log labels to visualize strategy performance during backtesting.

Exit Mechanisms: The strategy can exit trades through multiple methods: stop-loss hit, take-profit reached, trend reversal, or trailing stop activation. The trade log identifies which exit method was used.

Re-Entry Logic: When "Re-Enter on Long Trend" is enabled with ZLEMA trend confirmation, the strategy can take multiple long positions during extended uptrends as long as all entry conditions remain valid.

Capital Efficiency: Default setting uses 100% of equity per trade. Adjust "default_qty_value" to manage position sizing based on risk tolerance.

Realistic Backtesting: Strategy includes commission (0.1%) and slippage (3 ticks) to provide realistic performance expectations. These values should be adjusted based on your broker and market conditions.

Recommended Use Cases

Trending Markets: Best suited for markets with clear directional moves where trend-following strategies excel

Medium to Long-Term Trading: The default length of 70 makes this strategy more appropriate for swing trading rather than scalping

Risk-Conscious Traders: Multiple stop-loss options allow traders to customize risk management to their comfort level

Backtesting & Optimization: Comprehensive performance tracking features make this strategy ideal for testing different parameter combinations

Limitations & Considerations

Like all trend-following strategies, performance may suffer in choppy or ranging markets

Default 100% position sizing means full capital exposure per trade - consider reducing for conservative risk management

Higher length values (70+) reduce signal frequency but may improve signal quality

Multiple simultaneous risk management features may create conflicting exit signals

Past performance shown in backtests does not guarantee future results

Customization Tips

For more aggressive trading:

Reduce length parameter (minimum 70)

Decrease band multiplier for tighter bands

Enable short trades

Use lower profit target R:R ratios

For more conservative trading:

Increase length parameter

Enable ZLEMA trend confirmation

Use wider ATR stop-loss multipliers

Enable break-even stop-loss

Reduce position size from 100% default

For optimal choppy market performance:

Enable ZLEMA trend confirmation

Increase band multiplier

Use tighter profit targets

Avoid re-entry on trend continuation

Visual Elements

The strategy plots several elements on the chart:

ZLEMA line (color-coded by trend direction)

Upper and lower volatility bands

Long entry markers (green triangles)

Short entry markers (red triangles, when enabled)

Stop-loss levels (when positions are open)

Take-profit levels (when enabled and positions are open)

Trailing stop lines (when enabled and positions are open)

Optional ZLEMA trend markers (triangles at highs/lows)

Optional trade log labels showing complete trade information

Exit Reason Codes (for CSV Export)

When CSV export is enabled, exit reasons are coded as:

0 = Manual/Other

1 = Trailing Stop-Loss

2 = Profit Target

3 = ATR Stop-Loss

4 = Trend Change

Conclusion

Zero Lag Trend Signals V7 provides a robust framework for trend-following with extensive customization options. The strategy balances simplicity in its core logic with sophisticated risk management features, making it suitable for both beginner and advanced traders. By reducing moving average lag while incorporating volatility-based signals, it aims to capture trends earlier while managing risk through multiple configurable exit mechanisms.

The modular design allows traders to start with basic trend-following and progressively add complexity through ZLEMA confirmation, multiple stop-loss methods, and advanced exit strategies. Comprehensive performance tracking and export capabilities make this strategy an excellent tool for systematic testing and optimization.

Note: This strategy is provided for educational and backtesting purposes. All trading involves risk. Past performance does not guarantee future results. Always test thoroughly with paper trading before risking real capital, and adjust position sizing and risk parameters according to your risk tolerance and account size.

================================================================================

TAGS:

================================================================================

trend following, ZLEMA, zero lag, volatility bands, ATR stops, risk management, swing trading, momentum, trend confirmation, backtesting

================================================================================

CATEGORY:

================================================================================

Strategies

================================================================================

CHART SETUP RECOMMENDATIONS:

================================================================================

For optimal visualization when publishing:

Use a clean chart with no other indicators overlaid

Select a timeframe that shows multiple trade signals (4H or Daily recommended)

Choose a trending asset (crypto, forex major pairs, or trending stocks work well)

Show at least 6-12 months of data to demonstrate strategy across different market conditions

Enable the floating stats table to display key performance metrics

Ensure all indicator lines (ZLEMA, bands, stops) are clearly visible

Use the default chart type (candlesticks) - avoid Heikin Ashi, Renko, etc.

Make sure symbol information and timeframe are clearly visible

================================================================================

COMPLIANCE NOTES:

================================================================================

✅ Open-source publication with complete code visibility

✅ English-only title and description

✅ Detailed explanation of methodology and calculations

✅ Realistic commission (0.1%) and slippage (3 ticks) included

✅ All default parameters clearly documented

✅ Performance limitations and risks disclosed

✅ No unrealistic claims about performance

✅ No guaranteed results promised

✅ Appropriate for public library (original trend-following implementation with ZLEMA)

✅ Educational disclaimers included

✅ All features explained in detail

================================================================================

NOVA Breakout Signals v2.2 (TF M30)A clean, rules-based breakout signal tool for 30-minute charts.

It detects Dow swing breakouts and filters them with RSI, MACD and Volume so you only see the higher-quality entries. The script does not place trades and does not calculate SL/TP – it only prints clear LONG/SHORT labels at the entry price.

⸻

How it works

1. Timeframe enforcement – Signals are generated only on M30. On other timeframes the script shows a notice and stays silent.

2. Breakout engine (Dow swings) – The last confirmed swing high/low (pivots) is tracked.

• Breakout Up: bar closes above the last swing high by a small buffer.

• Breakout Down: bar closes below the last swing low by a small buffer.

3. Quality filters (all must be true):

• RSI (default length 30):

• Long: RSI > threshold and rising.

• Short: RSI < threshold and falling.

• MACD (12/26/9):

• Long: histogram > 0 and line > signal.

• Short: histogram < 0 and line < signal.

• Volume: current volume > SMA(volume, 20) × multiplier.

4. Debounce / anti-spam

• Cooldown of 4 hours (8 M30 bars) after any signal.

• Minimum price distance from the previous signal to avoid clustered labels.

Signals appear once the bar closes (barstate.isconfirmed). No swing lines are drawn to keep the chart clean; only entry labels are shown.

⸻

Inputs (key)

• RSI length & thresholds for Long/Short confirmation.

• MACD uses 12/26/9 (fixed).

• Volume multiplier (relative to SMA 20).

• Breakout buffer %, Cooldown hours, Min distance %.

• Show labels (on/off).

⸻

Usage tips

• Start with gold/major FX/indices on M30; use “Once per bar close” if you attach alerts.

• Increase the breakout buffer and volume multiplier in choppy markets.

• Tighten RSI thresholds (e.g., 55/45) if you want fewer but stronger signals.

⸻

Notes & limitations

• Pivots confirm after a few bars by definition; signals themselves are printed only on confirmed bar close and do not repaint once shown.

• This is a signal indicator, not investment advice. Always manage risk.

KD-10-20 Cross No Chop ChopThis strategy avoids 80% of the choppy trades. Take entry when it gives a buy signal and put TP and SL as per your convenience. Happy Trading!

Liquidity Sniper V3 (ANTI-FAKEOUT)An advanced institutional trading indicator combining liquidity pool targeting, smart money concepts, and momentum-based entries with comprehensive risk management.

🎯 CORE FEATURES:

- Liquidity Sniper Module: Identifies and targets major liquidity pools (PDH/PDL, PWH/PWL, Equal Highs/Lows, HVN/LVN edges)

- Anti-Fakeout Stack: 10-layer confirmation system including VWAP reclaim, micro BOS, displacement, relative volume, and mitigation entries

- Momentum Engulf Add-On: Catches high-velocity impulsive moves with engulfing candles, volume spikes, and volatility breakouts

- GARCH Volatility Filter: Dynamic volatility analysis to avoid choppy conditions

- Multi-Timeframe Confirmation: Ensures alignment across timeframes before entries

📊 SIGNAL CLASSIFICATION:

- BEST (Green): Highest probability setups with all confirmations aligned - 6.0+ score

- BETTER (Medium Green): Strong setups with most confirmations - 4.5-6.0 score

- GOOD (Light Green): Valid setups with basic confirmations - 3.0-4.5 score

🔍 TRADE SCENARIOS:

S1: Liquidity Reversal - Sweeps + reversals at key levels with displacement

S2: Continuation - Trend following with VWAP mean reversion

S3: Mean Reversion - Extreme deviations (2σ+) with Fibonacci exhaustion

S4: Deep Sweep - 3σ sweeps at major liquidity with high confluence

⚡ MOMENTUM TRIGGERS:

- MET (Momentum Engulf): Bullish/bearish engulfing with 1.5x+ volume spike and ATR impulse

- VBT (Volatility Breakout): Range breakouts with sigma bursts and participation

🛡️ RISK MANAGEMENT:

- Dynamic TP/SL based on ATR, VWAP bands, and liquidity pools

- 3-tier targets (T1: VWAP, T2: Nearest pool, T3: 5R extension)

- Early invalidation tracking (0.5R movement monitoring)

- Minimum 2:1 RR requirement with cooldown periods

- RTH session filters and anti-spam protection

📈 TECHNICAL EDGE:

- SMT Divergence detection vs ES correlation

- CVD (Cumulative Volume Delta) divergence confirmation

- FVG (Fair Value Gap) and Order Block mitigation entries

- Equal highs/lows clustering analysis

- Volume profile HVN/LVN identification

⚙️ FULLY CUSTOMIZABLE:

All parameters adjustable including cooldowns, proximity thresholds, ATR multipliers, RR floors, and scenario weights.

Perfect for: ES/NQ futures, forex majors, and liquid stocks. Works on 1-15 min timeframes. Best results during NY session (9:35-11:00 AM & 1:30-3:30 PM ET).

Created for serious traders seeking institutional-grade edge with quantifiable risk/reward and high-probability setups

DAMMU AUTOMATICAL AI ENRTY AND TARGET AND EXITMain Components

Supertrend System –

Detects market trend direction (Buy/Sell zones).

→ Green = Uptrend (Buy)

→ Red = Downtrend (Sell)

SMA Filter –

Uses 50 & 200 moving averages to confirm overall trend.

→ Price above both → Bullish

→ Price below both → Bearish

Buy/Sell Signals –

Generated when Supertrend flips direction and SMA confirms.

→ Triangle up = Buy

→ Triangle down = Sell

Take Profit / Stop Loss Levels –

Automatically calculated after Buy/Sell entry.

→ TP1, TP2, SL shown on chart

ADX (Sideways Zone Filter) –

If ADX < 25 → Market sideways → Avoid trades

Shows “No Trade Zone” area

Smart Money Concepts (SMC) Tools –

🔹 Market structure (HH, HL, LH, LL)

🔹 Order blocks (OB)

🔹 Equal highs/lows

🔹 Fair Value Gaps (FVG)

🔹 Premium & Discount zones

Helps find institutional entry points

Visual Display –

Color-coded background (trend zones)

Labels for buy/sell/structure

Optional FVG and order block boxes

Risk Management –

Input-based position sizing, SL & TP management

(to calculate profit levels and minimize loss)

Advanced Multi-Timeframe Trend & Signal System═══════════════════════════════════════════════════════════════

ADVANCED MULTI-TIMEFRAME TREND & SIGNAL SYSTEM v1.0

═══════════════════════════════════════════════════════════════

Created by: Zakaria Safri

License: Mozilla Public License 2.0

A comprehensive technical analysis tool designed for traders seeking

multi-dimensional market insights. This indicator combines proven

technical analysis methods with modern visualization techniques.

═══════════════════════════════════════════════════════════════

KEY FEATURES

═══════════════════════════════════════════════════════════════

✓ SUPERTREND SIGNAL GENERATION

- Customizable sensitivity settings

- Clear long/short entry signals

- Automatic trend direction detection

- ATR-based dynamic calculations

✓ MULTI-TIMEFRAME DASHBOARD

- Real-time trend analysis across 6 timeframes

- Synchronized trend confirmation

- Customizable table position and size

- Current: 1M, 5M, 15M, 1H, 1D coverage

✓ QQE REVERSAL DETECTION

- Quantitative Qualitative Estimation algorithm

- Early reversal signal identification

- Adjustable RSI and smoothing parameters

- Confirmation-based plotting

✓ DYNAMIC SUPPORT & RESISTANCE

- Pivot-based level calculation

- Quick and standard pivot detection

- Color-coded zones (8 levels)

- Automatic level updates

✓ MOMENTUM BREAKOUT SIGNALS

- Ichimoku-inspired calculations

- Bullish and bearish breakout detection

- Visual zone highlighting

- Trend confirmation filters

✓ RISK MANAGEMENT SYSTEM

- ATR-based stop loss calculation

- Multiple take profit targets (TP1, TP2, TP3)

- Customizable risk-to-reward ratios

- Dynamic price level tracking

- Hit detection markers

✓ VOLATILITY BANDS

- Keltner Channel implementation

- Multiple band layers (3 levels)

- EMA-based calculations

- Adaptive to market conditions

✓ TREND CLOUD VISUALIZATION

- Dual moving average cloud

- Clear trend direction indication

- Customizable color scheme

- Trend bar coloring

═══════════════════════════════════════════════════════════════

HOW TO USE

═══════════════════════════════════════════════════════════════

SETUP:

1. Add indicator to your chart

2. Configure sensitivity in Core Signals section

3. Enable desired features (signals, reversals, breakouts)

4. Set up risk management levels if trading

5. Position MTF dashboard to preference

SIGNAL INTERPRETATION:

• LONG Signal: Price crosses above Supertrend

• SHORT Signal: Price crosses below Supertrend

• REV (Reversal): QQE indicates potential trend change

• Diamond Breakouts: Momentum shift confirmation

• T1/T2/T3: Take profit level hits

MULTI-TIMEFRAME ANALYSIS:

• Green (BULL): Higher timeframe supports uptrend

• Red (BEAR): Higher timeframe supports downtrend

• Use for trend alignment and confirmation

• Best results when multiple timeframes align

RISK MANAGEMENT:

• Enable Stop Loss for automatic SL calculation

• Activate TP levels based on trading style

• Adjust Risk-to-Reward ratio (1:1 to 1:10)

• Monitor hit detection circles for exits

═══════════════════════════════════════════════════════════════

TECHNICAL SPECIFICATIONS

═══════════════════════════════════════════════════════════════

CALCULATIONS:

• Supertrend: ATR-based with customizable multiplier

• QQE: Modified RSI with Wilders smoothing

• Keltner Channels: EMA basis with ATR bands

• Pivots: Standard left/right bar methodology

• Support/Resistance: Multi-level pivot analysis

PARAMETERS:

• Supertrend Sensitivity: 0.5 to 10.0 (default: 2.0)

• RSI Period: 5 to 50 (default: 14)

• QQE Multiplier: 1.0 to 10.0 (default: 4.238)

• Risk-to-Reward: 1 to 10 (default: 4)

TIMEFRAMES:

Compatible with all timeframes. MTF dashboard displays:

• 1 Minute (1M)

• 5 Minutes (5M)

• 15 Minutes (15M)

• 1 Hour (1H)

• 1 Day (1D)

• Current chart timeframe

═══════════════════════════════════════════════════════════════

CUSTOMIZATION OPTIONS

═══════════════════════════════════════════════════════════════

VISUAL:

• Professional color scheme (Cyan/Orange)

• Adjustable table position (9 positions)

• Table size options (tiny/small/normal/large)

• Transparent zone highlighting

• Clean, modern label design

TOGGLES:

• Enable/disable any feature independently

• Show/hide signals, reversals, breakouts

• Toggle S/R levels and zones

• Control trend cloud and bands

• Master trend line optional

ALERTS:

The indicator provides visual signals that can be used with

TradingView's alert system by setting alerts on the indicator.

═══════════════════════════════════════════════════════════════

BEST PRACTICES

═══════════════════════════════════════════════════════════════

✓ Combine signals for higher probability setups

✓ Use MTF dashboard for trend confirmation

✓ Respect S/R levels for entry/exit planning

✓ Monitor QQE reversals at key price levels

✓ Adjust sensitivity based on asset volatility

✓ Test on demo/paper trading first

✓ Use proper risk management always

═══════════════════════════════════════════════════════════════

IMPORTANT DISCLAIMER

═══════════════════════════════════════════════════════════════

This indicator is a technical analysis tool and does NOT:

• Guarantee profitable trades

• Provide financial advice

• Predict future price movements with certainty

• Replace proper risk management

• Substitute for personal due diligence

Past performance does not indicate future results. All trading

involves risk. Users should:

- Understand the indicator's logic

- Test thoroughly before live trading

- Use appropriate position sizing

- Never risk more than they can afford to lose

- Consult financial advisors if needed

═══════════════════════════════════════════════════════════════

CODING STANDARDS

═══════════════════════════════════════════════════════════════

This indicator follows PineCoders Coding Conventions:

✓ Proper variable naming (prefixes: i_, f_, c_)

✓ Clear function documentation

✓ Organized code structure

✓ Type declarations

✓ Efficient calculations

✓ No repainting (confirmed signals)

✓ Proper use of request.security

═══════════════════════════════════════════════════════════════

SUPPORT & UPDATES

═══════════════════════════════════════════════════════════════

Version: 1.0

Author: Zakaria Safri

License: MPL 2.0

Last Updated: 2024

For questions, feedback, or suggestions, please comment below.

═══════════════════════════════════════════════════════════════

#trading #signals #supertrend #multiTimeframe #QQE #reversals

#supportResistance #riskManagement #trendAnalysis #momentum

TriAnchor Elastic Reversion US Market SPY and QQQ adaptedSummary in one paragraph

Mean-reversion strategy for liquid ETFs, index futures, large-cap equities, and major crypto on intraday to daily timeframes. It waits for three anchored VWAP stretches to become statistically extreme, aligns with bar-shape and breadth, and fades the move. Originality comes from fusing daily, weekly, and monthly AVWAP distances into a single ATR-normalized energy percentile, then gating with a robust Z-score and a session-safe gap filter.

Scope and intent

• Markets: SPY QQQ IWM NDX large caps liquid futures liquid crypto

• Timeframes: 5 min to 1 day

• Default demo: SPY on 60 min

• Purpose: fade stretched moves only when multi-anchor context and breadth agree

• Limits: strategy uses standard candles for signals and orders only

Originality and usefulness

• Unique fusion: tri-anchor AVWAP energy percentile plus robust Z of close plus shape-in-range gate plus breadth Z of SPY QQQ IWM

• Failure mode addressed: chasing extended moves and fading during index-wide thrusts

• Testability: each component is an input and visible in orders list via L and S tags

• Portable yardstick: distances are ATR-normalized so thresholds transfer across symbols

• Open source: method and implementation are disclosed for community review

Method overview in plain language

Base measures

• Range basis: ATR(length = atr_len) as the normalization unit

• Return basis: not used directly; we use rank statistics for stability

Components

• Tri-Anchor Energy: squared distances of price from daily, weekly, monthly AVWAPs, each divided by ATR, then summed and ranked to a percentile over base_len

• Robust Z of Close: median and MAD based Z to avoid outliers

• Shape Gate: position of close inside bar range to require capitulation for longs and exhaustion for shorts

• Breadth Gate: average robust Z of SPY QQQ IWM to avoid fading when the tape is one-sided

• Gap Shock: skip signals after large session gaps

Fusion rule

• All required gates must be true: Energy ≥ energy_trig_prc, |Robust Z| ≥ z_trig, Shape satisfied, Breadth confirmed, Gap filter clear

Signal rule

• Long: energy extreme, Z negative beyond threshold, close near bar low, breadth Z ≤ −breadth_z_ok

• Short: energy extreme, Z positive beyond threshold, close near bar high, breadth Z ≥ +breadth_z_ok

What you will see on the chart

• Standard strategy arrows for entries and exits

• Optional short-side brackets: ATR stop and ATR take profit if enabled

Inputs with guidance

Setup

• Base length: window for percentile ranks and medians. Typical 40 to 80. Longer smooths, shorter reacts.

• ATR length: normalization unit. Typical 10 to 20. Higher reduces noise.

• VWAP band stdev: volatility bands for anchors. Typical 2.0 to 4.0.

• Robust Z window: 40 to 100. Larger for stability.

• Robust Z entry magnitude: 1.2 to 2.2. Higher means stronger extremes only.

• Energy percentile trigger: 90 to 99.5. Higher limits signals to rare stretches.

• Bar close in range gate long: 0.05 to 0.25. Larger requires deeper capitulation for longs.

Regime and Breadth

• Use breadth gate: on when trading indices or broad ETFs.

• Breadth Z confirm magnitude: 0.8 to 1.8. Higher avoids fighting thrusts.

• Gap shock percent: 1.0 to 5.0. Larger allows more gaps to trade.

Risk — Short only

• Enable short SL TP: on to bracket shorts.

• Short ATR stop mult: 1.0 to 3.0.

• Short ATR take profit mult: 1.0 to 6.0.

Properties visible in this publication

• Initial capital: 25000USD

• Default order size: Percent of total equity 3%

• Pyramiding: 0

• Commission: 0.03 percent

• Slippage: 5 ticks

• Process orders on close: OFF

• Bar magnifier: OFF

• Recalculate after order is filled: OFF

• Calc on every tick: OFF

• request.security lookahead off where used

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Fills and slippage vary by venue

• Shapes can move during bar formation and settle on close

• Standard candles only for strategies

Honest limitations and failure modes

• Economic releases or very thin liquidity can overwhelm mean-reversion logic

• Heavy gap regimes may require larger gap filter or TR-based tuning

• Very quiet regimes reduce signal contrast; extend windows or raise thresholds

Open source reuse and credits

• None

Strategy notice

Orders are simulated by TradingView on standard candles. request.security uses lookahead off where applicable. Non-standard charts are not supported for execution.

Entries and exits

• Entry logic: as in Signal rule above

• Exit logic: short side optional ATR stop and ATR take profit via brackets; long side closes on opposite setup

• Risk model: ATR-based brackets on shorts when enabled

• Tie handling: stop first when both could be touched inside one bar

Dataset and sample size

• Test across your visible history. For robust inference prefer 100 plus trades.

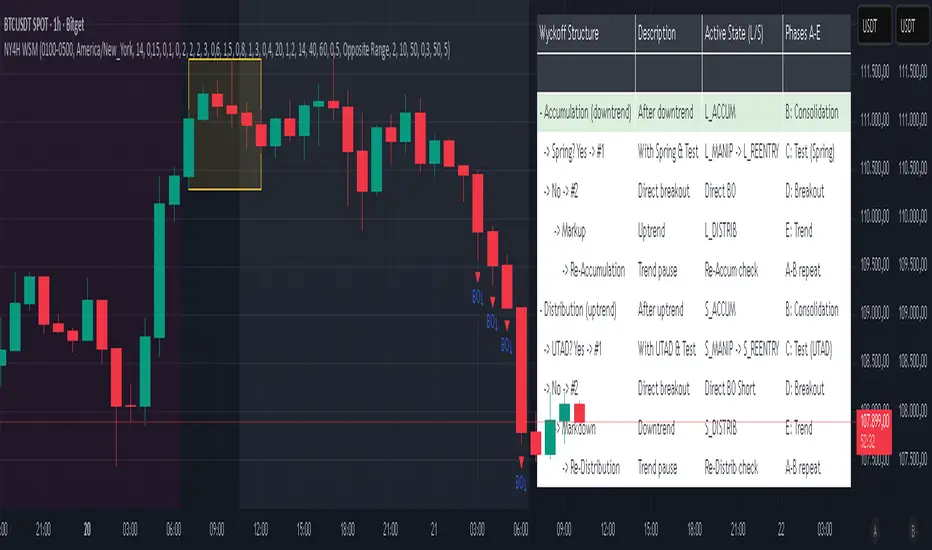

NY 4H Wyckoff State Machine [CHE] NY 4H Wyckoff State Machine — Full (Re-Entry, Breakout, Wick, Re-Accum/Distrib, Dynamic Table) — One-Candle Wyckoff Re-Entry (OCWR)

Summary

OCWR operationalizes a one-candle session workflow: mark the first four-hour New York candle, fix its high and low as the session range when the window closes, and drive entries through a Wyckoff-style state machine on intraday bars. The script adds an ATR-scaled buffer around the range and requires multi-bar acceptance before treating breaks or re-entries as valid. Optional wick-cluster evidence, a proximity retest, and simple volume or RSI gates increase selectivity. Background tints expose regimes, shapes mark events, a dynamic table explains the current state, and hidden plots supply alert payloads. The design reduces random flips and makes state transitions auditable without higher-timeframe calls.

Origin and name

Method name: One-Candle Wyckoff Re-Entry (OCWR)

Transcript origin: The source idea is a “stupid simple one-candle scalping” routine: mark the first New York four-hour candle (commonly between one and five in the morning New York time), drop to five minutes, observe accumulation inside, wait for a manipulation move outside, then trade the re-entry back inside. Stops go beyond the excursion extreme; targets are either a fixed reward multiple or the opposite side of the range. Preference is given to several manipulation candles. This indicator codifies that workflow with explicit states, acceptance counters, buffers, and optional quality filters. Any external performance claims are not part of the code.

Motivation: Why this design?

Session levels are widely respected, yet single-bar breaches around them are noisy. OCWR separates range discovery from trade logic. It locks the range at the end of the window, applies an ATR-scaled buffer to ignore marginal oversteps, and requires acceptance over several bars for breaks and re-entries. Wick evidence and optional retest proximity help confirm that an excursion likely cleared liquidity rather than launched a trend. This yields cleaner transitions from test to commitment.

What’s different vs. standard approaches?

Baseline: Static session lines or one-shot Wyckoff tags without process control.

Architecture: Dual long and short state machines; ATR-buffered edges; multi-bar acceptance for breaks and re-entries; optional wick dominance and cluster checks; optional retest tolerance; direct and opposite breakout paths; cooldown after fires; distribution timeout; dynamic table with highlighted row.

Practical effect: Fewer single-bar head-fakes, clearer hand-offs, and on-chart explanations of the machine’s view.

Wyckoff structure by example — OCWR on five minutes

One-candle setup:

On the four-hour chart, mark the first New York candle’s high and low, then switch to five minutes. Solid lines show the fixed range; dashed lines show ATR-buffered edges.

Long path (verbal mapping):

Phase A, Stopping Action: Price stabilizes inside the range.

Phase B, Consolidation: Sustained balance while the window is closed and after the range is fixed.

Phase C, Test (Spring): Excursion below the buffered low with preference for several outside bars and dominant lower wicks, then a return inside.

Re-entry acceptance: A required run of inside bars validates the test.

Phase D, Breakout to Markup: Long signal fires; stop beyond the excursion extreme; objective is the opposite range or a fixed reward multiple.

Phase E, Trend (Markup) and Re-Accumulation: Advance continues until target, stop, confirmation back against the box, or timeout. A pause inside trend may register as re-accumulation.

Short path mirrors the above: A UTAD-style move forms above the buffered high, then re-entry leads to Markdown and possible re-distribution.

Variant map (verbal):

Accumulation after a downtrend: with Spring and Test, or without Spring; both proceed to Markup and may pause in Re-Accumulation.

Distribution after an uptrend: with UTAD and Test, or without UTAD; both proceed to Markdown and may pause in Re-Distribution.

Note: Phases A through E occur within each variant and are not separate variants.

How it works (technical)

Session window: A configurable four-hour New York window records its high and low. At window end, the bounds are fixed for the session.

ATR buffer: A margin above and below the fixed range discourages triggers from tiny oversteps.

Inside and outside: Users choose close-based or wick-based detection. Overshoot requirements are expressed verbally as a fraction of the range with an optional absolute minimum.

Manipulation tracking: The machine counts bars spent outside and records the side extreme.

Re-entry acceptance: After a return inside, a specified number of inside bars must print before acceptance.

Direct and opposite breakouts: Direct breakouts from accumulation and opposite breakouts after manipulation are supported, subject to acceptance and optional filters.

Targets and exits: Choose the opposite boundary or a fixed reward multiple. Distribution ends on target, stop, confirmation back against the range, or timeout.

Context filters (optional): Volume above a scaled SMA, RSI thresholds, and a trend SMA for simple regime context.

Diagnostics: Background tints for regimes; arrows for re-entries; triangles for breakouts; table with row highlights; hidden plots for alert values.

Central table (Wyckoff console)

The table sits top-right and explains the machine’s stance. Columns: Structure label, plain-English description, active state pair for long and short, and human phase tags. Rows: Start and range building; accumulation branch with Spring and Test as well as direct breakout; Markup and re-accumulation; distribution branch with UTAD and Test as well as direct short breakout; Markdown and re-distribution. Only the active state cell is rewritten each last bar, for example “L_ACCUM slash S_ACCUM”. Row highlighting is context-aware: accumulation, Spring or UTAD, breakout, Markup or Markdown, and re-accumulation or re-distribution checks can highlight independently so users see simultaneous conditions. The table is created once, updated only on the last bar for efficiency, and functions as a read-only console to audit why a signal fired and where the path currently sits.

Parameter Guide

Session window and time zone: First four hours of New York by default; time zone “America/New_York”.

ATR length and buffer factor: Control buffer size; larger reduces sensitivity, smaller reacts faster.

Minimum overshoot (fraction and absolute): Demand meaningful extension beyond the buffer.

Break mode: Close-based is stricter; wick-based is more reactive.

Acceptance counts: Separate counts for break, re-entry, and opposite breakout; higher values reduce noise.

Minimum bars outside: Ensures manipulation is not a single spike.

Wick detection and clusters (optional): Dominance thresholds and cluster size within a short window.

Retest required and tolerance (optional): Gate re-entry by proximity to the buffered edge.

Volume and RSI filters (optional): Simple gates on activity and momentum.

TP mode and reward multiple: Opposite range or fixed multiple.

Cooldown and distribution timeout: Rate-limit signals and prevent endless distribution.

Visualization toggles: Background phases, labels, table, and helper lines.

Reading & Interpretation

Solid lines are the fixed session bounds; dashed lines are buffers. Backgrounds tint accumulation, manipulation, and distribution. Arrows show accepted re-entries; triangles show direct or opposite breakouts. Labels can summarize entry, stop, target, and risk. The table highlights the active row and the current state pair.

Practical Workflows & Combinations

OCWR baseline: Each morning, mark the New York four-hour candle, move to five minutes, prefer multi-bar manipulation outside, then wait for a qualified re-entry inside. Stop beyond the excursion extreme. Target the opposite range for conservative management or a fixed multiple for uniform sizing.

Trend following: Favor direct breakouts with trend alignment and no contradictory wick evidence.

Quality control: When noise rises, increase acceptance, raise the buffer factor, enable retest, and require wick clusters.

Discretionary confluences: Fair-value gaps and trend lines can be added by the user; they are not computed by this script.

Behavior, Constraints & Performance

Closed-bar confirmation is recommended when you require finality; live-bar conditions can change until close. The script does not call higher-timeframe data. It uses arrays, lines, labels, boxes, and a table; maximum bars back is five thousand; table updates are last-bar only. Known limits include compressed buffers in quiet sessions, unreliable wick evidence in thin markets, and session misalignment if the platform time zone is not New York.

Sensible Defaults & Quick Tuning

Start with ATR length fourteen, buffer factor near zero point fifteen, overshoot fraction near zero point ten, acceptance counts of two, minimum outside duration three, retest required on.

Too many flips: increase acceptance, raise buffer, enable retest, and tighten wick thresholds.

Too slow: reduce acceptance, lower buffer, switch to wick-based breaks, disable retest.

Noisy wicks: increase minimum wick ratio and cluster size, or disable wick detection.

What this indicator is—and isn’t

A session-anchored visualization and signal layer that formalizes a Wyckoff-style re-entry and breakout workflow derived from a single four-hour New York candle. It is not predictive and not a complete trading system. Use with structure analysis, risk controls, and position management.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

MACD + Supertrend + DEMA StrategySTRATEGY 📊 STRATEGY LOGIC:

Long Entry: When ALL of these occur simultaneously:

MACD histogram crosses above 0

Supertrend is bullish (green)

Short DEMA > Long DEMA

Short Entry: When ALL of these occur simultaneously:

MACD histogram crosses below 0

Supertrend is bearish (red)

Short DEMA < Long DEMA

Exits: Based on your TP/SL percentages from entry price

This follows the same clean structure as your MACD strategy but adds the alignment concept and proper risk management!

Dammu AI PROType & Purpose

Multi-functional trend, swing, and smart money concept indicator.

Combines SuperTrend, SMA, ATR-based risk management, swing structures, order blocks, EQH/EQL, and Fair Value Gaps (FVG).

Designed for identifying trends, entries/exits, and support/resistance zones.

2. Trend Detection

SuperTrend with ATR smoothing (nsensitivity*7 factor) for buy/sell signals.

SMA filter (8 & 9 periods) confirms trend strength.

Bar color changes:

Green if close > supertrend.

Red if close < supertrend.

Cirrus Cloud highlights trend zones with semi-transparent colors.

3. Swing & Structure

Detects pivot highs/lows and labels them as HH/LH (Highs), HL/LL (Lows).

Generates BOS (Break of Structure) and CHoCH (Change of Character) signals.

Internal swing structures and order blocks for short-term intraday moves.

4. Order Blocks

Internal Order Blocks (iOBs) and Swing Order Blocks (OBs).

Boxes drawn for bullish/bearish zones.

Auto-delete when broken.

Option to filter blocks by ATR or Cumulative Mean Range.

5. Risk Management

TP/SL levels based on ATR and user-defined % risk.

Shows lines and labels for:

Entry

Stop Loss

TP1, TP2, TP3

Adjustable line style (solid/dashed/dotted).

6. Fair Value Gaps (FVG)

Highlights bullish and bearish gaps.

Option for auto-threshold filtering.

Extendable FVG boxes.

7. EQH/EQL

Detects Equal Highs (EQH) and Equal Lows (EQL) for potential reversals.

Dotted lines with labels.

8. Smart Money Concepts (SMC) Features

Shows:

Swings (internal & swing structure)

Internal order blocks

Premium/Discount zones

Fair Value Gaps

Highs/Lows from previous day/week/month

Configurable for historical vs present display.

9. Alerts

Buy/Sell triggers:

bull = crossover of close above SuperTrend.

bear = crossunder of close below SuperTrend.

Alerts for BOS/CHoCH, EQH/EQL, and OB breaks.

10. Visualization

Trend clouds, colored bars, SMA markers, SuperTrend labels.

Multi-layered info displayed without cluttering the chart.

Customizable colors, line styles, and transparency.

✅ Summary:

This indicator is a comprehensive trading tool for trend detection, swing structure, order block analysis, and risk management. It’s built for smart money and SMC-based trading, offering visual cues and alerts for key trading decisions.

nadia

Gold ramon strategy based on 50 candles and atr of 12

You enter the maximum of 50 candles once the most bearish starts to rise, we expect 10 candles, if you don't go up in 10 candles, you don't enter, if you go up before 10 candles, you enter.

When is TP? Enough with 5 candles

The temporality is 1 hour. It can be adjusted to 1 minute temporality for scalping.

It is never lost, because it always exceeds the previous maximums.

ES cuhthis strategy uses laggard rsi to compute the best parameters to go long and tp at key levels. the overall trend strength within the rsi laggard indicator is what is used to automate the calculations within the script. enjoy and paramter optimize

Solana 4H RSI->MACD — Counter-Trend By TetradTetrad RSI→RSI Cross→MACD (Sequenced) — Counter-Trend (SL-Only)

Category: Market-neutral, counter-trend, sequenced entries

Timeframe default: Works on any TF; designed around 4H On Solana

Markets: Any (spot, perp, futures); parameterize to your asset

What it does

This strategy hunts reversals using a 3-step sequence on RSI and MACD, then optionally restricts entries by market regime and a price gate. It shows stop-loss lines only when hit (clean chart), and paints a Donchian glow for quick read of backdrop conditions.

Entry logic (sequenced)

1. RSI Extreme:

Long path activates when RSI < Oversold (default 27.5).

Short path activates when RSI > Overbought (default 74).

2. RSI Cross confirmation:

Long path: RSI crosses up back above the oversold level.

Short path: RSI crosses down back below the overbought level.

Each step has a max bar lookback so stale signals time out.

3. MACD Cross trigger:

Long: MACD line crosses above Signal.

Short: MACD line crosses below Signal.

→ When step 3 fires and gates are satisfied, a trade is entered.

Optional gates & filters

Regime Filter (Counter-Trend):

Longs allowed in **Range / Short Trend / Short Parabolic** regimes.

Shorts allowed in **Range / Long Trend / Long Parabolic** regimes.

Based on ADX/DI and ATR% intensity.

* Price Gate (Long Ceiling):

Toggle to **disable new longs above a chosen price (default 209.0 For SOL).

Useful for assets like SOL where you want longs only below a cap.

Exits / Risk

* Stop-Loss (% of entry):** default **14%**, toggleable.

* SL visualization:** plots a **thin dashed red line only on the bar it’s hit**.

* (No take-profit or time-based exit in this version—keep it pure to the sequence and regime. Add TP/time exits if desired.)

Visuals

* Donchian Glow (50): background band only (upper/lower lines hidden).

* Regime HUD: compact table (top-right) highlighting the active regime.

* Minimal marks: no entry/exit “arms” clutter; only SL-hit lines render.

Inputs (key)

* Core: RSI Length, Oversold/Overbought, MACD Fast/Slow/Signal.

* Sequence: Max bars from Extreme→RSI Cross and RSI Cross→MACD Cross.

* Regime: ADX Length, Trend/Parabolic thresholds, ATR length & floor.

* Stops: Enable/disable; SL %.

* Price Gate: Enable; Long ceiling price.

Alerts

Sequenced Long (CT): RSIhigh → RSI cross down → MACD bear cross.

## Notes & Tips

Designed for counter-trend fades that become trend rides. The regime filter helps avoid fading true parabolics and aligns entries with safer contexts.

The sequence is stateful (steps must occur in order). If a step times out, the path resets.

Works on lower TFs, but the 4H baseline reduces noise and over-trading.

Consider pairing with volume or structure filters if you want fewer but higher-conviction entries.

Past performance ≠ future results. **Educational use only. Not financial advice.

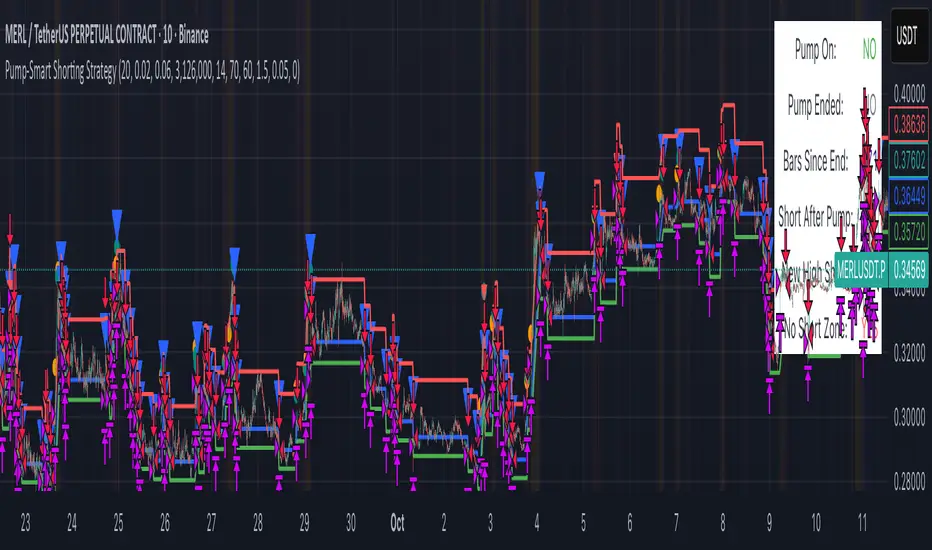

Pump-Smart Shorting StrategyThis strategy is built to keep your portfolio hedged as much as possible while maximizing profitability. Shorts are opened after pumps cool off and on new highs (when safe), and closed quickly during strong upward moves or if stop loss/profit targets are hit. It uses visual overlays to clearly show when hedging is on, off, or blocked due to momentum, ensuring you’re protected in most market conditions but never short against the pump. Fast re-entry keeps the hedge active with minimal downtime.

Pump Detection:

RSI (Relative Strength Index): Calculated over a custom period (default 14 bars). If RSI rises above a threshold (default 70), the strategy considers the market to be in a pump (strong upward momentum).

Volume Spike: The current volume is compared to a 20-bar simple moving average of volume. If it exceeds the average by 1.5× and price increases at least 5% in one bar, pump conditions are triggered.

Price Jump: Measured by (close - close ) / close . A single-bar change > 5% helps confirm rapid momentum.

Pump Zone (No Short): If any of these conditions is true, an orange or red background is shown and shorts are blocked.

Cooldown and Re-Entry:

Cooldown Detection: After the pump ends, RSI must fall below a set value (default ≤ 60), and either volume returns towards average or price momentum is less than half the original spike (oneBarUp <= pctUp/2).

barsWait Parameter: You can specify a waiting period after cooldown before a short is allowed.

Short Entry After Pump/Cooldown: When these cooldown conditions are met, and no short is active, a blue background is shown and a short position is opened at the next signal.

New High Entry:

Lookback New High: If the current high is greater than the highest high in the last N bars (default 20), and pump is NOT active, a short can be opened.

Take Profit (TP) & Stop Loss (SL):

Take Profit: Short is closed if price falls to a threshold below the entry (minProfitPerc, default 2%).

Stop Loss: Short is closed if price rises to a threshold above the entry (stopLossPerc, default 6%).

Preemptive Exit:

Any time a pump is detected while a short position is open, the strategy closes the short immediately to avoid losses.

Visual Feedback:

Orange Background: Market is pumping, do not short.

Red Background: Other conditions block shorts (cooldown or waiting).

Blue Background: Shorts allowed.

Triangles/Circles: Mark entries, pump start/end, for clear trading signals.

Measured Pattern Move (Bulkowski) [SS]Hey everyone,

This is the Measured Pattern Move using Bulkowski's process for measured move calculation.

What the indicator does:

The indicator has the associated measured move across 20 of the most common and frequent Bulkowski patterns, including:

Double Bottom / Adam Eve Bottom

Double Top / Adam Eve Top

Inverse Head and Shoulders

Bear Flag

Bull Flag

Horn Bottom

Horon Top

Broadening Top

Descending Broadening Wedge

Broadening Bottoms

Broadening Tops

Cup and Handle

Inverted cup and handle

Diamond Bottom

Diamond Top

Falling Wedge

Rising Wedge

Pipe Bottom

Pipe Top

Head and Shoulders

It will calculate the measured move according to the Bulkowski process.

What is the Bulkowski Process?

Each move has an associated continuation percentage, which Bulkowski has studied, analyzed and concluded statistically.

For example, Double tops have a continuation percent of 54%. Bear flags, 47%. These are "constants" that are associated with the pattern.

Bulkowski applies them to the daily, but how I have formulated this, it can be used on all timeframes, and with the constant, it will correctly calculate the measured move of the pattern.

What this indicator DOES NOT DO

This indicator will not identify the pattern for you.

I tried this using Dynamic Time Warping (DTW) using my own pre-trained Bulkowski model in R. I was successfully able to get Pinescript to calculate DTW which was amazing! But applying it to all these patterns actually went over the execution time limit, which is understandable.

As such, you will need to identify the pattern yourself, then use this indicator to hilight the pattern and it will calculate the measured move based on the constant and the pattern range.

Let's look at some examples:

Use examples

Double bottom / adam eve bottom on SPY on the 1-Minute chart

Adam and Eve Double Bottom QQQ 1-Hour Chart

Adam Eve Double Bottom MSFT Daily Chart

Bearish Head and Shoulders Pattern MSFT Daily

You get the point.

How to use the indicator

To use the indicator, identify the pattern of interest to you.

Then, highlight the pattern using the indicator (it will ask you to select start time of the pattern and end time of the pattern). The indicator will then highlight the pattern and calculate the measured move, as seen in the examples above.

Best approaches

To make the most of the indicator, its best to draw out your pattern and wait for an actual break, the point of the break is usually the end of the pattern formation.

From here, you will then apply this indicator to calculate the expected up or down move.

Let me show you an example:

Here we see CME_MINI:ES1! has made an Adam bottom pattern. We know the Eve should be forming soon and it indeed does:

We mark the top of the pattern like so:

Then we use our Measured move indicator to calculate the measured move:

Measured move here for CME_MINI:ES1! is 6,510.

Now let's see....

Voila!

Selecting the Pattern

After you highlight the selected pattern, in the indicator settings, simply select the type of pattern it is, for example "head and shoulders" or "Broadening wedge", etc.

The indicator will then adjust its measurements to the appropriate constant and direction.

Concluding remarks

That is the indicator!

It is helpful for determining the actual projected move of a pattern on breakout.

Remember, it does not find the pattern for you , you are responsible for identifying the pattern. But this will calculate the actual TP of the pattern for you, without you having to do your own calculations.

I hope you find it useful, I actually use this indicator every day, especially on the lower timeframes!

And you will find, the more you use it, the better you get at recognizing significant patterns!

If you are not aware of these patterns, Bulkowski lists all of this information freely accessible on his website. I cannot link it here but you can just Google him and he has graciously made his information public and free!

That's it, I hope you enjoy and safe trades!

Disclaimer

This is not my intellectual property. The pattern calculations come from the work of Thomas Bulkowski and not myself. I simply coded this into an indicator using his publicly accessible information.

You can get more information from Bulkowski's official website about his work and patterns.

EA M1 Signals with Persistent ATR TP/SL1 Minute scalper for XAU/USD - uses multiple integrated indicators to provide signals upon a breakout and pullback

Daytrade Forex Scalper TwinPulse Auction Timer IndicatorWhat this indicator is

TwinPulse Auction Timer is a multi component execution aid designed for liquid markets. It looks for two families of opportunities

Breakouts that leave a compression area after a fresh sweep

Reversals that trigger after a sweep with strong wick polarity

It does not try to predict future prices. It measures present auction conditions with transparent rules and shows you when those conditions align. You get a simple table that says LONG SHORT or WAIT, optional session shading, clean entry and exit level visuals, and alerts you can wire to your workflow.

Why it is different

Most tools show a single signal. TwinPulse combines several independent signals into an Edge Score that you can tune. The components are

• Pulse. A signed measure of wick asymmetry with candle body direction

• Compression. Current true range compared with an average range

• Sweep timer. Bars elapsed since the most recent sweep of a prior high or low

• Bias. Direction of a higher timeframe candle

• Regime. Efficiency ratio and the relation of micro to macro volatility

• Location. Distance from the daily anchored VWAP

• Session. London and New York filter by time windows

Each component is visible in the inputs and in the table so you can understand why a suggestion appears. The script uses request.security() with lookahead off in all calls so it does not peek into the future. Shapes may move while a bar is open since price is still forming. They stop moving when the bar closes.

What you will see on the chart

• L and S shapes on entry bars

• An Exit shape at the price where a stop or the runner target would have been hit

• Four horizontal lines while a trade is active

Entry

Stop

TP1 at one R

TP2 at the runner target expressed in R

• Labels anchored to each line so you can instantly read Entry SL TP1 and TP2 with current values

• Optional shading during your session windows

• Optional daily VWAP line

The table in the top right shows

Action LONG SHORT IN LONG IN SHORT or WAIT

Session ON or OFF

Bias UP DOWN or FLAT

Pulse value

Compression value

Edge L percent and Edge S percent

How it works in detail

Pulse

For each bar the script measures up wick minus down wick divided by range and multiplies that by the sign of the candle body. The result is averaged with pulse_len. Positive numbers indicate aggressive buying. Negative numbers indicate aggressive selling. You control the minimum absolute value with pulse_thr.

Compression

Compression is the ratio of current range to an average range. You can choose the range basis. HL SMA uses simple high minus low smoothed by range_len. ATR uses classic True Range smoothed by atr_len. Values below comp_thr indicate a coil.

Sweeps and the timer

A sweep occurs when price trades beyond the highest high or lowest low seen in the previous sweep_len bars. A strict sweep requires a close back inside that prior range. The timer measures how many bars have elapsed since the last sweep. Breakout setups require the timer to exceed timer_thr.

Bias on a confirmation timeframe

A higher timeframe candle is read with confirm_tf. If close is above open bias is UP. If close is below open bias is DOWN. This keeps breakouts aligned with the prevailing drift.

Regime filters

Efficiency ratio measures the straight line change over the sum of absolute bar to bar changes over er_len. It rises in trendy conditions and falls in noise. Minimum efficiency is controlled by er_min.

Micro to macro volatility ratio compares a short lookback average range with a longer lookback average range using your chosen basis. For breakouts you usually want micro volatility to be near or above macro hence mvr_min. For reversals you often want micro volatility that is not overheated relative to macro hence mvr_max_rev.

VWAP distance gate

Daily anchored VWAP is rebuilt from the open of each session. The script computes the absolute distance from VWAP in units of your average range and requires that distance to exceed vwap_dist_thr when use_vwap_gate is true. This keeps entries away from the mean.

Edge Score

Each gate contributes a weight that you control. The script sums weights of the satisfied gates and divides by the sum of all weights to produce an Edge percent for long and an Edge percent for short. You can then require a minimum Edge percent using edge_min_pct. This turns the indicator into a step by step checklist that you can tune to your taste.

Using the indicator step by step

Choose markets and timeframes

The logic is designed for liquid instruments. Major currency pairs, index futures and cash index CFDs, and the most liquid crypto pairs work well. On intraday use one to fifteen minutes for signals and fifteen to sixty minutes for confirmation. On swing use one hour to one day for signals and one day for confirmation.

Decide on entry mode

Breakouts require a compression area and a sweep timer. Reversals require a strict sweep and a strong pulse. If you are unsure leave the default which allows both.

Pick a range basis

For FX and crypto HL SMA is often stable. For indices and single name equities with gaps ATR can adapt better. If results look too reactive increase the window. If results are too slow reduce it.

Tune regime filters

If you trade trend continuation raise er_min and mvr_min. If you trade counter rotation lower them and rely on the reversal path with the strict sweep condition.

Set the VWAP gate

Enabling it helps you avoid entries at the mean. Push the threshold higher on range bound days. Reduce it in strong trend days.

Table driven decision

Watch Action and the Edge percents. If the script says WAIT you can read Pulse and Compression to see what is missing. Often the best trades appear when both Edge percents are well separated and your session switch is ON.

Use the visuals

When a suggestion triggers you will see entry stop and targets. You can mirror the levels in your own workflow or use alerts.

Consider bar close

Signals are computed in real time. For a strict process you can wait until the bar closes to reduce noise.

Inputs explained with quick guidance

Setup

Signal TF chooses where the logic is computed. Leave blank to use the chart.

Confirm TF sets the higher timeframe for bias.

Session filter restricts signals to the London and New York windows you specify.

Invert flips long and short. It is useful on inverse instruments.

Logic options

Entry mode allows Breakouts Reversals or Both.

Average range basis selects HL SMA or ATR.

ATR length is used when ATR is selected.

Pulse source can be Regular OHLC or Heikin Ashi. Heikin Ashi smooths noisy series, but the script still runs on regular bars and you should publish and use it on standard candles to respect the platform guidance.

Core numeric settings

Sweep lookback controls the size of the liquidity pool targeted by the sweep condition.

Pulse window smooths the wick polarity measure.

Average range window controls your base range when you use HL SMA.

Pulse threshold sets the minimum polarity required.

Compression threshold sets the maximum current range relative to average to consider the market coiled.

Expansion timer bars sets how much time has passed since the last sweep before you allow a breakout.

Regime filters

Efficiency ratio length and minimum value keep you out of aimless drift.

Micro and Macro range lengths feed the micro to macro ratio.

Minimum micro to macro for breakouts and maximum micro to macro for reversals steer the two entry families.

VWAP gate and distance threshold keep you away from the mean.

Levels and trade management visuals

Runner target in R sets TP2 as a multiple of initial risk.

Stop distance as average range multiple sets initial risk size for the visuals.

Move stop to entry after one R touch turns on break even logic once price has traveled one risk unit.

Trail buffer as R fraction uses the last sweep as an anchor and keeps a dynamic stop at a chosen fraction of R beyond it.

Cooldown after exit prevents immediate re entries.

Edge Score

Weights for pulse compression timer bias efficiency ratio micro to macro VWAP gate and session let you align the checklist with your style.

Minimum Edge percent to suggest applies a final filter to LONG or SHORT suggestions.

UI

Table and markers switch the compact dashboard and the shapes.

TP and SL lines and labels draw and name each level.

TP1 partial label percent is printed in the TP1 label for clarity.

Session shading helps with focus.

Daily VWAP line is optional.

Alerts

The script provides alerts for Long Short Exit and for Edge percent crossing the threshold on either side. Use them to drive notifications or to sync with webhooks and your broker integration. Alerts trigger in real time and will repaint during a bar. For conservative use trigger on bar close.

Recommended presets

Intraday trend continuation

Confirm TF fifteen minutes

Entry mode Breakouts

Range basis HL SMA

Pulse threshold near 0.10

Compression threshold near 0.60

Timer around 18

Minimum efficiency ratio near 0.20

Minimum micro to macro near 1.00

VWAP gate enabled with distance near 0.35

Edge minimum 50 or higher

Intraday mean reversion at sweeps

Entry mode Reversals

Pulse source Regular OHLC

Compression threshold can be a little higher

Maximum micro to macro near 1.60

Efficiency ratio minimum lower near 0.12

VWAP gate enabled

Edge minimum 40 to 60

Swing trend continuation

Signal TF one hour

Confirm TF one day

Range basis ATR

ATR length around 14

Average range window 20 to 30

Efficiency ratio minimum near 0.18

Micro to macro windows 12 and 60

Edge minimum 50 to 70

These are starting points only. Your instrument and timeframe will require small adjustments.

Limitations and honest warnings

No indicator is perfect. TwinPulse will mark attractive conditions that do not always lead to profitable trades. During economic releases or very thin liquidity the assumptions behind compression and sweeps may fail. In strong gap environments the HL SMA basis may lag while ATR may overreact. Heikin Ashi pulse can help in choppy markets but it will lag during sharp reversals. Session times use the exchange time of your chart. If you switch symbol or exchange verify the windows.

Edge percent is not a probability of profit. It is the fraction of satisfied gates with your chosen weights. Two traders can set different weights and see different Edge readings on the same bar. That is the design. The score is a guide that helps you act with discipline.

This indicator does not place orders or manage real risk. The lines and labels show a model entry a model stop and two model targets built from the average range at entry and from recent swing points. Use them as references and not as hard rules. Always test on historical data and demo first. Past results do not guarantee anything in the future.

Credits and originality

All code in this publication is original and written for this indicator. The concept of the efficiency ratio originates from Perry Kaufman. The use of a daily anchored volume weighted average price is a standard industry tool. The specific combination of pulse from wick polarity strict sweep timing compression and the tunable Edge Score is unique to this script at the time of publication. If you reuse parts of the open source code in your own work remember to credit the author and contribute meaningful improvements.

How to read the table at a glance

Action reflects your current state.

IN LONG or IN SHORT appears while a trade is active.

LONG or SHORT appears when conditions for entry are met and the Edge threshold is satisfied.

WAIT appears when at least one gate is missing.

Session shows ON during your chosen windows.

Bias shows the color of the confirmation candle.

Pulse is the smoothed polarity number.

Comp shows current range divided by the average range. Values below one mean compression.

Edge L percent and Edge S percent show the long and short checklists as percents.

Final thoughts

Markets move because orders accumulate at certain prices and at certain times. The indicator tries to measure two things that often matter at those turning points. One is the existence of a hidden imbalance revealed by wick polarity and by sweeps of prior extremes. The other is the presence of energy stored in a coil that can release in the direction of a drift. Neither force guarantees profit. Together they can improve your selection and your timing.

Use the defaults for a few days so you learn the personality of the signals. After that adjust one group at a time. Start with the session filter and the Edge threshold. Then tune compression and the timer. Finally adjust the regime filters. Keep notes. You will learn which weights matter for your market and timeframe. The result is a process you can apply with consistency.

Disclaimer

This script and description are for education and analysis. They are not investment advice and they do not promise future results. Use at your own risk. Test thoroughly on historical data and in simulation before considering any live use.

Larry Williams - Smash Day (SL/TP in %)This strategy implements Larry Williams’ “Smash Day” reversal concept on any symbol and timeframe (daily is the classic). A Smash Day is a bar that closes beyond a recent extreme and then potentially reverses on the next session.

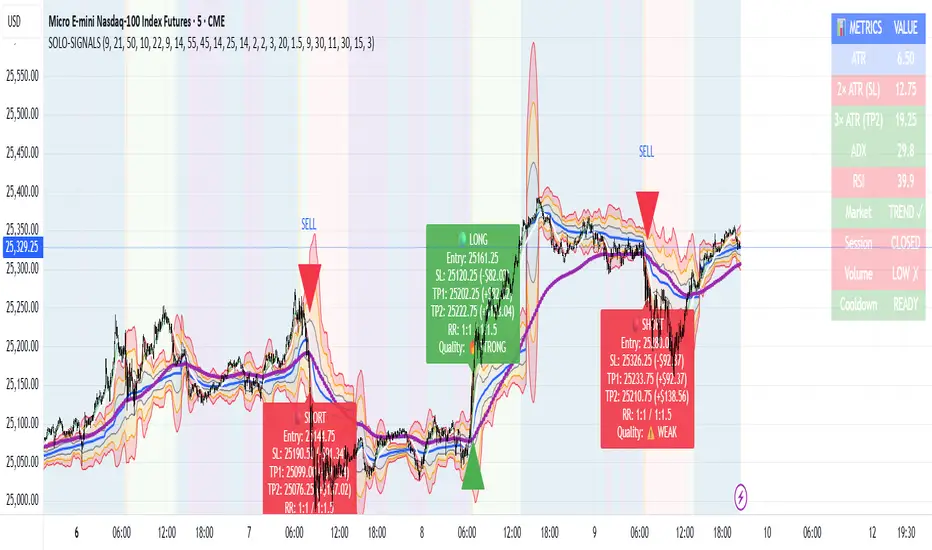

MNQ Morning Indicator | Clean SignalsMNQ Morning Trading Indicator Summary

What It Does

This is a TradingView indicator designed for day trading MNQ (Micro Nasdaq-100 futures) during morning sessions. It generates BUY and SELL signals only when multiple technical conditions align, helping traders identify high-probability trade setups.

Core Strategy

BUY Signal Requirements (All must be true):

✅ Price above VWAP (volume-weighted average price)

✅ Fast EMA (9) above Slow EMA (21) - uptrend confirmation

✅ Price above 15-minute 50 EMA - higher timeframe confirmation

✅ MACD histogram positive - momentum confirmation

✅ RSI above 55 - strength confirmation

✅ ADX above 25 - trending market (not choppy)

✅ Volume 1.5x above average - strong participation

SELL Signal (opposite conditions)

Key Features

🎯 Risk Management

Stop Loss: 2× ATR (Average True Range)

Take Profit 1: 2× ATR (1:2 risk-reward)

Take Profit 2: 3× ATR (1:3 risk-reward)

Dollar values: Calculates P&L based on MNQ's $2/point value

⏰ Session Filter

Default: 9:30 AM - 11:30 AM ET (customizable)

Safety feature: Avoids first 15 minutes (high volatility period)

Won't generate signals outside trading hours

🛡️ Signal Quality

Rates each signal: 🔥 STRONG, ⚡ MEDIUM, or ⚠️ WEAK

Requires minimum 15 bars between signals (prevents overtrading)

📊 Visual Dashboard

Shows real-time metrics:

ATR values

ADX (trend strength)

RSI (momentum)

Market condition (TREND/CHOP)

Session status

Volume status

Signal cooldown timer

Visual Elements

📈 VWAP with standard deviation bands (1σ, 2σ, 3σ)

📉 Multiple EMAs with trend-based coloring

🟢/🔴 Buy/Sell arrows on chart

📋 Detailed trade labels showing entry, SL, TPs, and risk-reward ratios

🎨 Background highlighting for market conditions

Safety Features

Cooldown period between signals

Session restrictions (no trading outside set hours)

First 15-minute avoidance (post-open volatility)

Multi-confirmation requirement (all 7 conditions must align)

Trend filter (ADX minimum to avoid choppy markets)

Best For

Day traders focused on morning sessions

MNQ futures traders

Traders who prefer systematic, rule-based entries

Those wanting pre-calculated risk management levels

Customization

All parameters are adjustable:

EMA periods

MACD settings

RSI thresholds

ADX minimum

ATR multipliers

Session times

Visual preferences

This indicator is designed to be conservative — it waits for strong confirmation before signaling, which means fewer but potentially higher-quality trades.